Modeling discrete common-shock risks through matrix distributions

Abstract

We introduce a novel class of bivariate common-shock discrete phase-type (CDPH) distributions to describe dependencies in loss modeling, with an emphasis on those induced by common shocks. By constructing two jointly evolving terminating Markov chains that share a common evolution up to a random time corresponding to the common shock component, and then proceed independently, we capture the essential features of risk events influenced by shared and individual-specific factors. We derive explicit expressions for the joint distribution of the termination times and prove various class and distributional properties, facilitating tractable analysis of the risks. Extending this framework, we model random sums where aggregate claims are sums of continuous phase-type random variables with counts determined by these termination times, and show that their joint distribution belongs to the multivariate phase-type or matrix-exponential class. We develop estimation procedures for the CDPH distributions using the expectation-maximization algorithm and demonstrate the applicability of our models through simulation studies and an application to bivariate insurance claim frequency data.

Keywords: Phase-type distribution; Discrete bivariate distribution; Common shocks; Expectation-maximization algorithm.

1 Introduction

Ever since their conception in Jensen, (1954), phase-type distributions, which represent the time until absorption in a finite state-space Markov chain, have been extensively used due to their flexibility in approximating a wide range of distributions and their analytical tractability (see Bladt and Nielsen, (2017) for a review). Such a class of distributions has also gained popularity in actuarial science in the last two decades. In insurance ruin problems, phase-type distributions can be used to model the claim amounts (e.g. Drekic et al., (2004); Frostig et al., (2012)) and/or the inter-arrival times (an assumption implicitly embedded in the class of risk processes with Markovian claim arrivals; see e.g. Cheung and Landriault, (2010)). Interested readers are referred to Asmussen and Albrecher, (2010) and Badescu and Landriault, (2009) for comprehensive reviews. Outside ruin theory, Hassan Zadeh and Stanford, (2016) developed Bayesian and Bühlmann credibility theories under phase-type claims whereas Wang et al., (2018) derived the distribution of the discounted aggregate claims under phase-type renewal process. Generalizations of phase-type distributions have also been proved to be successful for fitting insurance loss data. In particular, Ahn et al., (2012) utilized log phase-type distribution to fit the well-known Danish fire data, and Bladt and Yslas, 2023a proposed a phase-type mixture-of-experts regression model to fit the severities from the French Motor Third Party Liability dataset. Apart from modeling insurance losses and interclaim times, phase-type mortality law was studied by Lin and Liu, (2007), and a review of the use of phase-type distributions in health care systems can be found in Fackrell, (2009). While all the above works are concerned with continuous phase-type distributions, discrete phase-type (DPH) distributions have also been applied to model claim frequencies. For example, Panjer-type recursions for the calculations of compound distributions under DPH claim counts were developed by Eisele, (2006); Wu and Li, (2010); Ren, (2010).

In modern risk theory and insurance mathematics, there is increasing need for researchers and practitioners to accurately model the dependencies among multiple risk factors or risk events, as this is crucial for effective risk management. Such dependence modeling is particularly important in scenarios where different risks are influenced by shared factors or catastrophic events—commonly referred to as common shocks, leading to realization of random variables that are strongly dependent. For example, an accident or a natural disaster can cause claims in both personal injury and property damage, resulting in correlated claim counts and dependent losses in different insurance contracts or business lines. Capturing dependencies is essential for a realistic assessment of joint behavior of risks. While the use of copulas is popular (see e.g. Frees and Valdez, (1998) for a review), specific models for multivariate claim counts (e.g. Shi and Valdez, (2014); Pechon et al., (2018); Bolancé and Vernic, (2019); Fung et al., (2019)) and multivariate losses (e.g. Lee and Lin, (2012); Willmot and Woo, (2015)) have been developed as well. The presence of dependency has also led to related research topics in actuarial science, such as multivariate risk measures (see e.g. Cossette et al., (2016); Landsman et al., (2016)) and multivariate ruin problems (see e.g. Badila et al., (2015); Albrecher et al., (2022)).

Dependencies also commonly arise in the applied probability literature, and several approaches to constructing continuous multivariate phase-type distributions have been proposed in the field. These models often introduce dependencies by coupling the underlying Markov processes in specific ways, namely, by employing the exit times from different sets as in Assaf et al., (1984), or by using accumulating reward systems as in Kulkarni, (1989). In Bladt and Nielsen, (2010), a class of multivariate matrix-exponential (MME) distributions, characterized by rational multivariate Laplace transforms, was introduced. However, the multivariate matrix distributions in Kulkarni, (1989) and Bladt and Nielsen, (2010) do not necessarily admit closed-form probability density function in general, possibly limiting their applications. With an emphasis on explicit results and ease of applications in an actuarial context, recent efforts have also been made in Cheung et al., (2022); Bladt, (2023); Albrecher et al., (2023); Bladt and Yslas, 2023b to introduce new classes of distributions which are conditionally independent mixtures of matrix distributions. Specifically, in Bladt, (2023), the author proposed to employ a system of Markov jump processes that agree on the initial state and evolve independently from that point onward.

Despite the increasing interest in continuous multivariate matrix distributions mentioned above, extensions of the DPH class to a multivariate setting, particularly in the context of matrix distributions, are relatively scarce in the literature. One of the first attempts is the work by He and Ren, 2016a , who constructed a multivariate DPH distribution via the numbers of different types of batches that have arrived before absorption of a discrete-time Markov chain, with an accompanying estimation scheme discussed in He and Ren, 2016b . A discrete analog of Kulkarni, (1989)’s continuous multivariate phase-type distributions was considered in Navarro, (2019); however, such a class, like its continuous counterpart, does not admit closed-form expressions for the joint probability mass function (pmf). A more recent development was presented by Bladt and Yslas, 2023b which is a discrete version of Bladt, (2023)’s work, where the authors investigated the termination time of discrete-time Markov chains that begin in the same initial state but otherwise behave independently. However, many of these models impose dependencies that do not necessarily explicitly capture the common-shock scenarios that arise.

In this paper, we introduce a novel class of bivariate common-shock discrete phase-type (CDPH) distributions. Our approach extends the DPH framework to a bivariate setting by constructing two temporarily jointly evolving Markov chains that share a common evolution up to a random time—the occurrence of the common shock (or the number of common shocks)—after which they evolve independently. This construction effectively models the dependency induced by common shocks while retaining the tractability of DPH distributions. More precisely, we consider two discrete-time Markovian processes, and , which evolve identically until a decoupling time , after which they proceed independently and terminate at possibly different times and . We derive explicit expressions for the joint distribution of , which characterize the CDPH distributions. This framework allows us to model scenarios where two types of risks are affected by shared events before diverging due to independent factors. We can show that, in the bivariate case, our proposed class of CDPH distributions is larger than the class of multivariate DPH distributions in Bladt and Yslas, 2023b and is a subclass of that considered by Navarro, (2019). Building on this foundation, we explore applications of the CDPH distributions in risk modeling involving random sums with common shocks. In particular, we consider aggregate risks represented as sums of random variables whose counts are determined by and . This setup is particularly relevant in insurance, where aggregate claims may depend on both shared catastrophic events and independent claim occurrences. We characterize the joint distributions of these random sums, demonstrating the practicality and analytical convenience of our models.

Our contributions can be summarized as follows: We introduce the CDPH distributions, a new class of bivariate DPH distributions designed to effectively model dependencies induced by common shocks. To facilitate their applications in loss modeling, we provide explicit formulas for the joint pmf and probability generating function (pgf) of the CDPH class and prove various closure properties. Characterizations of the associated random sums are also provided. Furthermore, we develop estimation procedures for the CDPH distributions using the expectation-maximization (EM) algorithm, enabling their statistical implementation. Finally, we illustrate the applicability and effectiveness of our models through simulation studies, highlighting their potential in practical risk assessment scenarios. In essence, our work extends the versatility of phase-type distributions in modeling complex dependencies in arising in actuarial science, offering both theoretical insights and practical tools for actuaries and risk managers.

The remainder of the paper is organized as follows. In Section 2, we define the CDPH distributions and derive their fundamental properties. Section 3 applies these distributions to analyze random sums. In Section 4, we address the estimation of the CDPH distributions from data, proposing an EM algorithm tailored to our models. Section 5 presents simulation studies that demonstrate the implementation and performance of our estimation procedures, as well as an application to a dataset comprising bivariate insurance claim frequencies. Finally, Section 6 concludes the paper and suggests directions for future research.

2 A new class of CDPH distributions

This section provides some of the essential properties of CDPH distributions, starting from basic principles and then treating more intricate class properties. Throughout, we link our class to related constructions in the literature.

2.1 Background on DPH

Consider a Markov chain evolving in a finite state-space according to some initial probability vector and subprobability matrix , where is the set of non-negative integers. Here, is assumed to be (almost surely) terminating, meaning that while in state , it gets absorbed in the next step with probability . We note that if has no superfluous states, then the property of terminating is equivalent to the eigenvalues of being strictly contained in the complex unit circle (see e.g. Theorem 1.2.63 in Bladt and Nielsen, (2017)).

An alternative setup is to consider the augmented state-space , where is an absorbing cemetery state used to indicate the termination of . In this setup, evolves according to the probability vector and a block-partitioned transition matrix

where denotes a column vector of ones of appropriate dimension ( in this case), corresponds to the sum of probabilities from each state to all others in , and denotes a zero matrix of appropriate dimension (a zero row vector of dimension in this case). The final ‘1’ is a scalar representing the probability of remaining in the state once entered. Both setups—the terminating and the absorbing ones—are interchangeable for our purposes, and we switch back and forth depending on the situation.

Define to be the step in which gets terminated, that is, let

where is the set of positive integers. Then follows what is known as a DPH distribution, which we denote by . The class of DPH distributions is particularly tractable (see e.g. Chapter 1.2.6 in Bladt and Nielsen, (2017)). For instance, its pmf over is explicitly given by

Likewise, the pgf takes the tractable form

where denotes the identity matrix. Note that the above formula is valid for all on the real line such that the eigenvalues of lie within the complex unit circle (the set that contains the interval ).

2.2 Definition, joint probability and joint moments of CDPH

As mentioned in the introduction, literature on the construction of multivariate DPH distributions is rather limited. Our paper is inspired by the approach in Bladt and Yslas, 2023b , adding the flexibility that the Markov chains evolve synchronously for some period of time (rather than just starting in the same initial state) before proceeding independently. The exact details behind our novel construction are as follows. Consider two jointly evolving terminating processes, and , each taking values in the state space , where and . We construct the joint process such that each marginal process is a Markov chain, with a specific joint dependence structure: we let for all up to the first time they exit the set . After this point, they evolve independently within and eventually terminate, possibly at different times.

More explicitly, we let be a terminating Markov chain that evolves according to the block-partitioned initial probability vector and subprobability matrix

where is a subprobability matrix over (like before), denotes the transition probabilities from to , is a subprobability matrix over . It is further assumed that each row of the submatrix sums to one, so that the Markov chain (and also below) must enter before termination. For , we define for all , where

Obviously, follows a distribution. After time , we let evolve independently as a terminating Markov chain within according to the subprobability matrix . This construction yields as a Markov chain in that evolves according to the block-partitioned initial probability vector and subprobability matrix

We now define the bivariate random variable via the termination times of and so that, for ,

For each , the marginal distribution of is clearly . Moreover, and are greater than . Specifically, by writing and , one observes that and are dependent for two reasons:

-

•

Both and share the term , the time until which the Markov chains and evolve identically. The random variable can be regarded as the common shock component.

-

•

Although the Markov chains and evolve independently after time , the remaining times until they get absorbed (namely and ) are only conditionally independent given the state of the Markov chain at the time . Unconditionally, the variables and are dependent.

The joint distribution of is provided in the following proposition.

Proposition 2.1.

For , , and , define the unconditional and conditional joint pmf’s of by

and define the auxiliary functions

Then, we have

| (2.1) | ||||

| (2.2) |

and

| (2.3) | ||||

| (2.4) |

where and denote the one-step probabilities of termination from the states in for and , respectively; denotes the -th canonical column vector, and denotes the Hadamard (entrywise) product of two vectors.

Proof.

Using Proposition 2.1, one can readily show the following corollary.

Corollary 2.2.

For , the joint pgf of is given by

| (2.5) |

Moreover, the joint pgf of is given by

| (2.6) |

Employing Corollary 2.2, we are able to compute the cross moments of via the following result regarding falling factorial moments. Here, for and a generic random variable , we let denote the falling factorial of .

Corollary 2.3.

For , the joint factorial moments of are given by

| (2.7) |

where

with , and .

Proof.

It is standard that the -th falling factorial moment is obtained from the joint pgf (2.5) by taking derivatives with respect to for all and then evaluating at so that

Exploiting the linearity of differentiation yields (2.7) as long as one can prove the formula

where can be , or . It can be seen from the proof of Theorem 1.2.69 of Bladt and Nielsen, (2017) that the above equation is indeed valid, concluding our proof. ∎

Remark 2.1.

While Corollary 2.3 does not explicitly provide the cross moments of and , by writing and followed by applying binomial expansions of their powers, it can be readily seen that the afore-mentioned moments can be represented as linear combinations of the falling factorial moments in (2.7). For instance, one finds

Note that the support of is . For modeling purposes, it is often useful to consider discrete random variables that have a lattice different from . Thus, for and , one can define the vector where

| (2.8) |

We then say in a broad sense (see Remark 2.2) that the bivariate random variable follows a bivariate CDPH distribution with support on and parameters . Employing Proposition 2.1, we obtain the following immediate result.

Corollary 2.4.

Let follow a bivariate distribution with support and parameters . Then, the joint pmf of for and , namely , is given by

where .

2.3 Relationships with other bivariate DPH distributions

Let us first note that the (bivariate version of) the so-called class considered in Bladt and Yslas, 2023b is a subclass of our proposed . Indeed, if we let be a probability row vector and a subprobability matrix, then choosing the parameters , , , and for a over the lattice (i.e. and ) yields an distribution. This distribution arises from starting two terminating processes in the same state according to the initial probability vector then and evolving them independently from there onwards according to the subprobability matrix .

In turn, the with support in forms a subclass of the class introduced in Chapter 5.2 of Navarro, (2019). These distributions accumulate integer-valued rewards across each occupation epoch within a shared Markov chain, rather than bifurcating into independent processes after a common shock component concludes. Specifically, let us consider a partitioned state-space and a Markov chain defined over it. The chain evolves within while the common shock is ongoing, then jumps to (here we take the lexicographic order of ) while the independent components are active, and finally either terminates, jumps to , or jumps to . These transitions occur depending on whether the independent components terminate at the same time, the first coordinate terminates before the second, or the second coordinate terminates before the first. Thus, we define the bivariate random vector as

| (2.9) |

where corresponds to the termination time of so that . The above representation of the bivariate vector is already in the form of Equation (5.5) of Navarro, (2019). It remains to specify the transition probability of the terminating Markov chain .

To mimic the distributional properties of the original processes and embedded in the Markov chain , we take the block-partitioned parameters , and the subprobability matrix

| (2.10) |

where is defined by , with denoting the Kronecker delta and the -th element of , and represents the Kronecker product between matrices. Then, is . Note that the resulting parameters are similar to those used to compute the distribution of the maximum between two discrete phase-type distributions (Bladt and Nielsen,, 2017, Theorem 1.2.67). The derivation of these parameters for the process is as follows:

-

•

The process evolves in according to , mimicking the common shock component , eventually jumping from a state to a state with probability .

-

•

It then evolves in according to such that a transition from to occurs with probability (where, for , we use to denote the -th element of ). Then, either both components terminate simultaneously according to the exit column vector ; the first terminates while the second remains active, moving to ; or the second terminates while the first remains active, moving to .

-

•

If the process jumps to or , it continues evolving according to the matrix or , respectively.

The above results are summarized in the following proposition.

Proposition 2.5.

Concerning bivariate distributions, our proposed class satisfies the relationships

where is the class introduced by Bladt and Yslas, 2023b and is the class introduced by Navarro, (2019).

It is important to emphasize that, although the class in Navarro, (2019) is a larger class than our CDPH class on , a CDPH distributed bivariate random vector admits explicit joint pmf as in Proposition 2.1 while the same is not true for the class.

Remark 2.2.

Since the general distributed random vector in (2.8) with support on is merely linear transformation of its basic version which has support on , from now we shall simply use to denote the class with support on , and say that follows a distribution.

2.4 Further distributional and closure properties

Below, we explore further properties of the class. In particular, we investigate certain operations on the vector that belong to the class of or distributions.

Minimum and maximum between and

Consider again the Markov chain driven by (2.10), with initial vector , state-space and termination time . One can easily see that indeed corresponds to the maximum of and . Moreover, the minimum is simply the exit time of the Markov chain from the set . Defining the matrix

| (2.11) |

the next proposition follows as a direct consequence.

Aggregation of coordinates

When considering the sum of the coordinates of , it is helpful to represent it as . That is, counts twice the steps in which both and have not terminated, and then adds the steps during which the larger value exceeds the smaller one. Consequently, we have

| (2.12) |

We have the following proposition.

Proposition 2.7.

Given a random vector , the sum follows a distribution.

Proof.

With the representation (2.12) for the random variable , it follows from Theorem 5.2 in Navarro, (2019) that the distribution of is a mixture of a probability mass at zero and a distribution. However, both and are at least one from their definitions, implying that the afore-mentioned probability mass at zero must be non-existent and hence follows a distribution. The construction of the parameters of such a distribution can be found in Chapter 5.1.1.2 in Navarro, (2019) and is omitted for brevity. ∎

Mixture of CDPH random vectors

For each , suppose that the random vector is CDPH distributed. Let a mixture be formed where the component is chosen with probability . The following proposition shows that the class of CDPH distributions is closed under finite mixture.

Proposition 2.8.

Suppose that a mixture is formed such that a bivariate random vector is chosen to be with probability , such that is distributed and . Then, follows a distribution, where the parameters are given by

Proof.

Indeed, the initial distribution is simply a weighted combination of the initial probabilities of the component CDPH distributions, with weight assigned to . The transition matrix is a block-diagonal matrix, where each block corresponds to the transition matrix of the -th component. Similarly, and are block-diagonal matrices, where each block corresponds to , , and , respectively. Such block-diagonal structure ensures that there is no interaction among the components (i.e. across different ’s) once a specific component is chosen according to the mixing weights . This construction guarantees that the resulting parameters describe a valid CDPH distribution for . ∎

Sum of CDPH random vectors

Suppose that the random vector is CDPH distributed for each , and the random vectors are independent. Then one could be interested in the joint distribution of the sum . Indeed, this follows a CDPH distribution. In the next proposition, we provide a proof for the case and explicitly state the resulting parameters.

Proposition 2.9.

Consider the bivariate random vector , where is distributed for , and the random vectors and are independent. Then, follows a distribution, where the parameters are given by

| (2.13) |

| (2.14) |

| (2.15) |

with and . The state space corresponding to the transitions specified by is , and that for the transitions specified by and is . Here, with the obvious notation, is the state space of the underlying terminating Markov chains that define the vector .

Proof.

In order to explain the key ideas behind the proof, for it will be helpful to write . Here the random variable is the common shock component for the pair . We can thus decompose each coordinate of the random vector as

To show that follows a CDPH distribution, we note from the above representation that can be regarded as the common shock component from which we can construct . After and are realized and given the states in and entered upon exiting and , the variables and are conditionally independent: such observation can be used to construct and . The construction of the matrix parameters of the CDPH representation of is described as follows:

-

•

We start by considering the part that belongs to the common shock . The process underlying starts in with the initial probability (which explains (2.13)) and then transitions within according to . Upon exiting , the variable is realized and the process underlying enters according to . While one can start counting the remaining common shock component using the initial probability and transition probability matrix within , it is important to also keep track of the state in because this will have an impact on the distributions of and . These explain the block matrix representation of in (2.14). The submatrix of in (2.14) subsequently takes care of the termination of as the process exits and enters .

-

•

Once the underlying process of has entered , the clocks for and start ticking independently within the set according to the transition matrices and , respectively, while keeping the state in fixed. When (resp. ) terminates according to the probability vector (resp. ), one no longer needs to keep track of the state space , and then we move on to consider (resp. ) as the process evolves within according to (resp. ) until it gets absorbed. Such arguments lead to the specification of the matrices and in (2.15).

The above construction ensures that is CDPH distributed, and the proof is complete. ∎

It is clear that for values of greater than two still follows a CDPH distribution by summing the CDPH bivariate random vectors one at a time and using Proposition 2.9 repeatedly.

3 Compound sums under bivariate CDPH claim count

Having defined the class of bivariate CDPH distributions, we now turn our attention to a class of bivariate random variables with a random sum representation

| (3.1) |

where, for each coordinate , we aggregate a random number of positive variables , with the total number drawn from a bivariate CDPH distribution. In actuarial science, can be interpreted as bivariate claim count for correlated business lines. For , if are the individual claim amounts specific to line , then the compound sum corresponds to the aggregate loss for line . Before analyzing the distribution of in detail, we briefly outline the assumptions we make regarding the sequence . Firstly, we assume that is a sequence of independent and identically distributed bivariate random vectors following the same distribution as a reference random vector . Secondly, the sequence is independent of . While the CDPH distributed has support on , the cases where the counting variables are replaced by more general CDPH distributed with support on for can be addressed by modifying our arguments with minimal technical effort (see Remark 2.2).

We shall consider two scenarios for and : the case where they are independent, discussed in Subsection 3.1, and the case where they are dependent, addressed in Subsection 3.2.

3.1 Independent summands

Suppose that is independent of . Below, we provide information about the distribution of under this assumption.

Proposition 3.1.

For , the joint Laplace transform of the bivariate random sum in (3.1) is given by

where is the Laplace transform of for .

Proof.

By conditioning on , we have

The above expression is simply the joint pgf in (2.6) evaluated at the arguments . Since and are the Laplace transforms of positive random variables, one must have for . This yields the desired result. ∎

Proposition 3.1 provides a characterization of the distribution of in terms of the joint Laplace transform while leaving the distributions of and unspecified. It is easy to see that if and are rational in and respectively, then is rational in and . Since univariate rational Laplace transform characterizes matrix-exponential distributions (see e.g. Chapter 4 in Bladt and Nielsen, (2017)) while multivariate rational Laplace transform characterizes the class of MME distributions proposed by Bladt and Nielsen, (2010), we have the following corollary as an immediate consequence.

Corollary 3.2.

In the following subsection, we establish a related result by showing that if belongs to the subclass of multivariate phase-type distributions () proposed in Kulkarni, (1989) then so does . The main advantage of distributions is that, unlike the MME class, they possess a simple probabilistic interpretation.

3.2 Dependent summands

Here we assume that follows a bivariate version of Kulkarni’s class which we briefly describe next. Such an distribution is constructed using a single terminating continuous-time Markov jump process with finite state space and a system of state-dependent rewards. Specifically, let be the parameters, where:

-

•

is the initial probability vector;

-

•

is the subintensity matrix governing the continuous-time transitions between transient states; and

-

•

is the reward matrix, where represents the instantaneous non-negative reward associated to the -th state in and -th coordinate for .

With these elements, evolves according to and the coordinates and are defined via

where is the termination time of . The random vector obtained through this construction is said to follow an distribution.

This construction allows for capturing dependencies between and through the shared underlying Markov process . Apart from including independence as a special case, the class of distributions is known to be dense within the class of bivariate distributions with support on the positive quadrant. Unfortunately, the class is not particularly tractable in the general case as the joint distribution function cannot be expressed in closed form. However, its joint Laplace transform is known to be

for , where

Our aim is to prove that, under this setup, the bivariate random vector defined in (3.1) with each distributed as the generic bivariate random vector follows an distribution as well.

Proposition 3.3.

Suppose that each bivariate random vector in the sequence follows an distribution with parameters . Then the pair defined in (3.1) follows an distribution with an underlying continuous-time Markov jump process on the state-space , initial probability vector , subintensity matrix

and reward matrix

Here, for , the quantity represents the row vector such that

Proof.

We follow a probabilistic approach similar to that in Theorem 3.1.28 of Bladt and Nielsen, (2017). The key idea is to construct a continuous-time Markov jump process whose accumulated rewards correspond to the random variables and .

Recall is the discrete-time Markov chain that leads to the representation (2.9). That is, is a Markov chain on the state space . For each , suppose that is the process underlying the pair . Then, we concatenate independent realizations of ’s to match the number of steps of prior to termination. Thus, we construct a process that keeps track of the state of while simultaneously evolving within . After starting according to the initial distribution , the constructed process evolves as follows:

-

•

While in (representing the common-shock phase), evolves according to the transition matrix and evolves independently according to the subintensity matrix . In this phase, both and accumulate rewards, reflecting that both components are active.

-

•

When leaves , it transitions to with transition probabilities given by , and the constructed process moves into representing the phase after the common shocks. Here, evolves according to the Kronecker product , while continues to evolve according to . Both and continue to accumulate rewards.

-

•

If one of the components reaches absorption (i.e., transitions to or ), the process moves to or , respectively, representing single-coordinate continuation in or for the constructed process. In , only continues to accumulate rewards, while the reward accumulation for ceases. Conversely, in , only continues to accumulate rewards.

-

•

The process terminates when both components have reached absorption.

By constructing the Markov jump process as described and defining the rewards accordingly, we ensure that the accumulated rewards and correspond to the total occupation times of their respective components before absorption. This setup mirrors the dynamics of the original distribution for the pair , thus completing the proof. ∎

With the random vector fully characterized as an distribution, the joint moments of the pair follow directly from Theorem 8.1.5 in Bladt and Nielsen, (2017).

4 Estimation for bivariate CDPH random variables

We shall perform parameter estimation given the data , where each for is an independent realization from our proposed bivariate CDPH distribution. For later use, we denote as the joint process underlying the -th CDPH random vector with realization . We first review the fully observed case, and then proceed to provide maximum likelihood estimation through the use of the EM algorithm.

4.1 The fully observed case

Let the parameters be collected in . The likelihood is given by

where we place emphasis on the dependence of the pmf on by writing instead of (see Proposition 2.1).

While direct optimization via gradient methods is possible and relatively quick for very small dimensions, the EM algorithm is more precise and efficient for moderate matrix dimensions and . Thus, we introduce the following latent variables:

-

1.

: the number of times the processes start in state .

-

2.

: the total number of jumps of from state to .

-

3.

: the total number of jumps of from state to .

-

4.

: the total number of jumps of from state to , where .

-

5.

: the total number of jumps of from state to the absorbing state, where .

Having specified the above sufficient statistics, we are able to reconstruct the paths of each of the Markov jump processes. Recall that is the -th element of the row vector for as well as the notation , and . For , we further define to be the -th element of the column vector for . Then, we can write the complete likelihood as

The above specification is particularly convenient since it belongs to the exponential dispersion family of distributions, and thus has fully explicit maximum likelihood estimators (with a ‘’ placed on top of the corresponding parameter) given by

4.2 The EM algorithm

Since the full-trajectory data is not observed, we employ the EM algorithm to find the Maximum Likelihood Estimate iteratively. This implies that at each iteration, the conditional expectations of the sufficient statistics, given the absorption times, are computed, corresponding to the E-step. Subsequently such conditional expectations are replaced into instead of the statistics themselves, and so upon maximization, we obtain updated parameters , commonly referred to as the M-step.

The conditional expectations required in the E-step are given as follows:

Lemma 4.1.

Let be the observed data. The conditional expectations required in the E-step are given as follows:

Proof.

The key in all expressions is to apply the disintegration formula by conditioning on the common shock. All the remaining calculations then follow along similar lines as in the univariate case, since the paths evolve independently thereafter. ∎

5 Simulations and real data analysis

In this section, we investigate the flexibility and applicability of our proposed CDPH model on count data. Specifically, we conduct simulations involving bivariate Poisson and Poisson-Lindley distributions, followed by an application to real-world insurance claims data. Our focus is on assessing how well CDPH can capture or mimic these distributions.

5.1 Bivariate Poisson distribution with common shocks

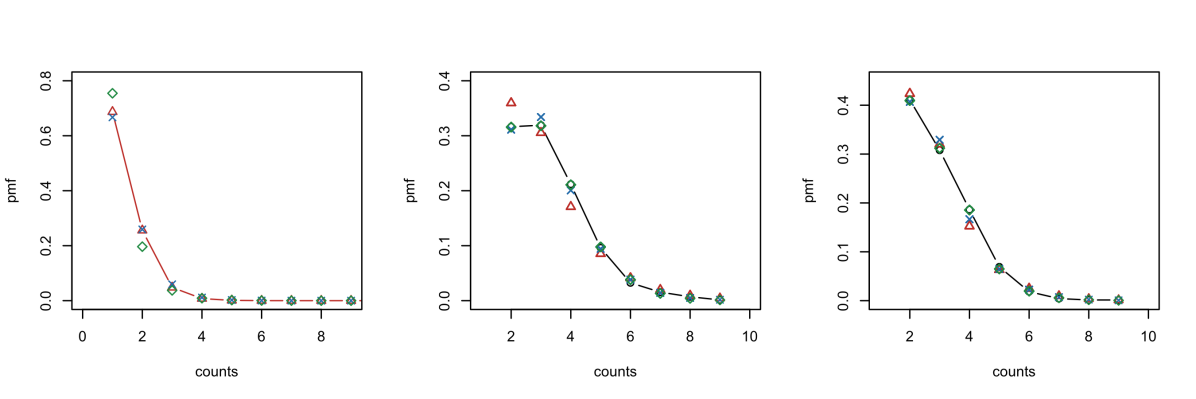

We begin by demonstrating that our proposed CDPH model can effectively fit a bivariate Poisson distribution. Although the Poisson distribution itself is not a special case of the DPH distribution, we aim to show that the CDPH model provides a good approximation.

To define the bivariate Poisson distribution, we let be a bivariate Poisson distributed pair such that and , where , , and are independent Poisson random variables with parameters , , and , respectively. Under this construction, the marginal distributions are again Poisson with intensities and . The joint pmf of is provided in Equation (2) of Holgate, (1964).

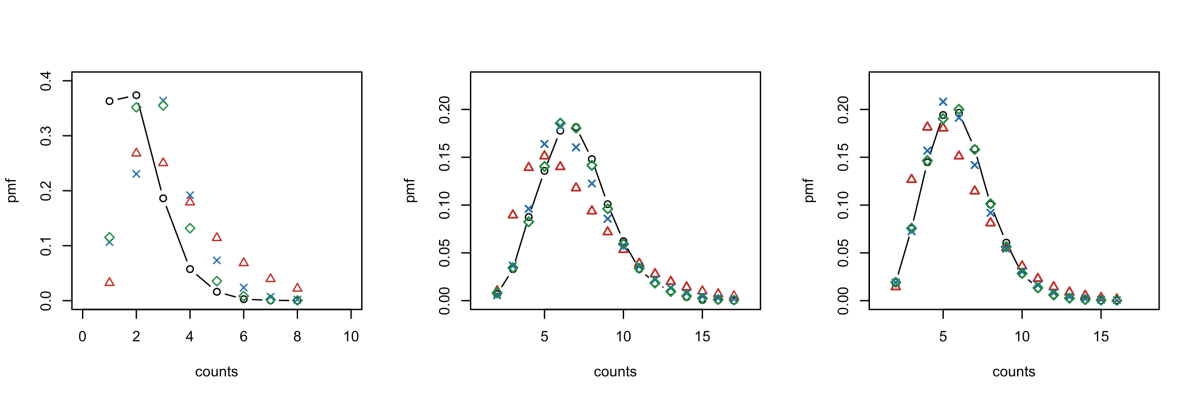

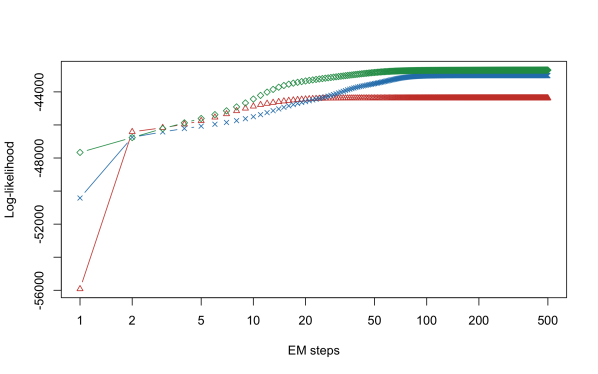

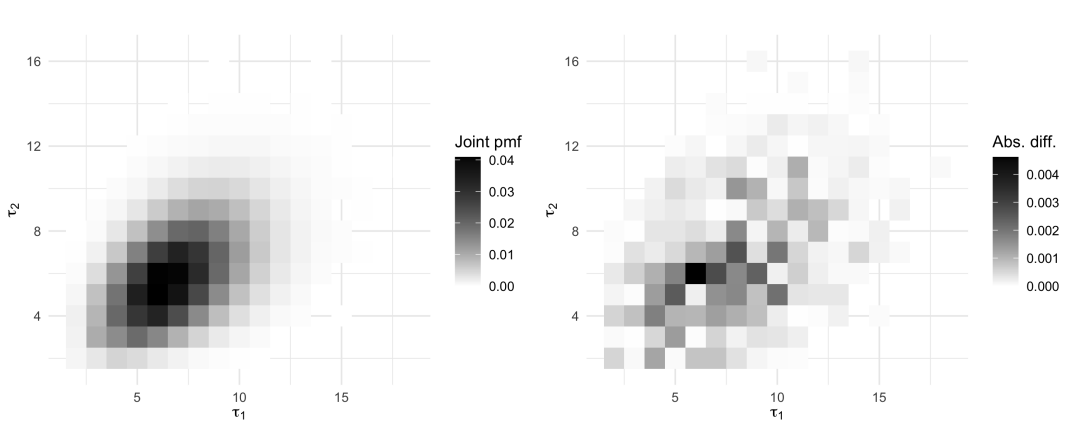

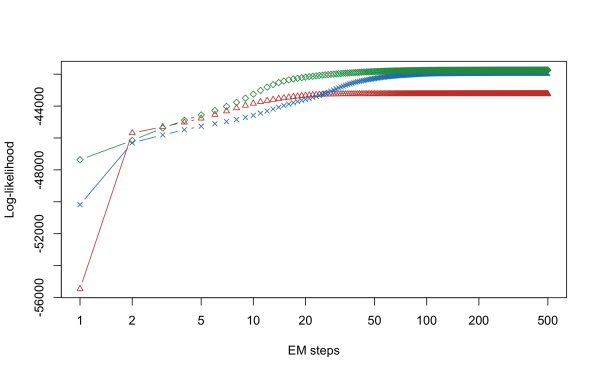

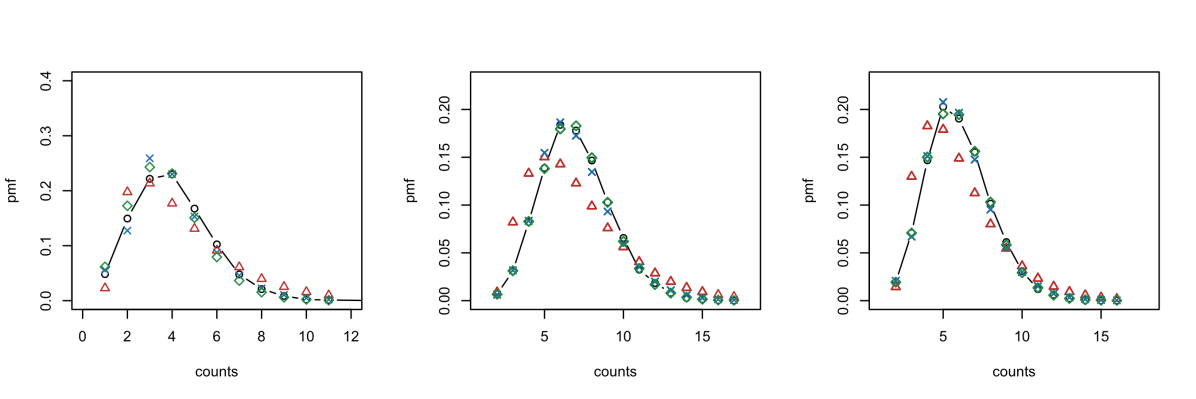

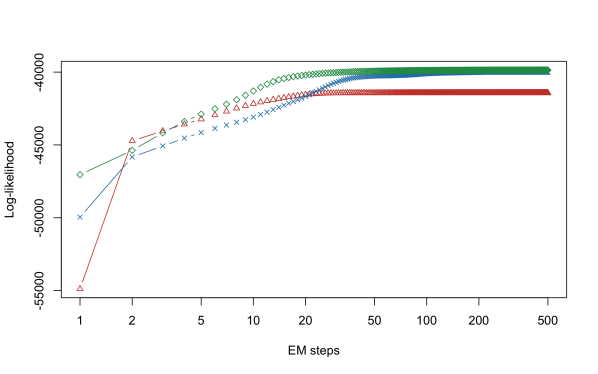

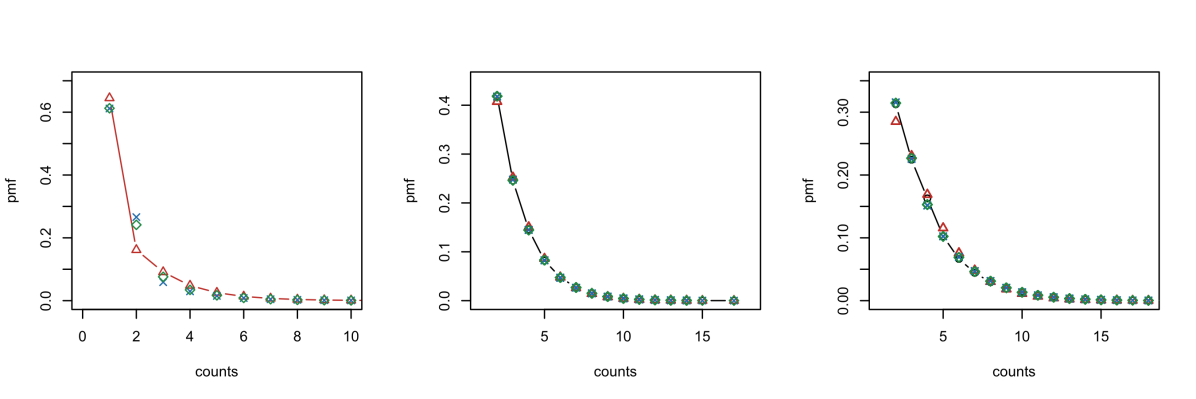

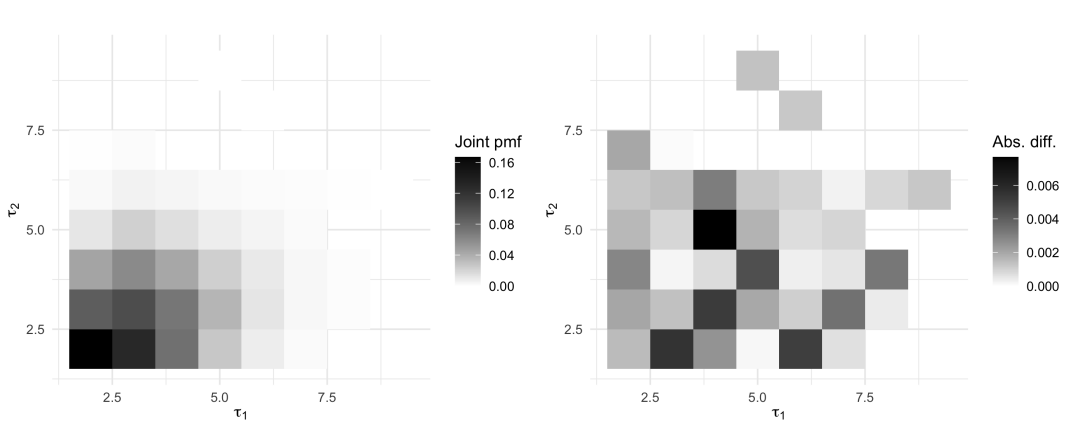

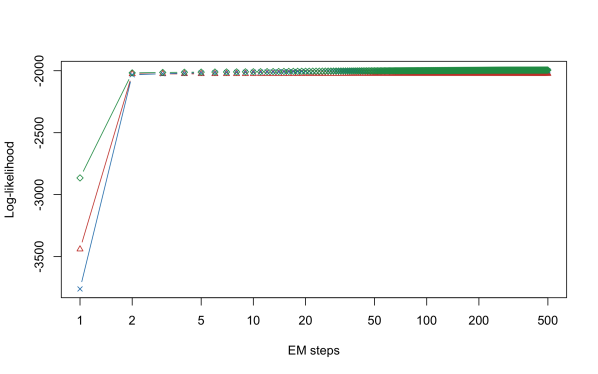

To evaluate the effectiveness of our model, we simulate data from and then fit using our CDPH approach111In this paper, the initial parameters for estimation are randomly generated (independent uniform random variables), suitably transformed to comply with the matrix constraints.. An interesting aspect of the study is to observe how the proposed model performs as the value of the common shock rate increases, while keeping and fixed. Specifically, we fix and and consider three different values of , namely 1, 2, and 3. The results are presented in Figures 5.1, 5.2, and 5.3. For each value of , we explore three different model configurations with dimensions , , and . Since matrix representations are not unique and hence not identifiable, the use of Akaike Information Criterion (AIC) and Bayesian Information Criterion (BIC) is not appropriate in this context. Instead, we track the evolution of the likelihood as a function of the EM iteration step to assess model performance.

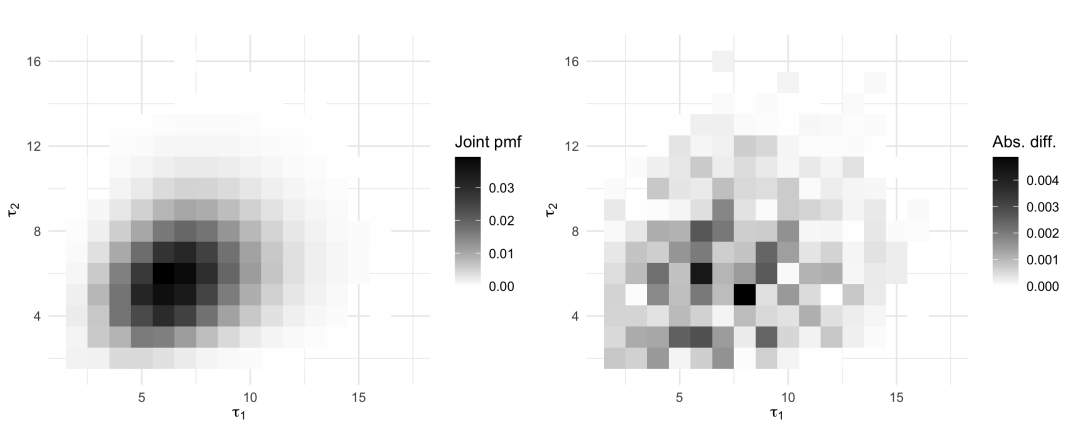

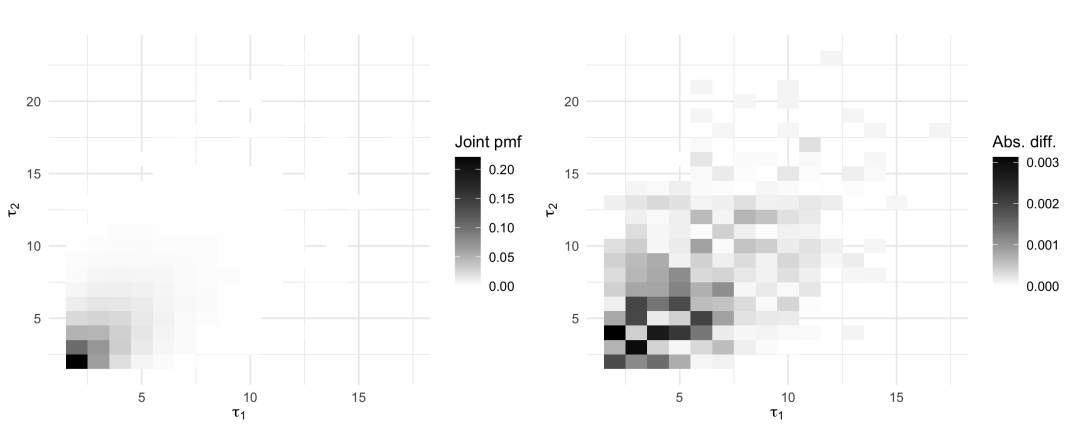

The simulations suggest that as the common shock component becomes more pronounced, our model captures it more effectively. Nevertheless, in all cases, the model provides a satisfactory fit, which is quantified through heatmap plots, showing the best fitted pmf among the three considered models (which is the most complex one with dimensions ), as well as the absolute difference between the empirical pmf and the best fitted one.

5.2 Bivariate Poisson-Lindley distribution

In addition to the bivariate Poisson case, we now investigate the ability of our model to capture overdispersion in claim counts, where the variance is not necessarily equal to the mean. The Poisson-Lindley is a mixture distribution that serves as a natural candidate for this setting. Specifically, the bivariate Poisson-Lindley distribution is constructed by considering conditionally independent Poisson random variables, where the Poisson parameter is mixed over a Lindley distribution that depends on a parameter (see Definition 2 in Gómez-Déniz et al., (2012)). The joint pmf in the bivariate case is also provided in Equation (17) of Gómez-Déniz et al., (2012).

To examine the performance of our model, we simulate from this distribution and apply our CDPH model to the transformed data . Concretely, we simulate a Lindley random variable with , and subsequently construct and as independent Poisson with parameters and , respectively. This is then repeated times. We again consider three model configurations with dimensions , , and . The evolution of the likelihood across EM iterations is tracked, as in the previous study, to assess convergence and fitting accuracy. The results are provided in Figure 5.4, and they further illustrate the adaptability of our CDPH approach in modeling overdispersed count data. Unlike the bivariate Poisson setting, the Poisson-Lindley mixture does not inherently possess a common shock component. Remarkably, however, our model is still able to effectively capture and mimic dependencies between the two components, demonstrating its practical modeling flexibility.

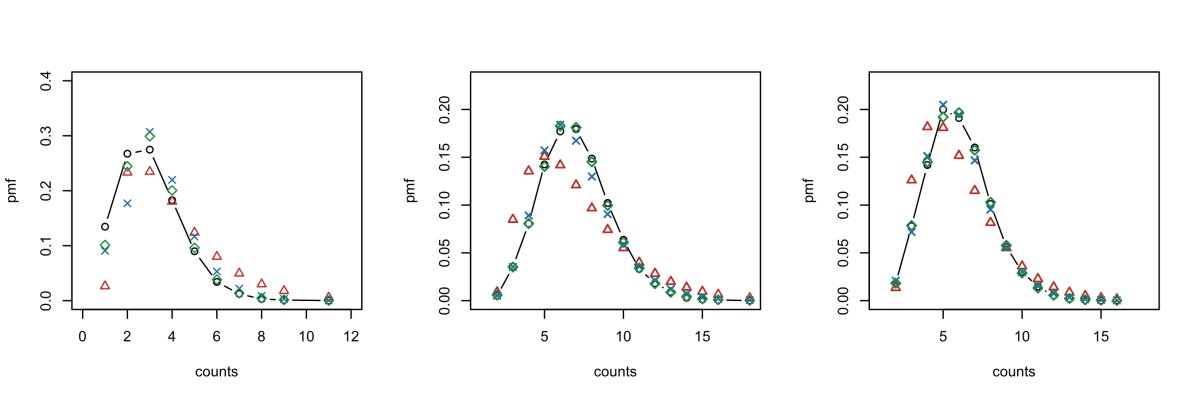

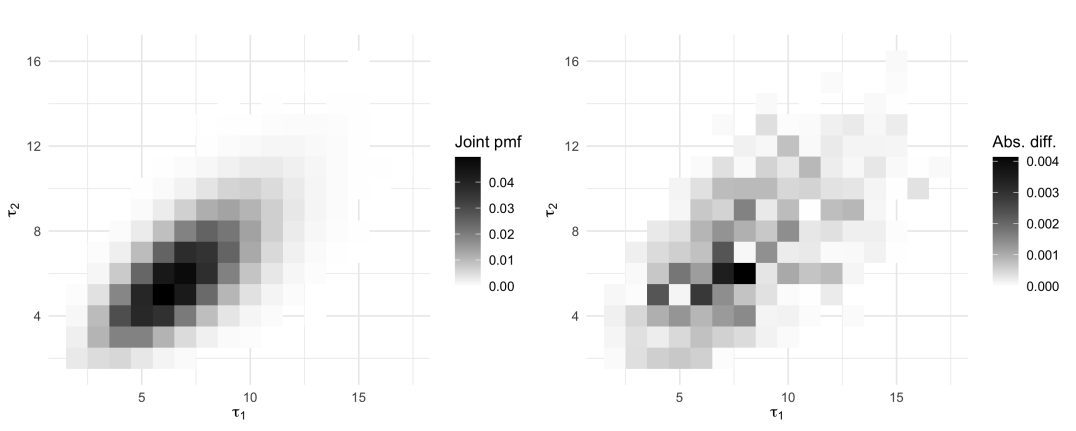

5.3 Application to insurance data

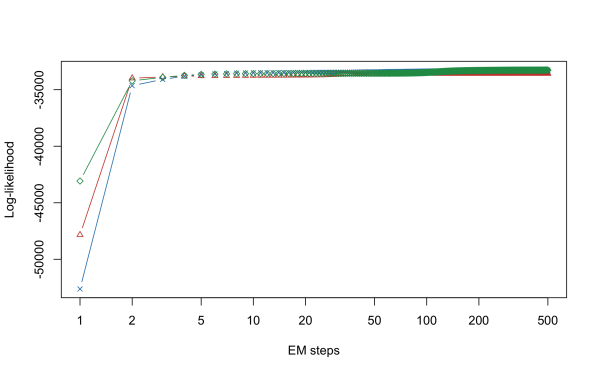

We now apply our model to real-world insurance data, previously analyzed in Vernic, (2000). The dataset can be found in Table 1 of Vernic, (2000), and was originally modeled using the bivariate generalized Poisson distribution (BGPD). It consists of claim frequencies from two related insurance categories, with a total of claims.

We fit this dataset to our proposed CDPH distribution, applying the same shift transformation as before. The plots in Figure 5.5 illustrate the results for the same three different model configurations: , , and . As with the previous cases, we track the likelihood evolution over EM iterations and evaluate the fit using probability plots. The CDPH model in general provides a good fit to the insurance dataset, even in the case of low dimensions. It is interesting to note that a non-negligible common shock component is estimated quite robustly by the three models, which by the previous simulation studies suggests that there could either be a true underlying common shock, or that the bivariate distribution is well approximated by the CDPH class. Despite the structural differences between BGPD and CDPH, our approach is also able to capture dependencies effectively.

6 Conclusion

In this paper, we have introduced a novel class of common-shock bivariate discrete phase-type distributions, abbreviated as CDPH, to model dependencies in risk models induced by common shocks. The key idea is that the two random variables of the CDPH distribution are defined as the termination times of two Markov chains that first evolve jointly (resembling common shocks influenced by shared risk factors) and then proceed independently (following individual-specific dynamics). In addition to deriving explicit and tractable formulas for the joint pmf and the joint pgf, we have also established clear relationships between our CDPH class and other classes of bivariate DPH distributions proposed by Bladt and Yslas, 2023b and Navarro, (2019). We have proved a number of closure properties of the CDPH class as well. In particular, , and are shown to be DPH whereas mixtures and sums of independent and identically distributed copies of belong to the CDPH class. Further properties of compound sums with CDPH claim counts are also discussed, and an EM algorithm for the CDPH class is developed for parameter estimation and subsequently implemented in our numerical studies.

Our proposed class of bivariate CDPH distributions opens up new research directions for modeling dependencies in multivariate risk modeling, particularly in situations where common shocks play a significant role. Future research could explore extensions to higher dimensions, incorporate covariate information, or consider the tail behavior through the introduction of inhomogeneity functions. We leave these as open questions.

Acknowledgement. MB would like to acknowledge financial support from the Swiss National Science Foundation Project 200021_191984, as well as from the Carlsberg Foundation, grant CF23-1096. EC and JKW acknowledge the support from the Australian Research Council’s Discovery Project DP200100615.

References

- Ahn et al., (2012) Ahn, S., Kim, J. H. T., and Ramaswami, V. (2012). A new class of models for heavy tailed distributions in finance and insurance risk. Insurance: Mathematics and Economics, 51(1):43–52.

- Albrecher et al., (2023) Albrecher, H., Bladt, M., and Müller, A. J. (2023). Joint lifetime modeling with matrix distributions. Dependence Modeling, 11(1):20220153.

- Albrecher et al., (2022) Albrecher, H., Cheung, E. C. K., Liu, H., and Woo, J.-K. (2022). A bivariate Laguerre expansions approach for joint ruin probabilities in a two-dimensional insurance risk process. Insurance: Mathematics and Economics, 103:96–118.

- Asmussen and Albrecher, (2010) Asmussen, S. and Albrecher, H. (2010). Ruin Probabilities (2nd edition). World Scientific.

- Assaf et al., (1984) Assaf, D., Langberg, N. A., Savits, T. H., and Shaked, M. (1984). Multivariate phase-type distributions. Operations Research, 32(3):688–702.

- Badescu and Landriault, (2009) Badescu, A. L. and Landriault, D. (2009). Applications of fluid flow matrix analytic methods in ruin theory - a review. RACSAM - Revista de la Real Academia de Ciencias Exactas, Fisicas y Naturales. Serie A. Matematicas, 103(2):353–372.

- Badila et al., (2015) Badila, E. S., Boxma, O. J., and Resing, J. A. C. (2015). Two parallel insurance lines with simultaneous arrivals and risks correlated with inter-arrival times. Insurance: Mathematics and Economics, 61:48–61.

- Bladt, (2023) Bladt, M. (2023). A tractable class of multivariate phase-type distributions for loss modeling. North American Actuarial Journal, 27(4):710–730.

- Bladt and Nielsen, (2010) Bladt, M. and Nielsen, B. F. (2010). Multivariate matrix-exponential distributions. Stochastic Models, 26(1):1–26.

- Bladt and Nielsen, (2017) Bladt, M. and Nielsen, B. F. (2017). Matrix-Exponential Distributions in Applied Probability. Springer.

- (11) Bladt, M. and Yslas, J. (2023a). Phase-type mixture-of-experts regression for loss severities. Scandinavian Actuarial Journal, 2023(4):303–329.

- (12) Bladt, M. and Yslas, J. (2023b). Robust claim frequency modeling through phase-type mixture-of-experts regression. Insurance: Mathematics and Economics, 111:1–22.

- Bolancé and Vernic, (2019) Bolancé, C. and Vernic, R. (2019). Multivariate count data generalized linear models: Three approaches based on the Sarmanov distribution. Insurance: Mathematics and Economics, 85:89–103.

- Cheung and Landriault, (2010) Cheung, E. C. K. and Landriault, D. (2010). A generalized penalty function with the maximum surplus prior to ruin in a MAP risk model. Insurance: Mathematics and Economics, 46(1):127–134.

- Cheung et al., (2022) Cheung, E. C. K., Peralta, O., and Woo, J.-K. (2022). Multivariate matrix-exponential affine mixtures and their applications in risk theory. Insurance: Mathematics and Economics, 106:364–389.

- Cossette et al., (2016) Cossette, H., Mailhot, M., Marceau, E., and Mesfioui, M. (2016). Vector-valued Tail Value-at-Risk and capital allocation. Methodology and Computing in Applied Probability, 18(3):653–674.

- Drekic et al., (2004) Drekic, S., Dickson, D. C. M., Stanford, D. A., and Willmot, G. E. (2004). On the distribution of the deficit at ruin when claims are phase-type. Scandinavian Actuarial Journal, 2004(2):105–120.

- Eisele, (2006) Eisele, K. T. (2006). Recursions for compound phase distributions. Insurance: Mathematics and Economics, 38(1):149–156.

- Fackrell, (2009) Fackrell, M. (2009). Modelling healthcare systems with phase-type distributions. Health Care Management Science, 12(1):11–26.

- Frees and Valdez, (1998) Frees, E. W. and Valdez, E. A. (1998). Understanding relationships using copulas. North American Actuarial Journal, 2(1):1–25.

- Frostig et al., (2012) Frostig, E., Pitts, S. M., and Politis, K. (2012). The time to ruin and the number of claims until ruin for phase-type claims. Insurance: Mathematics and Economics, 51(1):19–25.

- Fung et al., (2019) Fung, T. C., Badescu, A. L., and Lin, X. S. (2019). A class of mixture of experts models for general insurance: Application to correlated claim frequencies. ASTIN Bulletin, 49(3):647–688.

- Gómez-Déniz et al., (2012) Gómez-Déniz, P., Sarabia, J. M., and Balakrishnan, N. (2012). A multivariate discrete Poisson-Lindley distribution: Extensions and actuarial applications. ASTIN Bulletin, 42(2):655–678.

- Hassan Zadeh and Stanford, (2016) Hassan Zadeh, A. and Stanford, D. (2016). Bayesian and Bühlmann credibility for phase-type distributions with a univariate risk parameter. Scandinavian Actuarial Journal, 2016(4):338–355.

- (25) He, Q.-M. and Ren, J. (2016a). Analysis of a multivariate claim process. Methodology and Computing in Applied Probability, 18:257–273.

- (26) He, Q.-M. and Ren, J. (2016b). Parameter estimation of discrete multivariate phase-type distributions. Methodology and Computing in Applied Probability, 18(3):629–651.

- Holgate, (1964) Holgate, P. (1964). Estimation for the bivariate Poisson distribution. Biometrika, 51(1/2):241–245.

- Jensen, (1954) Jensen, A. (1954). A Distribution Model Applicable to Economics. Thesis Dissertation, Munksgaard, Copenhagen.

- Kulkarni, (1989) Kulkarni, V. G. (1989). A new class of multivariate phase type distributions. Operations Research, 37(1):151–158.

- Landsman et al., (2016) Landsman, Z., Makov, U., and Shushi, T. (2016). Multivariate tail conditional expectation for elliptical distributions. Insurance: Mathematics and Economics, 70:216–223.

- Lee and Lin, (2012) Lee, S. and Lin, X. S. (2012). Modeling dependent risks with multivariate Erlang mixtures. ASTIN Bulletin, 42(1):153–180.

- Lin and Liu, (2007) Lin, X. S. and Liu, X. (2007). Markov aging process and phase-type law of mortality. North American Actuarial Journal, 11(4):92–109.

- Navarro, (2019) Navarro, A. C. (2019). Order Statistics and Multivariate Discrete Phase-Type Distributions. Thesis Dissertation, Technical University of Denmark.

- Pechon et al., (2018) Pechon, F., Trufin, J., and Denuit, M. (2018). Multivariate modelling of household claim frequencies in motor third-party liability insurance. ASTIN Bulletin, 48(3):969 –993.

- Ren, (2010) Ren, J. (2010). Recursive formulas for compound phase distributions–univariate and bivariate cases. ASTIN Bulletin, 40(2):615–629.

- Shi and Valdez, (2014) Shi, P. and Valdez, E. A. (2014). Multivariate negative binomial models for insurance claim counts. Insurance: Mathematics and Economics, 55:18–29.

- Vernic, (2000) Vernic, R. (2000). A multivariate generalization of the generalized Poisson distribution. ASTIN Bulletin, 30(1):57–67.

- Wang et al., (2018) Wang, Y. F., Garrido, J., and Léveillé, G. (2018). The distribution of discounted compound PH-renewal processes. Methodology and Computing in Applied Probability, 20(1):69–96.

- Willmot and Woo, (2015) Willmot, G. E. and Woo, J.-K. (2015). On some properties of a class of multivariate Erlang mixtures with insurance applications. ASTIN Bulletin, 45(1):151–173.

- Wu and Li, (2010) Wu, X. and Li, S. (2010). Matrix-form recursions for a family of compound distributions. ASTIN Bulletin, 40(1):351–368.

Martin Bladt

Department of Mathematical Sciences, University of Copenhagen, Copenhagen, Denmark

Email address: martinbladt@math.ku.dk

Eric C. K. Cheung

School of Risk and Actuarial Studies, UNSW Business School, University of New South Wales, Sydney, Australia

Email address: eric.cheung@unsw.edu.au

Oscar Peralta

Department of Actuarial and Insurance Sciences,

Autonomous Technological Institute of México,

México City, México

Email address: oscar.peralta@itam.mx

Jae-Kyung Woo

School of Risk and Actuarial Studies, UNSW Business School, University of New South Wales, Sydney, Australia

Email address: j.k.woo@unsw.edu.au