Nested Expectations with Kernel Quadrature

Abstract

This paper considers the challenging computational task of estimating nested expectations. Existing algorithms, such as nested Monte Carlo or multilevel Monte Carlo, are known to be consistent but require a large number of samples at both inner and outer levels to converge. Instead, we propose a novel estimator consisting of nested kernel quadrature estimators and we prove that it has a faster convergence rate than all baseline methods when the integrands have sufficient smoothness. We then demonstrate empirically that our proposed method does indeed require fewer samples to estimate nested expectations on real-world applications including Bayesian optimisation, option pricing, and health economics.

1 Introduction

We consider the computational task of estimating a nested expectation, which is the expectation of a function that itself depends on another unknown conditional expectation. More precisely, let be a Borel probability measure with density on and a Borel probability measure with density on which is parameterized by . Given integrable functions and , we are interested in estimating:

| (1) |

Nested expectations arise within a wide range of tasks, such as the computation of objectives in Bayesian experimental design (Beck et al., 2020; Goda et al., 2020; Rainforth et al., 2024), of acquisition functions in active learning and Bayesian optimisation (Ginsbourger and Le Riche, 2010; Yang et al., 2024), of objectives in distributionally-robust optimisation (Shapiro et al., 2023; Bariletto and Ho, 2024; Dellaporta et al., 2024), and of statistical divergences (Song et al., 2020; Kanagawa et al., 2023). Computing nested expectations is also a key task beyond machine learning, including in fields ranging from health economics (Giles and Goda, 2019) to finance and insurance (Gordy and Juneja, 2010; Giles and Haji-Ali, 2019), manufacturing (Andradóttir and Glynn, 2016) and geology (Goda et al., 2018).

The estimation of nested expectations is particularly challenging since there are two levels of intractability: the inner conditional expectation, and the outer expectation, both of which must be approximated accurately in order to approximate accurately. The most widely used algorithm for this problem is nested Monte Carlo (NMC) (Lee and Glynn, 2003; Hong and Juneja, 2009; Rainforth et al., 2018). It approximates the inner and outer expectations using Monte Carlo estimators with and samples respectively. NMC is consistent under mild conditions, but has a relatively slow rate of convergence. Depending on the regularity of the problem, existing results indicate that we require either or evaluations of to obtain a root mean squared error smaller or equal to . This tends to be prohibitively expensive; for example, we would expect in the order of either or million observations to obtain an error of . This will be infeasible for the many applications where obtaining samples or evaluating is expensive.

This issue has led to the development of a number of methods aiming to reduce the cost. Bartuska et al. (2023) proposed replacing the Monte Carlo estimators with quasi-Monte Carlo (QMC) (Dick et al., 2013). This algorithm, called nested QMC (NQMC), requires only function evaluations to obtain an error of size (so that we only need in the order of observations for an error of ). However, NQMC requires strong regularity assumptions which may not hold in practice (a monotone second and third derivative for ). Separately, Bujok et al. (2015); Giles and Haji-Ali (2019); Giles and Goda (2019) proposed to use multi-level Monte Carlo (MLMC) and showed that this can further reduce the number of function evaluations to (so that we only need in the order of observations for an error of ). The algorithm has relatively mild assumptions on and , which makes it broadly applicable but sub-optimal for applications where and are smooth and where we might therefore expect further reductions in cost.

To fill this gap in the literature, we propose a novel algorithm called nested kernel quadrature (NKQ), which is presented in Section˜3. NKQ replaces the inner and outer MC estimators of NMC with kernel quadrature (KQ) estimators (Sommariva and Vianello, 2006). We show in Section˜4 that NKQ requires only function evaluations to guarantee an error smaller or equal to . Here denotes up to logarithmic terms. Here, are constants relating to the smoothness of and in and , and we have and . In the least favorable case, we therefore recover the of NMC, but when the integrand is smooth and the dimension is not too large, we are able to have a cost which scales better than and the method significantly outperforms all competitors. In those cases, we may only need in the order of a few hundred or thousands observations for an error of . This fast rate is demonstrated numerically in Section˜5, where we show that NKQ can provide significant accuracy gains in problems from Bayesian optimisation to option pricing and health economics. Moreover, we show that NKQ can be combined with QMC and MLMC, providing an avenue to further accelerate convergence.

2 Background

Notation

Let denote the positive integers and . For , and are vectorized notation for and respectively. For a vector , define . For a distribution supported on and , is the space of functions such that and is the space of functions that are bounded -almost everywhere. When is the Lebesgue measure over , we write . For , denotes the space of functions whose partial derivatives of up to and including order are continuous. For two positive sequences and , means that is a positive constant. For two positive functions , means that and means that for some positive constant .

Existing Methods for Nested Expectations

Standard Monte Carlo (MC) is an estimator which can be used to approximate expectations/integrals through samples (Robert and Casella, 2000). Given an arbitrary function with , and independent and identically distributed (i.i.d.) realisations from , standard MC approximates the expectation of under as follows:

For the nested expectation in (1), the use of a MC estimator for both the inner and outer expectation leads to the nested Monte Carlo (NMC) estimator (Hong and Juneja, 2009; Rainforth et al., 2018) given by

| (2) |

where are i.i.d. realisations from and are i.i.d. realisations from for each . The root mean-squared error of this estimator goes to zero at rate when is Lipschitz continuous (Rainforth et al., 2018). Hence, taking leads to an algorithm which requires function evaluations to obtain error smaller or equal to . When has bounded second order derivatives, the root mean-squared error converges at the improved rate of (Rainforth et al., 2018). Taking therefore leads to an algorithm requiring function evaluations to get an error of (Gordy and Juneja, 2010; Rainforth et al., 2018). Despite its simplicity, NMC therefore requires a large number of evaluations to reach a given .

As a result, two extensions have been proposed. Firstly, Bartuska et al. (2023) proposed to use (2), but to replace the i.i.d. samples with QMC points. QMC points are points which aim to fill in a somewhat uniform fashion (Dick et al., 2013), with well-known examples including Sobol or Halton sequences. Bartuska et al. (2023) used randomized QMC points, which removes the bias of standard QMC by using a randomized low discrepancy sequence (Owen, 2003). For nested expectations, they showed that nesting randomized QMC estimators can lead to a faster convergence rate and hence a smaller cost of . However, the approach is only applicable when and are Lebesgue measures on unit cubes (or smooth transformations thereof), and the rate only holds when has monotone second and third order derivatives.

Alternatively, Bujok et al. (2015); Giles (2015); Giles and Haji-Ali (2019); Giles and Goda (2019) proposed to use multi-level Monte Carlo (MLMC), which decomposes the nested expectation using a telescoping sum on the outer integral, then approximates each term with MC. The integrand with the ’th fidelity level is constructed as the composition of with an inner MC estimator based on samples. More precisely, the MLMC treatment of nested expectations consist of using:

| (3) |

Under some regularity conditions, Theorem 1 from Giles (2015) shows that taking and leads to an estimator requiring function evaluations to obtain root mean squared error smaller or equal to . Although MLMC has the best known efficiency for nested expectations, the and need to grow exponentially with , and we therefore need a very large sample size for its theoretical convergence rate to become evident in practice (Giles and Haji-Ali, 2019; Giles and Goda, 2019). MLMC also requires making several challenging design choices, including the coarsest level to use, and the number of samples per level. Most importantly, MLMC as well as all existing methods fail to account for the smoothness of the functions and .

Kernel Quadrature

Kernel quadrature (KQ) (Sommariva and Vianello, 2006; Rasmussen and Ghahramani, 2002; Briol et al., 2019) provides an alternative to standard MC for (non-nested) expectations. Consider an arbitrary function and distribution on , and suppose we would like to approximate . KQ is an estimator which can be used when is sufficiently regular, in the sense that it belongs to a reproducing kernel Hilbert space (RKHS) (Berlinet and Thomas-Agnan, 2004) with kernel . We recall that for a positive semi-definite kernel , the RKHS is a Hilbert space with inner product and norm (Aronszajn, 1950) such that: (i) for all , and (ii) the reproducing property holds, i.e. for all , , . An important example of RKHS is the Sobolev space (), which consists of functions of certain smoothness encoded through the square integrability of their weak partial derivatives up to order ,

| (4) |

where denotes the -th (weak) partial derivative of .

Assuming and , the KQ estimator uses weights obtained by minimizing an upper bound on the absolute error:

where is the kernel mean embedding (KME) of in the RKHS (Smola et al., 2007). Minimizing the right hand side with an additive regulariser term over the choice of weights leads to the KQ estimator:

| (5) |

where is the identity matrix, is the Gram matrix and is a regularisation parameter ensuring the matrix is numerically invertible. The KQ weights are given by and are optimal when .

KQ takes into account the structural information that so the absolute error goes to at a fast rate as . Specifically, when the RKHS is the Sobolev space (), KQ achieves the rate (Kanagawa and Hennig, 2019; Kanagawa et al., 2020). This is known to be minimax optimal (Novak, 2006, 2016), and significantly faster than the rate of standard MC. Interestingly, existing proof techniques that obtain this rate take in (5) and require the Gram matrix to be invertible, whilst the new proof technique based on kernel ridge regression in this paper obtains the same optimal rate while allowing a positive regularization , which improves numerical stability when inverting . (See ˜B.2)

Despite the optimality of the KQ convergence rate, the rate constant can be reduced by selecting points other than through i.i.d. sampling. Strategies include importance sampling (Bach, 2017; Briol et al., 2017), QMC point sets (Briol et al., 2019; R. Jagadeeswaran, 2019; Bharti et al., 2023; Kaarnioja et al., 2025), realisations from determinental point processes (Belhadji et al., 2019), point sets with symmetry properties (Karvonen and Särkkä, 2018; Karvonen et al., 2019) and adaptive designs (Osborne et al., 2012; Gunter et al., 2014; Briol et al., 2015; Gessner et al., 2020). Most relevant to our work is the combination of KQ with MLMC to improve accuracy in multifidelity settings (Li et al., 2023).

The two main drawbacks of KQ compared to MC are the worst-case computational cost of (due to computation of the inverse of the Gram matrix), and the need for a closed-form expression of the KME . Fortunately, numerous approaches can mitigate these drawbacks. To reduce the cost, one can use geometric properties of the point set (Karvonen and Särkkä, 2018; Karvonen et al., 2019; Kuo et al., 2024), Nyström approximations (Hayakawa et al., 2022, 2023), randomly pivoted Cholesky (Epperly and Moreno, 2023), or the fast Fourier transform (Zeng et al., 2009). To obtain a closed-form KME, KQ users typically refer to existing derivations (see Table 1 in Briol et al. (2019) or Wenger et al. (2021)), or use Stein reproducing kernels (Oates et al., 2017, 2019; Si et al., 2021; Sun et al., 2023).

In this paper, we tackle both drawbacks through a change of variable trick. Suppose we can find a continuous transformation map such that where are samples from a simpler distribution of our choice. A direct application of change of variables theorem (Section 8.2 of Stirzaker (2003)) proves that , so the integrand changes from to and the kernel quadrature estimator becomes , where . The measure is typically chosen such that the KME is known in closed-form, and the KQ weights can be pre-computed and stored so that KQ becomes a weighted average of function evaluations with computational complexity. See Section˜F.1 for further details.

Before concluding, we note that the KQ estimator is often called Bayesian quadrature (BQ) (Diaconis, 1988; O’Hagan, 1991; Rasmussen and Ghahramani, 2002; Briol et al., 2019; Hennig et al., 2022) since it can be derived as the mean of the pushforward of a Gaussian measure on conditioned on (Kanagawa et al., 2018). The advantage of the Bayesian interpretation is that it provides finite-sample uncertainty quantification, and it also allows for efficient hyperparameter selection through empirical Bayes.

3 Nested Kernel Quadrature

We can now present our novel algorithm: nested kernel quadrature (NKQ). To simplify the formulas, we write

| (6) |

so that the nested expectation in (1) can be written as . We will assume that we have access to

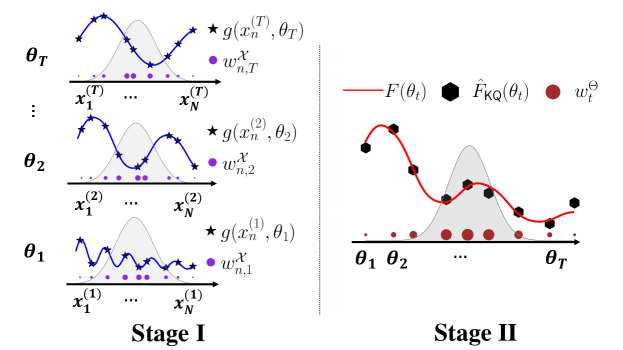

for all , and is a function that can be evaluated. We do not specify how the point sets are generated, although further (mild) assumptions will be imposed for our theory in Section˜4. Using the same number of function evaluations per is not essential, but we assume this as it significantly simplifies our notation. Given the above, we are now ready to define NKQ as the following two-stage algorithm, which is illustrated in Figure˜1.

Stage I

For each , we estimate the inner conditional expectation evaluated at with observations and using a KQ estimator:

| (7) |

Here is a reproducing kernel on , is the KME of and is an Gram matrix. Using the same kernel for each is not essential, but we assume this to be the case for simplicity. Given these KQ estimates, we then we apply the function to get .

Stage II

We use a KQ estimator to approximate the outer expectation using the output of Stage I:

| (8) |

Here is a reproducing kernel on , is the embedding of and is a Gram matrix.

Combining stage I and II, NKQ can be expressed in a single equation as a nesting of two quadrature rules:

| (9) |

where are the KQ weights used in stage I for and are the KQ weights used in stage II. Although these weights are stage-wise optimal when thanks to the optimality of KQ weights, it is unclear whether they are globally optimal due to the non-linearity of . Note that NMC can be recovered by taking all stage I weights to be and all stage II weights to be , which is sub-optimal.

NKQ inherits the two main drawbacks of KQ. Firstly, solving the linear systems to obtain the stage I and II weights has a worst-case computational complexity of . Secondly, NKQ requires closed-form KMEs at both stages: for all in stage I, and in stage II. Fortunately, we can use the approaches discussed in the previous section to reduce the complexity to and obtain closed-form kernel embeddings.

NKQ requires the selection of hyperparameters, including for the kernels in both stage I and II. We typically take and to be Matérn kernels whose orders are determined by the smoothness of and (as justified by ˜1; see Section˜4 for details). This leaves us with a choice of kernel hyperparameters which include lengthscales and amplitudes . The lengthscales are selected via the median heuristic. The regularizers are set to and where is selected with grid search over following ˜1. Finally, we standardise our function values (by subtracting the empirical mean then dividing by the empirical standard deviation), and then set the amplitudes to . This last choice could further be improved using a grid search, but we do not do this as we do not notice significant improvements when doing so in experiments and this tends to increase the cost.

Before presenting our theoretical results, we briefly comment on the connection with existing KQ methods. If we could evaluate the exact expression for the inner conditional expectation pointwise, then (following (5)) the KQ estimator for would be . Comparing with (8), NKQ can thus be seen as KQ with noisy function values (replacing the exact values in (8)). Although it is proved in Cai et al. (2023) that noisy observations make KQ converge at a slower rate, we prove that the stage II observation noise is of the same order as the stage I error, and consequently, we can still treat stage II KQ as noiseless kernel ridge regression and the additional error caused by the stage II observation noise would be subsumed by the stage I error (See ˜4.1). NKQ is also closely related to a family of regression-based methods for estimating conditional expectations (Longstaff and Schwartz, 2001; Chen et al., 2024b). Indeed, with a slight modification of Stage II in (8), we can obtain an estimator of that we call conditional kernel quadrature (CKQ)

| (10) |

CKQ highly resembles conditional BQ (CBQ) (Chen et al., 2024b); the difference is in stage II, where CBQ uses heteroskedastic Gaussian process regression whilst CKQ uses kernel ridge regression. Interestingly, the proof in this paper leads to a much better rate for CKQ than the best known rate for CBQ (see ˜4.2).

4 Theoretical Results

In this section, we derive a convergence rate for the absolute error as the number of samples . Before doing so, we recall the connection between RKHSs and Sobolev spaces. A kernel on is said to be translation invariant if for some positive definite function whose Fourier transform is a finite non-negative measure on (Wendland, 2004, Theorem 6.6). Suppose has a Lipschitz boundary, if is translation invariant and its Fourier transform decays as when for , then its RKHS is norm equivalent to the Sobolev space (Wendland, 2004, Corollary 10.48). More specifically, it means that their set of functions coincide and there are constants such that holds for all . In this paper, we call such kernel a Sobolev reproducing kernel of smoothness . An important example of Sobolev kernel is the Matérn kernel— the RKHS of a Matérn- kernel is norm-equivalent to with . All Sobolev kernels are bounded, i.e. for some positive constant . When the context is clear, we use to denote the Sobolev space norm.

Theorem 1.

Let and . Suppose are i.i.d. samples from and are i.i.d samples from for all . Suppose further that and are Sobolev kernels of smoothness and , and that the following conditions hold

-

(1)

There exist such that ; and for any , .

-

(2)

There exists such that for any and any with , .

-

(3)

There exist such that for any , and .

-

(4)

There exists such that derivatives of up to and including order are bounded by .

Then, there exists such that for , we can take and to obtain the following bound

which holds with probability at least . are two constants independent of .

Corollary 1.

Suppose all assumptions in ˜1 hold. If we set and , then samples are sufficient to guarantee that holds with high probability.

To prove these results, we can decompose into the sum of stage I and stage II errors, which can be bounded by terms of order and respectively; see Appendix˜C. Interestingly, note that the stage II error does not suffer from the fact that we are using noisy observations and we maintain the standard KQ rate up to logarithmic terms (see ˜4.1). We emphasize that our bound indicates that the tail behavior of is sub-exponential. This contrasts with existing work on Monte Carlo methods, which typically only provides upper bounds on the expectation of error with no constraints on its tails (Giles, 2015; Bartuska et al., 2023).

We now briefly discuss our assumptions. Assumption LABEL:as:equivalence is mild and allows (resp. ) to be norm equivalent to (resp. ), which is widely used in statistical learning theory that involves Sobolev spaces (Fischer and Steinwart, 2020; Suzuki and Nitanda, 2021). Since our proof essentially translates quadrature error into generalization error of kernel ridge regression, Assumptions LABEL:as:app_true_g_smoothness, LABEL:as:app_true_J_smoothness, LABEL:as:app_lipschitz ensure that functions and the density have enough regularity so that the regression targets in both stage I and stage II belong to the correct Sobolev spaces. These are more restrictive, but are essential to obtain our fast rate and are common assumptions in the KQ literature. Assumptions LABEL:as:app_true_g_smoothness, LABEL:as:app_true_J_smoothness, LABEL:as:app_lipschitz can be relaxed if mis-specification is allowed; see e.g. Fischer and Steinwart (2020); Kanagawa et al. (2023); Zhang et al. (2023). ˜1 shows that for NKQ to have a fast convergence rate, one ought to use Sobolev kernels which are as smooth as possible in both stages. Furthermore, when (e.g. when the integrand and kernels belong to Gaussian RKHSs), our proof could be modified to show an exponential rate of convergence in a similar fashion as Briol (2018, Theorem 10) or Karvonen et al. (2020).

Remark 4.1 (Noisy observations in Stage II of NKQ).

Note that NKQ employs noisy observations in stage II kernel quadrature rather than the ground truth observations . Although Cai et al. (2023) establishes that kernel quadrature (KQ) with noisy observations converges at a slower rate than KQ with noiseless observations, a key distinction in our setting is that, as shown in (C), the observation noise in stage II KQ is of order , whereas the noise in Cai et al. (2023) remains at a constant level. As a result, we can still use KQ in stage II as if the observations are noiseless, and the additional error it introduces happens to be of the same order as the stage I error and is therefore subsumed by it.

Remark 4.2 (Convergence rate for CKQ).

For CKQ estimator defined in (10) from Section˜3 that approximates the parametric expectation uniformly over all , its error can be upper bounded in the same way as NKQ. For defined in (C.11), the error of can be decomposed as following:

The first term corresponds to the stage I error and can be shown to be using the same analysis from (C) to (C.16). The second term corresponds to the stage II error and can be shown to be using the same analysis from (C) to (C). Combining the two error terms, we have holds with probability at least . The rate is better than the best known rate of CBQ proved in Theorem 1 of (Chen et al., 2024b) since . The intuition behind the faster rate is that CKQ benefits from the extra flexibility of choose regularization parameters ; while CBQ, as a two stage Gaussian Process based approach, is limited to choose equal to the heteroskedastic noise from the first stage. It may be possible to modify the proof of (Chen et al., 2024b) to improve the rate further, but this has not been explored to date.

| Method | Cost |

|---|---|

| NMC | or |

| NQMC | |

| MLMC | |

| NKQ (˜1) |

In Table˜1, we compare the cost of all methods evaluated by the number of evaluations required to ensure . We can see that NKQ is the only method that explicitly exploits the smoothness of in the problem so that it outperforms all other methods when .

We have previously mentioned that KQ could potentially be combined with other algorithms to further improve efficiency, and studied this for both MLMC and QMC. For the former (i.e. NKQ+MLMC), we derived a new method called multi-level NKQ (MLKQ), which closely related to multilevel BQ algorithm of Li et al. (2023) and for which we were able to prove a rate of . Similarly to NKQ, when , the rate for MLKQ is faster than that of NMC, NQMC and MLMC. However, the rate we managed to prove is slower than that for NKQ, and a slower convergence was also observed empirically (see Figure˜6). We speculate that the worse performance is caused by the accumulation of bias from the KQ estimators at each level. See Section˜D.2 for details.

We also consider combining NKQ and QMC. In this case, we expect the same rate as in ˜1 can be recovered by resorting to the fill distance technique in scatter data approximation (Wendland, 2004). This is confirmed empirically in Section˜5, where we observe that using QMC points can achieve similar or even better performance than NKQ with i.i.d. samples.

5 Experiments

We now illustrate NKQ over a range of applications, including some where the theory does not hold but where we still observe significant gains in accuracy. The code to reproduce experiments is available at https://github.com/hudsonchen/nest_kq.

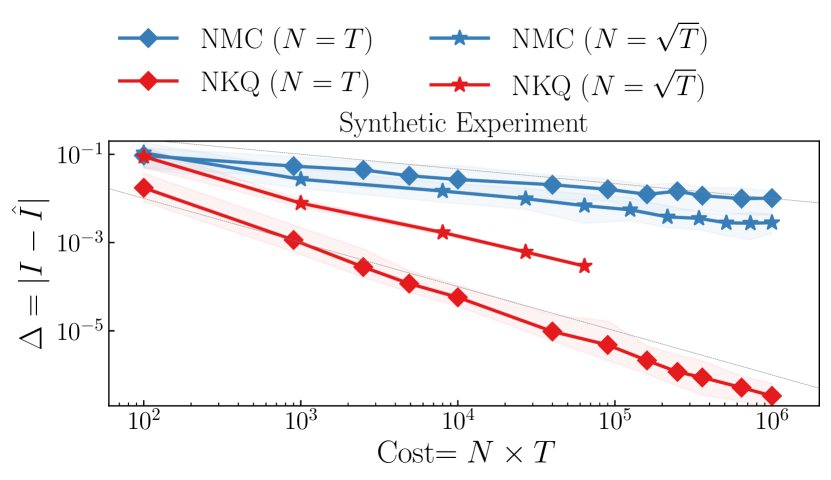

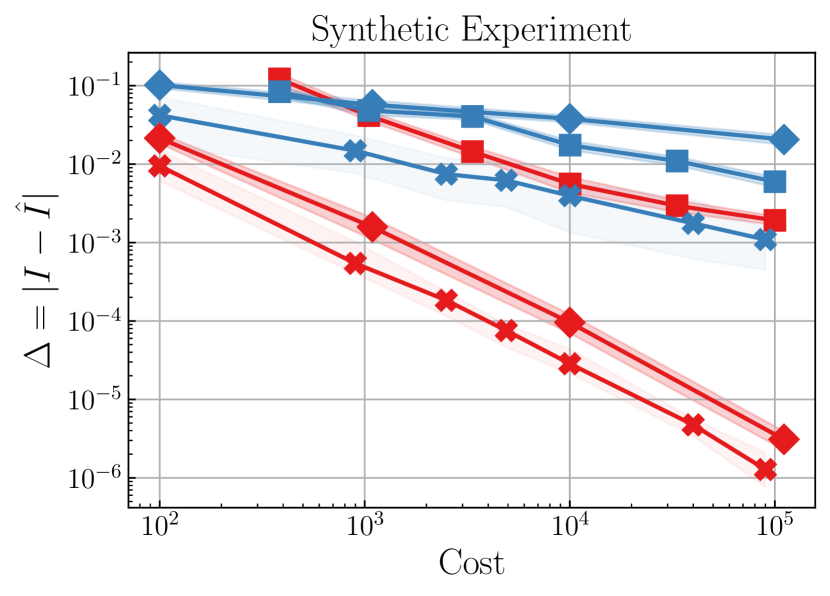

Synthetic Experiment

We start by verifying the bound in ˜1 using the following synthetic example: , , , and , in which case can be computed analytically. We estimate with i.i.d. samples and i.i.d. samples for . The assumptions from ˜1 are satisfied with and (see Section˜F.2). Therefore, to reach the absolute error threshold , we choose for NKQ following ˜1. On the other hand, based on Theorem 3 of Rainforth et al. (2018), the optimal way of assigning samples for NMC is to choose .

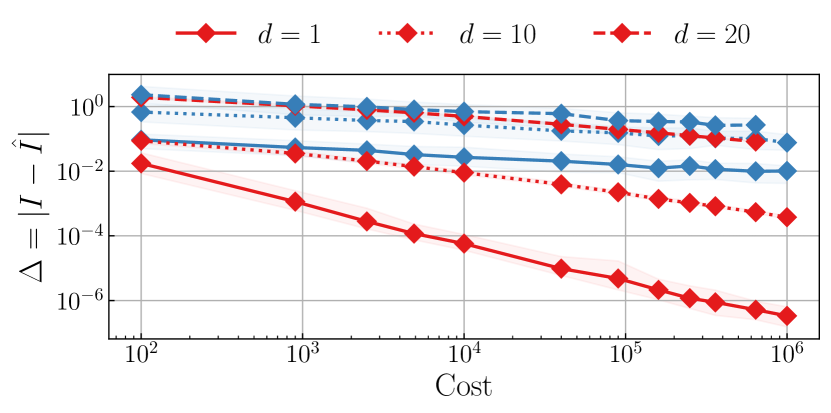

In Figure˜2 Top, we see that the optimal choice of and suggested by the theory indeed results in a faster rate of convergence for both NMC and NKQ. For this synthetic problem, we confirm that both the theoretical rates of NKQ () and NMC () from ˜1 and Rainforth et al. (2018, Theorem 3) are indeed realized. We also adapt the synthetic problem to higher dimensions () in (F.42) and observe in Figure˜2 Bottom that the performance gap between NKQ and NMC closes down as dimension grows. Such behaviour is expected because the cost of NKQ is and therefore degrades as the dimensions and increase; whilst the cost of NMC remains the same.

We also conduct ablation studies, which are reserved for Figure˜5 in the appendix. In the left-most plot, we see that the result are not too sensitive to , although very large values decrease accuracy whilst very small values cause numerical issues. In the middle plot, we see that selecting the kernel lengthscale using the median heuristic provides very good performance. In the right-most plot, we see that NKQ with Matérn- kernels outperforms Matérn- kernel, indicating practitioners should use Sobolev kernels with the highest order of smoothness permissible by ˜1.

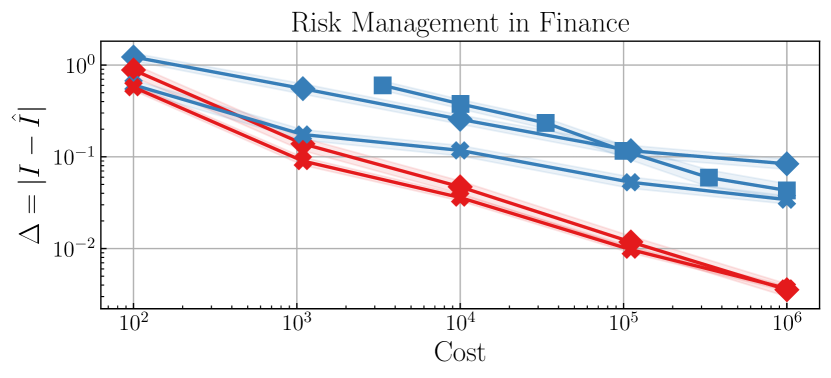

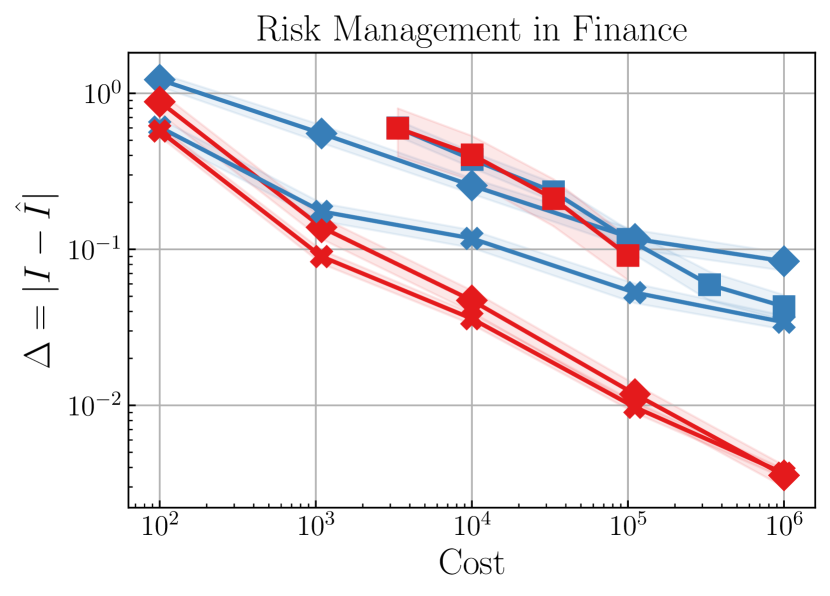

Risk Management in Finance

We now move beyond synthetic examples, starting in finance. Financial institutions often face the challenge of estimating the expected loss of their portfolios in the presence of potential economic shocks, which amounts to numerically solving stochastic differential equations (SDEs) over long time horizons (Achdou and Pironneau, 2005). Given the high cost of such simulations, data-efficient methods like NKQ are particularly desirable.

Suppose a shock occurs at time and alters the price of an asset by a factor of for some . Conditioned on the asset price at the time of shock, the loss of an option associated with that asset at maturity with price can be expressed as , where measures the shortfall in option payoff and the distribution is induced by the price of the asset which is described by the Black-Scholes formula. The payoff function we consider is that of a butterfly call option: for . Since we incur a loss only if the final shortfall is positive, the expected loss of the option at maturity can be expressed as . Under this setting, and can be computed analytically.

In this experiment, Assumptions LABEL:as:app_true_g_smoothnessLABEL:as:app_true_J_smoothness are satisfied with , but the max function is not in which violates Assumption LABEL:as:app_lipschitz (see Section˜F.3). Nevertheless, we still run NKQ with and being Matérn- kernels and choose for NKQ following ˜1. For NMC, we follow Gordy and Juneja (2010) and choose . For MLMC, we use levels and allocate samples at each level following Giles and Goda (2019).

In Figure˜3 Top, we present the mean absolute error of NKQ, NMC and MLMC with increasing cost. We see that NKQ outperforms both NMC and MLMC as expected. For each method, we obtain the empirical rate by linear regression in log-log space, and compare this against the theoretical rate in Table˜1. For NMC, our estimate of matches theory (), but when using QMC samples instead, our estimate of shows we under-perform compared to the theoretical rate (). This is likely because the domains are unbounded and the measures are not uniform, breaking key assumptions. Finally, for NKQ, we obtain for i.i.d samples and for QMC samples which match (and even slightly outperform) the theoretical rate ().

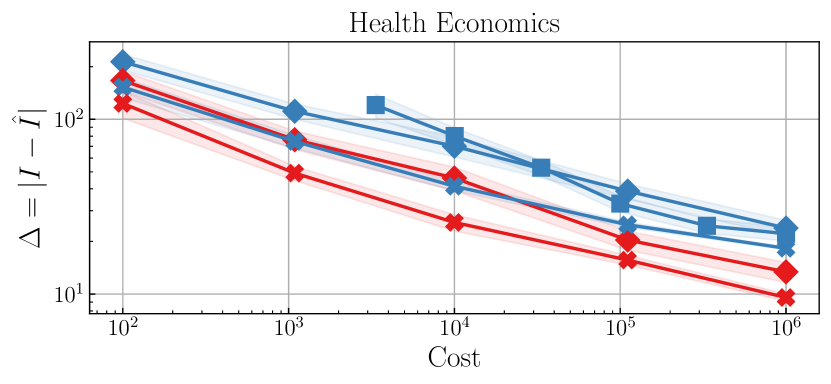

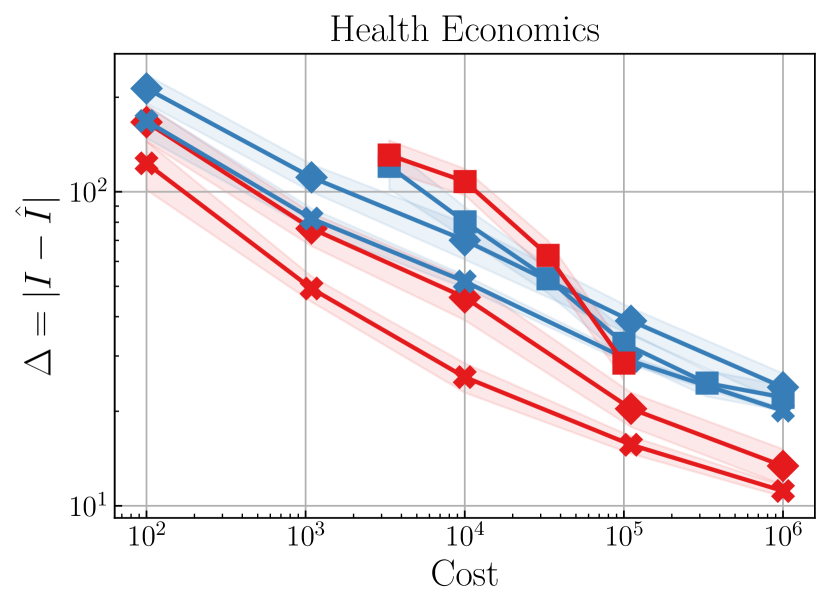

Health Economics

In medical decision-making, a key metric to evaluate the cost-benefit trade-off of conducting additional tests on patients is the expected value of partial perfect information (EVPPI) (Brennan et al., 2007; Heath et al., 2017). Formally, let denote the patient outcome (such as quality-adjusted life-years) under treatment in a set of possible treatments , and represent the additional variables that may be measured. Then, represents the expected patient outcome given the measurement of . The EVPPI is defined as , where and and therefore consists of nested expectations.

We follow Section 4.2 of Giles and Goda (2019), where both and are Gaussians, and and . The exact practical meanings of each dimension of and can be found in Section˜F.4, but includes quantities such as ‘cost of treatment’ and ‘duration of side effects’. Here we have and , the former being relatively high dimensional. The ground truth EVPPI under this setting is provided in Giles and Goda (2019).

For estimating both and , Assumptions LABEL:as:app_true_g_smoothnessLABEL:as:app_true_J_smoothness are satisfied with infinite smoothness , but the max function in is only in which violates Assumption LABEL:as:app_lipschitz. As a result, for estimating we take to be a Gaussian kernel and to be Matérn- kernel (so as to be conservative about the smoothness in ). For estimating , we select both and to be Gaussian kernels. For NKQ, we choose whereas for NMC, we choose . For MLMC, we use levels and allocate the samples at each level following Giles and Goda (2019). We run NKQ and NMC with both i.i.d. samples and QMC samples. In Figure˜3 Bottom, we present the mean absolute error of NKQ, NMC and MLMC with increasing cost. We can see that NKQ consistently outperforms other baselines.

Bayesian Optimization

We conclude with an application in Bayesian optimization. Typical acquisition functions are greedy approaches that maximize the immediate reward, while look-ahead acquisition functions optimize accumulated reward over a planning horizon, which results in reduced number of required function evaluations (Ginsbourger and Le Riche, 2010; González et al., 2016; Wu and Frazier, 2019; Yang et al., 2024). The utility of a two-step look ahead acquisition functions can be written as the following nested expectation.

where are the posterior distributions given data and . In this experiment, the prior is a Gaussian process with zero mean and Matérn- covariance so the posterior remain a Gaussian process. Here, is the reward function and we use q-expected improvement (Wang et al., 2020) with so and . The constant is the maximum reward obtained from previous queries. Although (resp. ) is a Gaussian process, we only ever consider its evaluation on (resp. ), and we therefore only have to integration against two-dimensional Gaussians. Notationally speaking, correspond to and correspond to in (1) (i.e. ), but we use the notation of to stay consistent with the GP literature. As a result of the max operation, but we do not have sufficient smoothness in .

We benchmark NKQ, NMC and MLMC on three synthetic tasks from BoTorch (Balandat et al., 2020). For NKQ, both and are Matérn- kernels since we want to be conservative about the smoothness. Although both and are Gaussian so closed-form KMEs are available, we use the “change of variable trick” in Section˜F.1 to reduce the computational complexity of NKQ to . To reach a specific error threshold , following Table˜1, we choose for NMC and for NKQ. For MLMC, we use the same code as Section 5 of Yang et al. (2024). The normalized mean squared error (NMSE) is used as the performance metric, where (resp. ) is queried data at initialization (resp. after iterations), is the black box function to be optimized and is the maximum reward.

In Figure˜4, we compare the efficiency of each method by plotting their NMSE against cumulative computational time in wall clock. We can see that NKQ achieves the lowest NMSE among all methods under a fixed amount of computational time across all three datasets. Even though the assumptions of ˜1 are not all satisfied, NKQ still outperforms NMC and MLMC. Furthermore, since the Dropwave, Ackley, and Cosine8 functions are synthetic and computationally cheap, we expect the advantages of NKQ to be more pronounced for Bayesian optimization on real-world expensive problems.

6 Conclusion

This paper introduced a novel estimator for nested expectations based on kernel quadrature. We proved in ˜1 that our method has a faster rate of convergence than existing methods provided that the problem has sufficient smoothness. This theoretical result is consistent with the empirical evidence in several numerical experiments. Additionally, even when the problem is not as smooth as the theory requires, NKQ can still outperform baseline methods potentially due to the use of non-equal weights.

Following our work, there remain a number of interesting future problems and we now highlight two main ones. Firstly, we proposed a combination of KQ and MLMC that we call MLKQ in Section˜D.2. However, we believe our current theoretical rate for MLKQ is sub-optimal due to the sub-optimal allocation of samples at each level. Further work will therefore be needed to determine whether this is a viable approach in some cases. Secondly, for applications where function evaluations are extremely expensive, NKQ could be extended to its Bayesian counterpart. This would allow us to use the finite sample uncertainty quantification for adaptive selection of samples, which could further improve performance.

Acknowledgments

The authors acknowledge useful discussions with Philipp Hennig and support from the Engineering and Physical Sciences Research Council (ESPRC) through grants [EP/S021566/1] (for ZC and MN) and [EP/Y022300/1] (for FXB).

References

- Achdou and Pironneau [2005] Yves Achdou and Olivier Pironneau. Computational methods for option pricing. SIAM, 2005.

- Adams and Fournier [2003] Robert A Adams and John JF Fournier. Sobolev spaces. Elsevier, 2003.

- Alfonsi et al. [2021] Aurélien Alfonsi, Adel Cherchali, and Jose Arturo Infante Acevedo. Multilevel Monte Carlo for computing the SCR with the standard formula and other stress tests. Insurance: Mathematics and Economics, 100:234–260, 2021.

- Alfonsi et al. [2022] Aurélien Alfonsi, Bernard Lapeyre, and Jérôme Lelong. How many inner simulations to compute conditional expectations with least-square Monte Carlo? arXiv preprint arXiv:2209.04153, 2022.

- Andradóttir and Glynn [2016] Sigrun Andradóttir and Peter W. Glynn. Computing Bayesian means using simulation. ACM Transactions on Modeling and Computer Simulation, 26(2):1–26, 2016.

- Aronszajn [1950] Nachman Aronszajn. Theory of reproducing kernels. Transactions of the American mathematical society, 68(3):337–404, 1950.

- Bach [2017] Francis Bach. On the equivalence between kernel quadrature rules and random feature expansions. Journal of Machine Learning Research, 18(19):1–38, 2017.

- Balandat et al. [2020] Maximilian Balandat, Brian Karrer, Daniel Jiang, Samuel Daulton, Ben Letham, Andrew G Wilson, and Eytan Bakshy. Botorch: A framework for efficient Monte-carlo Bayesian optimization. Advances in Neural Information Processing Systems, 33:21524–21538, 2020.

- Bariletto and Ho [2024] Nicola Bariletto and Nhat Ho. Bayesian Nonparametrics meets Data-Driven Robust Optimization. In Advances in Neural Information Processing Systems, 2024.

- Bartuska et al. [2023] Arved Bartuska, Andre Gustavo Carlon, Luis Espath, Sebastian Krumscheid, and Raul Tempone. Double-loop randomized Quasi-Monte Carlo estimator for nested integration. arXiv:2302.14119, 2023.

- Beck et al. [2020] Joakim Beck, Ben Mansour Dia, Luis Espath, and Raúl Tempone. Multilevel double loop Monte Carlo and stochastic collocation methods with importance sampling for Bayesian optimal experimental design. International Journal for Numerical Methods in Engineering, 121(15):3482–3503, 2020.

- Behzadan and Holst [2021] Ali Behzadan and Michael Holst. Multiplication in Sobolev spaces, revisited. Arkiv för Matematik, 59(2):275–306, 2021.

- Belhadji et al. [2019] Ayoub Belhadji, Rémi Bardenet, and Pierre Chainais. Kernel quadrature with DPPs. Advances in Neural Information Processing Systems, 32, 2019.

- Bennett and Sharpley [1988] Colin Bennett and Robert C Sharpley. Interpolation of operators. Academic press, 1988.

- Berlinet and Thomas-Agnan [2004] Alain Berlinet and Christine Thomas-Agnan. Reproducing Kernel Hilbert Spaces in Probability and Statistics. Springer Science+Business Media, New York, 2004.

- Bharti et al. [2023] Ayush Bharti, Masha Naslidnyk, Oscar Key, Samuel Kaski, and François-Xavier Briol. Optimally-weighted estimators of the maximum mean discrepancy for likelihood-free inference. In International Conference on Machine Learning, pages 2289–2312, 2023.

- Brennan et al. [2007] Alan Brennan, Samer Kharroubi, Anthony O’Hagan, and Jim Chilcott. Calculating partial expected value of perfect information via Monte Carlo sampling algorithms. Medical Decision Making, 27(4):448–470, 2007.

- Briol [2018] François-Xavier Briol. Statistical computation with kernels. PhD thesis, University of Warwick, 2018.

- Briol et al. [2015] François-Xavier Briol, Chris Oates, Mark Girolami, and Michael Osborne. Frank-Wolfe Bayesian quadrature: Probabilistic integration with theoretical guarantees. In Advances in Neural Information Processing Systems, pages 1162–1170, 2015.

- Briol et al. [2017] François-Xavier Briol, Chris Oates, Jon Cockayne, Ye Chen, and Mark Girolami. On the sampling problem for kernel quadrature. In Proceedings of the International Conference on Machine Learning, pages 586–595, 2017.

- Briol et al. [2019] François-Xavier Briol, Chris Oates, Mark Girolami, M. A. Osborne, and D. Sejdinovic. Probabilistic integration: A role in statistical computation? (with discussion). Statistical Science, 34(1):1–22, 2019.

- Bujok et al. [2015] Karolina Bujok, Ben M Hambly, and Christoph Reisinger. Multilevel simulation of functionals of bernoulli random variables with application to basket credit derivatives. Methodology and Computing in Applied Probability, 17:579–604, 2015.

- Cai et al. [2023] X. Cai, C. T. Lam, and J. Scarlett. On average-case error bounds for kernel-based Bayesian quadrature. Transactions on Machine Learning Research, 2023.

- Chen et al. [2024a] Zonghao Chen, Aratrika Mustafi, Pierre Glaser, Anna Korba, Arthur Gretton, and Bharath K Sriperumbudur. (de)-regularized maximum mean discrepancy gradient flow. arXiv preprint arXiv:2409.14980, 2024a.

- Chen et al. [2024b] Zonghao Chen, Masha Naslidnyk, Arthur Gretton, and François-Xavier Briol. Conditional Bayesian quadrature. Conference on Uncertainty in Artificial Intelligence, 2024b.

- Dellaporta et al. [2024] Charita Dellaporta, Patrick O’Hara, and Theodoros Damoulas. Decision making under the exponential family: Distributionally robust optimisation with Bayesian ambiguity sets. arXiv:2411.16829v1, 2024.

- Diaconis [1988] Persi Diaconis. Bayesian numerical analysis. Statistical Decision Theory and Related Topics IV, pages 163–175, 1988.

- Dick et al. [2013] Josef Dick, Frances Kuo, and Ian H. Sloan. High-dimensional integration: The Quasi-Monte Carlo way. Acta Numerica, 22(April 2013):133–288, 2013.

- Eberts and Steinwart [2013] Mona Eberts and Ingo Steinwart. Optimal regression rates for SVMs using Gaussian kernels. 2013.

- Edmunds and Triebel [1996] David Eric Edmunds and Hans Triebel. Function spaces, entropy numbers, differential operators. (No Title), 1996.

- Epperly and Moreno [2023] Ethan N. Epperly and Elvira Moreno. Kernel quadrature with randomly pivoted cholesky. In Advances in Neural Information Processing Systems, pages 65850–65868, 2023.

- Evans [2022] Lawrence C Evans. Partial differential equations, volume 19. American Mathematical Society, 2022.

- Fischer and Steinwart [2020] Simon Fischer and Ingo Steinwart. Sobolev norm learning rates for regularized least-squares algorithms. Journal of Machine Learning Research, 21(205):1–38, 2020.

- Gessner et al. [2020] Alexandra Gessner, Javier Gonzalez, and Maren Mahsereci. Active multi-information source Bayesian quadrature. In Uncertainty in Artificial Intelligence, pages 712–721. PMLR, 2020.

- Giles [2015] Michael B. Giles. Multilevel Monte Carlo methods. Acta Numerica, 24:259–328, 2015.

- Giles [2018] Michael B. Giles. MLMC for nested expectations. Contemporary computational mathematics-A celebration of the 80th birthday of ian sloan, pages 425–442, 2018.

- Giles and Goda [2019] Michael B. Giles and Takashi Goda. Decision-making under uncertainty: using MLMC for efficient estimation of EVPPI. Statistics and computing, 29:739–751, 2019.

- Giles and Haji-Ali [2019] Michael B. Giles and A-L Haji-Ali. Multilevel nested simulation for efficient risk estimation. SIAM/ASA Journal on Uncertainty Quantification, 7(2):497–525, 2019.

- Ginsbourger and Le Riche [2010] David Ginsbourger and Rodolphe Le Riche. Towards Gaussian process-based optimization with finite time horizon. In mODa 9 - Advances in Model-Oriented Design and Analysis, pages 89–96, 2010.

- Goda et al. [2018] Takashi Goda, Daisuke Murakami, Kei Tanaka, and Kozo Sato. Decision-theoretic sensitivity analysis for reservoir development under uncertainty using multilevel Quasi-Monte Carlo methods. Computational Geosciences, 22(4):1009–1020, 2018.

- Goda et al. [2020] Takashi Goda, Tomohiko Hironaka, and Takeru Iwamoto. Multilevel Monte Carlo estimation of expected information gains. Stochastic Analysis and Applications, 38(4):581–600, 2020.

- González et al. [2016] Javier González, Michael Osborne, and Neil Lawrence. Glasses: Relieving the myopia of Bayesian optimisation. In Artificial Intelligence and Statistics, pages 790–799. PMLR, 2016.

- Gordy and Juneja [2010] Michael B. Gordy and Sandeep Juneja. Nested simulation in portfolio risk measurement. Management Science, 56(10):iv–1872, 2010.

- Gretton [2013] Arthur Gretton. Introduction to rkhs, and some simple kernel algorithms. Advanced Topics in Machine Learning. Lecture Conducted from University College London, 16(5-3):2, 2013.

- Gunter et al. [2014] Tom Gunter, Michael A Osborne, Roman Garnett, Philipp Hennig, and Stephen J Roberts. Sampling for inference in probabilistic models with fast Bayesian quadrature. Advances in Neural Information Processing Systems, 27, 2014.

- Hang and Steinwart [2021] Hanyuan Hang and Ingo Steinwart. Optimal learning with anisotropic Gaussian SVMs. Applied and Computational Harmonic Analysis, 55:337–367, 2021.

- Hayakawa et al. [2022] Satoshi Hayakawa, Harald Oberhauser, and Terry Lyons. Positively weighted kernel quadrature via subsampling. In Advances in Neural Information Processing Systems, pages 6886 – 6900, 2022.

- Hayakawa et al. [2023] Satoshi Hayakawa, Harald Oberhauser, and Terry Lyons. Sampling-based Nyström approximation and kernel quadrature. In International Conference on Machine Learning, volume 202, pages 12678–12699, 2023.

- Heath et al. [2017] Anna Heath, Ioanna Manolopoulou, and Gianluca Baio. A Review of Methods for Analysis of the Expected Value of Information. Medical Decision Making, 37(7):747–758, 2017.

- Hennig et al. [2022] Philipp Hennig, Michael A. Osborne, and Hans Kersting. Probabilistic Numerics: Computation as Machine Learning. Cambridge University Press, 2022.

- Hong and Juneja [2009] Jeff L. Hong and Sandeep Juneja. Estimating the mean of a non-linear function of conditional expectation. In Proceedings of the 2009 Winter Simulation Conference, pages 1223–1236, 2009.

- Hytonen et al. [2016] Tuomas Hytonen, Jan Van Neerven, Mark Veraar, and Lutz Weis. Analysis in Banach spaces, volume 12. Springer, 2016.

- Kaarnioja et al. [2025] Vesa Kaarnioja, Ilja Klebanov, Claudia Schillings, and Yuya Suzuki. Lattice rules meet kernel cubature. arXiv:2501.09500, 2025.

- Kanagawa et al. [2023] Heishiro Kanagawa, Wittawat Jitkrittum, Lester Mackey, Kenji Fukumizu, and Arthur Gretton. A kernel stein test for comparing latent variable models. Journal of the Royal Statistical Society Series B: Statistical Methodology, 85:986–1011, 2023.

- Kanagawa and Hennig [2019] Monotobu Kanagawa and Philipp Hennig. Convergence guarantees for adaptive Bayesian quadrature methods. In Advances in Neural Information Processing Systems, pages 6237–6248, 2019.

- Kanagawa et al. [2020] Monotobu Kanagawa, Bharath K. Sriperumbudur, and Kenji Fukumizu. Convergence analysis of deterministic kernel-based quadrature rules in misspecified settings. Foundations of Computational Mathematics, 20:155–194, 2020.

- Kanagawa et al. [2018] Motonobu Kanagawa, Philipp Hennig, Dino Sejdinovic, and Bharath K Sriperumbudur. Gaussian processes and kernel methods: A review on connections and equivalences. arXiv preprint arXiv:1807.02582, 2018.

- Karvonen and Särkkä [2018] Toni Karvonen and Simo Särkkä. Fully symmetric kernel quadrature. SIAM Journal on Scientific Computing, 40(2):697–720, 2018.

- Karvonen et al. [2019] Toni Karvonen, Simo Särkkä, and Chris Oates. Symmetry exploits for Bayesian cubature methods. Statistics and Computing, 29:1231–1248, 2019.

- Karvonen et al. [2020] Toni Karvonen, Chris Oates, and Mark Girolami. Integration in reproducing kernel Hilbert spaces of Gaussian kernels. Mathematics of Computation, 90(331):2209–2233, 2020.

- Kuo et al. [2024] Frances Y Kuo, Weiwen Mo, and Dirk Nuyens. Constructing Embedded Lattice-Based Algorithms for Multivariate Function Approximation with a Composite Number of Points. Constructive Approximation, 2024.

- Lee and Glynn [2003] Shing Hoi Lee and Peter W. Glynn. Computing the distribution function of a conditional expectation via Monte Carlo: Discrete conditioning spaces. ACM Transactions on Modeling and Computer Simulation, 13(3):238–258, 2003.

- Li et al. [2023] Kaiyu Li, Daniel Giles, Toni Karvonen, Serge Guillas, and François-Xavier Briol. Multilevel Bayesian quadrature. In International Conference on Artificial Intelligence and Statistics, pages 1845–1868. PMLR, 2023.

- Long et al. [2024] Jihao Long, Xiaojun Peng, and Lei Wu. A duality analysis of kernel ridge regression in the noiseless regime. arXiv preprint arXiv:2402.15718, 2024.

- Longstaff and Schwartz [2001] Francis A Longstaff and Eduardo S Schwartz. Valuing american options by simulation: a simple least-squares approach. The review of financial studies, 14(1):113–147, 2001.

- Novak [2006] Erich Novak. Deterministic and stochastic error bounds in numerical analysis, volume 1349. Springer, 2006.

- Novak [2016] Erich Novak. Some results on the complexity of numerical integration. Monte Carlo and Quasi-Monte Carlo Methods: MCQMC, Leuven, Belgium, April 2014, pages 161–183, 2016.

- Oates et al. [2017] Chris Oates, Mark Girolami, and Nicolas Chopin. Control functionals for Monte Carlo integration. Journal of the Royal Statistical Society B: Statistical Methodology, 79(3):695–718, 2017.

- Oates et al. [2019] Chris J. Oates, Jon Cockayne, François-Xavier Briol, and Mark Girolami. Convergence rates for a class of estimators based on Stein’s identity. Bernoulli, 25(2):1141–1159, 2019.

- O’Hagan [1991] Anthony O’Hagan. Bayes–Hermite quadrature. Journal of Statistical Planning and Inference, 29:245–260, 1991.

- Osborne et al. [2012] Michael Osborne, Roman Garnett, Zoubin Ghahramani, David K Duvenaud, Stephen J Roberts, and Carl Rasmussen. Active learning of model evidence using Bayesian quadrature. Advances in Neural Information Processing Systems, 25, 2012.

- Owen [2003] Art B Owen. Quasi-Monte carlo sampling. Monte Carlo Ray Tracing: Siggraph, 1:69–88, 2003.

- R. Jagadeeswaran [2019] Fred J. Hickernell R. Jagadeeswaran. Fast automatic Bayesian cubature using lattice sampling. Statistics and Computing, 29(6):1215–1229, 2019.

- Rainforth et al. [2018] Tom Rainforth, Rob Cornish, Hongseok Yang, Andrew Warrington, and Frank Wood. On nesting Monte Carlo estimators. In International Conference on Machine Learning, pages 4267–4276. PMLR, 2018.

- Rainforth et al. [2024] Tom Rainforth, Adam Foster, Desi R. Ivanova, and Freddie B. Smith. Modern Bayesian experimental design. Statistical Science, 39(1):100–114, 2024.

- Rasmussen and Ghahramani [2002] Carl Rasmussen and Zoubin Ghahramani. Bayesian Monte Carlo. In Advances in Neural Information Processing Systems, pages 489–496, 2002.

- Ritter [2000] Klaus Ritter. Average-case analysis of numerical problems. Number 1733. Springer Science & Business Media, 2000.

- Robert and Casella [2000] Christian P. Robert and George Casella. Monte Carlo Statistical Methods. Springer, 2000.

- Rudin [1964] Walter Rudin. Principles of mathematical analysis, volume 3. McGraw-hill New York, 1964.

- Shapiro et al. [2023] Alexander Shapiro, Enlu Zhou, and Yifan Lin. Bayesian distributionally robust optimization. SIAM Journal on Optimization, 33(2):1279–1304, 2023.

- Si et al. [2021] Shijing Si, Chris J. Oates, Andrew B. Duncan, Lawrence Carin, and François-Xavier Briol. Scalable control variates for Monte Carlo methods via stochastic optimization. Proceedings of the 14th Conference on Monte Carlo and Quasi-Monte Carlo Methods. arXiv:2006.07487, 2021.

- Smola et al. [2007] Alex Smola, Arthur Gretton, Le Song, and Bernhard Schölkopf. A hilbert space embedding for distributions. In International conference on algorithmic learning theory, pages 13–31. Springer, 2007.

- Sommariva and Vianello [2006] Alvise Sommariva and Marco Vianello. Numerical cubature on scattered data by radial basis functions. Computing, 76:295–310, 2006.

- Song et al. [2020] Yang Song, Sahaj Garg, Jiaxin Shi, and Stefano Ermon. Sliced Sscore matching: A scalable approach to density and score estimation. In Uncertainty in Artificial Intelligence Conference, pages 574–584, 2020.

- Steinwart [2008] Ingo Steinwart. Support Vector Machines. Springer, 2008.

- Steinwart et al. [2009] Ingo Steinwart, Don R Hush, Clint Scovel, et al. Optimal rates for regularized least squares regression. In COLT, pages 79–93, 2009.

- Stirzaker [2003] David Stirzaker. Elementary Probability. Cambridge University Press, 2003.

- Sun et al. [2023] Zhuo Sun, Alessandro Barp, and François-Xavier Briol. Vector-valued control variates. In International Conference on Machine Learning, pages 32819–32846, 2023.

- Suzuki and Nitanda [2021] Taiji Suzuki and Atsushi Nitanda. Deep learning is adaptive to intrinsic dimensionality of model smoothness in anisotropic Besov space. Advances in Neural Information Processing Systems, 34:3609–3621, 2021.

- Vershynin [2018] Roman Vershynin. High-dimensional probability: An introduction with applications in data science, volume 47. Cambridge university press, 2018.

- Wang et al. [2020] Jialei Wang, Scott C Clark, Eric Liu, and Peter I Frazier. Parallel Bayesian global optimization of expensive functions. Operations Research, 68(6):1850–1865, 2020.

- Wendland [2004] Holger Wendland. Scattered data approximation, volume 17. Cambridge university press, 2004.

- Wenger et al. [2021] Jonathan Wenger, Nicholas Krämer, Marvin Pförtner, Jonathan Schmidt, Nathanael Bosch, Nina Effenberger, Johannes Zenn, Alexandra Gessner, Toni Karvonen, François-Xavier Briol, et al. ProbNum: Probabilistic Numerics in Python. arXiv preprint arXiv:2112.02100, 2021.

- Wu and Frazier [2019] Jian Wu and Peter Frazier. Practical two-step lookahead Bayesian optimization. Advances in Neural Information Processing Systems, 32, 2019.

- Wynne et al. [2021] George Wynne, François-Xavier Briol, and Mark Girolami. Convergence guarantees for Gaussian process means with misspecified likelihoods and smoothness. The Journal of Machine Learning Research, 22(1):5468–5507, 2021.

- Yang et al. [2024] Shangda Yang, Vitaly Zankin, Maximilian Balandat, Stefan Scherer, Kevin Thomas Carlberg, Neil Walton, and Kody JH Law. Accelerating look-ahead in Bayesian optimization: Multilevel Monte Carlo is all you need. In Forty-first International Conference on Machine Learning, 2024.

- Zeng et al. [2009] Xiaoyan Zeng, Peter Kritzer, and Fred J. Hickernell. Spline methods using integration lattices and digital nets. pages 529–555, 2009.

- Zhang et al. [2023] Haobo Zhang, Yicheng Li, Weihao Lu, and Qian Lin. On the optimality of misspecified kernel ridge regression. In International Conference on Machine Learning, pages 41331–41353. PMLR, 2023.

Supplementary Material

Table of Contents

Additional notations

For two normed vector spaces , means that and are norm equivalent, i.e. their sets coincide and the corresponding norms are equivalent. In other words, there are constants such that holds for all , written as . For , is said to be continuously embedded in if the inclusion map between them is continuous, written as . denotes the norm of an operator . For a function and , we use to denote the standard derivative and to denote the weak derivative. For , we use to denote its Sobolev space norm. means up to some positive multiplicative constants.

Appendix A Existing Results on Kernel Ridge Regression

In this section, we present ˜1 to 3 which are adaptation of theorems from Fischer and Steinwart [2020] applied to Sobolev spaces. These propositions are foundations of the proof of ˜1 in Appendix˜C.

In the standard regression setting, we are given observations which are i.i.d sampled from an unknown joint distribution on . Here, is a compact domain. The marginal distribution of on is , and the conditional distribution satisfies the Bernstein moment condition [Fischer and Steinwart, 2020]. In other words, there exists constants independent of such that

| (A.1) |

is satisfied for -almost all and all . For example, (A.1) is satisfied with when is a Gaussian distribution with bounded variance . Additionally, (A.1) is also satisfied when there is no noise in the observation so , which will be discussed in Appendix˜B.

In a regression problem, the target of interest is the Bayes predictor , . One way of estimating is through kernel ridge regression [Fischer and Steinwart, 2020]: given a reproducing kernel , the kernel ridge regression estimator is defined as the solution to the following optimization problem ():

| (A.2) |

is the reproducing kernel Hilbert space (RKHS) associated with a kernel . Fortunately, it has the following closed-form expression [Gretton, 2013, Section 7]

We also introduce an auxiliary function which is the solution to another optimization problem:

| (A.3) |

In regression setting, it is of interest to study the generalization error between the estimator and the Bayes optimal predictor , , and particularly its asymptotic rate of convergence towards as the number of samples tend to infinity. The generalization error can be decomposed into two terms, through a triangular inequality,

| (A.4) |

where the first term is known as the estimation error and the second term is known as the approximation error. Next, we are going to present propositions that study these two terms separately under the following list of conditions.

Proposition 1 (Approximation error).

Under Assumptions LABEL:as:kernel-LABEL:as:noise,

Proof.

This is direct application of Lemma 14 of [Fischer and Steinwart, 2020] with and . ∎

Proposition 2 (Estimation error).

Proof.

This proposition is a special case of Theorem 16 in Fischer and Steinwart [2020] under the following adaptations towards our Sobolev space setting: 1) ˜1 proves that and ˜2 proves that for . 2) is upper bounded by proved in Corollary 15 of Fischer and Steinwart [2020]. is the norm of the covariance operator defined in (E.40). ∎

Proposition 3.

Suppose Assumptions LABEL:as:kernel-LABEL:as:noise hold. For and defined above in ˜2, if , then with probability at least ,

Appendix B Noiseless Kernel Ridge Regression (Kernel Quadrature)

In this section, we present the upper bound on the generalization error in ˜3 adapted to the noiseless regression setting, which will be employed in the proof of ˜1 in the next section. Our proof follows the outline of the proof for Theorem 1 in [Fischer and Steinwart, 2020], modified for our choice of regularization parameter . Note that this section is of independent interest to some readers as it presents the first standalone proof on the convergence rate of kernel quadrature that 1): it allows positive regularization parameter and 2): it provides convergence in high probability rather than in expectation. The closely-related work is Bach [2017] which requires i.i.d samples from an intractable distribution; and Long et al. [2024] which provides a more general analysis on noiseless kernel ridge regression in both well-specified and mis-specified setting.

Suppose we have observations which are i.i.d sampled from an unknown distribution on along with noiseless function evaluations where . The setting appears for instance when the measurement of the output values is very accurate, or when the output values are obtained as a result of computer experiments.

Proposition 4.

Let be compact, and be i.i.d. samples from . Define , and suppose conditions LABEL:as:kernel-LABEL:as:noise are satisfied. Then, if , there exists an such that for all ,

| (B.6) |

holds with probability at least , for a constant that only depends on .

Proof.

Notice that is precisely the solution to the optimization problem defined in (A.2) only with replaced by . Similarly, we define as the solution to the optimization problem defined in (A.3) only with replaced by . Note that Assumption LABEL:as:noise is instantly satisfied with .

Similar to the proof of ˜3, we decompose the generalization error into an estimation error term and an approximation error term .

Approximation error

Take , then from ˜1, we have

Estimation error

Combine approximation and estimation error

Combining the above two inequalities on approximation error and estimation error , we have with probability at least ,

Finally, following the arguments of ˜2 that the operator norm of is bounded, we have where is a constant that depends on . With probability at least ,

for , which concludes the proof. ∎

Corollary 2.

Let be a compact domain in and are i.i.d samples from . is the KQ estimator defined in (5). Suppose conditions (A1)-(A3) are satisfied. Take , then there exists such that for ,

| (B.8) |

holds with probability at least . Here is a constant that is independent of .

Remark B.1.

We prove in ˜4 that the generalization error of in noiseless regression setting is , which is faster than the minimax optimal rate in standard regression setting. The fast rate is expected because we are in the noiseless regime so “overfitting" is not a problem — hence our choice of regularization parameter decays to at a faster rate than in standard kernel ridge regression [Fischer and Steinwart, 2020, Corollary 5]. The rate is also optimal (up to logarithm terms) and cannot be further improved because it matches the lower bound of interpolation (Sections 1.3.11 and 1.3.1 of Novak [2006], Section 1.2, Chapter V of Ritter [2000]).

Remark B.2 (Comparison to existing upper bound of kernel (Bayesian) quadrature).

The upper bound in ˜2 matches existing analysis based on scattered data approximation in the literature of both kernel quadrature and Bayesian quadrature [Sommariva and Vianello, 2006, Briol et al., 2019, Wynne et al., 2021] and is known to be minimax optimal [Novak, 2016, 2006]. Existing analysis takes and requires the Gram matrix to be invertible, in contrast, our result allows a positive regularization parameter which improves numerical stability of matrix inversion in practice. Closely-related work is Bach [2017] which requires i.i.d samples from an intractable distribution; and Long et al. [2024] which provides a more general analysis on noiseless kernel ridge regression in both well-specified and mis-specified setting.

Appendix C Proof of ˜1

Remark C.1.

In this section, we use to denote the density so that we can use to denote the mapping . Although we introduce a shorthand notation of kernel mean embedding in the main text, , in this section we are going to write it out with its explicit formulation.

For any , and are two functions that generalize the definition of and in (7) to all . To be more specific, for any , given samples consisting of i.i.d. samples from ,

| (C.9) | ||||

| (C.10) |

where we explicitly specify the dependence of samples on in the above two equations. Next, we define

| (C.11) |

which marginalize out the dependence on samples . We can see that since from Assumption LABEL:as:equivalence and LABEL:as:app_true_J_smoothness; and . Also because is Lipschitz continuous from Assumption LABEL:as:app_lipschitz. Therefore, the absolute error can be decomposed as follows:

| (C.12) |

The last inequality holds because . Next, we analyze Stage I error and Stage II error separately.

Stage I Error

From Assumption LABEL:as:app_lipschitz, is Lipschitz continuous and the Lipschitz constant is bounded by ,

| (C.13) |

where the first inequality holds by Jensen inequality and the last inequality holds by Lipschitz continuity of . Define

| (C.14) |

Here because the Sobolev reproducing kernel is bounded and measurable; and by Assumption LABEL:as:app_true_J_smoothness. Thus,

| (C.15) |

Based on Assumption LABEL:as:app_true_g_smoothness, for any . Therefore, based on ˜4, if one takes , then there exists such that for ,

| (C.16) |

holds with probability at least . The probability is taken over the distribution of , i.e . Here is a constant independent of . Hence, with ˜4, we have

| (C.17) |

By plugging the above inequality back into (C.15), we obtain

Therefore, the Stage I error can be upper bounded by

| (C.18) |

where is a constant independent of .

Stage II Error

The upper bound on the stage II error is done in five steps. In step one, we prove that given fixed samples . In step two, we show that . In step three, we upper bound through the triangular inequality that . In step four, we upper bound through marginalizing out the samples . In the last step, we use kernel ridge regression bound proved in ˜3 to upper bound the stage II error.

Step One. In this step, we are going to show that lies in the Sobolev space given fixed samples . Notice that the dependence of on is through two mappings: and . We are going to show that lies in the Sobolev space for any . To this end, we are going to demonstrate it possesses weak derivatives up to and including order that lie in . Take to be any infinitely differentiable function with compact support in (commonly denoted as ), with its standard, non-weak derivative of order denoted by . Since , for any it has a weak derivative . Then,

| (C.19) |

In the above chain of derivations, we are allowed to swap the integration order in by the Fubini theorem [Rudin, 1964] because is bounded and the fact that since (Assumption LABEL:as:app_true_J_smoothness) and ; holds by definition of weak derivatives for ; and holds again by the Fubini theorem. By definition of weak derivatives, (C.19) shows that has a weak derivative of order of the form

Also, since is bounded and , the weak derivative above is in . Consequently, we have

In the above chain of derivations, holds because for compact , holds because is upper bounded by and from Assumption LABEL:as:app_true_J_smoothness, holds because for any based on Assumption LABEL:as:app_true_J_smoothness. Also, one can interchange the order of integration in by the Fubini’s theorem [Rudin, 1964].

As a result, for any , we have and from Assumption LABEL:as:app_true_J_smoothness. Therefore, we know from ˜3 that their product hence as a linear combination of is in .

Step Two. In this step, we are going to show that is also in the Sobolev space . Since both and , we know from ˜3 that . By following the same steps as in (C.19), we obtain that for any ,

| (C.20) |

We are now ready to study the Sobolev norm of ,

| (C.21) |

Here, holds by (C.20), holds since for compact , follows from the definition of Sobolev norm, and holds by ˜3 and Assumption LABEL:as:app_true_J_smoothness that , .

Step Three. In this step, we study the Sobolev norm of for some fixed , by upper bounding it with . Since by Assumption LABEL:as:app_true_J_smoothness, it holds that is in for any fixed . Therefore,

| (C.22) |

where the first inequality holds by ˜3 and the second inequality holds by Assumption LABEL:as:app_true_J_smoothness that . Now, we consider the Sobolev norm of ,

| (C.23) |

where the above chain of derivations (i) — (iv) follow the exact same reasoning as (C.19) and (C). Next, notice that

| (C.24) |

By Assumption LABEL:as:app_true_g_smoothness, for any . Therefore, by applying ˜4 with , and , we get that

| (C.25) |

holds with probability at least , for a that only depends on . From Assumption LABEL:as:equivalence, we know that (they are norm equivalent) and for any . Therefore, for any and any , with probability at least ,

| (C.26) |

By plugging (C) into (C), and then plugging the result into (C), we get that with probability at least ,

| (C.27) |

By combining this result with the bound proven in (C), we get that with probability at least and any it holds that

| (C.28) |

where is defined as the smallest integer for which the first term is subsumed by the second term.

Step Four. In this step, we are going to upper bound the Sobolev norm of . From Chapter 5, Exercise 16 of [Evans, 2022], we have is in because has bounded derivatives up to including and with probability at least proved in (C). Hence, holds with probability at least . Next, recall the definition of in (C.11),

For any , we know that from Assumption LABEL:as:app_true_J_smoothness and proved above. Therefore, from ˜3 we have is bounded, so is Bochner integrable with respect to the Lebesgue measure . From ˜5, we have,

| (C.29) |

The last inequality holds by from Assumption LABEL:as:app_true_J_smoothness and so .

Step Five. We are now ready to upper bound the stage II error, which was defined as

The idea is to treat the stage II error as the generalization error of kernel ridge regression—which can be bounded via ˜3. Given i.i.d. observations , the target of interest in the context of regression is the conditional mean, which in our case is precisely defined in (C.11). Alternatively, can be treated as noisy observation of the target function where the observation noise is defined as with . So we automatically have . For any positive integer ,

| (C.30) |

In the above chain of derivations, holds because . holds because we know from (C.15) and (C.16) that holds with probability at least , and so can be bounded via ˜4. Therefore, by comparing (C) with (A.1), we can see that the observation noise indeed satisfy the Bernstein noise moment condition with

for a constant independent of . Before we employ ˜3, we need to check the Assumptions LABEL:as:kernel—LABEL:as:noise. Assumption LABEL:as:kernel is satisfied for our choice of kernel . Assumption LABEL:as:density is satisfied due to Assumption LABEL:as:equivalence. Assumption LABEL:as:bayes_predictor is satisfied due to (C). Assumption LABEL:as:noise is satisfied for the Bernstein noise moment condition verified above. Next, we compute all the constants in ˜3 in the current context. is the effective dimension defined in ˜1 upper bounded by , with defined in ˜2 is upper bounded by a constant , is the norm of the covariance operator defined in (E.40). Hence

Applying ˜3 shows that, for ,

| (C.31) |

holds with probability at least . We take , then similar to the derivations from (B.7),

| (C.32) |

It means there exists a finite such that holds for any . Notice that, with probability at least ,

| (C.33) |

based on (C) and the fact that with , we have

We plug back the definition of and , so the above (C) can be further upper bounded by

are two constants independent of . In , we use , we also use the following

Therefore, we have that,

| Stage II error | ||||

| (C.34) |

holds with probability at least .

Combine stage I and stage II error

Appendix D Multi-Level Nested Kernel Quadrature

In this section, we are going to introduce a novel method that combines nested kernel quadrature (NKQ) with multi-level construction as mentioned in Section˜4.

D.1 Multi-Level Monte Carlo for Nested Expectation

First, we briefly review multi-level Monte Carlo (MLMC) applied to nested expectations introduced in Section 9 of Giles [2015] and Giles and Goda [2019]. At each level , we are given samples sampled i.i.d from and we have samples sampled i.i.d from for each . The MLMC implementation is to construct an estimator at each level such that can be decomposed into the sum of .

The estimator for is

Compared with (2) in the main text, notice that here we use the ‘antithetic’ approach which further improves the performance of MLMC [Giles, 2015, Section 9]. The MLMC estimator for nested expectation can be written as

| (D.35) |

At each level , the cost of is and the expected squared error provided that has bounded second order derivative [Giles, 2015, Section 9]111Section 9 of [Giles, 2015] uses variance , which is equivalent to the expected square error since is an unbiased estimate of .. Here the expectation is taken over the randomness of samples. So the total cost and expected absolute error of MLMC for nested expectation can be written as

| (D.36) |

Theorem 1 of [Giles, 2015] shows that, in order to reach error threshold , one can take and . Therefore, one has along with .

D.2 Multi-Level Kernel Quadrature for Nested Expectation (MLKQ)

In this section, we present multi-level kernel quadrature applied to nested expectation (MLKQ). Note that MLKQ is different from the multi-level Bayesian quadrature proposed in Li et al. [2023] because our MLKQ is designed specifically for nested expectations. At each level , we have samples sampled i.i.d from and we have samples sampled i.i.d from for each . Different from MLMC above, we define

The estimator for when is the difference of two nested kernel quadrature estimator defined in (8).

where is a vectorized notation for and similarly for . At level , we define . The multi-level nested kernel quadrature estimator is constructed as

Same as MLMC above, the cost of is . The following theorem studies the error .

Theorem 2.

Let and . At level , are i.i.d. samples from and are i.i.d. samples from for all . Both kernels and are Sobolev reproducing kernels of smoothness and . Suppose the Assumptions LABEL:as:equivalence, LABEL:as:app_true_g_smoothness, LABEL:as:app_true_J_smoothness, LABEL:as:app_lipschitz in Theorem 1 hold. Suppose . Then, for sufficiently large and , with and ,

holds with probability at least .

The proof of the theorem is relegated to Section˜D.3. Under ˜2, the expected error based on ˜4, up to logarithm terms. Here, the expectation is taken over the randomness of samples. Therefore, similarly to (D.36), the total cost and expected absolute error of multi-level nested kernel quadrature can be written as

| (D.37) |

If we take , then the error and the cost is

Equivalently, to reach error , the cost is .

Remark D.1 (Comparison of MLKQ and MLMC).

To reach a given threshold , the cost of MLKQ is , which is smaller than the cost of MLMC when the problem has sufficient smoothness, i.e. when . If we compare (D.36) and (D.37), the superior performance of MLKQ can be explained by the faster rate of convergence in terms of at each level when . Nevertheless, we can see in (D.37) that the MLKQ rate at each level in terms of is which is slower than the MLMC rate in (D.36). An empirical study of MLKQ is included in Figure˜6 which shows that MLKQ is better than MLMC in some settings but both are outperformed by NKQ by a huge margin. A more refined analysis of MLKQ is reserved for future work.

D.3 Proof of ˜2

The proof uses essentially the same analysis as in Step Five of Appendix˜C which translates into the generalization error of kernel ridge regression. First, we know that by following the same derivations as in (C) that

Given i.i.d. observations , the target of interest in the context of regression is the conditional mean, which in our case is precisely

Alternatively, can be viewed as noisy observation of the true function where the noise satisfied the following condition. For each and positive integer , similar to (C) we have,

where the second last inequality follows by replicating the same steps in (C), and the last inequality is true because . As a result, by replicating the steps for (C), we have

| (D.38) |

holds with probability at least . Next, we are going to upper bound . To this end, notice that

Using the same steps in (C) and (C) subsequently, we have

holds with probability at least . Similarly, we have which holds with probability at least . Consequently, we have which holds with probability at least . Therefore, plugging it back to (D.3), we obtain

holds with probability at least . Therefore, by taking , we obtain with probability at least ,

The proof is concluded.

Appendix E Further Background and Auxiliary Lemmas

All the results in this section are existing results in the literature. We provide them here and prove some of them in the specific context of Sobolev spaces explicitly for the convenience of the reader.

More technical notions of Sobolev spaces and the Sobolev embedding theorem

In the main text, we provide in (4) the standard definition of Sobolev spaces when . Actually, Sobolev spaces can be extended to that are positive real numbers. Such extension could be realized through real interpolation spaces (see [Bennett and Sharpley, 1988, Definition 1.7]), where .222Strictly speaking, the definition of (4) extended to real numbers actually corresponds to the complex interpolation space of Sobolev spaces. Fortunately, complex interpolation spaces and real interpolation spaces coincide under Hilbert spaces [Hytonen et al., 2016, Corollary C.4.2], which is precisely our setting since . Actually, such interpolation relations hold for any and [Adams and Fournier, 2003, Section 7.32],

| (E.39) |

A special case of the above relation is .

The Sobolev embedding theorem [Adams and Fournier, 2003], when applied to , states that if (where is the dimension of , then can be continuously embedded into , the space of continuous and bounded functions. In other words, for every equivalence class , there exists a unique continuous and bounded representative , and the embedding map : , defined by , is continuous. This continuous embedding can be written as . Since every continuous linear operator is bounded, we have bounded by a constant that only depends on .

More technical notions of reproducing kernel Hilbert spaces (RKHSs)

For bounded kernels, , its associated RKHS can be canonically injected into using the operator with its adjoint given by . and its adjoint can be composed to form a endomorphism called the integral operator, and a endomorphism

| (E.40) |

(where denotes the tensor product such that for ) called the covariance operator. Both and are compact, positive, self-adjoint, and they have the same eigenvalues . Please refer to Section 2 of Chen et al. [2024a] for more details.

Lemma 1 (Effective dimension ).

Let be a compact domain, be a probability measure on with density . is a Sobolev reproducing kernel of order . are the eigenvalues of the integral operator . Define the effective dimension as . If for any , then with constant that only depends on and .

Proof.

First, we study the asymptotic behavior of the eigenvalues of the integral operator . Theorem 15 of [Steinwart et al., 2009] shows that the eigenvalues share the same asymptotic decay rate as the squares of the entropy number of the embedding . Denote as the Lebesgue measure on . Since for any , we know so , and consequently we have from Equation (A.38) of Steinwart [2008] that

Moreover, [Edmunds and Triebel, 1996, Equation 4 on p. 119] shows that the entropy number for some constant , so we have and consequently we have .

Next, we have

where is a constant that depends on the domain and . ∎

Lemma 2.

Let be a compact domain, be a probability measure on with density . is a Sobolev reproducing kernel of order . are the eigenvalues and eigenfunctions of the integral operator . If there exists such that for any , then

| (E.41) |

holds for any . Here, is a constant that depends on and .

Proof.