Robust Optimization of Rank-Dependent Models

with Uncertain Probabilities††thanks: We are very grateful to Ronny Ben-Tal and to conference and seminar participants at

EURANDOM,

the SIAM Conference on Optimization (OP23),

the University of Amsterdam and

the University of Vienna for their comments and suggestions.

Python code to implement the optimization procedures developed in this paper is available from https://github.com/GuanJinNL/ROptRDU.github.io.git.

This research was funded in part by the Netherlands Organization for Scientific Research under grant NWO VICI 2020–2027 (Jin, Laeven).

Email addresses: G.Jin@uva.nl, R.J.A.Laeven@uva.nl, and D.denHertog@uva.nl.

Abstract

This paper studies distributionally robust optimization for a large class of risk measures with ambiguity sets defined by -divergences. The risk measures are allowed to be non-linear in probabilities, are represented by a Choquet integral possibly induced by a probability weighting function, and include many well-known examples (for example, CVaR, Mean-Median Deviation, Gini-type). Optimization for this class of robust risk measures is challenging due to their rank-dependent nature. We show that for many types of probability weighting functions including concave, convex and inverse -shaped, the robust optimization problem can be reformulated into a rank-independent problem. In the case of a concave probability weighting function, the problem can be further reformulated into a convex optimization problem with finitely many constraints that admits explicit conic representability for a collection of canonical examples. While the number of constraints in general scales exponentially with the dimension of the state space, we circumvent this dimensionality curse and provide two types of upper and lower bounds algorithms. They yield tight upper and lower bounds on the exact optimal value and are formally shown to converge asymptotically. This is illustrated numerically in two examples given by a robust newsvendor problem and a robust portfolio choice problem.

JEL Classification: C61, D81.

OR/MS Classification: Programming: Stochastic.

Decision analysis: Risk.

Keywords: Distributionally robust optimization; rank dependence; -divergence; probability weighting.

1 Introduction

Many stochastic optimization problems in management science, operations research, applied probability, economics, and finance arise from decisions involving risk (probabilities given) and ambiguity (probabilities unknown).

A variety of models for decision under risk has been proposed. Among the most popular and empirically viable models is the rank-dependent utility (RDU) model of Quiggin, (1982).111See also Schmeidler, (1986, 1989) for related pioneering developments. In RDU, the utility loss associated to a random variable under the probabilistic model is measured by a rank-dependent evaluation with respect to a non-additive, distorted measure :

where is a utility function, assumed to be non-decreasing, and , with and non-decreasing, a distortion or probability weighting function. RDU serves as a pivotal building block of prospect theory (Tversky and Kahneman,, 1992) and encompasses expected utility (von Neumann and Morgenstern,, 1944) when is linear and the dual theory of Yaari, (1987) when is affine. It accommodates Allais, (1953) type phenomena that are incompatible with expected utility. The utility function captures attitude toward wealth and the shape of the distortion function, e.g., concave, convex or (inverse) -shaped, dictates attitude toward risk. Importantly, under RDU the probabilities of outcomes are weighted according to , leading to an evaluation that is non-linear in probabilities, which depend on the ranking of outcomes. These non-linear and rank-dependent features bring major computational challenges.

In the aforementioned theories of decision under risk, is assumed to be given. When ambiguity is present, is unknown. Ambiguity is often treated via a worst-case approach that is robust against malevolent nature. For example, Gilboa and Schmeidler, (1989) propose maxmin expected utility, a.k.a. multiple priors, under which risks are evaluated according to their worst-case expected utility taken over a set of probabilistic models. Hansen and Sargent, (2001, 2007) introduce multiplier preferences under which probabilistic models far away from a reference model are penalized according to the Kullback-Leibler divergence (a.k.a. relative entropy). The variational preferences of Maccheroni et al., (2006) admit a general penalty function, thus significantly generalizing both models. Laeven and Stadje, (2023) develop a rank-dependent theory for decision under risk and ambiguity that encompasses both the dual and rank-dependent counterparts of Gilboa and Schmeidler, (1989) and Maccheroni et al., (2006).

Parallel to these developments, the field of (distributionally) robust optimization has been studying risk and ambiguity from a computational perspective. In robust optimization, ambiguity sets are often constructed exogenously from data, as a confidence region of the true underlying distribution, rather than endogenously based on preferences. A widely used family of statistical estimators for distributional uncertainty is given by -divergences (Csiszár,, 1975; Ben-Tal and Teboulle,, 1986, 1987; Pardo,, 2006). Many distributionally robust optimization problems with these types of ambiguity sets can be reformulated into a tractable robust counterpart, which can then be solved efficiently using standard optimization algorithms (see e.g., Ben-Tal et al.,, 2013, Wiesemann et al.,, 2014, and Esfahani and Kuhn,, 2018).

Although a variety of distributionally robust optimization techniques have been developed for optimization under uncertainty, most of the literature is concerned with models in which the probabilities appear linearly in the optimization problems, such as (possibly generalized) variants of expected value or expected utility maximization. Despite the growing interest in and applications of rank-dependent models across a wide variety of fields (see e.g., Denneberg,, 1994, Wakker,, 2010, Föllmer and Schied,, 2016, Eeckhoudt and Laeven,, 2021, and the references therein), optimization of these models, whether ambiguity is involved or not, is still relatively underdeveloped. The main difficulties lie in both the non-linearity in probabilities and the rank-dependence: for each value of a decision vector, the rank-dependent evaluation of an uncertain objective or constraint can be different, since the ranking of the outcomes may depend on the decision vector.

In this paper, we develop an efficient approach for optimizing rank-dependent models, with and without uncertain probabilities. More precisely, we study the following nominal and robust minimization problems, in a discrete probability setting:

| (1) | |||

| (2) |

where is the decision vector, is a set of constraints, is a random vector, is a deterministic function, is a -divergence ambiguity set (formally defined in (8)), and is a rank-dependent evaluation (formally defined in (5)), for some probability vectors .

Our main contributions can be summarized as follows:

- •

-

•

For concave distortion functions, we show that the reformulated robust counterpart admits a conic representation, if and are conic representable functions. For a list of canonical examples of and , we provide explicit epigraph representations of the reformulated robust counterpart that can directly be implemented into standard conic optimization programs such as CVXPY.

-

•

While the reformulated robust counterpart is more tractable than (1) and (2), its number of constraints increases exponentially in the dimension of the underlying discrete probability space. We provide two types of algorithms that can circumvent this curse of dimensionality. Each of them yields tight upper and lower bounds that, as we formally establish, converge to the optimal objective value of the exact problem. Moreover, we show that one of our algorithms can also be applied to a more general type of rank-dependent model, namely Choquet expected utility (Schmeidler,, 1989).222Under this model, the non-additive measure may, but need not, be obtained by distorting an additive probability measure.

-

•

We provide numerical examples of our approach in applications of robust optimization with rank-dependent models and uncertain probabilities, in the context of portfolio optimization and inventory planning. We obtain optimal decisions that are robust against uncertainty. Concrete examples with codes are provided on https://github.com/GuanJinNL/ROptRDU.github.io.git.

1.1 Related Literature

Our work builds on the decision theoretic literature on evaluating risk and ambiguity. Specifically, we consider rank-dependent evaluations of Quiggin, (1982) and adopt a robust approach as in Gilboa and Schmeidler, (1989), Hansen and Sargent, (2001, 2007), Maccheroni et al., (2006) and Laeven and Stadje, (2023), which can be viewed as generalized decision-theoretic foundations of the classical decision rule of Wald, (1950); see also Huber, (1981). We contribute to this literature by developing corresponding optimization techniques.

An initial connection between robust risk measures and robust optimization has been studied in an early paper by Bertsimas and Brown, (2009). They show that a decision maker’s preference, as represented by a coherent risk measure, can provide a device for constructing an uncertainty set for robust optimization purposes. The authors were able to obtain tractability results for distortion risk measures under a specific parameterization and the (strict) assumption that the underlying discrete probability space is uniform. Our paper relaxes these assumptions, while also providing a blueprint for constructing uncertainty sets tailored to general risk and ambiguity preferences. Postek et al., (2016) studied distributionally robust optimization (DRO) problems for a broad collection of uncertainty sets and risk measures. However, for certain classes of risk measures, such as distortion risk measures, the tractability remained unknown (see their Table I); they are covered as special cases in this paper. Although different choices of uncertainty sets are possible, our paper focuses on uncertainty sets defined by -divergences, which constitute a family of divergences including the Kullback-Leibler divergence, Burg entropy and Hellinger distance. The study of -divergences in DRO is motivated by several earlier studies; see Ben-Tal and Teboulle, (1986, 1987, 2007) and Ben-Tal et al., (1991).

Recently, Cai et al., (2023) and Pesenti et al., (2020) studied DRO problems involving distortion risk measures with general non-concave distortion functions. Their interesting results show that the DRO problem associated with a non-concave distortion function is equivalent to that with its concave envelope approximation, provided that the underlying uncertainty set obeys certain moment conditions. In this paper, we show that this equivalence is typically not satisfied in our general setting, thus requiring novel techniques. Optimization of nonexpected utility models with possibly non-concave distortion functions has also been studied by He and Zhou, (2011), in particular in the context of portfolio choice, introducing the so-called quantile method; see also Carlier and Dana, (2006). The effectiveness of this method relies on the ability to parametrize the distributions of all random objective functions , by a set of quantile functions that satisfy finitely many constraints. For a general convex function and feasibility set that are considered in (1), there is, however, no systematic approach to obtain such a quantile formulation. Our work provides a method to optimize (both robust and nominal) rank-dependent models for a broad class of decision problems and can directly be implemented in standard optimization software. Finally, Delage et al., (2022) and Wang and Xu, (2023) analyze ‘preference robust’ optimization, which considers uncertainty in the distortion function rather than in the underlying probabilistic model.

The remainder of the paper is organized as follows. Section 2 introduces the setting and notation. Sections 3 to 5 study the optimization problems (1) and (2) for concave distortion functions. The techniques we develop are extended in Section 6 to non-concave, inverse -shaped distortion functions. Section 7 presents our numerical experiments. Concluding remarks are in Section 8. In an Electronic Companion, we provide all the proofs, additional examples, and technical details.

2 Setup and Notation

2.1 Rank-Dependent Evaluation

Let be a measurable space. We define the rank-dependent evaluation of the utility loss associated with a random variable under a given probability measure on as the integral with respect to the non-additive measure (Denneberg,, 1994), or equivalently, as a Choquet integral (Choquet,, 1954):

| (3) | ||||

| (4) |

Here, is a non-decreasing utility function defined on a suitable domain containing the support of . Furthermore, the function is a distortion, or probability weighting, function that is non-decreasing and satisfies and . We note that is also known as a distortion risk measure when is the identity function. In this paper, we consider distortion functions that may be concave, convex or inverse -shaped.

Definition 1.

We say that is inverse -shaped if, for some , we have that is concave for and is convex for .

If is discrete with , then the integral (4) reduces to a rank-dependent sum. Let denote the ranked realizations of , with denoting the indices of the ranked realizations. The monotonicity of preserves the ranking of . Therefore, we have

| (5) |

where denotes the probability vector associated to and , by convention.

A well-known example of a rank-dependent evaluation is the Conditional-Value-at-Risk (a.k.a. Expected Shortfall), , which is defined as

| (6) |

where , , is the Value-at-Risk. For a certain level , can be interpreted as the (sign-changed) average of the left tail of the risk . It is easily verified that is a rank-dependent evaluation with linear utility function and distortion function . Other canonical examples of distortion functions are given in Table 4. The distortion function captures attitude toward risk whereas the utility function describes attitude toward wealth (see e.g., Quiggin,, 1982, Yaari,, 1987, Chew et al.,, 1987, and Eeckhoudt and Laeven,, 2021).

2.2 -Divergence Ambiguity Sets

In this paper, we construct ambiguity sets using -divergences. For discrete outcome spaces with , the -divergence between two probability vectors is defined as

| (7) |

Here, is a convex function that satisfies the following conventions: , and (see Pardo,, 2006, Definition 1.1). For a nominal probability vector and , the -divergence ambiguity set is defined as

| (8) |

Here, are the vectors with all entries equal to 0 and 1, respectively. As outlined in Ben-Tal et al., (2013) (Section 3.2), one may construct as a statistical confidence set by replacing with an empirical estimator . Indeed, as shown in Pardo, (2006) (Corollary 3.1), under the null-hypothesis , the following object converges to a chi-squared distribution:333From a statistical perspective, it may be more natural to consider , where the true model appears as the reference model. However, in the robust optimization literature, appears more commonly. Fortunately, according to Theorem 3.1 and Corollary 3.1 of Pardo, (2006), both objects have the same limiting distribution under the null.

| (9) |

Here, is the second derivative of evaluated at , is the sample size used for constructing the empirical estimator, and is the quantile of the chi-square distribution with degrees of freedom.444That is, , for . Using (9), one can construct an asymptotic confidence set by choosing

| (10) |

2.3 Problem Formulations, Terminology and Assumptions

We study the following nominal and robust minimization problems:

| (P-Nom) |

| (P) |

where is the decision vector contained in a compact set of constraints consisting of convex inequalities, is a random vector, is a jointly convex function in , is a -divergence ambiguity set defined in (8) with respect to a nominal probability vector , and is a rank-dependent evaluation defined in (5), with respect to some probability vector .

Henceforth, we often consider the robust rank-dependent evaluation in a constraint form induced by the following epigraph formulation:

| (11) |

and similarly for the nominal problem:

| (12) |

That is, we emphasize that we are able to deal with a robust rank-dependent evaluation both in the objective and in the constraint, where in the latter case we consider the following type of problem:

| (P-constraint) | ||||

where is convex in , and is a fixed parameter (in contrast to being an epigraph variable). The nominal version of (P-constraint) is defined analogously, with the only difference that the robust constraint is replaced by the nominal constraint (12).

Additionally, we would like to mention the alternative, but highly related, approach of defining a robust rank-dependent evaluation, which appears in the decision theory literature (see e.g., Laeven and Stadje,, 2023):

| (13) |

In Electronic Companion EC.4, we provide additional details on how (13) can be reformulated similar to (11), and that the minimization problem (P) is equivalent to minimizing (13) for a specific .

We let for an integer . The following assumptions are made throughout this paper:

Assumption 2.

The nominal probability vector satisfies for all .

Assumption 3.

The functions are lower-semicontinuous on their respective domains.

Assumption 4.

(P-constraint) is finite and contains a Slater point, i.e., there exists such that . Furthermore, we assume .

Assumption 1 can be satisfied if the image set is contained in a bounded interval. Assumption 2 constitutes a weak redundancy condition. Assumption 3 is to ensure that the optimization problem (P) has an optimal solution in , and Assumption 4 is to ensure that (P-constraint) satisfies the strong duality theorem.

In this paper, the term robust solution refers to an optimal solution of (P) or (P-constraint). Similarly, a nominal solution refers to an optimal solution of (P-Nom) or the nominal version of (P-constraint).

2.4 Further Notation

For a convex function , we denote by its convex conjugate , where is the effective domain of . Note that is always convex, since it is the pointwise supremum of a linear function in . Furthermore, is non-decreasing if . For , the perspective of is the function . By convention, and for . Note that is convex if is convex. The epigraph of a function is the set . An epigraph may have a conic representation expressed in a conic inequality , where is a proper cone (i.e., pointed, closed, convex and with a non-empty interior) and denotes its dual cone, defined as

see Chares, (2009) and Ben-Tal and Nemirovski, (2019) for further details.

3 Robust Counterpart of Rank-Dependent Models

In this section, we show how the optimization problems (P-Nom) and (P) can be reformulated into rank-independent problems with finitely many constraints. Our idea is to leverage the insight that a rank-dependent evaluation with a concave distortion function admits a dual representation that is itself a robust optimization problem with linear probabilities and convex uncertainty set. Although the dual representation holds only for concave distortion functions, we show in Section 6, how the same idea can be extended to encompass convex and inverse -shaped distortion functions. This enables us to conduct robust optimization with a broad class of rank-dependent models.

3.1 Reformulation of the Robust Counterpart

We start by reformulating the constraints (11) and (12) with concave distortion functions, since they form the basis of the more complicated convex and inverse -shaped cases described in Section 6. In Sections 3–5, we assume the utility function to be concave. The reformulation relies on utilizing the following dual representation, which involves a composite uncertainty set.

Theorem 1.

As a consequence, Theorem 1 implies that the robust problem (P) is equivalent to the following problem that is more suitable for robust optimization techniques:

| (P-ref) | ||||

Similarly, the nominal problem (P-Nom) can be reformulated to

| (P-Nom-ref) | ||||

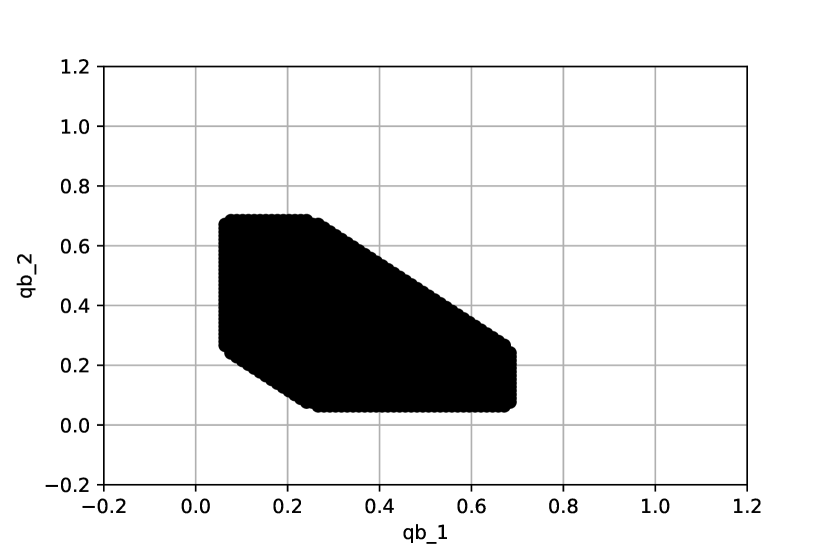

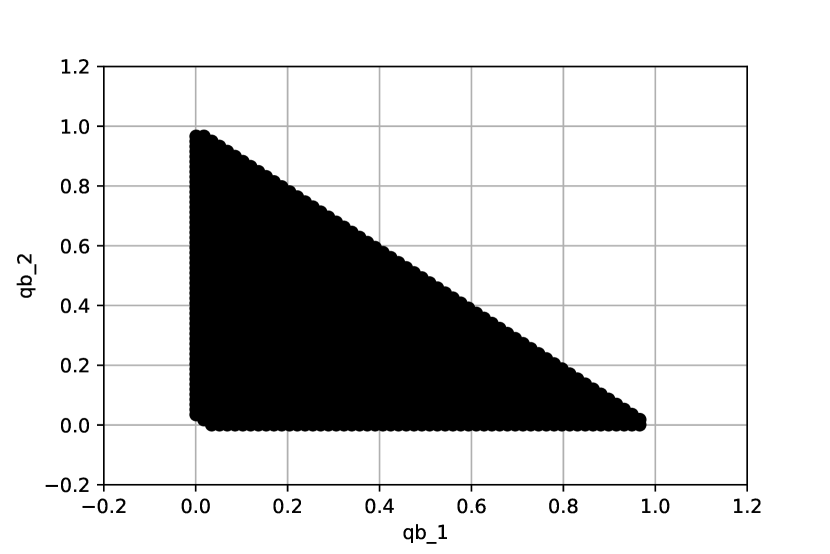

Moreover, the equivalence between (11) and (14) features an interpretation somewhat similar to that in Bertsimas and Brown, (2009), which connects the shape of an uncertainty set to decision theory. Indeed, this equivalence can be viewed as a device for constructing a myriad of preference-based uncertainty sets for robust optimization. In Figure 5 of Electronic Companion EC.5, we provide a visualization of the widely varying shapes of uncertainty sets that can be generated by selecting the deterministic, univariate functions and .

The following theorem states how the semi-infinite constraints (14) and (20) can be further reformulated into finitely many constraints.

Theorem 2.

Let be a concave distortion function. Then, we have that, for all , the inequality (14) holds if and only if there exist , such that

| (25) |

where are all subsets of , except the empty set and the set itself.

In the nominal case, we have that the inequality (20) holds if and only if there exist , such that

| (26) |

Remark 1.

For technical reasons, the conjugate in Theorem 2 is taken with respect to the domain : , by defining for all .

Remark 2.

In Table 4, we provide explicitly for a collection of canonical examples. (P-ref) can also be further reformulated using the “optimistic dual counterpart” (Gorissen et al.,, 2014). This approach is particularly useful if cannot be computed analytically, as is the case e.g., for , , with the standard normal cdf; see Wang, (2000) and Goovaerts and Laeven, (2008). Further details are provided in Electronic Companion EC.6.

3.2 Conic Representability of the Robust Counterpart

In this subsection, we explore the conic representability of the robust counterpart reformulated in Theorem 2. Following Ben-Tal and Nemirovski, (2019), a set is conic representable by a cone if and only if

A function is said to be conic representable if its epigraph is. The reformulated robust counterpart (25) in Theorem 2 contains constraints that are expressed in the perspective of the univariate conjugate functions and . We focus on the conic representability of these constraints:

In practice, the derivation of the conjugate functions might be difficult. However, the epigraph representation of a conjugate function does not always require an explicit form of the conjugate function itself. The following two lemmas provide a generic approach for determining the conic representation of the epigraph of the perspective function through that of the function itself. Interestingly, this procedure does not require any derivation of the conjugate function. In Tables 4 and 5, we provide explicit conic representation for many canonical examples of the conjugate functions and , where the representations are composed of a combination of standard cones such as the quadratic, the power, and the exponential. These explicit conic representations are useful for the implementation of these constraints in standard optimization software such as CVXPY. Details on the derivations of the epigraph representations can be found in the Electronic Companion EC.3.

The following two lemmas originate from Ben-Tal and Nemirovski, (2019) (Propositions 2.3.2 and 2.3.4), which were stated only for the quadratic cones. However, they can easily be extended to general cones.

Lemma 1.

If is conic representable with a cone , i.e., there exist such that

and for some , then is conic representable with the dual cone :

In particular, and are representable by the same cone if is self-adjoint.

Lemma 2.

If is conic representable with a cone , then so is its perspective.

We provide an example illustrating how the ideas in the proofs of Lemmas 1 and 2 can be systematically applied to determine the conic representation of the epigraph of the perspective transformation of a distortion function.

Example 1.

Consider the distortion function . Instead of deriving a closed-form expression of , which can be challenging, we determine a conic representation of the epigraph by first determining a conic representation of . We have

due to the fact that is decreasing on . Following the proof of Lemma 1, we have that if and only if

Since this is a bounded convex problem satisfying Slater’s condition, the duality theorem implies that the minimization problem is equal to

where in the last equality we computed explicitly.555 This gives that if and only if there exist such that

Finally, it follows from Lemma 2 that if and only if there exist such that

which is a combination of the power cone and the exponential cone.

In some cases, one can also calculate a conjugate function by writing it as an inf-convolution. For example, if is a sum of individual ’s: , then the conjugate of a sum is the inf-convolution of the sum of the conjugates (see Theorem 2.1, Bertsimas and den Hertog,, 2022):

where the infimum can eventually be omitted when considering the epigraph formulation.

4 Solving the Robust Problem I: A Cutting-Plane Method

As shown in Theorem 2, the number of reformulated constraints grows exponentially, as , where is the dimension of the probability vector. If is of small or moderate size, then the reformulations in (25) and (26) can be applied to solve the minimization problems (P) and (P-Nom) exactly. However, for larger , this becomes computationally intractable. In this section, we show how the reformulation of (P) to (P-ref) (and similarly for (P-Nom) to (P-Nom-ref)) by Theorem 1 enables us to devise a suitable cutting-plane method, which circumvents this curse of dimensionality.

4.1 The Cutting-Plane Algorithm

The basic cutting-plane algorithm is one of the most practical algorithms to solve robust optimization problems and has shown great efficiency in many applications (e.g., Mutapcic and Boyd,, 2009, Bertsimas et al.,, 2016). The general idea is simple: Approximate the uncertainty set with a suitably chosen subset and solve the corresponding robust problem, which is often a simpler problem, similar to the nominal problem. If the solution is feasible according to the robust evaluation with respect to the original set , then the process is terminated. Otherwise, the worst-case parameter in associated with the current solution is added to , and the process is repeated.

In our case, we apply the cutting-plane method to the reformulated problem (P-ref), where the uncertainty set is given by the composite set . After obtaining a candidate solution, we verify its feasibility with respect to the original uncertainty set . This involves solving the following optimization problem, for a given solution :

At first sight, this seems problematic due to the number of constraints in . Fortunately, this can be avoided, since the equivalent robust rank-dependent evaluation is the optimization problem:

| (27) |

This can be solved efficiently. Indeed, for a given solution , we can assess the ranking of the outcomes: . Then, by rewriting the alternating sum in (5), problem (27) is equal to the following convex optimization problem:

| (28) |

where . The optimal solution of (28) is a probability vector . This probability vector further yields a such that and , which is precisely the probability vector that constitutes the rank-dependent sum (5). The following lemma justifies that we may add the probability vectors as the worst-case probabilities at each iteration of the cutting-plane procedure.

Lemma 3.

We have that .

We can now describe the cutting-plane procedure in full detail, which we do more precisely in Algorithm 1.

| (29) | ||||

We note that the cutting-plane algorithm always computes a lower bound on the optimal objective value of (P-ref), since solving (29) at each iteration with respect to a subset is a less conservative problem. Moreover, the lower bounds are improved iteratively, since . Furthermore, by solving (28), which is a robust rank-dependent evaluation of a particular feasible solution, we also obtain an upper bound on (P-ref) at each iteration. Hence, at the final step of the cutting-plane algorithm, we obtain an upper and a lower bound on the exact optimal objective value (P-ref), with a gap value that can be chosen arbitrarily small.

The natural question that arises is whether the cutting-plane algorithm actually terminates after finitely many iterations, thus yielding convergent upper and lower bounds as . The following theorem, which has its roots in Mutapcic and Boyd, (2009), states that, for any , the termination is indeed guaranteed. We note that Mutapcic and Boyd, (2009) imposes Lipschitz continuity conditions, which we avoid in our setting.

Theorem 3.

Suppose . Then, for all , Algorithm 1 terminates after finitely many iterations.

4.2 Robust Optimization with a Rank-Dependent Evaluation in the Constraint

In the previous subsection, we have shown that our cutting-plane algorithm yields convergent upper and lower bounds to problem (P), where the rank-dependent evaluation appears in the objective function. In this subsection, we also discuss how the cutting-plane algorithm can be adapted to the robust problem (P-constraint), where the RDU model appears in the constraint, to provide a convergent lower bound. The adaptation of Algorithm 1 to problem (P-constraint) is relatively easy666In a nutshell, replace (29) in Algorithm 1 by (P-constraint) adapted to the set and replace in step 4 by the constraint parameter . and is presented in full detail in Algorithm 4 in Electronic Companion EC.2. The following theorem establishes the convergence of the cutting-plane algorithm.

Theorem 4.

Suppose . Then, for all , Algorithm 4 terminates after finitely many iterations. Moreover, the optimal objective value of the final solution obtained from Algorithm 4 converges to that of (P-constraint), as .

Thus, using the cutting-plane algorithm, we can obtain lower bounds that converge to the exact optimal objective value of (P-constraint), as . Naturally, one would also like to obtain an upper bound on (P-constraint), as well as a feasible solution of (P-constraint). We note that this is not guaranteed by the cutting-plane algorithm as described in Algorithm 4, since it only provides a solution that is feasible within a tolerance . With this objective in mind, we explore the rank-dependent nature of and propose a method to obtain an upper bound and a feasible solution of (P-constraint), which requires solving an optimization problem with only number of constraints. We first state the following definition.

Definition 2.

Given an , we let denote the set of all permutations of the index vector such that the ranking holds.

The idea is that for any given solution , we can determine a ranking of the realizations and obtain a vector of indices . A natural upper bound on (P-constraint) can then be computed by solving the following optimization problem induced by the ranking of :

| (30) | ||||

where the rank-dependent uncertainty set is

Indeed, since , solving (30) (which can be done using Theorem 2) would yield an upper bound and a feasible solution of (P-constraint). In particular, if is a good approximation of the optimal solution of (P-constraint), such that the ranking coincides, then is exactly equal to the optimal objective value of (P-constraint). This observation is made precise in the following lemma and is pivotal for developing a convergent upper bound for (P-constraint).

Lemma 4.

Let be a minimizer of (P-constraint). Then, for any such that , we have that the value as defined in (30) is equal to the optimal objective value of (P-constraint).

Lemma 4 suggests that if one approximates the optimal solution of (P-constraint) with a sequence of cutting-plane solutions as , then under certain continuity conditions, the upper bounds computed in (30) also converge to the exact value. This is established in the following theorem.

Theorem 5.

Assume . If the functions and are continuous on , for all , and is a sequence of solutions obtained from Algorithm 4 with , then is a sequence of upper bounds that converges to the optimal objective value of (P-constraint).

4.3 Choquet Expected Utility

In this subsection, we briefly discuss how our cutting-plane method can also be extended to solve optimization problems for a more general rank-dependent model, namely the Choquet expected utility model (Schmeidler,, 1986, 1989). Let be a monotone set function777 if . such that . The Choquet expected utility model evaluates a random variable by the Choquet integral:

| (31) |

The rank-dependent evaluation as defined in (4) is a special case of the Choquet expected utility, where . If is a submodular set function,888. then the Choquet expected utility can also be written as a worst-case expectation (see Denneberg,, 1994), similar to Theorem 1:

| (35) |

The uncertainty set has essentially the same structure as the set defined in (19) and consists of only linear constraints. Therefore, the same procedure of the cutting-plane algorithm can be extended naturally to solve the more general rank-dependent minimization problem . By contrast, the piecewise-linear approximation methods, which we will discuss in Section 5, constitute a more restrictive approach.

5 Solving the Robust Problem II: Piecewise-Linear Approximation

In this section, we develop a different method for computing lower and upper bounds on the optimal objective value of (P-ref), which is achieved by approximating the distortion functions, and is leveraged in Section 6.

5.1 Piecewise-Linear Distortion Functions

In this subsection, we show that if the distortion function is concave and piecewise-linear, then the exponential number of constraints in can be reduced to the order of , where is the dimension of the probability vector, and is the number of linear pieces of .

More precisely, we consider a function , with affine functions , such that the slopes are decreasing, and the intercepts are increasing. The affine functions are assumed to be defined on a set of support points , such that , for all . Furthermore, we impose and , so that and . We refer to this type of function as a -piecewise-linear distortion function. We note that these functions are non-decreasing and concave.

Lemma 5.

Let be a -piecewise-linear distortion function. Then, if and only if there exists a such that the variables satisfy the constraints:

| (36) |

Therefore, for -piecewise-linear distortion functions, we have the following reformulation of the robust counterpart (14).

Theorem 6.

Thus, for -piecewise-linear distortion functions, the exponential complexity in the uncertainty set can be reduced. This result provides us a tractable approximation for general non-piecewise-linear concave distortion functions, as we outline in the next subsection, exploiting that each concave function can be approximated uniformly by a piecewise-linear concave function.

5.2 Piecewise-Linear Approximation of General Concave Distortion Functions

For a general concave distortion function , we can also reduce the complexity in by approximating with a piecewise-linear function , such that for any given . An upper approximation and a lower approximation yield an upper and a lower bound on the optimal objective value of (P-ref), respectively. Uniform approximation of concave functions with piecewise-linear functions has been studied in the literature (see, e.g., Imamoto and Tang,, 2008, Cox,, 1971). Using the concavity of , one can approximate from below by choosing a set of support points and considering the concave piecewise-linear function that connects the values . Given an , the required number of support points can be minimized.

We outline the method of determining the minimal support points such that can be lower approximated by a piecewise-linear function with a prescribed error . This can be done as follows: Set . At the -th iteration, we choose the next support point such that the maximal error is equal to :

| (39) |

If , then we simply choose . Otherwise, we choose such that (39) holds. By construction, the piecewise-linear approximation induced by this set of support points has a maximum approximation error of and satisfies , due to concavity. The existence of such at each iteration is verified in the following lemma. Moreover, it suggests that we can solve (39) for using the bisection method.

Lemma 6.

Let be a continuous, increasing, strictly concave function on . Then, is an increasing and continuous function in . In particular, for any and iteration , if , then there exists a such that .

5.3 The Piecewise-Linear Approximation Method and its Convergence

Given a piecewise-linear lower approximation of , we can approximate the uncertainty set with and apply Theorem 6. This yields a lower bound on (P-ref). Similarly, the concave distortion function , which we define as

| (40) |

yields an upper approximation of with uniform error . Hence, we can also approximate by and apply Theorem 6 (note that the constraints (37) for are the same as those for , but with replaced by ). This yields an upper bound for (P-ref) since . Therefore, we obtain an upper and a lower bound using the piecewise-linear approximation method that we summarize in Algorithm 2. We also show that both bounds converge to the optimal objective value of the exact problem (P-ref), if the approximation error approaches zero. Thus, Algorithm 2 terminates for any parameter . This also applies, mutatis mutandis, to problem (P-constraint).

Theorem 7.

Suppose . Then, Algorithm 2 terminates after finitely many iterations, for any . This also holds if Algorithm 2 is applied to problem (P-constraint).

6 Non-Concave Distortion Functions

In the previous sections, we have discussed how to optimize a rank-dependent model when the distortion function is concave. We now extend these ideas to inverse -shaped distortion functions, which are often found in empirical work (see e.g., Wakker,, 2010, Prelec,, 1998). Optimization problems with non-concave distortion functions are challenging due to their non-convex nature. Moreover, rank-dependent models with non-concave distortion functions lack a dual representation, which was the major tool that allowed us to reformulate the rank-dependent problem. In some of the recent literature (e.g., Cai et al.,, 2023 and Pesenti et al.,, 2020), uncertainty sets with a specific structure have been identified for which optimizing the robust distortion risk measure with non-concave distortion function is equivalent to optimizing the same model with replaced by its concave envelope .999The concave envelope of a function is the smallest concave function that dominates . However, this equivalence is typically not satisfied in our setting, as we state in the following proposition.

Proposition 1.

Let be a compact set of probability vectors. Enumerate the realizations of as and suppose that does not contain the probability vector for which , which is concentrated on . Then, there exists a continuous distortion function such that

Therefore, it is necessary to study how to reformulate a robust or nominal rank-dependent evaluation constraint, in the case of an inverse -shaped distortion function. We will first study how to reformulate a nominal constraint of the form (12).

6.1 The Nominal Problem

Although rank-dependent models do not admit a dual representation for general non-concave distortion functions, we can still express them as an inner robust optimization problem if the distortion function is inverse -shaped. The idea is to treat the concave and the convex parts of the inverse -shaped function separately, where the convex part is transformed into a concave part via the dual function . This result is stated in the following theorem.

Theorem 8.

Remark 4.

In particular, if is convex, we have that

| (50) |

with .

Theorem 8 thus shows that (12) can be reformulated into rank-independent constraints (41), where the supremum constraint can be reformulated further as in Theorem 2. However, both (45) and (49) still contain an exponential number of constraints. As outlined in the previous section, we can circumvent this using piecewise-linear approximation. Let be a piecewise-linear, inverse -shaped distortion function with its concave and convex parts specified by the concave functions (note that is the dual of the convex part of ), respectively, on the domains and . Due to concavity and monotonicity, they can be expressed as minima of linear functions:

| (51) |

defined on the support points

such that, for all ,

| (52) |

The following theorem establishes a reformulation of the constraints in (41), when is piecewise-linear.

Theorem 9.

We note that (53) contains a non-convex constraint due to the product term . Therefore, the computation of the nominal problem (12) with the reformulated constraints in (53) requires a mixed-integer nonlinear programming (MINLP) solver, such as BARON that uses the branch and reduce search method to obtain a global optimum (see e.g., Ryoo and Sahinidis,, 1996). In particular, if the set is polyhedral (i.e., ), and is piecewise-linear, then the nomimal problem (12) with constraints (53) can also be solved efficiently by Gurobi (Gurobi Optimization, LLC,, 2023), using bilinear and SOS2 constraints; see the precise formulation in (EC.39) in Electronic Companion EC.8, further elaboration on the SOS2 constraints in (55), and a numerical study on the performance of Gurobi in this setting in Section 7.3.1.

6.2 Robust Rank-Dependent Models with Inverse -Shaped Distortion

In this subsection, we study the robust constraint (11) when is inverse--shaped. We note that then (11) cannot be reformulated using a composite uncertainty set as in (14), since the convex part of the distortion function gives rise to a sup-inf term when combining the set with (49). However, we can still circumvent this using a cutting-plane approach, where we iteratively solve a nominal problem using (53) and compute the robust rank-dependent evaluation for each nominal solution.

Indeed, for any given feasible solution , we can assess the ranking of the outcomes . Then, we calculate the robust rank-dependent evaluation:

| (54) |

Again, this non-convex problem can be computed using a solver such as BARON. If is piecewise-linear and the divergence function is linear or quadratic, then one can also solve (54) using SOS2 constraints in Gurobi. Specifically, given a set of support points , where , the SOS2 constraints can be formulated as follows:

| (55) | ||||

The SOS2 constraints control, for each , the variables in a way such that only two adjacent can be non-zero. Since the support points are ordered, the two non-zero adjacent variables ensure that we are only optimizing within each interval .

Thus, we can now introduce Algorithm 3, the cutting-plane approach that allows us to solve the robust problem (P) for piecewise-linear, inverse -shaped distortion functions.

| (56) | ||||

The following theorem establishes that this cutting-plane method terminates after finitely many iterations.

Theorem 10.

Let be an inverse -shaped, piecewise-linear distortion function. Suppose that . Then, for all , Algorithm 3 terminates after finitely many iterations.

Theorem 11.

Let be any two distortion functions such that . Suppose that . Then, the optimal objective value of (P-Nom) for converges to that of , as .

We note that when is an inverse--shaped distortion function, the piecewise-linear approximation specified by in (51) provides neither a lower bound nor an upper bound on , for all . Indeed, is a lower approximation of on , whereas is an upper approximation of on . Nonetheless, if one aims to bound on the entire , then we can apply the same device as in (40): translate with an (the maximal error) to obtain an upper piecewise-linear approximation of on , or do the same with the dual function for a lower approximation on . Theorem 11 then implies that the corresponding lower and upper bounds on the optimal objective value of (P-Nom) (or (P)), computed from these piecewise-linear approximations of , will converge to the exact optimal value, as .

Finally, we note that Algorithm 3 can also be adapted (similar to Algorithm 4 in the Electronic Companion) to solve problem (P-constraint), where the rank-dependent evaluation with inverse--shaped distortion function is in the constraint. Hence, we also present the following theorems with similar statements as in Theorems 10 and 11.

Theorem 12.

Let be an inverse -shaped, piecewise-linear distortion function. Suppose that is continuous in for all . Then, for any , Algorithm 3 terminates after finitely many iterations when applied to (P-constraint). If is also continuous, then the final solution of Algorithm 3 gives a lower bound that converges to the optimal objective value of (P-constraint) as .

Theorem 13.

Let be an inverse -shaped distortion function. Suppose that is continuous in for all . If , appearing in the objective, and are continuous, then for any distortion function such that for all and , the optimal objective value of (P-constraint) for converges to that of , as .

7 Numerical Examples

In this section, we apply the methods developed in this paper to two canonical examples of optimization problems: the newsvendor and portfolio choice problems. For both examples, we compare the solution of the robust problem (P) to the solution of the nominal problem (P-Nom). We use the phrase “robust/nominal solution” to refer to the solution of the robust/nominal problem.

7.1 Robust Single-Item Newsvendor

In the single-item newsvendor problem, a seller is uncertain about the demand for a certain product and has to decide in advance how many units of the product need to be ordered. Let be the realization of the demand in state . Furthermore, let be the cost of one unit of order, be the selling price, be the salvage value per unsold item returned to the factory, and be the loss per unit of unmet demand, which may include both the cost of a lost sale, and a penalty for the lost customer goodwill. Finally, let be the number of items ordered, i.e., the decision variable. The profit function is defined as

| (57) |

We note that is concave in since it is a sum of concave piecewise-linear functions in for all . Assume that the demand corresponding to low demand, medium demand, and high demand, with nominal probabilities . We assume that the number of items ordered will not exceed the maximum demand, i.e., . Furthermore, we set the parameter values .

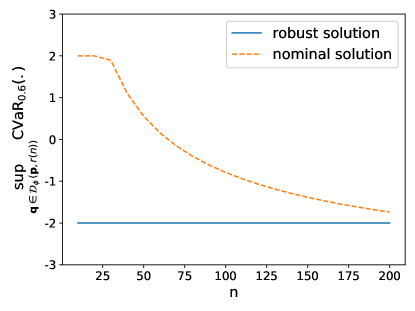

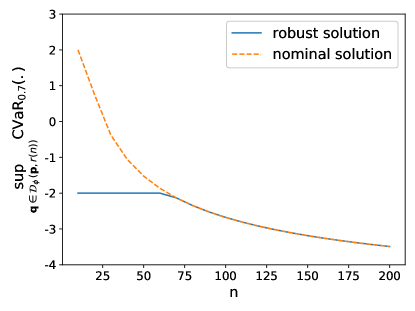

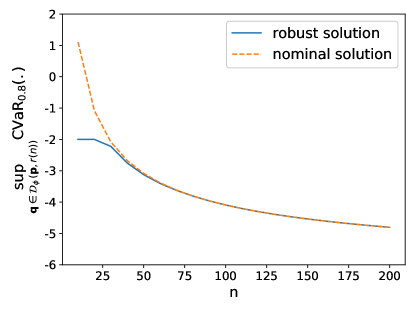

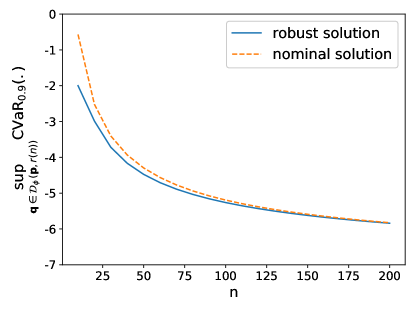

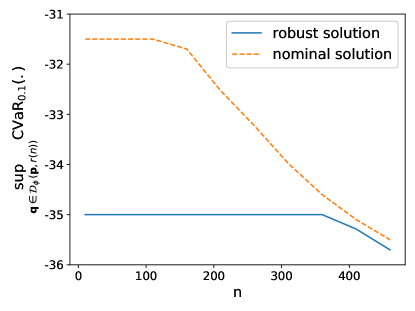

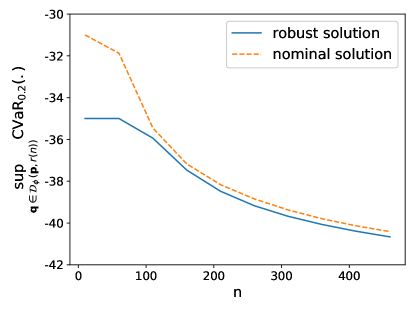

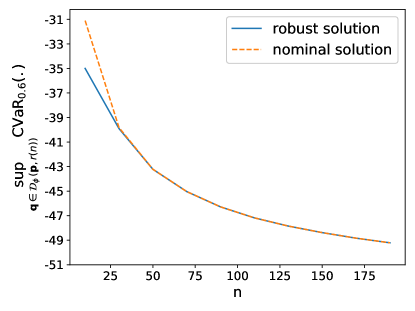

We solve both the robust problem (P) and the nominal problem , where is the decision variable subject to the constraint , is the uncertain parameter, and is the random objective function. We choose (see (6)) to be our rank-dependent evaluation . This corresponds to a piecewise-linear distortion function and a linear utility function . For the robust problem (P), we choose the KL-divergence function , and set the radius of the divergence set to be as in (10), where is a fictitious sample size that we assume that is estimated from.

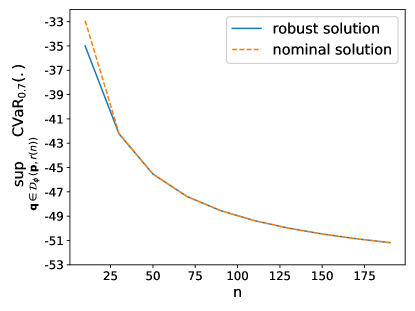

Since the number of realizations of the uncertain parameter is merely 3, we can simply apply Theorem 2 to solve both the reformulated nominal and robust problems (P-ref) and (P-Nom-ref), without using any approximations to reduce the number of constraints. We then perform the following experiment: For each , we first obtain a nominal solution by solving (P-Nom). Then, for each radius , we solve (P) to obtain a robust solution. To compare the robust solution with the nominal solution, we calculate their worst-case evaluation under the radius . This is repeated for a range of , and . As increases, the -divergence radius decreases, and thus there is less ambiguity. Therefore, we expect the difference between the worst-case evaluations of both solutions to decrease as increases. We also expect a decrease of the value of the worst-case evaluation as decreases, since the risk measure has a lower value with a smaller .

The results are displayed in Figure 1, which agree with our expectations. Furthermore, we see that for lower values of , the difference between the worst-case evaluations of both solutions is already small for low sample size of . We also observe a constant worst-case evaluation of the robust solution at . This is the largest value that the robust rank-dependent evaluation can attain for a solution . This conservativeness happens when is sufficiently small.

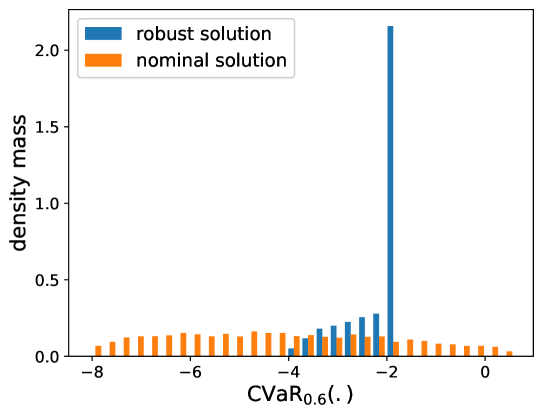

To further illustrate the difference between the robust and nominal solutions, we use the Hit-and-Run algorithm (see Electronic Companion EC.7 for further details) to sample probability vectors from the KL-divergence uncertainty set for . For each sampled vector , we calculate the evaluation under the sampled distribution vector for .

As shown in Figure 2, the evaluation of the nominal solution exhibits a large variance. It also exceeds the largest evaluation of the robust solution. On the other hand, the robust solution shows less variance and is concentrated at the value , which as mentioned before, is the most conservative evaluation that the robust optimal solution can attain.

7.2 Robust Multi-Item Newsvendor

We also examine the multi-item newsvendor problem, where each item has its own uncertain demand. Let be the -th realization of the -th item’s demand, . We assume that the demand takes on the same possible values for all items, i.e., for all . We take and consider the sum of the individual profit functions

| (58) |

where

| (59) |

with the parameters corresponding to item . Since each realization of contributes to a possible realization of , there are in total possible realizations. We solve again the problems (P) and (P-Nom) with the same set-ups as in the single-item problem. Since the risk measure has a piecewise-linear distortion function, we can apply Theorem 37 to solve (P-ref) and (P-Nom-ref). We take the nominal probability to be the probability of each combination of realizations of , which is the product of the probabilities of each individual realization. The parameters we used for our example are taken from Ben-Tal et al., (2013) and are given in Table 1.

| 1 | 4 | 6 | 2 | 4 | 0.375 | 0.375 | 0.25 |

| 2 | 5 | 8 | 2.5 | 3 | 0.25 | 0.25 | 0.5 |

| 3 | 4 | 5 | 1.5 | 4 | 0.127 | 0.786 | 0.087 |

Similar to the single-item problem, we investigate the difference in the worst-case risk evaluation of the robust and nominal solutions, for a range of and . We choose to compare the result with the single-item problem and to explore the higher values of . As shown in Figure 3, we see that in the multi-item problem, the worst-case risk evaluation value is much lower than the single-item problem. The pattern is similar to the single-item case, namely that for relatively lower , the difference in worst-case risk evaluation values between the robust solution and the nominal solution is smaller compared to the relatively higher . The same holds as the sample size increases.

7.3 Robust Portfolio Choice

In this subsection, we investigate the performance of the cutting-plane algorithm and the piecewise-linear approximation method described in Algorithms 1 and 2, by studying robust portfolio optimization problems. We use the returns of the six portfolios formed on size and book-to-market ratio (23) obtained from Kenneth French’s data library. We choose monthly returns from January 1984 to January 2014. This gives us a total of return realizations for each of the six portfolios. The nominal probability is set to be the empirical distribution with . We use the modified chi-squared divergence function , with radius . We choose the distortion function , motivated by two decision-theoretic papers: Eeckhoudt et al., (2020) and Eeckhoudt and Laeven, (2021). Furthermore, we choose the exponential utility function with .

We solve the following robust and nominal portfolio optimization problems:

| (60) | ||||

| (61) |

where is the total wealth after one period, evaluated under the rank-dependent model. The decision variable is subject to the constraints . We denote by the uncertain return of the six portfolios with realizations .

We solve problems (61) and (60) with the cutting-plane method described in Algorithm 1, and compare its performance to the piecewise-linear method described in Algorithm 2. As shown in Table 2, both algorithms yield a very small gap between the upper and lower bounds they provide. The piecewise-linear approximation method is typically faster, but this is not surprising, since the cutting-plane method is a more general method and utilizes less structure of the problems at hand.

| Panel A: The cutting-plane method | |||||

|---|---|---|---|---|---|

| Problem | Lower Bound | Upper Bound | # Cuts | Run Time | Optimal Portfolio |

| Robust | -0.08953 | -0.08948 | 5 | 54 sec | |

| Nominal | -0.09403 | -0.09397 | 5 | 22 sec | |

| Panel B: Piecewise-linear approximation | ||||

|---|---|---|---|---|

| Problem | Lower Bound | Upper Bound | Total Run Time | Optimal Portfolio (lb) |

| Robust | -0.08951 | -0.08948 | 14 sec | |

| Nominal | -0.09401 | -0.09398 | 7 sec | |

Additionally, for the two solutions obtained from the cutting-plane algorithm, we calculate the worst-case rank-dependent evaluation of the nominal solution, which is equal to . We also calculate the evaluation of the robust solution under the nominal distribution , which is equal to . As we can see, the worst-case evaluation of the nominal solution is not much larger than that of the robust solution, suggesting that the nominal solution is already “near-optimal” for the robust problem (61). Similarly, the robust solution is also “near-optimal” for the nominal problem (60). It seems that when the dimension of the state space is large, the robust and nominal problems do not yield very different solutions.

7.3.1 Robust Portfolio with Inverse -shaped Distortion Function

In this subsection, we investigate portfolio optimization problems (60) and (61), where is an inverse -shaped distortion function. In particular, we examine Prelec’s distortion function (Prelec,, 1998):

| (62) |

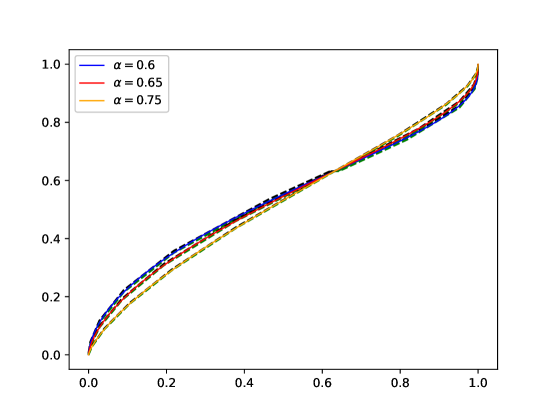

We examine three values of , where is the benchmark value that is most consistent with common empirical findings. To obtain an upper and a lower bound on the problems (60) and (61), we approximate the Prelec’s function from above and from below, using piecewise-linear functions consisting of 13 pieces. The approximation procedure is carried out by applying the method described in Section 5.2 separately to the concave and convex parts of the Prelec’s function, where we minimized the number of linear pieces under certain approximation error 101010The approximation error was chosen to be , , for respectively .. The shape of the Prelec’s functions with the chosen values of , and their respective upper and lower approximations, are plotted in Figure 4.

We generate 100 return data points for 5 assets using the same numerical scheme as in Esfahani and Kuhn, (2018), where the returns for each asset are composed of two factors:

where we have a systematic risk factor and an idiosyncratic risk factor , for the -th asset. Here, denotes the Gaussian distribution. By construction, the asset with a higher index has a higher expected return and variance.

We obtain lower and upper bounds on the nominal problem (60) by implementing the constraints (53) respectively for the lower and upper linear approximation of in the Gurobi (Version 11.0.3) solver. A lower bound for the robust problem (61) is obtained by calculating the lower bound obtained through the cutting-plane method described in Algorithm 3 (where we set ), while also using a lower approximation of . Then, with the solution obtained from the cutting-plane method, we determine an upper bound on (61) by calculating its worst-case evaluation using the SOS2-constraints as in (55). For the robust problem, we investigate both the total variation divergence and the modified chi-squared divergence . We choose the radius for both robust problems to be , where . The results are shown in Tables 3. As we can see, Gurobi solves the nominal problem (60) efficiently, but the robust problem (61) takes longer time (and considerably longer if is quadratic). Moreover, we observe tight upper and lower bounds, where most gap values are around .

| Panel A: Solutions Nominal Problem | |||||

| LB | UB | Run Time (LB) | Run Time (UB) | ||

| 0.6 | -1.146 | -1.142 | 0.77 sec | 0.76 sec | |

| 0.65 | -1.148 | -1.146 | 0.88 sec | 2.12 sec | |

| 0.75 | -1.153 | -1.152 | 0.45 sec | 1.00 sec | |

| Panel B: Solutions Robust Problem with | ||||||

| LB | UB | # Cuts | Run Time (LB) | Run Time (UB) | ||

| 0.6 | -1.042 | -1.040 | 9 | 227 sec | 1.29 sec | |

| 0.65 | -1.041 | -1.039 | 9 | 209 sec | 1.03 sec | |

| 0.75 | -1.039 | -1.038 | 9 | 127 sec | 1.21sec | |

| Panel C: Solutions Robust Problem with | ||||||

| LB | UB | # Cuts | Run Time (LB) | Run Time (UB) | ||

| 0.6 | -1.059 | -1.060 | 9 | 3700 sec | 334 sec | |

| 0.65 | -1.062 | -1.060 | 10 | 3825 sec | 521 sec | |

| 0.75 | -1.062 | -1.061 | 11 | 4262 sec | 162 sec | |

8 Concluding Remarks

In this paper, we have shown that non-robust and robust optimization problems involving rank-dependent models can be reformulated into rank-independent, tractable optimization problems. When the distortion function is concave, we have demonstrated that this reformulation admits a conic representation, which we have explicitly derived for canonical distortion and divergence functions. Whereas the number of constraints in the reformulation increases exponentially with the dimension of the underlying probability space, we have developed two algorithms to circumvent this curse of dimensionality. We have established that the upper and lower bounds the algorithms generate converge to the optimal objective value. Finally, we have illustrated the good performance of our methods in two examples involving concave as well as inverse--shaped distortion functions, yielding very tight upper and lower bounds.

As a direction for future research, one can investigate whether the approach developed in this paper can be extended to encompass robust optimization problems with general law-invariant convex risk measures, which also admit a dual representation.

References

- Allais, (1953) Allais, M. (1953). Le comportement de l’homme rationnel devant le risque: Critique des postulats et axiomes de l’école américaine. Econometrica, 21:503–546.

- Beck and Ben-Tal, (2009) Beck, A. and Ben-Tal, A. (2009). Duality in robust optimization: Primal worst equals dual best. Operations Research Letters, 37:1–6.

- Ben-Tal et al., (1991) Ben-Tal, A., Ben-Israel, A., and Teboulle, M. (1991). Certainty equivalents and information measures: Duality and extremal Principles. Journal of Mathematical Analysis And Applications, 157(1):211–236.

- Ben-Tal et al., (2013) Ben-Tal, A., den Hertog, D., de Waegenaere, A., Melenberg, B., and Rennen, G. (2013). Robust solutions of optimization problems affected by uncertain probabilities. Management Science, 59(2):341–357.

- Ben-Tal and Nemirovski, (2019) Ben-Tal, A. and Nemirovski, A. (2019). Lectures on Modern Convex Optimization. SIAM.

- Ben-Tal and Teboulle, (1986) Ben-Tal, A. and Teboulle, M. (1986). Expected utility, penalty functions, and duality in stochastic nonlinear programming. Management Science, 32(11):1445–1466.

- Ben-Tal and Teboulle, (1987) Ben-Tal, A. and Teboulle, M. (1987). Penalty functions and duality in stochastic programming via -divergence functionals. Mathematics of Operations Research, 12(2):224–240.

- Ben-Tal and Teboulle, (2007) Ben-Tal, A. and Teboulle, M. (2007). An old-new concept of convex risk measures: The optimized certainty equivalent. Mathematical Finance, 17(3):449–476.

- Berge, (1963) Berge, C. (1963). Topological Spaces: Including a Treatment of Multi-Valued Functions, Vector Spaces, and Convexity. Courier Corporation.

- Bertsimas and Brown, (2009) Bertsimas, D. and Brown, D. B. (2009). Constructing uncertainty sets for robust linear optimization. Operations Research, 57(6):1483–1495.

- Bertsimas and den Hertog, (2022) Bertsimas, D. and den Hertog, D. (2022). Robust and Adaptive Optimization. Dynamic Ideas LLC Belmont, Massachusetts.

- Bertsimas et al., (2016) Bertsimas, D., Dunning, I., and Lubin, M. (2016). Reformulation versus cutting-planes for robust optimization. Computational Management Science, 13(2):195–217.

- Bélisle et al., (1993) Bélisle, C. J., Romeijn, H. E., and Smith, R. L. (1993). Hit-and-Run algorithms for generating multivariate distributions. Mathematics of Operations Research, 18(2):255–266.

- Cai et al., (2023) Cai, J., Li, J. Y.-M., and Mao, T. (2023). Distributionally robust optimization under distorted expectations. Operations Research, 0(0).

- Carlier and Dana, (2006) Carlier, G. and Dana, R.-A. (2006). Law invariant concave utility functions and optimization problems with monotonicity and comonotonicity constraints. Statistics & Risk Modeling, 24(1):127–152.

- Chares, (2009) Chares, P. R. (2009). Cones and Interior-Point Algorithms for Structured Convex Optimization Involving Powers and Exponentials. Ecole polytechnique de Louvain, Université catholique de Louvain.

- Chew et al., (1987) Chew, S., Karni, E., and Safra, Z. (1987). Risk aversion in the theory of expected utility with rank dependent probabilities. Journal of Economic Theory, 42:370–381.

- Choquet, (1954) Choquet, G. (1954). Theory of capacities. Annales de l’Institut Fourier, 5:131–295.

- Cox, (1971) Cox, M. (1971). An algorithm for approximating convex functions by means by first degree splines. The Computer Journal, 14(3):272–275.

- Csiszár, (1975) Csiszár, I. (1975). -divergence geometry of probability distributions and minimization problems. Annals of Probability, 3:146–158.

- Delage et al., (2022) Delage, E., Guo, S., and Xu, H. (2022). Shortfall risk models when information of loss function is incomplete. Operations Research, 70(6):3511–3518.

- Denneberg, (1994) Denneberg, D. (1994). Non-Additive Measure and Integral. Springer.

- Eeckhoudt and Laeven, (2021) Eeckhoudt, L. R. and Laeven, R. J. (2021). Dual moments and risk attitudes. Operations Research, 70(3):1330–1341.

- Eeckhoudt et al., (2020) Eeckhoudt, L. R., Laeven, R. J., and Schlesinger, H. (2020). Risk apportionment: The dual story. Journal of Economic Theory, 185:104971.

- Esfahani and Kuhn, (2018) Esfahani, P. M. and Kuhn, D. (2018). Data-driven distributionally robust optimization using the Wasserstein metric: Performance guarantees and tractable reformulations. Mathematical Programming, 171:115–166.

- Föllmer and Schied, (2016) Föllmer, H. and Schied, A. (2016). Stochastic Finance, 4th ed. Berlin: De Gruyter.

- Gilboa and Schmeidler, (1989) Gilboa, I. and Schmeidler, D. (1989). Maxmin expected utility with non-unique prior. Journal of Mathematical Economics, 18(2):141–153.

- Goovaerts and Laeven, (2008) Goovaerts, M. J. and Laeven, R. J. A. (2008). Actuarial risk measures for financial derivative pricing. Insurance: Mathematics and Economics, 42(2):540–547.

- Gorissen et al., (2014) Gorissen, B. L., Blanc, H., Ben-Tal, A., and den Hertog, D. (2014). Technical Note- Deriving robust and globalized robust solutions of uncertain linear programs with general convex uncertainty sets. Operations Research, 62(3):672–679.

- Gorissen and den Hertog, (2015) Gorissen, B. L. and den Hertog, D. (2015). Robust nonlinear optimization via the dual. Optimizations Online.

- Gurobi Optimization, LLC, (2023) Gurobi Optimization, LLC (2023). Gurobi Optimizer Reference Manual.

- Hansen and Sargent, (2001) Hansen, L. P. and Sargent, T. J. (2001). Robust control and model uncertainty. American Economic Review, 91:60–66.

- Hansen and Sargent, (2007) Hansen, L. P. and Sargent, T. J. (2007). Robustness. Princeton University Press, stu-student edition.

- He and Zhou, (2011) He, X. D. and Zhou, X. Y. (2011). Portfolio choice via quantiles. Mathematical Finance, 21(2):203–231.

- Huber, (1981) Huber, P. J. (1981). Robust Statistics. Wiley, New York.

- Imamoto and Tang, (2008) Imamoto, A. and Tang, B. (2008). Optimal piecewise linear approximation of convex functions . Proceedings of the World Congress on Engineering and Computer Science.

- Laeven and Stadje, (2023) Laeven, R. J. and Stadje, M. (2023). A rank-dependent theory for decision under risk and ambiguity. Technical Report.

- Maccheroni et al., (2006) Maccheroni, F., Marinacci, M., and Rustichini, A. (2006). Ambiguity aversion, robustness, and the variational representation of preferences. Econometrica, 74(6):1447–1498.

- Muller, (1959) Muller, M. E. (1959). A note on a uniformly method for generating points on -dimensional spheres. Commun. Ass. Comput. Math., 2(4):19–20.

- Mutapcic and Boyd, (2009) Mutapcic, A. and Boyd, S. (2009). Cutting-set methods for robust convex optimization with pessimizing oracles. Optimization Methods & Software, 24(3):381–406.

- Pardo, (2006) Pardo, L. (2006). Statistical Inference Based on Divergence Measures. Chapman & Hall/ CRC Boca Raton.

- Pesenti et al., (2020) Pesenti, S., Wang, Q., and Wang, R. (2020). Optimizing distortion riskmetrics with distributional uncertainty. Paper. Available on ArXiv.

- Postek et al., (2016) Postek, K., den Hertog, D., and Melenberg, B. (2016). Computationally tractable counterparts of distributionally robust constraints on risk measures. SIAM Review, 58(4):603–650.

- Prelec, (1998) Prelec, D. (1998). The probability weighting function. Econometrica, 66(3):497–527.

- Quiggin, (1982) Quiggin, J. (1982). A theory of anticipated utility. Journal of Economic Behavior and Organization, 3(4):323–343.

- Rockafellar, (1970) Rockafellar, R. T. (1970). Convex Analysis. Princeton University Press, Princeton, NJ.

- Ryoo and Sahinidis, (1996) Ryoo, H. S. and Sahinidis, N. V. (1996). A branch-and-reduce approach to global optimization. Journal of Global Optimization, 8(2):107–138.

- Schmeidler, (1986) Schmeidler, D. (1986). Integral representation without additivity. Proceedings of the American Mathematical Society, 97:255–261.

- Schmeidler, (1989) Schmeidler, D. (1989). Subjective probability and expected utility without additivity. Econometrica, 57(3):571–587.

- Tversky and Kahneman, (1992) Tversky, A. and Kahneman, D. (1992). Advances in prospect theory: Cumulative representation of uncertainty. Journal of Risk and Uncertainty, 5:297–323.

- von Neumann and Morgenstern, (1944) von Neumann, J. and Morgenstern, O. (1944). Theory of Games and Economic Behavior. Princeton University Press, Princeton, 3 edition.

- Wakker, (2010) Wakker, P. P. (2010). Prospect Theory for Risk and Rationality. Cambridge University Press.

- Wald, (1950) Wald, A. (1950). Statistical Decision Functions. Wiley, New York.

- Wang, (2000) Wang, S. S. (2000). A class of distortion operators for pricing financial and insurance risks. The Journal of Risk and Insurance, 67(1):15–36.

- Wang and Xu, (2023) Wang, W. and Xu, H. (2023). Preference robust distortion risk measure and its application. Mathematical Finance, 33(2).

- Wiesemann et al., (2014) Wiesemann, W., Kuhn, D., and Sim, M. (2014). Distributionally robust convex optimization. Operations Research, 62(6):1358–1376.

- Yaari, (1987) Yaari, M. E. (1987). The dual theory of choice under risk. Econometrica, 55(1):95–115.

Appendix

Appendix EC.1 Proofs

Proof of Theorem 1.

Let be any probability vector and denote its corresponding probability measure on the sigma-algebra (the set of all subsets of ). The set function , is by Example 2.1, Denneberg, (1994), a monotone, submodular set function. It then follows from Proposition 10.3 of Denneberg, (1994) that for any random variable , we have

Hence, we have that

∎

Proof of Theorem 2.

Suppose a pair of satisfies

| (EC.1) |

Then, the left-hand side of (EC.1) is a maximization problem upper bounded by . Moreover, the set contains as a slater point, since and for all subsets that is not and .111111This is because for all due to concavity (excluding the trivial case where for all ) Therefore, strong duality holds, and we examine the Lagrangian function:

for and . We examine , which excluding the constant is equal to:

We examine both supremum terms separately. The first supremum gives:

The second supremum gives:

where and are the conjugates of and . Therefore, strong duality implies that a pair satisfies

if and only if

| subject to |

Since the infimum is attained due to the strong duality theorem and the boundedness of the primal problem (EC.1), we may remove the infimum sign and obtain that the above holds if and only if there exists such that

For the nominal problem, the Lagrangian function would be

Hence, we have

where the above strong duality holds since we are solving a linear programming problem. Therefore, we have that , if and only if there exists such that

∎

Proof of Lemma 1.

The proof is identical to Ben-Tal and Nemirovski, (2019), except that we replace the quadratic cone with a general cone. We have,

Therefore, we have if and only if

This minimization problem is strictly feasible and bounded from below. Hence, the conic duality theorem (see Ben-Tal and Nemirovski,, 2019) implies that it is equal to

Therefore, we have

∎

Proof of Lemma 3.

Proof of Theorem 3.

The proof follows the idea presented in Mutapcic and Boyd, (2009). First, we have, for any , that the following inequality holds:

| (EC.2) | ||||

where the first inequality follows from Cauchy-Schwarz. The second inequality follows from for a probability vector, since for .

Suppose now that the cutting-plane method has not terminated at the -th iteration, i.e., the optimal solution and objective value violate the -feasibility condition at step 4 of Algorithm 1. Let be the new worst-case scenario’s that are added to at step 5 of Algorithm 1. Then, by definition, we have

| (EC.3) |

For any , we also have that at the -th iteration:

| (EC.4) |

Since this is part of the constraint at the -th iteration. Let be the optimal objective value of (P-ref). By Assumption 1, we have that . Furthermore, we have for any iteration since the cutting-plane algorithm always yields a lower bound on (P-ref). Hence, we may assume that for and sufficiently large, the lower bounds improvement is upper bounded, i.e., , since otherwise the cutting-plane will yield a lower bound that exceeds , after finitely many iterations. Therefore, it follows from (EC.3) and (EC.4) that

which implies that

| (EC.5) |

This shows that the minimum distance between any two outcomes of the cutting-plane method, when evaluated in utility, is at least . The idea is now to show that if the cutting-plane method does not terminate, then there is a sequence of infinitely many cutting-plane solutions for which the corresponding vector remains in a bounded set. Since we know from above that each of these solutions, their utility values are of a distance away from each other, we conclude that the cutting-plane method must terminate since a bounded set can not contain infinitely many disjoint balls with radius , as argued in Mutapcic and Boyd, (2009).

Therefore, we define

Then, for all iterations , we have , since for all , we have the inequality . We show that is bounded in the Euclidean 2-norm . Indeed, by assumption, . Hence, for all vectors , its individual entry is always bounded from above by . It remains to show that all its entries are also bounded from below. Let (by Assumption 2 and . Then, we have for all

which implies,

Hence, is bounded in the Euclidean 2-norm . ∎

Before we proceed to the next proof, we need to recall the notion of KKT-vector. For a convex optimization problem,

the KKT-vector corresponding to the constraints is a vector such that

The existence of the KKT-vector is guaranteed by the Slater’s condition and the boundedness of the optimization problem (see Theorem 28.2, Rockafellar,, 1970).

Proof of Theorem 4.

The proof consists of two parts. In the first part, we show that Algorithm 4 terminates after finitely many iterations, for any . The second part shows the convergence as .

First part: We reexamine the proof of Theorem 3. First, we have, for any , the following inequality:

Let be an iteration where Algorithm 4 is not yet terminated. Let be the new worst-case scenario’s that are added to . Then, we have

For any , we also have that at the -th iteration:

Hence,

which implies that

We define the set

Then, for all iterations , we have , since for all . It follows from the proof of Theorem 3 that must be bounded in the Euclidean 2-norm . Hence, Algorithm 4 must terminate after finitely many steps.

Second part: Let be the objective value of the solution obtained at the final iteration of Algorithm 4, for a tolerance parameter . Let be the optimal objective value of (P-constraint). Define, for an ,

By construction, we have since is feasible for the problem of . Furthermore, the cutting-plane algorithm yields a lower bound on . Hence, for all . Therefore,

Therefore, it remains to bound from above. This can be done by utilizing the strong duality theorem, which is guaranteed by Assumption 4. Therefore, we have for any ,

where is the KKT-vector of the problem corresponding to the supremum constraint, which is a strictly positive constant (by Assumption 4) independent of . Hence, we have,

Therefore, the convergence follows as . ∎

Proof of Lemma 4.

We first show that for any , we have that

| (EC.6) |

for any set of ranking as in Definition 2. We fix and denote and a ranking , which by the monotonicity of induces a ranking . By the definition (4) of , we have that in a discrete probability setting, is equal to the rank-dependent sum

where . We now claim that we have an equality between the rank-dependent sum and the following optimization problem:

Indeed, we can define , where . Then, , and is a probability vector since , , and that is non-decreasing. Hence, is feasible for the above optimization problem. Furthermore, since for all , the maximum is attained at a vector such that the constraint is an equality for all , which uniquely defines . An expansion of the alternating sum shows that it is also equal to the sum . Therefore, (EC.6) holds for all and any ranking . Let be the optimal objective value of (P-constraint). Then, for any such that , we have that , since is feasible for the problem (30) by (EC.6). On the other hand, we also have the upper bound relation , since for any index vector . Hence, . ∎

Proof of Theorem 5.

Let . Denote . Since the set is compact, 121212The set is compact, due to the lower-semicontinuity assumption made in Assumption 3. we may assume that there exists a limit , as . We show that must be an optimal solution for (P-constraint). Indeed, since are maximizers, we have that

Taking the limit yields

Hence, by Theorem 1, this implies that is feasible for (P-constraint). Since is a sequence of solutions such that converges to the optimal objective value of (P-constraint) by Theorem 4, it follows from the continuity of that equals to the optimal objective value of (P-constraint). Hence, is an optimal solution of (P-constraint). Continuity of the functions in , for all , implies that there exists some , such that for all , we have the inclusion of the set of ranking: . Therefore, Lemma 4 implies that converges to the optimal objective value of (P-constraint). ∎

Proof of Lemma 5.

Proof of Theorem 6.

We reformulate the constraint,

where

We note that is a slater point in and that the above maximization problem is upper bounded by . Therefore, strong duality holds, and we examine the Lagrangian function:

We have

| (EC.7) | ||||

| (EC.8) |

Therefore, with the same argument as in the proof of Theorem 2, the reformulated robust counterpart is given by

In the nominal case where , we have to reformulate the following constraint:

where

Note that the above maximization problem is a linear programming problem bounded from above. Therefore, strong duality applies, and we examine the Lagrangian function:

By (EC.7) and (EC.8), we have that

Hence, the reformulated robust counterpart is

∎

Proof of Lemma 6.

We have that

since by the “decreasing slope” property of concavity, this supremum is only taken in the interval . Therefore, we can also extend the feasibility region to .

Using again the fact that a concave function has decreasing slope, we have that is an increasing function of , for all . Therefore, is increasing in . It is also a continuous function in . This is because the function

is convex in . Indeed, since it is a supremum of a linear function of . Hence, is continuous on the interior of its domain, which is the whole because is a supremum of a continuous function on a compact interval. Hence, exists and is finite everywhere. This implies that is continuous for all , since is a composition of continuous function, for all .

Finally, to show the existence of a such that , for any given , under the assumption that . This is true if we can find a such that . Since has decreasing slope and increasing, we have that for any , that for all :

Therefore,

Taking , it follows by the continuity of that such a point must exist. ∎

Proof of Theorem 7 (Part I).