FinMamba: Market-Aware Graph Enhanced Multi-Level Mamba for Stock Movement Prediction

Abstract.

Recently, combining stock features with inter-stock correlations has become a common and effective approach for stock movement prediction. However, financial data presents significant challenges due to its low signal-to-noise ratio and the dynamic complexity of the market, which give rise to two key limitations in existing methods. First, the relationships between stocks are highly influenced by multifaceted factors including macroeconomic market dynamics, and current models fail to adaptively capture these evolving interactions under specific market conditions. Second, for the accuracy and timeliness required by real-world trading, existing financial data mining methods struggle to extract beneficial pattern-oriented dependencies from long historical data while maintaining high efficiency and low memory consumption. To address the limitations, we propose FinMamba, a Mamba-GNN-based framework for market-aware and multi-level hybrid stock movement prediction. Specifically, we devise a dynamic graph to learn the changing representations of inter-stock relationships by integrating a pruning module that adapts to market trends. Afterward, with a selective mechanism, the multi-level Mamba discards irrelevant information and resets states to skillfully recall historical patterns across multiple time scales with linear time costs, which are then jointly optimized for reliable prediction. Extensive experiments on U.S. and Chinese stock markets demonstrate the effectiveness of our proposed FinMamba, achieving state-of-the-art prediction accuracy and trading profitability, while maintaining low computational complexity. The code is available at https://github.com/TROUBADOUR000/FinMamba.

1. Introduction

Stock movement prediction plays a pivotal role in data science-driven quantitative trading applications due to its potential to guide profitable investment strategies (Zou et al., 2023; Xia et al., 2024; Qian et al., 2024). Unlike general time series forecasting, stock prices record human-brain-armed game behaviors, which are influenced by various factors, including investor behavior, economic indicators, political events, and global news. This high level of volatility and the multifaceted nature of these influences make accurate prediction a particularly daunting challenge. Traditional machine learning approaches (Li et al., 2019; Zheng et al., 2024) have been used to address these challenges, but often require expert-designed features and struggle to capture the intricate dependencies between stocks. Recently, deep learning-based methods (Zeng et al., 2023; Wang et al., 2022b; Zhu et al., 2024) have shown great promise in overcoming these limitations by effectively combining stock features with inter-stock correlations (Yan and Tan, 2024). However, such a paradigm could still be unsatisfactory due to the following two limitations.

..

❶ Multifaceted inter-stock relationships under various market conditions. As is well known, synergy within the stock market is a key aspect, with related stocks often moving in sync (Wang et al., 2022b), providing valuable insights for more accurate predictions. Meanwhile, inter-stock relationships are influenced by various factors, such as sector dynamics, regulatory politics, and the macroeconomic market environment. Therefore, comprehensive modeling of relationships between stocks is crucial. Some of the existing methods (Gao et al., 2023; Xu et al., 2021; Wang et al., 2022b) rely on incomplete prior knowledge, which may introduce biases. For instance, solely grouping stocks by industry sectors can overlook cross-sector influences from broader macroeconomic factors. Additionally, stock relationships are dynamic, evolving with market fluctuations, making it difficult for static models to accurately reflect these changes. In contrast, posterior-based methods construct adjacency matrices to model dynamic correlations between stocks based on dynamic time warping (Xia et al., 2024), Pearson correlation coefficients (Xiang et al., 2022), Euclidean distance (Yan and Tan, 2024) or learning-based methods (Chen et al., 2024; Li et al., 2024). However, posterior methods can lead to spurious correlations, where stocks with no actual relationship exhibit high sequence similarity due to coincidental trends. Thus, we propose a graph-based structure to integrate both static prior correlations, such as industry classifications, and dynamic posterior correlations derived from stock price sequences, providing a more comprehensive framework for capturing inter-stock dependencies.

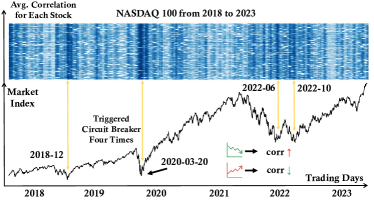

Furthermore, the role of macroeconomic markets in shaping stock relationships is often overlooked, despite their significant influence on inter-stock correlations (Wang and Li, 2020). As the stock market evolves, the inter-stock relationships also shift dynamically. As Fig. 1 depicts, during financial crises, stocks within the same industry tend to exhibit stronger correlations due to shared risk factors and similar investor behavior (Dimpfl, 2014). This phenomenon is amplified by the impact of market indices, which heighten the influence of macroeconomic conditions on stock performance during turbulent periods (Ma et al., 2022). Therefore, market indices are not only critical for gauging overall market performance but also play a key role in driving the dynamic relationships between stocks. To better capture these shifts, we propose a graph optimization strategy that refines stock relationship modeling by leveraging market index feedback, retaining dominant edges based on index movements while pruning those that fail to reflect dynamic changes. This approach enables the model to adaptively adjust inter-stock correlations in response to market fluctuations, resulting in more flexible predictions.

..

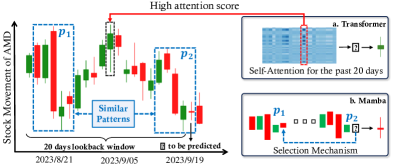

❷ Pattern-oriented dependencies under the timeliness constraints. The time series studied in the deep learning literature (Dai et al., 2024; Liu et al., 2024b) tend to exhibit some regularity (e.g., solar energy, traffic flow), facilitating the extraction of highly relevant features from similar repetitive patterns (Huang et al., 2024). In contrast, stock prices often lack regular repetitive patterns due to low signal-to-noise ratios (Duan et al., 2022), with similar patterns appearing at different periods and amplitudes. Recently, the Transformer (Vaswani et al., 2017), which calculates interactions between all sequence elements to capture their dependencies, has become a mainstream approach. However, its self-attention mechanism often assigns disproportionate importance to outliers, leading to an overemphasis on anomalous patterns and hindering the effective capture of smoother, more common trends across different time scales (Hu et al., 2024) (see Fig. 2(a)). After that, Mamba (Gu and Dao, 2024) has shown great potential in dynamic sequence modeling, with notable success in the other fields (Guo et al., 2024; Hatamizadeh and Kautz, 2024). The selective mechanism of Mamba enables it to recall temporal patterns from historical inputs, making the model particularly well-suited for capturing temporal dependencies in stock prices (see Fig. 2(b)). Moreover, real-time market trading imposes strict efficiency requirements for timely decision-making (Pan et al., 2024). In light of this, Mamba offers a key advantage with its lower linear complexity compared to the Transformer, significantly enhancing prediction efficiency.

Additionally, stock prices exhibit distinct characteristics across different time levels, gradually transitioning from micro to macro levels (Luo et al., 2021). On short-term, minute-level levels, price fluctuations are primarily driven by market microstructures, such as trader sentiment, high-frequency trading strategies, and market liquidity, often influenced by news, rumors, or technical indicators. As the time horizon extends to daily levels, mid-term factors like corporate performance, industry trends, and policy changes come into play (Lu and Wang, 2017). At weekly or monthly levels, macroeconomic forces such as economic growth, inflation, and monetary policy become the dominant drivers, reflecting structural market shifts and long-term trends. Therefore, analyzing stock price movements on a single time scale fails to comprehensively capture the full spectrum of temporal dependencies.(Ding et al., 2020).

Based on the above motivations, we propose FinMamba with Market-Aware Graph (MAG) and Multi-Level Mamba (MLM) to address existing limitations on the 1) multifaceted inter-stock relationships and 2) pattern-oriented characteristics of stock prices. Specifically, the MAG module adapts to effectively capture inter-stock relationships by integrating both the posterior and prior information, while refining according to macroeconomic market conditions. Then, the MLM module jointly models the micro- and macro-time level dependencies across the financial time series. Extensive experiments on U.S. and Chinese stock markets demonstrate the effectiveness of the proposed FinMamba, along with its low computational complexity. In a nutshell, our contributions are summarized as follows:

-

•

To the best of our knowledge, this is the first work that enhances the inter-stock relationships under specific macroeconomic market conditions, leading to a more impressive understanding of market dynamics.

-

•

We propose FinMamba that constructs a Market-Aware Graph integrating both static priors and dynamic posteriors, refines these relationships using market index feedback, and models stock pattern-oriented dependencies across multiple levels through a Multi-Level Mamba framework.

-

•

Extensive experiments on both U.S. and Chinese real-time stock markets demonstrate the state-of-the-art performance of the proposed FinMamba with high computational efficiency. The visualization results provided valuable insights into the dynamics of stock patterns.

2. Related Work

2.1. Stock Movement Prediction

Due to the growing interest in stock market investing and the evolution of deep learning, most contemporary research endeavors now center around implementing and refining deep learning models in the realm of stock movement prediction. Consequently, combining stock features with inter-stock correlations has become a common and effective approach for stock movement prediction. For example, THGNN (Xiang et al., 2022) employs a temporal and heterogeneous graph framework to extract insights from price history and relationships. MASTER (Li et al., 2024) mines the momentary and cross-time stock correlation with learning-based methods. CI-STHPAN (Xia et al., 2024) constructs channel independent hypergraphs among stocks with similar stock price trends based on dynamic time warping. Despite their success, current methodologies may still fall short by overlooking the fact that the relationship between individual stocks and the market index is such that it strengthens when the index falls and weakens when the index rises, especially during periods of market volatility.

2.2. Mamba and State Space Models

State Space Models (SSMs) (Gu et al., 2022; Gu and Dao, 2024; Dao and Gu, 2024) have emerged as a promising architecture for sequence modeling. Mamba, leveraging selective SSMs and a hardware-optimized algorithm, has achieved strong performance in several areas, including Natural Language Processing (Gu and Dao, 2024), Computer Vision (Guo et al., 2024; Hatamizadeh and Kautz, 2024). For time series forecasting, Timemachine (Ahamed and Cheng, 2024) selects contents for prediction against global and local contextual information with four SSM modules. Chimera (Behrouz et al., 2024) incorporates 2-dimensional SSMs with different discretization processes and input-dependent parameters to dynamically model the dependencies. However, the application of Mamba in quantitative trading is still in its infancy, with approaches such as MambaStock (Shi, 2024) applying the original Mamba for individual stock modeling and SAMBA (Mehrabian et al., 2024) using bidirectional Mamba blocks to capture long-term dependencies. In our work, we enhance Mamba by modeling similar stock patterns across different time spans through multi-level projection, while also incorporating inter-stock relationships and market influences to improve stock movement prediction.

3. Problem Definition

In this section, we will introduce some concepts in our proposed FinMamba framework and formally define the problem of stock movement prediction. For certain concepts and phenomena, we provide examples to facilitate understanding.

Definition 1. Stock Context. The set of all stocks is defined as , where represents a specific stock, denotes the total number of stocks, denotes the length of the lookback window and is the number of features. For any given stock , its data on trading day is defined as . Closing price is one of the features of and a one-day return ratio . On any given trading day , there exists an optimal ranking of the stock scores . For any two stocks , if , there exists an overall order between the ranks . Such an ordering of stocks on a trading day represents a ranking list, where stocks achieving higher ranking scores are expected to achieve a higher investment revenue (profit) on day .

Definition 2. Industry Decay Matrix. Investors believe that firms with similar industry characteristics should earn similar returns on average (Xia et al., 2024). The Industry Decay Matrix is designed to enhance the similarity characteristics within industries. Specifically, it assigns different decay coefficients to firms that belong to the same secondary industry , the same primary industry , or different industries.

..

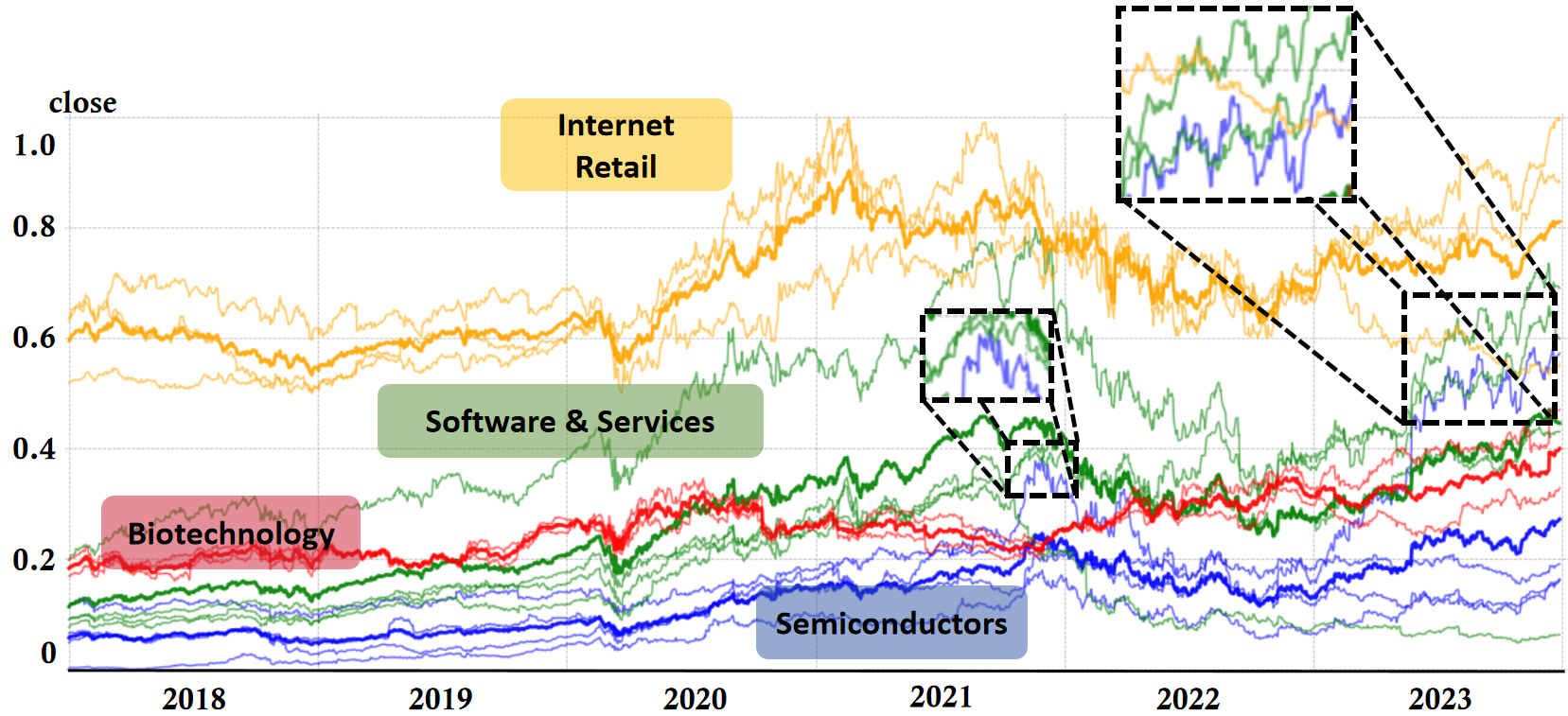

Example 1. Fig. 3 shows an example of fairly consistent movements among stocks within the same secondary industries. Moreover, within the same primary industries, such as Software & Services and Semiconductors, there are also similar movements over certain periods, reflecting higher-level relationships.

Definition 3. Dynamic Stock Correlation Graph. Given that stock relationships are subject to daily changes and shaped by market dynamics, we propose a Dynamic Stock Correlation Graph (DSCG) to capture and represent them. Let’s define the DSCG as , where represents a specific stock correlation for one day. In graphs, the node set denotes each stock and the edge set represents stock correlations. Each node corresponds to a stock . Each edge is assigned a weight , representing the relationship between and on trading day , where is the adjacency matrix. The edges with the top similarities indicate the dominant interactive relationships on trading day .

Definition 4. Market Index. A market index is defined as a statistical measure that tracks the performance of a specific segment of the macroeconomic financial market.

..

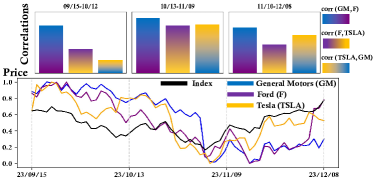

Example 2. Fig. 1 visualizes the correlation between the market index and individual stocks in the NASDAQ 100 from 2018 to 2023. A clear pattern emerges: the stock correlation strengthens as the market index falls and weakens as the market index rises. For instance, in March 2020, the COVID-19 outbreak in the U.S. revealed corporate debt risks and triggered a liquidity crisis, causing four circuit breakers in the stock market.

We propose the following hypothesis to explain this phenomenon: (1) From the perspective of investors and risk concentration, when the market index declines, systemic risk rises and investor pessimism increases, leading to greater synchronization among stocks and higher correlation. Conversely, when the market performs well, optimism drives capital into diverse sectors, causing stock performance to diverge and reducing correlation. (2) When the index rises, significant capital inflows into individual stocks can lower serial correlations, as diversified investment strategies spread buying interest, making price movements less synchronized.

Problem 1. Stock Movement Prediction. Formally, given the stock-specific information (e.g., historical price, stock correlation) of , we aim to learn a ranking function that outputs a score to rank each stock on the next day regarding expected profit.

4. Method

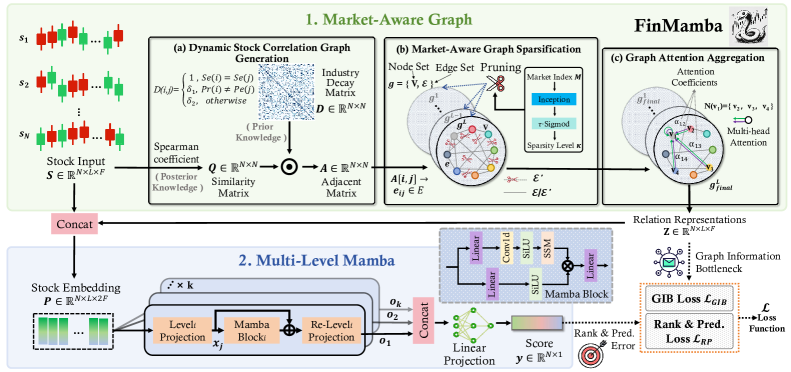

In the following sections, we will describe the architecture of the FinMamba as illustrated in Fig. 4, including the Market-Aware Graph and the Multi-Level Mamba. Market-Aware Graph extracts the dependencies between stocks over a period of time under specific market conditions, including both the posterior short-term relationship between stock sequences and the prior long-term industry relationship, while Multi-Level Mamba effectively captures similar stock movement patterns at multiple levels.

4.1. Market-Aware Graph

Market-Aware Graph captures stock node representations from graphs generated on each trading day and consists of three key components: Dynamic Stock Correlation Graph Generation, Market-Aware Graph Sparsification, and Graph Attention Aggregation.

Dynamic Stock Correlation Graph Generation

To model the comprehensive inter-stock correlations, represented by the adjacency matrix , we approach from the perspective of the posterior sequence correlations and the prior relationships of the primary and secondary industries.

In light of the fact that relationships between stocks are multifaceted and evolve on a daily basis (Qian et al., 2024), it is evident that the methodologies employed in previous studies, which rely on prior static correlation graphs based on predefined concepts or rules (Feng et al., 2019; Wang et al., 2022a), or those that generate posterior relationships directly from market history trends without incorporating additional domain-specific knowledge or news sources (Xiang et al., 2022; Yan and Tan, 2024; Liu et al., 2024c), are inadequate to accurately capture the dynamic and real-time inter-stock correlations.

Given these considerations, we first calculate the posterior Spearman coefficient between the actual stocks within a -length look-back window to measure the interactions between the stocks, yielding the similarity matrix . On trading day , the similarity between and can be formalized with:

| (1) |

where is the rank function.

Subsequently, we propose the prior Industry Decay Matrix , which models the relationships from an industry perspective, thereby extending the analysis beyond the inherent correlations within financial sequences themselves. To model the variety of different types of relationships existing between companies (e.g., Franchisor and Franchisee, shareholders and invested companies), we introduce primary and secondary industries, and define as follows:

| (2) |

Thus, represents a posterior short-term relationship that changes daily, while is a constant prior long-term relationship. Ultimately, we obtain an adjacency matrix by performing a dot product , where indicates an edge . Then a fully connected graph , representing a comprehensive and refined correlations between stocks , is generated.

Market-Aware Graph Sparsification

In the long-term process of adapting to market changes, a fundamental observation of investors is that interactions between stocks evolve over time, dynamically activating and expiring. This means that certain relationships may effectively reflect similar stock movements in certain market conditions but not in others. Traditional investors perform repeated statistical checks to identify relationships that are effective for portfolio selection, which is labour-intensive and challenging when combined with deep learning-based methods. To reduce manual effort, we propose the Market-Aware Graph Sparsification module, which incorporates market information to automatically select important inter-stock relationships.

Specifically, to ensure fairness without introducing additional information, for trading day , the market index is represented by the mean value of the stocks included in the target set of length preceding that day, rather than utilising an actual market index. The process of calculating market-aware sparsity level is formalized as follows:

| (3) |

where is a constant used to adjust the sparsity level. First, the 2D tensor is processed by a parameter-efficient inception block (Szegedy et al., 2015), designated as , which incorporates multi-scale 2D kernels and is widely recognized as a prominent vision backbone. Subsequently, the output of passes through the activation function to obtain the pruning sparsity level .

Finally, adaptive pruning is performed on the already generated fully connected graph to obtain the dominant correlations between stocks as perceived by the market over a certain period. The process of sparsification is formalized as follows:

| (4) |

where only modifies the edge set without altering the node set , and denotes the removed edges. The retained edges correspond to the edges with the top largest weights , where .

Graph Attention Aggregation

After generating a set of DSCG , we leverage a multi-head attention mechanism to aggregate the messages from neighboring nodes within graph structures. Concretely, for each stock (node ) on the trading day , we compute the attention coefficient of its neighboring stock (node ), denoting the importance of the edge in the pruned graph . It can formalized with:

| (5) |

where is the feature representation of nodes and , is the learnable weight matrix, is the weight vector of relation in -th head and function denotes the set of neighbors of node .

Then we aggregate the features of neighboring nodes of node using attention coefficients to generate a neighboring representation :

| (6) |

where denotes a non-linear activation function GELU and denotes the concatenation of the outputs from all heads.

Once we have the original representations and the neighboring representation , we concatenate them and get the stock embedding .

4.2. Multi-Level Mamba

Compared to other financial time series forecasting methods (e.g., RNN, CNN, Transformer), Mamba introduces a input-dependent selection mechanism that balances short-term and long-term dependencies, which is suitable for modeling stock data where similar stock patterns occur over different time spans. In earlier modules, we have already generated sequences that capture both short-term and long-term relationships, providing a strong foundation for this adaptive mechanism. However, stock data exhibit different temporal variations across various scales. Intuitively, in a stock price series, daily fluctuations are influenced by monthly economic trends, which in turn are influenced by annual market cycles. To better model the diverse patterns within the non-stationary dynamics of stocks, we designed a Multi-Level Mamba.

Technically, given the input , we project it onto different levels through distinct linear mappings, each designed to capture features at varying levels of granularity. These mappings, parameterized by unique transformation matrices, allow the model to extract multi-level pattern-oriented information by emphasizing either fine-grained local details or broader global patterns, enabling a richer representation. For each level , it is fed into Mamba block, where the continuous state space mechanism produces a response based on the observation of hidden state and the input , where is the output dimension. It can be formulated as:

| (7) | ||||

where , and are the parameters of Mamba block (Gu and Dao, 2024).

Afterward, we apply another linear mapping to restore the original level and concatenate them. Finally, a linear layer is used to obtain the predicted score of next trading day and is formed by concatenating along the time dimension.

| (8) |

Empowered by the multi-level state space mechanism, FinMamba learns similar stock patterns over random intervals at different levels, enabling it to integrate complementary forecasting capabilities from mixed multi-level series.

| Models | CSI 300 | CSI 500 | S&P 500 | NASDAQ 100 | ||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| ARR | AVol | MDD | ASR | IR | ARR | AVol | MDD | ASR | IR | ARR | AVol | MDD | ASR | IR | ARR | AVol | MDD | ASR | IR | |

| BLSW (1988) | -0.076 | 0.113 | -0.231 | -0.670 | 0.311 | 0.110 | 0.227 | -0.155 | 0.485 | 0.446 | 0.199 | 0.318 | -0.223 | 0.626 | 0.774 | 0.368 | 0.339 | -0.222 | 1.086 | 1.194 |

| CSM (1993) | -0.185 | 0.204 | -0.293 | -0.907 | -0.935 | 0.015 | 0.229 | -0.179 | 0.066 | 0.001 | 0.099 | 0.250 | -0.139 | 0.396 | 0.584 | 0.116 | 0.242 | -0.145 | 0.479 | 0.603 |

| AlphaStock (2019) | -0.164 | 0.153 | -0.245 | -1.072 | -1.098 | -0.017 | 0.148 | -0.166 | -0.115 | -0.043 | 0.122 | 0.140 | -0.126 | 0.871 | 0.892 | 0.372 | 0.178 | -0.134 | 1.781 | 1.869 |

| DeepPocket (2021) | -0.036 | 0.135 | -0.175 | -0.270 | -0.258 | 0.006 | 0.127 | -0.148 | 0.050 | 0.115 | 0.165 | 0.142 | -0.126 | 1.165 | 1.045 | 0.346 | 0.157 | -0.116 | 2.197 | 1.882 |

| Transformer (2017) | -0.240 | 0.156 | -0.281 | -1.543 | -1.695 | 0.154 | 0.156 | -0.135 | 0.986 | 0.867 | 0.135 | 0.159 | -0.140 | 0.852 | 0.908 | 0.268 | 0.175 | -0.131 | 1.531 | 1.441 |

| Mamba (2024) | -0.141 | 0.155 | -0.290 | -0.910 | -1.240 | 0.076 | 0.157 | -0.180 | 0.484 | 0.337 | 0.141 | 0.170 | -0.156 | 0.829 | 0.892 | 0.281 | 0.170 | -0.143 | 1.651 | 1.504 |

| FactorVAE (2022) | -0.048 | 0.134 | -0.175 | -0.335 | -0.348 | 0.006 | 0.127 | -0.147 | 0.047 | 0.112 | 0.160 | 0.142 | -0.132 | 1.128 | 1.013 | 0.356 | 0.159 | -0.119 | 2.234 | 1.907 |

| THGNN (2022) | -0.015 | 0.172 | -0.152 | -0.088 | -0.003 | 0.048 | 0.128 | -0.141 | 0.375 | 0.432 | 0.271 | 0.141 | -0.094 | 1.921 | 1.778 | 0.644 | 0.204 | -0.146 | 3.147 | 2.543 |

| MambaStock (2024) | -0.132 | 0.158 | -0.227 | -0.836 | -0.857 | 0.106 | 0.154 | -0.158 | 0.690 | 0.339 | 0.145 | 0.158 | -0.146 | 0.916 | 0.932 | 0.280 | 0.166 | -0.140 | 1.684 | 1.489 |

| CL (2024) | -0.035 | 0.148 | -0.183 | -0.241 | -0.193 | 0.051 | 0.146 | -0.128 | 0.351 | 0.390 | 0.308 | 0.189 | -0.171 | 1.629 | 1.451 | 0.351 | 0.172 | -0.122 | 2.041 | 1.821 |

| MASTER (2024) | 0.102 | 0.151 | -0.126 | 0.681 | 0.726 | 0.128 | 0.130 | -0.098 | 0.989 | 0.997 | 0.335 | 0.171 | -0.134 | 1.958 | 1.895 | 0.654 | 0.188 | -0.102 | 3.479 | 2.683 |

| CI-STHPAN (2024) | -0.078 | 0.167 | -0.144 | -0.466 | -0.355 | 0.021 | 0.151 | -0.129 | 0.136 | 0.211 | 0.123 | 0.233 | -0.254 | 0.527 | 0.632 | 0.454 | 0.208 | -0.124 | 2.178 | 1.855 |

| VGNN (2024) | -0.037 | 0.163 | -0.197 | -0.227 | -0.201 | 0.111 | 0.166 | -0.175 | 0.668 | 0.564 | 0.299 | 0.202 | -0.169 | 1.473 | 1.406 | 0.616 | 0.181 | -0.099 | 3.405 | 2.798 |

| PatchTST (2023) | -0.224 | 0.158 | -0.279 | -1.415 | -1.563 | 0.118 | 0.152 | -0.127 | 0.776 | 0.735 | 0.146 | 0.167 | -0.140 | 0.877 | 0.949 | 0.239 | 0.185 | -0.138 | 1.296 | 1.233 |

| iTransformer (2024a) | -0.115 | 0.145 | -0.190 | -0.793 | -0.775 | 0.214 | 0.168 | -0.164 | 1.276 | 1.173 | 0.159 | 0.170 | -0.139 | 0.941 | 0.955 | 0.188 | 0.196 | -0.202 | 0.963 | 0.937 |

| TimeMixer (2024) | -0.156 | 0.159 | -0.232 | -0.983 | -1.028 | 0.078 | 0.153 | -0.114 | 0.511 | 0.385 | 0.254 | 0.162 | -0.131 | 1.568 | 1.448 | 0.264 | 0.188 | -0.131 | 1.401 | 1.346 |

| Crossformer (2023) | -0.071 | 0.162 | -0.437 | -0.383 | -0.039 | 0.163 | 0.217 | -0.238 | 0.686 | 0.650 | 0.284 | 0.159 | -0.114 | 1.786 | 1.646 | 0.363 | 0.181 | -0.167 | 2.010 | 1.860 |

| FinMamba (Ours) | 0.106 | 0.163 | -0.102 | 0.653 | 0.705 | 0.227 | 0.163 | -0.106 | 1.389 | 1.339 | 0.341 | 0.164 | -0.086 | 2.063 | 1.937 | 0.685 | 0.190 | -0.097 | 3.601 | 2.851 |

4.3. Optimization Objectives

In stock movement prediction, the learning goal of FinMamba is to estimate the predicted denoting the positive return of all stocks on trading day t. For overall optimization, we combine point-wise regression loss and pair-wise ranking loss as:

| (9) |

Moreover, to guarantee that the learned stock embeddings efficiently capture the correlation within the dynamic graph structure and address the graph information bottleneck (Wu et al., 2020) issue by minimizing uncertainty in the graph, we incorporate GIB loss to minimize mutual information between the aggregation embedding and the original input, ensuring key information is retained while reducing irrelevant details.

| (10) |

Combining these two loss, we reach the complete end-to-end loss function with a weighting coefficient :

| (11) |

5. Expeiments

5.1. Experiment Setup

Datasets.

We conduct thorough experiments in both the U.S. and Chinese stock markets, selecting entities from the S&P 500111https://hk.finance.yahoo.com/quote/%5EGSPC/history/, NASDAQ 100222https://hk.finance.yahoo.com/quote/%5EIXIC/history, CSI 300333https://cn.investing.com/indices/csi300, and CSI 500444https://cn.investing.com/indices/china-securities-500. Our datasets comprise historical day-level market information, such as close, open, high, low, turnover and volume, from 2018 to 2023. See Sec. A.1 for a more detailed description of the datasets.

Baseline Models.

We compare FinMamba with other competitive models from different categories as follows: (1) Quantitative Investment Methods: a. Classic strategies: Buying-Loser-Selling-Winner (BLSW) (Poterba and Summers, 1988) and Cross-Sectional Mean reversion (CSM) (Jegadeesh and Titman, 1993); b. Deep Reinforcement Learning methods: AlphaStock (Wang et al., 2019), DeepPocket (Soleymani and Paquet, 2021); c. Deep Learning methods: Transformer (Vaswani et al., 2017), Mamba (Gu and Dao, 2024), FactorVAE (Duan et al., 2022), THGNN (Xiang et al., 2022), MambaStock (Shi, 2024), CL (Du et al., 2024), MASTER (Li et al., 2024), CI-STHPAN (Xia et al., 2024) and VGNN (Xing et al., 2024); (2) General Time Series Forecasting methods: PatchTST (Nie et al., 2023), iTransformer (Liu et al., 2024a), TimeMixer (Wang et al., 2024), and Crossformer (Zhang and Yan, 2023).

Metric.

We employ five widely used metrics to evaluate the overall performance of each method: Annual Return Ratio (ARR), Annual Volatility (AVol), Maximum Draw Down (MDD), Annual Sharpe Ratio (ASR), and Information Ratio (IR). Lower absolute values of AVol and MDD, along with higher ARR, ASR, and IR, indicate better performance. See Sec. A.3 for detailed descriptions.

Implementation Details.

Our experiment is trained on the NVIDIA V100 GPU, and all models are built using PyTorch (Paszke et al., 2019). The training and validation sets are kept consistent for all models. The number of GNN layers is 2, the number of levels is 2, and the window size is 20. See Sec. A.4 for detailed settings.

| Models | CSI 500 | NASDAQ 100 | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| ARR | AVol | MDD | ASR | CR | IR | ARR | AVol | MDD | ASR | CR | IR | |

| w/o industry decay matrix | 0.146 | 0.165 | -0.111 | 0.887 | 1.312 | 0.914 | 0.677 | 0.190 | -0.101 | 3.559 | 6.717 | 2.825 |

| w/o Market-Aware Sparsification | 0.064 | 0.162 | -0.186 | 0.391 | 0.341 | 0.462 | 0.399 | 0.184 | -0.112 | 2.166 | 3.543 | 1.923 |

| w/o Dynamic Stock Correlation | 0.128 | 0.168 | -0.113 | 0.757 | 1.125 | 0.799 | 0.384 | 0.188 | -0.115 | 2.043 | 3.351 | 1.831 |

| single level Mamba | 0.129 | 0.163 | -0.110 | 0.789 | 1.172 | 0.827 | 0.432 | 0.184 | -0.115 | 2.347 | 3.754 | 2.052 |

| w/o Mamba | 0.046 | 0.148 | -0.130 | 0.310 | 0.353 | 0.378 | 0.312 | 0.179 | -0.149 | 1.743 | 2.098 | 1.631 |

| FinTransformer | 0.194 | 0.168 | -0.144 | 1.152 | 1.352 | 1.142 | 0.671 | 0.183 | -0.117 | 3.676 | 5.726 | 2.717 |

| FinMamba | 0.227 | 0.163 | -0.106 | 1.389 | 2.135 | 1.339 | 0.685 | 0.190 | -0.097 | 3.601 | 7.085 | 2.851 |

..

Trading Protocols.

Following (Xiang et al., 2022), we use the daily buy-hold-sell trading strategy to evaluate the performance of stock movement prediction methods in terms of returns. During the test period, the trading process for each day is simulated as follows: First, at the end of the trading on day , the traders use FinMamba to generate prediction scores and rank expected returns for all stocks. Then, at the opening of , the traders sell the stocks purchased on day and buy those with higher predicted returns, focusing on the top ranked stocks. If a stock continues to be ranked with the highest predicted returns, it remains in the trader’s portfolio. Notably, the experiment does not take transaction costs into account.

5.2. Experiment Results

The overall performance is reported in Tab. 1. Our proposed FinMamba outperforms all other methods on most metrics. Based on these experimental findings, we draw the following conclusions:

TSF methods.

Deep learning-based general time series forecasting (TSF) methods, such as Crossformer (Zhang and Yan, 2023) and iTransformer (Liu et al., 2024a), do not exploit the graph relationships between stocks, making it difficult for them to achieve state-of-the-art performance. Moreover, such TSF methods rely primarily on historical data to predict future trends, lacking real-time decision-making and dynamic feedback mechanisms. Given the complexity of stock markets, relying solely on predictions is often insufficient to mitigate risk.

Graph-based quantitative investment methods.

Graph-based stock prediction models, such as THGNN (Xiang et al., 2022), VGNN (Xing et al., 2024) and CI-STHPAN (Xia et al., 2024) perform exceptionally well, demonstrating that incorporating relationships between stocks can significantly improve predictive performance. By leveraging graph structures to simulate synergies, these models capture the complex interactions and dependencies that exist between different stocks.

Marker-Aware quantitative investment methods.

The proposed FinMamba refines the inter-stock dependencies in the global set of stocks based on market feedback, while MASTER (Li et al., 2024) employs a gating mechanism to select effective factors for individual stocks, achieving optimal and suboptimal results respectively. This demonstrates the powerful ability of market information to optimize portfolio strategies. It is important to note that FinMamba performs well in ARR, ASR, CR, and IR across all four datasets, highlighting its superiority in stock movement prediction. FinMamba also shows strong performance in MDD, confirming that market-aware graph effectively captures complex, non-linear market behaviors by incorporating interactions with the market environment.

5.3. Ablation Study

To evaluate the effectiveness of each module in FinMamba, we perform extensive ablation experiments on the CSI 500 and NASDAQ 100 datasets, with results shown in Tab. 2. Excluding the industry decay matrix (w/o industry decay matrix) reduces performance, confirming the importance of our primary and secondary industry-related graph construction. Omitting Market-Aware Sparsification (w/o Market-Aware Sparsification) leads to a significant drop in performance, highlighting the module’s role in leveraging the relationship between the macroeconomic market index and whole stocks set and eliminating unnecessary noise introduced by irrelevant edges. Furthermore, ignoring stock relationships and treating Mamba purely as a time-series prediction task (w/o Dynamic Stock Correlation) or ignoring time-series information and using GNN purely for aggregating stock relationships (w/o Mamba) both result in performance degradation.

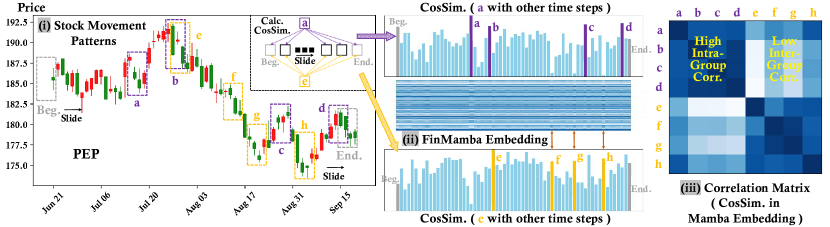

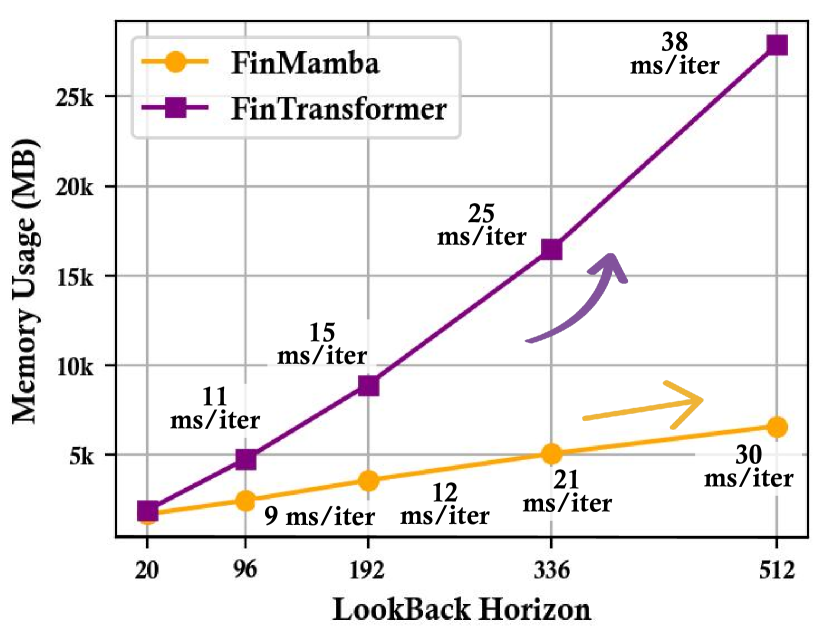

For a detailed comparison between Transformer (Vaswani et al., 2017) and Mamba (Gu and Dao, 2024), we first replace Mamba in FinMamba with Transformer (FinTransformer) for experiments, resulting in a slight performance decline. Subsequently, we visualize the model embeddings of the PEP stock from 23/06/21 to 23/09/20 in Fig. 5(a) (i). In the daily candlestick chart, we identify two groups of similar stock movement patterns: a to d and e to h. In the FinMamba embedding, we calculate the cosine similarity between pattern a and all other patterns, and also for pattern e, as shown in Fig. 5(a) (ii). The correlation matrix of the eight patterns is presented in Fig. 5(a) (iii). We observe that FinMamba effectively captures strong intra-group correlations, modeling well the temporal dependencies within similar patterns, and exhibits low inter-group correlations, reducing the impact of noise. This suggests that FinMamba can selectively retain similar inputs across different time intervals, making it highly effective for modeling stock data where recurring patterns may appear over varying time spans. Lastly, we evaluate the model complexity in terms of memory usage (MB) and inference time (ms/iter) for longer lookback horizons, as depicted in Fig. 5(b). The lightweight and efficient design of FinMamba, with its linear complexity, meets the timeliness requirement of algorithmic trading.

..

..

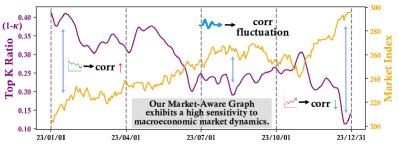

5.4. Sparsity Level in Market-Aware Graph

As shown in the Fig. 6, our Market-Aware Graph Sparsification is highly effective. When the market index is high, the relationships between stocks become weaker and it tends to retain fewer edges. Conversely, when the market index is low, the interactions between stocks become stronger and it tends to retain more edges.

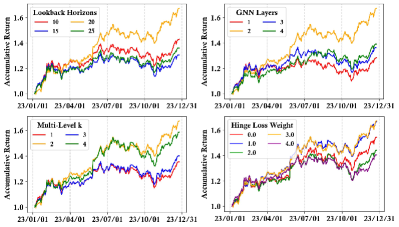

5.5. Parameter Sensitivity

Fig. 7 shows the effect of four hyperparameters on the NASDAQ 100 dataset. It appears that increasing lookback horizons enhances performance, but only up to a certain length, beyond which the additional input introduces more noisy signals, diminishing the effectiveness of information capture. A similar pattern occurs when increasing the number of GNN layers and the number of levels in MLM. In addition, since hinge loss guides the model more effectively in learning ranking information, it improves ranking performance but is constrained by MSE loss, which limits prediction accuracy.

5.6. Case Study

On 15 September 2023, the United Auto Workers (UAW) initiated its first-ever simultaneous strike against the “Detroit Big Three” automakers: General Motors, Ford, and Stellantis. Lasting a month and a half, the strike is expected to hinder these companies’ ability to compete with non-union automakers like Tesla and foreign brands. This case study examines the stock market’s response, focusing on the relationship between GM (General Motors), F (Ford) and TSLA (Tesla). As in Fig. 8, the correlation between GM and F remained strong throughout all three periods, reflecting their close ties as traditional auto giants. In contrast, TSLA’s correlation with GM and F was weaker in the first period, perhaps reflecting its distinct market position and growth prospects. However, in the subsequent periods, as the strike continued and competition intensified, the relationship between TSLA and the other two stocks notably strengthened. This suggests that FinMamba more accurately captures the evolving dynamics between the stocks, reflecting their interdependencies.

..

6. Conclusion

In this paper, we introduce a novel framework, FinMamba, which integrates a Market-Aware Graph and Multi-Level Mamba architecture. Through comprehensive quantitative and qualitative analysis of real-world stock market data, including CSI, NASDAQ, and S&P, we explore the ability of FinMamba to effectively extract features from financial time series and dynamic relational graphs enriched by market feedback. Our analysis demonstrates its potential for accurate stock movement prediction across diverse market environments. Looking ahead, we will further explore the broader applications of the Mamba architecture in quantitative trading.

References

- (1)

- Ahamed and Cheng (2024) Md Atik Ahamed and Qiang Cheng. 2024. TimeMachine: A Time Series is Worth 4 Mambas for Long-term Forecasting.

- Behrouz et al. (2024) Ali Behrouz, Michele Santacatterina, and Ramin Zabih. 2024. Chimera: Effectively Modeling Multivariate Time Series with 2-Dimensional State Space Models. In The Thirty-eighth Annual Conference on Neural Information Processing Systems. https://openreview.net/forum?id=ncYGjx2vnE

- Chen et al. (2024) Weijun Chen, Shun Li, Xipu Yu, Heyuan Wang, Wei Chen, and Tengjiao Wang. 2024. Automatic De-Biased Temporal-Relational Modeling for Stock Investment Recommendation. In Proceedings of the Thirty-Third International Joint Conference on Artificial Intelligence, IJCAI-24, Kate Larson (Ed.). International Joint Conferences on Artificial Intelligence Organization, 1999–2008. https://doi.org/10.24963/ijcai.2024/221 Main Track.

- Dai et al. (2024) Tao Dai, Beiliang Wu, Peiyuan Liu, Naiqi Li, Jigang Bao, Yong Jiang, and Shu-Tao Xia. 2024. Periodicity Decoupling Framework for Long-term Series Forecasting. International Conference on Learning Representations (2024).

- Dao and Gu (2024) Tri Dao and Albert Gu. 2024. Transformers are SSMs: Generalized Models and Efficient Algorithms Through Structured State Space Duality. In International Conference on Machine Learning. https://openreview.net/forum?id=ztn8FCR1td

- Dimpfl (2014) Thomas Dimpfl. 2014. A note on cointegration of international stock market indices. International Review of Financial Analysis 33 (2014), 10–16. https://doi.org/10.1016/j.irfa.2013.07.005

- Ding et al. (2020) Qianggang Ding, Sifan Wu, Hao Sun, Jiadong Guo, and Jian Guo. 2020. Hierarchical Multi-Scale Gaussian Transformer for Stock Movement Prediction. In Proceedings of the Twenty-Ninth International Joint Conference on Artificial Intelligence, IJCAI-20, Christian Bessiere (Ed.). International Joint Conferences on Artificial Intelligence Organization, 4640–4646. https://doi.org/10.24963/ijcai.2020/640 Special Track on AI in FinTech.

- Du et al. (2024) Kelvin Du, Rui Mao, Frank Xing, and Erik Cambria. 2024. Explainable Stock Price Movement Prediction using Contrastive Learning. In Proceedings of the 33rd ACM International Conference on Information and Knowledge Management (CIKM ’24). Association for Computing Machinery, New York, NY, USA.

- Duan et al. (2022) Yitong Duan, Lei Wang, Qizhong Zhang, and Jian Li. 2022. FactorVAE: A Probabilistic Dynamic Factor Model Based on Variational Autoencoder for Predicting Cross-Sectional Stock Returns. Proceedings of the AAAI Conference on Artificial Intelligence (2022).

- Feng et al. (2019) Fuli Feng, Xiangnan He, Xiang Wang, Cheng Luo, Yiqun Liu, and Tat-Seng Chua. 2019. Temporal Relational Ranking for Stock Prediction. ACM Trans. Inf. Syst. (2019).

- Gao et al. (2023) Siyu Gao, Yunbo Wang, and Xiaokang Yang. 2023. StockFormer: Learning Hybrid Trading Machines with Predictive Coding. In International Joint Conference on Artificial Intelligence.

- Gu and Dao (2024) Albert Gu and Tri Dao. 2024. Mamba: Linear-Time Sequence Modeling with Selective State Spaces. In First Conference on Language Modeling. https://openreview.net/forum?id=tEYskw1VY2

- Gu et al. (2022) Albert Gu, Karan Goel, and Christopher Re. 2022. Efficiently Modeling Long Sequences with Structured State Spaces. In International Conference on Learning Representations. https://openreview.net/forum?id=uYLFoz1vlAC

- Guo et al. (2024) Hang Guo, Jinmin Li, Tao Dai, Zhihao Ouyang, Xudong Ren, and Shu-Tao Xia. 2024. MambaIR: A Simple Baseline for Image Restoration with State-Space Model. In ECCV.

- Hatamizadeh and Kautz (2024) Ali Hatamizadeh and Jan Kautz. 2024. MambaVision: A Hybrid Mamba-Transformer Vision Backbone.

- Hu et al. (2024) Yifan Hu, Peiyuan Liu, Peng Zhu, Dawei Cheng, and Tao Dai. 2024. Adaptive Multi-Scale Decomposition Framework for Time Series Forecasting.

- Huang et al. (2024) Hongbin Huang, Minghua Chen, and Xiao Qiao. 2024. Generative Learning for Financial Time Series with Irregular and Scale-Invariant Patterns. In International Conference on Learning Representations. https://openreview.net/forum?id=CdjnzWsQax

- Jegadeesh and Titman (1993) Narasimhan Jegadeesh and Sheridan Titman. 1993. Returns to Buying Winners and Selling Losers: Implications for Stock Market Efficiency. Journal of Finance 48 (1993), 65–91. https://api.semanticscholar.org/CorpusID:13713547

- Li et al. (2024) Tong Li, Zhaoyang Liu, Yanyan Shen, Xue Wang, Haokun Chen, and Sen Huang. 2024. MASTER: Market-Guided Stock Transformer for Stock Price Forecasting. Proceedings of the AAAI Conference on Artificial Intelligence 38 (2024).

- Li et al. (2019) Zhige Li, Derek Yang, Li Zhao, Jiang Bian, Tao Qin, and Tie-Yan Liu. 2019. Individualized Indicator for All: Stock-wise Technical Indicator Optimization with Stock Embedding. In Proceedings of the 25th ACM SIGKDD International Conference on Knowledge Discovery & Data Mining (Anchorage, AK, USA) (KDD ’19). Association for Computing Machinery, New York, NY, USA, 894–902. https://doi.org/10.1145/3292500.3330833

- Liu et al. (2024c) Mengpu Liu, Mengying Zhu, Xiuyuan Wang, Guofang Ma, Jianwei Yin, and Xiaolin Zheng. 2024c. ECHO-GL: Earnings Calls-Driven Heterogeneous Graph Learning for Stock Movement Prediction. Proceedings of the AAAI Conference on Artificial Intelligence (2024).

- Liu et al. (2024b) Peiyuan Liu, Beiliang Wu, Yifan Hu, Naiqi Li, Tao Dai, Jigang Bao, and Shu-Tao Xia. 2024b. TimeBridge: Non-Stationarity Matters for Long-term Time Series Forecasting. arXiv preprint arXiv:2410.04442 (2024).

- Liu et al. (2024a) Yong Liu, Tengge Hu, Haoran Zhang, Haixu Wu, Shiyu Wang, Lintao Ma, and Mingsheng Long. 2024a. iTransformer: Inverted Transformers Are Effective for Time Series Forecasting. In International Conference on Learning Representations.

- Lu and Wang (2017) Yunfan Lu and Jun Wang. 2017. Multivariate multiscale entropy of financial markets. Communications in Nonlinear Science and Numerical Simulation 52 (2017), 77–90. https://doi.org/10.1016/j.cnsns.2017.04.028

- Luo et al. (2021) Changqing Luo, Lan Liu, and Da Wang. 2021. Multiscale financial risk contagion between international stock markets: Evidence from EMD-Copula-CoVaR analysis. The North American Journal of Economics and Finance 58 (2021), 101512. https://doi.org/10.1016/j.najef.2021.101512

- Ma et al. (2022) Chaoqun Ma, Ru Xiao, and Xianhua Mi. 2022. Measuring the dynamic lead–lag relationship between the cash market and stock index futures market. Finance Research Letters 47 (2022), 102940. https://doi.org/10.1016/j.frl.2022.102940

- Mehrabian et al. (2024) Ali Mehrabian, Ehsan Hoseinzade, Mahdi Mazloum, and Xiaohong Chen. 2024. Mamba Meets Financial Markets: A Graph-Mamba Approach for Stock Price Prediction.

- Nie et al. (2023) Yuqi Nie, Nam H Nguyen, Phanwadee Sinthong, and Jayant Kalagnanam. 2023. A Time Series is Worth 64 Words: Long-term Forecasting with Transformers. In International Conference on Learning Representations.

- Pan et al. (2024) Kaiming Pan, Yifan Hu, Li Han, Haoyu Sun, Dawei Cheng, and Yuqi Liang. 2024. Cross-contextual Sequential Optimization via Deep Reinforcement Learning for Algorithmic Trading. In Proceedings of the 33rd ACM International Conference on Information and Knowledge Management (Boise, ID, USA) (CIKM ’24). Association for Computing Machinery, New York, NY, USA, 4811–4818.

- Paszke et al. (2019) Adam Paszke, Sam Gross, Francisco Massa, Adam Lerer, James Bradbury, Gregory Chanan, Trevor Killeen, Zeming Lin, Natalia Gimelshein, Luca Antiga, et al. 2019. Pytorch: An imperative style, high-performance deep learning library. Advances in neural information processing systems 32 (2019).

- Poterba and Summers (1988) James M. Poterba and Lawrence H. Summers. 1988. Mean reversion in stock prices: Evidence and Implications. Journal of Financial Economics (1988).

- Qian et al. (2024) Hao Qian, Hongting Zhou, Qian Zhao, Hao Chen, Hongxiang Yao, Jingwei Wang, Ziqi Liu, Fei Yu, Zhiqiang Zhang, and Jun Zhou. 2024. MDGNN: Multi-Relational Dynamic Graph Neural Network for Comprehensive and Dynamic Stock Investment Prediction. Proceedings of the AAAI Conference on Artificial Intelligence (2024).

- Shi (2024) Zhuangwei Shi. 2024. MambaStock: Selective state space model for stock prediction.

- Soleymani and Paquet (2021) Farzan Soleymani and Eric Paquet. 2021. Deep graph convolutional reinforcement learning for financial portfolio management – DeepPocket. Expert Syst. Appl. (2021).

- Szegedy et al. (2015) Christian Szegedy, Wei Liu, Yangqing Jia, Pierre Sermanet, Scott Reed, Dragomir Anguelov, Dumitru Erhan, Vincent Vanhoucke, and Andrew Rabinovich. 2015. Going deeper with convolutions. In IEEE Conference on Computer Vision and Pattern Recognition (CVPR). 1–9. https://doi.org/10.1109/CVPR.2015.7298594

- Vaswani et al. (2017) Ashish Vaswani, Noam Shazeer, Niki Parmar, Jakob Uszkoreit, Llion Jones, Aidan N Gomez, Łukasz Kaiser, and Illia Polosukhin. 2017. Attention is all you need. Advances in neural information processing systems (2017).

- Wang et al. (2022b) Heyuan Wang, Tengjiao Wang, Shun Li, Jiayi Zheng, Shijie Guan, and Wei Chen. 2022b. Adaptive Long-Short Pattern Transformer for Stock Investment Selection. In Proceedings of the Thirty-First International Joint Conference on Artificial Intelligence, IJCAI-22, Lud De Raedt (Ed.). International Joint Conferences on Artificial Intelligence Organization, 3970–3977. https://doi.org/10.24963/ijcai.2022/551 Main Track.

- Wang et al. (2019) Jingyuan Wang, Yang Zhang, Ke Tang, Junjie Wu, and Zhang Xiong. 2019. AlphaStock: A Buying-Winners-and-Selling-Losers Investment Strategy using Interpretable Deep Reinforcement Attention Networks. In Proceedings of the 25th ACM SIGKDD International Conference on Knowledge Discovery & Data Mining.

- Wang and Li (2020) Rui Wang and Lianfa Li. 2020. Dynamic relationship between the stock market and macroeconomy in China (1995–2018): new evidence from the continuous wavelet analysis. Economic Research-Ekonomska Istraživanja 33, 1 (2020), 521–539. https://doi.org/10.1080/1331677X.2020.1716264

- Wang et al. (2024) Shiyu Wang, Haixu Wu, Xiaoming Shi, Tengge Hu, Huakun Luo, Lintao Ma, James Y. Zhang, and JUN ZHOU. 2024. TimeMixer: Decomposable Multiscale Mixing for Time Series Forecasting. In International Conference on Learning Representations. https://openreview.net/forum?id=7oLshfEIC2

- Wang et al. (2022a) Yunong Wang, Yi Qu, and Zhensong Chen. 2022a. Review of graph construction and graph learning in stock price prediction. Procedia Comput. Sci. (jan 2022), 771–778.

- Wu et al. (2020) Tailin Wu, Hongyu Ren, Pan Li, and Jure Leskovec. 2020. Graph Information Bottleneck. In Advances in Neural Information Processing Systems, H. Larochelle, M. Ranzato, R. Hadsell, M.F. Balcan, and H. Lin (Eds.), Vol. 33. Curran Associates, Inc., 20437–20448. https://proceedings.neurips.cc/paper_files/paper/2020/file/ebc2aa04e75e3caabda543a1317160c0-Paper.pdf

- Xia et al. (2024) Hongjie Xia, Huijie Ao, Long Li, Yu Liu, Sen Liu, Guangnan Ye, and Hongfeng Chai. 2024. CI-STHPAN: Pre-trained Attention Network for Stock Selection with Channel-Independent Spatio-Temporal Hypergraph. Proceedings of the AAAI Conference on Artificial Intelligence 38, 8 (Mar. 2024), 9187–9195. https://doi.org/10.1609/aaai.v38i8.28770

- Xiang et al. (2022) Sheng Xiang, Dawei Cheng, Chencheng Shang, Ying Zhang, and Yuqi Liang. 2022. Temporal and Heterogeneous Graph Neural Network for Financial Time Series Prediction. In Proceedings of the 31st ACM International Conference on Information & Knowledge Management.

- Xing et al. (2024) Rong Xing, Rui Cheng, Jiwen Huang, Qing Li, and Jingmei Zhao. 2024. Learning to Understand the Vague Graph for Stock Prediction With Momentum Spillovers. IEEE Trans. on Knowl. and Data Eng. (April 2024), 1698–1712. https://doi.org/10.1109/TKDE.2023.3310592

- Xu et al. (2021) Wentao Xu, Weiqing Liu, Lewen Wang, Yingce Xia, Jiang Bian, Jian Yin, and Tie-Yan Liu. 2021. HIST: A Graph-based Framework for Stock Trend Forecasting via Mining Concept-Oriented Shared Information.

- Yan and Tan (2024) Wenbo Yan and Ying Tan. 2024. TCGPN: Temporal-Correlation Graph Pre-trained Network for Stock Forecasting.

- Zeng et al. (2023) Zhen Zeng, Rachneet Kaur, Suchetha Siddagangappa, Saba Rahimi, Tucker Balch, and Manuela Veloso. 2023. Financial Time Series Forecasting using CNN and Transformer.

- Zhang and Yan (2023) Yunhao Zhang and Junchi Yan. 2023. Crossformer: Transformer Utilizing Cross-Dimension Dependency for Multivariate Time Series Forecasting. In International Conference on Learning Representations. https://openreview.net/forum?id=vSVLM2j9eie

- Zheng et al. (2024) Jiajian Zheng, Duan Xin, Qishuo Cheng, Miao Tian, and Le Yang. 2024. The Random Forest Model for Analyzing and Forecasting the US Stock Market in the Context of Smart Finance. arXiv:2402.17194

- Zhu et al. (2024) Peng Zhu, Yuante Li, Yifan Hu, Qinyuan Liu, Dawei Cheng, and Yuqi Liang. 2024. LSR-IGRU: Stock Trend Prediction Based on Long Short-Term Relationships and Improved GRU. International Conference on Information and Knowledge Management (2024).

- Zou et al. (2023) Jinan Zou, Qingying Zhao, Yang Jiao, Haiyao Cao, Yanxi Liu, Qingsen Yan, Ehsan Abbasnejad, Lingqiao Liu, and Javen Qinfeng Shi. 2023. Stock Market Prediction via Deep Learning Techniques: A Survey.

Appendix A Experiment Details

A.1. Datasets Details

For the four datasets (S&P 500, NASDAQ 100, CSI300, CSI500), the train set is from 2018-01-01 to 2021-12-31, the validation set is from 2022-01-01 to 2022-12-31, and the test set is from 2023-01-01 to 2023-12-31. The statistics of each dataset is shown in Tab. 3.

| Dataset | Stocks (Nodes) | train set | validation set | test set |

|---|---|---|---|---|

| CSI 300 | 285 | 943 | 242 | 242 |

| CSI 500 | 450 | 943 | 242 | 242 |

| S&P 500 | 498 | 1008 | 251 | 249 |

| NASDAQ 100 | 99 | 1008 | 251 | 249 |

A.2. Baseline Models

We briefly describe the selected baseline models:

(1) Quantitative Investment Methods:

a. Classical Strategy:

-

•

Buying-Loser-Selling-Winner (BLSW) (Poterba and Summers, 1988): which utilizes reversal strategies by identifying trends that are likely to reverse based on technical indicators and taking positions opposite to prevailing market direction.

-

•

Cross-Sectional Mean reversion (CSM) (Jegadeesh and Titman, 1993): whcih employs momentum strategies by identifying assets or securities with strong recent price trends and taking positions in the direction of those trends.

b. Deep Reinforcement Learning methods:

-

•

AlphaStock (Wang et al., 2019): which is the first to offer an interpretable investment strategy using deep reinforcement attention networks.

-

•

DeepPocket (Soleymani and Paquet, 2021): which consists of an autoencoder for feature extraction, a convolutional network to collect underlying information shared among financial instruments and an actor–critic RL agent. The source code is available at https://github.com/MCCCSunny/DeepPocket.

c. Deep Learning Methods:

-

•

Transformer (Vaswani et al., 2017) is a universal DL method featuring an Encoder-Decoder framework based on self-attention.

-

•

Mamba (Gu and Dao, 2024) is a state space model introducing a data-dependent selection mechanism that balances short-term and long-term dependencies.

-

•

FactorVAE (Duan et al., 2022): which integrates the dynamic factor model (DFM) with the variational autoencoder (VAE), and proposes a prior-posterior learning method which can approximate an optimal posterior factor model with future information. The source code is available at https://github.com/ytliu74/FactorVAE.

-

•

THGNN (Xiang et al., 2022): which designs a temporal and heterogeneous graph neural network model to learn the dynamic relations among price movements in financial time series. The source code is available at https://github.com/TongjiFinLab/THGNN.

-

•

MambaStock (Shi, 2024): which mines historical stock market data with Mamba framework, eliminating the need for meticulous feature engineering or extensive preprocessing. The source code is available at https://github.com/zshicode/MambaStock.

-

•

CL (Du et al., 2024): which predicts stock price movements by comparing textual and quantitative features of the current time interval against those of a prior time span for contrastive learning.

-

•

MASTER (Li et al., 2024): which models the momentary and cross-time stock correlation and leverages market information for automatic feature selection. The source code is available at https://github.com/SJTU-DMTai/MASTER.

-

•

CI-STHPAN (Xia et al., 2024): which is a two-stage framework for stock selection, involving Transformer and HGAT based stock time series self-supervised pre-training and stock-ranking based downstream task fne-tuning. The source code is available at https://github.com/Harryx2019/CI-STHPAN.

-

•

VGNN (Xing et al., 2024): which is a decoupled graph learning framework for stock prediction with a tensor-based fusion module, a hybrid attention mechanism and a message-passing mechanism. The source code is available at https://github.com/JiwenHuangFIC/VGNN.

(2) Time Series Forecasting Methods:

-

•

PatchTST (Nie et al., 2023) is a Transformer-based model utilizing patching and channel independence technique. It also enable effective pre-training and transfer learning across datasets. The source code is available at https://github.com/yuqinie98/PatchTST.

-

•

iTransformer (Liu et al., 2024a) embeds each time series as variate tokens and is a fundamental backbone for time series forecasting. The source code is available at https://github.com/thuml/iTransformer.

-

•

TimeMixer (Wang et al., 2024) is a Linear-based model enabling the combination of the multiscale information in both history extraction and future prediction phases. The source code is available at hhttps://github.com/kwuking/TimeMixer.

-

•

Crossformer (Zhang and Yan, 2023) is a Transformer-based model introducing the Dimension-Segment-Wise (DSW) embedding and Two-Stage Attention (TSA) layer to effectively capture cross-time and cross-dimension dependencies. The source code is available at https://github.com/Thinklab-SJTU/Crossformer.

A.3. Metric Details

We employ five widely used metrics to evaluate the overall performance of each method: Annual Return Ratio (ARR), Annual Volatility (AVol), Maximum Draw Down (MDD), Annual Sharpe Ratio (ASR) and Information Ratio (IR). The lower the absolute values of AVol and MDD, the higher the value of ARR, ASR, and IR, and the better the performance.

-

•

ARR measures the percentage increase or decrease in the value of an investment over the course of a year.

(12) -

•

AVol quantifies the volatility of an investment’s return over the course of a year. denotes the daily return of the portfolio.

(13) -

•

MDD represents the maximum drop from a peak to a trough in an investment’s value.

(14) -

•

ASR measures the risk-adjusted return of an investment over one year.

(15) -

•

IR measures the excess return of an investment relative to a benchmark adjusted for its volatility. is the daily return of the market index.

(16)

A.4. Implementation Details

Our experiment is trained on one NVIDIA V100 GPU, and all models are built using PyTorch (Paszke et al., 2019). The training and validation sets are kept consistent for all baseline models. The number of GNN layers is , the level in MLM is , and the lookback horizon is . The learning rate is for S&P 500 and NASDAQ 100, and for CSI 300 and CSI 500. The weight of the hinge loss is set to , while the weight of the GIB loss is set to . We set to for the selected top- ranked stocks in the experiment.

Appendix B Extra Experimental Results

Here we provide the extra results and analysis of experiments for FinMamba.

B.1. Additional Cases of Dynamic Interplay Between Stock Market Indices and Inter-Stock Correlations

As shown in Fig. 1, the correlation between stocks becomes stronger when the market index falls and weaker when the market index rises. In particular, the relationship between stocks becomes very tight during several market downturns. For example, US stocks experienced a sharp pullback in the fourth quarter of 2018, driven by a combination of inflation concerns, interest rate hikes, a global economic slowdown and technical market factors. Similarly, from January to October 2022, inflationary pressures, post-pandemic supply chain disruptions and Federal Reserve policy shifts led to a prolonged decline in US equities.

B.2. System Deployment Framework

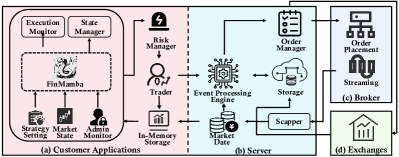

To validate our proposed FinMamba in a realistic environment, we conduct an online deployment in the Chinese stock market.The deployed architecture of FinMamba is shown in Fig. 9. To efficiently adapt to changing market conditions, the FinMamba is updated offline once a week. The newly updated model is then used to make online trading decisions throughout the following week. In the live trading process, the server connects trading signals directly to the exchanges, with the event processing engine managing the flow of real-time trade orders. The market data system provides investors with up-to-date market information. The server database aggregates three types of data: live exchange data, historical data stored in memory, and real-time streaming data obtained from the broker’s scraper service. All of this data is refined and transformed into actionable market information. Trader applications subscribe to these market data, which are then stored in an in-memory engine before being passed to the FinMamba trading decision agent. Trading signals generated by FinMamba are first validated by an independent risk management system before being passed to the event processing engine. Final trade orders are routed to the Order Manager, where they are encrypted using exchange-provided APIs before being sent back to the exchange for execution.

B.3. Online Deployment

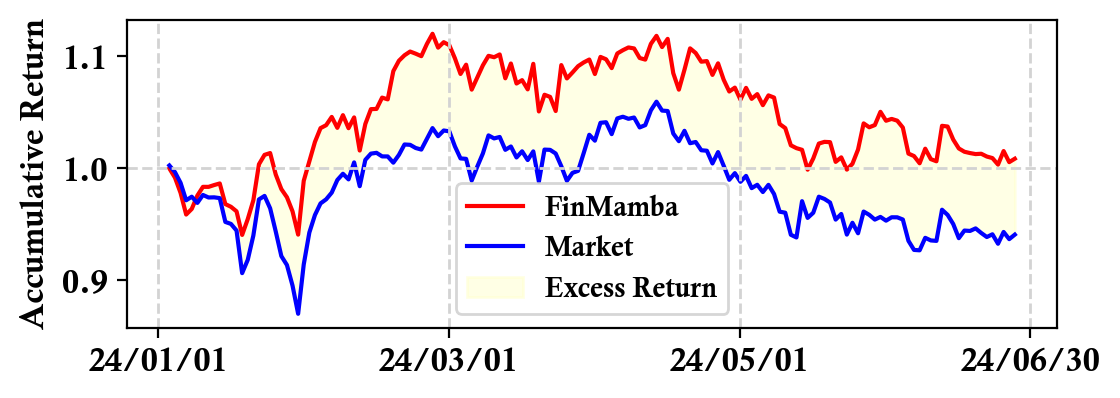

To validate our model in a realistic environment, we conduct an online deployment based on the above framework in the Chinese stock market from 1 January 2024 to 30 June 2024. Based on the predictions, we employ different strategies to trade within the first half hour of the next trading day’s opening. The accumulative wealth of FinMamba and the market return are depicted in Fig. 10. Over half a year, all strategies in our model significantly outperform the market.

..