Covariates-Adjusted Mixed-Membership Estimation: A Novel Network Model with Optimal Guarantees 111The research is in part supported by the NSF grants DMS-2412029, DMS-2210833, and DMS-2053832.

Abstract

This paper addresses the problem of mixed-membership estimation in networks, where the goal is to efficiently estimate the latent mixed-membership structure from the observed network. Recognizing the widespread availability and valuable information carried by node covariates, we propose a novel network model that incorporates both community information, as represented by the Degree-Corrected Mixed Membership (DCMM) model, and node covariate similarities to determine connections.

We investigate the regularized maximum likelihood estimation (MLE) for this model and demonstrate that our approach achieves optimal estimation accuracy for both the similarity matrix and the mixed-membership, in terms of both the Frobenius norm and the entrywise loss. Since directly analyzing the original convex optimization problem is intractable, we employ nonconvex optimization to facilitate the analysis. A key contribution of our work is identifying a crucial assumption that bridges the gap between convex and nonconvex solutions, enabling the transfer of statistical guarantees from the nonconvex approach to its convex counterpart. Importantly, our analysis extends beyond the MLE loss and the mean squared error (MSE) used in matrix completion problems, generalizing to all the convex loss functions. Consequently, our analysis techniques extend to a broader set of applications, including ranking problems based on pairwise comparisons.

Finally, simulation experiments validate our theoretical findings, and real-world data analyses confirm the practical relevance of our model.

Keywords: community detection, network with covariates, convex relaxation, nonconvex optimization, maximum likelihood estimator.

1 Introduction

Network data plays a crucial role across various fields, ranging from finance (Fan et al.,, 2022; Bhattacharya et al.,, 2023) to social science (Adamic and Glance,, 2005; Ji et al.,, 2022), where understanding its latent structure is essential for effective analysis and application. A prominent model in this context is the Degree-Corrected Mixed Membership (DCMM) model, which models the structure of the network within the community regime. However, in many practical scenarios, the connections between nodes are often influenced by more than just the community structure; they are also affected by specific covariates information associated with each node. For example, on a professional networking platform, the connections between individuals are determined by diverse factors like their industry sector, educational background, and skill sets. When observing whether two individuals are connected, covariates are often collected and significantly influence the network structure. Given the importance and availability of covariates, researchers have modified classical models to integrate this information, as seen in works like Yan et al., (2018); Huang et al., (2018); Ma et al., (2020).

This work focuses on community detection while incorporating adjustments for these covariates. Specifically, we propose a generative model for the entries of the observed adjacency matrix . Given the observed covariates for individuals, the Bernoulli random variables are assumed to be mutually independent, and for each pair :

Here, the symmetric matrix moderates the influence of covariates on edge formation, while represents the component as in the DCMM model (Jin et al.,, 2017). captures degree heterogeneity, is the mixed membership profile matrix, and reflects the connection probabilities between communities. The key insight is that both latent communities and covariates jointly influence network connections. Unlike Huang et al., (2018), which assumes that follows a Poisson distribution—allowing the use of spectral methods—our model deals with binary , more reflective of real-world connections. The challenge, however, is that our model makes spectral methods inapplicable, requiring alternative approaches to handle the network structure effectively. Our contributions are threefold:

-

1.

From a methodological perspective, we introduce the Covariates-Adjusted Mixed Membership (CAMM) model. To estimate the model parameters, we propose a constrained regularized maximum likelihood estimator (MLE), which takes the following form:

s.t. where and represents the projection onto the column space of . The objective function includes a standard logistic loss and a regularization term given by the nuclear norm, which acts as a convex surrogate for the rank function to capture the low-rank structure of . The constraints are necessary to ensure the identifiability of the model. This formulation results in a convex optimization problem, allowing for efficient solution methods. By incorporating covariate adjustments, our model provides a principled approach to community detection in networks, making it a natural extension of classical models to handle real-world complexities. Once the convex optimization problem is solved with solution , we further apply the Mixed-SCORE algorithm (Jin et al.,, 2017) to reconstruct the community memberships based on .

-

2.

From a theoretical perspective, our contributions are: (1) We establish optimal statistical guarantees for the solutions of the convex optimization problem, specifically, . (2) We also provide optimal statistical guarantees for the reconstructed membership matrix , specifically, . Our analysis of the convex optimization problem involves two key components: (i) analyzing the nonconvex gradient descent, and (ii) demonstrating the equivalence between the convex and nonconvex solutions. Due to the complexity of the logistic loss function—whose first derivative is not linear in the variables, unlike the mean square error commonly used in matrix completion problems (Chen et al.,, 2020)—we employ the debiased estimator technique in the latter part of our analysis. We highlight that this approach can be generalized to all convex loss functions, making it potentially useful in a variety of contexts. Furthermore, for the membership reconstruction, our analysis goes beyond the traditional sub-Gaussian noise assumption that is prevalent in the literature (e.g., Jin et al., (2017); Bhattacharya et al., (2023)) by incorporating results on the estimation of , which is critical for handling the more complex noise structures in our setting.

-

3.

From an application perspective, we demonstrate through simulation studies that the estimation errors of the model parameters with respect to align perfectly with our optimal statistical guarantees, thereby verifying our theoretical results. Additionally, we validate the practical utility of our model by applying it to an S&P 500 dataset, further showcasing its effectiveness in capturing complex network structures. We include popular covariates in our model and find that they explain a substantial part of the network. Furthermore, the recovered membership structure is highly consistent with the company sectors, and these results deepen our understanding of the underlying structure of the S&P 500 companies.

1.1 Related work

In this work, we focus on model-based community detection methods, where a probabilistic model that encodes the community structure is applied to effectively analyze the network data. Widely recognized models in this field include the stochastic block model (Holland et al.,, 1983), latent space models (Hoff et al.,, 2002; Gao et al.,, 2020), mixture model (Newman and Leicht,, 2007), degree-corrected stochastic block model (Karrer and Newman,, 2011), and hierarchical block model (Peixoto,, 2014). However, these models do not account for the influence of covariates on the nodes’ connections. Recently, researchers have started to modify the classical models to incorporate covariates information. Based on the relationship between covariates, community membership, and network structure, these modified models are generally divided into two categories: covariates-adjusted models and covariates-assisted models.

Covariates-adjusted network models

Our work focuses on covariate-adjusted network models, where both covariates and community membership jointly influence the network structure. A concrete example is a citation network, where citations between papers depend on their research topics (community membership), and the likelihood of citation increases if the authors share similar attributes, such as working at the same institution or having similar academic backgrounds. Adjusting for these covariates is crucial for accurately recovering the true community memberships. For covariates-adjusted network models, Yan et al., (2018) studied a directed network model, which captured the link homophily via incorporating covariates. But their work did not take the potential community structures into consideration. Huang et al., (2018) introduced a pair-wise covariates-adjusted stochastic block model. They studied the MLE for the coefficients of the covariates and investigated both likelihood and spectral approaches for community detection. Ma et al., (2020) incorporated covariates information into latent space models, and presented two universal fitting algorithms: one based on nuclear norm penalization and the other based on projected gradient descent. Mu et al., (2022) extended the generalized random dot product graph (GRDPG) to include vertex covariates, and conducted a comparative analysis of two model-based spectral algorithms: one utilizing only the adjacency matrix, and the other incorporating both the adjacency matrix and vertex covariates. In contrast, our goal is to investigate a variant of the DCMM model that includes covariates adjustment into the network modeling.

Covariates-assisted network models

Covariates-assisted network models refer to models where both the network structure and covariates incorporate information about community membership. A typical example is a social media interaction network. User interactions—such as likes, and comments—often depend on their shared interests (i.e., belonging to the same community). At the same time, the type of content users post or engage with (e.g., workout routines, photo-editing tips, or game reviews) is also driven by these shared interests. Integrating both covariates and network structure information can better reveal the underlying community memberships. Examples of work in this area include Newman and Leicht, (2007); Yan and Sarkar, (2021); Abbe et al., (2022); Xu et al., (2023); Hu and Wang, (2024). However, covariates-assisted network models are not the primary focus of this paper.

Notation

We use to denote the spectral norm of matrix , and for the entrywise norm. Let and represent the -th row and -th column of matrix , respectively. The Hadamard product (element-wise product) between two matrices and is denoted by . We use and to denote the largest and smallest non-zero singular values of , respectively, and correspondingly, and to denote the largest and smallest non-zero eigenvalues of . The pseudoinverse of is denoted by . The vectorization of a matrix is denoted by , which is obtained by stacking the rows of the matrix on top of one another, i.e., . For matrices , which may have different dimensions, we define

Finally, or means for some constant when is sufficiently large; means for some constant when is sufficiently large; and if and only if and .

2 Problem Setup

We consider an undirected graph with nodes and communities. The edge information is incorporated into a symmetric adjacency matrix , namely if there exists an edge between nodes and and otherwise. We assume each node is associated with a degree heterogeneity parameter , a community membership probability vector , and a covariates vector . Conditional on , the Bernoulli random variables are assumed to be mutually independent, and for each pair :

| (1) |

Here represents the entry of as in the DCMM model, where , represents the mixed membership profile matrix, and is a matrix capturing the relative connection probability between communities. Unlike the standard DCMM model, we do not assume to be nonnegative. This flexibility allows our model to capture both dense and sparse networks more effectively. We employ a symmetric matrix to moderate how the covariates affect the edge formation. Only the adjacency matrix and the covariates are observed.

We impose the following identifiability condition for our model (1).

Assumption 1.

Let . We assume that , where denotes the projection onto the column space of . Additionally, we assume: (1) for all , and (2) each community contains at least one pure node, i.e., there exists some such that .

The orthogonality between the column space of and ensures the identifiability of the model parameters . The remaining assumptions guarantee the identifiability of the DCMM model, as demonstrated in Proposition 3.4.

Due to the low-rank structure of and the constraint , we consider the following constrained convex optimization problem:

| (2) | ||||

| s.t. | ||||

where is some regularization parameter and denotes the nuclear norm of , enforcing the low-rank structure. Let be the solution returned by (2). The primary goal of this paper is to establish optimal statistical guarantees for this obtained solution and subsequently reconstruct the mixed membership structure based on .

3 Main Results

In this section, we present the key theoretical results of the paper, starting with the necessary assumptions in Section 3.1, followed by the estimation guarantees for the proposed model in Section 3.2, and concluding with the membership reconstruction results in Section 3.3.

We begin by introducing some additional notations that will be used throughout the following sections. Let the singular value decomposition (SVD) of be given by , where . We denote the largest and smallest non-zero singular values of by and , respectively, and define the condition number of as . Next, we define and , which ensures that .

3.1 Assumptions

Before proceeding, we introduce several key model assumptions that are crucial for the development of our theoretical results. These assumptions relate to the structure of the covariates, the incoherence properties of the latent membership matrix , and the characteristics of the Hessian matrix in the corresponding nonconvex optimization problem. These conditions form the basis for establishing the statistical guarantees presented in the following sections.

Assumption 2 (Scale Assumption).

There exists constants and such that the following holds:

where .

Assumption 2 ensures that the interaction term stays within a controlled range, preventing the edge probabilities from becoming too close to either zero or one, which could lead to an ill-posed problem.

Assumption 3.

We assume is full rank and there exists some constants and such that

And, without loss of generality, we assume . This can always be achieved by rescale and adjust correspondingly.

Assumption 3 ensures that the covariance structure of the covariates contains sufficient information and prevents the covariates from collapsing into a lower-dimensional subspace, which would otherwise result in information loss and inaccurate estimation of . To recover the low-rank matrix , we impose the commonly used incoherence assumption; see Chen et al., (2020) for an example.

Assumption 4 (Incoherent).

We assume is -incoherent, that is to say

Our theoretical results leverage nonconvex optimization analysis, which will be discussed in Section 4.1. As an analog to Assumptions 3 and 4, the following assumptions ensure the nonconvex optimization is well-behaved. We denote by and Consider

which represents the Hessian matrix of the nonconvex counterpart at the ground truth . The following assumptions are required for .

Assumption 5.

We assume there exists some constants and such that

Assumption 6.

We assume there exists some constants such that

The convergence rate of the optimization algorithm depends on the condition number, which is the ratio of the largest and smallest eigenvalue of the Hessian matrix. Assumption 5 is the nonconvex counterpart of Assumption 3, and it ensures the eigenvalues of the Hessian matrix are balanced. While Assumption 5 focuses on the non-zero eigenvalues of , we emphasize here that has a null space with dimension and a mild condition is required for this null space, which is Assumption 6. Assumption 6 can be viewed as an analog of Assumption 4, and it is saying the projection onto the null space of is incoherent.

Although Assumptions 5 and 6 aid in the analysis of nonconvex optimization, the solution from the nonconvex optimization is in fact closely tied to that of the convex problem (2). The following assumption is crucial in unveiling this connection.

Assumption 7.

We define a matrix such that

Suppose is given by

We assume that there exists a constant such that

In fact, Assumption 7 provides conditions that are nearly necessary and sufficient for the convex and nonconvex solutions to be equivalent. While this assumption may not seem intuitive at first, it is typically easy to satisfy in practical applications, with the upper bound often being quite small. Specifically, Assumption 7 holds in common settings such as stochastic block models.

3.2 Estimation results

In this section, we present rigorous theoretical guarantees for the estimation of the model parameters. We demonstrate that, under the given assumptions, the solution obtained from the convex optimization problem (2) achieves optimal estimation errors for both the matrix up to the logarithmic terms, which captures the effects of the covariates, and the low-rank membership matrix .

3.3 Membership reconstruction results

In this subsection, we shift focus to reconstructing the latent community memberships based on the estimated matrix . We describe a vertex-hunting algorithm for efficiently estimating the mixed-membership vectors and provide theoretical bounds on the accuracy of the reconstructed memberships. We first state the identifiability condition as follows.

Proposition 3.4.

Consider the DCMM model . If we assume (1) for all , (2) each community has at least one pure node, then the DCMM model is identifiable.

-

•

Obtain , where are the largest (in magnitude) eigenvalues of and are the corresponding eigenvectors.

-

•

Obtain .

Definition 3.5 (Efficient Vertex Hunting).

A Vertex Hunting (VH) algorithm is efficient if it satisfies

for some constant .

Remark 3.6 (Example of an Efficient VH Algorithm: Successive Projection).

We present an example of an efficient VH algorithm known as Successive Projection (Algorithm 2).

According to Jin et al., (2017), Lemma 3.1, the successive projection method is an efficient VH algorithm.

Align with Jin et al., (2017), we make the following assumptions.

Assumption 8.

We assume the following conditions hold.

-

1.

Let , and . We assume there exists a constant such that and a constant such that

-

2.

Recall that . Let . We assume , and for some constant .

-

3.

Let be the -th largest right eigenvalue of in magnitude, and be the associated right eigenvector, . For a constant and a sequence such that , we assume

We also assume

Theorem 3.7.

4 Proof Strategy and Key Innovations

In this section, we outline our proof strategy and highlight the key technical contributions of this work. Directly analysis on convex problem (2) is unable to give the sophisticated control on . To address this, we leverage nonconvex optimization to facilitate the analysis of the convex problem. Our approach consists of two main components: analyzing the nonconvex gradient descent using the leave-one-out technique and establishing the equivalence between the convex and nonconvex solutions. While this analysis framework is well-established in the literature (Chen et al.,, 2020), our work extends it to handle the logistic loss, overcoming the limitations of existing methods that only apply to mean squared error (MSE) loss. Our approach can be further generalized to other convex loss functions. In the following sections, we describe these contributions in detail.

4.1 Nonconvex problem

We begin by introducing a nonconvex optimization problem to aid our proof. We reparameterize , where , and consider the following nonconvex problem as an alternative to (2)

| s.t. | ||||

| (3) |

Here, we replace with and the nuclear norm with , motivated by the fact that for any rank- matrix ,

as shown in Srebro and Shraibman, (2005); Mazumder et al., (2010). This reparameterization exploits the low-rank structure of and reduces the number of parameters from to , which allows us to better control . We solve this nonconvex problem using gradient descent.

Although one might be concerned that this nonconvex optimization depends on the value of , which is unknown, we emphasize that this approach is purely an analytical tool to study the convex problem by defining a sequence of ancillary random vectors, rather than an algorithm to be directly applied. We initialize gradient descent at , , and , and run for a fixed number of iterations . For , we compute:

We can show, with high probability, that there exists a sequence of rotation matrices such that:

for all . See Lemma C.4 for more details. This implies that the nonconvex optimization path remains close to the true parameters , , and throughout the iterations.

Furthermore, defining

we can show that

See Lemma C.6 for more details. Therefore, if we define as the nonconvex solution, it then satisfies:

-

1.

The gradient of at (after projection) is sufficiently small.

-

2.

The errors are well-controlled:

This further implies .

4.2 Bridge convex and nonconvex

Although is defined from a hypothetical algorithm that cannot be applied, we will show that the nonconvex solution is very close to the convex solution, in the sense that . This allows us to transfer the theoretical guarantees of the nonconvex solution directly to the convex solution, leading to Theorem 3.2.

Define

Notice that is the unique minimizer of the convex problem (2) if it satisfies:

| (4) |

Here is the SVD of and with , where is the tangent space of .

Therefore, as long as we can verify (4) for approximately (recall that the gradient of at is very small, but not exactly zero), we are able to show the different between the convex solution and nonconvex solution is extremely small. This idea and corresponding analysis, first proposed by Chen et al., (2020), was previously limited to the MSE because the derivative of the MSE is linear with respect to the variable. In this paper, we introduce a more elaborated approach to analyze the nonconvex solution and to verify (4), and this technique can be potentially extended to many other problems.

For simplicity, let’s assume the gradient is exactly zero ( is sufficiently small). Then, one can show that the gradient of after projection can be expressed as:

where is the SVD of and is a matrix from the orthogonal complement of the tangent space of . In order to show is equivalent to the convex solution, it suffices to show , which is equivalent to verifying that . If the loss function in was the mean square error, then would be linear with and , simplifying the analysis. However, since the logistic loss is used in our case, we need to analyze this gradient in more depth. To tackle this, we begin with the Taylor expansion of at

| (5) |

where the matrix is defined as:

The first term on the right-hand side of (5) is a mean zero random matrix which can be well controlled with the random matrix theory. We thus focus on the second term.

The key idea of our analysis is to isolate the bias and stochastic error in and . To achieve this, we define the corresponding debiased ‘estimator’ as:

| (6) |

where

This debiased estimator can be viewed as running one Newton–Raphson step from . Similarly, we run a Newton–Raphson step from to define as

| (7) |

This allows us to decompose as:

| (8) |

Note that can be decomposed and analyzed similarly, so here we focus on as an example.

Our key observation is that the term is the dominating term in (8) as long as is properly chosen, and we confirm this statement by controlling term and term accordingly. On the other hand, since has an explicit form from (6), we are able to fully characterize the error .

To control the term and , we first notice that is also explicitly defined by (7), so term can be controlled directly, as shown in Proposition D.2. In fact, since (7) has nothing to do with , term can be controlled by term as long as is properly chosen. When it comes to term , it represents the difference between two Newton–Raphson steps with different initializations. Since we have shown the difference between these two initializations and are well-controlled, the difference shrinks further after the Newton–Raphson step. To be more concrete, in Theorem D.3, we show that

which implies .

As for the main term , its properties are guaranteed by Assumption 7. In fact, Assumption 7 provides a necessary and sufficient condition for the equivalence between the convex and nonconvex solutions, according to our analysis.

Once we obtain the equivalence of the convex solution and nonconvex solutions, the theoretical guarantees for the nonconvex solution can be immediately transferred to the convex solution, which is the estimator we proposed. This is how we leverage the debiased ‘estimator’ and uncertainty quantification to derive the error bounds for our estimator.

5 Simulation Studies

In our experiments, we generated synthetic data to evaluate the performance of our model in estimating and . For each trial, we randomly generated the ground truth parameters , , and , based on predefined values for the number of nodes , the number of communities , and the dimension of covariates .

The matrix was constructed as a symmetric matrix using the following process: First, we generated , an diagonal matrix, that represents individual node effects and is generated by drawing random values uniformly between 0.83 and 1.0. The community structure is encoded in the and matrices. , an matrix, defines the interaction strength between communities. It is initialized with for all off-diagonal values, representing weak inter-community connections, while the diagonal entries are set to 1 to indicate strong intra-community ties. The matrix, an matrix, represents the probability distribution of each node’s affiliation across communities. The values in the first column of are drawn from a Beta distribution with parameters and , while the second column is defined such that each row sums to 1. This setup biases nodes to be closer to one of the two pure community types, or . The overall matrix is then computed as , capturing the combined effects of both individual node attributes and community structures on connectivity.

The covariate matrix is constructed to lie in the null space of , ensuring that it satisfies the orthogonality condition . First, the null space of is computed, and a random orthogonal matrix is applied to the resulting null space matrix to generate an orthonormal basis for . Finally, is scaled by to standardize its values. The symmetric matrix , which defines the influence of covariates on edge formation, is chosen as follows:

Using the generated covariates , symmetric interaction matrix , and matrix , we constructed the adjacency matrix according to our model (1), where the probability of an edge forming between two nodes is governed by a logistic function of their covariates and the corresponding entries of .

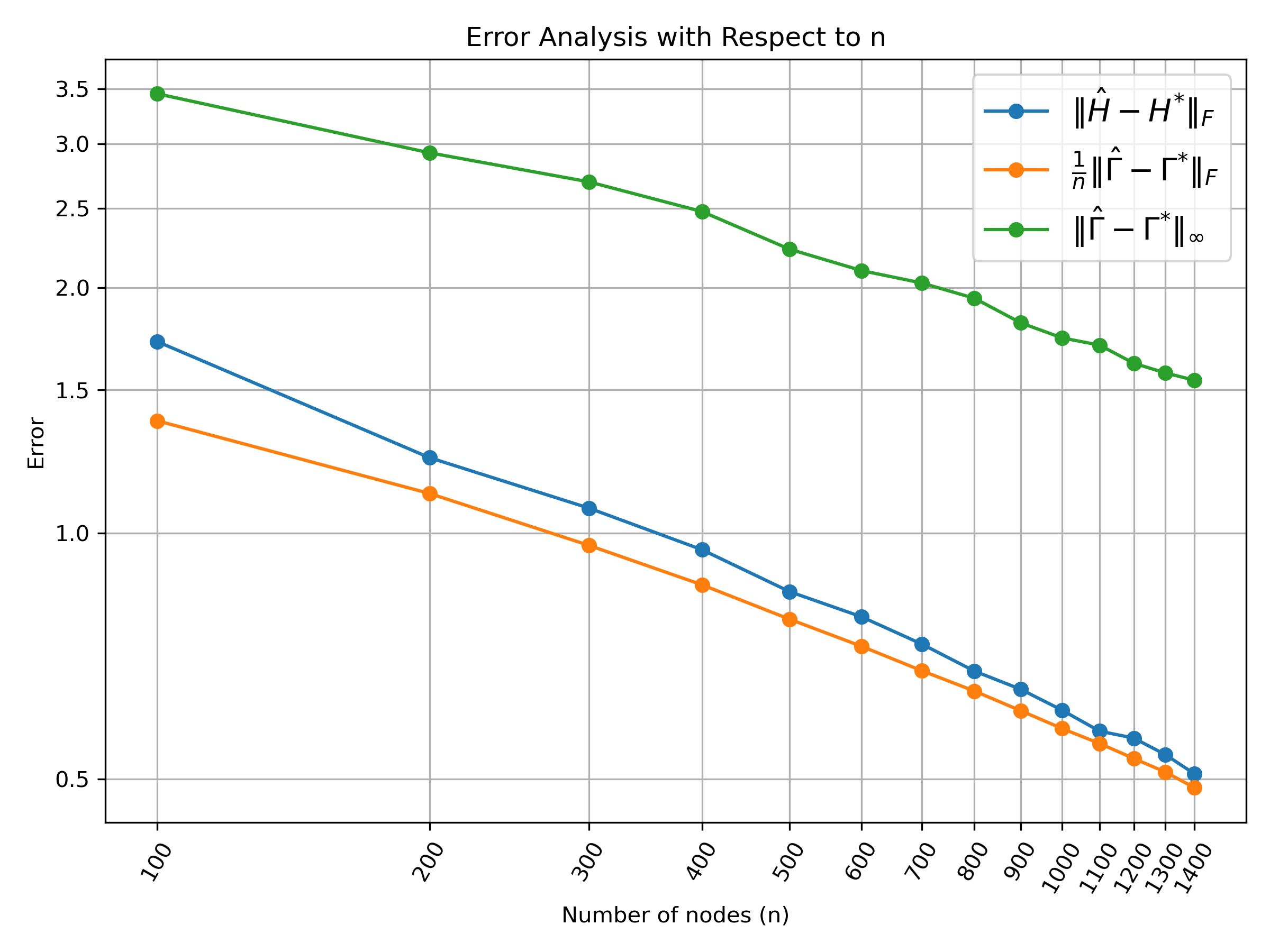

To estimate and , we applied a Nesterov-accelerated gradient descent method with a nuclear norm penalty on for regularization. For each value of , we repeated the simulation over runs to account for randomness in the data generation process. We evaluated the model’s performance by calculating the absolute estimation errors , and for each run. The mean errors across all runs were computed for each .

Finally, in Figure 1, we visualized the results by plotting the mean estimation errors for and as functions of .

6 Real Data Analysis

In this section, we apply our model to a stock network. We use the daily return data of S&P 500 stocks from November 10, 2021, to November 10, 2024, obtained from Wharton Research Data Services. The daily return is defined as the change in the total value of an investment in a common stock over a specified period per dollar of initial investment. The data is filtered to exclude assets with missing values and scaled by a factor of 100.

To construct the stock network, we analyze the correlations of the processed data. Since much of the variation in stock excess returns is known to be driven by common factors, such as the Fama–French factors, we first remove the influence of these common factors. Specifically, we remove the first five principal components of the processed data matrix, which primarily represent the market portfolio. The network is then built using the correlation matrix of the idiosyncratic components (the residuals). Let represent the correlation matrix of these idiosyncratic components. An edge is defined between nodes and if and only if , resulting in the adjacency matrix .

We consider six covariates: price-to-earnings (PE), price-to-sales (PS), price-to-book (PB), price-to-free-cash-flow (PFCF), debt-to-equity ratio (DER), and return on equity (ROE). These covariates are constructed for each firm using financial data from November 10, 2021, to November 10, 2024. To preprocess the data, we first remove all infinite and missing values. Firms with no valid data remaining for certain covariates after this adjustment are excluded from the analysis. After preprocessing, we retain companies in the network. For each firm, we compute the mean values of the relevant financial metrics over the given period. For example, when calculating the PE ratio, we first compute the mean values of price and earnings separately. If both mean values are positive, we compute their ratio. This ratio is then capped at a predefined lower bound for each covariate to mitigate extreme values and numerical instability. If one or both mean values are non-positive, we assign the predefined lower bound directly. In our experiment, we set the lower bounds as follows: for PE, PS, and PB; for PFCF; for DER; and for ROE. We then apply a logarithmic transformation to the obtained ratios and standardize each covariate across firms. This process results in a covariate matrix .

Using our proposed model, along with the obtained adjacency matrix and covariate matrix , we employ a Nesterov-accelerated gradient descent method, initialized with zero matrices, to estimate and . A nuclear norm penalty is applied to for regularization. The regularization parameter is set to be and the estimated has a rank of . The scatter plot of the 3-dimensional eigenratio for each stock exhibits a distinct tetrahedral structure. The four vertices of the tetrahedron correspond to the coordinates of four firms: Arch Capital Group (ACGL), PepsiCo (PEP), BXP, Inc. (BXP) and Pentair (PNR). Subsequently, we employ Algorithm 1 to reconstruct the membership, yielding a estimated membership matrix .

In Figure 2, we show the 3-dimensional scatter plot of . (Since each row of adds up to , the last column of can be simply expressed by the other three columns.) As we can see from Figure 2, the estimated membership shows a strong cluster effect. We mark companies from financials, real estate, consumer staples, and industrials sectors in black in the four subplots respectively. They occupy the four vertices, and there are very few other companies on those vertices. That is to say, we can observe a clear mixed membership structure behind the S&P 500 companies, with financials, real estate, consumer staples, and industrials sectors being the vertices. In addition to that, the utilities sector also forms a cluster, which is located in the middle of the tetrahedral. It is also worth mentioning that the information technology companies are scattered in the central area of the entire tetrahedron, indicating the wide variety of technology companies.

With our observations on the membership structure shown above, let’s now turn to the covariates part. Under our identifiability condition , we can view as the regression coefficients of regressing on

with being the intercept and being the residuals. Recall is defined by in (2), which can be further written as

to ensure the mean of residue is . Therefore, the of the described regression represents the proportion of that can be explained by the covariates. By the definition of , we have

Plugging our estimated and , we get , which means the covariates explain a significant part of . In contrast, if we randomly shuffle the rows of the covariate matrix and repeat the above calculation, it results in . This implies that our model extracts a substantial amount of information from the covariates.

We then compare the goodness of fit of our model to that of a model without covariate adjustment, given by , where . Since, on average, should be close to , we use a -type of statistic

| (9) |

as a measurement to assess the goodness of fit of the estimator. Note that the variance of is , and the denominator in (9) serves to normalize the mean squared error. We compute this error for both our model (2) and the model without covariates, where the latter’s estimate is obtained by solving the following optimization problem:

The results are presented in Table 1. As one can see, the covariates contributes a substantial part to the goodness of fit of our model.

| With Covariates | Without Covariates | % Decrease | |

|---|---|---|---|

| ERROR |

We further evaluate how the covariates associated with each individual sector influence its specific position within the network. As an analog of the , the sector-wise is calculated by grouping companies into their respective sectors. For each sector, the corresponding rows of the covariate matrix and the centered matrix (i.e., ) are extracted. The for a sector is computed using the formula:

where is the sector-specific submatrix of and is the corresponding rows of . The numerator represents the explained variance for the sector, while the denominator represents the total variance. We report these values in Table 2. Sectors are ranked based on their values, providing a measure of how well the covariates explain variability within each sector.

| Rank | Sector | |

|---|---|---|

| 1 | Utilities | 0.8370 |

| 2 | Financials | 0.6378 |

| 3 | Health Care | 0.6265 |

| 4 | Real Estate | 0.6022 |

| 5 | Consumer Staples | 0.5612 |

| 6 | Consumer Discretionary | 0.5482 |

| 7 | Materials | 0.5127 |

| 8 | Energy | 0.5126 |

| 9 | Information Technology | 0.4651 |

| 10 | Industrials | 0.4404 |

| 11 | Communication Services | 0.4350 |

Next, we examine the overall impact of each covariate on the collective structure of the network. More specifically, we consider six covariates: price-to-earnings (PE), price-to-sales (PS), price-to-book (PB), price-to-free-cash-flow (PFCF), debt-to-equity ratio (DER), and return on equity (ROE). For the -th covariate, we test the null hypothesis to determine its significance.

To perform the hypothesis test, we estimate and , similar to the procedure for the full model. The key difference is the inclusion of an additional constraint, , which enforces the null hypothesis by setting the -th covariate’s effect to zero. We then compute the objective function for both the full model (including all covariates) and the restricted model (with the null constraint applied). The objective function reflects the likelihood of the observed network under the model, regularized by the nuclear norm of . The test statistic is calculated as . To assess significance, we randomly shuffle the -th column of the covariate matrix 1000 times, effectively decoupling the effect of the -th covariate. For each shuffled dataset, we compute the test statistic using the same procedure. Table 3 reports the average, 95th percentile, and 99th percentile of across these 1000 shuffles.

We find that statistics for PE, PS, PB, PFCF, and DER are significantly larger than the values obtained from the shuffled data, highlighting their statistical significance.

| PE | PS | PB | PFCF | DER | ROE | |

|---|---|---|---|---|---|---|

| 190.74 | 1242.49 | 1046.17 | 1492.37 | 1277.67 | 36.71 | |

| -avg | 22.43 | 21.98 | 24.37 | 16.83 | 21.47 | 23.89 |

| -95%quantile | 56.79 | 50.25 | 59.18 | 38.51 | 50.75 | 55.89 |

| -99%quantile | 75.78 | 74.58 | 84.57 | 54.30 | 79.78 | 91.90 |

References

- Abbe et al., (2022) Abbe, E., Fan, J., and Wang, K. (2022). An theory of pca and spectral clustering. The Annals of Statistics, 50(4):2359–2385.

- Adamic and Glance, (2005) Adamic, L. A. and Glance, N. (2005). The political blogosphere and the 2004 us election: divided they blog. In Proceedings of the 3rd international workshop on Link discovery, pages 36–43.

- Bhattacharya et al., (2023) Bhattacharya, S., Fan, J., and Hou, J. (2023). Inferences on mixing probabilities and ranking in mixed-membership models. arXiv preprint arXiv:2308.14988.

- Chen et al., (2020) Chen, Y., Chi, Y., Fan, J., Ma, C., and Yan, Y. (2020). Noisy matrix completion: Understanding statistical guarantees for convex relaxation via nonconvex optimization. SIAM journal on optimization, 30(4):3098–3121.

- Fan et al., (2022) Fan, J., Fan, Y., Han, X., and Lv, J. (2022). Simple: Statistical inference on membership profiles in large networks. Journal of the Royal Statistical Society Series B: Statistical Methodology, 84(2):630–653.

- Gao et al., (2020) Gao, F., Ma, Z., and Yuan, H. (2020). Community detection in sparse latent space models. arXiv preprint arXiv:2008.01375.

- Hoff et al., (2002) Hoff, P. D., Raftery, A. E., and Handcock, M. S. (2002). Latent space approaches to social network analysis. Journal of the american Statistical association, 97(460):1090–1098.

- Holland et al., (1983) Holland, P. W., Laskey, K. B., and Leinhardt, S. (1983). Stochastic blockmodels: First steps. Social networks, 5(2):109–137.

- Hu and Wang, (2024) Hu, Y. and Wang, W. (2024). Network-adjusted covariates for community detection. Biometrika, page asae011.

- Huang et al., (2018) Huang, S., Sun, J., and Feng, Y. (2018). Pairwise covariates-adjusted block model for community detection. arXiv preprint arXiv:1807.03469.

- Ji et al., (2022) Ji, P., Jin, J., Ke, Z. T., and Li, W. (2022). Co-citation and co-authorship networks of statisticians. Journal of Business & Economic Statistics, 40(2):469–485.

- Jin et al., (2017) Jin, J., Ke, Z. T., and Luo, S. (2017). Estimating network memberships by simplex vertex hunting. arXiv preprint arXiv:1708.07852, 12.

- Jin et al., (2023) Jin, J., Ke, Z. T., and Luo, S. (2023). Mixed membership estimation for social networks. Journal of Econometrics.

- Karrer and Newman, (2011) Karrer, B. and Newman, M. E. (2011). Stochastic blockmodels and community structure in networks. Physical review E, 83(1):016107.

- Ma et al., (2018) Ma, C., Wang, K., Chi, Y., and Chen, Y. (2018). Implicit regularization in nonconvex statistical estimation: Gradient descent converges linearly for phase retrieval and matrix completion. In International Conference on Machine Learning, pages 3345–3354. PMLR.

- Ma et al., (2020) Ma, Z., Ma, Z., and Yuan, H. (2020). Universal latent space model fitting for large networks with edge covariates. Journal of Machine Learning Research, 21(4):1–67.

- Mazumder et al., (2010) Mazumder, R., Hastie, T., and Tibshirani, R. (2010). Spectral regularization algorithms for learning large incomplete matrices. The Journal of Machine Learning Research, 11:2287–2322.

- Mu et al., (2022) Mu, C., Mele, A., Hao, L., Cape, J., Athreya, A., and Priebe, C. E. (2022). On spectral algorithms for community detection in stochastic blockmodel graphs with vertex covariates. IEEE Transactions on Network Science and Engineering, 9(5):3373–3384.

- Newman and Leicht, (2007) Newman, M. E. and Leicht, E. A. (2007). Mixture models and exploratory analysis in networks. Proceedings of the National Academy of Sciences, 104(23):9564–9569.

- Peixoto, (2014) Peixoto, T. P. (2014). Hierarchical block structures and high-resolution model selection in large networks. Physical Review X, 4(1):011047.

- Srebro and Shraibman, (2005) Srebro, N. and Shraibman, A. (2005). Rank, trace-norm and max-norm. In International conference on computational learning theory, pages 545–560. Springer.

- Stewart, (1977) Stewart, G. W. (1977). On the perturbation of pseudo-inverses, projections and linear least squares problems. SIAM review, 19(4):634–662.

- Xu et al., (2023) Xu, S., Zhen, Y., and Wang, J. (2023). Covariate-assisted community detection in multi-layer networks. Journal of Business & Economic Statistics, 41(3):915–926.

- Yan and Sarkar, (2021) Yan, B. and Sarkar, P. (2021). Covariate regularized community detection in sparse graphs. Journal of the American Statistical Association, 116(534):734–745.

- Yan et al., (2018) Yan, T., Jiang, B., Fienberg, S. E., and Leng, C. (2018). Statistical inference in a directed network model with covariates. Journal of the American Statistical Association.

- Yan et al., (2024) Yan, Y., Chen, Y., and Fan, J. (2024). Inference for heteroskedastic pca with missing data. The Annals of Statistics, 52(2):729–756.

Appendix A Preliminaries

As we have mentioned in Section 4, our proof strategy leverages the analysis of nonconvex optimization. Since the condition number of Hessian matrix plays an important role in the analysis of gradient descent, we rescale our variables without changing the objective in the beginning to ensure the Hessian matrices involved in the analysis have small condition numbers. Specifically, we let

Note that this rescaling step does not change the value of objective at all. However, the Hessian matrices involved in our proof are now having balanced non-zero eigenvalues. We will use the variables with subscript ‘appendix’ in the appendix sections, and the results proved in the appendix are transformed back to the original scale in the main body of this paper. For simplicity, we will omit the subscript ‘appendix’ in the following content.

We define two types of logistic loss functions and their corresponding objectives. First, the nonconvex logistic loss is given by:

| (10) |

The nonconvex objective is defined as:

| (11) |

Next, we introduce the convex logistic loss:

| (12) |

The convex objective is defined as:

| (13) |

We have the following proposition.

Proposition A.1.

Suppose Assumption 3 holds. For rescaled , we have is full rank and

Proof of Proposition A.1.

Note that

Thus, we have

Consequently, after rescaling, it holds that

∎

Appendix B Local geometry

We define

where .

Lemma B.1 (Local geometry).

Proof.

See Appendix E. ∎

Appendix C Properties of the nonconvex iterates

In this section, we study the gradient descent starting from the ground truth . Note that this algorithm cannot be implemented in practice because we do not have access to the ground truth parameters. More specifically, we consider the following algorithm:

| (14) | ||||

| (15) |

Here is the step-size, and the update in (15) is to guarantee that always holds on the trajectory.

Leave-one-out objective

For , we define the following leave-one-out objective

and , , , are defined correspondingly.

Properties

Let

We will inductively prove the following lemmas.

Proof.

See Appendix F.1. ∎

Proof.

See Appendix F.2. ∎

Proof.

See Appendix F.3. ∎

Proof.

See Appendix F.4. ∎

Proof.

See Appendix F.5. ∎

Lemma C.6.

Proof.

See Appendix F.6. ∎

Appendix D Properties of debiased nonconvex estimator

Let

And we denote . It then holds that

| (17) | ||||

| (18) |

Moreover, we have

Let

We define the debiased estimator as

| (19) |

which then satisfies:

| (20) |

Here the second condition leads to the fact that .

Similarly, let

We define

| (21) |

which then satisfies

| (22) |

Here the second condition leads to the fact that .

The distance between the debiased estimator and the original estimator can be captured by the following proposition.

Proposition D.1.

We have

Proof.

See Appendix G.1. ∎

Similarly, we have the following proposition.

Proposition D.2.

We have

Moreover, it holds that

Proof.

See Appendix G.2. ∎

We can then establish the following theorem.

Theorem D.3.

Proof.

See Appendix G.3. ∎

Appendix E Proofs of Section B

Observations

Based on the constraints on , it can be seen that:

This further implies that

where we use the fact that . Moreover, we have

| (Cauchy) | |||

where we use the fact that . Thus, we obtain

Based on Assumption 2, we know and this leads to the fact that as long as . We will use the above observations in the following proofs.

Lemma E.1.

Define as

which removes the diagonal entries of matrices. Consider satisfies

for a rotation matrix and let be the tangent space of

where is the SVD of . We denote by the projection operator which projects matrices to space . Then we have

as long as . As a directly corollary, we have

Proof.

Without loss of generality we can assume , otherwise we can place with and the statement is not affected. Then the statement can be written as

It is equivalent to show

Again since , the above statement is also equivalent to

To verify this, we begin with the explicit expression . Then we have

| (23) |

It remains to control and . By definition we can write . As a result, we have

| (24) |

since , and

Similarly, for we also have .

∎

Lemma E.2.

It holds that

Proof.

To show the upper bound, note that

Thus, it holds that

By Weyl’s inequality, we have

As long as , we have

which implies

For the lower bound, note that

where

Based on the fact that and , we have

By the definition of , as long as , we have

Moreover, on the observations, we have

Thus, we have

As a result, we have

Here we use Weyl’s inequality to obtain that

As long as , we have

∎

Proof of Lemma B.1.

According to the definition of , we have

Thus, it holds that

| (25) |

We first deal with the last term, which is the only term that contains and thus has randomness. Note that

For the first term, we have

| (mean-value theorem) | ||||

| (Cauchy) |

Note that

| (26) |

where the last equation follows from the fact that and . Thus, we have

| (By the observations) | ||||

| (as long as for some ) | ||||

| () |

For the second term, note that is mean-zero -subgaussian variable. By the independency, it holds that

is mean-zero -subgaussian variable. Thus, with probability at least , we have

As a result, with probability at least , we have

| (as long as ) | |||

| () |

To summarize, we show that with probability at least ,

For the rest of the terms, note that

| (27) |

where the second inequality follows from Assumption 3, the third inequality follows from the fact that and the last inequality follows from Lemma E.2. Combine this with (E), we final obtain that with probability at least , we have

as long as . In other words, we obtain

It’s easy to see that the above upper bound also holds for .

Now let’s focus on the lower bond. One can see that

| (28) |

Here the last equation follows from the fact that and , and the inequality follows from Assumption 3. On the one hand, one can control the last term as

| (29) |

On the other hand, by Lemma E.2 we have

| (30) |

as long as . Combine (29) and (30) with (28) we get

Plugging this in (E) we get

as long as

∎

Appendix F Proofs of Section C

We define

Thus, we have . Note that for any , , and , we have

which will be used in the following proofs. We first present the following lemmas, which will be constantly used in the proofs.

Lemma F.1.

Let be the ground truth parameters and . Under Assumption 2, it holds with probability at least that

Proof of Lemma F.1.

In the following, we will bound and , respectively. To bound , note that

By Assumption 2, we have

Thus, by matrix Bernstein inequality, with probability at least , we have

which implies that .

We then bound . Note that

where the last inequality follows from the fact that . Here

Note that

Thus, by matrix Bernstein inequality, with probability at least , we have . Consequently, it holds that

∎

Proof of Lemma F.2.

We denote

Note that

For the first term, we have

| (by mean value theorem) | |||

where the last inequality follows from the same argument as (E) and

For the second term, as bound in the proof of Lemma F.1, we have with probability at least that

As a result, we have

| (recall the definition of ) | ||||

We then finish the proof. ∎

F.1 Proofs of Lemma C.1

Suppose Lemma C.1-Lemma C.5 hold for the -th iteration. In the following, we prove Lemma C.1 for the -th iteration. By the gradient decent update, we have

which then gives

| (31) |

Consequently, we only need to bound the RHS of (31). Note that

Also, notice that

Thus, we have

For notation simplicity, we denote

Since Lemma C.4 holds for the -th iteration, we know satisfies the local geometry properties as outlined in Lemma B.1 as long as , . By triangle inequality, we have

In the following, we bound (1)-(3), respectively.

- 1.

- 2.

- 3.

F.2 Proofs of Lemma C.2

Suppose Lemma C.1-Lemma C.5 hold for the -th iteration. In the following, we prove Lemma C.2 for the -th iteration. More specifically, we fix and aim to bound

Claim F.3.

It holds that

Proof of Claim.

By the definition of , for any , we have

Choosing , we then have

which then finishes the proofs. ∎

By Claim F.3, we have

Moreover, by the gradient decent update, we have

which further implies that

| (32) |

Thus, we only need to control the RHS of (F.2).

Notice that and , we have

Moreover, we have

As a result, we have

where

In the following, we bound the Frobenius norm of (1)-(3), respectively.

- 1.

-

2.

We then bound (2). Note that

Since the first and second terms are similar, we only focus on bounding the norm of the first term in the following. Notice that

Thus by matrix Berstein’s inequality, we have with probability at least that

(33) Notice that

where the last equation follows from Assumption 4 and the fact that Lemma C.1 and Lemma C.2 hold for the -th iteration. Thus by matrix Berstein’s inequality, we have with probability at least that

(34) Similarly, we have with probability at least that

(35) -

3.

We then bound (3). Notice that

Then following the same argument as bounding term (2) in Appendix F.1, we have

Thus, it holds that

Combine the bounds of Frobenius norm of (1)-(3), we conclude that

as long as and . By (F.2), we further have

Finally, by the arbitrariness of , we finish the proofs.

F.3 Proofs of Lemma C.3

Suppose Lemma C.1-Lemma C.5 hold for the -th iteration. In the following, we prove Lemma C.3 for the -th iteration. Note that

where the -th row of the first and second terms are all zeros. Thus, by the gradient descent update, we have

By the mean value theorem, we have for some that

Note that

Thus, we further have

Consequently, we have

| (36) |

where

We bound in the following.

- 1.

-

2.

For (b), note that

Moreover, we have

Thus, we have

(38) -

3.

For (c), note that

Thus, we have

(39) -

4.

For (d), we have

(40) -

5.

Finally, we bound (e). We denote

Note that, by Cauchy-Schwartz, we have

Thus, it can be seen that and we have

Note that

Regarding the term , we have the following claim.

Claim F.4.

With probability at least , we have

Consequently, we have

(41) It remains to prove Claim F.4.

Proof of Claim F.4.

To facilitate analysis, we introduce an auxiliary point where

We have the following claim.

With this claim at hand, by Lemma J.5 with and , we have

(42) (by Claim F.5 and the definition of ) (by Lemma J.5) (by Claim F.5) Here for a matrix with SVD . Note that

where we denote

This enables us to obtain

We then bound in the following. Note that

For the first term, we have

(by mean value theorem) For the second term, same as bounding in the proof of Lemma F.1, we have

Consequently, we have

Thus, we have

By (42), we obtain

(as long as small enough) as long as . We then prove Claim F.4.

∎

Similarly, we have

| (43) |

where

Denote

It can be seen that

Thus, . On the other hand, we want to lower bound the smallest eigenvalue of . For any , where , we have

| (46) |

An important observation is that are submatrices of , a fact we will leverage in the subsequent proofs. We denote by such that

Then we know that

| (47) |

Denote by , then Assumption 5 implies

| (48) |

On the other hand, we have

according to Assumption 6. Therefore, as long as , we have . Combine this with (47) and (48) we get

Similarly, we have

Plugging these in (46) we know that

Since this holds for all , we know that

To sum up, as long as , we have

F.4 Proofs of Lemma C.4

F.5 Proofs of Lemma C.5

Suppose Lemma C.1-Lemma C.5 hold for the -th iteration. In the following, we prove Lemma C.5 for the -th iteration.

We first show . We denote

Same as Lemma 15 in Chen et al., (2020), it can be seen that

| (49) |

Note that

Moreover, by Lemma C.1 for the -th iteration, we have

Thus, we have

By Lemma F.2, we have

This implies

| (50) |

Combine (49) and (50), we have

as long as and . The upper bound on the leave-one-out sequences can be derived similarly.

F.6 Proofs of Lemma C.6

Proof.

Summing (16) from to leads to

Thus, we have

| (51) |

where we use the fact that . Thus, it remains to control . Note that

where lies in the line segment connecting and . By triangle inequality, we have

| (52) |

By Lemma C.4, it holds that

Thus, by Lemma B.1, we have

where the last inequality follows from Lemma C.1.

Consequently, by (F.6) and Lemma F.1, we have shown that

where we use the fact that by Assumption 4. By Lemma C.1, this further implies that

as long as . Thus, we have

as long as (which holds as long as large enough). Together with (F.6), we finish the proofs.

∎

Appendix G Proofs of Section D

We first prove some useful lemmas in the following.

Lemma G.1.

Proof of Lemma G.1.

We first control in the following. Note that

Thus, it holds that

| (53) |

For the first term, we have

| (by mean-value theorem) | |||

Note that

where the last inequality follows from (17) and Assumption 4. Since we have , it then holds that

| (54) |

For the second term, note that for any ,

Note that

where (i) follows from Lemma C.1. Similar arguments hold for the other terms, for which we omit the proofs. We then have

Consequently, we have

| (55) |

Combine (G), (G) and (G), we have

By Weyl’s inequality, we have

Since , we then have as long as is large enough.

∎

G.1 Proofs of Proposition D.1

G.2 Proofs of Proposition D.2

In order to show the second part of the result, we introduce the following lemma first.

Lemma G.2.

Consider some fixed constants for , and random variable

Then with probability at least we have

Proof.

Denote by . Then we know that and . Therefore, by Hoeffding inequality, with probability at least , we have

| (56) |

On the other hand, since are independent random variables, we know that

As a result, we have . Combine this with (56) we get

with probability exceeding . ∎

Let’s come back to control

According to the definition of from (21), we know that each entry of can be written as linear combinations of , since is a linear combination of . Then by Lemma G.2, we know that given any index we have

with probability at least . Taking a union bound for all indices we know that

| (57) |

with probability at least . On the other hand, from (21) we know that

Therefore, one can see that

Plugging this in (57) we get

with probability at least .

G.3 Proofs of Theorem D.3

We first prove the following lemma.

Proof of Lemma G.3.

| (58) |

For notation simplicity, we denote

We can further decompose the third term on the RHS of (G.3) as

Consequently, we have

| (59) |

In the following, we bound (1)-(4), respectively.

- 1.

- 2.

-

3.

For (3), we have

- 4.

Combine the bounds for (1)-(4), we have

Consequently, it holds that

We then finish the proofs. ∎

Proof of Theorem D.3.

For notation simplicity, given , we let , which is the convex counterpart of . We denote

which will be used in the following proofs. By Proposition D.1, Proposition D.2 and Lemma C.1, all the Frobenius norms related to (e.g., , , ) are bounded by . Additionally, all the Frobenius norms related to (e.g., ) are bounded by .

We define the quadratic approximation of the convex loss (defined in (12)) as

which implies for all

| (60) |

Note that

where the second equation follows from (60) with . Rearranging the terms gives

By multiplying both sides with , we have

| (61) |

For the LHS of (G.3), we have

| (62) |

as long as . To control , we write . Then . One can see that

By Proposition D.1, Lemma C.1 and Assumption 4 we know that

Therefore, we have

Similarly, for we also have

Combine them together, we know that

Plugging this back to (62), we know that

| (63) |

where we define .

For the RHS of (G.3), we will bound (1), (2) and (3), respectively.

-

1.

We first bound (1). We denote

It then holds that

Thus, we have

Note that

(mean-value theorem) By the definition of , we have

where the last inequality follows from the definition of . Moreover, notice that

where . Thus, we have

and

where the third inequality follows from Lemma G.3, Proposition D.1, Proposition D.2 and Lemma C.1. Consequently, we have

and for all

As a result, we obtain

where .

-

2.

We then bound (2). Note that

(64) For the first term, recall the definition of , we have

Note that

Thus we have

(65) By (20), we have

Moreover, note that . Thus, it holds that

Combine the above result with (2), we have

(66) Similarly, we have

(67) Combine (2) and (2), we obtain

(68) where

(69) As bounding (1), we have

(70) for . It remains to bound . Note that

(Cauchy-Schwarz) (by Assumption 3) Similarly, we have

and

Also, we have

(Cauchy-Schwarz) and

Follow the proofs in Appendix E, we have

and

As a result, we obtain

Combine this with (2) and (2), we show that

-

3.

We finally bound (3). By (60) with , we have

which then implies

(71) We will deal with the first term in the following. Recall the definition of , follow the same argument as in (2), we have

(72) By (22), we have . Moreover, note that . Thus, we have

where the last equation follows the same argument as that in bounding (2). Plug this into (72), we have

(73) Similarly, recall the definition of , we have

(74) Combine (3) and (3), we then have

(75) where

Following the same argument as in bounding (2), we have

Appendix H Proofs of Section 3

H.1 Proofs of Proposition 3.1

In this example, we have

where with the first rows being and the last rows being . It then holds that

| (76) |

where . We denote

Since , we then have

In what follows, we view as a matrix and denote

where . Recall that we have

where we view as vectors. Thus, we have

| (77) |

Based on the specific form of and , it can be seen that the solutions must have the following form:Why???

| (78) |

The matrix on the RHS has its first rows being and last rows being for some . By (77), we have

| (79) |

With a little abuse of notion, we denote the one-hot vector in the following. And we denote . It then holds that

| (80) |

Combine (76), (78), (79), (H.1), we have

which implies

We denote

It then holds that

and

| (81) |

Combine with (76), we have

By the definition of , we have

Thus, we have

Note that

has singular values equal to and singular values equal to . And in this example, we have . Thus we verify

That is to say Assumption 7 holds with . Thus, we finish the proofs.

H.2 Bridge convex optimizer and approximate nonconvex optimizer

In this section, we aim to prove the following theorem.

Theorem H.1.

H.2.1 Useful claims and lemmas

In this section, we establish several useful claims and lemmas that will support the proof of Theorem H.1. For notation simplicity, in this section, we denote the solution given by gradient descent as instead of .

Claim H.2.

Let be the SVD of . There exists an invertible matrix such that , and

| (82) |

Here is the SVD of Q.

Proof of Claim H.2.

Let

By the definition of and , we have

In addition, the definition of and allow us to obtain

Here, the last inequality follows from the fact that . In view of Lemma J.6, one can find an invertible such that , and

where is a diagonal matrix consisting of all singular values of . Here the second inequality follows from

which implies as long as . This completes the proof. ∎

With Claim H.2 in hand, we are ready to establish the following claim.

Claim H.3.

Proof of Claim H.3.

Recall the notations in the proof of Claim H.2, we have

| (83) |

By the definition of , we have

| (84) |

From the definition of , we have

| (85) |

In addition, by Claim H.2, we have

| (86) |

for some invertible matrix , whose SVD obeys (82). Combine (83) and (84), we have

which together with (86) yields

Apply the triangle inequality to get

| (87) |

In order to further upper bound (H.2.1), we first recognize the fact that as long as ,

which holds since

Second, Claim H.2 and (18) yields

This in turn implies that . Putting the above bounds together yields

Similarly, we can show that

These bounds together with (H.2.1) result in

| (88) |

In the following, we establish the bound for . Note that

Suppose for the moment that

| (89) |

Then, by Weyl’s inequality, we have

Since with singular values of , we conclude that

Thus, it remains to verify the two conditions listed in (89). For the first condition, by (88), we have

which is guaranteed by (18). We then verify the second condition in the following. For notation simplicity, we denote

Then we have

We define a matrix such that

It then holds that

| (90) |

Recall the definition of where

We then have for :

where the last inequality follows from the mean-value theorem and the fact that for any . This further implies that

where the last inequality follows from (17) and Assumption 4. Thus, as long as large enough, we have

| (91) |

Moreover, as shown in the proofs of Lemma F.1, we have

| (92) |

as long as . Thus, it remains to deal with . Note that

| (93) |

In what follows, we will deal with (1),(2) and (3), respectively.

-

1.

For (1), note that

where the last inequality follows the same trick we used before and we omit the details here. By Theorem D.3, we obtain

(94) as long as is large enough.

- 2.

-

3.

We denote such that

With a little abuse of notation, we denote such that

Then by Assumption 7, we have

for some . We further have the following claim.

Claim H.4.

It holds that

where

(96) Proof of Claim H.4.

By the definition of , we have

By the definition of the debiased estimator, we have

For notation simplicity, we denote

and It then holds that

(97) In the following, we control , , , and , respectively.

- (a)

- (b)

-

(c)

For , by Lemma G.1, we have .

-

(d)

For , we have

as long as .

∎

By Weyl’s inequality, we have

By Claim H.4, we can bound the Frobenius norms on the RHS respectively.

-

(a)

For the first Frobenius norm, we have

- (b)

Combine the above bounds, we have

as long as ( is large enough). By Weyl’s inequality, we have

(by Proposition D.1) (103) as long as ( is large enough).

Finally, combine (H.2.1), (91), (92), (H.2.1) and apply Weyl’s inequality, we have

Thus, we finish the proof of Claim H.3.

∎

Lemma H.5.

Given any and which satisfies

then we have

Proof.

We have

as long as . Here (i) follows from the fact that , , and . ∎

H.2.2 Proof of Theorem H.1

Proof of Theorem H.1.

In the following, we fix a constant . We define a constraint convex optimization problem as

| (105) |

where is the convex objective defined in (13). By (17), is feasible for the constraint of (105). By the optimality of , we have

| (106) |

We denote

By mean value theorem, there exists a set of parameter which is a convex combination of and such that

| (107) |

Therefore, we have

Combine this with (106) we get

| (108) |

In addition, by the convexity of , we have

for any obeying . In the following, we pick such that . We then obtain , and consequently, by (108), we have

Recall the definition of in (84), we further have

By Claim H.3, we have

As a result, one can see that

| (109) |

with some constant .

On the other hand, note that for some constant

| (110) |

where the last inequality follows Lemma H.5. Here (1) follows from the following argument: note that

Further, by (17), we have

| (Cauchy) | ||||

Thus, by (17) and Assumption 2, as long as is large enough, we have . Similarly, we have

Further, by the constraints, we have . Since lies between and , we conclude that . Consequently, we have for some constant , which implies (1).

Combine (H.2.2) and (H.2.2), we have

| (111) |

for . By (106) and (111), we obtain

| (112) |

Recall that . Consequently, we have

Recall the definition of in (84), we further have

| (113) |

By Claim H.3, we have

| (114) |

Combine (H.2.2) and (114) we get

| (115) |

In the sequel, we deal with . One can see that

| (116) |

By Lemma E.1 we know that

| (117) |

On the other hand, by (109) we have

| (118) |

Combine (116), (117) and (118) we know that

Combine this with (115), we get

where . Since , we know that

As a result, we get

| (119) |

Further by (18), we obtain

Consequently, we show that

as long as is large enough. In other words, the minimizer of (105) is in the interior of the constraint. By the convexity of (105), we have . Consequently, by (119), we have

Thus, we prove Theorem H.1. ∎

H.3 Proofs of Theorem 3.2

Appendix I Proofs of Proposition 3.4 and Theorem 3.7

I.1 Proofs of Proposition 3.4

Compared to (Jin et al.,, 2023, Proposition A.1), the only difference between our identifiable condition and theirs is the sign of diagonal entries of . In fact, as to the proof of this condition, we only need to make a slight modification on the basis of (Jin et al.,, 2023, Proposition A.1).

Assume that we have two sets of and which satisfy Proposition 3.4 and . According to (Jin et al.,, 2023, Proof of Proposition A.1), if the row of (or ) represents a pure node, then the row of (or ) also represents a pure node, and these two sets of pure nodes are identical up to a permutation of the columns. Therefore, without loss of generality, we assume that and are all equal to the identity matrix. Comparing the submatrices and , which should be identical, we get

| (120) |

Particularly, we know that for all . Since , we know that and must have the same sign. By Proposition 3.4, . Therefore, we know that . This also implies , and thus . Plugging this back in (120), we get . The rest of the proof is the same as (Jin et al.,, 2023, Proof of Proposition A.1), and we finally reach . That is to say, the DCMM model is identifiable under the conditions in Proposition 3.4.

I.2 Proofs of Theorem 3.7

In this section, we will frequently using (Jin et al.,, 2023, Lemma C.2, C.3, C.4). Since our condition on is slightly adapted from (Jin et al.,, 2023, Proposition A.1), the (Jin et al.,, 2023, Lemma C.2) has to be modified here. We state the result we are going to use as follows.

Let be the SVD of and assume the diagonal entries of are sorted in a descending order. We denote by

We choose the signs such that the left singular vectors are coincident with the eigenvectors associated with the largest (in magnitude) eigenvalues. Also, let be the SVD of , where are the nonconvex estimators given in Section D. Define

We begin with the following lemma.

Lemma I.2.

Define

Then it holds that

Proof.

We define

By Weyl’s inequality and the proof of Theorem 3.2, we have

which implies . By Davis-Kahan Theorem, we have

where (1) follows from Theorem H.1 and (18). Also, by Davis-Kahan Theorem we know that

Since

as long as is large enough, by Lemma J.2 we have

| (121) |

We define . It’s easy to see that

| (122) |

We then turn to control . By Claim H.2, there exists an invertible matrix such that and (82) holds. By the definition of , we have . Thus, we have

| (123) |

It then holds that

| (124) |

where the last inequality follows from (17) and the fact that

Note that

Since satisfies (82), we have . Moreover, we have show that . Thus, we obtain

| (125) |

By (I.2), we have

where the last inequality follows from Lemma C.1 and the fact that

By Davis-Kahan Theorem and (122), we have

Thus, we have

| (126) |

Combine (125) and (126), we get

| (127) |

Further by (I.2), we have

Combine above inequality with (121), we obtain

We then finish the proof of Lemma I.2. ∎

Let be the -th to -th column of and be the -th to -th column of . Define as the rotation matrix aligns and , i.e.,

Moreover, without loss of generality, we choose the direction of such that . Then we have the following results.

Lemma I.3.

It holds that

Proof.

We define

According to this definition, one can see that

Therefore, we can control the different between and as

By Davis-Karhan Theorem and Lemma 2 in Yan et al., (2024), we have

Similarly, according to Assumption 8, we have

Combine these two results we get

| (128) |

On the other hand, can be written as

| (129) |

It remains to control . Notice that

Therefore, can be controlled as

| (130) |

The term can be further controlled as

| (131) |

Plugging (131) in (130) we get

Combing this with (128) and (129) we have

Now we turn to control . Similarly, one can see that

On the other hand, can be decomposed into

Since , the inequality (131) also applies to . Therefore, can be controlled as

∎

As a direct corollary of Lemma I.3, we have the following result.

Corollary I.4.

, it holds that

Proof.

Then we are ready to control the estimation error of the eigen ratio .

Lemma I.5.

Proof.

By definition we can write

Therefore, we have

∎

By Lemma I.5, the eigen ratio can be estimated uniformly well in the sense that

| (132) |

Recall the definition of efficient vertex-hunting algorithms, we have

| (133) |

We then prove Theorem 3.7 in the following.

Proof of Theorem 3.7.

Claim I.6.

Under Assumption 8, it holds that

By Claim I.6, we have . By Weyl’s inequality, we have

Thus, it holds that

| (134) |

Note that

Consequently, we have

where the last inequality follows from (134). Note that

where the last inequality follows from the fact that . Thus, we obtain

Further by (132) and (133), we obtain

| (135) |

Next, let’s control . By definition we have

| (136) |

By (Jin et al.,, 2023, Eq. (C.22)) we know that . On the other hand, by Weyl’s inequality we know that

| (137) |

It remains to control . Define

we can write

| (138) |

Furthermore, we write

| (139) |

The first term on the RHS can be controlled as

| (140) |

The second term can be controlled as

| (141) |

The last term can be further controlled by

Combine this with (141) we know that

Plugging this and (140) in (139) we get

as long as .

Before we go back to (138), we need to control and . By Assumption 4 and (Jin et al.,, 2023, Lemma C.3), it can be controlled as

And, as long as

we also have . As a result, from (138) we know that

Combine this with (137) and plug them back in (136) we get

By Lemma I.1 we know that

Therefore, we have

Appendix J Technical lemmas

Lemma J.1.

For matrix , we have

Lemma J.2.

Suppose are three matrices such that

where stands for the -th largest singular value of . Denote

Then the following two inequalities hold:

Proof of Lemma J.3.

Proof of Lemma J.4.

By Weyl’s inequality, we have

Note that

| (by Lemma J.3) | ||||

and . We then have

which implies

Similarly, we can show that

∎

Lemma J.5.

Let be a nonsingular matrix. Then for any matrix with , one has

where denotes the matrix sign function, i.e. for a matrix with SVD .

Proof.

See Lemma 36 in Ma et al., (2018). ∎

Lemma J.6.

Let be the SVD of a rank- matrix with . Then there exists an invertible matrix such that and . In addition, one has

| (140) |

where is the SVD of . In particular, if and have balanced scale, i.e., , then must be a rotation matrix.

Proof.

See Lemma 20 in Ma et al., (2018). ∎