Dynamic Pricing in the Linear Valuation Model using Shape Constraints

Abstract

We propose a shape-constrained approach to dynamic pricing for censored data in the linear valuation model that eliminates the need for tuning parameters commonly required in existing methods. Previous works have addressed the challenge of unknown market noise distribution using strategies ranging from kernel methods to reinforcement learning algorithms, such as bandit techniques and upper confidence bounds (UCB), under the Lipschitz (and stronger) assumption(s) on . In contrast, our method relies on isotonic regression under the weaker assumption that is -Hölder continuous for some . Simulations and experiments with real-world data obtained by Welltower Inc (a major healthcare Real Estate Investment Trust) consistently demonstrate that our method attains better empirical regret in comparison to several existing methods in the literature while offering the advantage of being completely tuning-parameter free.

1 Introduction

Dynamic pricing is the process of continuously adjusting product prices in response to customer feedback based on statistical learning and policy optimization. As a fundamental aspect of revenue management, dynamic pricing has been widely applied across various industries. A key challenge in this area is balancing the need to explore customer demand with exploiting current knowledge to set optimal prices that maximize revenue. This tradeoff between exploration and exploitation has been extensively studied in fields such as statistics, machine learning, economics, and operations research Besbes & Zeevi (2009); Keskin & Zeevi (2014); Cheung et al. (2017); Cesa-Bianchi et al. (2019); den Boer & Keskin (2020). A large literature focuses on an important dynamic pricing problem where contextual information, such as product features and market conditions, is available at each time step. By leveraging this contextual data, we aim to refine pricing strategies and improve revenue outcomes. This approach, known as feature-based or contextual pricing, allows for more customized pricing decisions that better reflect product heterogeneity, leading to more effective revenue management in today’s data-rich environment.

This paper focuses on the problem of pricing a single product over a finite time horizon , where the market value of the product is unknown to the seller and may vary over time . The market value is modeled as a linear function of observed features (covariates) of the product

| (1) |

where contains in the first component to consider for the intercept, is some unknown parameter and are independent of the noise that are i.i.d. with unknown cumulative distribution function (c.d.f.) . After the seller proposes a price , they observe whether the item is sold or not, i.e. and collect revenue . The seller aims to design a policy that maximizes the total revenue , given the uncertainty in the market value and the limited information available to the seller, that is . The determination of the optimal revenue entails learning the model parameters for which various statistical tools have been employed such as kernel-based methods, bandit technique, and UCB (Fan et al., 2021; Luo et al., 2022; 2024; Xu & Wang, 2022; Tullii et al., 2024).

Building on the semi-parametric structure of the model and recent advances in shape-constrained statistics, we propose a novel policy that requires minimal assumptions about the underlying distribution of market noise. Specifically, we estimate using ordinary least squares (OLS) and using non-parametric least squares (NPLS), subject to the natural constraint that is non-decreasing.

A key advantage of our shape-constrained approach is that it is entirely data-driven and does not require the specification of any tuning parameters, unlike existing non-parametric methods. For example, the kernel-based technique proposed by Fan et al. (2021) requires bandwidth selection for optimizing the error of the estimator. In contrast, the UCB-based strategy of Luo et al. (2022) requires a set of subjective parameters including a tuning parameter.

Contribution.

Our main contributions are:

-

(1)

We propose a new tuning parameter-free method, unlike existing non-parametric methods for estimating the market noise distribution , leveraging the shape constraint that is non-decreasing and assuming only that is -Hölder continuous for some .

-

(2)

We derive an upper bound on the total expected regret of order , where ,

(2) and excludes log factors (under Lipshitzianity of , this rates becomes ), and we provide a thorough assessment of its empirical performance with comparisons to existing algorithms through a number of simulations, as well as an emulation experiment based on real data. Our algorithm shows strong empirical performance: in particular, it dominates the algorithm proposed by Tullii et al. (2024) in their simulation setting up to very large time horizons. Additionally, our algorithm when applied to a real data set obtained by Welltower Inc continues to demonstrate stronger performance than Tullii et al. (2024); Luo et al. (2022) and is competitive with the nonparametric method proposed by Fan et al. (2021), though the latter relies on stronger smoothness assumptions.

-

(3)

Beyond the application of antitonic regression, our work involves establishing a concentration inequality for the uniform norm of the antitonic regression estimator error, which is required to derive the expected regret upper bound. Although the existing literature on isotonic regression explores the rate of convergence of the uniform error, explicit tail probability bounds (stronger than statements) of the type presented in this work (see Theorem˜4.8) appear to be missing.

1.1 Related Works

The linear valuation model for contextual dynamic pricing, as defined in Equation˜1, has been extensively studied under various assumptions. Recent works have explored statistical models—both linear and their extensions—for the pricing problem, assuming that (the noise distribution) is either known, partially known111Meaning is unknown but belongs to a parameterized family. (Miao et al., 2019; Ban & Keskin, 2021; Javanmard & Nazerzadeh, 2019; Golrezaei et al., 2019), or fully unknown (Fan et al., 2021; Xu & Wang, 2022; Luo et al., 2022). For comprehensive overviews of dynamic pricing from a broader perspective, we refer readers to Den Boer (2015) and Kumar et al. (2018).

We focus on the results most relevant to our work—specifically, the case where both the parameter and the distribution are fully unknown. In this setting, Fan et al. (2021) estimate using kernel methods and derive a regret upper bound of , where denotes the degree of smoothness of . In the realm of reinforcement learning, Luo et al. (2022) introduces the Explore-then-UCB strategy, which balances revenue maximization, estimation of the linear valuation parameter, and nonparametric learning of the noise distribution. Under Lipschitz continuity on , their approach achieves a regret rate of , and under (an additional) second-order smoothness assumption, a regret of . However, their regret bounds depend on a regularization parameter , which is hard to tune dynamically, and the impact of the choice of on the regret is not clearly described. Xu & Wang (2022) propose the D2-EXP4 algorithm, which is based on discretizing both the parameter space of and . With appropriate choices of the discretization parameters, they establish a regret upper bound of . However, as noted in Xu & Wang (2022, Section 6), they were unable to perform numerical experiments on D2-EXP4 due to the exponential time complexity of the EXP4 learner with a policy set of size , making their algorithm impractical for application. Furthermore, Assumption 1 of their paper requires their and to have non-negative entries. While they claim that this assumption entails no loss of generality, this assumption is heavily used in the proofs of Theorem 6 and Theorem 5 of their work, and it is far from clear whether their derivations are generalizable to the situation when such sign constraints are not imposed. While the positivity of covariates can be ensured under boundedness by adding constants and adjusting the intercept parameter, the assumption that all covariates have a positive impact on the valuation is quite unrealistic for any regression model.

In contrast to Fan et al. (2021); Luo et al. (2022); Xu & Wang (2022), we propose a tuning parameter-free policy that achieves a regret upper bound of order when (i.e. is Lipschitz). Furthermore, estimating the parameters and is computationally efficient: is estimated using ordinary least squares (OLS), and is estimated via isotonic regression222Alternatively, estimating using antitonic regression. using the Pool Adjacent Violators Algorithm (PAVA) introduced by Robertson et al. (1988), which, in our problem, has a computational complexity of (see Section˜3.1).

Very recent work by Tullii et al. (2024) provides a UCB-LCB-based algorithm named VAPE (Valuation Approximation-Price Elimination). The main idea is to update the estimate of at time when is far from previously observed covariate values; otherwise, update the UCB-LCB around and deploy the optimal price. They prove that their regret is upper bounded by under Lipschitz assumption on (i.e. ), which attains the lower bound in , established in Xu & Wang (2022). We summarize the regret upper bounds and the underlying assumptions in Table˜1.

| Method | Regret Upper Bound | Hölder Continuity | Lipschitz Continuity | 2nd Order Smoothness | |

|---|---|---|---|---|---|

| Fan et al. (2021) | |||||

| Luo et al. (2022) | |||||

| Tullii et al. (2024) | |||||

| This Work |

1.2 Notation

For an interval , we use . For any given matrix , we write or if or is semi-definite. For any event , we let be an indicator random variable which is equal to if is true and otherwise. For two positive sequences , we write or if there exists a positive constant such that . In addition, we write or if with some constant . Moreover, we let represent the same meaning with except for ignoring log factors. For a random variable we will denote by , and its corresponding density function and probability measure, respectively. For a c.d.f. we will use to denote . Given a function we write . We say that a function is -Hölder (continuous) for some constant if for all in it’s domain.

2 Problem Setting

We consider the pricing problem where a seller has a single product for sale at each time period . Here is the total number of periods (i.e. length of the horizon) and may be unknown to the seller. The market value of the product at time is denoted by and is unknown to the seller. At each period , the seller posts a price for . If , a sale occurs, and the seller collects a revenue of . Otherwise, no sale occurs and no revenue is obtained. Let be the response variable that indicates whether a sale has occurred at period :

and let the collected revenue at time . We model the market value as a linear function of the product’s observable i.i.d features

| (3) |

where is an unknown parameter (which includes the intercept term), and are i.i.d sequence of idiosyncratic noise drawn from an unknown distribution with mean and bounded support

| (4) |

We assume that the first entry in equals to account for the intercept term in . The overall procedure is summarized in Box 2. The expected revenue for any offered price given is

Note that, since is a survival function, it is non-increasing. The optimal price at time is defined by a maximizer of the expected revenue function at the round,

| (5) |

Note that , depends on . The regret at step is defined by the difference between the expected revenues from the optimal price and the offered price : . In other words, we consider the problem of maximizing revenue as minimizing the following maximum regret

where the expectation is taken with respect to the idiosyncratic noise , the covariates , and the offered prices that depend on the specific policy.

As the firm’s goal is to design a policy that sets prices as close as possible to the optimal prices defined in Equation˜5, we first estimate and then we plug in the estimate as in Equation˜6 to get an estimated optimal price . Accurate estimation of thereby ensures that the resulting policy incurs low regret.

3 Proposed Algorithm

We employ an epoch-based design (also known as the doubling trick) that segments the given horizon into several clusters of rounds, called epochs or episodes, and executes identical pricing policies on a per-epoch basis. Let be the first episode, where is a prefixed constant. For , define , and the set of times in the -th episode.

We partition into two sub-phases, , where represents the exploration phase, dedicated to collecting data for estimating the parameters , while denotes the exploitation phase, during which we apply the optimal prices based on the estimated parameters . The length of the exploration phase, , is set to , chosen to minimize the expected regret . Specifically, as we show in the proof of Theorem˜4.10, if for some , then is minimized if and satisfy the condition . is further divided into two equal-sized intervals and . In we collect data to estimate . In we collect data to estimate . The details are stated in Algorithm˜1, and a picture of a general episode is shown in Figure˜1. In the following portion of this section, we examine the details of exploration-exploitation for a fixed episode .

Estimation of .

For all the seller observe , deploy and observes . Let and estimate

Estimation of .

For , the seller observe , sample , propose a price and observes . Estimate

where is the set of non-increasing function in .

Exploitation.

For every , observe , set

| (6) |

and get reward .

3.1 Complexity of the antitonic regression

The algorithmic complexity for estimating is . Indeed by Grotzinger & Witzgall (1984); Tibshirani et al. (2011) the computational complexity for the antitonic estimator is , where is the sample size. In our case, the estimation of happens in (half of) the exploration phase which has length proportional to , then, using that , we have .

4 Regret Analysis

Before proceeding with the regret analysis we need to discuss the convergence rates of to and to . We present our main theorems and proofs. We defer to the Appendix for the missing proofs.

4.1 Estimation of

Assumption 4.1 (Bounded parameter space).

The parameter is an interior point of and the parameter space is a compact convex set.

Assumption 4.2 (Bounded i.i.d. contexts).

(a) is i.i.d. drawn a distribution that does not involve and , and for all , for some unknown . (b) There exists reals , s.t. , where and the identity matrix.

4.2 Estimation of via antitonic regression

In this section, we provide a uniform convergence result of to . For simplicity of notation, we re-index as , and we denote by , which was estimated using data independent of . In this section, all the results must be considered as conditioned on . We report in Box 4.2 a more detailed explanation of the estimation of during the exploration phase in as expounded in the box highlighted in Algorithm˜1.

This produces a set of data points that we are going to use for estimating . To estimate we would need to know in advance, indeed remember that , which design points depend on . However, our knowledge is limited to an approximation of , and the observable design points are . This implies that we are only able to estimate . We then estimate considering as coming from a sample in the ordinary current status model, where the data has the form , the observation times have uniform density and where with probability at observation .

Remark 4.4 (The choice of the design points ).

The choice of the distribution for is motivated by the fact that when the density of design points is uniform, we obtain convergence guarantees for the estimator of . Specifically, as mentioned by Mösching & Dümbgen (2020), if the density of the design points is bounded away from zero – which holds for the uniform distribution – then are “asymptotically dense” within any interval contained in (defined in Equation˜4). Ensuring that the design points have a density bounded away from zero is a sufficient condition for the convergence result in Theorem˜4.8 (see Lemma˜A.2 for further details). However, this choice is not restrictive; any distribution whose density is bounded away from zero in would still satisfy the convergence result. The only consequence of using a non-uniform density is that the regret will depend on the multiplicative constant , which may be different from if is not the uniform density in . Furthermore, since each episode is independent of any other episode for , it is possible to select a different density for each episode , provided that it remains bounded away from zero in . An interesting extension of our work would be to adaptively update the design density based on the previous design in an optimal manner, namely that converges to the optimal design density as , that is the density that minimizes the integrated mean square error. This approach, known as sequential optimal design, has been extensively studied in the literature (see, e.g., Müller (1984); Zhao & Yao (2012); Bracale et al. (2024)). A key advantage of an optimal design algorithm is that it dynamically allocates more data to regions where the estimation of is less accurate, thereby progressively improving its precision. However, it is important to note that while this adaptive approach can optimize the multiplicative constant in the regret bound, it does not affect the rate of the regret itself.

Remark 4.5 (The difference between the conditional distributions of and ).

We want to highlight the difference between the conditional distributions of and . The first is independent of , indeed we have that

while, the distribution of depends on because where , and, since data is generated as in Box 4.2, we have that

| (7) |

where the first equality is by definition, in the second we use the tower property and in the last equality, we use that is sampled independently of . Note from Remark˜4.5 that is non-increasing for all because , being a survival function, is non-increasing.

Proposition 4.6.

is non-increasing for every . Moreover, if is -Hölder with , then is -Hölder uniformly in and uniformly in .

Proposition˜4.6 is crucial because it tells us that we can estimate under the antitonic constraint and that is close to as long as is close to , which will be used to prove Theorem˜4.10. Guided by Proposition˜4.6, we estimate using antitonic regression, denoted as

| (8) |

where is the set of non-increasing functions in . The minimizer is a piecewise constant function with jumps at a subset of . The order statistics on which is based are the order statistics of the values and the values of the corresponding . To be more specific, let the different value of the observed . For set

For every let

It is well known that may be represented by the following minimax and maximin formulae, see Robertson et al. (1988): for

The is also known as the antitonic regression on data , and we will denote it as

We are now prepared to demonstrate the convergence of to . To establish this result, we require that is -Hölder for some uniformly in . According to Proposition˜4.6, this condition is satisfied provided we make the following assumption:

Assumption 4.7.

for some , and for all .

Theorem 4.8.

Let be as defined in Box 4.2 and let Assumption 4.7 hold. Then for every and there exists and (where is defined in Equation˜4) such that

where and , with .

Remark 4.9.

Our Theorem˜4.8 parallels Theorem 3.3 in Mösching & Dümbgen (2020), with the key distinction being the nature of the observed response variable. While Mösching & Dümbgen (2020) directly observes the response variable (which corresponds to our valuation ), we observe the binary indicator . This difference simplifies our proof, as it only requires establishing a concentration inequality for , where

In our setting, this concentration inequality can be readily obtained using Hoeffding’s inequality uniformly over . Specifically, as demonstrated in Lemma˜A.1, for any constant , is at least , where .

4.3 Regret Upper Bound

We are now ready to establish an upper bound on the expected regret for our Algorithm˜1.

Theorem 4.10.

Suppose that Assumptions 4.1, 4.2 and 4.7. For sufficiently large the cumulative regret of Algorithm˜1 has upper bound of order

5 Simulations

We first perform simulations for theoretical validation in Section˜5.1 and a simulation to compare our algorithm with the minimax algorithm by Tullii et al. (2024) and Fan et al. (2021) algorithm in Section˜5.2.

5.1 Simulation for theoretical validation

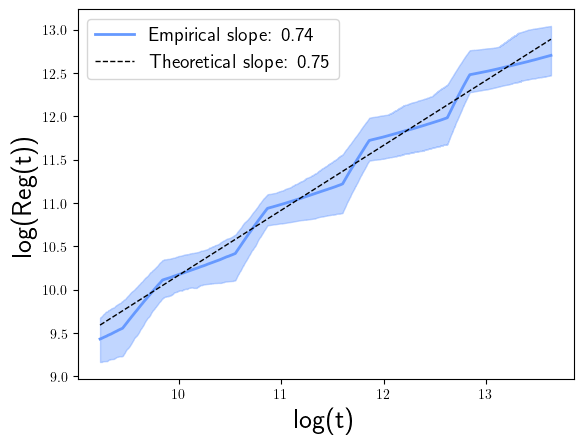

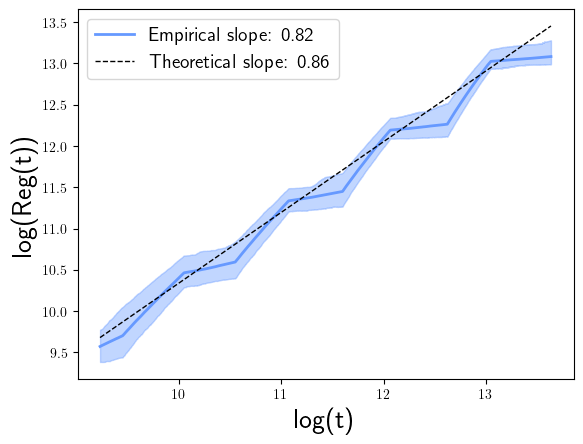

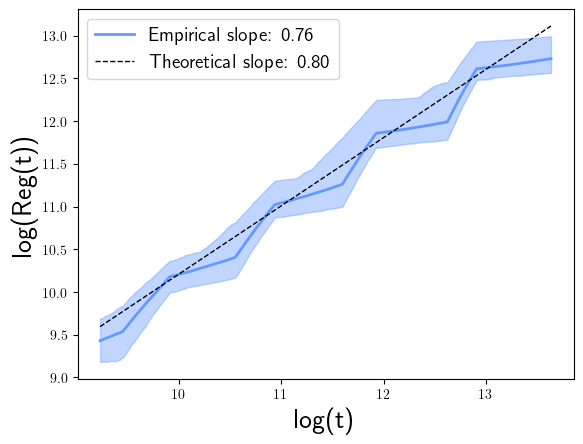

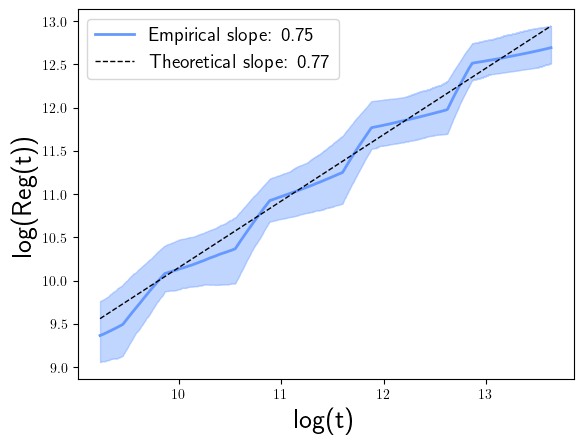

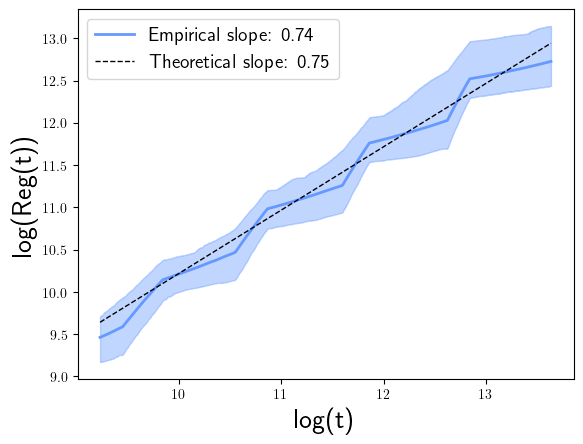

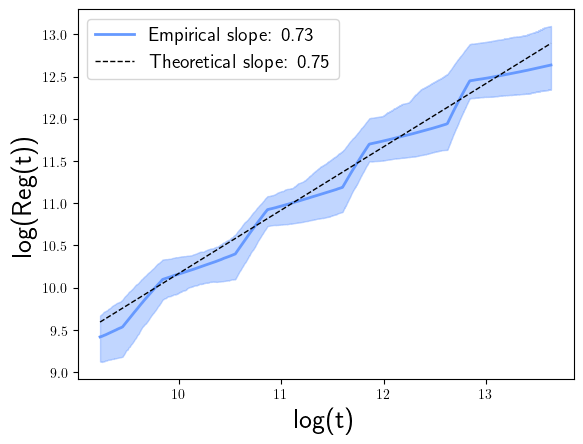

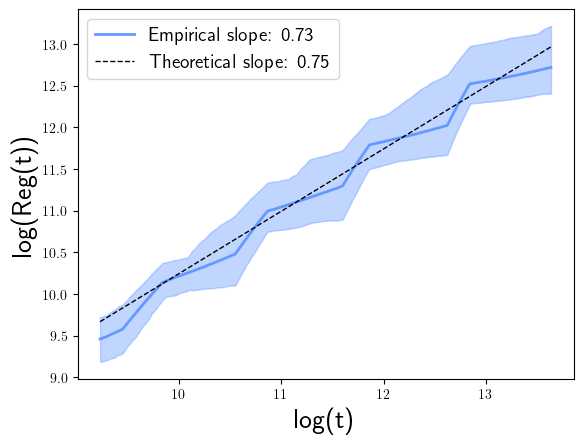

To this end, we replicate the simulation settings used by Fan et al. (2021). We set (known), the feature dimension (known), the distribution of (unknown), and the coefficient (unknown), where . We also choose and (known). For we consider different choices: : for , for , for . : we use choices of : a Gaussian truncated at , the c.d.f. used by Fan et al. (2021) with density , a Laplace with location and scale truncated at , and a Cauchy with location and scale truncated at .

We start with and compute total episodes. At every time we follow Algorithm 1 to compute , with the additional computation of the oracle and the corresponding cumulative regret . We repeated the experiment times and we computed the mean and the confidence interval in a plot. As illustrated in Figure˜2, we validate our approach by comparing the estimated slope of the linear regression of versus with the theoretical upper bound rate. Due to space constraints, the plot corresponding to the used by Fan et al. (2021) with density is provided in Appendix˜B.

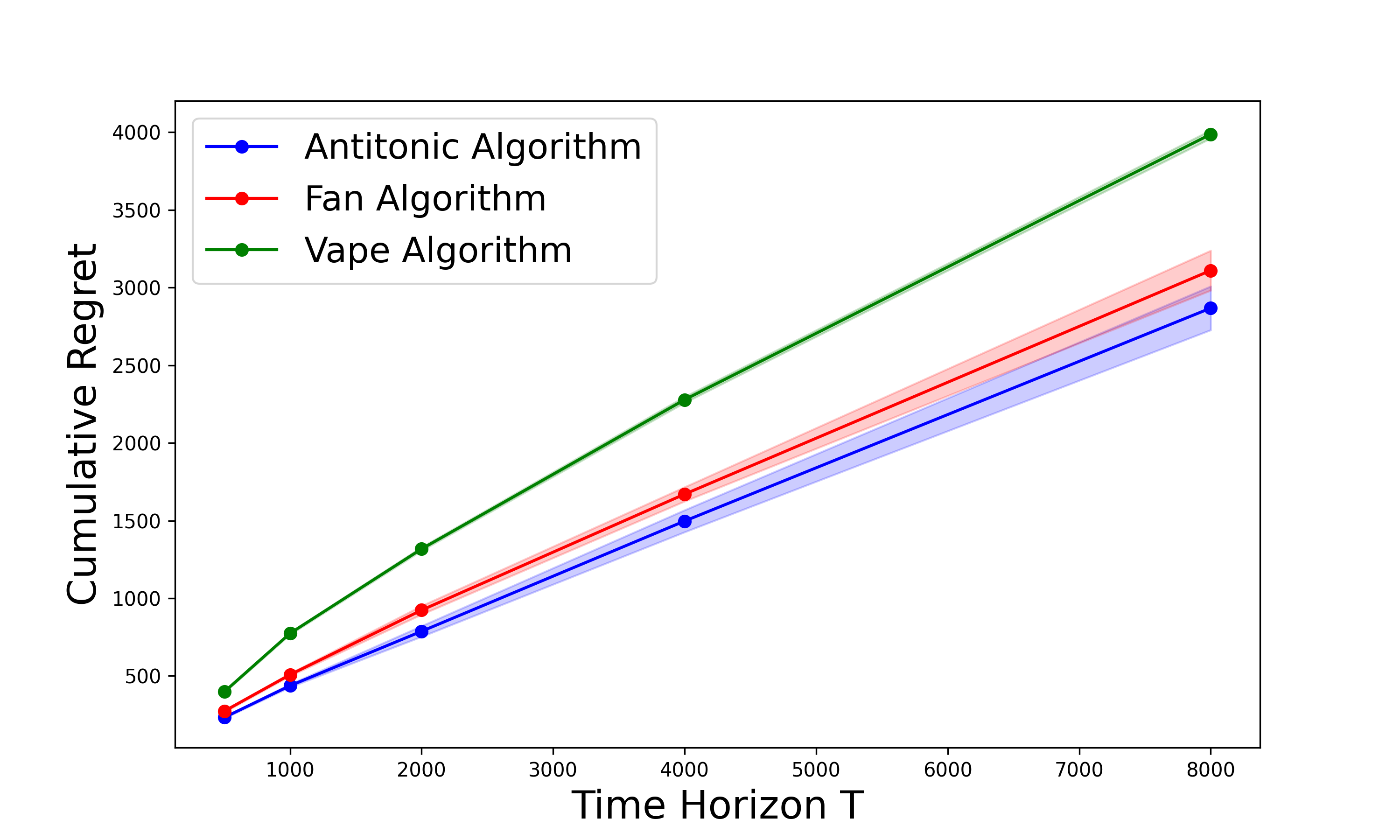

5.2 Comparison with Tullii et al. (2024) under Lipschitz assumption of

We first recall that the regret upper bound by Tullii et al. (2024) is of order under Lipschitz assumption on (), which is smaller than our regret upper-bound . For this reason, we perform the following simulations.

In their work, Tullii et al. (2024, Supplemenary Material A) compared their VAPE method to the kernel-based method by Fan et al. (2021) that is: they built a dataset of contexts belonging to generated by a canonical Gaussian distribution and subsequently normalized. Throughout the run, the contexts are chosen from this set uniformly at random, while the noise term is picked from a Gaussian distribution truncated between and with mean and variance . Similarly, also the parameter is a normalized vector initially drawn from a Gaussian distribution. Note that for this simulation, the error distribution is twice differentiable (i.e. smoother than what Tullii et al. (2024) and us allow in our theory), then Fan et al. (2021) is applicable with smoothness parameter . Tullii et al. (2024) showed that the algorithm by Fan et al. (2021), has stronger performance.

We apply our antitonic regression-based algorithm with , using the same code and simulation setting provided by Tullii et al. (2024, Supplemenary Material A). The algorithm has been tested on time horizons . We computed the regret times and the corresponding 95% confidence interval. In Figure˜3 we show the results. Although the work by Fan et al. (2021) applies to distributions of the error that are at least twice differentiable – which is the case in this simulation – their algorithm has weaker performance than ours in this setting. Comparing our antitonic method with the VAPE algorithm by Tullii et al. (2024) (which have the same assumption on , i.e. Lipschitzianity of ) the empirical performance of VAPE is worse than our method up to very large time horizons (), achieving smaller regret.

6 Real Application

This study applies our method to a real data set obtained by Welltower Inc to simulate the dynamic pricing process. The dataset consists of various characteristics and the transaction price for units in the United States (see Table˜2 for more details). In our experiments, we present each rental unit to the dynamic pricing algorithm in a sequential fashion to simulate the dynamic pricing game. The unique aspect of the dataset is it includes the exact transaction price, which allows us to evaluate the regret of the algorithm directly.

| Variable | Description |

| : act_rate_d | Final transaction price. |

| : mkt_rate_d | Typical rate of similar unit in the primary market area. |

| : sqft | Square footage of unit. |

| : unit_type | Type of unit (bedroom, studio, or other). |

| : med_home | Median home value of primary market area. |

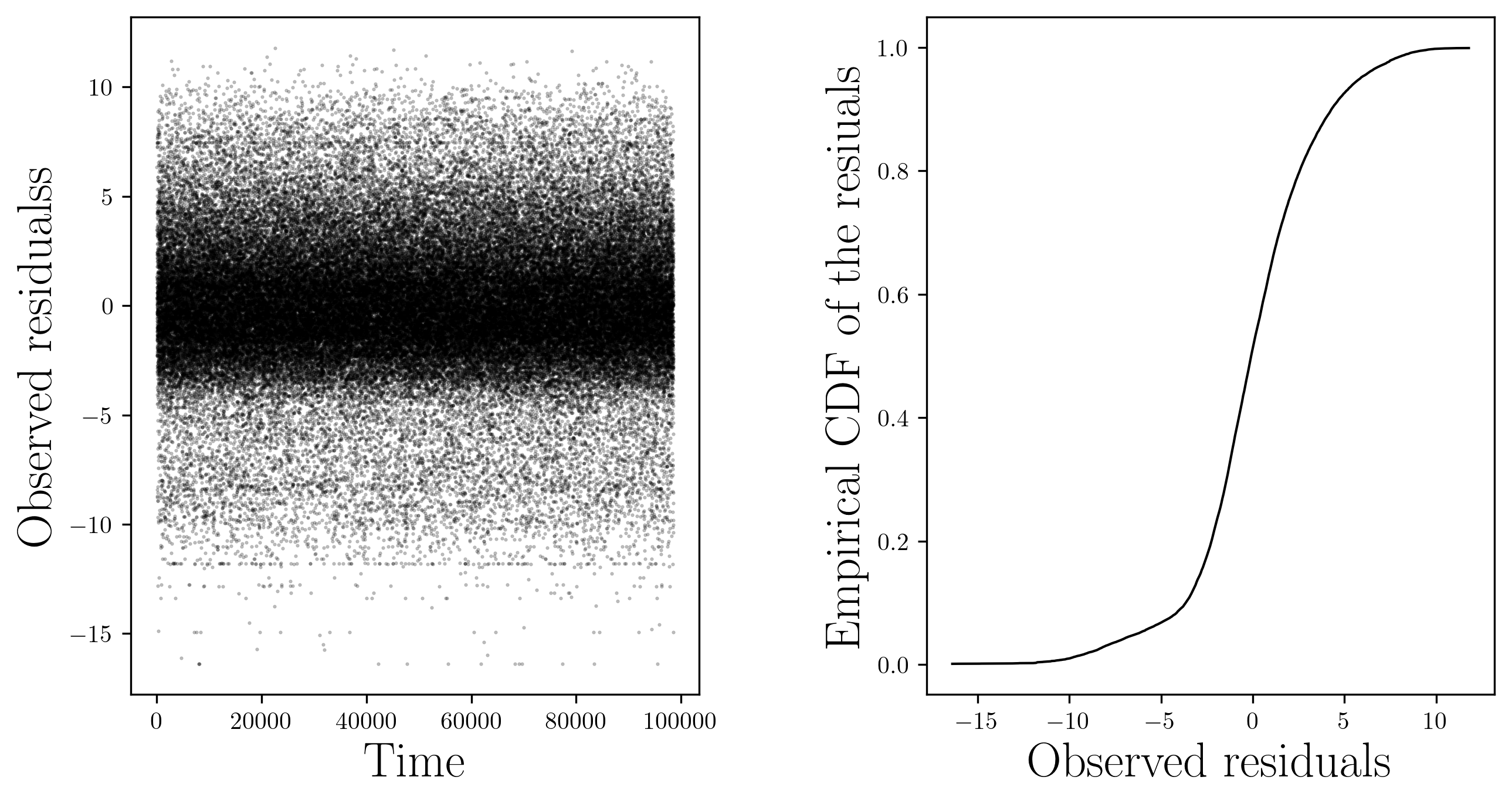

This dataset doesn’t contain the variable , i.e. whether the sales occurred. Our knowledge is limited to the final transaction prices act_rate_d. To overcome this we make the following adjustment: at each time point , we consider the transaction price act_rate_d as the customer valuation , which we treat as unobserved; a price is posted by the firm, which finally collects the data point where . Here the vector contains all the variables in Table˜2 except act_rate_d, and in the first entry to account for the intercept. As we assume for some unknown and unknown c.d.f. of , we validate this linear validation model. To this end, we perform a linear model using data : the p-value of the statistics is close to and the slopes of all the variables are statistically significant at a significance level of (see Table˜4). The residuals and the associated empirical distribution function (an estimate of ) are depicted in Figure˜4, from which we notice that is approximatively . Moreover and are the maximum and minimum values of .

| mkt_rate_d | sqft | 12min_med_home_val | 20min_med_home_val | act_rate_d | |

| min | 0.00 | 0.00 | 131131.52 | 139845.11 | 0.00 |

| 25% | 1764.12 | 334.00 | 356391.42 | 350603.75 | 139.00 |

| 50% | 2598.32 | 428.00 | 478335.94 | 481045.88 | 181.00 |

| mean | 3210.69 | 465.64 | 561100.96 | 531395.52 | 200.19 |

| 75% | 3811.40 | 546.00 | 689176.88 | 681712.58 | 233.00 |

| max | 56475.71 | 1782.00 | 1650871.95 | 1529372.81 | 1494.63 |

| Model: | OLS | Adj. R-squared: | 0.597 | |||

| Df Model: | 6 | F-statistic: | 2.432e+04 | |||

| Df Residuals: | 98552 | Prob (F-statistic): | 0.00 | |||

| R-squared: | 0.597 | Scale: | 11.956 | |||

| Coef. | Std.Err. | t | Pt | [0.025 | 0.975] | |

| const | 15.0307 | 0.0116 | 1299.4124 | 0.0000 | 15.0081 | 15.0534 |

| mkt_rate_d | 7.7899 | 0.0272 | 286.1036 | 0.0000 | 7.7365 | 7.8432 |

| sqft | -0.5291 | 0.0164 | -32.3591 | 0.0000 | -0.5612 | -0.4971 |

| 12min_med_home_val | 0.5431 | 0.0136 | 39.8486 | 0.0000 | 0.5164 | 0.5698 |

| unit_type_2 bed | 0.1804 | 0.0167 | 10.7981 | 0.0000 | 0.1477 | 0.2132 |

| unit_type_other | 0.1420 | 0.0175 | 8.1030 | 0.0000 | 0.1076 | 0.1763 |

| unit_type_studio | 0.0753 | 0.0218 | 3.4532 | 0.0006 | 0.0326 | 0.1181 |

Prior to implementing the methods, we conducted cross-validation to tune the UCB algorithm’s parameters and , as defined in Luo et al. (2022). We searched over a grid with . After selecting the optimal parameters, we ran the algorithm for each method. The initial episode length was set to , with subsequent episodes doubling in length according to , for a total of episodes. Each algorithm then chooses its exploration phase according to its rule. We conducted iterations, randomly shuffling the data before each run. For our algorithm, we set .

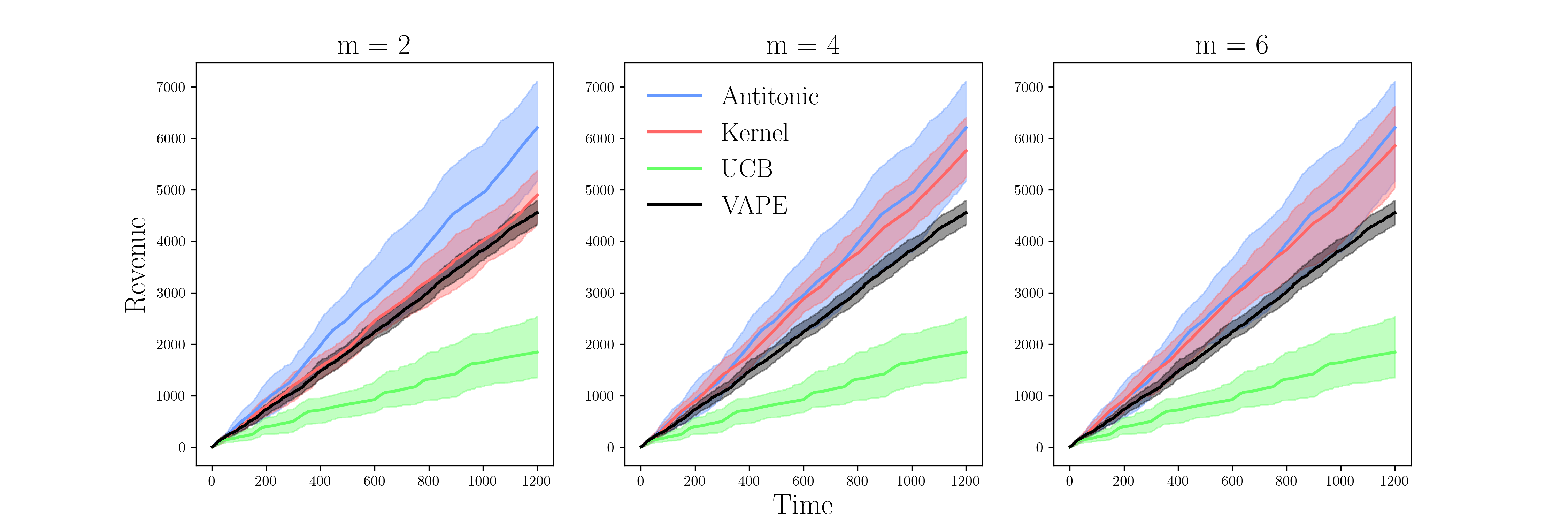

Figure˜5 showcases the (empirical) revenue , obtained using our antitonic method (blue line), the UCB method by Luo et al. (2022) (green line), the kernel method by Fan et al. (2021) (red line) and the VAPE algorithm by Tullii et al. (2024) (black line). Higher lines indicate better performance. We present three plots corresponding to different values of the smoothness parameter , which affects only the kernel method. We let the antitonic, UCB, and VAPE methods remain the same across all three plots, while the kernel method’s performance changes with varying . Overall, our antitonic method generally outperforms the other approaches. The kernel method by Fan et al. (2021) also performs well and tends to improve as the smoothness parameter increases. Despite tuning its parameters, the UCB method by Luo et al. (2022) performs poorly, while as far as the VAPE algorithm by Tullii et al. (2024) shows worse performance than our method and kernel-based method.

7 Conclusions

We introduced a novel method for estimating the market noise distribution by leveraging its natural shape constraint: monotonicity. Our analysis led to an expected upper bound on the total regret of order , where is defined in Equation˜2, matching certain previous rates in when and enjoying the additional advantage of being tuning parameter-free. Compared to existing methods such as Tullii et al. (2024); Fan et al. (2021); Luo et al. (2022), our proposed algorithm shows stronger empirical performance in both simulations and real data applications.

An interesting direction for future research is the study of lower bounds on the expected regret under the Hölder condition on and an investigation into whether our rate matches this bound. In the special case when (i.e. Lipschitzianity of ), the regret lower bound of established in Xu & Wang (2022), has been attained in Tullii et al. (2024). Another promising extension, particularly for practical applications, is the incorporation of optimal design strategies, as discussed in Remark˜4.4. This could significantly improve the multiplicative constants in the regret, leading to more efficient algorithms.

Acknowledgements

We used generative AI tools when preparing the manuscript; we remain responsible for all opinions, findings, and conclusions or recommendations expressed in the paper. This paper is based on research supported by the National Science Foundation under grants 2027737, 2113373, and 2414918.

References

- Ban & Keskin (2021) Gah-Yi Ban and N Bora Keskin. Personalized dynamic pricing with machine learning: High-dimensional features and heterogeneous elasticity. Management Science, 67(9):5549–5568, 2021.

- Besbes & Zeevi (2009) Omar Besbes and Assaf Zeevi. Dynamic pricing without knowing the demand function: Risk bounds and near-optimal algorithms. Operations research, 57(6):1407–1420, 2009.

- Bracale et al. (2024) Daniele Bracale, Subha Maity, Moulinath Banerjee, and Yuekai Sun. Learning the distribution map in reverse causal performative prediction. arXiv preprint arXiv:2405.15172, 2024.

- Cesa-Bianchi et al. (2019) Nicolo Cesa-Bianchi, Tommaso Cesari, and Vianney Perchet. Dynamic pricing with finitely many unknown valuations. In Algorithmic Learning Theory, pp. 247–273. PMLR, 2019.

- Cheung et al. (2017) Wang Chi Cheung, David Simchi-Levi, and He Wang. Dynamic pricing and demand learning with limited price experimentation. Operations Research, 65(6):1722–1731, 2017.

- Den Boer (2015) Arnoud V Den Boer. Dynamic pricing and learning: historical origins, current research, and new directions. Surveys in operations research and management science, 20(1):1–18, 2015.

- den Boer & Keskin (2020) Arnoud V den Boer and N Bora Keskin. Discontinuous demand functions: Estimation and pricing. Management Science, 66(10):4516–4534, 2020.

- Fan et al. (2021) Jianqing Fan, Yongyi Guo, and Mengxin Yu. Policy optimization using semiparametric models for dynamic pricing. arXiv preprint arXiv:2109.06368, 2021.

- Golrezaei et al. (2019) Negin Golrezaei, Adel Javanmard, and Vahab Mirrokni. Dynamic incentive-aware learning: Robust pricing in contextual auctions. Advances in Neural Information Processing Systems, 32, 2019.

- Grotzinger & Witzgall (1984) Stephen J Grotzinger and Christoph Witzgall. Projections onto order simplexes. Applied mathematics and Optimization, 12(1):247–270, 1984.

- Javanmard & Nazerzadeh (2019) Adel Javanmard and Hamid Nazerzadeh. Dynamic pricing in high-dimensions. Journal of Machine Learning Research, 20(9):1–49, 2019.

- Keskin & Zeevi (2014) N Bora Keskin and Assaf Zeevi. Dynamic pricing with an unknown demand model: Asymptotically optimal semi-myopic policies. Operations research, 62(5):1142–1167, 2014.

- Kumar et al. (2018) Subodha Kumar, Vijay Mookerjee, and Abhinav Shubham. Research in operations management and information systems interface. Production and Operations Management, 27(11):1893–1905, 2018.

- Luo et al. (2022) Yiyun Luo, Will Wei Sun, and Yufeng Liu. Contextual dynamic pricing with unknown noise: Explore-then-ucb strategy and improved regrets. Advances in Neural Information Processing Systems, 35:37445–37457, 2022.

- Luo et al. (2024) Yiyun Luo, Will Wei Sun, and Yufeng Liu. Distribution-free contextual dynamic pricing. Mathematics of Operations Research, 49(1):599–618, 2024.

- Miao et al. (2019) Sentao Miao, Xi Chen, Xiuli Chao, Jiaxi Liu, and Yidong Zhang. Context-based dynamic pricing with online clustering. arXiv preprint arXiv:1902.06199, 2019.

- Mösching & Dümbgen (2020) Alexandre Mösching and Lutz Dümbgen. Monotone least squares and isotonic quantiles. 2020.

- Müller (1984) Hans-Georg Müller. Optimal designs for nonparametric kernel regression. Statistics & Probability Letters, 2(5):285–290, 1984.

- Robertson et al. (1988) Tim Robertson, Richard Dykstra, and FT Wright. Order restricted statistical inference. (No Title), 1988.

- Tibshirani et al. (2011) Ryan J Tibshirani, Holger Hoefling, and Robert Tibshirani. Nearly-isotonic regression. Technometrics, 53(1):54–61, 2011.

- Tullii et al. (2024) Matilde Tullii, Solenne Gaucher, Nadav Merlis, and Vianney Perchet. Improved algorithms for contextual dynamic pricing. arXiv preprint arXiv:2406.11316, 2024.

- Xu & Wang (2022) Jianyu Xu and Yu-Xiang Wang. Towards agnostic feature-based dynamic pricing: Linear policies vs linear valuation with unknown noise. In International Conference on Artificial Intelligence and Statistics, pp. 9643–9662. PMLR, 2022.

- Zhao & Yao (2012) Zhibiao Zhao and Weixin Yao. Sequential design for nonparametric inference. Canadian Journal of Statistics, 40(2):362–377, 2012.

Appendix A Missing Proofs

A.1 Proof of Proposition˜4.6

Proof.

By Remark˜4.5 we have , from which we note that is non-increasing, because is non-increasing. Moreover if is -Hölder,

and

where in the last inequality we used Cauchy-Scwartz and that . ∎

A.2 Proof of Theorem˜4.8

Lemma A.1.

Let

and

Then for any constant ,

Proof.

First, the by Hoeffding’s inequality, since are independent random variables taking values with mean , for every we have

Note that is the maximum of the quantities

Consequently,

for arbitrary . But the right hand side converges to zero as if for some . ∎

Before proceeding with the technical Lemma˜A.2, let’s define

and the Lebesgue measure, and denote by the empirical measure of the design points , that means

Lemma A.2.

Let i.i.d. points with density that satisfies for some universal constant (which is the case for the uniform distribution), then for a given constant , and for any , there exists and a sequence , such that

where is the event

Proof.

This is immediately derived from the proof of the more general result by Mösching & Dümbgen (2020, Section 4.3) which can be stated as follows: let such that while (as ). Then for every , there exists and , such that

where is the probability measure of the design points , that is

and

where . The value is the smallest integer that satisfies . ∎

Now we prove Theorem˜4.8.

Proof.

Let be sufficiently large so that and such that the event in Lemma˜A.2 occurs. Since is the uniform distribution, the value defined in Lemma˜A.2 corresponds to . For the indices

are well-defined, because is a subinterval of of length . Note that by Lemma˜A.2 this interval contains at least one observation . Moreover,

where is defined as in Lemma˜A.2. Consequently, with as in Lemma˜A.1, we have

In the first step, we used antitonicity of , and in the second last step we used antitonicity of , and the last step utilizes that by ˜4.7. But on the event , the previous considerations implies that

where , and we recall that and is any real value strictly greater than . But happens in which has probability

where we used that by Lemma˜A.1, for any fixed we have and by Lemma˜A.2 for any we have . The last two inequalities come from choosing sufficiently large.

Analogously one can show that on ,

with the same constant and with the same probability tail. ∎

A.3 Proof of Theorem˜4.10

Fix and define and and . Let and . For the exploration phase . Now fix

| (9) |

where for , .

Lemma A.3.

If Assumptions in Theorem˜4.10 hold, for sufficiently large we have for with .

Let for be sufficiently large as in Lemma˜A.3. Summing up for all , yields that

Merging with the exploration phase of episode we get

Using that for to be determined such that they minimize the total regret, and that we get that the RHS of the last inequality is

The exponents of the factor are , and . As the second exponent is always negative we equalize the first and the third exponent, i.e. to get . The exponents of the exponential factor are , and . Equalizing the first two factors, we get , however for , is equal for and less for . Then for we equalizing the first and last factors, obtaining to get .

Case . The expected regret in episode , is upper bounded by

where we used that for . Putting together the phases we get

where we used that .

Case . The expected retreat in episode , , is upper bounded by

where we used that for . Putting together the phases we get

where we used that , which concludes the proof.

A.4 Proof of Lemma˜A.3

Let and and . Define the event where we recall

as defined in Lemma˜4.3, and

Recall that

and define , where by definition in Remark˜4.5

Now let for some . We can write

Analyzing the :

By Lemma˜4.3 we have .

Analyzing the :

is less or equal than two times

| (10) |

Analyzing on : Define the event , where . For sufficiently large, by Theorem˜4.8 we have that

where we chose .

Analyzing on : By Proposition˜4.6, is -Hölder, then .

Analyzing on : By Proposition˜4.6 we have .

Combining the terms and from Equation˜10: we get

Appendix B Additional Plots of Section˜5.1