Algorithms with Calibrated Machine Learning Predictions

Abstract

The field of algorithms with predictions incorporates machine learning advice in the design of online algorithms to improve real-world performance. While this theoretical framework often assumes uniform reliability across all predictions, modern machine learning models can now provide instance-level uncertainty estimates. In this paper, we propose calibration as a principled and practical tool to bridge this gap, demonstrating the benefits of calibrated advice through two case studies: the ski rental and online job scheduling problems. For ski rental, we design an algorithm that achieves optimal prediction-dependent performance and prove that, in high-variance settings, calibrated advice offers more effective guidance than alternative methods for uncertainty quantification. For job scheduling, we demonstrate that using a calibrated predictor leads to significant performance improvements over existing methods. Evaluations on real-world data validate our theoretical findings, highlighting the practical impact of calibration for algorithms with predictions.

1 Introduction

In recent years, advances in machine learning (ML) models have inspired researchers to revisit the design of classic online algorithms, incorporating insights from ML-based advice to improve decision-making in real-world environments. This research area, termed algorithms with predictions, seeks to design algorithms that are both robust to worst-case inputs and achieve performance that improves with prediction accuracy (a desideratum termed consistency) (Lykouris and Vassilvitskii, 2018). Many prediction-aided algorithms have been developed for online decision-making tasks ranging from rent-or-buy problems like ski rental (Purohit et al., 2018, Anand et al., 2020, Sun et al., 2024) to sequencing problems like job scheduling (Cho et al., 2022).

Algorithms in this framework often rely on global uncertainty parameters intended to summarize the trustworthiness of all of the model’s predictions, with extreme settings indicating that predictions are either all perfect or all uninformative (e.g., Mahdian et al., 2007, Lykouris and Vassilvitskii, 2018, Purohit et al., 2018, Rohatgi, 2020, Wei and Zhang, 2020, Antoniadis et al., 2020). However, ML models often produce local, input-specific uncertainty estimates, exposing a disconnect between theory and practice. For instance, many neural networks provide calibrated probabilities or confidence intervals for each data point. In this paper, we demonstrate that calibration can serve as a powerful tool to bridge this gap. An ML predictor is said to be calibrated if the probabilities it assigns to events match their observed frequencies; when the model outputs a high probability, the event is indeed likely, and when it assigns a low probability, the event rarely occurs. Calibrated predictors convey their uncertainty on each prediction, allowing decision-makers to safely rely on the model’s advice, and eliminating the need for global uncertainty estimates. Moreover, calibrating models after training can be easily achieved through popular methods (e.g. Platt Scaling (Platt et al., 1999) or Histogram Binning (Zadrozny and Elkan, 2001)) and reduces overconfidence, particularly in neural network models (Vasilev and D’yakonov, 2023).

Although we are the first to study calibration for algorithms with predictions, Sun et al. (2024) proposed using conformal prediction in this setting—a common tool in uncertainty quantification (Vovk et al., 2005, Shafer and Vovk, 2008). Conformal predictions provide instance-specific confidence intervals that cover the true label with high probability. We prove that calibration offers key advantages over conformal prediction, especially when the predicted quantities have high variance. In extreme cases, conformal intervals can become too wide to be informative: for binary predictions, a conformal approach returns unless the true label is nearly certain to be or . In contrast, calibration still conveys information that aids decision-making.

1.1 Our contributions

We demonstrate the benefit of using calibrated predictors through two case studies: the ski rental and online job scheduling problems. Theoretically, we develop and give performance guarantees for algorithms that incorporate calibrated predictions. We validate our theoretical findings with strong empirical results on real-world data, highlighting the practical benefits of our approach.

Ski rental.

The ski rental problem serves as a prototypical example of a broad family of online rent-or-buy problems, where one must choose between an inexpensive, short-term option (renting) and a more costly, long-term option (buying). In this problem, a skier will ski for an unknown number of days and, each day, must decide to either rent skis or pay a one-time cost to buy them. Generalizations of the ski rental problem have informed a broad array of practical applications in networking (Karlin et al., 2001), caching (Karlin et al., 1988), and cloud computing (Khanafer et al., 2013). We design an online algorithm for ski rental that incorporates predictions from a calibrated predictor. We prove that our algorithm achieves optimal expected prediction-level performance for general distributions over instances and calibrated predictors. At a distribution level, its performance degrades smoothly as a function of the mean-squared error and calibration error of the predictor. Moreover, we demonstrate that calibrated predictions can be more informative than the conformal predictions of Sun et al. (2024) when the distribution over instances has high variance that is not explained by features, leading to better performance.

Scheduling.

We next study online scheduling in a setting where each job has an urgency level, but only a machine-learned estimate of that urgency is available. This framework is motivated by scenarios such as medical diagnostics, where machine-learning tools can flag potentially urgent cases but cannot fully replace human experts. We demonstrate that using a calibrated predictor provides significantly better guarantees than prior work (Cho et al., 2022), which approached this problem by ordering jobs based on the outputs of a binary predictor. We identify that this method implicitly relies on a crude form of calibration that assigns only two distinct values, resulting in many ties that must be broken randomly. In contrast, we prove that a properly calibrated predictor with finer-grained confidence levels provides a more nuanced job ordering, rigorously quantifying the resulting performance gains.

1.2 Related work

Algorithms with predictions.

There has been significant recent interest in integrating ML advice into the design of online algorithms (see, e.g., Mitzenmacher and Vassilvitskii (2022) for a survey). Much of the research in this area assumes uniform uncertainty over prediction reliability (e.g., Lykouris and Vassilvitskii, 2018, Purohit et al., 2018, Wei and Zhang, 2020). Subsequent work has studied more practical settings, assuming access to ML predictors learned from samples (Anand et al., 2020), with probabilistic correctness guarantees (Gupta and Ramdas, 2021), or in the case of binary predictions, with a known confusion matrix (Cho et al., 2022). Recently, Sun et al. (2024) proposed a framework for quantifying prediction-level uncertainty based on conformal prediction. We prove that calibration provides key advantages over conformal prediction in this context, particularly when predicted quantities exhibit high variance.

Calibration for decision-making.

A recent line of work examines calibration as a tool for downstream decision-making. Gopalan et al. (2023) show that a multi-calibrated predictor can be used to optimize any convex, Lipschitz loss function of an action and binary label. Zhao et al. (2021) adapt the required calibration guarantees to specific offline decision-making tasks, while Noarov et al. (2023) extend this algorithmic framework to the online adversarial setting. Though closely related to our work, these results do not extend to the (often unwieldy) loss functions encountered in competitive analysis.

2 Preliminaries

For clarity, we follow the convention that capital letters (e.g., ) denote random variables and lowercase letters denote realizations of random variables (e.g., the event ).

Prediction-aided algorithm design.

With each algorithmic task, we associate a set of possible instances, a set of features for those instances, and a joint distribution over . Given a target function that provides information about each instance, we assume access to a predictor that has been trained to predict the target over . Let denote the range of .

If is the cost incurred by algorithm with prediction on instance , and is that of the offline optimal solution, the goal is to minimize the expected competitive ratio (CR) defined multiplicatively as

or additively as

(that is, the performance of relative to OPT over ). When , , and the CR type (multiplicative or additive) are clear from context, we denote the expected competitive ratio as . This measure is consistent with prior work on training predictors from samples for algorithms with predictions (Anand et al., 2020).

Calibration.

An ML model is said to be calibrated if its predictions are, on average, correct. Formally,

Definition 2.1.

A predictor with target is calibrated over if

When , the equivalent condition is , i.e., directly represents the probability that . Achieving perfect calibration is difficult, so in practice we aim to minimize calibration error, such as the max calibration error, which measures the largest deviation from perfect calibration for any prediction.

Definition 2.2.

The max calibration error of a predictor with target over is

3 Ski Rental

In this section, we analyze calibration as a tool for uncertainty quantification in the classic online ski rental problem. All omitted proofs in this section are in Appendix A.

3.1 Setup

Problem.

A skier plans to ski for an unknown number of days and has two options: buy skis at a one-time cost of dollars or rent them for dollar per day. The goal is to determine how many days to rent before buying, minimizing the total cost. If were known a priori, the optimal policy would rent for days when and buy immediately otherwise, costing . Without knowledge of , competitive ratios of 2 (Karlin et al., 1988) and (Karlin et al., 1994) are tight for deterministic and random strategies, respectively. For convenience, we study a continuous variant of this problem where as in prior work (Anand et al., 2020, Sun et al., 2024).

Predictions.

Let be a set of skier features, be the set of possible days skied, and be an unknown distribution over feature/duration pairs . Motivated by the form of the optimal offline algorithm, we analyze a calibrated predictor for the target , indicating if the skier will ski for more than days. For , a prediction of (respectively, ) means (respectively, ) with high certainty.

Prediction-aided ski rental.

A deterministic prediction-aided algorithm for ski rental takes as input a prediction and returns a recommendation: “rent skis for days before buying.” The cost of following this policy when skiing for days is

Our goal is to select that minimizes the multiplicative expected CR, denoted .

3.2 Ski rental with calibrated predictions

In Algorithm 1, we introduce a deterministic policy for ski rental based on calibrated predictions. To avoid following bad advice, the algorithm defaults to a worst-case strategy of renting for days unless the prediction is confident that the skier will ski for at least days. In this second case, the algorithm smoothly interpolates between a strategy that rents for days and one that rents for days, where is a bound on local calibration error that hedges against greedily following predictions.

Theorem 3.1.

Given a predictor with mean-squared error and max calibration error , Algorithm 1 achieves

As the predictor becomes more accurate (i.e., both and decrease), the algorithm’s expected CR approaches 1. The rest of this subsection will build to a proof of Theorem 3.1.

Prediction-level analysis.

We begin by upper bounding . Let be the event that predicts and be the event that the number of days skied is more than . Then

| (1) | ||||

Lemma 3.2 bounds each of the quantities from Equation 1.

| Condition | ||

|---|---|---|

Lemma 3.2.

Given a predictor with max calibration error , for all ,

-

1.

-

2.

-

3.

-

4.

.

Proof sketch.

(1) and (2) follow from the fact that predicts with max calibration error . Under , one of conditions (iii) or (iv) from Table 1 hold. In either case, . Under , one of conditions (i) or (ii) hold. for (i). For (ii),

∎

Applying all four bounds to Equation 1 yields

| (2) |

The renting strategy from Algorithm 1 is the minimizer of the upper bound in Equation 2.

Theorem 3.3.

Given a predictor with max calibration error , for any prediction , Algorithm 1 achieves

Proof sketch.

Given a prediction , Algorithm 1 rents for days where

Evaluating the right-hand-side of Equation 2 at gives

The fact that for and for completes the proof. ∎

Moreover, no deterministic prediction-aided algorithm for ski rental can outperform Algorithm 1 for general distributions and calibrated predictors . The construction is non-trivial, so we refer the reader to the proof in Appendix A.

Theorem 3.4.

For all renting strategies , predictions and , there exists a distribution and a calibrated predictor such that

Global analysis.

In extracting a global bound from the conditional guarantee in Theorem 3.3, we encounter a term that is an upper bound on the variance of the conditional distribution . Lemma 3.5 relates this quantity to error statistics of .

Lemma 3.5.

If has mean-squared error and max calibration error , then

Finally, we prove this section’s main theorem.

Proof of Theorem 3.1.

By the tower property of conditional expectation,

Applying Theorem 3.3 yields

Recall that for random variables . Furthermore, the function is concave over the unit interval, so by Jensen’s inequality

Finally, observe that

We apply Lemma 3.5 to bound . ∎

3.3 Comparison to previous work

It is well known that for , any -consistent algorithm for deterministic ski rental must be at least -robust (Wei and Zhang, 2020, Angelopoulos et al., 2020, Gollapudi and Panigrahi, 2019). While Algorithm 1 is subject to this trade-off in the worst case, calibration provides sufficient information to hedge against adversarial inputs in expectation, leading to substantial improvements in average-case performance. Indeed, it can be seen from the bound in Theorem 3.3 that Algorithm 1 is 1-consistent and always satisfies when advice is calibrated.

We are not the first to explore uncertainty quantified predictions for ski rental. Sun et al. (2024) take an orthogonal approach based on conformal prediction. Their method, Algorithm 2, assumes access to a probabilistic interval predictor . outputs an interval containing the true number of days skied with probability at least . Interval predictions are especially useful when the uncertainty and returned interval width are both small. However, as features become less informative, the width of prediction intervals must increase to maintain the same confidence level. This can result in intervals that are too wide to provide meaningful insight into the true number of days skied. Lemma 3.6 and Theorem 3.7 demonstrate that there are infinite families of distributions for which calibrated predictions are more informative than conformal predictions for ski rental.

Lemma 3.6.

For all , there exists an infinite family of input distributions for which Algorithm 2 defaults to a worst-case break-even strategy for all interval predictors with uncertainty .

Proof sketch.

The construction places mass on some day and mass on . Any with must output an interval containing both and . Moreover, and by construction. ∎

Theorem 3.7.

For all , all instantiations of Algorithm 2 using PIPs with uncertainty , and all distributions from Lemma 3.6, if is a predictor with mean-squared error and max calibration error satisfying , then .

Proof sketch.

For the distributions in Lemma 3.6, the number of days skied is greater than with probability . Thus, the expected competitive ratio of the break-even strategy is The result follows from the bound on given in Theorem 3.1. ∎

4 Online Job Scheduling

In this section, we explore the role of calibration in a model for scheduling with predictions first proposed by Cho et al. (2022) to direct human review of ML-flagged abnormalities in diagnostic radiology. Omitted proofs from this section can be found in Appendix B.

4.1 Setup

Problem.

There is a single machine (lab tech) that needs to process jobs (diagnostic images), each requiring one unit of processing time. Job has some unknown priority that is independently high with probability and low with probability . Although job priorities are unknown a priori, the priority is revealed after completing some fixed fraction of job . Upon learning , a scheduling algorithm can choose to complete job , or switch to a new job and “store” job for completion at a later time. The goal is to schedule the jobs in a way that minimizes the weighted sum of completion times where is the completion time of job , and are costs associated with delaying a job of each priority for one unit of time. In hindsight, it is optimal to schedule jobs in decreasing order of priority.

ML predictions.

Based on the assumption that the jobs to be scheduled are iid, let be a set of job features, be the set of possible priorities, and be an unknown joint distribution over feature/priority pairs. The prediction task for this problem involves training a predictor whose target is the true priority of each job . This amounts to training a 1-dimensional predictor that acts on the jobs independently:

Prediction-aided scheduling.

Cho et al. (2022) introduce a threshold-based scheduling rule informed by probabilities that job is high priority based on identifying features (Algorithm 3). Their algorithm switches between two extremes—a preemptive policy that starts a new job whenever the current job is revealed to be low priority, and a non-preemptive policy that completes any job once it is begun—based on the threshold parameter

In detail, jobs are opened in decreasing order of . Jobs with are processed preemptively, and the remaining jobs are processed non-preemptively.

A prediction-aided algorithm for job scheduling determines the probabilities from ML advice. Cho et al. (2022) assume access to a binary predictor of job priority and study the case where . These probabilities can be computed using Bayes’ rule, and because is binary, this procedure effectively assigns each job one of two probabilities. Although not explicitly discussed by Cho et al. (2022), this amounts to a basic form of post-hoc calibration. In contrast, our results extend to arbitrary calibrated predictors —a more general framework that calls for new mathematical techniques—allowing us to significantly improve upon their results. In this setting, takes the predictions as input and executes Algorithm 3 with probabilities .

To quantify the optimality gap of , Cho et al. (2022) note that compared to OPT, Algorithm 3 incurs (1) a cost of for each inversion, or pair of jobs whose true priorities are out of order, and (2) a cost of for each pair of low priority jobs encountered when acting preemptively. When acting non-preemptively, Algorithm 3 incurs (3) a cost of for each inversion. Thus, for fixed predictions and true job priorities ,

| (3) |

where and count occurrences of (1), (2), and (3), respectively (see Table 2 for details).

| Quantity | Description | Relevant setting |

|---|---|---|

| Number of jobs likely to be high priority. | — | |

| Number of inversions among jobs likely to be high priority. | Preemptive | |

| Number of low-priority job pairs among jobs likely to be high priority. | Preemptive | |

| Number of inversions among job pairs where at least one is likely to be low priority. | Non-preemptive |

4.2 Scheduling with calibrated predictions

Calibration and job sequencing.

To build intuition for why finer-grained calibrated predictors sequence jobs more accurately, we begin by observing that Algorithm 3 orders jobs with the same probability randomly. Given a calibrated predictor , consider the coarse calibrated predictor

obtained by averaging the predictions of above and below the threshold . Whereas may be large, is only capable of outputting values. As a result, when ordering jobs with features according to predictions from , all jobs with will be sequenced before jobs with , but the ordering of jobs within these bins will be random. In contrast, predictions from provide a more informative ordering of jobs (Figure 1). Note, however, that when has no variance in its predictions above or below the threshold . We demonstrate in Theorem 4.3 that this intuition holds in general — improvements scale with the granularity of predictions.

Performance analysis.

Building off of Equation (3), we bound the expected competitive ratio by bounding each of , , and . The dependence on the ordering of predictions from in these random counts means our analysis heavily involves functions of order statistics. For example, considering the shared summand of and ,

for the function . Similarly, the analysis for the summand of yields for . Based on this, our high-level strategy is to relate “ordered” expectations of the form

to their “unordered” counterparts

which are simple to compute. Lemma 4.1 shows that the ordered and unordered expectations are, in fact, equivalent when the function satisfies .

Lemma 4.1.

Let be iid random variables with order statistics . For any symmetric function ,

This result is sufficient to compute the expectation of exactly. For the other counts, the analysis is more technical as is not symmetric. Lemma 4.2 characterizes the relationship between the ordered and unordered expectations for the function .

Lemma 4.2.

Let be iid samples from a distribution over the unit interval with order statistics . Then,

Proof sketch.

With careful conditioning to deal with random summation bounds, we apply Lemma 4.2 to bound the expectations of and , giving this section’s main theorem. Of note, Theorem 4.3 says that the expected number of inversions of high and low priority jobs decreases with predictor granularity, measured by and . For the method from Cho et al. (2022), and the inequalities are tight.

Theorem 4.3.

Let be calibrated, with , ,

Then

-

1.

-

2.

-

3.

Remark 4.4.

is 1-consistent: when .

5 Experiments

We now evaluate our algorithms on two real-world datasets, demonstrating the utility of using calibrated predictions. See Appendix C for additional details about our datasets and model training, as well a broader collection of results for different ML models and parameter settings.

5.1 Ski rental: Citi Bike rentals

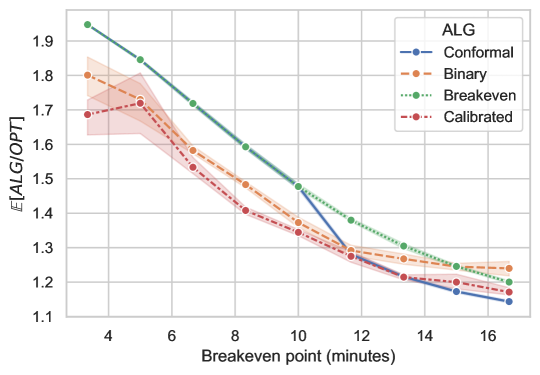

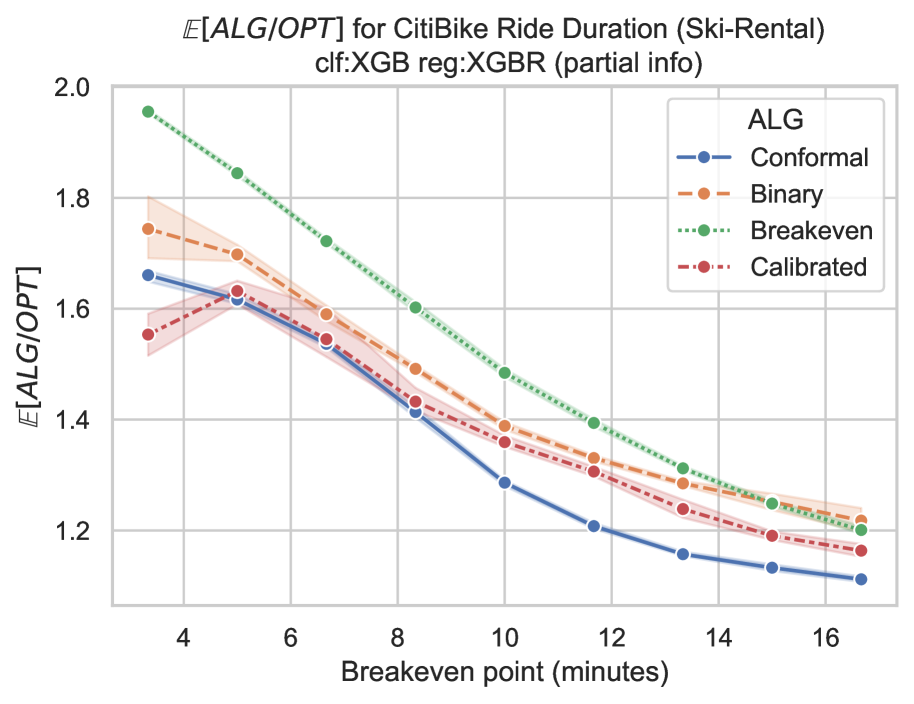

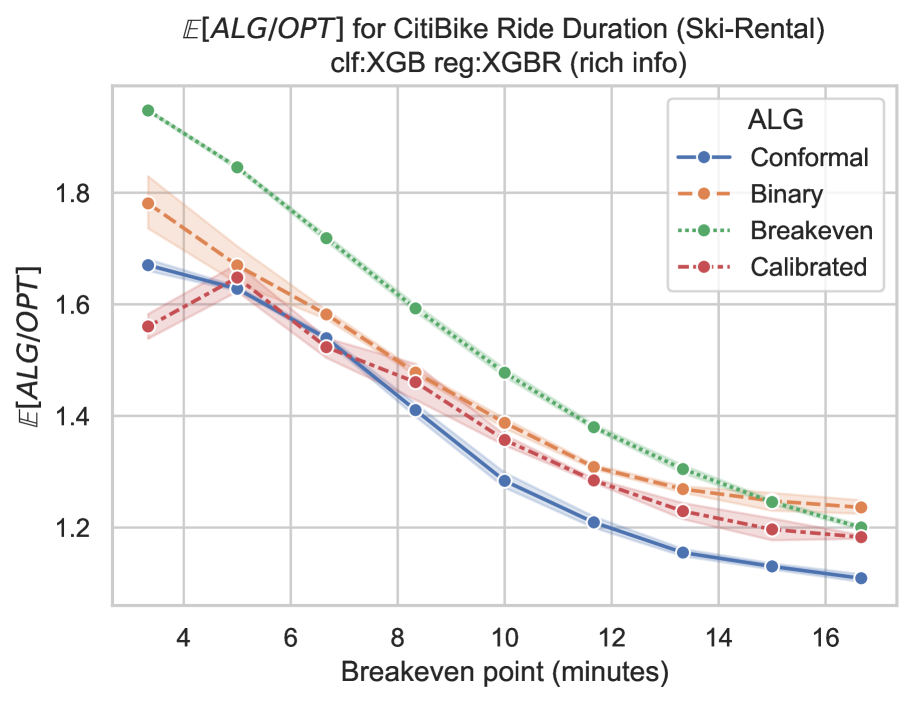

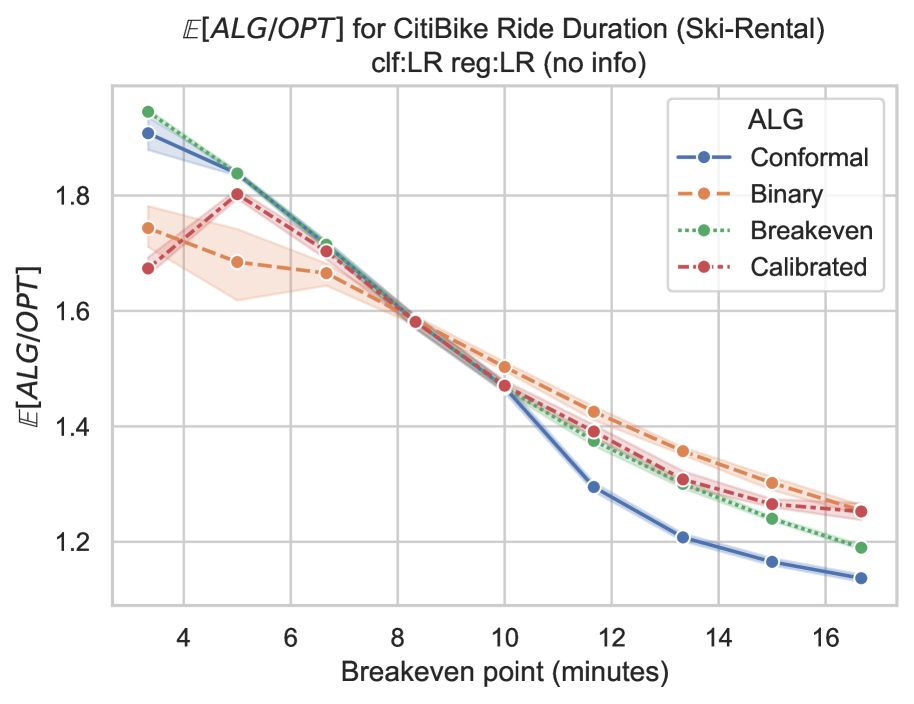

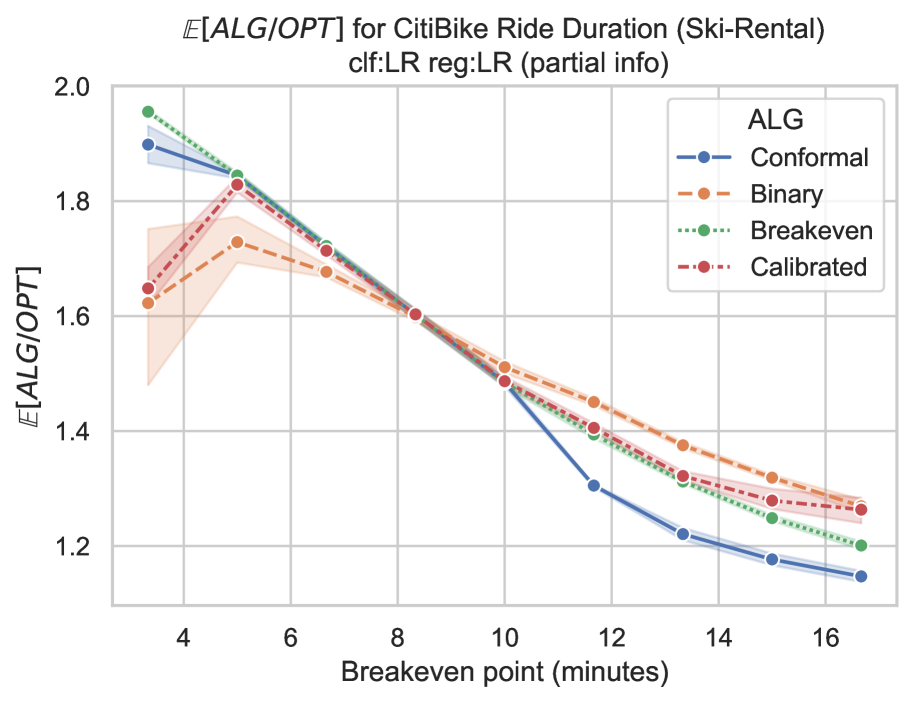

To model the rent-or-buy scenario in the ski rental problem, we use publicly available Citi Bike usage data.111Monthly usage data is publicly available at https://citibikenyc.com/system-data.. This dataset has been used for forecasting (Wang, 2016), system balancing (O’Mahony and Shmoys, 2015), and transportation policy (Lei and Ozbay, 2021), but to the best of our knowledge, this is its first use for ski rental. In this context, a Citi Bike user can choose one of two options: pay by ride duration (rent) or purchase a day pass (buy). If the user plans to ride for longer than the break-even point of minutes, it is cheaper to buy a day pass than to pay by trip duration.222The day pass is designed to be more economical for multiple unlocks of a bike (e.g., minutes for 1 unlock). However, ride data is anonymous, so we cannot track daily usage. We use single-ride durations to approximate the rent vs. buy trade-off for a spectrum of break-even points . The distribution over ride durations can be seen in Appendix C.

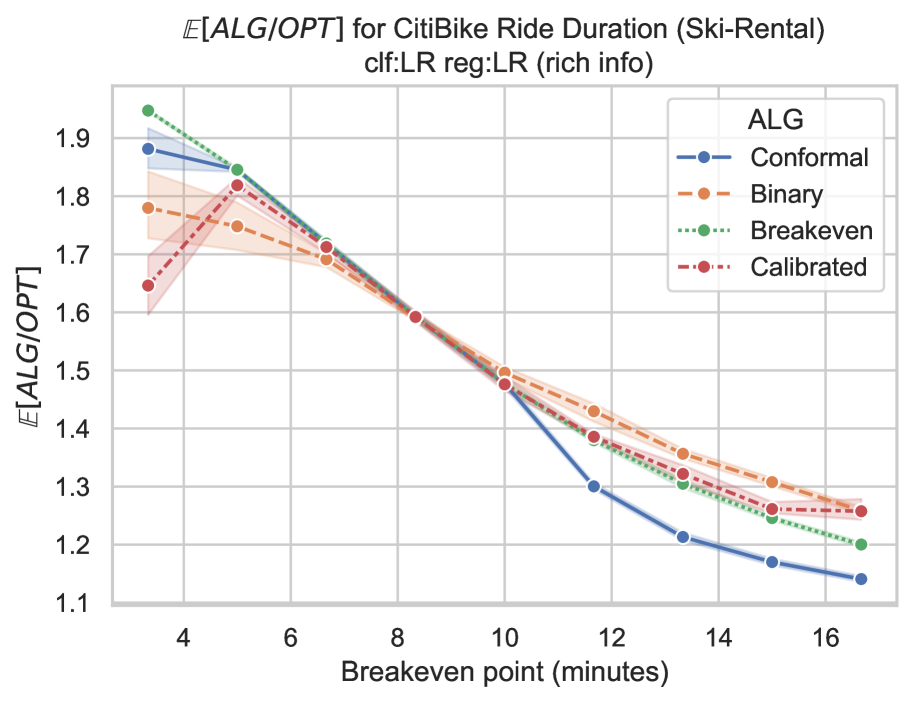

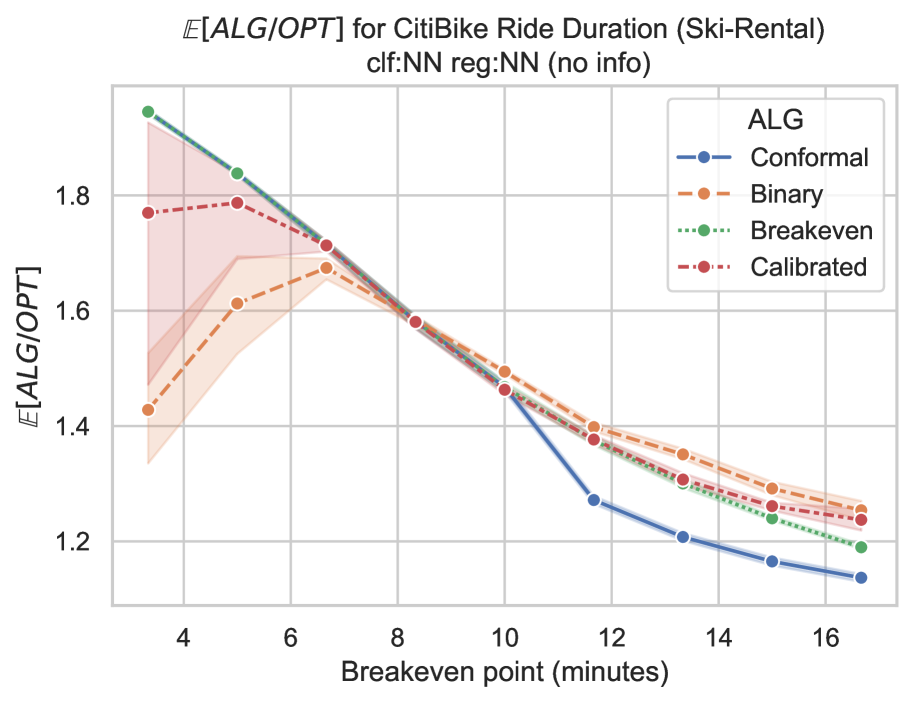

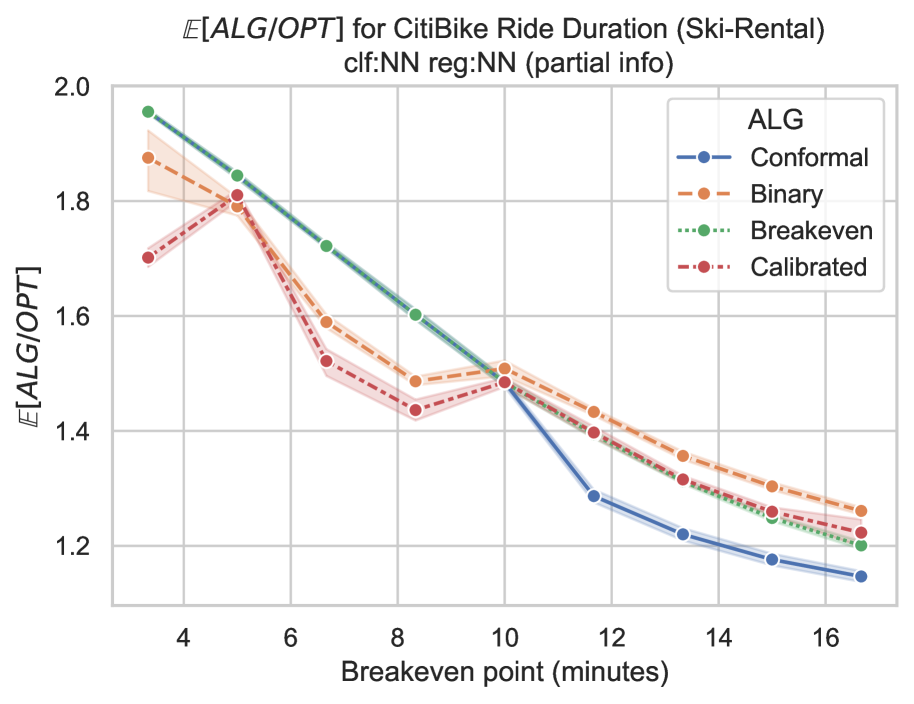

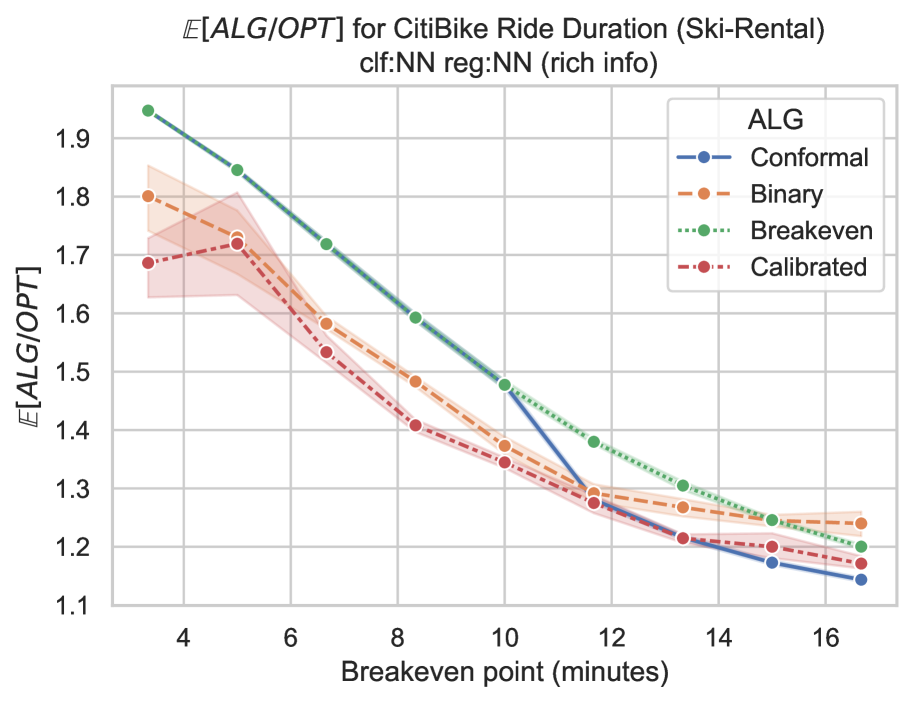

We analyze the impact of advice from multiple predictor families, including XGBoost, logistic regression, and small multi-layer perceptrons (MLP). Each predictor has access to available ride features: start time, start location, user age, user gender, user membership, and approximate end station latitude. While these features are not extremely informative, most predictor families are able to achieve AUC and accuracy above 0.8 for . Figure 2 summarizes the expected competitive ratios achieved by our method from Algorithm 1 (Calibrated) and baselines from previous work when given advice from a small neural network. Baselines include the worst-case optimal deterministic algorithm that rents for minutes (Karlin et al., 1988) (Breakeven), the black-box binary predictor ski-rental algorithm by Anand et al. (2020) (Binary), and the PIP algorithm described in Algorithm 2 (Sun et al., 2024) (Conformal). Though each algorithm is aided by predictors from the same family, the actual advice may differ. For example, Conformal assumes access to a regressor that predicts ride duration directly. While performance is distribution-dependent, we see that our calibration-based approach often leads to the most cost-effective rent/buy policy in this scenario.

5.2 Scheduling: sepsis triage

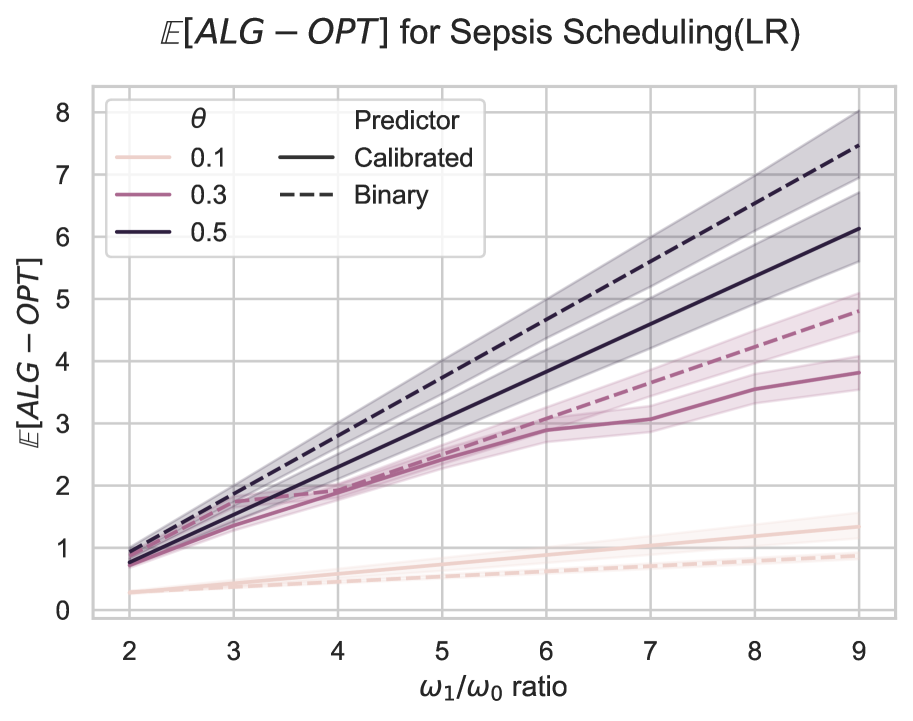

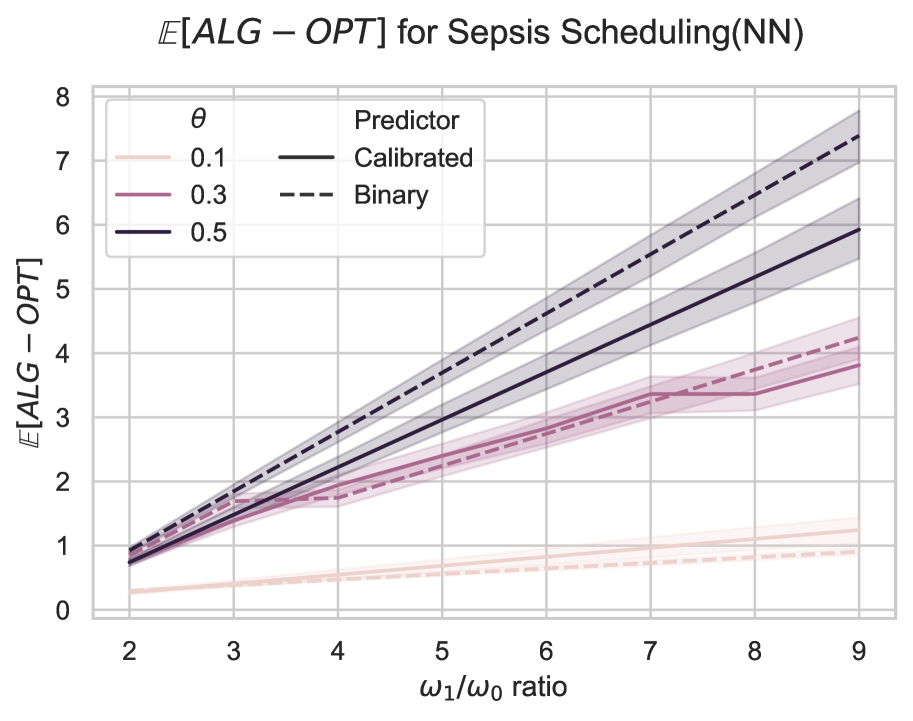

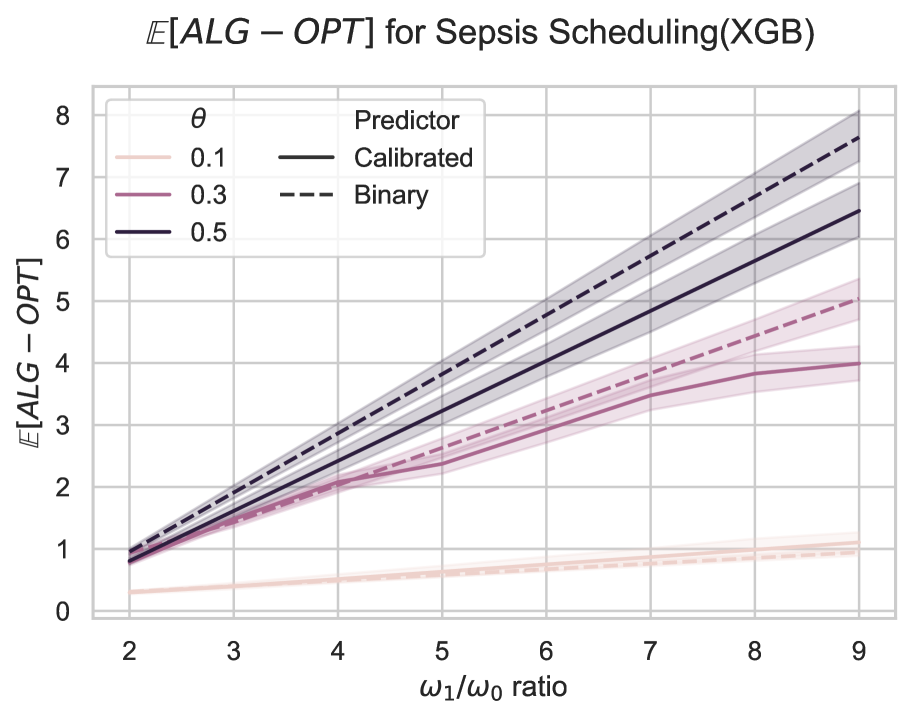

We use a real-world dataset for sepsis prediction to validate our theory results for scheduling with calibrated predictions. Sepsis is a life-threatening response to infection that typically appears after hospital admission (Singer et al., 2016). Many works have studied using machine learning to predict the onset of sepsis, as every hour of delayed treatment is associated with a 4-8% increase in mortality (Kumar et al., 2006, Reyna et al., 2020); existing works aim to better predict sepsis to treat high-priority patients earlier. Replicating results from Chicco and Jurman (2020) we train a binary predictor for sepsis onset using logistic regression on a dataset of 110,204 hospital admissions. The base predictor achieves an AUC of 0.86 using age, sex, and septic episodes as features. We then calibrate this predictor using both the naive method from Cho et al. (2022) (Binary) and more nuanced histogram calibration (Zadrozny and Elkan, 2001) (Calibrated). Figure 3 shows the expected competitive ratio (normalized by the number of jobs ) achieved by Algorithm 3 when provided advice from each of these predictors for varying delay costs and information barrier . We see that the more nuanced predictions consistently result in schedules with smaller delay costs.

6 Conclusion

In this paper, we demonstrated that calibration is a powerful tool for algorithms with predictions, bridging the gap between traditional theoretical approaches—which rely on global uncertainty estimates—and modern ML methodologies that offer fine-grained, instance-specific uncertainty quantification. We focused on the ski rental and online scheduling problems, developing online algorithms that exploit local calibration guarantees to achieve strong average-case performance. For both problems, we highlighted settings where our algorithms outperform existing approaches, and we supported these theoretical findings with empirical evidence on real-world datasets. Beyond these two case studies, we believe calibration-based approaches offer broad potential for designing online decision-making algorithms, particularly in scenarios that require balancing worst-case robustness with reliable per-instance predictions.

Acknowledgements

Judy Hanwen Shen is supported by the Simons Foundation Collaboration on the Theory of Algorithmic Fairness, Anders Wikum is supported by a National Defense Science & Engineering Graduate (NDSEG) fellowship, and Ellen Vitercik acknowledges the support of NSF grant CCF-2338226. We thank Bailey Flanigan for stimulating early discussions that inspired us to pursue this research direction, and Ziv Scully for a technical insight in the proof of Lemma 4.2.

References

- Anand et al. (2020) Keerti Anand, Rong Ge, and Debmalya Panigrahi. Customizing ML predictions for online algorithms. In International Conference on Machine Learning (ICML), pages 303–313, 2020.

- Angelopoulos et al. (2020) Spyros Angelopoulos, Christoph Dürr, Shendan Jin, Shahin Kamali, and Marc Renault. Online computation with untrusted advice. In Innovations in Theoretical Computer Science (ITCS), 2020.

- Antoniadis et al. (2020) Antonios Antoniadis, Themis Gouleakis, Pieter Kleer, and Pavel Kolev. Secretary and online matching problems with machine learned advice. In Conference on Neural Information Processing Systems (NeurIPS), 2020.

- Chicco and Jurman (2020) Davide Chicco and Giuseppe Jurman. Survival prediction of patients with sepsis from age, sex, and septic episode number alone. Scientific reports, 10(1):17156, 2020.

- Cho et al. (2022) Woo-Hyung Cho, Shane Henderson, and David Shmoys. Scheduling with predictions. arXiv preprint arXiv:2212.10433, 2022.

- Gollapudi and Panigrahi (2019) Sreenivas Gollapudi and Debmalya Panigrahi. Online algorithms for rent-or-buy with expert advice. In International Conference on Machine Learning (ICML), 2019.

- Gopalan et al. (2023) Parikshit Gopalan, Lunjia Hu, Michael P. Kim, Omer Reingold, and Udi Wieder. Loss minimization through the lens of outcome indistinguishability. In Innovations in Theoretical Computer Science (ITCS), 2023.

- Gupta and Ramdas (2021) Chirag Gupta and Aaditya Ramdas. Distribution-free calibration guarantees for histogram binning without sample splitting. In International Conference on Machine Learning (ICML), 2021.

- Karlin et al. (1988) Anna R. Karlin, Mark S. Manasse, Larry Rudolph, and Daniel D. Sleator. Competitive snoopy caching. Algorithmica, 3(1–4):79–119, 1988.

- Karlin et al. (1994) Anna R. Karlin, Mark S. Manasse, Lyle A. McGeoch, and Susan Owicki. Competitive randomized algorithms for nonuniform problems. Algorithmica, 11(6):542–571, 1994.

- Karlin et al. (2001) Anna R Karlin, Claire Kenyon, and Dana Randall. Dynamic tcp acknowledgement and other stories about e/(e-1). In Proceedings of the Annual Symposium on Theory of Computing (STOC), pages 502–509, 2001.

- Khanafer et al. (2013) Ali Khanafer, Murali Kodialam, and Krishna PN Puttaswamy. The constrained ski-rental problem and its application to online cloud cost optimization. In Proceedings IEEE INFOCOM, pages 1492–1500. IEEE, 2013.

- Kumar et al. (2006) Anand Kumar, Daniel Roberts, Kenneth E Wood, Bruce Light, Joseph E Parrillo, Satendra Sharma, Robert Suppes, Daniel Feinstein, Sergio Zanotti, Leo Taiberg, et al. Duration of hypotension before initiation of effective antimicrobial therapy is the critical determinant of survival in human septic shock. Critical care medicine, 34(6):1589–1596, 2006.

- Lei and Ozbay (2021) Yiyuan Lei and Kaan Ozbay. A robust analysis of the impacts of the stay-at-home policy on taxi and Citi Bike usage: A case study of Manhattan. Transport Policy, 110:487–498, 2021.

- Lykouris and Vassilvitskii (2018) Thodoris Lykouris and Sergei Vassilvitskii. Competitive caching with machine learned advice. In International Conference on Machine Learning (ICML), 2018.

- Mahdian et al. (2007) Mohammad Mahdian, Hamid Nazerzadeh, and Amin Saberi. Allocating online advertisement space with unreliable estimates. In ACM Conference on Economics and Computation (EC), page 288–294, 2007.

- Mitzenmacher and Vassilvitskii (2022) Michael Mitzenmacher and Sergei Vassilvitskii. Algorithms with predictions. Communications of the ACM, 65(7):33–35, 2022.

- Noarov et al. (2023) Georgy Noarov, Ramya Ramalingam, Aaron Roth, and Stephan Xie. High-dimensional prediction for sequential decision making. In Conference on Neural Information Processing Systems (NeurIPS), 2023.

- O’Mahony and Shmoys (2015) Eoin O’Mahony and David Shmoys. Data analysis and optimization for (Citi) bike sharing. In AAAI Conference on Artificial Intelligence, 2015.

- Platt et al. (1999) John Platt et al. Probabilistic outputs for support vector machines and comparisons to regularized likelihood methods. Advances in large margin classifiers, 10(3):61–74, 1999.

- Purohit et al. (2018) Manish Purohit, Zoya Svitkina, and Ravi Kumar. Improving online algorithms via ML predictions. In Conference on Neural Information Processing Systems (NeurIPS), pages 9661–9670, 2018.

- Reyna et al. (2020) Matthew A Reyna, Christopher S Josef, Russell Jeter, Supreeth P Shashikumar, M Brandon Westover, Shamim Nemati, Gari D Clifford, and Ashish Sharma. Early prediction of sepsis from clinical data: the physionet/computing in cardiology challenge 2019. Critical care medicine, 48(2):210–217, 2020.

- Rohatgi (2020) Dhruv Rohatgi. Near-optimal bounds for online caching with machine learned advice. In Annual ACM-SIAM Symposium on Discrete Algorithms (SODA), 2020.

- Shafer and Vovk (2008) Glenn Shafer and Vladimir Vovk. A tutorial on conformal prediction. Journal of Machine Learning Research, 9(3), 2008.

- Singer et al. (2016) Mervyn Singer, Clifford S Deutschman, Christopher Warren Seymour, Manu Shankar-Hari, Djillali Annane, Michael Bauer, Rinaldo Bellomo, Gordon R Bernard, Jean-Daniel Chiche, Craig M Coopersmith, et al. The third international consensus definitions for sepsis and septic shock (sepsis-3). Jama, 315(8):801–810, 2016.

- Sun et al. (2024) Bo Sun, Jerry Huang, Nicolas Christianson, Mohammad Hajiesmaili, Adam Wierman, and Raouf Boutaba. Online algorithms with uncertainty-quantified predictions. In International Conference on Machine Learning (ICML), 2024.

- Vasilev and D’yakonov (2023) Ruslan Vasilev and Alexander D’yakonov. Calibration of neural networks. arXiv preprint arXiv:2303.10761, 2023.

- Vovk et al. (2005) Vladimir Vovk, Alexander Gammerman, and Glenn Shafer. Algorithmic learning in a random world, volume 29. Springer, 2005.

- Wang (2016) Wen Wang. Forecasting Bike Rental Demand Using New York Citi Bike Data. PhD thesis, Technological University Dublin, 2016.

- Wei and Zhang (2020) Alexander Wei and Fred Zhang. Optimal robustness-consistency trade-offs for learning-augmented online algorithms. In Conference on Neural Information Processing Systems (NeurIPS), 2020.

- Zadrozny and Elkan (2001) Bianca Zadrozny and Charles Elkan. Obtaining calibrated probability estimates from decision trees and naive bayesian classifiers. In International Conference on Machine Learning (ICML), pages 609–616, 2001.

- Zhao et al. (2021) Shengjia Zhao, Michael P. Kim, Roshni Sahoo, Tengyu Ma, and Stefano Ermon. Calibrating predictions to decisions: A novel approach to multi-class calibration. In Conference on Neural Information Processing Systems (NeurIPS), 2021.

Appendix A Ski Rental Proofs

See 3.2

Proof.

Recall that is the event that predicts , and is the event that the true number of days skied is at least . Because is a predictor of the indicator function with max calibration error ,

and

This establishes (1) and (2). In the remainder of the proof we will reference the costs from conditions - in Table 1.

-

(3)

. Under the event (), one of conditions or must hold. The bound is tight when condition holds. Under condition , it must be that , so

-

(4)

.

Under the event (, one of conditions or hold. The bound is trivial under condition . Under condition , because and ,

∎

See 3.3

Proof.

Let be the event that predicts , and let be the event that the true number of days skied is at least . By the law of total expectation and Lemma 3.2,

Finding the number of days to rent skis that minimizes this upper bound on competitive ratio amounts to solving two convex optimization problems — one for the case , and a second for — then taking the minimizing solution.

| (a)Minimize | ||||

| s.t. |

Note first that (b) has optimal solution . The Lagrangian of (a) is

with KKT optimality conditions

We’ll proceed by finding solutions to this system of equations via case analysis.

-

1.

. Then, and by complementary slackness. But at least one of the stationarity or dual feasibility constraints are violated, since

-

2.

and . Then, by complementary slackness. Stationarity and dual feasibility are satisfied only when , since in this case

-

3.

and . Then, the first constraint gives that

Recall that , so this constraint is only satisfied when and .

Because is the optimal solution to both (a) and (b) when , it must be the case that if . When , the optimal solution to (a) is and the optimal solution to (b) is . The value of the former is , while the value of the latter is . Taking the argmin yields

which is exactly Algorithm 1 and achieves a competitive ratio of

∎

See 3.4

| Condition | ||

|---|---|---|

Proof.

Let and . The calibrated predictor will deterministically output , while the distribution will depend on whether algorithm buys before or after day .

Case 1: . Define a distribution where in a fraction of the data the true number of days skied is , and in a fraction the number of days skied is , where is sufficiently small that

By construction, condition from Table 3 is satisfied when with

Similarly, condition holds when with

By the law of total expectation,

Some basic calculus yields , and evaluating the lower bound at gives

Case 2: .

Define a distribution where in a fraction of the data the true number of days skied is , and in a fraction the number of days skied is . Condition is satisfied when with . Condition is satisfied when with . By the law of total expectation,

In both cases, is calibrated with respect to since . Moreover, because the cases are exhaustive, at least one of the corresponding lower bounds must hold. It follows immediately that

∎

See 3.5

Proof.

We have from the law of total expectation that

Applying the definition of the local calibration error ,

The observation that gives the result. ∎

See 3.1

Proof.

This result follows from Theorem 3.3, Lemma 3.5, and an application of Jensen’s inequality. To begin,

| (Tower property) | ||||

| (Theorem 3.3) | ||||

with the final line following from the fact that for random variables . Next, we argue from basic composition rules that the function is concave for . The concavity of over its domain follows from the facts that (1) the function is concave and increasing in its argument and (2) is concave. Moreover, is well-defined for all . With concavity established, an application of Jensen’s inequality yields

To finish the proof, we will bound the term within the square root using Lemma 3.5. Notice that

Finally,

| (Lemma 3.5) | ||||

∎

See 3.6

Proof.

Let and consider a distribution that, for each unique feature vector , has a true number of days skied that is either with probability or with probability . By construction, any interval prediction with must satisfy that and . This means , so Algorithm 2 makes a determination of which day to buy based on the relative values of , , and 2. In particular, the algorithm follows the break-even strategy of buying on day when and

It is clear that . Next, recall the definition of .

When , we see that . To handle the case where , we will show that

for all and . Plugging in and noting that implies the desired bound. Toward that end, notice that is increasing in , and so for all we have that

All that is left is to show that . This is straightforward: for ,

and multiplying through by gives the desired inequality. In summary, we’ve shown that , , and for the family of distributions described above. For this particular case, Algorithm 2 rents for days. ∎

See 3.7

Proof.

Let and consider any distribution from the infinite family given in Lemma 3.6. In particular, in any of these distributions, the number of days skied is greater than with probability . Therefore, the expected competitive ratio of the break-even strategy that rents for days before buying is

The result follows from the bound on from Theorem 3.1. ∎

Appendix B Scheduling Proofs

See 4.1

Proof.

Beginning with the facts that

it follows from the symmetry of that

∎

See 4.2

Proof.

We’ll begin by removing a shared term from both sides of the inequality. Notice that

by Lemma 4.1 with . So, it is sufficient to show that

By linearity of expectation, the first term on the left-hand side is equal to . The random variables in the second term are not identically distributed, however, so a different approach is required. We will use a trick to express the sum in terms of the symmetric function , which allows us to remove the dependency on order statistics using Lemma 4.1.

| ( since ) | ||||

| (Lemma 4.1 with ]) |

Thus, the second term on the RHS is equal to . All that is left is to show that

Toward that end, we can write

so . Finally, using the fact that are iid, we have

∎

See 4.3

Proof.

Given jobs to schedule with features and the predictions , let be a random variable that counts the number of samples from with prediction larger than . We’ll begin by computing expectations conditioned on before taking an outer expectation.

| (Tower property) | ||||

| (Definition of ) | ||||

| (Independence) | ||||

| (Calibration) | ||||

Performing the same computation for counts and gives

and

| . |

At this point, we can compute the conditional expectation of directly. By Lemma 4.1 with ,

| (Lemma 4.1) | ||||

| (Independence) | ||||

| (Calibration) | ||||

| (Bayes’ rule) | ||||

The same technique cannot be used to evaluate the expectations of and because the function is not symmetric. Instead, we will provide upper bounds on the conditional expectations using Lemma 4.2, then evaluate the unordered results as before. For the conditional expectation of , we have

| (Lemma 4.2) | ||||

Similarly for the conditional expectation of the second term of

For the first term of , we simply apply the rearrangement inequality in lieu of Lemma 4.2 for unordering, since the sum has the form where is an increasing sequence and is a decreasing sequence.

Next, we take an outer expectation to remove the dependency on . Recall that follows a Binomial distribution, so one can easily verify that

-

1.

-

2.

-

3.

It follows immediately that

where

∎

Appendix C Experimental Details

C.1 Ski-Rental: CitiBike

Our experiments with CitiBike use ridership duration data from June 2015. Although summer months have slightly longer rides, the overall shape of the distributions is similar across months (i.e. left-skewed distribution). Figure 4 illustrates the distribution of scores. This indicates that using this dataset for ski rental, the breakeven strategy will be better as increases since most of the rides will be less than . This is an empirical consideration of running these algorithms that prior works do not consider. Thus, we select values of between and as a reasonable interval for comparison.

Feature Selection

The original CitiBike features include per-trip features including user type, start and end times, location, station, gender, and birth year of the rider. We tested predictors with three types of feature: no information about final destination, partial information about final destination (end latitude only), and rich information about final destination (end longitude and latitude). Even with rich information, the best accuracy of the model’s we consider are around 80% accuracy. This is because there are many factors affecting the ride duration. However with no information about the final destination, many of our models were close to random and thus do not serve as good predictor (Figure 5).

Model Selection

We tested a variety of models for both classification (e.g. linear regression, gradient boosting, XGBoost, k-Nearest Neighbors, Random Forest and a 2-layered Neural Network) and regression (e.g. Linear Regression, Bayesian Ridge Regression, XGBoost Regression, SGD Regressor, and Elastic Net, and 2-layered Neural Network). We ended up choosing three representative predictors of different model classes: regression, boosting, and neural networks. To fairly compare regression with classification we choose similar model classes: (Linear Regression, Logistic Regression), (XGBoost, XGBoost Regression), and two-layer neural networks.

Calibration

To calibrate an out-of-the box model, we tested histogram calibration (Zadrozny and Elkan, 2001), binned calibration (Gupta and Ramdas, 2021), and Platt scaling (Platt et al., 1999). While results from histogram and bin calibration were similar, Platt scaling often produced calibrated probabilities within a very small interval. Though it is implemented in our code, we did not use it. A key intervention we make for calibration is to calibrate according to balanced classes in the validation set when the label distribution is highly skewed. This approach ensures that probabilities are not artificially skewed due to class imbalance.

Regression

For a regression model as a fair comparison, we assume that the regression model also only has access to the 0/1 labels of the binary predictor for each . To use convert the output conformal intervals to be used in the algorithm from Sun et al. (2024), we multiply the 0/1 intervals by .

C.2 Scheduling: Sepsis Triage

Dataset

We use a dataset for sepsis prediction: ‘Sepsis Survival Minimal Clinical Records’. 333https://archive.ics.uci.edu/dataset/827/sepsis+survival+minimal+clinical+records This dataset contains three characteristics: age, sex, and number of sepsis episodes. The target variable for prediction is patient mortality.

Additional Models

We also include results for additional base models: 2 layer perception (Figure 9(b)) and XGBoost (Figure 9(c))