Carefree multiple testing with e-processes

Abstract

E-processes enable hypothesis testing with ongoing data collection while maintaining Type I error control. However, when testing multiple hypotheses simultaneously, current -value based multiple testing methods such as e-BH are not invariant to the order in which data are gathered for the different -processes. This can lead to undesirable situations, e.g., where a hypothesis rejected at time is no longer rejected at time after choosing to gather more data for one or more processes unrelated to that hypothesis. We argue that multiple testing methods should always work with suprema of -processes. We provide an example to illustrate that e-BH does not control this FDR at level when applied to suprema of -processes. We show that adjusters can be used to ensure FDR-sup control with e-BH under arbitrary dependence.

1 Introduction

The -process is a recent innovative conceptual framework for hypothesis testing. An -process is a nonnegative stochastic process , which starts at a value of and is continually updated over time as more information comes in. It does not grow in expectation if the null hypothesis is true, that is, for every stopping time and for every . Therefore, we may reject when, at any time point , we have . Doing so will control Type I error, since, if is true, Ville’s inequality (Ramdas and Wang [2024], Fact 6.4) guarantees that -processes have the property that

| (1) |

In contrast to -values, -processes can be repeatedly evaluated until, hopefully, rejection follows for some . This means that a researcher can continue gathering data as long as they like. Notably, where the definition of -processes involves a stopping time, the Type I error control property (1) involves the supremum of the process. This implies that data gathering is carefree: the researcher never has to regret gathering more data. For example, suppose that the researcher decided to gather before properly evaluating . If but , then they can still reject and appeal to (1) for Type I error control, effectively undoing the gathering of , as long as was fixed a priori (or even if it is not: see Koning [2024], Grünwald [2024]).

If more than one hypothesis is of interest, multiple testing considerations apply. There is by now a large literature on -based multiple testing. Most notably, the e-BH procedure [Wang and Ramdas, 2022] generalizes the Benjamini-Hochberg procedure for controlling the False Discovery Rate (FDR). However, this literature has so far almost exclusively focused on multiple testing with -values, which are single instances of -processes, i.e., random variables for which if is true. When applied to parallel -processes , as we will show below, e-BH guarantees that

| (2) |

Unfortunately, data gathering under the guarantee (2) is not carefree. Let us illustrate this with an example. For -values, e-BH rejects any hypothesis for which the -value exceeds , and both hypotheses if both -values exceed . Now suppose that at time we have and . Gathering more data for both -processes, however, the situation could reverse, and and . Now, the researcher regrets gathering more data for , since (2) does not support any rejection now, but would have supported rejection of both null hypotheses if the researcher would have stopped , taking . The lack of the carefree property hugely complicates experimental design.

For carefree data gathering, the researcher must always be allowed to revert any -process back to an earlier time point. The optimal reversion is to the maximum so far, so a carefree procedure should guarantee

| (3) |

We argue that (3), the FDR-sup, is the proper FDR criterion for -processes. In this paper, we investigate how to construct procedures controlling (3).

2 FDR control with e-processes

2.1 The e-BH procedure

Let be hypotheses, denote the set of their indices with , and let be the true data-generating probability measure. For each , is called true if . Let be the set of indices of true null hypotheses and let be its cardinality. For each , is associated with an -value .

When there is only one observation of the -value for each hypothesis, it has been shown [Wang and Ramdas, 2022] that the classical Benjamini-Hochberg (BH) procedure can be modified to accommodate -values. The most powerful property of this e-BH procedure, is that it provides FDR control for any dependence structure between the -values, in contrast with the classical BH procedure, which requires the assumption of positive regression dependence on a subset (PRDS). Both the classical BH and also the Benjamini-Yekutieli (BY) procedures can be recovered as special cases of the e-BH procedure.

2.2 e-BH with e-processes

Formally, a non-negative process is called an -process when for any stopping time , where the expectation is taken under any distribution in the null hypothesis. For each , let be associated with an e-process , and let be their arbitrary stopping times. Let be the stopped -processes.

Procedure 1 (Naive e-BH with e-processes).

Let for be the -th order statistic of , sorted from the largest to the smallest, such that is the largest stopped -process. The stopped e-BH procedure then rejects hypotheses with the largest stopped -processes, where

Fact 1.

The stopped e-BH procedure applied to arbitrarily dependent e-processes has FDR at most .

Since a stopped -process has expectation under the null bounded by one, i.e. , the set of stopped -processes is a set of -variables. Thus, this procedure reduces to the standard e-BH procedure on the stopped -processes , and the FDR guarantee [Wang and Ramdas, 2022] carries over.

2.3 Related work

Online multiple testing has been considered both classically with -values [Fischer et al., 2024] and -values [Fischer and Ramdas, 2024a, b, Xu and Ramdas, 2023], but online is here to be understood in the dimension of the hypothesis space: time points represent the addition of an hypothesis. The only paper to our knowledge that considers multiple testing with -values where data can be added sequentially, is [Xu and Ramdas, 2023], where they introduce the doubly sequential framework. For -values there is work on interim-analyses and group-sequential multiple testing, e.g. [Sarkar et al., 2019] on FDR; but to the best of our knowledge there is no work on any-time valid methods.

3 FDR with the running maximum of an e-process

We have argued that multiple-testing procedures for -processes should possesses the carefree property that sequential data gathering will not lead to regrets, and that this requires the procedure to work with the running maximum of the -process: .

It is straightforward to observe that in such a procedure, the set of rejected hypotheses forms a non-decreasing set. That is, if a hypothesis is rejected at a given point in time, it will remain rejected in all subsequent time points. It therefore automatically possesses the accept-to-reject property, as introduced in [Fischer and Ramdas, 2024b]: a multiple testing method that can change earlier non-rejections into a rejection at a later point in time, but not the other way around. As noted before, in that work the sequential aspect was in terms of adding hypotheses rather than data points. We argue however that also in the latter context, the accept-to-reject principle is a desirable feature of any multiple testing method.

Procedure 2 (Running maximum e-BH procedure).

Let for be the -th order statistic of , sorted from the largest to the smallest so that is the largest maximum of an -process. The stopped e-BH procedure then rejects hypotheses with the largest maxima of -processes, where

Since the running maximum of an -process is not an -process itself (see Choe and Ramdas [2024] for more on this), we cannot directly deduce FDR control for this procedure. However, in the case that all -processes are independent, it is straightforward to see that this procedure ensures FDR control. This is because, in essence, the inverse of the running maximum of the -processes is a valid -process [Choe and Ramdas, 2024]. Thus, applying this procedure to the running maximum is equivalent to applying the classical BH procedure.

However, in the case of arbitrary dependence between -processes, the e-BH procedure loses its FDR control, as asserted by the following proposition.

Proposition 1.

The running maximum e-BH procedure applied to arbitrarily dependent -processes does not provide FDR control at level .

3.1 Proof of Proposition 1

We present a counterexample that demonstrates how the e-BH procedure, when applied to the running maxima of -processes, fails to control the FDR at the nominal level . The FDR is evaluated numerically.

Consider two true null hypotheses with corresponding -processes and , defined as:

where the initial values are distributed as:

and the increments are distributed as:

The variables , , and all are independent.

It is straightforward to verify that the expected values of and are equal to 1 at all times, i.e., , which ensures that both and are valid -processes. However, the processes and are not independent because the random variables and , as well as , , are dependent.

Since the null hypotheses are true, the FDR-sup is equal to the probability of rejecting at least one of them. This corresponds to the event:

where as above. To confirm the validity of this example, we performed simulations of the described e-processes (the code is provided in the Appendix B).

The results of the simulations show that, in this scenario, the FDR of the e-BH procedure applied to the running maxima is approximately . In our simulations, we used Monte Carlo iterations. Therefore, based on the standard error formula , the estimated standard deviation of the error is approximately . This demonstrates that when using running maxima, additional corrections or normalizations are necessary to ensure proper FDR control.

4 Adjusting running maxima

Since Proposition 1 shows that e-BH does not control the FDR-sup, one way forward is to use adjusters, which can transform the running maximum process such that it becomes an -process. Adjusters were introduced in the context of option pricing [Dawid et al., 2011a] and game theoretic probability [Dawid et al., 2011b, Shafer et al., 2011], ensuring against loss of capital or evidence, and in [Choe and Ramdas, 2024] as means to combine evidence across filtrations.

An admissible adjuster Choe and Ramdas [2024] is an increasing function if and only if it is right-continuous, , and Examples can be found in the aforementioned papers, where they are named lookback adjuster, capital calibrator, martingale calibrator, or adjuster. If is the running maximum of an -process for a family of null hypotheses , then is also an -process for . Since the adjusted process is non-decreasing, it will never result in regretting having collected more evidence.

4.1 FDR-sup control with the adjusted running maximum

Theorem 1.

The e-BH procedure applied to the adjusted running maxima of e-processes controls the FDR-sup at level .

4.2 Example: e-BH with the adjusted running maximum

Two examples of admissible adjusters are

| (4) |

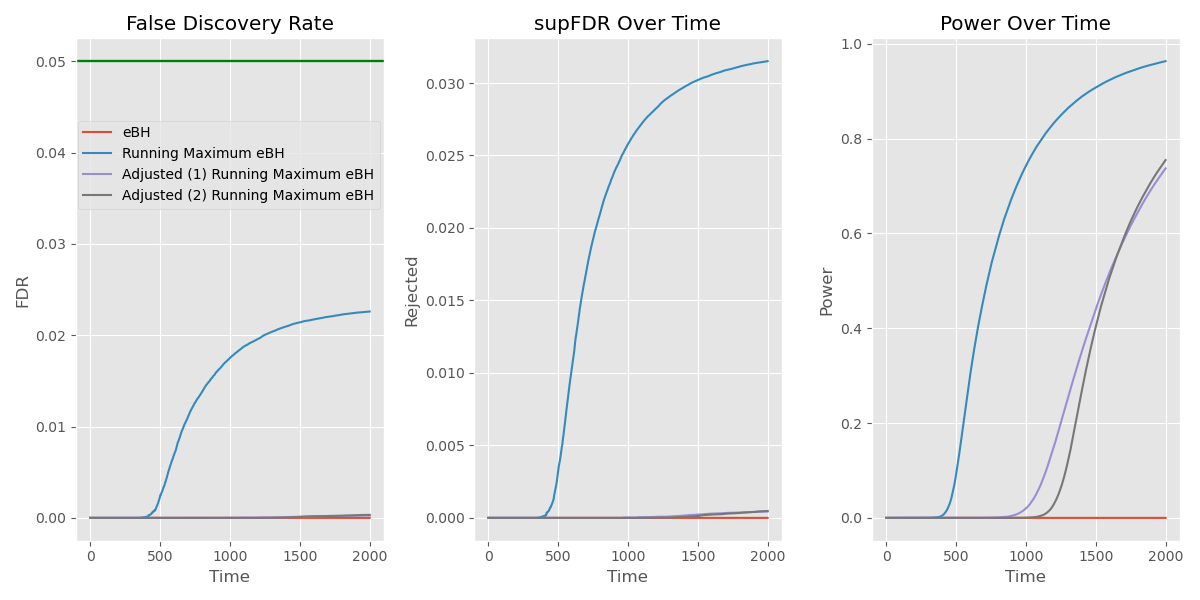

In Figure 1 we see an example of running e-BH on the running maximum of an -process adjusted by (4). The code to generate these plots can be found in Appendix B.

We conducted simulations to evaluate the performance of three procedures: standard e-BH, running maximum e-BH, and adjusted running maximum e-BH. The simulation involves hypotheses, where the null hypothesis () assumes a normal distribution with mean , and the alternative hypothesis () assumes . For each hypothesis, data is generated sequentially, creating a time series of observations.

The simulation includes dependencies among the hypotheses, introduced via a fixed randomly generated correlation matrix for the multivariate normal distributions for , which are independent over time. To construct the -process for each hypothesis, we compute the likelihood ratio at each time step as follows:

Each simulation generates observations for each hypothesis, and the performance metrics (e.g., FDR, power, number of rejections) are averaged over repetitions. This setup allows us to compare the efficiency and FDR control of the three methods under a dependent data structure.

In this example, we see that standard e-BH on the running maximum does not reach level . E-BH is known to be very conservative [Wang and Ramdas, 2022, Lee and Ren, 2024, Xu and Ramdas, 2024], which is why the methods seems to control FDR, even though Proposition 1 says this is not the case in general. We also see that the adjusted maximum processes remain below level as expected, and, unfortunately, we see an appreciable loss of power. Power could be boosted by using techniques such as conditional calibration [Lee and Ren, 2024] or stochastic rounding [Xu and Ramdas, 2024]. Still, the power loss of adjusted processes remains an important drawback of this way of controlling the FDR-sup.

5 Conclusion

We have argued that multiple testing procedures based on -processes should be carefree, meaning that the researcher should never lose out on any rejections because they chose to gather more data for one or more -processes. If procedures are not carefree, experimental design becomes highly complex, since the decision when to gather more data for which -processes becomes consequential. Carefree multiple testing procedures must operate on the running maxima of -processes. Such running maxima are not themselves -processes, but can be turned into e-processes by adjusters. Adjustment is costly, however, in terms of power.

Declaration of funding

Rianne de Heide’s work was supported by NWO Veni grant number VI.Veni.222.018.

References

- Choe and Ramdas [2024] Y. J. Choe and A. Ramdas. Combining Evidence Across Filtrations. (arXiv:2402.09698), Feb. 2024.

- Dawid et al. [2011a] A. P. Dawid, S. de Rooij, P. Grunwald, W. M. Koolen, G. Shafer, A. Shen, N. Vereshchagin, and V. Vovk. Probability-free pricing of adjusted American lookbacks. (arXiv:1108.4113), Aug. 2011a. doi: 10.48550/arXiv.1108.4113.

- Dawid et al. [2011b] A. P. Dawid, S. de Rooij, G. Shafer, A. Shen, N. Vereshchagin, and V. Vovk. Insuring against loss of evidence in game-theoretic probability. Statistics & Probability Letters, 81(1):157–162, Jan. 2011b. ISSN 0167-7152. doi: 10.1016/j.spl.2010.10.013.

- Fischer and Ramdas [2024a] L. Fischer and A. Ramdas. Online closed testing with e-values. (arXiv:2407.15733), July 2024a.

- Fischer and Ramdas [2024b] L. Fischer and A. Ramdas. An online generalization of the e-BH procedure. (arXiv:2407.20683), July 2024b. doi: 10.48550/arXiv.2407.20683.

- Fischer et al. [2024] L. Fischer, M. Bofill Roig, and W. Brannath. The online closure principle. The Annals of Statistics, 52(2), Apr. 2024. ISSN 0090-5364. doi: 10.1214/24-AOS2370.

- Grünwald [2024] P. D. Grünwald. Beyond neyman–pearson: E-values enable hypothesis testing with a data-driven alpha. Proceedings of the National Academy of Sciences, 121(39):e2302098121, 2024.

- Koning [2024] N. W. Koning. Post-hoc $ Hypothesis Testing and the Post-hoc $p$-value. (arXiv:2312.08040), Sept. 2024. doi: 10.48550/arXiv.2312.08040.

- Lee and Ren [2024] J. Lee and Z. Ren. Boosting e-BH via conditional calibration. (arXiv:2404.17562), Apr. 2024. doi: 10.48550/arXiv.2404.17562.

- Ramdas and Wang [2024] A. Ramdas and R. Wang. Hypothesis testing with e-values. (arXiv:2410.23614), Nov. 2024. doi: 10.48550/arXiv.2410.23614.

- Sarkar et al. [2019] S. K. Sarkar, A. Chen, L. He, and W. Guo. Group sequential BH and its adaptive versions controlling the FDR. Journal of Statistical Planning and Inference, 199:219–235, 2019. ISSN 0378-3758. doi: https://doi.org/10.1016/j.jspi.2018.07.001. URL https://www.sciencedirect.com/science/article/pii/S0378375818301320.

- Shafer et al. [2011] G. Shafer, A. Shen, N. Vereshchagin, and V. Vovk. Test Martingales, Bayes Factors and p-Values. Statistical Science, 26(1):84–101, Feb. 2011. ISSN 0883-4237, 2168-8745. doi: 10.1214/10-STS347.

- Wang and Ramdas [2022] R. Wang and A. Ramdas. False Discovery Rate Control with E-values. Journal of the Royal Statistical Society Series B: Statistical Methodology, 84(3):822–852, July 2022. ISSN 1369-7412. doi: 10.1111/rssb.12489.

- Xu and Ramdas [2023] Z. Xu and A. Ramdas. Online multiple testing with e-values. (arXiv:2311.06412), Nov. 2023.

- Xu and Ramdas [2024] Z. Xu and A. Ramdas. More powerful multiple testing under dependence via randomization. (arXiv:2305.11126), Apr. 2024. doi: 10.48550/arXiv.2305.11126.

Appendix A Proofs of FDR-sup control with adjusted e-BH.

A.1 Proof of Theorem 1

In one way to prove that the e-BH procedure with -processes controls the FDR-sup, an adjuster is needed to make the last step of the classical proof by Wang and Ramdas [2022] work. Let denote the e-BH rejection set based on a set of -values , which can be obtained from different time points . I.e., if and only if . Then the FDR-sup at time is

| (5) | ||||

| (6) | ||||

| (7) |

The last expectation would be upper bounded by one, would the integrand be an -value. This is however not the case, but when we use an adjuster on the expression, i.e. we take , this is an -process, and the expectation is again upper bounded by one and the FDR-sup is controlled at level .

Appendix B Code

B.1 Code for the proof of Proposition 1

The code can be found at the following link: https://github.com/tavyrikov/runmax_eBH/blob/main/counterexpample.py

B.2 Code for generating Figure 1

The code can be found at the following link: https://github.com/tavyrikov/runmax_eBH/blob/main/simulation.py