Global stability of perturbed chemostat systems

Abstract

This paper is devoted to the analysis of global stability of the chemostat system with a perturbation term representing any type of exchange between species. This conversion term depends on species and substrate concentrations but also on a positive perturbation parameter. After having written the invariant manifold as a union of a family of compact subsets, our main result states that for each subset in this family, there is a positive threshold for the perturbation parameter below which, the system is globally asymptotically stable in the corresponding subset. Our approach relies on the Malkin-Gorshin Theorem and on a Theorem by Smith and Waltman about perturbations of a globally stable steady state. Properties of steady-states and numerical simulations of the system’s asymptotic behavior complete this study for two types of perturbation term between species.

1 Introduction

General context. The so-called chemostat system allows to model thanks to ordinary differential equations, the evolution of microbial species present in lakes or lagoons. In biotechnology, it can also be used to study the behavior of microbial species, with the aim, for example, of controlling the production of molecules of interest or reducing certain concentrations for water treatment [3, 13]. When the dilution rate is constant (this parameter allows to regulate the input substrate concentration) and in the presence of a single limiting substrate, the competitive exclusion principle (CEP) makes it possible to predict the asymptotical behavior of species concentrations. When considering non-decreasing kinetics for the species (such as Monod’s kinetics [20, 21]), the CEP asserts that, generically, only one species survives asymptotically [16, 26]. It is worth mentioning that in the chemostat system with a single limiting substrate, the species do not interact directly with each other but only indirectly through the substrate equation.

Main objective. The aim of this paper is to study stability properties of the chemostat system when an exchange term111We will also use the terminology “perturbation term” thoughout the paper. between species is incorporated. This additional term in the system is quantified by a generally low perturbation parameter and has several origins. It can represent, for example, mutation between species (due to gene transfer) and in that case, the perturbation parameter can be seen as a mutation rate. To remain general, we prefer to use in this paper the terminology perturbed chemostat system, to describe the resulting dynamical system. In presence of this phenomenon, each species is able to convert into neighboring species. Theoretical and numerical approaches to study the chemostat system with a perturbation term as well as related questions can be found in [2, 4, 5, 7, 8, 10, 11, 14, 19, 22] (among others). In this paper, we are interested in addressing the next question : what can we say about the asymptotic behavior of a perturbed chemostat system particularly when the perturbation is “small222This is made more precise in the rest of the paper.”? Depending on the data defining the system (such as dilution rate, perturbation parameter, kinetics), we wish to know if there is an invariant subset of the state space in which the perturbed system is globally asymptotically stable around a coexistence333This is an equilibrium point such that all species are present asymptotically. steady-state. Even if the system in question is close to the chemostat system (in a way that has yet to be quantified), this question is not obvious. Indeed, it is well-known that the properties of a perturbed dynamical system can differ significantly from those of the non-perturbed system, potentially resulting in the emergence of multiple steady states or periodic orbits that would not exist without perturbation.

It is worth mentioning that for the chemostat system, previous studies (such as [4, 10]) indicate that the techniques for studying the asymptotical behavior of a perturbed version of the chemostat system differ from the classical approaches for the chemostat system (using for instance Lyapunov functions [15, 17, 26]).

Related results. In order to highlight the novelty of our work, we would like first to recall some results in [4, 10]. First, the article [10] provides a first insight into the above question and it is as follows. Global stability is proven provided that kinetics are in a sufficiently narrow bundle (the limiting case being that they are all equal to a Monod type’s kinetics) and that all yield coefficients are close to each other (the limiting case being that they are all equal to one). The paper [4] provides a similar global stability result provided that kinetics are of Monod type and that the dilution rate is small enough (the limiting case being that the dilution rate is zero). Additionally, the occurrence of a single coexistence steady-state (apart from the washout) is established which differs from the chemostat system where several steady states occur (the number of them being equal to the number of species apart from the wash-out). This work is in line with the preceding studies, but, it is probably set in the most natural case, i.e., when the kinetics are monotone (but arbitrarily), when the dilution rate is also arbitrarily (which is more realistic than in [4] from an experimental point of view) and when the perturbation parameter tends to zero. Furthermore, we also consider the case of a non-linear exchange term depending both on the substrate and species concentrations and non-necessarily linear w.r.t. species concentrations as in [4].

Main contribution. In order to study global stability of a general perturbed dynamical system (knowing that the non perturbed system is globally asymptotically stable), Smith and Waltman introduced in [27, Theorem 2.2] (see also their Corollary 2.3) sufficient conditions on the system to guarantee that global stability is preserved as the perturbation parameter tends to zero. In order to apply this fundamental result in our setting, it is essential to verify one of the hypotheses which states that all trajectories of the perturbed system should enter after a certain time into a (fixed) compact subset of the invariant manifold and remain in it. In our setting, this hypothesis is not evident to verify. A good approach is to use the Malkin-Gorshin Theorem [25] (see also [23, 24]). This result is part of the folklore and it allows to show that trajectories of the perturbed system remain close to trajectories of the non-perturbed one provided that the perturbation parameter is small enough. It is proved in [25] in the context of B-stability which in some sense is a weaker notion than local stability. The B-stability of a differential system is verified if the original system is exponentially stable. Since the chemostat system fulfills the latter condition, we shall not enter into the notion of B-stability throughout this paper. In order to combine the Malkin-Gorshin Theorem and [27, Theorem 2.2], we need to introduce a family of compact subsets of the invariant manifold (to apply the Malkin-Gorshin Theorem uniformly w.r.t. the initial condition). Our main result states that for each subset in this family, there is a positive threshold for the perturbation parameter below which, the system is globally asymptotically stable in the corresponding subset (Theorem 2.4). We complete this study by analyzing steady-states when the perturbation term depends on the substrate but is linear w.r.t. concentration species. Numerical simulations are carried out for two types of exchange terms and highlight the behavior of the perturbed dynamical system as expected thanks to Theorem 2.4.

Organization of the paper. The paper is structured as follows. In Section 2, we present the model and our main hypotheses. Additionally, we provide Theorem 2.2 that is a slight extension of [27, Corollary 2.3] to our setting and Theorem 2.3 which provides a simplified version of the Malkin-Gorshin Theorem. For sake of completeness, these propositions are proved in the Appendix. In section 3, we analyze in details steady-states of the perturbed system in the case where the perturbation term is linear w.r.t. species concentrations. Finally, Section 4 develops numerical simulations of the perturbed chemostat system for two types of exchange terms. Section 5 explores various perspectives derived from the results obtained in this paper.

2 Model presentation and main result

2.1 The chemostat system with a general perturbation term

Throughout this paper, we consider the chemostat system with a single limiting substrate and species, and we also incorporate an exchange term between them that depends on species concentrations, substrate concentration, and on a perturbation parameter called . This yields the following dynamical system

| (2.1) |

where:

-

is a vector containing the species concentrations for ;

-

and denote respectively the substrate and input substrate concentration ( is fixed) ;

-

denotes the diagonal matrix where for all , the function is the kinetics of species ;

-

for all , is the yield coefficient associated with species ;

-

is the dilution rate and is the perturbation parameter ;

-

the function represents the perturbation term so that for all , describes how species converts into other species at a rate .

The perturbation parameter plays different roles depending on the interaction type considered between species (typically, it can represent a mutation rate or a constant probability of mutation). Regardless of the biological meaning of , it is relevant in our formulation as it will allow us to see (2.1) as a perturbation of the chemostat system. Let us now introduce the following hypotheses on the data. Hereafter, stands for the euclidean norm of a vector .

-

(A1)

For all , is of class , non-decreasing, bounded over , and such that .

-

(A2)

The function is of class and satisfies for all . Moreover, it is with linear growth, i.e., for all there is such that for all ,

(2.2) -

(A3)

For all and all , if , then for all , one has .

-

(A4)

For every , one has

Some comments on the preceding hypotheses are in order.

Remark 1.

(i). Hypothesis (A1) is standard when considering chemostat type’s systems (see, e.g., [26]). However, depending on the application model, other types of kinetics are relevant such as Haldane444Such kinetics allow to take into account inhibition through substrate. type’s kinetics which are non-monotonic or kinetics with a more complicated behavior such as in [6]. In this paper, we shall restrict our attention to monotone kinetics only.

(ii). Supposing that vanishes for (see (A2)) allows us to retrieve the chemostat system

| (2.3) |

for . This hypothesis is important in our study in order to investigate global stability properties of (2.1). Note that (2.2) is a standard hypothesis in the theory of ordinary differential equations in order to prevent the blow-up phenomenon of solutions.

(iii). Hypothesis (A3) is essential for biological purpose to guarantee that all species remain non-negative over time

and Hypothesis (A4) implies that mass is conserved during the exchange process between species (this property is crucial in our study, particularly for proving Lemma 2.1 and Proposition 2.1).

2.2 Invariant domain and related properties

In this section, we introduce the invariant domain that will be considered throughout the paper. The next lemma is a preliminary result in order to introduce this set.

Lemma 2.1.

Proof.

The existence of a unique solution to (2.1) essentially follows from (2.2) which guarantees that solution are defined globally over . The fact that is invariant follows from (A3) and using that and . This takes care of (i). To prove (ii), observe that if , then for every , one has thanks to (A3). Now, (A4) implies that , hence, we must have for every as wanted. The fact that is a steady-state of (2.1) follows from the equality for every . This ends the proof. ∎

From Lemma 2.1, is forward invariant for (and also attractive in ), hence, without any loss of generality, we will suppose that , throughout the paper. In addition, it is readily seen that for all time (even if ) provided that . Regarding the positivity of the variables , obtaining such a property depends on the assumptions made about the function . The next lemma provides a sufficient condition ensuring positivity of for and .

Lemma 2.2.

Proof.

Take such that and suppose by contradiction that vanishes over . Let then . Since over , we deduce that so that . If , we get . By a similar argumentation we deduce that so that if and , condition (2.4) implies that . By an inductive reasoning, we deduce that , hence, Lemma 2.1 implies that for every which is a contradiction since . Hence, we deduce that for every . The same reasoning applies to all other indexes as well which ends the proof. ∎

We give in Section 4 two examples where the latter hypothesis about is fulfilled implying that every species is present at any time (in contrast with the chemostat system where for all , either if or for all time ).

We now turn to the definition of the invariant set for (2.1). Set and let be defined as

| (2.5) |

This set will play a significant role in the remainder of the paper (in particular to state our global stability results). Hereafter, we say that a set is (forward) invariant for a dynamical system if every solution starting in this set at time remains in it for all time . We say that it is attracting if the distance between this set and solutions starting outside the set at time converges to zero as .

Proposition 2.1.

Proof.

Let us set . We have

from which we deduce that for every time , one has

| (2.6) |

implying that is invariant through (2.1). Take an initial condition and let be the unique solution to (2.1) starting at from this initial condition. If there is a time such that , we obtain using a similar argumentation as (2.6) that for all time which shows that the distance of the solution to is zero for all . On the other hand, if for every , one has , we obtain that

for every . Hence, the distance of the solution to (that is proportional to since the active part of boundary of is the hyperplane of equation in ) goes to zero as . To prove the rest of the proposition, suppose that does not converge to as . If for all time , the function necessarily converges to from (2.6). Hence, there is such that . This proves exactly that the trajectory has entered into in finite time. ∎

Remark 2.

(i). In Lemma 2.1 and in Proposition 2.1, (A1) can be weakened supposing that is only non-negative, continuous and null at , but, as said in Remark 1, we shall not consider non-monotonic kinetics in this paper.

(ii) In the case of the chemostat system, it is relevant to introduce so that changing into if necessary, satisfies

. In that case, is an invariant and attractive manifold of (2.3), but, solutions to (2.3) starting outside this set never enter into in finite time.

A key difference that arises whenever is that solutions to (2.1) with may enter the region in finite time, provided that the function does not converge to .

We highlight this property numerically in Section 4 (see Fig. 6 and Fig. 7).

2.3 Competitive exclusion principle

The analysis of stability properties of (2.1) when the perturbation parameter tends to zero is closely related to properties of the chemostat system (2.3) corresponding to (2.1) for , that is why, we wish now to recall the competitive exclusion principle (see, e.g., [16, 26]). In what follows, we set

Note that can be equal to if is greater than for every . For , (2.1) has at most exactly steady-states (depending on the value of ), namely,

together with . The CEP can be formulated as follows.

Theorem 2.1.

Suppose that (A1) is fulfilled. If there is a unique such that , then, for every initial condition such that , the unique solution of (2.1) for starting at at time , converges to , and this steady state is locally exponentially stable. If , then, for every initial condition , the unique solution to (2.1) with starting at at time converges to .

Fig. 1 illustrates Theorem 2.1 in two cases (kinetics are given in Table 1) with five species and . The first case is with where species dominates the culture () whereas case 2 is with so that wash-out occurs leading to extinction of species ().

As it is well-known the behavior of a perturbed dynamical system may slightly differ from the behavior of the non-perturbed system. In our setting and as far as we know, the available methods to prove the CEP (such as Lyapunov functions) cannot be straightforwardly transferred to study (2.1). That is why, we will enunciate in the next section intermediate results before stating the main theorem about the behavior of (2.1).

2.4 Global stability of the perturbed chemostat system

In this section, we prove Theorem 2.4 which is our main result. We start by recalling a result by Smith and Waltman from [27], but adapted to our context (Theorem 2.2) and we also state a weaker version of the Malkin-Gorshin Theorem555This result is demonstrated in [25] in the context of B-stability. However, we deal here with asymptotic stability which is a stronger notion but sufficient for our purpose. to be found in [25] (Theorem 2.3). Doing so, let us consider a general Cauchy problem

| (2.7) |

where is of class , is such that 666Throughout the paper, the interior of a set is denoted by ., , and is a parameter. We suppose that for every , the unique solution to (2.7) denoted by is defined over and that is forward invariant by (2.7). The next result777We raise this result as a theorem since [27, Corollary 2.3] is just a consequence of [27, Theorem 2.2] which is one of the main result of [27]. is a slight adaptation of [27, Corollary 2.3].

Theorem 2.2.

Let be a subset of such that and . Suppose that there is such that , is Hurwitz, and is attracting888This means that for every as . for solutions of (2.7) in with . Moreover, assume that the following hypothesis is fulfilled:

-

(H1)

There exist a compact set and such that for each and for each , the unique solution to (2.7) reaches meaning that for every large enough.

Then, there are and a unique point such that for every , one has and for all as .

The only difference with [27, Corollary 2.3] is that is not supposed to be invariant but rather contained in another set which is invariant. For this reason, we propose a proof of this proposition in the Appendix following [27] (also, the proof is made in the context of ordinary differential equations and not in an abstract setting). Finally, we would like to insist on the fact that the point may belong to the boundary of the set if the dynamics can be extended to an open set around whose intersection with is convex (as it is mentioned in [27, Remark 2.1]).

We now turn to the Malkin-Gorshin Theorem [25, Theorem 4] which is part of the folklore in the theory of dynamical systems involving regular perturbations. A version of this result involving the concept of B-stability can be found in [25]. We provide below a version of this result in the (stronger) setting of asymptotic stability which is enough for our purpose.

Theorem 2.3.

Let be such that . Suppose that is Hurwitz and that is attracting for solutions of (2.7) with and initial conditions in a non-empty compact set . Then, for every , there is such that for all and all ,

The proof of this result (using local stability) can be found in the Appendix. Let us emphasize the fact that the parameter depends on a compact set for initial conditions (in contrast with [25, Theorem 4] which involves a single initial condition). In our approach, considering such a compact set will be needed to prove Theorem 2.4 whose proof relies on the combination of Theorem 2.2 and Theorem 2.3 in the setting of (2.1). More precisely, the result of Theorem 2.3 will allow us to verify (H1) in Theorem 2.2.

Coming back to (2.1), for every and for every , we define a non-empty compact subset of as

so that for a fixed index , the union of these sets is associated with through the following relationship:

Note that the sets are not necessarily invariant for (2.1). Our main result states that (2.1) has a steady-state (apart from the wash-out) that is attracting in subsets provided that the perturbation parameter is small enough (where given a value of the dilution rate , represents the index of the species that dominates the competition in Theorem 2.1).

Theorem 2.4.

Proof.

Let be defined as

| (2.8) |

for every and all . Set where so that and recall that , hence, . For every , we denote by the unique solution to (2.1) starting at at time . In virtue of Theorem 2.1, we have for every whose -th component is positive at time . It follows that there is an instant (that depends on the initial condition ) such that

for every where is such that ( does not depend on ). Now, the Jacobian matrix of w.r.t. at is just the Jacobian matrix of the chemostat system at the globally asymptotically stable steady-state . Hence, it is of Hurwitz type (this property is standard, see, e.g., [16, 26]). Moreover, for , the CEP implies that is attracting for solutions to (2.1) (with ) and starting in at time . We are now in a position to apply Theorem 2.3 to at the point with . Take such that . It follows that there is such that for every , for every , and for every ,

Now, take . We deduce that there is (as before, depending on ) such that for every ,

Therefore, for every , every , and every . We have just checked hypothesis (H1) of Theorem 2.2 with (remind that ) and . Note that the point lies on the boundary of since for every such that and that . But, thanks to the expression defining as given in (2.8), can be straightforwardly extended to a new function (still denoted by ) defined over . Hence, we are in a position to apply Theorem 2.2 (see [27, Remark 2.1]). It follows that there exists such that for every , there is a unique point satisfying and such that for every . We conclude by taking and which, by continuity w.r.t. , is not the wash-out. ∎

The previous result asserts a global stability type property for (2.1) once the dilution rate and the corresponding subset have been chosen where is such that and . It is also natural to ask how (2.1) behaves if instead we are given some initial condition in . This question can be answered in a simple way as follows.

Corollary 2.1.

Proof.

Let be such that . It follows that belongs to and so is . The result then follows from Theorem 2.4. ∎

2.5 Comments about Theorem 2.4

Theorem 2.4 sets up the existence of a perturbed equilibrium point together with its stability in . It could be interesting to find general conditions on which guarantee that the perturbed steady-state is such that all species are present asymptotically (i.e., for all ). In the next section, we answer to this question when the perturbation term is linear w.r.t. .

The reasoning as deployed in the proof of Theorem 2.4 does not allow us to obtain global stability of the steady-state in for a fixed . Indeed, for every initial condition such that , the system (2.1) with does not converge to (but to some other steady state, thanks to the CEP). It follows that for , the time to reach from an initial condition in such that and goes to infinity. This prevents us to apply Theorem 2.3 that requires a compact set for initial conditions in order to uniformly control the distance between perturbed and non-perturbed trajectories for all . However, numerical simulations (as performed in Section 4) indicate that global stability of the perturbed system (for a fixed ) should be verified in in two particular cases for the perturbation term. Proving global stability in the set for a general function seems rather a delicate question in general and it could be first addressed when the perturbation term is as in Section 3.

3 Analysis of steady-states in the case of a linear exchange term

The objective of this section is to study properties of steady-states of (2.1) when the interaction term is linear w.r.t. and the perturbation parameter enters linearly into the system, that is,

| (3.1) |

for all where is continuous. Considering such a linear coupling w.r.t. is motivated by several application models, see, e.g., [4, 10, 11]. The fact that the interaction term is now more specific than in the preceding section will allow us to give additional properties concerning the steady-state as given in Theorem 2.4. When is given by (3.1), (2.1) can be equivalently rewritten as :

| (3.2) |

where the matrix is defined as

If a pair is a steady state of (3.2), then, we necessarily have

| (3.3) |

As a consequence, is always a steady-state of (3.2). On the other hand, if a steady-state of (3.2) is such that is non-null, then, is necessarily an eigenvector associated with the eigenvalue of the matrix . To study the occurrence of such a steady-state, in the next section, we will recall classical definitions related to the Perron-Frobenius Theorem and give properties of the matrices and .

3.1 Application of the Perron-Frobenius Theorem

A matrix999As usual, matrices are named using capital letters and coefficients are represented by lower case letters. is said to be essentially non-negative if , for all and irreducible if there are and such that all entries of are positive. Moreover denotes the largest real part of the eigenvalues of . When dealing with , we shall also refer to the Perron root of . Let us now introduce some additional hypotheses about the matrix .

-

(A5)

For all , is essentially non-negative, irreducible and for all ;

-

(A6)

For all such that , the function is non-decreasing and there is such that for all , is also increasing for every .

For future reference, note that in (A6), corresponds to the i-th entry of . From (A5) we can prove the following property related to .

Property 3.1.

Suppose that (A5) is satisfied. Then, one has for every .

Proof.

Given and , one has , where is the ith vector of the canonical basis of . Now, the Perron-Frobenius Theorem implies that

whence the result (using that any matrix and its transpose have same eigenvalues). Since is continuous, we obtain that combining the continuity of (which follows from the continuity of the spectral radius w.r.t. the matrix) and the fact that for any . ∎

For every , we define the critical dilution rate as

| (3.4) |

It will allow us to determine if there is another steady-state than the washout depending on the value of w.r.t. . The dependence of the matrix on complicates the approach compared to the one presented in [4]. Therefore, before delving into this issue, we will first recall two results from [1] related to :

-

the convexity of the largest real part of the sum of two matrices101010This result is known as Cohen’s convexity Theorem, which pertains to the spectral bound of essentially nonnegative matrices in relation to their diagonal elements. (Theorem 3.1 below) ;

-

properties of a function of two variables that is convex in the second variable (Lemma 3.1 below).

Theorem 3.1 ([1], Theorem 2).

If is a diagonal matrix and an essentially nonnegative matrix, then, is a convex function of .

Lemma 3.1 ([1], Lemma 1 (3)).

If , is a function satisfying:

-

1.

for all and all , ,

-

2.

for all , is convex over ,

then, for all , one has except possibly at a countable number of points where the one-sided derivatives111111The notation stands for the right and left derivatives of w.r.t. at the point . of exist but differ, and, at these points, one has .

The next statement establishes properties of the matrix and of the critical dilution rate extending [4, Lemma 3.1] to the case of a non-constant and non-necessarily symmetric matrix , and whenever yield coefficients are non-necessarily equal. It is also useful for proving Proposition 3.2.

Proposition 3.1.

Proof.

To prove (i), let and . One has , thus, (thanks to (A5)). From the Perron-Frobenius Theorem, for every , exists and is of multiplicity one, hence, we can uniquely define as the unitary associated eigenvector (which is thus with positive coordinates). Now, given , (A6) implies that entry-wise. Thus, by the Collatz-Wielandt formula121212For every essentially non-negative matrix , . and using (A6), we deduce that

where the strict inequality comes from the second part of (A6). We obtain that is strictly monotone over and, therefore, over as well which proves (i).

To prove (ii), we adapt the proof of Proposition 3.5 in [4] using the aforementioned results ([1]) in the case where depends on . First, we can directly conclude from the CEP that . Recall now that for any essentially non-negative and irreducible matrix , the Perron-Frobenius Theorem ensures that is simple, hence, there is a neighborhood of in such that is simple for every . Furthermore, the following (standard) result holds true (see, e.g., [12]) : the derivative of w.r.t. , denoted by is given by , where are uniquely defined by

Observe that is essentially non-negative, irreducible and that . Thus, if and are given by (3.5), one has . Next, let us set

for and let . When , the Perron root is simple since is also simple, hence, is differentiable at and using the chain rule formula, we get that

Thus, using a first-order expansion of around , we obtain as :

where as . We deduce that as . To show that is non-increasing over , we use Theorem 3.1 and Lemma 3.1. Let us first check that fulfills the hypotheses of Lemma 3.1. Doing so, observe that for , satisfies . Next, Theorem 3.1 implies that is convex w.r.t. the diagonal matrix given that by Assumption (A5), is essentially non-negative. This property implies that is convex w.r.t. , hence, we are in a position to apply Lemma 3.1.

Furthermore, from (A5), the matrix is essentially non-negative and irreducible for all so that is simple. It follows that is differentiable over and that for every , one has:

and therefore, is non-increasing131313We are ignoring that the one-side derivatives may differ (see Lemma 3.1) since is differentiable..

∎

3.2 Coexistence steady-state

In this section, we discuss the occurrence of a coexistence steady-state when the perturbation term is given by 3.1. Our discussion on steady-states of (3.2) is divided into two cases, whether or . The next proposition presents similarities with [4, Propostion 3.3], but, as explained before, yield coefficients are not necessarily all equal to one (in contrast with [4]) and the perturbation matrix is now a function of (and non-necessarily symmetric). That is why we provide the proof in details.

Proposition 3.2.

Suppose that (A1) and (A5)-(A6) hold true and that there is a unique such that .

(i) If is such that , then is the only equilibrium of (3.2) and it is stable. If , then is globally asymptotically stable.

(ii) If is such that , then, there are only two equilibria for (3.2), namely the wash-out that is unstable and a coexistence steady-state . Furthermore, for every , there is (where ) such that for every , is locally asymptotically stable.

Proof.

Assume that . We will see that is the only solution of (3.3). Suppose by contradiction that there is satisfying (3.3) and such that . Hence, we necessarily have . Moreover, is an eigenvector of associated with the eigenvalue , implying that . On the other hand, by Proposition 3.1, is increasing, thus

therefore we have a contradiction so that we must have . Let us now turn to the stability of . We claim that for every there is a such that and for every solution of (3.2) with and . First, notice that , but , hence, we deduce that for every . Now, fix and observe that

where . Let us set and then take and . We deduce first that for all and that if at some time we have , then

It follows that for all time , one has which allows us to conclude on the stability of . Finally, in the case where , we have

using that . Since , we conclude that as which proves (i).

Suppose now that and let be a steady-state of (3.2). If , then, we have . We easily check that the Jacobian matrix of (3.2) at is a block matrix whose first block is which is such that . It follows that is unstable, thus, . Thanks to the Perron-Frobenius Theorem, is an eigenvector associated with the zero eigenvalue of (the largest one), hence, it is with positive coordinates.

The vector is uniquely defined as follows. Since is continuous and increasing and given that and , there is a unique solution to the equation . Now, is proportional to the Perron vector141414It is the unique unitary eigenvector in the eigenspace of for the zero eigenvalue. associated with the zero eigenvalue of , thus, there is a unique such that . From (3.3), we conclude that

| (3.6) |

The vector is then uniquely defined. Finally, it is well-known that for , the Jacobian matrix of (3.2) at the steady-state is a Hurwitz matrix (see, e.g., [16, 26]). The existence of follows from the continuity of the eigenvalues of a matrix w.r.t. parameters. This ends the proof. ∎

Remark 3.

(i). The equilibrium is called coexistence steady-state because one has for every . Remind that is defined by and that where is defined in (3.6) and is the (unitary) Perron vector associated with . Note that for an arbitrary pair , it would be interesting to know whether the Jacobian matrix of (2.3) at this point is Hurwitz, however, this question presents some difficulties.

(ii). In propositions 3.1 and 3.2, the fact that is not optimal (in the sense that we only conclude

for ), but, the parameter is not necessarily

“small” since it is defined by (for instance, in the example of section 4.2).

When does not depend on , (A6) is obviously true for all , hence, .

Finally, extending these results for when depends on is certainly not straightforward, and it may not even be true in general.

4 Numerical simulations

In this section, we provide a numerical analysis of (2.1), our goal being to confirm the theoretical study conducted previously while highlighting other properties of the system numerically. This numerical study is conducted for two types of linear perturbations w.r.t. :

-

Case 1 : where is a given symmetric matrix ;

-

Case 2 : where for every , is a given matrix involving the kinetics and that is non-symmetric neither constant.

For case 1, we shall refer to the case with a constant perturbation matrix (or transition matrix) and for case 2, we shall refer to a non-constant perturbation matrix (or transition matrix). The exact definition of and and the discussion of the corresponding dynamical system can be found in Section 4.1 and 4.2 respectively. Section 4.3 presents numerical simulations of trajectories that are carried out with the SciPy library in Python and more specifically using the function solve_ivp that solves numerically ordinary differential equations using an explicit Runge-Kutta method of fifth order151515The scripts for reproducing the numerical experiments of this paper can be found in the repository https://github.com/calvarezlatuz/simulation_CM. The number of grid points is around 400.

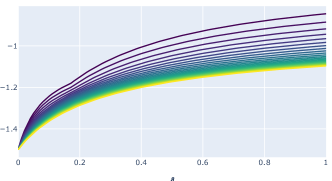

The parameters used for the numerical simulations are defined as follows. We assume that kinetics are of Monod type, i.e., , where are positive parameters for every (it is easily seen that (A1) is fulfilled). Figure 2 depicts the kinetics that have been chosen for the examples. The values of yield coefficients and other coefficients can be found below.

In the numerical simulations of (2.1) related to its asymptotic behavior, note that we have chosen a constant dilution rate value fixed to . From the CEP, we deduce that for , then species survives (see Fig. 2) so that in Theorem 2.4, the index is such that .

| Species number | 1 | 2 | 3 | 4 | 5 | |

| Coefficients of | 0.84 | 0.46 | 0.34 | 0.48 | 0.76 | |

| 0.28 | 0.90 | 0.11 | 0.09 | 0.36 | ||

| Yield coefficients | 1.00 | 1.50 | 2.00 | 2.50 | 3.00 | |

| Simulation parameters | ||||||

4.1 Case 1 : perturbation term defined via a constant perturbation matrix

In this section, we suppose that where the matrix is defined as

so that (2.1) rewrites

| (4.1) |

To explain, the origin of , let us examine the following population dynamics model structured around a single phenotypic trait called and where is with values within a fixed segment . It describes the evolution of both species and substrate with concentrations and respectively:

| (4.2) |

where and . In the preceding integro-differential system, denotes the kinetics (depending now on the substrate and on the trait), denotes the Laplacian of w.r.t. , and the function replaces the yield coefficients to be found in the finite-dimensional setting for the species. To ensure that the integro-differential system (4.1) is well-posed, it is typically coupled with appropriate initial and boundary conditions, which help to guarantee both the uniqueness and existence of a solution to (4.1). Since our purpose in this paper is to address stability properties for a finite number of species, we will not further discuss the preceding system. We just want to point out that can be seen as a discretization of the diffusion term for Neumann boundary conditions.

Note that the main difference between (4.1) and the model studied in [4] is that in the present setting, yield coefficients are not all equal to one (in contrast with the model in [4]). Furthermore, it is important to note that the dynamical system examined in [4] is only analyzed in the asymptotic case where approaches zero. In contrast, our study maintains at a fixed constant value while is a small parameter (which seems more reasonable from a practical viewpoint).

In order to apply the results of Section 3, we can easily verify the following :

-

assumption (A6) is satisfied for every so that .

Hence, for every such that , Section 3 ensures the existence of a unique coexistence steady-state of (4.1) apart from the wash-out. Global stability of this steady-state is described in Theorem 2.4.

Finally, it can be checked that if , then, the corresponding solution to (4.1) satisfies for every and every (to prove this, it is sufficient to apply Lemma 2.2, whose main hypothesis (2.4) is easy to verify). In view of the link between and the discretization of the Laplacian operator, this property is in line with the well-known regularizing effect of the heat equation.

4.2 Case 2 : perturbation term defined via a non-constant perturbation matrix

In this section, we suppose that where the matrix is defined as

| (4.3) |

so that (2.1) rewrites

| (4.4) |

Observe that is a tridiagonal matrix that includes two coefficients located at the position and . The origin of this matrix is derived from [9], which describes the effect of mutations within a cultivated biomass, leading to the consideration of each species as a distinct gene mutation. For every , the so-called mutation matrix is derived considering a probability of mutation, leading that way to the above circulant matrix. The system as described in (4.4) is also closely related to the one studied in [19, Section 4.2].

In order to apply the results of Section 3, we check (A5) and (A6):

-

it is easily seen that for any , the matrix is essentially non-negative, irreducible and such that for every so that (A5) is satisfied.

-

(A6) is satisfied for every with .

Hence, for every such that , Section 3 ensures the existence of a unique coexistence steady-state of (4.4) apart from the wash-out. As in the previous case, global stability of this steady-state is described in Theorem 2.4 and all species are with positive values over provided that (the hypothesis (2.4) in Lemma 2.2 is also easy to check).

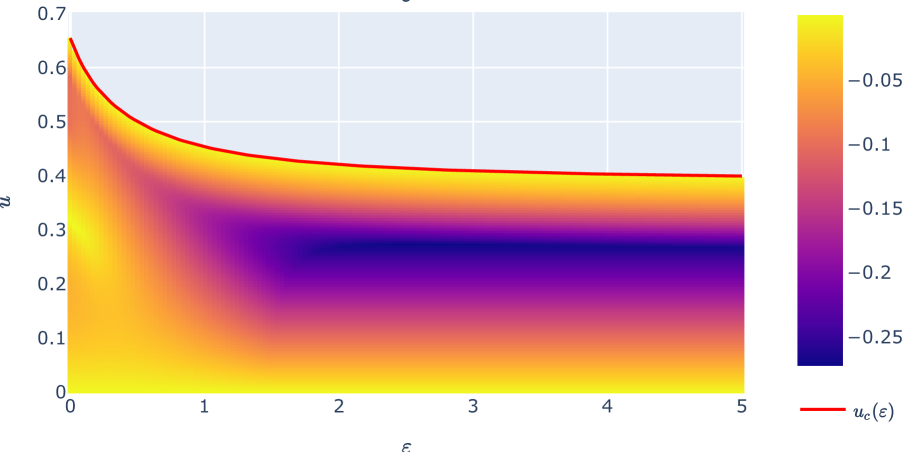

Interestingly, with the data given in Table 1, we verified numerically that still exists for every and every (see the discussion in Remark 3 (ii)). This is why, the numerical analysis as performed in Section 4.3 has also been carried out for (this is only for figures 8(b) and 9(b)). The next two figures show (numerically) that is always increasing which is sufficient to ensure the validity of Proposition 3.1 and 3.2 when is given by (4.3).

4.3 Results for both examples

The numerical simulations on systems (4.1) and (4.4) are intended to highlight their various properties and are organized as follows:

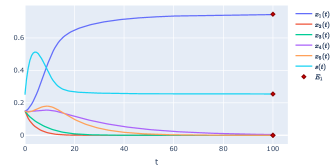

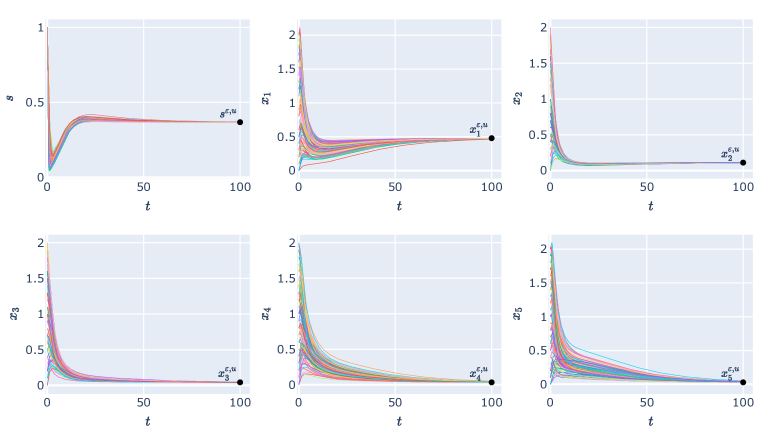

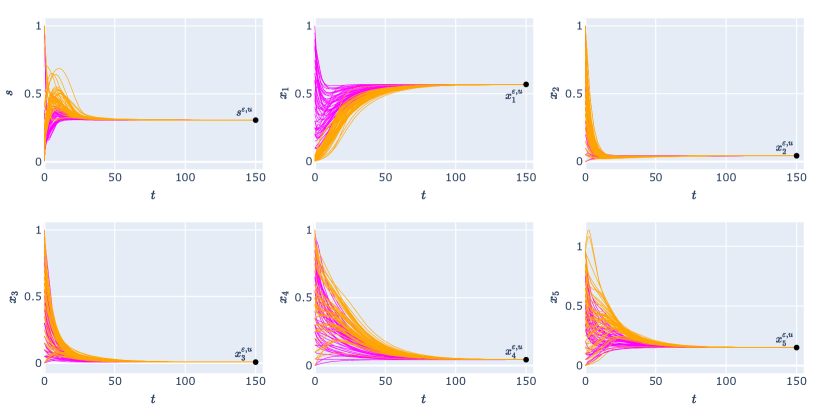

Comments on Fig. 4 & Fig. 5. This figure shows that all simulated trajectories converge to the coexistence steady-state even if initial conditions are taken outside the set . Numerical values of this equilibrium are as follows:

In contrast with the case (corresponding to the chemostat system) where only one species survives, thanks to the CEP, we see that all species are present asymptotically. In the first case, dominant species have an index close to , the index of the species that wins the competition for (see also [4]). In the second case, the matrix depends on the substrate, so, this property is not clear as Fig. 5 shows.

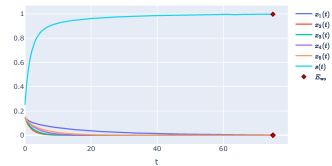

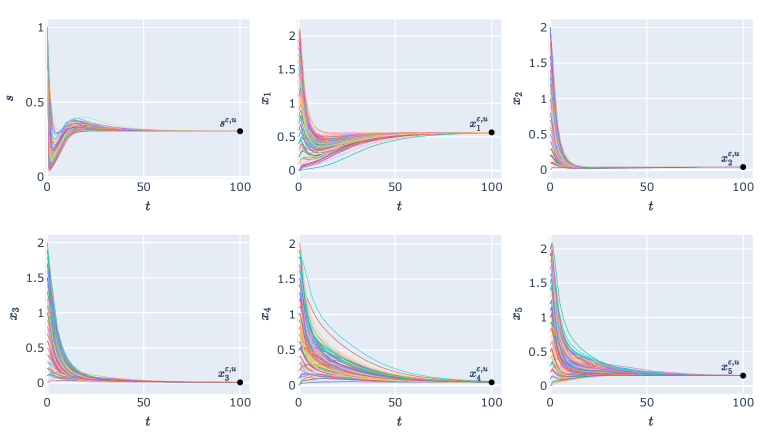

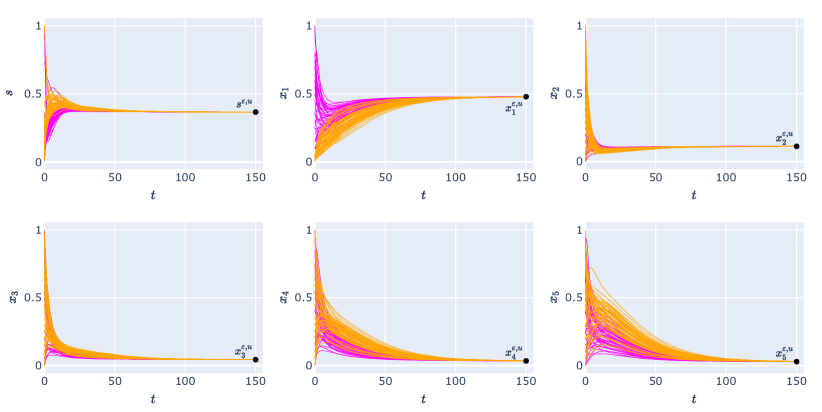

Comments on Fig. 6 & Fig. 7. As expected, trajectories starting in converge to the coexistence steady-state, but, this figure shows that it is also the case if initial conditions are in although it is not predicted by Theorem 2.4.

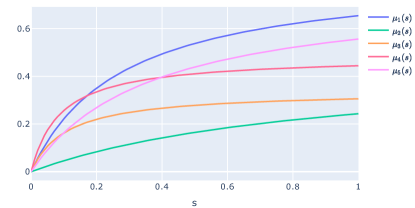

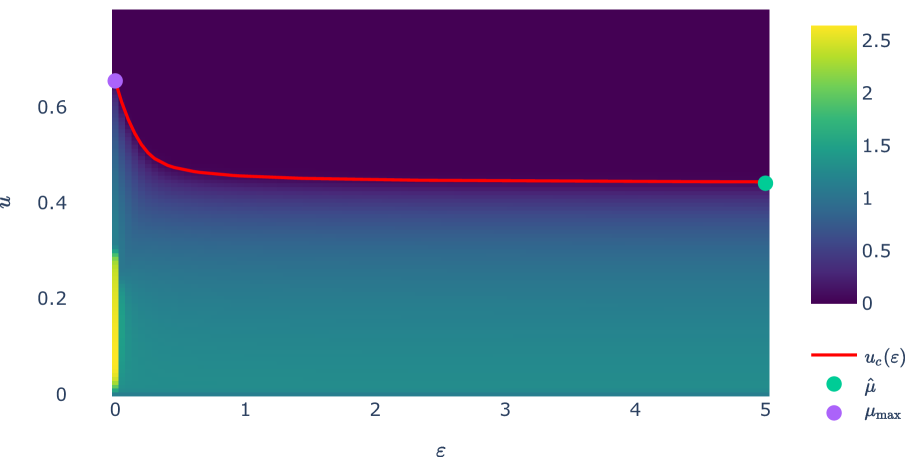

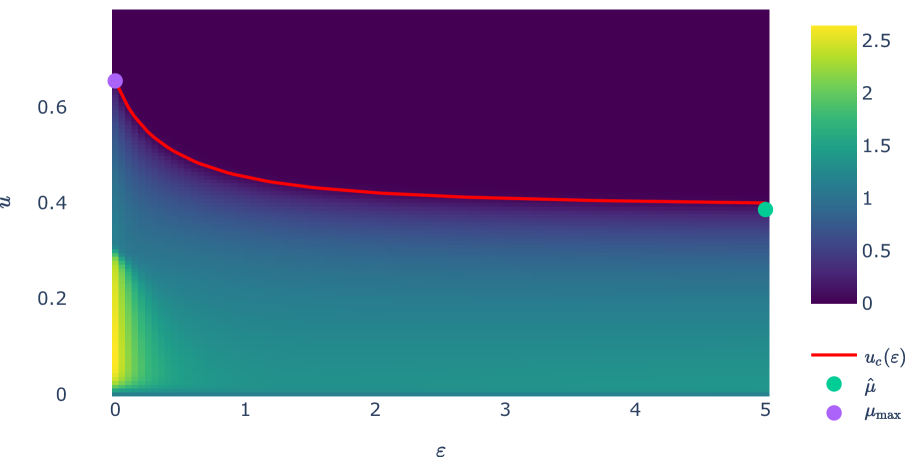

Comments on Fig. 8. As expected, decreases from to . In both cases, we have (see Proposition 3.1) whereas in the case of the constant matrix , one has and in the second case, one has . This figure is related to Proposition 3.2 and can be seen as an operating diagram :

-

above the red curve , the wash-out is the only steady-state and it is globally asymptotically stable ;

-

on the red curve , the wash-out is the only steady-state and it is stable ;

-

below the red curve , there are two steady-states, namely the wash-out (unstable) and the coexistence steady-state. The behavior of the system toward the coexistence steady-state is described in Theorem 2.4.

The figure confirms that whenever , then the system converges to the wash-out whereas this is not the case whenever .

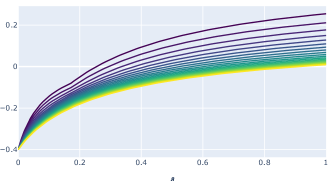

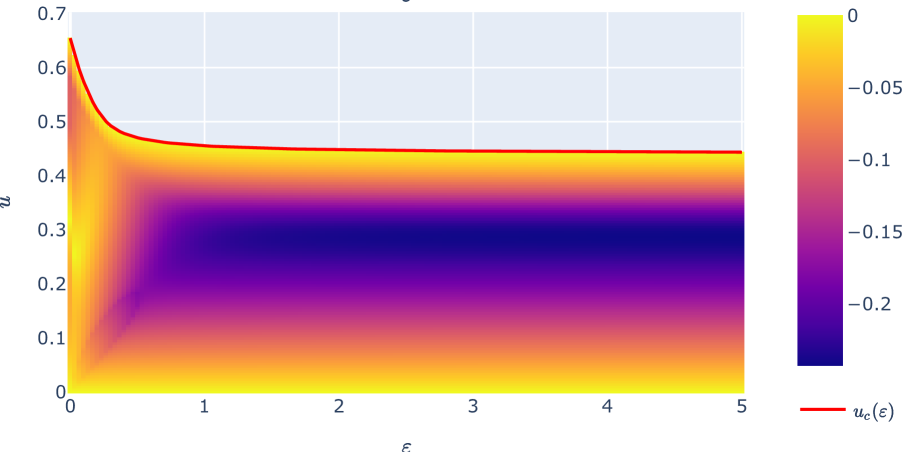

Comments on Fig. 9. The figure indicates for every such that the value of , the goal being to check numerically that is Hurwitz so that is locally asymptotically stable. Note that does not exist for .

5 Conclusion and perspectives

In this paper, we have addressed the question of global stability of the chemostat system including a perturbation term modeling any interaction type between species. In this context, the perturbation term depends on the species concentration (to model interaction between them) and on a perturbation parameter quantifying the amplitude of the perturbation w.r.t. the non-perturbed dynamics, but it may also depend on the substrate concentration. We have demonstrated a global stability result toward an equilibrium point in a subset of the invariant set (parametrized by a “small” parameter ) provided that the perturbation parameter is small enough. Our methodology relies on the combination of the Malkin-Gorshin Theorem [25] and a result by Smith and Waltman about the conservation of global attractivity when considering perturbed dynamical systems [27]. The index corresponds to the species that dominates the competition in the chemostat system (without any perturbation). Our result may not be sharp, however, as we noted, proving global stability within the invariant set (let’s say, for small enough) is likely a challenging problem. This is because, according to the competitive exclusion principle, solutions to the non-perturbed system do not converge to the equilibrium point when the initial condition is on the boundary of , specifically when .

Our approach has also shown that one can consider a large class of functions modeling the exchange term although accurate properties of the equilibrium point as given by Theorem 2.4 can be obtained whenever the perturbation term is linear w.r.t. species (but possibly non-linear with respect to the substrate). It is important to note that the global stability result has extended the study conducted in [4], which examined stability as the dilution rate approaches zero, to the case where the perturbation parameter tends to zero. When the exchange term depends linearly on , a numerical study of the system (asymptotic stability, operational diagram, computation of the Jacobian, etc.) supported the theoretical study conducted in two sub-cases (relying on whether the transition matrix depends on the substrate or not). These simulations highlight the fact that as soon as the exchange term is linear, then the globally stable equilibrium is such that all species are present asymptotically.

It would be interesting to prove that the coexistence steady-state is locally asymptotically stable for all such that (based on a thorough study of the Jacobian matrix which is a rank-one perturbation of a Hurwitz matrix). Additionally, it would be valuable to show the existence of a uniform bound on the perturbation parameter (i.e., independent of ), probably by using another approach (such as Lyapunov functions). This would allow us to obtain a global stability result for all initial conditions in . Another perspective beyond this work would be to carry out a similar analysis but in the case of a population dynamics model structured around a single phenotypic trait which can be seen as if we were considering an infinite number of species in the system.

Acknowledgements

We are grateful to Tewfik Sari for taking the time to have discussions on global stability of dynamical systems involving regular perturbations and for indicating to us references related to the Malkin-Gorshin Theorem.

6 Appendix

Proof of Theorem 2.2 (based on [27, Corollary 2.3]). Hereafter, stands for the spectral radius of a matrix .

Step 1. Let be fixed and recall that is a steady-state of (2.7) with , i.e., . By using standard results about the differentiability of the solution to an ordinary differential equation w.r.t. the initial condition, we have

| (6.1) |

where . Since is a Hurwitz matrix, we deduce that

Thus, there exist a norm on and a real such that

see, e.g., [28] for the existence of such a norm. By using the continuity of , there is (remind that is defined in (H1)) such that161616Here, stands for the open ball in (for the norm ) of center and of radius . and satisfying

| (6.2) |

By continuity of w.r.t. , we can also find such that

| (6.3) |

From (6.2), we deduce, thanks to the mean value inequality, that

| (6.4) |

Combining (6.3) and (6.4) then yields

Therefore, for every , is a contraction mapping from into itself. Using the uniform contraction mapping theorem, we deduce that there is a continuous mapping such that and such that for all , one has . Furthermore, the fixed point satisfies the following attractivity property:

| (6.5) |

Step 2. Our objective now is to prove the following:

| (6.6) |

i.e., that (6.5) holds true for all (and not only over ) up to reducing . Doing so, we claim the following:

| (6.7) |

To prove this property, we proceed by contradiction. It follows that there is a sequence such that and there is a sequence such that for all , and satisfying

Since is compact, we may assume that there is such that (extracting a sub-sequence if necessary). Now, for , is attracting in , thus there is such that Moreover, as , hence, there is such that

which is a contradiction, hence (6.7) holds true. Let now . By (H1), there is such that for all one has . Take such that so that . From (6.7), there is such that . We can now apply (6.5) which implies (6.6) as wanted.

Step 3. Take and let . By (H1) there exists such that for every , one has . Thus, we obtain from (6.6) that

But (6.6) also implies that as , hence, since is continuous,

We have thus proved that for every and for every , one has

| (6.8) |

We deduce that for , is a steady-state of (2.7), i.e., , so that by Cauchy-Lipschitz’s Theorem, one has for every . Finally, let us prove that for every and every , one has as . By contradiction, suppose that there exist , , , and with such that

Let us write where and . Since is bounded, there is such that, up to a sub-sequence, . By using (6.6) and the continuity of , we obtain

where the last equality follows from the fact that is a steady-state of (2.7).

Hence, we have a contradiction. We have thus proved that for all and for all , as which proves the desired result (taking ).

Proof of Theorem 2.3. We recall that the Euclidean norm of is denoted by . Hereafter, stands for the open ball in (for the Euclidean norm) of center and of radius . We start by proving the following property:

| (6.9) |

Let then be fixed. First, recall that is a Hurwitz matrix, hence is exponentially stable for . Since exponential stability implies B-stability (see [25]), Theorem 4 in [25] implies that there is such that for all , one has

| (6.10) |

Observe that , namely, because for any initial condition , one has from (6.10). Second, we claim that uniformly converges over to as . This result is standard and it follows by combining the local stability property of together with the compactness of and the continuity of an ordinary differential equation w.r.t. initial conditions (that is why, we omit the details). Applying this property then implies

| (6.11) |

Using the continuity of solutions to an ordinary differential equation w.r.t. a parameter, we get

| (6.12) |

Then, combining (6.11) and (6.12) yields

hence, for every and for every , one has . Set and let us given and . Applying (6.10) with yields

This, together with (6.11) implies that

since . Finally, (6.12) gives

We can then conclude that

This ends up the proof of the Theorem setting .

References

- [1] L. Altenberg, Resolvent positive linear operators exhibit the reduction phenomenon, Proceedings of the National Academy of Sciences, vol. 109, 10, pp. 3705–3710, 2012.

- [2] S.S. Arkin, Microbial evolution in the chemostat, PhD Thesis, 2010, http://hdl.handle.net/10044/1/11305.

- [3] G. Bastin, D. Dochain, On-line estimation and adaptive control of bioreactors, Elsevier, New York, 1990.

- [4] T. Bayen, H. Cazenave-Lacroutz, J. Coville, Stability of the chemostat system including a linear coupling, Discrete Contin. Dyn. Syst. Ser. B, vol. 28, 3, pp. 2104–2129, 2023.

- [5] T. Bayen, J. Coville, F. Mairet, Stability of the chemostat system including a linear coupling, Optimal Control Appl. Methods, vol. 44, 6, pp. 3342–3360, 2023.

- [6] T. Bayen, P. Gajardo, F. Mairet, Optimal synthesis for the minimum time control problems of fed-batch bioprocesses for growth functions with two maxima, J. Optim. Theory Appl., vol. 158, , pp. 521–553, 2013.

- [7] T. Bayen, F. Mairet, Optimization of the separation of two species in a chemostat, Automatica J. IFAC, vol. 50, 4, pp. 1243–1248, 2014.

- [8] T. Bayen, F. Mairet, Optimization of strain selection in evolution experiments in chemostat, Internat. J. Control, vol. 90, 12 , pp. 2748–2759, 2017.

- [9] D. Courgeau, Mutations, migrations et structures géniques, Population (french edition), pp. 935–940, 1969.

- [10] P. De Leenheer, J. Dockery, T. Gedeon, S.S. Pilyugin, The chemostat with lateral gene transfer, J. Biol. Dyn., vol. 4, 6, pp. 607–620, 2010.

- [11] P. De Leenheer, S.S. Pilyugin, Multistrain virus dynamics with mutations: A global analysis, Math. Med. Biol., vol. 25, 4, pp. 285–322, 2008.

- [12] E. Deutsch, M. Neumann, Derivatives of the Perron Root at an Essentially Nonnegative Matrix and the Group Inverse of an AA-Matrix, J. Math. Anal. Appl., 102, pp. 1–29, 1984.

- [13] D. Dochain, P. Vanrolleghem, Dynamical modelling and estimation in wastewater treatment processes, IWA Publishing, vol. 4, London, 2001.

- [14] C. Fritsch, F. Campillo, O. Ovaskainen, A numerical approach to determine mutant invasion fitness and evolutionary singular strategies, Theoretical Population Biology, vol. 115, pp. 89–99, 2017.

- [15] P. Gajardo, F. Mazenc, H. Ramirez, Competitive exclusion principle in a model of chemostat with delays, Dyn. Contin. Discrete Impuls. Syst. Ser. A Math. Anal., vol. 16, pp. 253–272, 2009.

- [16] J. Harmand, C. Lobry, A. Rapaport, T. Sari, The Chemostat: Mathematical Theory of Microorganism Cultures, Wiley-ISTE, 2017.

- [17] S.-B. Hsu, Limiting behavior for competing species, SIAM J. Appl. Math., vol. 34, pp.760–763, 1978.

- [18] H. Khalil, Nonlinear systems; 3rd ed. Prentice-Hall, Upper Saddle River, NJ, 2002.

- [19] C. Lobry La compétition dans le chémostat, Travaux En Cours 81 : Des Nombres et des Mondes, pp. 119–187, édition Herman, Paris, 2013.

- [20] J. Monod, Recherches sur la Croissance des Cultures Bactériennes, Hermann, Paris 1942.

- [21] J. Monod, La technique de culture continue théorie et applications, Ann. Inst. Pasteur, 79, pp. 390–410, 1950.

- [22] A. Novick, L. Szilard, Experiments with the chemostat on spontaneous mutations of bacteria, PNAS 36: pp. 708–719, 1950.

- [23] T. Sari, Nonstandard perturbation theory of differential equations, In: Invited talk at the International research symposium on nonstandard analysis and its applications, ICMS, Edinburgh, pp. 11–17, 1996.

- [24] T. Sari, Stroboscopy and long time behaviour in dynamical systems, Memorandum from Institute of Economic Research Faculty of Economics, University of Groningen, 1988.

- [25] T. Sari, B.S. Kalitin, B-stability and its applications to the Tikhonov and Malkin-Gorshin theorems, Differential Equations, Kluwer Academic Publishers-Plenum Publishers, Edinburgh, vol. 37, pp. 11–16, 2001.

- [26] H.L. Smith, P. Waltman, The theory of the chemostat, Dynamics of microbial competition, Cambridge University Press, 1995.

- [27] H.L. Smith, P. Waltman, Perturbation of a globally stable steady state, Proc. Amer. Math. Soc., vol. 127, 2, pp. 447–453, 1999.

- [28] E.Zeidler, Nonlinear functional analysis and its applications: Fixed-point theorems, Springer-Verlag, 1993.