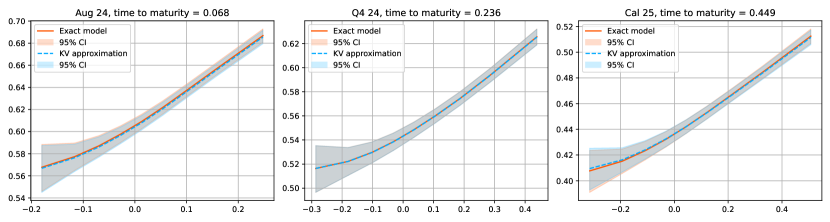

Heath–Jarrow–Morton meet lifted Heston in energy markets for joint historical and implied calibration

Abstract

In energy markets, joint historical and implied calibration is of paramount importance for practitioners yet notoriously challenging due to the need to align historical correlations of futures contracts with implied volatility smiles from the option market. We address this crucial problem with a parsimonious multiplicative multi-factor Heath-Jarrow-Morton (HJM) model for forward curves, combined with a stochastic volatility factor coming from the Lifted Heston model. We develop a sequential fast calibration procedure leveraging the Kemna-Vorst approximation of futures contracts: (i) historical correlations and the Variance Swap (VS) volatility term structure are captured through Level, Slope, and Curvature factors, (ii) the VS volatility term structure can then be corrected for a perfect match via a fixed-point algorithm, (iii) implied volatility smiles are calibrated using Fourier-based techniques. Our model displays remarkable joint historical and implied calibration fits - to both German power and TTF gas markets - and enables realistic interpolation within the implied volatility hypercube.

- Mathematics Subject Classification (2010): 91G20, 91G60

- JEL Classification: C02, Q41, C63

- Keywords:

-

Energy markets, Multi-factor HJM, Nelson-Siegel, Stochastic Volatility, Lifted Heston, Kemna-Vorst, Calibration

Introduction

In power markets, futures contracts deliver electricity continuously over a fixed period, rather than on a fixed delivery date as is typical for commodities like oil. These contracts are settled either physically or financially with respect to the average spot price of electricity over the delivery period. Due to the inability to efficiently store electricity in large quantities, these instruments are often referred to as swaps, as the holder effectively exchanges the forward rate against the spot price of the commodity.

The unique characteristics of electricity markets, such as the need to maintain equilibrium between real-time production and consumption, distinguish them from other commodity markets. Real-time delivery is typically managed through intra-day and imbalance markets, which align production and consumption levels and can exhibit frequent price spikes or even negative prices during periods of significant imbalance. Moreover, financial futures with very short-term deliveries often show low correlation with long-term futures, which are highly correlated among themselves. This behavior is accompanied by exponentially increasing realized volatility as the time to delivery reduces, the so-called Samuelson (2016) effect.

Following the deregulation of European electricity markets, an extensive body of literature has emerged on the modeling of electricity markets. We refer to the survey by Deschatre, Féron, and Gruet (2021) and the book by Benth, Benth, and Koekebakker (2008) for an overview of key modeling approaches and market dynamics.

Several approaches to energy market modeling are considered in the literature, differing in the choice of the initial stochastic quantity to be modeled. The first class of models focuses on the spot price process, as seen in works like Mishura, Ottaviano, and Vargiolu (2023); Schmeck and Schwerin (2021); Cortazar, Lopez, and Naranjo (2017). Another approach, inspired by the LIBOR market model , see Brigo and Mercurio (2006), models futures contracts with specific delivery periods (e.g., monthly contracts, as in Kiesel, Schindlmayr, and Börger (2009), Gardini and Santilli (2024)), using these contracts as building blocks to derive the prices of other contracts under no-arbitrage conditions. The third class of models, inspired by the well-known Heath, Jarrow, and Morton (1992) (HJM) interest rate model, takes infinitesimal futures contracts as a starting point and uses them to reconstruct futures contracts with any delivery period. This type of model ensures consistent dynamics across all futures contracts while also guaranteeing the absence of arbitrage between futures contracts with overlapping delivery periods.

Early commodity models primarily focus on historical calibration, which involves calibrating the covariance structure of traded futures contracts’ returns; see for example Andersen (2010) for the calibration of a HJM model to gas prices, Edoli, Tasinato, and Vargiolu (2013) for a multi-underlyings calibration using the quadratic variations of two-factor models for each market, Gardini and Santilli (2024) where they calibrate a LIBOR market Black-Scholes-type factor model using historical swap prices, and Féron and Gruet (2024) for a historical calibration of a multi-factor HJM model using maximum likelihood and a Kalman filter where they also comment on the number of factors to capture the historical covariance of futures’ returns.

Since April 2024, brokers have started quoting smiles for vanilla options on German power. These vanilla options are written on monthly contracts, quarterly contracts, and calendar (yearly) contracts, which can overlap. For example, the first quarter of 2025 and the calendar 2025 can have quoted smiles. Another specificity of the power market is that for one calendar underlying, three or four smiles can be quoted. With the increasing liquidity of the electricity derivatives market in Europe, there has been significant growth in research in option pricing in power market models, see Schmeck and Schwerin (2021); Cortazar, Lopez, and Naranjo (2017); Benth, Piccirilli, and Vargiolu (2017). However, few studies as in Piccirilli, Schmeck, and Vargiolu (2021); Musti, Fanelli, and Maddalena (2016) address the challenge of implied calibration, which involves calibrating model parameters to fit available option prices. Note that implied calibration in the energy market is exceptionally challenging, as it requires the simultaneous calibration of multiple volatility surfaces associated with different underlyings, which are interconnected through the futures price curve.

The most significant limitation of the models mentioned above is that they allow for either historical calibration or implied calibration, but not both simultaneously. Hence the following questions:

Is joint historical and implied calibration possible in energy markets?

If so, can we do it with a parsimonious and tractable model?

We answer both questions affirmatively with a parsimonious multiplicative multi-factor Heath, Jarrow, and Morton (1992) (HJM) model for forward curves, combined with a stochastic volatility factor coming from the Lifted Heston model of Abi Jaber (2019).

On the one hand, by capturing historical covariances and implied volatility levels, our model provides insights on the futures correlation structure between liquid and non-liquid futures contracts. On the other hand, implied calibration allows the entire implied volatility smile, not just the At-The-Money (ATM) volatilities, to be represented by the model. Moreover, the proposed implied calibration takes into account potential multiple maturities for a given underlying futures contract. Thus, the joint historical and implied calibration matches both the correlation between futures and quoted smiles –— a problem of paramount importance for market practitioners — leading to more accurate pricing of exotic contracts like Asian options or swing options. One potential difficulty is that implied calibration may affect the historical one, but we will see that this influence is negligible. To the best of our knowledge, this paper is the first to address both calibration problems with a single model, taking into account the entire implied volatility smile.

Contributions.

More precisely, to solve the joint historical and implied calibration problem, we introduce in Section 1 an HJM model with

-

(i)

parsimonious parametric Level, Slope and Curvature risk-factors in order to capture both historical covariances of rolling futures’ log returns and implied volatility levels with a few factors,

-

(ii)

two piece-wise constant functions to perfectly match the implied volatility term structure, including early maturities,

-

(iii)

a stochastic volatility component coming from the lifted Heston model with three time-scales to match the implied volatility skews.

Such model is by construction arbitrage-free with respect to futures contracts with overlapping delivery periods.

In Section 2, we present our Market data. We recall the typical liquid “absolute” futures quoting on power markets, we detail a stripping algorithm to construct rolling futures contracts satisfying absence of overlapping arbitrage and used to estimate historical covariances. Furthermore, we propose a novel multi-contract SSVI parametrization to extract Variance Swap (VS) volatilities from listed options.

Then, we detail a novel three-step sequential calibration methodology relying on the Kemna and Vorst (1990) (KV) approximation of futures contracts in order to

-

1)

jointly capture the historical covariances of rolling futures’ daily log returns and the implied VS volatility levels of absolute futures via a non-linear – linear cone program, see Section 3,

-

2)

correct and fit perfectly the VS volatility term structure via a fast fixed-point algorithm based on VS prices, see Section 4.2,

- 3)

It is worth noting that these three steps are decoupled, done sequentially and made highly tractable thanks to the KV approximation. Our model displays remarkable joint historical and implied calibration fits to both German power and TTF gas markets. In order to validate our calibration methodology, we show a posteriori how close the KV approximated futures are to the exact arbitrage-free futures in terms of sample trajectories, implied volatility smiles and correlations between futures contracts. Finally, we show that such a fully calibrated model can be used to interpolate the implied volatility hypercube in a consistent manner. The main calibration results are collected in Section 5. Additional model algorithmic insights and calibration results are postponed to the appendices.

Related literature.

The paper of Piccirilli, Schmeck, and Vargiolu (2021) is the work most closely related in spirit to our approach, although there are several important differences. The authors propose a two-factor model with Normal Inverse Gaussian Lévy factors, while our model is a stochastic volatility model with a continuous process as the variance. Their calibration procedure considers only one smile per contract, ignoring multiple maturities for a given futures contract. Our model accounts for these “early maturities”, enabling a more refined calibration of the volatility term structure.

Notations.

For , we denote by (resp. ) the set of definite (resp. semi-definite) positive matrices, and denotes a weighted Euclidean norm with weights such that . We define similarly the weighted Frobenius norm , with matrix weights . We will omit the indices and for standard Euclidean and Frobenius norms and respectively. We will also denote by the infinity norm and .

1 The model: HJM with lifted Heston

Fix a filtered probability space satisfying the usual conditions, where represents the risk-neutral probability. We model the futures price curve under , i.e. the infinitesimal futures contract prices , à la Heath, Jarrow, and Morton (1992) (HJM), enhanced with a stochastic volatility component coming from the lifted Heston model of Abi Jaber (2019) in the form

| (1.1) |

where

-

•

is an -dimensional Brownian motion with a correlation matrix .

-

•

Each is a deterministic continuous and bounded function, capturing the realized futures contracts’ covariances and the implied volatility levels. We set .

-

•

is a stochastic variance process responsible for the implied smile of the form

(1.2) where the factors , weighted by , are driven by the same Brownian motion , but mean-revert at different speeds such that

(1.3) Here is a one-dimensional Brownian motion correlated with , via , to take into account the leverage effect such that

(1.4) where is a scalar Brownian motion independent from which is a standard -dimensional Brownian motion constructed from via the Cholesky decomposition (see, for example, Horn and Johnson (2013))

(1.5) so that

(1.6) -

•

and are deterministic bounded positive functions correcting the implied volatility levels to match the volatility term structure for the contracts with several maturity dates.

For a fixed , represents the quote observed at date of the contract that delivers a unit amount of commodity between dates and , where denotes an infinitesimal amount of time. The special case is seen as the spot price of such a commodity: , which is well-defined as soon as .

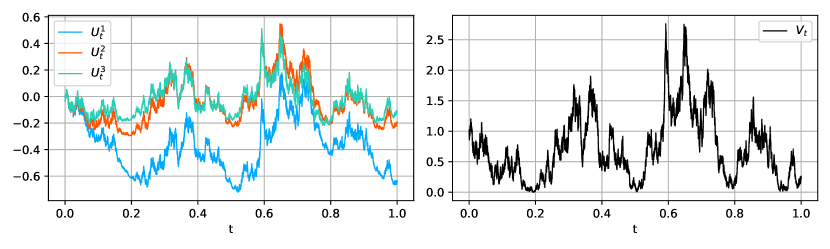

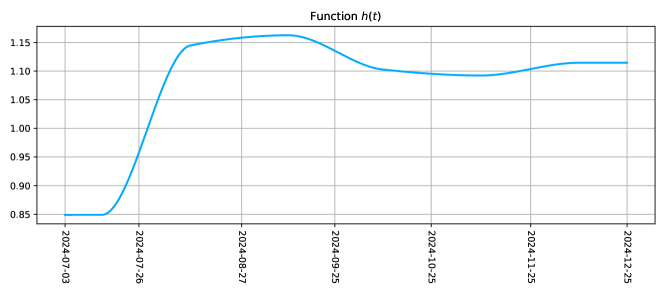

We prove in the next theorem that the model (1.1) is indeed well-defined leveraging results from Abi Jaber (2019). In particular, we note that although the different factors can become negative, the variance process is always nonnegative, as illustrated on Figure 1. Furthermore, the variance process (1.2) is Markovian in the state variables with a state space corresponding to the set of such that

where see Abi Jaber, Bayer, and Breneis (2024).

Theorem 1.1.

Proof.

The equation (1.1) can be rewritten as a one-dimensional diffusion,

| (1.8) |

where the Brownian motion is given by

| (1.9) |

The factor processes can be written as

| (1.10) |

so that the variance dynamics (1.2) reads

| (1.11) |

where . The equation (1.11) means that is a Volterra square-root process understood in the sense of (Abi Jaber, Larsson, and Pulido, 2019, Section 6). An application of (Abi Jaber, 2019, Theorem A.1) yields the existence and uniqueness of strong solution , such that the variance process , as well as the existence and uniqueness of the strong solution to (1.8) given by (1.7). The proof of the martingality of follows exactly the proof of (Abi Jaber, Larsson, and Pulido, 2019, Lemma 7.3) taking into account that the correlation coefficient in (1.8) is time-dependent. ∎

In practice, the infinitesimal futures contracts given by (1.1) are not observed in the market and therefore must be related to market traded futures contracts. Using practitioners’ vocabulary, “absolute” futures contracts delivering electricity on a fixed calendar delivery period are typically quoted in organized markets until a few days before their first delivery date i.e. for dates such that , equal to a few days. We recall in Section 2.1 the typical futures quoting in power markets. From the model perspective, the unitary absolute futures contract delivering continuously a unitary power unit of electricity over is given by111We assume a zero discount rate () for simplicity.

| (1.12) |

ensuring the absence of arbitrage opportunity for futures contracts with overlapping delivery periods.

On the other hand, a “rolling” futures contract is a contract that depends on the observation date, , and maintains a constant time to delivery, , with a fixed and contiguous delivery period of duration . As a result, the contract’s delivery period adjusts as the observation date changes, ensuring that the contract always quotes. However, its quote is typically not directly observable in the market. Instead, it must be derived using no-arbitrage principles based on market quotes available at each observation date. Its quote is expressed in our model by the formula

| (1.13) |

Example 1.2 (Distinction between absolute and rolling futures).

For example, on the of August 2024, the next absolute monthly futures contract quoting on the market corresponds to the contract September 2024 delivering electricity between the to the of September 2024. Fixing to seven days, and to thirty days, one can define a month-ahead rolling contract delivering electricity from the of August to the of September 2024. On the of August 2024, such rolling contract becomes the one delivering electricity from the of August to the of September 2024, while the forward September 2024 keeps the same delivery period.

1.1 The Kemna-Vorst approximation

The dynamics of the futures contract cannot be written explicitly in our model, since (1.12) involves an arithmetic mean, and not a geometric one. For this reason, we will use the Kemna and Vorst (1990) approximation such that

| (1.14) | ||||

| (1.15) | ||||

| (1.16) |

where

| (1.17) |

Consequently, the approximated dynamics of the futures contract is given by

| (1.18) |

We stress that depends essentially on and , but for the sake of brevity, we omit these arguments. The equation (1.18) admits

| (1.19) | ||||

| (1.20) |

as the unique strong solution, recall Theorem 1.1 for the existence and uniqueness of .

Recall that futures contracts’ quotes defined by (1.12) are free from arbitrage opportunities in the case of overlapping delivery periods. In contrast, arbitrage may arise in the Kemna-Vorst approximated futures prices from (1.19), as they do not strictly satisfy (1.12). However, such approximated futures’ quotes offer a tractable approach for calibration including

-

•

the explicit computation of their variance swaps’ volatilities as shown in the next Section 1.2,

-

•

the explicit computation of their covariances as detailed in Section 3.1,

-

•

the fast pricing of call and put options written on such futures contracts using a Fourier inversion technique as shown in Subsection 4.1.

Once the model (1.1) is calibrated using the Kemna-Vorst approximated futures , we will illustrate numerically a posteriori that, not only are the trajectories of the arbitrage-free futures’ quotes’ similar to the ones of , but also that their instantaneous futures correlation structure and associated vanilla option prices are nearly identical. Indeed, all these quantities with respect to futures with quotes given by (1.12) can be approximated by Monte-Carlo techniques as detailed in Section 5.2.

From now on, we fix a delivery period and use the approximation everywhere instead of the exact dynamics. Accordingly, we also use the notation , leaving the delivery period implicit when there is no ambiguity.

1.2 Variance swap price and volatility

By definition, the variance swap price with maturity , denoted by , is the expected integrated quadratic variation of the futures contract following the dynamics (1.18) given by

| (1.21) |

and the variance swap volatility satisfies the equation , so that

| (1.22) |

Why considering variance swaps for calibration?

The variance swap volatility is a zero-order approximation of the ATM volatility level as shown by Bergomi and Guyon (2011), allowing us to formalize the idea of the implied volatility smile level.

In fact, in our model (1.1), variance swap prices (1.21) depend the functions and also , via the deterministic futures’ volatilities (1.17), but not on the parameters of from (1.2) since we conveniently set . This allows to first calibrate the variance swap prices, i.e. the smile level with the functions and , and then solve independently the smile shape calibration problem with the parameters of .

Furthermore, the evaluation of the variance swap prices (1.21) turn out to be in practice less time-consuming than the evaluation of ATM volatilities since they are given by the closed formula (1.21), while the ATM volatilities are extracted via the Lewis formula (4.1) which require the computation of the log-price characteristic function, see Section 4.1 for more details.

Although Variance Swaps (VS) are not traded in power markets, their market prices can be extracted efficiently from the prices of vanilla option quotes as shown in Section 2.2.2. Thus, given a family of futures contracts whose smiles are quoting, these VS volatilities (1.22) define the implied volatility term structure that we will aim to calibrate by fitting a priori , and then perfecting the match with the functions and .

For now, let us introduce a flexible parametrization for the functions .

1.3 A Nelson-Siegel parametrization for the volatility functions

Back in 1985, Charles B. Nelson and Andrew F. Siegel proposed in Nelson and Siegel (1987) the following “parsimonious” parametrization for the instantaneous forward rate with days to maturity

| (1.23) |

as an alternative to the previously used polynomial fitting techniques to match the yields of US Treasury bills of maturity , obtained in their formulation by integrating from zero to the forward rate (1.23) and dividing by . They showed that such expression of the forward rate has a desirable non-explosive asymptotic behavior, and is capable of reproducing humps, -shapes, and monotonic curves.

In our case, the volatility functions in the HJM model (1.1) aim at capturing with parsimony both the realized covariance structure of a family of rolling futures contracts’ daily log returns as well as the VS volatility term structure of the futures contracts whose smiles quote in the market.

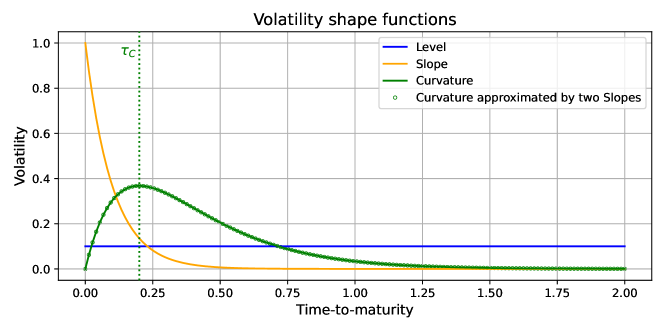

Inspired by the Nelson–Siegel parametrization (1.23), we specify three possible forms for the volatility shape functions , which yield respectively three distinct types of factors, named Level (), Slope () and Curvature (), including

-

•

one -factor which has a constant volatility function in order to capture the long-term volatility level of the curve

(1.24) -

•

-factors having an exponentially increasing volatility as time to maturity decreases to capture the Samuelson (2016) effect

(1.25) -

•

-factors aiming at capturing “humps” in the volatility term structure, thereby capturing potential “anti-Samuelson effect” for long-term deliveries, i.e. a decreasing volatility with time to maturity, such that

(1.26)

with such that . We display in Figure 2 the three distinct volatility shapes in terms of time to maturity.

The use of both and factors is not new, see for example Kiesel, Schindlmayr, and Börger (2009), Gardini and Santilli (2024). By contrast, we are not aware of previous works trying to calibrate factors to power markets. Notice in particular that both - and -factors vanish when time to maturity goes to infinity, i.e. , hence only the -factor remains in such regime and therefore captures the long-term volatility level of the energy curve.

Consequently, such -- parametrization writes explicitly as

| (1.27) |

In a similar spirit as Nelson and Siegel (1987) who noted that their parametrization (1.23) can be easily fitted to market data by least-squares, given a provisional , fixing the parameters , in (1.27) leads to an efficient calibration problem for the remaining parameters of the -- factors, and their correlation matrix formulated as a linear cone program ensuring that remains non-negative definite as detailed in Section 3.

Remark 1.4 (Are -- volatility shapes redundant?).

On the one hand, notice that taking in a -factor parametrization (1.25) yields a -factor parametrization (1.24). Moreover, by considering two perfectly anti-correlated -factors with identical parameters and distinct mean reversion rates, it is possible to approximate the behavior of a -factor parametrization (1.26) as illustrated in green dots in Figure 2. Thus, it is indeed reasonable to restrict oneself to -factors only to identify systematically in the market those distinct level, slope and curvature volatility behaviors but to the price of losing parsimony, as was done for example in Féron and Gruet (2024). On the other hand, a single curvature shape cannot approximate properly either a level or a slope volatility shape, nor a level shape can approximate neither a slope or a curvature shape.

1.4 Joint calibration: overview and snapshots

The main practical advantage of our model is the possibility to decouple the joint calibration problem into three independent optimization problems to be solved consecutively, without the need to modify the parameters calibrated in previous steps.

-

1)

A combined historical and implied calibration of the parameters () to capture with parsimony i.e. with a minimum number of deterministic risk factors, the historical correlation of rolling futures contracts’ daily log returns as well as the overall term structure of the implied VS volatility deduced from the market quotes of vanilla options.

-

2)

An exact calibration correction of the term structure of the implied VS volatility not captured in step 1), thanks to the functions and .

-

3)

A calibration of the entire shape of the smile using the parameters of the stochastic variance process in (1.2), that is and .

The flow chart in Figure 3 illustrates the successive calibration procedure with the data used in each step as well as the resulting calibrated model parameters.

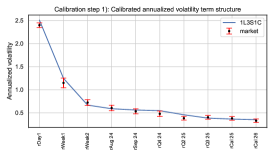

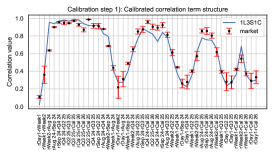

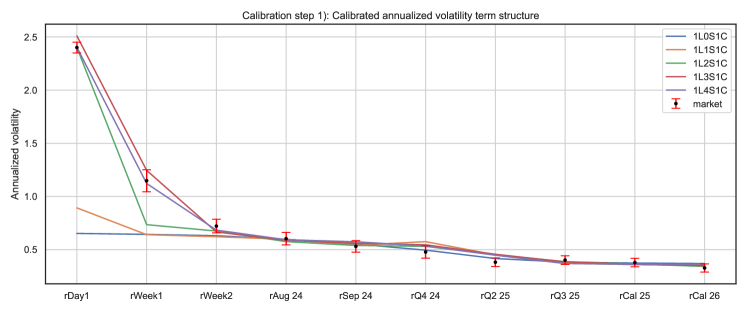

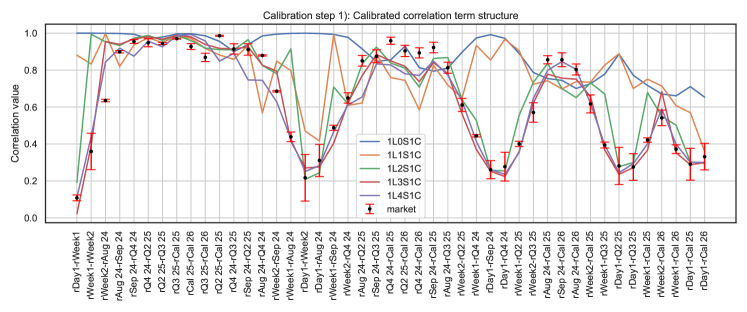

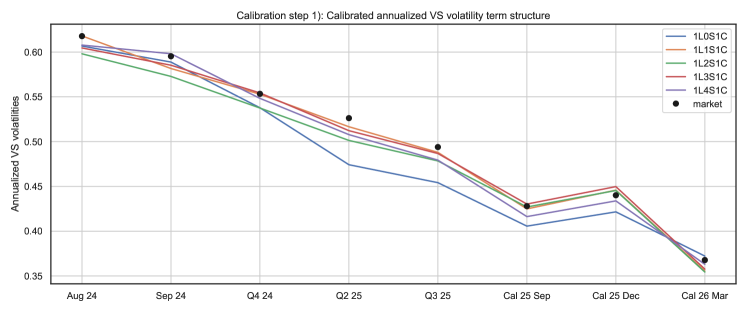

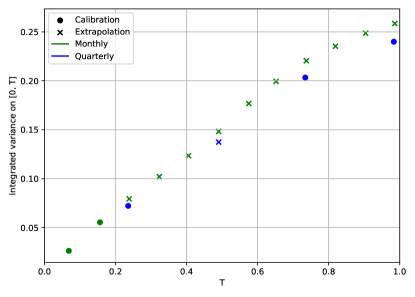

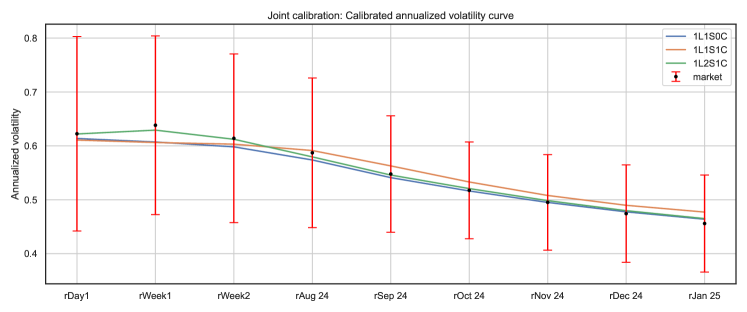

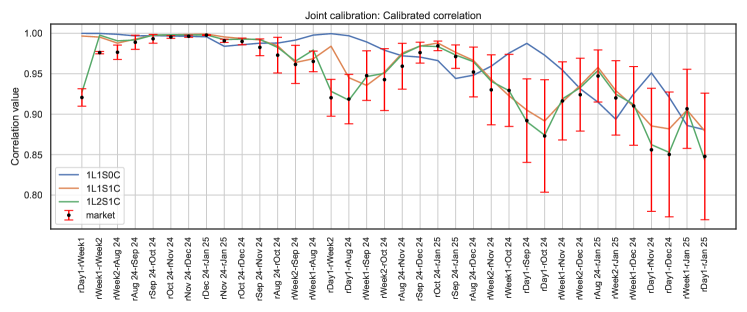

In Figure 4, we provide a calibration snapshot that summarizes the results of all three calibration steps for the case of the German power market as of the of July 2024. For this date, -- risk factors with , , and stochastic volatility factors were used, which yields 222Our choice of 19 parameters (5 factors) remains conservative compared to the literature on historical calibration in power markets: Féron and Gruet (2024) consider 5 -factors (20 parameters), Gardini and Santilli (2024) use 10 factors with parameters to fit the realized volatility of futures from six different markets, and a PCA study in Koekebakker and Ollmar (2005) supports a similar order of factors. (resp. ) calibrated parameters for step 1 (resp. step 3). Our model achieves an excellent fit of the historical volatilities and correlations in step 1, a perfect fit of the VS term structures in step 2 and a remarkable fit of the whole implied volatility surface in step 3, see also Figure 15. More detailed specification of model factors and calibrated parameters will be described further in Section 5.1.

2 Market data

2.1 Futures contracts’ quotes

The market data used to calibrate the futures contracts’ instantaneous correlation structure are the realized closing market quotes of unitary base-load333The other main traded profile, although less liquid, is the peak-load delivering electricity during working hours of the week. We chose to focus on the base-load data for illustrating our approach. futures contracts i.e. typically the price per MWh for the delivery of electricity every hour of a given delivery period444A precise specification of the contract can be found at https://www.eex.com/en/markets/power/power-futures for the German power market and at https://www.theice.com/products/27996665/Dutch-TTF-Gas-Futures for futures traded on the TTF gas market.. We present here several types of liquid futures contracts on power markets, these notations that will be used further in Section 4.

-

•

Day-ahead contracts, denoted by DayX with , typically the day-ahead contract (DA1) whose price is set by auction for the delivery of electricity for the following day, with set to the first hour of delivery the next day and equals plus one day.

-

•

Week-ends, denoted by WeekX with , working days or week-ahead contracts, and also balance of month contracts which quotes the price of delivery of electricity such that, in theses cases, is set accordingly depending on the observation date, and equals plus, respectively, two days, five days and the number of days until the end of the running month.

-

•

Monthly contracts denoted by Mon YY: delivering during the fixed month “Mon” of the year “20YY”. For these contracts, an are equal to the first and the last day of the delivery month.

-

•

Quarterly contracts denoted by QX YY: delivery period is the “X”-th quarter of the year “20YY” with X . Here, the first quarter corresponds to the first three months of the year, the second one corresponds to the forth-sixth months, and so on. In this case, is equal to the first date of the first month of the quarter, and is the last day of the last quarter month.

-

•

Calendar contracts denoted by Cal YY: contracts delivering during the whole year “20YY”. and correspond to the first and the last days of the year.

Similarly, we use the notation rContract to refer to the rolling future contract with same time to delivery and delivery duration as Contract.

2.1.1 Stripping optimization to construct rolling futures contracts

Recall that, except for the first day-ahead contract, a rolling futures contract with time to delivery and delivery duration is typically not exchanged in standard markets555Although at some specific observation dates , a rolling future with time to delivery and delivery duration may coincide with the absolute futures contract delivering on if (2.1) , and therefore its quote cannot be observed directly. Yet, it is possible to construct the quotes of such rolling futures contracts from the ones of the absolute futures contracts observed on the market via a stripped forward curve defined as follows.

Definition 2.1 (Stripped forward curve).

Fix an observation date and consider a family of absolute futures contracts’ quotes

and denote . Then, a stripped forward curve, at observation date , is a smooth666 can be uniquely defined when some additional regularizing criterion is imposed. price curve such that the absence of superposition arbitrage opportunities is verified, i.e. such that the equality constraints

| (2.2) |

are all satisfied. In particular, the quote of any rolling contract at date can be obtained from the stripped forward curve by the following formula

| (2.3) |

and we define its realized, or historical, log returns over a period of days at date by

| (2.4) |

where the delivery period is held fixed, so that their respective sample Fourier spectra (resp. auto-correlations) don’t display any significant frequency peak (resp. lag) i.e. absence of weekly effect from working days to week-ends (resp. independent increments assumption) hold valid with such log returns construction, see for example (Cartea and Figueroa, 2005, Figure 4) or (Gardini and Santilli, 2024, Figure 3).

In order to formulate the stripping optimization problem, we use the same notations as in Definition 2.1, and we set the daily time grids

| (2.5) | ||||

| (2.6) |

where (resp. ) denotes the number of days in the time interval (resp. in ).

As detailed in Definition 2.1, the stripping optimization problem aims to build a stripped daily forward curve from a family of absolute forwards’ quotes observed on the markets such that

-

(i)

the absence of superposition arbitrage opportunities (2.2) is satisfied;

-

(ii)

a smoothing criterion is applied ensuring the well-posedness of the algorithm: the sum of daily increments of the curve squared is minimized.

Then, the daily stripped forward curve at observation date is given by , where is defined as the unique minimizer of

| (2.7) |

with denoting the set of admissible curves defined by

| (2.8) |

and where, for , denotes the family of daily weights associated to the forward depending on the profiling of the underlying delivery, e.g. for a calendar contract in base profile.

The optimization problem (2.7) can be reformulated as a Quadratic Program with linear equality constraints in the sense of (Boyd and Vandenberghe, 2004, Chapter 4, 4.4) and admits a unique solution by strict convexity. Market data should be without absence of arbitrage to ensure the existence of such solution. Some day-ahead futures contracts may display negative quotes, hence in general, yet it is possible to look for a non-negative stripped curve by adding the constraints if all the quoting market futures contracts are non-negative. The interested reader may look at (Benth and Koekebakker, 2008, Chapter 7) for additional insights on stripping including seasonal effects.

2.1.2 Estimated covariance of rolling futures’ log returns from past historical data

Given a family of stripped forward curves constructed at various observation dates by solving the stripping optimization problem (2.7), we can reconstitute any family of rolling forward contracts satisfying for any using (2.3), and then estimate a family of time series of their respective realized daily log returns by setting day using (2.4).

Without any surprise, the rolling futures’ log returns display heavy tails across all deliveries, and particularly for short-term ones. Since the futures’ log returns’ historical covariances will be used to calibrate a log normal distribution under the KV approximation (1.16) in the first calibration step, i.e. calibrate , with specified in (1.27), we first filter out futures contracts’ log returns’ large values away from three standard deviations (computed on the whole time-series) and setting them equal to three standard deviations, in the same spirit as in Cartea and Figueroa (2005).

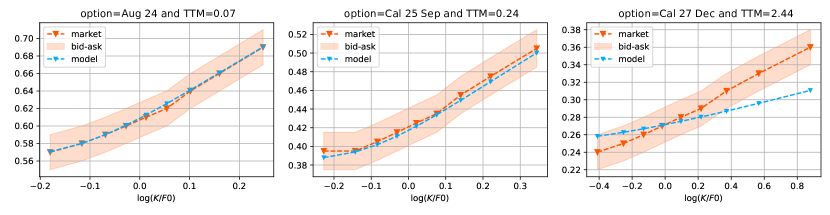

Then, we construct a biased averaged covariance estimator of such daily log returns in order to assign higher weights to newer data points and diminishing weights to older data, and we extract some confidence bounds when weighting differently the past observations. We postpone to Appendix B.1 the detailed estimation procedure.

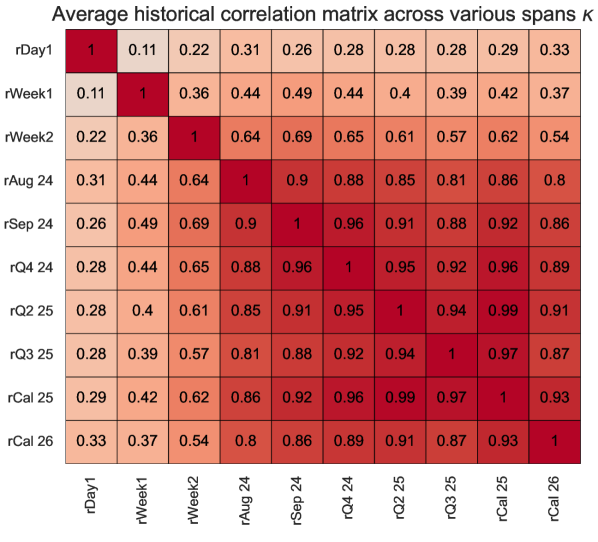

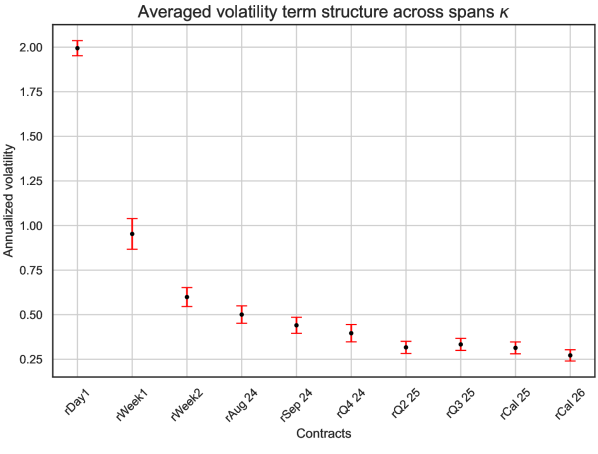

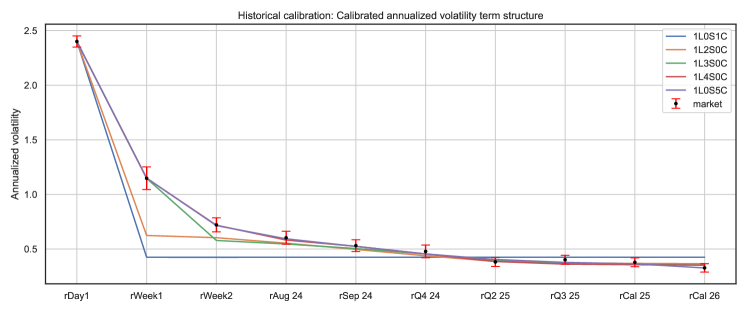

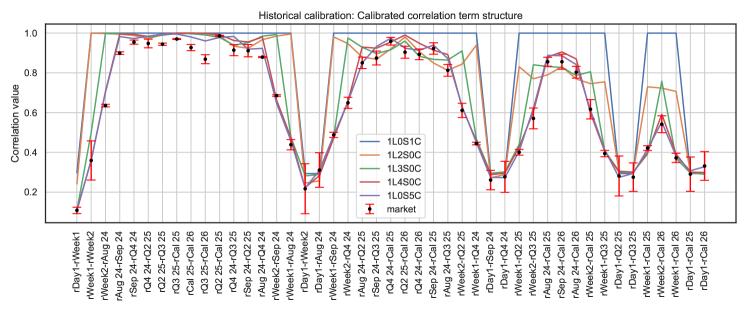

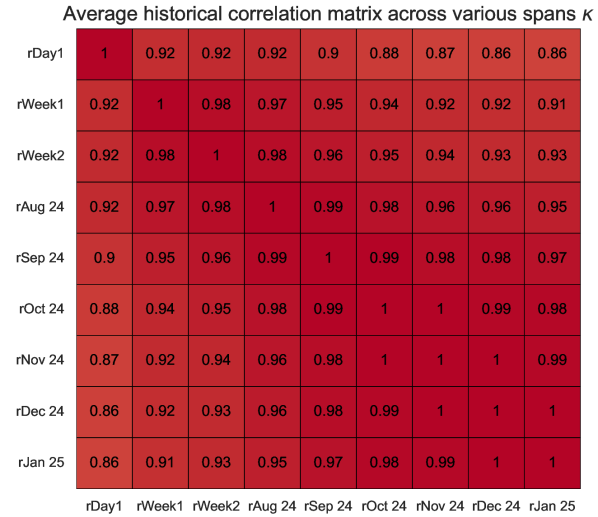

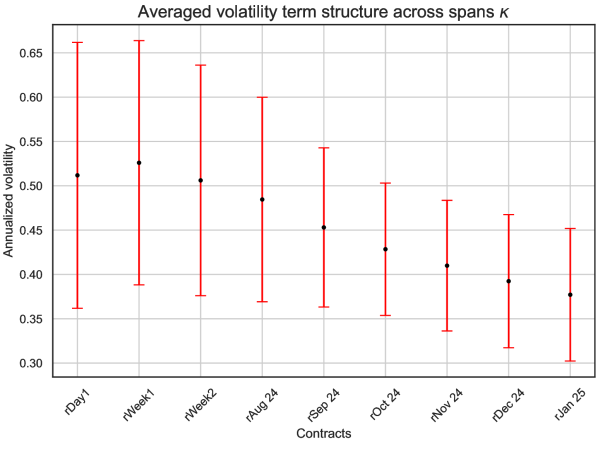

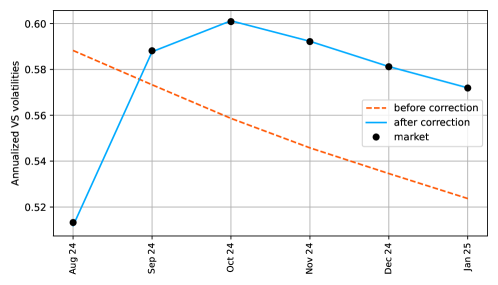

Finally, we extract the futures contracts’ volatilities by taking the square root of the diagonal of the resulting covariance estimator, and their correlations by normalizing their respective covariances by the corresponding volatilities. Figure 5 displays the resulting realized correlation and volatility term structures on the German power market from January 2023 to July 2024.

2.2 Options data

2.2.1 Typical options quoted in power markets

We are interested in calibrating a diverse set of volatility smiles corresponding to different underlying futures contracts. The most liquid options are typically written on three types of underlying futures contracts: the first few months, quarters and calendar contracts. These liquid options are linear combinations of vanilla options like call spreads, put spreads, butterflies or fences. The descriptions of vanilla options can be found on the ice website (ICE).777https://www.ice.com/products/65898946/German-Power-Financial-Base-Options

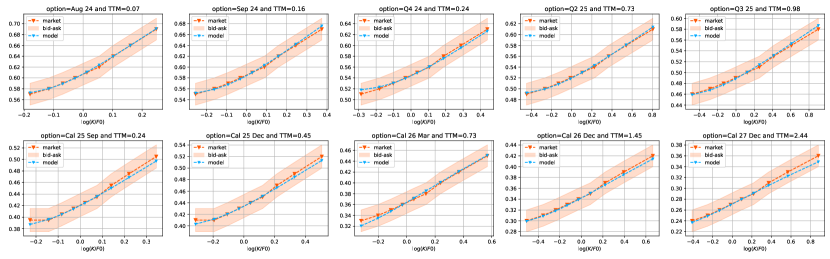

Vanilla options on monthly or quaterly futures have a single maturity: they expire several business day before the first day of the delivery period. However, vanilla options on calendar futures can have different maturities. The December maturity is generally the most liquid. The other maturities such as September, June and March — referred to as early expiries — are also quoted. To avoid confusion, the maturity month (of the year preceding the delivery year) is specified in the option name. For example, “Cal 26 Mar” corresponds to the smile with maturity at the end of March 2025. The precise maturities can be found on the site of the European Energy Exchange (EEX)888https://www.eex.com/en/market-data/power/equity-styled-options.

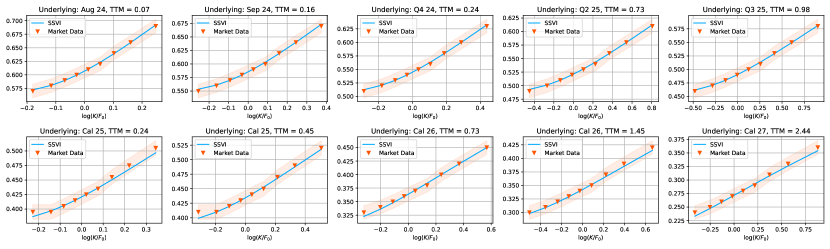

For our numerical experiments, we use the following ten implied volatility smiles observed on the on the July 2024 from the German power option market corresponding to eight different underlying futures contracts: Aug 24, Sep 24, Q4 24, Q2 25, Q3 25, Cal 25 Sep, Cal 25 Dec, Cal 26 Mar, Cal 26 Dec, Cal 27 Dec.

2.2.2 Variance swaps deduced from option prices

Variance Swap (VS) volatility can be interpreted as an overall smile level and will be used for the first two steps of calibration, recall Figure 3, and can be deduced from VS contracts, recall Section 1.2. As already mentioned, such contracts are not quoted on power markets. However, we show how variance swap market prices can be extracted from vanilla option prices.

Indeed, these prices can be expressed as prices of European options with logarithmic payoff, further referred to as log-contracts, that can be extracted from the implied volatility smile by the Carr and Madan (1998) formula:

| (2.9) |

where and denote respectively the prices of put and call vanilla options.

Notations.

The calibration will be performed on call and put options written on the futures contracts for , where the -th futures contract is identified with its delivery period . For , we denote by the number of (sorted) maturities i.e. the number of smiles, associated to the underlying . The implied market data contains a family of European call and put option prices

where denotes the number of underlyings, denotes the set of strikes corresponding to maturity , and (resp. ) denotes the price of the European call option with maturity , strike , and underlying . We denote by the corresponding Black implied volatility.

The market price of the variance swap with underlying and maturity is deduced from the call and put options by (2.9) as follows

| (2.10) |

where stands for the initial price of the -th underlying futures contract. Then the VS volatility is extracted by

| (2.11) |

Typically, the number of strikes per smile (no more than ) present in market data is not enough to apply the discretized formula (2.10) directly. Thus, a consistent smiles arbitrage-free extrapolation model is needed. An example of such a model for surface parametrization is given by the SSVI parametrization of Gatheral and Jacquier (2014). However, in our case, multiple surfaces are present at the same time, and a more general model is needed. Thus, we propose a multi-contract SSVI parametrization of the implied volatility surfaces for all contracts which allows us to interpolate and extrapolate the smiles and compute numerically the integrals in (2.10).

Multi-contract SSVI parametrization.

Initially introduced by Gatheral and Jacquier (2014), the Surface SVI (SSVI) parametrization specifies the total implied variance , with corresponding time to maturity and log-moneyness . Namely, the implied total variance of the -th futures contract is given by

| (2.12) |

where

-

•

is the at-the-money (ATM) total variance of the underlying ;

-

•

is a skew parameter interpreted as a spot-vol correlation for the contract ;

-

•

is a parametric function satisfying a list of conditions to guarantee the absence of static arbitrage.

Due to the presence of multiple surfaces to be parametrized together, we specify individual correlation parameters for each contract , and a common function since we assume the same nature of volatility across all the underlying futures contracts. This choice appears consistent with observed market data and allows us to simultaneously parametrize all the volatility surfaces using a small number of parameters. We set

and

which is consistent with the empirically-observed term structure of the volatility skew and such that (2.12) generates static-arbitrage-free surfaces for the respective futures contracts (Gatheral and Jacquier, 2014, Remark 4.4).

A calibrated multi-contract SSVI model allows itself for an efficient smile interpolation and extrapolation for a fixed maturity as well as for a surface extrapolation for the contracts being in the calibration set. However, in contrast to the HJM stochastic volatility model (1.1), it cannot generate a volatility surface for a futures contract not present in the calibration set unless its ATM volatility and correlation parameter are provided. Thus, it can interpolate individual volatility surfaces, but not the volatility hypercube. That is why we limit our use of this parametrization to the evaluation of the implied variance swap prices (2.9). In addition, the calibrated values can be further used to obtain an initial guess for the spot-vol correlations in the smile calibration procedure.

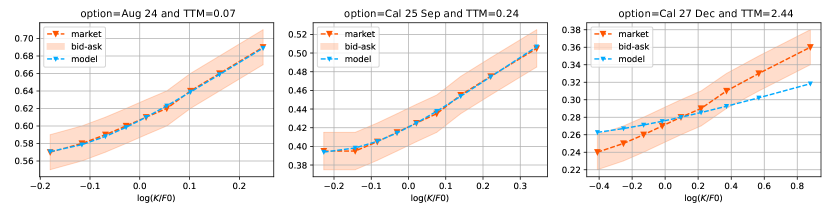

The results of the multi-contract SSVI calibration to the market data are shown in Figure 6. We show a bis-ask spread as well to give an idea of the parametrization quality. The value of spread is consistent with actual market liquidity and will be further used as a benchmark for smile calibration.

3 Calibration methodology for historical covariances and Variance Swaps (VS)

For such calibration step, we set

| (3.1) |

in (1.1). Our aim is to calibrate the risk factors’ volatility functions as well as their correlation matrix in order to match

- •

-

•

the VS volatility term structure estimated from market data using the Carr-Madan formula (2.9) for the respective deliveries and maturities associated to implied volatility smiles corresponding to different underlying futures contracts.

First, we derive explicit formulas of the normalized integrated covariance of rolling futures contracts’ log returns and of the VS volatility when the infinitesimal forward rate’s dynamics is given by the -- specification of the form (1.27).

3.1 Explicit model covariance and VS volatility term structure

Let denote the number of days considered for the historical past horizon and a period in days. In this section, we derive explicit formulas for the covariances of the rolling futures contracts’ log-returns as well as their VS volatilities under the KV approximation (1.16).

Stationarity of rolling futures’ volatility.

To start with, by leveraging the stationary property of the -- volatility functions (1.24)–(1.25)–(1.26), that is

| (3.2) |

see for example Andersen (2010) for additional insights on this property, we readily obtain, by a change of variable, the following stationary property of the volatility (1.17) of the rolling forward contract such that

| (3.3) |

Following the definition of the rolling forward contract (1.13) delivering on , we define its log returns over a period of -days under the KV approximation by

| (3.4) | ||||

| (3.5) |

Lemma 3.1.

Fix two rolling futures contracts with respective time to deliveries and delivery durations . Define their normalized integrated covariance of their respective log returns over a period of -days at observation date by

| (3.6) |

Then, the covariance is explicitly given by

| (3.7) |

and is independent of the observation date .

Proof.

Straightforward calculus yields

| (3.8) | ||||

| (3.9) | ||||

| (3.10) |

where we used respectively the change of variable and the stationary property of the volatility function (3.3) to get the second and third equalities. ∎

Separability of rolling futures’ volatility.

Furthermore, notice that the respective , and volatility functions (1.24), (1.25) and (1.26) enjoy the following separable property such that for any

| (3.11) |

with , and some explicit functions depending only on parameters , and where denotes the total number of separable state variables . Notice that both and -factors are readily identified to their unique state variable respectively, while, for we can decompose the -factor as the sum of two separable state variables and such that

| (3.12) |

where we define the volatility functions associated respectively to and by

We detail in Table 1 the explicit functions and for the four distinct state variables .

We are now ready to derive the explicit formulas of the rolling futures contracts log returns and VS volatilities which will play a key role in the formulation of the first step calibration problem.

Proposition 3.2.

Using the same notations as in Lemma 3.1, the normalized stationary covariance (3.7) is explicitly given by

| (3.13) |

where, for , we set the variables

| (3.14) |

and

| (3.15) |

with .

Similarly, the variance swap variance level (1.22) is explicitly given by

| (3.16) |

Proof.

3.2 Loss function for the historical covariances - VS volatility term structure calibration problem

We consider Variance Swap (VS) contracts with respective maturities and volatilities computed using (2.11). Such VS contracts are indeed associated to the implied volatility smiles we aim to calibrate the initial model (1.1) on, whose underlying are respectively the futures contracts with delivery periods , recall the notations from Section 2.2.2.

Denote by the number of past observation days until the date of calibration considered for the calibration. Then we introduce a family of rolling contracts constructed by solving (2.7) and we use their respective daily log returns time-series

computed from (2.4), for the estimation of the historical daily log returns’ covariances via the estimator (B.4). In our case, we typically chose , with the set of the rolling forwards’ delivery periods including those of the absolute underlying futures contracts, i.e.

to ensure that the historical covariance term structure captures a priori, somehow, the futures correlation structure of those absolute futures.

We introduce a convex combination of losses between the fit of historical log returns’ variance-covariance term structure of rolling forward contracts and the fit of the implied variance swap volatility levels such that

| (3.17) |

with

| (3.18) | ||||

| (3.19) |

where the entry of and entry of are respectively given by (3.13) and (3.16), while and are respectively estimated by (B.4) and (2.9). Furthermore, denotes a family of weights associated to the matrix Frobenius norm, while are weights for the vector Frobenius norm, specified respectively as in (B.5) and uniformly in our case. Finally, notice that the hyper-parameter conveniently controls the trade-off between the fit of the historical covariances and that of the VS volatility term structure.

Then, for a fixed , the joint historical - VS variance term structure calibration is formulated as the following minimization problem under constraints

| (3.20) |

where the admissible set of parameters is given by

| (3.21) |

The functional (3.17) is clearly non-convex in , depending in particular on exponential terms in the parameters , so we cannot guarantee a priori the existence of a global minimizer of such optimization problem (3.20).

3.3 Solver specification

The admissible set of parameters (3.21) can be very large, with dimension in , where recall is the total number of factors in the Nelson-Siegel parametrization (1.27), and include positive constraints as well as a non-trivial positive definite cone constraint for the correlation matrix . In order to simplify and fasten the numerical implementation of the optimization problem (3.20), we start by noticing the three following facts.

- (i)

-

(ii)

Note that the loss functional (3.23) is expressed in terms of the state variables, and for each , the -factor has two state variables sharing the same parameter and the same Brownian motion so that we need to impose the following equality constraints on the variables (3.14) ordered as such that

(3.26) -

(iii)

(resp. -factors) are inter-changeable, which may cause numerical instability.

Successive non-linear – linear cone program formulation.

Consequently, instead of solving (3.20) globally, we will solve the following iterative minimization problems

| (3.27) |

On the one hand, the outward minimization is performed by an unconstrained non-linear solver (e.g. Powell minimizer from SciPy), where we optimize on the parameters

| (3.28) |

such that the following change of variables

| (3.29) |

ensures that the parameters are indeed positive and strictly increasing for the -factors and the -factors respectively.

Solver initialization and optimal parameters extraction.

All that remains to do is to initialize properly the outward non-linear solver in the iterative formulation (3.27) and then extract the optimal parameters upon convergence. Indeed, a good initialization is of paramount importance to be able to reach a good local minimum in practice.

Fortunately the solver algorithm runs relatively fast, from a few seconds to a few minutes depending on the number of factors, so we can afford to iterate over various randomized initial guesses. As a rule of thumb, we construct the initial values starting from the mid-points of delivery periods such that the resulting factors with time-scales cover reasonably well the futures curve across all deliveries. In our case, since we have and , we first reduce the number of such mid-points by taking convex combinations of them to the number of and factors, and then add up some randomness to obtain the initial positive .

Once an optimizer of the iterative optimization problem (3.27) has been reached, then we extract the optimal parameters injecting into (3.29), and by positive-definiteness of the calibrated -- factors’ covariance (extracted from an optimal solution of (B.7), with denoting the set of indices relative to state variables, of cardinal ), we get

| (3.30) |

and

| (3.31) |

Remark 3.3.

Note that the linear cone program (B.7) only guarantees the matrix to be semi-definite positive while the inversion formulas (3.30)–(3.31) are well-defined if is positive definite. If zero happens to belong to the spectrum of , then it means the number of factors could be reduced, either by withdrawing any factor associated to , or, if is indeed well-defined by (3.31), by summing (resp. subtracting) the volatility shape functions of the perfectly correlated (resp. anti-correlated) factors with respect to all the other factors. See for example (Féron and Gruet, 2024, Table 13-16-19) where such latter phenomenon is repeatedly observed when calibrating historical futures’ returns on the Italian, Swiss and UK markets respectively. In practice however, it is always possible to regularize or to tune the hyper-parameters of the non-linear solver such that (e.g. the tolerance threshold, the number of iterations, etc).

4 Calibration methodology for implied smiles

Implied calibration focuses on calibrating the model to observed market option prices. We show how the prices of vanilla options can be computed in our model and propose a way to decouple the implied calibration into the correction of the implied volatility term structure given by the VS volatilities to achieve a perfect fit, and the calibration of smile shapes.

4.1 Fourier option pricing for implied calibration

In this section, we describe the vanilla options pricing techniques used in the implied calibration for a futures contract with arbitrary delivery period in our model, where is given by (1.18) following the KV approximation.

The characteristic function of .

The European call option prices can be calculated using the Lewis (2001) formula

| (4.1) |

where denotes the characteristic function of the normalized log-price. Due to the affine structure of the variance diffusion of the lifted Heston model of Abi Jaber (2019), we show in the following theorem that the characteristic function of in the model (1.18) is known up to the solution of a Riccati equation.

Theorem 4.1.

Fix such that . For , the characteristic function of is given by

| (4.2) |

where , and satisfies the Riccati equation

| (4.3) |

for and the function is defined by

| (4.4) |

The Riccati equation (4.3) admits a unique global solution , which is differentiable a.e. and satisfies .

Proof.

The futures price dynamics (1.18) can be rewritten as a one-dimensional diffusion, i.e. there exists a Brownian motion such that

| (4.5) |

Note that our model is a particular specification of the Volterra Heston model (Abi Jaber et al., 2019, Section 7) setting the kernel to

| (4.6) |

and Repeating the proof of (Abi Jaber et al., 2019, Theorem 7.1 (ii)) adapted to take into account the bounded deterministic volatility component , we can prove the existence of satisfying , which is the solution to the Volterra–Riccati equation

| (4.7) |

The solution can be written in the form , where, for , satisfies

| (4.8) |

which is equivalent to the equation (4.3) by the variation of constants formula. Moreover, (4.8) implies that is absolutely continuous, hence is differentiable a.e., which concludes the proof. ∎

Numerical scheme for the Riccati equation.

For , the Riccati equation (4.3) can be rewritten in the integral form

so that satisfies

which is used as a numerical scheme to solve the Riccati equation (4.3). Such numerical scheme is more stable and precise than the explicit Euler discretization scheme, especially if one of the mean-reversion speeds reaches extreme values.

4.2 Exact calibration correction of the VS volatility term structure

The second step of the joint calibration consists of the correction and perfect match of the VS volatility term structure using the functions and . Precise calibration of the VS volatilities is indeed crucial for achieving a good overall implied fit in step 3: since , the stochastic volatility parameters responsible for the smile shape do not impact the VS volatilities, and hence cannot correct the VS volatility term structure.

Although the VS volatilities are calibrated by the -- risk factors in step 1, as described in Section 3, their fit is often not exact since the primary goal of this step is to capture the historical futures’ correlation structure with as few factors as possible but also match a priori the VS volatilities, where fitting the latter can be considered an implied regularization in the loss (3.17). Yet, at the same time, this regularization is necessary to capture the VS volatility term structure at least approximately in order to avoid over-fitting the functions and . Indeed, if the VS term structure were calibrated poorly at step 1, then the functions and would vary significantly, which would lead to a strong non-stationarity of the volatility (see Lemma 3.1) and eventually degrade the model’s extrapolation ability, mostly induced by step 1. Hence, it is important to keep these functions and close to one in practice.

In what follows, we assume that the functions and are piece-wise constant. The discontinuity points of the function are the delivery start and end dates of the underlying futures contracts, while the discontinuities of are the maturities of the associated vanilla options.

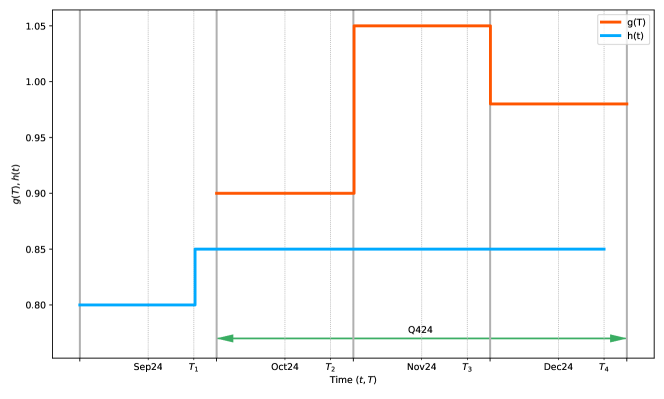

Motivating example.

Here, we provide some intuition on the calibration of the functions and and clarify why only one of these functions is not enough to fit the VS volatility term structure by considering a simple calibration set containing only five futures contracts: Oct 24, Nov 24, Dec 24, Q4 24, and Cal 25, with observation date the September 2024, see Figure 7. The maturities of options on monthly contracts are five days before the start of delivery (at , and for Oct 24, Nov 24, and Dec24 respectively). The quarterly contract Q4 24 expires in September at , and the calendar futures Cal 25 has two maturities and corresponding to September and December expiries.

The VS term structure calibration consists in matching model and market log-contract prices respectively given by (1.21) and (2.10), i.e. for any IV smile on a futures contract with delivery period and maturity , one should ensure that

| (4.9) |

where . This can be achieved in two ways:

-

•

either adjusting the function on the interval ;

-

•

or modifying the function on .

In our example, each monthly futures can be calibrated with the function which is constant on each of three months with the values chosen to verify (4.9). However, if all the three monthly futures are calibrated with the function , there is no more degree of freedom to adjust the variance swap price for the quarterly contract Q4 24. Alternatively, one could calibrate three smiles on Oct 24, Nov 24 and Q4 24 using the value of on Dec 24 to fit the calibration condition (4.9) for the smile on Q4 24.

Moreover, the function cannot calibrate the early expiries of the calendar contract Cal 25 (for instance, calibrate simultaneously the log-contract prices for the maturities and ) since impacts on the overall volatility level of the futures contract: therefore can fit the smile level for only one maturity per delivery.

For these reasons, the function needs to be introduced: we could fix the value of on to satisfy (4.9) for the smile on Cal 25 with maturity , then adjust on to ensure (4.9) holds its smile with maturity . Alternatively, one could calibrate the value of on to fit (4.9) for the smile on Q4 24 while the smiles on monthly futures are calibrated with the function . However, two problems arise.

First, is is impossible to calibrate simultaneously both smiles written on Q4 24 and on Cal 25 since they share the same maturity . Hence, one of them should be necessarily calibrated with the function . In this example, the following solution is possible:

-

1.

smiles on Oct 24, Nov 24, Dec 24, and Cal 25 with maturity are calibrated with the function ,

-

2.

smiles on Q4 24 and on Cal 25 with maturity are calibrated with the function .

Second, once the monthly contracts are calibrated with the function , any modification of the function (up to the smile maturity) made during the calibration of smile on Q4 24, will impact the log-contract price corresponding to the monthly futures, and vice-versa. This is simply due to the fact that the log-contract price in (4.9) depends both on on and on on .

That is why an iterative calibration algorithm is needed. One step of such algorithm should include the calibration of the function to fit (4.9) for one part of smiles and then the calibration of taking into account the modifications of to verify (4.9) for the remaining smiles (possibly breaking this condition for the smiles from the first group). If such iterative algorithm converges to a fixed-point, at the limit, the smiles from both groups will be calibrated. This fixed-point algorithm is the key idea of the proposed calibration method and will be discussed in more detail below.

Two groups of smiles.

From the discussion above it is clear that the implied volatility smiles should be divided into two groups: for the smiles in the first group the calibration condition is guaranteed by the function , while the smiles from the second one are calibrated with the function . It also follows from the example, that these groups should satisfy the following conditions.

Conditions on the smiles calibrated with the function :

-

1.

one maturity per futures: Only one smile for a given futures contract can be calibrated with ,

-

2.

linear independence: The underlying futures corresponding to these smiles should be linearly independent, i.e. no delivery period should be representable as a union of delivery periods of other futures contracts.

Condition on the smiles calibrated with the function :

-

3

no coinciding maturities: for a given maturity, only one smile may be chosen.

Note that such division may be not unique. To fix the division, we decide to calibrate the smiles on monthly and quarterly contracts with the function and all the smiles on calendar contracts with the function . Although the latter arbitrary division is not always available, it is almost always possible to find another division satisfying the conditions 1–3.

Calibration of the function .

We strip the function to match the variance swap prices implied from the volatility smiles in (2.9) and the variance swap prices given by the model (1.21) for futures contracts , for each . Fixing referring to the -th smile of the -th contract, we set on equal to

| (4.10) |

where is the previous smile maturity in the sorted list of all maturities and

Note that in (4.10) depends on the function through the deterministic variance .

Calibration of the function .

The discontinuity points of coincide with contracts’ delivery start and end dates . We adopt the following notation for the values of : if the function is constant on a delivery period , we will denote its value by . Otherwise, if other delivery periods of futures contracts are included in , we will denote by the value of on , where stands for the indices of futures contracts which smiles are calibrated with the function and which delivery periods are included in . We also denote by the volatility of a futures contract delivering over a set with such that

| (4.11) |

where stands for the Lebesgue measure of . With a slight abuse of notation, we use interchangeably and , recall (1.17).

Hence, the deterministic volatility component of the contract is given by

| (4.12) |

where

| (4.13) |

denotes the relative weight of the contract volatility in the volatility of which is proportional to the length of its delivery period.

For the volatility smiles with underlying futures contract and maturity (for some , uniquely determined thanks to condition 1 of smile division), such that , matching the log-contract prices (4.9) leads to

| (4.14) |

since by (4.12). Note that, since is uniquely determined for each contract, it can be omitted in the notation .

For the contracts not calibrated yet, i.e. such that , the function should be chosen

| (4.15) |

where is a solution of the quadratic equation

| (4.16) |

with the deterministic volatility component given by (4.12) with already calibrated by (4.14). Note that the set is non-empty thanks to the linear independence condition imposed on the smiles division.

Fixed-point calibration algorithm.

Note that the model is calibrated when the equation (4.9) is verified for all smiles simultaneously. Since the functions and are interdependent, we propose the following algorithm which is supposed to converge to the desired solution.

Denoting one iteration of this algorithm by , we note that model is calibrated if and only if is a fixed-point of this mapping, i.e. .

Under additional conditions on the implied volatility data consistency, the following result holds:

Theorem 4.2.

Suppose that all the smiles calibrated with have the same underlying and that for the remaining contracts . Suppose also that all the instantaneous correlations between the futures contracts are positive. Then,

- (i)

-

(ii)

All the fixed points are stable.

-

(iii)

If the contract has only one maturity, the fixed point is unique.

Proof.

The proof is given in Appendix C. ∎

This result is clearly partial as it does not cover the case of multiple underlyings corresponding to smiles calibrated with and does not admit the nested contracts for smiles calibrated with . However, the numerical experiments demonstrated the existence of a unique stable fixed point for all the test cases, even the ones not covered by Theorem 4.2. Thus, we believe that the provided result can be proved in a much more general case, though the direct approach used in the proof of Theorem 4.2 is not applicable there.

Remark 4.3.

Note that Theorem 4.2 provides condition (4.17) which seems to be a universal condition ensuring that the model can be calibrated. Indeed, it can be interpreted as a no-arbitrage condition for the variance swaps. For example, consider the smile on Cal 25 with maturity calibrated with and Q2 25 with maturity calibrated by . In this case, (4.17) reads

| (4.18) |

Since in the calibrated model

| (4.19) |

the condition (4.18) is equivalent to

| (4.20) |

The integrand in the left-hand side expression is the part of variance of Cal 25 contract corresponding to Q2 25. Since the covariances are supposed to be positive, this part of variance is smaller than the whole variance of Cal 25, and thus, the price of the variance swap on Cal 25 should be greater than the integral on the left. Thereby, (4.17) is a condition describing the consistency of the variance swap data with historically calibrated deterministic volatility functions .

4.3 Smile shape calibration

Parametrization of the correlations.

Fix . For the approximated futures contract , the smile skew is determined by the “spot-vol” correlation

| (4.21) |

where denotes a vector filled with ones, and is a lower triangular matrix from the Cholesky decomposition (1.5). As lies in , should be in for the extended covariance matrix of to be well-defined.

Since the skew of the the implied volatility smile is determined by the correlations (4.21), it is more natural to use them and not in the calibration routine for several reasons. First, if the number of contracts is smaller than the number of historical risk factors , this will reduce the number of parameters. Second, one spot-vol correlation impacts only one smile related to the corresponding futures contract, whereas the coefficients impact all the smiles in a way difficult to interpret. Thus, we expect to see a better solver behavior when the variables being optimized are the “spot-vol” correlations. Finally, even if one decides to calibrate directly, the “spot-vol” correlations may provide a reasonable initial guess given by the calibrated correlations in the multi-contract SSVI parametrization described in Section 2.2.2.

In order to reconstruct from a set of “spot-vol” correlations , we find numerically a solution to the following optimization problem

| (4.22) |

and set .

Optimization problem.

We denote the parameters being calibrated by , where the spot-vol correlations are transformed to by (4.22). The optimization problem then reads

| (4.23) |

where denotes the Black-Scholes vega corresponding to the market implied volatility .

5 Numerical results

5.1 Calibration results

In this section, we illustrate and detail all three calibration steps of the HJM model (1.1), cf. Figure 3, onto the German power market, and we postpone to Appendix A.2 the calibration results obtained on the TTF gas market.

To assess the quality of the calibration we consider the differences between model quantities and those used to calibrate the model: historical correlations and volatilities of rolling futures contracts, variance swap variance term structure and the implied volatility smiles. We also validate the quality of the Kemna-Vorst approximation. The calibrated model can be used to represent the market, and especially to deduce market quantities that are not quoted: the smile for all monthly contracts especially those which are not quoted, the at-the-money volatility of daily, monthly and quarterly contracts and finally the instantaneous correlations. Finally, we check the coherence between calibrated and interpolated quantities.

5.1.1 Step 1: Joint historical covariances – implied VS variances calibration results

The first calibration step aims at calibrating the -- factors’ parameters , , as well as their correlation matrix , following the methodology described in Section 3.

We consider the German power i.e. DE PW futures market with historical covariances estimated from daily log returns’ time series running from January 2023 to July 2024, and the estimated realized futures correlation structure is displayed on the bottom left corner of Figure 5.

In order to avoid to have more calibratable parameters than market quantities to calibrate on, one needs to ensure that

| (5.1) |

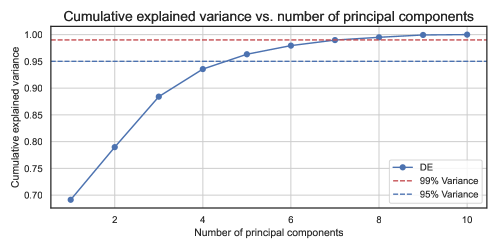

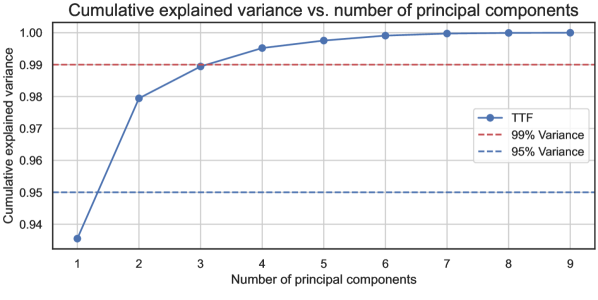

Furthermore, although season-averaging effects tend to distort Principal Components Analysis (PCA) results, the number of Principal Components (PCs) required to reach a given threshold of explained variance gives some insights on the number of factors to model the futures curve, see for example Koekebakker and Ollmar (2005), Andersen (2010), Gardini and Santilli (2024). Figure 8 displays the PCA’s results for the rolling futures contracts’ daily log returns. Note that PCs are sufficient to explain at least of variance, while PCs are required to reach , which is consistent with

-

1.

our quality of fit results for the historical calibration described in Figures 9;

-

2.

the observations made by Féron and Gruet (2024)[Figure 3] when applying BIC and AIC statistical measurements to the German market, where they found that factors appears to be a good trade-off between quality of fit and model complexity.

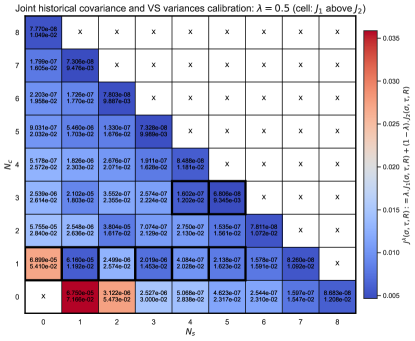

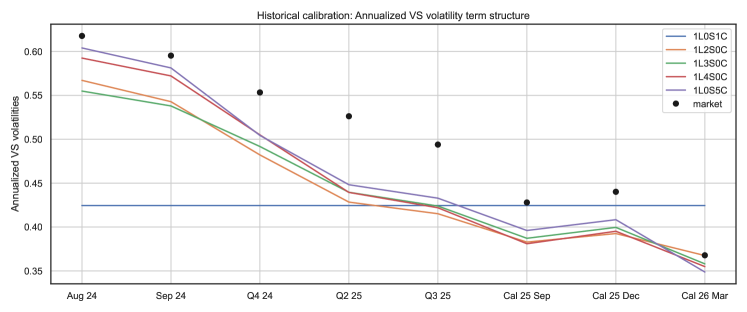

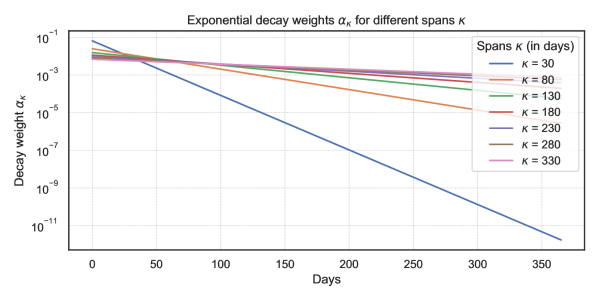

The results of the joint historical covariance and VS variances calibration is then summarized in the left matrix of Figure 9 where, given there is one -factor, we display in a single matrix the losses and from (3.18)–(3.19) respectively for all possible pairs of - and -factors such that the under-parametrization inequality (5.1) is satisfied for the strict lower part of the matrix, and is strictly violated by one additional factor on the main diagonal, corresponding to over-parametrization. For each cell, we used random initializations of and kept the best calibration fit. Notice that the overall joint loss from (3.17), for , indeed decreases as the number of factor increases when moving from the lower left angle to the main diagonal of the fit matrix. For a fixed number of factors , we also highlighted by a bold square the model with the best fit along each diagonal.

Furthermore, we show in Figure 10 the respective quality of fits obtained on the selected rolling contracts’ historical volatility and correlation term structures, as well as the fit of the VS volatility term structure. Notice that the fit is not perfect, yet it’s possible to additionally fine-tune the parameter in the joint calibration loss function in order to better fit either the historical target covariance values (with ) or the implied VS volatility term structure (with ). In the next step, we calibrate the functions and in order to actually fit perfectly the latter in the case the joint calibration has not succeeded in fitting it well enough to fit the smile shapes in the latter calibration step.

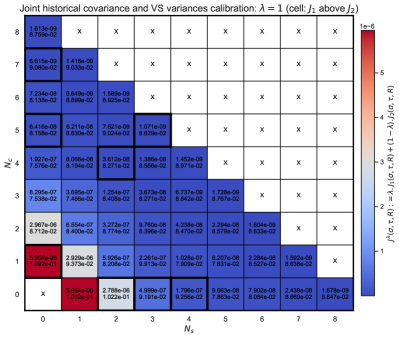

We did the same numerical experiments for the historical covariance fit only by taking in the loss , and display the values of the losses in the right hand-side matrix of Figure 9, and the quality of fits in Figure 11. Notice that the quality of fit of both the historical volatility and correlation term structures is much better, but the associated VS volatility term structure is systematically under-estimated by such historical calibration.

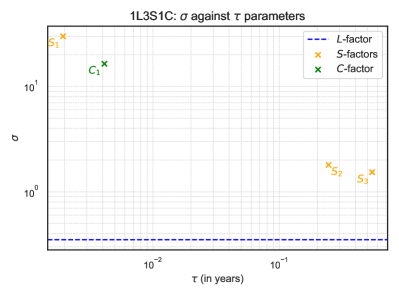

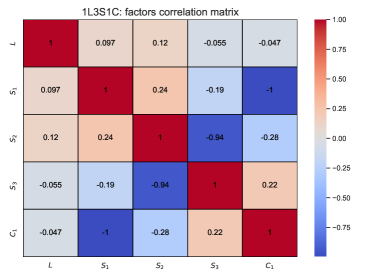

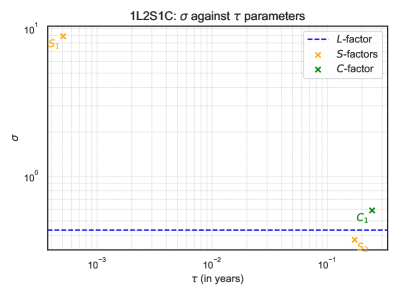

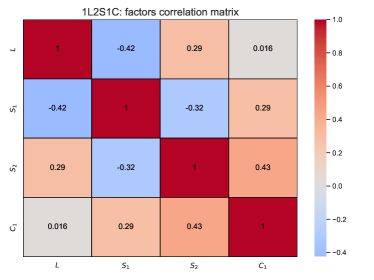

For the implied calibration, we choose the model as it gives a good trade-off between parsimony and the joint calibration quality, and display its calibrated parameters in Figure 12. Notice the -factor indeed captures the long-term volatility level, with lying in-between the annualized volatilities of long-term contracts rCal 25 and rCal 26, respectively equal to and while the factor is placed at the beginning of the curve to capture the short-term volatility behavior in the case of . For conciseness, the calibrated parameters of the other models mentioned in Figure 9 are not displayed.

It is worth mentioning that the choice of the historical volatility factors does not impact significantly the results of the following calibration steps as long as the fit of the VS term structure is satisfactory. Otherwise, the calibrated functions and may deviate significantly from degrading the model’s interpolation capabilities.

5.1.2 Step 2: Term structure exact calibration correction

This part addresses the correction of the VS volatility term structure with the functions and following the methodology proposed in Section 4.2.

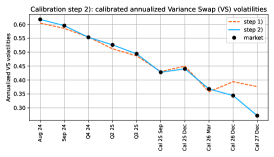

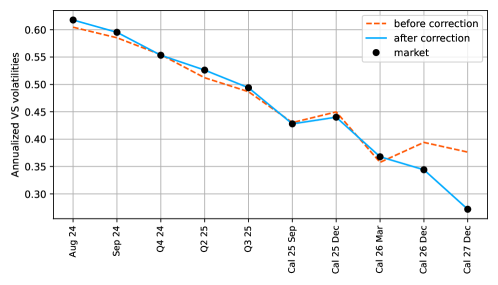

In order to avoid jumps of the day-ahead contracts volatility, both functions and are smoothed during calibration. At each step of the fixed point algorithm, we update and as piece-wise constant functions and then interpolate it using the monotonicity preserving algorithm PCHIP of Fritsch and Butland (1984). Despite the smoother results, the algorithm is more time-consuming due to the numerical optimization involved in the calibration. On the left-hand side of Figure LABEL:fig:calibrated_g below, we plot the results of the term structure calibration of piece-wise constant functions and , and on the right-hand side, same results with smoothing interpolation. In both cases, the fixed-point algorithm converges in approximately – iterations, providing an almost perfect fit for the VS volatilities shown in Figure 14.

We also note that thanks to the calibration of the VS volatilities at the first step of the calibration, the functions and are needed only to slightly correct the volatility level, so that they remain close to for the months following the observation date. For longer maturities, the function deviates significantly from since the VS volatilities of smiles Cal 26 Dec and Cal 27 Dec were not calibrated at the first calibration step due to the poor quality of covariance estimations for contracts with long time to delivery.

5.1.3 Step 3: Implied smile shapes calibration

Finally, we calibrate the parameters of the stochastic variance process , as well as the correlations , using the procedure described in Section 4.3.

For the stochastic variance component calibration, we choose a model with pseudo-factors in (1.2) which allow us to cover different volatility timescales and consistently achieve an acceptable fit on various calibration sets. The advantage of using multiple pseudo-factors is demonstrated in Appendix A.1, where we compare the quality of fit between the Heston model and the Lifted Heston model.

The calibrated parameters of the stochastic volatility are provided in Table 3. For the calibrated values, the loss function defined by (4.23) equals . It is interesting to notice that the first mean-reversion coefficient is very close to zero and corresponds to very long mean-reversion periods, while the two others correspond approximately to the timescales of one month and 2.5 weeks respectively.

| Parameter | Calibrated value |

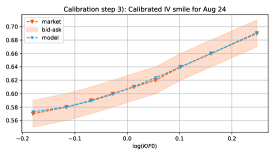

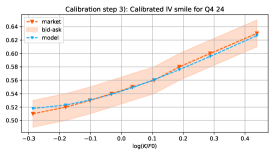

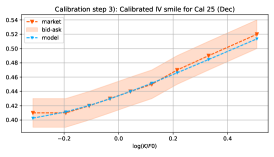

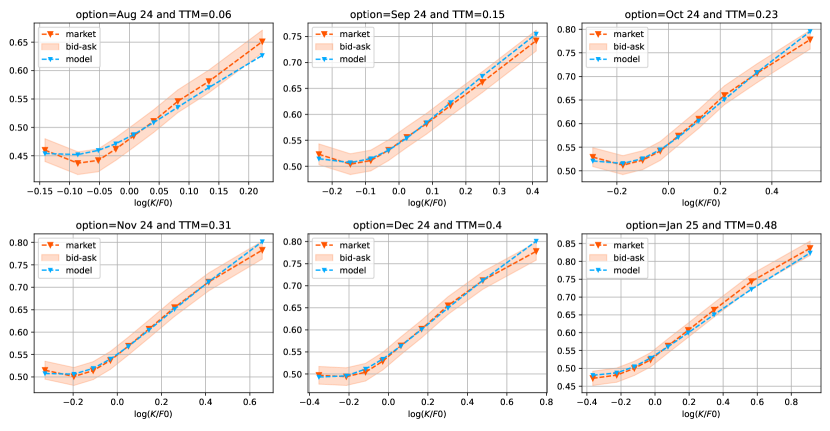

The implied volatility smiles in the calibrated model with smoothed and functions, are shown in Figure 15. We also plot the bid-ask spread equal to 5% as a realistic and even conservative proxy to the market spread observed in the power market. Thus, the plot demonstrates sufficiently high quality of fit for the model to be used for practical needs.

5.2 A posteriori validation of model approximations

As discussed in Section 1.1, the use of the Kemna-Vorst (KV) approximated model futures from (1.18) leads to potential arbitrage opportunities for futures contracts with overlapping deliveries, e.g. between monthly futures and the resulting quarter composed by such delivery months. However, we show in the next subsections that the futures prices’ trajectories, as well as the futures correlation structures and implied volatility smiles are extremely close in the approximated model and in the exact model future from (1.12).

From the forward rate definition (1.1), the exact model is given explicitly by

| (5.2) | ||||

| (5.3) |

Numerically, we consider a one-day discretization step, which corresponds in practice to the futures contracts with the shortest delivery period quoted in the futures market

| (5.4) | ||||

| (5.5) |

Since the exact daily contracts are computed using a Monte Carlo scheme, the exact model becomes significantly slower in terms of pricing and simulation time than the approximated one.

Besides the KV approximation, it is important to notice that the introduction of the function prevents the futures volatility from being stationary. However, if , which is the case in our model as the variance swap volatilities are mostly calibrated at the first calibration step, then the futures contracts dynamics remains almost stationary. Furthermore, the function impacts the instantaneous correlations between absolute contracts. These correlations are affected by the KV approximation as well. In the following numerical experiments, we demonstrate that neither KV approximation nor the function have a significant impact on the futures correlation structure.

5.2.1 Sample path trajectories errors

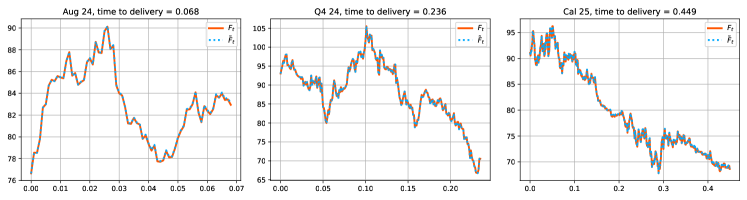

As an illustration of the quality of this approximation, we provide in Figure 16 the trajectories of the exact futures contracts and their approximations , simulated with the same random numbers, for three different futures contracts: Sep 24, Q1 25 and Cal 25. Recall that is defined in (1.12) with explicitly given by (1.7). The mean distance on is defined as a sample Root Mean Squared Error (RMSE) over sample trajectories by

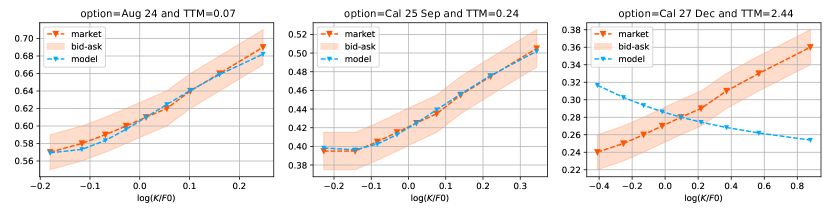

where is the number of steps in the daily subdivision of . The estimated distance with between the approximated and exact trajectories estimated over simulations equals , and for three futures contracts correspondingly. We observed that this error depends both on the interval length as well as on the length of the delivery period. Both dependencies are non-linear, the first one is strictly increasing in . As for second one, the error is greater for small (up to one-two months) and for large intervals (two years or more) delivery periods. The worst-case RMSE numerically reaches of the initial futures value .

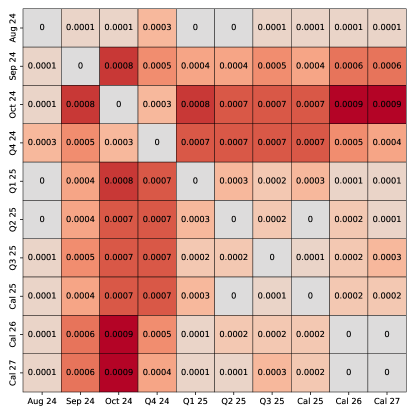

5.2.2 Instantaneous correlations

In this section, we assess numerically the impact of the function on the futures contracts’ instantaneous correlations. Indeed, unlike the function and the stochastic variance component which only modify the futures’ volatility term structure but not their correlations, the function also impacts the correlations as it changes the approximated futures contract volatilities defined by (1.17). Indeed, for , the instantaneous correlation between the approximated futures contracts and obtained just after the first calibration step, and implied by the historical futures correlation structure of rolling futures, is defined by

| (5.6) |

where was defined by (4.11). However, after the second calibration step, the futures contract volatility is given by , and the instantaneous correlation equals

| (5.7) |

Note that these two values coincide if and only if is constant on and on , as in this case, and , where and denote the values of the function on the intervals and correspondingly.