Synthetic Data for Portfolios:

A Throw of the Dice Will Never Abolish Chance

Abstract

Simulation methods have always been instrumental in finance, and data-driven methods with minimal model specification—commonly referred to as generative models—have attracted increasing attention, especially after the success of deep learning in a broad range of fields. However, the adoption of these models in financial applications has not kept pace with the growing interest, probably due to the unique complexities and challenges of financial markets. This paper aims to contribute to a deeper understanding of the limitations of generative models, particularly in portfolio and risk management. To this end, we begin by presenting theoretical results on the importance of initial sample size, and point out the potential pitfalls of generating far more data than originally available. We then highlight the inseparable nature of model development and the desired use case by touching on a paradox: generic generative models inherently care less about what is important for constructing portfolios (in particular the long-short ones). Based on these findings, we propose a pipeline for the generation of multivariate returns that meets conventional evaluation standards on a large universe of US equities while being compliant with stylized facts observed in asset returns and turning around the pitfalls we previously identified. Moreover, we insist on the need for more delicate evaluation methods, and suggest, through an example of mean-reversion strategies, a method designed to identify poor models for a given application based on regurgitative training, i.e. retraining the model using the data it has itself generated, which is commonly referred to in statistics as identifiability.

Keywords: generative models, synthetic data, machine learning, generative adversarial networks, high-dimensional returns, principal component analysis, portfolio construction

1 Introduction

In 1887, the French poet Stéphane Mallarmé composed “Un coup de dés jamais n’abolira le hasard” (in English A Throw of the Dice will Never Abolish Chance), which was a first step in the direction of concrete poetry. In a context of the flourishing scientific developments in Europe, especially in probability and statistics (think about Adolphe Quetelet and Bernoulli’s and Poisson’s work on the “loi des grands nombres”, the law of large numbers), the message of the poem was as simple as its title: in the context of randomness, drawing one realization does not cancel the reality of the underlying stochastic phenomenon. This paper is about that: in the highly non-stationary and high-dimensional realm of returns of financial instruments, drawing synthetic data made of the informational content of a small sample is not abolishing the depth of this initial randomness.

The practice of drawing samples from a model to address specific financial tasks dates back to at least the 1960s, when [Hertz, 1964] proposed using simulations for investment risk analysis. The potential of this approach was quickly realized for the valuation of options, with one of the earliest applications appearing in [Boyle, 1977]. The adoption of such techniques, along with the effort to develop more realistic models, has grown significantly with the increasing complexity of derivatives pricing (e.g., [Broadie and Glasserman, 1996] and [Carriere, 1996]), the need for stress-testing and accurate risk estimation (e.g., Value-at-Risk) for large portfolios of non-linear instruments (e.g., [Berkowitz, 1999] and [Jamshidian and Zhu, 1996]), and the optimization of portfolios with sensitivity to extreme losses [Rockafellar and Uryasev, 2000], among many other applications across various areas in finance.

The conventional approach, known as Monte Carlo methods (see [Glasserman, 2004] and [Jäckel, 2002]), involves random sampling from a parametric model specified by the user to ensure that it accurately represents the process, distribution, or environment being modeled. The parameters of the specified model are typically calibrated using the available historical data. Despite the interpretability provided by the parametric nature of the model, a major limitation of this approach is its inherent dependence on the initial assumptions about the model design, which might not accurately reflect the underlying reality. Another drawback is its questionable scalability as the complexity of the system increases, requiring the user to have an extremely deep understanding of the environment—a task that can be practically impossible in some cases.

Therefore, machine learning methods that make minimal assumptions about the underlying distribution and allow the data to speak for itself have been gaining increasing attention within the financial community [Capponi and Lehalle, 2023]. This growing interest is likely driven not only by the limitations of traditional methods but also by the remarkable achievements in deep generative modeling, particularly in areas like text and image generation (e.g., [Brown, 2020] and [Ramesh et al., 2022]) although it is worth mentioning that recent academic papers identify drawbacks and degenerate behaviors that stem from synthetic data [Shumailov et al., 2024].

At the heart of generative modeling lies the idea of training a model that generates samples from the same distribution as the training data. Aside from early examples like energy-based models [Hinton and Sejnowski, 1983], recent approaches such as variational autoencoders (VAE) [Kingma and Welling, 2013], generative adversarial networks (GAN) [Goodfellow et al., 2014], and diffusion models [Ho et al., 2020] achieve this by learning a function, typically a neural network, that can transform lower-dimensional random inputs (noise) into realistic higher-dimensional outputs. These methods differ primarily in how they learn the parameters of the generative network that handles this transformation.

Academics and practitioners have not hesitated to test these approaches in various financial applications. GANs have emerged as the most common architecture, being used for simulating financial return time-series [Wiese et al., 2020], implied volatility surfaces [Vuletić and Cont, 2023], equity correlation matrices [Marti, 2020], and limit order books [Cont et al., 2023], not to mention other applications. Similarly, VAEs have been applied to generate paths [Buehler et al., 2020], for credit portfolio risk modeling [Caprioli et al., 2023], and for multivariate time-series generation [Desai et al., 2021]. Diffusion models have also found applications, such as in financial tabular data generation [Sattarov et al., 2023].

However, it would be fair to say that these applications have not yet proven to be as successful as their counterparts in text and image generation. This is likely due to the unique complexities and characteristics inherent in financial markets. When focusing on multivariate asset returns, which is central to this paper, certain differences become apparent compared to text and image data. Firstly, asset prices are influenced not only by the activity of informed trades but also by irrelevant elements perceived as information [Black, 1986]. This introduces noise into prices, and consequently returns, which can obscure any statistically relevant patterns that the model should detect. Secondly, asset returns exhibit specific statistical properties, both at the marginal and joint levels, referred to as the stylized facts of asset returns [Cont, 2000], which are not straightforward to capture. For example, asset return distributions are often heavy-tailed and asymmetric [Mandelbrot, 1997]. Additionally, there is an intertemporal dependence structure between different time points, as evidenced by volatility clustering and leverage effects (see [Ding et al., 1993], [Bouchaud et al., 2001] and [Zumbach, 2007]). On a joint level, assets can exhibit a complex and dynamic co-movement structure, where the number of cross-asset relationships increases polynomially with the number of assets studied [Plerou et al., 1999]. Ideally, a generative model should capture these properties effectively at both the marginal and joint levels, as well as any other relevant characteristics not explicitly known to the user.

The limited availability of data (30 years of daily returns amounts to only about 7,500 observations) adds another layer of complexity compared to applications in text and images, where vast datasets are readily available. Moreover, using the entire historical dataset may not always be ideal, as older data can be less relevant due to the non-stationary nature of financial markets and the influence of macroeconomic regime shifts [Issler and Vahid, 1996] and business cycles [Romer, 1999] on asset returns. These constraints make brute-force approaches, such as scaling up model parameters and dataset sizes, less feasible in finance compared to their proven effectiveness in other domains [Kaplan et al., 2020].

Some papers recognize the challenges and the infeasibility of simply training a state-of-the-art generative model on financial data. As a result, they modify or engineer these models to make them more suitable for financial applications, giving them a better chance to perform well despite the difficulties mentioned earlier. For instance, [Liao et al., 2024] demonstrates that using a mathematical property of signatures can reduce the challenging min-max problem required for training GANs to a simpler supervised problem, significantly easing the training process. [Cont et al., 2022] replaces the classical loss functions used in GANs with a financially relevant one based on the joint elicitability of a risk measure couple, thereby forcing the model to better learn the tails of return distributions. Another approach involves modifications during the data processing phase. For example, [Wiese et al., 2020] employs a Lambert-W transformation [Goerg, 2015] to normalize the training data and eliminate heavy-tails, while [Peña et al., 2023] transforms multivariate data to obtain orthogonal variables, thereby simplifying the model’s task of handling cross-dependencies.

Another very crucial aspect of generative modeling is the evaluation of the quality of generate data, although there is no consensus on how to evaluate and validate what is produced by the trained model (see [Borji, 2018] for a review of evaluation measures). It is natural to expect different evaluation measures in different domains, but the lack of a common set of intra-domain measures makes it difficult to compare and horse-race models that have been instrumental in the theoretical progress of deep learning over the last decade, as we have seen with ImageNet [Deng et al., 2009]. The considerable efforts being made to benchmark and evaluate LLMs also underline the importance of the issue [Hendrycks et al., 2020]. In finance, given the difficulty of evaluating returns for a high-dimensional universe of assets, the evaluation process is often generic. It typically involves checking if the generated data reproduces stylized facts and is distributionally close to the training set, with minimal analysis specific to the intended application.

The goal of this paper is to explore to what extent and how generative models can be efficiently utilized in finance, particularly for portfolio construction. We aim to identify the requirements for more reliable and effective development and evaluation of these models in an environment where there is growing demand for their use in highly specialized tasks, such as optimizing the hyperparameters of long-short quantitative strategies to balance the trade-off between expected return and risk [Lopez-Lira, 2019].

To this end, we begin by theoretically underlining the crucial relationship that must be considered between the initial sample size of the training set and the amount of generated data. While the endless generation of synthetic data is often taken for granted in other domains, in finance, the initial sample size must remain a constant point of concern both before and after training.

Next, we demonstrate why a plug-and-play approach with classical generative models may not be suitable for finance, emphasizing the need for model design to be tailored to the specific use case. We illustrate this through an example that we believe is quite fundamental and can serve as a basis for other approaches. Specifically, we show why the following does not work: using a generative model trained under generic loss functions to construct mean-variance portfolios.

In light of these results and with a specific application in mind—backtesting mean-reversion strategies—we propose a generative pipeline designed to address the limitations discussed earlier. This pipeline begins with appropriate data transformations and decompositions, followed by the use of GANs and parametric models to generate high-dimensional financial multivariate time-series. We evaluate our generative pipeline using a real dataset of US stocks, subjecting it to rigorous tests with a demanding and detail-oriented approach, though initially without direct consideration of the final application.

Finally, we propose a methodology for evaluating generative models for financial time-series, focusing on their identifiability at the level the intended application. This involves regurgitative training—a term coined by [Zhang et al., 2024] to describe the process of training large language models (LLM) using synthetic data. This approach assesses whether the model can effectively learn about the underlying application from its own generated data and might be of use to detect poor models in the sense that they are not able to identify the underlying model that generated the data, even when it belongs to their own class. In statistics it is commonly referred to as identifiability of the approach (cf. [Picci, 1977] and references therein).

In Section 2, we present theoretical results on the influence of the initial sample size and on potential pitfalls of constructing portfolios using synthetic data generated by a generic generative model. Section 3 begins with a review of existing generative models in the literature and then details the generative pipeline we propose. In Section 4, we report on the evaluation of the data generated by our pipeline, applied to a specific dataset of US stocks, and provide insight into the stylized facts of asset returns that support our design choices. Finally, Section 5 outlines how a real evaluation should integrate the desired application into the evaluation process. We demonstrate this through our case where the generative model is specifically designed to backtest mean-reversion strategies.

2 The essentials of generative modeling in finance

2.1 The influence of the initial sample size

In this subsection, we demonstrate that, when using a generative model to estimate a statistic, the initial sample size cannot be ignored. Specifically, we will show that generating an excessive number of samples using the generative model does not necessarily improve the accuracy of the estimated statistic. Instead, if the number of generated samples becomes too large, it can introduce a bias into the results.

Let us consider the class of U-statistics to stay as generic as possible (see [Serfling, 2009] for a general introduction). A -statistic is a type of estimator defined as the average value of a symmetric function (kernel) applied to all possible increasing tuples of a fixed size.111In a more general case, the kernel can also be chosen to be non-symmetric. Precisely, for a sample of independent and identically-distributed random variables ,

where is a set of -tuples (distinct and increasing) of indices from with and and the law is assumed to ensure the existence of finite moments up to the required order.

By selecting different kernels , a wide range of useful estimators can be derived, such as the sample mean (, ), sample variance (, ), estimators for the moments and the variance-covariance matrix for multivariate data, among many others. Moreover, the -statistic satisfies the asymptotic normality property [Hoeffding, 1948]:

where the variance is a strictly positive value that can be computed using the Hoeffding decomposition, precisely it is the variance of where .

Berry-Esseen-type error bounds for -statistics have been studied extensively (see [Bentkus et al., 2009] and [Chen and Shao, 2007]). If and for ,

| (1) |

where is the cumulative density function of the standard normal distribution and represents a value that does not depend on or .222Precisely, where represent a constant that does not depend on the specific variables or parameters of the problem. While tighter bounds are possible, the bound provided by Inequality (1) is sufficient for our analysis.

Suppose we aim to estimate a statistic , a true characteristic of an unknown distribution , using a generative model. To do so, we first train the generative model on a dataset of size sampled from . After training, the generative model produces samples from a distribution , and the corresponding statistic under this distribution is , which serves as an estimate of the true statistic .

However, due to the finite size of the initial training sample and / or biases introduced during the learning process, an inherent discrepancy , referred to as the learning accuracy, arises between and . Given this context, when the goal is to estimate within a desired tolerance , a natural question arises: can increasing the size of the synthetic dataset generated by the model improve the estimate of , or are there fundamental limitations imposed by the initial training sample size that cannot be mitigated by simply enlarging ?

Assumption 1.

The learning accuracy is inversely related to a power of the initial sample size .

Assumption 1 essentially states that with more data, one will obtain a model that better represents reality. Indeed, when the number of parameters of the model increases, the sample size needed to guarantee a given accuracy increases too. The paradox of universal approximators like neural networks is that to guarantee their convergence via results like [Hornik et al., 1989], an infinite number of parameters is needed, and hence an infinite number of data is required. Moreover, recent results like [Ben Arous et al., 2019] show that it is not enough to have an infinite number of data points if the ratio of the number of neurons over the sample size is maintained over a certain threshold.

Using Inequality (1), we can write the following error bound for a -statistic computed using synthetic dataset of size drawn from :

where can be considered the counterpart to the constant that appears in Inequality (1) under the generative model and is an estimate of the variance .

While increasing the number of synthetic data points will cause to converge toward , the ultimate goal is to improve the estimate of . To formalize, we are interested in the probability that is within a distance of , given that is away from , where is strongly related to the initial sample size under Assumption 1. This probability is represented by the shaded area in Figure 1. The bounds for this probability can be given by the following proposition.

Proposition 1 (Probability bounds for synthetic data estimators approximating true statistics).

Let denote the size of synthetic dataset generated by a generative model trained on an initial dataset of size , and let represent the estimate of the true statistic under the generative model. Assume that denotes the learning accuracy. The probability that , the -statistic computed using the synthetic dataset, is within a distance of satisfies the following bounds:

| (2) |

where and , , and are constants related to the statistics of interest, as defined above.

The proof of this result can be found in Appendix LABEL:appendix:error_bounds. This expression illustrates how the accuracy of as an estimator for depends on several factors: the sample size that we generate, the learning accuracy of from that is often unknown, the target distance within which we want to fall, and other parameters which are related to the underlying statistics of interest and the distribution of the random variable on which this statistic is computed. However, a more interesting result emerges in the limiting case.

Corollary 2 (Excessive synthetic data generation leads to biased conclusions).

If and is computed using samples from the learned generative model,

Therefore, generating more data points with the generative model does not ensure that the estimated statistics will be closer to the true values. Instead, it can introduce bias and ensure a discrepancy from the true statistics unless the learning accuracy is acceptably small—a condition achievable only with a sufficiently large dataset.

Beyond U-statistics.

It is possible to extend such results to -statistics (cf. [Aaronson et al., 1996] for asymptotics). In finance, this is not a mere detail, as widely used risk measures like Value-at-Risk and Expected Shortfall belong to this class of statistics.

Short discussion on Assumption 1.

This assumption states that a (generative) model learned on a dataset is centered close to the empirical expectation (i.e. the average) of this sample of points. In more formal terms: whatever the number of synthetic data, computed on the generative model learned from is close to that is known only thanks to the initial sample of observations.

Of course some methods are known to reduce some biases in the data (for instance the jackknife, for some specific dependence of the bias in the sample size), but since only a finite sample is known, and since the purpose of synthetic data generation is to be model free, it is not consistent to assume the nature of the biases is known, and in any case they would have to be encoded by hand in the structure of the generative model.

Nevertheless, the purpose of penalization methods is to drive estimators away from their natural unbiased versions. In any case: penalization is a way to prevent too much non-linearity to appear in the model, not to give a specific shape to the model, especially when the true underlying model is unknown. This discussion is well known in the machine learning community and is usually referred to as the no free lunch theorem argument, see [Wolpert, 1996].

To conclude on the aspect of drawing examples from a model based on an initial sample size of : without any good reason to have chosen a specific generative model that is close to the way economics shapes the returns of financial instruments, Corrolary 2 stands and tells generating too many synthetic data gets the estimated statistics on these data away from their true values. In statistics, and especially with the context of the bootstrap, practitioners seem to have a rule of thumb that is to generate the same order of magnitude of points as the original sample size. In the light of Inequality (2), we can say that one should preserve the distance between the empirical value of the -statistic and its theoretical counterpart in the hope that will not be too close to this empirical mean.

2.2 Generic generative models in conflict with portfolio construction

This subsection focuses on how expected returns interact with modern portfolio construction. It demonstrates that Markowitz-like portfolio optimizations involve expected returns with the inverse of the covariance matrix of the instruments’ returns. Consequently, the principal components and eigenvalues of this covariance matrix play a crucial role in how expected returns are reshaped to determine portfolio weights. In the context of a statistical risk model—where the co-movement structure is driven by a few factors, plus a noise term that preserves the system’s variance—we show that the contribution of expected returns to portfolio construction predominantly resides in the subspace spanned by the lower-variance principal components.

Next, we argue that generative models trained under traditional loss functions are not ideal candidates for portfolio construction tasks, as they impose a hierarchical structure between principal components, with a tendency towards learning high-variance factors better. However, we show that errors made in the subspace covered by low-variance factors are much more costly from a portfolio construction point of view, highlighting the importance of an architecture that removes this hierarchy and learns low-variance factors as well as high-variance ones.

Basics of portfolio construction.

First recall the basics of portfolio construction (see [Boyd et al., 2024] for details). Given the vector of expected return and the matrix of expected covariances between stocks being , most portfolio constructions boil down to

| (3) |

where represents the maximum portfolio volatility that can be tolerated by the user.

Assume that is derived from a statistical factor model constructed as follows. Let be an initial covariance matrix estimated from a sample or obtained through other means. We perform principal component analysis (PCA) and select the first eigenvectors (stacked in the matrix of dimension ) as the significant components or factors. These eigenvectors are associated with the largest eigenvalues , which are stored in the diagonal matrix of dimension . The remaining eigenvectors are stacked in the matrix , and the remaining eigenvalues are replaced with a fixed value , ensuring that the trace of the original matrix is preserved. This process is equivalent to applying eigenvalue clipping to .

It corresponds to having the following risk model:

| (4) |

where and .

It is important to note that is smaller than the smallest eigenvalue in :

The following definitions will be useful for simplifying the expression of Problem (3):

Definition 1 (Natural space).

We define the natural space of a d-dimensional random vector as the space of its coordinates, where the squared distance between and (from the same set) is given by .

Definition 2 (Principal space).

We define the principal space of the same vector, with a covariance matrix , as the space resulting from a change of coordinates to the principal components and rescaling by the inverse of the square roots of the eigenvalues. In this space, the squared distance between and is given by .

In the context of Model (4), the principal space is formed by the concatenation (i.e., horizontal stacking ) of and , as

| (5) |

As a result, the associated distance between two vectors and in the principal space is given by

Once we express Problem (3) in the principal space, setting and with to note an horizontal stacking and to note a vertical stacking it reads

| (6) |

Using Lagrange multipliers, the solution comes immediately as

| (7) |

Keeping in mind that the portfolio weights is the transformation by of the vertical concatenation of the two upper vector, the following property becomes immediate:

Proposition 3 (Rescaling of the expected returns operated by the portfolio construction).

Expressed in the principal space, the portfolio weights are made of the first expected returns (or signal) multiplied by the inverse of the variances of the principal components: , and for the second and last part by an exact copy of the expected returns .

This can be expressed coordinate by coordinate as follows.

Proposition 4 (Reducing the exposure to large eigenvectors).

Qualitatively, it means the portfolio construction scales down the exposures to the first eigenvectors proportionally to their eigenvalues, and it does not change the remaining components. Keep in mind that , that implies is smaller than one.

These observations have implications for the generation of synthetic time-series of returns that will be used for portfolio construction. Proposition 4 implies that the generated data should be more accurate along specific directions, particularly those corresponding to smaller , within the subspace spanned by . In other words, for portfolio construction, components associated with smaller variances are more critical than those with larger variances.

The way generic generative models learn.

On the other hand, generative models are typically trained to minimize the distance between the real data distribution and the synthetic one in the natural space. Such objective can be formalized as

| (9) |

where is a function from the set and the -Wasserstein distance [Kantorovich, 1960].333Formally, it is defined as where and are two probability distributions defined on a metric space , is the distance between points and in and is the set of all couplings of and , i.e., the set of joint distributions on with marginals and .

However, generative models trained to minimize the Wasserstein distance between the real data distribution and the synthetic one tend to make larger errors on the eigenvectors associated with small eigenvalues compared to those with large eigenvalues. As a result, the synthetic data generated for portfolio construction are exposed to uncontrolled errors. This issue is related to the following theorem.

Theorem 5 (Theorem 1 in [Feizi et al., 2017]).

Let , where is a full-rank covariance matrix, and let be a generator function that maps an -dimensional noise vector to a -dimensional space. Assume and that is the family of linear functions. Then, in the population setting, the solution to Problem (9) satisfies , where is a rank- matrix. Moreover, the eigenvectors of coincide with the top- eigenvectors of , and its eigenvalues correspond to the top- eigenvalues of .

Theorem 5 suggests that the generic loss functions of generative models drive to focus more on learning the components that explain the largest portion of total variance in the system. This can also be interpreted as these models giving less priority to, or paying less attention to, factors with smaller variance.

Although simplified, the task described in Theorem 5 is quite similar to what most generative models aim to achieve. In many applications, learning the latent factors with high variance is more crucial for generating results that appear realistic. This is often the case even when evaluating generative models that produce synthetic asset returns, where the synthetic returns are assessed based on their similarity to historical data. However, in portfolio construction, the introduction of the inverse of the covariance matrix (or similar effects) makes learning the components with lower variance at least as important as those with higher variance.

Portfolio sensitivity to eigenvector perturbations.

To better understand the impact of a generative model’s error on an eigenvector, consider the following perturbation in the column of :

where is a unit vector belonging to the subspace spanned by and is the error term controlling the magnitude of the perturbation.

Without the loss of generality, let . In this case, the first eigenvector should also be adjusted in a way that we conserve orthogonality, such as,

We denote the resulting covariance matrix under this perturbation as

| (10) |

To measure how much we deviate, at the portfolio level, due to an perturbation in the th eigenvector of under a given vector , we can define

Proposition 6 (Overall effect of perturbing a specific eigenvector in a covariance matrix).

Consider perturbing, as described above, the th eigenvector of a covariance matrix , expressed as in Model (4), by that specifies the magnitude of the perturbation. The resulting error, under an arbitrary vector , is given by:

The proof of this result is provided in Appendix LABEL:appendix:perturb.

Corollary 7 (Errors on low-variance factors are magnified).

If (which is often the case, in finance, for covariance matrices of returns), for a given vector of expected returns satisfying (recall that ), meaning there is not a significant difference between expected returns in the principal space, the following inequality holds:

where corresponds to a low-variance factor and corresponds to a higher-variance factor.

Corollary 7 highlights the fact that the same amount of error made in different eigenvectors has different impacts on the final portfolio. Specifically, errors in low-variance factors lead to significantly larger deviations between the calculated portfolio and the true optimal portfolio. Consequently, learning schemes that introduce larger errors in the subspace spanned by low-variance factors, such as generic generative models, are more likely to lead to significant errors at the portfolio level. These results underline the importance of adopting architectures that learn in the principal space rather than in the natural space—a goal we aim to achieve with the architecture proposed in the next section.

A short note on the perturbation methodology.

When perturbing an eigenvector with another vector that resides in the subspace spanned by a set of remaining eigenvectors, one must also adjust these eigenvectors to maintain orthogonality with the perturbed eigenvector. This adjustment introduces additional impacts on the portfolio, complicating a marginal analysis focused on a specific eigenvector. For this reason, we use the first eigenvector, expected to have less influence on the final portfolio, to introduce errors into other eigenvectors belonging to . If one chooses , the impact of the necessary adjustments to dominates the error introduced by a perturbation applied to . This motivates our choice of when analyzing the impact of a perturbation in .

3 Generative models for financial time-series

Now that previous section establishes that it is counterproductive to generate too many synthetic data points, and that the accuracy of the model should not be focused on directions carrying more variance, we can address the practical aspect of existing generative models and propose ourself one approach.

That for, we will first review existing models, then we will present a architecture turning around the propensity of standard generative models to focus on directions carrying the more variance.

3.1 Review of existing models

While several papers review generative models for financial time-series (e.g., [Assefa, 2020], [Eckerli, 2021], [Ericson et al., 2024], [Horvath et al., 2023], [Potluru et al., 2023]), no mention is made of two particularly important aspects of portfolio construction:

-

•

The multivariate nature of the model: Are the assets generated independently, or is there a dependency structure?

-

•

The type of financial instruments and the length of the historical data used for training.

Moreover, in existing papers, the mode of evaluation of the synthetic approach can be qualitative (it is often the case) or quantitative, and there can be (or not) an out-of-sample assessment.

| Reference | Journal | Model | Multi-asset | Cond. | Data | Visual Metrics* | Quant. Metrics* | OoS? |

| [Liao et al., 2024] | MathFin | Sig-CWGAN | Yes | Yes | S&P500 and DJI prices and realized volatilities (daily, -), BTC-USD (hourly, 2020-2021) | corr., return dist. | Sig-W1 | Yes |

| [Peña et al., 2023] | QFin | Modified-CTGAN | Yes | Yes | 10 market indices (daily, 2008-2022) | pair-plot, corr. | KS, ES, HH, and TC | Yes |

| [Sun et al., 2023] | ACM | DAT-CGAN | Yes | Yes | 4 U.S. ETFs (weekly, 1999-2016) | — | WD | Yes |

| [Dogariu et al., 2022] | ACM TOMM | GMMN (+others) | Yes | Yes | 1,506 components of S&P500 (2000-2020) | HM, ACF, VC, tails, trend ratio | KL, JS, WD | No |

| [Wiese et al., 2020] | QFin | Quant GAN | No | No | S&P500 (daily, 2009-2018) | return dist., ACF (with CI) | WD, DY, ACF, VC, LE | No |

| [Yoon et al., 2019] | NeurIPS | TimeGAN | Yes | No | Google stock open, close, high, low, adj. close, volume (daily, 2004-2019) | t-SNE | MAE, DS | No |

| [Takahashi et al., 2019] | Phys.A | FIN-GAN | No | No | 486 S&P500 components (daily, 1962-2016) | return dist., ACF, VC, LE, G/LA, CFVC | — | No |

| [Fu et al., 2022] | arXiv | TA-GAN, TT-GAN | No | No | S&P500 (2009-2020) | — | WD, HM, ACF, VC, LE (no CI) | No |

| [Cont et al., 2022] | arXiv | Tail-GAN | Yes | No | AAPL, AMZN, GOOG, JPM, and QQQ (intraday, Nov 2019-Dec 2019) | corr., ACF | VaR, ES, SBT, CT | Yes |

| [Lezmi et al., 2020] | arXiv | Cond. Bernoulli RBM/W-GAN | Yes | Yes | 6 futures contracts (daily, 2007-2019) | QQ-plot, return dist., ACF | mean, vol., quantiles, SR | No |

| [Buehler et al., 2020] | arXiv | VAE-Signature | No | Yes | S&P500 (daily, weekly, monthly, -) | paths, return dist., signature projections | MMD, KS | No |

| [Da Silva and Shi, 2019] | arXiv | DAE+CNN | No | No | AUD-USD (daily, 2009-2018) | ACF, technical analysis | mean, vol., HM, KS, VRT | No |

| [de Meer Pardo, 2019] | — | WGAN-GP/RaGAN | 2-d | Yes | S&P500 and VIX, 2000-2016; 2004-2019 | corr., ACF, HM | — | No |

| [Kondratyev and Schwarz, 2019] | SSRN | Bernoulli RBM | Yes | Yes | 4 currency pairs: EUR-USD, GBP-USD, USD-JPY, USD-CAD (1999-2019) | QQ-plot, return dist., ACF | corr., vol., quantiles | No |

Table 1 summarizes the elements of papers proposing generative models for financial time-series. We began with existing review papers and examined their bibliographies. We excluded papers that did not focus on time-series of financial instrument returns, those centered on return prediction (e.g., [Kaastra and Boyd, 1996], [Kim et al., 2019], [Koshiyama et al., 2019], [Lezmi and Xu, 2023], [Mariani et al., 2019], [Saad et al., 1998] or [Vuletić et al., 2023]), and those focusing on implied volatility (e.g., [Henry-Labordere, 2019], [Limmer and Horvath, 2023], [Vuletić and Cont, 2023] or [Wiese et al., 2019]). Although we find them very interesting, we exclude studies like [Morel et al., 2023] and [Parent, 2024], which do not rely on neural networks, to maintain the focus and feasibility of this review.

Only seven of the 14 reviewed papers have been published in journals or conference proceedings.444[Pardo and López, 2019] is not reviewed, but [de Meer Pardo, 2019] is; their models are very similar. These are listed in the upper part of the table, sorted by publication year from the most recent to the oldest. The following elements are documented:

-

•

The multivariate aspect: Are the time-series of financial instruments generated independently or not? Most models are univariate or bivariate, with the notable exception of [Dogariu et al., 2022], which generates all 1,506 time-series simultaneously.

-

•

The presence of a conditioner that can synchronize the generated time-series. Typically, this is a volatility regime indicator (e.g., instructing the model to generate high volatility or low volatility time-series). Note that conditioning can introduce correlation among time-series; for example, [Sun et al., 2023] uses the same random seed for four US ETF time-series, creating a dependency, and [de Meer Pardo, 2019] first generates one time-series corresponding to the first PCA component of returns, then conditions the other two series on this first step.

-

•

The number of time-series and the historical period: It is important to note whether no historical dataset is used, the sample is unspecified, or fewer than 10 time-series are utilized.

-

•

While some papers only provide a visual check; we list the quantitative metrics used in other papers.

-

•

Only four papers use out-of-sample data. Surprisingly, only three of the seven published papers provide out-of-sample metrics.

In conclusion, only two papers, [Dogariu et al., 2022] and [Flaig and Junike, 2023], generate more than 10 time-series in a correlated way. Additionally, while many authors check in-sample distances between generated and reference data (often part of the loss function), there is a consensus on testing the stylized facts of financial returns. See [Cont, 2010] for a description of these properties: autocorrelations, heavy tails, volatility clustering, very short memory of returns, long memory of squared returns, and skewness. These characteristics are expected in generated financial time-series to validate the use of the generative model for further applications.

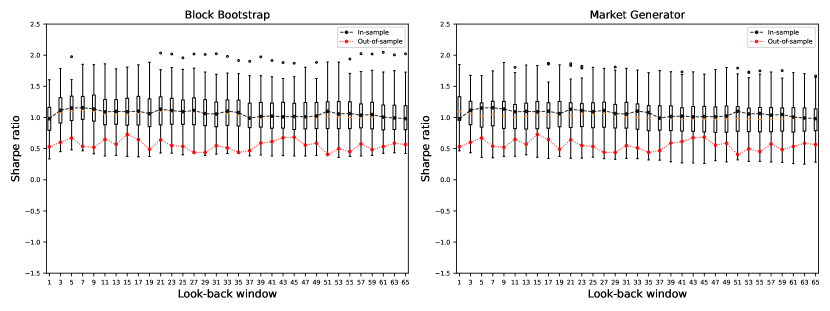

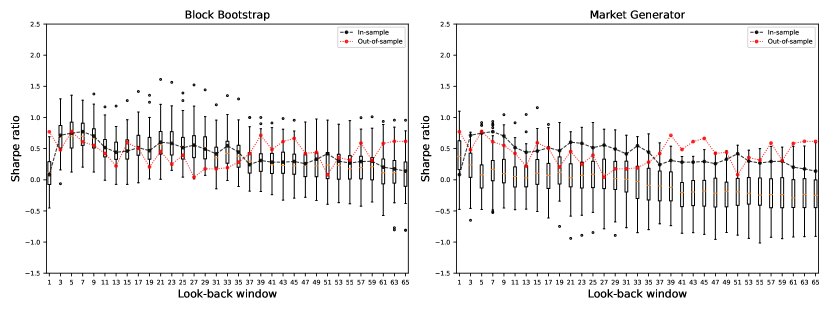

A few papers extend this analysis to check stylized facts on combinations of returns, such as profits and losses of portfolios, which are linear combinations of returns. For example, [Lezmi et al., 2020] checks risk parity portfolios, and [Peña et al., 2023] checks long-only mean-variance portfolios. We believe this is a valuable metric, as stylized facts on mean-reversion and momentum are well-known, and papers like [Bryzgalova et al., 2019] may provide a method for constructing numerous portfolios to test synthetic data from multivariate market generators.

3.2 A proposal of a generative model architecture

In this section, we propose a generative pipeline that addresses the issues outlined in the previous section and generates synthetic multivariate asset returns for use in backtesting dynamic long-short strategies. The goal is to capture the true, unknown behavior of actual asset returns as accurately as possible, ensuring relevance for the intended application.

Let be a -dimensional stochastic process of asset returns.555The index set is used to maintain coherence in the analysis presented in the following sections. The objective of generative modeling is to develop a model that captures the true characteristics of the return process using a limited sample of realizations / observations from the process, denoted by , along with any available prior knowledge about its behavior.

The basis of our framework is to model , as a function of two underlying processes:

| (11) |

where is a projection matrix, and are random variables associated with , an -dimensional process of factor returns and , a -dimensional process of residual returns, respectively. The vectors and represent the means and volatilities of individual asset returns, respectively. The underlying processes are assumed to be independent and have zero mean, i.e. and . Furthermore, we assume that where . These assumptions ensure that the individual asset means and volatilities are preserved as specified by and .

In the following subsections, we present a framework to transform in a way that we can separately learn models for the underlying components and to effectively capture the dynamics of .

3.2.1 Extracting factors from noisy returns

Let us first standardize the sample using the vectors of sample mean and volatility to obtain a sample of standardized asset returns with columns of zero means and unit variances. The covariance matrix of standardized asset returns (or the correlation matrix of ) is computed by , which can be expressed in terms of its eigen decomposition as

where is a diagonal matrix containing the eigenvalues , arranged in decreasing order, and is a matrix comprising orthogonal columns that holds the corresponding eigenvectors.666Note that , due to orthogonality.

A sample of uncorrelated factor returns can therefore be obtained through the linear transformation

where is actually a sample of the first principal component (or factor) returns which are uncorrelated with variances of , respectively.

By applying an inverse transformation, we can achieve a partial (or complete, when ) reconstruction of which allows for obtaining the remaining part in the form of residuals

where is a sample of residual returns.

Consequently, the initial sample can be written as

| (12) |

This encourages us to learn and estimate the variables and parameters that appear in Equation (11) using the above decomposition, given the obvious similarity between the two forms. Indeed, for instance, the projection matrix is estimated by .

One critical point in this approach is the choice of , which determines the part of asset returns that will be associated with the factors. The choice of is in fact free and can be obtained discretionally or using a statistical methodology of a specific kind. In this paper, we propose to use results from random matrix theory to determine the optimal number of factors .

In simplest terms, as with the ratio remaining constant, the distribution of eigenvalues of a covariance matrix computed from an matrix, whose columns consist of i.i.d. random entries with variance , converges almost surely to the Marcenko-Pastur distribution [Marchenko and Pastur, 1967] :

| (13) |

with where and .

The value sets an upper bound for the eigenvalues of covariance matrices computed on i.i.d. samples. Based on this fact, we treat, in our analysis, the eigenvalues exceeding this threshold as objects related to factors that break the i.i.d-ness, leading to a deviation from the Marcenko-Pastur distribution. Therefore, we simply use to choose . Basically, is equal to the number of eigenvalues which are greater than .777Note that in our case since is computed using standardized returns.

In this subsection, we introduced a modeling framework that views as a function of and and a means of decomposing the sample of asset returns into two samples, and . In the next subsections, we will focus on the tasks of modeling these components using the obtained samples while treating them differently in terms of modeling approaches.

3.2.2 Capturing memory using Generative Adversarial Networks

Let us first tackle the problem of modeling the factor returns . To recall, we not only want to capture the cross-asset properties of , but also existing linear and / or non-linear dependency structures across time for each of its components. In fact, we intend to capture these properties at the factor level first, which is relatively an easier task given that the number of factors is typically much smaller than the number of assets. Moreover, thanks to the orthogonal decomposition mentioned in the previous subsection, we dare to model the factors separately. We expect that reproducing these properties at the factor level will also be useful for reproducing them at the asset level, preserving cross-asset relationships through the projection matrix. Additionally, by focusing on factor-level learning, our generative pipeline becomes sensitive to factors with lower variances, as governed by the number of factors chosen, addressing the issue raised in Section 2.2.

We use the Generative Adversarial Network (GAN) framework proposed by [Goodfellow et al., 2014] to model factors. A GAN is typically composed of two neural networks, namely the generator and the discriminator, trained simultaneously on a sample of input data in order to find the set of parameters for the generator network that is capable of producing simulated data (from noise) whose distribution matches that of the input data.

We prefer to describe this process mathematically, on the basis of a concrete example of what we ultimately want to achieve to model factor returns. Let us consider the first factor which is associated with the univariate stochastic process of returns of the first factor with a sample of realizations in the form of a univariate time-series. We cannot directly use this sample for training since we want to model the relationships across time. We therefore need to build a training set out of by slicing out windows of the size we assume to be that of the length of the memory, denoted by , in the process. Consequently, we get the training set . The generator is therefore supposed to learn the joint distribution of an -dimensional random variable following a probability distribution from which is assumed to be sampled.

If we denote the generator by the function where is the parameter space for the function parameters, the goal is to find such that where is a -dimensional random variable, so-called the noise, generally assumed to follow a uniform or normal distribution.888The noise does not necessarily have to be characterized as a vector of fixed size. It can also be characterized as a matrix or higher-dimensional objects of variable size, depending on the network architecture. The optimal parameters , under which can transform random inputs into realistically looking simulations, are found through adversarial training of the generator against the discriminator denoted by the function whose output can be interpreted as the probability that the input vector is coming from .999 represents the parameter space for the discriminator parameters, which do not have to belong to the same space as the generator parameters, since the generator and discriminator can have different architectures. During adversarial training, together with , the discriminator parameters are optimized to continuously improve the discriminator’s ability to distinguish between real and synthetic data produced by the generator. This is achieved through the following optimization problem:

| (14) |

The above problem illustrates the nature of adversarial learning. For a given generator, the discriminator parameters are adjusted so that the discriminator outputs higher values if the input comes from the data distribution and lower values if the input comes from the generator. On the other hand, the generator aims to find a parameterization for which the discriminator cannot successfully perform such a distinction between real and synthetic data.

This formulation is equivalent to minimizing the Jensen-Shannon divergence [Lin, 1991] between and where denotes the probability distribution of the synthetic data . Consequently, the cross-entropy formulation in Problem (14), which we use in this paper, is theoretically justified as a way of ensuring that synthetic data will be distributionally close to the real data.101010Other types of divergence or distance measures are also used (e.g., [Arjovsky et al., 2017] and [Nowozin et al., 2016]). Regarding the use of GANs in finance, [Cont et al., 2022] proposes a loss function based on the joint elicitability property of a certain class of risk measures to capture heavy tails in asset returns.

In addition to the loss function (the objective function in Problem (14)), another critical point is the architecture choice for the generator and discriminator. We use Temporal Convolutional Networks (TCNs) as they have proven to be effective for time-series generation, initially proposed by [van den Oord et al., 2016] for raw audio and successfully applied to financial data by [Wiese et al., 2020]. They are capable of learning complex relationships between distant time points thanks to their dilation mechanism respecting at the same time the order of data. Another advantage, particularly for the generator, is that they can produce variable-sized outputs which can be determined as a function of the noise dimension.

3.2.3 Data augmentation via factor clustering

Since we aim to model factor returns separately and have already seen how to create a training set of time-series of size from a single time-series, the initial idea can be to model each factor using an individual GAN. For each factor , we can construct the sample from the time-series to obtain generators, each specific to one factor.

However, implementing separate models may not be ideal, especially when is large and since GANs are known to be data-hungry [Karras et al., 2020]. To address this, we propose to group the factors into a smaller number of clusters, specifically clusters (). This strategy enables us to model components with similar characteristics using a single model, thereby improving the ratio between the sample size and the number of parameters of the network.

First, we scale the factor returns using the associated eigenvalues to obtain series with identical first two moments. We denote this sample of scaled factor returns by where . As a result, contains time-series in its columns that have zero mean and unit variance, which should allow the clustering method to focus on more nuanced properties. This scaling will also be useful for training the GANs for the clusters, as it ensures that the training data fed into the model have the same mean and variance.

The range of methods available for clustering time-series data is extensive (see [Aghabozorgi et al., 2015]). Clustering can be handled in a fully data-driven way or by specifying relevant statistics for the properties we want to capture and running a clustering algorithm on these variables. We adopt a simple approach and use agglomerative clustering for the scaled factors , based on five statistics: skewness, kurtosis (expressed in excess throughout this paper), eigenvalue, volatility clustering score, and leverage effect score, which will be detailed in the following sections.111111The eigenvalue can be interpreted as an importance score, included to decrease the probability that significant factors (e.g., ) and less significant factors (e.g., ) fall into the same cluster unless they are very similar in other properties. This helps avoid the disruption of high-impact factors by much lower-impact factors when modeling.

As each factor now belongs to a cluster, we can build the training set on which each of the GANs will be trained. We first construct the sample for each scaled factor using the sliding window method mentioned above to obtain the sample . Then we bring these samples together by concatenating them (by rows) to obtain, for each cluster, a training set , where is the number of elements in , the set that holds the indices of the factors in the corresponding cluster. Consequently, the factors within the cluster will be learned by a single GAN, whose estimated generator parameters are denoted by , allowing it to learn from a larger dataset composed of factor return time-series with similar distributions.

3.2.4 Variance correction with non-normal white noise

In the preceding subsection, we studied the problem of modeling the first component of the random term in Model (11). We now need to focus on the second component, which might account for a significant portion of the variance observed in asset returns.

In Section 3.2.1, we related the residual returns to eigenvalues smaller than , which correspond to the part of the spectral distribution of the covariance matrix that would be formed by i.i.d. entries. Based on this choice, we model each as if they are i.i.d. without cross-dependencies. However, being aware that they can possess non-normal distributional structures, we should model the marginal distribution of in a way that is flexible enough to capture the distributional properties that can arise in univariate distributions of residual returns.

A mixture of two Student-t distributions can be a good candidate among the endless classes of parametric models. A random variable is said to follow a univariate Student-t mixture distribution with two components if

where for all , follows a Student-t distribution with location , scale , and degrees of freedom parameters and is a discrete random variable with values in and and and are mutually independent.

The probability density function is given by

| (15) |

where is the density of Student-t distribution and .121212The density of Student-t distribution is .

The advantage of Student-t mixtures is that they allow for the modeling of skewness and heavy-tails, which are two characteristics that might be observed in residual returns. We should therefore estimate from to have a model for , for all . A common approach to estimating the parameters of mixture models involves using the expectation-maximization method [Dempster et al., 1977].

Another reason why we propose Student-t mixtures is that they encompass other simpler distributions, such as Gaussian mixtures (the case when and ), Student-t () and Gaussian ( and ). These simpler distributions can be chosen to minimize the effective number of parameters to be estimated by fixing the necessary parameters in advance.

Figure 2 provides a schematic illustration of the entire pipeline depicted in this section.

3.2.5 The market generator

The above subsections are devoted to describing the transformations applied to the original data and the learning process of the generative model. Here, we focus on how to simulate a synthetic sample of length once we have the estimates for all the necessary parameters , , , and .

As a matter of fact, a simulated sample is generated by

| (16) |

where is the cumulative distribution function associated with the density in (15), is a sample (of a specific size such that the output of is of size ) with elements drawn from a standard normal distribution, is the element of the output of and is a point drawn from a uniform distribution on .

4 A fit on the S&P500 universe

In this section, we test the above pipeline on the specific dataset of daily returns of 433 stocks from Jan-2010 and May-2024 selected from the S&P500 Index.131313We use the index components as of Sep-2023 and obtain 433 stocks after removing stocks that has no data prior to Jan-2010. We split the dataset into two parts: a training set from Jan-2010 to Dec-2021 and a test set from Jan-2022 to May-2024. The aim of this section is to demonstrate that the reasoning behind our proposed modeling framework is supported by the data and that the model’s ability to generate synthetic data is reasonably satisfying at first glance under conventonial evaluation measures.

4.1 Uncovering stylized facts in asset return components

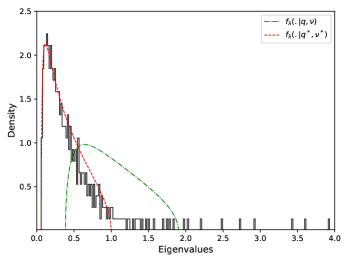

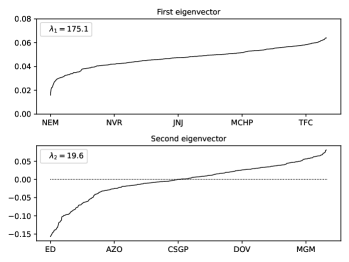

In this subsection, we analyze our specific dataset to assess the adequacy of the proposed pipeline. Let us start by applying the steps described in Section 3.2.1 to the training set . We begin by standardizing the data using the sample means and standard deviations , followed by computing the sample covariance matrix on which a full principal component decomposition is applied. The resulting eigenvalues should be used to make the distinction between factors and residuals using the upper bound which is estimated as a function of the shape of the training set and the variance of its elements, for which our dataset yields and .141414To choose a better , one could try to find the parameters providing the best fit as proposed by [de Prado, 2020]. We do not use this method in this paper for the sake of robustness and clarity although we illustrate such a fit in Figure 3 which would yield and thus 44 factors. There are 16 factors associated with eigenvalues greater then explaining 58.9% of the variance, as part of the distribution of eigenvalues illustrated in Figure 3. The chart also displays the elements of the first two eigenvectors, showing that the first factor is the market factor, with positive components for all stocks, representing a long-only portfolio of the given universe. This factor is associated with an eigenvalue significantly higher than the second one, which contains both positive and negative components and can be interpreted as a long-short portfolio.

With the chosen number of factors, a decomposition (as in Equation (12)) of standardized asset returns to the level of factors and residuals can be performed. In other words, the return of a stock for a given date with the index , , can be expressed as the sum of a factor-based return and a residual return . We adopt different modeling approaches for these components, as detailed in Section 3.2.2 and Section 3.2.4, based on the premise that factor-based returns are responsible for the dependence properties of returns, both cross-sectionally and across time, observed in financial markets [Cont, 2000].

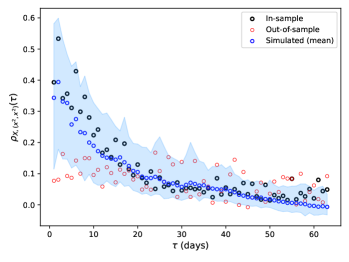

A time-dependency analysis for a given and lag is usually performed using an autocorrelation function defined as

where and denote specific functions chosen according to the analysis in question and is the correlation function between two random variables.

For example, it is well documented that asset returns generally do not exhibit significant linear autocorrelation [Fama, 1970], unless analyzed at the microstructure level, with , for . On the other hand, some interesting non-linear relationships emerge for different choices of and .

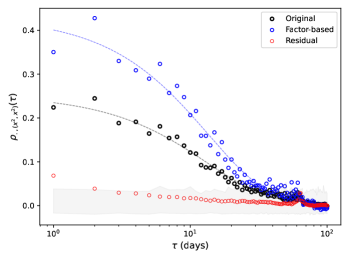

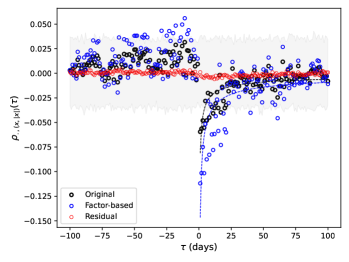

One notable phenomenon is the tendency for large price changes to be followed by other large price changes, also known as volatility clustering, as shown by the fact that or is significantly positive, at least for non-large [Ding et al., 1993]. Another important but less obvious relationship is known as the leverage effect [Bouchaud et al., 2001], which implies that negative returns lead to an increase in future volatility, often evidenced by , for . Absence of this relationship for pointing out to the time-reversal assymetry in asset returns [Zumbach, 2007].

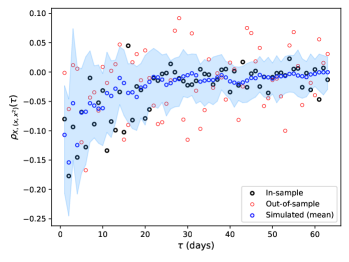

As illustrated in Figure 4, we carry out similar statistical analyses at the level of factor-based and residual returns, as well as at the level of original asset returns, to investigate how these two elements, which make up asset returns, contribute to the temporal dependence structure observed in financial markets.151515Precisely, the relevant autocorrelation value is calculated for each of the 433 stocks for a range of . Then, for each , the median value of these 433 values is plotted. Firstly, although not shown in the figure, we found that the two components do not exhibit significant linear autocorrelation, nor do the asset returns themselves. However, more interesting insights are revealed from a non-linear analysis. Indeed, factor-based returns tend to show a more severe volatility clustering effect, while this effect is relatively negligible (but not totally absent) on the residual side.161616It should be noted that these findings are obtained for the specific choice of 16 factors. The non-significant correlation observed in the squared residual returns for small lags may disappear after the inclusion of a larger number of factors. In the literature, the function is often found to be a slow-decay function as a power law with , especially when computed on intraday data [Cont et al., 1997]. In our case, for daily returns, exponential function () provides significantly better fits both for the original returns ( and ) and the factor-based returns ( and ).

Similar conclusion can be drawn regarding the leverage effect which is evident not only in the original asset returns ( and ) but also and more in the components of factor-based returns ( and ) with power law () fits indicating a significant but fast-decay of this effect. As a result, we can argue that the observed inter-temporal properties of asset returns represent a diluted form of the more pronounced effects presented by factor-based returns, but noised by residuals, underlining the importance of capturing memory in factors in our modeling framework.

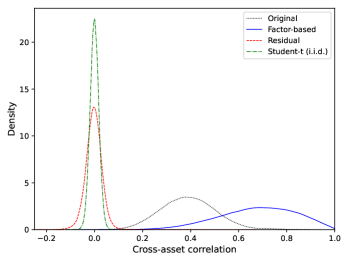

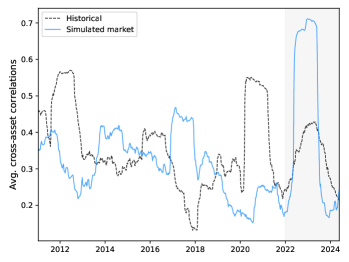

While the time-dependency properties of returns of a single asset are an area of interest for academics and practitioners, most financial problems are high-dimensional and require an understanding of the joint behavior of a large number of assets. The correlation matrix of asset returns is the main tool for analyzing these relationships linearly. It is often preferred over the covariance matrix for pure co-movement analysis, as it is unaffected by individual asset volatilities. For example, in the case of equities, stock returns within the same market tend to exhibit high correlations, with even higher correlations observed between stocks in the same sector, resulting in clusters within the correlation matrix.

However, it is fair to say that the roles of factor-based and residual returns in contributing to asset correlations are not necessarily the same although their impacts to the total variance are similar. As indicated in Section 3.2.1, the distribution of eigenvalues associated with residuals resembles the spectral distribution of a correlation matrix calculated on random entries. The fact that the correlations between asset returns are induced by a few factors forming factor-based returns is demonstrated in Figure 5 and Table 2 where we see that the correlations between residual returns are small and centered around zero. Figure LABEL:fig:correl_of_three_comps in Appendix LABEL:appendix:visual provides an illustration of the three correlation matrices computed on historical data.

| Cross-asset correlations | |

|---|---|

| Original | 0.39 [0.18, 0.63] |

| Factor-based | 0.69 [0.34, 0.94] |

| Residual | 0.00 [-0.07, 0.06] |

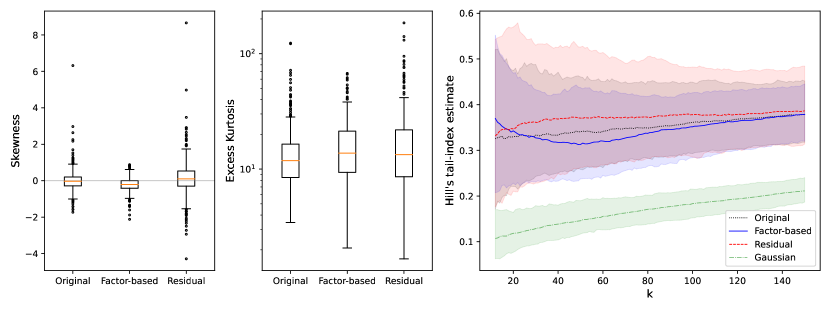

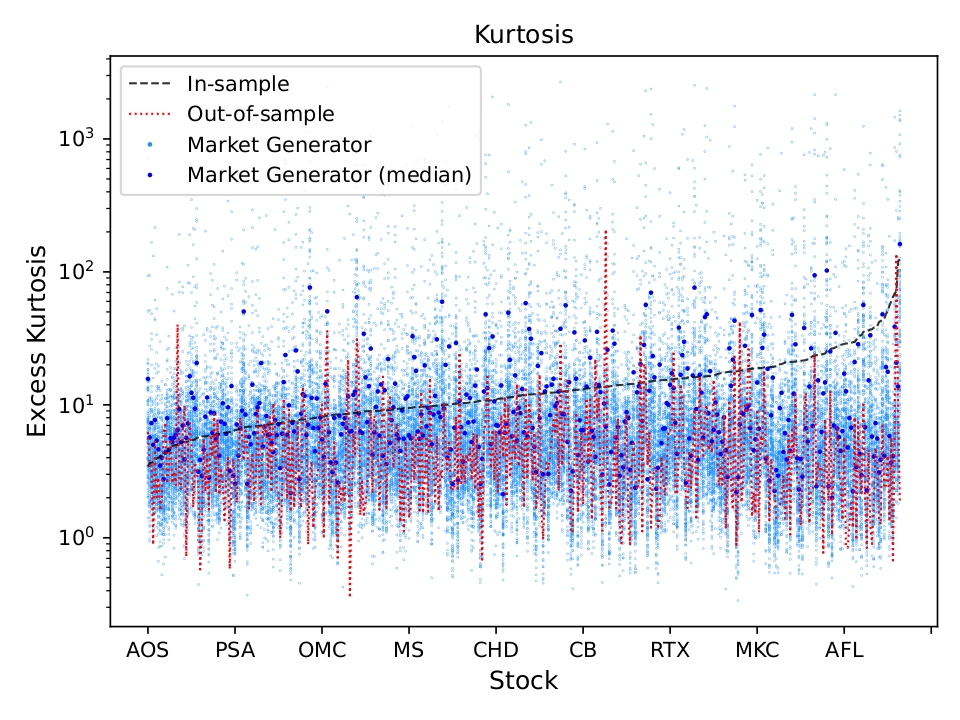

In addition to inter-temporal and cross-asset dependencies, the marginal distributions of asset returns also exhibit unique properties. Among the most notable are asymmetry in gains and losses and the heavy-tailedness of the asset return distribution. The former is often characterized by the negative skewness of asset returns, indicating a tendency for more extreme downward movements than upward movements, with downward moves being less frequent. While kurtosis can provide insight into heavy-tailedness, a more nuanced analysis on losses involves estimating the tail-index of the marginal distribution of asset returns using alternative estimators, such as Hill’s tail-index estimator:

| (17) |

where denotes the order statistic of a given sample of asset returns . Loosely speaking, the parameter , specified based on the sample size, sets the threshold beyond which it is believed the tail begins.171717This is why the term inside the logarithm in Equation (17) is often positive, preventing any issues from arising. However, the estimated value of can be highly dependent on the choice of . Therefore, it is common practice to compute it for different values of . Intuitively, this estimator evaluates how losses beyond a certain quantile deviate from the selected level on average, offering an estimation of the heaviness of the left-tail where the tail-index is estimated by .

Figure 6 provides some interesting insights into the marginal distributions of the different components of returns. First, factor-based returns appear to exhibit a consistent negative skewness for most assets, while skewness estimates for residual and original returns tend to vary around zero, although they can reach significantly high positive or negative levels. This suggests that the widely observed negative asymmetry in asset returns may be attributed more to common components that drive returns rather than being solely a feature of individual assets. However, the same argument may not hold for extreme returns and losses, as both components of asset returns exhibit particularly high kurtosis for almost all assets. A similar analysis focusing on the left tail can be carried out by estimating the tail index. Essentially, the well-known phenomenon of heavy tails in asset returns cannot be attributed solely to the presence of a single component, since the factor-based returns and residuals for the majority of stocks simultaneously exhibit this phenomenon in their distributions, as supported by Table 3.

| Skewness | Kurtosis | Tail Index | |

|---|---|---|---|

| Original | -0.03 [-1.01 1.18] | 11.8 [4.4 42.9] | 2.84 [2.19 3.62] |

| Factor-based | -0.21 [-1.10 0.55] | 13.8 [3.8 46.1] | 2.91 [2.30 3.75] |

| Residual | 0.10 [-1.82 2.21] | 13.3 [4.0 64.2] | 2.68 [1.99 3.67] |

In conclusion, the observations above serve as motivation for our approach to modeling asset returns from the perspective of two distinct components with differing characteristics. We have observed that most of the stylized facts of asset returns are present in the factor-based returns, sometimes more prominently, suggesting that they may warrant modeling using complex tools capable of capturing properties at both the temporal and cross-sectional levels. For the former, we use a memory of length of days, and for the latter, the cross-sectional properties are incorporated exogenously via the projection matrix .

Conversely, residuals can be treated as independent and identically distributed (i.i.d.) given the relative absence of linear and non-linear dependence over time, and the insignificant correlations. However, the model should still better account for their skewed and heavy-tailed nature, making a mixture of Student-t distributions a reasonable choice. For the sake of simplicity, we omit the asymmetry of residual returns and use a Student-t distribution (fixing in Equation (15)) and estimate the parameters for residuals of each asset using the maximum likelihood approach.

Recall from Section 3.2.3 that the selected factors are to be modeled by a smaller number of GANs trained on clusters of factors. In our numerical case, 16 factors are grouped into clusters based on 5 features. Specifically, these features include sample skewness and kurtosis computed on standardized daily factor returns, the eigenvalue associated with each factor, the volatility clustering score, and the leverage effect score computed over 63 days according to the following formula, with appropriate choices of being and , respectively:181818The sign of the final score is adjusted based on the slope of the curve, if necessary, to prevent bias caused by the symmetric nature of the score function around the x-axis.

| (18) |

The agglomerative clustering algorithm applied to the above features results in the sets , and . Therefore, 3 GANs with the same architecture and initial hyperparameters are trained using the training sets constructed based on the given clusterings. Details about the neural network architecture and training design are provided in Appendix LABEL:appendix:TCN, along with figures related to the evaluation of data generated by each of the three generators in Appendix LABEL:appendix:visual.

The training pipeline depicted in this subsection allows us to obtain the necessary parameters for the market generator as described by Equation (16). In the next section, we will assess the quality of the simulated data to determine whether it can effectively reproduce the learned properties present in asset returns.

4.2 A first look at simulated data

Although generative models have attracted attention and been used in a wide range of fields, there is no consensus on how to evaluate and validate what is produced by the trained model (see [Borji, 2018] for a review of evaluation measures). It is natural to expect different evaluation measures in different domains, but the lack of a common set of intra-domain measures makes it difficult to compare and horse-race models that have proved instrumental in the theoretical progress of deep learning over the last decade, as we have seen with ImageNet [Deng et al., 2009]. The considerable efforts being made to benchmark and evaluate LLMs also underline the importance of the issue [Hendrycks et al., 2020].

The absence of a generic evaluation procedure in finance is probably not due to the negligence of academics and practitioners, but to the specific character of the field. First of all, visual human inspection is extremely difficult, if not impossible, as opposed to the above mentioned cases of image-recognition and text-generation. Second of all, the nature of the generated data can be quite diverse, like market microstructure data [Cont et al., 2023], implied volatility surfaces [Vuletić and Cont, 2023], retail transactions [Lopez-Rojas and Axelsson, 2015], asset return / price processes and more.

The third point, which we touched on theoretically in Section 2.2 and which we shall explore in greater depth in Section 5, is the influence of the final application in the evaluation process, and the problematic nature of using the same measures even if the data generated is of the same type but comes from two distinct models designed for different purposes. In this subsection, we put this latter point aside and aim to perform a generic evaluation to assess the quality of the data generated by our market generator as rigorously as possible for a high-dimensional universe independent of the ultimate application, and show that we can obtain quite promising results from the market generator at least at first sight.

4.2.1 A marginal point of view

If we are in a context of generating multivariate asset returns, a generative model should ideally be capable of capturing the joint dynamics of the universe both cross-sectionally and inter-temporally. It is often more appropriate to carry out such an assessment with multiple evaluation steps, given the difficulty of doing a one-shot evaluation of the model as a whole.191919An asset-by-asset evaluation can also be performed, as demonstrated for a specific stock in Figure LABEL:fig:jpm_eval in Appendix LABEL:appendix:visual, however this approach is not scalable and does not provide insight about the correlation structure.

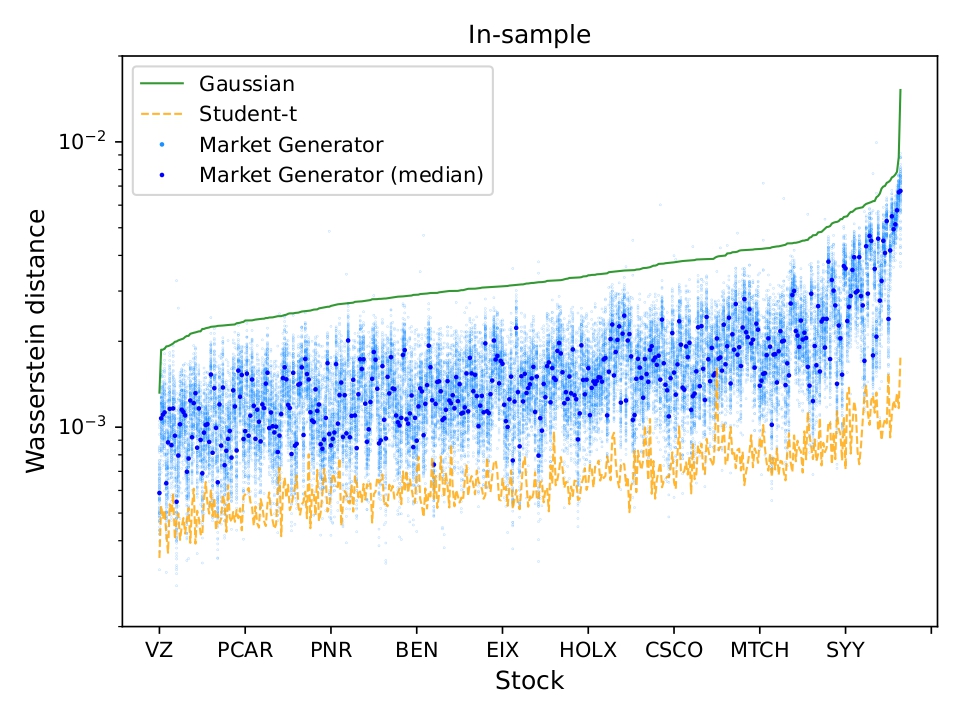

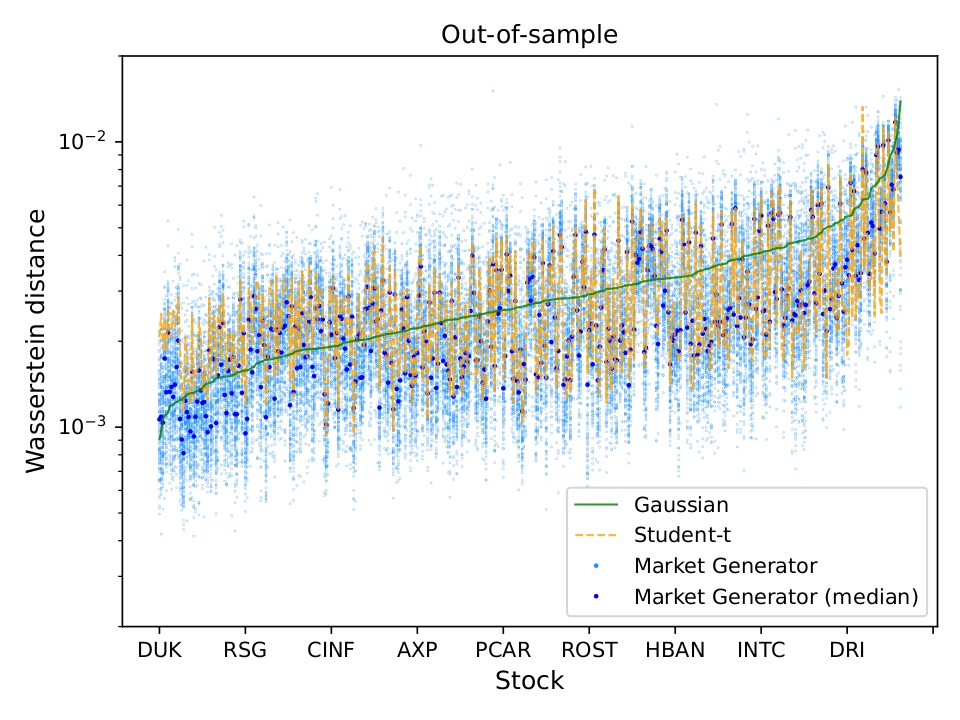

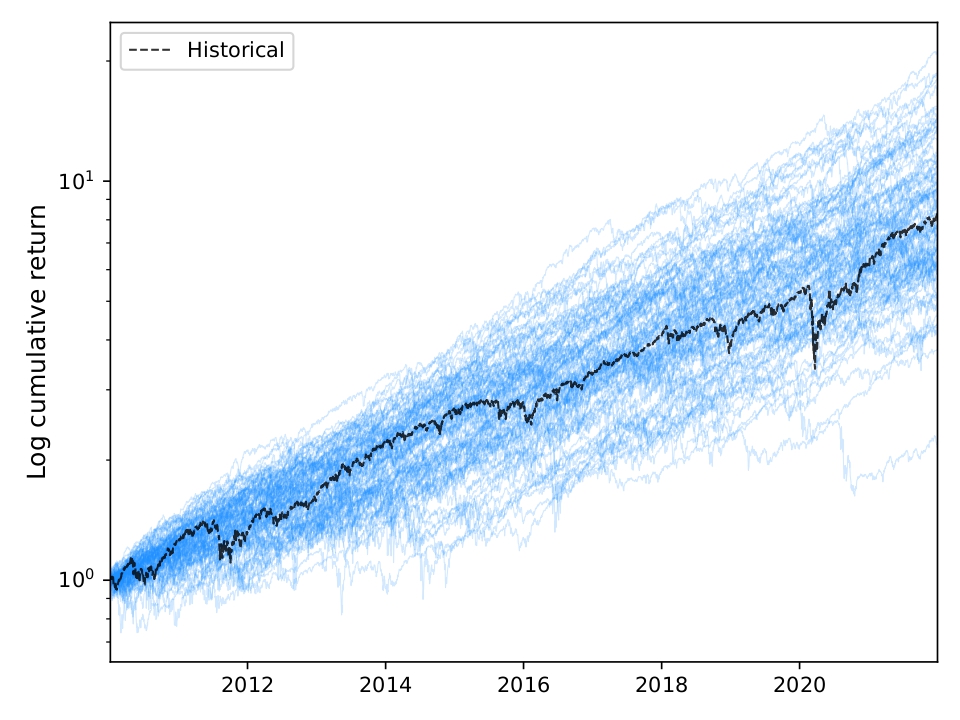

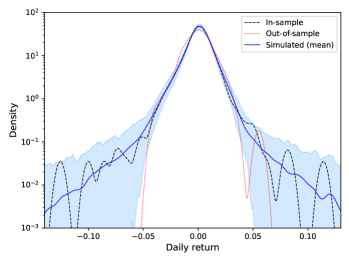

First, we generate 100 simulated samples of the length of the training set, , from the market generator following the ideas developed in Section 2.1 regarding the balance between initial sample size and generated data.202020It corresponds to generating 100 different . We begin by understanding whether the marginal distributions of asset returns in the generated scenarios are close to those observed historically, both in-sample (training set) and out-of-sample (test set). We use 1-Wasserstein distance as a measure of distance between simulated and historical distributions. For the empirical distributions, it boils down to a simple function of order statistics of the historical and simulated samples.

Figure 7 illustrates the distances between the distribution of returns for each asset, in all scenarios, and the in-sample / out-of-sample distributions.212121For a fair comparison with out-of-sample scenarios, we generate another 100 simulated samples of the length of the test set, . For ease of comparison, the distances obtained by Gaussian and Student-t fits (obtained marginally for each asset using the training set) are also included. We see that the market generator provides better out-of-sample results on average, while Student-t distributions fit well in-sample but underperform out-of-sample due to likely overfitting issues, as shown in Table 4. The results look reasonably satisfactory in terms of marginal distributions for a modeling framework in which we do not learn directly from marginal distributions.

| In-sample | Out-of-sample | |

|---|---|---|

| Gaussian | 3.19 [2.02, 6.84] | 2.69 [1.23, 7.59] |

| Student-t | 0.65 [0.43, 1.24] | 2.40 [1.21, 7.21] |

| Market Generator | 1.45 [0.79, 4.35] | 2.26 [1.07, 7.10] |

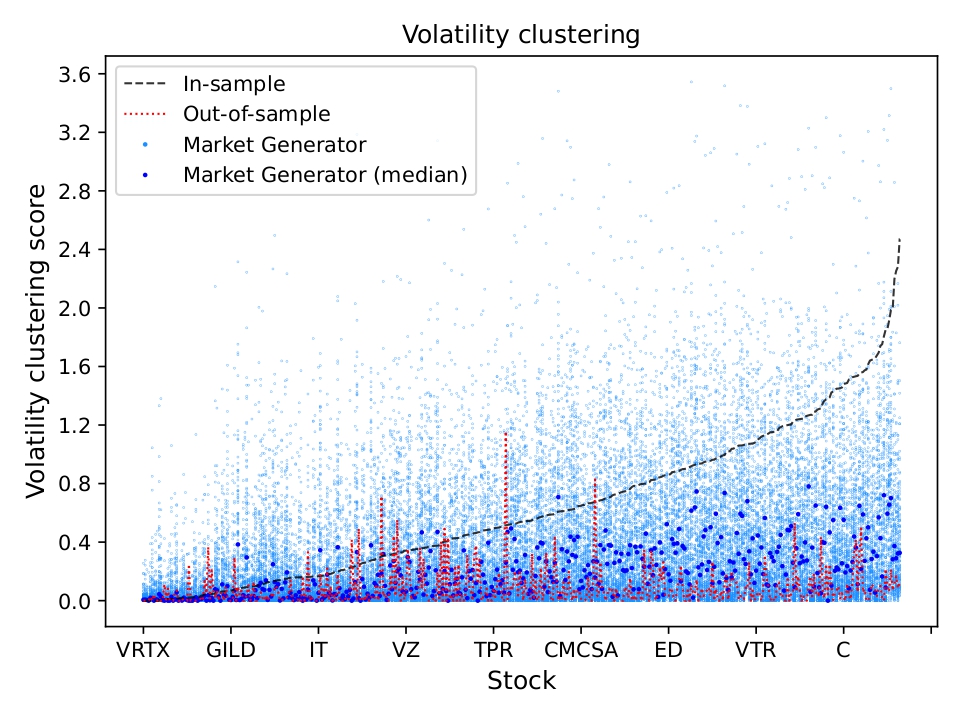

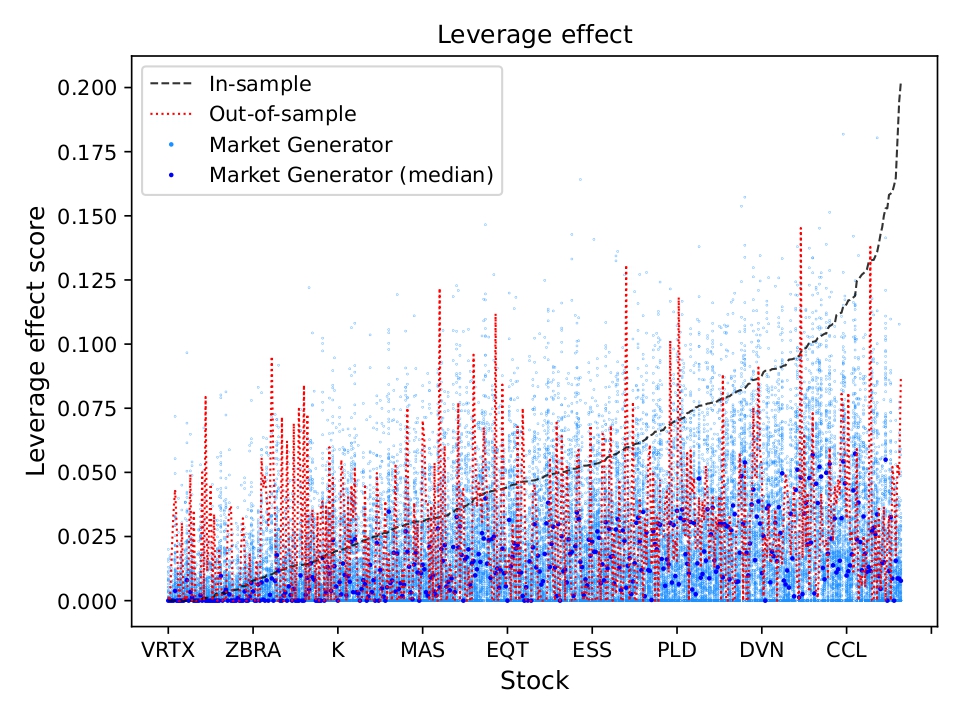

To understand the model’s ability to reproduce inter-temporal effects at the asset level, we can consult the volatility clustering and leverage effect scores as defined in Equation (18). Figure 8 illustrates the scores computed on historical and simulated samples for each asset. It seems that the upward trend in in-sample scores is captured by the market generator up to a certain level, as shown by the increasing dispersion of the calculated scores and the upward trend in median scores for the simulated samples. Table 5 also shows that, in the market scenarios produced by the market generator, asset returns exhibit a time-dependency structure similar to that which we observe historically.

| Volatility Clustering | Leverage Effect | |

|---|---|---|

| In-sample | 53.88 [0.69, 174.34] | 4.69 [0.0, 14.65] |

| Out-of-sample | 3.60 [0.0, 42.94] | 2.08 [0.0, 8.77] |

| Market Generator | 14.66 [0.0, 63.77] | 1.16 [0.0, 4.84] |

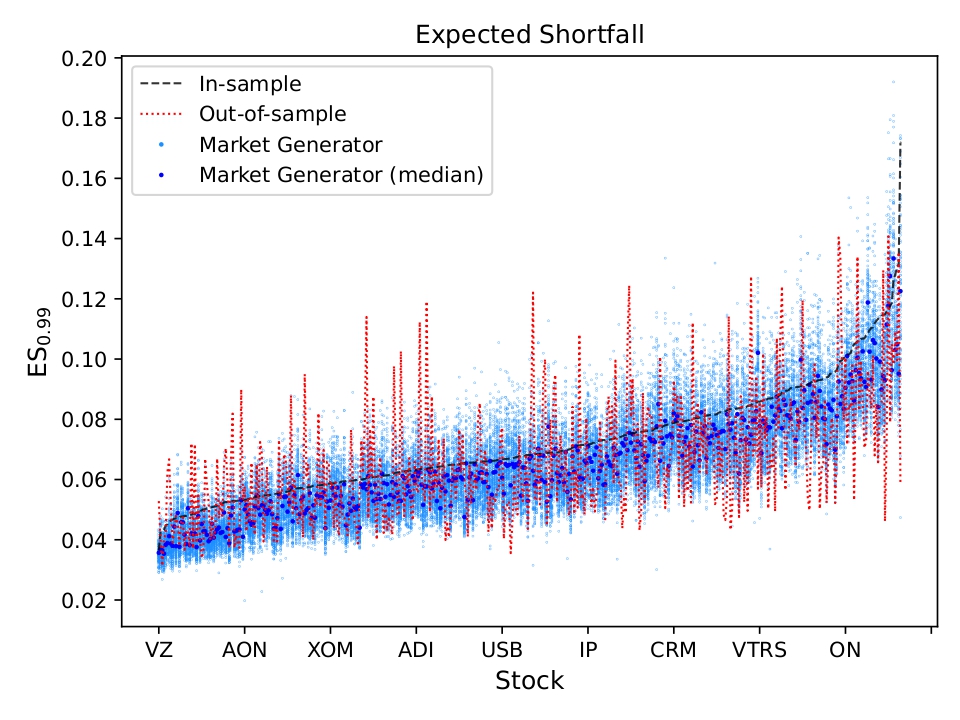

Another aspect that deserves particular attention is the tail of asset return distributions, which are one of the most significant properties of asset returns, particularly when it comes to risk. Consequently, a market generator unable to generate extreme losses misses out one of the most crucial phenomena of asset returns.

A standard way to conduct an analysis of the left-tail of return distributions is to use Value-at-Risk (VaR) and Expected Shortfall. VaR at the level is simply a quantile of loss distribution of a real-valued random variable (regarded as a loss) and Expected Shortfall, on the other hand, is the average loss given that the loss exceeds .222222Formally, and Consequently, the similarity of VaR and Expected Shortfall (at high levels of ) computed on historical and simulated samples, along with high kurtosis, should give an indication of the heavy-tailedness of the simulated marginal distributions, as summarized in Table 6 and illustrated in Figure 9.

| In-sample | Out-of-sample | Market Generator | |

|---|---|---|---|

| 2.5 [1.7, 4.1] | 2.7 [1.8, 4.8] | 2.6 [1.8, 4.5] | |

| 4.6 [3.1, 7.5] | 4.6 [3.0, 8.0] | 4.5 [2.9, 7.5] | |

| 4.0 [2.7, 6.6] | 4.0 [2.7, 7.0] | 3.9 [2.6, 6.6] | |

| 6.8 [4.7, 11.4] | 6.1 [3.9, 11.9] | 6.2 [3.8, 10.2] | |

| Kurtosis | 11.8 [4.4, 42.9] | 3.4 [0.9, 24.2] | 4.7 [1.9, 14.2] |

Until now, we have tried to verify whether we could get close to the marginal properties of individual asset returns by omitting the relationships between them, which are one of the most critical parts of multivariate modeling. To understand if at least linear relationships exist within the universe in a similar way to those observed historically, we analyze the distance between the sample correlation matrix calculated on simulated and historical returns :

where denotes a sample correlation matrix calculated on a simulated sample and denotes a sample correlation matrix calculated on a historical sample (in-sample or out-of-sample). We also include two other estimators in our analysis to make the distance values meaningful. The first is what we call the one-factor model, which is simply a correlation matrix in which all correlations between assets are equal to the average correlations calculated in-sample. Although overly structured, such an approach is not completely unrealistic. The second correlation matrix estimator we consider is obtained using the covariance matrix estimate resulting from the Ledoit-Wolf estimator:

where is the sample covariance matrix and is the trace of the covariance matrix. The optimal can then be found such that the distance to the true covariance matrix is minimized (see [Ledoit and Wolf, 2003]).

| In-sample | Out-of-sample | |

|---|---|---|

| One-Factor | 13.27 | 20.98 |

| Ledoit-Wolf | 0.04 | 13.23 |

| Market Generator | 2.27 [0.79, 11.71] | 16.39 [11.60, 112.10] |