none \acmConference[] \copyrightyear \acmYear \acmDOI \acmPrice \acmISBN \affiliation \institutionSingapore University of Technology and Design \countrySingapore \affiliation \institutionSingapore University of Technology and Design \countrySingapore \settopmatterprintacmref=false \setcopyrightnone

Truthful mechanisms for linear bandit games with private contexts

Abstract.

The contextual bandit problem, where agents arrive sequentially with personal contexts and the system adapts its arm allocation decisions accordingly, has recently garnered increasing attention for enabling more personalized outcomes. However, in many healthcare and recommendation applications, agents have private profiles and may misreport their contexts to gain from the system. For example, in adaptive clinical trials, where hospitals sequentially recruit volunteers to test multiple new treatments and adjust plans based on volunteers’ reported profiles such as symptoms and interim data, participants may misreport severe side effects like allergy and nausea to avoid perceived suboptimal treatments. We are the first to study this issue of private context misreporting in a stochastic contextual bandit game between the system and non-repeated agents. We show that traditional low-regret algorithms, such as UCB family algorithms and Thompson sampling, fail to ensure truthful reporting and can result in linear regret in the worst case, while traditional truthful algorithms like explore-then-commit (ETC) and -greedy algorithm incur sublinear but high regret. We propose a mechanism that uses a linear program to ensure truthfulness while minimizing deviation from Thompson sampling, yielding an frequentist regret. Our numerical experiments further demonstrate strong performance in multiple contexts and across other distribution families.

Key words and phrases:

Contextual linear bandit, private context, truthful mechanism, regret bound1. Introduction

The contextual bandit problems have received increasing attention over the past decade, beginning with Auer’s introduction of the concept Auer (2002); Chu et al. (2011); Abbasi-yadkori et al. (2011); Agrawal and Goyal (2013); Abeille and Lazaric (2017). In the contextual bandit model, an arbitrary set of observable actions is available at each time step, and the reward for each action is determined by an unknown parameter shared across all actions. The contextual bandit excels in making personalized decisions by using contextual information to select the best possible actions. This allows for more efficient learning and better adaptation to dynamic environments compared to traditional bandit models.

However, these models do not align with scenarios involving private contexts and fail to capture the challenges posed by private information. In the new stochastic bandit problem involving private contexts Lazaric and Munos (2009); Goldenshluger and Zeevi (2013); Rakhlin and Sridharan (2016); Bastani et al. (2021), at each time step, a new agent arrives, reports her private context, and the system selects one of the available arms, where each arm is associated with a different unknown parameter. The agent then receives a stochastic reward based on the system’s chosen action, after which she leaves. This scenario is common in applications like clinical trials and online recommendations, where agents may strategically misreport private contexts to maximize single-round personal rewards. For example, in adaptive clinical trials of phase 2 INSIGHT trial where hospitals test treatments for glioblastoma based on patients’ symptoms and medical history, some patients may misreport side effect histories like allergies or anemia to avoid the less-established abemaciclib treatment Food and Administration (2017); Rahman et al. (2023). On online platforms like Netflix or Amazon, many users prefer recommendations based on popular choices or expert curation GrowthSetting (nd).

In this new stochastic contextual linear bandit problem with private contexts, previous works assume observable and public contexts and do not consider the agents’ strategic behavior to game the system. The conflict between the system’s long-term reward and the individual’s immediate reward in the multi-armed bandit problem has been studied for the past decade Kremer et al. (2014); Mansour et al. (2020, 2022); Sellke and Slivkins (2021); Hu et al. (2022); Immorlica et al. (2020); Sellke (2023). Kremer et al. Kremer et al. (2014) initiate the research within a Bayesian exploration framework, introducing a recommendation mechanism for incentivizing exploration with deterministic rewards. Mansour et al. Mansour et al. (2020) further develop the problem to the stochastic rewards. Sellke and Slivkins Sellke and Slivkins (2021) first prove that Thompson sampling algorithm can be naturally incentive-compatible (IC) if provided with sufficient initial samples. Then Hu et al. Hu et al. (2022) and Simchowitz and Slivkins Sellke (2023) extend this result to the combinatorial and linear bandit problems. Beyond recommendation mechanisms, Immorlica et al. Immorlica et al. (2020) apply selective disclosure of historical information to encourage exploration. Simchowitz and Slivkins Simchowitz and Slivkins (2024) also study this problem in reinforcement learning. These works assume that the system has the full information about agents for the recommendation, then the problem is to design the IC mechanisms that ensure agents follow the recommendation. In contrast, our system needs agents to report their private contexts, where the system lacks context information, and agents may strategically misreport their private contexts, rendering these methods ineffective for the problem addressed in this paper.

Our main contributions are summarized as follows:

-

•

We are the first to study agents’ strategic context misreporting to maximize their one-time individual expected rewards in the new contextual bandit problem. We demonstrate that existing algorithms perform poorly under misreporting. Specifically, existing truthful algorithms, such as the greedy and explore-then-commit (ETC) methods, suffer from relatively high regret, while low-regret algorithms like UCB family algorithms and Thompson sampling exhibit a regret of under strategic misreporting.

-

•

We propose a truthful mechanism based on Thompson sampling algorithm which guarantees that agents have no incentive to misreport their contexts. We prove that our algorithm achieves a frequentist regret upper bound of in the Bayesian contextual linear bandit setting. Additionally, our experiments show that the mechanism has sublinear regret when applied to multiple contexts and across some other sub-Gaussian distributions.

1.1. Related work

Stochastic contextual linear bandit algorithms can be categorized into deterministic algorithms, which make deterministic choices, and stochastic algorithms, which maintain a probability distribution among arms for selection. When facing agents’ context misreporting, deterministic algorithms in which the choice depends on context cannot ensure truthful reporting in exploration because the resulting arm choices are predictable. Therefore, deterministic low-regret algorithms like the UCB family Chu et al. (2011); Abbasi-yadkori et al. (2011) suffer from linear regret in the worst-case scenario as shown in Section 3 in this paper. Another deterministic algorithm, the Explore-Then-Commit (ETC) algorithm, does not rely on agents’ context but is inefficient, incurring a relatively high regret of order Lattimore and Szepesvári (2020). For stochastic algorithms, the -greedy algorithm is truthful as its exploration probability is independent of the context, but it also incurs a regret order of Slivkins et al. (2019).

Another stochastic low-regret algorithm is Thompson sampling, which was first adapted by Agrawal and Goyal in Agrawal and Goyal (2013) for the contextual linear bandits problem. Abeille and Lazaric in Abeille and Lazaric (2017) further improve the frequentist regret of linear Thompson sampling. Thompson sampling is also widely applied to Bayesian bandit problems, as it naturally leverages posterior distributions. Russo and Van Roy Russo and Van Roy (2014, 2016) provide the Bayesian regret upper bound for Thompson sampling, with frequentist regret serving as an upper bound on Bayesian regret. However, we will show in Section 3 that Thompson sampling is not truthful and still suffer from linear regret under misreporting behavior.

Regarding context misreporting behavior, Buening et al. examine this phenomenon in a different problem in Buening et al. (2024). Their work considers arms as repeated strategic entities that manipulate rewards to increase their chances of being chosen. While they also address context misreporting behavior, their focus fundamentally differs from ours, and their approach is inapplicable to our problem, as our agents are non-repeated and myopic.

2. Problem formulation

We consider the Bayesian contextual linear bandit model in Bastani et al. (2021). There are arms in the set , each associated with an unknown, fixed -dimensional hidden parameter . These parameters are unknown to both the system and the agents but are drawn from a known prior distribution . The prior distributions for any are common knowledge for both the system and the agents. We define the prior mean of each as and the covariance matrix as .

At each time , a new agent arrives with a private context , where is a set of finite contexts. We assume that each takes the value with a known probability , where 111Our mechanism also works when the arrival probability is unknown. We can initialize the mechanism with a uniform discrete context distribution and adjust as we learn and update it throughout the process.. The system first provides its history , which includes previously observed contexts, actions, and rewards, as well as the arm selection policy for all contexts which defines a probability distribution over the arms, to the agent. After receiving this information, the agent reports the context to the system. Based on the reported context , the system selects an arm and only observes the corresponding reward , where is a zero-mean random variable. The system then updates the posterior estimation of the chosen arm to , and the posterior distribution to .

We begin by considering Gaussian priors and Gaussian noise to provide a clearer illustration of the problem and to facilitate the analysis of frequentist regret, as in Agrawal and Goyal (2013, 2017). Specifically, we assume and . This assumption allows for closed-form updates of and , making the analysis more tractable. Still, our mechanism is applicable to any family of prior and noise distributions. In Section 7, we use simulations to demonstrate that the mechanism design in Section 4 achieves good regret performance under other sub-Gaussian distributions. Under Gaussian priors and Gaussian noise, the posterior distribution is , where and are updated as follows:

| (1) |

where denotes the set of time steps when the system chooses arm before time .

We now formulate the objectives of both the agents and the system. Given the arm choice policy for any provided by the system, the agent arriving with context chooses to report the context that maximizes her expected reward, expressed as:

| (2) |

where represents the matrix of posterior estimates at time . Based on Eq. (2), we then present the definition of the truthful mechanism as follows:

Definition \thetheorem.

A mechanism is considered truthful in our Bayesian contextual linear bandit problem if no agent can increase her expected reward by misreporting her true context at any time step. Formally, for any history and any pair of distinct contexts and in , the following condition holds at each time step :

| (3) |

When a context has an incentive to misreport as another context , we say that contexts and have conflict.

Conversely, the system’s objective is to maximize the cumulative reward, or equivalently, to minimize the expected total regret by choosing for each time step in the truthful mechanism . Let denote the optimal arm for the agent arriving at time . The expected total regret is:

| (4) |

Building on the truthful mechanism defined above, we will next analyze the behavior of existing bandit algorithms under misreporting.

3. Performance analysis of existing algorithms under misreporting

In this section, we present comprehensive studies on the performances of existing deterministic and stochastic algorithms under agents’ possible misreporting.

3.1. Deterministic Algorithms

In deterministic algorithms, the algorithm selects one of the arms based on the history with probability 1 at each time step. A well-known class of deterministic algorithms for the contextual linear bandit problem is the UCB family, including LinUCB Chu et al. (2011) and OFUL Abbasi-yadkori et al. (2011), which select arms at each time step based on upper confidence bounds. However, UCB family algorithms are vulnerable to misreporting because their allocation is predictable, allowing agents to easily manipulate their reported context to favor the currently optimal arm, which can lead to linear regret in the worst-case scenario.

In contrast, the deterministic Explore-Then-Commit (ETC) algorithm, which first operates in a round-robin exploration phase before switching to a purely greedy strategy, is truthful because its decisions are independent of personal contexts, making agents’ context reporting irrelevant to the algorithm’s choice. However, the ETC algorithm incurs a relatively high regret of Lattimore and Szepesvári (2020).

3.2. Stochastic Algorithms

In stochastic algorithms, the algorithm maintains a probability distribution over the arms at each time step and selects an arm according to this distribution. The -greedy algorithm, which selects the greedy arm with probability and chooses an arm uniformly at random with probability , is truthful since can be set so that the selection probability is independent of the contexts. However, it also suffers from a relatively high regret of Slivkins et al. (2019). Next, we consider Thompson sampling algorithm Agrawal and Goyal (2013).

In Thompson sampling, given the reported context at each time step, the system draws a sample from the posterior distribution of , denoted as , and then selects arm . Note that represents the posterior distribution of at time , whereas is the posterior distribution of . The process of first sampling from and then multiplying it by yields the same result as directly sampling from when assuming Gaussian prior and noise. Therefore, the distribution of arm selection in Thompson sampling, which is also the policy at time is:

| (5) |

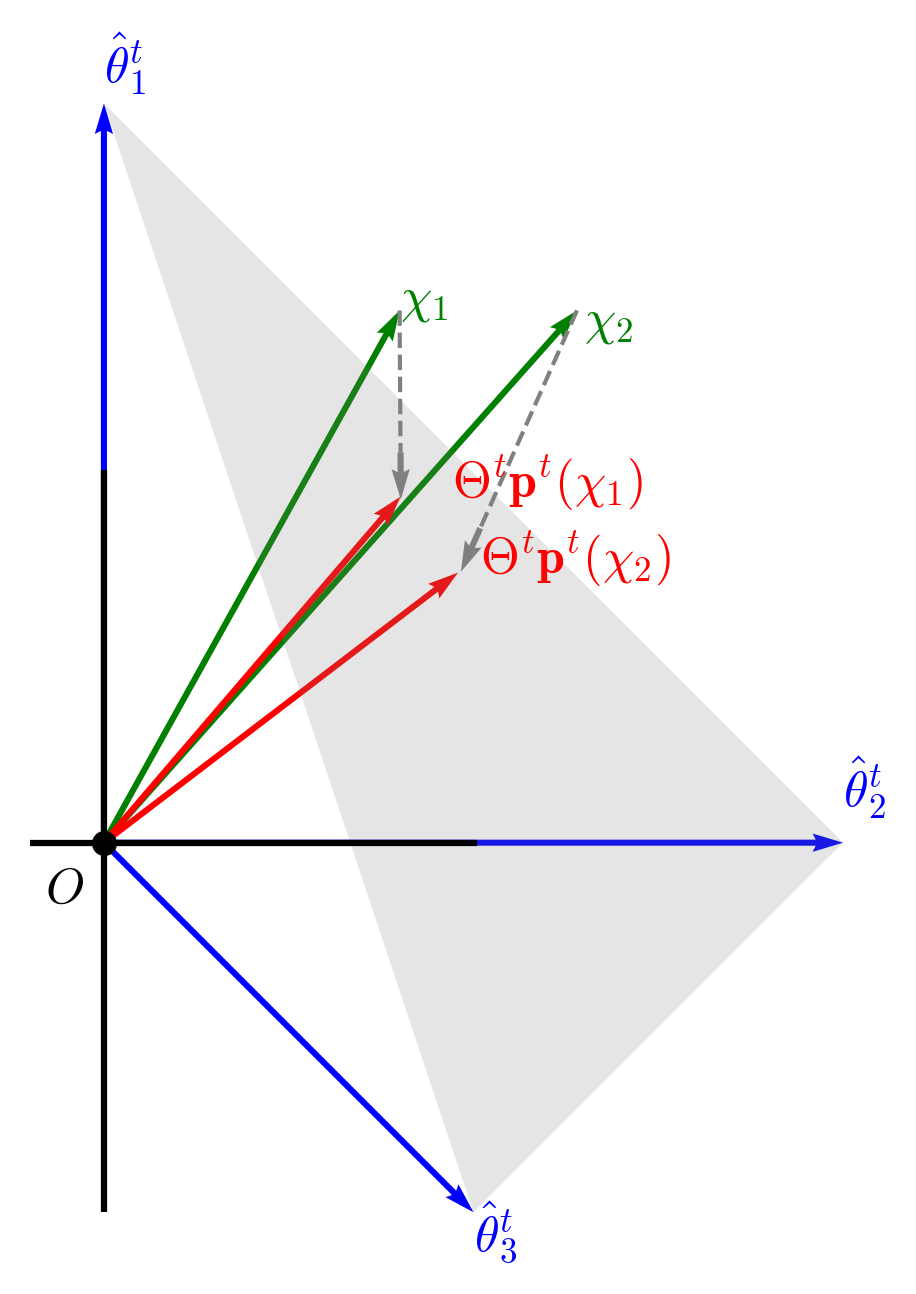

We can demonstrate that Thompson sampling is not truthful through a simple example in Fig. 1. At time , given the posterior estimation for all and the expected arm choice policy in (5), the resulting expected parameter lies within the convex hull . Therefore, Thompson sampling can be seen as a mapping from any context to within the convex hull. In the Thompson sampling mapping of and in Fig. 1, context yields a higher inner product with than with . Consequently, if arrives at time , it will misreport as .

We further prove the regret of Thompson sampling under the context misreporting.

Lemma \thetheorem

Thompson sampling algorithm cannot ensure truthful context reporting and results in linear regret in the worst case.

Sketch of Proof.

We prove the lemma by constructing an example in which, given a specific prior , one of the contexts has an incentive to misreport. Then, under a certain context arrival distribution , we find a positive probability that the algorithm fails to identify the true optimal arm for this context throughout the process and ultimately converge to a suboptimal arm for this context. The complete proof of Lemma 3.2 can be found in Appendix A. ∎

Given that existing deterministic and stochastic algorithms fail due to either untruthfulness or inefficiency, there is a need to design more effective, truthful mechanisms.

4. Truthful Thompson sampling mechanism

In this section, we introduce our truthful-Thompson sampling (truthful-TS) mechanism for contextual linear bandits to ensure truthful reporting under Thompson sampling. Our objective is to determine a new probability distribution across the arms at each time for any that guarantees truthfulness. We derive from the Thompson sampling probabilities in Eq. (5), aiming to keep as close as possible to . To achieve this, we formulate a linear optimization problem (LP) at each time , given by:

| minimize | ||||

| s.t. | ||||

| (6) |

In (6), the objective is to minimize the maximum difference between any and across all possible contexts, keeping the new distribution as aligned as possible with the Thompson sampling probabilities. The first constraint ensures that the agent with private context cannot obtain a higher expected reward by misreporting as than the reward by truthfully reporting. The second constraint ensures that the weighted average of choosing arm across all contexts, based on the arrival probability of context , remains the same as the weighted average of Thompson sampling probability . The third and fourth constraints ensure that the solution for each forms a valid probability distribution.

Based on (6), we present our truthful-TS mechanism in Mechanism 1. To demonstrate the feasibility of our mechanism, we first need to show that the LP in problem (6) has a feasible and convergent solution, where the probability of selecting the optimal arm converges to 1. We can easily construct such a feasible solution. Define the conflict clustering , where each is a subset of contexts and each context belongs to exactly one cluster . Within each cluster, every context has a conflict with at least one other context in the same cluster and has no conflicts with contexts in any other clusters. Let be a mapping from any context to its respective cluster, such that . Then, we can construct a feasible solution for (6) as follows:

| (7) |

However, a better solution for can be obtained by solving (6), under the condition in Lemma 4.

Lemma \thetheorem

Sketch of proof.

It is straightforward to observe that setting as the weighted average of within each subset of conflicting contexts, with weights proportional to , yields a feasible solution. To prove the second part of the lemma, we start by noting that the feasible solution of (6) must take the form , where . By substituting into (6) and redefining the variables in terms of for all , we then reformulate problem (6) into an equivalent form as follows:

| s.t. | ||||

| (9) |

We can reformulate the first three constraints of (9) as a convex cone given by

where represents the first rows and first columns of matrix , and is a constant matrix constructed for each . We show that this convex cone has a non-zero measure when all vectors for are linearly independent, based on the properties of the constructed matrix . Furthermore, since the distribution for any lies within the interior of the simplex , representing all probability distributions over arms, we can construct a feasible solution space with a non-zero measure. For the complete proof of this lemma, please refer to Appendix B. ∎

When Eq. (8) is satisfied, we can modify the first constraint of problem (6) to , where is a sufficiently small positive value to ensure that truthful reporting becomes a strictly dominant strategy for agents. Furthermore, when the feasible space has a non-zero measure, it can yield an improved optimal value for problem (6) compared to in (7).

However, solving the linear program in (6) incurs a complexity higher than Cohen et al. (2021), whereas identifying (7) has a lower complexity of , which arises from the process of identifying conflict clusters. For larger and , we can improve efficiency of Mechanism 1 by using from (7) as a substitute for solving (6).

5. Regret Analysis Under the Same Optimal Arm for two contexts

In this section, we analyze the regret performance of our truthful mechanism in the simple but fundamental case of two contexts. The two-context scenario is common in real-world settings. For example, online platforms often categorize users as either Mac or Windows users to tailor sales strategies Adekotujo et al. (2020). Similarly, in clinical trials, hospitals categorize patients as either treatment-naive or treatment-experienced when conducting studies Neale et al. (2007). For agents with two possible contexts, the scenarios are limited to either having the same or different optimal arms to misreport the other context. As increases, the misreporting patterns become exponentially more intricate among agents, significantly complicating the regret analysis. In Section 7, we still run simulations for multiple contexts to show similar results as presented in this section.

We focus on problem-dependent frequentist regret because misreporting behavior is influenced by the specific realization of the prior, requiring separate analysis for different cases. Specifically, we divide the realizations into two cases: (1) when the two contexts share the same optimal arm, and (2) when the two contexts have different optimal arms. The differing misreporting incentives for each case lead to major differences in regret analysis. Still, Bayesian regret can be obtained by taking the expectation over our frequentist regret, yielding the same order. We begin by analyzing the regret in the scenario where the two contexts, and , share the same optimal arm in this section. Addressing the other scenario requires new extra techniques (see Section 6).

When two contexts share the same optimal arm, the probability of selecting the optimal arm will eventually converge to 1 for both contexts. However, one context must converge faster than the other. Consequently, the context with a slower convergence rate may have an incentive to misreport for most of the time steps during the process. Inspired by this, we consider the two contexts collectively and derive an upper bound on the total number of suboptimal pulls for both contexts. {theorem} For the realization of prior, , such that the two contexts and share the same optimal arm , the frequentist regret of our truthful-TS mechanism in Mechanism 1 is to be upper bounded by

where is the reward gap between the optimal arm and arm for context . is a constant for and .

Proof.

Let denote the optimal arm for both contexts. Recall that represents the arm chosen under our truthful-TS mechanism in Mechanism 1, and represents the arm chosen under the standard TS algorithm. Since the two contexts share the same optimal arm, we can decompose the regret in equation (4) as follows:

| (10) |

The expectation in the first equality is taken over the arrivals of contexts, the arm selections, and the observed rewards. Then, using the second constraint of our LP in (6), the last expression of (10) equals the following:

In this way, we convert the regret of our truthful-TS mechanism into the regret under the Thompson sampling algorithm. We then rewrite each term involving arm in the last expression as follows:

| (11) |

which is obtained by moving inside the inner expectation and applying the tower rule. Then (11) is upper bounded by

| (12) |

where represent the number of agent arrivals with context before time . From the derivation above, we upper bound the in (10) by the expected number of pulls of suboptimal arm in Thompson sampling, conditioned on the history where consistently arrives.

Define as the value sampled from the posterior distribution for arm by context at time in the Thompson sampling algorithm. Inspired by the method from Agrawal and Goyal (2017), which bounds the number of suboptimal arm pulls in Thompson sampling, we decompose Eq. (12) by considering the following two events: one event where the posterior mean estimate does not deviate significantly from the true value , and the other event where remains close to the posterior mean at time . These events are formally defined as follows:

Considering the realization of these events above, we decompose (12) as follows:

| (13) |

Inspired by the method in Agrawal and Goyal (2017), we upper bound the three terms using the following Lemmas 5, 5, and 5, respectively. The complete proofs of these lemmas can be found in Appendix C, D and E. The upper bound of the first term directly follows from Lemma 5. The upper bounds of the second and third terms are obtained from Lemma 5 and Lemma 5 by setting . Let summarize all the constant parts in (12), then we obtain and complete the proof of Theorem 5.

Lemma \thetheorem

In Thompson sampling with arm action at time , the expected total number of pulls of a suboptimal arm by context , together with the occurrence of events and , can be upper bounded by a constant for and :

Lemma \thetheorem

In Thompson sampling with arm action at time , the expected total number of pulls of a suboptimal arm by context , together with the occurrence of event for , can be upper bounded as follows:

Lemma \thetheorem

In Thompson sampling with arm action at time , the expected total number of pulls of suboptimal arm under any context , together with the occurrence of event for , can be upper bounded as follows:

∎

Theorem 5 and our proof demonstrate that our truthful-TS mechanism shares the same regret order as the Thompson sampling algorithm, indicating that our mechanism can achieve an optimal regret order while ensuring truthfulness.

6. Regret Analysis Under Different Optimal Arms for two contexts

When two contexts have different optimal arms, define the true optimal arms for and as and , respectively, with . The regret-bounding method used in the previous section, where contexts share the same optimal arm, cannot be applied here. This is because arm is suboptimal for context but optimal for context , which prevents us from jointly bounding the total number of pulls of arm across both contexts. As a result, we must also consider the number of pulls of the optimal arm for context , which is not considered when bounding the regret in Thompson sampling.

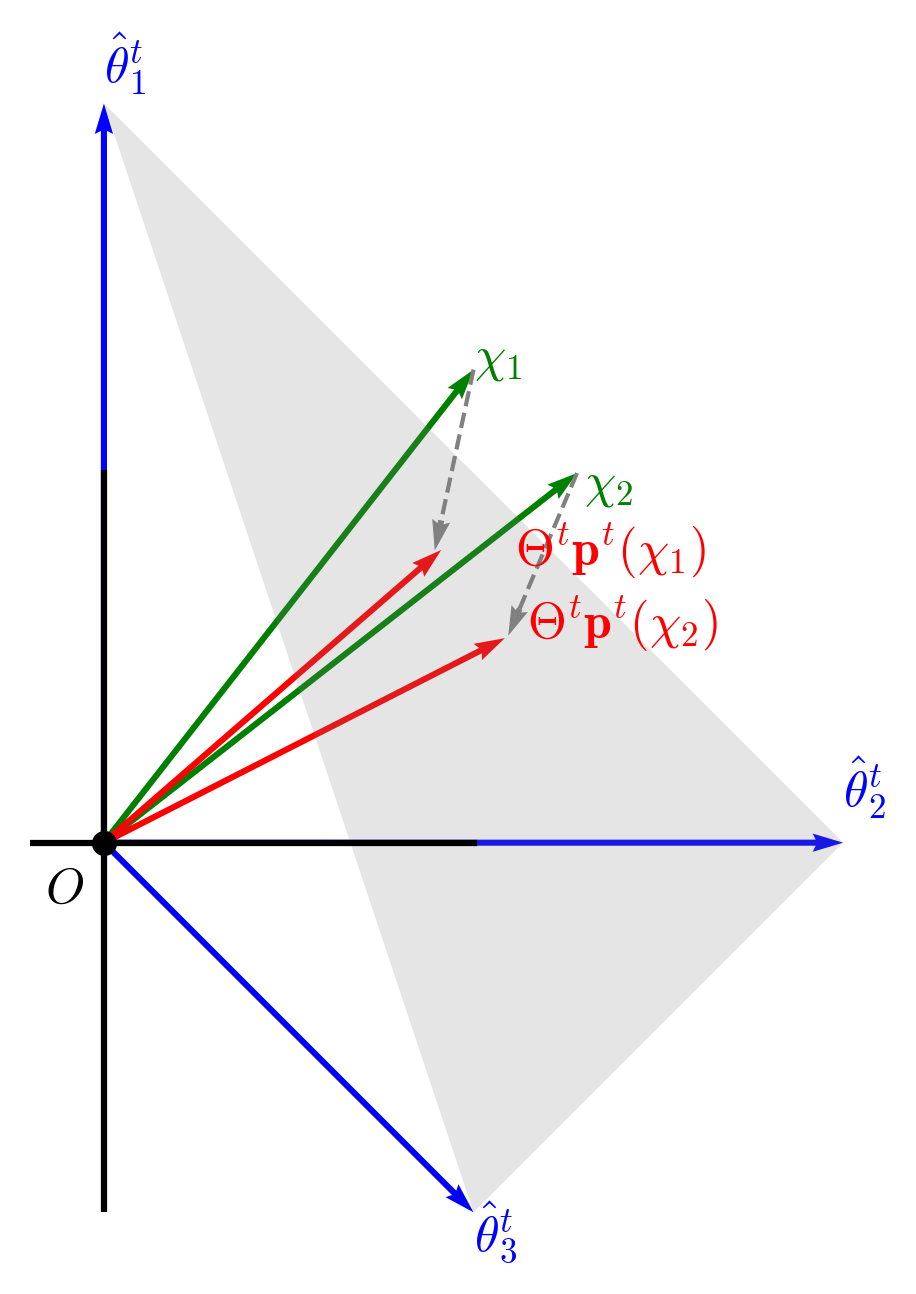

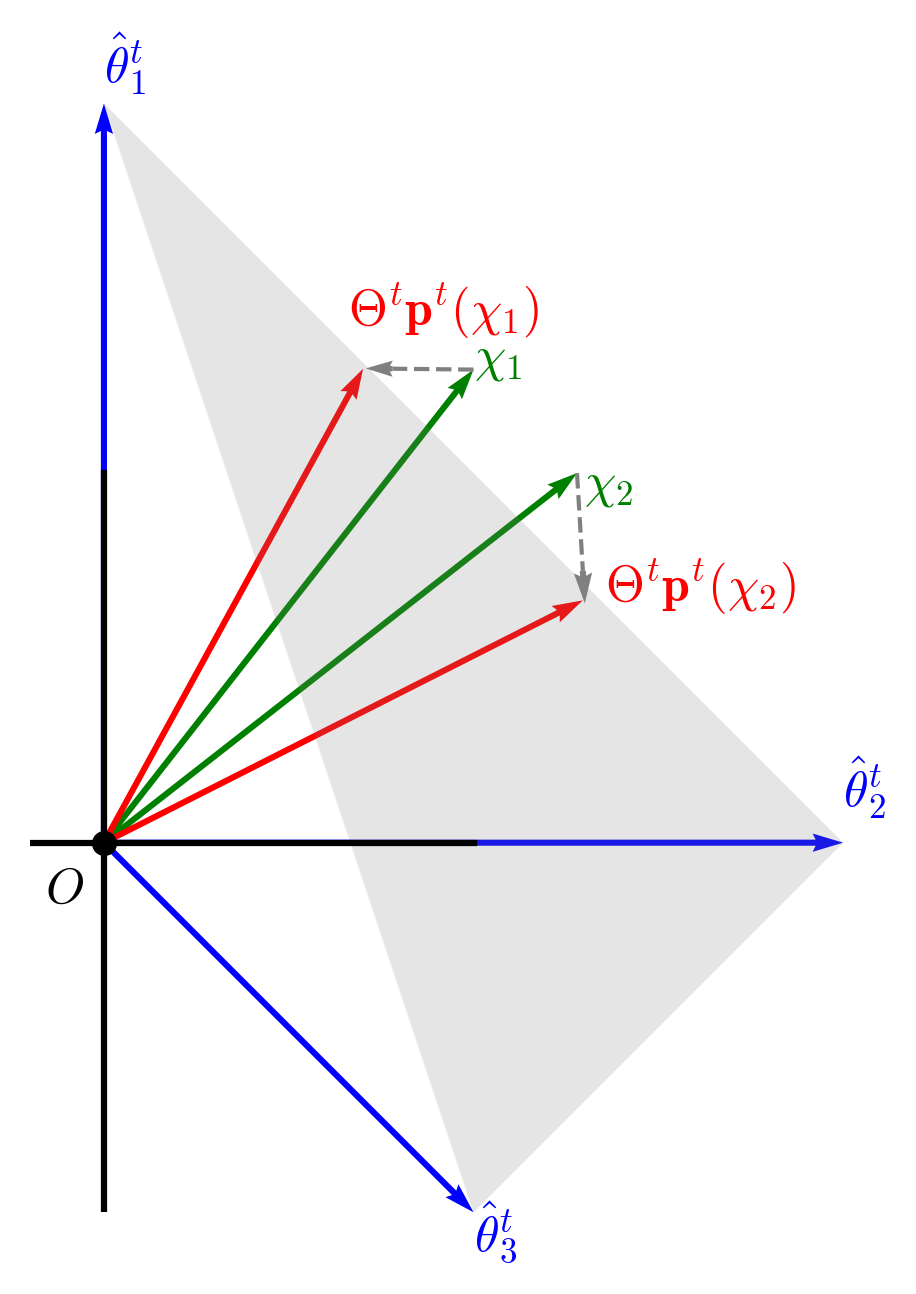

First, we illustrate the misreporting incentives over time in Thompson sampling when agents have different optimal arms based on their beliefs, which provides insight into our proof approach. For illustration, we assume an ideal Thompson sampling scenario in which agents report truthfully in Fig. 3 and 3. Initially, agents may have an incentive to misreport even if they have different prior optimal arms, as illustrated in Fig. 3. This is because, at first, the variance of the prior distribution is relatively large to encourage exploration, causing the range under the Thompson sampling mapping from to to be concentrated near the center of . As a result, even though the probability of selecting ’s prior optimal arm 2 is higher than that of (), can still obtain a higher expected reward by misreporting as . As the algorithm progresses and posterior variance decreases, the range of the Thompson sampling mapping shifts towards the extreme points of the simplex , as shown in Fig. 3, where each context ultimately achieves a higher expected reward under its own Thompson sampling distribution. Thus, when contexts have different optimal arms, the number of pulls of arm by can be analyzed by separately considering the time steps when the contexts are in conflict and when they are not.

For the realization of prior, such that the two contexts and have the different optimal arms and , the frequentist regret of our truthful-TS mechanism in Mechanism 1 is to be upper bounded by

where is the reward gap between the optimal arm and arm for context . is the minimum reward gap for context . is a constant for and , and is the constant part for .

Proof.

To upper bound the regret when the contexts have different optimal arms, we need to consider the expected number of times that either context has an incentive to misreport, which introduces an additional part on regret analysis compared to Theorem 5. Define as the event that the two contexts have conflict at time , meaning:

Similar to the proof of Theorem 5, we first decompose the regret in (4) as follows:

| (14) |

where the last inequality is because when happens, the mechanism will operate the same as Thompson sampling. We further derive an upper bound for the last term in the last expression of (14) as follows:

where the equality holds because is chosen according to from (6), whose second constraint enables us to convert it to for Thompson sampling. Substituting the last expression into the last expression of (14), we obtain an upper bound for (14) given by

| (15) |

The first two lines of Eq. (15) can be upper bounded using the procedure for bounding the number of suboptimal pulls described in (11) to (13) from the last section. For the last term, since it only relates to actions under Thompson sampling, we proceed to upper bound it by analyzing a virtual process with an ideal Thompson sampling algorithm that does not involve misreporting. We first present Lemma 6 that transforms the event including to an other event involving .

Lemma \thetheorem

Let denote the empirically worst arm for context in any bandit process at any given time. Let denote

| (16) |

The probability of event , where either or has an incentive to misreport at time , can be upper bounded by the probability of the following event:

The complete proof of this lemma can be found in Appendix F. Using Lemma 6, we then decompose the last term in (15) below:

The equations above hold because, given the history , the context arrival is independent of . The final expression can be further decomposed and upper bounded as follows:

| (17) |

When summing from to , the term in the last line above can be upper bounded using the same method as in (11) through (13) from the last section, then applying Lemmas 5, 5, and 5. The upper bound for the summation from to of the first two terms in (17) is provided in Lemma 6 below.

Lemma \thetheorem

Let denote the expression in (16). Then the expected number of pulls of by together with the occurrence of event is upper bounded by:

where is a constant for .

7. Simulation Experiments

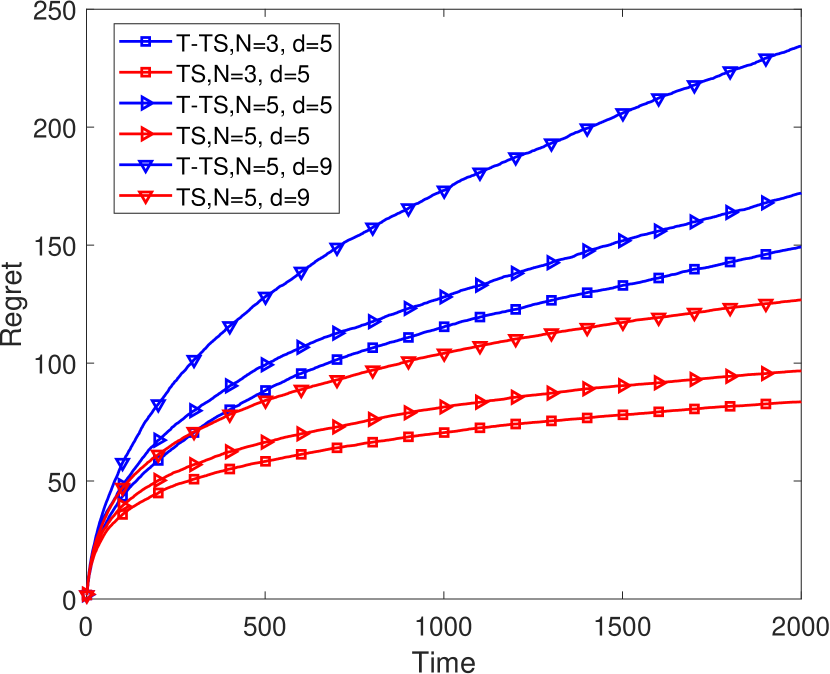

In this section, we use simulation experiments to evaluate the performance of our truthful-TS mechanism for more than two contexts and non-Gaussian noise distribution.

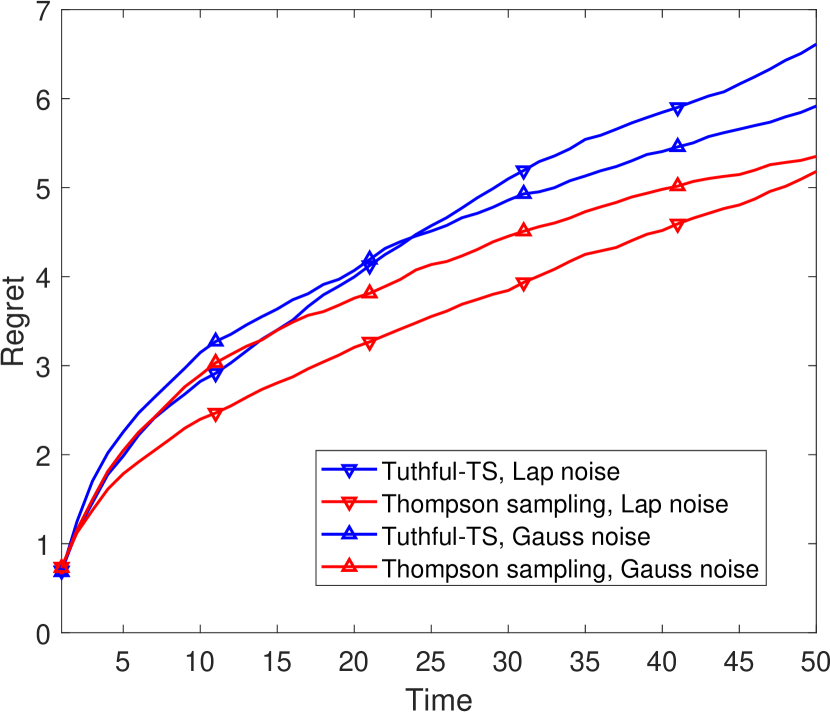

We first extend Gaussian noise to Laplace noise as a typical sub-Gaussian distribution in Fig. 5. Since the Laplace noise yields a non-closed form and non-standard posterior distribution, we turn to numerical methods to update the posterior and compute the probabilities in (5). To ensure a small error of inherent approximation in numerical methods, we conduct this experiment for the small scale case with and time steps. For a fair regret comparison, we set the same Gaussian prior for both noises where prior mean and and prior covariance matrix . The variances of both Laplace and Gaussian noises are set to 1 in Fig. 5. To compare with our mechanism in Mechanism 1, we use the ideal Thompson sampling (always assuming agents’ truthful reporting) as the performance upper bound. Fig. 5 implies that our truthful-TS mechanism yields a similar regret order to Thompson sampling. Since Laplace noise has a heavier tail than Gaussian noise, the regret order under Laplace noise remains sublinear but is slightly higher than that under Gaussian noise. As observed, the regrets for both the truthful-TS mechanism and the Thompson sampling algorithm under Laplace noise will exceed those under Gaussian noise after . We can have the same conclusion when extending to other sub-Gaussian noises such as uniform and Cauchy distributions.

Similar to the experiment setting in Bastani et al. (2021), we then extend the setting to contexts and dimensions under Gaussian prior and noise. We consider arms for recommendations among these contexts. For each arm , we set its prior distribution such that is a vector with a single 1 in the -th entry and is the identity matrix. Different contexts are sampled from a multivariate uniform distribution over . For each parameter setting, we run 100 simulations, generating new realizations of from the prior distribution of each time, and calculate the average regret. The results are displayed in Fig. 5. According to Fig. 5, like the ideal Thompson sampling, our truthful-TS mechanism still exhibits sublinear order for different and , which is consistent with our Theorems 5 and 6. Though ideal Thompson sampling algorithm’s regret grows with and , our mechanism grows faster. The reason is that as there are more contexts, a context may envy more other contexts with higher convergence rates and our Mechanism 1 will reduce the exploitation of those contexts, thereby slowing down the overall convergence.

8. Conclusion

In this paper, we investigate the problem of strategic misreporting of private contexts by agents within the Bayesian contextual linear bandit framework. We are the first to analyze this issue and demonstrate that existing algorithms fail to perform effectively under such misreporting behavior. To address this, we propose a novel truthful mechanism based on the Thompson sampling algorithm, which solves a LP at each time step to ensure incentive compatibility. We prove that our mechanism achieves a problem-dependent regret bound of in the two-context case with Gaussian priors and noise. Furthermore, our numerical results suggest that the proposed mechanism retains a comparable regret order across multiple contexts and under heavier tails of noise.

References

- (1)

- Abbasi-yadkori et al. (2011) Yasin Abbasi-yadkori, Dávid Pál, and Csaba Szepesvári. 2011. Improved Algorithms for Linear Stochastic Bandits. In Advances in Neural Information Processing Systems, Vol. 24.

- Abeille and Lazaric (2017) Marc Abeille and Alessandro Lazaric. 2017. Linear thompson sampling revisited. In Artificial Intelligence and Statistics. PMLR, 176–184.

- Abramowitz and Stegun (1948) Milton Abramowitz and Irene A Stegun. 1948. Handbook of mathematical functions with formulas, graphs, and mathematical tables. Vol. 55. US Government printing office.

- Adekotujo et al. (2020) Akinlolu Adekotujo, Adedoyin Odumabo, Ademola Adedokun, and Olukayode Aiyeniko. 2020. A comparative study of operating systems: Case of windows, unix, linux, mac, android and ios. International Journal of Computer Applications 176, 39 (2020), 16–23.

- Agrawal and Goyal (2013) Shipra Agrawal and Navin Goyal. 2013. Thompson sampling for contextual bandits with linear payoffs. In International conference on machine learning. PMLR, 127–135.

- Agrawal and Goyal (2017) Shipra Agrawal and Navin Goyal. 2017. Near-optimal regret bounds for thompson sampling. Journal of the ACM (JACM) 64, 5 (2017), 1–24.

- Auer (2002) Peter Auer. 2002. Using confidence bounds for exploitation-exploration trade-offs. Journal of Machine Learning Research 3, Nov (2002), 397–422.

- Bastani et al. (2021) Hamsa Bastani, Mohsen Bayati, and Khashayar Khosravi. 2021. Mostly exploration-free algorithms for contextual bandits. Management Science 67, 3 (2021), 1329–1349.

- Buening et al. (2024) Thomas Kleine Buening, Aadirupa Saha, Christos Dimitrakakis, and Haifeng Xu. 2024. Strategic Linear Contextual Bandits. arXiv preprint arXiv:2406.00551 (2024).

- Chu et al. (2011) Wei Chu, Lihong Li, Lev Reyzin, and Robert Schapire. 2011. Contextual bandits with linear payoff functions. In Proceedings of the Fourteenth International Conference on Artificial Intelligence and Statistics. JMLR Workshop and Conference Proceedings, 208–214.

- Cohen et al. (2021) Michael B Cohen, Yin Tat Lee, and Zhao Song. 2021. Solving linear programs in the current matrix multiplication time. Journal of the ACM (JACM) 68, 1 (2021), 1–39.

- Food and Administration (2017) U.S. Food and Drug Administration. 2017. Drug Approval Package: Verzenio (abemaciclib). Technical Report. U.S. Food and Drug Administration. https://www.accessdata.fda.gov/drugsatfda_docs/nda/2017/208716Orig1s000TOC.cfm Accessed: 2024-09-04.

- Goldenshluger and Zeevi (2013) Alexander Goldenshluger and Assaf Zeevi. 2013. A linear response bandit problem. Stochastic Systems 3, 1 (2013), 230–261.

- GrowthSetting (nd) GrowthSetting. n.d.. How Netflix Enhances User Experience with AI Recommendations. https://growthsetting.com Accessed: 2024-10-11.

- Hu et al. (2022) Xinyan Hu, Dung Ngo, Aleksandrs Slivkins, and Steven Z Wu. 2022. Incentivizing combinatorial bandit exploration. Advances in Neural Information Processing Systems 35 (2022), 37173–37183.

- Immorlica et al. (2020) Nicole Immorlica, Jieming Mao, Aleksandrs Slivkins, and Zhiwei Steven Wu. 2020. Incentivizing Exploration with Selective Data Disclosure. In Proceedings of the 21st ACM Conference on Economics and Computation. 647–648.

- Kremer et al. (2014) Ilan Kremer, Yishay Mansour, and Motty Perry. 2014. Implementing the “wisdom of the crowd”. Journal of Political Economy 122, 5 (2014), 988–1012.

- Lattimore and Szepesvári (2020) Tor Lattimore and Csaba Szepesvári. 2020. Bandit algorithms. Cambridge University Press.

- Lazaric and Munos (2009) Alessandro Lazaric and Rémi Munos. 2009. Hybrid Stochastic-Adversarial On-line Learning.. In COLT. Citeseer.

- Mansour et al. (2020) Yishay Mansour, Aleksandrs Slivkins, and Vasilis Syrgkanis. 2020. Bayesian incentive-compatible bandit exploration. Operations Research 68, 4 (2020), 1132–1161.

- Mansour et al. (2022) Yishay Mansour, Aleksandrs Slivkins, Vasilis Syrgkanis, and Zhiwei Steven Wu. 2022. Bayesian exploration: Incentivizing exploration in Bayesian games. Operations Research 70, 2 (2022), 1105–1127.

- Neale et al. (2007) Joanne Neale, Michele Robertson, and Michael Bloor. 2007. ‘Treatment experienced’and ‘treatment naïve’drug agency clients compared. International Journal of Drug Policy 18, 6 (2007), 486–493.

- Rahman et al. (2023) Rifaquat Rahman, Lorenzo Trippa, Eudocia Q Lee, Isabel Arrillaga-Romany, Geoffrey Fell, Mehdi Touat, Christine McCluskey, Jennifer Wiley, Sarah Gaffey, Jan Drappatz, et al. 2023. Inaugural results of the individualized screening trial of innovative glioblastoma therapy: a phase II platform trial for newly diagnosed glioblastoma using Bayesian adaptive randomization. Journal of Clinical Oncology 41, 36 (2023), 5524–5535.

- Rakhlin and Sridharan (2016) Alexander Rakhlin and Karthik Sridharan. 2016. Bistro: An efficient relaxation-based method for contextual bandits. In International Conference on Machine Learning. PMLR, 1977–1985.

- Russo and Van Roy (2014) Daniel Russo and Benjamin Van Roy. 2014. Learning to optimize via posterior sampling. Mathematics of Operations Research 39, 4 (2014), 1221–1243.

- Russo and Van Roy (2016) Daniel Russo and Benjamin Van Roy. 2016. An information-theoretic analysis of thompson sampling. Journal of Machine Learning Research 17, 68 (2016), 1–30.

- Sellke (2023) Mark Sellke. 2023. Incentivizing exploration with linear contexts and combinatorial actions. In International Conference on Machine Learning. PMLR, 30570–30583.

- Sellke and Slivkins (2021) Mark Sellke and Aleksandrs Slivkins. 2021. The price of incentivizing exploration: A characterization via thompson sampling and sample complexity. In Proceedings of the 22nd ACM Conference on Economics and Computation. 795–796.

- Simchowitz and Slivkins (2024) Max Simchowitz and Aleksandrs Slivkins. 2024. Exploration and incentives in reinforcement learning. Operations Research 72, 3 (2024), 983–998.

- Slivkins et al. (2019) Aleksandrs Slivkins et al. 2019. Introduction to multi-armed bandits. Foundations and Trends® in Machine Learning 12, 1-2 (2019), 1–286.

Appendix A Proof of Lemma 3.2

Consider a Bayesian contextual linear bandit problem with two contexts: and , arriving with probabilities and , respectively. There are two arms drawn from and with prior means and and prior covariances . By prior belief, according to the Thompson sampling probabilities in (5), we have and , which means that agent with context will have the incentive to misreport as to obtain a higher expected reward . Therefore, if the first context is , this first agent will misreport her context as .

We will demonstrate that, under a specific realization of and from the instance above, which satisfy the following conditions:

| (18) |

where , the Thompson sampling algorithm has a positive probability of failing to correctly identify arm as superior to arm for context . Consequently, context will continue misreporting as throughout the learning process, causing the algorithm to converge on selecting arm with probability 1 for both contexts. This outcome will result in linear regret over time. The following proof shows this result by using condition in (18).

To establish this, we first introduce two stochastic processes. Let denote the total number of times arm is pulled over the entire time horizon. Reorder the subset of time steps within during which the Thompson sampling algorithm selects arm into a new sequence . For each , define a stochastic process as follows:

| (19) |

In the following lemma, we prove that for is a martingale under context ’s misreporting.

Lemma \thetheorem

If context always misreports as , the stochastic process in (19) forms a martingale. Moreover, .

Proof.

Assume that at each time step, the misreporting condition: holds. Under a Gaussian prior and noise, according to lemma C, the posterior mean for under misreporting is given by:

| (20) |

where . Then the expectation of is calculated as

Then the following equalities further show that is a martingale:

where the last equality follows from . Then we obtain Lemma A and complete the proof. ∎

Under (18), we have and . Then, by Doob’s inequality for martingales, we have:

Substituting (19) for into the inequalities above, we obtain:

and

Recall that under the realization of and in (18), we have . By combining this with the two inequalities above, we have:

This result implies that, starting from time , where context begins to misreport, there is a probability at least that the Thompson sampling algorithm will misidentify arm as the optimal arm for context . Simultaneously, will persist in misreporting at each subsequent time , upon observing for . As a result, its posterior estimate will follow the martingale , forming a logical loop with the event to happen. Additionally, when misidentifies arm 1 as the optimal arm, context must correctly identify arm 1 as the optimal arm by calculating similarly to Eq. (20), because:

where the two sides in the last line are and , respectively. Since arm 1 is always the posterior optimal for both contexts, the probability of choosing arm 1 will always be higher than . The regret, therefore, is at least

under the condition in Eq. (18). Furthermore, the region of and in Eq. (18) has a non-zero measure, implying that this realization has a positive probability of occurring. This completes the proof.

Appendix B Proof of Lemma 4

Based on the second constraint of LP (6), any feasible solution must take the form , where may be positive or negative, and . We can thus rewrite problem (6) as follows:

| s.t. | ||||

| (21) |

Using the second and third equality constraints, we can set and . We will then use this to reformulate the first three constraints in (21) using only variables of for . Define as , which is the submatrix of the first columns in . Substituting this and into the first constraint, we get:

| (22) |

The above equation holds for and . When and , the constraint should be expressed as:

| (23) |

When and , the constraint should be expressed as:

Let denote the matrix formed by the first rows and columns of matrix . Combining Eqs. (22) and (23), the constraint for truthful reporting of with , for any , can be rewritten as:

| (24) | |||

and the row appears in the -th row of the matrix on the left-hand side.

Similarly, the constraint for truthful reporting with can be expressed as:

| (25) | |||

Stacking the inequalities in Eqs. (24) and (25) for all forms the following convex cone:

| (26) |

where the convex cone has a non-zero measure when there is no group of rows in the matrix of the left-hand side pointing in the opposite direction. Formally, let the rows of this matrix be denoted as , and define . If the following condition holds for all nonnegative (not all zero):

then the set of inequalities in (26) will have a non-zero measure. This condition is equivalent to stating that the origin 0 does not lie within the convex hull of . A sufficient condition for the origin not to lie within the convex hull of is that the vectors are linearly independent. When the vectors are linearly independent, the origin cannot be expressed as a convex combination of them, thereby ensuring that the condition is satisfied. Then we further give a sufficient condition for being linearly independent in the following lemma.

Lemma \thetheorem

If are linearly independent, all the rows in (26) must also be linearly independent.

Proof.

We prove the lemma by contradiction. For simplification, let . Define , where represents the -th column of . It follows directly from (24) and (25) that must be linearly independent.

Assume that the vectors for all are linearly independent. Suppose there exists a set of scalars for , not all zero, such that:

We can rewrite this expression as:

Since are linearly independent, the only way for this equation to hold is:

However, because are linearly independent, it follows that all . This contradicts our initial assumption that not all are zero. Therefore, we reach a contradiction, completing the proof.

∎

Given the conclusion that the first three constraints of (21) define a non-zero measure space under the condition in Lemma B, we now turn our attention to the fourth constraint in problem (21). In the Thompson sampling algorithm, the probability of arm choice, , ensures that each arm has a strictly positive probability of being selected at every time step. This condition guarantees that the point lies within the interior of the simplex , formed by all possible distributions over arms.

As a result, there exists a positive such that a -ball centered at is entirely contained within the simplex. This implies when the condition in Lemma 4.1 holds, the intersection between a -ball around the origin and the convex cone defined by (26) constitutes a feasible space for problem (21) with non-zero measure. Then we complete the proof.

Appendix C Proof of Lemma 5

We first present the concentration and anti-concentration inequalities for posterior estimate and Thompson sampling value by context for all in Lemmas C and C used throughout the remaining proofs.

Lemma \thetheorem

The following concentration and anti-concentration inequalities are from [3]. If and ,

Lemma \thetheorem

For any arm , when an algorithm collects samples which are all from context at time , the posterior estimate follows a Gaussian distribution:

| (27) |

where , and . The matrix has the closed-form expression:

| (28) |

Furthermore, for any , the posterior estimate satisfies the following concentration inequality:

| (29) |

Proof.

We begin by writing the difference between the posterior estimate and the true parameter as follows:

where represents the set of time steps when the algorithm chose arm before time . Therefore, the posterior mean of follows a Gaussian distribution with mean and variance .

When all the collected samples are from the context , we apply the Sherman–Morrison–Woodbury formula to obtain:

Also by Sherman–Morrison–Woodbury formula, we further expand the term :

Finally, applying the concentration inequality for the Normal distribution (Lemma C), we get:

∎

Lemma \thetheorem

In Thompson sampling, for any suboptimal arm and any history , the probability of selecting arm at time , together with the occurrence of events and , can be upper-bounded as follows:

| (30) |

Proof.

When the Thompson sampling algorithm chooses arm conditioned on events and , since the algorithm bases this choice on the sampled value , it must follow that the sampled values for all other arms are less than or equal to . Therefore, we have:

On the other hand, if the sampling value for the optimal arm is higher than , the algorithm must select arm . Therefore, we have:

Finally, combining these two bounds, we arrive at:

This completes the proof. ∎

By Lemma C, our objective of can be upper bounded by:

The last expression can then be rewritten as

| (31) |

where is the number of pulls of any arm by context before time . Recall that is a sample from porsteior distribution . Then can be rewritten as

where the represents the cumulative density function of standard normal distribution and when by Lemma C. Substituting the final expression and the probability density function of from Lemma C into Eq. (31), we obtain:

| (32) |

where we denote . Next, we first examine the first term in the final expression of (32):

where the second inequality follows from Lemma C. With some algebraic manipulation, the final integral can be derived as:

Substituting and into this expression, we obtain

| (33) |

First, the expression above must be finite. Then, as increases, the first term in the expression (33) converges exponentially. For the second term, we can show that there exists such that when , it will become negative. This implies that summing the expression above from to yields a constant value, summarized as .

Next we further derive the second term in the last line of Eq. (32). For the term where , can be either positive or negative depending on the realization of the prior. However, there must exist a time such that for all . When , the second term simplifies to:

| (34) |

Therefore, summing the second term in Eq. (32) from to also yields a constant value, summarized as . Further denote for the summation from to of the upper bounds in (33) and (34), we obtain the result in Lemma 5.2 and complete the proof.

Appendix D Proof of Lemma 5

To prove Lemma 5, decompose the left-hand side of the inequality in Lemma 5 into two parts with and as follows:

where the third inequality follows from the concentration inequality in Lemma C, and the last inequality is obtained by using from Lemma C. Choosing above, we obtain:

This completes the proof.

Corollary \thetheorem

In Thompson sampling, the expected number of pulls of suboptimal arm under any context , together with the occurrence of event , can be upper bounded as follows:

Appendix E Proof of Lemma 5

To prove Lemma 5, choose such that for , we can use (29) in Lemma C to upper bound the probability of . We then divide the process into two parts with and , and apply Lemma C in the fourth inequality below :

where the last equality follows from . The following corollary of Lemma 5 will be used for the proof of Lemma 6:

Corollary \thetheorem

In Thompson sampling, the expected number of pulls of suboptimal arm under any context , together with the occurrence of event , can be upper bounded as follows:

Appendix F Proof of Lemma 6

Recall the definition of :

We decompose as follows:

In the last line, applying and to the first two terms, we obtain the following lower bound for the last line:

Therefore, implies that the above expression must also be less than 0, which is:

Combining this condition for both and yields the result.

Appendix G Proof of Lemma 6

We first rewrite the complete version of Lemma 6 as follows:

Lemma \thetheorem

Let denote the following expression:

Then the expected number of pulls together with the occurrence of event is upper bounded by:

where is a constant given in Eq. (40).

To start the proof of Lemma G, we define the following four events:

| (35) |

where . Denote the event of as . We then decompose as follows:

| (36) |

The second equality holds because, when occurs at time , is strictly positive. Furthermore, since the Thompson sampling algorithm will select arm with probability 1 when occurs, this contradicts the event .

Using in Corollaries D and E, the summation from to of the first two terms in the last expression in (36) is upper bounded by:

| (37) |

Then we upper bound the remaining terms in Eq. (36). We next introduce a key lemma to aid in proving the remaining part, which converts the terms with to terms with .

Lemma \thetheorem

When the events and happen, the probabilies of selecting the optimal arm and the suboptimal arm for context in Thompson sampling satisfy the following inequality:

Proof.

When events and happen, the Thompson sampling value of arm falls within the interval . Therefore, selecting arm through Thompson sampling together with events and implies that no other arm has a Thompson sampling value exceeding at time , which leads to the following:

where the last equality holds because the Thompson sampling values for any arms are mutually independent, conditional on the history . Conversely, if the Thompson sampling value of a suboptimal arm exceeds , while the values for all other arms remain below , the Thompson sampling algorithm will select arm . Therefore, we have:

Combining these two inequalities then we complete the proof of Lemma G.

∎

For the third and fourth terms in (36), although they include additional parts and compared to Lemma G, following the same procedure as in the proof of Lemma G still yields similar upper bounds. We first proceed with the third term in (36). The upper bound of the third term in (36) are upper bounded by (38) as follows:

| (38) |

Summing up from to , we continue to proceed with Eq. (38) as follows:

| (39) |

The second last inequality holds because, conditioned on event , there is a probability of that occurs with . Thus, when , we have:

which implies that

To preceed with (39), we choose such that for , we can use Eq. (29) to upper bound the probability of where . We then divide the process into two parts with and , and apply the concentration inequality (29) in Lemma C to the denominator of (39) and the anti-concentration inequality in Lemma C to the numerator of (39) to upper bound (39) as follows:

| (40) |

Since by Lemma C, the first term in the first line of (40) decays exponentially with , while the first term in the second line converges to a constant, and the last term is a constant. Thus, the entire equation in (40) last a constant, summarized by .

After completing the upper bound for the third term in (36), we proceed with the fourth term. By Lemma G, the fourth term in (36) satisfies the following inequality:

| (41) |

where the first equality holds because the joint event and is equivalent to the event itself. Applying the anti-concentration and concentration inequalities from Lemma C to the numerator and denominator of (41), respectively, (41) is upper bounded by:

| (42) |

Since this expression is conditioned on event follows from (41), is in the range of . Then (42) is upper bounded by the following:

| (43) |

Summing it up from to for the total process, we separate the last expression to and :

Choose , we obtain the upper bound of the fourth term in Eq. (36):

| (44) |

By upper bounding the summation from to for each term in by (37), (40), and (44), we derive the results presented in Lemma G. Furthermore, by denoting all constant components in Lemma G as , we arrive at Lemma 6, thus completing the proof.