[1]\fnmAndrius \surGrigutis

[1]\orgdivInstitute of Mathematics, \orgnameVilnius university, \orgaddress\streetNaugarduko 24, \cityVilnius, \postcodeLT-03225, \countryLithuania

Several facts about Theodor Wittstein, Gaetano Balducci, and some expressions of the net single premiums under their mortality assumption

Abstract

The mathematical essence in life insurance spins around the search of the numerical characteristics of the random variables , , , etc., where (deterministic) denotes the discount multiplier and (random) is the future lifetime of an individual being of years old. This work provides some historical facts about T. Wittstein and G. Balducci and their mortality assumption. We also develop some formulas that make it easier to compute the moments of the mentioned random variables assuming that the survival function is interpolated according to Balducci’s assumption. Derived formulas are verified using some hypothetical mortality data.

keywords:

survival function, future lifetime, Balducci’s assumption, net single premium, exponential integralpacs:

[MSC Classification]91G05, 62P05, 62N99

1 Introduction

Let be the absolutely continuous random variable determining a person’s lifetime. By we denote the integer age of a certain person. Let denote the survival function. In life insurance, based on some mortality table, the exact values of the survival function in many instances are given over the integers only, i.e. , and the problems that life insurance deals with, ask to compute certain numerical characteristics of under the certain interpolation of . More precisely, given the fixed age , we shall connect the value with when varies over , and characterize some random function of . Perhaps, the most common and simple interpolation of is the assumption of uniform distribution of deads (UDD):

| (1) |

In other words, the UDD assumption (1) states that the survival function is linear over the intervals , , Notice that when and defines the fractional age of a person.

Another widely known assumption on interpolation is the so called Balducci’s assumption:

| (2) |

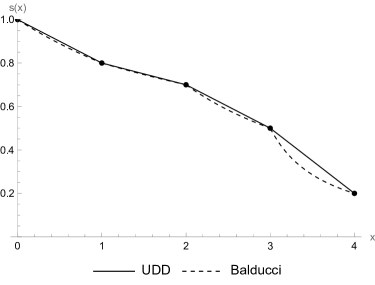

In comparison to the UDD assumption (1), Balducci’s assumption (2) states that the function (as long as ) is linear over the intervals , , , see Figure 1.

For , we denote the future lifetime by of a person who is years old, i.e. given that , where is the absolutely continuous random variable that determines a person’s lifetime. Let denote the conditional survival function, i.e., given that ,

Then, by we denote the conditional density, under condition , of the random variable (person’s lifetime) and define it as derivative

| (3) |

Let us also denote , , and . Under Balducci’s assumption (2), the conditional density (3) is

| (4) |

where , and . In comparison, under UDD assumption (1), the conditional density (3) is

| (5) |

where represents the expected number of survivors to age from the newborns, i.e. , and denote the number of deaths between ages and . Let be some real-valued function. In life insurance, to characterize the random variable essentially means to compute the expectation

| (6) |

The computation of in (6) is much easier using the density of UDD as the left-hand-side of (5) does not depend on , and the same job becomes more complicated using the density (4).

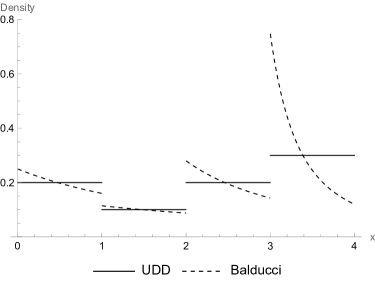

If the function in (6) represents the random discount multiplier according to the future lifetime, i.e. , where denotes the fixed annual interest rate, then the expectations of type (6) are called the net actuarial values. As mentioned, the computation of the net actuarial values under the UDD assumption is more simplistic than the same under Balducci’s assumption: under UDD we integrate over the ”steps”, while under Balducci’s assumption, we are tasked to do the same over the ”arcs of hyperbolas”, see Figure 2.

Moreover, if the function in (6) is differentiable and non-increasing (non-decreasing), then the expected value of under Balducci’s mortality assumption (2) is never less (greater) than under the UDD assumption (1), see Lemma 3. So, if then the net single premium under Balducci’s assumption is never less than the net single premium under the UDD assumption. In practice, this leads to the higher expected payoff of the threatened claim and consequently the larger insurance price.

It can be computed, see for instance [1], [2], that under Balducci’s assumption, the force of mortality is

| (7) |

while the same under the UDD assumption is

| (8) |

Since the force of mortality (7) decreases over the year, given that the one in (8) increases, there are many insights and interpretations as to whether Balducci’s mortality assumption is realistic for some human populations, see, for instance, [1, p. 5] cf. [2, p. 105]. The authors believe Balducci’s assumption can be realistic for some human populations. For instance, newborns, teenagers who just reached the legal age to drive, consume alcohol, etc., or those individuals who, let’s say, periodically face something that increases their death probability.

It is curious about the circumstances of how Balducci’s assumption arose. Unfortunately, most publicly available sources, especially the electronic ones in English, lack even the basic facts about the life of Italian actuary Gaetano Balducci (1887 – 1974), see [3, p. 148] where these birth and death years are provided. Balducci did numerous prominent works and officiated in state institutions during his lifetime. For example, it is most famously known that G. Balducci was a State general Accountant for Italy for almost ten years during the middle of the 20th century, see [4, p. 7]. Notably, he was also an active member of the Society of Actuaries (the global professional organization for actuaries), sharing his insights on life insurance theories in several issues of the Journal of Economists and Statistical Review, e.g. [5], [6], [7]. Here we collect and interpret more facts about the assumption (2) named after this Italian actuary.

In fact, the interpolation (2), as well as UDD and constant mortality force, was first introduced by German mathematician Theodor Ludwig Wittstein (1816 – 1894), see [2, p. 68]. In contrast to Balducci, Wittstein’s life appears to be much better documented in easily accessible public sources, see, for example, [8, p. 358]. In short, Wittstein was a high school teacher and textbook author, known for his contributions to the mathematical statistics field. In his work (1862) [9] Wittstein studied population mortality under certain assumptions and concluded that the mortality probability for the fractional ages can be computed as

what is equivalent to (2). In 1917, in work [7] Balducci studied the development of certain populations too and concluded the same as Wittstein earlier. In our opinion, Balducci was unaware of Wittstein’s work due to the different languages and the limited spread of information at the time. See the source [10] and references therein for more facts and language unification regarding the studies by Wittstein and Balducci.

Let us mention that the formulas of the net actuarial values under UDD are well known, they are derived in many sources, see, for example, [2]. Also, the constant mortality force implies the future lifetime (regardless of person’s age) being distributed exponentially, i.e. , , . So, the numerical characteristics of under the constant mortality force are nothing but characteristics of the exponential distribution. In this work, we derive some formulas that make it easier to compute the net actuarial values under Balducci’s assumption. We show that the described computation, dependently on the type of insurance and other circumstances, is essentially based on the exponential integral (10) whose values can be computed by many software.

The main results of this work are listed in Section 2. In Propositions 1-4 we compute the -th moments of the random variables , , , respectively, where denotes the integer part function. The provided moments are computed over the yearly intervals: , , , , where , , provides the years of deferment, and describes the maturity (in years) of insurance. As the random variables and were already introduced, we mention that the random variable describes the present value of the uniformly increasing insurance, while denotes the present value of yearly increasing insurance when the payoff is immediate after the insurer’s death. Based on these random variables, there are various other modifications possible: , , etc. In the next two statements, Propositions 5 and 6, we divide each year in equal pieces and compute the -th moments of the random variables

| (9) |

where the first random variable in (9) can be used to express some net actuarial value when the installments are paid times per year, and the second random variable in (9) describes the present value of the payoff when the insurance amount increases times per year. Authors anticipate that the studied expectations of the provided random variables cover the most relevant insurance types or can be easily modified in a desired way.

2 Main results

Let us denote the exponent integral

| (10) |

and recall two more standard notations in actuarial mathematics:

where denotes the annual return rate, see [12] for more international actuarial notations used in the further text. We start with the statement on the -th moment of the random variable .

Proposition 1.

Remark 1: computing in (12) we shall let run up to such a number that due to which is valid as long as . In other words, if for some in sum (11), then these corresponding summands are zeros due to and

Of course, implies that the survival function for all . In addition, in (11) it can be shown that as if exists.

Remark 2: if for some in sum (11), then these corresponding summands, including the multiplication by , shall be understood as

due to

Let us mention that the values of the exponential integral (10) can be computed according to the formula , where

| (14) |

is the Euler (also known as Euler-Mascheroni) constant. See [13], [14], and [15] for the various approximations the exponent integral.

The next proposition provides some numerical characteristics of the future lifetime when the survival function over the fractional ages is interpolated as in (2). In this case, the sum of hypergeometric functions [16] can give the general expression of the -th moment. However, this provides little value in this context, and we explicitly write down just a few of the first moments. In all subsequent propositions, is allowed under the same means as in Proposition 1 and description in Remark 1.

Proposition 2.

Say that the survival function , is interpolated according to Balducci’s assumption (2) and let denote the future lifetime of a person being of years old. If for all , where , , then

| (15) |

where .

In particular, if, in addition, for all , and , then

| (16) | ||||

| (17) | ||||

| (18) |

Remark 3: Formula (16) does not depend on the interpolation of over fractional age. The expression (17) in a different form with and is also given in [17, p. 24]. It can be shown that if and , exists. The summands in (17) and (18) (also (2)) are zeros if for some , and

as for some . See Remark 1 under Proposition 1 also.

In the next Proposition, we compute the -th moment of the random variable , which describes the present value of uniformly increasing payoff. Again, the general expression is complicated and we write down explicitly just the first two moments.

Proposition 3.

Say that the survival function , is interpolated according to Balducci’s assumption (2) and let denote the future lifetime of a person who is years old. If for all , where , , then

| (19) |

where .

In particular, if, in addition, and for all , then

| (20) |

where

and denotes the exponent integral (10).

Remark 4: as previously, the summands in (20) and (21) are zeros if for some . If for some in the corresponding terms of two sums of (20), then the limit, as , is . If for some in some summands in (21), then the limit, as , is .

In the following proposition, we compute the -th moment of the random variable which describes the present value of the yearly increasing payoff.

Proposition 4.

Remark 5: again, if for some in some summands in (4), then they are zeros. If for some in some summands in (4), then the limits in these corresponding summands, as , are , see also Remark 2 above.

In this work, we do not develop any formulas for the present actuarial values as they admit the representations via the net single premiums computed in Proposition 1, see [2, Ch. 5]. On the other hand, when the insurer pays a certain amount with a different intensity than yearly (as long as he/she is alive), we shall look for some more convenient formulas that convert the present value of such cash flows to the present values of yearly mortality data-based cash flows.

Let us consider the time slot from up to years and split every single year in intervals as follows:

| (23) |

In the next proposition, we provide the formula to compute the -th moment of the random variable , , where the future lifetime is distributed over the intervals in (23). In this situation, insurance deferment can be described by ””, where provides years, and means the number of periods whose length is . For instance, if , then and describe the deferment of a year and two months.

Proposition 5.

Say that the survival function , is interpolated according to Balducci’s assumption (2) and let denote the future lifetime of a person being of years old. If , , and , then

| (24) |

In the last proposition, we provide the formula to compute the -th moment of the random variable , , where the future lifetime again is distributed over the intervals in (23).

Proposition 6.

Remark 6: as previously, implies zero summands in Proposition 6. If , then

3 Some illustrative examples

In this section, we give two examples that verify Propositions 1–6 based on some hypothetical survival laws. As mentioned in the Introduction, the obtained outputs are double-verified according to the formula (6). These examples serve the purpose of convincing the correctness of the given computational formulas rather than reflecting on something from real life, see [18], [19], [20], references therein, and many other sources for studying the survival laws of human populations. On the other hand, papers such as [21], deal with some theoretical studies regarding the survival (tail) function.

The provided conditional survival function implies

Proposition 3 gives:

Proposition 4 yields:

The conditional probability distribution in (25) is known as a discrete Weibull distribution with positive parameters and , see Figures 4, 4, and sources [22], [23], on some recent studies regarding this distribution.

, , , .

The provided mortality law implies

Thus, according to Proposition 1:

Proposition 2:

Proposition 3:

Proposition 4:

4 Lemmas

In this section, we formulate and prove three auxiliary statements. Let us recall that

and

Lemma 1.

Let , , , and suppose that and . Then

| (26) |

where

Proof.

The proof is straightforward

∎

Lemma 2.

Let , , and . Then, under Balducci’s mortality assumption (2),

Proof.

Lemma 3.

Let be the real, differentiable and non-increasing function over the intervals Then the expected value of under Balducci’s mortality assumption is never less than under the UDD assumption.

Conversely, suppose that the function is non-decreasing under the same conditions. In that case, the expected value of under Balducci’s mortality assumption is never greater than under the UDD assumption.

5 Propositions’ proofs

In this Section, we prove all propositions formulated in Section 2.

Proof of Proposition 2.

As is the continuous random variable, eq. (16) is straightforward due to

and elementary rearrangements.

Proof of Proposition 3.

According to the proof of Proposition 1, we shall compute

The last integral, multiplied by , is

Due to the change of variable and rearrangements, the last integral, multiplied by , equals to

Thus

and finally

We now compute the second moment

The last integral, multiplied by , is

Let us denote

Then, omitting the details of elementary rearrangements, we obtain

| (29) |

| (30) |

Thus,

∎

Proof of Proposition 4.

Arguing the same as before, we get

∎

6 Acknowledgments

We thank our colleague Professor Jonas Šiaulys for reviewing the first draft of the manuscript.

References

- \bibcommenthead

- Batten [1978] Batten, R.W.: Mortality Table Construction. Risk, Insurance and Security Series. Prentice-Hall, New Jersey (1978)

- Bowers(Jr.) et al. [1986] Bowers(Jr.), N.L., Gerber, H.U., Hickman, J.C., Jones, D.A., Nesbitt, C.J.: Actuarial Mathematics, 1st edn. Society of Actuaries, Itasca (1986)

- Einaudi [1993] Einaudi, L.: Diario 1945-1947. Editori Laterza, Italy (1993). https://www.bancaditalia.it/pubblicazioni/collana-storica/documenti/documenti-11/CSBI-documenti-11.pdf

- [4] Mosca, M.: Precedenti Storici e Conseguenze Economiche Dell’articolo 81 della Costituzione. http://manuelamosca.com/progetti/artbilancio.pdf

- Unknown [1952] Unknown: Gaetano Balducci, ragionere generale dello Stato, 1952. Italian magazine Epoca, Vol. VII, n. 86, 31 May 1952 (1952)

- Gaetano [1911] Gaetano, B.: La tavola di sopravvivenza della popolazione maschile italiana (1901) interpolata mediante la formola del makeham. Giornale degli Economisti e Rivista di Statistica 42(4), 394–403 (1911)

- Balducci [1917] Balducci, G.: Costruzione e critica delle tavole di mortalità. Giornale degli Economisti e Rivista di Statistica 55 (Anno 28)(6), 455–484 (1917)

- Beyer [1903] Beyer, O.W.: Deutsche Schulwelt des Neunzehnten Jahrhunderts in Wort und Bild. Pichler, Leipzig und Wien (1903). https://scripta.bbf.dipf.de/viewer/!image/481079971/366/-/

- Wittstein [1862] Wittstein, T.: Die mortalität in gesellschaften mit successiv eintretenden und ausscheidenden mitgliedern. Archiv der Mathematik und Physik 39, 67–92 (1862)

- Puzey [1993] Puzey, G.: New techniques for the development of general-purpose parallel programming systems. Phd thesis, City University London (1993). https://openaccess.city.ac.uk/id/eprint/29597/1/Puzey%20thesis%201993%20PDF-A.pdf

- [11] Inc., W.R.: Mathematica, Version 14.0. Champaign, IL, 2024. https://www.wolfram.com/mathematica

- Wolthuis [2014] Wolthuis, H.: International Actuarial Notation. John Wiley & Sons, Ltd, ??? (2014). https://doi.org/10.1002/9781118445112.stat04347

- Giao [2003] Giao, P.H.: Revisit of well function approximation and an easy graphical curve matching technique for theis’ solution. Groundwater 41(3), 387–390 (2003) https://doi.org/10.1111/j.1745-6584.2003.tb02608.x

- Tseng and Lee [1998] Tseng, P.-H., Lee, T.-C.: Numerical evaluation of exponential integral: Theis well function approximation. Journal of Hydrology 205(1), 38–51 (1998) https://doi.org/10.1016/S0022-1694(97)00134-0

- Barry et al. [2000] Barry, D.A., Parlange, J.-Y., Li, L.: Approximation for the exponential integral (theis well function). Journal of Hydrology 227(1), 287–291 (2000) https://doi.org/10.1016/S0022-1694(99)00184-5

- Andrews et al. [1999] Andrews, G.E., Askey, R., Roy, R.: The Hypergeometric Functions. Encyclopedia of Mathematics and its Applications, pp. 61–123. Cambridge University Press, Cambridge (1999)

- Bravo [2007] Bravo, J.: Tábuas de mortalidade contemporâneas e prospectivas: Modelos estocásticos, aplicações actuariais e cobertura do risco de longevidade. Universidade de Évora, Évora (2007)

- Castellares et al. [2022] Castellares, F., Patrício, S., Lemonte, A.J.: On the Gompertz–Makeham law: A useful mortality model to deal with human mortality. Brazilian Journal of Probability and Statistics 36(3), 613–639 (2022) https://doi.org/10.1214/22-BJPS545

- Richards [2012] Richards, S.J.: A handbook of parametric survival models for actuarial use. Scandinavian Actuarial Journal 2012(4), 233–257 (2012) https://doi.org/10.1080/03461238.2010.506688

- Amarjit Kundu and Balakrishnan [2023] Amarjit Kundu, S.C., Balakrishnan, N.: Ordering properties of the smallest and largest lifetimes in gompertz–makeham model. Communications in Statistics - Theory and Methods 52(3), 643–669 (2023) https://doi.org/10.1080/03610926.2021.1919898

- Puišys et al. [2024] Puišys, R., Lewkiewicz, S., Šiaulys, J.: Properties of the random effect transformation. Lithuanian Mathematical Journal 64, 177–189 (2024) https://doi.org/10.1007/s10986-024-09633-3

- Kreer et al. [2024] Kreer, M., Kizilersu, A., Thomas, A.W.: When is the discrete weibull distribution infinitely divisible? Statistics & Probability Letters 215, 110–238 (2024) https://doi.org/10.1016/j.spl.2024.110238

- Endo et al. [2022] Endo, A., Murayama, H., Abbott, S., Ratnayake, R., Pearson, C.A.B., Edmunds, W.J., Fearon, E., Funk, S.: Heavy-tailed sexual contact networks and monkeypox epidemiology in the global outbreak, 2022. Science 378(6615), 90–94 (2022) https://doi.org/10.1126/science.add4507