remarkRemark \newsiamremarkhypothesisHypothesis \newsiamthmclaimClaim \headersLévy Score and Score-Based Particle AlgorithmY. HUANG, C. LIU and X. ZHOU

Lévy Score Function and Score-Based Particle Algorithm for Nonlinear Lévy–Fokker–Planck Equations††thanks: Submitted to the editors DATE. \fundingThis work was funded by the Hong Kong General Research Funds (11308121, 11318522, 11308323), and the NSFC/RGC Joint Research Scheme [RGC Project No. N-CityU102/20 and NSFC Project No. 12061160462.

Abstract

The score function for the diffusion process, also known as the gradient of the log-density, is a basic concept to characterize the probability flow with important applications in the score-based diffusion generative modelling and the simulation of Itô stochastic differential equations. However, neither the probability flow nor the corresponding score function for the diffusion-jump process are known. This paper delivers mathematical derivation, numerical algorithm, and error analysis focusing on the corresponding score function in non-Gaussian systems with jumps and discontinuities represented by the nonlinear Lévy–Fokker–Planck equations. We propose the Lévy score function for such stochastic equations, which features a nonlocal double-integral term, and we develop its training algorithm by minimizing the proposed loss function from samples. Based on the equivalence of the probability flow with deterministic dynamics, we develop a self-consistent score-based transport particle algorithm to sample the interactive Lévy stochastic process at discrete time grid points. We provide error bound for the Kullback–Leibler divergence between the numerical and true probability density functions by overcoming the nonlocal challenges in the Lévy score. The full error analysis with the Monte Carlo error and the time discretization error is furthermore established. To show the usefulness and efficiency of our approach, numerical examples from applications in biology and finance are tested.

keywords:

score function; stochastic differential equation; Lévy–Fokker–Planck equation; probability flow; score-based particle method; Lévy noise.65M75, 65C35, 68T07, 60H35

1 Introduction

Stochastic processes, such as the Itô diffusion process and the Lévy jump process, play prominent roles in a variety range of fields including science, engineering, economics, and statistics. The temporal evolution of the probability distribution, satisfying the initial-value forward Kolmogorov equation, can be also viewed as a path or curve in the space of probability distributions. The path connecting two probability density functions associated certain stochastic processes is the crucial mathematical tool the basis of score-based generative algorithms [38].

The viewpoint of probability flow is to treat the time evolution of the probability density function as the continuity equation whose velocity field contains the gradient of the density function in the self-consistent way. In the setting of a diffusion process , the density function of is given by the Fokker-Planck equation

| (1) |

where is the drift term and corresponds to the diffusion matrix. If the term , denoted by the score function , is known a prior, then (1) takes the form of a continuity equation corresponds to the transportation between the density functions and by a underlying deterministic ODE flow with the new vector field . This observation is also the theoretic foundation of reversing a Markov diffusion process in score-based diffusion models since the time reverse from to can implemented by the time-reversed deterministic flow. However, the various numerical methods [19, 36, 38, 34] to find the score function for the generative modeling like image synthesis are limited to the constant drift or the Orenstein-Ulenbeck process, because these simple processes suffice to inject Gaussian noise to the data. In such simple systems, the transition probability is analytically available.

Motivated by the probability flow and score-based generative models, a number of studies [29, 33, 24, 28, 4, 32] have been recently carried out to learn the underlying velocity field that drives the probability density function in Fokker-Planck equations, instead of directly simulating the diffusion SDE or solving the Fokker-Planck PDE. These methods, usually referred to as score-based transport modeling[4], deterministically push samples from the initial density onto samples from the solution at any later time by employing particle methods to learn the score function from the samples following the deterministic flow. By finding the above mentioned score function appearing in the new velocity field, this numerical strategy works well due to the self-consistency of the Fokker-Planck equation [24, 24] in the form of fixed-point argument. Compared with the traditional grid-based numerical methods for the Fokker–Planck equation, these score-based methods can scale well in high dimensions. Compared to the traditional numerical SDE schemes, the deterministic flow is faster to compute and offers the expression of the density function to facilitate calculating many non-equilibrium statistical quantities like the probability current, the entropy production rate and the heat [39, 5]. The theoretic works related to these algorithms include the error analysis for Kullback-Leibler divergence due to the approximate score function [32, 33, 28, 4]. There are also substantial extensions from the Fokker-Planck equation to the McKean-Vlaso equation [29, 32, 28] and the Fokker-Planck-Landau equation[20, 17].

However, the existing score-based transport modeling only studied the diffusion process with the focus on the conventional score function and the score matching error as the loss function to train the score. Despite the popularity in applications of the diffusion model, the non-Gaussian processes such as Lévy processes are preferred to more accurately represent complex stochastic events than conventional Gaussian models [22, 3, 35]. Recently, the Lévy-Itô model with the fractional score function , , is used in [41] for score-based generative models to generate more diverse samples by taking advantage of the heavy-tailed properties of the -stable Lévy process. In [16], the same fractional score function is computed for the Lévy–Fokker–Planck equation by training the fractional score-based physics-informed neural networks from a large number of sample stochastic trajectories as the training data.

In this paper, we systematically investigate the score-based transport modeling for the general Markov process of non-Gaussian type and develop the score-based theories and algorithms to simulate the underlying jump-diffusion process. This paper delivers mathematical derivation, numerical algorithm, and error analysis focusing on the corresponding score function in non-Gaussian systems with jumps and discontinuities represented by the nonlinear Lévy–Fokker–Planck equations. We propose the Lévy score function for such stochastic equations, which features a nonlocal double-integral term, and its training algorithm by minimizing the proposed loss function from samples. Based on the equivalence of the probability flow with deterministic dynamics, we develop a self-consistent score-based transport particle algorithm to sample the interactive Lévy stochastic process at discrete time grid points.

Contributions

-

1.

For the nonlinear stochastic differential equation (2) driven by the Brownian and Lévy noise as well as the mean-field interaction, we derive the continuity equation for the nonlinear Lévy-Fokker-Planck equation (4) to identify the vector field in the probability flow. We propose the generalized score function, in (8), consisting of both the conventional diffusion score function and the Lévy score function. The latter has the non-local double-integral terms involving the Lévy measure.

-

2.

We show in Theorem 3.2 that, the Kullback–Leibler divergence between the numerical score-based and the true density function is bounded by a loss function we derived from the fixed-point argument. This is a significant extension to [32, 33, 4, 28] since our analysis takes into account of both the non-Gaussian process and the mean-field interactions.

-

3.

We propose the score-matching training algorithm to learn both the diffusion and Lévy score functions by one single neural network, then develop the sequential score-based particle algorithm (Algorithm 1) to solve the Lévy–Fokker–Planck equation based on the idea of score-based transport modeling. We test several numerical examples to demonstrate the effectiveness of our approach.

- 4.

Related works:

Score-based diffusion model and the error analysis. The score-based diffusion model is formulated as the forward and backward continuous Itô stochastic differential equations in [38]. The score matching to train the score function by neural networks includes [19, 37, 15, 34, 14, 27]. For comprehensive reviews on related topics, we refer readers to [12]. There are also extensive works to analyze the convergence and error estimates, for instance [10, 8, 7].

Score-based transport modeling for Fokker-Planck equation. These methods are all based on (1) – the equivalence to probability flow – to simulate the time evolution of Fokker–Planck solutions. [29] runs a large number of interacting deterministic particles where the gradient–log–density (score) function is approximated in the reproducing kernel Hilbert space (RKHS). [33, 32] formulated a fixed-point problem for the self-consistency of the probability flow for the Fokker–Planck equation, but the optimization for the diffusion score function is based on the adjoint method which is in general slow and challenging to implement. The score-based transport modeling in [4] is to march the flow sequentially in time with the forward Euler scheme. Instead, [24] proposed to learn the velocity field as a whole for by an iterative update of the velocity field.

Score-based generative models with -stable Lévy processes. [41] proposed score-based generative models with a simple forward Lévy process , where follows the data distribution, and the noise follows the isotropic -stable distribution with the scalar parameter . The fractional score function with , is proposed for the pdf in order to define the time-reversal Lévy process. This fractional score function is approximated by a neural network and simple enough to use the denoising score-matching similarly to the score-based diffusion models.

Fractional score-based physics-informed neural networks(PINN) for -stable Lévy processes . [16] proposed the score-fPINN method for the log-likelihood of an -stable Lévy process by minimizing the PINN loss for the two nonlinear PDEs of and respectively, which involve the pairs and , and , respectively, where is the same fractional score defined as in [41]. The fractional score serves only as an intermediate variable to compute from to . By the score-matching method applicable to any stochastic process [37], the diffusion score is computed by the neural network, entirely based on the simulated long trajectories of the SDE beforehand.

Finally, we provide some remarks in the following to further explain a few other aspects of our works.

- •

-

•

Our algorithm and analysis cover the systems with mean-field interactions as in [28, 32]. Our theorems apply to the interaction kernels of the bounded interaction and the Biot-Savart interaction as in [32] for the Fokker–Planck equation. But due to the challenges from the Lévy score, we have not yet prove for the Column interaction as the diffusion process in [32].

- •

-

•

Even though our numerical algorithm to train the score is sequential in time as in [4], the approach in [24] of the self-consistent velocity matching by learning from the whole simulated trajectories until a terminal time is applicable to the Lévy–Fokker–Planck equation here, because the same fixed-point formulation works with the new defined Lévy score function in our work.

The structure of this paper is as follows: Section 2 shows how to define the generalized score function (the diffusion score and the Lévy score) and establish the probability flow equivalence. Section 3 introduces a particle system-based numerical method, presents bounds on the Kullback–Leibler divergence in Theorem 3.2, and analyzes discretization errors in Theorem 3.4. Section 4 demonstrates the method through numerical experiments. The conclusion part is summarized in Section 5.

2 Probability Flow of Jump-Diffusion and Lévy Score Function

2.1 Mckean–Vlasov SDE driven by Lévy noise

We consider the following Mckean–Vlasov stochastic differential equation that incorporates non-Gaussian noise:

| (2) |

where denotes the set of probability measures in with finite quadratic moment and denotes the law of . The domain is either or the torus (a hypercube with periodic boundary condition), is a standard Brownian motion in and is an independent Poisson random measure on with the associated compensator and the intensity measure which is a Lévy measure, i.e., . The mappings , , , , , , all assumed to be measurable for and . denotes some interaction kernel and denotes the convolution operation, i.e., . We introduce the following assumptions on the drift term , diffusion coefficient , the jump noise coefficients and the Lévy measure .

Assumption 1.

-

1.

For every , and are -measurable functions for and . There exists positive constants such that where denotes the Euclidean norm in .

-

2.

The functions , the Lévy measure satisfies , and there exist constants and dependent on such that .

Our analysis will focus on the following two cases of the interaction kernel .

-

1.

(Bounded interaction) The kernel and there exists a positive constant such that .

-

2.

(Biot–Savart interaction) The dimension and the interaction term is the Biot–Savart kernel, i.e., where . This kernel is used to describe the dynamics of electromagnetism [13].

For the bounded interaction case 1, under Assumption 1, the well-posedness of the SDE (2) can be established by applying the interlacing technique to exclude large jumps (defined as exceeding 1) [26, Theorem 4]. For the Biot–Savart interaction case 2, to the best of our knowledge, there is no literature rigorously proving the well-posedness of (2). However, we do not focus on this issue in the present paper, and thus omit further discussion. To manage possible singularities in the interaction kernel , one can consider the regularized form, for instance, for the potential, the modification ensures is bounded for every .

2.2 Lévy–Fokker-Planck equation and Lévy score function

The probability flow serves as a crucial link between the forward Kolmogorov equation and the continuity equation for the density function, as illustrated in (1). It effectively handles (nonlinear) diffusion processes through an ODE flow framework facilitated by a well-defined score function. In the following, we investigate the counterpart to the conventional diffusion score function for (2), which we refer to as the Lévy score function. To identify this score function, we first need to convert the Lévy-Fokker-Planck equation into a continuity equation. Our formulation of the Lévy-Fokker-Planck equation has appeared in our other work [18]. The result is more general than the stable Lévy process considered in [16, 41], and has no explicit term of the fractional Laplacian. We start from the infinitesimal generator[1, 25] for (2):

| (3) | ||||

for each function and each point . We apply the Taylor’s theorem to and at the point : . Substitute it to (3), and compute the adjoint operator of , with more details in [18], we then have the following form of the Lévy–Fokker-Planck equation associated with (2):

| (4) | ||||

which can be rewritten as the continuity equation:

| (5) | ||||

Based on (5), the solution density to the Lévy-Fokker-Planck equation (4) can be interpreted as the pushforward of under the flow map governed by

| (6) |

referred to as the probability flow equation. Here the vector field depends on the in a self-consistent way:

| (7) | ||||

In the above, we define the generalized score function as follows:

| (8) | ||||

| (9) | ||||

The gradient term in of (8) is recognized as the conventional score function derived from the Laplacian terms associated with Gaussian noise, which will be referred to as diffusion score. in (9) consist of non-local double integral terms, arising from jump noise, which is called the Lévy score function.

2.3 Isotropic -stable Lévy process

The fractional score function , is proposed in Lévy-type score-based generative modeling [41] and used in [16] to solve the Lévy–Fokker–Planck equation through physics-informed neural networks. This fractional score function is the special case of our result above. Consider the special -stable Lévy processes: which fall within our diffusion-jump SDE (2) with , , and is the -stable Lévy measure ; note that . In this special case, the Lévy–Fokker-Planck equation (4) reads

where denote the fractional Laplacian of order [6], i.e.,

with a normalizing constant . Note that [41, Lemma C.1]

So the Lévy score function we define in (9) reduces to the fractional score function .

2.4 Probability flow for probability density function

The remarkable property of the continuity equation (5) is the following: The flow associated with the deterministic ordinary differential equation (6) transports the initial distribution forward exactly along the density distribution of the SDE (2). To turn this idea into a feasible numerical algorithm certainly needs to obtain the generalized score or the velocity in (7) beforehand, which will be studied in next section. If is a sample from the initial distribution , then in (6) will be a sample from . We use to denote the push-forward operation, then can be determined at any position using the change of variables formula [31, 40]:

| (10) |

where is the divergence of the velocity field defined in (7). It is straightforward to observe that , the solution of the Lévy–Fokker-Planck equation (4), is the fixed point of the map

By evolving an ensemble of independent realizations of (6), referred to as “particles”, according to

| (11) |

an empirical approximation to is obtained:

3 Score-based Particle Approach: Theoretical and Numerical Analysis

Recall (10), the general principle involves here addresses the following fixed-point problem: For any given velocity field , the flow dictated by the ODE (6) will transport the initial density to obtain , and this transported furthermore induces the new velocity field defined via (7). It is evident that the true velocity field is the fixed point of this map . Thus, if we are provided with a set of vector fields , and obtain its corresponding probability flows via (6), the ideal choice of these vector fields that approximate the true vector field is the one that minimizes the following loss function with some samples from :

Moving forward, we will first establish a theoretical foundation for our method in Section 3.1 using the above loss function. Following this, we will develop a specific algorithm in Section 3.2 and conduct a detailed error analysis in Section 3.3.

3.1 The Kullback–Leibler divergence error

For simplicity, we introduce the following notations

| (12) | ||||

| (13) | ||||

| (14) | ||||

| (15) |

And recall the vector field (7), it is written as

| (16) |

Now suppose we are given a family of time-varying hypothesis velocity fields for some index set , and let be the solution to the continuity equation

| (17) |

Similar with previous arguments, the solution density can be viewed as the push forward of under the flow map of the ordinary differential equation

| (18) |

and thus the density function can be written as

| (19) |

as discussed before.

Let us make some assumptions on the the initial distribution , the Lévy-Fokker-Planck solution , and the parametrized vector fields . In the remainder of this paper, we will focus on the case where is a torus. The method for extending this to an unbounded domain is similar to the approach detailed in [32, Appendix G], which requires additional assumptions about the regularity of the initial distribution and the true probability flow .

Assumption 2.

-

1.

The initial distribution is absolutely continuous with respect to the Lebesgue measure (we still denote its density as ) and there exists a positive constant such that and ;

-

2.

For every , the solution to (4) for every and there is a positive constant such that .

-

3.

The velocity field for every . For every , there is a positive constant such that .

Remark 3.1.

3.2 Sequential Lévy score-based particle method

By Theorem 3.2, we can minimize the following function to control the KL divergence between the numerical and the true : , where is defined in (16). By (6) and (7), the velocity field is given by

| (21) |

where is the numerical score function parametrized by ,

| (22) |

Now the optimization problem turns to

| (23) | ||||

The primary difficulty with this optimization problem (23) is that depends on , since the velocity used in (17) depends on . Such an issue has been observed in [4]. To make the resulting minimization of the right-hand side of (20) practical, we consider to learn separately at each time sub-interval in a time-discrete way so that can be assumed unchanged within each short time sub-interval.

Then we consider the loss at any given time , by assuming is frozen:

Note that the second term contains no , so we can drop it during the optimization procedure. For the remaining first and third terms, we shall express them by the expectation w.r.t. . That is, , and . And by integral by part, . And for the non-local terms by (12) we have,

In summary, we have the following loss function for the function at time as

| (24) | ||||

Given the current samples of from law at any time , we can obtain via direct minimization of objective in (24). Given , we propagate forward in time up to time via (18). The resulting procedure, which alternates between self-consistent score estimation and sample propagation, is presented in Algorithm 1 for the choice of a forward-Euler integration routine as to .

Here the one dimensional integral of is discretized by any quadrature scheme, like the trapezoidal rule. The integral w.r.t. in is approximated by the quadrature scheme in low dimension or by the Monte Carlo average in high dimension. is pre-computed as a function of only.

Remark 3.3.

Algorithm 1 trains neural networks to approximate the sum of the Lévy score function and the negative interaction term. So, the probability flow in Algorithm 1 can evolve the particles independently without any interaction. This approach contrasts with the one described in [28], which did not include the score contribution from the interaction term. The extra cost here is the double sum of in the loss function for the score training, but since the training process is based on the mini-batch, the random batch method of randomly selecting particles is easily applied here for this double sum.

3.3 Error analysis of Algorithm 1

Now we focus on analyzing the discrete error associated with Algorithm 1. The following theorem demonstrates that the discrete numerical error of Algorithm 1 is on the order of , where represents the number of particles utilized in the algorithm.

Theorem 3.4.

Let , , , and be defined as in Algorithm 1 and denote , as the approximation error of a neural network function , with the solution of the Lévy–Fokker–Planck equation (4). Denote the numerical transport map obtained from Algorithm 1 by stacking the transport map in each sub-interval starting from . Let starting from solve the deterministic probability flow equation , corresponding to ODE (11), and are given in (12), (13). Under Assumption 2, for any ,

| (25) |

as , and all tend to 0.

3.4 Proof of Theorem 3.2

We first present a lemma about the bounds of the squared -norm of two probability density functions by their KL divergence, which will be used in our main proof.

Lemma 3.5.

Suppose and are two probability densities on , and there exists a positive constant such that . Then we have

Proof 3.6.

Define . Then . Define two Borel sets as follows, . We obtain that for , where ; for , where . Note that and are two probabilities density on , that is , which implies that . Thus

For the first term in right hand side of the above equality, we have . For the second term, we have . Finally, we have .

Proof 3.7 (Proof of Theorem 3.2).

The proof is inspired by the methodologies presented in [4, Proposition 1] and [32, Appendix E]. However, dealing with the Lévy term introduces substantial complexity, requiring the introduction of novel techniques for a thorough analysis.

Firstly, according to the definition of KL divergence, we derive that

where we used and the integration by parts.

With the expression of (12), we decompose the derivative of the KL divergence as follows,

where .The bounds for these four terms are studied below respectively in four steps.

(Step 1.) For the perturbation part, by the Cauchy–Schwarz inequality we have

(Step 2.) For the interaction part, there are two cases 1 and 2 for the interaction kernel . We discuss each case respectively.

(Bounded interaction) By the Cauchy–Schwarz inequality we have

where we use the Csiszár–Kullback–Pinsker inequality [40] for the last inequality.

(Biot–Savart interaction) For the Biot–Savart interaction kernel, as noted by [21], it can be written as:

We follow the statement in [32, Appendix E.1] to have

we use the Csiszár–Kullback–Pinsker inequality to obtain the last inequality.

(Step 4.) The last part is about the Lévy terms . We have the following estimate:

where the inequality “” arises from the Cauchy–Schwarz inequality, and “” comes from Assumption2-2. is the constant given in Remark 3.1. Similarly, we have

By Lemma 3.5, the squared -norm of can be controlled by the KL divergence between and , thus we know that for any ,

where

| (26) |

Finally, we aggregate the above four bounds to get the upper bound for the derivative of the KL divergence between and . It is treated for two cases of interaction kernels as below.

(Bounded interaction)

(Biot–Savart interaction)

By Gronwall inequality, we obtain that

where

| (27) |

3.5 Proof of Theorem 3.4

Proof 3.8 (Proof of Theorem 3.4).

For convenience and simplicity, we write , as , . For , using Taylor expansion and the smoothness of the velocity , we have

| (28) | ||||

for some . According to Algorithm 1, we have

| (29) |

where is a set of samples from initial density . Note that is the total “score” term, we could separate it into three parts that correspond to the interaction, diffusion and Lévy losses respectively. Let

| (30) |

Subtracting equation (28) by (29) we have

| (31) | ||||

where and are given in the following. First, based on the law of large numbers and the assumption that the kernel function is twice-differentiable, for the bounded interaction (1),

where . For the Biot–Savart interaction (2),

where .

Second,

where .

Third,

where .

4 Numerical Experiments

We examine several examples to demonstrate the effectiveness of our algorithm 1. The time interval is uniformly partitioned into sub-intervals , where for . On each sub-interval , the transport map is approximated by a neural network , modeled as a multi-layer perceptron (MLP) with hidden layers, neurons per layer, and the activation function. The algorithm is implemented with the following parameter settings: the time step size of , the time horizon of , and the sample size of .

The initial condition of (2) in all examples is set as the Gaussian distribution for its simplicity in generating initial samples (unless otherwise specified, it is assumed to be the standard normal distribution). For each time step in training the score function , we use the warm start for the optimization by initializing the neural network parameter by the obtained parameters from the previous step, followed by the standard the Adam optimizer with a learning rate of to optimize .

To evaluate our method, we use the total variation (TV) distance of the generated samples to compare out method with the Monte Carlo simulation method. At each time , we identify the smallest rectangular domain covering all sample points and discretize it into uniform grid cells . The distribution for each method is then approximated by a histogram: . We denote these binned empirical distributions as for Monte Carlo and for our method, and the TV distance between these two distributions is then numerically computed by

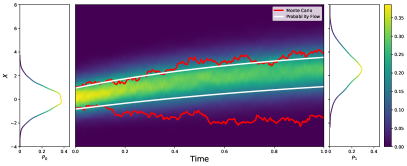

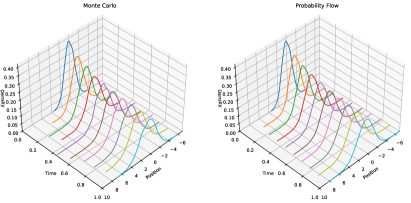

Example 4.1 (1D Jump-diffusion with finite jump activity).

To test the efficiency of our proposed method, we consider the following one-dimensional SDE:

| (32) |

which has been applied in [9] to model emissions and fuel-switching strategies. In this example, we set , , and . The process is assumed to be a Poisson process with intensity , while the jump sizes are drawn from a Gaussian distribution with mean and standard deviation . To compare with (2), the jump term is equivalently written as , i.e., , where is a Poisson random measure with Lévy measure , and the numerical integration with respect to is based on a quadrature formula within a truncated interval .

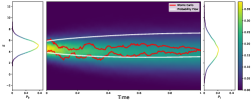

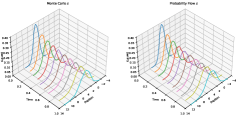

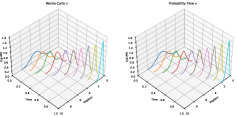

Figure 1 illustrates the temporal evolution of probability flows and probability density functions for Equation (32), obtained via both the Monte Carlo simulation and the proposed method. Specifically, the Monte Carlo simulation employs the following Euler–Maruyama discretization scheme: where , is a Poisson random variable with rate , and ’s are i.i.d. random variables for jump sizes distributed as .

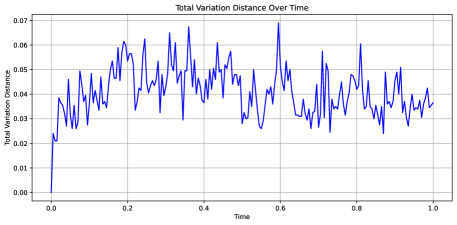

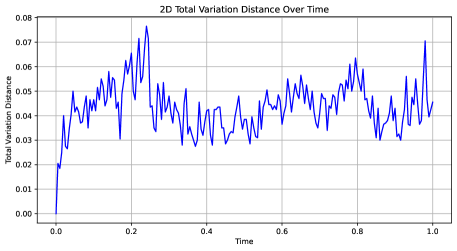

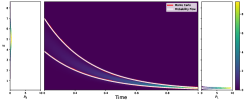

Figure 2 illustrates the TV distance between and . The TV distance remains consistently on the order of , which demonstrates the relative accuracy of our method across time.

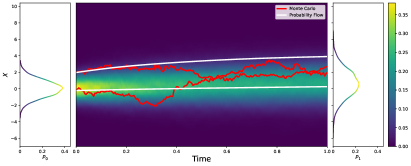

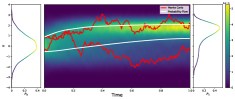

Example 4.2 (Jump-diffusion with -stable Lévy noise).

In this example, we consider the following one-dimensional SDE:

| (33) |

which has been widely used to capture dynamics with both continuous fluctuations and heavy-tailed, discontinuous shocks, making them relevant in fields such as finance, physics [2], and generative modeling [41]. This system captures mean reversion, diffusion, and an -stable Lévy motion with Lévy measure:

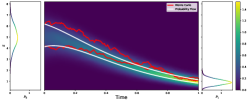

We set while keeping all other hyperparameters the same as in Example 4.1. To avoid the singularity of the intensity measure at , the numerical integration with respect to is restricted to the interval . In this example, the Monte Carlo simulation is based on the following Euler–Maruyama scheme: , where the jump increments follow a stable distribution .

Figure 3 and Figure 4 depict the evolutions of probability flow and the TV distance between and . The proposed method demonstrates convincing performance in handling -stable Lévy processes and singular intensity measures, maintaining a TV distance on the order of .

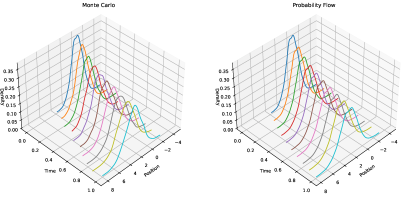

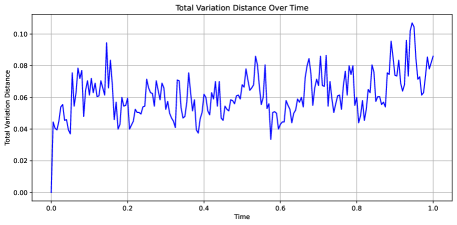

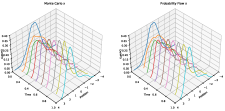

Example 4.3 (Double-well system with interaction force).

Next, we consider the following two-dimensional interactive SDE:

| (34) | ||||

where the interaction kernel is . We set the parameters and to be the same as those in Example 4.1, and the Monte Carlo simulation is based on the following Euler–Maruyama method:

| (35) | ||||

where and are independent random variables sampled from the Gaussian distribution .

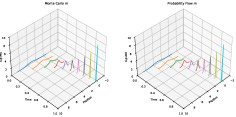

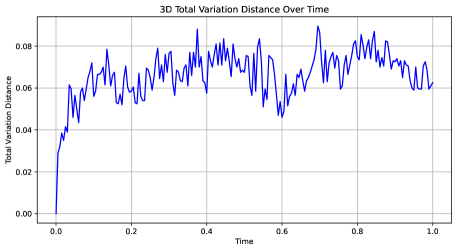

Figure 5 illustrates the evolution of probability flows obtained from Equation (34), computed using both the Monte Carlo simulation and the proposed approach. Figure 6 depicts the probability flow evolution on the -plane at different time steps for both methods. Finally, Figure 7 presents the TV distance between and , consistently demonstrating values on the order of . These results confirm the accuracy of the proposed method in approximating the probability flows for systems with interaction terms.

Example 4.4 (State-dependent jump-diffusion).

To conclude our numerical study, we consider the following three-dimensional SDE which describes the asset price dynamics under both jump and stochastic volatility conditions[23]

| (36) | ||||

Here is the standard Brownian motion in and is an independent Poisson process with the state-dependent rate . The jump component follows the exponential distribution with the expectation . Meanwhile, the jump component for the stock price, , follows a shifted log-normal distribution, where is characterized by the parameters and , leading to .The parameters are from [23] and specified as follows: = , , and .

We set the initial condition as a three-dimensional Gaussian distribution with the mean vector and the covariance matrix of a identity matrix. The numerical integration for is performed over a two-dimensional uniform grid defined on , which is designed to capture the critical density features required for accurate numerical evaluation. The Monte Carlo approximation is easy to achieve by noting that the numerical approximation of is where are i.i.d samples from the law of and . Similarly is approximated by where are i.i.d samples from the law of .

Let , the SDE (36) can be rewritten as

where denotes a random Poisson measure on with Lévy measure , and the jump-size measure . In this expression, .

Figure 8 illustrates the evolution of probability flows for each marginal derived from Equation (36). Figure 9 presents the TV distance between the probabilities and , demonstrating that the distance remains on the order of . These results highlight the capability of our proposed method to accurately and efficiently solve complex state-dependent jump-diffusion systems.

5 Conclusions

In this paper, we introduced the concept of the generalized score function, which unifies the conventional diffusion score and the Lévy score, thereby accommodating a broad class of non-Gaussian processes. Leveraging this generalized score function, we developed a score-based particle algorithm to efficiently solve the nonlinear Lévy-Fokker-Planck equation through sampling of probability flow data. Furthermore, we demonstrate that the Kullback-Leibler divergence between the numerical solution and the ground truth is bounded by a specific loss function, derived from a fixed-point perspective. The rigorous numerical analysis was conducted to validate the theoretical properties of our algorithm. Finally, several numerical examples were presented to illustrate the effectiveness and accuracy of the proposed method.

Data Availability

The datasets generated and/or analyzed during the current study are available in the GitHub reposItôry, accessible via the following link: https://github.com/cliu687/sbtm-levy. All scripts and supporting files necessary to reproduce the findings are openly provided in this reposItôry.

References

- [1] D. Applebaum, Lévy processes and stochastic calculus, Cambridge university press, 2009.

- [2] T. Ariga, K. Tateishi, M. Tomishige, and D. Mizuno, Noise-induced acceleration of single molecule kinesin-1, Physical review letters, 127 (2021), p. 178101.

- [3] P. Barthelemy, J. Bertolotti, and D. S. Wiersma, A Lévy flight for light, Nature, 453 (2008), pp. 495–498.

- [4] N. M. Boffi and E. Vanden-Eijnden, Probability flow solution of the Fokker–Planck equation, Machine Learning: Science and Technology, 4 (2023), p. 035012.

- [5] N. M. Boffi and E. Vanden-Eijnden, Deep learning probability flows and entropy production rates in active matter, P NATL ACAD SCI USA, 121 (2024), p. e2318106121.

- [6] L. Caffarelli and L. Silvestre, An extension problem related to the fractional Laplacian, Communications in partial differential equations, 32 (2007), pp. 1245–1260.

- [7] Y. Cao, J. Chen, Y. Luo, and X. Zhou, Exploring the optimal choice for generative processes in diffusion models: Ordinary vs stochastic differential equations, Advances in Neural Information Processing Systems, 36 (2024).

- [8] H. Chen, H. Lee, and J. Lu, Improved analysis of score-based generative modeling: User-friendly bounds under minimal smoothness assumptions, in Proceedings of the 40th International Conference on Machine Learning, vol. 202, 2023, pp. 4735–4763.

- [9] J. Chevallier and S. Goutte, Estimation of Lévy-driven Ornstein–Uhlenbeck processes: Application to modeling of CO2 and fuel-switching, Annals of Operations Research, 255 (2017), pp. 169–197.

- [10] V. De Bortoli, J. Thornton, J. Heng, and A. Doucet, Diffusion Schrödinger bridge with applications to score-based generative modeling, in Advances in Neural Information Processing Systems, vol. 34, Curran Associates, Inc., 2021, pp. 17695–17709.

- [11] P.-E. C. de Raynal, J.-F. Jabir, and S. Menozzi, Multidimensional stable driven Mckean–Vlasov SDEs with distributional interaction kernel: a regularization by noise perspective, Stochastics and Partial Differential Equations: Analysis and Computations, (2024), pp. 1–54.

- [12] D. Gallon, A. Jentzen, and P. von Wurstemberger, An overview of diffusion models for generative artificial intelligence, arXiv preprint arXiv:2412.01371, (2024).

- [13] F. Golse, On the dynamics of large particle systems in the mean field limit, Macroscopic and large scale phenomena: coarse graining, mean field limits and ergodicity, (2016), pp. 1–144.

- [14] G. Gottwald, F. Li, Y. Marzouk, and S. Reich, Stable generative modeling using diffusion maps, arXiv preprint arXiv:2401.04372, (2024).

- [15] J. Ho, A. Jain, and P. Abbeel, Denoising diffusion probabilistic models, in Advances in Neural Information Processing Systems, vol. 33, Curran Associates, Inc., 2020, pp. 6840–6851.

- [16] Z. Hu, Z. Zhang, G. E. Karniadakis, and K. Kawaguchi, Score-fPINN: Fractional score-based physics-informed neural networks for high-dimensional Fokker-Planck-Lévy equations, arXiv preprint arXiv:2406.11676, (2024).

- [17] Y. Huang and L. Wang, A score-based particle method for homogeneous Landau equation, arXiv preprint arXiv:2405.05187, (2024).

- [18] Y. Huang, X. Zhou, and J. Duan, Probability flow approach to the Onsager–Machlup functional for jump-diffusion processes, SIAM Applied Math(accepted). arXiv:2409.01340.

- [19] A. Hyvärinen and P. Dayan, Estimation of non-normalized statistical models by score matching., Journal of Machine Learning Research, 6 (2005).

- [20] V. Ilin, J. Hu, and Z. Wang, Transport based particle methods for the Fokker-Planck-Landau equation, ArXiv, abs/2405.10392 (2024).

- [21] P.-E. Jabin and Z. Wang, Quantitative estimates of propagation of chaos for stochastic systems with kernels, Inventiones mathematicae, 214 (2018), pp. 523–591.

- [22] K. Kanazawa, T. G. Sano, A. Cairoli, and A. Baule, Loopy Lévy flights enhance tracer diffusion in active suspensions, Nature, 579 (2020), pp. 364–367.

- [23] D. Kristensen, Y. J. Lee, and A. Mele, Closed-form approximations of moments and densities of continuous–time Markov models, Journal of Economic Dynamics and Control, (2024), p. 104948.

- [24] L. Li, S. Hurault, and J. Solomon, Self-consistent velocity matching of probability flows, in Thirty-seventh Conference on Neural Information Processing Systems, 2023.

- [25] M. Liang, M. B. Majka, and J. Wang, Exponential ergodicity for SDEs and Mckean–Vlasov processes with Lévy noise, Annales de l’Institut Henri Poincare (B) Probabilites et statistiques, 57 (2021), pp. 1665–1701.

- [26] H. Liu and J. Y. Lin, Stochastic Mckean–Vlasov equations with Lévy noise: Existence, attractiveness and stability, Chaos, Solitons & Fractals, 177 (2023), p. 114214.

- [27] Y. Liu, M. Yang, Z. Zhang, F. Bao, Y. Cao, and G. Zhang, Diffusion-model-assisted supervised learning of generative models for density estimation, Journal of Machine Learning for Modeling and Computing, 5 (2024).

- [28] J. Lu, Y. Wu, and Y. Xiang, Score-based transport modeling for mean-field Fokker-Planck equations, Journal of Computational Physics, 503 (2024), p. 112859.

- [29] D. Maoutsa, S. Reich, and M. Opper, Interacting particle solutions of Fokker–Planck equations through gradient–log–density estimation, Entropy, 22 (2020), p. 802.

- [30] C. Olivera and M. Simon, Microscopic derivation of non-local models with anomalous diffusions from stochastic particle systems, arXiv preprint arXiv:2404.03772, (2024).

- [31] F. Santambrogio, Optimal transport for applied mathematicians, Birkäuser, NY, 55 (2015).

- [32] Z. Shen and Z. Wang, Entropy-dissipation informed neural network for Mckean-Vlasov type PDEs, Advances in Neural Information Processing Systems, 36 (2024).

- [33] Z. Shen, Z. Wang, S. Kale, A. Ribeiro, A. Karbasi, and H. Hassani, Self-consistency of the Fokker–Planck equation, in Conference on Learning Theory, PMLR, 2022, pp. 817–841.

- [34] J. Song, C. Meng, and S. Ermon, Denoising diffusion implicit models, in International Conference on Learning Representations, 2021.

- [35] M. S. Song, H. C. Moon, J.-H. Jeon, and H. Y. Park, Neuronal messenger ribonucleoprotein transport follows an aging Lévy walk, Nature communications, 9 (2018), pp. 1–8.

- [36] Y. Song and S. Ermon, Generative modeling by estimating gradients of the data distribution, in NeurIPS, vol. 32, Curran Associates, Inc., 2019.

- [37] Y. Song, S. Garg, J. Shi, and S. Ermon, Sliced score matching: A scalable approach to density and score estimation, in Uncertainty in Artificial Intelligence, PMLR, 2020, pp. 574–584.

- [38] Y. Song, J. Sohl-Dickstein, D. P. Kingma, A. Kumar, S. Ermon, and B. Poole, Score-based generative modeling through stochastic differential equations, International Conference on Learning Representations (ICLR), (2021).

- [39] T. Tomé and M. Oliveira, Stochastic Dynamics and Irreversibility, Graduate Texts in Physics, Springer International Publishing, 2014.

- [40] C. Villani et al., Optimal transport: old and new, vol. 338, Springer, 2009.

- [41] E. B. Yoon, K. Park, S. Kim, and S. Lim, Score-based generative models with Lévy processes, Advances in Neural Information Processing Systems, 36 (2023), pp. 40694–40707.