Central limit theorems for vector-valued composite functionals with smoothing and applications ††thanks: The support of the Office of Naval Research under grant N00014-21-1-216 is gratefully acknowledged.

Abstract:

This paper focuses on vector-valued composite functionals, which may be nonlinear in probability. Our primary goal is to establish central limit theorems for these functionals when mixed estimators are employed. Our study is relevant to the evaluation and comparison of risk in decision-making contexts and extends to functionals that arise in machine learning methods. A generalized family of composite risk functionals is presented, which encompasses most of the known coherent risk measures including systemic measures of risk. The paper makes two main contributions. First, we analyze vector-valued functionals, providing a framework for evaluating high-dimensional risks. This framework facilitates the comparison of multiple risk measures, as well as the estimation and asymptotic analysis of systemic risk and its optimal value in decision-making problems. Second, we derive novel central limit theorems for optimized composite functionals when mixed types of estimators: empirical and smoothed estimators are used. We provide verifiable sufficient conditions for the central limit formulae and show their applicability to several popular measures of risk.

Keywords coherent measure of risk, stochastic programming, systemic risk

1 Introduction

In the area of machine learning, business, engineering, and others, optimization under uncertainty and risk are indispensable. A plenitude of literature addresses the properties of and efficient numerical approach to data-driven stochastic optimization problems. Recently, the methods of risk-averse optimization and learning have become a subject of increased interest and our paper aims to contribute to that area.

Our main focus is placed on the following general functions.

| (1) |

where is a random vector defined on the probability space with realizations in . The probability measure induced by the random vector is denoted by . The vector functions , and are assumed -integrable with respect to their last argument and for they are continuous with respect to the first argument. The standard notation stands for the set of -dimensional random vectors defined on the probability space that are indistinguishable on sets of -measure zero and have finite moments. We assume that with some .

Many coherent measures of risk may be cast in this form. In [4], we have shown that the mean-semi deviations measures of order , the Average Value at Risk at level , as well as the higher-order measures of risk can be represented as (optimized) composite functionals of form (1) with being a decision vector when optimization of risk control is involved. For more information on these measures, we refer to [15, 16, 18, 14]. A comprehensive treatment of optimization models with risk measures is provided in [23, 5]. Furthermore, problems in other areas, such as machine learning, deal with composite optimization as well [28, 10].

Suppose a sample of independent realizations of the random vector is available. We are interested in the case when we need to use the entire sample for estimating the expected values at all levels. This need arises when we do not have a large sample for the given dimension of and sampling is expensive or difficult. The empirical estimator of the composite risk functional is the following

| (2) |

When , we shall consider optimizing a risk measure. In that case, we shall assume that all functions depend additionally on a decision variable and we solve the following problem.

| (3) |

assuming that is closed convex set in . Let be the set of optimal solutions of problem (3). Our assumptions will guarantee that When the risk measure is estimated based on a sample, then the optimal value becomes an estimator itself.

In our study, we intend to pursue the analysis of vector-valued composite functionals with the use of various estimators beyond empirical ones and to provide analysis that are novel also for the univariate case. The need to introduce vector-valued functionals arises in several contexts. First, in the context of investment decisions, we may want to compare the riskiness of two different investment portfolios based on observed data, which may or may not come from the same basket of securities. Furthermore, we may need to compare the risk of the two portfolios with respect to several measures of risk, which reflect the preferences of multiple investors. A very important case, when we need to use vector-valued risk functionals is when evaluating and optimizing a complex stochastic system. In these situations, we deal with systemic risk, which is very essential in both financial as well as engineering, logistics, medical, and many other problems. In those applications, the decision maker deals with complex distributed systems, where each component (unit, or agent) has its own risk of operation. It is well-known that the risk is not additive and various risk aggregation methods are suggested in the literature to reflect the risk of the entire system; the latter is termed systemic risk. Most practical approaches to systemic risk evaluation are based on (weighted) linear or nonlinear aggregations of risks of the system’s components. The decision problems optimizing such complex distributed systems incorporate measures of risk for each agent (unit), as well as a measure of systemic risk associated with a common task, integrity of the system, etc. In [1], these aggregation methods are discussed and it is shown that they are in-line with an axiomatic foundation of high-dimensional risks. The statistical evaluation of the systemic risk as well as the need to work with more than one measure of risk leads to the vector-valued setting, which we discuss in this work.

Given the observations of our earlier work [2, 3], we aim at analyzing the properties of the smoothed estimators, as well as the mixed smoothed and empirical ones, at a deeper level and address some of the nested expected value functionals for the vector-valued case. In this paper, we establish central limit formulae which are novel for smoothed and mixed estimators for both scalar-valued and vector-valued composite functionals. We underline that our setting has the flexibility to employ also other estimators across different layers using the entire sample; our findings are not tied to a single estimator. Smoothing is a widely used technique both in the context of statistical estimation as well as in the context of randomized optimization methods (e.g., [6], [8]). We have also shown that smoothing has the potential for bias reduction in stochastic optimization ([2, 3]). The results in this paper may further the convergence analysis of such techniques.

Finally, we apply our technique and results to compare differences in risk measures and estimate systemic risk in various forms.

Our paper is organized as follows. Section 2 introduces the foundational framework and presents an overview of the existing univariate central limit theorems pertaining to empirical estimators for composite risk functionals. We also define the notion of strong approximate identity, which is germane to the analysis of the smoothed estimators. We pay particular attention to the kernel estimators. Section 3 contains a central limit formula for general smoothed estimators of scalar-valued composite risk functionals, which is based on verifiable assumptions without assuming the boundedness of the functions involved, or non-negativity of the smoothing measures. Additionally, we show that the kernel estimators represent a strong approximate identity under very mild conditions. We further extend these results to vector-valued composite risk functionals and examine two compelling applications. Section 5 contains the results of our simulation study, which compares the kernel estimator against the empirical estimator to gauge the precision of our approximation. Finally, Section 6 summarizes our conclusions.

2 Framework and Preliminaries

Let be the set of all probability measures on the set . The following functions and sets will play a role in our discussion. For a measure , we define

| (4) | ||||

If , i.e., the expectation is exact, not approximated by using measure , then the superscript will be omitted. Notably, different estimators could be employed across different layers. These encompass not only empirical or various smoothed estimators but also their amalgamation to yield more refined estimation results. The composite risk function is expressed through a combination of multiple estimators, as follows:

| (5) |

Here, denotes a set of distinct estimators of the respective expected values across various layers. We shall denote the convergence in distribution by the symbol

We fix compact sets such that , , and , where stands for the interior of Without loss of generality, we assume that , are convex sets. We define the space:

where is the space of -valued continuous function on , equipped with the supremum norm. The space is equipped with the product norm. We set and . Let the vector-valued function have block coordinates , , and . Similarly, we define with block coordinates , , and .

Recall that a function is Hadamard-directionally differentiable at a point in a direction if for all sequences and such that and , , the limit

exists and is well-defined. Compositions of Hadamard-directionally differentiable functions are Hadamard-directionally differentiable. In our setting for every direction , we define recursively the sequence of vectors:

| (6) |

A Central Limit Theorem for the plug-in estimator of a univariate composite risk functional is proved in [4]. For the risk-averse optimization problem of form (3), the counterpart central limit formula is established in [4, Theorem 3] assuming that only empirical estimators are used.

We pay special attention to estimators that are obtained by convolution of the empirical measure with a measure . One of our goals is to obtain a central limit formula for this type of estimators when they are used in compositions.

A comprehensive examination of the asymptotic behavior of smoothed empirical processes is available in [25], [29], and [30]. Thorough explorations of the one-dimensional functional central limit theorem for smoothed empirical processes, assuming a uniformly bounded class of functions or invariance under translation (which in turn implies uniform boundedness) are extensively covered in [7], [12], and [17]. The requirement of uniform boundedness is relaxed in [9] and [20] by assumptions about the entropy and the tail behavior for smoothed estimators. These assumptions are quite involved in may not be easy to verify. In our context, we need to further propagate the relevant properties through the compositions which form the risk functionals. To resolve these issues, we offer sufficient conditions, which are verifiable and allow for the extension of the analysis to vector-valued composite stochastic optimization problems. Our starting point is our earlier work [3], where we have considered several smoothed estimators for the composite risk functionals and have shown their consistency under relatively mild assumptions.

We choose a sequence of measure , which are independent of the empirical measure , and throughout the entire paper, we assume that all measures are normalized, i.e. . The following notion will be used.

Definition 2.1.

The sequence of measures is called a proper approximate convolutional identity of order , if it converges weakly to the point mass when and the integrals are finite for all .

The kernel estimators of the following form constitute a special case:

where is a -dimensional density function with respect to the Lebesgue measure and is a smoothing parameter such that . We have . The estimators may take a more general form than the kernel estimator just defined for illustration (cf. [24, 13]). When using kernels, we shall assume the following properties.

-

(k1)

The kernel of order is a density function with respect to the Lebesgue measure satisfying the symmetry condition for , with being the largest integer smaller than

-

(k2)

The -th order moment of the kernel: , is finite.

For illustration, in the case of , we deal with a functional with two layers. We could use the empirical estimator as in the outer layer and a kernel estimator as in the inner layer. In that case, the two-layer estimation based on a finite sample of size and is represented as follows:

In order to avoid cluttering the notation, we shall omit the area of the integration when it does not lead to ambiguity. We shall denote the index set and the set shall contain all indices of the composition level, where smoothing is applied. We use the notation for the estimator, in which for and for

3 Central limit theorems for mixed smoothed and empirical estimators

3.1 Scalar-valued composite risk functionals

In this section, we establish a central limit theorem for univariate composite risk functionals and their optimized version. We define the following sets of continuous functions associated with the risk functional (1):

The associated envelope functions is given by

Due to the compactness of , the functions , are well-defined and they are also measurable ([23, Theorem 7.42]). We do not assume is a translation invariant class, which is a common assumption in the literature ([25],[11] and [29]) because this assumption automatically implies that is uniformly bounded, which would limit substantially the intended application of our results.

We recall the notions of covering and bracketing numbers. The covering number is the minimal number of balls of radius needed to cover the set .

Given two functions and , the bracket is the set of all functions with . An -bracket is a bracket with . The bracketing number is the minimum number of -brackets needed to cover .

Suppose that the envelope functions satisfy for Then the classes , have finite bracketing numbers for all . This implies that is a -Glinvenko-Cantelli class, i.e.

| (7) |

We propose the following central limit theorem for smoothed composite vector-valued functions and provide more details for its covariance.

Theorem 3.1.

Suppose an index set is fixed, , and the following conditions are satisfied:

-

(a1)

The sequence of normalized measures converges weakly to the point mass at zero.

-

(a2)

For all , is finite and for all and , is finite.

-

(a3)

Functions , with a finite norm exists such that for all and all

-

(a4)

The following two conditions are satisfied for all :

(8) (9) -

(a5)

The functions , are Hadamard directional differentiable for all and for their directional derivatives are -integrable for all directions .

Then , where is zero-mean Brownian process on . Here is a Brownian process of dimension on , , and is an -dimensional normal vector. The covariance function of has the following form:

| (10) |

Proof.

We shall show that the classes with have uniformly integrable entropy. To this end, it is sufficient to show that for some constant and all , the following bound holds:

Here the supremum is taken over all finitely discrete probability measures on such that

Using assumption (a3), we observe that for any norm such that , the following bound hold:

| (11) |

where denotes the minimal number of balls with radius that are necessary to cover . Indeed, let , with form an -net on , that is the closed balls with centers and radius cover . Then the brackets

cover , and they are of size at most . According to Lemma 2.7.8 in [26], there is an universal bound for the logarithm of the covering number of all compact convex subsets of given by with a constant , which depend only on the volume and dimension of . Furthermore, since the covering numbers are smaller than the bracketing numbers, we have

This shows that the functions in have uniformly integrable entropy. This together with conditions (a1), (a2) and (a4) implies that the assumptions of [21, Theorem 2.2] are satisfied. Note that we do not require to be included in as in [21, Theorem 2.2] because (a2) insures the necessary integrability. Hence, the class of functions is - Donsker. The classes with are -Donsker due to assumption (a3). This entails that

where , is a standard Brownian process with zero-mean and covariance function

| (12) |

We define a subset of the space containing all elements for which

, .

Further, we define the operator as follows

Consider the perturbation function as follows: its -th component is given by

| (13) |

We define the functional by setting

The Hadamard-directional differentiability of at is needed in order to apply the delta method.

Note that is an element of and it is also an interior point of due to assumption (a3). The perturbations are in the space as well. We need them to be Hadamard-directionally differentiable. To this end, we only need consider the components with index and observe that it is sufficient to argue that is Hadamard-directionally differentiable. Using the definition, we have

We could take the limit under the integral by virtue of the Lebesgue dominated convergence theorem due to assumption (a2). The integral on the right hand side is finite by virtue of assumption (a5).

An explicit formula of the Hadamard-differentiable derivative can be derived as follows. Consider and . For , . Then if , , we have

| (14) |

The chain rule entails that . This fact allows us to use the delta theorem presented in [19] to transfer the convergence of to the convergence of . The Delta Theorem [19], the Donsker property, and the Hadamard directional differentiability of at imply that

| (15) |

The covariance structure (10) of follows directly from (12). ∎

Relations 8 and 9 in Theorem 3.1 play a crucial role in obtaining a central limit theorem. We provide a sufficient condition that may be easier to verify in the context of composite functionals. To this end, we introduce the following notion.

Definition 3.2.

We call a proper approximate convolution identity a strong approximate identity of order , if

| (16) |

Observe that when (16) is satisfied, then [27, Definition 6.8 (i)] implies that converges to in the sense of the mass transportation distance of order . However, (16) provides also a rate for that convergence.

Theorem 3.3.

Proof.

First, we shall show that (9) holds. Using the growth condition and the Jensen’s inequality, we obtain

| (18) | ||||

The term on the right-hand side of equation (18) converges to zero due to (16), which proves (9). To prove (8), we proceed in a similar way.

| (19) | ||||

We have already proved that the maximum converges to zero. Since is continuous, we infer that the right-hand side of (19) converges to zero. Consequently, (8) holds as well. ∎

We obtain more handy conditions when we use the usually kernels smoothing in stochastic optimization. We can state the following result.

Theorem 3.4.

Suppose conditions (a3) and (a5) of Theorem 3.1 as well as the locally Lipschitz condition (17) are satisfied. Let a symmetric kernel with finite moment be given such that (k1)-(k2) as well as the following conditions are satisfied:

-

(s1a)

The integrals are finite for all and for any .

-

(s2b)

The smoothing parameter satisfies

Then the result of Theorem 3.1 holds when .

Proof.

We substitute by and augment the function defined in the proof of Theorem 3.1 accordingly. To verify the assumptions of Theorem 3.1 , we notice that assumption (s1a) and the definition of the kernel imply (a1) and (a2). We only have to verify conditions (a4). Using Theorem 3.3, it is sufficient to verify conditions

We see that

Since the kernel has finite moment, , assumption (s2b) implies the desired convergence. Therefore, Theorem 3.1 applicable and yields the result. ∎

Notice that the smooth estimator and kernel estimator have the same asymptotic distribution.

Popular measures of risk are the mean semi-deviation measures. We shall verify (a3) in the Theorem 3.1 and the local Lipschitz condition (17) in Theorem 3.3. Consider the case when small values are preferred, e.g. the random variable represents losses.

where and . In this case,

The function satisfies the (a3) if we assume there is an upper bound of set , which is a compact set

The functions evidently satisfy the local Lipschitz condition and also meet the requirements of condition (a3) when has sufficiently high moments. We only need to analyze the function . When , the function has a global Lipschitz constant of 1 with respect to both variables. Consider the case of . Then the function is continuously differentiable, and we obtain the following.

Here, is a constant associated with the compact set . Similarly, we can verify (a3) for . We have

Here is the diameter of the set When the random variable has sufficiently high moments, the function would have finite norm and assumption (a3) will be satisfied as well.

4 Central limit theorem for vector-valued composite functionals

We proceed to establish a more general form of the central limit theorem, extending its applicability to situations involving aggregation of risk measure, which is necessary in evaluation of systemic risk for distributed systems. Let us assume that we deal with a system of agents (components). We consider the random vector comprising the random losses of the agents, i.e., the component represents the random loss of agent . When assessing the total risk of the system, two primary approaches are known in literature. The first approach involves selecting a univariate risk measure and applying it to a function , which aggregates the outcomes of the agents. Our results are applicable to this case, as we only need to include the aggregation function in the composition. This approach to systemic risk is applicable when not proprietary information or privacy concerns for the individual agents are present. The second approach evaluates the total risk by recording the risk evaluation of the individual agents and subsequently aggregating the obtained values. This approach requires handling multiple risk measures at once and estimating their aggregation. The goal of this section is to address this situation.

Let , and the probability space is defined by using a vector such that as a probability mass function on and as the collection of all subsets of . We assume that a set of univariate risk measures are used to evaluate the risk of each agent (or system component). There are several ways to aggregate the risk evaluations , . We could use an aggregation function to this end, where the simplest aggregation would be a linear scalarization, i.e., the total risk would be given by

for the vector in the simplex of . In financial literature, it is assumed that is non-linear function with monotonicity, possibly convexity, and other properties. Alternatively, we may apply a more complex aggregation as follows. We define the random variable on the space be setting:

Choosing a scalar measure of risk , we define the measure of the total risk (systemic risk) as follows:

This measure was proposed in [1], where it was established that it satisfies postulated axioms for systemic measures. Notice that becomes equal to when on the probability space Hence, can represent both linear and nonlinear aggregations of . To address the statistical estimation of the systemic risk, we shall establish a Central Limit Theorem for vector-valued composite functionals. We shall show how it applies to the systemic risk estimation in due course.

For the sake of generality, we shall consider the case of random vectors with realization in , , which may be dependent. We define a random vector where containing all vectors stacked, i.e., and . We define composite risk functionals as follows:

| (20) |

where for . For , we define , and . Similarly to the univariate case, we define for the following:

Assume for a moment a common nesting order , we shall show later that this can always be achieved with no loss of generality. We define functions in the following way

So that, where and where . Then we have the multiple composite risk functional

| (21) |

Note that . The following quantities become relevant

Hence by construction. We redefine the collection of functions to include all the functions involved.

| (22) | ||||

We now state the central limit theorem of mixed smoothed and empirical estimators for the scalar-valued composite risk functional defined as above.

Theorem 4.1.

Suppose a sequence of smoothing measures on is given and an index set is fixed. If the conditions of Theorem 3.1 are satisfied for , for all functions involved in the definition of (21), and for the envelope functions of the classes (22), then

where is a zero-mean Brownian bridge with being an -dimensional zero-mean Brownian bridge, is a zero mean Brownian bridge of dimension , and

| (23) | ||||

The covariance function is given by

Additionally, if all functions are differentiable for all values of their last argument, then has the normal distribution where is the covariance of , and

Here denotes the Jacobian of with respect to the first argument calculated at

Proof.

Each functional is a composition of functions , and . We note that the value of does not change if the composition of functions continued beyond by composition with the identity function. One can compose with the identity any number of times without changing the form or value of the resulting risk measure. Hence, without loss of generality, we may assume that is a common number for all risk functionals , . Otherwise we may set and relabel the indices, redefining the functions as so that is the identity function for all , . The statement (i) follows immediately from Theorem 3.1.

Now consider the differentiable case. In the construction of , we obtain

Proceeding the same way, we get

Substituting the random vector in place of the direction we obtain the following expression for the limiting distribution,

| (24) |

where the matrices are defined as stated. Relation (24) implies so that the variance is given by ∎

We observe that if the functions with satisfy the Lipschitz conditions (17), then condition (b2) is satisfied.

Corollary 4.2.

Proof.

∎

4.1 Central limit theorem for sample-based stochastic optimization

In this section, we return to the kernel-smoothed estimator of the optimal value of a composite optimization problem. Recall the formulation of the associated composite optimization problems.

| (25) |

where is a m-dimensional random vector; is a closed convex set in and the function , with , and are continuous. We shall assume that problem (25) is solvable and has a unique optimal solution denote . We fix a sufficiently large compact set such that Further, we again fix compact sets such that , , and , where stands for the interior of Without loss of generality, we assume that and , are convex sets.

Our first goal is to show a central limit formulae for the optimal value of problem (25) which used mixed smooth and empirical estimators and in a second step, we shall specialize the statement when the smoothing uses the same kernel. We shall follow a similar line of proofs with slightly modified definitions of the auxiliary objects. Analogous functions are defined as:

| (26) |

The vector function is defined on be setting

We modify the classes of functions as follows:

The associated envelope functions is given by

Due to the compactness of , the functions , are well-defined and measurable ([23, Theorem 7.42]). The space is now defined as follows:

where is the space of -valued continuous function on , which is continuous with respect to the first component and continuously differentiable with respect to the second component. We denote the Jacobian of with respect to the second argument calculated at by . For every direction , we define recursively the following elements:

| (27) |

Suppose an index set is fixed to determine the layers at which we shall apply smoothing.

Theorem 4.3.

Suppose assumptions (a1)-(a2) of Theorem 3.1 is satisfied and additionally the following conditions hold.

-

(b1)

Functions , with a finite norm exists such that for all and all

-

(b2)

The following two conditions are satisfied for all :

(28) (29) -

(b3)

The functions , are continuously differentiable for every . Moreover, their derivatives are continuous with respect to the first two arguments and is uniformly bounded by a -integrable function

Then where is zero-mean Brownian process on . The covariance function of has the following form:

| (30) | ||||

Proof.

We start from the function .

| (31) |

The function is defined as We observe again that all assumptions - of Theorem 3.1 are satisfied if we consider the pair instead of . Hence, we infer

where is a standard Brownian process with zero-mean and covariance function

We define the operator as follows

and consider the optimal value of the parametric problem

When , we have . When , we have These facts allow us to use the infinite-dimensional delta theorem in [19] to transfer the convergence of to the convergence of provided that we verify the Hadamard directional differentiability of the optimal value function at . To this end, we use the Theorem 4.13 in [22], which implies that the optimal value function is Fréchet differentiable. Denoting its derivative by , we infer the Hadamard directional differentiability of at in every direction with

The remaining part of the proof is the same as the proof of Theorem 3.1. ∎

Notice that if the functions with satisfy the Lipschitz conditions (17), then condition (b2) is satisfied.

Consider now smoothing my kernels. The following result may be proved in an analogous way as Theorem 4.3.

Corollary 4.4.

Proof.

For stochastic problem, we introduce a portfolio optimization problem where the random returns of the securities are represented by a random vector . The portfolio itself is characterized by a vector , which denotes the allocation of the available capital across the securities. The objective is to address the mean-semideviation optimization problem for potential losses. The problem is formulated as follows:

where and . In this case,

To verify the locally Lipschitz condition, has a modulus of continuity , where is the maximum of the norm of . Specifically, we have

where the last inequality follows from the Cauchy-Schwarz inequality. The same verification applies to in a similar manner. The remaining verifications follow the same process as the previous example.

5 Application

5.1 Risk measures representable as optimal value of an optimization problem

Now we discuss the special case of two-level composite stochastic optimization

This structure appears when we evaluate the Average (Conditional) Value-at-Risk or higher order measures of risk. Recall that higher order risk measure with is defined as follows ([14, 5]:

| (32) |

We represent this measure as a the optimal value of a composite functional by setting:

For and , the optimization problem on the right-hand side of (32) has a unique solution, which we denote by . In that case, we can select a compact set sufficiently large to contain the point For , we do not need a composition; the problem reduces to the optimization of the expected value of a convex function as well as the case in this paper specialized to one layer.

Consider the estimators based on a proper approximate identity and on a kernel , respectively.

Following the same technique, we define the functions:

The mapping , where the operator , and the space is equipped with product norm of the Euclidean norm on and supremum norm of . The functional is defined , where . It is easy to see that , and . We denote the set of optimal solutions in (5.1) as . The class for this setting is defined as .

Corollary 5.1.

Suppose the conditions (a1)-(a4) of Theorem 3.1 are satisfied and additionally is differentiable for all , and both and its derivative w.r.t. the second argument are continuous w.r.t. both arguments. Then

where is a zero-mean Brownian process on with covariance function

Moreover, if the optimal solution set contains only one element , then

where is a zero-mean normal vector with covariance

The proof follows the same line of arguments as the proof of Theorem 4.3 and it is omitted.

Corollary 5.2.

Suppose the conditions (a1)-(a4) of Theorem 3.1 are satisfied, additionally is differentiable for all , and both and its derivative w.r.t. the second argument are continuous w.r.t. both arguments and as well as the locally Lipschitz condition (17) are satisfied for . Let the symmetric kernel satisfy (k1)-(k2) and (s1)–(s2). Then the conclusions of Corollary 5.1 are satisfied for .

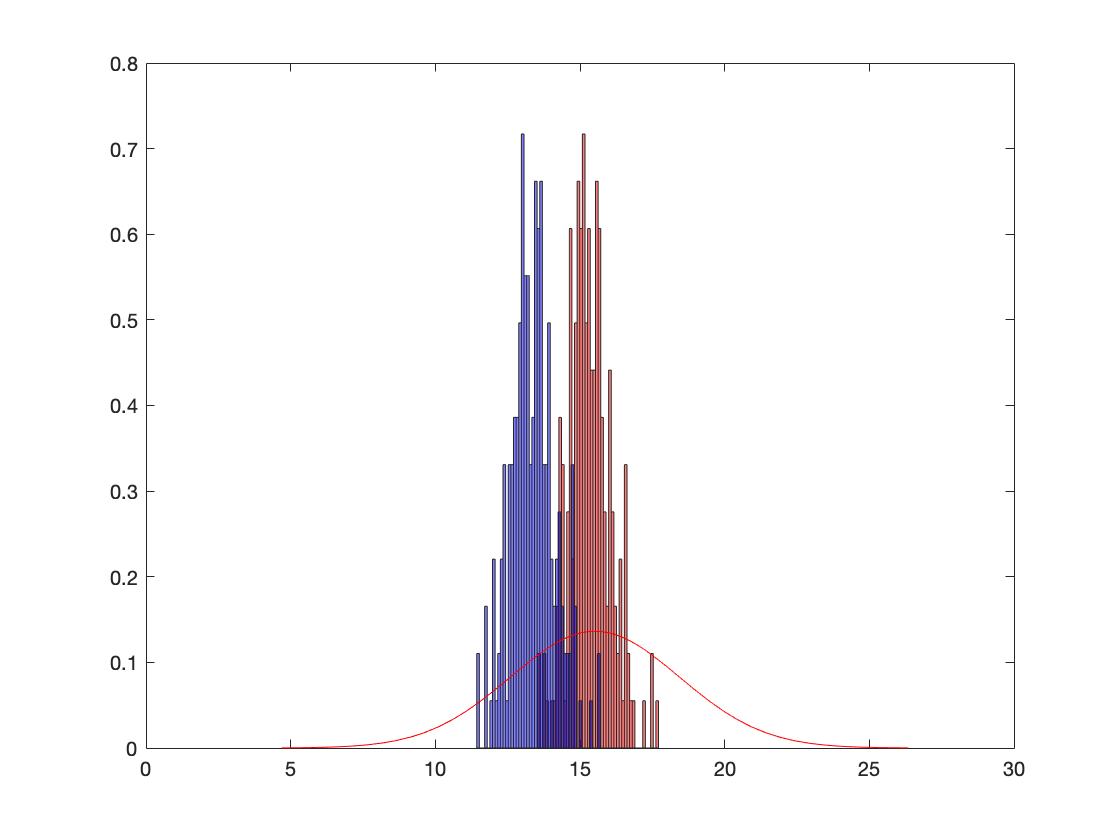

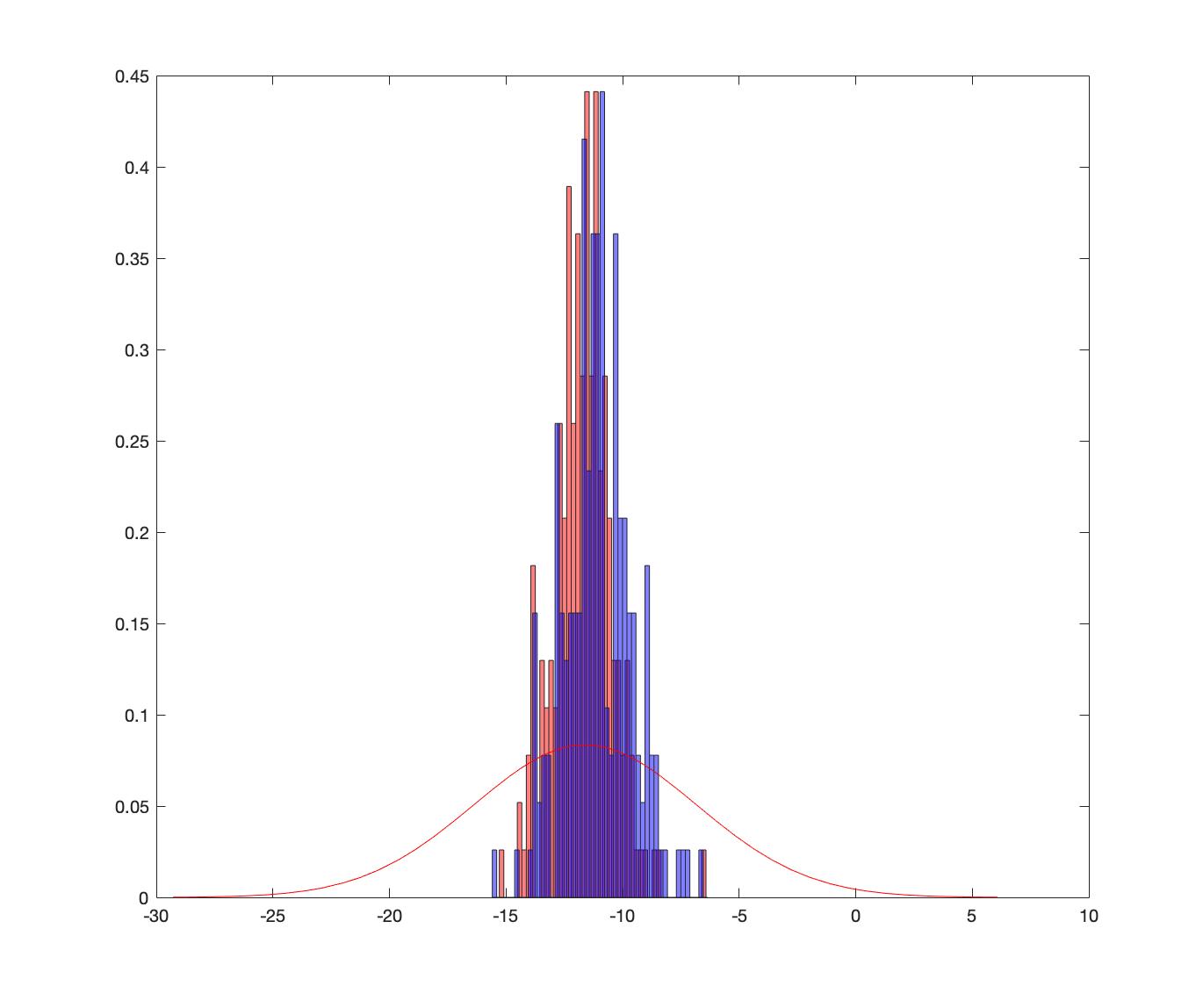

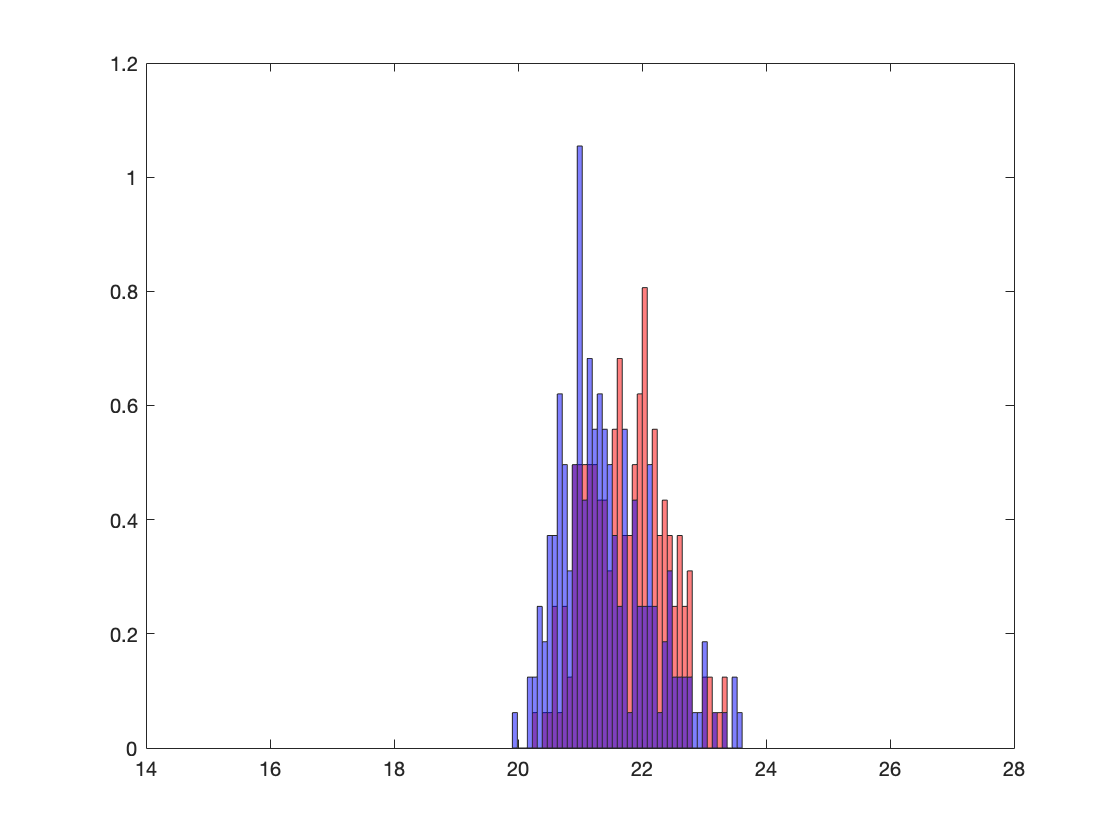

In our numerical experiments, we have used the higher-order inverse risk measure as defined in (32) with parameters and . We take independent identically distributed observations from an independent identically distributed observations. The theoretical minimum is attained at resulting in the risk value . We consider the uniform kernel estimation with support on .

The estimators for sample size are evaluated by replications. which comes

where is a standard normal random variable with zero and variance

We use the bandwidth calculated according to the formula , where is the estimated standard deviation of the data. As the sample size increases, both the empirical estimator (blue) and the uniform kernel estimator (red) progressively converge towards the true standard Brownian process depicted by the solid red curve. It is worth noting that the uniform kernel estimator exhibits less bias compared to the empirical estimator. This is our motivation to consider this type of estimate as frequently in practice, obtaining data is costly and we need to work with small samples.

5.2 Comparison of two risk measures

Within the following two subsections, we present two primary applications of the Multivariate Central Limit Theorem (CLT) for smoothed estimators. Initially, we delve into the comparative analysis of two portfolios, denoted as and , even if their independence is not assured. This scrutiny aims to discern the relative levels of risk attributed to each portfolio while employing a consistent measure of risk derived from sample-based approximations. Subsequently, we turn our attention to a unified portfolio and try to elucidate disparities arising from the utilization of distinct risk measures.

First, we consider the difference in risk for two variables. Let and be random variables in , not necessarily independent. Let , and let and be available random samples of size and , respectively. We consider a composite risk functional defined in (21) and such that the assumptions of Theorem 4.1 are satisfied. Recall

| (33) |

We introduce additional function , defined as follows: and observe that Theorem 3.1 implies for

| (34) |

This allows us to conduction statistical comparison for the two measures of risk.

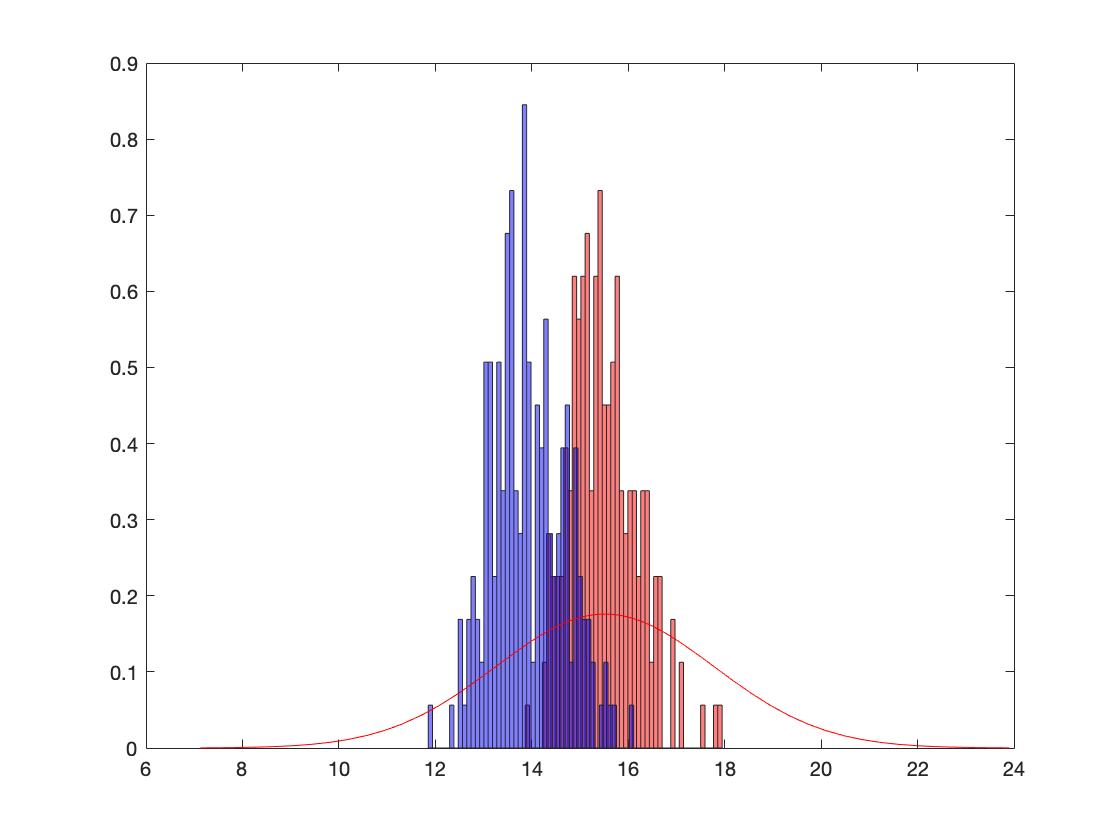

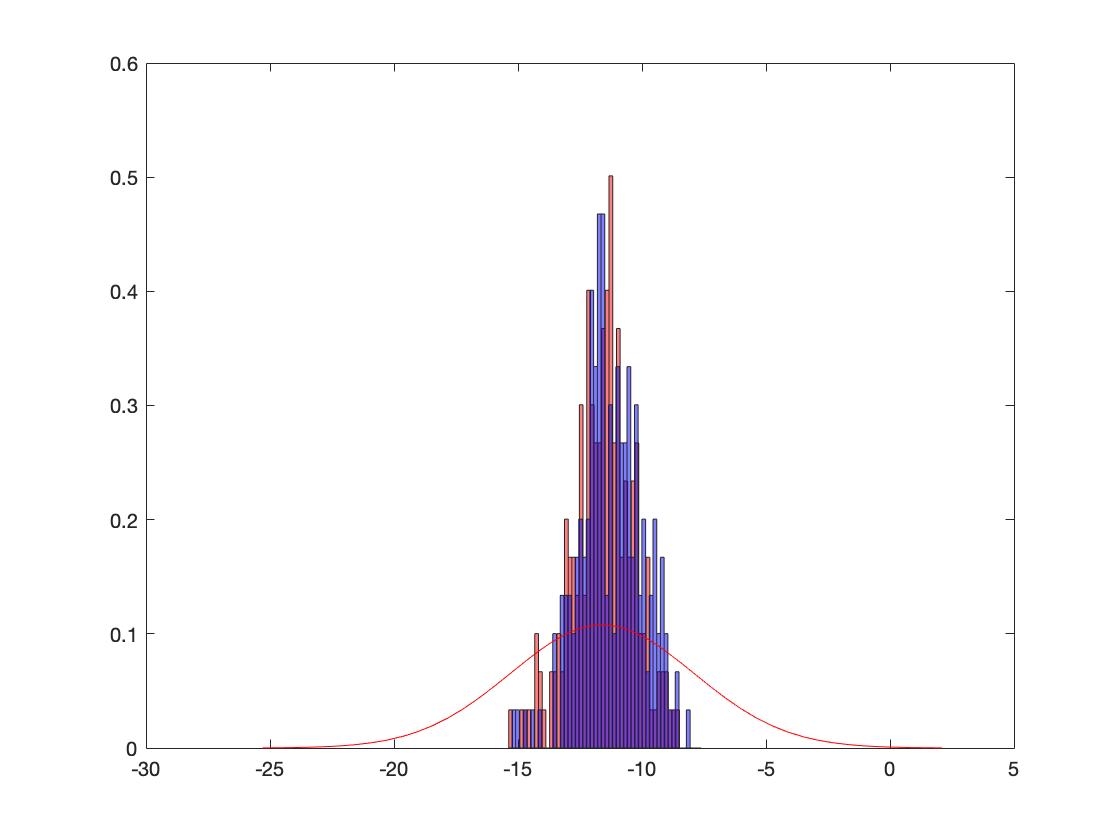

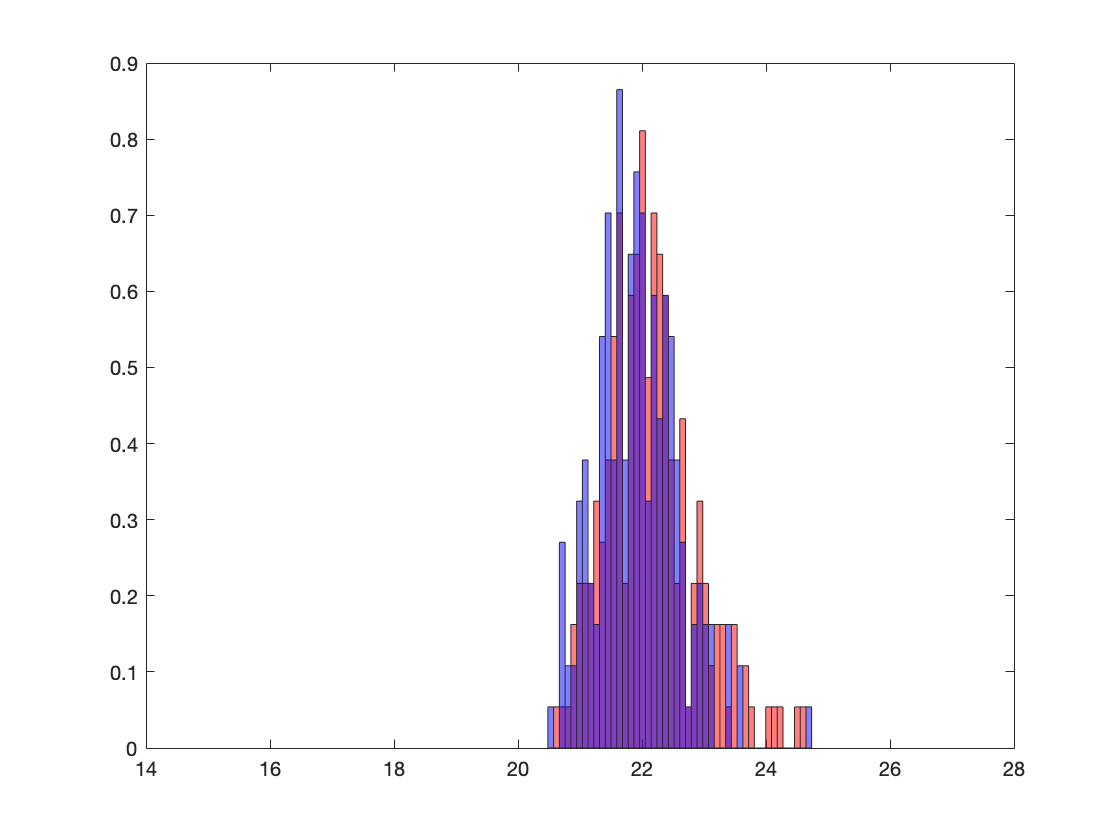

In our numerical experiments, we consider independent identically distributed observations from a normal distribution . In the model (32), we set the parameters as and and compare , where has the normal distribution . The difference in the risk values is given by . The histogram is overlaid on the distribution , see in Figure 2.

It has been observed that as both and increase, the resulting outcome becomes increasingly closer to the theoretical distribution. The simulation study’s findings indicate that, even when dealing with limited sample data in a vector-valued scenario, the uniform kernel estimator outperforms the empirical estimator in terms of accuracy. We use the same sample to estimate the risk with the smooth estimator and empirical estimator, aiming to address the challenge of limited sample size and enhance the quality of our estimation.

We also note that in the same way, we could compare two distinct risk measures should this be desired.

5.3 Central Limit Theorem for Systemic Risk

Our study offers insights into addressing the issue of evaluating risk for a complex distributed system. Each individual risk is given by the following composite form:

| (35) |

If the systemic risk is evaluated by a nonlinear aggregation function , we define the total risk as follows:

| (36) |

Here the functions are defined as in section 4. Hence, we obtain the following statement.

Corollary 5.3.

Assume that the conditions of Theorem 4.1 are satisfied and the function is Hadamard directionally differentiable, then the systemic risk satisfies the following central limit formula:

If the aggregation is obtained via an outer coherent risk measure as described in section 4, then we can observe that we can evaluate directly with additional composition since we have a finite probability space . We can illustrate this point by using the mean semi-deviation of order as the outer risk measure. Let . Thus, we have

where is a fixed parameter. The following statement holds for the systemic measure of risk obtained in this way.

Theorem 5.4.

Assume that the conditions of Theorem 4.1 are satisfied and the outer risk measure in the definition of is coherent, then the systemic risk satisfies the following central limit formula:

| (37) |

Proof.

Denoting , we observe that the random variables with realizations , converges point-wise to the random variable with the speed of Since every coherent measure of risk is convex with respect to its argument, it is also Hadamard directionally differentiable. We obtain that

We use the form of the directional derivative in direction of a coherent measure of risk. It is given by the Hence, we obtain the form of the limiting distribution as in (37). ∎

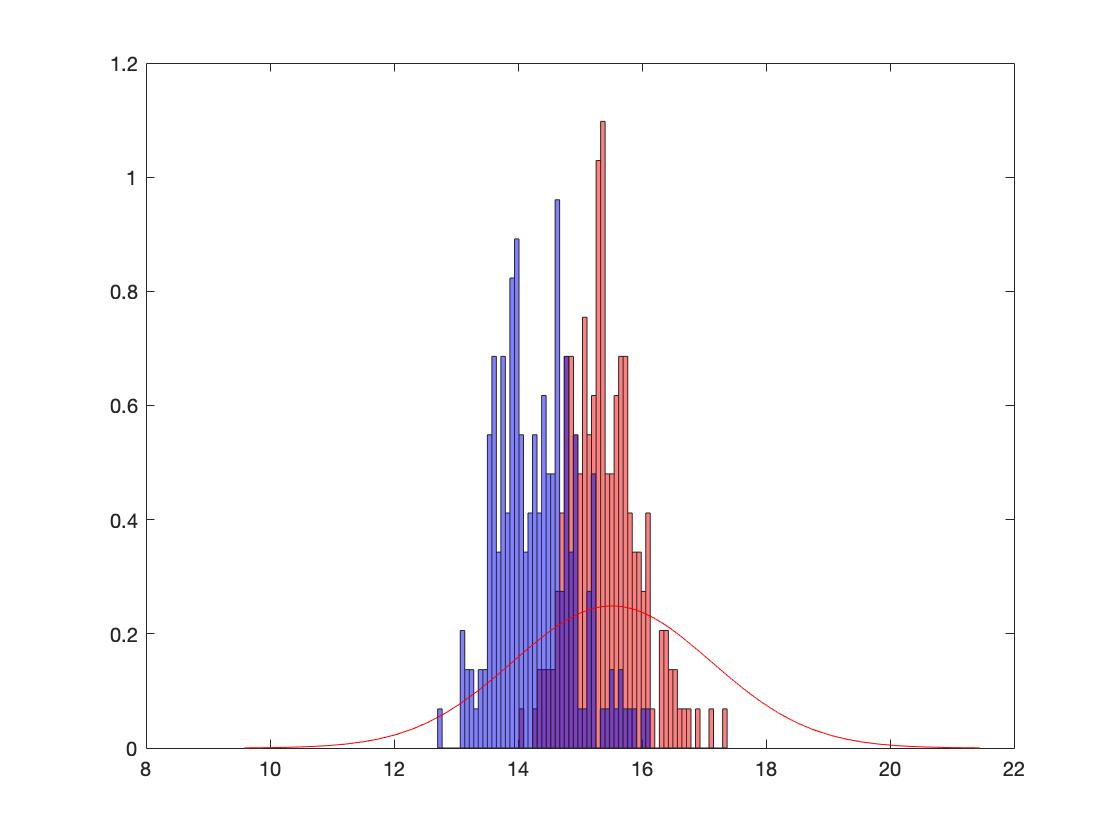

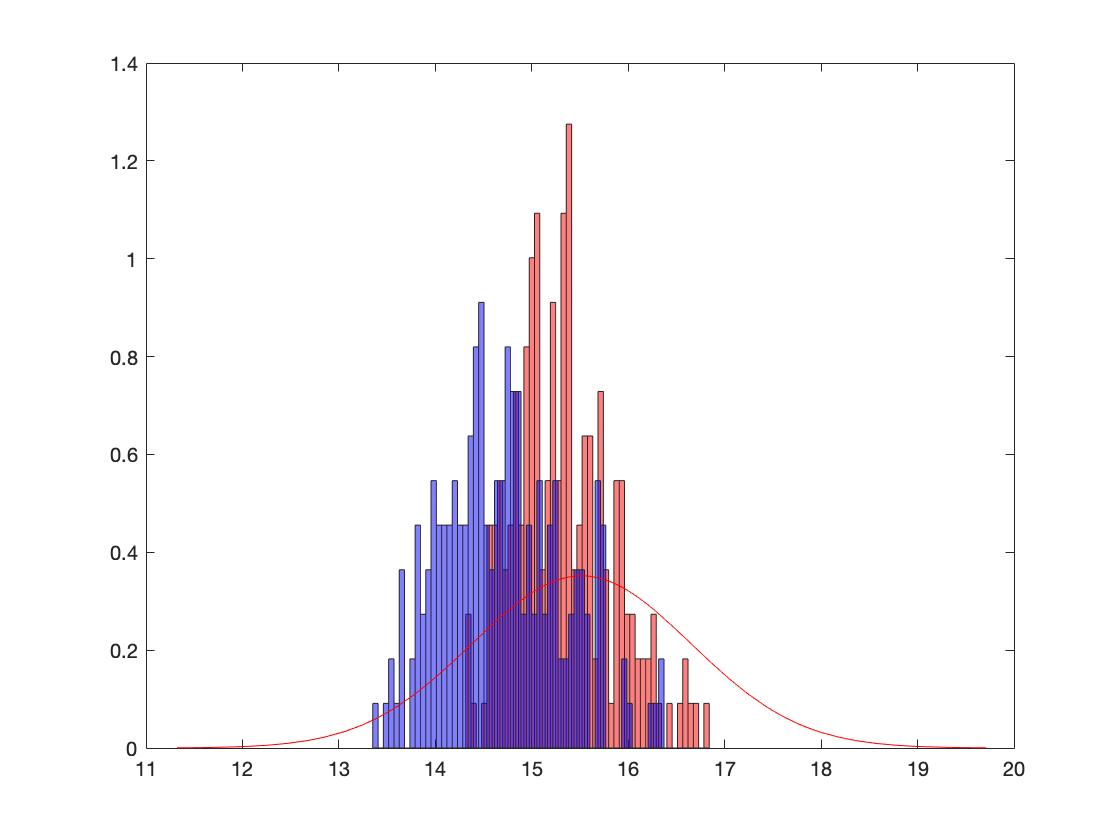

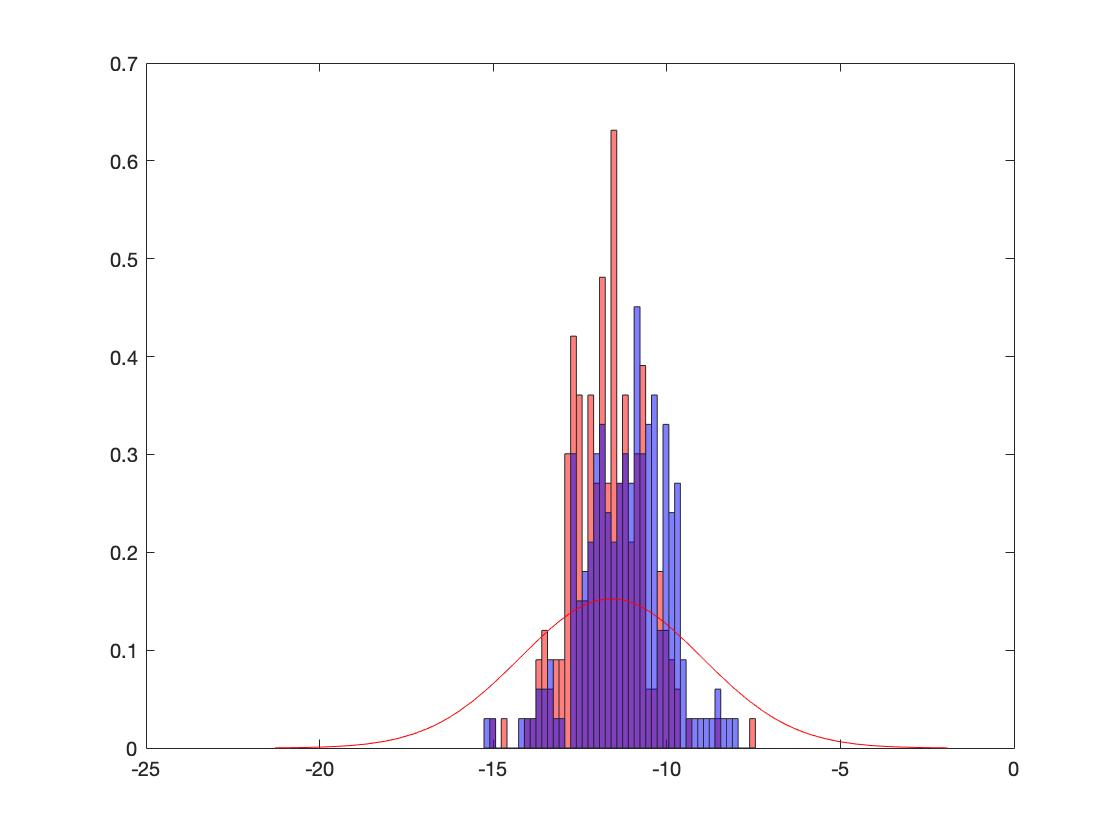

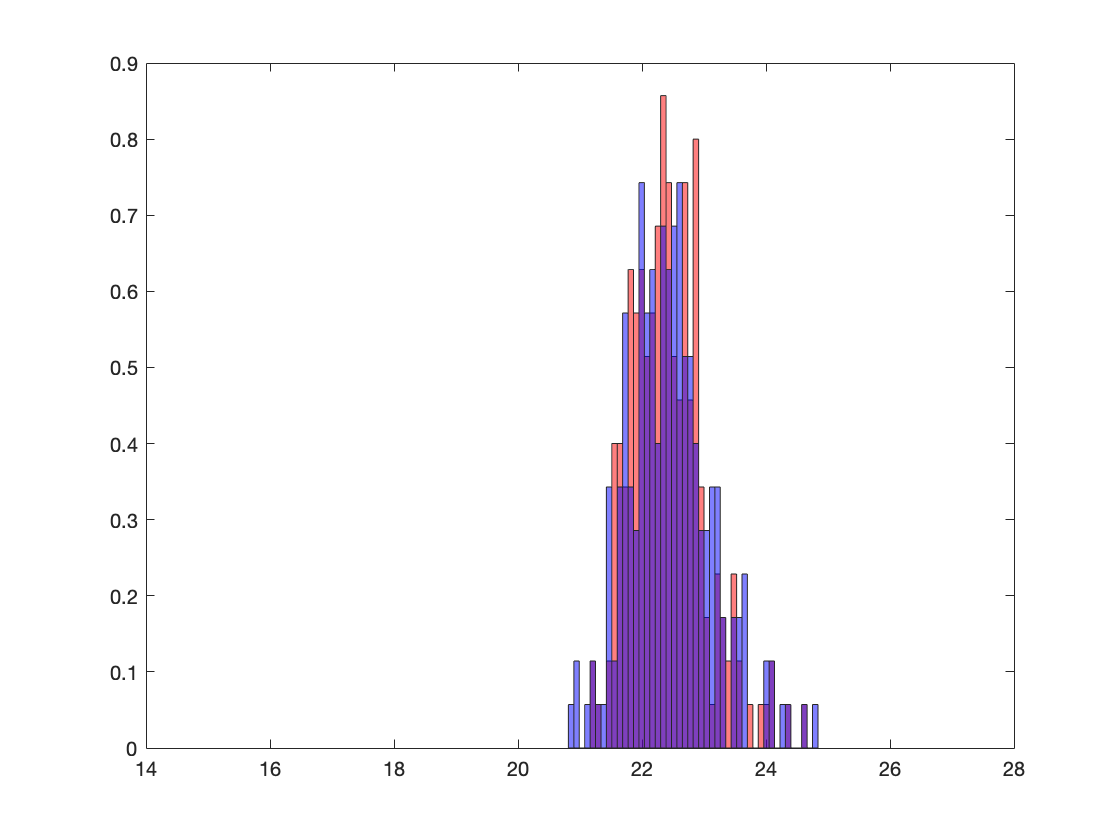

In accordance with the numerical experiment setup described in Subsections 5.1 and 5.2, we proceed by employing the mean semi-deviation of order as the outer risk measure. Specifically, let , where and . For the parameters , , and , we compute to be approximately . By comparing the empirical and uniform kernel estimators, we can derive the following asymptotic behavior: It is observed that the smooth estimator exhibits less bias, with its mean value closer to , compared to the empirical estimator when the outer mean semi-deviation risk measure is applied.

6 Conclusions

In conclusion, our paper makes significant contributions in several key areas. We introduce a novel central limit theorem for composite risk functionals that incorporate mixed estimators, encompassing both smoothing and empirical methods. Additionally, we extend our analysis to multi-variate measures, providing insights into the verification of assumptions crucial for the central limit formulae. This extension proves valuable for the statistical estimation of systemic risk as well as in the context of statistical tests aimed at comparing levels of riskiness. Furthermore, we specialize our central limit theorem to the application of kernel estimator showing conditions for the bandwidth behavior. Our simulation study demonstrates that the adoption of a smooth estimator yields reduced bias compared to an empirical estimator, a trend observed across both univariate and multivariate scenarios, particularly in addressing challenges associated with small sample sizes.

References

- [1] Aray Almen and Darinka Dentcheva. On risk evaluation and control of distributed multi-agent systems. Journal of Optimization Theory and Applications, 2024.

- [2] Darinka Dentcheva and Yang Lin. Bias reduction in sample-based optimization. SIAM Journal on Optimization, 32(1):130–151, 2022.

- [3] Darinka Dentcheva, Yang Lin, and Spiridon Penev. Stability and sample-based approximations of composite stochastic optimization problems. Operations Research, 71(5):1871–1888, 2023.

- [4] Darinka Dentcheva, Spiridon Penev, and Andrzej Ruszczyński. Statistical estimation of composite risk functionals and risk optimization problems. Annals of the Institute of Statistical Mathematics, 69(4):737–760, 2017.

- [5] Darinka Dentcheva and Andrzej Ruszczyński. Optimization of Measures of Risk. Springer Nature Switzerland, Cham, 2024.

- [6] John C Duchi, Peter L Bartlett, and Martin J Wainwright. Randomized smoothing for stochastic optimization. SIAM Journal on Optimization, 22(2):674–701, 2012.

- [7] Uwe Einmahl and David M. Mason. Uniform in bandwidth consistency of kernel-type function estimators. The Annals of Statistics, 33(3):1380–1403, 2005.

- [8] Yuri M. Ermoliev, Vladimir I. Norkin, and Roger J-B. Wets. The minimization of semicontinuous functions: Mollifier subgradients. SIAM Journal on Control and Optimization, 33(1):149–167, 1995.

- [9] Peter Gaenssler, Daniel Rost, and Klaus Ziegler. On random measure processes with application to smoothed empirical processes. In Ernst Eberlein, Marjorie Hahn, and Michel Talagrand, editors, High Dimensional Probability, pages 93–102, Basel, 1998. Birkhäuser Basel.

- [10] Saeed Ghadimi, Andrzej Ruszczyński, and Mengdi Wang. A single timescale stochastic approximation method for nested stochastic optimization. SIAM Journal on Optimization, 30(1):960–979, 2020.

- [11] Evarist Giné and Richard Nickl. Uniform central limit theorems for kernel density estimators. Probability Theory and Related Fields, 141(3-4):333–387, 2008.

- [12] Evarist Giné and Richard Nickl. Uniform central limit theorems for kernel density estimators. Probability Theory and Related Fields, 141:333–387, 01 2008.

- [13] Evarist Giné and Richard Nickl. Cambridge Series in Statistical and Probabilistic Mathematics. Cambridge University Press, 2015.

- [14] PAVLO A. Krokhmal. Higher moment coherent risk measures. Quantitative Finance, 7(4):373–387, 2007.

- [15] Włodzimierz Ogryczak and Andrzej Ruszczyński. On consistency of stochastic dominance and mean–semideviation models. Mathematical Programming, 89(2):217–232, jan 2001.

- [16] WLodzimierz Ogryczak and Andrzej Ruszczynski. Dual stochastic dominance and related mean-risk models. SIAM Journal on Optimization, 13(1):60–78, jan 2002.

- [17] Dragan Radulovifá and Marten Wegkamp. Necessary and sufficient conditions for weak convergence of smoothed empirical processes. Statistics & Probability Letters, 61(3):321–336, 2003.

- [18] R.Tyrrell Rockafellar and Stanislav Uryasev. Conditional value-at-risk for general loss distributions. Journal of Banking & Finance, 26(7):1443–1471, 2002.

- [19] Werner Romisch. Encyclopedia of statistical sciences(2nd ed.), Wiley Online Library, 2th ed. edition, 2006.

- [20] Daniel Rost. Limit theorems for smoothed empirical processes. 01 2000.

- [21] Daniel Rost. Limit theorems for smoothed empirical processes. In Evarist Giné, David M. Mason, and Jon A. Wellner, editors, High Dimensional Probability II, pages 107–113, Boston, MA, 2000. Birkhäuser Boston.

- [22] Alexander Shapiro. Consistency of sample estimates of risk averse stochastic programming. Journal of Applied Probability, 50:533–541, 2013.

- [23] Alexander Shapiro, Darinka Dentcheva, and Andrzej Ruszczynski. Society for Industrial and Applied Mathematics, 2021.

- [24] Alexandre B Tsybakov. Springer series in statistics. Springer, Dordrecht, 2009.

- [25] Aad van der Vaart. Weak convergence of smoothed empirical processes. Scandinavian Journal of Statistics, 21(4):501–504, 1994.

- [26] AW van der Vaart and J. Wellner. Weak Convergence and Empirical Processes: With Applications to Statistics. Springer Series in Statistics. Springer, 1996.

- [27] Cédric Villani et al. Optimal transport: old and new, volume 338. Springer, 2009.

- [28] Mengdi Wang, Ji Liu, and Ethan X. Fang. Accelerating stochastic composition optimization. Advances in Neural Information Processing Systems, 21:1714–1722, 2016.

- [29] J. E. Yukich. Weak convergence of smoothed empirical processes. Scandinavian Journal of Statistics, 19(3):271–279, 1992.

- [30] J.E. Yukich. A note on limit theorems for perturbed empirical processes. Stochastic Processes and their Applications, 33(1):163–173, 1989.