mathx”17

Localized Exploration in Contextual Dynamic Pricing Achieves Dimension-Free Regret ††footnotetext: Author names are sorted alphabetically. Duan’s research is supported by an NSF grant DMS-2413812. Fan’s research is supported by NSF grants DMS-2210833 and DMS-2053832 and ONR grant N00014-22-1-2340. Wang’s research is supported by an NSF grant DMS-2210907 and a startup grant at Columbia University.

| Jinhang Chai† | Yaqi Duan⋄ | Jianqing Fan† | Kaizheng Wang∗ |

| Department of Operations Research and Financial Engineering |

| Princeton University† |

| Department of Technology, Operations and Statistics |

| Stern School of Business, New York University⋄ |

| Department of Industrial Engineering and Operations Research |

| Columbia University∗ |

January 7, 2025

Abstract

We study the problem of contextual dynamic pricing with a linear demand model. We propose a novel localized exploration-then-commit (LetC) algorithm which starts with a pure exploration stage, followed by a refinement stage that explores near the learned optimal pricing policy, and finally enters a pure exploitation stage. The algorithm is shown to achieve a minimax optimal, dimension-free regret bound when the time horizon exceeds a polynomial of the covariate dimension. Furthermore, we provide a general theoretical framework that encompasses the entire time spectrum, demonstrating how to balance exploration and exploitation when the horizon is limited. The analysis is powered by a novel critical inequality that depicts the exploration-exploitation trade-off in dynamic pricing, mirroring its existing counterpart for the bias-variance trade-off in regularized regression. Our theoretical results are validated by extensive experiments on synthetic and real-world data.

Keywords: Contextual Dynamic Pricing, Localized Exploration, Dimension-Free Regret, Exploration-Exploitation Trade-off, Critical Inequality

1 Introduction

In recent years, the rise of online sales platforms has transformed how sellers acquire and utilize customer data, such as demographics, purchasing history, and social media interactions. At the same time, market insights—such as industry trends, competitor behavior, and economic cycles—provide a broader understanding of the forces shaping the marketplace. By integrating these data streams and employing personalized pricing strategies, retailers can significantly enhance their profitability. This evolution has fueled a growing interest in contextual dynamic pricing, which sets optimal prices in real time based on sales data and various covariates.

In this work, we study contextual dynamic pricing under a linear demand model. To tackle the celebrated exploration-exploitation dilemma in decision-making, we propose a localized Explore-then-Commit (LetC) algorithm with three stages. The first one is a burn-in stage, where we perform pure exploration by alternating between two prices to obtain a pilot estimate of the demand model. This stage gains substantially statistical information but at the expenses of big revenue losses. The second stage conducts localized exploration, where we explore only near the learned optimal pricing policy. This new stage gains the statistical information at small losses of revenue. With a proper choice of localization, the benefit of statistical precision is shown to exceed the cost of revenue. Eventually, the parameters are learnt so precisely that we can fully deploy the optimal stragegy. The third and final stage simply deploys the optimal policy estimated from the collected data. Compared to popular Explore-then-Commit (ETC) pricing strategies (Javanmard & Nazerzadeh, , 2019; Ban & Keskin, , 2021; Fan et al., , 2022), our additional localized exploration stage refines the initial policy at a low cost and helps achieve a sharp regret bound.

Our contributions

Our main contributions are summarized as follows.

-

1.

We develop a novel three-stage algorithm for contextual dynamic pricing. Under a linear demand model, we offer clear guidelines for determining the lengths of each stage and the size of price perturbations for localized exploration.

-

2.

We prove a dimension-free regret bound for the algorithm with long horizons. Surprisingly, when the time horizon and the covariate dimension satisfy , the regret is at most of order . We also derive a matching minimax lower bound. The above statements only hide polylogarithmic factors in .

-

3.

We extend our theoretical framework to cover the entire spectrum of time, enabling a seamless transition from short to long horizons. To capture the exploration-exploitation trade-off in dynamic pricing, we introduce a critical inequality analogous to the existing one for bias-variance trade-off in penalized regression. The inequality identifies the optimal size of localized exploration.

Related works

Here, we give a selective review of related work in the literature. Dynamic pricing without covariates has been extensively studied over the past two decades (Broder & Rusmevichientong, , 2012; Besbes & Zeevi, , 2015; den Boer, , 2015; Wang et al., , 2021). Recently, there has a growing attention on how to incorporate contextual information in pricing. Nambiar et al., (2019); Chen & Gallego, (2021); Bu et al., (2022) studied demand models that involve general nonparametric functions of the covariate . The generality comes with the curse of dimension in regret. On the other hand, parametric and semi-parametric demand models can deal with high-dimensional covariates. A number of works in this direction assumed that the demand depends on the price and the covariate through a linear link function , where and are unknown coefficients. For instance, Qiang & Bayati, (2016) studied a linear demand model in a well-separated regime; Chen et al., (2022) considered a logit choice model in the offline setting; Javanmard & Nazerzadeh, (2019) worked on parametric binary choice models; Xu & Wang, (2022); Luo et al., (2024); Fan et al., (2022) investigated semi-parametric demand models.

Since the coefficient of the price does not depend on the covariate , the above models do not capture the heterogeneous price sensitivity in the population. To handle such challenge, Ban & Keskin, (2021) considered parametric demand models of the form , where is a known function and is a coefficient vector governing the influence of covariates on the price sensitivity. They considered the high-dimensional setting where is large, but and only have a small number of non-zero entries. They proposed a two-stage Explore-then-Commit algorithm that first alternates between two candidate prices to collect data and then deploys the optimal pricing policy based on the learned demand model. We consider the scenario where is the identity function, but the coefficients can be non-sparse. The result in Ban & Keskin, (2021) implies a regret bound of order , up to logarithmic factors. Our theory shows that under mild assumptions, one can achieve a dimension-free regret for large . Compared to the Explore-then-Commit algorithm, the significant improvement of our regret is due to an additional localized exploration stage that conducts low-cost experiments to refine the initial estimates.

Localized random exploration is a popular method in control (Moore, , 1990; Amin et al., , 2021), where an agent chooses from a perturbed set of best known actions. Our localized exploration stage uses similar ideas. In the dynamic pricing literature, price perturbation has been adopted for different purposes, such as addressing endogeneity (Nambiar et al., , 2019; Bu et al., , 2022) and handling reference effects (den Boer & Keskin, , 2022). Those works only considered pricing without contextual information.

Paper organization

The rest of the paper is organized as follows. Section 2 provides the background and problem setup. Section 3 outlines our algorithmic framework. Section 4 presents the main theoretical results. Section 5 demonstrates the practical performance of our approach through extensive numerical simulations and real-data experiments. Finally, Section 6 concludes the paper. For conciseness, all proofs are deferred to the appendix.

Notation

The constants may vary from line to line. We use boldface Greek letters to denote vectors, boldface capital letters to denote matrices, and plain letters to denote scalars. For nonnegative sequences and , we write or if there exists some universal constant such that for sufficiently large , and write or if there exists some universal constant such that for sufficiently large . Furthermore, we write or if both and hold. Similarly, we use , , and for similar meanings with exceptions up to some logarithmic factors. For random event , stands for its indicator function. We use to denote the set of symmetric matrices, and to denote the unit sphere with ambient dimension . For a random variable , the Orlicz norm is defined as where ; and for a random vector , we denote . In most cases, we omit the subscript when the dimension is clear from the context, e.g., the identity matrix is denoted as .

2 Problem set-up

We consider a dynamic pricing problem where a seller aims to maximize its revenue by adjusting the price of a single product over time. The demand for the product is modeled by a linear function that depends on contextual information. Below, we outline the key components of the problem.

Contextual linear demand model:

Suppose the demand for a product is influenced by contextual factors, such as customer demographics, purchase history, or market conditions. At each time period , the seller observes a -dimensional context vector , which encodes the relevant information about the customer or market environment.

Given the context , the seller selects a price from the feasible interval . The customer or market responds to the selected price , conditioned on the current context , by generating a random demand , modeled as:

| (2.1) |

Here represents random demand shocks, which are assumed to be sub-Gaussian with zero mean and a variance proxy of ; vectors are unknown model parameters. For notational convenience, we define as the concatenation of vectors and . This contextual linear demand model (2.1) was introduced by Ban & Keskin, (2021).

The demand model (2.1) is called linear for two reasons: (i) The demand function is linear in the price , with the intercept and the slope . (ii) Both the intercept and slope are linear in the context vector .

We adopt this model for its analytical simplicity, though it can be extended to account for nonlinear and higher-order effects of context and price on demand. As in the traditional linear regression models, the linear models in the intercepts and slopes here accommodate the transformed features, their interactions, and tensors. Despite its straightforward structure, the model unveils several interesting phenomena.

Optimal pricing policy:

Recall the seller’s goal is to maximize the revenue at each stage by selecting an appropriate price . The (expected) revenue is defined as

| (2.2) |

which is quadratic with respect to the price . To maximize revenue, the optimal price is set as 111We omit the effect of truncation to the interval for now.

| (2.3) |

At this price, the resulting revenue is

| (2.4) |

Therefore, if the true parameters were known, the optimal price could be determined analytically from the observed context using equation (2.3). However, since the model parameters are not directly observable, we must estimate them from the available data.

Online learning process:

The objective of this paper is to derive a statistically efficient method for learning the optimal pricing strategy in an online setting.

In the online learning process, at each time , the seller observes a context , which is independently drawn from a population distribution over the feature space . Based on the observed history,

the seller then selects a price . Next, the seller observes the demand based on equation (2.1), where the noise terms are independent across time steps. The realized revenue at time , denoted by , is given by equation (2.2).

| For any online learning algorithm that helps the seller choose the price , we assess its effectiveness by considering the cumulative regret at a (pre-specified) terminal stage : 222It can be easily extended, through a doubling trick, to anytime-valid results that do not require pre-specifying the terminal stage. | |||

| (2.5a) | |||

| At each stage, the regret measures the difference between the expected revenue achieved by the algorithm and the optimal revenue that could be achieved with the best price. After some algebra, we can express the regret as: | |||

| (2.5b) | |||

| This inequality shows how the closeness between the implemented price and the optimal price governs the overall regret in terms of revenue. | |||

In the following analysis, we focus on an efficient method to minimize the expected regret , where the expectation is taken over both the randomness in the data generation process and the randomness of the learning algorithm.

3 A localized explore-then-commit algorithm

In this section, we introduce a three-stage LetC pricing procedure featuring a novel localized exploration strategy. The complete algorithm is provided in Algorithm 1. Below, we elaborate on each stage in detail. We will use a clipping operator to project any proposed price to its feasible value in the interval .

Stage 1: Burn-in exploration.

In this stage, the main goal is to collect observations about the system without concern for revenue loss due to suboptimal pricing. To ensure effective exploration of the feature space, we alternate between the two extreme prices within the feasible range. Specifically, the prices are independently drawn from a binary distribution, taking or , each with probability . The binary design is optimal for learning parameters in the linear demand model. This pure exploration strategy has also been used in previous algorithms in the literature (Broder & Rusmevichientong, , 2012; Ban & Keskin, , 2021; Bastani et al., , 2022).

| This initial phase proceeds for steps, where is determined by the choice of the total termination time and other problem-specific structures, with the optimal value to be detailed later in Section 4.2. After collecting data from these steps, we form an estimate of the parameter using the historical data . Specifically, we employ ordinary linear squares (OLS) regression: Define an empirical quadratic loss function as | |||

| (3.1a) | |||

| The estimate is obtained by minimizing the loss, i.e. | |||

| (3.1b) | |||

| The optimal pricing strategy(before truncation), based on the estimate , is then given by | |||

| (3.1c) | |||

| which aligns with the definition of the optimal price in equation (2.3). Of course, we will round to a feasible value. | |||

We comment that a pure exploration phase is quite practical in real-world scenarios. When introducing a new product to the market, it is often beneficial to experiment with extreme pricing before settling on an optimal point. For instance, offering substantial discounts or coupons to encourage initial purchases simulates the effect of low prices. On the other hand, launching a premium or exclusive version of the product at a higher price helps gauge customer sensitivity and willingness to pay, providing insight into price elasticity.

Stage 2: Localized exploration.

The localized exploration in Stage 2 is a novel contribution of our work, distinguishing our method from those proposed in Ban & Keskin, (2021); Fan et al., (2022); Chen et al., (2021); Zhao et al., (2023). Recall that following the first stage, we have obtained an initial pricing policy , though the estimate of the parameters in the demand function may still lack sufficient precision due to the cost of exploration. In the second phase, we aim to refine it by using as a baseline while sampling around it to further fine-tune the parameters. This stage aims at gaining statistical information at low cost of revenue loss. With a proper choice of localization parameter, the statistical information gain will exceed the revenue lost.

Specifically, at each time for , we flip a coin. If heads, we set the price as ; if tails, we set . Here, and are parameters that will be determined later in Section 4.2. We express the sampling scheme as

| (3.2) |

where are independent Rademacher random variables.

At the end of this stage, we update the parameter estimate using the newly collected data from the second phase, incorporating it into the loss function as presented in equation (3.1a). Specifically, we define the updated parameter estimate as

| (3.3) |

where data from to in Stage 2 is used. The refined pricing policy(before truncation) is then defined as , consistent with equation (3.1c). It is worth noting that, in practice, data from the first stage can also be included, allowing the use of all data up to . However, for simplicity in theoretical analysis, we restrict the update to Stage 2 data, as this is sufficient to achieve the optimal rate of regret.

This localized exploration strategy balances exploration and exploitation effectively. By using the initial estimate , we can secure a near optimal level of revenue, which corresponds to exploitation. At the same time, the exploration component (adding random noises to pricing) continues to play a role by allowing us to capture more nuanced patterns in market behavior (with relatively low regret), leading to a better pricing strategy. For a linear demand model, it is well known from the design of experiment that setting the exploring prices driven by Rademacher random perturbations maximizes the information gain in learning for any distributions with the same support. The revenue lost due to the use of non-optimal price is of order . Therefore, it will be shown in our proof that with a proper choice of , the gain of statistical information in learning the parameter outbenefits the revenue loss due to the local exploration and this benefit diminishes when is sufficiently large that parameters are sufficiently accurately estimated. Hence, we can now apply the learned optimal pricing strategy as if the true parameters were known.

Stage 3: Committing.

At the final stage of the algorithm, we implement the refined policy for the remaining steps . Since the estimates have reached sufficient precision, further exploration is unnecessary, and pure exploitation of the learned knowledge ensures minimal regret.

Input: Numbers of steps in Stages 1 and 2, and ;

magnitude of local perturbation, ; feasible price range .

Output: Prices at each step, .

We comment that the first two stages of exploration occupy only a small portion of the overall learning process, allowing the algorithm to focus primarily on pure exploitation for most of the time so that the revenue loss in the first two stages is negligible. As will become clear in Theorem 1 in Section 4.2, by setting and for , we achieve optimal rate of regret by effectively balancing exploration and exploitation.

Doubling trick to make the algorithm fully online:

We propose a variant of our algorithm suited for a fully online procedure. In its current form, the choices of hyperparameters , , and in Algorithm 1 require knowledge about the termination time . However, we often want to design an algorithm that achieves minimal regret (up to a constant) at any time .

To address this, we can apply the doubling trick (Auer et al., , 1995; Besson & Kaufmann, , 2018). Specifically, we double the time horizon iteratively, which apply (reset) Algorithm 1 sequentially for time horizons of lengths for a given . For each new interval, we recompute the parameters and apply Algorithm 1 with the corresponding . This ensures the algorithm performs efficiently without requiring prior knowledge of . With this modification, the theoretical guarantees of the original algorithm are preserved, ensuring statistical efficiency throughout the process.

Further refining the algorithm by using time-varying perturbation :

We also conjecture that optimal regret could still be achieved by using a time-varying perturbation, , which would eliminate the need for Stage 3 entirely. This modification enables a more dynamic and seamless balance between exploration and exploitation throughout the learning process, potentially improving efficiency in an online setting. However, it requires refitting the model at each time step, which may impose a significant computational burden. Therefore, we maintain the procedure in Algorithm 1 due to its simplicity in both practical implementation and theoretical analysis.

4 Theoretical guarantees

We now present the main theretical results of our LetC algorithm. In Section 4.1, we start by providing an upper bound on the cumulative regret of our algorithm, which scales as and is independent of the dimension of the context vectors when is large. This leads to our first key finding: when the planning horizon is sufficiently large (specifically, when ), the regret becomes dimension-free. In Section 4.2, we extend this result to a more general, non-asymptotic upper bound on the regret that applies to any planning horizon . This bound explicitly accounts for the effect of dimensionality when is relatively small. The analysis hinges on a critical inequality that balances exploration and exploitation, which becomes particularly important in high-dimensional settings with a limited planning horizon. Finally, in Section 4.3, we establish a minimax lower bound that matches the dimension-free upper bound from Section 4.1, confirming the statistical efficiency of our method.

4.1 Dimension-free regret upper bound for large time horizon

Our first main result establishes a dimension-free upper bound on the cumulative regret. To build towards this result, we start by outlining the assumptions under which the bound is valid.

4.1.1 Assumptions

Regularity on the feature distribution:

We first impose regularity conditions on the distribution of the feature vectors :

Assumption 1 (Regularity on the feature ).

-

1.

The feature vectors are i.i.d. sub-Gaussian random vectors. Their -norm is bounded above by a constant , i.e. for all , .

-

2.

The second-moment matrix is well-conditioned. Its eigenvalues are bounded as for some constants .

Regularity on model parameters:

In addition to the assumptions on the feature distribution , we also impose some regularity conditions on the demand model (2.1):

Assumption 2 (Regularity on model parameters).

There exist constants such that:

-

1.

For every feature , the corresponding optimal price defined in equation (2.3) lies in the feasibility interval and is bounded away from the boundaries. That is, for some small constant , . Additionally, the range is of constant order.

-

2.

For every feature , the intercept and the slope in equation (2.1) are also of constant order, satisfying .

Sufficient exploration conditions:

Recall that in our model (2.1), the expected demand is a linear function of the augmented covariate . To achieve sublinear regret, typically converges to over time. Consequently, the following second-moment matrix plays a crucial role in our analysis:

| (4.1) |

The matrix represents the “limiting” second-moment matrix associated with the estimation process, especially when the pricing strategy is estimated with high accuracy. To ensure that the data we collect during the learning process effectively explores the feature space, it is crucial that has favorable spectral properties. In the following, we provide a characterization of the spectral structure of the matrix under relatively mild and natural assumptions, as shown below:

Assumption 3 (Sufficient exploration).

-

1.

The distribution of feature satisfies an anti-concentration property: There exists a constant such that for any symmetric matrix with ,

(4.2) -

2.

The demand model (2.1) is non-degenerate, meaning there exists a constant such that and . Moreover, the vectors and are not collinear, satisfying for a constant .

Remark.

Under the conditions specified in Assumption 3, we can characterize the spectrum of the matrix as stated in Lemma 1 below. The proof is provided in Section A.6.1.

Lemma 1.

The second-moment matrix has the following property:

-

1.

The rank of satisfies , with the vector always lying in its null space.

Furthermore, under Assumptions 2 and 3, we have

-

2.

, and its null space is one-dimensional, spanned by the vector .

-

3.

The second smallest eigenvalue of is bounded below by a positive constant.

As highlighted in Lemma 1, when the second-moment matrix is singular, this dynamic pricing problem falls into the category of “incomplete learning” (Keskin & Zeevi, , 2014; Bastani et al., , 2021) under a greedy algorithm. Without explicit efforts to introduce price dispersion, there is no guarantee that parameter estimates will converge to their true values. The existing literature suggests addressing this issue by employing semi-myopic policies (Keskin & Zeevi, , 2014) such as ETC or UCB. In contrast, we address this problem by learning through active local exploration.

We conclude the introduction of 3 by making a few remarks: (i) The anti-concentration property ensures that the feature sufficiently explores all directions in the feature space , preventing any direction from being underrepresented. (ii) By ensuring that the vectors and are not strongly collinear, the optimal pricing function remains sensitive to changes in the features. This prevents from being constant and allows for better exploration across the entire feature space. At the end of Section 4.1, we will outline some moment conditions for Assumption 3.1, and present a simple example to demonstrate that Assumptions 1, 2 and 3 are well-posed and not overly restrictive.

4.1.2 Main result

With all the necessary assumptions at hand, we are ready to present the main result of this section: a dimension-free regret bound that holds when the planning horizon is sufficiently large.

A major contribution of our theory is providing practical recommendations for selecting the hyperparameters , , and in Algorithm 1. We propose setting the lengths of the burn-in period and localized exploration stage as:

| (4.3a) | ||||

| (4.3b) | ||||

| With this setup, the initial exploration phase () becomes negligible in the long run, i.e., and the revenue loss is at most , while the second stage () uses only a small fraction of the time horizon. This leaves the majority of the horizon focused on committing to and exploiting the learned policy. | ||||

For the perturbation level during localized exploration, our theory requires

| (4.3c) |

where are constants to be determined later. The optimal choice of roughly corresponds to setting , which is approximately on the same scale as the estimation error in Stage 1.

We now present our main result, Theorem 1, which establishes statistical guarantees for the cumulative regret of Algorithm 1 using the hyperparameters specified above. The detailed proof can be found in Section A.1.2.

Theorem 1 (Dimension-free regret upper bound).

Suppose Assumptions 1, 2 and 3 hold. There exist constants , determined solely by the parameters specified in these assumptions, such that the following results hold. If the planning horizon is sufficiently large, satisfying

| (4.4) |

and the hyperparameters are set according to equations (4.3a)-(4.3c), then Algorithm 1 achieves the following guarantees:

-

(a)

With probability at least , the cumulative regret is bounded by

(4.5a) -

(b)

Additionally, the expected cumulative regret satisfies

(4.5b)

We highlight that by choosing the perturbation level as

the regret bound in (4.5a) (and similarly in (4.5b)) achieves its optimal order:

| (4.6) |

This bound is dimension-free, meaning the regret does not grow with the dimension . Intuitively, this is because when is large, we only need to actively explore in the singular direction, as indicated by Assumption 3. To reach this dimension-free regime, a larger planning horizon is needed in higher-dimensional settings, as indicated by condition (4.4). Nevertheless, as increases, the cumulative regret eventually converges to the dimension-free rate of , regardless of the feature dimension. We will further illustrate this behavior with simulation studies in Section 5.1.

Comparison to Ban & Keskin, (2021).

The contextual linear pricing framework was first introduced in Ban & Keskin, (2021). We highlight a few key differences in assumptions and results. The major difference is that we impose the benign eigen structure of , the “limiting” second-moment matrix associated with the estimation process. We provide a clear and transparent condition to ensure this, as outlined in Assumption 3. In the same linear modeling framework as ours, Ban & Keskin, (2021) establishes a regret bound of . To address high-dimensional settings, they further derive a regret bound of under a sparsity assumption. In contrast, we are able to even eliminate using better algorithmic design and relatively mild assumptions.

4.1.3 Comments on the anti-concentration property in Assumption 3

To conclude this subsection, we highlight a few moment conditions that guarantee the anti-concentration property (Assumption 3.1), and then present a simple problem instance that meets Assumptions 1-3, as required in Theorem 1. The example illustrates that the assumptions are reasonable and compatible.

Lemma 2.

Let be a random vector with independent coordinates, and . Assume the following moment conditions:

-

1.

for ;

-

2.

and for some constant and .

-

3.

the minimum singular value of is bounded as .

Then, the anti-concentration property (4.2) holds for any symmetric matrix .

The second condition essentially states that the kurtosis of each coordinate is strictly greater than , which holds for nondegenerate distributions. Many common distributions, such as the Gaussian and Uniform distributions, satisfy both conditions 1 and 2. We now prove the lemma.

Proof.

Let first consider the specific case so that . For any symmetric matrix , by leveraging the conditions that for , we derive through some straightforward algebraic calculations

Next, using the relations and for , we obtain

Now, for the general case, for any symmetric , it follows from the above result that

In other words, we have shown that the anti-concentration property (4.2) is indeed satisfied with . ∎

Example 1.

In this example, we consider features , where the entries are independently distributed according to

It is straightforward to show that 1 naturally holds for this feature distribution . Also, satisfies the above moment conditions 1 and 2, and hence Assumption 3.1.

We now turn to selecting a demand model (2.1) with parameters and that satisfy Assumptions 2 and 3.2.

Let be the unit vector with its first entry as one and all others as zero. To satisfy 2, we pick vectors and . Specifically, we set such that . From this choice, we can derive

Similarly, it can be shown that . We also select such that , which ensures . These bounds on and imply that the optimal price is also bounded, thereby satisfying 2.

4.2 Non-asymptotic regret upper bound for any time horizon

In Section 4.1, we established a regret upper bound that, surprisingly, turned out to be dimension-free. However, the result only applies when the planning horizon is sufficiently large, specifically requiring . It naturally raises the following questions: what happens when is smaller? Can we still effectively control regret in such cases?

To address this limitation, we extend our analysis to shorter planning horizons by conducting a more detailed study of the spectral properties of the covariance matrix defined in equation (4.1). This extended analysis builds on Assumptions 1 and 2 from Section 4.1, without relying on 3.

We start by establishing a critical inequality in Section 4.2.1, which forms the backbone of our analysis. In Section 4.2.2, we derive a new regret bound that holds for any , expanding the applicability of our results. Our theory also provides practical guidance on tuning the hyperparameters in Algorithm 1 to achieve an effective balance between exploration and exploitation in a broader range of scenarios.

Finally, in Section 4.2.3, we draw connections to ridge regression and show that (i) localized exploration in online dynamic pricing resembles adding a ridge penalty in regression, and (ii) our critical inequality closely mirrors that in kernel ridge regression. While the critical inequality in kernel ridge regression characterizes the bias-variance tradeoff, ours focuses on the exploration-exploitation tradeoff. This comparison highlights how our method adapts regularization techniques to dynamic settings while introducing novel adjustments for online decision-making.

4.2.1 Critical inequality

Let us begin by introducing a critical inequality that serves as a cornerstone of our analysis. This inequality centers on the spectrum of the second-moment matrix , which, for reference, is defined as follows:

| (4.1) |

Let denote the eigenvalues of matrix , ordered non-increasingly.

Degenerate dimension:

To simplify our analysis of the online learning process and define the critical inequality, we first introduce a concept called the degenerate dimension, defined as

| (4.7) |

From Lemma 1, the smallest eigenvalue is zero. Therefore, the degenerate dimension always satisfies , although it may not necessarily be an integer.

Critical inequality:

We set the perturbation level as a small, positive solution to the critical inequality:

| (4.8) |

In this expression, is a constant that will be specified later in Theorem 2.

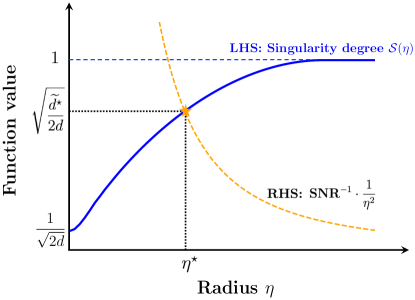

The left-hand side of the critical inequality (4.8) features a singularity function at level , which we denote as . This function captures the “proportion” of eigenvalues that fall below the threshold . It starts at a minimum value of at least when is close to zero and increases continuously to as grows larger. 333 To understand why ranges between and , let us revisit the properties of the covariance matrix . According to Lemma 1, this matrix is rank deficient, meaning it has some zero eigenvalues. As a result, when , the singularity function behaves as . On the other hand, as increases, once it exceeds the largest eigenvalue, i.e., , all the eigenvalues become smaller than . In this case, the singularity function reaches its maximum value .

The right-hand side of the critical inequality (4.8) is a decreasing function with respect to the parameter . It diverges to as and decreases to as . The inequality involves the inverse of a signal-to-noise ratio (SNR), defined as

| (4.9) |

The value of SNR increases with a longer planning horizon , indicating stronger signals as more information is collected over time. In contrast, SNR decreases as the dimension increases since the signal strength is diluted across multiple directions, weakening its impact.

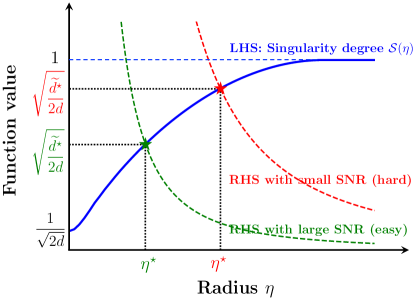

In Figure 1 below, we illustrate the basic geometry of the critical inequality (4.8) to provide a more intuitive understanding of its structure. This figure shows how varying levels of SNR influence the behavior of the critical inequality and, consequently, affect the solutions.

|

|

|

|---|---|---|

| (a) | (b) |

Critical radius and regular solution:

Due to the monotonic behavior of the two sides of the critical inequality (4.8), they intersect at exactly one point, leading to a unique solution for that satisfies the equality. We refer to this intersection point as the critical radius, denoted by . Formally, we define it as . In other words, represents the smallest positive solution to the inequality.

In practice, however, computing the exact value of is generally infeasible, so we aim to approximate it instead. For this purpose, we introduce the concept of a regular solution: A solution is termed -regular for some parameter if the scaled value no longer satisfies the critical inequality (4.8). In cases where is unspecified, we refer to simply as regular, with treated as an adjustable constant for controlling the approximation quality.

The concept of degenerate dimension extends the idea of effective or statistical dimension, which is widely used in kernel ridge regression (see Yang et al., (2017)). Traditionally, effective dimension is determined by counting the eigenvalues that exceed a given threshold. In contrast, our approach emphasizes eigenvalues below the cutoff . This reframing shifts the focus to identifying directions where the model is less confident. These directions of singularity indicate areas where further exploration is needed, thereby guiding the learning process more effectively.

4.2.2 Main theorem

With the stage now set, we are ready to present our main theorem. Our theory recommends setting the perturbation level in the localized exploration stage to satisfy the critical inequality (4.8):

| Choose such that it solves the critical inequality (4.8). | (4.10a) | |||

| The degenerate dimension at the chosen perturbation level is hard to determine in practice. We make a guess such that , and then set the lengths of exploration stages as follows: | ||||

| (4.10b) | ||||

| (4.10c) | ||||

With the above configuration, we establish non-asymptotic guarantees on the cumulative regret, as stated in Theorem 2, without 3 for a wider range of . The full proof can be found in Section A.1.3.

Theorem 2 (A general regret upper bound).

Suppose Assumptions 1 and 2 hold. Let be constants determined solely by the parameters specified in these assumptions. If the planning horizon is sufficiently large, such that

| (4.11) |

and the hyperparameters are set according to equations (4.10a)-(4.10c), then Algorithm 1 achieves the following guarantees:

-

(a)

With probability at least , the cumulative regret is bounded by

(4.12a) -

(b)

Additionally, the expected cumulative regret satisfies

(4.12b)

We now provide some clarifications on how to refine the regret bound by properly scaling the parameters and .

-

•

If satisfies the critical inequality (4.8) as a regular solution444Recall that a regular solution defined at the end of Section 4.2.1 means the solution is near the critical point of (4.8)., the regret bound stated in (4.12a) (and similarly in (4.12b)) can be tightened to

(4.13a) The proof of this claim can be found in Section A.1.3.

-

•

If, in addition, we have , the regret bound simplifies even further to

(4.13b) In this case, the extra complexity term vanishes, resulting in the optimal scaling of the regret.

Below, we provide key insights into the implications of our main theorem.

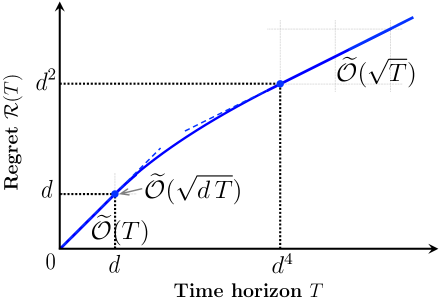

Characterization of regret across the full range of :

One of the key contributions of Theorem 2 is its ability to characterize the regret behavior across the entire range of planning horizons . Importantly, the lower bound (4.11) on the planning horizon required for our analysis is quite mild. When , the regret can always be bounded as

| (4.14) |

This, combined with the bound (4.13b), provides a comprehensive characterization of the regret for any .

We identify two critical boundaries where the behavior of the regret changes:

- •

- •

We will rigorously establish these transitions in Section A.6.3, focusing on how the degenerate dimension scales at these key boundaries.

For values below the first transition point, the linear bound (4.14) applies. For beyond the second transition point, the dimension-free bound (4.6) dominates. Between these two points, the bound (4.13b) adapts smoothly by adjusting the degenerate dimension according to the value of . This dynamic adjustment allows the bound to seamlessly cover the entire range of planning horizons.

The full regret bound, covering all values of , is summarized as

| (4.15) |

A visual representation of this bound is provided in Figure 2.

Exploitation-exploration tradeoff:

The critical inequality (4.8) encapsulates the tradeoff between exploitation and exploration. To better understand this, we can equivalently reformulate it as

| (4.16) |

In the reformulated inequality, the left-hand side represents the regret loss caused by exploration during Stage 2. Increasing the strength of the exploration noise results in higher regret from this exploration phase. On the other hand, the right-hand side captures the revenue loss due to inaccurate estimation of demand function during exploitation in Stage 3, which depends on the data collected using the specified level of . A larger value of increases and reduces the right-hand side of the inequality. This means that using a higher level of exploration noise improves the coverage of the data collected, leading to lower error during the exploitation phase.

The inequality (4.16) highlights the delicate balance between these two opposing effects. When it holds as equality, it indicates an optimal balance, achieving the best possible tradeoff between exploration and exploitation.

4.2.3 Connection with ridge regression

We now discuss the connection between our localized exploration-then-commit method for dynamic pricing and ridge regression.

Localized exploration as a ridge penalty:

In terms of estimating the parameter , adding exploration noise with magnitude has an effect similar to adding a ridge regularization term in the linear regression problem (3.3). To illustrate this connection, we present an informal version of Lemma 3. The full, detailed version is provided in Lemma 6 in Section A.1.1.

Lemma 3 (Estimation error in from Stage 2 (informal)).

Under suitable assumptions and with properly chosen hyperparameters, there exists a constant such that, with high probability

| (4.17) |

The bound (4.17) reveals that increasing the noise level effectively increases the eigenvalues of the covariance matrix by , analogous to the effect of ridge regularization. This improved conditioning reduces the estimation error, similar to how ridge regression stabilizes estimates in ill-conditioned problems.

Comparison with the critical inequality:

In this work, one of our key contributions is to extend the framework of critical inequalities, originally developed for kernel ridge regression (e.g., Bartlett et al., (2005); Yang et al., (2017); Wainwright, (2019); Duan et al., (2024); Duan & Wainwright, (2022)), to an online learning setting where the focus shifts from the bias-variance tradeoff to the exploration-exploitation tradeoff. These critical inequalities share a common principle: they examine the spectrum of the covariance matrix to characterize effective or degenerate dimensions. However, they target different balances depending on the specific regime of interest.

To delineate the connection between these two frameworks, let us revisit the critical inequality used in kernel ridge regression:

| (4.18) |

Here are the eigenvalues of a kernel-based covariance operator. The left-hand side , known as the kernel-complexity function at radius , reflects the variance incurred by using basis directions where the signal strength exceeds the threshold . The quantity is known as the statistical dimension. The right-hand side, a linear function of , represents the bias introduced by cutting off bases below this threshold , with the slope determined by a signal-to-noise ratio SNR. Tuning KRR according to the solution to this inequality captures the optimal balance between variance and bias.

Our critical inequality (4.8) parallels (4.18) but is adapted to the online learning context, where the focus shifts to exploring the degenerate dimensions and the singularity of the covariance matrix. Unlike the kernel ridge regression setting, where the complexity emphasizes function class richness, we instead focus on how well the exploration phase covers directions of singularity to optimize the tradeoff between exploration and exploitation.

In essence, while both inequalities utilize similar language and concepts, they address different challenges: kernel ridge regression focuses on balancing bias and variance, whereas our approach targets efficient exploration and exploitation in dynamic settings. We present their comparisons in Table 1.

| Linear Dynamic Pricing | Kernel Ridge Regression | |

|---|---|---|

| Tradeoff | Exploration-exploitation tradeoff | Bias-variance tradeoff |

| Dimension | Degenerate Dimension | Statistical Dimension |

4.3 Minimax lower bound

Thus far, we have established some regret upper bounds on the performance of our proposed LetC algorithm. To what extent are these bounds improvable? In order to answer this question, it is natural to investigate the fundamental (statistical) limitations of the dynamic pricing problem itself. Although previous studies, such as Ban & Keskin, (2021), have explored this question, the provided lower bounds do not account for the precise dependence on the context dimension. In this section, we fill this gap by deriving a precise minimax regret lower bound on this problem.

We start by defining the model class . To facilitate fair comparison with the upper bound, should satisfy Assumptions 2, 3. More specifically, for some constants , such that , and , let

be the pricing model class under consideration. The lower bound should be uniform for any measurable policy that maps the data collected prior to time to the price at time , for any time .

We can prove the following lower bound, whose proof is delegated to Appendix B. The proof utilizes the multivariate van Trees inequality, as similarly applied in Keskin & Zeevi, (2014); Ban & Keskin, (2021). For notational simplicity, we introduce two shorthands, and in the following stated theorem.

Theorem 3.

The key takeaway from this result is that when the time horizon is sufficiently large, even an oracle algorithm knowing all the contexts beforehand cannot beat the lower bound on the regret. By comparing the upper and lower bounds, we conclude that both are tight and unimprovable. Notably, while parameter estimation becomes more challenging as the dimension increases, the complexity of decision-making can remain unchanged.

5 Numerical experiments

In this section, we conduct simulations and real data experiments to corroborate our theory, as well as test the efficacy of our proposed algorithm. The code and all numerical results are available at https://github.com/jasonchaijh/LetC.

5.1 Simulation studies

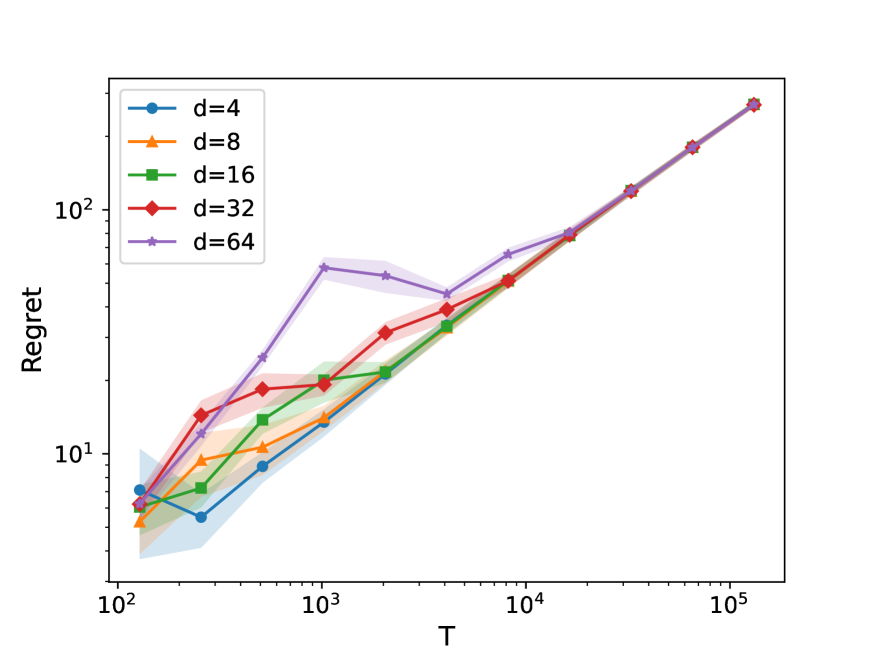

A key property of our algorithm is that its regret remains independent of the dimensionality and scales proportionally to the square root of the time horizon. The primary goal of our simulation study is to demonstrate this characteristic.

We begin by generating sales data using the linear demand model in (2.1), with the data-generating process defined as follows:

-

1.

We sample the context independently and identically distributed (i.i.d.) from , where the first coordinate of is a constant , and the other coordinates are i.i.d. .

-

2.

For , we fix the ground truth coefficients and .

-

3.

The noises are generated from .

-

4.

At each time , given the feature and the price chosen by the chosen algorithm, we generate the demand as where is a shorthand for the mean demand.

According to our theoretical framework, we set

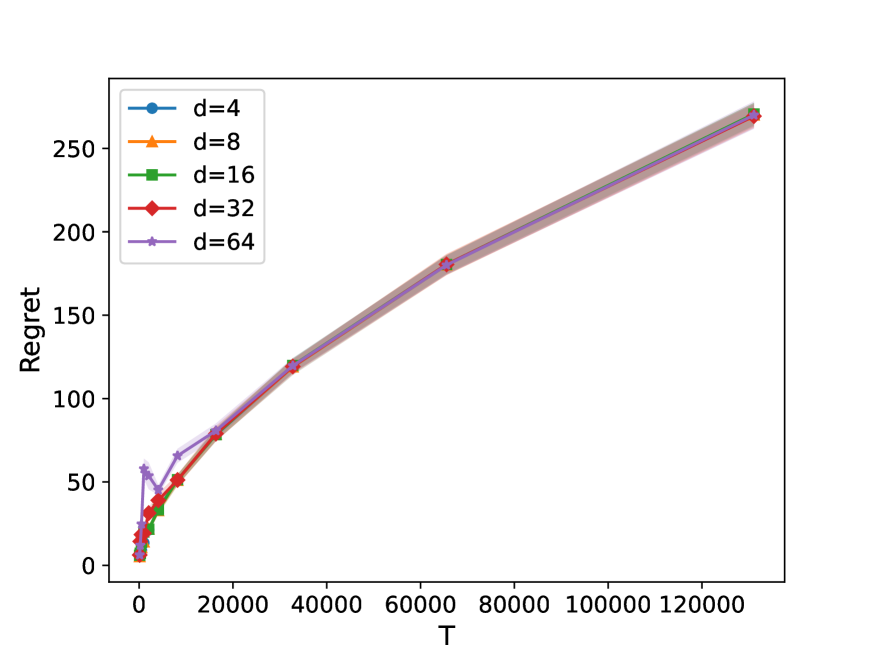

based on the tuning hyperparameters . Note that these hyperparameters should be scale-dependent, and we take which remain fixed throughout the experiment. For each and , we run LetC with simulation trials. The resulting average regret and log-log regret plots are presented in Figure 3(a) and 3(b), respectively. The shaded areas indicate the standard deviation across the parallel trials.

The figures highlight two key phenomena. First, the regret of our algorithm remains largely independent of the dimension as the time horizon increases and scales in a square-root manner, which can be seen in the log-log plot that the slope tends to . Second, consistent with our theoretical findings, there are certain thresholds above which the regret exhibits standard scaling, with these thresholds being higher for larger dimensions.

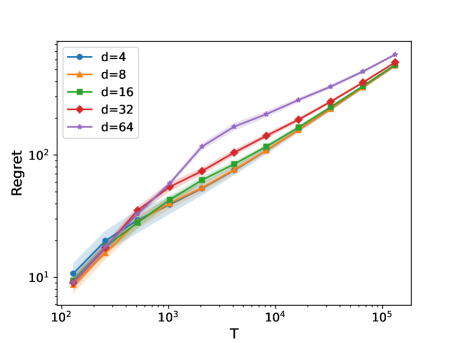

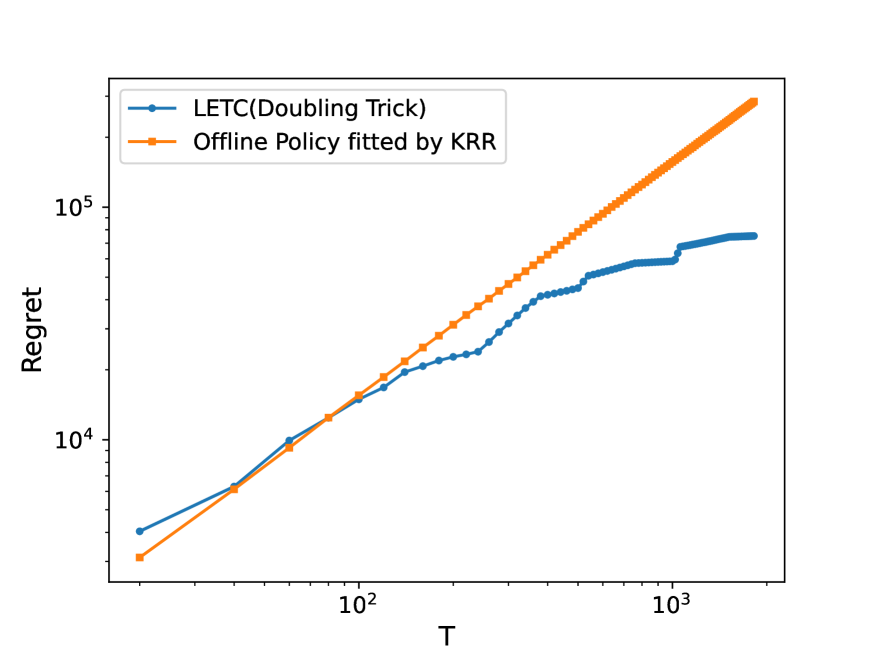

In practice, the seller does not have prior knowledge of the time horizon . To address this, we employ the doubling trick (see Section 4 for details) to generate a single trajectory of increasing regret over time. Figure 4 demonstrates similar behavior, showing that the regret scales in a square-root manner and is roughly independent of .

5.2 Real-data examples

We evaluate our proposed algorithm using a real-world dataset available at the INFORMS 2023 BSS Data Challenge Competition. Since the ground truth model, required for generating online responses to any input algorithm, is inaccessible, we adopt a parametric bootstrap (or calibration) approach (Ban & Keskin, , 2021; Fan et al., , 2022), treating the fitted model as the underlying ground truth for conducting online experiments. Specifically, using the historical sales dataset, we fit a linear demand model and simultaneously estimate the distribution of features. These components are then used to generate semi-synthetic data for the testing period.

To evaluate the efficacy of our LetC algorithm, we aim to compare it with some benchmark offline pricing policy. It is reasonable to assume that the prices in the dataset result from some “good” pricing strategy (given the monetary stakes involved) deployed by the seller, which we aim to learn from the data. Specifically, we will fit the price as a function of features using a kernel method and the resulting pricing function will be regarded as the seller’s policy. We apply these two policies (LetC and fitted pricing function) in the testing period. The details of the raw data and the testing data-generating process are elaborated below.

Data Description

The dataset consists of daily price and sales data for over 200 office products from Blue Summit Supplies (BSS), an e-commerce company, covering a span of approximately seven seasons from January 1, 2022, to September 23, 2023. Due to product heterogeneity, we employ distinct models for different products. We extracted nine features from the dataset: the first seven are indicator variables representing the days of the week to capture weekday effects. The eighth and ninth features correspond to the minimum and maximum competitor prices for the same product observed in the recent period, respectively. It is worth noting that the allowable price bounds 555For each product, we denote the minimum allowable price as , and the maximum allowable price as , for notation consistency. act as constraints on the realized prices but are not included in the model fitting process.

Semi-synthetic Data Generation

As illustrated, the data contains 9 features includes 7 binary variables and 2 continuous variables. For the binary variables that capture weekday effects, it is straightforward to generate in time order. For the continuous features, we fit a mixture of multivariate Gaussian to approximate its distribution. Specifically, for each day of the week, we fit the pair ()666We denote the minimum price for competitors as and the maximum price for competitors as separately. Using rejection sampling, we continue generating features, accepting a feature if and only if both of the following conditions are satisfied.

-

1.

;

-

2.

for all , where we recall is the mean demand.

To ensure that the realized demand remains positive, we generate the realized demand using the Poisson distribution: , where we recall that is the expected demand.

Offline Policy Estimation

We will demonstrate the efficacy of our policy by comparing it with a benchmark offline pricing policy, which we assume was deployed by the seller. To fit this offline pricing strategy, we use kernel ridge regression with the radial basis function (RBF) kernel on the original dataset, with the 9 constructed features. Hyperparameters are found as regularization strength ‘alpha’= 0.2, kernel bandwidth ‘gamma’= 0.05 were selected through 5-fold cross-validation. The fitted policy is a mapping from the features to a selling price.

Experiment 1

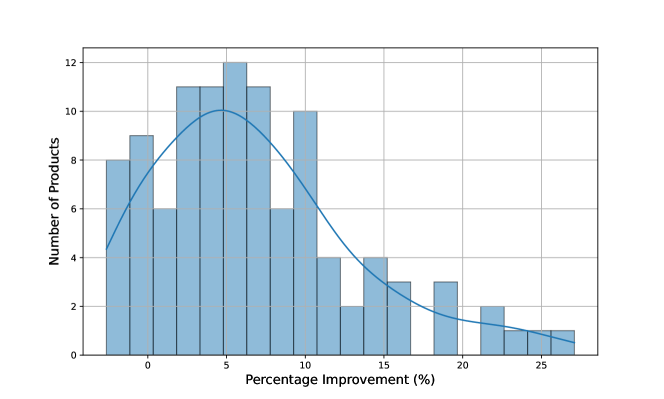

In the first experiment, we compare the offline policy with the policy chosen by our LetC algorithm in the testing period of one year (365 days), across different products. For the hyperparameters of LetC algorithm, we pick . From the complete set of products, we select 105 whose demand models are suitable for linear representation. Specifically, we run the semi-synthetic feature generation process for a particular product, and if a feature is not accepted after 10,000 generations (typically due to violation of condition 2), we discard the product, as it is likely unsuitable for linear demand modeling. The histogram result in Figure 5 demonstrates significant revenue improvements when using our policy compared to the offline policy.

Experiment 2

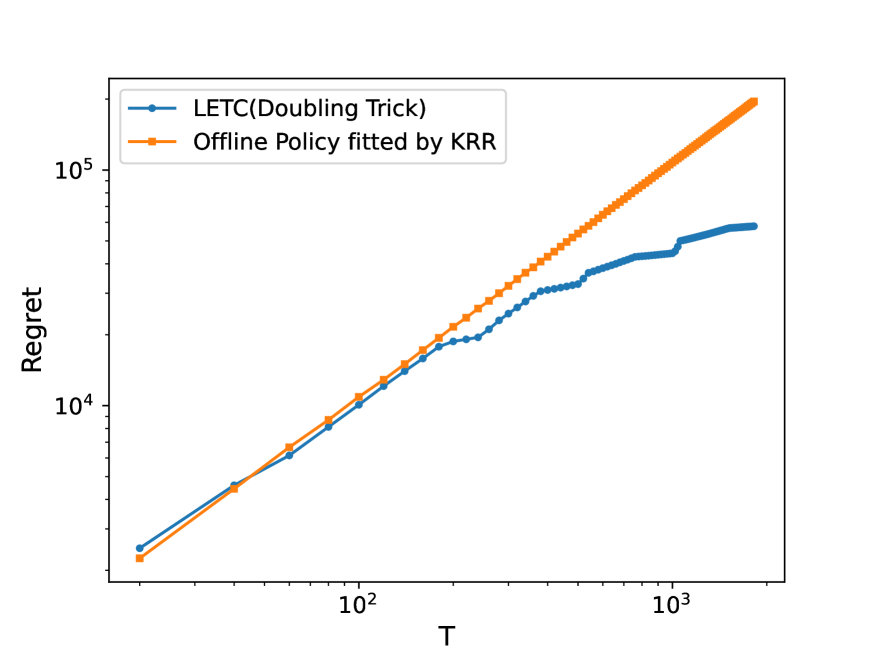

In the second experiment, we compare the offline policy with the policy chosen by our LetC algorithm with a doubling trick in a testing period of five years ( days). We randomly pick two products, “Misc School Supplies SKU 17” and “Classification Folders SKU 11”, and draw their regret curves over time. The results are shown in Figure 6(a) and 6(b). We conduct trials for each policy and depict the standard error as the shaded area in the plot. As we can see, our proposed policy performs almost uniformly better than the static offline policy, which incurs linear regret across testing time. Our proposed policy scales sub-linearly with time horizon, implying a decrease in average regret as more information about the pricing model is accumulated.

6 Conclusion

In this paper, we study the problem of contextual dynamic pricing under a linear demand model. We propose a novel three-stage online algorithm leveraging the idea of local exploration. Theoretic analysis shows the regret of the algorithm achieves a minimax lower bound when the time horizon exceeds a mild threshold polynomial in the dimension. Furthermore, our method demonstrates a smooth transition in regret behavior across the entire range of time horizons, from small to large. Additionally, we establish the critical inequality for dynamic pricing, which captures the trade-off between exploration and exploitation. Our analysis provides valuable insights into the eigenstructure of the “augmented” covariance matrix. The effectiveness of the proposed algorithm is validated through both simulations and real-world data experiments, confirming its theoretical guarantees and practical utility.

There are several directions worth exploring in the future. First, while we focus on the linear model for simplicity and clarity, the proposed algorithmic framework could potentially be extended to more complex settings like a generalized linear model, parametric model, or nonparametric model. Second, we believe our new critical inequality can be further generalized to other problems of statistical decision-making. And we leave these intriguing questions in future endeavor.

References

- Amin et al., (2021) Amin, S., Gomrokchi, M., Satija, H., Van Hoof, H., & Precup, D. (2021). A survey of exploration methods in reinforcement learning. arXiv preprint arXiv:2109.00157.

- Auer et al., (1995) Auer, P., Cesa-Bianchi, N., Freund, Y., & Schapire, R. E. (1995). Gambling in a rigged casino: The adversarial multi-armed bandit problem. In Proceedings of IEEE 36th annual foundations of computer science (pp. 322–331).: IEEE.

- Ban & Keskin, (2021) Ban, G.-Y. & Keskin, N. B. (2021). Personalized dynamic pricing with machine learning: High-dimensional features and heterogeneous elasticity. Management Science, 67(9), 5549–5568.

- Bartlett et al., (2005) Bartlett, P. L., Bousquet, O., & Mendelson, S. (2005). Local rademacher complexities. Annals of Statistics, (pp. 1497–1537).

- Bastani et al., (2021) Bastani, H., Bayati, M., & Khosravi, K. (2021). Mostly exploration-free algorithms for contextual bandits. Management Science, 67(3), 1329–1349.

- Bastani et al., (2022) Bastani, H., Simchi-Levi, D., & Zhu, R. (2022). Meta dynamic pricing: Transfer learning across experiments. Management Science, 68(3), 1865–1881.

- Besbes & Zeevi, (2015) Besbes, O. & Zeevi, A. (2015). On the (surprising) sufficiency of linear models for dynamic pricing with demand learning. Management Science, 61(4), 723–739.

- Besson & Kaufmann, (2018) Besson, L. & Kaufmann, E. (2018). What doubling tricks can and can’t do for multi-armed bandits. arXiv preprint arXiv:1803.06971.

- Broder & Rusmevichientong, (2012) Broder, J. & Rusmevichientong, P. (2012). Dynamic pricing under a general parametric choice model. Operations Research, 60(4), 965–980.

- Bu et al., (2022) Bu, J., Simchi-Levi, D., & Wang, C. (2022). Context-based dynamic pricing with separable demand models. Available at SSRN 4140550.

- Chen & Gallego, (2021) Chen, N. & Gallego, G. (2021). Nonparametric pricing analytics with customer covariates. Operations Research, 69(3), 974–984.

- Chen et al., (2022) Chen, X., Owen, Z., Pixton, C., & Simchi-Levi, D. (2022). A statistical learning approach to personalization in revenue management. Management Science, 68(3), 1923–1937.

- Chen et al., (2021) Chen, X., Zhang, X., & Zhou, Y. (2021). Fairness-aware online price discrimination with nonparametric demand models. arXiv preprint arXiv:2111.08221.

- den Boer, (2015) den Boer, A. V. (2015). Dynamic pricing and learning: historical origins, current research, and new directions. Surveys in operations research and management science, 20(1), 1–18.

- den Boer & Keskin, (2022) den Boer, A. V. & Keskin, N. B. (2022). Dynamic pricing with demand learning and reference effects. Management Science, 68(10), 7112–7130.

- Duan & Wainwright, (2022) Duan, Y. & Wainwright, M. J. (2022). Policy evaluation from a single path: Multi-step methods, mixing and mis-specification. arXiv preprint arXiv:2211.03899.

- Duan et al., (2024) Duan, Y., Wang, M., & Wainwright, M. J. (2024). Optimal policy evaluation using kernel-based temporal difference methods. Ann. Statist., 52(5), 1927–1952.

- Fan et al., (2022) Fan, J., Guo, Y., & Yu, M. (2022). Policy optimization using semiparametric models for dynamic pricing. Journal of the American Statistical Association, (pp. 1–29).

- Fan et al., (2020) Fan, J., Ke, Y., & Wang, K. (2020). Factor-adjusted regularized model selection. Journal of Econometrics, 216(1), 71–85.

- Fan et al., (2013) Fan, J., Liao, Y., & Mincheva, M. (2013). Large covariance estimation by thresholding principal orthogonal complements. Journal of the Royal Statistical Society Series B: Statistical Methodology, 75(4), 603–680.

- Gill & Levit, (1995) Gill, R. D. & Levit, B. Y. (1995). Applications of the van trees inequality: a bayesian cramér-rao bound. Bernoulli, (pp. 59–79).

- Javanmard & Nazerzadeh, (2019) Javanmard, A. & Nazerzadeh, H. (2019). Dynamic pricing in high-dimensions. Journal of Machine Learning Research, 20(9), 1–49.

- Keskin & Zeevi, (2014) Keskin, N. B. & Zeevi, A. (2014). Dynamic pricing with an unknown demand model: Asymptotically optimal semi-myopic policies. Operations research, 62(5), 1142–1167.

- Luo et al., (2024) Luo, Y., Sun, W. W., & Liu, Y. (2024). Distribution-free contextual dynamic pricing. Mathematics of Operations Research, 49(1), 599–618.

- Moore, (1990) Moore, A. W. (1990). Efficient memory-based learning for robot control. Technical report, University of Cambridge, Computer Laboratory.

- Nambiar et al., (2019) Nambiar, M., Simchi-Levi, D., & Wang, H. (2019). Dynamic learning and pricing with model misspecification. Management Science, 65(11), 4980–5000.

- Qiang & Bayati, (2016) Qiang, S. & Bayati, M. (2016). Dynamic pricing with demand covariates. arXiv preprint arXiv:1604.07463.

- Vershynin, (2010) Vershynin, R. (2010). Introduction to the non-asymptotic analysis of random matrices. arXiv preprint arXiv:1011.3027.

- Vershynin, (2018) Vershynin, R. (2018). High-dimensional probability: An introduction with applications in data science, volume 47. Cambridge university press.

- Wainwright, (2019) Wainwright, M. J. (2019). High-dimensional statistics: A non-asymptotic viewpoint, volume 48. Cambridge university press.

- Wang, (2023) Wang, K. (2023). Pseudo-labeling for kernel ridge regression under covariate shift. arXiv preprint arXiv:2302.10160.

- Wang et al., (2021) Wang, Y., Chen, B., & Simchi-Levi, D. (2021). Multimodal dynamic pricing. Management Science, 67(10), 6136–6152.

- Xu & Wang, (2022) Xu, J. & Wang, Y.-X. (2022). Towards agnostic feature-based dynamic pricing: Linear policies vs linear valuation with unknown noise. In International Conference on Artificial Intelligence and Statistics (pp. 9643–9662).: PMLR.

- Yang et al., (2017) Yang, Y., Pilanci, M., & Wainwright, M. J. (2017). Randomized sketches for kernels: Fast and optimal nonparametric regression.

- Zhao et al., (2023) Zhao, Z., Jiang, F., Yu, Y., & Chen, X. (2023). High-dimensional dynamic pricing under non-stationarity: Learning and earning with change-point detection. arXiv preprint arXiv:2303.07570.

Appendix A Proof of non-asymptotic upper bounds

This section provides detailed proofs for the non-asymptotic upper bounds stated in Theorems 1 and 2. The analysis hinges on bounding the estimation errors for the parameters and at each stage. To begin, in Section A.1, we present an overview of the proof. This section introduces key lemmas that quantify the estimation errors and leverages these results to derive regret bounds under both the large and limited time horizon regimes. The detailed proofs of the key lemmas introduced in Section A.1 are provided in Sections A.2, A.3, A.4 and A.5. Finally, Section A.6 includes auxiliary results and technical details that are essential for completing the proofs of Theorems 1 and 2.

A.1 Overview

The proof of Theorems 1 and 2 is divided into two main steps. First, we establish bounds on the estimation errors for the parameters in Stage 1, in Stage 2, as well as for the pricing strategies and used in Stages 2 and 3. These key results are presented in Section A.1.1. Building on these bounds, we then proceed to finalize the proofs of Theorem 1 and Theorem 2 in Section A.1.2 and Section A.1.3, respectively. In each case, we carefully choose the hyperparameters , , and to balance the regret contributions from different stages.

A.1.1 Analysis of each stage

In this part, we present non-asymptotic upper bounds on the estimation errors for the parameter in Stage 1, the pricing strategy in Stage 2, the parameter in Stage 2, and the pricing strategy in Stage 3.

It is important to note that the results in this section hold for any hyperparameters that satisfy the conditions specified in the lemmas. Although the same notations for constants (e.g., ) may be used across different lemmas, their values may vary depending on the context.

The first result Lemma 4 provides an upper bound on the estimation error for , obtained from the burn-in Stage 1. The proof can be found in Section A.2.

Lemma 4 (Estimation error in from Stage 1).

Building on Lemma 4, our next result Lemma 5 characterizes the deviation of the prices from the optimal price in Stage 2. The proof is provided in Section A.3.

Lemma 5 (Pricing accuracy in Stage 2).

Now it comes to our most technical Lemma 6, which concerns the estimation error in parameter from Stage 2. This lemma extends its simplified version presented earlier in Lemma 3 and is key to our analysis as it shows the effect of localized exploration. The proof of Lemma 6 is presented in Section A.4.

Lemma 6 (Estimation error in from Stage 2, full version of Lemma 3).

As shown in the bound (A.3b), introducing a localized perturbation effectively increases the eigenvalues of the matrix by , which helps address any singularities in the covariance matrix: Even if some eigenvalues are nearly zero, adding ensures that the bound remains stable and does not diverge. This stabilizing effect is essential for keeping the bound under control.

The role of adding is similar to regularization in ridge regression, where boosting the eigenvalues also stabilizes the solution. However, unlike in regression where regularization emphasizes the most informative directions, in on-line learning, the term helps mitigate the impact of under-explored or degenerate directions in the feature space.

Building on the estimation error of established in Lemma 6, Lemma 7 characterizes the accuracy of the prices used in Stage 3. The proof for Lemma 7 can be found in Section A.5.

Lemma 7 (Pricing accuracy in Stage 3).

Under the conditions of Lemma 6, there are constants and such that, if

| (A.4a) |

then with probability at least ,

| (A.4b) |

A.1.2 Proof of Theorem 1

The proof of Theorem 1 proceeds in three main steps.

We first derive a general upper bound on the regret using results from Lemmas 4, 5, 6 and 7. This bound holds for any set of hyperparameters that satisfy the conditions specified in these key lemmas.

Next, we consider the specific choice of hyperparameters as suggested by equations (4.3a)-(4.3c). We show that, under the condition (4.4) on the planning horizon , this choice effectively balances the regret contributions from each stage, achieving an optimal exploration-exploitation tradeoff. Finally, we translate the high-probability regret bound into a bound on the expected regret, completing the proof.

Let us dive into each step of the proof in detail.

Step 1: Regret bound by combining Lemmas 5 and 7.

Given that Lemmas 4, 5, 6 and 7 hold, we are now ready to derive an upper bound on the regret . To begin, let us revisit the definition of cumulative regret from equation (2.5a). By breaking it down across the three stages, we decompose the regret as follows

We will now address the regret contributions from each part separately.

| During Stage 1, the burn-in phase, under 2, the single-step regret is controlled by a (uniform) upper bound on . Therefore, we derive | |||

| (A.5a) | |||

For the remaining two stages, similar to the bound derived in (2.5b), the regret can be expressed in terms of the difference between the implemented price and the optimal price:

where the second inequality follows from 2, ensuring that the slope term satisfies . Using the bounds from Lemmas 5 and 7 for price deviations in Stages 2 and 3, we obtain

| (A.5b) | ||||

| (A.5c) |

Step 2: Balancing the terms by choosing proper hyperparameters.

Now, let us derive a specific form of the regret bound (A.6) by choosing the hyperparameters , and as suggested by equations (4.3a)-(4.3c).

First, using our choices for and from equations (4.3a) and (4.3b), we can control the regret contributions for Stages 1 and 2 as follows:

| (A.7a) | ||||

| (A.7b) | ||||

| The analysis for Stage 3 (Commitment Phase) is a bit more involved. From our choice of using equation (4.3c), we get: | ||||

| (A.8a) | ||||

| Additionally, the planning horizon condition (4.4) ensures | ||||

| (A.8b) | ||||

From Lemma 1, we know that the eigenvalues of the matrix satisfy for some constant . Therefore, we can bound the sum of inverses as

| (A.9) |

where the last inequality follows from the bounds (A.8a) and (A.8b). With our choice of from equation (4.3b), the regret contribution from Stage 3 simplifies to

| (A.10) |

Finally, combining the bounds from Stages 1, 2, and 3 ((A.7a), (A.7b), and (A.10)), we reduce the overall bound (A.6) to

| (A.11) |

This matches inequality (4.5a) from Theorem 1. By using a union bound, we conclude that this regret bound holds with probability at least , as long as the conditions in Lemmas 4, 5, 6 and 7 are satisfied.

It remains to verify that our chosen hyperparameters satisfy the conditions required in Lemmas 4, 5, 6 and 7.

We begin by verifying the conditions in Lemma 4 and Lemma 5. For the burn-in stage, we have set as specified in (4.3a). The lower bound on the planning horizon given in (4.4) ensures that and , which satisfies condition (A.1a) and the first part of condition (A.2a). Moreover, our chosen perturbation level in (4.3c) guarantees that , fulfilling the second part of (A.2a). Therefore, the conditions required by both Lemma 4 and Lemma 5 are confirmed to be satisfied.

We now proceed to verify the conditions for Lemmas 6 and 7. First, let us confirm that the condition in (A.3a) is met. This holds naturally by setting in our choice of as specified in (4.3c). Next, we need to verify that , as required by (A.3a). According to the bound derived in (A.8a), we have

By selecting a sufficiently large constant in (4.3c), we ensure that . Therefore, the condition (A.3a) is satisfied. Lastly, for condition (A.4a), we observe that

based on (A.9). This confirms that (A.4a) is also satisfied.

In summary, we have shown that our chosen hyperparameters, as specified in (4.3a), (4.3b) and (4.3c), satisfy all the conditions required by Lemmas 4, 5, 6 and 7. Consequently, this ensures that the high-probability regret bound (A.11) holds, thereby completing the proof of inequality (4.5a) stated in Theorem 1.

Step 3: Converting high-probability bounds to expected value bounds.

Above, we have shown that the regret admits an upper bound (4.12a) with probability at least . To translate this into a bound on the expected regret , we begin by defining an event and decomposing the expectation as follows

Here can be controlled by the high-probability upper bound on the right-hand side of inequality (4.12a). As for the other term , we notice that is always bounded above by a constant and even on the complement event . Therefore, we have

where we have used the property that . Combining these bounds, we obtain

which completes the derivation of the expected regret bound as stated in Theorem 1. With this, we conclude the proof of Theorem 1.

A.1.3 Proof of Theorem 2

The proof of Theorem 2 follows the same structure as the proof of Theorem 1 in Section 4.1, with the key difference being in Step 2: balancing the terms by selecting appropriate hyperparameters.

In this section, we explicitly calculate each term in the regret bound (A.6) using our chosen values for the hyperparameters , , and , as defined in equations (4.10a), (4.10b) and (4.10c). This will allow us to derive a final bound in the form of inequality (4.12a).

The detailed verification that these hyperparameter choices satisfy the conditions required by Lemmas 4, 5, 6 and 7 is provided in Section A.6.2.

We start by analyzing the contributions to the regret from the first two exploration stages in the expression (A.6). By applying our chosen parameters and as defined in equations (4.10b) and (4.10c), we obtain

| (A.12a) | ||||

| (A.12b) | ||||

We now focus on the regret incurred during the exploitation phase (Stage 3). First, using the definition of the degenerate dimension from equation (4.7), we have

| (A.13) |

Recall that our choice of the noise level satisfies the critical inequality 4.8, which implies

Given that our parameter choice ensures , we can simplify this to

| (A.14) |

We then use inequalities (A.13) and (A.14) to bound the regret term from Stage 3 in the overall regret expression (A.6). Using (A.13) along with the definition of in (4.10c), we obtain

Substituting inequality (A.14), we further simplify this to

| (A.15) |

By using the upper bounds derived in equations (A.12a), (A.12b) and (A.15), we can express the overall regret as

which corresponds to the bound stated in inequality (4.12a) in Theorem 2. This holds with probability at least by union bound.

The bound on the expected regret can be derived in a similar manner by following the argument used in Step 3 of Section A.1.2. This completes the proof of Theorem 2.

In what follows, we will prove the claims (4.13a) and (4.13b) mentioned in the comments immediately after Theorem 2.

Proof of claim (4.13a):

When is a regular solution to the critical inequality 4.8, by definition, there exists a constant such that no longer satisfies 4.8. This implies

| (A.16) |

We also observe that

| (A.17) |

By combining inequalities (A.16) and (A.17), we obtain

| (A.18) |

By plugging this upper bound for from (A.18) into the regret expression in (4.12a), we derive the refined regret bound as claimed in (4.13a).

Proof of claim (4.13b):

A.2 Proof of Lemma 4, estimation error in from Stage 1

In Stage 1, we estimate the parameters using least-squares regression. Specifically, we compute an estimate based on the dataset .

According to standard results from fixed-design regression (see Lemma 8 in Section C.1), with high probability , we can bound the error between our estimate and the true parameter as follows:

| (A.19) |

where the matrix is the empirical covariance matrix of the features and prices, given by

It is then important to ensure that matrix is well-conditioned. In particular, we can show that, if , then the inverse of satisfies

| (A.20) |

Applying a union bound, we conclude from inequalities (A.19) and (A.20) that

| (A.21) |

with probability at least .

This result (A.21) completes the proof of Lemma 4. The remaining task is to prove the condition on the covariance matrix in inequality (A.20), which we will address next.

A.2.1 Proof of inequality (A.20), trace of inverse covariance matrix

We define the population counterpart of the matrix as

This matrix represents the expected value of the random matrix , i.e. .

Our analysis relies on two key results:

| (A.22a) | ||||

| (A.22b) |

The bound in (A.22a) comes from our exploration scheme, which considers two extreme price points. Inequality (A.22b) is established using a concentration bound for sub-Gaussian random vectors.

By combining (A.22a) and (A.22b), we see that with high probability,

| (A.23) |

Therefore, we can conclude

which validates inequality (A.20).

Proof of inequality (A.22a):

We first show that the population covariance matrix is well-conditioned, i.e., .

We begin by reformulating the matrix as

Using the properties of the operator norm , we bound as

Next, we compute

By combining these bounds, we obtain

This ensures that

| (A.24) |

2 guarantees that the right-hand side of inequality (A.24) is bounded below by a positive constant. Therefore, the property in inequality (A.22a) holds.

Proof of inequality (A.22b):

Next, we show that the empirical covariance matrix is concentrated around its population counterpart . A key observation is as follows: since contexts are i.i.d. sub-Gaussian with variance proxy (as per 1) and the prices are uniformly bounded by (by 2), the combined context-price vector in Stage 1 are also i.i.d. sub-Gaussian. The variance proxy is , which is of constant order.

A.3 Proof of Lemma 5, pricing accuracy in Stage 2

To begin with, recall that the price during localized exploration is set as with . We claim that, to prove inequality (A.2b), it suffices to show that and

| (A.26) |

Specifically, if and (A.26) holds, then , this together with in Assumption 2.1 leads to , hence and (A.2b). As , the condition is ensured by setting . In what follows, we aim to prove (A.26).

Using the expressions for and from equations (3.1c) and (2.3), we have

| (A.27) |

By applying 2, which states that with , we find that, given the condition

| (A.28) |

the bound (A.27) reduces to

| (A.29) |

Now, we claim that the following bounds hold for with probability at least :

| (A.30a) | ||||

| (A.30b) | ||||

Combining the bounds (A.29), (A.30a) and (A.30b), we derive that there exists a constant such that

Therefore, by choosing , we ensure that for all in Stage 2, which verifies inequality (A.26).

In the next step, we will prove the inequalities (A.30a) and (A.30b) based on the error bound for given in Lemma 4.

Proof of inequalities (A.30a) and (A.30b):

For , note that under the assumption that is sub-Gaussian, and due to the independence between and , the term is also sub-Gaussian, conditional on . Its variance proxy is . This allows us to apply concentration results for sub-Gaussian random variables.

Specifically, for any single , with some sufficiently large constant and with probability at least , the following holds:

| (A.31) |

We use a union bound to extend this result over all in the range . By doing so, we conclude that with probability at least , the bound in (A.31) holds for all in this range.

A.4 Proof of Lemma 6, estimation error in from Stage 2

In this section, we aim to analyze the localized exploration stage and control the estimation error of the parameter .

Our parameter is estimated via linear regression using the dataset . By applying Lemma 8, we obtain that with probability at least ,

| (A.33) |

where the empirical covariance matrix is defined

| (A.34) |

The core of our analysis shows that under certain conditions, the trace of the inverse covariance matrix satisfies the following bound

| (A.35) |

Here represents the eigenvalues of matrix , which is introduced in equation (4.1).

By combining inequalities (A.33) and (A.35), we arrive at the conclusion of our analysis, as stated in Lemma 6.

Proof of inequality (A.35), trace of inverse covariance matrix:

The next critical step is to establish the trace bound in (A.35). To achieve this, we first define a “statistical dimension” as

| (A.36) |