[orcid=0000-0003-3686-0793] \cormark[1] [orcid=0009-0004-8814-8946] [orcid=0000-0002-3219-7587]

Assessing the viability of non-light water reactor concepts for electricity and heat generation in decarbonized energy systems

Abstract

Recent pledges to triple global nuclear capacity by 2050 suggest a "nuclear renaissance," bolstered by reactor concepts such as sodium-cooled fast reactors, high-temperature reactors, and molten salt reactors. These technologies claim to address the challenges of today’s high-capacity light-water reactors, i.e., cost overruns, delays, and social acceptance, while also offering additional non-electrical applications. However, this analysis reveals that none of these concepts currently meet the prerequisites of affordability, competitiveness, or commercial availability. We omit social acceptability. The cost analysis reveals optimistic FOAK cost assumptions of 5,623 to 9,511 USD per kW, and NOAK cost projections as low as 1,476 USD per kW. At FOAK cost, the applied energy system model includes no nuclear power capacity, and thus indicates that significant cost reductions would be required for these technologies to contribute to energy system decarbonization. In low-cost scenarios, reactors capable of producing high temperature heat become competitive with other low-carbon technologies. We conclude that, for reactor capacties to increase significantly, a focus on certain technology lines ist necessary. However, until a concept becomes viable and commercially available, policymakers should prioritize existing technologies to decarbonize energy systems.

keywords:

nuclear power \sepdecarbonized energy system \sepnuclear renaissance \sepnon-light water reactors \sepcogeneration \sepenergy system model \sepnon-electrical applicationsAnalysis of historical and ongoing non-electrical applications of nuclear power

Assessment of the viability of different reactor concepts for such applications

Detailed cost analysis for proposed non-light water reactor concepts

Energy system modeling of nuclear cogeneration with parallel renewables expansion

1 Introduction

There is a broad consensus that decarbonizing energy systems is necessary to limit global warming and reduce the potentially hazardous effects of climate change [1]. However, extensive debates exist on the means to this end, especially regarding the technologies that are part of a cost-efficient and executable solution. In these debates, nuclear power is often considered a low-carbon technology that will play a significant part in global energy system decarbonization [2, 1], albeit existing uncertainties regarding the cost-efficiency and availability of this technology [3, 4, 5, 6, 7, 8]. In the last decade, these prospects have launched a narrative of a so-called "nuclear renaissance" coinciding with the promotion of so-called new reactor (SNR) concepts, or "advanced" reactor technologies [9, 10]. This is supported by recent governmental proclamations of plans to triple the installed nuclear power plant capacity by 2050 [11].

These ambitious expansion targets stand against a number of challenges that the industry is currently facing [7], including cost escalations when building new high-capacity light water reactors (LWR) [3, 4], uncertainty regarding the availability of so-called "small modular reactors" (SMR) and other "advanced" reactor concepts [5] as well as a limited actor base [12]. These challenges raise concerns about whether the nuclear industry will be able to live up to the high expectations raised by proponents of the proclaimed nuclear renaissance.

Currently, several SNR concepts are being developed. According to a 2023 report by the U.S. "Committee on Laying the Foundations for New and Advanced Nuclear Reactors" [13, p.43], these concepts must fulfill four conditions to be competitive in an energy system with a high share of fluctuating renewables: They must be 1) "affordable for owner investment without ’betting the company’", 2) "economically competitive with other technologies […]", 3) "socially acceptable", and 4) "commercially available." This coincides with required overnight construction costs in the range of 2000 to 6000 USD per kW and the establishment and diffusion of non-electrical uses for nuclear power plants [14, 15, 13]. However, there is a considerable discrepancy between cost assumptions or projections and actual costs of high capacity LWR projects, especially in OECD countries [8]. For SMR and SNR concepts, limited operational experience hinders the availability of accurate cost and other performance data [7]. Especially for SMR concepts, manufacturers’ cost projections appear somewhat optimistic compared to production theory [5]. Nonetheless, smaller sizes, non-electrical uses, and other benefits of nuclear, such as reliability and flexibility, could increase the competitiveness of both SNR and SMR concepts [16, 17, 18].

Further, most previous studies limit their assessment of the role of nuclear power in future energy systems to existing technologies (i.e., high capacity LWRs) and electricity production [14, 19, 20, 8]. At the same time, some literature refers to "advanced" reactor technologies with links to (thermal) storage options (e.g., [2, 21]). However, to our knowledge, a gap exists regarding the detailed assessment of the potential of non-electrical applications for nuclear power. Further, a model-based consideration of the potential non-electrical applications of different nuclear reactor concepts is missing due to the limitation of previous studies on a single respective reactor design.

Thus, in this work, we assess the potential validity of SMR and SMR concept applicability in future energy systems, including non-electrical applications, by following a three-step approach. First, based on an extensive literature assessment, we investigate potential non-electrical applications of nuclear power, e.g., for heat applications, and discuss technology availability. Second, we discuss the potential costs for each technology based on an analysis of 51 references. Third, based on the prior steps, we investigate the economic efficiency of these technologies by integrating them into a European energy system model [22] with the ability to generate both electricity and heat. Assuming SNR technologies become commercially available, we find that costs must be reduced substantially, i.e., well below current LWR project costs in Europe, and reactor concepts compete mainly for heat provision in which competitive low-carbon technologies are similarly expensive.

The remainder of this work is structured as follows. Section LABEL:background provides the main results of the literature assessment on use cases and technology availability, and of the cost data analysis. Section 3 introduces the applied energy system model and relevant assumptions and data. The results of the energy system model are presented in Section 4, and are discussed in Section 5. Section 6 concludes. Further background information is provided in the Appendix.

2 Background

LABEL:background

This section gives an overview of potential non-electrical use cases for nuclear power and of reactor concept availability. Further, we provide an assessment of cost projections for these currently commercially unavailable reactor concepts. This section provides relevant background information for the implementation of the energy system model regarding scenario definition and technology selection.

2.1 Potential Non-electrical Applications of Nuclear Power

Despite the dominance of LWRs in today’s global nuclear fleet, which is mainly used to generate electricity [23], the cogeneration of electricity and heat has been the subject of literature and technology development for decades, as in general, nuclear reactors are already "heat generation devices" [24, p. 23]. Csik and Kupitz [24] further differentiate between reactors intended for heat generation only and those that can also produce electricity, allowing some degree of flexibility. However, cogeneration experience remains limited to individual applications; see Appendix A. This results from the low-level output temperature from LWRs, which limits the economic retrievability of energy. However, this output temperature could theoretically be raised at the expense of electricity generation [25].

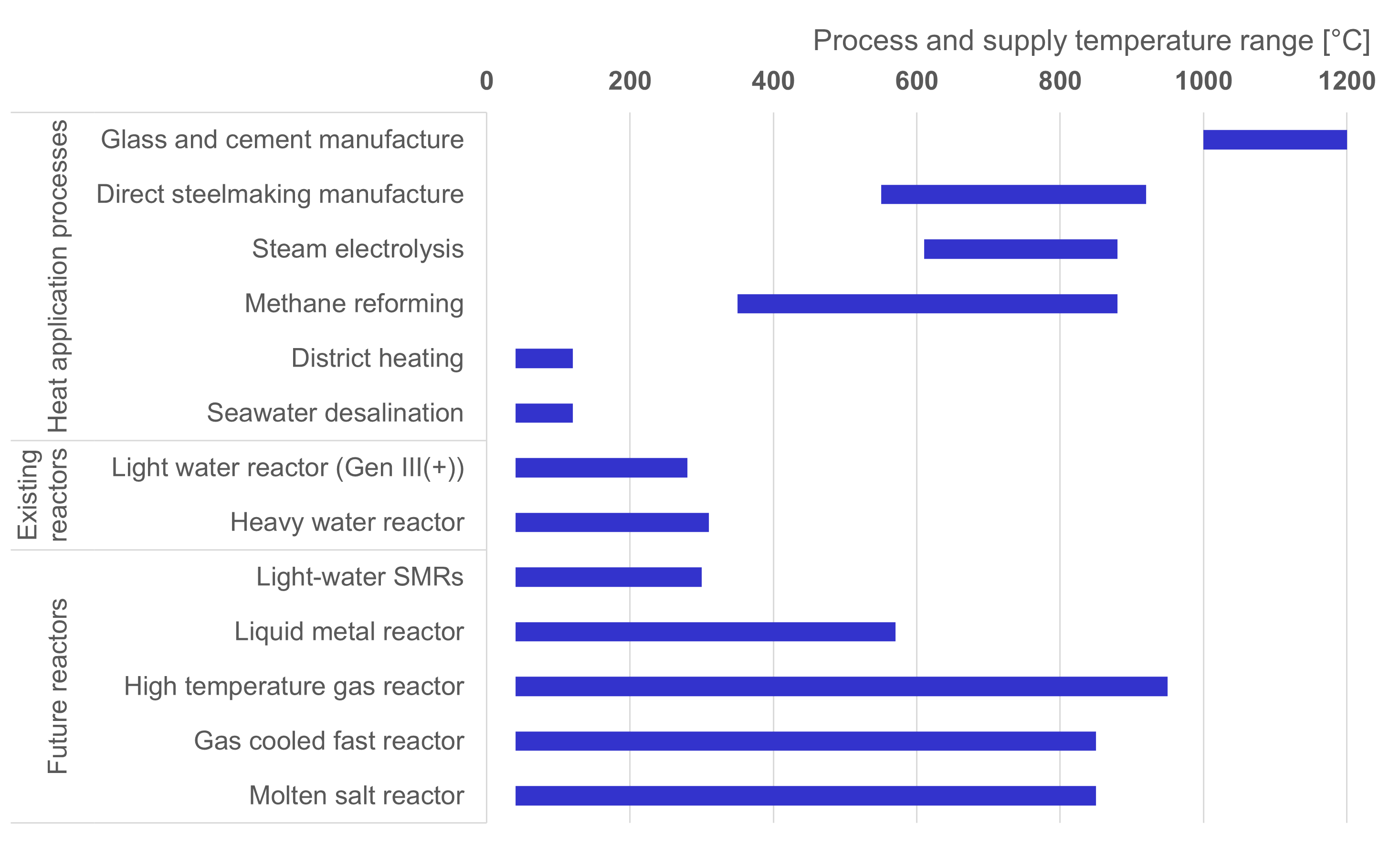

The remainder of this section provides an overview of the potential applications of nuclear power plants for non-electrical uses, such as the provision of industrial and district heat. An overview of possible applications and potential reactor types is shown in Figure 1, and several agency reports provide detailed overviews of potential applications of nuclear cogeneration [26, 27, 28, 29]. A list of nuclear power plants used for non-electrical energy provision is provided in Appendix A, showing that historical applications are limited to individual plants.

2.1.1 District Heat

Nuclear power reactors have been supplying low-temperature heat up to 100°C for district heating for decades [30, 31]. While there are issues related to acceptance, e.g., addressing the proximity to populated areas [13], regulation, e.g., regarding the establishment of emergency planning zones [31, 18], as well as technology, e.g., the challenge of efficiency losses when transferring heat over long distances [25, 17], SMRs and SNRs are thought to be especially applicable to this use case [31]. There have been several attempts to design reactors specifically for district heating in Sweden, Finland, and China [30, 31]. Mostly in Eastern Europe, there exists decade-long experience with district heating via nuclear cogeneration, for example, at the Kozloduy plant in Bulgaria, the Bohunice V-2 plant in Slovakia, or the Paks plant in Hungary. The heat is used for small demand centers nearby [32, 29]. Additionally, in 2019, two Westinghouse AP1000 reactors began providing district heat to the city of Haiyang in China [33].

2.1.2 Process Heat for Industry

Decarbonizing the provision of heat for industrial processes such as cement production and steel manufacturing is challenging as most processes require heightened temperature levels of several hundred °C and a near-constant provision of energy [34]. For decades, it has been argued that nuclear power can provide both the required heat and capacity. For example, current high-capacity LWRs can theoretically produce heat ranging from 200 to 300 °C, applicable for pulp, paper, and textiles manufacturing or seawater desalination (see Section 2.1.4), and advanced gas-cooled reactors currently operating in the U.K., can provide heat up to 650°C, a temperature level relevant for the chemical industry [24]. So far, however, experience is limited to individual, mostly low-capacity demonstration projects that use mainly excess heat from electricity generation. Examples include the Calder Hall gas-cooled reactors, built in the 1950s in the U.K., which provided steam to the nearby Windscale reprocessing plant, or the Gösgen plant in Switzerland, which has been supplying heat to a nearby cardboard factory using 1% of its steam since 1979 [35]. In Canada, the Bruce heavy-water nuclear plant provided heat for its own usage but also to a greenhouse, an ethanol plant, and a plastic film production plant, amongst others, covering distances of over six kilometers [32]. The Norwegian boiling heavy water research reactor in Halden provided heat that would have otherwise been dissipated into a nearby river to a paper mill until the reactor was closed in 2018 [28].

2.1.3 Hydrogen Production

The use of hydrogen in industrial processes, but also for energy storage, is becoming increasingly relevant in decarbonization efforts [36, 34]. In general, there exist two ways in which nuclear energy could be utilized for hydrogen production. Either via heat provision for steam methane reforming [37] and for other thermo-chemical processes such as sulfur-iodine hydrogen production at temperatures greater than 750°C [38, 39], or via the generation of electricity for an electrolyzer, which would lead to further competition with renewables and raise efficiency concerns [38, 40]. Pinsky et al. [41] assess the applicability of so-called nuclear hybrid systems for hydrogen production and conclude that most currently available technologies for which nuclear could become competitive remain commercially unavailable. This assessment is supported by the lack of commercial nuclear hydrogen production projects, such as the scrapped U.S. Department of Energy project [37, 42].

2.1.4 Other Applications

Other non-electrical nuclear power applications include marine propulsion technology, most recently applied in Russia for the Akademik Lomonosov [23], and in nuclear submarines [43]. Other nuclear propulsion devices are used in outer space [26]. Seawater desalination is a particular use case for nuclear power applied at several locations [44]. Different desalination processes require different forms of energy, such as electricity (reverse osmosis) or heat (multi-effect distillation or multi-stage flash) [45], and are thus applicable to different reactor types or configurations. Required temperatures range from 200 to 300 °C [24]. Operational experience is limited to Japan, where since 1978, one BWR and seven PWRs use district heat for small seawater desalination plants, to Kazakhstan, where the first nuclear desalination facility at Aktau operated a sodium-cooled fast reactor from 1973 to 1999, to several Russian civilian nuclear-powered ships, operated since the 1980s, and to the Diablo Canyon power plant in California [46, 32].

2.2 Nuclear Technologies and Availability

The nuclear industry has been in decline for several decades, especially in OECD countries, as only a few projects were realized, which were behind schedule, well over budget, and resulted in a decline of major industry actors (e.g., the bankruptcy of Westinghouse) [12]. Most discussed nuclear technologies are either unavailable or economically disadvantageous compared to other low-carbon technologies, and thus, new-builds are mainly realized in state-owned spheres, especially in China and Russia [4, 23]. Regardless, ambitious expansion plans for nuclear power are being publicly announced [11], and nuclear power continues to play a significant role in energy scenarios [1]. While the global nuclear fleet is dominated by high-capacity LWRs, electrical and non-electrical applications are envisioned to be implemented by using LWRs with capacity of less than 300 MWel (referred to here as "small-modular reactors" (SMRs)) and so-called "new reactor concepts" (SNR), also referred to as "advanced" or "Generation IV" reactors, that comprise several non-light water reactor concepts [7, 29]. These alternative concepts must also fulfill four prerequisites to be viable for large-scale deployment in a future decarbonized energy system. They must be 1) affordable, 2) economically competitive with other low-carbon technologies, 3) socially acceptable, and 4) available on a commercial scale [13]. In the following, we briefly discuss these prerequisites for often discussed reactor types, while omitting questions of social acceptance. See Appendix B for more technical details and information on past and ongoing research and development for the here-discussed non-light water reactor technologies.

2.2.1 Light Water Reactors

High-capacity LWR

High-capacity light water reactors (LWR), i.e., reactors exceeding capacities of 300 MWel, referred to also as "Generation III(+)" reactors, dominate global reactor fleets today [23]. These reactors are usually operated as "baseload" plants with relatively high capacity factors and are mostly limited to electricity production. As discussed in Section 2.1, individual plants have also produced district or process heat. Currently, the construction of new plants is limited mostly to Russian and Chinese projects and will have to compensate for aging reactor fleets facing closure [23]. Projects in Europe and the U.S. are pained by cost and construction duration escalations [3], and a limited actor base shows an industry in decline [12]. Thus, it is highly questionable whether these reactor types will be available on a sufficient scale for energy system decarbonization in the coming decades [7]. Independent and reliable cost data is available for Western (OECD) countries [16]. At current cost levels, LWRs are not economically competitive against renewable energies in a low-carbon energy system [47, 8]. Nonetheless, assuming that aging fleets were to be replaced with new reactors, flexible operation and heat provision are technically feasible and could bring benefits to a system characterized by a high degree of renewables, such as lower system operational costs, increased reactor owner revenues, and reduced curtailment of renewables [19].

Small Modular Reactors (Low-capacity LWRs)

SMRs are envisioned to reduce costs compared to LWRs mainly due to modularization and factory production of components, facilitated regulation, passive safety systems, and shorter construction times that would reduce capital costs, amongst others [48, 5]. Further, SMRs are proposed for niche applications, such as energy-intensive operations in remote locations [49]. In 2014, Liu and Fan [50] assumed that light water SMRs could be on a high technology readiness level of 7 to 8 and could be elevated to level 9, i.e., the operation of a functioning system, within the next ten years because of experience of similar reactor concepts in the 1950s and 1960s. However, the transferability of knowledge from early concepts should be questioned, primarily due to increased safety requirements for nuclear reactors [51]. Operation and construction experience of SMRs is limited to a small number of research and prototype reactors that have, in parallel to their high-capacity counterparts, also suffered from decade-long construction times or are still in the licensing stage and remain years away from actual operation [7, 52]. Additionally, to be economically competitive with other low-carbon technologies, SMRs would first have to overcome diseconomies of scale, and even then, cost projections by manufacturers are likely overly optimistic [5]. Nonetheless, SMRs are considered for potential non-electrical applications. For example, the NuScale VOYGR is expected to be able to provide a pre-heated feedstock of heat for refinery processes at around 300 °C [45], and it is supposed to be compatible with a high-temperature electrolyzer for hydrogen production [45, 53, 37]. The only VOYGR order, however, was canceled in late 2023 due to cost escalations [54].

2.2.2 Reactors with Fast Neutron Spectra

Reactors operating on a fast neutron spectrum, so-called fast breeders (FBR), were historically considered to be part of historical nuclear capacity expansions in a so-called "plutonium economy" [55, 56]. The envisioned fuel cycle would reuse plutonium from spent fuel via reprocessing and MOX-fuel fabrication to decrease the demand for natural uranium (referred to as the closed fuel cycle) [57]. Proponents envisaged that FBRs would replace LWRs and energy would become "too cheap to meter" [58][p. 9]. There have been several attempts to establish FBRs for large-scale energy generation, but none have succeeded on a commercial scale [59]. The following section briefly addresses the two most common types, sodium-cooled fast reactors (SFR) and lead-cooled fast reactors (LFR). Gas-cooled fast reactors are omitted due to the lack of prototypes, see Appendix B.

Sodium-cooled Fast Reactors

SFRs were amongst the first reactor concepts to be developed in the wake of feared uranium source depletion that would ultimately render LWRs inoperable. However, while projected nuclear capacity expansions did not formulate and new uranium deposits were discovered, the economic deficiencies and the high technological complexity of SFRs remained, and a large-scale commercial deployment never happened [60, 61]. SFR projects are characterized by project failures rather than operational reactors, and due to, e.g., the high reactivity of sodium with air and water, operational reactors are unreliable [7]. Regardless, four SFRs are currently under construction [62], and increased thermal efficiency coupled with outlet temperatures of 400 to 450°C could make SFRs applicable for non-electrical applications in niche markets, despite economic deficiencies stemming mostly from additional safety requirements [63]. Current projects include a 345 MWel SFR coupled with a molten salt tank, designed by U.S.-company TerraPower, currently undergoing pre-licensing activities with regulators [23].

Lead-cooled fast reactors

Lead-cooled fast reactors (LFR) operate similarly to SFRs, but use lead as a coolant. Lead is less reactive than sodium and could thus reduce operational risks and necessary safety barriers [64]. However, operational experience is almost exclusively limited to Russia, where LFRs were experimented with for submarine propulsion, and a single reactor is currently under construction [60]. Further, a demonstration LFR with an accelerator-driven system is currently under development in Belgium (MYRRHA) [63]. Due to limited operational experience, cost information is scarce. However, it is expected that LFRs could be cheaper than SFRs due to reduced safety risks, and if a closed fuel cycle can be implemented, LFRs might also compete with current LWRs [64].

2.2.3 High temperature reactors

Like other non-light water reactor technologies, operational experience for high-temperature reactors (HTR) is also limited. Developed in the 1960s to operate on thermal spectra, different reactor concepts, such as the Dragon reactor in the UK or the pebble-bed reactor THTR-300 in Germany, were constructed as prototypes but faced significant technological challenges and were thus abandoned [63]. Current operational reactors are limited to China, where two prototypes based on the German pebble-bed design are running. In the U.S., X-energy is working on an 80 MWel HTR, the Xe-100, which is still in the design phase [65, 7]. Given their high operational temperature, HTRs are envisioned to be applicable for high-temperature heat provision of up to 1000°C [16, 63]. For example, a proposed design for a gas turbine modular helium reactor could produce outlet temperatures of 950°C and could be applied for sulfur-iodine hydrogen production with a process efficiency as high as 51% [66]. Potential cost disadvantages compared to LWRs, stemming from more complex designs, could, theoretically be offset by the provision of valuable high-temperature heat [67].

2.2.4 Molten salt reactors

Molten salt reactors (MSR) use molten salt as a coolant [68]. MSRs were initially developed for aircraft propulsion, and concepts vary regarding moderator, fuel, neutron spectrum, and fissile material. There are no commercially operational MSRs, but several concepts are currently under development in China, Switzerland, and Russia, amongst others [63]. MSRs could become applicable for heat provision in decarbonized energy systems as the proposed salts melt at around 500°C and boil at around 1400°C, allowing for outlet temperatures ranging from 600 to 700°C [68, 63]. Most MSR concepts are still in the early development stages, so information on their economic competitiveness is limited. While in the 1970s, capital costs of MSR were estimated in the same range as LWRs [69], current concepts are estimated to be cheaper. For example, the so-called "Advanced High-Temperature Reactor," also referred to as "Fluoride High-Temperature Reactor," is estimated to cost less than 1000 USD per kW, and the ThorCon concept MSR, developed by company Martingale, is envisioned to produce electricity for as little as 30 to 50 USD per MWh [70, 63].

2.3 Nuclear Cost Data Projections

Over the last decade, nuclear power has gained momentum in energy scenarios as a low-carbon technology. For example, over 80% of scenarios collected in the 6th Assessment Report of the IPCC show that to limit global warming to 1.5°C by the year 2100, it is necessary to increase absolute electricity generation from nuclear with an average annual growth rate of 3% [1, 7]. These models assume substantial overnight construction cost reductions for nuclear in the coming decades down to 5,000 or even 2,000 USD per kW [20] and highlight the necessity of cost reductions for nuclear to be competitive in energy systems with high shares of renewables [2, 71].

Thus, to assess the economic efficiency of non-light water reactors in the energy system model (see Section 3.1), it is first necessary to determine relevant cost data and other relevant information on potentially viable reactor types. Consequently, we conducted a literature analysis of cost projections and assumptions for various reactor types. Previous research has shown that for high-capacity LWRs, cost projections and experience differ strongly [8]. For SMR concepts, Steigerwald et al. [5] show that to-be-expected costs and industry expectations also vary substantially.

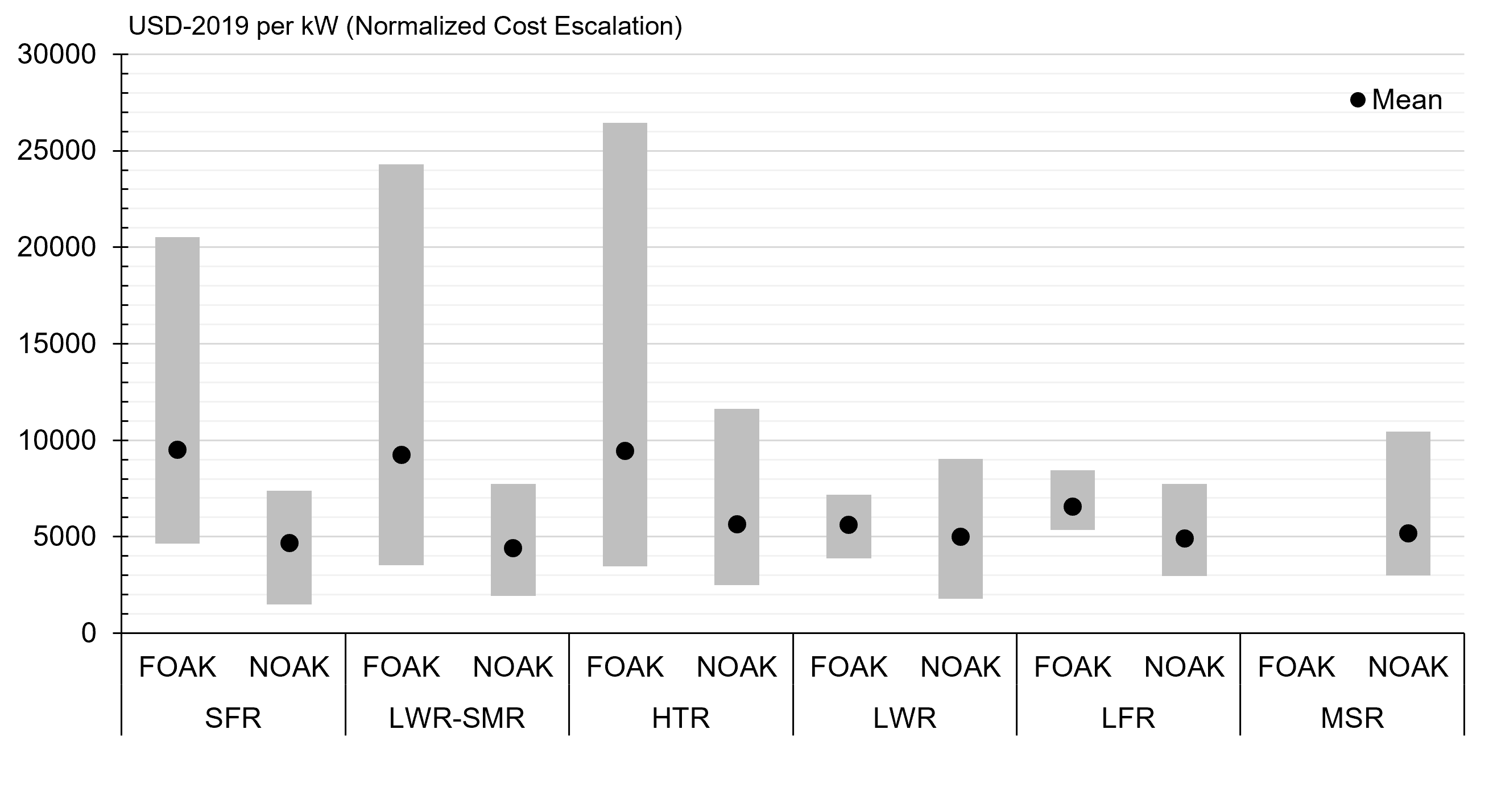

The here presented cost analysis is based on 51 references [72, 73, 3, 63, 74, 75, 76, 77, 78, 66, 79, 80, 81, 82, 83, 84, 85, 86, 87, 88, 89, 90, 91, 92, 93, 16, 94, 95, 96, 97, 98, 99, 100, 101, 102, 103, 104, 105, 106, 67, 15, 107, 108, 109]. About 60% are so-called grey literature, mostly industry and research organization reports. Peer-reviewed literature, i.e., journal and conference papers, account for about a third. Most references date from the 2010s, but given that the current decade is only four years old, it is remarkable that almost 40% were published in 2020 or later. A detailed overview of cost data and the corresponding references is given in the Appendix C.

Overnight construction cost (OCC) data are provided on different "readiness levels," i.e., either as so-called "first-of-a-kind" (FOAK) or "n-th-of-a-kind" (NOAK) estimates. FOAK cost estimates acknowledge that the first built reactor of a given type will likely experience unexpected complications and thus be more expensive than subsequent projects of the same design. NOAK cost estimates consequently assume that some learning process reduces unit cost [110]. Learning rates for nuclear vary and, depending on the assessment and data, range from 2 to 15% [111]. However, negative learning rates have also been observed [112]. n indicates the number of units produced to reach a certain cost level. In general, NOAK costs are calculated following Eq. 1 with the cost for the n-th produced unit NOAKn, the cost for the first produced unit FOAK, learning rate x and doubling d of production volume n [110].

| (1) |

Regardless of the readiness level, every value constitutes either an estimation or projection, as none of the discussed reactors have been built. Furthermore, from our gathered literature, we find that only Stewart et al. [94] and Stewart and Shirvan [111] attribute a concrete value to n, i.e., 10. Additionally, in both references, the FOAK starting point is far off from historical precedence, especially for high-capacity LWRs [8]. Regarding learning rates and the feasibility of industry cost reduction projections, refer to Steigerwald et al. [5] who assess learning rates and potential cost reductions for 19 SMR and advanced reactor concepts. For the following, cost data was normalized and adjusted to 2019-USD following the "cost escalation approach" by Abou-Jaoude et al. [113] to ensure comparability. 111If not otherwise indicated, all USD values are in 2019-USD.

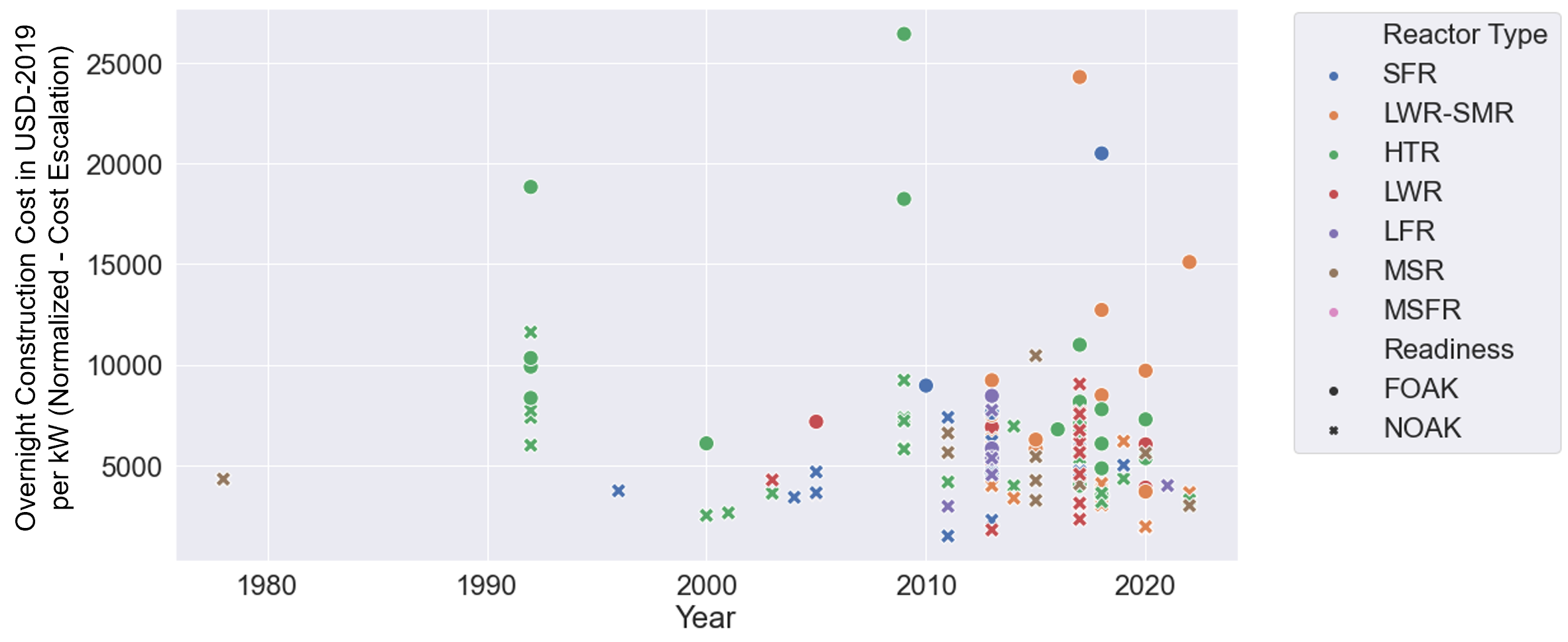

Figure 2 shows the variation of cost data between reactor types and readiness levels. FOAK cost data are not available for MSRs. In general, NOAK estimates are more numerous than FOAK estimates. Further, on average, NOAK estimates are lower than FOAK estimates by several thousand USD per kW . This indicates widespread expectations of future cost digressions despite lack of precedence [114, 112, 12]. Figure 3 shows the distribution of OCC values over time. The x-axis shows either the publication year or, if available, the stated reference year. Tables 4, 5 and 6 in Appendix C summarize cost data for OCC, as well as for fixed and variable operational costs for various reactor types. Fewer data points were identified for these cost data than for OCC, and information could not be found for each reactor type.

3 Methodology

The following section describes the methodology used to assess the economic viability of non-light water reactors in a future European energy system. First, we introduce the applied energy system model. Then, we motivate the selection of four reactor technologies for our application based on previous sections, and finally, we describe our cost assumptions, also based on previously discussed analyes.

3.1 Applied Energy System Model

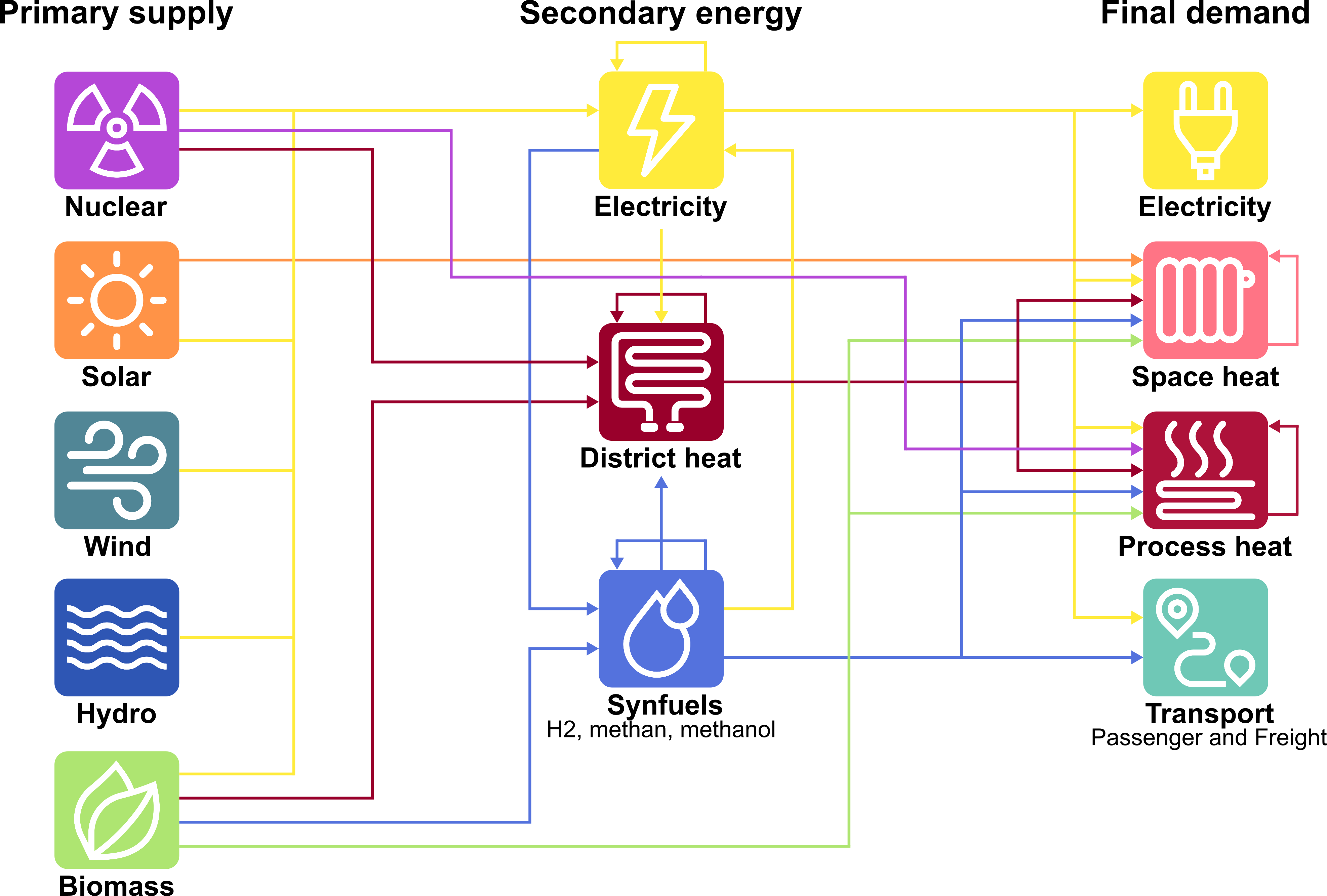

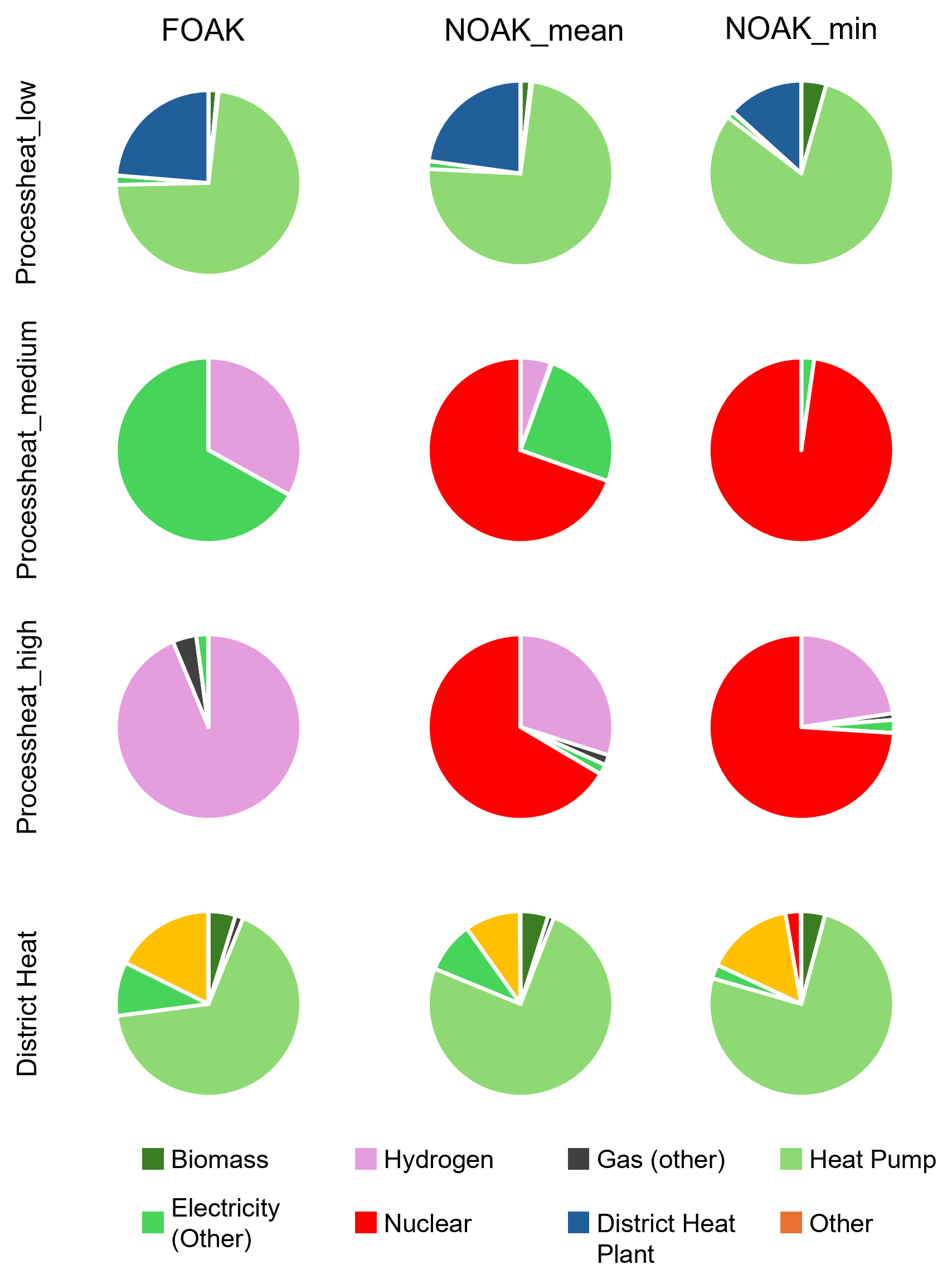

This work applies a comprehensive energy system model to assess different reactor concepts. It utilizes the AnyMOD.jl framework for energy system modeling [22]. Fig. 4 gives an overview of the energy vectors in the model. Sources of primary energy supply in the left column include nuclear and renewables, i.e., solar, wind, hydro, and biomass. The middle column of Fig. 4 lists the secondary energy carriers that can be generated from the primary supply and include electricity, district heat, and various synthetic fuels, including hydrogen, synthetic methane, and methanol. Finally, the right column shows the types of final energy demand that the model must cover. These include final demands for electricity, space heat, and process heat, respectively. The demand for process heat is further subdivided into three levels: low temperature up to 100°C, medium temperature from 100°C to 500°C, and high temperature above 500°C. Finally, the model also covers the demand for transport services, specifically private road, public road, and public rail transport for passengers and freight transport on heavy road, light road, and rail. As indicated in the figure, the model considers nuclear power not just as a source of electricity but also for the provision of district and process heat, as described in Section 3.2. [8]

The model is formulated as a linear optimization problem that decides on capacity investment and operation of capacities to satisfy a fixed final demand at the lowest cost possible. Investment options are different technologies to transport, convert, store, and generate different energy carriers, see Fig. 4. Technology data and demand are based on projections for the year 2040. The Appendix D gives an overview of the considered technologies besides nuclear power.

The spatial scope covers the European Union (excluding isolated island states), the U.K., Switzerland, Norway, and the Balkan region. The temporal scope consists of a single future year in a greenfield setting. Due to their long lifetimes, existing hydropower plants and power grids are available without additional investment. The model uses hourly profiles based on historical data from 2008 for electricity and heat demand as well as renewable capacity factors.

The spatial resolution of the model varies by context. For the characteristics of renewables, all types of heat and hydrogen, the spatial scope is split into 96 clusters. For the electricity balance and transport demand, the scope is split according to the zonal configuration of the European power market. Appendix E details the spatial configuration and the available transport infrastructure to exchange energy between regions. [8, 115]

3.2 Applied Nuclear Technologies and Assumptions

From the analysis of use cases and available technologies (see Sections 2.1 and 2.2) and the available cost data presented in Section 3.3 below, we derive the necessary input parameters for a total of four different reactor technologies to be implemented into the model. These are high-capacity (advanced) light-water reactors (LWR), low-capacity light-water reactors (SMR), sodium-cooled fast reactors (SFR), and high-temperature gas-cooled reactors (HTR). Each technology is assumed to be able to supply a particular form of heat in addition to electricity, see Table 1.

| Technology | Energy Carrier |

| LWR | Electricity; districtHeat |

| SMR | Electricity; processHeat_low |

| SFR | Electricity; processHeat_medium |

| HTR | Electricity; processHeat_medium; processHeat_high |

Nuclear power is sometimes portrayed as a dispatchable technology that could bring benefits to an energy system characterized by a high penetration from renewables [19, 116, 117]. Further assumptions relate to individual reactor technologies’ abilities to switch operational modes. We assume that reactors can flexibly switch from electricity to heat provision and vice versa without any downtime or incurred cost. Providing heat increases thermal efficiency levels by an average of 20%. Additionally, the reactors in the model operate without ramp-up time at a universal 90% capacity factor.

3.3 Nuclear Cost Assumptions

From obtained OCC data, total capital costs are calculated following Rothwell [118] by accounting for a uniform seven years of construction time and weighted average cost of capital of 10%. Input parameters that differ depending on reactor type and readiness level are given in Table 2. Due to the heterogeneity of provided data, OM costs are combined from fixed and variable values following the approach used in Göke et al. [8]. They explicitly exclude fuel costs that are included as a spererate value. Further, we assume uniform capacity factors of 90% and operational lifetimes of 40 years. To match other model input cost parameters, cost data for nuclear given in USD-2019 were converted to EUR-2020 with an inflation rate of 1.4% and an exchange rate of 0.8929.

| Readiness Level | Input Parameter | SFR | LWR | SMR | HTR |

| FOAK | OCCa | 9,511.47 | 5,622.9 | 9,241.42 | 9,438.52 |

| OMb | 50.48 | 27.03 | 47.49 | 45.29 | |

| Fuel costb | 11.9 | ||||

| NOAK (mean) | OCCa | 4,677.97 | 4,983.78 | 4,407.51 | 5,649.65 |

| OMb | 19.93 | 20.45 | 20.82 | 33.65 | |

| Fuel costb | 9.16 | ||||

| NOAK (min) | OCC | 1,476 | 1,782.62 | 1,940 | 2,501.33 |

| OMb | 13.31 | 8.37 | 15.05 | 3.13 | |

| Fuel costb | 9.16 |

4 Results

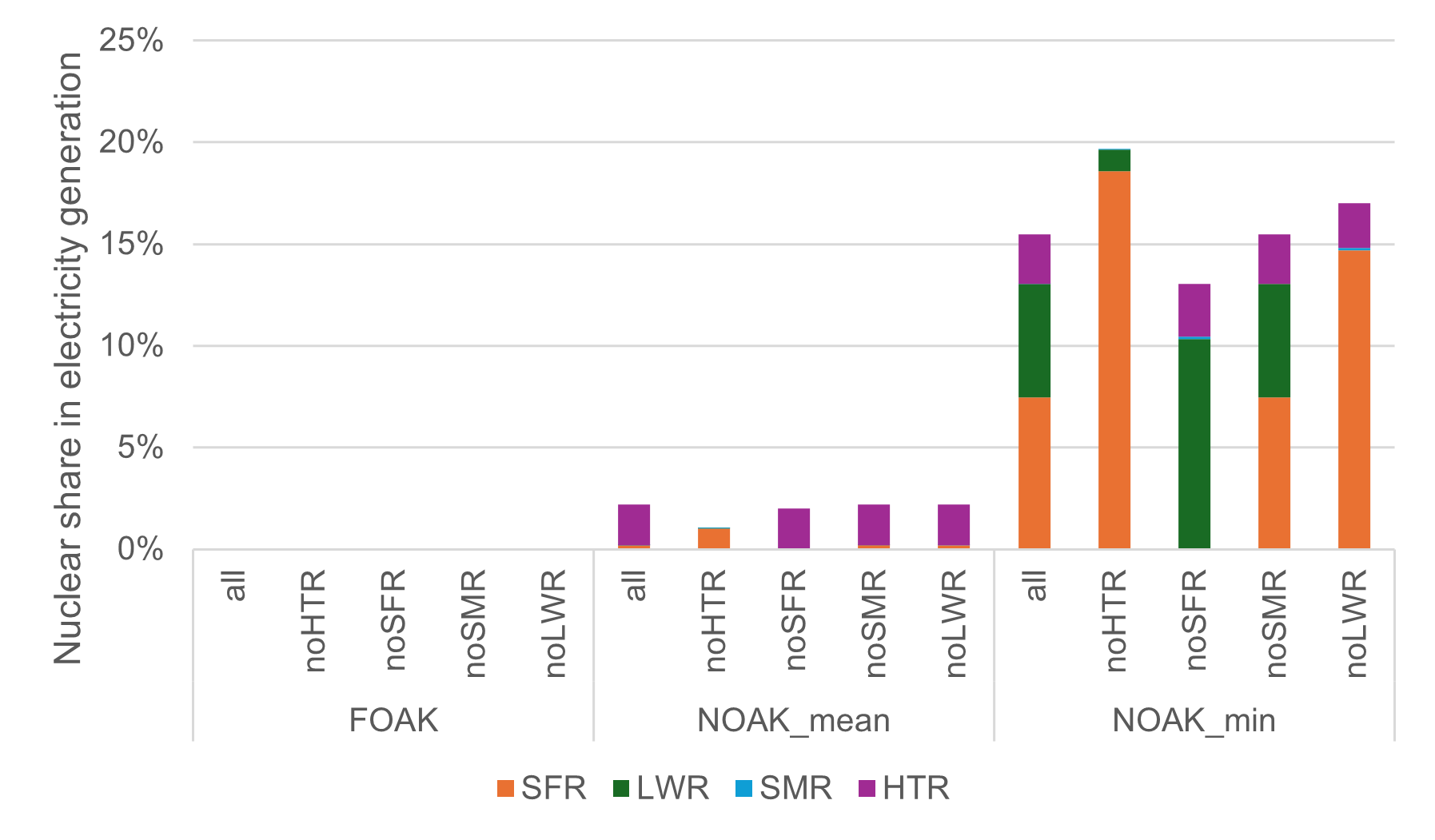

This section presents the results for three overall cost scenarios and model runs. The first assumes mean FOAK costs for each technology, the second mean NOAK costs, and the third minimum NOAK costs, see Table 2. Each of these scenarios contains five model runs. The resolution of each run is 4392 hours. While the first run assumes all four reactor technologies may be built, the other four each exclude one type (e.g., "noHTR" forbids the construction of HTRs). The model runs reflect potential variations in availability and indicate which nuclear technologies are dominated by the others. The results show the strong dependency of system design on input costs. Over all subsequently discussed technology input variations, FOAK cost assumptions lead to a de-facto exclusion of all assumed nuclear power technologies. In contrast, nuclear capacity is added to the system once mean NOAK costs are applied. In the following, we analyze the generation of electricity and heat and necessary capacity developments.

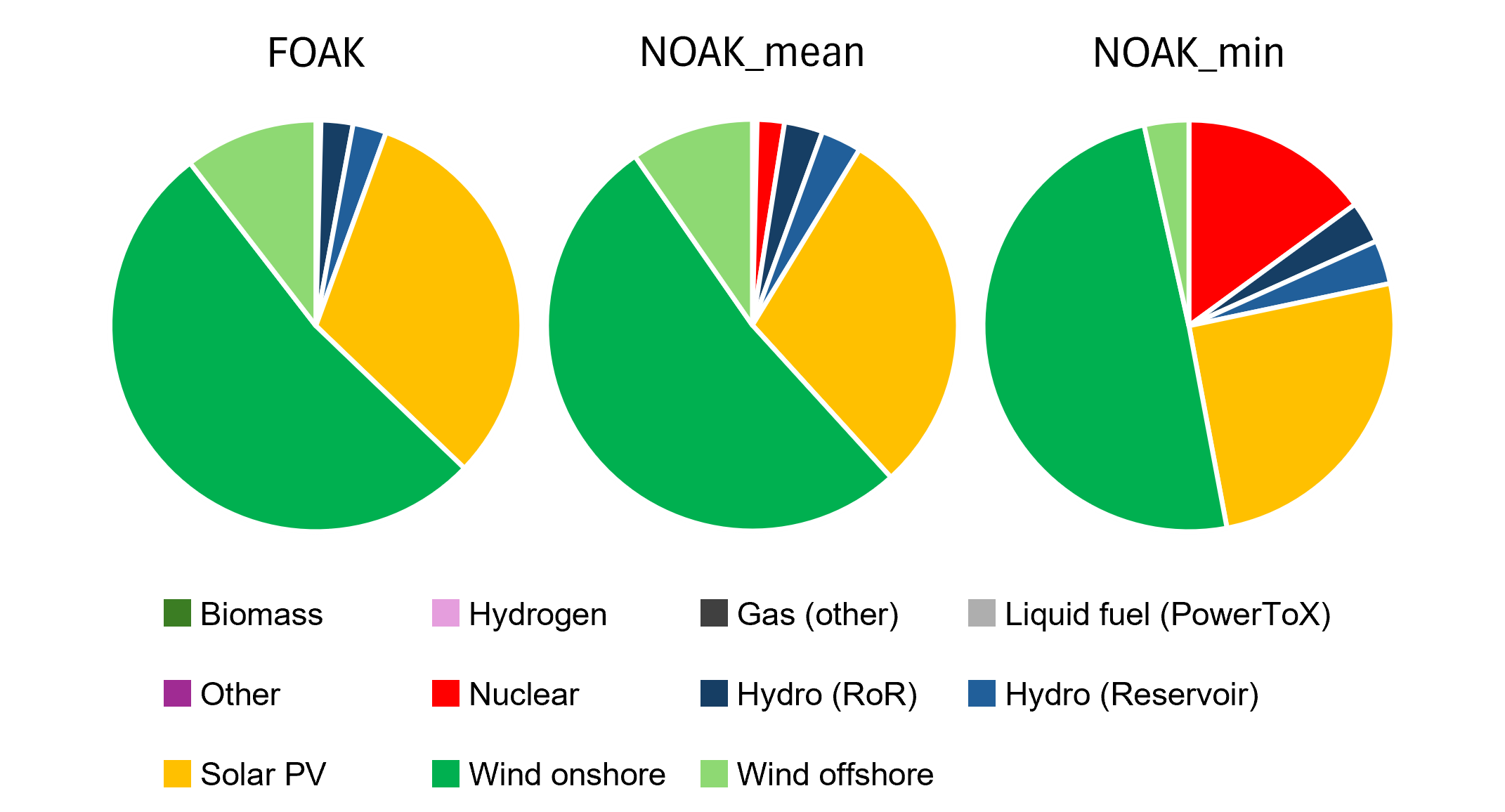

Figure 5 shows the cumulative share of nuclear in total electricity generation, while the composition of the electricity mix is shown in Figure 6. In FOAK scenarios, total electricity generation is around 7,472 TWh. For mean NOAK scenarios, electricity generation is at approximately 6,200 TWh, apart from scenario noHTR in which an additional 581 TWh of electricity is generated to cover the missing high process heat provision from HTRs. The lowest electricity generation of around 5,712 TWh is produced in the noSFR scenario for minimum NOAK cost. In these low-cost scenarios, average electricity generation lies at 5,918 TWh, with one outlier in the noHTR scenario (6,518 TWh).

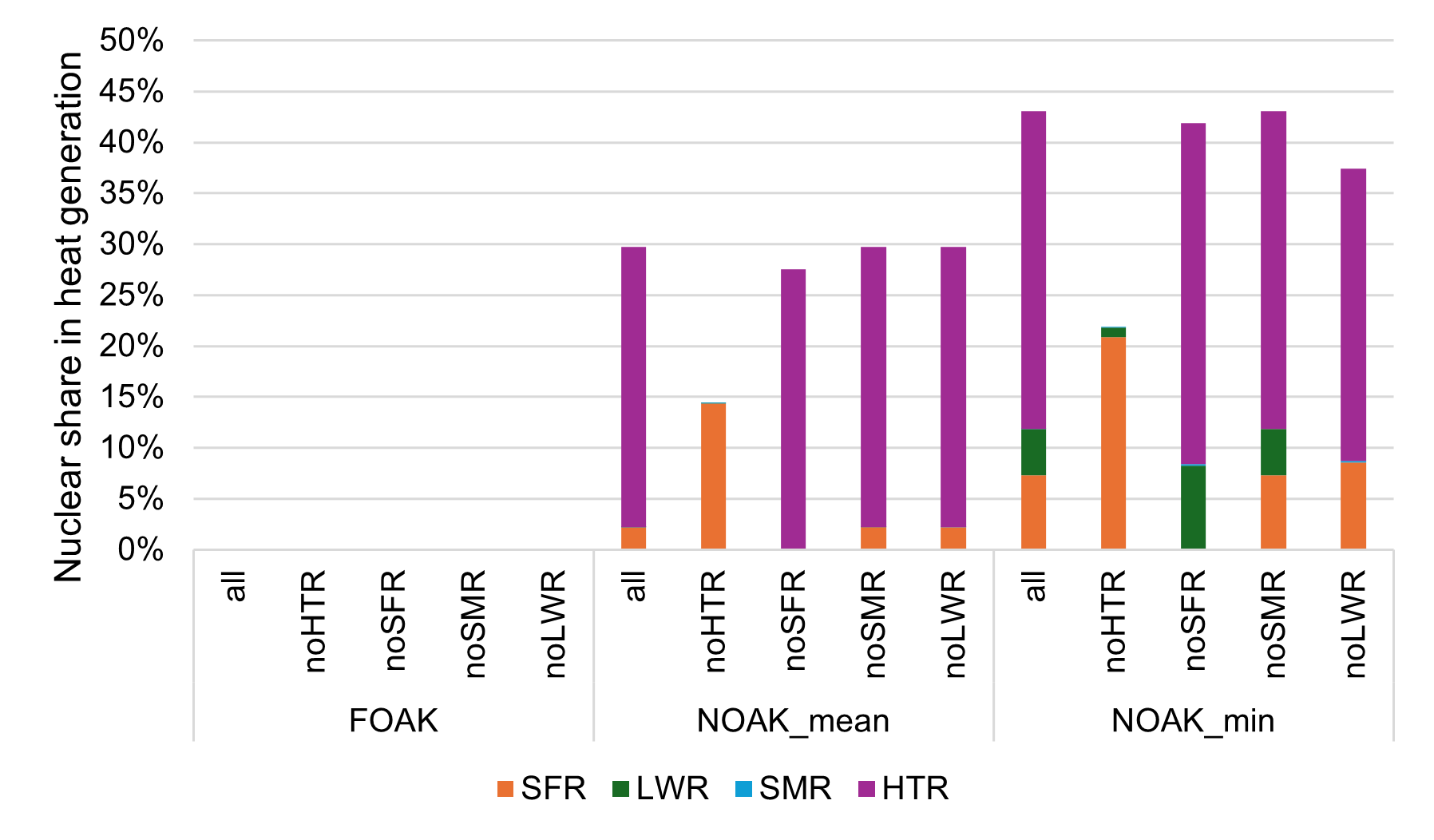

Analogously, Figures 7 and 8 show the same for heat provision. In all FOAK scenarios, electricity and heat generation from nuclear power is non-existent because no nuclear capacity is built at these cost levels, see Figure 9. Instead, heat demand is covered through a higher degree of power-to-x measures and a higher overall renewable electricity generation. Total heat generation is less variable across all scenarios. On average, 3,559 TWh of heat are generated, with a maximum of 3,589 TWh in the "noLWR" scenario for mean NOAK costs, and a minimum of 3,480 TWh for the "noHTR" scenario at minimum NOAK costs. Notably, LWRs become relevant for district heat generation only when SFRs are excluded, and costs are at minimum NOAK costs, while SMRs remain irrelevant across all scenarios. When nuclear is built, HTRs and SFRs dominate.

Once costs decrease to mean NOAK levels, the model adds nuclear power to the energy mix. However, most of this capacity refers to HTRs. While OCC input parameters for HTRs are higher than for all other reactor technologies, their ability to produce medium- and high-temperature process heat makes them competitive from an energy systems perspective as for these energy carriers, equivalent renewable technologies, i.e., high-temperature heat pumps or hydrogen, are comparatively expensive or also non-existent as of today. 1,109 GW of HTR capacity is built when all technologies are allowed, of which only 49 GW are used primarily for electricity, the remainder for heat provision. This HTR fleet is aided by 63 GW of SFRs that provide mainly medium-temperature process heat (61 GW dedicated to heat). If HTRs are excluded, additional SFR capacity is added (410 GW in total). Still, they cannot fully compensate, resulting in a substantially lower nuclear share in electricity and heat, down from 2% and 30% to 1% and 14%, respectively. LWRs and SMRs play little to no role due to their non-competitiveness with renewables for district and low-temperature process heat provision.

The dominance of HTRs in the installed nuclear fleet ends once costs drop to the minimum NOAK cost assumptions. Here, SFRs become competitive for electricity and heat provision. While they provide only 9% of nuclear heat in the "all" scenario, see Figure 7, they provide the overwhelming majority of nuclear electricity, adding to the substantial share of 23%. If HTRs are excluded, SFRs become even more dominant and are the only nuclear technology to be added to the grid (with a negligible 438 MW of SMRs added). Notably, high-capacity LWRs are introduced for the first time in these scenarios. SMRs are de facto not built in any scenario; they appear to be strictly dominated by other nuclear technologies, and low-temperature heat is provided by cheaper (renewable) alternatives, mainly heat pumps. When SFRs are excluded, the installed nuclear capacity is dominated by HTRs (1335 GW), and 395 GW of LWR capacities. Regardless, HTRs provide most process heat, while LWRs produce some district heat. 5 GW of SMR capacity is built. For all readiness levels, excluding SMR and LWR technologies has no noticable impact.

Total system costs for the FOAK scenarios are the highest, averaging at €317.5 billion with a standard deviation (sd) of €21.1 million. Mean NOAK scenarios average €307.2 billion (sd = €2.7 billion), and minimum NOAK scenarios are the cheapest, averaging only €290 billion (sd = €3.1 billion). The main differences in cost stem from the increased expansion of nuclear power capacity at comparatively low cost (compared to actual to be expected costs, see Section 3.3). In the FOAK scenarios, additional flexibility measures are built, such as open-circuit hydrogen power plants, and consequently, investments into powerToX technologies become necessary. Gas power plants are de facto not built in the minimum NOAK scenarios.

5 Discussion

The results shown above underline the lack of cost competitiveness of nuclear power compared to other energy generation technologies. They show that the cost-efficient capacity expansion of especially non-light water reactors would require substantial cost reductions that are, as described in Section 3.3, not to be expected in the coming years.

This work assumes that several different reactor concepts will have been fully developed, licensed, tested, commercialized, and produced in vast quantities in the next few years, which, given the current state of project developments, is an optimistic outlook.

However, if the above-mentioned optimistic cost reductions were to be achieved, the results show that non-light water reactor technologies could contribute to energy system decarbonization in Europe in this particular setting (e.g., assuming favorable capacity factors and industry capability, etc.). However, this is limited to mostly HTRs, which provide valuable heat energy at temperatures of up to 1000°C.

But regardless of costs, nuclear reactors feature additional challenges that would need to be overcome for a substantial capacity ramp-up. For example, the heterogeneity of fuel requirements for different SNR concepts corresponds with that of the reactor designs themselves. Many concepts additionally increase proliferation risks because of their requirement of high assay low enriched uranium (HALEU) fuel for which specialized fuel production facilities would have to be funded and constructed-which in turn requires substantial investment and long-term planning and the limitation of industry efforts to a handful of promising reactor designs [120, 121]. It is uncertain whether this type of infrastructure could be up and running in time for these reactor concepts to play a significant role in decarbonizing the European energy system.

Furthermore, the cost data mentioned above do not include external costs of nuclear, such as decommissioning and waste management, or social costs, such as risks relating to accidents, proliferation, or uranium mining and tilling [122, 123, 124, 125]. Additional waste challenges arise from implementing non-light water reactors that generate different kinds of waste from, e.g., HALEU fuel, creating additional and currently unstudied waste streams that would have to be dealt with [121]. However, with most nuclear waste responsibility lying with the respective governments [126, 127], substantial funding uncertainties could be removed from projects [128], as suggested to be implemented by Sawicki and Horbaczewska [129]. This would, however, require substantial political power to be achieved, especially in Europe. Additionally, long-term financial assurance and commitment to a limited number of reactor designs are necessary [17].

Additionally, the assumed flexibility of nuclear power plant operations without constraints can be contested. Lynch et al. [116] demonstrate that today’s LWRs can be an effective technology for load following, and Jenkins et al. [19] show in their model for the South-West U.S. that flexible nuclear operations can reduce system costs and increase reactor operator revenues. Loisel et al. [130, p. 281] even claim that "in practice, countries with […] high intermittent renewables […] need [nuclear power plants] to operate". However, despite theoretical technical feasibility, current nuclear reactors’ ability to run flexibly is seldom applied today, with operational experience limited mostly to France [42]. In the U.S., operational experience of flexibly dispatchable nuclear power plants has been limited despite regulations allowing for flexible operations and load following [131]. Reactors designed to operate as flexible backup capacities in energy systems based mainly on renewables face challenges of long standstills and fast ramp-ups. Running at high capacity factors generating heat for other purposes and then flexibly switching to power generation when required will be technologically challenging to implement, least finance [132, 51].

Our model approach faces some inevitable limitations that could limit the applicability of the results. First, the potential locality of heat demand is not accounted for. This is relevant because, for direct heat provision, sources must be located close to off-takers to minimize losses during transfer. This could be especially relevant for nuclear reactors as these technologies may face substantial opposition from local communities. Secondly, we assume that reactors can switch between operating modes without delay and incurred cost. Adding this to the high capacity factors of 90% is an assumption that is advantageous to nuclear. Whether SNRs can operate at such high capacity factors and operate flexibly remains highly uncertain given the lack of precedence in the historical track record of such concepts, see Section 2.2.

Regarding cost assumptions, we show that OCC must be drastically reduced for nuclear power to be competitive with renewable technologies. In our approach, we apply a uniform cost assumption for nuclear power that does not consider cost differences between vendors, financing schemes, or local cost differences that could occur between, for example, projects in Finland and Hungary.

The applied model to compute a cost-efficient share of the different nuclear power plants corresponds to or exceeds the state-of-the-art in energy planning. The high temporal resolution using two-hour blocks, resulting in 4380 steps, exceeds typical resolutions and accurately captures the fluctuations of wind and solar power, which are the main competitors of nuclear power. Inevitable limitations of the model impose a positive bias on nuclear power, so our results constitute an upper bound on the cost-efficient share. Most importantly, we neglect the operational constraints of nuclear power and do not impose restrictions on downtimes or production gradients to keep the underlying optimization problem computationally tractable. Of all considered technologies, these constraints are most relevant for nuclear, but according to previous literature, they are acceptable to ignore, especially if a model includes other short-term flexibility, like batteries or demand-side management [133, 134].

6 Conclusion and policy recommendations

Our analysis shows the various potential non-electrical use cases for nuclear reactors. We show that these applications are limited to individual reactors supplying heat to small localized demand centers. Most heat provision experience has been gathered in Eastern Europe, where a handful of reactors have provided district heat to neighboring towns, and to Japan, where some reactors service desalination plants. Consequentially, the industry’s experience in non-electrical use cases is limited, and it should be critically reflected upon propositions of localized heat provision given the challenge of implementing sufficient emergency planning zones, flexible operations, and the availability of potentially cheaper alternatives.

Regarding potential technologies, we find that as of today, both light and non-light water reactor concepts cannot fulfill the prerequisites defined by the Committee on Laying the Foundation for New and Advanced Nuclear Reactors in the United States et al. [13]. Most notably, our assessment shows that none of the discussed concepts is commercially available. Most concepts are in pre-licensing or licensing stages, and even for those under construction, the remaining challenges of becoming competitive and affordable (yet socially acceptable) remain to be proven.

Despite the lack of empirical data, many projections and assumptions exist regarding the future cost of diverse reactor concepts. The discrepancy between FOAK and NOAK cost estimations is substantial, and the range of cost estimations in a given readiness level is also. Notably, NOAK cost estimations are referenced more often, albeit the exact number "n" of required produced units to reach these costs through economies of multiples remains undefined. Compared to actual ongoing reactor construction projects in OECD countries, the cost assumptions are overly optimistic and could even be criticized as misleading. Furthermore, as cost overruns and construction delays have historically characterized the nuclear power industry, the costs for actual reactor projects are likely to be higher.

Nonetheless, we assess the potential application of light water reactors and SNR concepts in a future decarbonized energy system in Europe in the near future. We run five model calculations assuming variying technolgy availability in each of the three general readiness level scenarios (FOAK, mean NOAK, minimum NOAK for OCC, fuel, and OM cost). For FOAK cost scenarios, the cost-optimizing model builds no nuclear and relies on renewables to provide all necessary energy services. At mean NOAK cost, on average 60% of FOAK cost assumptions, nuclear power plant capacities are added to the grid, primarily for heat provision. At minimum NOAK cost, on average of FOAK cost assumptions, nuclear power plants dominate medium and high process heat generation, primarily due to the construction of HTRs and SFRs, while both high- and low-capacity LWRs are mostly neglected.

Thus, to achieve technological readiness for the widespread implementation of non-light water reactor technologies and potentially reduce expansion costs, development efforts should be focused on a limited number of reactor concepts and focussed on technologies capable of providing high temperature process heat. For policymakers, this implies goal-oriented (financial) and reliable support of projects with the highest degree of success and future applicability. Cost reductions are only possible when a substantial number of reactors of the same design are built without continuous re-designs necessitating additional safety inspections and licensing procedures.

Based on the results described above, one could assume that nuclear power could play a substantial role in a future decarbonized energy system. However, the energy model’s assumptions are skewed positively towards nuclear power. This includes optimistic assumptions of 90% capacity factors, the assumption that reactors can be built at NOAK costs in a few years, full flexibility of reactors and the ability to switch between electricity and heat provision without ramp-up, the neglect of decommissioning and waste management costs, potential safety challenges of non-light water reactor concepts, increased proliferation risks, and the uncertainty regarding actual industry capability to deliver the required capacities.

Consequentially, policymakers must address these unresolved challenges of non-light water reactor concepts. Most notably this refers to the organization of new waste disposal routes—all while most countries have yet to safely dispose of today’s fleets spent fuel—as well as the assessment of proliferation and safety risks. Redesigning licensing procedures to account for the high number of necessary reactor installations and speeding up procedures while accounting for heterogeneous designs and associated risks, might become necessary.

To conclude, given the nuclear industry’s current capabilities, the non-availability of a limited number of tested reactor concepts to attempt the proposed mass production, unproven non-electrical applications on a large scale, unsolved waste issues with novel fuel concepts, potential safety challenges, and obvious social challenges for the large scale implementation of nuclear power, it seems unlikely, from a techno-economic perspective, that non-light water reactors will play a major role in a near-future decarbonized energy system.

Thus, while the here discussed reactor concepts might become available in the coming decades, and could at some point be economically competitive, regulators and policymakers should also focus on implementing available technologies, i.e., renewables and grid capacity expansion coupled with demand-side flexibility and sufficient storage options, to continue ongoing energy system decarbonization efforts necessary today.

Acknowledgments

The research leading to these results has received funding from the Deutsche Forschungsgemeinschaft (DFG) under project number 423336886 and the German Federal Office for the Safety of Nuclear Waste Management (BASE), grant number 4722B50101.

Declaration of Interest

The authors declare that they have no known competing financial interests or personal relationships that could have appeared to influence the work reported in this paper.

Data Availability

All data used in this research is listed either in the Appendix or will be made available upon request. Model code and input data can be accessed via https://github.com/leonardgoeke/EuSysMod/tree/greenfield_nuclearHeat. Due to their size, model outputs are not part of the repository but are available upon request. The applied model uses the open AnyMOD.jl modeling framework [22]. The applied version of the tool is openly available under this link: https://github.com/leonardgoeke/AnyMOD.jl/releases/tag/flexibleElectrificationWorkingPaper.

Author Contributions

A.W.: Conceptualization; Methodology; Formal analysis; Investigation; Data Curation; Writing - Original Draft; Writing - Review & Editing; Visualization; F.B.: Investigation; Validation; Writing - Review & Editing; L.G.: Methodology; Validation; Software; Writing - Review & Editing

References

- Byers et al. [2022] Edward Byers, Volker Krey, Elmar Kriegler, Keywan Riahi, Roberto Schaeffer, Jarmo Kikstra, Robin Lamboll, Zebedee Nicholls, Marit Sandstad, Chris Smith, Kaj van der Wijst, Franck Lecocq, Joana Portugal-Pereira, Yamina Saheb, Anders Stromann, Harald Winkler, Cornelia Auer, Elina Brutschin, Claire Lepault, Eduardo Müller-Casseres, Matthew Gidden, Daniel Huppmann, Peter Kolp, Giacomo Marangoni, Michaela Werning, Katherine Calvin, Celine Guivarch, Tomoko Hasegawa, Glen Peters, Julia Steinberger, Massimo Tavoni, Detlef van Vuuren, Alaa Al Khourdajie, Piers Forster, Jared Lewis, Malte Meinshausen, Joeri Rogelj, Bjorn Samset, and Ragnhild Skeie. AR6 Scenarios Database, April 2022. URL https://zenodo.org/record/5886912.

- Duan et al. [2022] Lei Duan, Robert Petroski, Lowell Wood, and Ken Caldeira. Stylized least-cost analysis of flexible nuclear power in deeply decarbonized electricity systems considering wind and solar resources worldwide. Nature Energy, February 2022. ISSN 2058-7546. 10.1038/s41560-022-00979-x. URL https://www.nature.com/articles/s41560-022-00979-x.

- Rothwell [2022] Geoffrey Rothwell. Projected electricity costs in international nuclear power markets. Energy Policy, 164:112905, May 2022. ISSN 03014215. 10.1016/j.enpol.2022.112905. URL https://linkinghub.elsevier.com/retrieve/pii/S0301421522001306.

- Lovins [2022] Amory B. Lovins. US nuclear power: Status, prospects, and climate implications. The Electricity Journal, 35(4):107122, May 2022. ISSN 10406190. 10.1016/j.tej.2022.107122. URL https://linkinghub.elsevier.com/retrieve/pii/S1040619022000483.

- Steigerwald et al. [2023] Björn Steigerwald, Jens Weibezahn, Martin Slowik, and Christian Von Hirschhausen. Uncertainties in estimating production costs of future nuclear technologies: A model-based analysis of small modular reactors. Energy, 281:128204, October 2023. ISSN 03605442. 10.1016/j.energy.2023.128204. URL https://www.sciencedirect.com/science/article/pii/S0360544223015980.

- Wealer et al. [2021] B. Wealer, S. Bauer, C.v. Hirschhausen, C. Kemfert, and L. Göke. Investing into third generation nuclear power plants - Review of recent trends and analysis of future investments using Monte Carlo Simulation. Renewable and Sustainable Energy Reviews, 143:110836, June 2021. ISSN 13640321. 10.1016/j.rser.2021.110836. URL https://linkinghub.elsevier.com/retrieve/pii/S1364032121001301.

- Böse et al. [2024] Fanny Böse, Alexander Wimmers, Björn Steigerwald, and Christian von Hirschhausen. Questioning nuclear scale-up propositions: Availability and economic prospects of light water, small modular and advanced reactor technologies. Energy Research & Social Science, 110(April 2024):103448, 2024. https://doi.org/10.1016/j.erss.2024.103448.

- Göke et al. [2023a] Leonard Göke, Alexander Wimmers, and Christian von Hirschhausen. Flexible nuclear power and fluctuating renewables? – A techno-economic analysis for decarbonized energy systems. 2023a. 10.48550/ARXIV.2302.14515. URL https://arxiv.org/abs/2302.14515. Publisher: arXiv Version Number: 1.

- Thomas [2010] Steve Thomas. Competitive energy markets and nuclear power: Can we have both, do we want either? Energy Policy, 38(9):4903–4908, September 2010. ISSN 03014215. 10.1016/j.enpol.2010.04.051. URL https://linkinghub.elsevier.com/retrieve/pii/S0301421510003435.

- Nuttall [2022] William J Nuttall. Nuclear renaissance: technologies and policies for the future of nuclear power. CRC Press, Boca Raton, 2022. ISBN 978-1-00-059502-4 978-1-00-303873-3 978-1-00-059510-9. URL https://www.taylorfrancis.com/books/9781003038733. OCLC: 1316697337.

- WNN [2023] WNN. Ministerial declaration puts nuclear at heart of climate action. World Nuclear News, February 2023. URL https://www.world-nuclear-news.org/Articles/Ministerial-declaration-puts-nuclear-at-heart-of-c.

- Markard et al. [2020] Jochen Markard, Nuno Bento, Noah Kittner, and Alejandro Nuñez-Jimenez. Destined for decline? Examining nuclear energy from a technological innovation systems perspective. Energy Research & Social Science, 67:101512, September 2020. ISSN 22146296. 10.1016/j.erss.2020.101512. URL https://linkinghub.elsevier.com/retrieve/pii/S221462962030089X.

- Committee on Laying the Foundation for New and Advanced Nuclear Reactors in the United States et al. [2023] Committee on Laying the Foundation for New and Advanced Nuclear Reactors in the United States, Nuclear and Radiation Studies Board, Board on Energy and Environmental Systems, Division on Engineering and Physical Sciences, Division on Earth and Life Studies, National Academy of Engineering, and National Academies of Sciences, Engineering, and Medicine. Laying the Foundation for New and Advanced Nuclear Reactors in the United States. National Academies Press, Washington, D.C., 2023. ISBN 978-0-309-69077-5. 10.17226/26630. URL https://www.nap.edu/catalog/26630. Pages: 26630.

- Fattahi et al. [2022] Amirhossein Fattahi, Jos Sijm, Machteld Van Den Broek, Rafael Martínez Gordón, Manuel Sanchez Dieguez, and André Faaij. Analyzing the techno-economic role of nuclear power in the Dutch net-zero energy system transition. Advances in Applied Energy, 7:100103, September 2022. ISSN 26667924. 10.1016/j.adapen.2022.100103. URL https://linkinghub.elsevier.com/retrieve/pii/S266679242200021X.

- Ingersoll et al. [2020] Eric Ingersoll, Kirsty Gogan, John Herter, Andrew Foss, Jane Pickering, and Romana Vysatova. Cost & Performance Requirements for Flexible Advanced Nuclear Plants in Future U.S. Power Markets. Report for the ORNL Resource team supporting ARPA-E’s MEITNER Program, Lucid Catalyst, July 2020. URL https://www.lucidcatalyst.com/_files/ugd/2fed7a_a1e392c51f4f497395a53dbb306e87fe.pdf.

- MIT [2018] MIT. The Future of Nuclear Energy in a Carbon-Constrained World. Technical report, Massachusetts Institute of Technology, Cambridge, MA, 2018. URL http://energy.mit.edu/wp-content/uploads/2018/09/The-Future-of-Nuclear-Energy-in-a-Carbon-Constrained-World.pdf.

- Brown [2022] Nicholas R. Brown. Engineering demonstration reactors: A stepping stone on the path to deployment of advanced nuclear energy in the United States. Energy, 238:121750, January 2022. ISSN 03605442. 10.1016/j.energy.2021.121750. URL https://linkinghub.elsevier.com/retrieve/pii/S0360544221019988.

- Black et al. [2023] G. Black, D. Shropshire, K. Araújo, and A. Van Heek. Prospects for Nuclear Microreactors: A Review of the Technology, Economics, and Regulatory Considerations. Nuclear Technology, 209(sup1):S1–S20, January 2023. ISSN 0029-5450, 1943-7471. 10.1080/00295450.2022.2118626. URL https://www.tandfonline.com/doi/full/10.1080/00295450.2022.2118626.

- Jenkins et al. [2018] J.D. Jenkins, Z. Zhou, R. Ponciroli, R.B. Vilim, F. Ganda, F. De Sisternes, and A. Botterud. The benefits of nuclear flexibility in power system operations with renewable energy. Applied Energy, 222:872–884, July 2018. ISSN 03062619. 10.1016/j.apenergy.2018.03.002. URL https://linkinghub.elsevier.com/retrieve/pii/S0306261918303180.

- Bistline et al. [2023] John Bistline, Shannon Bragg-Sitton, Wesley Cole, Brent Dixon, Erich Eschmann, Jonathan Ho, Augustine Kwon, Laura Martin, Caitlin Murphy, Christopher Namovicz, and Andrew Sowder. Modeling nuclear energy’s future role in decarbonized energy systems. iScience, 26(2):105952, February 2023. ISSN 25890042. 10.1016/j.isci.2023.105952. URL https://linkinghub.elsevier.com/retrieve/pii/S2589004223000299.

- Shirvan [2022] Koroush Shirvan. Overnight Capital Cost of the Next AP1000. Technical Report MIT-ANP-TR-193, Massachusetts Institute of Technology, Cambridge, MA, March 2022. URL https://web.mit.edu/kshirvan/www/research/ANP193%20TR%20CANES.pdf?trk=public_post_comment-text.

- Göke [2021] Leonard Göke. AnyMOD.jl: A Julia package for creating energy system models. SoftwareX, 16:100871, 2021. ISSN 2352-7110. 10.1016/j.softx.2021.100871. URL https://www.sciencedirect.com/science/article/pii/S2352711021001382.

- Schneider et al. [2024] Mycle Schneider, Antony Froggatt, Julie Hazemann, Ozgur Gurbuz, Paul Jobin, Phil Johnstone, Timothy Judson, Yuki Kobayashi, Doug Koplow, Edwin Lyman, M. V. Ramana, Sebastian Stier, Andy Stirling, Tatsujiro Suzuki, Christian Von Hirschhausen, Alexander Wimmers, Hartmut Winkler, Maahin Ahmed, Nina Schneider, Agnès Stienne, and Friedhelm Meinass. The World Nuclear Industry Status Report 2024. Technical report, Mycle Schneider Consulting, Paris, France, September 2024. URL https://www.worldnuclearreport.org/IMG/pdf/wnisr2024-v2.pdf.

- Csik and Kupitz [1997] Bela J. Csik and Jürgen Kupitz. Nuclear power applications: Supplying heat for homes and industries. IAEA Bulletin, 39(2):21–25, 1997. URL https://www.iaea.org/sites/default/files/publications/magazines/bulletin/bull39-2/39205082125.pdf.

- Safa [2012] H. Safa. Heat recovery from nuclear power plants. International Journal of Electrical Power & Energy Systems, 42(1):553–559, November 2012. ISSN 01420615. 10.1016/j.ijepes.2012.04.052. URL https://linkinghub.elsevier.com/retrieve/pii/S0142061512001792.

- IAEA [2002] IAEA, editor. Market potential for non-electric applications of nuclear energy. Number 410 in Technical reports series / International Atomic Energy Agency. Internat. Atomic Energy Agency, Vienna, 2002. ISBN 978-92-0-115402-6.

- IAEA [2017a] IAEA. Opportunities for cogeneration with nuclear energy. Number v.NP-T-4.1 in IAEA Nuclear Energy Series No. NP-T-4.1. International Atomic Energy Agency, Vienna, Austria, 2017a. ISBN 978-92-0-103616-2.

- IAEA [2019] IAEA. Guidance on Nuclear Energy Cogeneration. Technical Report NP-T-1.7, International Atomic Energy Agency, 2019. URL https://www.iaea.org/publications/13385/guidance-on-nuclear-energy-cogeneration.

- OECD and NEA [2022a] OECD and NEA. Beyond Electricity: The Economics of Nuclear Cogeneration. Nuclear TEchnology Development and Economics 7363, Nuclear Energy Agency, 2022a. URL https://www.oecd-nea.org/jcms/pl_71699/beyond-electricity-the-economics-of-nuclear-cogeneration?details=true.

- Nilsson and Hannus [1978] L. Nilsson and M. Hannus. SECURE Nuclear District Heating Plant. Nuclear Technology, 38(2):225–234, April 1978. ISSN 0029-5450, 1943-7471. 10.13182/NT78-A32017. URL https://www.tandfonline.com/doi/full/10.13182/NT78-A32017.

- Leppänen [2019] Jaakko Leppänen. A Review of District Heating Reactor Technology. Technical Report VTT-R-06895-18, VTT Technical Research Centre of Finland, October 2019. URL https://cris.vtt.fi/ws/portalfiles/portal/24936486/VTT_R_06895_18.pdf.

- Kupitz [2001] Jürgen Kupitz. Small and medium reactors: Development status and application aspects. pages 497–534, Trieste, Italy, December 2001. ICTP Lecture Notes. URL https://www.osti.gov/etdeweb/biblio/20854884.

- Kraev [2021] Kamen Kraev. City Of Haiyang ‘First In Country’ To Have District Heating System Powered By Nuclear. NucNet, December 2021. URL https://www.nucnet.org/news/city-of-haiyang-first-in-country-to-have-district-heating-system-powered-by-nuclear-11-5-2021.

- Pisciotta et al. [2022] Maxwell Pisciotta, Hélène Pilorgé, John Feldmann, Rory Jacobson, Justine Davids, Shelvey Swett, Zachary Sasso, and Jennifer Wilcox. Current state of industrial heating and opportunities for decarbonization. Progress in Energy and Combustion Science, 91:100982, July 2022. ISSN 03601285. 10.1016/j.pecs.2021.100982. URL https://linkinghub.elsevier.com/retrieve/pii/S0360128521000800.

- IAEA [2017b] IAEA. Industrial Applications of Nuclear Energy. Technical Report NP-T-4.3, International Atomic Energy Agency, 2017b. URL https://www.iaea.org/publications/10979/industrial-applications-of-nuclear-energy.

- OECD and NEA [2022b] OECD and NEA. The Role of Nuclear in the Hydrogen Economy: Cost and Competitiveness. Technical Report 7630, Nuclear Energy Agency, Boulogne-Billancourt, France, 2022b. URL https://www.oecd-nea.org/jcms/pl_73133/the-role-of-nuclear-power-in-the-hydrogen-economy.

- Bartels et al. [2010] Jeffrey R. Bartels, Michael B. Pate, and Norman K. Olson. An economic survey of hydrogen production from conventional and alternative energy sources. International Journal of Hydrogen Energy, 35(16):8371–8384, August 2010. ISSN 03603199. 10.1016/j.ijhydene.2010.04.035. URL https://linkinghub.elsevier.com/retrieve/pii/S0360319910007317.

- Nuttall and Bakenne [2020] William J. Nuttall and Adetokunboh T. Bakenne. Fossil Fuel Hydrogen: Technical, Economic and Environmental Potential. Springer International Publishing, Cham, 2020. ISBN 978-3-030-30907-7 978-3-030-30908-4. 10.1007/978-3-030-30908-4. URL http://link.springer.com/10.1007/978-3-030-30908-4.

- Doctor [2006] Richard D. Doctor. Evaluation of a Continuous Calcium-Bromine Thermochemical Cycle, May 2006. URL https://www.hydrogen.energy.gov/pdfs/review06/pd_16_doctor.pdf.

- Pregger et al. [2009] Thomas Pregger, Daniela Graf, Wolfram Krewitt, Christian Sattler, Martin Roeb, and Stephan Möller. Prospects of solar thermal hydrogen production processes. International Journal of Hydrogen Energy, 34(10):4256–4267, May 2009. ISSN 03603199. 10.1016/j.ijhydene.2009.03.025. URL https://linkinghub.elsevier.com/retrieve/pii/S0360319909004352.

- Pinsky et al. [2020] Roxanne Pinsky, Piyush Sabharwall, Jeremy Hartvigsen, and James O’Brien. Comparative review of hydrogen production technologies for nuclear hybrid energy systems. Progress in Nuclear Energy, 123:103317, May 2020. ISSN 01491970. 10.1016/j.pnucene.2020.103317. URL https://linkinghub.elsevier.com/retrieve/pii/S014919702030069X.

- Schneider et al. [2023] Mycle Schneider, Antony Froggatt, Julie Hazemann, Christian von Hirschhausen, M.V. Ramana, Alexander James Wimmers, Nina Schneider, Tatsujiro Suzuki, Agnès Stienne, Friedhelm Meinass, Doug Koplow, Timothy Judson, and Hartmut Winkler. World Nuclear Industry Status Report 2023. Technical report, Mycle Schneider Consulting, Paris, 2023. URL https://www.worldnuclearreport.org/IMG/pdf/wnisr2023-v1-hr.pdf.

- Rawool-Sullivan et al. [2002] Mohini Rawool-Sullivan, Paul D. Moskowitz, and Ludmilla N. Shelenkova. Technical and Proliferation-Related Aspects of the Dismantlement of Russian Alfa-Class Nuclear Submarines. The Nonproliferation Review, Spring:161–171, 2002. URL https://nonproliferation.org/wp-content/uploads/npr/91mosk.pdf.

- Al-Othman et al. [2019] Amani Al-Othman, Noora N. Darwish, Muhammad Qasim, Mohammad Tawalbeh, Naif A. Darwish, and Nidal Hilal. Nuclear desalination: A state-of-the-art review. Desalination, 457:39–61, May 2019. ISSN 00119164. 10.1016/j.desal.2019.01.002. URL https://linkinghub.elsevier.com/retrieve/pii/S0011916418323531.

- Ingersoll et al. [2014] D Ingersoll, Z Houghton, R Bromm, M McKellar, and R Boardman. Extending Nuclear Energy to Non - Electrical Applications. Technical report, The 19th Pacific Basin Nuclear Conference (PBNC 2014), August 2014. URL https://inldigitallibrary.inl.gov/sites/sti/sti/6303857.pdf.

- Faibish et al. [2002] R. S. Faibish, T. Konishi, and M. Gasparini. Application of Nuclear Energy for Seawater Desalination: Design Concepts of Nuclear Desalination Plants. In 10th International Conference on Nuclear Engineering, Volume 4, pages 15–22, Arlington, Virginia, USA, January 2002. ASMEDC. ISBN 978-0-7918-3598-2. 10.1115/ICONE10-22071. URL https://asmedigitalcollection.asme.org/ICONE/proceedings/ICONE10/35987/15/295413.

- Price et al. [2023] James Price, Ilkka Keppo, and Paul E. Dodds. The role of new nuclear power in the UK’s net-zero emissions energy system. Energy, 262:125450, January 2023. ISSN 03605442. 10.1016/j.energy.2022.125450. URL https://linkinghub.elsevier.com/retrieve/pii/S0360544222023325.

- Robb Stewart and Shirvan [2023] W. Robb Stewart and Koroush Shirvan. Construction schedule and cost risk for large and small light water reactors. Nuclear Engineering and Design, 407:112305, June 2023. ISSN 00295493. 10.1016/j.nucengdes.2023.112305. URL https://linkinghub.elsevier.com/retrieve/pii/S0029549323001541.

- Black et al. [2021] Geoffrey Black, David Shropshire, and Kathleen Araújo. Small modular reactor (SMR) adoption: Opportunities and challenges for emerging markets. In Handbook of Small Modular Nuclear Reactors, pages 557–593. Elsevier, 2021. ISBN 978-0-12-823916-2. 10.1016/B978-0-12-823916-2.00022-9. URL https://linkinghub.elsevier.com/retrieve/pii/B9780128239162000229.

- Liu and Fan [2014] Zhitao Liu and Jihong Fan. Technology readiness assessment of Small Modular Reactor (SMR) designs. Progress in Nuclear Energy, 70:20–28, January 2014. ISSN 01491970. 10.1016/j.pnucene.2013.07.005. URL https://linkinghub.elsevier.com/retrieve/pii/S0149197013001303.

- Ramana [2021] M. V. Ramana. Small Modular and Advanced Nuclear Reactors: A Reality Check. IEEE Access, 9:42090–42099, 2021. ISSN 2169-3536. 10.1109/ACCESS.2021.3064948. Conference Name: IEEE Access.

- Pistner et al. [2021] Christoph Pistner, Matthias Englert, Christian Küppers, Ben Wealer, Björn Steigerwald, Christian von Hirschhausen, and Richard Donderer. Sicherheitstechnische Analyse und Risikobewertung einer Anwendung von SMR-Konzepten (Small Modular Reactors). Technical Report Vorhaben 4720F50500, Bundesamt für die Sicherheit der nuklearen Entsorgung, Berlin, 2021. URL https://www.base.bund.de/SharedDocs/Downloads/BASE/DE/berichte/kt/gutachten-small-modular-reactors.pdf?__blob=publicationFile&v=6.

- Henderson and Taylor [2006] A. David Henderson and Amy Taylor. The US Department of Energy research and development programme on hydrogen production using nuclear energy. International Journal of Nuclear Hydrogen Production and Applications, 1(1):51, 2006. ISSN 1743-4939, 1743-4947. 10.1504/IJNHPA.2006.009868. URL http://www.inderscience.com/link.php?id=9868.

- Gardner and Mishra [2023] Timothy Gardner and Manas Mishra. NuScale ends Utah project, in blow to US nuclear power ambitions. Reuters, September 2023. URL https://www.reuters.com/business/energy/nuscale-power-uamps-agree-terminate-nuclear-project-2023-11-08/.

- Seaborg [1970] Glenn T. Seaborg. The Plutonium Economy of the Future, 1970. URL http://fissilematerials.org/library/aec70.pdf.

- Midttun and Baumgartner [1986] Atle Midttun and Thomas Baumgartner. Negotiating Energy Futures: The Politics of Energy Forecasting. Energy Policy, 14(3):219–241, June 1986. ISSN 0301-4215. 10.1016/0301-4215(86)90145-X. URL http://www.sciencedirect.com/science/article/pii/030142158690145X.

- Bunn et al. [2003] Matthew Bunn, Steve Fetter, John P. Holdren, and Bob van der Zwaan. The Economics of Reprocessing Versus Direct Disposal of Spent Nuclear Fuel. Technical report, Belfer Center for Science and International Affairs, Harvard Kennedy School, 2003.

- Strauss [1954] Lewis L. Strauss. Remarks Prepared by Lewis L. Straus, Chairman, United States Atomic Energy Commission, For Delivery At The Founders’ Day Dinner, National Association of Science Writers, On Thusday, September 16, 1954, New York, New York., September 1954. URL https://www.nrc.gov/docs/ML1613/ML16131A120.pdf.

- Cochran et al. [2010] Thomas B. Cochran, Harold A. Feiveson, Walter Patterson, Gennadi Pshakin, M.V. Ramana, Mycle Schneider, Tatsujiro Suzuki, and Frank von Hippel. Fast Breeder Reactor Programs: History and Status. Technical Report Research Report 8, International Panel on Fissile Materials, Princeton, N.J, 2010. URL http://fissilematerials.org/library/2010/02/fast_breeder_reactor_programs_.html.

- Schulenberg [2022] Thomas Schulenberg. The fourth generation of nuclear reactors: Fundamentals, Types, and Benefits Explained. Springer Berlin Heidelberg, Berlin, Heidelberg, 2022. ISBN 978-3-662-64918-3 978-3-662-64919-0. 10.1007/978-3-662-64919-0. URL https://link.springer.com/10.1007/978-3-662-64919-0.

- Ohshima and Kubo [2016] H. Ohshima and S. Kubo. Sodium-cooled fast reactor. In Handbook of Generation IV Nuclear Reactors, pages 97–118. Woodhead Publishing, Cambridge, UK, 2016. ISBN 978-0-08-100149-3. 10.1016/B978-0-08-100149-3.00005-7. URL https://linkinghub.elsevier.com/retrieve/pii/B9780081001493000057.

- IAEA [2022a] IAEA. Nuclear Power Reactors in the World. Number IAEA-RDS-2/42. International Atomic Energy Agency, Vienna, 2022a. ISBN 978-92-0-125122-0.

- Pistner et al. [2023] Christoph Pistner, Matthias Englert, Christian von Hirschhausen, Fanny Böse, Björn Steigerwald, and Lukas Gast. Analyse und Bewertung des Entwicklungsstands, der Sicherheit und des regulatorischen Rahmens für sogenannte neuartige Reaktorkonzepte. Zwischenbericht zu AP-1 und -2 Vorhaben 4721F50501, Bundesamt für die Sicherheit der nuklearen Entsorgung, Berlin, 2023. URL https://www.base.bund.de/SharedDocs/Downloads/BASE/DE/berichte/kt/zwischenbericht-gutachten-sogenannte-neuartige-reaktorkonzepte.pdf?__blob=publicationFile&v=4.

- Alemberti [2021] Alessandro Alemberti. Lead Cooled Fast Reactors. In Encyclopedia of Nuclear Energy, pages 523–544. Elsevier, Berkeley, California, 2021. ISBN 978-0-12-819732-5. 10.1016/B978-0-12-819725-7.00001-5. URL https://linkinghub.elsevier.com/retrieve/pii/B9780128197257000015.

- Zhang et al. [2016] Zuoyi Zhang, Yujie Dong, Fu Li, Zhengming Zhang, Haitao Wang, Xiaojin Huang, Hong Li, Bing Liu, Xinxin Wu, Hong Wang, Xingzhong Diao, Haiquan Zhang, and Jinhua Wang. The Shandong Shidao Bay 200 MWe High-Temperature Gas-Cooled Reactor Pebble-Bed Module (HTR-PM) Demonstration Power Plant: An Engineering and Technological Innovation. Engineering, 2(1):112–118, March 2016. ISSN 20958099. 10.1016/J.ENG.2016.01.020. URL https://linkinghub.elsevier.com/retrieve/pii/S2095809916301552.

- Schultz et al. [2003] K.R. Schultz, L.C. Brown, G.E. Besenbruch, and C.J. Hamilton. Large-scale production of hydrogen by nuclear energy for the hydrogen economy. In Proceedings, Washington, D.C., April 2003. URL https://www.osti.gov/servlets/purl/814028.

- Stewart and Shirvan [2021] William Robb Stewart and Koroush Shirvan. Capital Cost Estimation for Advanced Nuclear Power Plants. preprint, Open Science Framework, January 2021. URL https://osf.io/erm3g.

- Riley et al. [2019] Brian J. Riley, Joanna McFarlane, Guillermo D. DelCul, John D. Vienna, Cristian I. Contescu, and Charles W. Forsberg. Molten salt reactor waste and effluent management strategies: A review. Nuclear Engineering and Design, 345:94–109, April 2019. ISSN 00295493. 10.1016/j.nucengdes.2019.02.002. URL https://linkinghub.elsevier.com/retrieve/pii/S002954931930024X.

- Rosenthal et al. [1970] M. Rosenthal, P. Kasten, and R. Briggs. Molten-Salt Reactors: History, Status, and Potential. Nuclear Applied Technology, 8(107), 1970. URL https://moltensalt.org/references/static/downloads/pdf/NAT_MSRintro.pdf.

- WNA [2021] WNA. Molten Salt Reactors, May 2021. URL https://www.world-nuclear.org/information-library/current-and-future-generation/molten-salt-reactors.aspx.

- Baik et al. [2022] Ejeong Baik, Kais Siala, Thomas Hamacher, and Sally M. Benson. California’s approach to decarbonizing the electricity sector and the role of dispatchable, low-carbon technologies. International Journal of Greenhouse Gas Control, 113:103527, January 2022. ISSN 17505836. 10.1016/j.ijggc.2021.103527. URL https://www.sciencedirect.com/science/article/pii/S1750583621002784.

- Asuega et al. [2023] Anthony Asuega, Braden J. Limb, and Jason C. Quinn. Techno-economic analysis of advanced small modular nuclear reactors. Applied Energy, 334:120669, March 2023. ISSN 03062619. 10.1016/j.apenergy.2023.120669. URL https://linkinghub.elsevier.com/retrieve/pii/S0306261923000338.

- Rodriguez [2018] Gilles Rodriguez. ASTRID - Lessons Learned, July 2018. URL https://www.gen-4.org/gif/jcms/c_101347/gen-iv-webinar-series-22-astrid-lessons-learned-mr-gilles-rodriguez?details=true.

- Budi et al. [2019] Rfs Budi, Ap Rijanti, Sm Lumbanraja, Md Birmano, Es Amitayani, and E Liun. Fuel and O&M Costs Estimation of High Temperature Gas-cooled Reactors and Its Possibility to be Implemented in Indonesia. IOP Conference Series: Materials Science and Engineering, 536(1):012144, June 2019. ISSN 1757-8981, 1757-899X. 10.1088/1757-899X/536/1/012144. URL https://iopscience.iop.org/article/10.1088/1757-899X/536/1/012144.

- Green [2019] Jim Green. SMR cost estimates, and costs of SMRs under construction. Nuclear Monitor, 872-873:18–22, July 2019. ISSN 2542-5439.

- IAEA [2020] IAEA. Advances in Small Modular Reactor Developments. A Supplement to: IAEA Advanced Reactors Information System (ARIS). Technical report, International Atomic Energy Agency, Vienna, Austria, 2020. URL https://aris.iaea.org/Publications/SMR_Book_2020.pdf.

- Stein et al. [2022] Adam Stein, Jonah Messinger, Seaver Wang, Juzel LLoyd, Jameson McBride, and Rani Franovich. Advancing Nuclear Energy - Evaluating Deployment, Investmant, and Impact in Amercia’s Clean Energy Future. Technical report, The Breakthrough Institute, Berkeley, California, June 2022. URL https://thebreakthrough.org/articles/advancing-nuclear-energy-report.

- Dixon et al. [2017] B. W. Dixon, F. Ganda, K. A. Williams, E. Hoffman, and J. K. Hanson. Advanced Fuel Cycle Cost Basis – 2017 Edition. Technical Report INL/EXT–17-43826, 1423891, September 2017. URL http://www.osti.gov/servlets/purl/1423891/.

- Nian and Zhong [2020] Victor Nian and Sheng Zhong. Economic feasibility of flexible energy productions by small modular reactors from the perspective of integrated planning. Progress in Nuclear Energy, 118:103106, January 2020. ISSN 01491970. 10.1016/j.pnucene.2019.103106. URL https://linkinghub.elsevier.com/retrieve/pii/S0149197019302070.

- Faibish [2019] Ron Faibish. Status Report - EM² (General Atomics). Technical report, September 2019. URL https://aris.iaea.org/PDF/EM2(GeneralAtomics)_2020.pdf.