Serial Scammers and Attack of the Clones: How Scammers Coordinate Multiple Rug Pulls on Decentralized Exchanges

Abstract.

We explored in this work the ubiquitous phenomenon of serial scammers, who deploy thousands of addresses to conduct a series of similar Rug Pulls on popular decentralized exchanges (DEXs). We first constructed a list of about 384,000 scammer addresses behind all 1-day Rug Pulls on the two most popular DEXs, Uniswap (Ethereum) and Pancakeswap (BSC), and identified many distinctive scam patterns including star-shaped, chain-shaped, and majority-flow scam clusters. We then proposed an algorithm to build a complete scam network from given scammer addresses, which consists of not only scammer addresses but also supporting addresses including depositors, withdrawers, transferrers, coordinators, and most importantly, wash traders. We note that profit estimations in existing works on Rug Pulls failed to capture the cost of wash trading, leading to inflated figures. Knowing who the wash traders are, we established a more accurate estimate for the true profit of individual scam pools as well as of the entire (serial) scam network by taking into account the wash-trading expenses.

1. Introduction

The total crypto scam revenue from 2019 to 2023, according to the latest 2024 Crypto Crime Report by the leading blockchain analytics firm Chanalysis (chainalysis_report_2024, , p. 104), reached a staggering amount of nearly US $40 billion. The report also shows that Rug Pull, a common type of scam in the decentralized finance (DeFi) ecosystem, was among the top three fastest growing scams in 2023 (chainalysis_report_2024, , p. 105). Rug Pull, first reported in 2021 (Xia_etal_2021, ; chainalysis_report_2022, ), refers to scams in which the developer(s) of a cryptocurrency project (usually a new token) suddenly vanished with investors’ fund, leaving their purchased assets worthless. Rug-Pull scams were responsible for the loss of more than US $100 million in 2023 alone according to Immunefi’s Crypto Loss Report (immunefi_hack_fraud_reports, ), and are still costing millions of dollars every month in 2024111Note that Immunefi’s report considers only Rug Pulls for its “fraud” category.. Immunefi’s reports (immunefi_hack_fraud_reports, ) also identified Etherem and BNB as the two most targeted chains by hacks and Rug Pulls in 2023-2024.

Whenever there are scammers, there must be serial scammers. Some evidence of that was initially observed in Xia et al. (Xia_etal_2021, ) when they expanded their dataset of scam tokens on Uniswap by including also tokens that were created by known scammer addresses, which were later manually confirmed to be scam tokens (see (Xia_etal_2021, , Sect. 4.4)). In other words, there are addresses that created multiple scam tokens on Uniswap. Recently, in a comprehensive study of the token ecosystem in Ethereum and Binance Smart Chain (BNB), Cernera et al. (Cernera_etal_USENIX2023, ) also discovered a number of scammer addresses that performed multiple 1-day Rug Pulls (exchange pools that were rugged within a day). However, both works assumed that scammer addresses are independent, and the Rug Pulls carried out by them are unrelated, leaving the case of single scammers coordinating multiple scam addresses for future research (see (Cernera_etal_USENIX2023, , Sect. 11)).

Xia et al. (Xia_etal_2021, ) also investigated a related concept of collusion addresses of a scam token/pool creator, which are addresses that likely belong to the same scammer (there were money flow between them and the main scammer address who created the token and the pool) and operate on the same scam pool. While collusion addresses form a small part of our study, they are defined for individual scam pools and do not capture the setting of serial scammers where multiple addresses operate on multiple related scam pools. Xia et al. also noted that there might be more complex networks (e.g. to launder their fund) operating behind the scams that their analysis failed to capture, and hence there might be many more scam addresses not identified by their heuristics (see (Xia_etal_2021, , Sect. 6.3)). Similar to (Xia_etal_2021, ) and (Cernera_etal_USENIX2023, ), other existing works on Rug Pulls (Mazorra_etal_2022, ; Huynh_etal_arxiv_2023, ; Nguyen_etal_2023, ; Zhou_etal_ICSE_SEIP_2024, ) only investigated snapshots of the Rug-Pull scam landscape by zooming in to either individual scam tokens/pools or individual scammer addresses and treating them as independent entities.

In this paper, we seek to address the aforementioned research gap and settle the open problems raised by Xia et al. (Xia_etal_2021, ) and Cernera et al. (Cernera_etal_USENIX2023, ). To that end, we go one step deeper into the world of sophisticated serial (Rug-Pull) scammers by investigating groups of tightly connected addresses (supposedly belonging to the same scammers or scam organizations) that were behind multiple Rug-Pull scam tokens (ERC-20 on Uniswap and BEP-20 on Pancakeswap), which, not surprisingly, have highly similar contracts. In other words, we zoomed out and connected the dots to reconstruct a more comprehensive and accurate picture of how serial Rug-Pull scammers organized their operations.

To facilitate the exposition of the serial scammers, we restricted our investigation to 1-day Simple Rug Pull tokens, which are easy to identify and prevalent on Ethereum and BSC. Such tokens lived for only one day and were paired with a high-value token such as ETH or BNB in a pool, the liquidity of which was provided and removed by a scammer address within a day (see (Cernera_etal_USENIX2023, )). As shown in (Cernera_etal_USENIX2023, ), 1-day Rug-Pull tokens were abundant on Ethereum and BSC, accounting for nearly of all tokens222It was reported in (Cernera_etal_USENIX2023, ) that approximately 60% of tokens on Ethereum and BSC Smart Chain (BNB) have lifetime shorter than a day, and more than 80% among which were Rug Pulls at their time of study. on these chains from inception to March 2022. Note that 1-day Simple Rug Pulls are much easier to detect with higher confidence compared to longer-life Rug Pulls, which were usually labeled by less straightforward rules, e.g. inactive tokens (no activities for more than a month) where the corresponding pools had their liquidity completely removed or had their price dropped more than 90% at some point. Longer-life Rug-Pull tokens could be potentially mixed up with low-performing tokens where the creator decided to remove the liquidity after a long period of no profit without any ill intent.

Wash trading activities in the cryptocurrency ecosystem have been observed and studied in different contexts. For example, wash trading can be carried out to artificially increase the trading volume of cryptocurrency exchanges (LePennecFiedlerAnte_FRL_2021, ; VictorWeintraud_WWW21, ) to influence the perception of their popularity. Wash trading can also be used to boost the trading volume of a Non-Fungible Token (NFT) to reap the reward from an NFT marketplace or inflate its price for reselling (Morgia_etal_ICDCS_2023, ; VonWachter_etal_FCWorkshop22, ; Chen_etal_Internetware2024, ). Wash trading activities were also observed in the context of Rug Pulls of ERC-20 tokens on Uniswap in Xia et al. (Xia_etal_2021, , Sect. 5.3.3), under their investigation of collusion addresses. However, under their heuristics, only wash traders that have a direct transaction with the scammers, i.e. 1-hop neighbors, are included. Even the recently developed A-A Wash-Trading Detector for Uniswap V2 on Dune from SolidusLab (soliduslabs_washtrading_tool, ; soliduslabs_washtrading_blog, ) can only detect self wash trading (or 0-hop wash trader). This simple wash-trading model fails to capture more sophisticated scams in which wash traders are multiple hops away, as frequently observed from our datasets.

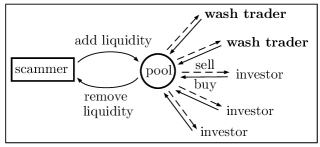

In our work, by building the scam networks of scammer addresses and scam-supporting addresses of serial scammers, we were able to identify all wash-trader addresses, which were funded by the scam networks and bought scam tokens to pump up their prices in order to lure the real investors in (see Fig. 1 and Fig. 2). This allows us to estimate more accurately the real profits of the scammers. As an example, the creator of the Uniswap pool that pairs ETH and a scam token called PUMPKIN added 1.8 ETH and removed 9.27 ETH, seemingly reaped a profit of more than 7 ETH (¿$10,000) after mere 37 minutes, creating the illusion of a highly successful scam. However, as discussed in Section 6.2, it turns out that all major investors were wash traders, and the real profit for the creator of PUMPKIN, after deducting the wash-trading expense, is almost zero!

Our contributions are summarized below.

-

•

We built large 1-day Rug-Pull datasets on Uniswap (uniswap, ) and Pancakeswap (pancakeswap, ) V2, consisting of nearly 632,000 scam pools and 383,000 scammer addresses behind them.

-

•

We formally defined and identified numerous scam patterns in our datasets, including the star-shaped, chain-shaped, and majority-flow clusters. The longest scam chain and the largest scam star consist of 713 and 843 scammer addresses, respectively. These patterns revealed distinctive ways serial scammers coordinated multiple scams on DEXs.

-

•

We further grouped the scammer addresses that interact with each other via a direct ETH/BNB transfer or via a scam pool into scam clusters, and found that token contracts used within each cluster are mostly similar, which indicates that they could be clones from the same source (same scammer).

-

•

Using a novel network explorer algorithm, we were able to reconstruct the complete picture of how serial scammers actually work. In particular, we propose a network-aware profit formula that factors in the wash-trading expenses to achieve a more accurate scam profit estimate.

2. Background

2.1. Ethereum and BNB Smart Chain

Ethereum is the second-most popular blockchain after Bitcoin, with a market capitalization of over US$300 billion at the time of this study (ethereum_cap, ). At the time of its launch in 2015, Ethereum had drawn great attention to the blockchain community by introducing Ethereum Virtual Machine (EVM) and a smart contract concept, becoming a pioneer in contract-supporting blockchains. Smart contracts are executable pieces of code holding business logic. Many applications have been implemented using smart contracts, boosting blockchain to rapidly develop and be widely applied to different domains, such as supply chain, health care, and governance (jaiman2020consent, ; casado2018blockchain, ; novo2018blockchain, ). One of the well-known smart-contract-based applications is fungible tokens.

Fungible tokens are the financial applications used widely as digital assets such as company shares, online game assets, or fiat currencies. Fungible tokens (ERC-20 on Ethereum or BEP-20 on BSC) must follow the common standard (erc20_standard, ; bep20_standard, ) by implementing a set of functions and events (see Table 5 in Appendix A). Accounts are the basic unit in blockchain that is represented by a 20-byte length unique address. Ethereum and BSC accounts are classified into externally owned account (EOA) and contract account (CA). The former is controlled by users via a private-public key pair mapped to the address, while the latter is managed by a contract that contains executable code. Transactions in blockchains are messages between two accounts. Transactions record all activities on blockchains, such as deploying a new smart contract or transferring a digital asset. A fee will be charged to a user when creating a transaction to pay the miners. Transactions are classified based on the type of the sender: a normal transaction is sent from an EOA, while an internal transaction is sent from a CA.

BNB Smart Chain (BSC), a hard fork of Ethereum, was established in 2020 with new features to boost the performance. One of the important updates is the use of a different consensus, allowing faster transaction processing times with lower fees. Similar to Ethereum, BSC is also a smart-contract-supporting blockchain with a very similar token standard (BEP-20).

2.2. Uniswap and Pancakeswap

Decentralised exchanges (DEXs) are financial platforms that operate based on price determination mechanisms such as order books and automated market makers (AMM), allowing users to exchange their digital assets without the involvement of central authorities (werner2022sok, ). Uniswap (uniswap, ) is one of the top popular DEXs, which debuted on Ethereum in 2018. Uniswap is the first DEX that adopted the AMM mechanism successfully with the concept of exchange pools and liquidity providers. An exchange pool in Uniswap operates like a money-exchange counter of two arbitrary currencies (fungible tokens). Exchange liquidity in a pool is provided by one or multiple users (liquidity providers). Anytime a provider adds liquidity (in the form of two corresponding tokens) into a pool, the pool’s smart contract will “mint” LP tokens and send them back to a provider as liquidity shares. A provider can send LP tokens to the pool to withdraw their funds anytime they need. When a pool receives LP tokens from a provider, its smart contract will “burn” them and send the fund back to a provider.

Although Uniswap has launched its fourth version, other versions are still operating as independent platforms. Among them, Uniswap version 2 (UniswapV2) entirely outperforms other versions in terms of the number of listed tokens and pools (coingecko_dex, ). Due to the popularity of this version and its open-source smart contracts, more than 650 DEXs across different blockchains are the forks of UniswapV2 (uniswap_forks, ), and PancakeswapV2 (pancakeswap, ) is the most successful fork on BSC. As such, we choose to study UniswapV2 and PancakeswapV2, noting that our approach is also applicable to other forks of UniswapV2 and other similar DEXs.

3. One-Day Rug Pull Datasets

We first define 1-day Rug Pull scam and then discuss how we constructed the datasets of scam pools, scam tokens, and scammer addresses on Uniswap V2 (Ethereum) and Pancakeswap V2 (BSC).

3.1. One-Day Rug Pull

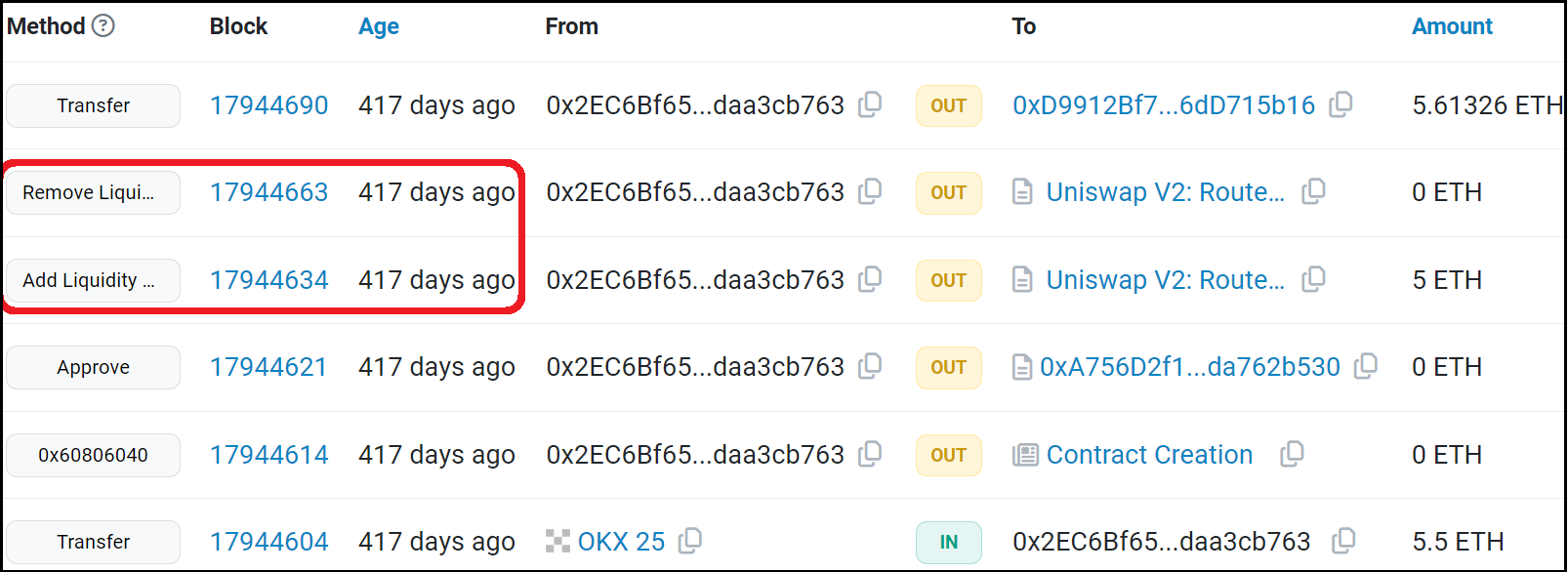

We follow the definition of 1-Day Rug Pull in Cernera et al. (Cernera_etal_USENIX2023, , Sec. 7.1). The definition of scammer addresses were first discussed in Xia et al. (Xia_etal_2021, , Sec. 5.3). See Fig. 10 (Appendix B) for an example of the transaction history of a typical Rug-Pull scammer address.

Definition 3.1 (1-Day Rug Pull).

A 1-day exchange pool is a pool that pairs a higher-value (lower reserve) token and a lower-value (higher reserve) token in which the first and last events happen within a day. An exchange pool is called a 1-day simple Rug Pull if a) it is 1-day, b) the lower-value token is paired in this pool only, and c) it has one mint event and one burn event that burns at least 99% of the minted LP tokens. The corresponding lower-value token of a 1-day simple Rug-Pull pool is also called a 1-day simple Rug-Pull token. We also refer to them as scam pool and scam token for short.

Definition 3.2 (Scammer Addresses).

Given a scam pool, we refer to the addresses of the scam token creator, the scam pool creator, the liquidity provider, and the liquidity remover as scammer addresses behind/associated with the pool.

3.2. Data Collection

We collected data on Uniswap and Pancakeswap from the time they were launched to the time of this study (July 2024).

Exchange Pools. Uniswap works based on three main contracts: Factory, Pair, and Router. The Factory generates an exchange pool (a Pair) for users from two given tokens. The Factory stores the addresses of created Pairs while a Pair stores the addresses of two listed tokens. We first used Web3.py (web3, ) to query all created pools by calling the allPairs function of the Factory. For each collected pool, we then called two functions token0 and token1 from its contract to retrieve the pair of listed tokens. Finally, we used Etherescan APIs (EtherscanAPI, ) and BSCscan APIs (BSCscanAPI, ) for retrieving related information of collected pools and tokens, including their creator address and their contract source codes. As a result, we collected 356,295 pools and 343,637 tokens on Uniswap, and 1,694,058 pools and 1,510,774 tokens on Pancakeswap.

Pool Events. Pool events are the logs of a Pair written down when the state of any property changes. In our study, we collected four pool events, including Mint, Burn, Transfer, and Swap. The first three events occur every time LP-token information is changed. For example, an exchange pool emits a Mint event each time LP-tokens are minted for a new liquidity adding. Similarly, a Burn event is raised when a pool burns the LP tokens received from a liquidity remover. A Transfer event is recorded any time an LP token is transferred from one address to another (ownership change). Unlike these three events, a Swap event is written each time a user swaps tokens in an exchange pool. To collect these events, we used the “getLogs” APIs from Etherscan and BSCscan. To reduce time and computation cost, we only download the first 1000 events of each pool, as it also will not impact our goal of collecting 1-day scam pools/tokens. The downloaded data was then decoded to extract useful information using our event decoder. In consequence, we gathered 2.2 million Mint events, 1.0 million Burn events, 4.7 million Transfer events and 49.9 million Swap events on Uniswap (resp. 17.3 million, 5.1 million, 38.0 million, and 154.9 million events on Pancakeswap).

Rug Pulls and Scammers. Next, with the pool events we gathered in the previous steps, we identify Rug Pull scams on each DEX by using the one-day Rug Pull definition. Notably, we collect all pools that only fire one Mint and one Burn event and examine if 99% of liquidity is burned within a day of it being added. Moreover, we only focus on ETH pools on Uniswap and BNB pools on BSC. This allows us to accurately assess the costs and benefits associated with these scams. According to our analysis, 96% number of pools on Uniswap are ETH pools, and 88% number of pools on Pancakeswap are BNB pools. Thus, the missing cases are not important for our study, but it is difficult to estimate the cost from the token prices. Finally, we extract scammers from identified rug pulls. It is worth noting that we exclude all public addresses (e.g., CEX, bots, bridges) and old addresses that have no transactions within our data collection period. These old addresses appear in our dataset because their tokens were created before the platforms were launched. Ultimately, 161,339 (47%) scam pools and 145,654 unique scammers are determined on Uniswap, and 470,712 (27.78%) scam pools and 238,280 unique scammers are found on Pancakeswap.

4. Serial Scam Patterns: Detection and Analysis

We explore in this section several distinctive funding patterns that reveal how scammer addresses, which potentially belong to the same serial scammers, receive fund to carry out their Rug-Pull scams and transfer the scammed money to another address in a highly coordinated manner. For one of our funding patterns: simple scam chain, we found the top 50 highest average transfer amounts per chain to average 902 ETH for Uniswap and 138 BNB for Pancakeswap. This is the first step in our investigation of serial scammers on DEXs where we deviate from most existing approaches (Xia_etal_2021, ; Cernera_etal_USENIX2023, ; Mazorra_etal_2022, ; Huynh_etal_arxiv_2023, ; Nguyen_etal_2023, ; Zhou_etal_ICSE_SEIP_2024, ), which often treat different scams as unrelated ones.

We henceforth define the following concepts to facilitate our discussion. Given an address A, an in-transaction is a transaction from another address B to A, and B is called an in-neighbor of A. Similarly, an out-transaction is a transaction from A to another address C, which is referred to as an out-neighbor of A. We refer to the buys and sells of a scam token as swap-ins (paying ETH/BNB to the pool) and swap-outs (geting ETH/BNB from the pool).

4.1. Star-Shaped Scam Patterns

We start our scam pattern exploration by defining three types of scam star, representing a commonly found pattern in which scammer addresses are coordinated by a center address (coordinator).

Definition 4.1 (Scam Star).

A scam star consists of a center address (coordinator) and scammer addresses (satellites) that satisfy one of the following patterns.

-

•

OUT-star (common funder): the satellites received at least 100% of the cost to create their first scam from the center but sent no fund to the center. The corresponding in-transaction from must be the largest in-transaction each satellite received before conducting the first scam.

-

•

IN-star (common beneficiary): the satellites received no fund from the center , but transferred at least 90% of their last scam revenue to the center. The corresponding out-transaction to must be the largest out-transaction from each scammer after conducting their last scam.

-

•

IN/OUT-star (common funder/beneficiary): the satellites received at least 100% of the cost to create their first scam from the center . The corresponding in-transaction from must be the largest in-transaction each satellite received before conducting the first scam. Moreover, the satellites transferred at least 90% of their last scam’s revenue to the center. The corresponding out-transaction to the center must also be the largest out-transaction from each scammer after conducting the last scam.

Examples of an IN-star and an IN/OUT-star are given in Fig. 3. Note that while we require that the funding amount from the center must cover 100% of the scam cost (in OUT-stars and an IN/OUT-stars), the value of the OUT transaction only needs to cover at least 90% of the last scam’s revenue. This reflects our observation that a scammer address may also operate as a wash trader, who spends some small portion of the sum received from the funder and from its scam pool to buy (i.e. wash trade) scam tokens from scam pools created by other scammer addresses. More details on how to detect stars are left to Appendix C. We ran our star detection algorithm on the entire Uniswap/BSC datasets and report the statistics below.

| Type | #Stars | Size | Fund In | Fund Out | Period (days) | #Scams |

|---|---|---|---|---|---|---|

| IN | 1575 | 585, 19 | 1173, 6 | 925, 95 | 585, 19 | |

| OUT | 61 | 66, 9 | 1310, 42 | 475, 56 | 66, 10 | |

| IN/OUT | 73 | 159, 15 | 1247, 37 | 1263,36 | 475, 55 | 159, 16 |

| Type | #Stars | Size | Fund In | Fund Out | Period (days) | #Scams |

|---|---|---|---|---|---|---|

| IN | 1815 | 505, 21 | 8436, 98 | 916, 135 | 843, 29 | |

| OUT | 153 | 129, 12 | 2682, 83 | 449, 54 | 616, 18 | |

| IN/OUT | 398 | 200, 16 | 2031, 76 | 2030, 60 | 857, 33 | 222, 20 |

4.2. Max-In-Max-Out Scam Chain

Definition 4.2 (Simple Scam Chain).

A simple scam chain, also referred to as a max-in-max-out scam chain, is a list of scammer addresses () satisfying the following conditions.

-

•

(C1) is the largest funder of , and is the largest beneficiary of , for every .

-

•

(C2) The transfer(s) from to occurred after has completed its last scam and before started its first scam.

A max-in-max-out scam chain is called maximal if no other EOAs can be added to the chain to obtain a longer chain. We only consider maximal scam chains in this work. It is obvious that each scammer belongs to at most one max-in-max-out chain.

| DEX | #Chains | Length | Ave. Transfer | Period (days) | #Scams |

|---|---|---|---|---|---|

| Uniswap | 4494 | 274, 4 | 642, 35 | 369, 3 | 339, 6 |

| Pancakeswap | 14028 | 713555The first address is 0x39b81c24b8aaf10182d63706e940b8994859866d., 4 | 1486, 13 | 251, 2 | 142, 2 |

A simple algorithm can be designed to find all (maximal) max-in-max-out scam chains among a given list of scammer addresses. Our findings on both datasets are reported in Table 3. Except the number of chains, the rest are measurements per chain.

4.3. Majority-Flow Cluster

While the max-in-max-out scam chains capture many cases where each scammer address has a major funder and then sent most scammed fund to another scammer address, they miss the case where there are more than one major funders and/or beneficiaries. For example, when two addresses funded the scammer with 50 and 51 ETH, only the one funding 51 ETH will be recorded by the chain.

We propose below the more sophisticated concept of majority-flow cluster, which takes into consideration the funding amount required to fund a scam (when providing liquidity) and its revenue (when removing liquidity). Such a cluster consists of three kinds of (scammer) addresses: input, internal, and output. Each internal address received 100% funding from input addresses and/or other internal addresses (called the major funders) to carry out its first scams, then transferred at least 90% of its last scam’s revenue to other internal and/or output addresses (called the major beneficiaries). Note that a scammer address may also spend some of its scam revenue on wash trading other scam pools (hence only 90% is required instead of 100% to account for those small spendings). Input addresses and output addresses behaved similarly, but the funders of input addresses and beneficiaries of output addresses do not belong to the cluster, respectively.

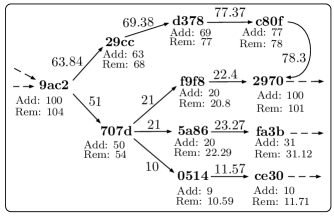

The majority-flow cluster concept reflects more accurately the major flow of funding for scams between scammer addresses on a DEX. An example of a partial majority-flow cluster is given in Fig. 11 (Appendix D). Note that the max-in-max-out chain can only capture scammer addresses along the path -9ac2-29cc-d378-c80f-2970- instead of the whole cluster.

Definition 4.3 (Majority-Flow Cluster).

Given a set of scammer addresses , a majority-flow cluster is subset of , , where every has a set of in-neighbors called the major funders and/or a set of out-neighbors called the major beneficiaries satisfying the following properties.

-

•

(P1) The set consists of the minimum number of in-neighbors with largest in-transaction values (top funders) before the first scam of occurred that together provide enough funding for to fund its first scam.

-

•

(P2) The set consists of the minimum number of out-neighbors with largest out-transaction values (top beneficiaries) after the last scam of occurred that together cover at least of the revenue of the last scam of .

-

•

(P3) For every , it holds that or , and or . Moreover, either or or both must be a subset of .

-

•

(P4) For every , it holds true that if and only if .

-

•

(P5) is connected in the sense that for every , , there is a path where or , for every .

Similar to the chains and stars, we only consider maximal majority-flow clusters, i.e. no other EOAs can be added to obtain a larger one. Each scammer belongs to at most one cluster (see Theorem D.1).

Although the majority-flow clusters require very strict properties, we were still able to find a good number of them on both chains (see Table 4). Those with width two (see Appendix D) have a chain shape (but not the same as the simple chains), whereas those with width larger than two represent the more sophisticated clusters with nodes having more than one major funder/beneficiary.

| DEX | No. Clusters | Size | Width | Fund In | Fund Out |

|---|---|---|---|---|---|

| Uniswap | 5298 | 156, 4 | 7, 2 | 1644.8, 31.8 | 1797, 33 |

| Pancakeswap | 16467 | 820, 4 | 6, 2 | 1098.8, 11.6 | 2625.9, 12 |

5. Scam Clusters Analysis

We have seen in Section 4 how scammer addresses fund themselves via scam clusters with special shapes. In this section, we investigate more general scam clusters, each of which consists of scammer addresses linked together via a direct ETH/BNB transaction or a scam pool. Note that all scam patterns investigated in Section 4 make use of direct ETH/BNB transactions only.

To corroborate our view that all such scammer addresses in the same cluster likely belong to the same serial scammer, we developed AST-Jaccard score (see Appendix E), a new code similarity score based on a careful integration of contract source code’s abstract syntax tree (AST), hash function, and Jaccard similarity to overcome typical code obfuscation techniques used in contract cloning. We measured the similarity among a large number of scam contracts, and found that intra-cluster contracts are mostly similar (average similarity score greater than 0.7) while inter-cluster contracts are mostly dissimilar (average similarity score less than 0.3). This is yet another strong indicator that scammer addresses within each cluster are controlled by the same serial scammer, apart from the fact that such addresses are already either behind the same scam pools or tightly connected in the transaction network. With the new concept of scam clusters and the affirmative contract similarity analysis of them, we have further broadened our understanding of how serial scammers created similar contracts to run a series of Rug-Pull scams on popular DEXs.

5.1. Generating Scam Clusters

Definition 5.1 (Scam Cluster).

Given a dataset of all scammer addresses, a scam cluster is a connected component (see below) , where is a set of scammer addresses and is a set of edges among them, satisfying the following conditions.

-

•

(C1) An edge exists if and only if and had a direct ETH/BNB transaction on the blockchain, or and are different scammer addresses associated with a common scam pool.

-

•

(C2) is connected, that is, for every , , there exists a path from to in .

Note that we only consider maximal scam clusters, i.e., no new scammer address can be added to achieve a larger one.

Given a dataset of all scammer addresses, one can identify all scam clusters by first forming an undirected graph with and is formed using (C1), replacing and by and , respectively, and then find all of its connected components. The scammer addresses belonging to each connected component form a scam cluster. We ran this simple algorithm on both the Uniswap and BSC datasets of scammer addresses and identified all (1-day simple Rug Pull) scam clusters on these DEXs. The results show that 109,471 groups on Uniswap and 136,221 groups on Pankaceswap are formed from 145,654 scammers and 238,280 scammers, respectively. The biggest Uniswap cluster contains 4,155 unique scammers, while the biggest cluster on Pancakeswap is established by 23,399 different addresses. There are also many one-scammer groups on both platforms that occupy nearly 92% Uniswap clusters and 87% Pancakeswap clusters.

5.2. Scam Cluster Analysis

We collected available token contracts from all the scammers in the scam clusters in Section 5, and obtained 111,300 token contracts for 74,254 clusters on Uniswap and 295,461 token contracts for 136,221 clusters on Pancakeswap. We first examined the similarity among contracts that were used by individual scammer addresses and found that nearly 68.8% of scammer addresses on Uniswap and 68.5% of scammer addresses on Pancakeswap deployed multiple contracts with over 80% similarity. Moreover, 2,038 Uniswap scammer addresses and 10,236 Pancakeswap scammer addresses reused the same contract (100% similarity) repeatedly. Among them, e9376660x2c1eb6ca34997f6601cffe791831ad6d5cb9e937 on Uniswap and e4e47770x50cd702d4b11cf6acec84bba739a3fd3a460e4e4 on Pancakeswap deployed the same contract at most 150 times and 1,191 times, respectively.

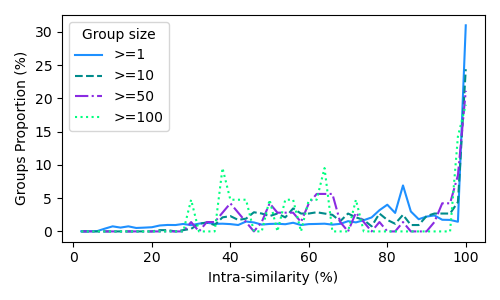

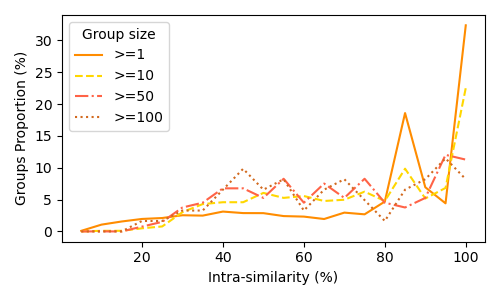

Intra-cluster similarity. Fig 9 (Appendix E) shows the statistic of intra-cluster similarity with different sizes of groups on Uniswap. Specifically, 5,483 groups (33%) on Uniswap have a similarity of over 95%. This proportion does not much change for the set of large-size groups. The opposite phenomenon is observed for the distribution of similarities on Pancakeswap. The proportion of over 95% similarity groups is the same as the proportion on Uniswap with the value of 32% (see Fig 10, Appendix E). However, this number decreases by 10% in the large-size group. The average intra-cluster similarities among all groups are 74% and 75% for Uniswap and Pancakeswap, respectively.

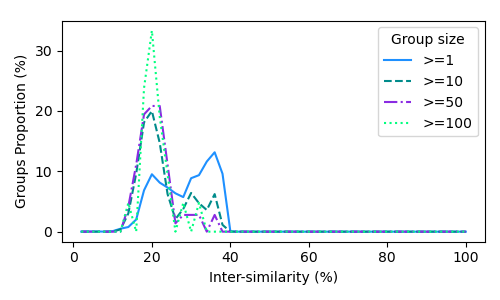

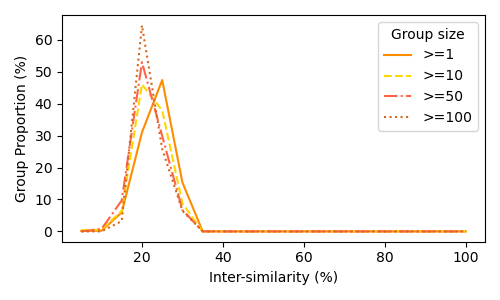

Inter-cluster similarity. Due to high computational cost, in our calculation, we randomly select up to 100 tokens in each group to compare with those in other groups. We also select randomly 500 groups to pair with the chosen group. Then we repeat the calculation 10 times and the final result is obtained by taking the average. The results in Fig 11 and Fig 12 (Appendix E) indicate that tokens in one group are dissimilar to tokens in other groups. Regardless of group size, the similarity is always below 39% for Uniswap clusters and 30% for Pancakeswap clusters. The average similarity for any pair of clusters on Uniswap is 27%, while that on Pancakeswap is 21%.

6. Scam Networks and Profit Estimates

We are now ready to present the most complete picture of how a Rug-Pull scam network (belonging to a serial scammer/scam organization) operates on Uniswap and Pancakeswap. A scam network contains not only scammer addresses but also other associated addresses that serve distinctive roles in the overall scam operation including wash traders, transferrers, depositors, withdrawers, and coordinators. A scam network contains the scam chains and scam stars (Section 4), as well as scam clusters (Section 5) as its subgraphs.

Apart from helping us obtain a complete view of the entire operations of a serial scammer, a concrete benefit of having a complete scam network reconstructed is that the knowledge of the wash traders in the network allows a more accurate computation of the true scam profits. Some of the existing research in DEX Rug Pull were aware of the wash trading activities (Xia_etal_2021, ; Cernera_etal_USENIX2023, ; Huynh_etal_arxiv_2023, ; Sharma_etal_2023, ) but leave it as a future work. This is because without the reconstruction of a scam network, it is impossible to calculate the wash-trading component. Our work seeks to address this research gap.

6.1. Node Labelling

We first define the main roles performed by addresses in a scam network, which are associated with three key operations of such networks: scamming (Rug Pull), wash trading (for scam pools), and (scam) money laundering. All addresses must be in the network.

-

•

S: scammer address - associated with a 1-day scam Rug-Pull pool (see Definition 3.2).

-

•

C: coordinator address - was the largest funder of at least five scammer addresses, and at least 50% of its EOA neighbors must be scammer addresses. The largest funder of an address A is one of the in-neighbours that transferred the maximum amount of high-value token (ETH/BNB) to A.

-

•

WT: wash-trader address - bought at least one 1-day scam token from a 1-day scam pool.

-

•

D/W: depositor/withdrawer address - sent fund to/withdraw from CEXs, mixers, or bridges.

-

•

T: transfer address - received and forwarded fund only and performed no other activities nor retained the fund received. More specifically, the address must only interact with EOAs and moreover, the total out transfers (including transaction fees) must be at least 99% of the total in transfers (not including transaction fees).

-

•

B: boundary address - is not scammer or coordinator, has at least ten token swap-ins and more than 50% of the swap-ins were with non-scam pools.

6.2. Wash Trading and Accurate Profit Estimate

While the presence of wash traders in Rug Pulls on Uniswap was observed as early as 2021 in Xia et al. (Xia_etal_2021, ) and also noted in subsequent works (Cernera_etal_USENIX2023, ; Sharma_etal_2023, ; Huynh_etal_arxiv_2023, ), the actual cost to run wash traders for scam pools, to the best of our knowledge, has never been studied in depth. Thanks to the introduction of the scam network concept, we can determine the wash-trading cost more accurately.

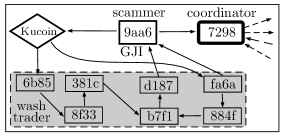

Note that Xia et al. (Xia_etal_2021, ) identified 1-hop wash traders that received direct transaction of ETH from scammer addresses before their swapping of scam tokens. A recently developed wash-trading detection tool by SolidusLab (soliduslabs_washtrading_blog, ; soliduslabs_washtrading_tool, ) can only detect 0-hop wash traders (self wash trading). However, from our datasets, we can see that wash traders could be multiple hops away and never interacted directly with the scammer addresses, e.g. see Fig. 5. The network of wash-trader addresses for GJI (Fig. 5) also provides an interesting counterexample to the common misperception that wash-trader addresses must receive fund from the scammer address before performing wash trading. In the example of GJI, wash traders received fund from a CEX (Kucoin) and among themselves, and even transferred the left-over amounts to the scammer address 9aa6 eventually. This would be somewhat counterintuitive if not for the knowledge of how a scam network operates.

We would also like to note that most research on wash trading for NFTs in the literature (see, e.g. (Morgia_etal_ICDCS_2023, ; VonWachter_etal_FCWorkshop22, ; Chen_etal_Internetware2024, ) and the references therein) studied a different setting in which accounts trade NFTs directly among themselves or via a centralized marketplace like OpenSea or LooksRare, not via an exchange pool. For example, in Morgia et al. (Morgia_etal_ICDCS_2023, ), a graph is built for each NFT with nodes being the addresses directly interacting with the NFT and edges being their direct trade of the NFT. Then, suspicious wash-trading groups include addresses that perform self-trade or strongly connected components that have a common funder or beneficiary, or maintain a zero-risk position (zero balance after all the transactions, factoring out the gas fees). The concept of zero-risk position is irrelevant to the exchange pool setting of fungible ERC-20/BEP-20, in which investors trade with the pool and not among themselves. Also, the edges of the connected components in the wash-trading graph in (Morgia_etal_ICDCS_2023, ) represent NFT tradings, which doesn’t exist in our setting as Uniswap/Pancakeswap investors do not trade ERC-20/BEP-20 tokens after buying them from the pool.

Definition 6.1.

(Existing scam profit formula, e.g. (Cernera_etal_USENIX2023, , Sec. 7.1)) The profit for a scam pool is , where

-

•

is the amount of high-value token (ETH/BNB) that the scammer addresses gave to the pool (by adding liquidity or swapping) plus transaction fees.

-

•

is the amount of high-value token (ETH/BNB) that the scammer addresses gained from the pool (by removing liquidity or swapping) minus transaction fees.

For example, the creator9990x6C1e7FfAe984b5644C2ab95FC3aDF5794317C6aE of the scam token PUMPKIN on Uniswap added ETH (0.014 fee), swapped in twice totaled 0.22 ETH (0.0006 fee) and removed ETH (0.0011 fee) from the pool. Ignoring the very small transaction fees, , and , leading to a sizable profit of (more than US $11,000 back then) for Pumpkin’s creator in less than an hour. We will see next that this estimation is far off from the real profit.

Definition 6.2 (Network-aware profit formula).

The profit for a scam pool within a scam network is , where

-

•

is the amount of high-value token (ETH/BNB) that the addresses in the network paid to the pool, including liquidity additions and swap-ins, plus transaction fees.

-

•

is the amount of high-value token (ETH/BNB) that the addresses in the network gained from the pool (by removing liquidity or swapping out), minus transaction fees.

Note that includes the term in Definition 6.1 and the new wash-trading component - the total amount of high-value token paid to the pool by the wash traders in .

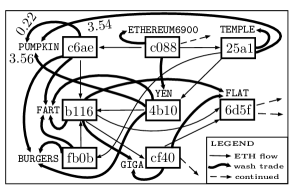

After building the scam network containing Pumpkin’s creator address using our ScamNetworkExplorer algorithm developed in Section 6.3, it becomes clear that all big investors were wash traders from that network. In particular, 4b10 and 25a1 swapped in (multiple times) 3.56 and 3.54 ETH in total, respectively, while the creator c6ae swapped in (twice) 0.22 ETH (see Fig. 6). Using our new formula (Definition 6.2), we obtain that , , and hence the real profit is merely ETH.

Finally, the total profit of a scam network is simply the sum of profits of all scam pools in the network , where is the total fee spent on direct high-value token (ETH/BNB) transactions among the addresses in .

6.3. Generating Scam Network

A natural choice to explore the scam network is to use a Breadth-First Search (BFS) as it can capture essential chain activities including fund transfer/deposit/withdraw and DEX-specific activities such as token swap and transfer, token/pool creation, liquidity providing and removal. Although theoretically straightforward, implementing BFS to identify scam networks on Ethereum and BSC chains is remarkably difficult. There are four main challenges (see Appendix F for a more detailed discussion), but the major one is to avoid network explosion and to prevent the BFS from including public or benign addresses. We will use accounts, addresses, and nodes interchangeably.

Existing approaches. To circumvent the network explosion problem (Challenge 4) when building the transaction subgraph (starting from one or more seed nodes), one must identify/define a boundary, or terminal nodes, at which the BFS stops expanding further. The simplest way is to set the boundary nodes to be just 1-hop neighbors of the scammer nodes (equivalently, from the scam pools). For example, Morgia et al. (Morgia_etal_ICDCS_2023, ) investigated weakly connected components of the subgraph generated by the 1-hop neighbours of the NFT scams to identify wash-trading groups. The issue with this approach is that it treats each scam as an isolated one and fails to recognize the connection among multiple scams (the main topic of our work). Another simple way is to explicitly set the maximum number of hops the BFS can reach, e.g. ten hops as in Yan et al. (Yan_etal_Cybersecurity_2023, , Algo. 1). However, this artificial threshold (ten hops) would lead to an inaccurate picture of a true scam clusters. For instance, we discovered in our work a number of very long scam chains with lengths up to a few hundreds (see Section 4.2). Limiting the BFS to a fixed, small number of hops would also lead to inaccurate statistics on scam clusters and their true profits.

Our modified BFS (see Appendix F) receives as input the scammer list , the scam pool list , and scam token list identified in the data collection phase. It then iterates over , starts from each unvisited address as a seed, retrieves the transaction history of the current address in consideration, and identifies and places its valid neighbors into BFS’s queue for future processing. Valid neighbors of the current address include unvisited/unqueued EOAs that had a non-zero-value transaction (in ETH/BNB) with or were scammer addresses behind the same scam pool as (if is a scammer), were scammer associated with a scam pool that traded with, or traded with the scam pool associated with given that is a scammer.

To address network explosion (Challenge 4), instead of setting the maximum number of hops like in (Morgia_etal_ICDCS_2023, ; Yan_etal_Cybersecurity_2023, ), we allow BFS to expand arbitrarily far, but identifying terminal nodes at which BFS stops expanding. The set of terminate nodes is described as follows. Public terminal nodes are publicly label nodes such as mixers, CEXs, bridges, MEVs, contract deployers, and DEX routers. Similar to most work in the literature, a list of such addresses can be collected from well-known sites such as Etherscan’s WordCloud and Dune, and also manually added on the fly. Normal trading (boundary) nodes are non-scammer/coordinator addresses that had at least 10 swap-ins and at least 50% of them were with non-scam exchange pool. If such an address is reached, BFS won’t add its neighbors to the queue. Big nodes are defined according to two limits and . Addresses that have more than transaction will be ignored. Addresses with more than but at most transactions will be ignored except for scammers and coordinators. We also implemented an address-poisoning-attack detector (see Appendix F) to prevent the BFS to branch out to benign victim addresses.

A case study. Starting from a scam cluster found in Section 5, referred to as Cluster 126, our algorithm outputs an entire network of 240 nodes (available at (research_data, )), including 201 scammers, 234 wash traders, three transferrers, two depositors, and two withdrawers. The total pool profits (across all pools) is , and after deducting the total transfer fee , the net profit is ETH.

7. Conclusion

In this work, we aim to explore and understand how Rug-Pull scammers really worked behind devastating scams on Uniswap and Pancakeswap. We detected many scam patterns, and examined the Rug-Pull scam operations on DEX as a large-scale coordinated network rather than as isolated incidents. We found that building an entire scam network is a challenging but highly rewarding goal. With the knowledge of such a network, several interesting facts were revealed, including a) serial scammers do exist and tend to clone their scam token contracts to organize a series of scams using a large number of addresses, b) the wash traders may not have a direct contact with scammer addresses, and c) the scam profit could have been inaccurately reported due to the neglection of the significant wash-trading amounts. The introduction of scam networks allows us to unite and explain in depth several observations in the literature on how Rug-Pull scammers on DEX work. There are plenty of rooms for future research, and one of the major ones is to develop efficient and accurate network construction and address labelling algorithms that can deal with medium- and large-scale scam networks.

References

- (1) Output research data (2024), https://www.dropbox.com/scl/fo/tiyxjefeli60wrkqm0du3/AMbWVVeCz-VS1tyDY9aa-Yk?rlkey=mikitsogx18zs56pxmymk6t2i&dl=0

- (2) Binance: BEP-20 token standard, https://academy.binance.com/en/glossary/bep-20

- (3) Binance: Binance CEO discusses $20 million scam attempt (2023), https://www.binance.com/en-IN/square/post/910258

- (4) Brill, E., Moore, R.C.: An improved error model for noisy channel spelling correction. In: Proceedings of the 38th annual meeting of the association for computational linguistics. pp. 286–293 (2000)

- (5) Casado-Vara, R., Prieto, J., De la Prieta, F., Corchado, J.M.: How blockchain improves the supply chain: Case study alimentary supply chain. Procedia computer science 134, 393–398 (2018)

- (6) Cernera, F., Morgia, M.L., Mei, A., Sassi, F.: Token spammers, rug pulls, and sniper bots: An analysis of the ecosystem of tokens in Ethereum and in the Binance Smart Chain (BNB). In: 32nd USENIX Security Symposium (USENIX Security 23). pp. 3349–3366 (2023)

- (7) Chainalysis: Chainalysis’s crypto crime report 2022 (2022), https://go.chainalysis.com/rs/503-FAP-074/images/Crypto-Crime-Report-2022.pdf

- (8) Chainalysis: Chainalysis’s crypto crime report 2024 (2024), https://go.chainalysis.com/crypto-crime-2024.html

- (9) Chen, S., Chen, J., Yu, J., Luo, X., Wang, Y.: The dark side of NFTs: A large-scale empirical study of wash trading. In: Proceedings of the 15th Asia-Pacific Symposium on Internetware. p. 447–456. Internetware ’24 (2024)

- (10) Chen, Z., Hu, Y., He, B., Luo, D., Wu, L., Zhou, Y.: Dissecting payload-based transaction phishing on Ethereum. In: Usenix Network and Distributed System Security Symposium (NDSS) - to appear (2025)

- (11) Coingecko: Decentralized exchanges (2024), https://www.coingecko.com/en/exchanges/decentralized?chain=ethereum

- (12) Coinmarketcap: Ethereum martket capitalisation (2024), https://coinmarketcap.com/currencies/ethereum/

- (13) Defillama: UniswapV2 Folks (2024), https://defillama.com/forks

- (14) Ehereum: ERC-20 Token Standard, https://ethereum.org/en/developers/docs/standards/tokens/erc-20/

- (15) Huynh, P.D., Silva, T.D., Dau, S.H., Li, X., Gondal, I., Viterbo, E.: From programming bugs to multimillion-dollar scams: An analysis of trapdoor tokens on decentralized exchanges (2023), https://arxiv.org/abs/2309.04700

- (16) Immunefi: Immunefi crypto losses report, https://immunefi.com/research/

- (17) Jaiman, V., Urovi, V.: A consent model for blockchain-based health data sharing platforms. IEEE access 8, 143734–143745 (2020)

- (18) Labs, S.: A-A wash trading detection on Uniswap V2: A new tool for investors & investigators (2023), https://dune.com/blog/a-a-wash-trading-detection-on-uniswap-v2-a-new-tool-for-investors-investigators

- (19) Labs, S.: A-A wash trading detector (uniswap v2) (2023), https://dune.com/trenlo/a-a-wash-trading-detector

- (20) Levenshtein, V.I., et al.: Binary codes capable of correcting deletions, insertions, and reversals. In: Soviet physics doklady. vol. 10, pp. 707–710. Soviet Union (1966)

- (21) Mazorra, B., Adan, V., Daza, V.: Do not rug on me: Leveraging machine learning techniques for automated scam detection. Mathematics 10(6) (2022)

- (22) Morgia, M.L., Mei, A., Mongardini, A.M., Nemmi, E.N.: A game of NFTs: Characterizing NFT wash trading in the Ethereum blockchain. In: 2023 IEEE 43rd International Conference on Distributed Computing Systems (ICDCS). pp. 13–24 (2023)

- (23) Nguyen, M.H., Huynh, P.D., Dau, S.H., Li, X.: Rug-pull malicious token detection on blockchain using supervised learning with feature engineering. In: Proceedings of the 2023 Australasian Computer Science Week. pp. 72––81. ACSW ’23 (2023)

- (24) Novo, O.: Blockchain meets IoT: An architecture for scalable access management in IoT. IEEE internet of things journal 5(2), 1184–1195 (2018)

- (25) OpenZeppelin: Smart Contracts Library (2024), https://www.openzeppelin.com/solidity-contracts

- (26) Pancakeswap: https://pancakeswap.finance/

- (27) Paterson, M., Dančík, V.: Longest common subsequences. In: International symposium on mathematical foundations of computer science. pp. 127–142. Springer (1994)

- (28) Pennec, G.L., Fiedler, I., Ante, L.: Wash trading at cryptocurrency exchanges. Finance Research Letters 43, 101982 (2021)

- (29) Sharma, T., Agarwal, R., Shukla, S.K.: Understanding rug pulls: An in-depth behavioral analysis of fraudulent NFT creators. ACM Trans. Web 18(1) (oct 2023)

- (30) Etherscan team, T.: BSCscan API (2015), https://bscscan.com/apis

- (31) Etherscan team, T.: Etherscan API (2015), https://etherscan.io/apis

- (32) Uniswap: https://uniswap.org/

- (33) Victor, F., Weintraud, A.M.: Detecting and quantifying wash trading on decentralized cryptocurrency exchanges. In: Proceedings of the Web Conference 2021. pp. 23––32. WWW ’21 (2021)

- (34) von Wachter, V., Jensen, J.R., Regner, F., Ross, O.: NFT wash trading: Quantifying suspicious behaviour in NFT markets. In: Financial Cryptography and Data Security. FC 2022 International Workshops: CoDecFin, DeFi, Voting, WTSC, Grenada, May 6, 2022, Revised Selected Papers. p. 299–311 (2023)

- (35) Web3.py: Python library for interacting with ethereum (2024), https://web3py.readthedocs.io/en/stable/

- (36) Werner, S., Perez, D., Gudgeon, L., Klages-Mundt, A., Harz, D., Knottenbelt, W.: Sok: Decentralized finance (defi). In: Proceedings of the 4th ACM Conference on Advances in Financial Technologies. pp. 30–46 (2022)

- (37) Wikipedia: Jaccard index (2024), https://en.wikipedia.org/wiki/Jaccard_index

- (38) Xia, P., Wang, H., Gao, B., Su, W., Yu, Z., Luo, X., Zhang, C., Xiao, X., Xu, G.: Trade or trick? Detecting and characterizing scam tokens on Uniswap decentralized exchange. Proc. ACM Meas. Anal. Comput. Syst. 5(3) (2021)

- (39) Yan, C., Zhang, C., Shen, M., Li, N., Liu, J., Qi, Y., Lu, Z., Liu, Y.: Aparecium: Understanding and detecting scam behaviors on Ethereum via biased random walk. Cybersecurity 6 (10 2023)

- (40) Zhou, Y., Sun, J., Ma, F., Chen, Y., Yan, Z., Jiang, Y.: Stop pulling my rug: Exposing rug pull risks in crypto token to investors. In: Proceedings of the 46th International Conference on Software Engineering: Software Engineering in Practice. pp. 228––239. ICSE-SEIP ’24 (2024)

Appendix A Functions and Events of ERC/BEP-20

Table 5 shows the set of common functions and events that ERC-20 tokens and BEP-20 tokens must follow.

| Type | Signature | Description |

| Method | name() | Getting name of the token (e.g., Dogecoin) |

| symbol() | Get symbol of the token (e.g., DOGE) | |

| decimals() | Get the number of decimals the token uses | |

| totalSupply() | Get the total amount of the token in circulation | |

| balanceOf() | Get the amount of token owned by given address | |

| transfer() | Transfer amount of tokens to given address from message caller | |

| transferFrom() | Transfer amount of tokens between two given accounts | |

| approve() | Allow a spender spend token on behalf of owner | |

| allowance() | Get amount that the spender will be allowed to spend | |

| Event | Transfer() | Trigger when tokens are transferred, including zero value transfers. |

| Approval() | Trigger on any successful call to approve() |

Appendix B One-Day Rug Pull Detection

One-day rug pull detection can be found in Procedure 1 below. Fig 10 illustrates an example of the transaction history of a typical Rug-Pull scammer address.

Appendix C Detecting Scam Stars

Given a list of scammer addresses, we developed StarDetector, an algorithm that detects all scam stars containing such addresses. First, for each scammer address , StarDetector identifies its major funder as the in-neighbour that satisfies the following conditions: F1) funded at least 100% of the cost of the first scam carried out by with a single in-transaction before the first scam, and F2) must be the (strictly) largest funder of . Similarly, StarDetector identifies the major beneficiary of as the out-neighbour that satisfies the following conditions: B1) transferred at least of its last scam’s revenue to in a single out-transaction after the last scam, and B2) the corresponding out-transaction must be the largest out-transaction after the last scam is conducted.

Next, StarDetector identifies the star type(s) that potentially belongs to as follows: if then may belong to a single IN/OUT-star with center ; otherwise, if never received any fund from then may belong to an OUT-star with center , and if never funded then may belong to an IN-star with center . Note that it is possible that belongs to both an IN-star and an OUT-star (with different centers). For each star type and the corresponding potential center or or , the algorithm then examines each of ’s neighbors and checks whether is also their potential star center of the corresponding type. If there are neighbors of (including the original scammer address ), then StarDetector returns the corresponding star, and then repeats with other addresses. The algorithm also keeps track of the star type each address already belongs to for avoiding redundant work.

Appendix D Detecting Majority-Flow Clusters

Finding all (maximal) majority-flow clusters among a given list of scammer addresses is a nontrivial task due to the strong properties required by the clusters. In particular, (P3) required that for every scammer address , its major funders either all lie inside or all lie outside . Similar requirement applies to its major beneficiaries. Especially, (P4) requires that for every two scammer addresses and in , is a major funder of if and only if is a major beneficiary of , which is a very strong condition, linking the funder-beneficiary addresses in both directions. We leave the details of the detection algorithm and its proof to Appendix D.

Theorem D.1 (Majority-Flow Clusters).

Given a set of scammer addresses, each address belongs to at most one majority-flow cluster, and moreover, FundingClusterDetectorcorrectly returns all maximal majority-flow clusters within (as in Definition 4.3) in time , where denotes the set of all transactions among scammer addresses within .

We proposed FundingClusterDetector, an efficient algorithm that identifies all (maximal) majority-flow clusters among all scammers in in polynomial time in . We describe below its main steps. The key idea is to first identify all minimal majority-flow clusters, i.e., those that satisfy (P1)-(P4), which contain no proper majority-flow sub-clusters. These minimal clusters will be the building blocks of the desired maximal clusters. This is done in Step 3, which groups together funder-to-beneficiary transactions within that must belong to the same majority-flow clusters. Step 4 constructs the maximal clusters by connecting the transaction groups (and hence the corresponding scammer addresses) that have at least one scammer address in common. This can be done by applying a breadth-first search algorithm to the transaction-clustering graph introduced in Step 4.

Step 1. The algorithm first constructs the sets of major funders and major beneficiaries (if any) for every scammer address . Remove all from where both and do not exist.

Step 2. From the sets and obtained in Step 1, the algorithm builds a set of majority-flow transactions , where and are the set of transactions from the major funders of to and from to its major beneficiaries (if any).

Step 3. The algorithm partitions the set of transactions into non-overlapping groups satisfying the following property: if , , contains a transaction (with and being the sender and the receiver, respectively), then it must also contain all transactions . Moreover, let be the set of all the scammer addresses being the sender or receiver in a transaction in . This step can be implemented efficiently using a FIFO queue.

Step 4. The algorithm first builds the so-called transaction-partiti-oning graph , with its vertex set consists of all the transaction groups, and its edge set defined as . The algorithm then finds all connected components of (e.g. by using the breadth-first search) and returns them as maximal majority-flow clusters in .

Appendix E Contract Similarity

We discuss in this appendix the preprocessing step and the construction of our newly developed AST-Jaccard similiarity score that can bypass a number of obfuscation techniques when comparing scam contracts.

Popular string metrics used for measuring the source code similarity between two contracts include Levenshtein (edit) distance (levenshtein1966binary, ), longest common subsequences (paterson1994longest, ), and Damerau-Levenshtein distance (brill2000improved, ). However, such metrics are not only expensive to compute over a large number of contract pairs but also susceptible to simple code obfuscation techniques. For example, to reduce the similarity score between two contract clones, scammers can employ techniques like (M1) comments and spaces insertion/deletion, (M2) identifier/variable names modification, or (M3) code reordering to increase the edit distance arbitrarily. To tackle these, we propose a token-based similarity score call AST-Jaccard score, which leverages source code’s AST, a collision-resistant hash function, and Jaccard similarity to compare scam contracts.

More specifically, as AST keeps the syntax and sematic information of the source code while ignoring non-essential information such as spaces, comments, specific function and variable names, using AST instead of the source code itself tackles (M1) and (M2). To bypass (M3) code reordering, e.g. swapping functions or variables around, the new score uses the Keccak-256 hashing algorithm to hash all tokens/components in the AST of each source code and group them into a set. As the order of elements is not important for a set, even when the variables and function were rearranged, the Jaccard similarity on sets still pick up the right overlapping ratio between the two sets corresponding to two contract codes. To further improve the accuracy, we also applied a preprocessing steps to remove all common libraries and interfaces in every source code, which account for 40%-50% of the code itself and would interfere with the score. More details about the preprocessing and the AST-Jaccard score can be found in Appendix E.

Common Libraries and Interfaces Removal. Fungible tokens are implemented by following the common standard (e.g ERC-20 or BEP-20 interface) so these tokens often contains the common codes from the interface, inflating their similarity. The similarity continues to increase if they used the same common libraries such as SafeMath, Address, or Ownable. Hence, to avoid this inflation, we remove all common libraries and interfaces from tokens before measuring their similarities. To that end, we first collect all common libraries on OpenZeppelin (openzeppelin, ), an open-source framework for writing secure and scalable smart contracts. Then we remove all these libraries and interfaces from token’s contracts before doing tokenisations.

Code Tokenisation. Our approach first parses the source code of a contract to an AST, which keeps the syntax and semantic information of a contract only. Subsequently, we extract a token from a type of each node in the AST (e.g., Mapping, IfStatement, BinaryOperation, Assignment). In this manner, some inessential information such as spaces, comments, function names, variable names and their values will be eliminated. Thus, we can solve M1 and M2. We run an extraction for each component in a contract, such as state variables, functions, events, and modifiers. Notably, code lines in a component will be parsed to an array of tokens. For example, we can get correspondingly an array of IfStatement, BlockIdentifier, IndexAccess, BinaryOperation, and Literal tokens from the if condition “if(sender[i] == ‘0x0d83a1’)”. In other words, each array of tokens marks the semantic information of each component in a contract.

Integration of AST, hash function, and Jaccard similarity Score. Next, we try to overcome M3 at a contract level, i.e. to identify a clone of a contract even if the scammer has reordered different components in the contract. Our approach does not focus on a component level because we are unsure whether different code line arrangements in a component will give out the same working logic or not (e.g., a code line is inside or outside a condition block) while our main goal is to build a ground truth dataset for a Trapdoor detection problem. Therefore, two contracts are totally the same if they contain the same list of components. To improve our algorithm’s performance, we concatenate all tokens in the token array of a component as a string and apply a Keccak-256 hash algorithm. As a result, each component in the contract will be represented as a unique hash (256 bits). Next, we employ the classic Jaccard index (jaccard, ) for two corresponding sets of hashes as in (1), where is the similarity between two contracts, is a list of hashes of the first contract and is a list of hashes of the second contract.

| (1) |

The overall algorithm is presented below.

Appendix F Scam Network Construction

There are many challenges when constructing a scam network using BFS.

Challenge 1. The background graph is non-homogeneous. Indeed, nodes in the transaction graph include externally owned accounts (EOAs) and contract accounts. Contract accounts could be a mixer, a centralized exchange, a bridge, a router, a bot (MEV, trading bots), a token deployer, each type behaves differently and requires a different treatment.

Challenge 2. Identifying an edge between two accounts is challenging and requires domain knowledge. For example, an edge exists between two EOAs A and B not only when A transferred fund to B directly, but also when A buys a scam token created by B or invested in a scam pool rugged by B. On the other hand, if A sends a 0-value transaction to B (a message-carrying transaction), that shouldn’t be counted as an edge121212Our algorithm initially hit a non-scam account that sent a transaction to a known scam account. It turns out that the transaction only carries a sneering message..

Challenge 3. The background graph is huge and unavailable. By contrast to the standard setting in the traditional graph theory, due to its sheer size, the complete underlying transaction graph among all accounts on Ethereum or BSC (or any other established chain) is not available and impossible to build131313For example, the Ethereum chain generates more than a million new transactions everyday (see https://ycharts.com/indicators/ethereum_transactions_per_day)..

Challenge 4. Network explosion. Starting from a (seed) scammer node, the standard BFS can quickly expand to include an unmanageable number of nodes in its queue, especially when the node in consideration starts transacting with public accounts (CEXs, mixers, bridges), or trading from non-scam pools. Thus, we must be able to recognize the boundary nodes associated with non-scam activities, to prevent BFS from including normal nodes unrelated to the scammers, which may have been active for years with thousands to hundreds of thousands of transactions and would fairly quickly overwhelm BFS’s memory and pollute the real scam cluster.

Apart from the above, irrelevant transactions generated by phishing attacks (e.g. address-poisoning attacks) can also confuse the BFS, making it jump out of the scam network by mistake.

Address-poisoning attacks can break BFS. Phishing attackers target everyone, including addresses in Rug-Pull scam networks. Dusting attack or dust value transfer (see, e.g. (Binance_20M_phishing, ; Chen_etal_NDSS2025, )) is a common type of address poisoning attack in which an address that looks very similar to the victim’s out-neighbor (see Fig. 13) transferred a tiny amount to the victim address. A naive BFS may expand from a node in the scam network that was the target of a dusting attack to visit the attacker address, then to its coordinator address (the one who coordinates all the phishing attacks) and then unknowingly to all of its (benign) victim addresses in the network. We implemented a simple phishing detector that excludes a phishing address from the set of valid neighbors for each address in BFS, which detected dozens to hundreds of such addresses for every network we tried.