remarkRemark \newsiamremarkhypothesisHypothesis \newsiamthmclaimClaim \headersGenerative Modeling with DiffusionJustin Le \dedicationProject advisors: Sebastien Motsch††thanks: Arizona State University, Tempe, AZ (). and Johannes Brust††thanks: Arizona State University, Tempe, AZ ().

Generative Modeling with Diffusion

Abstract

We introduce the diffusion model as a method to generate new samples. Generative models have been recently adopted for tasks such as art generation (Stable Diffusion, Dall-E) and text generation (ChatGPT). Diffusion models in particular apply noise to sample data and then ?reverse? this noising process to generate new samples. We will formally define the noising and denoising processes, then introduce algorithms to train and generate with a diffusion model. Finally, we will explore a potential application of diffusion models in improving classifier performance on imbalanced data.

1 Introduction

Generative models create new data instances. Recently, generative models have seen applications in image generation [15] and text generation [14]. In this article, we are interested in generative models that create data instances that

?mimic? some given sample data. Doing so will allow us to sample arbitrarily many points from the distribution underlying the original sample data. Fig. 1 shows a sketch for an image generating model. In a broad sense, the model receives a sample of training images, which

?learns? the structure of the images, then uses that knowledge to create new images that mimic the original sample. Common architectures used for generative models include Generative Adversarial Networks [6, 19], Variational Autoencoders [10], and Transformers [18, 9]. For this article, we will develop diffusion models [7, 20, 16]. In particular, we seek to formally define how diffusion models are trained and how diffusion models generate new samples.

In Section 4, we explore an application of diffusion models for improving classifier performance (this is in contrast to the typical application of diffusion models as image generators). To this end, we will focus on a dataset of credit card transactions, of which an exceedingly small minority are fraudulent, and the rest are legitimate. Our aim is to use diffusion models to generate data mimicking the fraudulent transactions, then augmenting the training data with this generated data before training the classifier.

1.1 Diffusion Models

Diffusion models iteratively apply noise to data until the initial distribution of the data is unrecognizable, and then, after learning this

?noising phase?, reverse the noising to recover the initial sample. We will refer to this noising phase as the forward process and this denoising phase the reverse process. More specifically, the forward process will transform the sample data into a standard normal distribution (that is, normal with mean 0 and unit variance). Then, to generate new data, we sample new points from a standard normal distribution and apply the reverse process to recover an approximation of the sample data. This scheme will allow us to generate arbitrarily many points that mimic the initial sample.

In addition to converging to a standard normal, we would also like the noising process to be continuous, converge quickly, and have randomness enforced at each time step. The randomness in the noising process is key, as this is what allows the generated data to be slightly different from the original sample when we denoise the data. To formally define the noising process, we will introduce the Ornstein-Uhlenbeck equation in Section 2, which is a type of Stochastic Differential Equation (SDE). The solution to this equation will satisfy the above properties and will therefore be used to define the forward process. After defining the forward process, we can then deduce the reverse process, and use this to generate samples.

2 Theory of Diffusion Models

Our first step towards developing diffusion models is to formally define the forward process. We achieve this with the following SDE.

2.1 The Ornstein-Uhlenbeck Equation

We consider an Ornstein-Uhlenbeck equation in given by

| (1) |

In contrast to an ODE, the solution to is a continuous-time stochastic process, and the initial condition is our original sample. The overarching goal of a diffusion model is to generate samples from the underlying distribution of .

The term is known as the drift and is the non-stochastic element of the SDE. Intuitively, this drift term contributes exponential decay, as it is known that the ODE

has as its solution

The stochastic process is responsible for enforcing randomness in this SDE. We call a Wiener process (or Brownian motion). A Wiener process can be thought of as modeling particles dispersing in space over time.

We will begin by proposing an explicit solution to equation (1).

Proposition 2.1.

This solution is the forward process described in Section 1.1. See Appendix A for more information of how this solution is obtained.

To condense our notation, we will denote

for all . Then, equation (2) becomes

| (3) |

Notice that for all . Moreover, since and , we have that converges in distribution to a standard normal as . Moreover, and are continuous and converge exponentially to their respective limits, meaning the forward process has the desired properties of randomness, rapid convergence to a standard normal, and continuity.

2.2 Discretizing the Time Domain

We now consider a discretization of the time domain to simulate solutions to equation (1). Fixing , let be a finite sequence of positive real numbers (we discuss a more detailed scheme to define the in Appendix B). Then, define and for . In other words, the represent our discrete time values while the describe the steps in time. We denote

This discretization allows us to define a recursive formula for computing , which comes as a corollary of Proposition 2.1.

Corollary 2.2.

For all ,

| (4) |

where are i.i.d. standard normal random variables.

This result is obtained similarly to (3) – see Appendix A for more details.

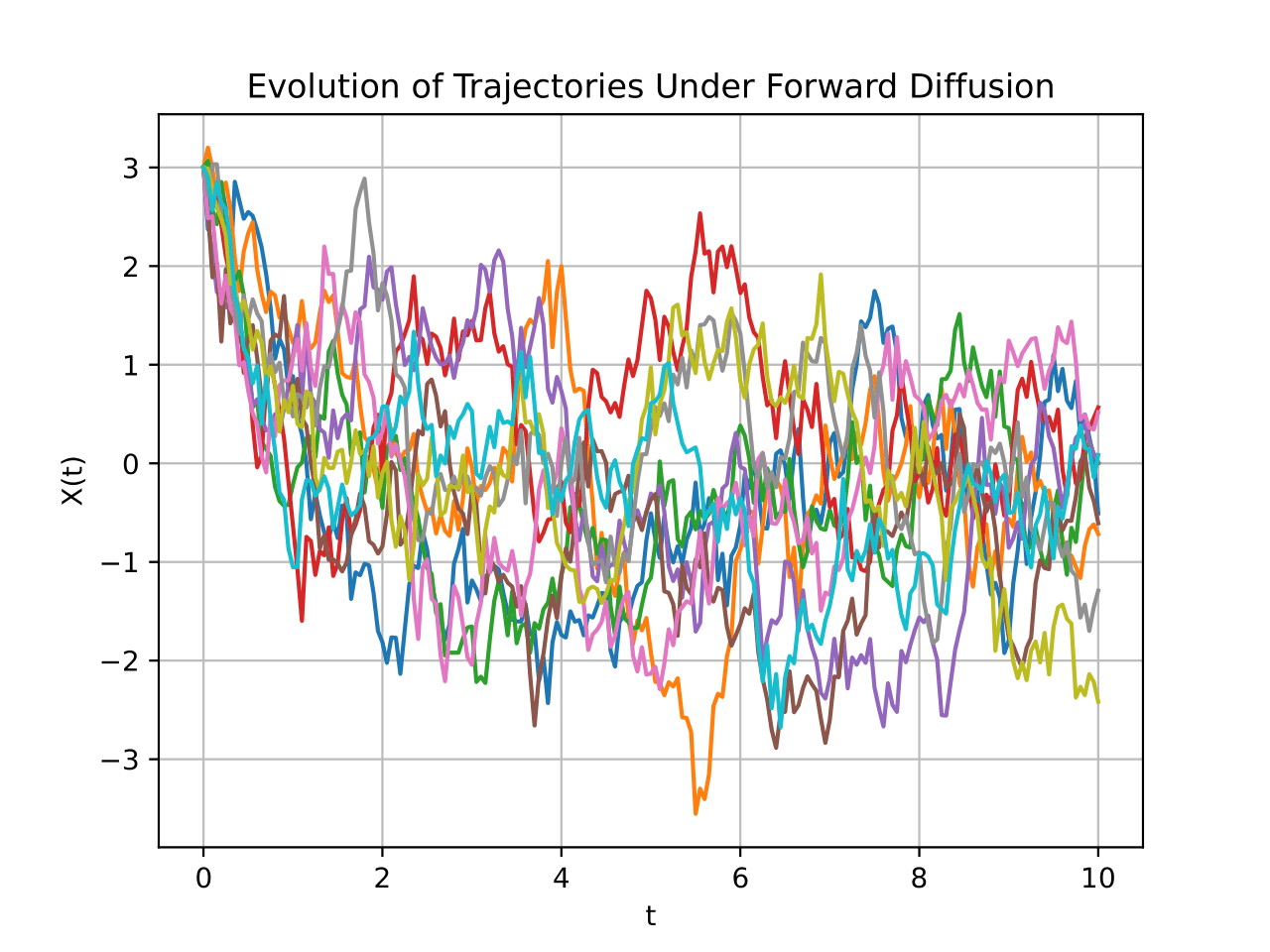

To simulate the forward process on sample data, we take and iteratively apply equation (4) with in place of , and sampled from a standard normal distribution in place of . Note that the are sampled independently in each iteration. Fig. 2 shows the trajectories and kernel density estimate (KDE) under equation (4) with being sampled from a Dirac mass centered at 3. Importantly, despite the fact that all 10 trajectories begin at the same position, each of the trajectories split off into different directions because of the randomness enforced in equation (4). Moreover, as increases, the distribution of begins to resemble that of a standard normal.

2.3 Reverse Diffusion

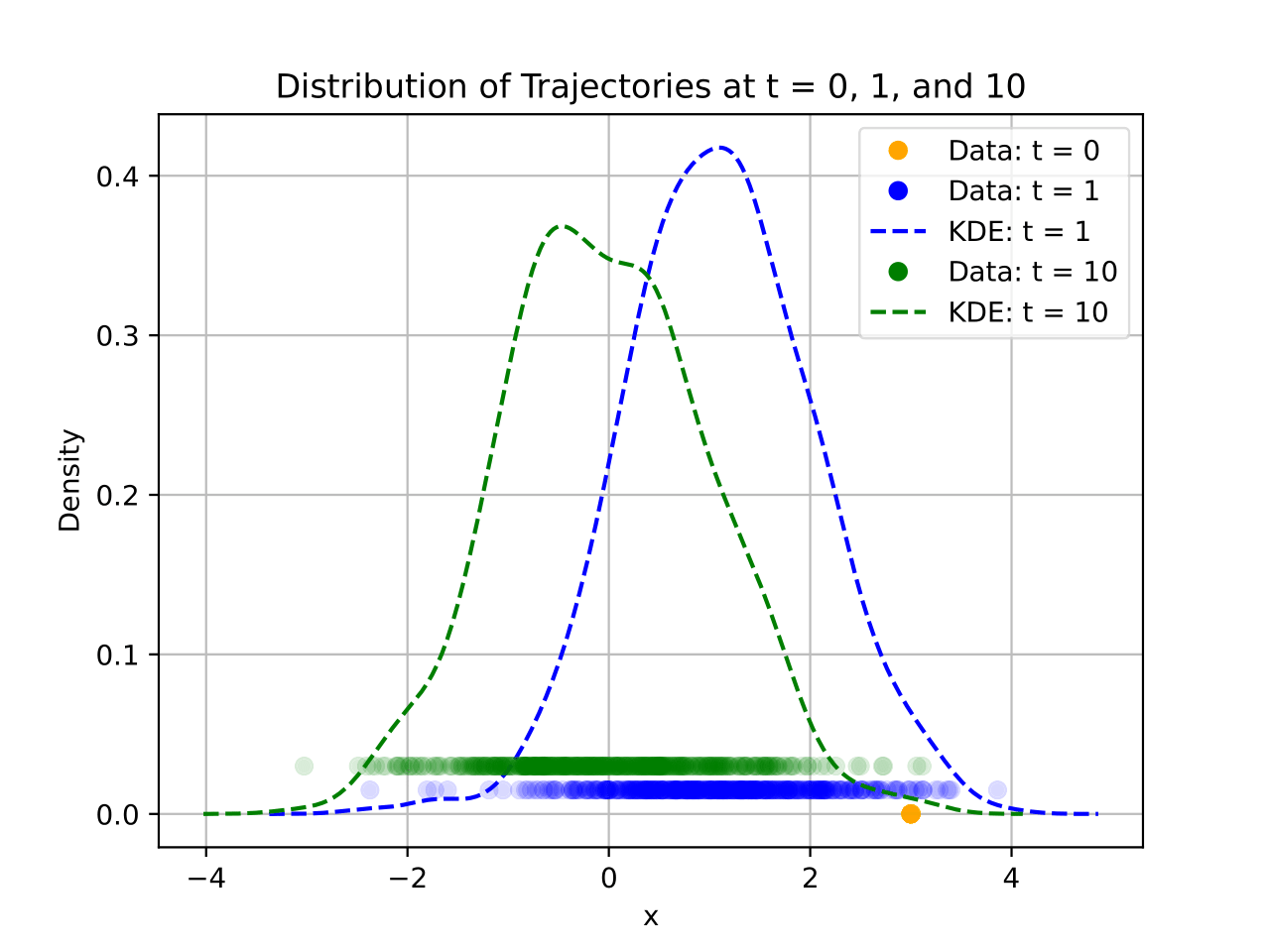

We have seen that the forward diffusion process takes any initial distribution and transforms it into a standard normal. We now ask whether or not the forward diffusion process can be reversed. In particular, starting from data sampled from a standard normal distribution, we want to know if the forward diffusion process can be applied in reverse to obtain data that mimics the original sample. Fig. 3 is a plot of the forward and reverse processes applied to a simple dataset in . Once again, the forward process begins with the original sample data and iteratively applies noise. To generate a new sample with the reverse process, we begin by sampling new points from a standard normal and iteratively denoising the data. The resulting ?denoised? data resembles the original sample, but is not exactly the same. Like with the forward process, the reverse process does obey an SDE (this is explored in [17]). In this paper, we are not interested in this reverse SDE – instead, we will deduce the reverse process by leveraging the discrete time steps we discussed in Section 2.2. Doing so will give us a discretized version of the reverse process.

Recall that the discretized forward diffusion process gives a finite sequence of random variables . We will assume and are chosen such that is approximately standard normal for the given initial condition . Ideally, we would want to determine the conditional density (that is, given the future position of a trajectory, we want to determine the distribution of its present position). However, deducing this conditional density is an ill-posed problem. This is because every initial condition converges to a standard normal under the forward diffusion process. Therefore, if we start from and have no information on the initial condition , the conditional density is not unique.

Instead, we will look to deduce – that is, given the future and initial position of a trajectory, we want to determine the distribution of its present position. Starting from and iteratively computing the conditional density of the previous time step will result in an approximation of .

The following proposition addresses how this conditional density is obtained:

Proposition 2.3.

Let and suppose and . Then,

| (5) |

with and defined as

| (6) |

| (7) |

See Appendix C for a detailed proof of this result.

With this proposition, we can determine the distribution of if we know the values taken on by

and . In fact, this proposition tells us that the discretized reverse diffusion process is nothing more than computing a mean and variance, then sampling from a normal distribution – Fig. 4 shows a sketch of this procedure. This result can also be extended to . In particular, if , equations Eq. 6 and Eq. 7 yield and . This is consistent with the fact that the conditional distribution of given is with probability 1.

What’s more, the discretized reverse diffusion will tend towards as tends to 0, confirming that this reverse diffusion process does indeed

?reverse? the forward process outlined in Section 2.1.

Importantly, the variance term only depends on the iteration (i.e., there is no dependence on the position of the trajectory). Because we control these iterations, the variance of the discretized reverse diffusion process is always known. On the other hand, the mean depends on both and . In other words, is the only quantity of interest in the reverse diffusion process that encodes information from the distribution of .

3 Building a Diffusion Model

When generating data with the reverse diffusion process, we must begin by sampling points from a standard normal. As a result, when applying the reverse diffusion process to these points, the initial condition (i.e., the value taken on by ) is not known, meaning cannot be directly computed. To circumvent this, we will construct a scheme to estimate while only knowing and . For this, we employ techniques from machine learning to ?learn? the value of from the original sample. Letting be the set of parameters of our model, we will let denote the expectation of predicted by our model and denote the true expectation of given and . A brief outline for training this model is as follows:

-

1.

Apply the forward diffusion process to for a finite number of steps.

-

2.

For each step, compute with equation .

-

3.

Use the model to predict for each step.

-

4.

Update to minimize the distance .

With this scheme, the information from gets encoded into the parameter set . In other words, our model learns the distribution underlying the original sample.

3.1 Alternative Methods to Approximate

Since our model will know the values of and , the only unknown quantity in the expression for is . Thus, instead of predicting directly with our model, we may instead opt to predict with our model and then use this prediction to compute an estimate of . This way, we avoid using the model to predict all the terms which are already known (namely, the terms dependent on and ). We also have another method for estimating :

Using equation (3), we write

| (8) |

where is sampled from a standard normal distribution. Substituting this into equation and simplifying will yield

| (9) |

Intuitively, one can think of as the ?noise? that transforms into . By predicting this noise term , we can estimate the value of . Using equations (6) and (9), we now define two alternative methods for determining :

| (10) | ||||

| (11) |

where and are (respectively) the estimates of and produced by our model. To summarize, we have three methods to estimate :

-

1.

Use the model to estimate .

-

2.

Use the model to estimate and compute with equation (10).

-

3.

Use the model to estimate and compute with equation (11).

Note that methods 2 and 3 are fundamentally identical and can simply be thought of as a change of variables. Going forward, we will choose to employ method 3 for estimating , and the training and generating algorithms discussed in subsections 3.2 and 3.3 will use method 3. With our method for estimating determined, we must address how is optimized such that approximates .

3.2 Learning from Forward Diffusion

Let be a discretized sample path of the forward process starting at . Solving for in equation gives us

| (12) |

for all time steps . In the pursuit of generating new datapoints, we are looking to learn without using the initial distribution . To achieve this, we will simulate trajectories of the forward process where the initial condition is the sample data. At each step, our model will predict as an estimate of . Then, the model will be tuned to minimize the distance between and . In doing so, the model will learn how to predict without ever seeing the initial condition. Algorithm gives a description of how a diffusion model is trained on a single point .

3.3 Generating with Reverse Diffusion

After training the model on multiple trajectories under the forward process starting at the points in the original sample, we are now able to synthesize arbitrarily many data points that ?mimic? our original data. Algorithm (2) describes how to generate a new data point. This algorithm simulates the reverse diffusion process – at each step, is computed as an approximation of the true noise . This is used to estimate , which then ?guides? the reverse trajectories towards an estimate of the initial condition.

4 Applications for Improving Classifier Performance

We will now consider diffusion models as a method to improve classifier performance. For this, we will use a dataset of credit card transactions [3, 4] from Kaggle (https://www.kaggle.com/datasets/mlg-ulb/creditcardfraud). This dataset contains information on 284,807 transactions, of which only 492 are fraudulent (this gives a fraud prevalence rate of approximately ). Because of this, one might be interested in generating data that mimics the fraudulent transactions, and then appending this generated data to the training data. In doing so, we may see improvement in a classifier’s ability to detect fraud. In particular, we are interested in a classifier’s precision and recall when trained with and without diffusion augmented data, which we define as follows:

| Precision | |||

| Recall |

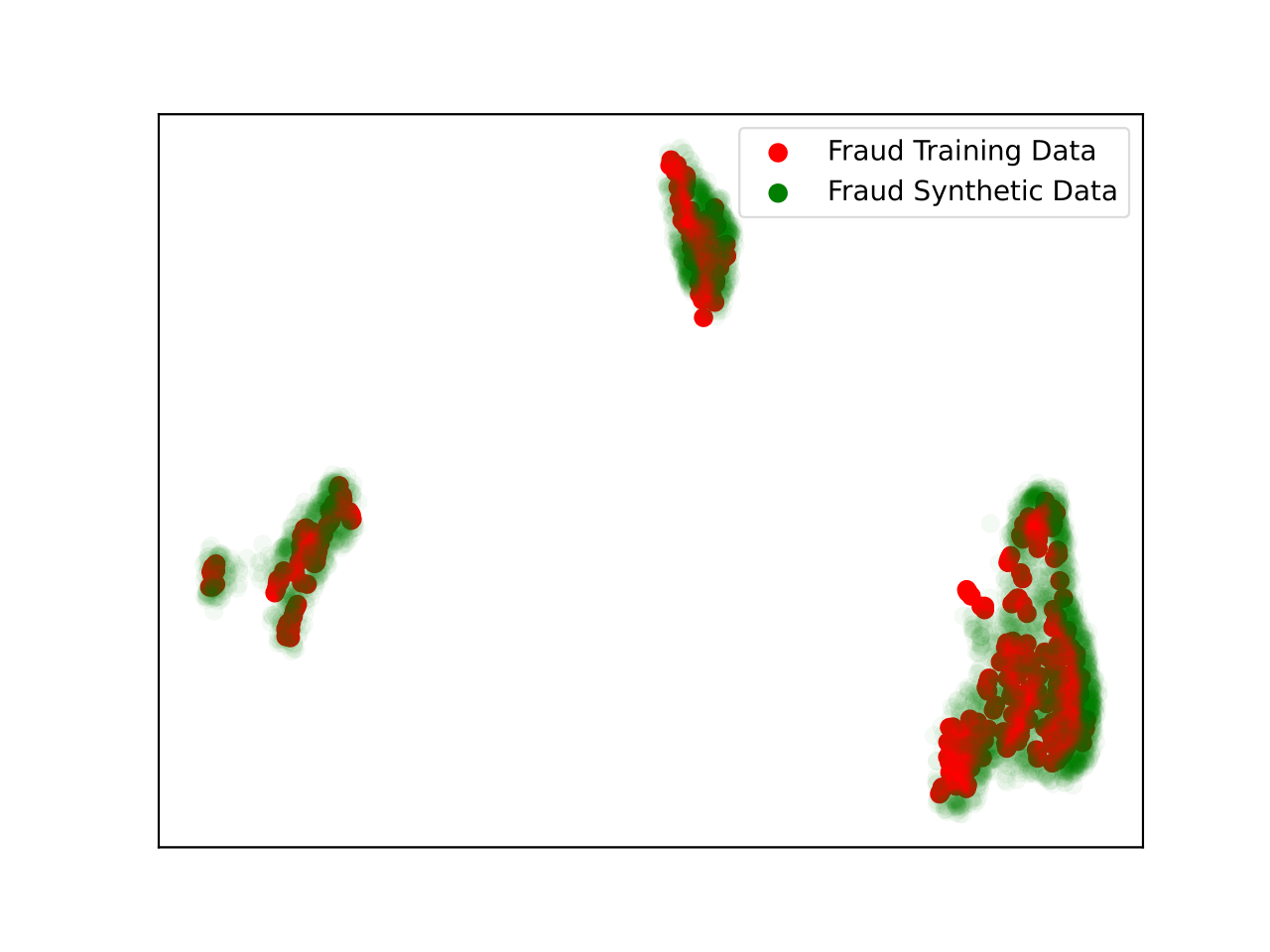

To append synthetic data, we first split the original data into train and test sets. Then, we train a diffusion model on the fraudulent transactions from the training data, generate data with this trained diffusion model, then append this synthetic data to the training data. Because the credit card data has 29 features, we cannot directly visualize the original and synthetic data. Instead, we use dimensionality reduction. In Fig. 5, we reduce the dimension of the original and synthetic fraudulent data using Uniform Manifold Approximation and Projection (UMAP [11]). In this reduced state, the synthetic data mostly agrees with the original fraud data, suggesting that the diffusion model was able to capture the structure underlying the fraud data even in 29 dimensions.

4.1 Classification on the Credit Card Dataset

After augmenting the training data with data generated by a diffusion model, we now perform classification. We use the XGBoost [2] and Random Forest [8] classifiers and train them on the unmodified training data and training data augmented with our diffusion models. Tables 2 and 6 show the precision, recall, and score (which is the harmonic mean of precision and recall) of XGBoost and Random Forest applied to the test set after being trained with these two methods. Notably, adding synthetic data improves the recall of both classifiers, meaning they are more successful in finding fraud when it occurs. However, with the Random Forest classifier, this comes at the tradeoff of precision, meaning the Random Forest model trained on augmented data is more likely to make ?false accusations? of fraud.

| Method | Precision | Recall | Score |

|---|---|---|---|

| No Augmentation | 0.8901 | 0.8265 | 0.8571 |

| Diffusion | 0.9222 | 0.8469 | 0.8830 |

| Method | Precision | Recall | Score |

|---|---|---|---|

| No Augmentation | 0.9524 | 0.8163 | 0.8791 |

| Diffusion | 0.8776 | 0.8776 | 0.8776 |

5 Closing Remarks

In this work, we formally developed diffusion models for generating new samples. To do so, we started by defining a forward process as modeled by a linear SDE. From this forward process, we deduced a discretized solution to the reverse process. The diffusion model is then trained by

?witnessing? the forward process (i.e., learning to estimate the noise ), and generates points by inferring the reverse process.

As an application to classification problems in imbalanced datasets, we found that data augmentation with diffusion improved recall on the credit card dataset for both classifiers. However, when using the Random Forest classifier, the precision noticeably suffers when augmenting data (that is, models trained on diffusion-augmented data can better detect fraud when it occurs, with the potential tradeoff of making more

?false accusations? of fraud). For classification problems in which failing to detect the minority class is more costly than incorrectly labeling data as belonging to the minority class, data augmentation with diffusion may be advantageous.

For future work on diffusion models, we can consider implementing the Negative Prompting algorithm [1], which currently only sees applications in image generation. The Negative Prompting algorithm allows one to generate data that mimics one class while avoiding another class. On the mathematical front, connections between the reverse SDE and PDE can be investigated utilizing a result known as Itô’s formula (discussed in [5]).

The GitHub repository containing our implementation of diffusion models can be found here: https://github.com/justinle4/Diffusion. In particular, we utilized the PyTorch [12] library in Python to design and train the neural network underlying our diffusion model.

Appendix A Solving the Ornstein-Uhlenbeck Equation

Solving (1) and SDEs more broadly requires the development of a new type of integration called ?Itô integration?. This is what allows us to make sense of the integral of , which, unlike the traditional notions of integration, integrates with respect to a stochastic process. A rigorous development of the Itô integral and the necessary properties of the integral to obtain equation (3) can be found in Evans’ text on SDE [5]. The key lemma from this text is that the integral of is not a number, but rather a random variable.

Lemma A.1.

Let and . Then, is normally distributed with

and

The proof of this lemma can also be found in [5] and is one of the key properties of the Itô integral. With this lemma, equation (2) can easily be obtained.

Proof A.2.

(Proposition 2.1) Our first step towards solving equation (1) is to make use of the method of integrating factors. Set and observe that

Integrating both sides over then yields

From here, we use lemma (A.1) to deduce

and

Now, we conclude

In other words,

so we can rewrite as follows:

with . This is equation (2).

To obtain equation (4), we simply repeat the steps above, but instead integrating over rather than .

Appendix B Time Discretization

We introduce an algorithm to choose the values of . With this algorithm, increases with respect to , meaning more time steps will be found closer to 0 (i.e., when the ?drift? portion of forward diffusion is most pronounced). Hence, a model trained with such a time discretization scheme will more thoroughly learn the drift, which is crucial when generating points with the reverse process.

Appendix C Deriving the Discretized Reverse Diffusion

We present a proof to proposition 2.3, which crucially leverages our discrete time steps by using Bayes’ theorem.

Proof C.1.

(Proposition 2.3) First, Bayes’ theorem gives us

Note that by equation (4), the all have the Markov property (in other words, the position of a trajectory at one time step depends only on its position at the previous time step). Hence, . Moreover, and are fixed, so the joint density is a constant. So, we have by corollary (2.2) and by proposition (2.1). Since we already know that is a density, we only need to consider the kernel of the right hand side, meaning all constants can be ignored. In particular, we will take all terms that are not dependent on and collect them into constants that we will denote as and :

Notice that

Using this fact, we find

We recognize this as the kernel of a distribution.

Acknowledgments

This article began as my honors thesis for my Bachelor’s degree at Arizona State University’s School of Mathematical and Statistical Sciences. I would like to thank my advisors, Dr. Sebastien Motsch and Dr. Johannes Brust, for their mentorship, expertise, and inspiration. Thank you as well to the School of Mathematical and Statistical Sciences and Barrett, the Honors College at Arizona State University for giving me the support to succeed as an undergrad. Finally, thank you to my high school calculus teacher Mr. Tutt, who ignited my passion for mathematics and started me on this incredible journey.

References

- [1] M. Armandpour, A. Sadeghian, H. Zheng, A. Sadeghian, and M. Zhou, Re-imagine the negative prompt algorithm: Transform 2d diffusion into 3d, alleviate janus problem and beyond, 2023, arXiv:2304.04968 [cs.CV].

- [2] T. Chen and C. Guestrin, Xgboost: A scalable tree boosting system, in Proceedings of the 22nd ACM SIGKDD International Conference on Knowledge Discovery and Data Mining, KDD ’16, New York, NY, USA, 2016, Association for Computing Machinery, p. 785–794, doi:10.1145/2939672.2939785, https://doi.org/10.1145/2939672.2939785.

- [3] A. Dal Pozzolo, G. Boracchi, O. Caelen, C. Alippi, and G. Bontempi, Credit card fraud detection: A realistic modeling and a novel learning strategy, IEEE Trans. Neural Netw. Learn. Syst., PP (2017), pp. 1–14, doi:10.1109/TNNLS.2017.2736643.

- [4] A. Dal Pozzolo, O. Caelen, Y.-A. Le Borgne, S. Waterschoot, and G. Bontempi, Learned lessons in credit card fraud detection from a practitioner perspective, Expert Syst. Appl., 41 (2014), p. 4915–4928, doi:10.1016/j.eswa.2014.02.026.

- [5] L. Evans, An Introduction to Stochastic Differential Equations, American Mathematical Society, 2013.

- [6] I. Goodfellow, J. Pouget-Abadie, M. Mirza, B. Xu, D. Warde-Farley, S. Ozair, A. Courville, and Y. Bengio, Generative adversarial networks, Commun. ACM, 63 (2020), p. 139–144, doi:10.1145/3422622, https://doi.org/10.1145/3422622.

- [7] J. Ho, A. Jain, and P. Abbeel, Denoising diffusion probabilistic models, in Advances in Neural Information Processing Systems, vol. 33, Curran Associates, Inc., 2020, pp. 6840–6851, https://proceedings.neurips.cc/paper_files/paper/2020/file/4c5bcfec8584af0d967f1ab10179ca4b-Paper.pdf.

- [8] T. K. Ho, Random decision forests, in Proceedings of 3rd International Conference on Document Analysis and Recognition, vol. 1, 1995, pp. 278–282 vol.1, doi:10.1109/ICDAR.1995.598994.

- [9] Y. Jiang, S. Chang, and Z. Wang, Transgan: Two pure transformers can make one strong gan, and that can scale up, in Advances in Neural Information Processing Systems, M. Ranzato, A. Beygelzimer, Y. Dauphin, P. Liang, and J. W. Vaughan, eds., vol. 34, Curran Associates, Inc., 2021, pp. 14745–14758, https://proceedings.neurips.cc/paper_files/paper/2021/file/7c220a2091c26a7f5e9f1cfb099511e3-Paper.pdf.

- [10] P. D. Kingma and M. Welling, Auto-encoding variational bayes, in Proceedings of 2nd International Conference on Learning Representations, 2014, arXiv:1312.6114 [stat.ML].

- [11] L. McInnes, J. Healy, N. Saul, and L. Großberger, Umap: Uniform manifold approximation and projection, J. Open Source Softw., 3 (2018), p. 861, doi:10.21105/joss.00861.

- [12] A. Paszke, S. Gross, F. Massa, A. Lerer, J. Bradbury, G. Chanan, T. Killeen, Z. Lin, N. Gimelshein, L. Antiga, A. Desmaison, A. Kopf, E. Yang, Z. DeVito, M. Raison, A. Tejani, S. Chilamkurthy, B. Steiner, L. Fang, J. Bai, and S. Chintala, Pytorch: An imperative style, high-performance deep learning library, in Advances in Neural Information Processing Systems, vol. 32, Curran Associates, Inc., 2019, https://proceedings.neurips.cc/paper_files/paper/2019/file/bdbca288fee7f92f2bfa9f7012727740-Paper.pdf.

- [13] F. Pedregosa, G. Varoquaux, A. Gramfort, V. Michel, B. Thirion, O. Grisel, M. Blondel, P. Prettenhofer, R. Weiss, V. Dubourg, J. Vanderplas, A. Passos, D. Cournapeau, M. Brucher, M. Perrot, and E. Duchesnay, Scikit-learn: Machine learning in Python, J. Mach. Learn. Res., 12 (2011), pp. 2825–2830, http://jmlr.org/papers/v12/pedregosa11a.html.

- [14] A. Radford, K. Narasimhan, T. Salimans, and I. Sutskever, Improving language understanding by generative pre-training, 2018, https://cdn.openai.com/research-covers/language-unsupervised/language_understanding_paper.pdf.

- [15] A. Ramesh, M. Pavlov, G. Goh, S. Gray, C. Voss, A. Radford, M. Chen, and I. Sutskever, Zero-shot text-to-image generation, in Proceedings of the 38th International Conference on Machine Learning, M. Meila and T. Zhang, eds., vol. 139 of Proceedings of Machine Learning Research, PMLR, 18–24 Jul 2021, pp. 8821–8831, https://proceedings.mlr.press/v139/ramesh21a.html.

- [16] J. Sohl-Dickstein, E. Weiss, N. Maheswaranathan, and S. Ganguli, Deep unsupervised learning using nonequilibrium thermodynamics, in International conference on machine learning, PMLR, 2015, pp. 2256–2265, https://proceedings.mlr.press/v37/sohl-dickstein15.html.

- [17] A. Thiéry, Denoising diffusion probabilistic models (ddpm), 2013, https://alexxthiery.github.io/notes/DDPM/DDPM.html.

- [18] A. Vaswani, N. Shazeer, N. Parmar, J. Uszkoreit, L. Jones, A. N. Gomez, L. u. Kaiser, and I. Polosukhin, Attention is all you need, in Advances in Neural Information Processing Systems, I. Guyon, U. V. Luxburg, S. Bengio, H. Wallach, R. Fergus, S. Vishwanathan, and R. Garnett, eds., vol. 30, Curran Associates, Inc., 2017, https://proceedings.neurips.cc/paper_files/paper/2017/file/3f5ee243547dee91fbd053c1c4a845aa-Paper.pdf.

- [19] K. Wang, C. Gou, Y. Duan, Y. Lin, X. Zheng, and F.-Y. Wang, Generative adversarial networks: introduction and outlook, IEEE/CAA J. Autom. Sin., 4 (2017), pp. 588–598, doi:10.1109/JAS.2017.7510583.

- [20] Y. Zhu, K. Zhang, J. Liang, J. Cao, B. Wen, R. Timofte, and L. Van Gool, Denoising diffusion models for plug-and-play image restoration, in Proceedings of the IEEE/CVF Conference on Computer Vision and Pattern Recognition (CVPR) Workshops, June 2023, pp. 1219–1229, arXiv:2305.08995 [cs.CV].