Thermal Macroeconomics:

An axiomatic theory of aggregate economic phenomena

Abstract

An axiomatic approach to macroeconomics based on the mathematical structure of thermodynamics is presented. We call the resulting theory Thermal Macroeconomics (TM). Subject to the axioms, this approach deduces relations between aggregate properties of an economy, concerning quantities and flows of goods and money, prices, and the value of money, without any recourse to ‘microeconomic’ foundations about the preferences and actions of individual economic agents.

The approach has three important payoffs. Firstly, it provides a new, and more solid, foundation for some aspects of standard macroeconomic theory, such as the existence of market prices, the value of money, the meaning of inflation, the symmetry and negative-definiteness of a macro-version of the Slutsky matrix, and the Le Chatelier-Samuelson principle, without relying on implausibly strong rationality assumptions over individual microeconomic agents. Secondly, the approach generates new results, including implications for money flow and trade when two or more economies are put in contact, in terms of new concepts such as economic entropy, economic temperature, goods’ “values”, and money capacity. We will see that some of these are related to standard economic concepts (e.g. marginal utility of money, market prices). Yet our approach derives them at a purely macroeconomic level and gives them a meaning independent of usual restrictions, e.g. to rational agents. Others of the concepts, such as economic entropy and temperature, have no direct counterparts in standard economics, though they have important economic interpretations and implications, as “aggregate utility” and the inverse marginal aggregate utility of money, respectively. Thirdly, this analysis promises to open up new frontiers in macroeconomics by building a bridge to ideas from non-equilibrium thermodynamics. In contrast to the strict economic notion of equilibrium, the present approach starts from a statistical physics notion of equilibrium and thereby has the potential to extend to the more realistic non-equilibrium settings, as in physics. More broadly, we hope that the economic analogue of entropy (governing the possible transitions between states of economic systems) may prove to be as fruitful for the social sciences as entropy has been in the natural sciences.

We restrict attention to “extensive” economic systems: those which can be subdivided into parts with the same properties apart from size (for example, we ignore possible “lumpiness” that might be caused by large individual companies). Following a long tradition in economics, we here also restrict attention to exchange economies, in which the total quantities of goods and money remain fixed, but can be redistributed between agents, for example through trade. We leave production, consumption, labour, finance etc. for future treatment. Building on an axiomatic approach to thermodynamics by Lieb and Yngvason, we explain how extensivity plus plausible economic assumptions lead to the definition of an economic analogue of entropy, which we consider to be an aggregate utility, and an economic temperature, whose inverse is the marginal (aggregate) utility of money. We obtain a “second law” of economics, governing the allowed direction of changes of economic state of a multi-part economy. This approach captures the ‘value’ of nominal money in a way that does not rely on the usual rather arbitrarily chosen “baskets of goods” and their prices. It explains the direction of financial flow in terms of temperature differences. We illustrate the theory with an economic analogue of the Carnot cycle whereby a trader makes money out of temperature differences.

We obtain quantitative conditions for trade: on making contact, nett trade flows occur if and only if they increase the total entropy. We highlight the subset of “mutually beneficial” trades, which increase the entropy of each economy. We derive some macroeconomic relations between cross-derivatives, in particular economic “flexibilities” (the inverse of the elasticities of standard economics). We also introduce the concept of “pure money”. We discuss limitations and possible extensions of our approach, in particular to relaxing the extensivity assumption and incorporating important aspects of real economies, including production, consumption and manufacturing.

1 Introduction

Economies appear to exhibit many large-scale regularities, concerning the balance between supply and demand to clear markets, patterns of interdependence between prices and volumes of different types of goods, the value of money, the movement of exchange rates, and many more. Yet economies also have many irregular properties—including crashes and booms, gluts and shortages, herding, fashion, and unpredictability due not just to technological or organizational innovation, but apparently due to endogenous, and little understood, fluctuations at many scales.

During the twentieth century, economists have primarily tried to explain the mix of regularity and irregularity in aggregate properties of the economy through attempts to establish micro-foundations, i.e., explaining aggregate properties as arising from the interaction of economic agents with specified properties. Roughly speaking, the interactions of fully rational and informed consumers and producers, each aiming to maximize their own utility, are presumed to generate regularities, most notably through the concept of general equilibrium. In parallel, there have been attempts to explain irregular aspects of economic behaviour by exploring how partial information and bounded rationality, can lead, for example, to booms and crashes. Thus, the pattern of explanation has been bottom-up: from the properties of economic agents and their interactions to the large-scale economic phenomena.

There is, however, an interesting complementary approach, which does not attempt to provide such micro-foundations, but instead makes assumptions about economic behaviour in the aggregate, and explores their consequences at the same aggregate level. This approach has the potential advantage that it may be possible to abstract away from detailed “micro” assumptions (e.g., about the psychological properties of consumers, or the behaviour of companies), which are likely to be very difficult to specify and highly variable between contexts. Interestingly, this strategy predates the modern emphasis on the micro-foundations of economics, and is implicit in arbitrage arguments from David Hume and Adam Smith onwards (see discussion in [Su]), and which are the basis for much of financial economics [V1].

In this paper, we explore this non-micro-foundational approach by applying conceptual and mathematical methods borrowed from “classical” thermodynamics, developed in the nineteenth century by Carnot, Joule, Clausius, Maxwell and Gibbs (“classical” means without involving statistical mechanics [LY99]). Classical thermodynamics begins with high-level principles, such as the conservation of energy (the first law of thermodynamics) and the non-decrease of entropy (the second law), and derives systems of relationships between large-scale observable phenomena including work, pressure, volume, temperature, and so on. It requires the existence of a priori abstract quantities, such as energy and entropy, which provide a concise and elegant framework for expressing these laws. These fundamental laws turn out to be extremely general and to apply to systems with very diverse components, from the earth’s climate system to the functioning of biological cells and chemical engineering. Thus, while in specific contexts there are elegant connections to microfoundations (e.g., to statistical properties of interacting gas particles), the principles of classical thermodynamics are more general and more abstract (e.g., [LY02, Go]) and apply to diverse physical systems, chemical reactions, and biological processes.

Can a similar approach work for economics? Specifically, is there a thermodynamics of economic systems that can derive macro-economic regularities without making detailed assumptions about consumers and companies? We formulate such a theory here, by reinterpreting thermodynamic quantities in economic terms. In particular, we map energy to money and deduce economic analogues of entropy and temperature, which in contrast to money are not standard economic quantities. Our economic entropy can be viewed as an aggregate utility, but importantly it is a cardinal rather than ordinal utility and applies to an economy as a whole rather than to individual agents; our economic temperature can be viewed as a macro-version of the inverse marginal utility of money. This provides an interesting new perspective on some well-known economic regularities, captured by equilibrium arguments in conventional mathematical economics. Most importantly, we establish an analogue of the second law of thermodynamics, for economic systems, which specifies possible transitions between states of an economy, ruling out those with non-decreasing entropy. Moreover, this approach provides a principled meaning for the value of nominal currency (e.g., dollars, euros), which does not depend on the prices of somewhat arbitrarily chosen “baskets of goods.” It also opens up the possibility of using generalizations of thermodynamics, developed in the natural sciences, to understand more complex economic phenomena (including the analysis of economic systems which are out of equilibrium) without recourse to microfoundational assumptions about lack of information or bounded rationality at the level of individual economic agents. If such a high-level thermodynamic approach to the economy proves fruitful, it has the potential to complement and inform traditional microeconomic analysis, just as in physics and chemistry, classical thermodynamics has complemented and informed statistical mechanics.

We begin in Section 2 by reviewing precursors of using thermodynamics in economics. We restrict attention in this paper to exchange economies, reviewed briefly in Section 3. In Sections 4-8 we state our main assumptions and their justifications. In Section 9 we deduce the existence of an entropy function for economies and the all-important second law of non-decrease of entropy. We compute the entropy for a simple example in Section 10 and Appendix A. After stating a few technical assumptions in Section 11, we deduce existence of a temperature function for economies and its relation to financial equilibrium in Section 12. A subsidiary concept of money capacity is introduced in Section 13 and its significance described. In Section 14 we deduce the existence of a market price for each good, via a concept of “value” of a good, and a key relation for reversible trade. In Section 15 we introduce the concept of “pure money” and discuss some of its consequences. Section 16 proposes a way to measure the temperature of an economy. Section 17 discusses the natural way to make money from price differences between two economies. Section 18 describes the less intuitive way to make money out of the temperature ratio between two economies. Section 19 gives quantitative conditions for trade and highlights the significance of mutually beneficial trades, which increase the entropy of all parties. Section 20 derives relations between various partial derivatives, based on the existence and concavity of entropy. Section 21 raises some further issues for exchange economies. Section 22 discusses potential directions for development of the theory beyond exchange economies. The paper concludes with a summary and conclusions in Section 23.

2 Precursors

Many previous researchers have considered possible links between classical thermodynamics and economics. Indeed, the architect of modern mathematical economics, Paul Samuelson, stressed the importance of Gibbs’ work as foundational to his own. But Samuelson (and precursors such as Slutsky) applied principles of maximization at the level of individual agents, rather than aggregate system properties. Samuelson despaired of numerous ill-thought-out proposals to attempt to find an economic analogue of entropy and doubted that such an analogue existed.

The present approach aims to vindicate those who have intuitively felt the existence of a deep connection between thermodynamics and economics, and to set Samuelson’s concerns aside. We begin by reviewing some of the most notable precursors of the approach developed here.

The idea that thermodynamics is relevant to economics goes back more than a century. Irving Fisher’s 1891 PhD (considered by many to be the first in Economics) was co-supervised (along with the sociologist Sumner) by Gibbs, an early champion of thermodynamics. Utility theory, as developed by Fisher, Slutsky, Hotelling, Houthakker, Samuelson and others, shares many features with thermodynamics. For example, the theory contains economic analogues of some of the Maxwell relations between partial derivatives (known in economics as the Hotelling conditions [S50]).

Connections between economics and thermodynamics are particularly prominent in Samuelson’s work (e.g. see the review of Samuelson’s legacy by Dixit [Di]). Specifically, Samuelson notes that [S72] “Pressure and volume, and for that matter absolute temperature and entropy, have to each other the same conjugate or dualistic relation that the wage rate has to labor or the land rent has to acres of land” and “My earlier formulation of the inequality [] owed much to Wilson’s lectures on thermodynamics.”222We will derive an analogue of this inequality in Section 20. Yet Samuelson was also scathing about attempts to make connections between the subjects [S72]: “There is really nothing more pathetic than to have an economist or a retired engineer try to force analogies between the concepts of physics and the concepts of economics”. In the light of Samuelson’s own inspiration from thermodynamics, this statement is rather puzzling, but it has certainly deterred researchers from the economic and natural sciences from pursuing such potential analogies further.333[SF] pick out a particularly clear instruction from Samuelson [S60] to economists and physicists to desist from seeking what he saw as spurious parallels: “The formal mathematical analogy between classical thermodynamics and mathematic economic systems has now been explored. This does not warrant the commonly met attempt to find more exact analogies of physical magnitudes – such as entropy or energy – in the economic realm. Why should there be laws like the first or second laws of thermodynamics holding in the economic realm? Why should ‘utility’ be literally identified with entropy, energy, or anything else? Why should a failure to make such a successful identification lead anyone to overlook or deny the mathematical isomorphism that does exist between minimum systems that arise in different disciplines?” The present paper shows that there is indeed a powerful economic notion of entropy and a corresponding second law of thermal macroeconomics, which go beyond the link between thermodynamics and maximization that was so productive in Samuelson’s work. In particular, while Samuelson found important links between thermodynamics and maximization problems in economics (typically defined for an individual agent, but including an individual company), the present link is more fundamental. Rather than beginning with a presumed economic analogue of entropy, we show that there exists a cardinal quantity such that economies, or systems or economies, can only change in ways that do not decrease that quantity. We call this quantity economic entropy.

An influential book published by Georgescu-Roegen in 1971 [GR] did appear to make a link between entropy and economics. But our reading of Georgescu-Roegen’s claim that entropy governs economics, has, we believe, a rather different aim than the project Samuelson was critiquing (and that we are pursuing here). Georgescu-Roegen’s aim was to explore how physical entropy might place constraints on economic activity, rather than attempting to create an analogue of entropy within economics itself. This direction has been pursued under various names including ecological economics, systems ecology (for one take, see [Ku]), and thermoeconomics (on which more shortly).

Subsequently, physicists like Jaynes [J] and Farjoun & Machover [FM], began again to address economics, but from the viewpoint of statistical mechanics, rather than classical thermodynamics. This developed into a vigorous field of research that was christened “Econophysics” by Gene Stanley in 1996. Particularly relevant articles from this school in our opinion are [Sas] and [RFP]; also the book [C+] on econophysics related to the Marxist view of economics, which centres on labour as measure of value. Some perspectives on relations between economics and thermodynamics have been given in [RMH] and [MM]. Econophysics has applied a wide variety of ideas and methods developed for analysing complex physical systems to economic phenomena and especially to financial markets. Yet econophysics has not generally found favour with economists.

Others have attempted to establish links between classical thermodynamics and economics, but like Samuelson, they typically focus on mapping thermodynamics onto the utility function of individual agents, rather than considering economies from a purely macro-perspective as here. For example, [SDa, SDb] aim to build links founded on the observation that both maximizing entropy and maximizing utility are problems of constrained optimization, and draw out a number of detailed formal parallels.444They also highlight early discussion hinting at analogies between the equations used in economics and thermodynamics including [CMIM, Da, Lis]. A particularly sophisticated bridge between the two fields is outlined by [SF], and our approach has various links with theirs that we will highlight at relevant points. A more recent development by Cooper and Russell [CR01, CR11] uses ideas from Samuelson to help formulate physical thermodynamics, drawing on ideas from symplectic geometry: thus, their primary focus has the opposite explanatory direction from the account developed here, and has a narrower scope. The present purely macroscopic approach, aiming to map the full axiomatic structure of thermodynamics into a macro-analysis of economics, seems to be new—although exploring potentially fruitful links with prior work is an interesting topic for future research.

The term we use for our approach, “Thermal Macroeconomics” (that we abbreviate to TM), aims to express our objective of providing an analysis of economic theory paralleling the mathematical structure of thermodynamics. We distinguish TM from the variety of loosely connected usages of the term “thermoeconomics”, which typically point to attempts that, like [GR], aim to combine economic and thermodynamic principles in contexts as diverse as understanding plant growth, the emergence of order in biological evolution, designing commercial energy systems, or clarifying the limits to economic growth.555For example, in applying economic ideas to understanding living systems [CK], [Co] states “The term ‘thermoeconomics’ denotes a paradigm shift in our understanding of the role of energy in living systems, and in evolution. It is based on the proposition that energy in biological evolution can best be defined and understood, not in terms of the Second Law of Thermodynamics but in terms of such economic criteria as productivity, efficiency, and especially the costs and benefits (or ‘profitability’) of various mechanisms for capturing and utilizing energy to build biomass and do work.” Others, apparently beginning with Myron Tribus in 1962 [MS], have used “thermoeconomics” for the exploration of how fundamental thermodynamic constraints in the physical world shape and constrain economic activity, whether at the level of the individual industrial processes [TE] or the entire economy in the tradition of [GR]. According to [DG], for example, “Thermoeconomics combines thermodynamic principles with economic analysis and brings some fundamental changes in the economic evaluation, design, and maintenance of processes.” In sum, no specific usage of the term has yet become well established. We use the new term “thermal macroeconomics” to distinguish the present approach from this work. In our usage, “thermal economics” applies the mathematical structure of classical thermodynamics, not its physical content, to model economic phenomena. Thus, it has no specific connection to economics questions concerning heat, energy or any other physical quantities.

The objective of TM is both narrower in scope and has a very different focus than thermoeconomics: aiming to map the mathematical structure of thermodynamics into economics, in order to provide a purely ‘macro-level’ analysis of economic phenomena. Thus, we aim to construct an economic theory using the mathematical and conceptual machinery of thermodynamics. Despite various past attempts, and the intuition among many researchers (but not, as we’ve seen, Samuelson) that such a link might exist, a purely thermodynamic approach to economics seems not yet to have reached fruition.666Our own efforts in building a link between thermodynamics and economics has had a long gestation. We started discussions on formulating a link in 2010, including supervising MSc student Daniel Sprague’s simulations of simple economic systems in 2011. We arrived at our present position only after many iterations and false starts.

A key ingredient for our thinking was provided by the axiomatic formulation of thermodynamics by Lieb and Yngvason in a series of papers surveyed in [LY02], which clarifies the underlying mathematical structure of thermodynamics, independent of its physical interpretation. Their approach formulates axioms governing abstract relations and between macro-states, which we shall introduce in Sections 5 and 6 respectively. Thus, any analogies between the domains of physics and economics can emerge naturally from the mathematics; equally, where there are disanalogies, these will emerge automatically too. The present work takes literally their invitation in [LY98]: “Maybe an ingenious reader will find an application of this same logical structure to another field of science.” Indeed, possible links to economics, and in particular to utility theory, are mentioned in [Y].

Reading [LY02] is not a prerequisite for our paper, however. We require only their axioms, Theorem 1 on the existence of entropy, and their subsequent results on its concavity and differentiability (all of which we review here). While our exposition is self-contained, we adopt their numbering system for the axioms (though inserting our own slight variants), and largely follow their notation.777We make slight adjustments to their notation for ‘adiabatic accessibility’ and ‘adiabatic equivalence’—and we also drop the term ‘adiabatic’ entirely, as it is unfamiliar in economics and is ambiguous even in physics where it can mean without heat flow or alternatively, slow variation, which are not equivalent. There are many nuances in their treatment that we skip over; we leave a more extensive analysis for future work.

The approach developed here is purely at the macro-economic level. Many of the topics treated below, such as the formation of market prices, are typically studied in microeconomics starting from fundamental assumptions about the rationality of individual economic agents. We treat these questions from an aggregate point of view, by making assumptions about markets as a whole, rather than their participants. This may create a more natural bridge from micro-economics to macroeconomic questions concerning, for example, the value of money and flows of trade. We see the ability to generate strong theoretical results without specific micro-foundations as a major advantage of this approach, regarding both generality and tractability. Nonetheless, the functional form of the resulting entropy function depends on the micro-foundations, and it is of course interesting to consider how a macro-analysis can connect with micro-foundations. We show how this can be done in the special case of an exchange economy consisting of agents with a Cobb-Douglas utility function.

The economics community is divided on the value of axiomatic approaches. On the one hand, the axiomatic approach of Arrow and Debreu [AD] and McKenzie [McK] to general equilibrium is regarded by many theoretical economists as a pinnacle of intellectual achievement. On the other hand, practical economists tend to be sceptical of axiomatic arguments and of mathematical theories in general, as encapsulated by Krugman’s comment on the 2008 financial crisis [Kr]: “The economics profession went astray because economists, as a group, mistook beauty, clad in impressive-looking mathematics, for truth.” We take a pragmatic view, justifying the axioms from economic reality as far as we can but identifying their limitations and proposing directions for extension. In the present context, that of building a link between thermodynamics and economics, an axiomatic approach is particularly valuable because it provides a rigorous way of clarifying a common underlying mathematical structure, rather than relying on intuitive analogies between ideas in each domain.

Finally, the economics community is, as we have already indicated, divided on the value of “imitating” physics [Mir, Yee]. We aim to set aside such general concerns, and focus on showing how a thermodynamic perspective on economic systems can yield valuable insights for economic analysis. We hope that, especially if the present approach can be extended beyond the exchange economies treated here, concepts of economic temperature, economic entropy, money capacity and so on, may become part of standard economic practice. Indeed, we suspect that the problematic relationship between economics and physics arises not because economists have been excessively entranced by attempting to imitate physics, but because the connections between the disciplines have not been pushed far enough.

3 Exchange economies

In this paper we restrict attention to exchange economies. In an exchange economy, agents exchange various sorts of durable good with each other; no goods are produced or consumed. This is of course a very limited view of economics, ignoring production, consumption, manufacturing, recycling, labour, interest rates, etc, but we intend to extend the approach in later work. In any case, it is fairly standard in economic and finance theory to reduce much to exchange, for example, exchanging options to consume a good, provide labour, money, or supply a service, on some future date or conditional on a specific state of the world [Ga, V2].

We suppose that the set of types of good is finite, that goods of the same type are indistinguishable, and that goods can be divided in any ratio. These are idealisations that we hope to relax in future work.

We suppose there is a particular durable good that we will use as a reference (a “numéraire” in economics) and will call money. We assume that at the aggregate level, more money is always “preferred” to less, no matter how much money and other goods are present already. A more precise meaning will become clear in our treatment below—but roughly this means that if a trader (a figure we will introduce in Section 5) were to offer freely to give or take money to or from members of an economy, they would in aggregate accept more money than they would give (we do not require the stronger assumption that this holds for every individual).888The corresponding aggregate property need not hold for other types of goods: there may be regimes where it is preferable not to have more, or even preferable to have less (e.g., if the good acts as a pollutant or is simply “surplus to requirements”). Money should also be easy to store and exchange, though in our exchange economies all goods are durable and exchangeable; in particular, we want it to be easily transferable to another economy. To avoid giving a national preference, we measure its amount in “aurum”, denoted by or . The unit is named after gold, in the light of gold’s historical role as a numéraire for a large part of the world. Money may or may not have intrinsic value (contrast gold with paper); we explore the consequences of “pure money” in Section 15. We leave extending the approach to settings in which there is more than one currency (touched on briefly in Section 21.1) for future work.

Some comment is required here on the meaning of conservation of money. In the real world, money can be printed, destroyed, created against debt, e.g. through the sale of bonds as in “quantitative easing” after the 2007/8 financial crisis. We regard that as consistent with conservation of money because money enters the system only in identified ways. This is analogous to the conservation of energy in physics: conservation of energy does not exclude arrival of sunlight into the earth system, the dissipation of the earth’s heat into space or the generation of energy by nuclear fission.

As noted in the previous section, we take a deliberately macroscopic view. Hence we do not have to specify the process by which individual people choose which bundles of goods to exchange nor how frequently they do so. Nonetheless, we will study one microeconomic example (Section 10) to illustrate how the thermodynamic quantities of our macroeconomic theory emerge from a microeconomic model. The literature contains many other examples of microeconomic model of exchange, for which some references can be found in a recent paper [DGMS]. Other recent references on exchange models include the special issue edited by [TSB] and the review [GG].

The most direct way to test the theory is by computer simulations of micro-interactions between simple economic agents. This allows direct comparison between the “macro” predictions of TM with the measured behavior of a simulated exchange economy with clear micro-foundations. In [LMC], we describe a wide range of simulations which are in good quantitative agreement with the predictions of TM.

4 Equilibrium

Our formulation depends on an assumption we call A0, that any closed exchange economy with given amounts of goods and money in a class of systems settles down to a unique statistical equilibrium state.999In their analysis of thermodynamic entropy, Lieb and Yngvason didn’t label the corresponding property as an axiom. Nonetheless, we feel it merits a label (A0). By a statistical equilibrium state we mean a stationary probability distribution over micro-states.101010It is important to distinguish the notion of micro-state from the macroscopic notion of “state” as a statistical state determined by aggregate quantities of goods and money, prices and so on, which is our main concern in TM.

It is possible to specify micro-level dynamics where A0 fails, in particular by including strong herding effects, e.g. [GBB]. To apply our theory to such systems would require some additional labels for the state, to indicate which equilibrium it has chosen. We avoid such considerations here.

Axiom A0 makes an exchange economy a “simple system” in the language of [LY02]: the state is specified by a point in a subset of , for some dimension , the coordinates being the amounts of each type of good and of money. One could also consider the number of agents as a coordinate for the state, but for present purposes we will take the number of agents in a system as fixed.

An implicit assumption is that a simple system is “financially indecomposable”: however the specified amount of money is initially distributed, it ends up distributed with the same probability distribution. So there is only one money coordinate. But we do not require the indecomposability assumption for types of good other than money. For example, we allow the possibility there might be no flow of a good from one part an economy to another, so that the amounts of that type of good in each part of the economy are independent coordinates for the state.

We emphasise that statistical equilibrium is not an equilibrium in the sense of Nash, where no player can benefit from a unilateral change [N50]. Nor is it an equilibrium in the sense of Arrow and Debreu, where prices are such that supply balances demand and then all exchanges stop [A51, D51]. Instead, it is a dynamic state of continuing exchanges but with a steady probability distribution for the micro-state. For example, it is entirely possible that people’s preferences continually vary (e.g., they become bored with objects they currently have and would rather exchange them for different ones). Perhaps the closest analogue in economics is dynamic stochastic general equilibrium (DSGE) [Ga], the workhorse of treasury modelling, but there the dynamics arises only as a response to external shocks. The idea of equilibrium in a strict sense has been criticised from early days in economics. For example, Irving Fisher wrote in 1933 [Fi] that “It is as absurd to assume that, for any long period of time, the variables in the economic organization, or any part of them, will ‘stay put,’ in perfect equilibrium, as to assume that the Atlantic Ocean can ever be without a wave.” A statistical equilibrium with steady (or slowly varying) macro-parameters is more plausible.111111A possible criticism of our equilibrium assumption, especially from finance practioners, is that it cannot account for endogenous business cycles. We note that there is considerable debate in the academic literature concerning the nature and even existence of such cycles [Sl37, FG94, Man89]. But we also note that the TM framework can potentially generate such cycles through the system being held out of equilibrium by fluxes of inputs and outputs, just as a physical system may exhibit oscillations when held out of thermodynamic equilibrium (e.g., in Rayleigh-Bénard convection or the Belousov-Zhabotinskii reaction [NN]). This is an important direction for future work. Here, however, we allow only temporary fluxes of inputs and outputs (e.g. with an external trader).

The notion of statistical equilibrium is itself, of course, a simplification of real economic activity, in which there are, among other things, continual technological and business innovations. These considerations do not arise in our idealized exchange economies. Nonetheless, we believe that the present approach could usefully be extended to deal with such cases, expanding on the intuition that the only innovations that catch on are those that increase economic entropy. For now, we note that entropy is useful in physics even in a time-varying environment and helps explain the formation of complex structure in physics, chemistry and biology. In particular, it is worth making a comparison with biochemistry. Concepts from equilibrium thermodynamics like changes in Gibbs free energy are very useful in understanding which processes occur in a cell, even if it is a highly structured environment and subject to time-varying conditions. The assumption behind this analysis is local thermodynamic equilibrium.

A different concern with the equilibrium assumption is that an economic system might have multiple equilibria [Fa]. This might well be the case when there are fluxes of inputs and outputs; but without inputs and outputs, it seems to us a plausible working assumption that an economic system with specified amounts of goods and money and no obvious barriers goes to a unique statistical equilibrium. This type of indecomposability assumption is widely made in analysing physical systems, in particular in statistical mechanics. It is analogous to the property of ergodicity in stochastic dynamics, meaning that there is a unique stationary distribution and it attracts all initial distributions [Li]. Similarly, it is analogous to the property of mixing for measure-preserving dynamics , meaning that for all measurable subsets and , the probability of converges to the product of the probabilities of and as [Wa].

To gain an intuition for the significance of the assumption that our exchange economy has a unique statistical equilibrium, it is useful to consider how this assumption can be violated. Suppose that the economic system under study is decomposable into two or more non-interacting parts (e.g., corresponding to islands which are entirely cut off from each other). Then there will be a continuum of ways in which goods and money can be divided between the parts (and this division will be conserved as the system evolves, because there is by assumption no trade between the parts). Thus each of the continuum of possible divisions will correspond to a distinct region of the state space with its own statistical equilibrium. We assume, unless specified as here, that this does not occur.121212As already indicated, there is a parallel in classical statistical mechanics: for example, one assumes that there is no extra conserved quantity, beyond those already identified as labels for the state, that would prevent wide exploration of the space corresponding to the state. More generally, one assumes that there is no invariant surface separating the space into two parts, or even more generally, one assumes ergodicity of the conditional of Liouville measure on the specified values of conserved quantities. For a simple introductory reference, see [Set].

Finally, note that an economic system with more than one money coordinate, corresponding to conserved amounts of money in financially disconnected parts of the systems, will be called “compound,” in contrast to “simple” systems with a single money coordinate.

5 Accessibility

The next key notion is the accessibility of one state of an economy from another when subject to external influence (for example, through interaction with other economies, or wealthy traders). Indeed, the main aim of the present approach is to understand which transitions between macro-level states are, or are not, possible.

To build an intuition for why the question of accessibility is crucial, consider the following. One might suspect that a sufficiently rich trader could rearrange goods between agents in the economy in any way desired, by paying people to buy and sell to each other to order; but to do this, the people in the economy would thereby have to be given additional money by the trader to incentivize them to engage in the desired transactions. But money is itself part of the state of the economy. So the trader does not have complete control after all—some state-transitions are possible and others are not. Indeed, suppose the trader wanted rapidly (rather than arbitrarily slowly) to reverse the allocations of goods to its original state. Doing so would require further financial inducements; so that while goods (apart from money) could be returned to the initial state, the economy would now contain more money than before. The reader may have the intuition that the trader forcibly “moving” goods about the economy seems analogous to doing work on a physical system (e.g., compressing a gas by a piston). Just as moving a physical system from one state to another and back again will “heat” the system being operated upon (except when the movement is arbitrarily slow), so forcibly moving an economic system from one state to another will increase the economic temperature of the system (by increasing the amount of money in the economy, and thus reducing the value of money). We will make these intuitions rigorous below.

We consider a system of one or more exchange economies connected to an external trader who has unlimited goods and money, and ask what effects on the system the trader can achieve.

Let us say that a state of an economic system is accessible from state , written , if the trader can move the system from state to state with no nett change in the trader’s assets apart from money. Note that our notation is slightly different from that of [LY02], who use instead.

For a simple exchange economy, specified just by total amounts of each type of good and money, because of the requirement that the trader end up with the same quantity of goods and our assumption that money is always desirable, we assume that the only accessible states are those with the same quantity of goods and at least as much money. But for a compound system, as the above discussion indicates, the set of accessible states is less obvious. A key contribution of the analysis below is to clarify this case, as we see shortly.

To continue introducing the framework, note that directly from the definition, we can see that is a pre-order (it is reflexive: , because the trader does not have to do anything to achieve no change; and it is transitive: implies , because the trader just has to make one change followed by the other). Transitivity of is A2 of [LY02] but we get it for free here.

We say state is reversibly accessible from , and write , if . It is an equivalence relation, because it is symmetric: iff , reflexive (which is A1 of [LY02] but again we get it for free) and transitive.

For later use, we will write if & .

Denote the state of a (compound) system consisting of two unconnected economies (or systems of economies) and in states respectively, by . In particular, if and then , because the trader can make the changes to and in parallel. This is A3 of [LY02] but we obtain it for free again.

6 Financial equilibrium

A further key notion is financial equilibrium. This will be crucial to making sense of the notion of the “temperature” of an economy, which will represent the reciprocal of the marginal utility of money at the macro-level.

Given two simple economies and , we define their financial join to be the joint economy where money is allowed to flow freely between them but no other goods can (we say they are in financial contact). There are various reasons why this might occur and the present approach is neutral between them. For example, people working in one economy might wish to send money to relatives in the other. Even more simply, one person could own assets in both economies; when financial contact is allowed, they can choose to send money from their holdings in one economy to their holdings in the other. It will make sense to send money to the economy in which its value is higher, i.e., to the one with the lower temperature (to be formalised in Section 12).131313A challenge for future work is to analyse some of the forces that drive real-world flows, such as interest rates and investment opportunities. We also leave treating surrogates for money, such as cheques or I-owe-yous (IOUs), and how to deal with credit, for later work.

Denote by the state of the financial join of that is reached from initial states after and have come to equilibrium. The equilibrium is specified by the total amount of money and the individual amounts of the other goods in each economy. Because and are assumed to be indecomposable, it is reasonable to assume that the equilibrium state of the financial join is to a high approximation independent of the way the join is made.141414As far as we can see, Lieb and Yngvason did not address the corresponding question about thermal joins. The idea is that if say were decomposable into then the effects of joining to or or both would certainly be different, depending on the distribution of goods and money between and , whereas if and are indecomposable then any way of letting money flow between them should produce approximately the same statistical state.

The process of coming to equilibrium will in general lead to a nett transfer of some money from one economy to the other, but in equilibrium there is no nett flow of money between them (though there will be on-going, but zero-mean, exchanges of money between the economies). Note that we are hereby applying A0 to the financial join and thus assuming that allowing money to flow between the two economies is enough to achieve ergodicity of the joint system. We deduce that , because the trader does not have to do anything. This is A11 of [LY02] but we get it for free.

We also deduce that there exist states such that . To see why, let be the states of and after financial contact. Then the only difference between the left- and right-hand sides is that the left-side has financial contact between and ; but the trader can act as a financial contact between and on the right-hand side by simply detecting if someone in wants to give money to someone in and making the transfer for them. So in the presence of the trader, the two sides are the same. Thus they are reversibly accessible from each other. This is A12 of [LY02] and we get it again for free.

If there is no nett flow of money between and on bringing them into financial contact, we say their states are in financial equilibrium and write . Thus, after nett money flow has occurred, . From the definition, is symmetric.151515[LY02] deduce symmetry of in their Lemma 2(ii), from their axioms A4, A5, A7, A11 and A12 but we have not yet introduced A4, A5, A7, and prefer to reduce our dependence on them.

We assume also (A13′) that is reflexive: i.e., that each state of an economy is in financial equilibrium with itself, or put differently, there are no internal barriers to money flow. Formally, this requires us to be able to make a copy of the system, to make the financial join of a system to itself, but let us suppose that this is possible. Then there is no money flow between these copies because of the assumed indecomposability of (each copy of) the system. Thus is reflexive.161616A13′ is not one of the axioms of [LY02]; instead they deduce it in their Lemma 2(i) from A4, A5, A7, A11 and A12. We prefer to list it as an axiom, to avoid relying on A4 and A5, and also reflexivity doesn’t seem to us as clear a logical consequence as they claim: it might depend on the way in which the join is made. So we treat reflexivity as an axiom, A13′.

Finally, we assume that is transitive. This is A13 of [LY02].171717One consequence to note is that this implies that for the equilibrium of a network of economies in financial contact, there are no nett cyclic flows of money. This is because the equilibrium for a spanning tree has no cycles so no nett money flows, and by transitivity when one adds the remaining links the economies are already in equilibrium, so there is no change to the nett flows. This assumption might not hold exactly for real economies but we hope it is a good enough approximation. One possible line of argument is that any cyclic flows of money would seem to provide arbitrage opportunities, and that such flows would therefore be reduced as those opportunities are exploited. Thus, is symmetric, reflexive and transitive, and hence is an equivalence relation.

To give some intuition for the significance of , we will see that economies which are in financial equilibrium, i.e., such that there is no nett tendency for money to flow from one to the other, are at the same “temperature,” although the notion of temperature is only derived later in the exposition. We will see that this corresponds intuitively to money having the same “value” in each economy, so that there is no tendency to generate a nett flow of money from one economy to another.

7 Accessibility and financial equilibrium

A key component of Lieb and Yngvason’s approach to thermodynamics is to formulate connections between the two binary relations and . In particular, we want A14: for each state of a simple system there are states with such that . Intuitively the reason that this assumption is important is that it ensures that the equivalence classes of reversible accessibility and financial equilibrium “cut across” each other and avoid “degeneracy”.181818A thermometer is such a degenerate case–a system which varies along a single dimension, so that for all , at different temperatures . For discussion of how to deal with this case, see [LY99]. We will introduce financial thermometers in Section 16. This assumption is crucial below in deriving what we will call the second law of thermal macroeconomics. Here we give a plausibility argument for this assumption in the economic context.

First let be the amount of money in state , be some fraction (e.g. ) of , and let be . Then because, as in Section 5, we have assumed that an economy accepts a macroscopic amount of money from the trader but will not give a macroscopic amount of money back to the trader for nothing. Thus, the trader can just give to move to and to move to , and each change is irreversible (so we get ).191919We do allow money to flow from one economy to another, as in Section 6, but we preclude the possibility that an economy will voluntarily hand over money to the trader.

Intuitively (though this is not actually required), under financial contact, money will tend to flow from an economy where it has less “value”, to an economy where it has greater value. Thus, consider two economies with the same goods, but different quantities of money. Within an economy, the value of any unit of money will be lower where the amount of money is greater (just as money is devalued when a central bank prints money). This means that the value of money will be lower in state than in .

So, clone the system into , with initial states . We wish to find a reversible path from to a new state and a reversible path from to a new state , such that the resulting states are in financial equilibrium. This can be done by the trader reversibly buying goods from .202020Note the implicit assumption that the economy has some type of good other than money; the trivial case of only money has to be excluded, else A14 is impossible. This increases the amount of money in comparison with the volumes of goods in that economy (and hence reduces the value of money there, to be formalised in Section 12). At the same time, the trader can reversibly sell those same goods to (increasing the value of money in that economy). The trader ends up in the same state except for amount of money. With sufficient trading, it is plausible that the two copies can be brought to financial equilibrium. Let be the states achieved, then .

Note that, as pointed out by [LY02], A14 implies that for each state there is a state such that , which is their A8. In economic terms, this just specifies that there is no “best” state—indeed, any state can be improved by the trader adding money.

8 Scaling symmetry: Extensivity

Next comes the crucial assumption A4 of scaling symmetry: that one can scale an economy by any positive real number to obtain a scaled economy and that if for then for . This assumption seems plausible if we think of an economy as consisting of lots of small units with a network of purely local interactions based on geographic proximity and we ignore the discreteness of the set of agents and possibly of some types of good. Then one can imagine a scaled version of the economy and it is plausible that the accessibility relation would inherit scaling symmetry. We call an economy satisfying A4 extensive.

Yet it may be a poor assumption for real economies. The concept of economies of scale is well-known and already argues against scaling symmetry. Indeed, an economy might need to be at least a certain size before it could include certain types of industry at all (say aircraft manufacture or investment banking).

In sum, the assumption of scalability is strong, and unlikely to hold in general in many aspects of real economies. Nonetheless, the analogy with thermodynamics in the natural sciences suggests that the assumption may be useful for many purposes. For example, classical entropy, which is based on the same scaling assumptions, has been of central importance in analyzing chemical reactions inside biological cells, although cells, like economies, are clearly enormously intricate mechanisms containing specific structures and processes operating at specific scales. In any case, we proceed with the scalability assumption, to explore whether it may provide a potentially useful idealization in some circumstances. Later we will briefly consider whether and how it may be relaxed.

A further assumption concerning scaling is A5: any system can be subdivided into two parts in an arbitrary ratio by cutting connections, and in particular the state can be decomposed into a state of the pair of systems, with . Again, it is not clear that this holds in the economic context: cutting internal connections might make a substantial change to an economy, and the economy might not be homogeneous so the two parts might not be just scaled versions of the whole. We proceed nonetheless (and leave implications of weaker assumptions for later work).

Then by Lemma 4 of [LY], we obtain the “comparison hypothesis”: for all states and of a system (with not necessarily the same subdivisions, but where necessarily ), then either or (including the possibility that ). That is, all states can be compared with each other by the accessibility relation. Note that this is a very strong claim: in economic terms, it means that for any two such states, and containing the same stock of goods, the trader can either move the system from to , or from to , or both. The trader can always guide exchanges of goods either in one direction, or the other, or both, and give or take money; but cannot create or destroy goods. The economy in question may itself be a compound of any number of smaller component economies, so that the trades required may be arbitrarily complex.

Finally, we also assume Lieb and Yngvason’s A6: if for some and a sequence of then . In economic terms, this means that if two economies are reversibly accessible when each is conjoined with an arbitrarily tiny scaled copy of some other economy, then they are also reversibly accessible from each other if that arbitrarily tiny scaled copy is entirely absent. This seems reasonable, if we set aside the discreteness of the set of agents and possibly of some types of good.

9 Economic Entropy

With the above assumptions we are now ready to begin to reap the rewards. The first reward is Theorem (Theorem 1 of [LY02] applied to this context): There is a function of state of all extensive economies such that for any two subdivisions of a system (using the notation of the previous section) then

| (1) |

and the function is unique up to orientation-preserving affine transformations: with . We illustrate the proof from [LY] in Figure 1.

In keeping with thermodynamics, we call entropy. The scale for entropy can be fixed by choosing a scale for temperature (to be defined in Section 12), leaving only its origin as arbitrary.

We deduce the all-important212121We note that this is unrelated to the “second law of economics” discussed in [Ku]. Second law of thermal macroeconomics: On putting two or more economies into contact (in any way), the total entropy can not decrease. The second law suggests that we can think of entropy as an aggregate utility or value of an economy. But in contrast to standard utility theory in which the utilities of different agents are typically not viewed as being on a common scale [ER], one can meaningfully compare, and indeed add, the entropies of different parts of an economic system. Indeed, it is only the total entropy that can not decrease. Thus, in some interactions between two economies, the entropy of one economy can decrease, as long as this is compensated by an equally large or larger increase of the entropy of the other economy. For example, this happens when money flows out of an economy where it has less value to an economy where money has greater value.

Nevertheless, the second law of TM can be seen as a substantiation of Adam Smith’s “invisible hand”: at the macro-level, putting economies in contact never decreases the total value of the joint system.

To prove the Second Law, take systems and in states , , respectively and put them in contact. It could be just financial contact or permitting arbitrary flow of goods and money or permitting flows corresponding to a given price. The joint system goes to a state equivalent to some (dependent on the type of contact). The trader does not do anything, so we have . By the property (1) we deduce that .

Note that [LY02] consider the second law to be just the existence of entropy with the property (1), but we consider it worth stating this particular consequence. Note also that the terminology “second law” is historical: the first law of thermodynamics is conservation of energy. It took physicists as much thought and experiment to settle on the first law as on the second one (for one account of this history, see [Sas2]). In our exchange economies, each type of good, including money, is assumed to be conserved, so that the “first law” of the conservation of money (and indeed, of goods) is trivial. In principle, there could be further conserved quantities needed to describe a macro-state, but at least in our context of exchange economies we do not see any.

For a simple system, with its state specified by total amounts of each type of good (including money), the accessibility relation is easy: a state is accessible from state if and only if differs from at most by having more money. But the consequences of entropy become significant for systems consisting of several parts with specifications of what transfers are possible.

For example, for a system with two parts, having a common money and a common type of good, with transfers only via a trader who has to end up with the same state except for money, the state space for the system is given by the amounts of goods and money in parts , but the allowed changes conserve . Within this 3D space, the 2D surface of constant total entropy separates the space into those states that are accessible from a point on this surface from those that are not accessible. Changes within the surface of constant total entropy are reversible. The others are not. This will be illustrated by a simple example in the next section.

Alternatively, one could leave out the trader, but allow transfers of goods and money between the two parts: that is, the economies trade directly with each other, rather than each transaction being mediated by the trader. Then the possible changes conserve both and . In this 2D space there are curves of constant total entropy which separate accessible states from inaccessible ones. The picture is analogous to the indifference curves for individuals in standard economics, but now at the level of a whole multi-part economic system. Again, this will be illustrated in the next section.

It is worth reflecting on how extraordinarily strong is the existence of entropy, with the property (1). On the one hand, it provides a very restrictive constraint on possible transitions from one equilibrium state of a system or set of systems to another: it precludes any transition that leads to a decrease in (total) entropy, whatever the trader (or other exogenous agent or agents) does. On the other hand, it specifies that there is always an available path by which the trader or other external agency can move the economy in any entropy-increasing way in the state space. Entropy-conserving changes can also be achieved in a limiting sense (in practise, requiring transitions to be carried out arbitrarily slowly).

If we interpret entropy as corresponding to aggregate utility, then the first observation implies that trade, or financial flow, between any two (exchange) economies does not decrease aggregate utility. That is, there will always be gains of trade, except for the limiting case of zero gains. Indeed, if any number of economies are put into contact using any network of trade or financial connections, trade or financial flows will yield non-negative gains of trade for the compound system. Furthermore, any reduction in restrictions on trade (e.g., removing a barrier to trade for one or more goods, or removing a prohibition on moving money from one economy to another) will lead to non-negative gains of trade. Note, though, that the gains of trade may be unequally distributed—indeed, one or more economy may lose entropy, as long as the entropy of the whole system increases. We analyse trade in detail in Section 19.

One consequence of existence and extensiveness of entropy is that it provides a rationale for the standard economics notion of representative agent,222222The notion of a representative agent, is widely and somewhat controversially used in providing a microfoundation for macroeconomic behaviour. [H96] traces the notion back to Alfred Marshall [M20], while [K92] finds similar ideas in Francis Edgeworth [E81]. The notion of a representative firm was critiqued by Lionel Robbins [R28]; and critiques of the broader coherence of the notion, in view of the heterogeneity of economic agents, have continued [K92]. Nonetheless, representative agent models continue to be influential in macroeconomics and finance [MP]. though with a twist. Given entropy function for an economy with agents, we can define and consider it as the utility for a representative agent to possess amounts of money and of goods. Maximising the sum of the entropies of several economies then corresponds exactly to maximising the average utility of their representative agents, weighted by the numbers of agents in each economy. There is no need, however, to scale entropy to the level of individual agents. Our approach says that each economy has a utility function (its entropy) and a collection of economies in contact act to maximise the sum of their constituent utilities (i.e., maximizing the entropy of the collection of economies as a whole). Note that this maximization of summed utility over the system of economies can arise purely from the interactions of myopic or selfish agents, from their ability to trade and to move money from one economy to another, as long as there is convergence to a unique statistical equilibrium (Section 4).

The “twist” is that there is no requirement that each economy attempts to “maximize its own utility.” For example, money can flow from one economy to another, lowering the entropy of one and increasing the entropy of the other, as long as the entropy of the whole system does not decrease. We will, though, also consider in Section 19.1 the important special case of what we will call “mutually beneficial” trade, which is defined by not decreasing the entropy of any economy (i.e., leading to an analogue of Pareto optimality at the level of economies).

To end this section, we discuss to what extent the entropy function depends on the choice of numeraire (money in our presentation so far).232323We are not aware whether Lieb and Yngvason discussed the analogous question in the physical case, but a difference is that they allow volume to change, whereas we fix the amount of goods. We restrict attention to numeraires for which it is always desirable to have more (required for Sections 5 and 7). A priori, the accessibility concept depends on the choice, because the state space for a system has fixed amounts of all goods except the numeraire. But one can consider the restricted set of changes that fix the amount of numeraire too. Then accessibility of one state from another is independent of which good is considered to be the numeraire. Hence the partial orders determined by the two entropy functions must be the same. Then extensivity of the entropies implies that one must be an affine transformation of the other.

10 A toy illustration with interacting agents

One of the distinctive characteristics of the conception of thermal macroeconomics developed here is that it proceeds entirely at the level of aggregate behaviour, positing axioms about trade and financial flows and deducing conclusions such as the second law. Thus, just as classical thermodynamics makes no reference to the molecular basis of pressure, heat, entropy and so on, so TM makes no reference to the micro-foundation of economic behaviour, in terms of the actions of individual agents. A great advantage of this strategy, both for physics and economics, is that the micro-foundations of real-world systems are often of great complexity and only partially known, so that providing a detailed micro-level analysis is not realistic—but nonetheless, laws at the aggregate level are still derived.

It is interesting, however, to illustrate the general theory by special cases in which micro-foundations are sufficiently simple that they can be analysed directly. In the physics context, a prime example is the molecular model of ideal gasses, leading to a foundational explanation of temperature and pressure and the entropy function , where is the number of molecules, and are the volume and energy per molecule and is the number of degrees of freedom per molecule (e.g. for a diatomic molecule like or , is the sum of three translational plus two rotational degrees of freedom, at normal temperatures where vibration is suppressed quantum-mechanically). Note that it is conventional to add and multiply by Boltzmann’s constant, but that is just an affine transformation.

In particular, let us compute the entropy for a toy example of an exchange economy with a single good in addition to money and independent identical “Cobb-Douglas” agents.242424We use the term slightly differently from [SF]. By Cobb-Douglas agents we mean firstly that they have a “utility” function

| (2) |

for amounts of good and of money, for some . It is natural to think of both goods and money as being desirable for each agent, in which case .252525We adopt the form (2) with minus ones in the exponents because it makes future formulae simpler. Exponent corresponds to indifference concerning amount of goods, while corresponds to preference for fewer goods, which allows one to take into account cases like pollutants. Nonetheless, our theory requires only that money is desirable and only at the aggregate level. Perhaps surprisingly, we will see that this is satisfied for all .

Importantly, in contrast to standard economic usage, our agents are not utility maximisers; instead, they use their utility functions to bias the probability rate for the outcome of random pairwise encounters towards increased utility for both, but with some “errors” (though these can be made arbitrarily small, by choosing high values of and ). Thus, our agents can be viewed as “noisy” utility maximizers, where the level of noise can be as small as desired but not zero.

We define the stochastic dynamics more precisely now. Let us consider an encounter between one agent and another agent . Label the amounts of money and goods for each agent before the encounter by pairs of positive 2-component vectors, and after the encounter by . We suppose that transitions are restricted to those that conserve both goods and money: and . We denote the probability rate from to by . Each agent biases the probability rate by making it proportional to their utility of the outcome. Thus we take

where is an encounter rate for and and the -functions enforce conservation of goods and money. We suppose that the outcome is independent of all previous encounters of all pairs, conditional on the current state. The constraints make the rate integrable and hence the stochastic process well-defined.

Assuming the graph formed by positive encounter rates between agents is connected, for given total goods and total money this stochastic process has a unique stationary probability that attracts all initial probability distributions (this property is called “ergodicity”). If the money and goods were quantised, ergodicity would follow from a standard result for irreducible continuous-time Markov processes on finite state spaces [Sen] (or positively recurrent ones on countable spaces, e.g. Thm 1.6 of [Ke]), but here the state space is continuous. Nevertheless, the result can be obtained for continuous spaces by use of more sophisticated techniques. For one treatment, see [DGS]. Their models have only money, but extension to an arbitrary finite number of types of good is straightforward. They give a detailed proof only in the case and equal encounter rates between all pairs of agents, but state that their method generalises. In another line of work, [CCL] proves ergodicity for the Kac model of a 1D gas, which is equivalent to the case . A project for the future is to prove ergodicity in a more direct way. A key point is to adapt the metric to measure distances between probability distributions appropriately. This was done in [M11] for discrete-time Markov processes with independent updates at each site conditional on the current state of the whole network, following ideas of Dobrushin, but requires extension to the case of exchange processes.

In fact, the process is reversible (in the sense of Markov chains) with respect to the distribution with density proportional to the product of the utilities, i.e.,

where now represent the vectors and . Hence we deduce that this distribution is the stationary one. It is a product of two Dirichlet distributions (one for the partition of goods, the other for money), and the normalisation constant is

| (3) |

The marginal distribution for one agent in this stationary distribution is a product of two independent Beta-distributions (one for goods, one for money). For example, the Beta-distribution for money has density

It is an illustration of how inequality of wealth can arise (on which there is a large literature, e.g. [C4]), though note that that for and large, the bulk of the distribution is peaked close to the mean , and that each agent samples the whole distribution as time evolves.262626In particular, wealth does not concentrate in a fixed set of agents.

To determine the entropy of this toy economy we need to spell out how each agent interacts with an external trader. We specify this to be consistent with how agents interact with the other agents, i.e., biased in the same way by their utility function. We suppose the trader offers to buy or sell arbitrary amounts at a price . Then the probability rate for each agent to transition from to is

for some , which is the trader’s encounter rate with agent . There is no contribution to the dependence on from the trader because it has unlimited goods and money. As the transition is along the “budget” line we can eliminate in favour of and write the rate as a function of just (given ):

This is a Beta-distribution again (though unnormalised), and its mean is

The means over the initial stationary distribution were . Thus the change from the mean of to the mean of is

Thus in a time we obtain a change

in the quantity of goods, where . is positive, zero or negative according as is less than, equal to, or greater than

| (4) |

The change in the amount of money is . So we see that

with equality iff . This is precisely the condition for infinitesimal changes in

| (5) |

Thus we deduce that (up to an affine transformation) the entropy of the toy economy is this function . The factors of are included to make the entropy scale correctly with .

For completeness of description of the model to fit with the axioms, we must also specify how the trader can exchange money with the economy. We propose that the trader makes available an amount of money; agent interacts with the trader at the rates and updates their money according to probability density proportional to , where the Heaviside function if , if , and is the initial total money in the economy. This produces a stationary density proportional to . It is relatively easy to check that this leads to an average transfer of money from the trader to the economy. Furthermore, it is relatively easy to check that the resulting model satisfies the axioms of thermal macroeconomics used here, including those that will come in the next section. We leave writing up the details for the future.

It is important to note that even though this example has homogeneous agents, the utility for the resulting representative agent is not the utility for a single Cobb-Douglas agent, which recall is . It is not even a function of the utility for a single agent. This is not too surprising, however, because our agents use their utility function to bias the probability rates, not to maximise utility. Nonetheless, if the exponents and of the Cobb-Douglas utility function are scaled up sufficiently, the agents will approach maximizing behaviour (as will be explained in Section 12).

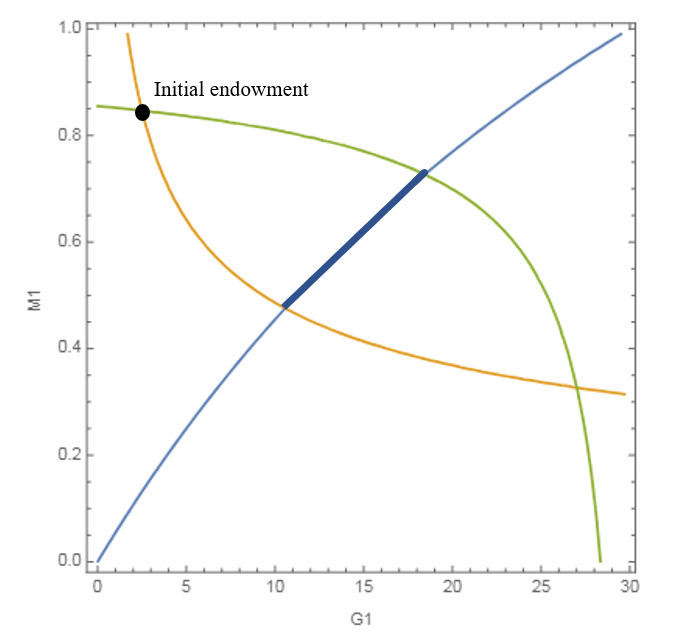

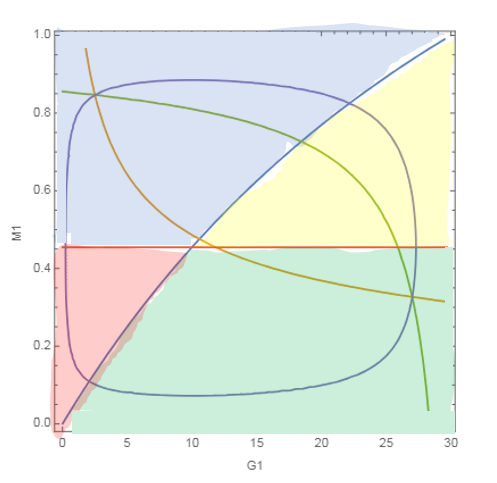

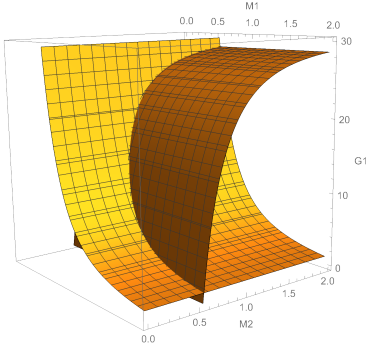

To illustrate the consequences of entropy, Figure 2

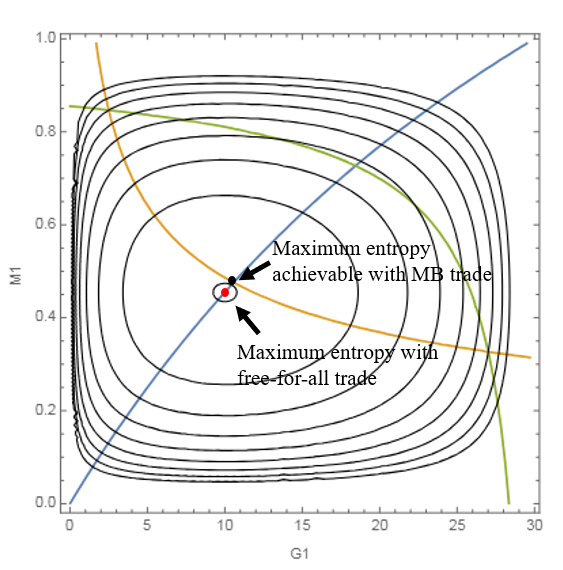

shows the boundary of the region accessible from an initial endowment of a system of two Cobb-Douglas economies272727The choice is perhaps unrealistic, because it implies the utility is independent of the amount of goods, but similar figures are obtained for .. We see that adding money to either economy is allowed, but also adding money to one while removing money from the other is allowed, within limits. More importantly, goods can be moved from one to the other but this might require adding money to one or both. Figure 3 shows contours of the entropy for division of goods and money between two Cobb-Douglas economies with no external trader. The allowed transitions are those that do not decrease the total entropy.

The reader may recognise (5) as the entropy of an ideal gas (discussed earlier), where is the number of molecules, represents volume of the container, represents internal energy, , and for ratio of specific heats (e.g. for a diatomic gas), modulo a conventional additional term that has no effect if is constant. Indeed, that analogy is why we chose this entropy function to try in (5). The analogy should not be pushed too far, however. In particular, in an accessible change for a gas driven by an external device whose only nett change is in the height of a weight (as in [LY02]), the volume available to the gas can change, whereas for our exchange economies, the quantity of goods should return to its initial value. Note, too, that in the more general case where there are different types of good, the quantities of the types of good correspond most naturally to the quantities of different types of molecule in the gas, rather than to the volume of the mixture of gases.282828It is interesting to consider the possibility that, instead of amount of goods, the number of agents in an economy may be more closely analogous to volume. Thus, population size could be represented explicitly, and allowed to change, in the short term through migration, and in the longer term, through births and deaths. Questions of population change and flow are, of course, of considerable relevance to analysis in political economy and this is a direction deserving study. Note, though, that the current analysis allows the possibility that agents own goods and money in more than one economy, so it is not yet clear what it would mean to assign them to a particular economy.

One could ask why the entropy of the trader was not considered in this analysis, but the assumption that the trader has unlimited goods and money can be regarded as saying that its entropy is independent of how much goods and money it has. More precisely, we are assuming that the trader has no preferences for amounts of goods and money, so all changes are allowed, which means all its states must have the same entropy. Strictly speaking, to talk about entropy of the trader we require it to be an extensive trading economy.

In the design of such micro-economic models, it is important to exclude the possibility of the trader acting as a Maxwell demon, which would probably lead to all states being accessible from all other states subject to conservation of the types of goods, and hence to failure of A14.

Instead of guessing an entropy function as above, and showing that it fits, a more principled way to derive the entropy function is via the strategy of proof of Theorem 1 of [LY02]. We do that in Appendix A.

This toy example also has wider significance. We have stressed that thermal macroeconomics, like thermodynamics, is defined purely at the “macro” level, and does not depend on specific microfoundational assumptions. This makes macro analysis possible for systems for which a detailed microfoundational analysis is infeasible—which will typically be true for realistic economic systems, in the light of the heterogeneity and complexity of human behaviour. It is nonetheless reassuring to find an explicit illustration of how there can be a bridge between the micro and macro accounts, where the micro-foundations are sufficiently simple to be tractable—just as statistical mechanics provides a micro-foundation for thermodynamics of sufficiently simple physical systems (e.g., ideal gases). Note this toy micro-economic model is also the starting point for the extensive tests of TM by computer simulation reported in [LMC].

A purely macro-analysis is sufficient to derive the second law and a variety of specific economic results in following sections; and macro-quantities, such as economic entropy and temperature can in principle be measured directly; these issues will be discussed further below. But a micro-foundation, where available, is nonetheless required to explain the specific form of the entropy function , and hence the detailed behaviour of an economic system.

This raises the interesting question of the impact of different stylized micro-foundational assumptions on aggregate behavior and how this behaviour aligns with the macro-description in a thermal macroeconomic framework, and in particular, the question of how different micro-foundational assumptions modify the entropy function. Many such assumptions are possible. Starting from our Cobb-Douglas model, for example, different agents could have different and (this leads to relatively straightforward extension of the above results, in particular the entropy has the averages of and in place of and ). Exchanges could be restricted to change of goods and money of opposite signs. Agents could make just a fraction of their holdings available at each interaction. There can be more than one sort of good (in addition to money). The utility function might incorporate substitution effects or complementarity effects. Goods and money might come in discrete amounts. Moreover, agents might be subject to behavioural biases, such as a status quo bias in favour of whatever goods they hold at the time [SZ] or tendencies to compare with, or imitate, their neighbours. We anticipate that, unlike this toy example, the preferences of agents in general result in an entropy function that is not just a sum of functions of the quantity of each type of good. Examples of some of these effects are treated in [LMC].