Bayesian optimal change point detection in high-dimensions

Abstract

We propose the first Bayesian methods for detecting change points in high-dimensional mean and covariance structures. These methods are constructed using pairwise Bayes factors, leveraging modularization to identify significant changes in individual components efficiently. We establish that the proposed methods consistently detect and estimate change points under much milder conditions than existing approaches in the literature. Additionally, we demonstrate that their localization rates are nearly optimal in terms of rates. The practical performance of the proposed methods is evaluated through extensive simulation studies, where they are compared to state-of-the-art techniques. The results show comparable or superior performance across most scenarios. Notably, the methods effectively detect change points whenever signals of sufficient magnitude are present, irrespective of the number of signals. Finally, we apply the proposed methods to genetic and financial datasets, illustrating their practical utility in real-world applications.

Key words: High-dimensional change point detection; mean vector; covariance matrix; maximum pairwise Bayes factor.

1 Introduction

Detecting change points in the mean vector or covariance matrix of multivariate data can be crucial in various scenarios. Changes in the mean vector may indicate shifts in the central tendency of the data, while changes in the covariance matrix signify alterations in the relationships among variables. For instance, in financial analysis, representing the returns of various assets as a multivariate time series allows the detection of changes in the mean or covariance during significant events or financial crises. Similarly, in manufacturing, monitoring multivariate data related to product characteristics helps ensure product quality. Identifying change points in the mean vector or covariance matrix can signal deviations in production processes, enabling timely interventions to maintain quality and minimize defects.

Suppose that we observe a sequence of random vectors independently from -dimensional Gaussian distributions, say for . We say that there exist change points, , if and

where and . In general, the number of change points and their locations are unknown. We focus on scenarios where changes occur in either the mean vector or the covariance matrix. Our primary objectives are (i) testing for the existence of change points and (ii) estimating the number and locations of change points if they are present. Notably, we consider a high-dimensional setting where the number of variables increases with the sample size and may even be much larger than .

In this paper, we develop two Bayesian methods for detecting change points in in mean and covariance structures, respectively. These methods build on the maximum pairwise Bayes factor approach introduced by Lee et al. (2021) and Lee et al. (2024), adapting it to address the challenges of high-dimensional change point detection. Specifically, we select a window size and compute the maximum pairwise Bayes factors using only the points before and after each central point . Choosing an appropriate window size is crucial, and the optimal choices depends on the data characteristics. To address this, we propose multiscale methods that consider multiple window sizes simultaneously, thereby mitigating the impact of suboptimal window size selection and achieving stable performance. Furthermore, we extend our methods to handle scenarios where both mean and covariance changes occur simultaneously, providing a comprehensive solution for change point detection in complex data structures. It is worth noting that while the pairwise Bayes factor approach has been previously applied to two-sample hypothesis testing, as in Lee et al. (2021) and Lee et al. (2024), extending such an approach to high-dimensional change point detection poses significant challenges, particularly on the theoretical front. Our work introduces technical innovations to establish minimax-optimal localization rates, making this the first Bayesian method to achieve such results in high-dimensional change point detection.

While several frequentist procedures have been proposed for change point detection in high-dimensional settings (e.g., Dette et al. (2022), Wang et al. (2021), Grundy et al. (2020), Wang and Samworth (2018), Avanesov and Buzun (2018), and Matteson and James (2014)), to the best of our knowledge, no Bayesian methods have been developed to address high-dimensional change point detections. The Bayesian methods proposed in this paper offer significant advantages, requiring weaker conditions compared to existing frequentist approaches—details of which will be elaborated later. Moreover, Bayesian change point detection inherently differs from its frequentist counterparts, with unique characteristics, making the development of such methods both important and of independent interest.

The main contributions of this paper are threefold. Firstly, we propose the first Bayesian tests for change point detection in either the mean or the covariance structure in high-dimensional settings, supported by theoretical foundations. We establish the consistency of the proposed Bayesian tests under both null and alternative hypotheses with mild conditions (Theorems 2.1 and 3.1). Secondly, building on the proposed Bayesian tests, we develop Bayesian change-point detection methods that estimate the location and number of change points, which consistently estimate both the number and locations of change points (Theorems 2.2 and 3.2). The proposed methods require weaker assumptions than existing approaches, while demonstrating nearly minimax localization rates (Theorems 2.3 and 3.4). Thirdly, the proposed Bayesian tests and change point detection methods are scalable to high-dimensional settings and feature straightforward implementation. Leveraging the modularization framework from Lee et al. (2021) and Lee et al. (2024), these methods significantly enhance computational efficiency by avoiding the inversion of singular matrices, making them practical and efficient for real-world applications.

The remaining of the paper are structured as follows: Section 2 (Section 3) introduces a Bayesian test for detecting change points and estimation methods for estimating the locations of these points in the mean (covariance) structure. Sections 4 and 5 assess the practical performance of the proposed methods through simulation studies and real data analysis, respectively. Concluding remarks are provided in Section 6, and proofs of the main results can be found in the supplementary material.

1.1 Notation

For any given constants and , we use the notation and to represent the maximum and minimum between the two, respectively. When considering a vector and a positive integer , the vector -norm is denoted as . When , it means the vector -norm, . For positive sequences and , the notation or equivalently indicates that as . means there exists a constant such that for all large . The notation implies both and . For a given matrix , the Frobenius norm is denoted as , the matrix -norm as , the spectral norm as , and the matrix maximum norm as . For given and , denote as a sub-matrix of consisting of th rows and th columns. For simplicity, let for any .

2 Change point detection in mean structure

Suppose we observe the data independently from -dimensional Gaussian distribution with a common covariance. Specifically, for . We are interested in testing the following hypotheses:

| (1) |

In this section, the main goals are (i) to develop a consistent Bayesian test for change point detection problem described in (1), and (ii) to estimate the number and locations of change points, should they exist.

2.1 Testing the existence of change points in mean structure

Rather than directly testing the hypothesis for change point detection in (1), we decompose the problem into a series of smaller hypothesis tests. Specifically, we begin by testing whether there is a change in the mean vector when moving from to , for each given . For each individual hypothesis test, only the observations within an appropriate window size are considered, rather than using all observations on both sides. Finally, we address the overall change point detection problem in (1) by aggregating the Bayes factors from these smaller hypothesis tests.

Let be a window size. For a positive integer , consider the model

| (2) |

where and , and the testing problem

| versus | (3) |

That is, we focus on observations to the left of , say , and observations to the right of , say , to detect a change point. We call the window size. If is true, we say that is a change point. Note that is true for all if and only if is true. Therefore, we will construct Bayes factors for (3) and then combine them to form the final Bayes factor for (1).

To construct the Bayes factor for hypothesis testing problem (3), we apply the maximum pairwise Bayes factor (mxPBF) framework (Lee et al., 2021). Specifically, the marginal models for the th variable in model (2) are

| (4) |

for , where is the entry of . For given window size and , the hypothesis testing problem (3) can be decomposed into small testing problems

| versus |

for , in the sense that is true if and only if is true for all . Thus, we first calculate the pairwise Bayes factors (PBFs) for each hypothesis testing problem versus , and then integrate them. Under , we impose the following prior ,

and the following prior under ,

where , and . The above priors, originally proposed in Lee et al. (2024), have been tailored to fit our setting. Then, the resulting log PBF is

where

Here, and are likelihood functions of (4) under and , respectively. Refer to Lee et al. (2024) for a detailed derivation of the resulting PBF. Now, the mxPBF idea can be adopted to construct the Bayes factor for (3):

| (5) |

To obtain the final mxPBF for testing the existence of change points, (1), we take the maximum once again over and define

| (6) |

We call (6) the mxPBF for testing the existence of change points in mean structure. For a given threshold , we conclude that is true if , or otherwise, we conclude that is true. Note that the mxPBF exceeds the specified threshold if and only if at least one PBF, , exceeds . Therefore, this Bayesian test based on the mxPBF detects a change point if any component of the mean vector undergoes a significant change at some point.

To justify the proposed Bayesian test based on the mxPBF, we establish its consistency. The consistency of mxPBF, denoted , means that under the null, we have , and under the alternative , we have as . Throughout the paper, we assume the following condition for the window size :

-

(A1)

and as .

Theorem 2.1 states that the resulting mxPBF defined in (6) is consistent for testing the existence of change points.

Theorem 2.1

Suppose that we observe , and consider a hypothesis testing (1). Assume that a window size satisfies condition (A1). Let and be constants arbitrarily close to but slightly larger than and , respectively.

-

(i)

Suppose is true, i.e., for all . If for some constants and

(7) then we have, for some constant ,

-

(ii)

Suppose is true and is the set of change points. If there exist and such that and

(8) for some constant , then we have, for some constant ,

When , the condition is satisfied if . In this case, we assume that is arbitrary close to , i.e., for some small constant , and .

Recently, Enikeeva and Harchaoui (2019) proposed a test for the change point detection in mean under sparse alternatives. The sparse alternative means that the changes occur only in variables among variables, for some constant . Note that this method does not permit changes to occur in only a fixed number of components; instead, the number of components undergoing changes must grow with the dimension of the data. Furthermore, they considered an identity covariance matrix, , and assumed there is at most one change point. For theoretical results, they assumed and as . This condition implies that the number of observations, , cannot be too large, which may not be a natural assumption. In Theorem 2.1, we do not impose such a requirement. Their test can detect a change point if (1) in moderate sparsity regime where or (2) in high sparsity regime where for some positive constants and , which turned out to be minimax or nearly minimax separation rate under the -norm. On the other hand, we consider a general unknown covariance matrix , allow changes to occur only at fixed locations, and assume that there can be multiple change points. However, our condition (8) can be seen as for some constant when , thus it uses a different type of criterion, the maximum of the elementwise maximum norm, compared to the conditions in Enikeeva and Harchaoui (2019). Therefore, our test and the test in Enikeeva and Harchaoui (2019) have different characteristics which are not directly comparable.

2.2 Estimation of change points in mean structure

The Bayesian test proposed in Section 2.1 can identify the presence of change points but does not provide estimates of their locations. In this section, we propose a procedure for estimating both the number and locations of the change points based on the maximum Bayes factor (mxPBF). For given window size and threshold , define an initial estimate of the first change point

where is defined at (5). Suppose that we have found and assume that . By Theorem 2.1, with probability tending to one, the mxPBF is (i) not greater than a fixed threshold if and (ii) greater than if . When , we cannot ensure the probabilistic behavior of mxPBF. What we can expect is that with high probability tending to one, which implies that as . Therefore, we aim to obtain a refined estimate for the first change point, say , by focusing on the interval and identifying the point with the strongest evidence for being a change point based on the mxPBF criterion:

After obtaining the refined estimate , the process of detecting subsequent change points is similar to the described process for detecting the first change point. Specifically, the proposed process for detecting change points can be described as follows, where is the refined estimate for the th change point and :

Let be the estimated change points. By the definition, we require for any , where . This is a reasonable assumption since we need enough data between the change points to consistently detect them.

Let be the class of distributions of with , , where change points exist with , , and . Therefore, represents the minimum distance between change points, and denotes the minimum scaled-mean difference at the change point. The following theorem shows that the final estimate consistently detects (i) the number and (ii) the locations of change points with the error bound .

Theorem 2.2

Wang and Samworth (2018) proposed a change point estimation method for high-dimensional mean vectors based on a sparse projection. In their settings, they assumed the data are independently generated from a -dimensional Gaussian distribution with mean vectors and a common diagonal covariance matrix for some known . Let and . To obtain the localization rate for change point detection (in their Theorem 2), they assumed

| (9) |

for some constant . Note that in their notation corresponds to in our notation, so the rate of the lower bound in (9) can be written as . Furthermore, (9) implies . On the other hand, when and for all , our condition implies that for some constant . Thus, condition is much weaker than condition (9) used in Wang and Samworth (2018). The difference between those conditions increases as approaches .

We say that the localization rate for change point detection is if

Thus, Theorem 2.2 implies that the localization rate is equal to . The next theorem says that, under certain conditions, this is indeed a nearly minimax rate up to a factor of .

Theorem 2.3

Let be the class of distributions of with , where only one change point exists and . Suppose . Then, we have

3 Change point detection in covariance structure

Suppose that we observe the data independently from -dimensional Gaussian distributions with mean zero, that is, for . Consider a hypothesis testing

| (10) |

The main goals in this section are (i) to develop a consistent Bayesian test for the change point detection problem (10) and (ii) to estimate the number and locations of change points if they exist.

3.1 Testing the existence of change points in covariance structure

Similar to the mean vector case in Section 2.1, we approach the hypothesis testing by decomposing it into multiple small testing problems. For a given window size and a positive integer , consider the following model

| (11) |

and the testing problem

| versus | (12) |

Thus, if is true, then is a change point. Note that is true for all if and only if is true. Hence, we will construct Bayes factors for (12) and then combine them to form the final Bayes factor for (10).

To construct the Bayes factor for (12), we again apply the mxPBF idea (Lee et al., 2021). Let , and for any , , where is the correlation matrix based on . For a given pair with , the conditional models from model (11) can be written as

| (13) |

For a given integer , the hypothesis testing problem (12) can be decomposed into the following small testing problems,

| versus |

for , in the sense that is true if and only if is true for all pairs such that . Let represent the inverse-gamma distribution with shape parameter and rate parameter . We will calculate the PBFs for each hypothesis versus . Let for some as before. Under , we use the following prior ,

where and , and the following prior under ,

where

Then, the resulting log PBF is

where is the gamma function,

and

Note that and

are likelihood functions of (13) under and , respectively. Refer to Lee et al. (2024) for a detailed derivation of the resulting PBF. Then the mxPBF for (12) is defined as

Similarly to the case of the mean vector, the final mxPBF for testing the existence of change points in the covariance structure is defined as follows:

| (14) |

For given threshold , we conclude that in (10) is true if , or otherwise, we conclude that is true.

We now introduce the following sufficient conditions to guarantee consistency of the mxPBF in (14).

-

(A2)

.

-

(A3)

There exist an index and a pair with satisfying

and

for the constant and some constant .

-

(A3⋆)

There exist an index and a pair with such that ,

for some constant and .

Condition (A2) is a sufficient condition for consistency of the mxPBF in (14) under the null . When there is no change point, it allows the cases where possibly and as at certain rates. When is true, suppose there exist change points . Conditions (A3) and (A3⋆) represent the minimum lower bound condition of the signal under the alternative . In fact, they can be roughly understood as the squared maximum standardized-difference condition between and , say

| (15) |

for some constant . Specifically, let

| (16) |

for some small constant . If (15) and (16) hold for and some , then condition (A3) or (A3⋆) is met. For a detailed statement, see Lee et al. (2024) (Lemma 3.1 in Supplementary material).

Theorem 3.1 says that we can consistently detect the existence of change points in the covariance structure based on the mxPBF in (14).

Theorem 3.1

Suppose that we observe , and consider a hypothesis testing problem (10). Assume that a window size satisfies condition (A1). Let be constant arbitrarily close to but slightly larger than 3.

-

(i)

Suppose is true, i.e., for all . If , for some positive constants and condition (A2) holds, then for some constant ,

-

(ii)

Suppose is true and is the set of change points. If there exist and a pair such that and satisfy condition (A3) or (A3⋆), then for some constant ,

When , the condition is satisfied if . In this case, we assume that is arbitrarily close to , i.e., for some small constant , and .

Theorem 3.1 assumes much weaker conditions compared with the existing literature. Avanesov and Buzun (2018) suggested a testing procedure based on bootstrap and multiscale idea for a change point detection. A set of window sizes was used to construct the test statistic. They investigated consistency of the test in high-dimensional settings under the sparsity assumption for precision matrices, where . Let be the number of subsamples for constructing bootstrap statistics, and let and be the minimum and maximum window sizes belonging to , respectively. To prove consistency of the proposed test, Avanesov and Buzun (2018) assumed and , which require the true precision matrices to be sufficiently sparse. Furthermore, irrepresentability conditions of the precision matrix were also assumed for the existence of a consistent estimator for the precision matrices. Hence, our test based on the mxPBF requires much weaker conditions on for consistency, while allowing multiple change points and not assuming any sparsity condition on covariance (or precision) matrices.

3.2 Estimation of change points in covariance structure

In this section, we suggest a procedure for estimating the number and locations of change points based on the mxPBF in Section 3.1. For given window size and threshold , let and

Similar to Section 2.2, let be the estimated change points.

Let be the class of distributions of with , , where change points exist with , , and conditions (A3) or (A3⋆) hold for all . The following theorem shows that consistently detect (i) the number and (ii) the locations of change points with the error bound .

Theorem 3.2

Suppose that . Let and be constants arbitrarily close to but slightly larger than 1 and 3, respectively. Assume that , , , and condition (A1) holds for some constants and . Then we have

We compare Theorem 3.2 with existing results in the literature. Wang et al. (2021) proposed two procedures to detect change points in covariance structures for sub-Gaussian random vectors. Their second procedure, called WBSIP, has a nearly minimax localization rate, , where and . To obtain theoretical results, they assumed that for any , there exists a constant such that . If we assume that and is a fixed constant, it becomes for some constant . On the other hand, under the same conditions, conditions (A3) and (A3⋆) are satisfied if for some constant . Thus their condition is stronger than ours if and , but a direct comparison is difficult due to the different criteria used to measure the magnitude of the change.

Recently, Dette et al. (2022) developed a two-step approach to detect a change point in covariance structures when there is only one change point and each component of an observation is a sub-Gaussian random variable. Let be the true change point and be a lower bound for the smallest nonzero entry in . They obtained the localization rate (Corollary 3.2 in Dette et al. (2022)) for some and such that . To obtain this result, they assumed , , and for some constants , , and , where is a threshold for the dimension reduction in their method. If we further assume that , and , then their localization rate becomes . Note that if we set , the localization rate in Theorem 3.2 coincides with . Furthermore, implies that the smallest nonzero entry in is larger than a fixed positive constant, which is stronger than our condition assuming the maximum nonzero entry in is larger than . Therefore, our result establishes the localization rate of the proposed change point detection method under relatively weaker assumptions compared to existing literature.

Theorem 3.2 implies that the localization rate is equal to . We will show that, in the following two theorems, this rate is minimax-optimal up to a factor of under certain conditions.

Theorem 3.3

For given constant and , define a class of joint distributions of ,

If , then we have

for some constant and all sufficiently large .

Theorem 3.3 says that if is smaller than certain constant, consistent estimation in terms of the localization rate is impossible. Specifically, this theorem implies that if , the localization rate is larger than some constant , at least in the worst case. Theorem 3.4 shows that if , the lower bound of localization rate becomes instead of .

Theorem 3.4

If , we have

for some constant and all sufficiently large .

This results means that if conditions (15) and (16) hold, the localization rate given at Theorem 3.2 coincides with the obtained minimax lower bound up to . Since in our setting by (15) and (16), has the same rate with . Thus, the localization rate in Theorem 3.2, , is nearly optimal in terms of the minimax. Furthermore, Theorems 3.3 and 3.4 show that should be larger than to have the minimax lower bound of the localization rate, . In our settings, for some constant by (15) and the condition . Thus, if , our condition is also rate-optimal.

4 Simulation study

In this section, we compare the proposed change point detection methods with several state-of-the-art methods. The comparison spans a wide range of scenarios, including both single and multiple change points, varying dimensions, different numbers and magnitudes of signals, and various covariance matrix structures. We consider situations where changes occur either in the mean or in the covariance, but not both. As competing methods, we choose the change point detection methods proposed by Dette et al. (2022), Grundy et al. (2020), Wang and Samworth (2018) and Matteson and James (2014). For simplicity, we refer to these competing methods as Dette, Geomcp, Inspect and Edivisive, respectively. Dette is designed to detect a single change in the covariance structure and will be included only in relevant scenarios. Inspect is intended for detecting changes in the mean structure and will be compared only in applicable settings. Geomcp can detect change points in both the mean and diagonal covariance structures. Edivisive is a nonparametric change point detection method.

4.1 Multiscale method

Selecting an appropriate window size is critical for the performance of the proposed methods. However, the optimal window size is case-dependent, which makes it challenging to choose the right size when there is limited prior knowledge about the data. To alleviate this issue and improve stability across various scenarios, we propose a multiscale approach inspired by Avanesov and Buzun (2018). Let denote the set of window sizes, where and is an odd number. For , let denote the set of detected change points from the mxPBF with window size . We sequentially use the window sizes to group the change points obtained from each mxPBF. Specifically, for each , we first construct intervals based on the narrowest window , defined as . We then count how many points are included in each interval among the estimated change points . If an interval contains at least points, the change points within that interval are grouped together. Once no interval contains or more points, we proceed to the next window size, , and use the change points in to construct the intervals . From these intervals, we again group change points if at least change points, excluding those that have already been grouped, fall within a single interval. If overlapping intervals contain exactly the same number of points, we prioritize grouping the interval with the smaller sample variance of the points within it. This process is repeated until groups are identified using the final window size . Each of the resulting groups corresponds to a single change point, and the final estimate of the change point is computed as the average of within each group.

Since the final decision is based on a majority rule, we refer to this multiscale approach as mxPBF_major throughout. In the numerical studies, we found that mxPBF_major achieves reasonable performance across a variety of scenarios, as detailed in the supplementary material. This multiscale method can also be theoretically justified. Specifically, if at least the window sizes in satisfy the conditions of Theorems 2.2 and 3.2, and if holds for , then it can be shown that the localization rate of the proposed multiscale approach is at most .

4.2 Choice of hyperparameters

The proposed mxPBFs for detecting changes in mean vectors and covariance matrices require the selection of hyperparameters. The mxPBF in (6), designed for mean structures, includes the hyperparameter . Similarly, the mxPBF in (14), for covariance structures, involves the hyperparameters , , , , and . We recommend selecting for all to minimize their impact on mxPBF. The choice of the hyperparameter in the mxPBFs (6) and (14) is more crucial for performance. Although Theorems 2.1 and 3.1 provide theoretical conditions for selecting , they may be overly conservative in practice. Therefore, we extend and adapt the method proposed in Lee et al. (2024) to select , which controls the empirical false positive rate (FPR). We select for each window size using the proposed FPR-based method, with detailed explanations provided in the supplementary material. By default, we set the prespecified FPR to 0.05, the threshold to 10, and the number of simulated datasets to .

4.3 Evaluation metrics

To illustrate the performance of each method, we use the F1 score and the Hausdorff distance. For a given integer , let true positive (TP) be the number of true change points whose differences from the estimated change points are less than , i.e., , where and are sets of true and detected change points, respectively. The precision and recall are then defined as and , respectively. The score is the harmonic mean of precision and recall:

The F1 score always falls between 0 and 1, with values closer to 1 indicating better performance.

The Hausdorff distance measures the robustness of detection methods by quantifying the largest discrepancy between a true change point and its corresponding estimated change point:

The Hausdorff distance is non-negative, with values closer to 0 indicating better performance.

Note that the F1 score is not defined if , and the Hausdorff distance is undefined if or . To address this, we include and as trivial change points both in and . This approach is suggested by Van den Burg and Williams (2020). This does not affect the interpretation of the detection results, as change points are considered the start of a new segment.

4.4 Simulation study: change point detection in mean structure

First, we compare the performance of mxPBF_major with Inspect, Geomcp and Edivisive in detecting change points in the mean structure through simulation studies. We set and as the dimensions of the dataset. In “single change” scenarios, the data is generated as follows: and , with the true change point . Under the null hypothesis, , we set . Under the alternative hypothesis, , we set and randomly choose entries in , setting them to , while the remaining entries are set to 0. In “multiple change” scenarios, the data is generated as follows: , , and , with the true change point set . Under the null hypothesis, we set . Under the alternative hypothesis, we set and randomly select entries in and , setting them to , while the remaining entries are set to 0. Here, represents the number of signals involved in a change, and is the magnitude of these signals.

We set , and the following scenarios for the number of signals are considered:

-

1.

(: Rare signals) To consider a scenario with only a few signals, we set .

-

2.

(: Many signals) To consider a scenario with a lot of signals, we set .

Furthermore, we consider the following two structures for the true precision matrix :

-

1.

(Sparse ) We randomly select of entries in and set their value to . The remaining entries in are set to 0. When the resulting is not positive definite, we make it positive definite by adding to .

-

2.

(Dense ) We randomly choose of entries in and set their value to 0.3. The rest of the steps for constructing is the same as above.

Note that the terms “rare” and “many” refer to the number of nonzero entries in under the alternative hypothesis, indicating the number of signals in a change. On the other hand, the terms “sparse” and “dense” refer to the number of nonzero entries in the precision matrix , irrespective of the number of signals.

When applying mxPBF_major, we use a set of window sizes , where the other hyperparameters are selected as described in Section 4.2. The R package hdbcp, which implements mxPBF_major, and the reproduction code for the simulation study are available on GitHub.111GitHub repository: https://github.com/JaeHoonKim98/hdbcp To apply Geomcp, we use the R package changepoint.geo (Grundy, 2020) and changepoint.np (Haynes and Killick, 2016). Since the covariance matrices in the scenarios are not diagonal, we employ the empirical cost function with the number of quantiles set to , as recommended by Grundy et al. (2020) and Haynes et al. (2016). We use the default MBIC penalty (Zhang and Siegmund, 2007) and set both the minimum segmentation parameter and the threshold for the reconciling method to . For the implementation of Edivisive method, we use the R package ecp (James et al., 2013). Following the recommendations of Matteson and James (2014), we set , a significance level of 0.05 and . Additionally, we set the minimum segment size to in line with our assumption. To implement the Inspect method, we use the R package InspectChangepoint (Wang and Samworth, 2016) with the default setting of . Setting implements a Binary Segmentation approach (Scott and Knott, 1974, Vostrikova, 1981) for detecting multiple change points. When setting , as suggested in Wang and Samworth (2018), a Wild Binary Segmentation approach (Fryzlewicz, 2014) is implemented. However, it detected more false positives compared to the default setting. The threshold for identifying change points is determined using the data-driven approach proposed by Wang and Samworth (2018). Since InspectChangepoint does not provide a parameter for setting a minimum segment length during binary segmentation, we include a post-processing step that removes change points with lower CUSUM statistics if the distance between detected points is less than . This process yields the same results as directly setting a minimum segment length parameter. Also, it significantly improves performance by reducing false positives through the elimination of redundant detections.

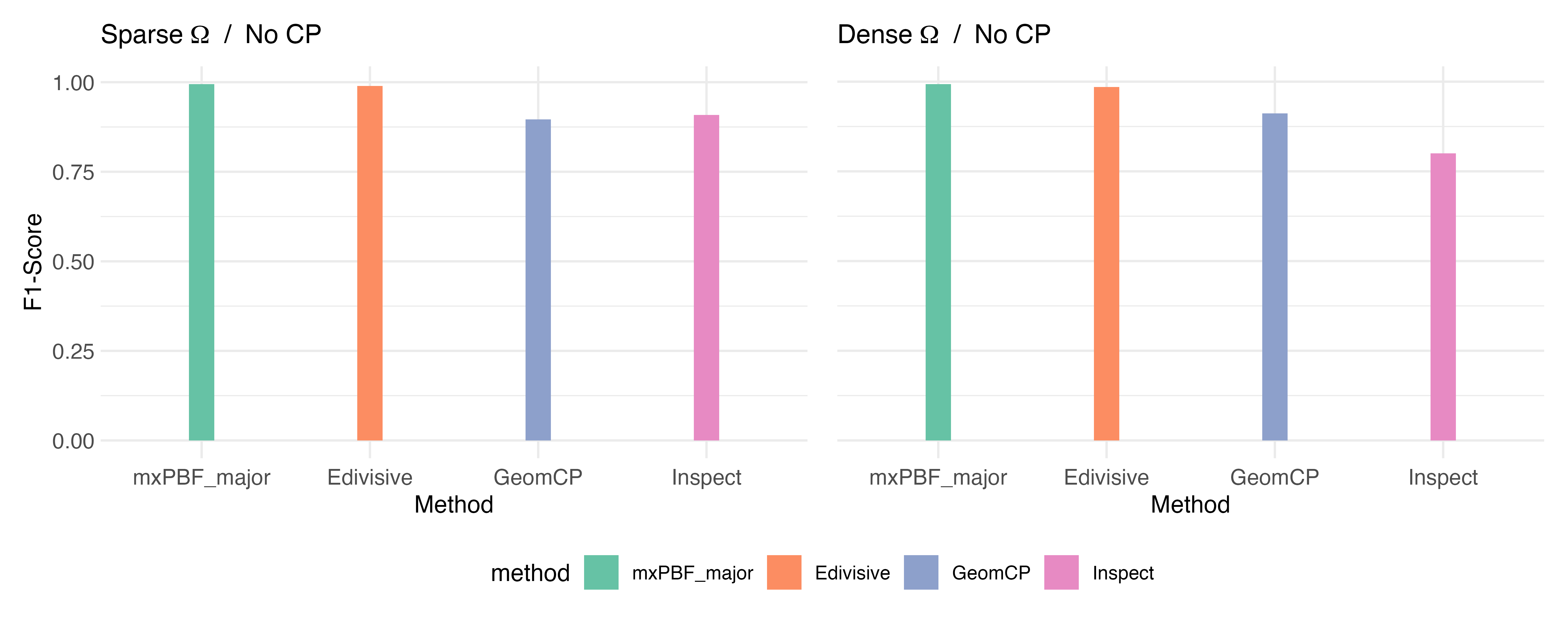

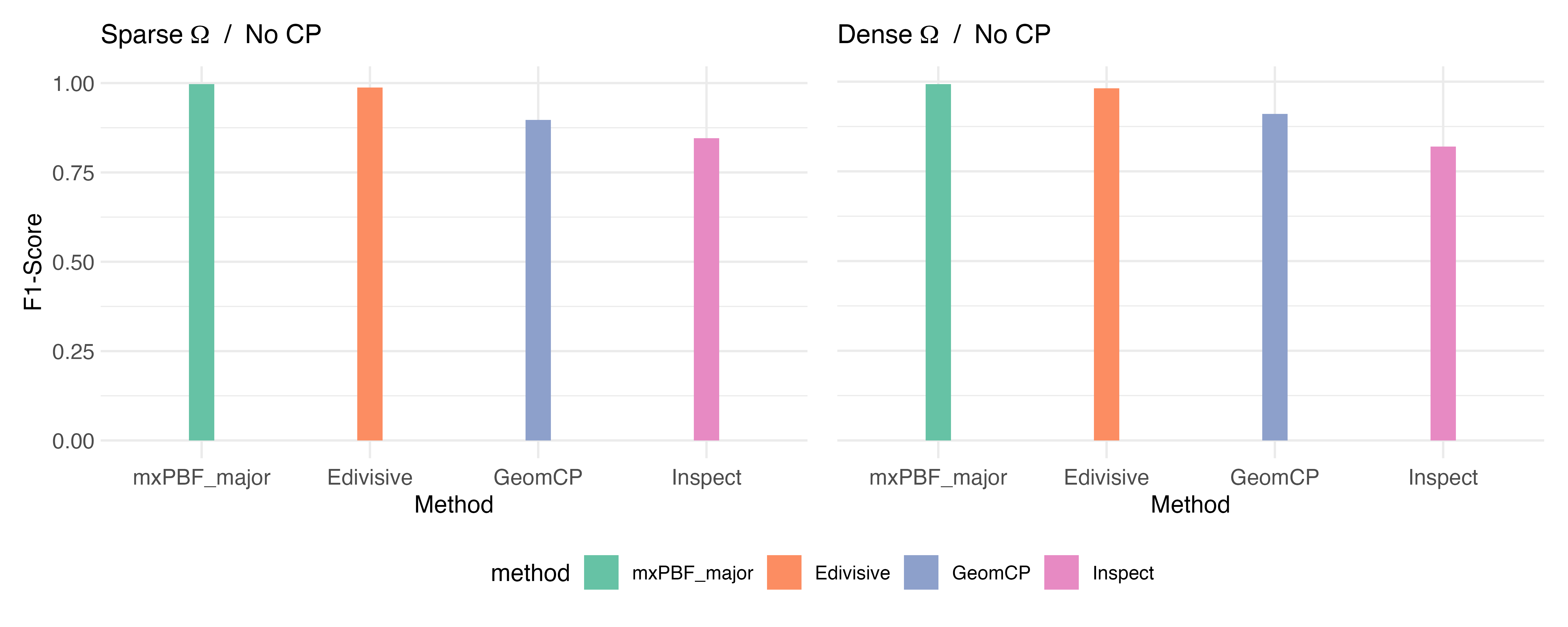

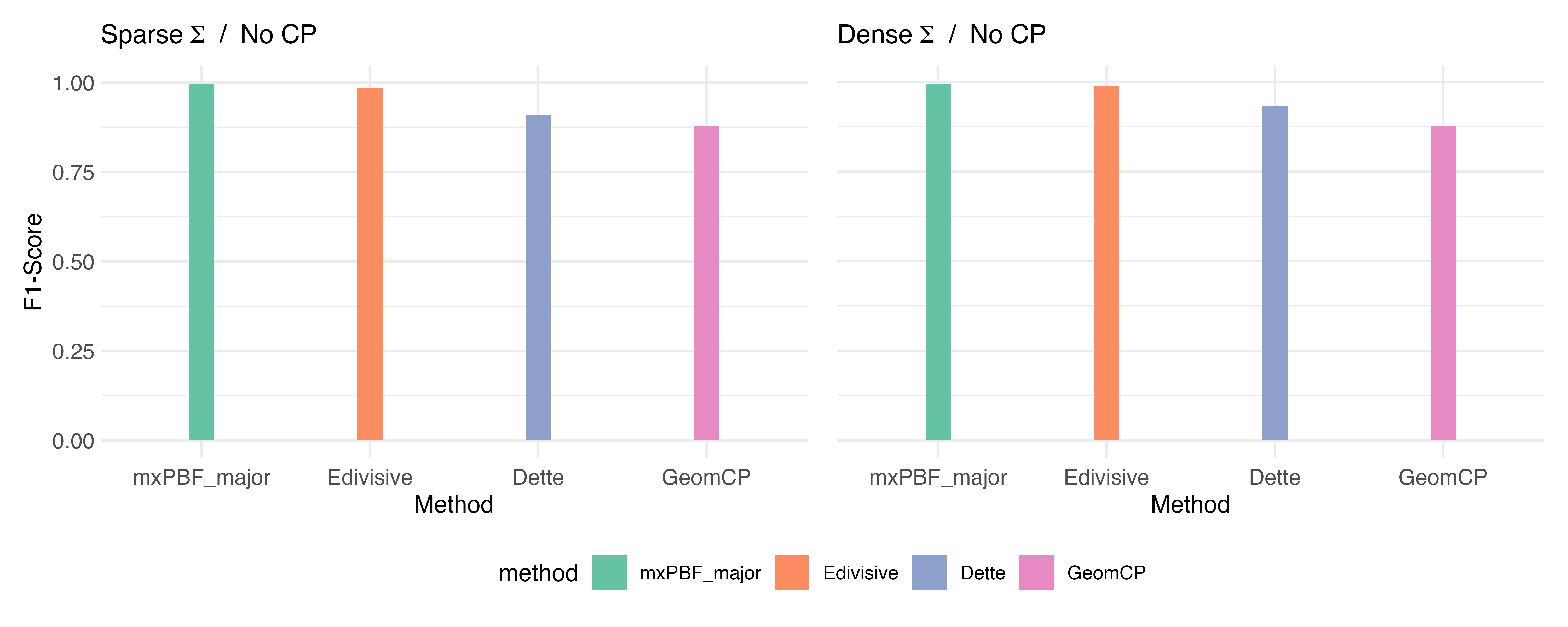

Figure 1 shows the F1 scores for each method, based on 50 simulated datasets under when . In this scenario, where no true change points exist, a higher F1 score indicates better performance in reducing false positives. Among the methods, mxPBF_major and Edivisive exhibit superior performance in this regard.

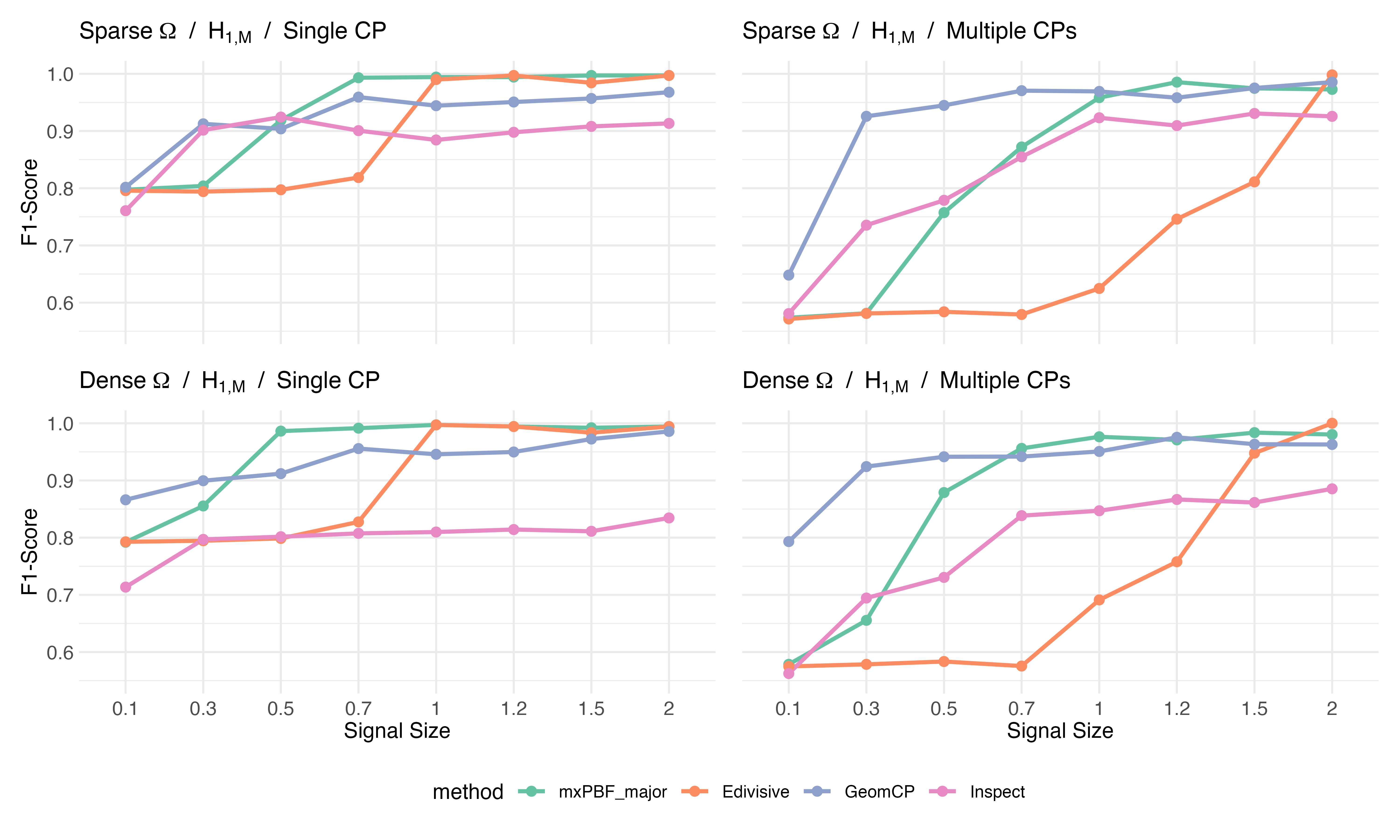

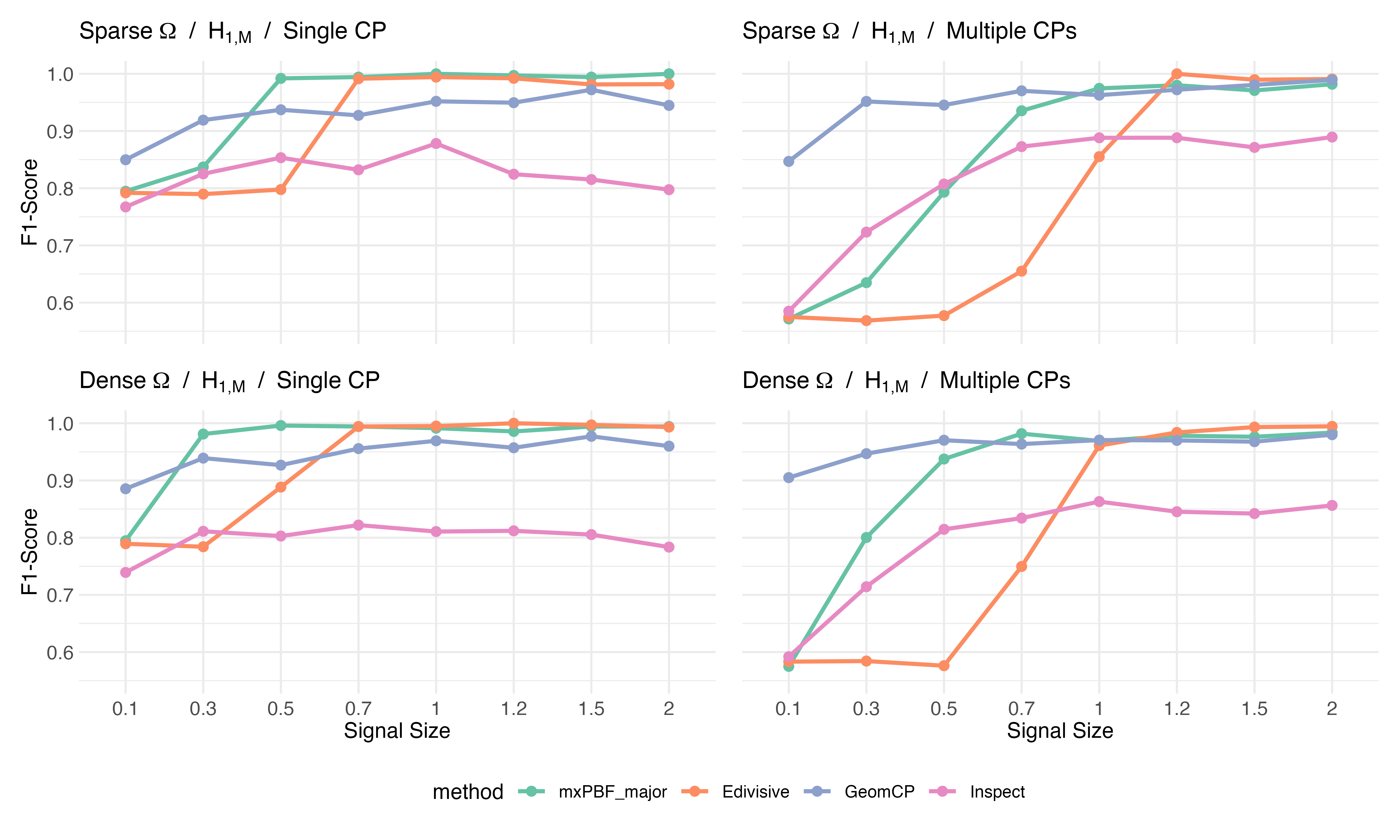

Figure 2 presents the F1 score and Hausdorff distance based on 50 simulated datasets under “rare signals” scenario , with . Under , the difference vector contains only five nonzero elements, each with a signal size of . Note that mxPBF_major demonstrates significant improvement as the signal size increases and outperforms the other methods in most scenarios. Inspect and Geomcp show improved performance as the signal size increases but tends to produce a large number of false positives. Additionally, Inspect performs better in scenarios where is sparse, likely because this method assumes a diagonal structure for . Edivisive appears to struggle in accurately detecting changes, which may stem from the method being more suited to scenarios involving numerous signals.

Figure 3 presents the F1 score and Hausdorff distance based on 50 simulated datasets under “many signals” scenario , with . Under , the difference vector contains nonzero elements, with each element having a signal size of . When signals are small, Inspect and Geomcp show decent performance. However, similar to the rare signals scenario, Inspect appears to detect numerous false positives. When signals are large, mxPBF_major and Edivisive also demonstrate improved performance, achieving results comparable to Geomcp. Notably, the performance of mxPBF_major improves rapidly as the signal size increases.

Since similar results are observed for and , we omit these results for brevity. The detailed results are provided in the supplementary material.

4.5 Simulation study: change point detection in covariance structure

Next, we demonstrate the performance of mxPBF_major, along with Dette, Geomcp and Edivisive, for detecting change points in the covariance structure. Similar to the settings in Section 4.4, we set and as the dimensions of the dataset. In “single change” scenarios, the data is generated as follows: and , with the true change point . Under the null hypothesis, , we set . Under the alternative hypothesis, , we set and , where is a symmetric matrix containing the signals. If or is not positive definite, we add to both matrices to make them positive definite. In “multiple change” scenarios, the data is structured as follows: , , , and , with the true change point set . Under the null hypothesis, we set for all . Under the alternative hypothesis, we set and set and to , with generated independently. Note that the symmetric matrix determines both the number and magnitude of signals under the alternative hypothesis. We set and consider the following two scenarios for generating :

-

1.

(: Rare signals) To consider a scenario with only a few signals, we randomly select five entries in the lower triangular part of and generate their values from . To ensure that is symmetric, the corresponding upper triangular part is assigned the same nonzero values, while the remaining elements are set to 0.

-

2.

(: Many signals) To consider a scenario with a lot of signals, we set , where and . It leads to signals in , except upper triangular part.

Note that is closely related to the magnitude of the signals. Furthermore, we consider the following two settings for the common covariance matrix :

-

1.

(Sparse ) We randomly select of the entries in the lower triangular part of and set their values to . To ensure that is symmetric, the corresponding upper triangular part is assigned the same nonzero values, while the remaining elements are set to 0. We define , where where , and set , where and . This corresponds to Model 3 in Cai et al. (2013).

-

2.

(Dense ) We set , where with , where . This corresponds to Model 4 in Cai et al. (2013).

Similar to the previous case, the terms “rare” and “many” describe the number of nonzero entries in under the alternative hypothesis and, thus, relate to the number of signals. On the other hand, the terms “sparse” and “dense” refer to the number of nonzero entries in the common covariance matrix, , regardless of the number of signals .

Since Dette is a method designed to detect a single change point, it was applied only in the “single change” scenario. When applying Dette, the threshold for dimension reduction is selected based on the resampling approach proposed by Dette et al. (2022). For the other methods, we use the same settings as described in Section 4.4.

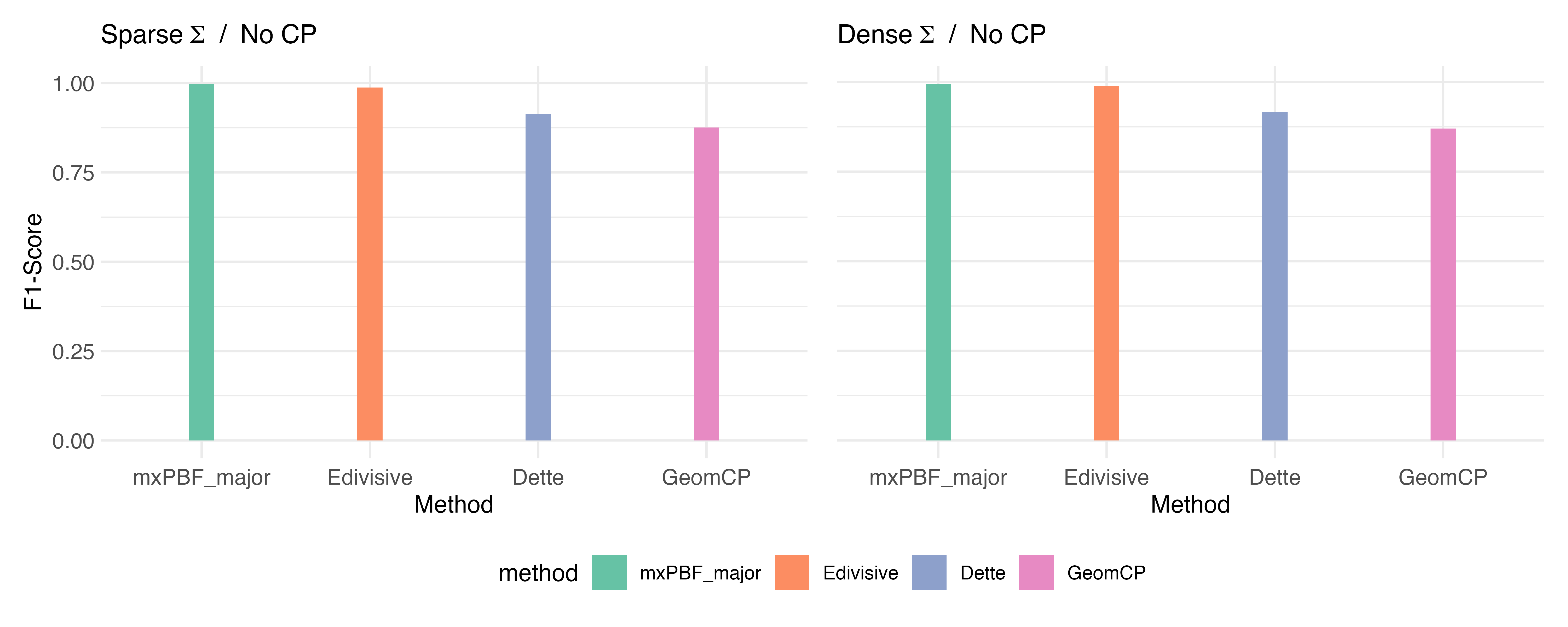

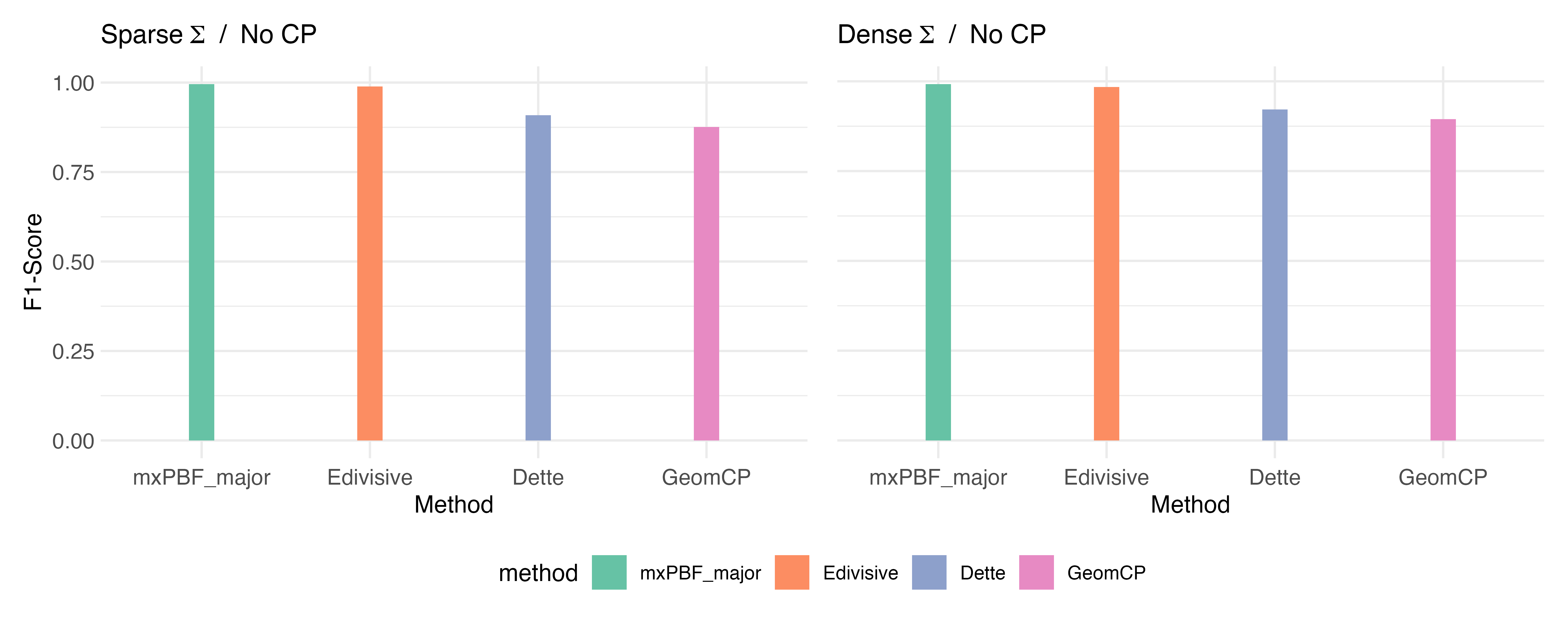

Figure 4 shows the F1 scores for each method, based on 50 simulated datasets under with . Similar to the change point detection results for the mean structure, mxPBF_major and Edivisive outperform other methods,

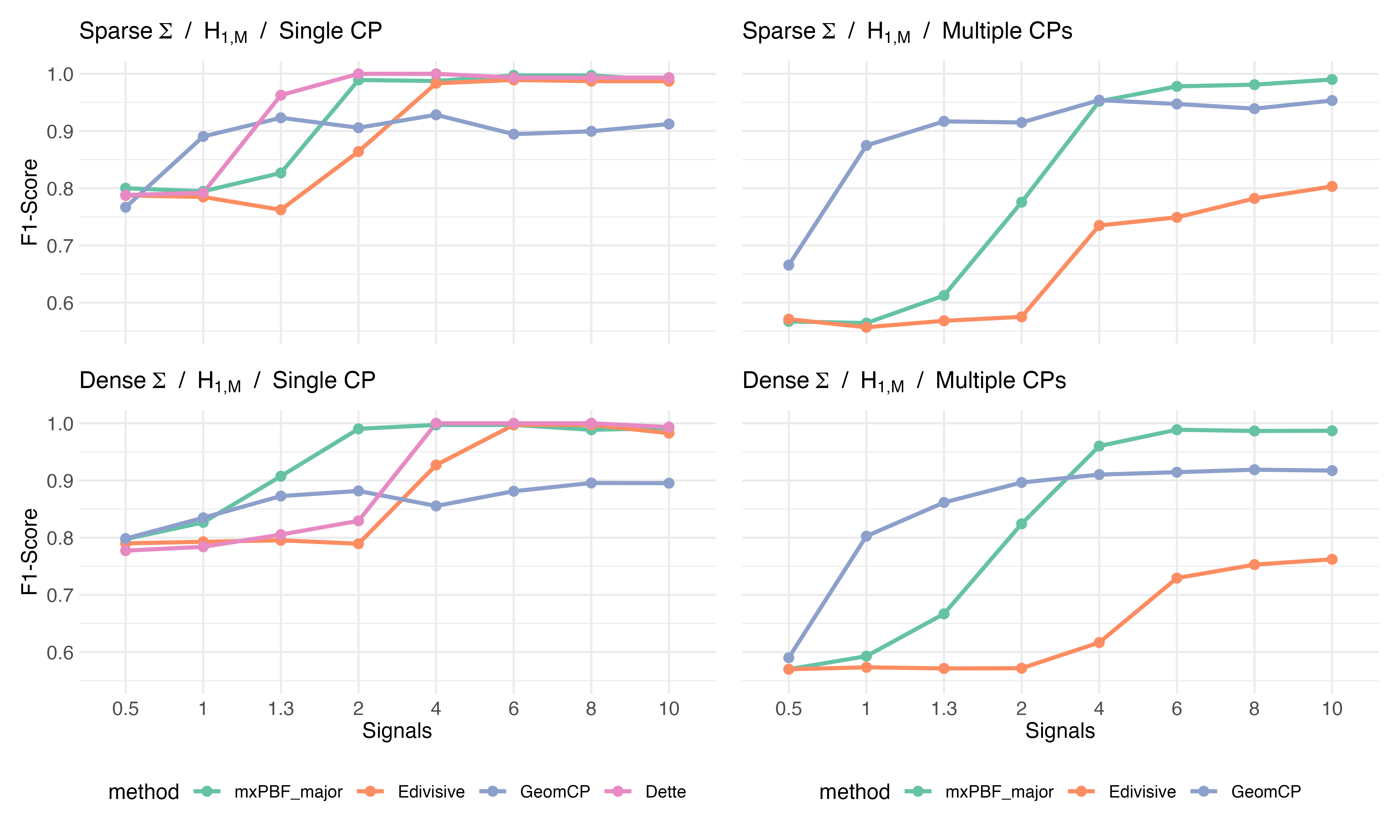

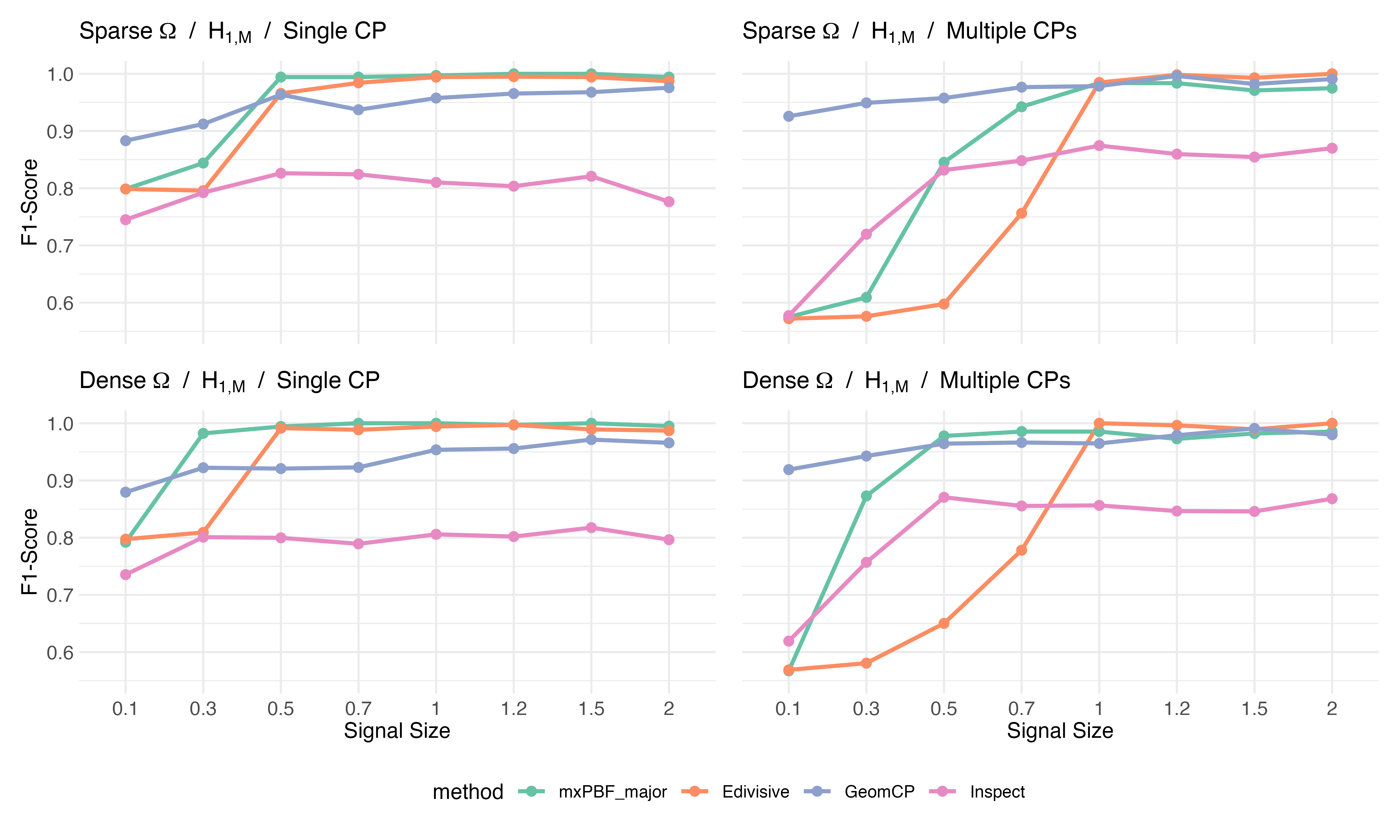

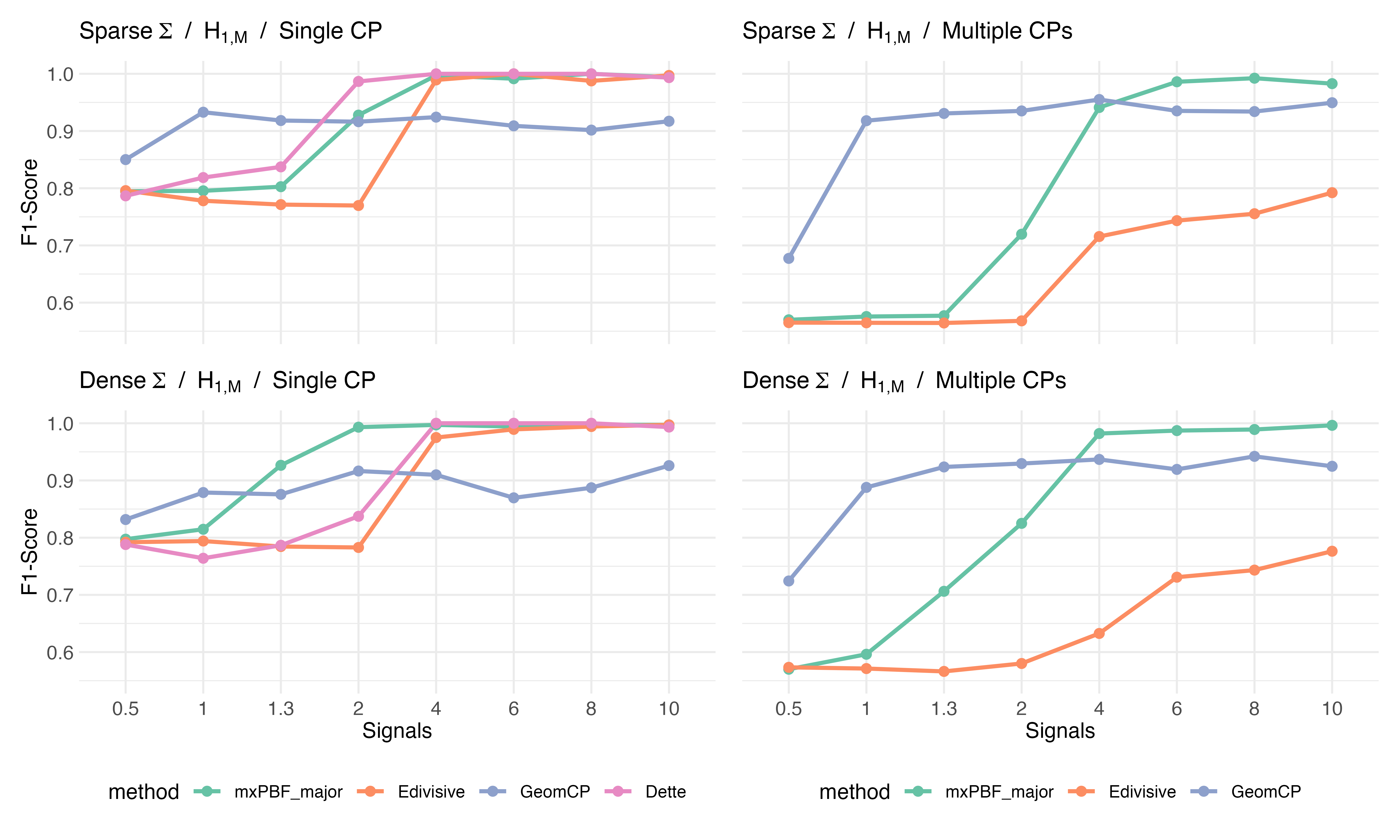

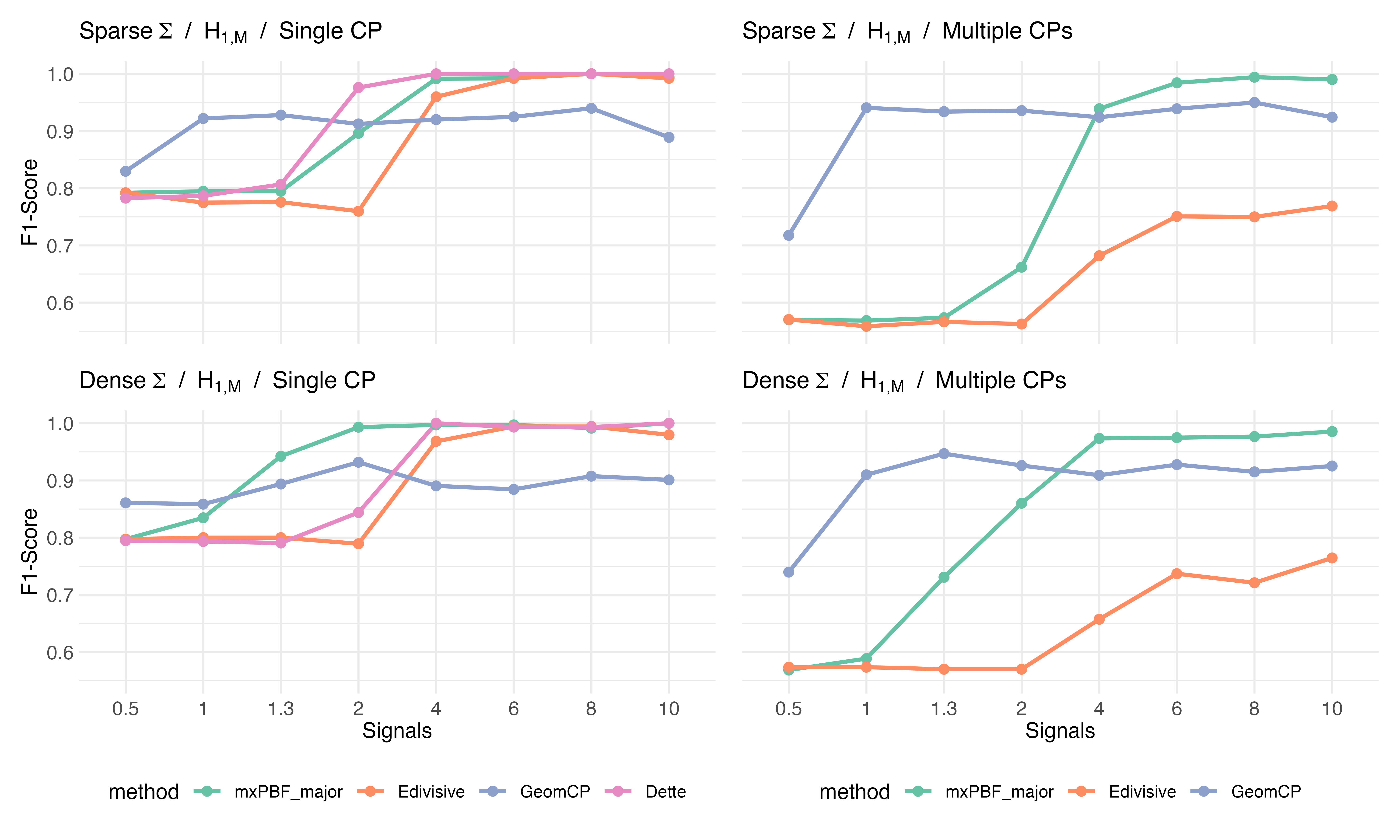

Figure 5 shows F1 score and Hausdorff distance based on 50 simulated datasets under “rare signals” scenario , with . Note that mxPBF_major outperforms the other methods in most scenarios, with its performance steadily improving as the signal size increases. Dette performs well in the sparse covariance scenario but struggles to detect changes when the covariance is dense. Edivisive and Geomcp struggle to detect change points, with their performance showing no improvement as the signal size increases. This may again be due to the fact that they were not designed to detect rare signals.

Figure 6 presents the F1 score and Hausdorff distance based on 50 simulated datasets under “many signals” scenario , with . When signals are small, Geomcp outperforms other methods. However, the improvement in its performance metrics is limited due to numerous false positives. In most settings, mxPBF_major outperforms other methods when signals are large, say . Dette and Edivisive effectively detect the change point in the single change scenario. However, in the multiple changes scenario, Edivisive struggles to accurately detect changes, even when signals are large.

We observe that the experiments for and show similar patterns. Thus, for brevity, the results are provided in the supplementary material.

5 Real data analysis

In this section, we apply the proposed change point detection methods to real datasets. In practice, it is unclear whether changes occur in the mean, covariance or both. To address this issue, we apply both of the proposed change point detection methods sequentially. We first apply the method for detecting change points in the covariance structure. To satisfy the assumption that the mean is a zero vector, we roughly center the observations using a given window size . Specifically, given where and , and a window size , the centered data is defined as , where . Then we apply the change point detection method for covariance matrices. If no changes are detected, we then apply the proposed change point detection method for mean vectors to the original, uncentered dataset. If one or more change points are detected, we divide the data based on the estimated change points. Since each segment is expected to share a common covariance matrix, we apply the proposed change point detection method for mean vectors within each segment. In this case, if some segments are smaller than twice the largest window size we used, we only use the available windows. Finally, we combine the change points detected in both the mean and covariance structures. Note that this process prioritizes changes in covariance matrices over changes in mean vectors.

5.1 Comparative Genomic Hybridization

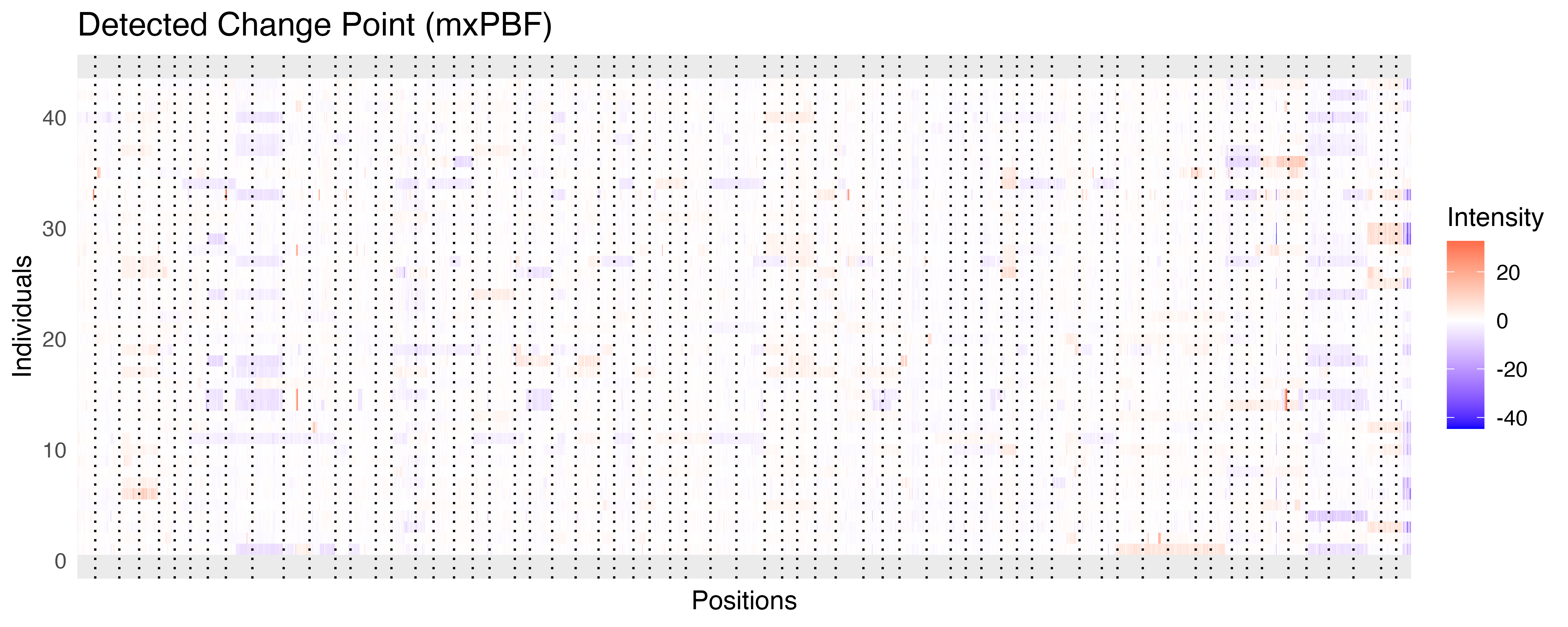

We first examine the comparative genomic hybridization microarray dataset from Bleakley and Vert (2011), which examines DNA copy number variations in individuals with bladder tumors. This technique involves comparing the fluorescence intensity levels of DNA fragments between a test sample and a normal reference sample to detect chromosomal copy number abnormalities. The dataset consists of log-intensity ratio measurements from 43 individuals with bladder tumors, collected at 2,215 positions across the genome. This dataset is available in the R package ecp (Matteson and James, 2014). Following the method described in Grundy et al. (2020), we scale each series using the median absolute deviation prior to applying the detection methods. For Geomcp, we use the CROPS algorithm (Haynes et al., 2017) as suggested in Grundy et al. (2020). For the other parameters, we use the same settings as described before.

As illustrated in Figure 7, mxPBF_major identifies 64 change points, while Inspect and Edivisive detect 59 and 64, respectively. There is a strong overlap among the change points detected by these methods. Within a margin of 15 points, approximately 83% of the change points identified by mxPBF_major match those detected by Inspect, and 86% overlap with those detected by Edivisive. Similarly, about 80% of the change points detected by Inspect and 88% of those detected by Edivisive correspond to those identified by mxPBF_major. Meanwhile, Geomcp detects 48 change points when the number of changes in distance and angle mappings are set to 46 and 42, respectively, based on diagnostic plots. The relatively small number of change points detected by Geomcp can be attributed to its design, which identifies only those changes that appear common across multiple individuals (Grundy et al., 2020). Approximately 85% of the change points detected by Geomcp align with those identified by mxPBF_major, suggesting that mxPBF_major is also capable of detecting these changes. Thus, mxPBF_major effectively detects not only individually specific change points but also those common across multiple individuals.

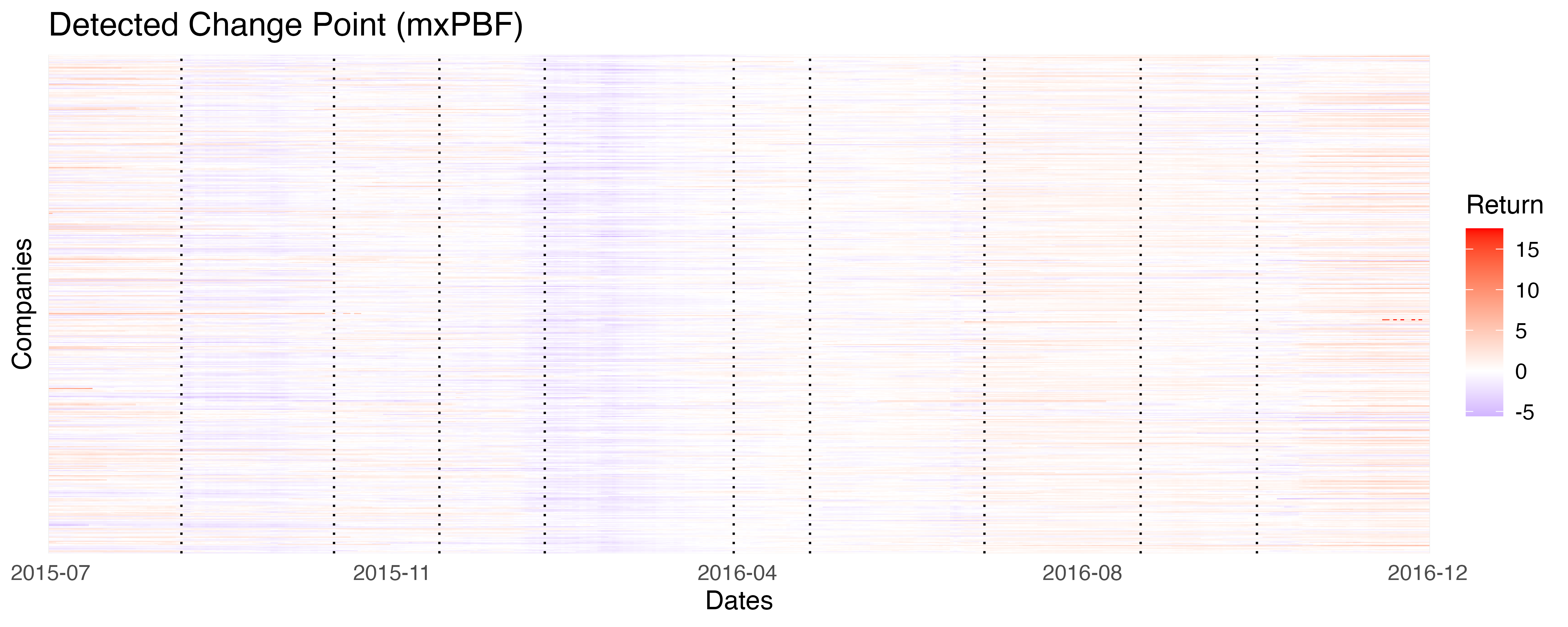

5.2 S&P500 Stock Prices

We now consider the daily log returns of the closing stock prices for companies in the S&P 500 from January 2015 to December 2016. The dataset was loaded using the R package SP500R (Foret, 2019). The initial dataset is a matrix with rows, corresponding to dates, and 500 columns representing companies. First, we remove 21 columns containing missing values, which results in . We then scale each series using the median absolute deviation, following the approach outlined in Grundy et al. (2020). For Geomcp, we use the normal cost function and the CROPS algorithm (Haynes et al., 2017), as suggested in Grundy et al. (2020). For the other parameters, we use the same settings as described previously.

As shown in the figure 8, mxPBF_major identifies 9 change points. These detected change points correspond to events that broadly impacted many companies. For example, the change points in August 2015 and January 2016 align with significant declines in the Chinese stock markets, which affected global markets, including the S&P 500 index. The changepoint in early July 2016 likely corresponds to the announcement and outcome of the British referendum to leave the European Union, while the one in late October reflects the U.S. presidential election. Inspect and Edivisive methods detect 11 and 10 change points, respectively. For Geomcp, we select 13 and 5 as the number of changes in distance and angle mappings, respectively, resulting in a total of 8 final change points. Similar to the result in (5.1), approximately 88% change points detected by Geomcp align with those identified by mxPBF_major within 15 time points. Furthermore, mxPBF_major and Edivisive demonstrate a strong relationship, as all change points detected by both methods overlap.

6 Discussion

In this paper, we proposed Bayesian change point detection methods for high-dimensional mean and covariance structures, building upon the mxPBF framework (Lee et al., 2024). We established the consistency of mxPBF and derived localization rates for the proposed methods under conditions that are either weaker or comparable to those required by existing approaches. Through extensive evaluations, the proposed methods demonstrated superior performance across a broad range of scenarios, outperforming current state-of-the-art techniques.

Several promising directions for future research emerge from this work. The first avenue involves enhancing the computational efficiency of the proposed methods. The primary bottleneck lies in selecting the hyperparameter which controls the empirical false positive rate. This process necessitates generating a large number of datasets and calculating mxPBF for each, significantly increasing the computational cost. To address this challenge, a possible solution is to calculate all pairwise Bayes factors (PBFs) for a given , retaining only those variables (or pairs of variables, in the case of covariance matrices) with “relatively large” PBF values. For example, the top 10% quantile could serve as the threshold for identifying these values. Since this approach relies on relative magnitudes of the PBFs, can initially be fixed arbitrarily. Subsequently, the false positive rate-based method can be applied to this reduced dataset to fine-tune , significantly alleviating the computational burden.

A second direction for future work is to develop adaptive change point detection methods capable of detecting both large changes in a few entries and small changes distributed across many entries. The current methods rely on mxPBF, a maximum-type Bayes factor, which may encounter difficulties in identifying change points involving numerous small-magnitude signals. Designing a Bayes factor capable of aggregating small changes across multiple components could address this limitation. By integrating such an aggregation-based approach with mxPBF, a more robust change point detection method could be developed, effectively detecting both prominent changes in a few components and subtle changes spread across many components.

Acknowledgements

We would like to thank Dr. Qing Yang for providing the MATLAB code to implement their method.

Appendix A Additional numerical results

A.1 Change point detection in mean structure

In this section, we present additional simulation results for change point detection in the mean structure. Recall that mxPBF_major, Geomcp, Inspect, and Edivisive refer to our multiscale method and those from Grundy et al. (2020), Wang and Samworth (2018), and Matteson and James (2014), respectively.

Figure 9 shows the F1 scores for each method, based on 50 simulated datasets under with and . Among the methods, mxPBF_major and Edivisive demonstrate superior performance, consistent with the results observed when .

Figures 10 and 11 describe the suggested metrics (F1 score and Hausdorff distance) based on 50 simulated datasets under “rare signals” scenario , with and , respectively. The results show similar trends to those observed when . mxPBF_major demonstrates significant improvement as the signal size increases and outperforms the other methods in most scenarios. Inspect and Geomcp show improved performance as the signal size increases but tends to produce a large number of false positives, and Edivisive appears to struggle in accurately detecting changes.

Figures 12 and 13 present the suggested metrics based on 50 simulated datasets under “many signals” scenario , with and , respectively. The results show similar trends to those observed when . When signals are small, Inspect and Geomcp show decent performance, but mxPBF_major and Edivisive also demonstrate improved performance when signals are large. Notably, the performance of mxPBF_major improves rapidly as the signal size increases.

A.2 Change point detection in covariance structure

Next, we present additional numerical results for change point detection in the covariance structure. Recall that mxPBF_major, Dette, Geomcp, and Edivisive refer to our multiscale method and those from Dette et al. (2022), Grundy et al. (2020), and Matteson and James (2014), respectively.

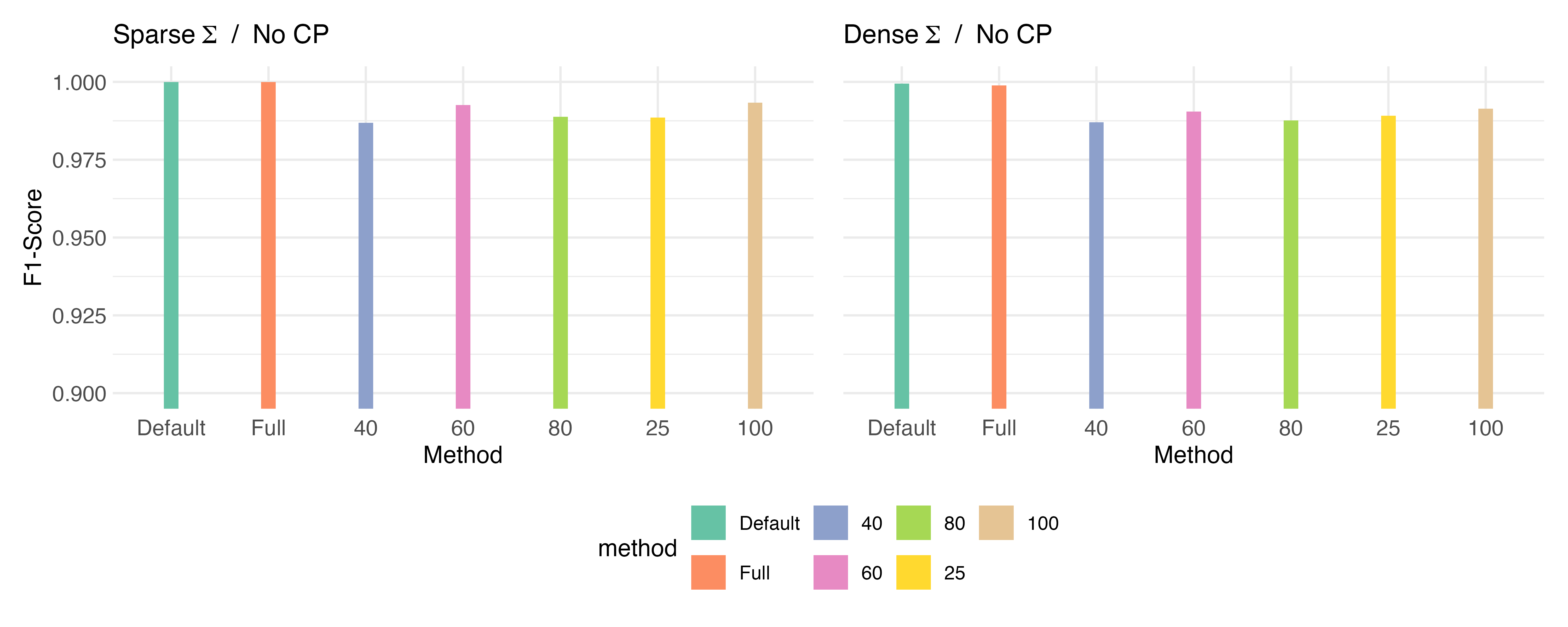

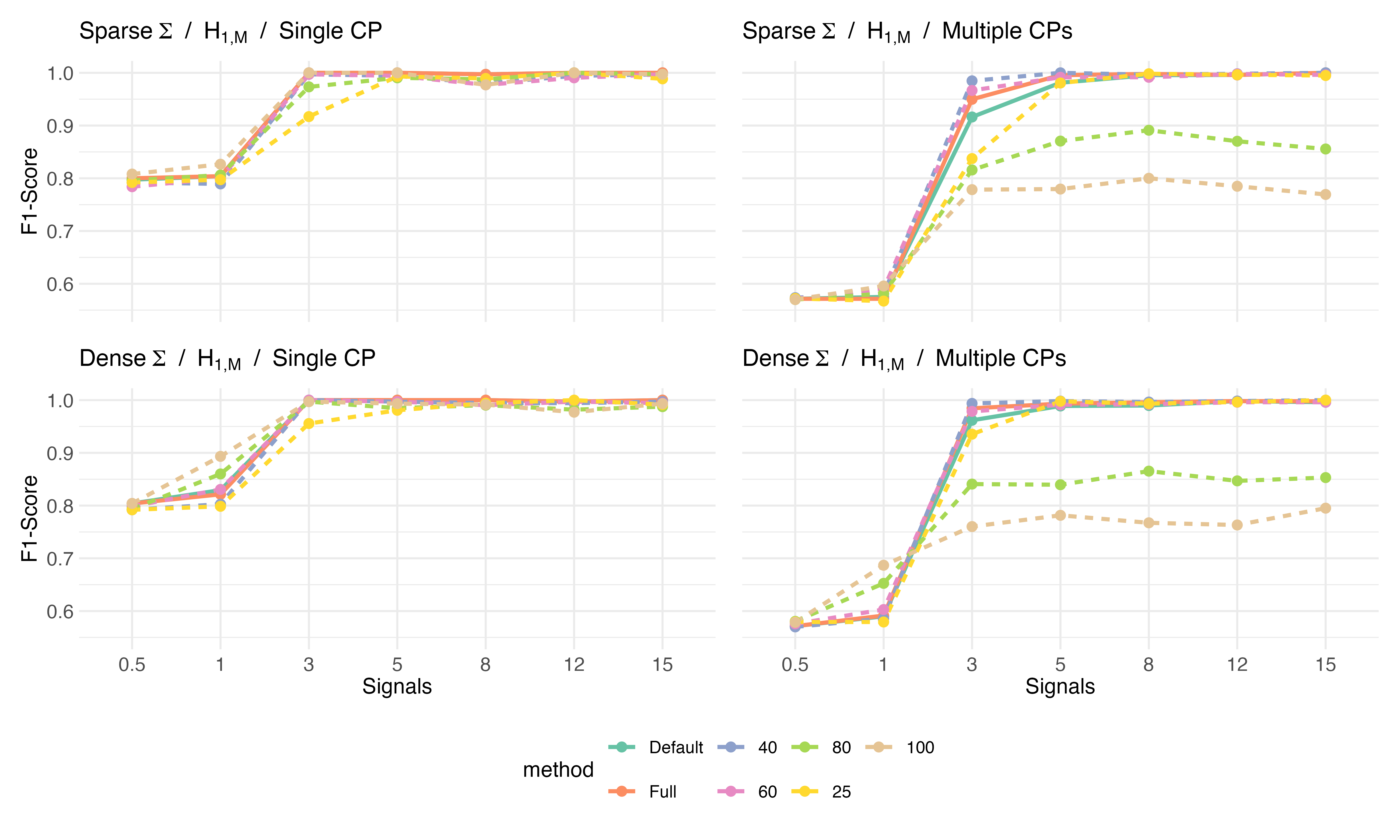

Figure 14 shows the F1 scores for each method, based on 50 simulated datasets under , with and . Similar to the result observed when , mxPBF_major and Edivisive demonstrate superior performance in avoiding false positives.

Figures 15 and 16 display the suggested metrics based on 50 simulated datasets under “rare signals” scenario , with and , respectively. Similar to the case when , Edivisive and Geomcp struggle to detect change points, showing no improvement in performance as the signal size increases. Dette performs well in the sparse covariance scenario but struggles to detect changes when the covariance is dense. Conversely, mxPBF_major outperforms the other methods in most cases, with its performance consistently improving as the signal size grows.

Figures 17 and 18 display the metrics derived from 50 simulated datasets under “many signals” scenario , with and , respectively. The results show similar trends to those observed when . In scenarios with many signals, all methods show improved performance, likely due to the increasing number of signals with higher dimensions. In scenarios with smaller signals, Geomcp outperforms the other methods. However, its performance gains are limited by the detection of numerous false positives. In the single change point scenario, mxPBF_major, Dette and Edivisive effectively detect changes. In the multiple change point scenario, Edivisive struggles to detect changes accurately, even with larger signals, while mxPBF_major performs nearly perfectly when .

Appendix B FPR-based method for selecting

In this section, we describe the false positive rate (FPR)-based method for selecting the hyperparameter of mxPBF. Given an observed data matrix , let and represent the sample mean and covariance matrix derived from , respectively. If is not positive definite, we make it positive definite by adding . We then generate a simulated dataset , where each is a random sample from . Note that can be considered a dataset simulated under the null hypothesis, with its mean vector and covariance matrix approximating those of the true data-generating distribution. For given a window size and a hyperparameter , we calculate the mxPBF based on , denoted as , and reject the null if the mxPBF exceeds the threshold . Note that can be either or , and an mxPBF exceeding the threshold corresponds to a false positive. By generating simulated datasets , we can calculate the following empirical FPR for each ,

We recommend setting the number of generations between 300 and 500 in practice. An experiment supporting this suggestion is described in Section B.1.

Note that, after calculating the mxPBF for a given , the mxPBF for a different can be easily computed as

where and . By forming a grid of values, such as , we can select the optimal value of , denoted , that achieves a prespecified FPR.

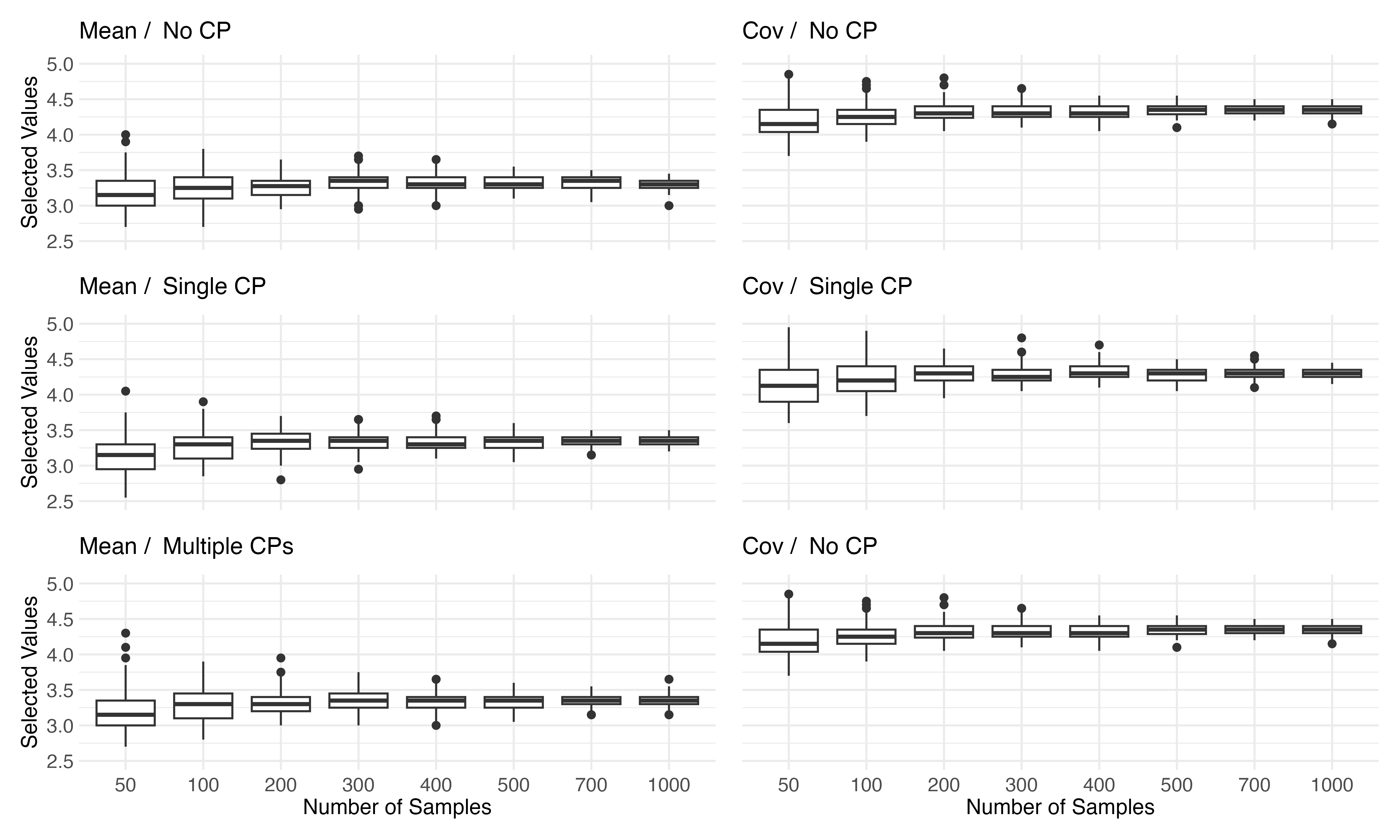

B.1 Sufficient number of simulated datasets

In this section, we provide empirical evidence to recommend a sufficient number of simulated datasets, , for the stable selection of the hyperparameter , which controls the empirical false positive rate. Since we generate simulated datasets using the sample mean and covariance, and select based on their quantiles, it is expected that generating more simulated datasets will lead to a more stable selection of . However, generating too many simulated datasets would require heavy computation. Therefore, we aim to find a proper range for generating samples that not only achieves stability in selecting , but is also computationally practical. Here, we design an experiment to empirically determine the sufficient range.

For simplicity, we fix and , consider many signals and a dense precision or covariance matrix, and set and under the alternative hypotheses for the mean and covariance structure. Additionally, we use a window size of and explore a wide range for the number of simulated datasets, . For each dataset and number of simulated datasets , we repeated the selection of 100 times. For other settings, we used those described in the paper.

Figure 19 presents the distribution of the selected , controlling the empirical false positive rate at 0.05 in each case. With a smaller number of generations, the selected appears unstable, exhibiting a wide range. However, once the number of generations reaches 200 or 300, it appears to stabilize. When , the range does not appear to become significantly narrower. In every scenario, a similar distribution of the selected is observed, which suggests that more than generations are generally sufficient.

Appendix C The multiscale method

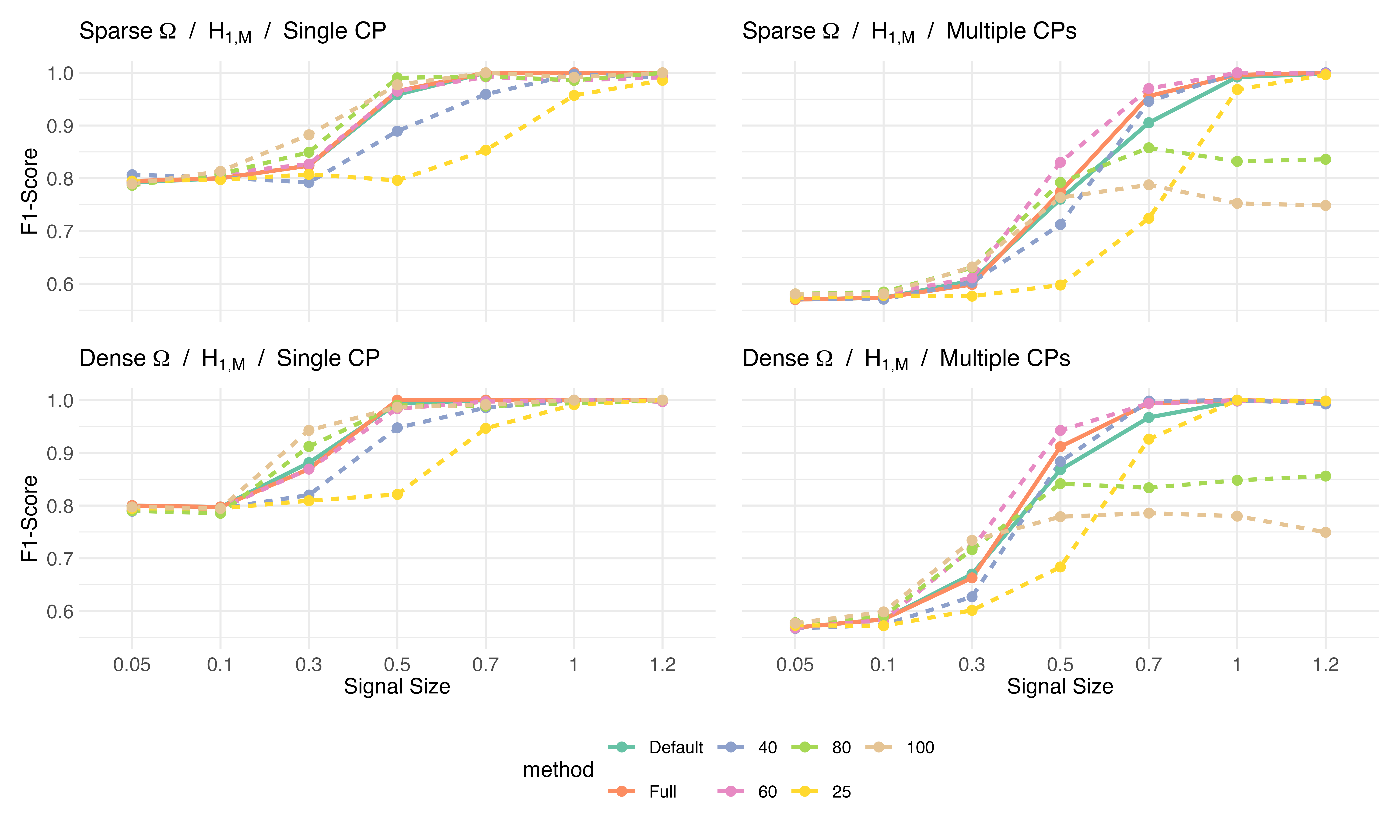

In this section, we compare the performance of the proposed methods using various window settings, including both single and multiple windows, to highlight the advantages of the multiscale approach. As explained in the paper, the proposed method requires careful selection of the window size, which can be challenging in many cases. We aim to demonstrate the impact of selecting an inappropriate window size and the effectiveness of the multiscale method. For simplicity, we fix and , considering only F1 scores. We compared the performance of five proposed methods using different single windows against two versions of mxPBF_major that utilize five and three windows, respectively. For mxPBF_major with five windows, we use a set of window sizes and denote this method as Full. For mxPBF_major with three windows, we use a set of window sizes and refer to this method as Default. For the methods using a single window, we use , respectively, denoting these methods by their window sizes. Unless indicated otherwise, we use the same settings described in the paper.

C.1 Performance of single window methods in the mean structure

First, we compare the performance in detecting changes in the mean structure. We consider signal sizes of .

Figure 20 shows the F1 scores for each method, based on 50 simulated datasets under with . Among the single-window methods, larger windows tend to detect more false positives. Both the Default and Full perform well in this regard, outperforming the single-window methods.

Figure 21 presents the F1 scores based on 50 simulated datasets under “rare signals” scenario , with . Within the single-window methods, window size 25 demonstrates inferior performance in most scenarios, indicating that it is insufficient for capturing signals. Additionally, window size 100 struggles to identify all changes in scenarios with multiple change points, as it fails to detect subsequent change points. In this regard, it can be said that window size 25 is suboptimal in most scenarios, particularly those with weak signals, while window size 100 is unsuitable for scenarios with multiple change points. Meanwhile, window sizes 40, 60, and 80 demonstrate decent overall performance, making them suitable options. Thus, Default and Full can be viewed as using one inappropriate window in single change scenarios and two in multiple change scenarios out of three and five windows, respectively. However, in most scenarios, both Full and Default demonstrate comparable performance to the appropriate window sizes. Additionally, Full slightly outperforms Default in multiple change point scenarios.

Figure 22 presents the F1 scores based on 50 simulated datasets “many signals” scenario , with . In this setting, window size 25 does not appear to be suboptimal for . Additionally, in multiple change point scenarios, window sizes 80 and 100 struggle to identify all changes. This suggests that the optimal window size depends on both the number and magnitude of the signals. In these scenarios, Full uses one inappropriate window in single-change scenarios where , two in multiple-change scenarios where , and three in multiple-change scenarios where , out of five windows. Similarly, Default uses one inappropriate window in both single-change scenarios where and multiple-change scenarios where , and two in multiple-change scenarios where , out of three windows. However, similar to the “rare signals” scenarios, both Full and Default show robust performance, with Full performing slightly better in multiple change point scenarios.

C.2 Performance of single window methods in the covariance structure

Next, we compare the performance in detecting changes in the covariance structure. We consider signal sizes of .

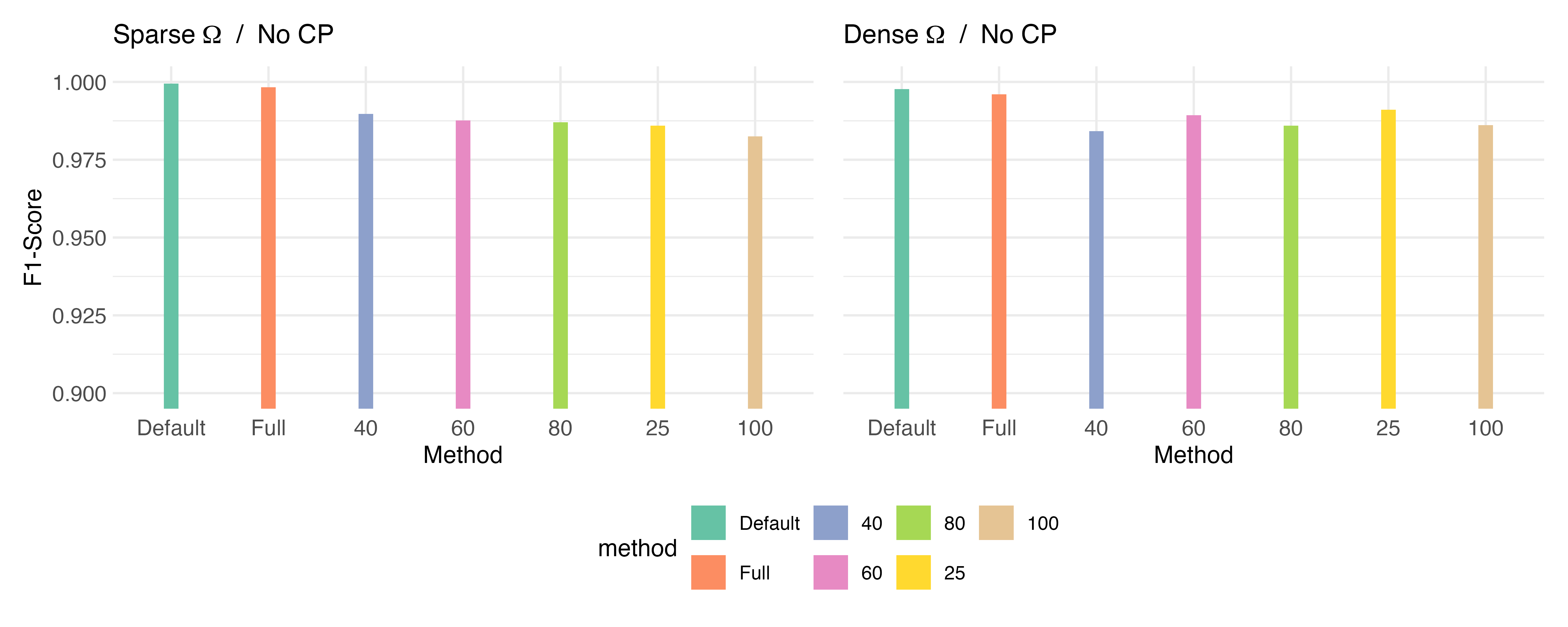

Figure 23 shows the F1 scores for each method, based on 50 simulated datasets under with . Similar to the results in mean change scenarios, both the Default and Full models outperform the single-window methods.

Figure 24 presents the F1 scores based on 50 simulated datasets under , with . Consistent with the findings from previous results, Full and Default models demonstrate robust performance in most settings. Window size 25 appears suboptimal in most scenarios, particularly those with weak signals, while window sizes 80 and 100 are unsuitable for multiple change scenarios.

Figure 25 shows the F1 scores based on 50 simulated datasets under , with . Full and Default show stable performance in most settings. In line with the previous results, window size 25 does not seem to be suboptimal for , whereas window sizes 80 and 100 struggle to identify all changes in multiple change point scenarios.

Appendix D Proofs of main results

D.1 Proofs of theorems in Section 2

-

Proof of Theorem 2.1

Suppose is true. Then,

for some constant and , where the last inequality holds by the proof of Theorem 2.1 in Lee et al. (2024) (Supplementary material, p.11). Since , it completes the proof under the null .

Suppose is true, then there exist change points . Let the indices and satisfy conditions (8) and . Then, again by the proof of Theorem 2.1 in Lee et al. (2024) (Supplementary material, p.12),

for some constant . It gives the desired result.

-

Proof of Theorem 2.2

Define

where are the true change points. Then if

and

for all , it implies that and by the definitions of . Thus, the proof is completed if we show that

as .

By the proof of Theorem 2.1,

for some constant , and

for some constant . Since we assume that and for some constant , it completes the proof.

-

Proof of Theorem 2.3

We closely follow the proof of Proposition 3 in Wang and Samworth (2018). Suppose . Let and correspond to and , respectively, and and . Then, and we have

Thus, if we show , it will complete the proof.

Note that

(17) where is the total variation between and . The last inequality holds because

Furthermore, for the Kullback-Leibler divergence ,

(18) where the inequality follows from Pollard (2002) (p. 62) and the first equality holds due to the Kullback-Leibler divergence between two multivariate normal distributions.

By applying (18) to (17), we have

which is the desired result.

D.2 Proofs of theorems in Section 3

-

Proof of Theorem 3.1

Suppose is true. Then,

for some constant such that , where the last inequality follows from the proof of Theorem 3.1 in Lee et al. (2024) (Supplementary material, p.19-20). The last term converges to 1 because the assumption . It completes the proof under the null because we assume .

Suppose is true, then there exist change points . Let the index and pair satisfy and condition (A3) or (A3⋆). Then, we have

for some constant , where if condition (A3) is met, or if condition (A3⋆) is met. Note that the last inequality follows from the proof of Theorem 3.1 in Lee et al. (2024) (Supplementary material, p.21-22 and p.24). It gives the desired result.

-

Proof of Theorem 3.2

Let be the true change points, and for . Then if

and

for all , it implies that and . Thus, it suffices to show that

as .

Note that

for some constant such that , by the proof of Theorem 3.1 Furthermore,

for some constant , by the proof of Theorem 3.1. It gives the desired result.

-

Proof of Theorem 3.3

We follow closely the line of the proof of Lemma 3 in Wang et al. (2021). Suppose that and , for some constant . For a given and , let , where is a unit vector with . Let be the joint distribution of random samples , where

and be the joint distribution of random samples , where

Define mixture distributions for and . Since and

provided that , it implies . If we denote as the change point in the joint distribution , we have , and . By Le Cam’s Lemma (See Lemma 1 of Yu (1997)),

where and is the joint density function corresponding to . If we show that , it completes the proof.

Consider a rescaled covariance . Let be the joint distribution of random samples , where

and be the joint distribution of random samples , where

Define mixture distributions for and . Since , it suffices to show that .

Let and be the joint distributions of and , respectively. Define the mixture distribution . Note that , where

and the inequality follows from the Jensen’s inequality. By Lemma 5.1 in Berthet and Rigollet (2013), we have

Thus,

because we choose for some constant , where the first inequality holds for all large . It implies that , which gives the desired result.

-

Proof of Theorem 3.4

We follow closely the line of the proof of Lemma 4 in Wang et al. (2021). Suppose that and . Similar to the proof of Theorem 3.3, let be the joint distribution of

and be the joint distribution of

for some . Then and . By Le Cam’s Lemma,

By the same arguments used in the proof of Theorem 3.3, we have

where and are joint distributions of and , respectively. Note that

where the last inequality follows from Lemma 15 in Wang et al. (2021). If we take , it gives

References

- (1)

- Avanesov and Buzun (2018) Avanesov, V. and Buzun, N. (2018). Change-point detection in high-dimensional covariance structure, Electronic Journal of Statistics 12(2): 3254–3294.

- Berthet and Rigollet (2013) Berthet, Q. and Rigollet, P. (2013). Optimal detection of sparse principal components in high dimension, The Annals of Statistics 41(4): 1780–1815.

- Bleakley and Vert (2011) Bleakley, K. and Vert, J.-P. (2011). The group fused lasso for multiple change-point detection, arXiv preprint arXiv:1106.4199 .

- Cai et al. (2013) Cai, T., Liu, W. and Xia, Y. (2013). Two-sample covariance matrix testing and support recovery in high-dimensional and sparse settings, Journal of the American Statistical Association 108(501): 265–277.

- Dette et al. (2022) Dette, H., Pan, G. and Yang, Q. (2022). Estimating a change point in a sequence of very high-dimensional covariance matrices, Journal of the American Statistical Association 117(537): 444–454.

- Enikeeva and Harchaoui (2019) Enikeeva, F. and Harchaoui, Z. (2019). High-dimensional change-point detection under sparse alternatives, The Annals of Statistics 47(4): 2051–2079.

- Foret (2019) Foret, P. (2019). Sp500r: Easy loading of sp500 stocks data. Github R package version 0.1.0.

- Fryzlewicz (2014) Fryzlewicz, P. (2014). Wild binary segmentation for multiple change-point detection, The Annals of Statistics 42(6).

- Grundy (2020) Grundy, T. (2020). Changepoint.geo: Geometrically inspired multivariate changepoint detection, CRAN: Contributed Packages .

- Grundy et al. (2020) Grundy, T., Killick, R. and Mihaylov, G. (2020). High-dimensional changepoint detection via a geometrically inspired mapping, Statistics and Computing 30(4): 1155–1166.

- Haynes et al. (2017) Haynes, K., Eckley, I. A. and Fearnhead, P. (2017). Computationally efficient changepoint detection for a range of penalties, Journal of Computational and Graphical Statistics 26(1): 134–143.

- Haynes et al. (2016) Haynes, K., Fearnhead, P. and Eckley, I. A. (2016). A computationally efficient nonparametric approach for changepoint detection, Statistics and Computing 27(5): 1293–1305.

- Haynes and Killick (2016) Haynes, K. and Killick, R. (2016). Changepoint.np: Methods for nonparametric changepoint detection, CRAN: Contributed Packages .

- James et al. (2013) James, N. A., Zhang, W. and Matteson, D. S. (2013). Ecp: Non-parametric multiple change-point analysis of multivariate data, CRAN: Contributed Packages .

- Lee et al. (2021) Lee, K., Lin, L. and Dunson, D. (2021). Maximum pairwise Bayes factors for covariance structure testing, Electronic Journal of Statistics 15(2): 4384 – 4419.

- Lee et al. (2024) Lee, K., You, K. and Lin, L. (2024). Bayesian optimal two-sample tests for high-dimensional gaussian populations, Bayesian Analysis 19(3): 869–893.

- Matteson and James (2014) Matteson, D. S. and James, N. A. (2014). A nonparametric approach for multiple change point analysis of multivariate data, Journal of the American Statistical Association 109(505): 334–345.

- Pollard (2002) Pollard, D. (2002). A user’s guide to measure theoretic probability, number 8, Cambridge University Press.

- Scott and Knott (1974) Scott, A. J. and Knott, M. (1974). A cluster analysis method for grouping means in the analysis of variance, Biometrics 30(3): 507.

- Van den Burg and Williams (2020) Van den Burg, G. J. and Williams, C. K. (2020). An evaluation of change point detection algorithms, arXiv preprint arXiv:2003.06222 .

- Vostrikova (1981) Vostrikova, L. J. (1981). Detecting “disorder” in multidimensional random processes., Soviet Mathematics Doklady 24: 55–59.

- Wang et al. (2021) Wang, D., Yu, Y. and Rinaldo, A. (2021). Optimal covariance change point localization in high dimensions, Bernoulli 27(1): 554–575.

- Wang and Samworth (2016) Wang, T. and Samworth, R. J. (2016). Inspectchangepoint: High-dimensional changepoint estimation via sparse projection, CRAN: Contributed Packages .

- Wang and Samworth (2018) Wang, T. and Samworth, R. J. (2018). High dimensional change point estimation via sparse projection, Journal of the Royal Statistical Society: Series B (Statistical Methodology) 80(1): 57–83.

- Yu (1997) Yu, B. (1997). Assouad, fano, and le cam, Festschrift for Lucien Le Cam, Springer, pp. 423–435.

- Zhang and Siegmund (2007) Zhang, N. R. and Siegmund, D. O. (2007). A modified bayes information criterion with applications to the analysis of comparative genomic hybridization data, Biometrics 63(1): 22–32.