The Stochastic Bessel operator at high temperatures

Abstract

We know from Ramírez and Rider [12] that the hard edge of the spectrum of the -Laguerre ensemble converges, in the high-dimensional limit, to the bottom of the spectrum of the stochastic Bessel operator. Using stochastic analysis techniques, we show that, in the high temperatures limit, the rescaled eigenvalues point process of the stochastic Bessel operator converges to a limiting point process characterized with coupled stochastic differential equations.

keywords:

Stochastic Bessel operator; Beta-Laguerre ensembleHugo Magaldi

1 Context and motivation

Coulomb gases, also known as -ensembles, are probability measures on sets of points. In statistical physics, these points are seen as elementary particles on the real line confined under a random potential while repelling each other. The Dyson parameter acts as an inverse temperature and can affect the shape of the potential and the strength of the repulsive force. When is close to , the system becomes ordered due to high repulsion between the particles. Conversely, when is close to , weak repulsion leads to a disordered system. In recent years, -ensembles and their connections to stochastic operators have attracted significant interest (see [5], [6], [8], [13], [1], [2], [14], [16], [17], [18]).

The size -Laguerre ensemble is a two-parameter family of distributions on with density function with respect to the Lebesgue measure

| (1) |

The parameters satisfy and , and is an explicitely computable normalizing constant. When (resp. , ), is the density of the eigenvalues of a real (resp. complex, unitary) Wishart matrix of size . This connection to random matrices was extended to any by Dimitriu and Edelman [5, Theorem 3.4], adapting earlier work from Silverstein [15]. They found a set of bidiagonal random matrices of size such that is the density of the eigenvalues of .

When tends to infinity, the rescaled empirical measure of the eigenvalues converges weakly a.s. to the Marchenko-Pastur distribution:

We refer to [7] for a review of the asymptotic global statistics of classical -ensembles.

Because of the positivity constraint for the eigenvalues of , is called a hard edge for the -Laguerre ensemble. To study local statistics at the hard edge in the high-dimensional limit, Ramírez and Rider [12] introduced a stochastic operator as limiting object for the -Laguerre ensemble.

Definition 1.1 (The stochastic Bessel operator)

Let be a standard Brownian motion on . For and , the stochastic Bessel operator (known as SBO) is the random differential operator

defined on a subset of with Dirichlet and Neumann boundary conditions at and at infinity, respectively.

They showed a connection between the eigenvalues of the -Laguerre ensemble at the hard edge and the low-lying eigenvalues of the SBO:

Proposition 1.2 (Limit of the -Laguerre ensemble at the hard edge [12, Theorem 1])

With probability one, when restricted to the positive half-line with Dirichlet conditions at the origin, has a discrete spectrum with single eigenvalues . Moreover, with the ordered points of the -Laguerre ensemble of size ,

(jointly in law) for any fixed as .

In this paper, we study the convergence of the lowest eigenvalues of the SBO in the high temperatures limit, when the inverse temperature parameter tends to .

2 Our result

When tends to , the smallest eigenvalues of the SBO get close to the hard edge at at an exponential rate. In order to get a non trivial limit, we therefore consider the rescaled eigenvalues

| (2) |

Note that we thus reverse the ordering of the eigenvalues, and that any is positive for small enough. We restrict ourselves to the case because the estimations computed in Section 4 and Section 5 differ if . Since the parameter is set, we omit it from our notations going forward.

Theorem 2.1 (Convergence of the low-lying eigenvalues of the SBO)

When tends to , the rescaled eigenvalues point process of the SBO converges in law towards a random simple point process on which can be described using coupled SDEs.

The convergence holds for a well chosen topology of measures on , corresponding to a left-vague/right-weak topology (see after Proposition 3.4 for more details). The limiting point process is simple in the sense that all its points are distinct almost surely. We will characterize it (similarly to the SBO eigenvalues) through the coupled diffusions (5) and (6).

Usually, one expects that, when the temperature is high, the limiting point process is no longer repulsive and corresponds to a Poisson point process as the noise becomes dominant. Here, we get a different result. It comes from the competition between the strong repulsive interaction and attraction at the hard edge for small (see (1)). Because of this interaction, the repulsive factor does not disappear in the limit.

3 Strategy of proof and limiting point process

3.1 Riccati transform

If solves the eigenvalues equation with initial conditions , , then Dumaz, Li and Valkó [4, Proposition 7] showed that is the unique strong solution of the stochastic differential equation system:

with the corresponding initial conditions, and the Brownian motion from Definition 1.1.

Using the Riccati transform from Halperin [9] defined away from the zeros of , Ramírez and Rider [12] introduced the family of coupled diffusions :

| (3) |

The choice provides the initial condition . The diffusion may explode to if hits , in which case it immediately restarts from . Indeed, at the first hitting time of by , we have ( since is positive near thus decreasing right before , and since and is not the null solution) and after . The same analysis can be conducted for potential successive hitting times of .

Ramírez and Rider proved the following equality in law that connects the family to the eigenvalues of :

| (4) |

It is crucial to note that the same Brownian motion from Definition 1.1 drives the whole family of SDEs in (3). It implies important properties such as the monotonicity of the number of explosions of (which turns out to be finite). In fact, the number of explosions of on is the number of eigenvalues of below .

3.2 Rescaled diffusions

We study the small beta limit of the family of diffusions from (3) when is properly rescaled with , i.e. when is such that is of order .

Notice that, when reaches , the random term vanishes and the diffusion drift is negative. It implies that never reaches from below. It is easy to check that the hitting times of form a discrete point process.

Let us fix and set . Using the property above, we define the diffusion , which equals

Using the Itô formula for a positive Itô process, we can show that the diffusions and follow the following SDEs:

| (5) | ||||

| (6) |

where is a Brownian motion corresponding to different rescalings of the initial Brownian motion . These rescalings, including the new magnitude , are chosen so that the Brownian motion stands on its own, allowing an easier comparison between the terms of the drift in the limit.

The diffusions may explode to in a finite time. By definition, the diffusion alternates between and : it starts to follow and each time (resp. ) reaches , immediately restarts from and follows (resp. ). This alternating system is a consequence of the logarithmic transformation, which leads to a change of diffusion each time changes sign.

Let us define the critical line:

| (7) |

This definition of makes sense in light of the last exponential term from (5) and (6). The positions of and with respect to condition the order of magnitude of this term and wether it prevails or not over the other terms of the drift.

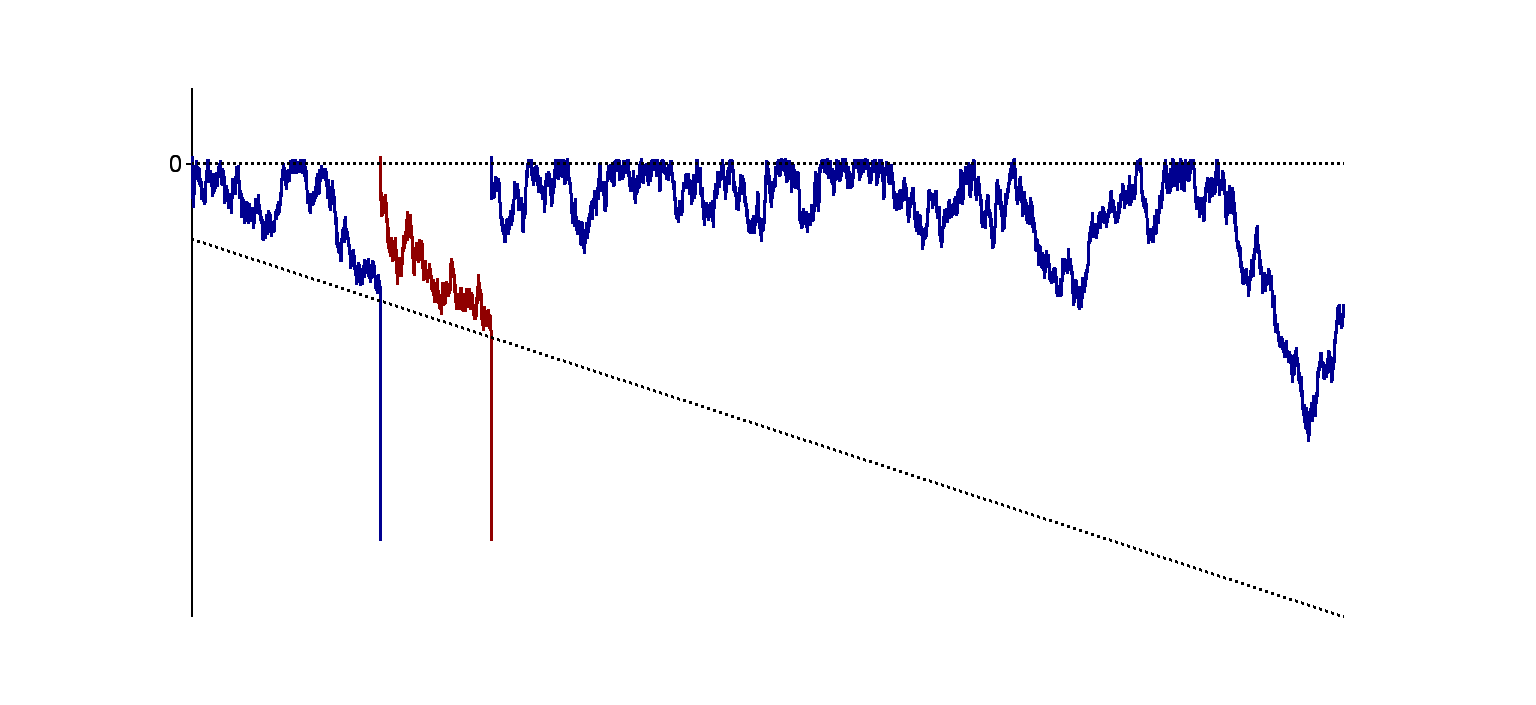

Figure 1 shows a sample path of the diffusion . On this event, the diffusion explodes one time as (blue), then one time as (red), and then stays above the critical line as (blue) and does not explode anymore.

Roughly, the diffusion behaves as follows after each explosion time. First, it quickly goes down to values around . Then, it spends some time between the line and , where it behaves as a reflected (downwards) Brownian motion with drift . If it reaches the line in a finite time then it quickly explodes to after this hitting time.

The behaviour of the diffusion is similar except that in the interval , it behaves as a reflected (downwards) Brownian motion with drift . Therefore, it almost surely hits when .

There are two types of explosions for : either explodes at a time such that , which corresponds to the (rescaled) hitting times of by the initial diffusion , or explodes at time such that , in which case we get the (rescaled) explosion times of the initial diffusion .

In the following, we denote by the explosion times of the diffusion and by

| (8) |

the measure corresponding to the (rescaled) explosions of .

We will prove that, for a well-chosen topology, the trajectory of the diffusion converges in law, when tends to , towards a non-trivial limit , that we describe in the following paragraph.

3.3 Description of the limiting point process

Let us now define , the limiting diffusion of , which will characterize the limiting point process from Theorem 2.1. Its definition involves Brownian motions with drift reflected downwards at . By definition, a Brownian motion with drift reflected downwards at is a diffusion Markov process with infinitesimal operator acting on the domain

where denotes the continuous and bounded functions on . Using the Skorohod problem, we can write this diffusion as

where is a Brownian motion starting at or any negative point.

To define the limiting diffusion , we use the same Brownian motion as in the diffusions and from (5) and (6).

Definition 3.1 (Limiting diffusion)

The limiting diffusion is defined as follows:

-

•

It starts at at time : .

-

•

It then follows a Brownian motion with drift reflected downwards at (built from )

(9) until its first hitting time of the critical line from (7).

-

•

If it reaches in a finite time, it immediately restarts at at this time, then follows a reflected downwards at Brownian motion with another drift (also built from )

(10) until its first hitting time of the critical line from (7).

And so on, alternating between and each time it hits and restarts at . Note that the probability that reaches the critical line decreases with time. On the other hand, since , almost surely hits the critical line in a finite time.

Let be the hitting times of the critical line by the diffusion , where we omit to display the dependency on for lighter notations. We define the random measure associated to the point process :

| (11) |

We then use the coupled random measures to define a discrete point process on . Since decreases from to almost surely, it is easy to prove the following proposition:

Proposition 3.2 (Limiting point process)

There is a random variable valued in the Borel sets of , such that, for all fixed ,

Almost surely, the measure is unique, discrete, bounded from above and has an accumulation point at .

3.4 Strategy of the proof of Theorem 2.1

We can now state the desired convergence results towards the limiting measures which we need to prove Theorem 2.1.

Proposition 3.3 (Convergence of the explosion times of )

It is immediate to extend this proposition for the joint law of when are fixed positive numbers. It directly implies the following result on the finite dimensional laws of the point process , with as in (2). Let us denote by the measure associated to this point process, i.e. .

Proposition 3.4 (Convergence of the finite-marginals of the eigenvalue process)

Fix . When , the random vector converges in law to the random vector .

Using a similar reasoning as in [3, Proof of Theorem ], we consider the space of measures on with the topology that makes continuous the maps for any continuous and bounded function with support bounded to the left. In other words, this is the vague topology towards and the weak topology towards . It allows to control the decreasing sequence of atom locations of from its first point.

Proposition 3.4 shows that the family of measures is tight (and therefore relatively compact by Prokhorov’s theorem): indeed, the above convergence provides the required control on the mass given by to for any given . Besides, this convergence uniquely identifies the finite-marginals of any limiting point. We thus deduce from Proposition 3.4 the convergence of the left-vague/right-weak topology of the eigenvalues point process stated in Theorem 2.1.

To conclude the proof of Theorem 2.1, we devote the rest of the paper to the proof of Proposition 3.3, also using the unique identification of the finite-marginals and the tightness of the family of measures. In Section 4, we control the first explosion time of the diffusion in (15) and deduce the weak convergence of its first explosions times. Then, in Section 5, we show the tightness of the family of measures .

Unless specified otherwise, the limits and now pertain to the asymptotics . For lighter notations, we also omit the dependency on of our variables.

3.5 Useful concepts and results

We will use the following estimates for any Brownian motion :

| (12) | |||

| (13) |

Consider a diffusion started from and the same diffusion reflected downwards at the origin:

For all , , therefore:

| (14) |

4 Control of the explosion times

In this section, we fix . Recall the definition of the critical line in (7). Consider the first two explosion times and of the diffusion . Until the first explosion time , by definition and follows the SDE (5).

Set and introduce the first hitting times by the diffusion :

We decompose the trajectory of into three parts. First, it reaches the axis in a short time (descent from ). Then, it spends a time of order in the region and behaves like , the reflected Brownian motion with drift from (9). Finally, if it approaches the critical line closer than , then it explodes with high probability within a short time (explosion to ).

Recall the first hitting times of the critical line by the diffusion from Definition 3.1.

Proposition 4.1 (Limit behavior of the diffusions and )

Set , independent of . There exist a deterministic function and an event , , on which, for small enough:

-

(a)

,

-

(b)

,

-

(c)

and .

The control (15) extends to any and for and ensures that, for any , , thus identifying the measure as the unique possible limit for .

The rest of this section is dedicated to the proof of Proposition 4.1. Recall that the diffusion differs from its counterpart only by its constant drift component (instead of for ), which makes decrease faster than . We prove the results for the diffusion , they extend to the diffusion with the same arguments.

We introduce the stationary diffusion on , which we use to approximate in the region where the drift component becomes negligible as tends to :

| (16) |

4.1 Descent from : proof of

It suffices to prove property for the diffusion , which bounds the diffusion from above. Set the level , so that . As tends to , when the diffusion is above the level , the term of leading order in the right-hand side of (16) is .

Consider the ordinary differential equation on :

which has for solution . The time at which reaches the level has the asymptotics

Introduce the diffusion . Its evolution writes:

Let . By the Brownian tail bound (12), . On the event and while , we have

and thus for small enough.

Therefore the diffusion is bounded from above by for small enough and hits the level before time . Since before time , for small enough, the diffusion hits the level before time .

After the level is reached, we use the Brownian motion to reach in a short additional time. Set the event

on which . Since , the lower bound (13) and the asymptotics and imply that , thus proving the property on the event .

4.2 Convergence to : proof of

The bound (12) shows that the probability of the following event tends to as tends to :

Recall that so , and note that the diffusion is equal in law to the diffusion (as in (9)), by the strong Markov property. Thus, to prove property , it suffices to show that, with overwhelming probability as tends to , for small enough,

| (17) |

where denotes the diffusion started from at time and its first hitting time of . We write the stationary diffusion from (16) started from at time . For , , so we have the bounds:

Since , to prove property (17), it is enough to show that, on an event of probability going to as tends to , for small enough,

| (18) |

To that end, we bound the diffusion from below and above by two reflected diffusions and that converge to as tends to .

We set the level , so that .

4.2.1 Lower bound

We set the level . Let be the following diffusion, reflected downwards at the barrier :

Since the element of drift decreases when goes through , we have the lower bound:

| (19) |

It is straightforward that

Since , for small enough,

4.2.2 Upper bound

We wish to bound the diffusion from above by the diffusion . To prove that this upper bound holds with high probability as tends to , we use the following result, that shows how unlikely it becomes for the diffusion to hit the level before any negative level.

Lemma 4.2 (Levels hitting times for the diffusion )

For any ,

Lemma 4.2 is proved in the Appendix using standard tools of diffusion analysis.

The choice of level in Lemma 4.2 provides the existence of an event of probability going to as tends to on which the diffusion hits the barrier before the level , and thus:

| (20) |

4.2.3 Conclusion

4.3 Explosion to : proof of

We denote by (resp. ) the diffusion started at time from position (resp. ). We introduce the first hitting time of the level by the diffusion , and the explosion time of the diffusion to .

Recall that . To prove property , we choose and show that there exists an event of probability going to as tends to on which, for small enough, and .

4.3.1 Control of

Recall that , so that and .

We use the variations of the Brownian motion to cross the critical line . The upper bound implies that on the event

and the Brownian tail bound from (13) shows that .

Note that the inclusion of events ensures that, on a subevent of (where if ) of probability going to as tends to , the diffusion hits the critical line while the diffusion crosses this line, between times and .

4.3.2 Control of

On each Brownian trajectory, the diffusion is bounded from above by the diffusion , with

Define the diffusion , with evolution

Consider the event , with .

On , for small enough:

so the diffusion is bounded from above by the solution of the ordinary differential equation

with solution

which explodes to in a time , smaller than for small enough. This remains true for and thus for , since while . Since , this proves the desired control on .

5 Tightness of the explosion times measures

In this section, we fix . Recall the measure of the explosion times from (8) . We prove in this section that there are and , such that, for all , there exist a finite time and a finite number of explosions so that:

| (21) |

Introduce , the law of the random measure . The bound (21) gives us the tightness condition:

| (22) |

Indeed, the set , where is the space of locally finite measures on , satisfies the following conditions:

| (23) |

where the second condition holds since, for any measure in and . It thus fulfills the Kallenberg criterion for weak relative compactness (see [10]), and its compact closure verifies the tightness condition (22).

Prokhorov’s theorem gives us the relative compactness of the family in , the set of probability measures on , and thus concludes the proof of Proposition 3.3.

The rest of this section is dedicated to the proof of (21). We first show a preliminary result that will be helpful to control the number of explosions. Recall that is the first explosion time of the diffusion from (5), started from at time .

Lemma 5.1 (Lower bound on the explosion time of )

For small enough,

Proof 5.2

We fix a deterministic such that . Recall the definition of the critical line in (7). When the diffusion is in the region between and , we have the lower bound, for small enough:

| (24) |

Introduce the diffusion on , defined as the Brownian motion started from at time and reflected downwards at : The bound (24) shows that, for small enough, the diffusion is bounded from below by the diffusion on each Brownian trajectory, up until the first hitting time of by .

We now turn to the proof of (21). Fix . We control the diffusion with two diffusions. The first diffusion starts at time at position and is reflected below the horizontal line with drift . The second diffusion starts at time at position , has a drift as well and is also reflected below .

We can choose high enough such that the diffusions and do not hit with probability greater than . Indeed, the sublinearity of the Brownian motion is such that

| (25) |

On the event where (25) holds, the diffusion stays above after time , and thus above the critical line . We now choose high enough so that with probability greater than until time , thus stays above before time as well. Therefore, on an event of probability greater than , the diffusion never hits . Similar arguments can be used for the second diffusion .

The term in the drift of the diffusion implies the existence of such that, almost surely, when started before time , the diffusion explodes before time .

If, at time , the diffusion evolves as the diffusion , then it almost surely explodes before time , after which it evolves as and stays above (for small enough such that ) and does not explode anymore.

If, at time , the diffusion evolves as the diffusion , then we distinguish between three cases:

First, if the diffusion hits between times and , then stays above and therefore does not explode.

Else, following the proof of property from Proposition 4.1 in Section 4, we can choose a deterministic level so that, if reaches between time and , then it explodes before time with probability greater than . After that, behaves as and almost surely explodes one last time before time , as previously.

Finally, if the diffusion starts above at time and stays in the interval for all , then it is bounded from below by a Brownian motion with a positive drift , and therefore it will be above at time with probability greater than . In this event, stays above the diffusion after time and thus does not explode.

Gathering the different cases, we thus obtain the existence of an event of probability greater than on which explodes at most once after time and does not explode after time .

6 Conclusion

We proved that, in the high temperatures limit , the properly rescaled point process of the low-lying eigenvalues of the stochastic Bessel operator converges towards a simple point process on , described using coupled SDEs. This limiting point process keeps a repulsive factor and therefore differs from the Poisson point process found by Dumaz and Labbé [3] as the high temperatures limit of the Stochastic Airy operator. Our result opens research perspectives to understand the properties of this new point process.

Appendix: Proof of Lemma 4.2

Recall that and . In this proof we denote by the diffusion . Set , and . Let . To compute the hitting times of , introduce the scale functions and :

The following lemma explicits the asymptotic behavior of .

Lemma 6.1 (Convergence of the scale functions)

For any ,

Furthermore, .

Since is a local martingale, is a martingale. By the stopping theorem, we get:

Lemma 6.1 readily implies that this probability tends to as tends to .

Proof 6.2 (Proof of Lemma 6.1)

We have, for all ,

which means that converges uniformly to on . Besides, the functions and are bounded on , and is uniformly continuous on so converges uniformly to on . Therefore, converges uniformly to on .

Now turning to . We can compute explicitly:

A study of the variations of shows that decreases before and increases afterwards. For small enough, , which tends to as tends to , and increases on , so that:

therefore .

I wish to thank Laure Dumaz for her precious help throughout this research project.

This research paper presents results found during my PhD thesis [11], funded with a research grant from the SDOSE Doctoral School and PSL University.

There were no competing interests to declare which arose during the preparation or publication process of this article.

References

- [1] Bourgade, P., Erdős, L. and Yau, H. T. (2012). Bulk universality of general -ensembles with non-convex potential. J. Math. Phys. 53, 095221.

- [2] Bourgade, P., Erdős, L. and Yau, H. T. (2014). Universality of general -ensembles. Duke Math. J. 163, 1127 – 1190.

- [3] Dumaz, L. and Labbé, C. (2022). The stochastic airy operator at large temperature. The Annals of Applied Probability 32, 4481 – 4534.

- [4] Dumaz, L., Li, Y. and Valkó, B. (2021). Operator level hard-to-soft transition for -ensembles. Electron. J. Probab. 26, 28.

- [5] Dumitriu, I. and Edelman, A. (2002). Matrix models for beta ensembles. J. Math. Phys. 43, 5830–5847.

- [6] Dumitriu, I. and Edelman, A. (2006). Global spectrum fluctuations for the -hermite and -laguerre ensembles via matrix models. J. Math. Phys. 47, 063302.

- [7] Duy, T. K. (2018). On spectral measures of random Jacobi matrices. Osaka J. Math. 55, 595–617.

- [8] Erdős, L. and Yau, H. T. (2015). Gap universality of generalized Wigner and -ensembles. J. Eur. Math. Soc. 17, 1927–2036.

- [9] Halperin, B. I. (1965). Green’s functions for a particle in a one-dimensional random potential. Phys. Rev. 139, A104–A117.

- [10] Kallenberg, O. (2017). Random Measures, Theory and Applications vol. 77.

- [11] Magaldi, H. (2022). Beta-ensembles and their high-temperature limit. PhD thesis. Université PSL.

- [12] Ramírez, J. and Rider, B. (2009). Diffusion at the random matrix hard edge. Commun. Math. Phys. 288, 887–906.

- [13] Ramírez, J. A., Rider, B. and Virág, B. (2011). Beta ensembles, stochastic Airy spectrum, and a diffusion. J. Am. Math. Soc. 24, 919–944.

- [14] Shcherbina, M. (2011). Orthogonal and symplectic matrix models: Universality and other properties. Commun. Math. Phys. 307, 761–790.

- [15] Silverstein, J. W. (1985). The smallest eigenvalue of a large dimensional Wishart matrix. Ann. Probab. 13, 1364–1368.

- [16] Sosoe, P. and Wong, P. (2012). Local semicircle law in the bulk for gaussian -ensemble. J. of Statist. Phys. 148, 204–232.

- [17] Valkò, B. and Virág, B. (2009). Continuum limits of random matrices and the brownian carousel. Inventiones mathematicae 177, 463–508.

- [18] Wong, P. (2012). Local semicircle law at the spectral edge for gaussian -ensembles. Commun. Math. Phys. 312, 251–263.