Treatment Effect Estimators as Weighted Outcomes

Abstract

Estimators weighting observed outcomes to form an effect estimate have a long tradition. The corresponding outcome weights are utilized in established procedures, e.g. to check covariate balancing, to characterize target populations, or to detect and manage extreme weights. This paper provides a general framework to derive the functional form of such weights. It establishes when and how numerical equivalence between an original estimator representation as moment condition and a unique weighted representation can be obtained. The framework is applied to derive novel outcome weights for the leading cases of double machine learning and generalized random forests, with existing results recovered as special cases. The analysis highlights that implementation choices determine (i) the availability of outcome weights and (ii) their properties. Notably, standard implementations of partially linear regression based estimators - like causal forest - implicitly apply outcome weights that do not sum to (minus) one in the (un)treated group as usually considered desirable.

Keywords: Augmented inverse probability weighting, causal forest, causal machine learning, covariate balancing, double machine learning, generalized random forest, partially linear regression

1 Introduction

Estimating the effect of treatment on outcome is a common goal in causal inference. This may involve adjusting for confounding variables and/or exploiting exogenous variation induced by an instrumental variable (IV). A variety of estimators is available for each setting depending on the target parameter and the assumptions imposed for identification <see, e.g. reviews by>Imbens2009,Athey2017,Abadie2018EconometricEvaluation,Imbens2024CausalSciences. Many of these estimators are a “white box” in the sense that they document how the sample is processed to obtain an effect estimate. Parametric regressions come with familiar coefficient outputs and other popular estimators have a representation as linear combination of observed outcomes:

| (1) |

where represents the weight assigned to the outcome of observation in estimating . Structure (1) is most prominent in the literature on propensity score matching/weighting <e.g.>Imbens2015CausalSciences, balancing estimators <e.g.>Ben-Michael2021TheInference, and synthetic controls <e.g.>Abadie2021UsingAspects. Furthermore, it is discussed for estimators of the local average treatment effect <e.g.>Imbens1997EstimatingModels,Abadie2003SemiparametricModels,Soczynski2024AbadiesEffect as well as for linear regression <e.g.>Imbens2015MatchingExamples,Chattopadhyay2023OnInference.

Outcome weights have established use cases, such as: (i) covariate balancing checks assessing internal validity in experimental and observational studies <e.g.>Rosenbaum1984ReducingScore,Rosenbaum1985ConstructingScore, (ii) target population characterization investigating external validity in IV settings <e.g.>Abadie2003SemiparametricModels, or when using OLS Chattopadhyay \BBA Zubizarreta (\APACyear2023), (iii) extrapolation diagnostics for estimators that could use negative weights Chattopadhyay \BBA Zubizarreta (\APACyear2023) (v) finite sample estimator stabilization by normalizing weights <e.g.>Hajek1971CommentOne, or by trimming extreme weights <e.g.>Lechner2019PracticalEstimation, (vi) variance estimation <e.g.>[Ch. 19]Imbens2015CausalSciences.

In contrast, recent estimators integrating supervised machine learning into the estimation process <see>[for a textbook]Chernozhukov2024AppliedAI can be considered as “grey box”. Their multi-step algorithms are transparent and their theoretical properties are well-understood. However, neither coefficients nor outcome weights are currently available to interrogate how these steps jointly process a concrete sample within a concrete implementation. A key take-away of the analysis below is that at least outcome weights can be available to open the grey box.

This paper introduces a simple but general framework to derive and analyze outcome weights of form (1). We establish conditions for a numerical equivalence between an original estimator representation as moment condition and a unique weighted representation. The framework is applied to derive novel outcome weights for the six leading cases of double machine learning Chernozhukov \BOthers. (\APACyear2018) and generalized random forest Athey \BOthers. (\APACyear2019). Knowing the closed-form of the outcome weights has the immediate practical benefit that they can be plugged into established routines for classic weighting estimators. For example, covariate balancing can now be assessed for conditional average treatment effects estimated by causal forest. A second benefit is that the framework naturally allows to investigate basic properties of the weights. In particular, it highlights that implementation decisions control whether outcome weights of the treated sum up to one and of the untreated to minus one. Such weights are often considered as intuitive, reasonable and desirable in the literature <e.g.>Imbens2015CausalSciences,Soczynski2024AbadiesEffect. However, the analysis reveals that estimators building on partially linear regression do not satisfy this property in their standard implementations.

The paper makes several contributions: (i) It introduces the first general framework to derive outcome weights; (ii) Its application to causal machine learning estimators yields novel outcome weights and provides a blueprint for applying the framework to other estimators; (iii) It illustrates how the new closed-form expressions enable established diagnostic tools from the weighting literature to be integrated off-the-shelf into causal machine learning applications; (iv) The theoretical results about conditions ensuring desirable estimator properties inform implementation decisions and complement the high-level conditions provided in asymptotic analyses; (v) The paper provides an additional piece in the continuing effort to blur the line between outcome weighting and outcome regression methods. \citeABruns-Smith2023AugmentedRegression show how weighting estimators can be expressed as regression estimators. This paper goes in the opposite direction by showing how estimators involving flexible outcome regression can be expressed as weighting estimators; (vi) The accompanying R package OutcomeWeights computes the weights presented in the paper for general use Knaus (\APACyear2024). The presented applications rely on this package and can be replicated in a supplementary Docker image.

1.1 Related literature

Outcome weights in form of (1) are leveraged as common structure of difference, weighting, subclassification, and matching estimators (Smith \BBA Todd, \APACyear2005; Huber \BOthers., \APACyear2013; Imbens \BBA Rubin, \APACyear2015, Ch. 19.4.). Similarly, the outcome weights are derived and used for ordinary and weighted least squares based estimators Kline (\APACyear2011); Imbens (\APACyear2015); Jakiela (\APACyear2021); Chattopadhyay \BBA Zubizarreta (\APACyear2023); Hazlett \BBA Shinkre (\APACyear2024), two-stage least squares (TSLS) Chattopadhyay \BBA Zubizarreta (\APACyear2021), and augmented inverse probability weighting implemented with (post-selection) OLS outcome regression Knaus (\APACyear2021); Chattopadhyay \BBA Zubizarreta (\APACyear2023). This paper shows that a broader class of estimators can have this structure with a particular focus on those incorporating flexible outcome regression, while covering the results in the literature as special cases.

Other types of weights are prominent in the causal inference literature but distinct from the outcome weights pursued in this paper. First, balancing weights are the result of a tailored optimization problem to achieve covariate balancing of some prespecified form Graham \BOthers. (\APACyear2012); Hainmueller (\APACyear2012); Imai \BBA Ratkovic (\APACyear2014); Zubizarreta (\APACyear2015); Zhao (\APACyear2019); Kallus (\APACyear2020); Armstrong \BBA Kolesár (\APACyear2021); Heiler (\APACyear2022). Thus, balancing weights are an explicit part of such balancing estimators. While balancing weights are a special case of outcome weights, this paper focuses on estimators where the outcome weights play no explicit role but are implicit in the common characterization of the estimation procedure. \citeAChattopadhyay2023OnInference call such weights “implied weights” in the context of OLS. Second, effect weights are central to understanding the estimand targeted by a given estimator. The pursued structures in this literature are variations of where is the weight an estimator assigns to the conditional treatment effect in expectation. Effect weights are derived under different identifying and functional form assumptions for OLS Angrist (\APACyear1998); Angrist \BBA Krueger (\APACyear1999); Humphreys (\APACyear2009); Aronow \BBA Samii (\APACyear2016); Goldsmith-Pinkham \BOthers. (\APACyear2021); Słoczyński (\APACyear2022), TSLS Imbens \BBA Angrist (\APACyear1994); Angrist \BBA Imbens (\APACyear1995); Heckman \BBA Vytlacil (\APACyear2005); Słoczyński (\APACyear2020); Blandhol \BOthers. (\APACyear2022), two-way fixed-effects <see>[for overviews] deChaisemartin2023Two-waySurvey,Roth2023WhatsLiterature, regression discontinuity estimators Lee \BBA Lemieux (\APACyear2010), and panel estimators Chernozhukov \BOthers. (\APACyear2013). The main difference between outcome weights and effect weights is that the former apply to observed outcomes and numerically reproduce the estimate without further assumptions, while the latter weight inherently unobservable effects and usually reproduce the estimate only in expectation. Both types of weights have their established use cases and are therefore complementary.

A small but growing body of literature provides nuance to the common notion that it is preferable for the outcome weights to sum to (minus) one within treatment groups. \citeADoudchenko2016BalancingSynthesis and \citeABreitung2024AlternativeDesigns challenge this view for synthetic control estimators, and \citeAKhan2023AdaptiveEstimation for average treatment effect estimation. \citeASoczynski2024AbadiesEffect note that some Abadie’s \APACyear2003 estimators are intermediate cases between normalized and unnormalized estimators, e.g. with treated weights summing to one but untreated weights not to summing minus one. This paper adds the observation that partially linear regression based estimators usually produce weights that overall sum up to zero but not to (minus) one for (un)treated.

Finally, the paper adds to recent works establishing numeric equivalences between different estimator representations Bruns-Smith \BOthers. (\APACyear2023) or estimators Słoczyński \BOthers. (\APACyear2023, \APACyear2024) for conceptual and/or practical insights.

2 A general framework to derive outcome weights

2.1 Notation

The estimators under consideration require access to data with observations indexed by . The data includes a binary treatment , an outcome , covariates , and an optional binary instrument , all collected in . The empirical mean of a variable is represented as .

Many results are stated in matrix notation where bold letters describe vectors or matrices of variables. denotes the identity matrix of dimension , and represent column vectors of length containing zeros and ones, respectively.

2.2 Pseudo-IV estimators

This paper focuses on estimators falling into the class of pseudo-IV estimators (PIVE):

Definition 1

(pseudo-IV estimators)

Define the class of pseudo-IV estimators (PIVE) as estimators solving an empirical moment condition of the form

| (2) |

with

-

•

: scalar pseudo-outcome

-

•

: scalar pseudo-treatment

-

•

: scalar pseudo-instrument

where , and are optional nuisance parameters.

Note that the PIVE representation is neither a unique, nor the most compact representation of an estimator. For example, a representation using a linear score with and would be equivalent, or vice versa any estimator with a linear score can be written as PIVE with , , and . However, the PIVE structure is essential for the goal of this paper. In particular, separating the pseudo-outcome from the pseudo-instrument makes the derivation and analysis of the outcome weights tractable.

Example (OLS): We use the canonical OLS estimator as running example to illustrate the general results throughout the paper. Consider a linear outcome model . The OLS estimator for can be expressed as PIVE using the residual-on-residual regression representation of the Frisch-Waugh-Lovell Theorem:

| (3) |

where and such that the pseudo-outcome is the outcome residual, and both pseudo-treatment and -instrument are the treatment residual.

2.3 Outcome weights of pseudo-IV estimators

Solving Equation 2 leads to parameter estimate

| (4) |

Now assume that the pseudo-outcome vector can be obtained by multiplying a unique transformation matrix with the outcome vector, i.e. . Then, Equation 4 can be written in the form of Equation 1

| (5) |

leading to a core result of the paper:

Proposition 1

(outcome weights of PIVE)

The outcome weights of a PIVE in the sense of Definition 1 have closed-form

| (6) |

if and a unique transformation matrix exists such that .

This simple result is constructive because it motivates a two step procedure to derive outcome weights:

-

1.

Express the estimator as PIVE.

-

2.

Find transformation matrix has closed-form.

These steps are illustrated below for a variety of estimators. However, the procedure is general and could be pursued for any other estimator fitting into the PIVE structure.

Example (OLS) continued: The solution of the residual-on-residual regression (3) in form of Equation 6 is

| (7) |

where we use the projection matrix to define the residual maker matrix , and the treatment residual vector . The residual maker matrix is therefore the outcome transformation matrix of OLS and is the outcome weights vector.111We deliberately do not use that is idempotent for illustration purposes but note that also the identity matrix would by a suitable transformation matrix in (7).

3 Outcome weights of concrete pseudo-IV estimators

This section leverages the new framework to provide the first characterization of outcome weights for six leading cases within the double machine learning (DML) and generalized random forest (GRF) frameworks (marked with ∗), while also recovering existing results for eight other estimators:

-

•

IF∗: Instrumental forest Athey \BOthers. (\APACyear2019)

-

•

PLR-IV∗: Partially linear regression with IV Chernozhukov \BOthers. (\APACyear2018)

-

•

TSLS: Two stage least squares

-

•

Wald: Wald estimator Wald (\APACyear1940)

-

•

CF∗: Causal forest Athey \BOthers. (\APACyear2019)

-

•

PLR∗: Partially linear regression Robinson (\APACyear1988); Chernozhukov \BOthers. (\APACyear2018)

-

•

OLS: Ordinary least squares

-

•

DiM: Difference in means

-

•

AIPW∗: Augmented inverse probability weighting Robins \BBA Rotnitzky (\APACyear1995); Chernozhukov \BOthers. (\APACyear2018)

-

•

RA: Regression adjustment <e.g. discussed by>Imbens2004NonparametricReview

-

•

IPW: Inverse probability weighting Horvitz \BBA Thompson (\APACyear1952)

-

•

Wald-AIPW∗: Wald type AIPW Tan (\APACyear2006); Chernozhukov \BOthers. (\APACyear2018)

-

•

Wald-RA: Wald type regression adjustment Tan (\APACyear2006)

-

•

Wald-IPW: Wald type inverse probability weighting Tan (\APACyear2006)

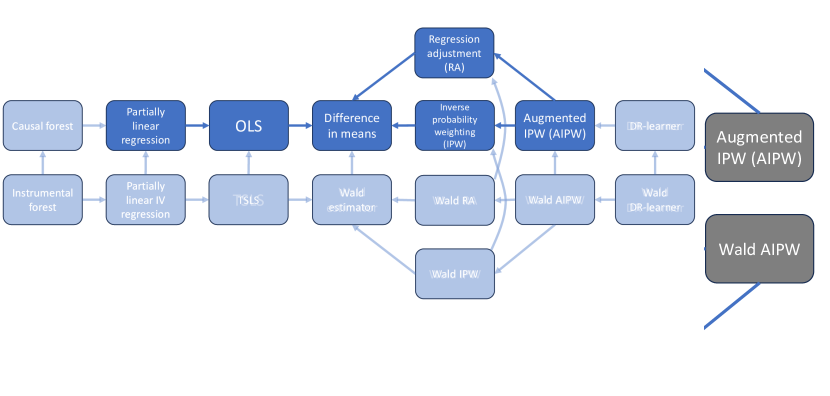

Conveniently it suffices to analyze the three estimators in bold letters - IF, AIPW and Wald-AIPW - because their subsequent estimators follow as special cases (see Figure A.1 for a graphical illustration). Each estimator is typically used at an intersection of three research designs (randomized controlled trials, unconfoundedness or instrumental variables), two aggregation levels (average or conditional effects), and three outcome model assumptions (none, partially linear, or linear models). Appendix A.1 summarizes the causal parameters and settings for which each estimator is usually applied. However, the main text ignores definition, identification and interpretation issues concentrating on the mechanics of the estimators.

3.1 Nuisance parameters

3.1.1 Definitions

The considered estimators require a variety of nuisance parameters in the form of approximated conditional expectations:

| (8) | ||||||

Furthermore, define the inverse probability weights of the treated and of the untreated .222We use to remind us that these weights are on a different scale than the weights. Using the corresponding definition would unnecessarily complicate notation below. Similarly, define the instrument inverse probability weights as and .

3.1.2 A crucial building block: Smoothers

The literature knows numerous regression methods to estimate the outcome nuisance parameters , , and . However, the class of smoothers <see e.g.>[Ch. 2-3]Hastie1990GeneralizedModels turns out to be crucial for the purpose of this paper. Smoothers produce outcome predictions by weighting/smoothing observed outcomes

| (9) |

where the smoother weight represents the contribution of unit ’s outcome to the prediction of unit .333The arrow notation is adapted from \citeALin2022OnEffect. Define also the smoother vector for the outcome prediction of unit by and the smoother matrix such that and .

The smoother weights in this paper are explicitly allowed to depend on the outcomes (adaptive smoother) and on random components (random smoother), i.e. .444The categorization of smoothers is inspired by \citeACurth2024WhySmoothers. This covers for example (post-selection) OLS, ridge, spline and kernel (ridge) regressions, regression trees, random forests or boosted trees with data-driven hyperparameter tuning (see Appendix A.2 for further discussion). However, the numerical equivalences established below require the mere existence of a smoother matrix:

Condition 1

(smoother matrix)

There exists a unique smoother matrix creating the outcome nuisance vectors if multiplied with the outcome vector:

(C1a)

(C1b) and

(C1c) and

Example (OLS) continued: The projection matrix is arguably the most prominent smoother matrix producing fitted values of an OLS regression as .

3.2 Concrete outcome weights

3.2.1 Instrumental forest and its special cases

The instrumental forest (IF) of \citeAAthey2017a runs an -specific weighted partially linear IV regression

| (10) |

where the -specific weights are obtained by the tailored splitting criterion described in \citeAAthey2017a and can be extracted via the get_forest_weights() function of their grf R package Tibshirani \BOthers. (\APACyear2024). The solution in the form of Equation 4 is

| (11) |

where , and are the instrument, treatment and outcome residual vectors, respectively. The PIVE structure is therefore established. The next step is to understand whether the pseudo-outcome can be obtained using a transformation matrix. This is only possible if a smoother is applied to obtain the outcome predictions, i.e. Condition 1a holds such that and

| (12) |

The transformation matrix of IF can therefore be considered as a generalized residual maker matrix. Equation 12 contains then the first concrete case of Proposition 1:

Corollary 1

(outcome weights of instrumental forest)

Under Condition 1a such that the outcome predictions can be written as ,

the outcome weights of instrumental forests take the form

| (13) |

Table 1 compactly shows how seven other estimators (in light gray) follow as special cases of IF. Starting from the dark gray row, we can follow an upward path to the Wald estimator or a downward path to DiM. The white rows between the gray rows document the modifications needed to recover the next estimator. For example, moving from IF to CF uses treatment residuals instead of instrument residuals and the CF specific weights in the pseudo-instrument, while pseudo-treatment and transformation matrix remain unchanged. Similarly setting the weights to one recovers PLR from CF and PLR-IV from IF. Continuing the paths up- and downwards replaces the generic predictions with linear projections to recover TSLS and OLS, respectively. Finally, using the projection matrix of a constant recovers Wald estimator and DiM.

-

•

Note: Starting from the darkest row and following the arrows, the table shows how estimators follow as special cases by imposing restrictions in the white rows.

Computational remark: The original implementation in the grf package applies a constant in the weighted residual-on-residual regression. This complicates notation but Appendix A.3.1 provides the details how numerical equivalence between original output of grf and the weighted representation is obtained in the OutcomeWeights package.

3.2.2 Augmented inverse probability weighting and its special cases

Augmented inverse probability weighting (AIPW) is developed in a series of papers <e.g.>Robins1994,Robins1995AnalysisData,Rotnitzky1998SemiparametricNonresponse,Chernozhukov2018. AIPW is a PIVE with empirical moment condition

| (14) |

and vector form

| (15) |

The next step is to provide the transformation matrix. This is possible under Condition 1b that the outcome predictions are obtained by smoothers such that . Plugging this into (15) and rearranging delivers the transformation matrix

| (16) |

and leads to the following result:555The AIPW implementation of the grf package uses an alternative moment condition. It is equivalent to (14) in expectation but uses different nuisance parameters and therefore differs numerically. However, also the outcome weights of this variant can be obtained as shown in A.3.2.

Corollary 2

(outcome weights of AIPW)

Under Condition 1b such that the treatment specific outcome predictions can be written as and , the outcome weights of AIPW take the form

| (17) |

Table 2 shows how RA can be obtained by setting all IPW weights to zero. IPW is recovered by setting all entries of the smoother matrices to zero.

3.2.3 Wald-AIPW and its special cases

Tan2006RegressionVariables propose an AIPW extension for the case of a binary instrument. This estimator has the same structure as the canonical \citeAWald1940TheError estimator but applies AIPW to estimate reduced form and first stage, respectively. Following \citeAChernozhukov2018, the Wald-AIPW empirical moment condition in the form of Equation 2 reads

| (18) | ||||

and in the form of Equation 4 becomes

| (19) | ||||

Following similar steps as in Section 3.2.2 establishes another special case of Proposition 1:

Corollary 3

(outcome weights of Wald-AIPW)

Under Condition 1c such that the instrument specific outcome predictions can be written as and , the outcome weights of Wald-AIPW take the form

| (20) |

Table 3 summarizes the involved manipulations to arrive at Wald-RA and -IPW applying similar transformations as for AIPW but for both reduced form and first stage.

3.3 Consolidation

This section provides the first characterization of outcome weights for IF, CF, PLR(-IV), and (Wald-)AIPW (the supplementary theory in action notebook illustrates that the numerical equivalences hold also in practice). The results highlight that the availability of outcome weights depends on the estimator implementation. In particular, it requires to apply smoothers for the involved outcome regressions (C1). This excludes methods with non-differentiable objective functions and/or non-linear link functions for outcome prediction, such as Lasso, (penalized) logistic regression, or many neural network architectures. However, it is important to note that the choices for instrument and treatment nuisance parameters do not affect the availability of outcome weights.

Overall, the simple framework of Section 2 proves very handy for compactly deriving new functional forms of outcome weights and recovering known ones. This is interesting and practically useful in its own right, as the obtained weights can be applied in any established weight-based routine. Additionally, the framework provides a natural lens to investigate basic properties of the outcome weights as we pursue in the following.

4 Weights properties of pseudo-IV estimators

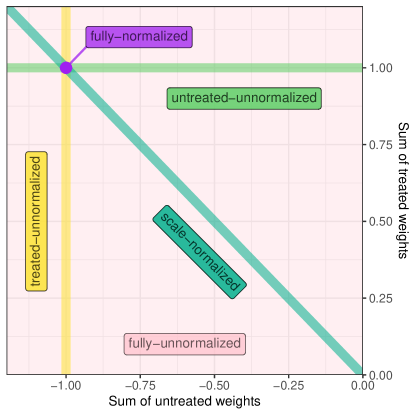

The results of the previous section enable users to ex post inspect whether outcome weights fulfill certain properties. For example, weights adding up to one for the treated (i.e. ) and to minus one for the untreated (i.e. ) are often considered desirable because they guarantee certain in- and equivariances of estimators Imbens \BBA Rubin (\APACyear2015); Słoczyński \BOthers. (\APACyear2024). However, the PIVE framework also allows to analytically investigate the weights properties of estimator implementations. This is conceptually appealing and practically relevant because it permits ex ante control over weights properties. Specifically, we investigate under which conditions estimators fulfill one of the five weights properties collected in Table 4 spanned by the total, treated, and untreated weight sums, respectively (see Figure A.2 for a graphical illustration).

| Weights property | |||

| fully-unnormalized | |||

| untreated-unnormalized | = 1 | ||

| treated-unnormalized | |||

| scale-normalized | = 0 | ||

| fully-normalized | = 0 | = 1 |

The literature documents examples for each class in Table 4.666The proposed class labels in Table 4 ensure that all three versions of unnormalized weights would also be labeled as unnormalized by \citeASoczynski2024AbadiesEffect. Although “normalized” is a loosely defined term, it seems reasonable in this context to use it for estimators whose outcome weights sum to zero, to remain consistent with previous work. Fully-unnormalized weights are associated with inverse probability weighting since \citeAHajek1971CommentOne. (Un)treated-unnormalized weights recently appeared in estimators building on Abadie’s \APACyear2003 and where only one group shows weights adding up to (minus) one Słoczyński \BOthers. (\APACyear2024). Scale-normalized weights are described by \citeASoczynski2023CovariateEffects in the context of covariate balancing propensity scores of \citeAImai2014CovariateScore. Such estimators have treated (untreated) weights summing to (minus) the same non-one constant and also appear prominently in the analysis of partially linear regression based estimators below. Fully-normalized weights are the norm <see overview in>[Ch. 19]Imbens2015CausalSciences.

4.1 Weights properties in the PIVE framework - general

The outcome weights properties in Table 4 are determined by three weight sums. This motivates the following protocol to classify PIVE weights:

-

1.

Calculate

-

•

If normalized

-

•

If unnormalized

-

•

-

2.

Calculate

-

•

If and untreated-unnormalized

-

•

If and scale-normalized

-

•

If and fully-normalized

-

•

-

3.

If and , calculate

-

•

If fully-unnormalized

-

•

If treated-unnormalized

-

•

Recall from Proposition 1 that PIVE weights take the form . Therefore classifying the weights properties of an estimator boils down to checking the first two or all of the following equations:

| (21) | ||||

| (22) | ||||

| (23) |

This implies that it suffices to investigate the following properties of the transformation matrix as shortcuts to classify the outcome weights:

-

1.

because it implies that Equation 21 holds

-

2.

because it implies that Equation 22 holds

-

3.

because it implies that Equation 23 holds

This shows how the PIVE structure offers substantial complexity reduction streamlining the derivations below to a large extent. It turns out that the weights properties are intimately tied to implementation choices as we first illustrate in the OLS example before moving to more involved cases.

Example (OLS) continued: Only one aspect of the implementation affects OLS weights properties in the sense of Table 4:

Condition 2

(covariate matrix with constant)

The covariate matrix contains a column of ones, which is by convention the first column. We can therefore write for a matrix with covariates .

Condition 2 is fulfilled in any reasonable application. However, making it explicit illustrates how implementation choices affect weights properties. We start by checking whether the weights sum to zero and use shortcut 1 focusing on the transformation matrix:

| If C2 |

We conclude that OLS is always normalized if we include a constant. Next, we investigate whether weights of treated sum up to one via shortcut 2:

The transformation matrix applied to the treatment recovers the pseudo-treatment, which is sufficient for treated weights adding up to one. Curiously, this holds without further conditions implying that OLS is untreated-unnormalized even without a constant. Both results taken together recover a well-known fact that OLS is fully-normalized under Condition 2. Additionally, following the proposed framework step by step uncovers a nuisance regarding the case without a constant.

4.2 Weights properties in the PIVE framework - concrete

4.2.1 Implementation details

This section collectively introduces implementation details that become relevant in the later derivations. We start with a relatively mild condition:

Condition 3

(affine smoother matrix)

In addition to Condition 1, all rows of the smoother matrices add up to one:

Most smoothers discussed in the literature fulfill this property. However, \citeACurth2024WhySmoothers note that boosted trees can be an exception.

The next condition is relevant for the treatment group specific outcome nuisances:

Condition 4

(no smoothing between treatment groups)

In addition to Condition 1b, the treatment group specific predictions are formed using only observations of the respective group. This ensures that

| (24) | |||

| (25) |

This condition is relevant for AIPW estimators and in line with standard implementations forming the group specific outcome models in the respective subgroups.

The next condition is less familiar but important for estimators based on partially linear regression and Wald-AIPW:

Condition 5

(outcome smoother matrix applied to treatment)

(C5a) The treatment predictions are formed using the outcome smoother matrix:

| (26) |

(C5b) The treatment predictions in the different instrument groups are formed using the respective outcome smoother matrix:

| (27) |

This goes against the idea of many flexible estimators to entertain different models for outcome and treatment predictions, respectively. Therefore, this condition is not in line with standard implementations.

The final condition is relevant for all estimators involving an inverse probability weighting component:

Condition 6

(normalized inverse probability weights)

(C6a) and

(C6b) and

C6a is the standard \citeAHajek1971CommentOne normalization and usually recommended in applications Busso \BOthers. (\APACyear2014). C6b is suggested by \citeAUysal2011ThreeMethods and recommended by \citeASoczynski2024AbadiesEffect.

4.2.2 Weights properties of Instrumental Forest and its special cases

Without further conditions in (11) is fully-unnormalized. In the following, we explore conditions leading to (fully-)normalized weights. First, we investigate how could be obtained:

| If C3 |

This establishes that the standard implementation of IF in grf uses normalized weights because it applies the affine smoother random forest (C3) to estimate the outcome nuisance.

The next question is when treated weights sum to one. To this end, it is sufficient to understand when :

| If C5a | |||

The two results span different scenarios. The practically relevant one being that Condition 3 holds but Condition 5a does not because different treatment and outcome models are applied. This means that in practice IF weights are only scale-normalized but not fully-normalized. Only applying the same affine smoother matrix to predict outcome and treatment ensures fully-normalized weights.777Curiously, applying the same non-affine smoother ensures that at least treated weights sum to one generalizing the observation regarding OLS without constant in the previous section.

Recall from Table 1 that CF, PLR-IV and PLR use the same transformation matrix as IF. Consequently, they are also scale-normalized in standard applications. In contrast, OLS and TSLS apply the same projection matrix to form treatment and outcome predictions such that C5a holds by construction. Again the observations regarding OLS in the previous section immediately apply for TSLS because they share pseudo-treatment and transformation matrix. Also TSLS with a constant is fully-normalized and untreated-unnormalized without a constant.

4.2.3 Weights properties of AIPW and its special cases

First, we investigate under which conditions AIPW is normalized:

| If C3 |

This result contains two surprising components. First, we did not apply normalized IPW weights (C6a) to achieve normalized AIPW. This means AIPW is self-normalizing once affine smoothers are applied. Second, normalized IPW weights alone do not normalize AIPW weights as a similar simplification is not possible under C6a only.

The second step investigates when treated weights sum to one:

| If C4 | |||

| If C3 & C4 |

This means that standard implementations using affine smoothers to estimate outcome nuisances in the (un)treated groups separately are self-fully-normalizing regardless which IPW weights are applied. This implies that RA inherits weights properties from AIPW because it can be considered as applying IPW weights of zero (see Table 2). In contrast, IPW can be considered as applying smoother matrices of zeros. These uninformative smoother matrices by construction fulfill C4 but not C3 such that IPW weights are not (fully-)normalized. This recovers the well-known result of \citeAHajek1971CommentOne regarding IPW as a special case of AIPW. Obviously IPW with explicitly fully-normalized weights (under C6a) are fully-normalized.888To see this within the framework note that under C6a and establishing full-normalization.

4.2.4 Weights properties of Wald-AIPW and its special cases

We can not directly apply the results of Section 4.2.3 because the pseudo-outcome and -treatment differ. However, to show that the estimator is normalized if affine smoothers are applied for the outcome regressions requires only to change the superscripts:

| If C3 |

However, the investigation of the sum of treated weights shows notable differences:

| If C5b | |||

Wald-AIPW is therefore only scale-normalized unless we apply the outcome smoothers to also predict the treatments. This goes against the idea of using different models for each nuisance parameter. Unlike AIPW, Wald-AIPW is therefore not expected to be fully-normalized in standard applications. Another point worth noting is that separating the sample by instrument value when estimating outcome/treatment nuisances - an IV version of C4 - is not sufficient to achieve fully-normalized weights of Wald-AIPW.

Similar to the previous section Wald-RA inherits all properties from Wald-AIPW. However, Wald-IPW is always untreated-unnormalized because it can be considered as applying the same zero smoother matrix to outcome and treatment (C5b). Additionally normalizing the weights (C6b) makes Wald-IPW even fully-normalized.999This follows by considering the full numerator of the weight and not only the transformation matrix such that due to Condition 6b. This recovers observations regarding Wald-IPW by \citeASoczynski2024AbadiesEffect within the framework of this paper. Also their findings regarding Abadie’s \APACyear2003 estimators can be obtained in the framework as shown in Appendix A.4.

4.3 Consolidation

Table 5 summarizes the sufficient conditions for closed-form and (fully-)normalized outcome weights.101010Table A.5.2 in the Appendix provides an extended table collecting which conditions are fulfilled by construction and including results for (un)treated-unnormalized weights for completeness. However, those are rather of academic value and we focus on the practically relevant cases in the main text. Estimators with a check mark in the second column always have a weighted representation. Those are the estimators based on IPW and OLS where the weights are either obvious or at least well-studied <e.g.>Imbens1997EstimatingModels,Imbens2015CausalSciences, Imbens2015MatchingExamples, Chattopadhyay2023OnInference. They are still included to demonstrate the generality of the framework but not to provide new insights. Those are obtained for more sophisticated outcome adaptive estimators for which weighted representations are not available in the literature.

| Estimator | Closed-form | Normalized | Fully-normalized |

| Instrumental forest | C1a | C3 | C3 & C5a |

| PLR-IV | C1a | C3 | C3 & C5a |

| TSLS | ✓ | C2 | C2 |

| Wald | ✓ | ✓ | ✓ |

| Causal Forest | C1a | C3 | C3 & C5a |

| PLR | C1a | C3 | C3 & C5a |

| OLS | ✓ | C2 | C2 |

| DiM | ✓ | ✓ | ✓ |

| AIPW | C1b | C3 | C3 & C4 |

| RA | C1b | C3 | C3 & C4 |

| IPW | ✓ | C6a | C6a |

| Wald-AIPW | C1c | C3 | C3 & C5b |

| Wald-RA | C1c | C3 | C3 & C5b |

| Wald-IPW | ✓ | C6b | C6b |

-

•

Abbreviations: DiM: difference in means; RA: regression adjustment; IPW: inverse probability weighting; AIPW: augmented IPW; OLS: ordinary least squares; PLR: partially linear regression; TSLS: two-stage least squares

The results collected in Table 5 highlight the crucial role of implementation details for availability and properties of outcome weights. First, column two documents that researchers can ensure that outcome weights can be accessed ex post by applying smoothers to form outcome predictions as shown in Section 3.2. Second, estimator specific implementation decisions ex ante determine certain weights properties. Columns three and four of Table 5 can serve as look-up table for researchers who want to ensure that a particular implementation of an estimator generates outcome weights of a desired class. They contain several surprising or at least undocumented results regarding the six DML and GRF leading cases:

-

1.

PLR(-IV), causal/instrumental forests, and Wald-AIPW are not fully-normalized in standard implementations because they usually apply different treatment and outcome models (C5 not fulfilled).

- 2.

4.4 Empirical Monte Carlo illustration

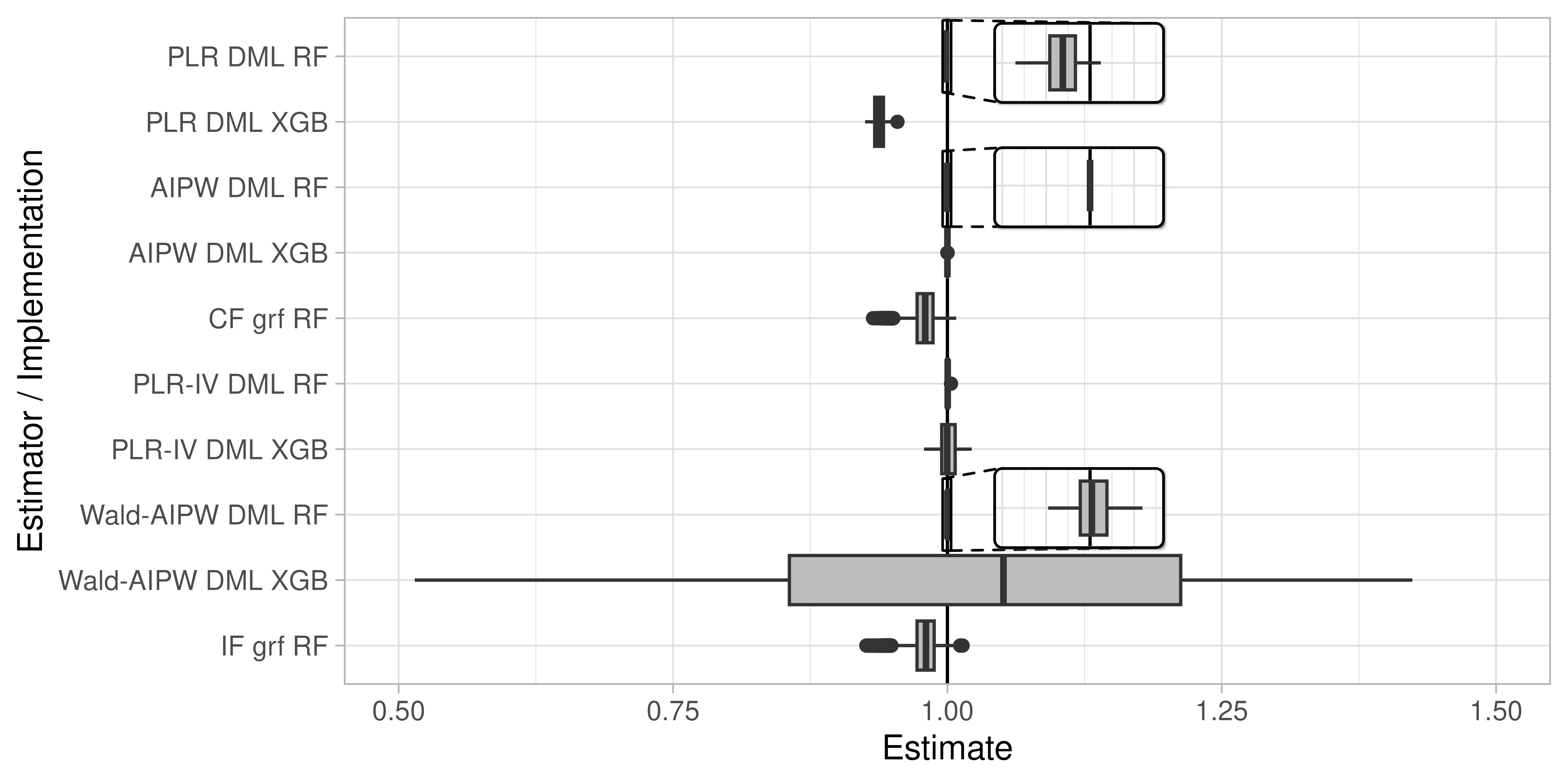

This section runs an Empirical Monte Carlo Study (EMCS) to illustrate that most standard implementations of DML and GRF are not fully-normalized. EMCS take a real dataset and modify some components such that the ground truth is known in the semi-synthetic dataset Huber \BOthers. (\APACyear2013); Wendling \BOthers. (\APACyear2018); Knaus \BOthers. (\APACyear2021). Here, we use the treatment, instrument, and covariates of the 401(k) data Chernozhukov \BOthers. (\APACyear2016) but with a noiseless outcome . This simulates the most powerful treatment leaving every untreated unit at one and shifting every treated unit to two. We expect estimators to estimate an effect of exactly one in this setting without outcome noise. However, only fully-normalized estimators are guaranteed to achieve this because for them, .

This exercise is run with the DoubleML Bach \BOthers. (\APACyear2024) and the grf Tibshirani \BOthers. (\APACyear2024) R packages applied to 100 bootstrap samples. The nuisance parameters in DoubleML are obtained using honest random forest (affine smoother) or XGBoost (non-affine smoother). Each function uses its default values. Table 6 summarizes the ten implementations under consideration. The final column shows whether an implementation is fully-normalized according to the theoretical results in Table 5 and therefore expected to find the “effect” of one.

| Label | Estimator | Package | Nuisance | Fully-normalized? |

| PLR DML RF | PLR | DoubleML | random forest |

no b/c |

| PLR DML XGB | PLR | DoubleML | XGBoost |

no b/c |

| AIPW DML RF | AIPW | DoubleML | random forest | yes |

| AIPW DML XGB | AIPW | DoubleML | XGBoost |

no b/c |

| CF grf RF | CF | grf | random forest |

no b/c |

| PLR-IV DML RF | PLR-IV | DoubleML | random forest |

no b/c |

| PLR-IV DML XGB | PLR-IV | DoubleML | XGBoost |

no b/c |

| Wald-AIPW DML RF | Wald-AIPW | DoubleML | random forest |

no b/c |

| Wald-AIPW DML XGB | Wald-AIPW | DoubleML | XGBoost |

no b/c |

| IF grf RF | IF | grf | random forest |

no b/c |

-

•

Notes: The final column provides details why the specific implementation are not expected to be fully-normalized.

Notes: Boxplots show the results of 100 bootstraps of the 401(k) data Chernozhukov \BOthers. (\APACyear2016) where the outcome is set to . The estimators are implemented using the default settings of the DoubleML and grf packages (see Table 6 for the labels). The causal/instrumental forest produces 9,915 estimates per replication such that their boxplots are based on million estimates. The simulated effect is always one indicated by the solid line. The shadowed boxes in rows 1, 3 and 9 zoom into the range between 0.996 and 1.003. 49 outliers of Wald-AIPW DML XGB ranging from -16 to 55 are omitted. See EMCS R notebook for the code and more details.

The theoretical predictions are confirmed in Figure 1. The boxplots show that only AIPW with an affine smoother finds an effect of exactly one in all bootstrap samples. The other methods deviate from one to varying degrees. The XGBoost Wald-AIPW stands out in estimating effects between -16 and 55 (the graph is truncated). However, also causal/instrumental forests estimate heterogeneous effects between 0.93 and 1.01 although there is no heterogeneity to be found in the provided data. This illustrates the theoretical findings even for DoubleML implementations where the extraction of the outcome weights is currently not possible because the required smoother matrices are not accessible.

5 Application: 401(k) covariate balancing

The novel outcome weights for DML and GRF can be used in established routines or to develop estimator-specific applications. We illustrate the former with covariate balancing, leaving the latter for future research. As in Section 4.4, we use the 401(k) data from \citeAChernozhukov2016High-DimensionalR, but this time with the real outcome “net assets”.

5.1 Average effects

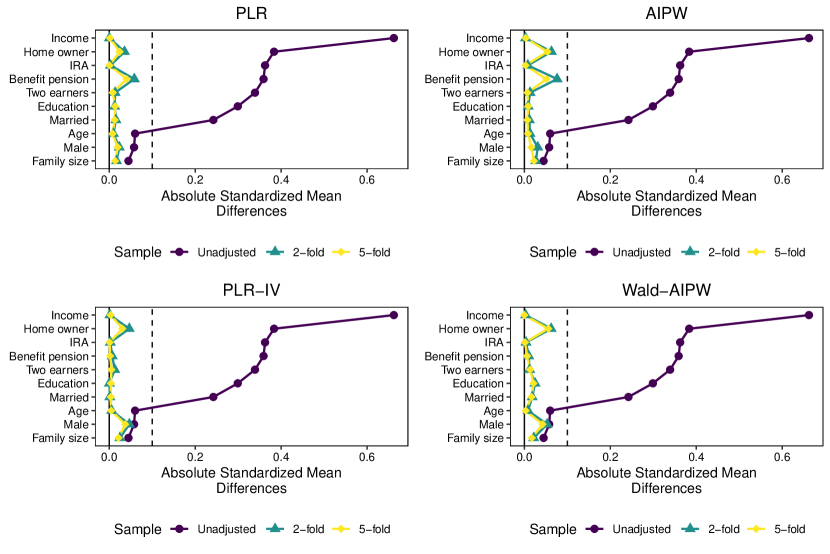

First, we investigate covariate balancing for DML estimated average effects. PLR(-IV) and (Wald-)AIPW are implemented using honest random forests with 2- and 5-fold cross-fitting. Figure 2 presents canonical balancing plots from the cobalt R package Greifer (\APACyear2024) displaying absolute standardized mean differences (SMD). We observe that each method successfully balances the previously unbalanced covariates, in particular the income variable. Furthermore, cross-fitting with 5-folds achieves better covariate balancing compared to 2-folds. This demonstrates how DML outcome weights can be utilized in the design phase described by \citeARubin2007TheTrials, allowing researchers to commit to the preferred implementation before examining the results.

The supplementary average effects R notebook also provides point estimates and additional results, such as showing that 10 cross-fitting folds provide no further improvement over 5 folds and that the scale-normalized weights sum to values close to one (0.995 and closer).

Notes: Each plot is created with the love.plot() function of the cobalt R package Greifer (\APACyear2024) and the weights derived in Section 3.

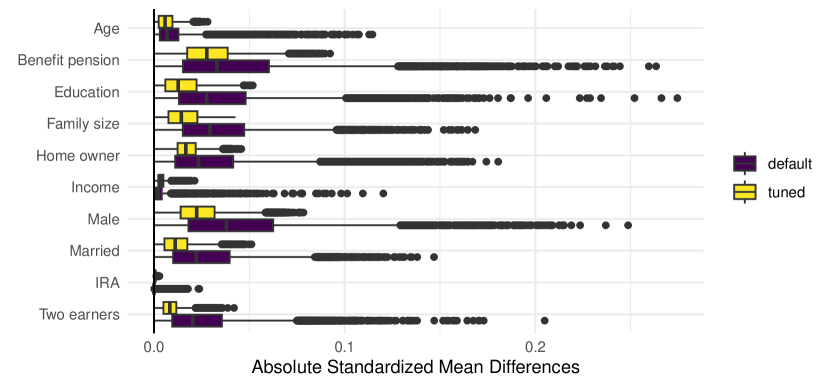

5.2 Causal forest

Checks like those in Figure 2 are standard when estimating average effects. Similarly, we can assess covariate balancing for all 9,915 conditional average treatment effects (CATEs) produced by causal forests. As an illustration, we investigate the importance of hyperparameter tuning for causal forests by comparing the default implementation with tune.parameters = "all". Figure 3 shows boxplots of absolute standardized mean differences. The results show that tuning the forests substantially improves covariate balancing in this application. The tuned version achieves absolute SMDs of 0.1 or lower, whereas the default settings frequently exceed this threshold, with some values even above 0.2. This highlights how standard diagnostics for average effects can also be applied to CATE estimates.

Notes: Boxplots of absolute standardized mean differences for conditional average treatment effects estimated by causal forest using the default and tuned hyperparameters.

The supplementary heterogeneous effects R notebook reveals that the imbalances in the default forest coincide with implausible effect sizes ranging from -$21k to $78k, whereas the tuned forest yields more plausible estimates between $8k and $23k. This highlights the importance of parameter tuning for causal forests in this application. A similar pattern is observed for the instrumental forest, though with higher levels of |SMD|.

The supplementary notebook additionally examines descriptive statistics of the outcome weights multiplied by to switch the sign of the untreated weights for better comparability. It documents that (i) both causal forests use negative weights, though to a limited extent, (ii) instrumental forests assign substantial negative weights to never-takers, consistent with the outcome weights in \citeAImbens1997EstimatingModels and the fact that the 401(k) has no always-takers by design, (iii) tuned forests use much smaller weights in absolute values, indicating more stable and reliable estimates, (iv) the sum of weights ranges from 0.98 to 1.02 for the default settings and from 0.995 to 1.005 for the tuned forest, making the tuned forest approximately fully-normalized in this application. Future work should explore whether this represents a general pattern.

6 Closing remarks

More estimators than previously noted can be expressed as weighted outcomes. The paper provides a general framework and derives novel weights for double machine learning and generalized random forest estimators. A key learning is that both availability and properties of the outcome weights depend on implementation choices and are therefore controlled by the user.

The paper focuses on providing general theoretical tools and standard illustrations. This acknowledges that access to their closed-form expressions is a prerequisite for developing new use cases or theoretical results for outcome weights. With the provided tools now available, many follow-up questions arise for future research:

-

•

Are there estimator specific use cases beyond the standard diagnostic tools?

-

•

What are the closed-form expressions and properties of other PIVE outcome weights?

-

•

Does the finding that several popular estimators do not use fully-normalized weights challenge the preference for such weights in the literature, or could explicitly normalizing the weights improve the finite sample performance of these estimators?

-

•

Does the need to restrict outcome predictors to smoothers for access to outcome weights suggest a trade-off between interpretability and performance for outcome adaptive causal effect estimators?

-

•

Do the provided outcome weights have implications for statistical inference, asymptotic properties, or double robustness robustness properties?

The investigation of the latter point most likely requires to restrict focus to analytically tractable smoothers in contrast to the generic smoothers allowed for in this paper. The fact that the smoothers and therefore the outcome weights may depend on the outcome pose non-trivial challenges. For example, it makes the outcome weights not compatible with approaches to use them for statistical inference as the existing approaches require outcome weights to be independent of the outcomes <e.g.>[Ch. 19]Imbens2015CausalSciences. Tailored sample splits as in \citeALechner2018 could ensure the required independence but explorations along these lines are left for future work.

References

- Abadie (\APACyear2003) \APACinsertmetastarAbadie2003SemiparametricModels{APACrefauthors}Abadie, A. \APACrefYear2003. \BBOQ\APACrefatitleSemiparametric instrumental variable estimation of treatment response models Semiparametric instrumental variable estimation of treatment response models.\BBCQ \APACjournalVolNumPagesJournal of Econometrics1132231–263. \PrintBackRefs\CurrentBib

- Abadie (\APACyear2021) \APACinsertmetastarAbadie2021UsingAspects{APACrefauthors}Abadie, A. \APACrefYear2021. \BBOQ\APACrefatitleUsing synthetic controls: Feasibility, data requirements, and methodological aspects Using synthetic controls: Feasibility, data requirements, and methodological aspects.\BBCQ \APACjournalVolNumPagesJournal of Economic Literature592391–425. \PrintBackRefs\CurrentBib

- Abadie \BBA Cattaneo (\APACyear2018) \APACinsertmetastarAbadie2018EconometricEvaluation{APACrefauthors}Abadie, A.\BCBT \BBA Cattaneo, M\BPBID. \APACrefYear2018. \BBOQ\APACrefatitleEconometric methods for program evaluation Econometric methods for program evaluation.\BBCQ \APACjournalVolNumPagesAnnual Review of Economics10465–503. \PrintBackRefs\CurrentBib

- Angrist (\APACyear1998) \APACinsertmetastarAngrist1998EstimatingApplicants{APACrefauthors}Angrist, J\BPBID. \APACrefYear1998. \BBOQ\APACrefatitleEstimating the labor market impact of voluntary military service using social security data on military applicants Estimating the labor market impact of voluntary military service using social security data on military applicants.\BBCQ \APACjournalVolNumPagesEconometrica662249–288. \PrintBackRefs\CurrentBib

- Angrist \BBA Imbens (\APACyear1995) \APACinsertmetastarAngrist1995Two-stageIntensity{APACrefauthors}Angrist, J\BPBID.\BCBT \BBA Imbens, G\BPBIW. \APACrefYear1995. \BBOQ\APACrefatitleTwo-stage least squares estimation of average causal effects in models with variable treatment intensity Two-stage least squares estimation of average causal effects in models with variable treatment intensity.\BBCQ \APACjournalVolNumPagesJournal of the American Statistical Association90430431–442. \PrintBackRefs\CurrentBib

- Angrist \BOthers. (\APACyear1996) \APACinsertmetastarAngrist1996IdentificationVariables{APACrefauthors}Angrist, J\BPBID., Imbens, G\BPBIW.\BCBL \BBA Rubin, D\BPBIB. \APACrefYear1996. \BBOQ\APACrefatitleIdentification of Causal Effects Using Instrumental Variables Identification of Causal Effects Using Instrumental Variables.\BBCQ \APACjournalVolNumPagesJournal of the American Statistical Association91434444–455. \PrintBackRefs\CurrentBib

- Angrist \BBA Krueger (\APACyear1999) \APACinsertmetastarAngrist1999EmpiricalEconomics{APACrefauthors}Angrist, J\BPBID.\BCBT \BBA Krueger, A\BPBIB. \APACrefYear1999. \BBOQ\APACrefatitleEmpirical strategies in labor economics Empirical strategies in labor economics.\BBCQ \BIn O\BPBIC. Ashenfelter \BBA D. Card (\BEDS), \APACrefbtitleHandbook of labor economics Handbook of labor economics (\BVOL 3A, \BPGS 1277–1366). \APACaddressPublisherElsevier. \PrintBackRefs\CurrentBib

- Armstrong \BBA Kolesár (\APACyear2021) \APACinsertmetastarArmstrong2021Finite-sampleUnconfoundedness{APACrefauthors}Armstrong, T\BPBIB.\BCBT \BBA Kolesár, M. \APACrefYear2021. \BBOQ\APACrefatitleFinite-sample optimal estimation and inference on average treatment effects under unconfoundedness Finite-sample optimal estimation and inference on average treatment effects under unconfoundedness.\BBCQ \APACjournalVolNumPagesEconometrica8931141–1177. \PrintBackRefs\CurrentBib

- Aronow \BBA Samii (\APACyear2016) \APACinsertmetastarAronow2016DoesEffects{APACrefauthors}Aronow, P\BPBIM.\BCBT \BBA Samii, C. \APACrefYear2016. \BBOQ\APACrefatitleDoes Regression Produce Representative Estimates of Causal Effects? Does Regression Produce Representative Estimates of Causal Effects?\BBCQ \APACjournalVolNumPagesAmerican Journal of Political Science601250–267. \PrintBackRefs\CurrentBib

- Athey \BBA Imbens (\APACyear2017) \APACinsertmetastarAthey2017{APACrefauthors}Athey, S.\BCBT \BBA Imbens, G\BPBIW. \APACrefYear2017. \BBOQ\APACrefatitleThe state of applied econometrics: causality and policy evaluation The state of applied econometrics: causality and policy evaluation.\BBCQ \APACjournalVolNumPagesJournal of Economic Perspectives3123–32. \PrintBackRefs\CurrentBib

- Athey \BOthers. (\APACyear2019) \APACinsertmetastarAthey2017a{APACrefauthors}Athey, S., Tibshirani, J.\BCBL \BBA Wager, S. \APACrefYear2019. \BBOQ\APACrefatitleGeneralized random forests Generalized random forests.\BBCQ \APACjournalVolNumPagesAnnals of Statistics4721148 - 1178. \PrintBackRefs\CurrentBib

- Athey \BBA Wager (\APACyear2019) \APACinsertmetastarAthey2019EstimatingApplication{APACrefauthors}Athey, S.\BCBT \BBA Wager, S. \APACrefYear2019. \BBOQ\APACrefatitleEstimating treatment effects with causal forests: An application Estimating treatment effects with causal forests: An application.\BBCQ \APACjournalVolNumPagesObservational Studies5237–51. \PrintBackRefs\CurrentBib

- Bach \BOthers. (\APACyear2024) \APACinsertmetastarBach2024DoubleML:R{APACrefauthors}Bach, P., Kurz, M\BPBIS., Chernozhukov, V., Spindler, M.\BCBL \BBA Klaassen, S. \APACrefYear2024. \BBOQ\APACrefatitleDoubleML: An object-oriented implementation of double machine learning in R DoubleML: An object-oriented implementation of double machine learning in R.\BBCQ \APACjournalVolNumPagesJournal of Statistical Software10831–56. \PrintBackRefs\CurrentBib

- Ben-Michael \BOthers. (\APACyear2021) \APACinsertmetastarBen-Michael2021TheInference{APACrefauthors}Ben-Michael, E., Feller, A., Hirshberg, D\BPBIA.\BCBL \BBA Zubizarreta, J\BPBIR. \APACrefYear2021. \APACrefbtitleThe balancing act in causal inference. The balancing act in causal inference. {APACrefURL} http://arxiv.org/abs/2110.14831 \PrintBackRefs\CurrentBib

- Blandhol \BOthers. (\APACyear2022) \APACinsertmetastarBlandhol2022WhenLate{APACrefauthors}Blandhol, C., Bonney, J., Mogstad, M.\BCBL \BBA Torgovitsky, A. \APACrefYear2022. \BBOQ\APACrefatitleWhen is Tsls Actually Late? When is Tsls Actually Late?\BBCQ \APACjournalVolNumPagesSSRN Electronic Journal. {APACrefDOI} \doi10.2139/ssrn.4021804 \PrintBackRefs\CurrentBib

- Breitung \BOthers. (\APACyear2024) \APACinsertmetastarBreitung2024AlternativeDesigns{APACrefauthors}Breitung, J., Bolwin, L.\BCBL \BBA Töns, J. \APACrefYear2024. \APACrefbtitleAlternative approaches for estimation and inference in synthetic control designs. Alternative approaches for estimation and inference in synthetic control designs. \PrintBackRefs\CurrentBib

- Bruns-Smith \BOthers. (\APACyear2023) \APACinsertmetastarBruns-Smith2023AugmentedRegression{APACrefauthors}Bruns-Smith, D., Dukes, O., Feller, A.\BCBL \BBA Ogburn, E\BPBIL. \APACrefYear2023. \APACrefbtitleAugmented balancing weights as linear regression. Augmented balancing weights as linear regression. {APACrefURL} http://arxiv.org/abs/2304.14545 \PrintBackRefs\CurrentBib

- Buja \BOthers. (\APACyear1989) \APACinsertmetastarBuja1989LinearModels{APACrefauthors}Buja, A., Hastie, T.\BCBL \BBA Tibshirani, R. \APACrefYear1989. \BBOQ\APACrefatitleLinear smoothers and additive models Linear smoothers and additive models.\BBCQ \APACjournalVolNumPagesThe Annals of Statistics172453–510. \PrintBackRefs\CurrentBib

- Busso \BOthers. (\APACyear2014) \APACinsertmetastarbusso2014new{APACrefauthors}Busso, M., DiNardo, J.\BCBL \BBA McCrary, J. \APACrefYear2014. \BBOQ\APACrefatitleNew evidence on the finite sample properties of propensity score reweighting and matching estimators New evidence on the finite sample properties of propensity score reweighting and matching estimators.\BBCQ \APACjournalVolNumPagesReview of Economics and Statistics965885–897. \PrintBackRefs\CurrentBib

- Chattopadhyay \BBA Zubizarreta (\APACyear2021) \APACinsertmetastarChattopadhyay2021OnInference{APACrefauthors}Chattopadhyay, A.\BCBT \BBA Zubizarreta, J\BPBIR. \APACrefYear2021. \APACrefbtitleOn the implied weights of linear regression for causal inference. On the implied weights of linear regression for causal inference. {APACrefURL} http://arxiv.org/abs/2104.06581v2 \PrintBackRefs\CurrentBib

- Chattopadhyay \BBA Zubizarreta (\APACyear2023) \APACinsertmetastarChattopadhyay2023OnInference{APACrefauthors}Chattopadhyay, A.\BCBT \BBA Zubizarreta, J\BPBIR. \APACrefYear2023. \BBOQ\APACrefatitleOn the implied weights of linear regression for causal inference On the implied weights of linear regression for causal inference.\BBCQ \APACjournalVolNumPagesBiometrika1103615–629. \PrintBackRefs\CurrentBib

- Chernozhukov \BOthers. (\APACyear2018) \APACinsertmetastarChernozhukov2018{APACrefauthors}Chernozhukov, V., Chetverikov, D., Demirer, M., Duflo, E., Hansen, C., Newey, W.\BCBL \BBA Robins, J. \APACrefYear2018. \BBOQ\APACrefatitleDouble/Debiased machine learning for treatment and structural parameters Double/Debiased machine learning for treatment and structural parameters.\BBCQ \APACjournalVolNumPagesThe Econometrics Journal211C1-C68. \PrintBackRefs\CurrentBib

- Chernozhukov \BOthers. (\APACyear2013) \APACinsertmetastarChernozhukov2013AverageModels{APACrefauthors}Chernozhukov, V., Fernández-Val, I., Hahn, J.\BCBL \BBA Newey, W. \APACrefYear2013. \BBOQ\APACrefatitleAverage and Quantile Effects in Nonseparable Panel Models Average and Quantile Effects in Nonseparable Panel Models.\BBCQ \APACjournalVolNumPagesEconometrica812535–580. \PrintBackRefs\CurrentBib

- Chernozhukov \BOthers. (\APACyear2024) \APACinsertmetastarChernozhukov2024AppliedAI{APACrefauthors}Chernozhukov, V., Hansen, C., Kallus, N., Spindler, M.\BCBL \BBA Syrgkanis, V. \APACrefYear2024. \APACrefbtitleApplied Causal Inference Powered by ML and AI Applied Causal Inference Powered by ML and AI. \APACaddressPublisherforthcoming. \PrintBackRefs\CurrentBib

- Chernozhukov \BOthers. (\APACyear2016) \APACinsertmetastarChernozhukov2016High-DimensionalR{APACrefauthors}Chernozhukov, V., Hansen, C.\BCBL \BBA Spindler, M. \APACrefYear2016. \APACrefbtitleHigh-Dimensional Metrics in R. High-Dimensional Metrics in R. {APACrefURL} http://arxiv.org/abs/1603.01700 \PrintBackRefs\CurrentBib

- Curth \BOthers. (\APACyear2023) \APACinsertmetastarCurth2023ALearning{APACrefauthors}Curth, A., Jeffares, A.\BCBL \BBA van der Schaar, M. \APACrefYear2023. \BBOQ\APACrefatitleA U-turn on double descent: Rethinking parameter counting in statistical learning A U-turn on double descent: Rethinking parameter counting in statistical learning.\BBCQ \BIn \APACrefbtitleThirty-seventh Conference on Neural Information Processing Systems. Thirty-seventh conference on neural information processing systems. \PrintBackRefs\CurrentBib

- Curth \BOthers. (\APACyear2024) \APACinsertmetastarCurth2024WhySmoothers{APACrefauthors}Curth, A., Jeffares, A.\BCBL \BBA van der Schaar, M. \APACrefYear2024. \APACrefbtitleWhy do random forests work? Understanding tree ensembles as self-regularizing adaptive smoothers. Why do random forests work? Understanding tree ensembles as self-regularizing adaptive smoothers. {APACrefURL} https://arxiv.org/abs/2402.01502v1 \PrintBackRefs\CurrentBib

- de Chaisemartin \BBA D’Haultfœuille (\APACyear2023) \APACinsertmetastardeChaisemartin2023Two-waySurvey{APACrefauthors}de Chaisemartin, C.\BCBT \BBA D’Haultfœuille, X. \APACrefYear2023. \BBOQ\APACrefatitleTwo-way fixed effects and differences-in-differences with heterogeneous treatment effects: a survey Two-way fixed effects and differences-in-differences with heterogeneous treatment effects: a survey.\BBCQ \APACjournalVolNumPagesEconometrics Journal263C1-C30. \PrintBackRefs\CurrentBib

- Doudchenko \BBA Imbens (\APACyear2016) \APACinsertmetastarDoudchenko2016BalancingSynthesis{APACrefauthors}Doudchenko, N.\BCBT \BBA Imbens, G\BPBIW. \APACrefYear2016. \APACrefbtitleBalancing, regression, difference-in-differences and synthetic control methods: A synthesis. Balancing, regression, difference-in-differences and synthetic control methods: A synthesis. {APACrefURL} https://arxiv.org/abs/1610.07748 \PrintBackRefs\CurrentBib

- Goldsmith-Pinkham \BOthers. (\APACyear2021) \APACinsertmetastarGoldsmith-Pinkham2021ContaminationRegressions{APACrefauthors}Goldsmith-Pinkham, P., Hull, P.\BCBL \BBA Kolesár, M. \APACrefYear2021. \APACrefbtitleContamination bias in linear regressions. Contamination bias in linear regressions. {APACrefURL} http://arxiv.org/abs/2106.05024 \PrintBackRefs\CurrentBib

- Graham \BOthers. (\APACyear2012) \APACinsertmetastarGraham2012InverseData{APACrefauthors}Graham, B\BPBIS., Pinto, C\BPBIC\BPBId\BPBIX.\BCBL \BBA Egel, D. \APACrefYear2012. \BBOQ\APACrefatitleInverse probability tilting for moment condition models with missing data Inverse probability tilting for moment condition models with missing data.\BBCQ \APACjournalVolNumPagesReview of Economic Studies7931053–1079. \PrintBackRefs\CurrentBib

- Greifer (\APACyear2024) \APACinsertmetastarGreifer2024Cobalt:Plots{APACrefauthors}Greifer, N. \APACrefYear2024. \APACrefbtitlecobalt: Covariate Balance Tables and Plots. cobalt: Covariate Balance Tables and Plots. \APACaddressPublisherR package version 4.5.5.9000. {APACrefURL} https://github.com/ngreifer/cobalt \PrintBackRefs\CurrentBib

- Hainmueller (\APACyear2012) \APACinsertmetastarHainmueller2012EntropyStudies{APACrefauthors}Hainmueller, J. \APACrefYear2012. \BBOQ\APACrefatitleEntropy balancing for causal effects: A multivariate reweighting method to produce balanced samples in observational studies Entropy balancing for causal effects: A multivariate reweighting method to produce balanced samples in observational studies.\BBCQ \APACjournalVolNumPagesPolitical Analysis20125–46. \PrintBackRefs\CurrentBib

- Hájek (\APACyear1971) \APACinsertmetastarHajek1971CommentOne{APACrefauthors}Hájek, J. \APACrefYear1971. \BBOQ\APACrefatitleComment on “An essay on the logical foundations of survey sampling, part one” Comment on “An essay on the logical foundations of survey sampling, part one”.\BBCQ \BIn V\BPBIP. Godambe \BBA D\BPBIA. Sprott (\BEDS), \APACrefbtitleFoundations of Statistical Inference Foundations of statistical inference (\BPG 236). \APACaddressPublisherTorontoHolt, Rinehart and Winston. \PrintBackRefs\CurrentBib

- Hastie \BBA Tibshirani (\APACyear1990) \APACinsertmetastarHastie1990GeneralizedModels{APACrefauthors}Hastie, T.\BCBT \BBA Tibshirani, R. \APACrefYear1990. \BBOQ\APACrefatitleGeneralized additive models Generalized additive models.\BBCQ \APACjournalVolNumPagesMonographs on Statistics and Applied Probability43. \PrintBackRefs\CurrentBib

- Hazlett \BBA Shinkre (\APACyear2024) \APACinsertmetastarHazlett2024UnderstandingSolutions{APACrefauthors}Hazlett, C.\BCBT \BBA Shinkre, T. \APACrefYear2024. \APACrefbtitleUnderstanding and avoiding the "weights of regression": Heterogeneous effects, misspecification, and longstanding solutions. Understanding and avoiding the "weights of regression": Heterogeneous effects, misspecification, and longstanding solutions. {APACrefURL} https://arxiv.org/abs/2403.03299 \PrintBackRefs\CurrentBib

- Heckman \BBA Vytlacil (\APACyear2005) \APACinsertmetastarHeckman2005StructuralEvaluation{APACrefauthors}Heckman, J\BPBIJ.\BCBT \BBA Vytlacil, E. \APACrefYear2005. \BBOQ\APACrefatitleStructural equations, treatment effects, and econometric policy evaluation Structural equations, treatment effects, and econometric policy evaluation.\BBCQ \APACjournalVolNumPagesEconometrica733669–738. \PrintBackRefs\CurrentBib

- Heiler (\APACyear2022) \APACinsertmetastarHeiler2022EfficientEffect{APACrefauthors}Heiler, P. \APACrefYear2022. \BBOQ\APACrefatitleEfficient covariate balancing for the local average treatment effect Efficient covariate balancing for the local average treatment effect.\BBCQ \APACjournalVolNumPagesJournal of Business and Economic Statistics4041569–1582. \PrintBackRefs\CurrentBib

- Horvitz \BBA Thompson (\APACyear1952) \APACinsertmetastarHorvitz1952{APACrefauthors}Horvitz, D\BPBIG.\BCBT \BBA Thompson, D\BPBIJ. \APACrefYear1952. \BBOQ\APACrefatitleA generalization of sampling without replacement from a finite universe A generalization of sampling without replacement from a finite universe.\BBCQ \APACjournalVolNumPagesJournal of the American statistical Association47260663–685. \PrintBackRefs\CurrentBib

- Huber \BOthers. (\APACyear2013) \APACinsertmetastarHuber2013{APACrefauthors}Huber, M., Lechner, M.\BCBL \BBA Wunsch, C. \APACrefYear2013. \BBOQ\APACrefatitleThe performance of estimators based on the propensity score The performance of estimators based on the propensity score.\BBCQ \APACjournalVolNumPagesJournal of Econometrics17511–21. \PrintBackRefs\CurrentBib

- Humphreys (\APACyear2009) \APACinsertmetastarHumphreys2009BoundsProbabilities{APACrefauthors}Humphreys, M. \APACrefYear2009. \APACrefbtitleBounds on least squares estimates of causal effects in the presence of heterogeneous assignment probabilities. Bounds on least squares estimates of causal effects in the presence of heterogeneous assignment probabilities. \PrintBackRefs\CurrentBib

- Imai \BBA Ratkovic (\APACyear2014) \APACinsertmetastarImai2014CovariateScore{APACrefauthors}Imai, K.\BCBT \BBA Ratkovic, M. \APACrefYear2014. \BBOQ\APACrefatitleCovariate balancing propensity score Covariate balancing propensity score.\BBCQ \APACjournalVolNumPagesJournal of the Royal Statistical Society: Series B761243–263. \PrintBackRefs\CurrentBib

- Imbens (\APACyear2004) \APACinsertmetastarImbens2004NonparametricReview{APACrefauthors}Imbens, G\BPBIW. \APACrefYear2004. \BBOQ\APACrefatitleNonparametric estimation of average treatment effects under exogeneity: A review Nonparametric estimation of average treatment effects under exogeneity: A review.\BBCQ \APACjournalVolNumPagesReview of Economics and Statistics8614–29. \PrintBackRefs\CurrentBib

- Imbens (\APACyear2015) \APACinsertmetastarImbens2015MatchingExamples{APACrefauthors}Imbens, G\BPBIW. \APACrefYear2015. \BBOQ\APACrefatitleMatching methods in practice: Three examples Matching methods in practice: Three examples.\BBCQ \APACjournalVolNumPagesJournal of Human Resources502373–419. {APACrefDOI} \doi10.3368/jhr.50.2.373 \PrintBackRefs\CurrentBib

- Imbens (\APACyear2024) \APACinsertmetastarImbens2024CausalSciences{APACrefauthors}Imbens, G\BPBIW. \APACrefYear2024. \BBOQ\APACrefatitleCausal Inference in the Social Sciences Causal Inference in the Social Sciences.\BBCQ \APACjournalVolNumPagesAnnual Review of Statistics and Its Application11123–152. \PrintBackRefs\CurrentBib

- Imbens \BBA Angrist (\APACyear1994) \APACinsertmetastarImbens1994IdentificationEffects{APACrefauthors}Imbens, G\BPBIW.\BCBT \BBA Angrist, J\BPBID. \APACrefYear1994. \BBOQ\APACrefatitleIdentification and estimation of local average treatment effects Identification and estimation of local average treatment effects.\BBCQ \APACjournalVolNumPagesEconometrica622467–475. \PrintBackRefs\CurrentBib

- Imbens \BBA Rubin (\APACyear1997) \APACinsertmetastarImbens1997EstimatingModels{APACrefauthors}Imbens, G\BPBIW.\BCBT \BBA Rubin, D\BPBIB. \APACrefYear1997. \BBOQ\APACrefatitleEstimating Outcome Distributions for Compliers in Instrumental Variables Models Estimating Outcome Distributions for Compliers in Instrumental Variables Models.\BBCQ \APACjournalVolNumPagesReview of Economic Studies644555–574. \PrintBackRefs\CurrentBib

- Imbens \BBA Rubin (\APACyear2015) \APACinsertmetastarImbens2015CausalSciences{APACrefauthors}Imbens, G\BPBIW.\BCBT \BBA Rubin, D\BPBIB. \APACrefYear2015. \APACrefbtitleCausal inference in statistics, social, and biomedical sciences Causal inference in statistics, social, and biomedical sciences. \APACaddressPublisherCambridge University Press. \PrintBackRefs\CurrentBib

- Imbens \BBA Wooldridge (\APACyear2009) \APACinsertmetastarImbens2009{APACrefauthors}Imbens, G\BPBIW.\BCBT \BBA Wooldridge, J\BPBIM. \APACrefYear2009. \BBOQ\APACrefatitleRecent developments in the econometrics of program evaluation Recent developments in the econometrics of program evaluation.\BBCQ \APACjournalVolNumPagesJournal of Economic Literature4715–86. \PrintBackRefs\CurrentBib

- Jakiela (\APACyear2021) \APACinsertmetastarJakiela2021SimpleEffects{APACrefauthors}Jakiela, P. \APACrefYear2021. \APACrefbtitleSimple diagnostics for two-way fixed effects. Simple diagnostics for two-way fixed effects. {APACrefURL} https://arxiv.org/abs/2103.13229v1 {APACrefDOI} \doi10.48550/arxiv.2103.13229 \PrintBackRefs\CurrentBib

- Kallus (\APACyear2020) \APACinsertmetastarKallus2020GeneralizedInference{APACrefauthors}Kallus, N. \APACrefYear2020. \BBOQ\APACrefatitleGeneralized optimal matching methods for causal inference Generalized optimal matching methods for causal inference.\BBCQ \APACjournalVolNumPagesJournal of Machine Learning Research21621–54. \PrintBackRefs\CurrentBib

- Khan \BBA Ugander (\APACyear2023) \APACinsertmetastarKhan2023AdaptiveEstimation{APACrefauthors}Khan, S.\BCBT \BBA Ugander, J. \APACrefYear2023. \BBOQ\APACrefatitleAdaptive normalization for IPW estimation Adaptive normalization for IPW estimation.\BBCQ \APACjournalVolNumPagesJournal of Causal Inference111. \PrintBackRefs\CurrentBib

- Kline (\APACyear2011) \APACinsertmetastarKline2011Oaxaca-BlinderEstimator{APACrefauthors}Kline, P. \APACrefYear2011. \BBOQ\APACrefatitleOaxaca-Blinder as a reweighting estimator Oaxaca-Blinder as a reweighting estimator.\BBCQ \APACjournalVolNumPagesAmerican Economic Review1013532–537. \PrintBackRefs\CurrentBib

- Knaus (\APACyear2021) \APACinsertmetastarKnaus2021ASkills{APACrefauthors}Knaus, M\BPBIC. \APACrefYear2021. \BBOQ\APACrefatitleA double machine learning approach to estimate the effects of musical practice on student’s skills A double machine learning approach to estimate the effects of musical practice on student’s skills.\BBCQ \APACjournalVolNumPagesJournal of the Royal Statistical Society. Series A: Statistics in Society1841282–300. \PrintBackRefs\CurrentBib

- Knaus (\APACyear2024) \APACinsertmetastarKnaus2024OutcomeWeights{APACrefauthors}Knaus, M\BPBIC. \APACrefYear2024. \APACrefbtitleOutcomeWeights. OutcomeWeights. \APACaddressPublisherR package version 0.1.0. {APACrefURL} https://github.com/MCKnaus/OutcomeWeights \PrintBackRefs\CurrentBib

- Knaus \BOthers. (\APACyear2021) \APACinsertmetastarKnaus2021{APACrefauthors}Knaus, M\BPBIC., Lechner, M.\BCBL \BBA Strittmatter, A. \APACrefYear2021. \BBOQ\APACrefatitleMachine learning estimation of heterogeneous causal effects: Empirical monte carlo evidence Machine learning estimation of heterogeneous causal effects: Empirical monte carlo evidence.\BBCQ \APACjournalVolNumPagesThe Econometrics Journal241134–161. \PrintBackRefs\CurrentBib

- Lechner (\APACyear2018) \APACinsertmetastarLechner2018{APACrefauthors}Lechner, M. \APACrefYear2018. \BBOQ\APACrefatitleModified causal forests for estimating heterogeneous causal effects Modified causal forests for estimating heterogeneous causal effects.\BBCQ \APACjournalVolNumPagesarXiv:1812.09487. {APACrefURL} https://arxiv.org/abs/1812.09487 \PrintBackRefs\CurrentBib

- Lechner \BBA Strittmatter (\APACyear2019) \APACinsertmetastarLechner2019PracticalEstimation{APACrefauthors}Lechner, M.\BCBT \BBA Strittmatter, A. \APACrefYear2019. \BBOQ\APACrefatitlePractical procedures to deal with common support problems in matching estimation Practical procedures to deal with common support problems in matching estimation.\BBCQ \APACjournalVolNumPagesEconometric Reviews382193–207. \PrintBackRefs\CurrentBib

- Lee \BBA Lemieux (\APACyear2010) \APACinsertmetastarLee2010RegressionEconomics{APACrefauthors}Lee, D\BPBIS.\BCBT \BBA Lemieux, T. \APACrefYear2010. \BBOQ\APACrefatitleRegression discontinuity designs in economics Regression discontinuity designs in economics.\BBCQ \APACjournalVolNumPagesJournal of Economic Literature201281–355. \PrintBackRefs\CurrentBib

- Lin \BBA Han (\APACyear2022) \APACinsertmetastarLin2022OnEffect{APACrefauthors}Lin, Z.\BCBT \BBA Han, F. \APACrefYear2022. \APACrefbtitleOn regression-adjusted imputation estimators of the average treatment effect. On regression-adjusted imputation estimators of the average treatment effect. {APACrefURL} https://arxiv.org/abs/2212.05424v2 \PrintBackRefs\CurrentBib

- Robins \BBA Rotnitzky (\APACyear1995) \APACinsertmetastarRobins1995SemiparametricData{APACrefauthors}Robins, J\BPBIM.\BCBT \BBA Rotnitzky, A. \APACrefYear1995. \BBOQ\APACrefatitleSemiparametric efficiency in multivariate regression models with missing data Semiparametric efficiency in multivariate regression models with missing data.\BBCQ \APACjournalVolNumPagesJournal of the American Statistical Association90429122–129. \PrintBackRefs\CurrentBib

- Robins \BOthers. (\APACyear1994) \APACinsertmetastarRobins1994{APACrefauthors}Robins, J\BPBIM., Rotnitzky, A.\BCBL \BBA Zhao, L\BPBIP. \APACrefYear1994. \BBOQ\APACrefatitleEstimation of regression coefficients when some regressors are not always observed Estimation of regression coefficients when some regressors are not always observed.\BBCQ \APACjournalVolNumPagesJournal of the American Statistical Association89427846–866. \PrintBackRefs\CurrentBib

- Robins \BOthers. (\APACyear1995) \APACinsertmetastarRobins1995AnalysisData{APACrefauthors}Robins, J\BPBIM., Rotnitzky, A.\BCBL \BBA Zhao, L\BPBIP. \APACrefYear1995. \BBOQ\APACrefatitleAnalysis of semiparametric regression models for repeated outcomes in the presence of missing data Analysis of semiparametric regression models for repeated outcomes in the presence of missing data.\BBCQ \APACjournalVolNumPagesJournal of the American Statistical Association90429106–121. \PrintBackRefs\CurrentBib

- Robinson (\APACyear1988) \APACinsertmetastarRobinson1988Root-n-consistentRegression{APACrefauthors}Robinson, P\BPBIM. \APACrefYear1988. \BBOQ\APACrefatitleRoot-n-consistent semiparametric regression Root-n-consistent semiparametric regression.\BBCQ \APACjournalVolNumPagesEconometrica564931. \PrintBackRefs\CurrentBib

- Rosenbaum \BBA Rubin (\APACyear1984) \APACinsertmetastarRosenbaum1984ReducingScore{APACrefauthors}Rosenbaum, P\BPBIR.\BCBT \BBA Rubin, D\BPBIB. \APACrefYear1984. \BBOQ\APACrefatitleReducing bias in observational studies using subclassification on the propensity score Reducing bias in observational studies using subclassification on the propensity score.\BBCQ \APACjournalVolNumPagesJournal of the American Statistical Association79387516–524. \PrintBackRefs\CurrentBib

- Rosenbaum \BBA Rubin (\APACyear1985) \APACinsertmetastarRosenbaum1985ConstructingScore{APACrefauthors}Rosenbaum, P\BPBIR.\BCBT \BBA Rubin, D\BPBIB. \APACrefYear1985. \BBOQ\APACrefatitleConstructing a control group using multivariate matched sampling methods that incorporate the propensity score Constructing a control group using multivariate matched sampling methods that incorporate the propensity score.\BBCQ \APACjournalVolNumPagesThe American Statistician39133–38. \PrintBackRefs\CurrentBib

- Roth \BOthers. (\APACyear2023) \APACinsertmetastarRoth2023WhatsLiterature{APACrefauthors}Roth, J., Sant’Anna, P\BPBIH., Bilinski, A.\BCBL \BBA Poe, J. \APACrefYear2023. \BBOQ\APACrefatitleWhat’s trending in difference-in-differences? A synthesis of the recent econometrics literature What’s trending in difference-in-differences? A synthesis of the recent econometrics literature.\BBCQ \APACjournalVolNumPagesJournal of Econometrics23522218–2244. \PrintBackRefs\CurrentBib

- Rotnitzky \BOthers. (\APACyear1998) \APACinsertmetastarRotnitzky1998SemiparametricNonresponse{APACrefauthors}Rotnitzky, A., Robins, J\BPBIM.\BCBL \BBA Scharfstein, D\BPBIO. \APACrefYear1998. \BBOQ\APACrefatitleSemiparametric regression for repeated outcomes with nonignorable nonresponse Semiparametric regression for repeated outcomes with nonignorable nonresponse.\BBCQ \APACjournalVolNumPagesJournal of the American Statistical Association934441321–1339. \PrintBackRefs\CurrentBib

- Rubin (\APACyear2007) \APACinsertmetastarRubin2007TheTrials{APACrefauthors}Rubin, D\BPBIB. \APACrefYear2007. \BBOQ\APACrefatitleThe design versus the analysis of observational studies for causal effects: Parallels with the design of randomized trials The design versus the analysis of observational studies for causal effects: Parallels with the design of randomized trials.\BBCQ \APACjournalVolNumPagesStatistics in Medicine26120–36. \PrintBackRefs\CurrentBib

- Słoczyński (\APACyear2020) \APACinsertmetastarSoczynski2020WhenLATEb{APACrefauthors}Słoczyński, T. \APACrefYear2020. \APACrefbtitleWhen should we (not) interpret linear IV estimands as LATE? When should we (not) interpret linear IV estimands as LATE? {APACrefURL} http://arxiv.org/abs/2011.06695 \PrintBackRefs\CurrentBib

- Słoczyński (\APACyear2022) \APACinsertmetastarSoczynski2022InterpretingWeights{APACrefauthors}Słoczyński, T. \APACrefYear2022. \BBOQ\APACrefatitleInterpreting OLS estimands when treatment effects are heterogeneous: Smaller groups get larger weights Interpreting OLS estimands when treatment effects are heterogeneous: Smaller groups get larger weights.\BBCQ \APACjournalVolNumPagesReview of Economics and Statistics1043501–509. \PrintBackRefs\CurrentBib

- Słoczyński \BOthers. (\APACyear2023) \APACinsertmetastarSoczynski2023CovariateEffects{APACrefauthors}Słoczyński, T., Uysal, S\BPBID.\BCBL \BBA Wooldridge, J\BPBIM. \APACrefYear2023. \APACrefbtitleCovariate balancing and the equivalence of weighting and doubly robust estimators of average treatment effects. Covariate balancing and the equivalence of weighting and doubly robust estimators of average treatment effects. {APACrefURL} https://arxiv.org/abs/2310.18563 \PrintBackRefs\CurrentBib