*

Optimisation Strategies for Ensuring Fairness in Machine Learning:

With and Without Demographics

Abstract

Ensuring fairness has emerged as one of the primary concerns in Artificial Intelligence (AI)and its related algorithms. Over time, the field of machine learning fairness has evolved to address these issues. This paper provides an extensive overview of this field and introduces two formal frameworks to tackle open questions in machine learning fairness.

In one framework, operator-valued optimisation and min-max objectives are employed to address unfairness in time-series problems. This approach showcases state-of-the-art performance on the notorious Correctional Offender Management Profiling for Alternative Sanctions (COMPAS)benchmark dataset, demonstrating its effectiveness in real-world scenarios.

In the second framework, the challenge of lacking sensitive attributes, such as gender and race, in commonly used datasets is addressed. This issue is particularly pressing because existing algorithms in this field predominantly rely on the availability or estimations of such attributes to assess and mitigate unfairness. Here, a framework for a group-blind bias-repair is introduced, aiming to mitigate bias without relying on sensitive attributes. The efficacy of this approach is showcased through analyses conducted on the Adult Census Income dataset.

Additionally, detailed algorithmic analyses for both frameworks are provided, accompanied by convergence guarantees, ensuring the robustness and reliability of the proposed methodologies.

Statement of Originality

The work is my own and that all else is appropriately referenced.

Copyright Declaration

The copyright of this thesis rests with the author. Unless otherwise indicated, its contents are licensed under a Creative Commons Attribution-Non Commercial 4.0 International Licence (CC BY-NC).

Under this licence, you may copy and redistribute the material in any medium or format. You may also create and distribute modified versions of the work. This is on the condition that: you credit the author and do not use it, or any derivative works, for a commercial purpose.

When reusing or sharing this work, ensure you make the licence terms clear to others by naming the licence and linking to the licence text. Where a work has been adapted, you should indicate that the work has been changed and describe those changes.

Please seek permission from the copyright holder for uses of this work that are not included in this licence or permitted under UK Copyright Law.

Acknowledgements

First and foremost, I am deeply grateful to my PhD advisers, Prof. Robert Shorten and Dr. Jakub Mareček, for their unwavering guidance, encouragement, and expertise.

I am grateful for the mentorship of Dr. Jakub Mareček, who has been my master thesis advisor at University of Edinburgh, who has shown me the wonders of research during the three-month master thesis project, and who is one of the reasons why I decided to pursue a PhD. I am likewise grateful for the guidance and support I have received across all aspects of my life during the PhD program. Especially during the challenging period of COVID-19 pandemic, it was often difficult to maintain focus on research and stay positive emotionally, but the mentorship has been a constant source of strength and encouragement. The two-month visit to Czech Technical University in Prague has been really enjoyable.

I am grateful to Prof. Robert Shorten for providing me with the opportunity to pursue a PhD at University College Dublin, as well as the chances to visit and transfer to Imperial College London. Thanks to the guidance that I received, I discovered my core area of interest, and constantly found myself “flowing” in the research111Pioneered by Prof. Mihaly Csikszentmihalyi, Flow describes a state in which individuals become fully involved in an activity, often to the extent that they are willing to continue despite significant challenges., which thrived on the encouragement for independent research, and was nurtured by care for daily life concerns, e.g., housing and health insurance. My research benefited greatly from the motivation to upskill and the pondering of “what if” and “why”, often ignited by the exceptional vision and insightful comments during our discussions. The dedicated attitude has helped me establish the goal of “going deeper”, and continuous reinforcement of this belief has brought out the best in me.

I extend my heartfelt appreciation to my colleagues and collaborators Aida Manzano Kharman, Christian Jursitzky, Pietro Ferraro, Pierre Pinson, Ramen Ghosh, Mengjia Niu, Xiaoyu He, and Petr Ryšavý, for their camaraderie, intellectual discussions, and support. I am thankful to the financial support by the Science Foundation Ireland, the European Union’s Horizon Europe research and innovation programme, as well as the Innovate UK under the Horizon Europe Guarantee. My sincere appreciation goes to my friends and family for their consistent encouragement and love throughout this journey.

Last but not least, I wish I could contribute something to science.

Acronyms

- AI

- Artificial Intelligence

- AR

- Auto-Regressive

- ARMA

- Auto-Regressive Moving-Average

- COMPAS

- Correctional Offender Management Profiling for Alternative Sanctions

- EU

- European Union

- GDPR

- General Data Protection Regulation

- GMP

- Generalised Moment Problem

- GNS

- Gelfand–Naimark–Segal

- KL

- Kullback–Leibler

- LDS

- Linear Dynamic System

- MAR

- Missing At Random

- MCAR

- Missing Completely At Random

- MNAR

- Missing Not At Random

- NCPOP

- Non-Commutative Polynomial Optimisation Problem

- NPA

- Navascués–Pironio–Acín

- nrmse

- Normalised Root Mean Square Error

- OT

- Optimal Transport

- POP

- Polynomial Optimisation Problem

- SDP

- Semi-Definite Programming

- TSSOS

- Term-Sparsity exploiting moment/SOS

- TV

- Total Variation

- UK

- United Kingdom

Chapter 1 Introduction

This chapter discusses the urgent need for fairness amidst the proliferation of machine-learning applications. In particular, we outline the emerging recognition of fairness in both AI regulation and academia. Then, we put forth the contributions of the thesis within this context.

Citizens across the world are becoming more and more aware of discrimination that can arise due to the poor design of algorithms that guide our everyday lives. Examples of algorithms that affect citizens range from benign recommendation systems, to the less benign machine learning algorithms that make decisions that affect the lives of citizens in profound ways (decisions on bank loans, school admissions, etc.). Consequently, citizens, politicians, and societies, are becoming very concerned with potential algorithmic bias and unfairness, and are driving demand for certification and audibility of algorithmic systems111See https://fairnessfoundation.com/. Unfairness not only undermines the health of democracies but, from a societal standpoint, emotional reactions to unfairness may engender feelings of exclusion, thus endangering cohesion222This dynamic is explored further in the context of a fair society in the report at https://op.europa.eu/webpub/jrc/fair-society/. This, in turn, can lead to reduced productivity and efficiency in societies. In light of these arguments, a fair society, which places a premium on diversity and strives for inclusivity, actively promotes the acceptance of individuals from varied backgrounds, cultures, and identities. This commitment plays a vital role in bridging educational gaps and facilitating social mobility. As fairness has been identified as a driver of motivation and performance (Hancock et al., , 2018), a fair society has the capacity to inspire higher levels of productivity and efficiency.

Fairness will become even more important in the coming years in the aftermath of the global economic crisis, triggered by the COVID-19 pandemic. The World Bank333See the “World Development Report 2022” at https://www.worldbank.org/en/publication/wdr2022. expresses concerns that the recovery is likely to be uneven as its initial economic impacts, with disadvantaged populations and regions facing a prolonged journey towards recovering pandemic-induced losses of livelihoods, thereby exacerbating existing inequalities and poverty. The International Monetary Fund444See the article “Inequality in the Time of COVID-19” at https://www.imf.org/external/pubs/ft/fandd/2021/06/inequality-and-covid-19-ferreira.htm. states that the pandemic has further intensified preexisting inequalities in the labour market, largely because the ability to work remotely is highly correlated with education, and hence with pre-pandemic earnings. Job and income losses are likely to have disproportionately affected lower-skilled and uneducated workers, particularly those in informal labour without access to furlough programs or unemployment insurance. This has forced hundreds of millions of such workers to make daily trade-offs between staying safe at home and risking infection to provide food for their families. Moreover, the burden of additional time required for childcare and housework, falling disproportionately on women, has likely widened gender inequality in earnings.

In the United Kingdom (UK), Public Health England555See the report “COVID-19: review of disparities in risks and outcomes” at https://www.gov.uk/government/publications/covid-19-review-of-disparities-in-risks-and-outcomes. has confirmed that COVID-19 has not only mirrored existing health inequalities but has, in some cases, worsened them. Individuals from Black, Asian, and other Minority Ethnic groups faced higher exposure, diagnosis rates, and mortality from COVID-19. As investigated by Local Government Association666See multiple reports at https://www.local.gov.uk/our-support/safer-and-more-sustainable-communities/health-inequalities-hub highlights interconnected factors such as deprivation, low income, minority ethnicity, and poor housing, all contributing to an increased risk of COVID-19, with pre-existing health inequalities unfairly disadvantage individuals in their ability to survive the pandemic.

It is in this context that the research in this thesis began. The focus is on fairness in machine learning, with two main directions of contributions.

The first set of contributions focuses on the development of technical tools in the optimisation context. More specifically, we introduce two algorithms to solve fairness problems that arise in applications of machine learning. The first algorithm focuses on learning for linear dynamic systems, innovatively eliminating the need for assumptions about the dimension of hidden states. The second algorithm introduces a group-blind projection map capable of projecting two distinct datasets into similar ones, innovating by eliminating the requirement for group membership information for each data point. The second set of contributions is the applications of the aforementioned technical tools to several applications.

1.1 Societal Impacts of Machine Learning

Machine learning, or the broader concept, AI, is already bringing significant social and economic advantages to individuals, ranging from medical diagnostics, autonomous vehicles to virtual assistants such as Apple Siri and Amazon Alexa. Recent progress in generative AI, exemplified by OpenAI ChatGPT, provides a preview of the vast opportunities awaiting us in the near future. Many of us are starting to grasp the transformative potential of AI as the technology advances rapidly.

However, as machine learning becomes more prevalent, especially in sensitive or human-related applications, it is crucial to carefully examine its impacts on society. A notorious example is the COMPAS system. It has been used by the U.S. states to assess the likelihood of a defendant re-offending. According to the COMPAS Practitioner’s Guide 777Northpointe (March 2015). “A Practitioner’s Guide to COMPAS Core” at https://s3.documentcloud.org/documents/2840784/Practitioner-s-Guide-to-COMPAS-Core.pdf., the risk scales for predicting general and violent recidivism, and for pretrial misconduct, were designed using behavioural and psychological constructs “of very high relevance to recidivism and criminal careers”. In 2016, a nonprofit organisation, ProPublica investigated the algorithm and found that “African-American defendants are almost twice as likely as Caucasian defendants to be labelled a higher risk but not actually re-offend,” whereas COMPAS “makes the opposite mistake among Caucasian defendants: They are much more likely than African-American defendants to be labelled lower-risk but go on to commit other crimes” (Angwin et al., , 2016).

The impact of unfair machine learning applications on society is significant, yet identifying and mitigating the unfairness is a complex challenge. It has been well understood (Mhasawade et al., , 2021; Barocas and Selbst, , 2016; Calders and Žliobaitė, , 2013) that seemingly neutral machine learning models and algorithms are capable of disproportionately negative effects on certain individuals or groups based on their membership in a protected class or demographic category, even if no sensitive attribute is used. While their use in other settings can be judged fair and there may be no explicit intention to discriminate, these models can still lead to biased outcomes.

There is vast array of risks associated with the use of AI, including those associated with unrepresentative training data, including outcomes-biases in the data, bias in the algorithms, and bias in user interactions with algorithms. The first-mentioned risk entails biases in data that skew what is learned by machine learning algorithms. These are designed to learn and replicate historical patterns in the data, even if such patterns are biased (e.g., if historically men were hired more frequently than women for technical positions). For example, if historical data shows a bias in hiring, such as a higher frequency of men being hired for technical positions than women, the algorithm may perpetuate this bias in its predictions or decisions. Secondly, algorithms may work to prevent themselves from making fair decisions, even when the data is unbiased. Consider two sub-populations: a privileged one and an unprivileged one, where unprivileged candidates may outperform privileged candidates with similar scores, possibly due to facing greater challenges. Relying solely on SAT scores for hiring decisions without considering candidates’ backgrounds in this scenario could lead to excluding high-potential unprivileged candidates. Thirdly, biased outcomes might impact user experience, thus generating a feedback loop between data, algorithms, and users that can reinforce or even amplify existing bias. For instance, if additional police officers are deployed to an area predicted as high-risk for crime, the subsequent increase in arrests within that area will further heighten the risk prediction according to the model (Ensign et al., , 2018).

1.2 Initiatives to Address Bias

To address the potential societal impact of AI technologies, there has been a remarkable surge of interest in studying fairness in machine learning within the academic community. Once a niche topic, fairness has evolved into a major subfield of machine learning (Chouldechova and Roth, , 2020). Fair algorithms are designed to prevent biased and discriminatory results, safeguard individuals and groups, foster trust, adhere to legal and ethical standards, and ultimately enhance the impact of machine learning systems (Mehrabi et al., , 2021; Osoba and Welser IV, , 2017). This commitment to fairness is not merely a short-term goal; it is essential for the long-term sustainability of machine learning applications. In the next chapter, we will discuss the current state of the art in academia.

At the same time, regulatory policies have emerged to address AI fairness in the European Union (EU), as well as in the United States of America and other regions, following the success of ChatGPT. Regulatory awareness plays a crucial role in establishing trust in AI among users, stakeholders, and the general public. When people believe that systems treat them fairly, they are more likely to accept and embrace these technologies.

The General Data Protection Regulation (GDPR)888See “General Data Protection Regulation” at https://gdpr-info.eu/, effective since May 25, 2018, is a cornerstone of EU privacy and human-rights law. Enshrined in Article 5, it establishes fundamental principles such as lawfulness, fairness, transparency, purpose limitation, data minimisation, accuracy, storage limitation, integrity and confidentiality, and accountability.

In March 2023, the UK Government introduced its AI White Paper999See “A pro-innovation approach to AI regulation” at https://www.gov.uk/government/publications/ai-regulation-a-pro-innovation-approach/white-paper. This emphasises setting expectations for AI development and usage. The government empowers existing regulators to issue guidance and regulate AI within their jurisdiction. The approach is rooted in five principles for responsible AI development across all sectors: safety, security, and robustness; appropriate transparency and explainability; fairness; accountability and governance; and contestability and redress.

Policy attention on fairness in AI is evident in the recently published AI Act of the EU. In December 2023, the EU Parliament provisionally agreed with the Council on the AI Act, marking the first regulation on artificial intelligence 101010See the “Artificial Intelligence Act” at https://www.europarl.europa.eu/news/en/headlines/society/20230601STO93804/eu-ai-act-first-regulation-on-artificial-intelligence. The AI Act adopts a risk-based approach, categorising AI systems based on risk levels and imposing regulations accordingly. The categories include unacceptable risk, high risk, limited risk, and minimal risk, as well as categories specific for general-purpose AI systems. The legislation prioritises five aspects: safety, transparency, traceability, non-discrimination, and environmental impact.

Furthermore, in numerous applications, such as those involving AI’s impact on financial markets, machine learning is subject to specific regulations tailored to the field. For instance, in financial services, fairness is pivotal to consumer-credit regulations and ensuring compliance with environmental, social, and governance criteria (Friede et al., , 2015, ESG). This alignment, in turn, promotes sustainable business practices and contributes to a positive societal impact.

1.3 Contributions of the Thesis

This section outlines the research conducted on fairness in machine learning throughout the course of this PhD program. Each point of contribution is then positioned within the framework of machine learning fairness (provided later in Chapter 2), as outlined below.

Proper Learning of Linear Dynamic Systems (Chapter 3):

There has been much recent progress in time series forecasting and estimation of system matrices of Linear Dynamic System (LDS). We present an approach to both problems based on an asymptotically convergent hierarchy of convexifications of a certain non-convex operator-valued problem, which is known as Non-Commutative Polynomial Optimisation Problem (NCPOP). We present promising computational results, including a comparison with methods implemented in Matlab System Identification Toolbox. This is published in the IEEE Transactions on Automatic Control (Zhou and Mareček, , 2023).

-

•

Problem: Identification of LDS.

-

•

Innovation: This method operates without assumptions about the dimensions of hidden dynamics, accommodating polynomial shape constraints with global optimality guarantees. The complexity can be mitigated through the exploitation of sparsity.

- •

Fairness in Forecast for Imbalanced Data (Chapter 4):

In machine learning, training data often capture the behaviour of multiple subgroups of some underlying human population. This behaviour can often be modelled as observations of an unknown dynamical system with an unobserved state. When the training data for the subgroups are not controlled carefully, however, under-representation bias arises. To counter under-representation bias, we introduce two natural notions of fairness in time-series forecasting problems: subgroup fairness and instantaneous fairness. These notions extend predictive parity to the learning of dynamical systems. We also show globally convergent methods for the fairness-constrained learning problems using hierarchies of convexifications of non-commutative polynomial optimisation problems. We also show that by exploiting sparsity in the convexifications, we can reduce the run time of our methods considerably. Our empirical results on a biased dataset motivated by insurance applications and the well-known COMPAS dataset demonstrate the efficacy of our methods. This is published in the Journal of Artificial Intelligence Research (Zhou et al., 2023a, ), with a preliminary version presented in the AAAI Conference on Artificial Intelligence (Zhou et al., , 2021).

Group-Blind Transport Map for Unavailable Sensitive Attributes (Chapter 5):

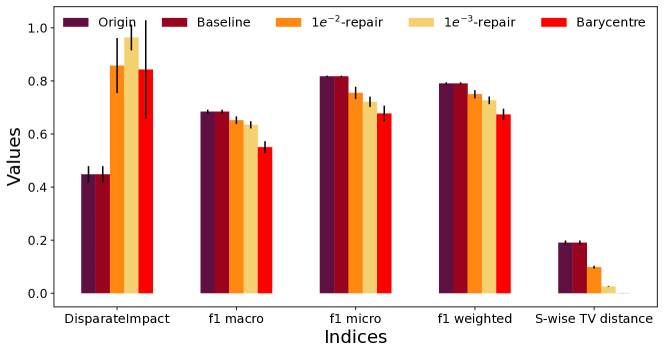

Fairness plays a pivotal role in the realm of machine learning, particularly when it comes to addressing groups categorised by sensitive attributes, e.g., gender, race. Prevailing algorithms in fair learning predominantly hinge on accessibility or estimations of these sensitive attributes. We design a single group-blind projection map that aligns the feature distributions of both groups in the source data, achieving (demographic) group parity, without requiring values of the sensitive attribute for individual samples in the computation of the map, as well as its use. Instead, our approach utilises the feature distributions of the privileged and unprivileged groups in a boarder population and the essential assumption that the source data are unbiased representation of the population. We present numerical results on synthetic data and the well-known Adult Census Income dataset. This is under review and can be found on arXiv (Zhou and Mareček, , 2023).

-

•

Problem: Unavailability of sensitive attributes (cf. Section 2.2.2).

-

•

Innovation: We design a single group-blind projection map. The map aligns feature distributions of both majority and minority groups in source data, achieving demographic parity (Dwork et al., , 2012) without requiring values of the protected attribute for individual samples in the computation or use of the map.

-

•

Methodology: Dykstra’s algorithm with Bregman projections (Bauschke and Lewis, , 2000).

1.4 Structure of the Thesis

-

•

Chapter 1: Introduction

-

–

Initiate a discussion on the societal impact of AI’s popularity, and present the efforts of governments and academia to address the associated concerns.

-

–

Outline the contributions of the thesis within this context.

-

–

Include a publication list.

-

–

-

•

Chapter 2: Preliminaries in Machine Learning Fairness

-

–

Introduce the state-of-the-art of machine learning fairness.

-

–

Outline the current open questions and common strategies.

-

–

- •

- •

-

•

Chapter 6: Concluding Remarks and Future Plans

-

•

Appendices:

-

–

Appendix A: Notation lists.

-

–

Appendix B: Provide the fundamentals of Semi-Definite Programming (SDP), serving as a preliminary for Generalised Moment Problem (GMP).

- –

- –

-

–

1.5 Publications

-

•

\bibentry

zhou2023learning

-

•

\bibentry

zhou2023fairness

-

•

\bibentry

zhou2023subgroup

-

•

\bibentry

zhou2021fairness

Chapter 2 Preliminaries in Machine Learning Fairness

After discussing fairness in broad terms, this chapter undertakes a tailored survey of fairness focused on the machine learning domain. It introduces the primary categories of fairness definitions, while also discussing prevalent open questions and common approaches within this field.

As mentioned in the previous chapter, the issue of fairness is very topical, not only in the machine learning community, but also in related areas, such as computer networking, smart cities, and behavioural economics. While the topic of fairness is broad, encompassing many subject domains, much of recent activities have emerged from the field of machine learning. The objective of this chapter is to provide a formal setting for the discussion of fairness in this machine learning context, and to provide a snapshot of available results and some of the most pressing open questions.

Generally speaking, unfairness in machine learning, can be attributed to various factors such as historical and systematic discrimination, conscious or unconscious prejudices, diverse forms of statistical bias, human negligence, and insufficient objective conditions. This multitude of factors lead to several problems when formulation a precise mathematical definition of fairness.

Fairness is also inherently subjective. While most individuals care deeply about fairness, they vary significantly in their definitions due to differing views on its relative importance. The diversity in perspectives and values within different communities adds complexity in establishing a universal definition of machine learning fairness. Furthermore, individuals not only care about “distributive justice”, which pertains to the allocation of resources or opportunities, but also about “procedural justice”, which involves how decisions are made.

Consequently, a proliferation of proposed definitions of fairness has emerged, with each seeking to confront a variety of potential biases in machine learning practices and design solutions to specific settings within real-life applications. There has been a widely-recognised foundational fairness framework within the machine learning fairness community (Caton and Haas, , 2023; Pessach and Shmueli, , 2022; Mehrabi et al., , 2021), which serves as a basis for categorising these definitions. Building upon this foundational framework, which we will discuss in the sequel, machine learning fairness concepts can be broadened through various applications, i.e., fair classification (Zafar et al., , 2019; Barocas et al., , 2023), fair prediction (Chouldechova, , 2017; Plečko et al., , 2024), fair ranking (Zehlike et al., 2022b, ; Zehlike et al., 2022a, ; Yang and Stoyanovich, , 2016; Feldman et al., , 2015), fair policy (Plecko and Bareinboim, , 2024; Chzhen et al., , 2021; Nabi et al., , 2019), and fair forecasting (Chouldechova, , 2017; Gajane and Pechenizkiy, , 2018; Locatello et al., , 2019; Jeong et al., , 2022). One can also mention in the passing that most problems of operations research have fairness-aware variants formulated, or to be formulated.

Although the foundational fairness framework offers practical guidance for promoting fairness, real-world scenarios can potentially undermine its effectiveness or even render it obsolete. The encouraging aspect is that, despite the vast range of applications, there are many similarities in the challenges encountered across these diverse scenarios. Later in this chapter, we will explore common challenges that cut across various applications and suggest prevalent methods to address them, with a focus on issues relevant to the upcoming chapters.

2.1 Fairness Definitions

2.1.1 Group Fairness Definitions

Group fairness is the most commonly utilised category of a notion of fairness and typically involves dividing the population into groups based on sensitive attributes, such as gender, sexual orientation, and race. The definitions in this category can be roughly divided into three principles (Barocas et al., , 2023). To expound upon these principles, we make the assumption, without loss of generality, that there are sensitive attributes (), ground-truth of target variables (), and the output of machine learning models (). In this COMPAS example mentioned above, could refer to race, actual re-offend status, and predicted probability assigned by the COMPAS model to each defendant.

In the context of group fairness:

Independence requires the output to be independent of sensitive attributes, i.e., , where the symbol denotes statistically independence. An illustrative instance is the concept of “demographic parity” (Dwork et al., , 2012), which demands the output of a model is consistent across different demographic groups. In this principle, half of Caucasian defendants being labelled as low risk would also entail the same proportion for African-American defendants. The opposite term, “disparate impact” (Barocas and Selbst, , 2016) denotes divergent outcomes that disproportionately benefit or harm a group of individuals sharing a value of a sensitive attribute more frequently than other groups.

Separation requires the output to be unrelated to sensitive attributes, but conditional on the target variables, i.e., . For example, “equal opportunity” (Hardt et al., , 2016) demands whether individuals who are qualified for an opportunity are equally likely to access it regardless of their group membership. In this principle, if half of Caucasian defendants without recidivism are labelled as low risk, the same proportion applies to African-American defendants without recidivism. The apparent advantage of this principle lies in the fact that when the output is absolutely accurate, it is also inherently fair in terms of the notion of separation. This implies that there is no trade-off between accuracy and fairness.

Sufficiency is derived from calibration and requires the target variables be independent from sensitive attributes conditional on the model output, i.e., . For instance, sufficiency would require that for any given COMPAS score, the recidivism rates in different groups are similar. We would consider the COMPAS system fair, following this principle, if the proportion of defendants who actually re-offend among those predicted to re-offend by the COMPAS system is equalised across different groups.

2.1.2 Individual Fairness Definitions

Individual fairness focuses on specific pairs of individuals, rather than on a quantity that is averaged over groups (Chouldechova and Roth, , 2020).

In the context of individual fairness:

Fairness through Unawareness of Dwork et al., (2012) requires to not explicitly employ sensitive features when making decisions, following the principle that if we are unaware of sensitive attributes while making decisions, our decisions will be fair. It aims to mitigate disparate treatment (Barocas and Selbst, , 2016), where deliberate inclusion of variables associated with sensitive attributes leads to disproportionate favouring of a specific class. However, this principle has been shown to be insufficient in many cases (Cornacchia et al., , 2023; Awwad et al., , 2020).

Fairness through Awareness of Dwork et al., (2012) requires “similar individuals should be treated similarly”. This principle necessitates a similarity metric that accurately reflects the ground truth (Petersen et al., , 2021; Sharifi-Malvajerdi et al., , 2019), and could be addressed through fair representation learning (Mukherjee et al., , 2020).

Counterfactual Fairness operates at the individual level, utilising causal methods to scrutinise whether a decision remains consistent when an individual’s sensitive attributes are altered (Kusner et al., , 2017). This concept distinguishes itself from notions based solely on correlations of statistical measures. Its generalised variant, path-specific fairness (Chiappa, , 2019; Nabi and Shpitser, , 2018), specifies the effects of sensitive attributes along certain path in a causal directed acyclic graph. Causal approaches go beyond the limitations of observational data, facilitating a better understanding of unfairness and its underlying reasons. A classic example of Simpson’s paradox involves a study on gender bias in graduate school admissions at the University of California, Berkeley, in 1973 (Bickel et al., , 1977). While the overall admission rates were about 44% for men and 35% for women, analysing decisions made by each department separately revealed equalised rates for both groups. The paradox emerged as women tended to apply to more competitive departments with lower admission rates, while men applied to less competitive departments with higher admission rates, resulting in the observed difference in admission rates.

2.2 Common Approaches and Open Questions

Next, we discuss typical obstacles to the fundamental framework and explore commonly employed strategies to overcome them. We start from the most direct source of unfairness – the data itself. The bias present in the training data has the potential to permeate into the trained model. This may arise from improper associations between sensitive attributes and other model inputs, the absence of sensitive attributes, or incomplete representation of all protected classes. Moreover, if not carefully examined, trained models may introduce new biases or magnify pre-existing ones. The pursuit of fairness also needs to strike a balance among multiple fairness definitions, as well as finding equilibrium with considerations, such as accuracy and privacy. While acknowledging that there are many further obstacles to be tackled, we focus on the challenges we address later in the thesis.

2.2.1 Proxies of Sensitive Attributes

Sensitive attributes can exhibit correlations with other attributes (proxies) in the data. For instance, race or religion might be associated with a specific city or neighbourhood within a city. “Fairness through unawareness” proves ineffective in practice because bias can persist through these proxies. Even if sensitive attributes are excluded, the model may still attempt to discern patterns connecting the data labels, that express this bias, through the remaining features that correlate with the removed sensitive attribute.

To confront this highly prevalent issue, there are three approaches. The first approach is fair representation learning, dating back to at least Zemel et al., (2013). This approach seeks intermediate data representations that optimally encode the data (preserving maximal information about individual attributes) while concurrently eliminating any information about membership with regard to sensitive attributes (Shui et al., , 2022; Zhao and Gordon, , 2022; Creager et al., , 2019). The second approach focuses on bias repairing schemes (Feldman et al., , 2015), that involve the modification of features to align the distributions from different groups, making it harder for the algorithm to differentiate among groups. Another approach is fair feature selection, which examines the input features used in the decision-making process and assesses how including or excluding certain features would impact outcomes. This aligns with the concept of procedural fairness (Grgić-Hlača et al., , 2018).

2.2.2 (Partial) Unavailability of Sensitive Attributes

Sensitive attributes are often not readily available due to privacy concerns, ethical considerations, difficulties in measurement111Some sensitive attributes, e.g., gender identity, are more of a spectrum, can be fluid and influenced by context., and legal regulations, as discussed in Andrus and Villeneuve, (2022). Many data protection laws, like the General Data Protection Regulation (GDPR) in Europe, impose restrictions on collecting and processing sensitive information. The unavailability of sensitive attributes, compounded by the prevalence of proxies, poses a key challenge. In contrast, most fairness-aware algorithms assume accessibility to individual-level sensitive attributes, creating a mismatch with real-world data limitations.

This challenge has been partially relaxed to considering sensitive attributes only at training time (Oneto and Chiappa, , 2020; Jiang et al., , 2020; Quadrianto and Sharmanska, , 2017; Zafar et al., 2017a, ). This approach trains a model that is blind to sensitive attributes by employing regularisation during training to penalise performance discrepancies across different groups. This line of research has recently been extended to require sensitive attributes only in a validation set (Elzayn et al., , 2023; Chai and Wang, , 2022) to guide the training process. In the two-stage framework of Liu et al., (2021), sensitive attributes in the validation set are employed to compute the worst-group validation error, which is then utilised for hyperparameter tuning.

Standard definitions of group fairness based on specific sensitive attributes, possess the practical benefit of being extensively recognised, researched, and are readily accessible in open-source toolkits. In practical scenarios, certain approaches aim to ensure fairness towards unspecified minority groups, often using proxies, or some noisy estimates. Amini et al., (2019); Oneto et al., (2019) introduce the latent variables as the proxies of unknown sensitive attributes. Additionally, Sohoni et al., (2020) explore clustering for a similar purpose. Zhao et al., (2022) minimises the correlation between proxies and model predictions to achieve fair classifier learning. Some methods employ distributional robust optimisation techniques to minimise the worst-case expected loss for groups identified by ambiguous sensitive attributes (Wang et al., , 2020; Sohoni et al., , 2020), or by regions where the model incurs (computationally-identifiable) errors (Lahoti et al., , 2020; Veldanda et al., , 2023).

Further along the road, some fairness definitions that does not focus on groups may better suit specific contexts, while necessitating more specialised expertise. “Fairness through awareness” could be one example that requires context-specific definitions of similarity among individuals. Liu et al., (2023) avoids any form of group memberships and uses only pairwise similarities between individuals to define inequality in outcomes, using the common property of social networks that individuals sharing similar (sensitive as well as non-sensitive) attributes are more likely to be connected to each other than individuals that are dissimilar.

Additionally, a survey in “Fairness Without Demographic Data” (Ashurst and Weller, , 2023) also discusses trusted third parties and cryptographic solutions to encourage the collection of sensitive attributes. These methods, e.g., Veale and Binns, (2017), focus on protecting sensitive attributes from misuse or use without informed consent, while also offering guidance or assessment for AI developers.

2.2.3 Imbalanced Data

In the domain of imbalanced learning (Kaur et al., , 2019; He and Ma, , 2013; Hoens and Chawla, , 2013), the presence of imbalanced data poses challenges across various realms of real-world research within machine learning. The inherent skewness in the distribution of primary data often introduces a bias favouring one group over another, resulting in representation bias. When the primary training objective prioritises overall accuracy without considering groups, established models tend to optimise for better accuracy in the majority group, consequently leading to sub-optimal accuracy for the minority group.

To address this issue, standard methods can be broadly categorised into two approaches. The first involves pre-processing techniques, which commonly encompass re-sampling and re-weighting strategies. Re-sampling may include methods such as over-sampling the minority or under-sampling the majority, while re-weighting assigns different weights to classes during the training process to rectify imbalances. Notably, Rolf et al., (2021); Chen et al., (2018) suggest promoting a more diverse representation in the training data as part of these pre-processing efforts. The second approach entails integrating regularises or constraints derived from group fairness definitions into the training process. These modifications are designed to discourage the model from exhibiting a bias toward the majority group and promote fair treatment of all groups during the learning process.

Imbalanced data may stem from mishandling missingness linked to sensitive attributes. The three missing data categories—Missing Completely At Random (MCAR), Missing At Random (MAR), and Missing Not At Random (MNAR)(Rubin, , 1976)—pose challenges, as seen in instances where men exhibit reluctance in disclosing income (MAR missingness) and gender itself has missing entries (MNAR missingness) (Tu et al., , 2019). While removing samples with missingness might seem tempting, it can lead to imbalanced data, disproportionately representing groups, especially in MAR or MNAR cases. In fact, missing data and fairness are intertwined, and empirical evidence supports imputing missing values instead of discarding rows (Fernando et al., , 2021). Literature, such as Caton et al., (2022); Fernando et al., (2021), explores imputation strategies for fairness with respect to missing data. Additionally, Tu et al., (2019) provides valuable strategies for causal-based fairness in the presence of missing data.

2.2.4 Dynamic Nature of Data Collection

In numerous machine learning scenarios, there is a dynamic nature where data are collected over time and decisions based on models shape subsequent data collection. This phenomenon is often referred to as a feedback loop or a self-reinforcing cycle, and it can lead to selection bias and the amplification of existing bias (D’Amour et al., , 2020; Liu et al., , 2018). For example, students from unprivileged backgrounds, facing additional challenges in achieving higher scores, are more likely to be classified as “low-performing” in early assessments. Subsequently, they may be placed in lower-level classes with limited resources. This situation impedes their educational experience, and their performance may conform to the initial classification, given the restricted opportunities available to them.

Fair sequential learning emphasises decisions made for short-term fairness can have repercussions on long-term fairness outcomes (long-term fairness). Striking a balance between exploiting existing knowledge and exploring sub-optimal solutions to gather additional data is crucial in navigating this complex landscape. The aim is to ensure that the learning process remains fair not only in immediate outcomes but also over an extended period, taking into account the evolving nature of data and decision-making contexts. Research studies such as Joseph et al., (2016) delve into fairness within bandits, while Wen et al., (2021); Jabbari et al., (2017) extends this exploration to fairness in reinforcement learning. These studies, based on long-term rewards, prioritise one decision over another if the former’s long-term reward surpasses the latter’s. Further extensions incorporate considerations of causal structures into the fairness framework (Creager et al., , 2020; D’Amour et al., , 2020; Nabi et al., , 2019; Hu and Zhang, , 2022).

2.2.5 Trade-offs

There is an inherent incompatibility among different concepts of group fairness (Mashiat et al., , 2022; Kleinberg et al., , 2017) and between group fairness and individual fairness (Binns, , 2020; Dwork et al., , 2012). This tension often makes it inherently challenging, or impossible, to concurrently fulfil multiple seemingly natural fairness criteria (Awasthi et al., , 2020; Kleinberg et al., , 2017). With the surge of numerous fairness notions, there have been efforts to design systems that address the challenge of balancing multiple potentially conflicting fairness measures (Awasthi et al., , 2020; Kim et al., , 2020; Lohia et al., , 2019). This becomes particularly relevant when there is no widely-recognised fairness notion that can be universally applied.

Trade-offs between fairness and accuracy have been well-identified (Sun et al., , 2024; Liu and Vicente, , 2022; Mandal et al., , 2020) while an empirical study on real-world problems by (Rodolfa et al., , 2021) challenges the presumed existence or magnitude of the trade-off between accuracy and fairness. Furthermore, maintaining accuracy introduces tension between fairness and interpretability (feature deduction) Agarwal, (2021). Inspired by concepts from fair division and envy-freeness in economics and game theory, a line of work has emerged focusing on achieving envy-free outcomes (Ustun et al., , 2019; Zafar et al., 2017b, ). This is based on the observation that, in certain decision-making scenarios, existing parity-based fairness notions may be too stringent. This stringency can potentially hinder the attainment of more accurate decisions that are also desired by every sensitive attribute group.

Dwork et al. (Dwork et al., , 2012) initiated a discussion about the relationship between privacy and fairness, that “Fairness Through Awareness” is generalisation of differential privacy (Dwork, , 2006). Both fairness and privacy can be improved by obfuscating sensitive information. Whereas, there are discussions about trade-offs between fairness and privacy in the literature (Tran et al., , 2021; Pinzón et al., , 2021; Chang and Shokri, , 2021; Cummings et al., , 2019).

Chapter 3 Non-Commutative Polynomial Optimisation to System Identification

There has been much recent progress in time series forecasting and estimation of system matrices of linear dynamical systems (West and Harrison, , 1997). We present an approach to both problems based on an asymptotically convergent hierarchy of convexifications of non-commutative polynomial optimisation. We present promising computational results, including a comparison with methods implemented in Matlab System Identification Toolbox. This chapter is based on the joint work with Dr. Jakub Mareček, and has been published in the IEEE Transactions on Automatic Control (Zhou and Mareček, , 2023).

We consider the identification of vector autoregressive processes with hidden components from time series of observations, which is a key problem in system identification (Ljung, , 1998). Its applications range from the identification of parameters in epidemiological models (Anderson and May, , 1992) and reconstruction of reaction pathways in other biomedical applications (Chou and Voit, , 2009), to identification of models of quantum systems (Bondar et al., , 2023, 2022). Beyond this, one encounters either partially observable processes or questions of causality (Schölkopf et al., , 2021; Geiger et al., , 2015) in almost any application domain. In the “prediction-error” approach to forecasting (Ljung, , 1998), it allows the estimation of subsequent observations in a time series.

To state the problem formally, let us define a Linear Dynamic System (LDS), represented by the tuple , as in West and Harrison, (1997)

| (LDS) |

where is the hidden state, is the observed output (measurements, observations), and are system matrices, and are normally distributed process and observation noises with zero mean and covariance of and respectively. The transpose of is denoted as . Learning (or proper learning) refers to identifying the quadruple given the output . We assume that the linear dynamical system is observable (Overschee and Moor, , 2012), i.e., its observability matrix (West and Harrison, , 1997) has full rank. Note that a minimal representation is necessarily observable and controllable, cf. Theorem 4.1 in Tangirala, (2014), so the assumption is not too strong.

There are three complications. First, the dimension of the hidden state is not known, in general. Although Sarkar et al., (2022) have shown that a lower-dimensional model can approximate a higher-dimensional one rather well, in many cases, it is hard to choose in practice. Second, the corresponding optimisation problem is non-convex, and guarantees of global convergence have been available only for certain special cases. Finally, the operators-valued optimisation problem is non-commutative, and hence much work on general-purpose commutative non-convex optimisation is not applicable without making assumptions (Bondar et al., , 2023, cf.) on the dimension of the hidden state.

Here, we aim to develop a method for proper learning of LDS that could also estimate the dimension of the hidden state and that would do so with guarantees of global convergence to the best possible estimate, given the observations. This would promote explainability beyond what forecasting methods without global convergence guarantees allow for. In particular, our contributions are the following.

- •

-

•

We show how to use Navascués–Pironio–Acín (NPA)hierarchy (Pironio et al., 2010a, ; Navascués et al., , 2012) of convexifications of the NCPOP to obtain bounds and guarantees of global convergence. The runtime is independent of the (unknown) dimension of the hidden state.

- •

This chapter is organised as follows. Section 3.1 set our work in the context of related work. Section 3.2 introduces our formulation of proper learning of LDS with an unknown dimension of the hidden state, following the discussion of NCPOP in Appendix D.1. Eventually, Section 3.3 presents promising computational results, including a comparison with methods implemented in Matlab™ System Identification Toolbox™.

3.1 Related Work in System Identification and Control

There is a long history of research within system identification (Ljung, , 1998). In forecasting under LDS assumptions (improper learning of LDS), a considerable progress has been made in the analysis of predictions for the expectation of the next measurement using Auto-Regressive (AR)processes in Statistics and Machine Learning. In Anava et al., (2013), first guarantees were presented for Auto-Regressive Moving-Average (ARMA)processes. In Liu et al., (2016), these results were extended to a subset of autoregressive integrated moving average (ARIMA) processes. Kozdoba et al., (2019) have shown that up to an arbitrarily small error given in advance, AR processes will perform as well as any Kalman filter on any bounded sequence. This has been extended by Tsiamis and Pappas, (2022) to Kalman filtering with logarithmic regret.

Another stream of work within improper learning focuses on sub-space methods (Katayama, , 2006; Overschee and Moor, , 2012) and spectral methods Hazan et al., (2017, 2018). Tsiamis et al., (2020); Tsiamis and Pappas, (2019) presented the present-best guarantees for traditional sub-space methods. Sun et al., (2020) utilise regularisations to improve sample complexity. Within spectral methods, Hazan et al., (2017) and Hazan et al., (2018) have considered learning LDS with input, employing certain eigenvalue-decay estimates of Hankel matrices in the analyses of an AR process in a dimension increasing over time. We stress that none of these approaches to improper learning are “prediction-error” methods; namely, they do not estimate the system matrices.

In proper learning of LDS, many state-of-the-art approaches consider the least squares method, despite complications encountered in unstable systems (Faradonbeh et al., , 2018). Simchowitz et al., (2018) have provided non-trivial guarantees for the Ordinary Least Squares (OLS) estimator in the case of stable and there being no hidden component, i.e., being the identity matrix and . Surprisingly, they have also shown that more unstable linear systems are easier to estimate than less unstable ones, in some sense. Simchowitz et al., (2019) extended the results to allow for a certain pre-filtering procedure. Sarkar and Rakhlin, (2019); Sarkar et al., (2022) extended the results to cover stable, marginally stable, and explosive regimes. Oymak and Ozay, (2019) provide a finite-horizon analysis of the Ho-Kalman algorithm. Most recently, Bakshi et al., (2023) provided a detailed analysis of the use of the method of moments in learning linear dynamical systems, which could be seen as a polynomial-time algorithm for learning a LDS from a trajectory of polynomial length up to a polynomial error. Our work could be seen as a continuation of the work on the least squares method, with guarantees of global convergence.

3.2 The Model

Given a trajectory of observations , loss is a one-step error function at time that compares an estimate with the actual observation . Within the least squares estimator, we aim to minimise the sum of quadratic loss functions, i.e.,

where the estimates are decision variables. The properties of the optimal least squares estimate are well understood: it is consistent, cf. Mann and Wald (Mann and Wald, , 1943) and Ljung (Ljung, , 1976), and has favourable sample complexity, cf. Theorem 4.2 of Campi and Weyer Campi and Weyer, (2002) in the general case, and to Jedra and Proutiere Jedra and Proutiere, (2020) for the latest result parameterised by the size of a certain epsilon net. We stress, however, that it has not been understood how to solve the non-convex optimisation problem, in general, outside of some special cases Hardt et al., (2018) and recent, concurrent work of Bakshi et al., (2023). In contrast to Hardt et al., (2018), we focus on a method achieving global convergence under mild assumptions, and specifically without assuming the dimension of the hidden state is known.

When the dimension of the hidden state is not known, we need operator-valued variables to model the state evolution, and some additional scalar-valued variables. We denote the process noise and the observation noise at time by and , respectively. We also denote as such the decision variables corresponding to the estimates thereof, if there is no risk of confusion. If we add the sum of the squares of and the sum of the squares of as regularisers to the objective function with sufficiently large multipliers and minimise the resulting objective, we should reach a feasible solution with respect to the system matrices with the process noise and observation noise being close to zero.

Overall, such a formulation has the form in Equations (3.1) subject to (3.2–3.3). The inputs are , i.e., the time series of the actual measurements, of a time window thereof, and multipliers . Decision variables are system matrices , ; noisy estimates , realisations , of noise, for ; and state estimates , for , which include the initial state . We minimise the objective function:

| (3.1) |

for a -norm over the feasible set given by constraints for :

| (3.2) | ||||

| (3.3) |

We call the term noise-free estimates, which are regarded as our simulated/ predicted outputs. Equations (3.1) subject to (3.2–3.3) give us the least squares model. We can now apply the techniques of non-commutative polynomial optimisation to the model so as to recover the system matrices of the underlying linear system.

Theorem 3.1.

For any observable linear system , for any length of a time window, and any error , under the Archimedean assumption, detailed in Theorem D.2, there is a convex optimisation problem whose objective function value is at most away from Equations (3.1) subject to (3.2–3.3). Furthermore, an estimate of can be extracted from the solution of the same convex optimisation problem.

Proof.

First, we need to show the existence of a sequence of convex optimisation problems, whose objective function approaches the optimum of the non-commutative polynomial optimisation problem. As explained in Appendix D.1 above, there is a sequence of SDP relaxations of Equation (NCPOP) (Pironio et al., 2010a, ; Burgdorf et al., , 2016). The convergence of the sequence of their objective-function values is shown by Theorem D.6, which requires the Archimedean assumption in Theorem D.2. The translation of a problem involving multiple scalar- and operator-valued variables in (3.1–3.3) to the form of Equation (NCPOP), also known as the product-of-cones construction, is somewhat tedious, but routine and implemented in multiple software packages, e.g., Wittek, (2015); Wang and Magron, 2021a . Second, we need to show that extraction of an estimate of from the SDP relaxation of order in the series is possible. As explained in Section 2.2 of Klep et al., (2018) or in Theorem D.8, when flatness condition is satisfied, one utilises the Gelfand–Naimark–Segal (GNS)construction (Gelfand and Neumark, , 1943; Segal, , 1947). Notice that (Lee et al., , 2023, cf.) the estimate of may have a higher error than . ∎

This reasoning can be applied to more complicated formulations, involving shape constraints. For instance, in quantum systems Bondar et al., (2023), density operators are Hermitian and this constraint can be added to the least squares formulation.

Crucially for the practical applicability of the method, one should like to exploit the sparsity in the NCPOP (3.1–3.3), as in Section D.2. Notice that one can decompose the problem (3.1–3.3) into subsets of variables involving , which satisfy the running intersection property in Assumption D.1.

Also, note that the extraction of the minimiser using the Gelfand–Naimark–Segal (GNS)construction, as explained in Theorem D.7, is stable to errors in the moment matrix, for any NCPOP, including the pre-processing above. See Theorem 4.1 in Klep et al., (2018). That is: it suffices to solve the SDP relaxation with a fixed error, in order to extract the minimiser.

One can also utilise a wide array of reduction techniques on the resulting SDP relaxations. Notable examples include facial reduction (Borwein and Wolkowicz, , 1981; Permenter and Parrilo, , 2018) and exploiting sparsity (Fukuda et al., , 2001). Clearly, these can be applied to any SDP, irrespective of the non-commutative nature of the original problem, but can also introduce (Kungurtsev and Marecek, , 2020) numerical issues. We refer to Majumdar et al., (2019) for an up-to-date discussion.

3.3 Numerical Illustrations

Let us now present the implementation of the approach using the techniques of NCPOP (Pironio et al., 2010a, ; Burgdorf et al., , 2016) and to compare the results with traditional system identification methods. Our implementation is available online 111https://github.com/Quan-Zhou/Proper-Learning-of-LDS.

3.3.1 The General Setting

Our formulation and solvers

For our formulation, we use Equations (3.1) subject to (3.2–3.3), where we need to specify the values of and . To generate the SDP relaxation of this formulation as in Equation (NCPOP-DSDP), we need to specify the moment order . Because the degrees of objective (3.1) and constraints in (3.2–3.3) are all less than or equal to , the moment order within the respective hierarchy can start from . (The reasoning of choosing moment order can be found in the definition of SDP relaxations in Equation (NCPOP-SDP) or (NCPOP-DSDP).)

In our implementation, we use a globally convergent NPA hierarchy (Pironio et al., 2010a, ) of SDP relaxations, and its sparsity-exploiting variant, known as the non-commutative variant of the Term-Sparsity exploiting moment/SOS (TSSOS)hierarchy (Wang et al., 2021b, ; Wang et al., 2021a, ; Wang and Magron, 2021a, ). The SDP of a given moment order within the NPA hierarchy is constructed using ncpol2sdpa 1.12.2222https://github.com/peterwittek/ncpol2sdpa of Wittek (Wittek, , 2015). The SDP of a given moment order within the non-commutative variant of the TSSOS hirarchy is constructed using the nctssos333https://github.com/wangjie212/NCTSSOS of Wang et al. (Wang and Magron, 2021a, ). Both SDP relaxations are then solved by mosek 9.2 MOSEK, ApS, (2020).

Baselines

We compare our method against leading methods for estimating state-space models, as implemented in Matlab™ System Identification Toolbox™. Specifically, we test against a combination of least squares algorithms implemented in routine ssest (“least squares auto”), subspace methods of Overschee and Moor, (2012) implemented in routine n4sid (“subspace auto”), and a subspace identification method of Jansson, (2003) with an ARX-based algorithm to compute the weighting, again utilised via n4sid (“ssarx”).

To parameterise the three baselines, we need to specify the estimated dimension of the state-space model. We would set directly or alternatively, iterate from to the highest number allowed in the toolbox when the underlying system is unknown, e.g., in real-world stock-market data. Then, we need to specify the error to be minimised in the loss function during estimation. In fairness to the baselines, we use the one-step ahead prediction error when comparing prediction performance and simulation error between measured and simulated outputs when comparing simulation performance.

The performance index

To measure the goodness of fit between the ground truth (actual measurements) and the noise-free simulated/ predicted outputs , using different system identification methods, we introduce the fit value444This definition follows the one used in Matlab™ System Identification Toolbox™, at https://uk.mathworks.com/help/ident/ref/compare.html

| (3.4) |

where and are the vectors consisting of the sequence and respectively. A higher fit value indicates better simulation or prediction performance.

3.3.2 Experiments on the Example of Hazan et al.

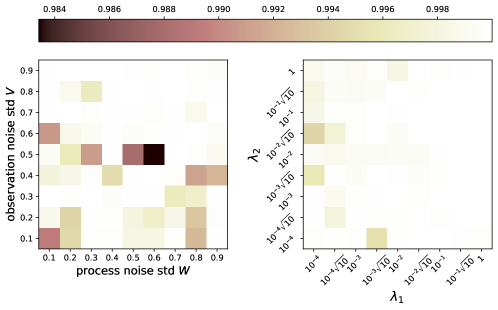

Experiments in Sections 3.3.2–3.3.3 utilise synthetic time series of observations generated using LDS of the form in Equation (LDS), with the tuple and the initial hidden state detailed next. We use the dimension to indicate that the time series of observations were generated using system matrices, while we use operator-valued variables to estimate these. The standard deviations of process noise and observation noise are chosen from . Note that is an matrix in general, while we consider the spherical case of , where is the -dimensional identity matrix, which we denote by .

In our first experiment, we explore the statistical performance of feasible solutions of the SDP relaxations using the example of Hazan et al.(Hazan et al., , 2017; Kozdoba et al., , 2019). We performed one experiment on each combination of standard deviations of process and observation noise from the discrete set , i.e., 81 runs in total.

Figure 3.1 illustrates the fit values of the runs of our method in different combinations of standard deviations of process noise and observation noise (left), and another experiments in different combinations of and (right). In the left subplot of Figure 3.1, we consider: , , , the starting point , and . In the right subplot of Figure 3.1, we have the same settings as in the left one, except for and the parameters being chosen from . It seems clear the highest fit value is to be observed for the standard deviation of both process and observation noises close to . While this may seem puzzling at first, notice that higher standard deviations of noise make it possible to approximate the observations by an AR process with low regression depth (Kozdoba et al., , 2019, Theorem 2). The observed behaviour is therefore in line with previous results (Kozdoba et al., , 2019, e.g., Figure 3).

3.3.3 Comparisons against the Baselines

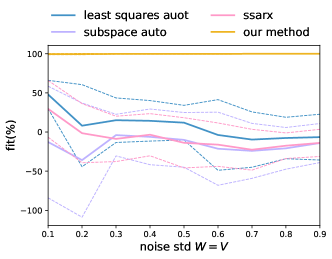

Next, we investigate the simulation performance of our method in comparison with other system identification methods, for varying LDS used to generate the time series. Our method and the three baselines described in Section 3.3.1 are run times for each choice of the standard deviations of the noise, with all methods using the same time series.

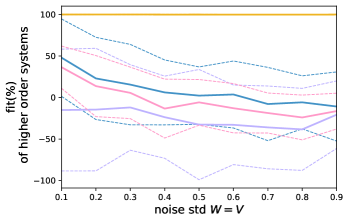

Figure 3.2 illustrates the results, with methods distinguished by colours: blue for “least squares auto”, purple for “subspace auto”, pink for “ssarx”, and yellow for our method. The upper left subplot presents the mean (solid lines) and mean one standard deviations (dashed lines) of fit values as standard deviation of both process noise and observation noise (“noise std”) increasing in lockstep from to . The underlying system is the same as in the left subplot of Figure 3.1, except for . The upper right subplot is similar, except the time series are generated by systems of a higher differential order:

| (3.5) |

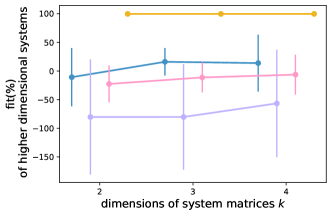

and the formulation of our method is changed accordingly. In the lower subplot of Figure 3.2, we consider the mean (solid dots) and mean one standard deviations (vertical error bars) of fit values at different dimensions of the underlying system in Equation (LDS).

As Figure 3.2 suggests, it is expected that other methods would perform better when the noise standard deviations approach zero, as shown in the upper subplots of Figure 3.2. However, despite the fact that the dimensions used by the baseline methods are the true dimensions of the underlying system (), the fit values of these methods rarely reach 50%, even when the noise standard deviations are very small. This could be due to the small number of observations (). (We will use “least squares auto”, which seems to work best within the other methods, in the following experiment on stock-market data.)

Our method outperforms primarily because the technologies of NCPOP do not assume the dimension of the variables, allowing it to handle the noise very well. However, as explained in Appendix D, due to the high complexity of iteratively increasing the moment order until the global optimality of NCPOP is detected, we cannot compute the exact optimal solution of NCPOP. Instead, the results of our method presented here are not the exact optimal solution of NCPOP but the solutions of its SDP relaxation at moment order . Furthermore, our method shows better stability; the gap between the yellow dashed lines in the upper or middle subplot, which suggests the width of two standard deviations, is relatively small.

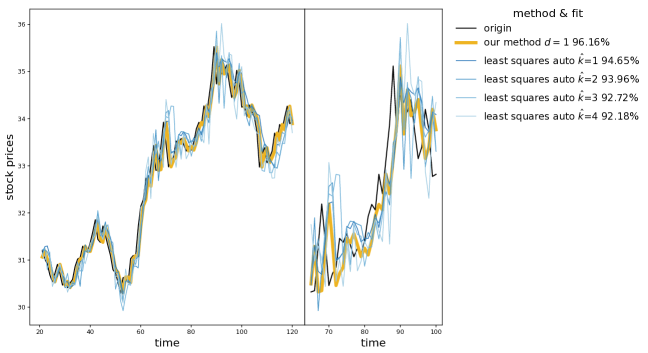

3.3.4 Experiments with Stock-Market Data

Our approach to proper learning of LDS could also be used in a “prediction-error” method for improper learning of LDS, i.e., forecasting its next observation (output, measurement). As such, it can be applied to any time series. To exhibit this, we consider real-world stock-market data first used in Liu et al., (2016). In particular, we predict the evolution of the stock price from the 21 period to the 121 period, where each prediction is based on the 20 immediately preceding observations (). For our method, we use the same formulation (3.1) subject to (3.2)–(3.3), but with the variable removed. For comparison, the combination of least squares algorithms “least squares auto” is used again. Since we are using the stock-market data, the dimension of the underlying system is unknown. Hence, the estimated dimensions of the “least squares auto” are iterated from to , wherein is the highest setting allowed in the toolbox for -period observations.

Figure 3.3 shows in the left subplot the results obtained by our method (a yellow curve), and the “least squares auto” of varying estimated dimensions (four blue curves). The true stock price “origin” is displayed by a dark curve. The percentages in the legend correspond to fit values (3.4). Both from the fit values and the shape of these curves, we notice that “least squares auto” performs poorly when the stock prices are volatile. This is highlighted in the right subplot, which zooms in on the 66-101 period.

3.3.5 Runtime

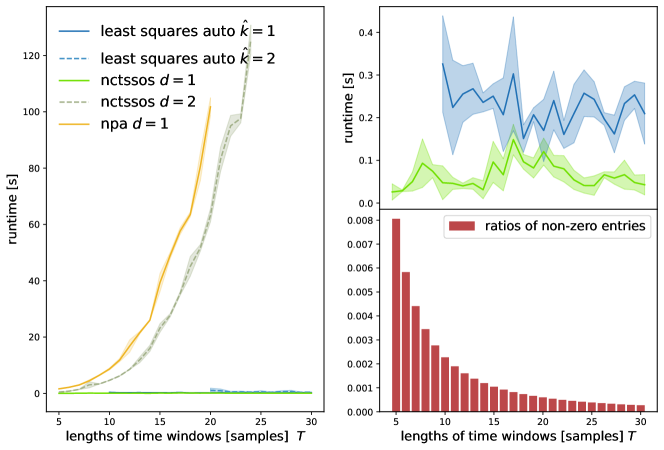

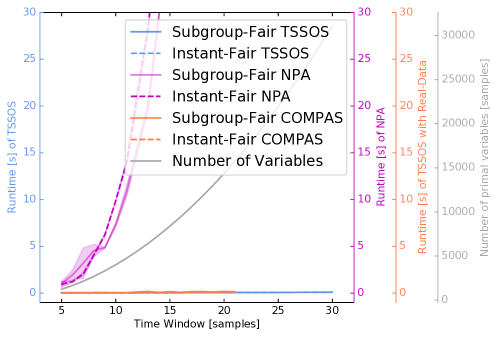

As discussed in Appendix D.2, the computational complexity of NCPOP is substantial. For variables in NCPOP formulation and a moment order , the cardinality of the monomial basis, is . Then, the number of variables in the corresponding SDP relaxation at the moment degree , is its square. The computation becomes impractical as the length of time windows, related to the number of variables in NCPOP formulation, increases. Efforts to exploit sparsity patterns in these SDP relaxations are also discussed in Appendix D.2.

To illustrate the effects, consider the runtime of two implementations of solvers for (3.1) subject to (3.2)–(3.3). The first implementation constructs the SDP relaxation of NPA hierarchy via ncpol2sdpa 1.12.2 with moment order . The second implementation constructs the non-commutative variant of the TSSOS hierarchy via nctssos, with moment order . For comparison purposes, we include the baseline “least squares auto” with estimated dimensions . We randomly select a time series from the stock-market data, with the length of time window chosen from , and run these three methods three times for each .

Figure 3.4 illustrates the runtime of the SDP relaxations and the baseline “least squares auto” as a function of the length of the time window. These implemented methods are distinguished by colours: blue for “least squares auto”, green for the non-commutative variant of the TSSOS hierarchy (“nctssos”), and yellow for the NPA hierarchy (“npa”). The mean and mean one standard deviation of runtime are displayed by (solid or dashed) curves and shaded error bands. The upper-right subplot compares the runtime of our method with “nctssos” at moment order against “least squares auto” with estimated dimension . The red bars in the lower-right subplot display the sparsity of NPA hierarchy of the experiment on stock-market data against the length of time window, by ratios of non-zero coefficients out of all coefficients in the SDP relaxations.

As in most primal-dual interior-point methods (Tunçel, , 2000), runtime of solving the relaxation to error is polynomial in its dimension and logarithmic in , but it should be noted that the dimension of the relaxation grows fast in the length of the time window and the moment order . It is clear that the runtime of solvers for SDP relaxations within the non-commutative variant of the TSSOS hierarchy exhibits a modest growth with the length of time window, much slower than that of the plain-vanilla NPA hierarchy.

3.4 Conclusion

We have presented an alternative approach to the recovery of hidden dynamic underlying a time series, without assumptions on the dimension of the hidden state. For the first time in system identification and machine learning, this approach utilises NCPOP, which has been recently developed within mathematical optimisation (Pironio et al., 2010a, ; Wittek, , 2015; Klep et al., , 2018; Wang and Magron, 2021a, ). This can accommodate a variety of other objectives and constraints, as we shall see in Chapter 4.

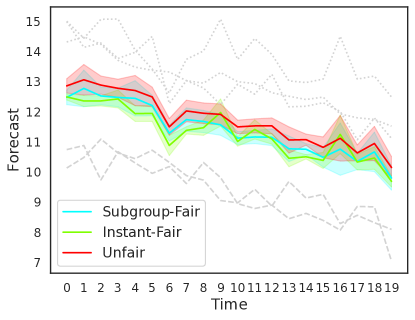

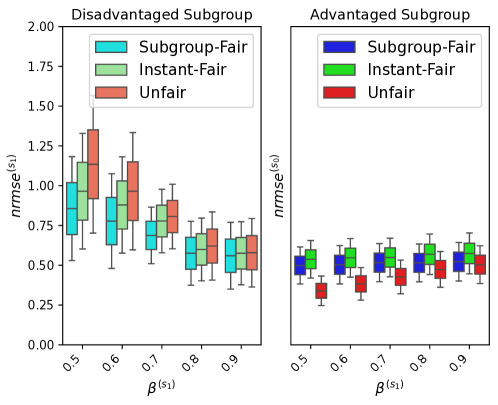

Chapter 4 Non-Commutative Polynomial Optimisation to Fairness in Forecasting

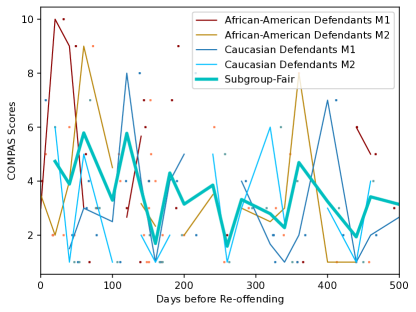

In machine learning, training data often capture the behaviour of multiple subgroups of some underlying human population. This behaviour can often be modelled as observations of an unknown dynamical system with an unobserved state. When the training data for the subgroups are not controlled carefully, however, under-representation bias arises. To counter this bias in learning dynamical systems, we introduce two natural notions of fairness in time-series forecasting problems: subgroup fairness and instantaneous fairness. Our empirical results on the well-known COMPAS dataset (Angwin et al., , 2016) demonstrate the efficacy of our methods. This chapter is a collaboration with Dr. Jakub Mareček and Prof. Robert Shorten, and has been published in the Journal of Artificial Intelligence Research (Zhou et al., 2023a, ).

Forecasts affect almost all aspects of our daily life, as a basis for access-control mechanisms. As the quality of the forecasts impacts our lives, for better or worse, it is becoming more and more apparent that many of the tools that produce the forecasts seem to be, or indeed are, unfair, in a sense we formalise below. If the tools used to produce the forecasts are unfair, society suffers.

One such example of a forecasting tool that shapes the very pillars of our society is the FICO Score (Fair Isaac Corporation, , 2021). FICO is a measure of an individual’s creditworthiness (or conversely, credit-default risk), computed by the Fair Isaac Corporation. It has been suggested (Nickerson et al., , 2016; Delis and Papadopoulos, , 2019; Hegarty, , 2019; Vogel et al., , 2021) that the FICO Score may be unfair to certain minorities, although this has been disputed (Avery et al., , 2012).

As another example, consider college admissions, where results of standardised tests were often presented as forecasts of potential academic success. In the context of COVID-19, forecasting algorithms utilising previous grades and input from teachers replaced standardised tests in determining the satisfaction of college-admission requirements in many jurisdictions.

Other forecasting tools are perhaps less well known, but perhaps even more alarming, as they have the potential to shape the very core of society. One striking example is Northpointe’s COMPAS. COMPAS is a criminal-risk assessment tool that is widely used in pretrial, parole, and sentencing decisions at courts in New York, Wisconsin, California, and Florida. COMPAS forecasts the likelihood that an individual will re-offend within two years. It has been suggested (Angwin et al., , 2016; Dressel and Farid, , 2021) that COMPAS under-predicts recidivism for Caucasian defendants, and over-predicts recidivism for African-American defendants.111 We note that this has been disputed (Kleinberg et al., , 2017; Dressel and Farid, , 2021), and that it has been suggested that such forecasts (Neil et al., , 2021) are difficult to make, in general, due to the cohort differences in group-based arrest trajectories.

The applications, where fairness seems most important, often capture the behaviour of multiple subgroups of some underlying human population in the training data. Let us consider a model, where there are a number of individuals within a population. The population is partitioned into subgroups indexed by . For each subgroup , there is a set of trajectories of observations available and each trajectory has observations for periods , possibly of varying cardinality . Each subgroup is associated with a model, . For all , , the trajectory , for , is hence generated by precisely one model . Throughout, the superscripts distinguish the trajectories and subgroups, while subscripts indicate the periods.

In this setting, under-representation bias (Blum and Stangl, , 2019, cf. Section 2.2) arises, where the trajectories of observations from one (“disadvantaged”) subgroup are under-represented in the training data. This is particularly important if the forecasting is constrained to be subgroup-blind, i.e., we wish to learn a single subgroup-blind model . This is the case when the use of sensitive attributes distinguishing each subgroup can be regarded as discriminatory, such as in the case of gender and race (Gajane and Pechenizkiy, , 2018; Kleinberg et al., , 2018). Notice that such anti-discrimination measures are increasingly stipulated legally, e.g., within insurance pricing, where the sex of the applicant cannot be used, despite being known. More broadly, under-representation bias harms both the accuracy of the forecast and fairness in the sense of varying accuracy across the subgroups.

To address under-representation bias in the training of a forecasting model, it is natural to seek a notion of fairness that captures the overall behaviour across all subgroups, while taking into account the varying amounts of training data for the individual subgroups. To formalise this, suppose that we learn one model from the multiple trajectories and define a loss function that measures the loss of accuracy for a certain observation when adopting the forecast for the overall population. For , , , we have

| (4.1) |

Let . Following the definitions of , there is no observation for , in which case, loss in Equation (4.1) does not exist. To evaluate the performance of the forecasts, we only consider made in periods . Note that, since each trajectory is of varying length, it is possible that for a certain triple , there is no observation .

Following much recent work on fairness in classification, e.g., Zliobaite, (2015); Hardt et al., (2016); Kilbertus et al., (2017); Kusner et al., (2017); Chouldechova and Roth, (2020); Aghaei et al., (2019), we propose two objectives to address the under-representation bias, which extend group fairness (Feldman et al., , 2015) to time series are the following.

-

1.

Subgroup Fairness. The objective seeks to equalise, across all subgroups, the sum of losses for the subgroup. Considering the number of trajectories in each subgroup and the number of observations across the trajectories may differ, we include cardinality as weights:

(4.2) -

2.

Instantaneous Fairness. The objective seeks to equalise the instantaneous loss, by minimising the maximum of the losses across all subgroups and all times:

(4.3)

We then cast the learning of a LDS with such fairness considerations as a NCPOP, which can be solved efficiently using a globally-convergent hierarchy of SDP relaxations, which can be of independent interest. A comprehensive comparison is given to illustrate the efficacy of our approach.

4.1 The Fair-Forecasting Framework

As the simplest example of the use of subgroup fairness and instantaneous fairness, cf. Equations (4.2) and (4.3), consider their applications in linear regression. For simplicity, let us assume that the cardinality of each subgroup is the same and the lengths of all trajectories are equal. Then:

where concatenates the regression coefficients. concatenates explanatory variables. is the dependent variable and is the actual observation in a compatible fashion. The auxiliary scalar variable is used to reformulate “” in the objective in Equations (4.2) and (4.3).

Next, let us consider more elaborate models, which assume that there exists a LDS corresponding to each subgroup . A discrete-time model of a LDS , as in West and Harrison, (1997) or Chapter 3, suggests that the random variable capturing the observed component (i.e., output, observations or measurements) evolves over time according to

| (LDS) |

where is the hidden component (state) and and are compatible system matrices. Random variables capture normally-distributed process noise and observation noise, with zero means and covariance matrices and , respectively.