Variational Bayes Portfolio Construction

Abstract

Portfolio construction is the science of balancing reward and risk; it is at the core of modern finance. In this paper, we tackle the question of optimal decision-making within a Bayesian paradigm, starting from a decision-theoretic formulation. Despite the inherent intractability of the optimal decision in any interesting scenarios, we manage to rewrite it as a saddle-point problem. Leveraging the literature on variational Bayes (VB), we propose a relaxation of the original problem. This novel methodology results in an efficient algorithm that not only performs well but is also provably convergent. Furthermore, we provide theoretical results on the statistical consistency of the resulting decision with the optimal Bayesian decision. Using real data, our proposal significantly enhances the speed and scalability of portfolio selection problems. We benchmark our results against state-of-the-art algorithms, as well as a Monte Carlo algorithm targeting the optimal decision.

1 Introduction

Portfolio construction (or selection) is a fundamental problem in modern finance (Markowitz, 1952; Merton, 1972), involving the strategic allocation of capital across multiple assets to achieve an optimal tradeoff between risk and return. As financial markets grow in complexity, designing robust portfolios that effectively account for market uncertainty has become increasingly critical. Traditional approaches, such as Markowitz’s mean-variance optimization (Markowitz, 1952), have provided a foundational framework for portfolio construction but are now facing challenges in modern finance problems. Markets are becoming increasingly dynamic, with non-Gaussian asset returns, and, in some cases, small dataset sizes. This has led to suboptimal performance in real-world scenarios (see discussions in Benichou et al. (2016)). Formally, the mean-variance framework of a portfolio of assets can be stated as choosing weights from a decision set111For example, we might consider the -dimensional simplex as a decision set, . by solving

| (1) |

where is the mean of observations, its covariance matrix, and is a risk tolerance parameter. Extensive research has focused on improving this framework by addressing key challenges, such as incorporating higher-order moments of return distributions (Harvey et al., 2010), introducing robust optimization techniques (Ismail and Pham, 2019), and refining covariance matrix estimation from noisy data (Benichou et al., 2016; Bun et al., 2017; Agrawal et al., 2022; Benaych-Georges et al., 2023). The Markowitz portfolio provides a systematic approach to balancing return and risk, and despite its limitations, continues to serve as a hard-to-beat benchmark.

Beyond variance-focused methods, utility-based portfolio construction considers an investor’s subjective perception of risk and reward, allowing for a nuanced approach to decision-making that can address concerns such as tail risks or other features not captured by variance alone. A particularly useful utility function in this context is the exponential utility function with risk parameter , defined as

| (2) |

which has the following remarkable property: when returns are Normally distributed, maximizing the expected exponential utility is equivalent to the mean-variance optimization in (1) (Merton, 1969),

This equivalence establishes a strong link between the mean-variance theory and utility-based approaches, making the latter a compelling alternative for capturing investor preferences (Gerber and Pafum, 1998). However, this equivalence does not hold beyond Normally distributed returns, since the expected utility function cannot be computed in closed-form. Despite recent advances on this problem (Luxenberg and Boyd, 2024), the general problem of decision in the face of uncertainty remains. Specifically, beyond point estimates, we need a reliable estimator of the mean and covariance of the recorded historical time series.

Contributions. We introduce a novel approach to portfolio construction, departing from traditional utility-based methods by adopting a Bayesian framework (Barry, 1974; Black and Litterman, 1992; De Franco et al., 2019; Kato, 2024). Specifically, we reformulate this task as a versatile minmax optimization problem, which can be efficiently addressed using Variational Bayes (VB) (Section 3), while providing formal consistency guarantees (Section 6). Furthermore, we instantiate our proposed algorithm (VB-Portfolio) for several relevant models (Section 4) that we test in practice on real data (Section 5), showing that it achieves state-of-the-art performance in several settings.

Notations. For an arbitrary probability space where is a Polish space, we denote as the set of probability distributions on . Throughout this paper, denotes a generic probability distribution, where its probability space will be clear from context. is the set of squared positive definite matrices of size . For a probability distribution and a random variable , denotes the expectation of when . The Kullback-Leibler (KL) divergence between two probability distributions and is denoted . For a random variable and a measure , we use the infinitesimal notation , generalizing the notation when is countable.

2 Problem Setting

We consider a supervised learning setting where we have access to observations , where each . We assume that is the realization of a stochastic process parameterized by an unknown parameter , . Until Section 4, we do not make any additional assumption on for now. We define a probability space associated with and express our initial uncertainty about this parameter through a prior distribution .

Building on the discussions in Section 1, we formalize our portfolio construction problem in the lens of Bayesian decision theory (Robert, 2007, Chapter 2). The Bayesian decision with respect to a utility function is the decision that maximises the posterior expected utility (or Bayesian risk),

| (3) |

where is the posterior predictive distribution of new (unseen) observation . Note that is a function of , , but this dependency is omitted to simplify notation. Under the particular choice of exponential utility (2), we can rewrite (3) as

| (4) |

for a given fixed by the user. One major challenge in Bayesian modelling is the lack of closed-form solutions for posterior predictive distributions, except for simple statistical models (see Section C.2). Hence, directly computing (4) in closed-form is generally infeasible. While various methods exist to numerically compute this integral (e.g. Monte-Carlo estimates), they tend to be computationally expensive, particularly in high-dimensional spaces. We address this in the following section by rewriting the objective function as a saddle point. We then make use of the same relaxation as in Variational Bayes (VB; Jordan et al., 1999) to approximate the inner optimisation.

3 Exponential Utility Maximization as a Saddle-Point Optimization

3.1 Main Observation

Our main contribution is to show that maximizing an exponential utility function is equivalent to solving a saddle-point optimization problem. We believe that the following result may be of independent interest to anyone seeking to maximize an exponential utility for various applications.

Theorem 1.

The optimal Bayesian decision (4) can be written as a saddle-point,

| (5) |

where is the posterior distribution over the joint parameter , is defined as and is a term that does not depend on .

The proof of this result relies on a well-known change-of-measure lemma, included below for completeness (see Alquier (Lemma 2.2; 2024) for a proof).

Lemma 1 (Change of measure lemma (Donsker and Varadhan, 1983)).

For any probability on a probability space and any measurable function such that ,

We now prove our main result, which applies this change-of-measure on the log of the exponential utility.

Proof of Theorem 1.

By rewriting (4),

where in (i) we took the log in front of the objective function, and in (ii) we marginalized out conditionally on (since ). Applying Lemma 1 with gives

| (6) |

We next have to show that the expression inside the supremum can be expressed as a KL divergence (up to an additive constant that does not depend on ); we observe that for any ,

and therefore, by introducing the probability measure defined as , we have

| (7) |

Combining (6) with (7), we can rewrite the Bayes optimal decision as

where the supremum is indeed achieved for . ∎

We introduce the risk function over all probability measures;

and is the decision that minimizes the risk .

3.2 Variational Bayes Approximation of

Computing is challenging because the normalization constant is intractable for non-conjugate models (for which it is equivalent to computing the integral (4)). We now demonstrate how the min-max formulation in (5) can be leveraged to enable the use of VB approximation.

Maximization over a subspace of measures. Fix an arbitrary decision . Since does not depend on , the distribution that solves the maximum writes222The negative sign is omitted for now but we will plug it in the final objective function.

| (8) |

where we emphasize that depends on since does. VB approximations instead solve a restriction of (8): we define a family of measures for which the restricted problem (8) over this family is considered tractable. For example, the mean-field family (Parisi and Shankar, 1988; Bishop, 2006) assumes independence between parameters: assuming factorizes as a product of subspaces, , the mean-field family of is defined as

Notice that does not make any assumption on the form of the distributions or ’s, but only relies on the factorisation assumption and the underlying statistical model. We denote by the Mean-field variational approximation of , that is,

| (9) |

Since we deal with a parametric underlying statistical model, is also parametric. The main advantage of using is that can be computed numerically since it is the solution of a fixed-point equation.

Proposition 1.

The variational distribution is written as , where for any we have

where for any , denotes the expectation with respect to the measures .

The proof of the previous equation is provided in Appendix C, and is a direct consequence of a well-known result for Mean-field variational inference (Chapter 10; Bishop, 2006).

Minimization over decisions. Once we found the variational approximation for a given , we define the corresponding variational decision by just plugging into (5),

| (10) |

where we introduced the objective function ,

| (11) |

Note that can be seen as an approximation of the risk function , where for all , . Then, one key observation is that once we computed , we don’t have to compute because

where does not depend on , and hence (11) can be computed in closed-form. Since depends on , optimizing with respect to requires to alternate Gradient-descent steps on (11) with adjustment steps (9) in the following way:

i) Gradient-Descent step. We perform one step of gradient descent with a constant step-size ,

ii) Adjustment step. We recompute the variational distribution solution to (5) for the decision . The pseudo-code of our general method (denoted as VB-Portfolio) is shown in Algorithm 1. In the following section, we will introduce specific statistical models to which this algorithm can be applied.

Convexity properties of the objective function. An important property of the objective function (11) is that it enjoys remarkable properties such as convexity and smoothness. Therefore, applying Projected Gradient Descent on , where the projection set is compact and convex ensures that the iterates will converge to an optimal point with value , that is, at rate . We state formally these results in Proposition 2. These properties will also play a crucial role in establishing the statistical convergence of .

Statistical guarantees of Variational Bayes. The restriction of the variational formulation to a smaller set of measures introduces a bias in the resulting decisions. There is a growing literature studying the statistical properties of variational Bayes approximation (Alquier et al., 2016; Wang and Blei, 2019; Alquier and Ridgway, 2020; Yang et al., 2020; Ray and Szabó, 2022; Huix et al., 2024). Those results are not directly transferable to our problem because we do not only require the convergence of the approximate measure but the convergence with respect to the of the objective function; we show that our VB algorithm converges asymptotically with respect to the sample size (see Section 6).

4 Application to Specific Statistical Models

So far, Algorithm 1 remained theoretical since we do not introduce assumptions on the statistical model yet, i.e. we derived a general algorithm that holds for any parametric statistical model . We now introduce relevant statistical models in the context of finance, where the core problem is to estimate the mean of investment returns, and the correlation between these returns. For all these models, we derive the corresponding fixed-point operator and the objective function in closed form in Appendix C.

4.1 Gaussian-Wishart (GW)

For this model, observations (returns) are assumed independent and Normally distributed with unknown mean and precision ; putting a Gaussian prior on the mean and a Wishart prior on the precision matrix,

| (12) | |||||

Since we put prior on both mean and covariance , this model does not have closed-form moments for its joint posterior distribution , so we cannot compute the integral (4) directly. The full expression of the fixed-point operator in Proposition 1 for this model is derived in Lemma 4, along with the corresponding objective function detailed in Lemma 5.

4.2 Autoregressive Model (AR)

The non-dynamic model defined in Section 4.1 is rather conservative, as it assumes no autocorrelation in returns, treating them as independent across time. While this simplifies learning and estimation, it overlooks the temporal dependencies often present in financial data such as market trends. Ignoring these patterns may limit the model’s capacity to capture the true structure of returns. To circumvent this limitation, we introduce a model that incorporates a dynamic in the observations. We first outline a few definitions.

Definition 1 (Matrix normal distribution (Quintana, 1987)).

We say that follows a matrix normal distribution with mean parameter , row-variance and column variance and denote if and only if

where we define as the concatenated vector in mn of a matrix , .

In this model, we arbitrarily333This first observation can be set thanks to previously collected data, which may be available in practice. set the initial value with . Then, the model writes

| (13) |

The full expression of the fixed-point operator in Proposition 1 for this model is derived in Lemma 6, along with the corresponding objective function detailed in Lemma 7.

4.3 Gaussian Process Model (GP)

Gaussian processes (GPs; Williams and Rasmussen, 2006) can model the correlations between returns without assuming a specific functional form, making them particularly well-suited for environments with non-linear dependencies. We first define formally multivariate GPs.

Definition 2 (Multivariate Gaussian process (MGP) (Chen et al., 2020)).

follows a multivariate Gaussian process with mean function , row variance function and column variance , and we denote , if, for every set of points with m any integer, we have , where and .

Putting a multivariate GP prior on the mean returns , the GP model is defined as

| (14) | ||||

where we emphasise that at time step , (i.e. is a multivariate stochastic process). We will use specific kernel functions in numerical experiments. The full expression of the fixed-point operator in Proposition 1 for this model is derived in Lemma 8, and the corresponding objective function in Lemma 9.

5 Numerical Experiments

5.1 Experiments on Real-world Dataset

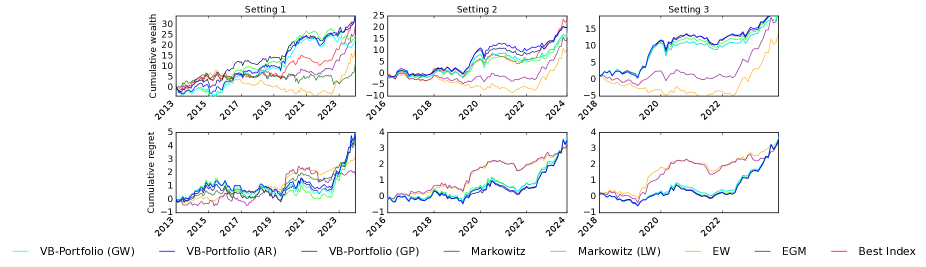

Dataset. We use financial indices associated with the G20 member countries, spanning the period from 2012 to 2024; these data are publicly available444https://finance.yahoo.com/markets/world-indices/. These indices are chosen over individual stock prices to minimize selection and survivorship biases. We apply Exponential Moving Averages (EMA) (Brockwell and Davis, 2002) with 8 different scales to each index and compute the corresponding EMA for all indices. The EMA-transformed signals are then aggregated by averaging across scales, producing dataset with experts, where each column represents the averaged EMA signal at a specific scale, capturing smoothed trends across the indices. Monthly observations are extracted from this transformed dataset, yielding three different settings of increasing sample sizes: (Setting 1), (Setting 2), and (Setting 3).

Baselines. We compare our algorithm, VB-Portfolio, instantiated with models (4.1), (4.2) and (14) against several baseline portfolios. The first is the Equal Weights portfolio (EW, also called the 1/ portfolio), which assigns uniform weights to all assets: . We also consider the Markowitz portfolio (Mwz), as described in Equation 1, . Additionally, a more refined approach is to regularize the covariance matrix estimate, which is particularly advantageous in data-poor regimes. The Ledoit-Wolf method (Ledoit and Wolf, 2003) employs a shrinkage technique to stabilize the sample covariance matrix by combining it with a structured target matrix, typically a scaled identity matrix. The resulting shrunk covariance matrix is defined as , where is the shrinkage intensity. Notably, the optimal value of can be explicitly computed, as derived in Ledoit and Wolf (2003). This adjustment balances bias and variance, resulting in a better-conditioned estimator for high-dimensional settings. We define the corresponding Markowitz-based portfolio as . Finally, we compare our approach against a state-of-the-art method, the Exponential Utility for Gaussian Mixtures (EGM), which maximizes the exponential utility under a Gaussian mixture model assumption for returns (Luxenberg and Boyd, 2024).

Prior parameters For all models, the Wishart prior is set as and , where is the empirical estimate of covariance matrix. For the GW model, we set the prior mean as the empirical mean, and . For the AR model, we set as the MLE estimate of the transition matrix obtained via linear regression on the observations , . We set the row-covariance and column-covariance as identities. For the GP model (14), we choose a Radial basis function kernel parameterized by i.e. , and tune trough Gradient-based optimization (with respect to marginal likelihood). We set the mean function to and the prior column variance as . The hyperparameter choices are discussed in Appendix E.

Results (Cumulative wealth and regret). For each allocation strategy, we compute the out-of-sample cumulative wealth, ( are observations of the testing set, i.e. observations from 2013 for Setting 1, from 2016 for Setting 2 and from 2018 for Setting 3). To enable a fair comparison across strategies with varying levels of risk, we rescale each cumulative wealth by its standard deviation. This risk-adjusted rescaling is a standard convention in portfolio construction literature. Additionally, we plot the strategy corresponding to allocating all mass on the best index in hindsight, defined as the index with the highest cumulative wealth at the end of the testing horizon. To further assess performance, we plot the cumulative regret for each strategy against this best index in hindsight, that is, the difference between the cumulative wealth of the best index in hindsight and the one of the given strategy. We rescale this cumulative difference by its standard deviation. Results are displayed in Figure 1, and show that while VB-Portfolio(GW) exhibits performance comparable to the Markowitz-based portfolio, VB-Portfolio, when instantiated with both the AR and GP models, outperforms the other strategies overall. This superior performance suggests that these models are particularly effective at adapting to evolving market conditions.

Sharpe Ratios Comparison

| Allocation Strategy | Annualized Sharpe Ratio | ||

|---|---|---|---|

| Setting 1 | Setting 2 | Setting 3 | |

| algVB (GW) | |||

| algVB (AR) | 0.90 | 1.16 | |

| algVB (GP) | 0.90 | 0.90 | |

| Markowitz | |||

| Markowitz (LW) | |||

| Equal Weights | |||

| EGM | |||

The Sharpe ratio (Sharpe, 1966, 1994) is a widely used metric for assessing the risk-adjusted performance of investment strategies. It is defined as the ratio of the mean return to the standard deviation, quantifying the return per unit of risk. Let denotes the mean return of strategy over the testing set, and its standard deviation. The annualized Sharpe ratio is then computed as . This metric facilitates meaningful comparisons across strategies by highlighting those that deliver higher returns relative to risk. As illustrated in Table 1, VB-Portfolio(AR) achieves the highest Sharpe ratio overall, closely followed by VB-Portfolio(GP). Both methods consistently outperform traditional approaches, such as the Markowitz portfolio, particularly in Settings 1 and 2, where the smaller sample sizes lead to less stable estimates for the other strategies. These findings underscore the robustness of the proposed methods in data-poor environments, demonstrating that Bayesian approaches are well-suited to regularizing estimates and mitigating the impact of limited training data.

5.2 Numerical Consistency

To assess the consistency of our approximation to , we use a gradient descent-based algorithm that leverages Markov Chain Monte Carlo (MCMC) sampling to estimate the gradient of the objective function.

Approximating the objective function. First, we want to approximate the integral (4) for any ;

where are samples from the predictive posterior distribution . This can be done with the Gibbs sampling algorithm (Geman and Geman, 1984): in fact, by remarking that

and since we now how to sample from the conditional posterior , we can generate samples from the joint posterior distribution . From this sequence, we can now sample from the distribution conditionally on one sample , by drawing a sample from the distribution

resulting in a sequence of samples .

Approximating the gradient . By Leibniz rule, we have

for which we can approximate by

The pseudo-code of this MCMC algorithm is shown in Algorithm 2. We instantiate this algorithm for GW and AR model in Appendix D, where we provide in particular the expressions of the conditional posteriors and .

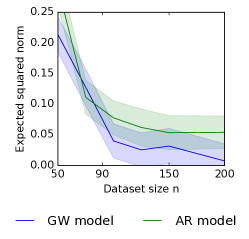

Consistency with synthetic data.

To evaluate the numerical consistency of our method, we show that converges to as the sample size grows. We generate synthetic datasets for both GW model and AR model with . For the GW model, we randomly set each component of the true mean return, , according to a uniform distribution, , and use an identity covariance matrix, . For the AR model, the true transition matrix is set to a diagonal matrix with values evenly spaced from 0.6 to 0.99, while the covariance matrix is . We generate datasets of varying sizes, with ranging from 50 to 200. For the GW model, we simulate data according to (4.1), and for the AR model, we follow (4.2). For each dataset, we compute the decision vector using both VB-Portfolio and MCMC-Portfolio, where the Gibbs sampler is run for iterations. We compute , where the expectation is taken over 50 repetitions with newly generated datasets.

Figure 2 illustrates the relationship between this expected norm difference and the dataset size . As increases, we observe that the difference between the two decision methods diminishes, confirming the numerical consistency of VB-Portfolio with respect to MCMC-Portfolio as the sample size grows.

6 Theoretical Guarantees

In this section, we assume that is compact and convex, as is the case when , the standard simplex. As discussed earlier, we cannot directly rely on existing results concerning the statistical efficiency of variational Bayes (VB) approximations. Instead, we focus on guarantees on which is a critical point of the objective function of the VB approximation. We introduce the notation for the result of our algorithm after iterations of Algorithm 1. Under the formal conditions stated below, we establish the following two key theoretical results:

Numerical convergence. converges to with respect to the number of iterations at rate .

Statistical consistency. converges with respect to the sample size to a Markowitz decision.

6.1 Numerical Convergence

We begin by addressing the convergence of our algorithm, which relies on the convexity and smoothness properties of the objective function .

Proposition 2 (Properties of ).

For a fixed dataset size , is convex and smooth. Let denote the smoothness constant of . Using Gradient descent with a step size of and initial point ensures

This result shows that if the fixed-point iteration converges to at each step we compute , then converges to at a rate . The proof of Proposition 2 (given in Section B.2) relies on expressing as a Fenchel-Legendre transformation of the strongly convex map .

6.2 Statistical Consistency

Next, we establish asymptotic consistency results as the sample size , focusing on the behaviour of the decision . For this, we introduce an assumption regarding the asymptotic behaviour of the fixed-point equation.

Assumption 1.

As the sample size , the variational distribution converges pointwise,

where is solution to the asymptotic fixed-point operator: denoting the fixed point operator defined in Proposition 1, for any , if then the operator satisfies .

Assumption 1 is a relatively strong assumption, as rigorously proving it would require showing that the fixed-point operator is contractant across all models considered. However, we provide numerical evidence in Section E.1 to support this assumption, indicating that it is reasonable in practice. Next we derive asymptotic consistency of the variational decision under this assumption.

Theorem 2 (Consistency of the variational decision).

The proof of Theorem 2, given in Section B.3, involves a key technical challenge: interchanging the limit and the . Specifically, we need to show:

In particular, this step requires epi-convergence of the sequence , which can be leveraged by the compacity property of and .

7 Conclusion

We showed that Bayesian optimal decision for exponential utility can be interpreted as a saddle-point problem. We developed a computationally efficient algorithm based on variational Bayes with provable convergence guarantees, demonstrating its effectiveness in real-world portfolio optimization problems.

Maximizing exponential utility functions. Our min-max formulation (Theorem 1) provides a versatile framework for scenarios where the expected utility lacks a closed-form solution. This methodology not only bridges theoretical and practical domains but also holds promise for broader applications, particularly in areas like reinforcement learning (Marthe et al., 2024), where exponential utility functions are pivotal for navigating decision-making under uncertainty.

Beyond Gradient-Descent.Although our objective function is convex and smooth, leveraging advanced optimization techniques could unlock further potential. Techniques such as Nesterov’s acceleration (Nesterov et al., 2018) and mirror-descent-based methods (Nemirovski, 2004) for saddle-point optimization present opportunities to enhance convergence rates and scalability. These methods could prove especially beneficial for portfolio construction in high-dimensional settings.

8 Acknowledgements

The authors would like to warmly thank Emmanuel Sérié for insightful discussions and remarks on this work. We also thank Vincent Fortuin for feedbacks.

Nicolas Nguyen and Claire Vernade are funded by the Deutsche Forschungsgemeinschaft (DFG) under both the project 468806714 of the Emmy Noether Programme and under Germany’s Excellence Strategy – EXC number 2064/1 – Project number 390727645.

Nicolas Nguyen and Claire Vernade thank the international Max Planck Research School for Intelligent Systems (IMPRS-IS).

References

- Agrawal et al. (2022) Raj Agrawal, Uma Roy, and Caroline Uhler. Covariance matrix estimation under total positivity for portfolio selection. Journal of Financial Econometrics, 20(2):367–389, 2022.

- Alquier (2024) Pierre Alquier. User-friendly introduction to pac-bayes bounds. Foundations and Trends® in Machine Learning, 17(2):174–303, 2024.

- Alquier and Ridgway (2020) Pierre Alquier and James Ridgway. Concentration of tempered posteriors and of their variational approximations. The Annals of Statistics, 2020.

- Alquier et al. (2016) Pierre Alquier, James Ridgway, and Nicolas Chopin. On the properties of variational approximations of gibbs posteriors. The Journal of Machine Learning Research, 17(1):8374–8414, 2016.

- Bach (2024) Francis Bach. Learning theory from first principles. MIT press, 2024.

- Barry (1974) Christopher B Barry. Portfolio analysis under uncertain means, variances, and covariances. The Journal of Finance, 29(2):515–522, 1974.

- Benaych-Georges et al. (2023) Florent Benaych-Georges, Jean-Philippe Bouchaud, and Marc Potters. Optimal cleaning for singular values of cross-covariance matrices. The Annals of Applied Probability, 33(2):1295–1326, 2023.

- Benichou et al. (2016) Raphael Benichou, Yves Lempérière, Julien Kockelkoren, Philip Seager, Jean-Philippe Bouchaud, Marc Potters, et al. Agnostic risk parity: Taming known and unknown-unknowns. arXiv preprint arXiv:1610.08818, 2016.

- Billingsley (2013) Patrick Billingsley. Convergence of probability measures. John Wiley & Sons, 2013.

- Bishop (2006) C Bishop. Pattern recognition and machine learning. Springer google schola, 2:531–537, 2006.

- Black and Litterman (1992) Fischer Black and Robert Litterman. Global portfolio optimization. Financial analysts journal, 48(5):28–43, 1992.

- Boyd and Vandenberghe (2004) Stephen Boyd and Lieven Vandenberghe. Convex optimization. Cambridge university press, 2004.

- Bradbury et al. (2018) James Bradbury, Roy Frostig, Peter Hawkins, Matthew James Johnson, Chris Leary, Dougal Maclaurin, George Necula, Adam Paszke, Jake VanderPlas, Skye Wanderman-Milne, and Qiao Zhang. JAX: composable transformations of Python+NumPy programs, 2018. URL http://github.com/google/jax.

- Brockwell and Davis (2002) Peter J Brockwell and Richard A Davis. Introduction to time series and forecasting. Springer, 2002.

- Bun et al. (2017) Joël Bun, Jean-Philippe Bouchaud, and Marc Potters. Cleaning large correlation matrices: tools from random matrix theory. Physics Reports, 666:1–109, 2017.

- Cesa-Bianchi and Lugosi (2006) Nicolo Cesa-Bianchi and Gábor Lugosi. Prediction, learning, and games. Cambridge university press, 2006.

- Chen et al. (2020) Zexun Chen, Bo Wang, and Alexander N Gorban. Multivariate gaussian and student-t process regression for multi-output prediction. Neural Computing and Applications, 32:3005–3028, 2020.

- Cover (1991) Thomas M Cover. Universal portfolios. Mathematical finance, 1(1):1–29, 1991.

- De Franco et al. (2019) Carmine De Franco, Johann Nicolle, and Huyên Pham. Bayesian learning for the markowitz portfolio selection problem. International Journal of Theoretical and Applied Finance, 22(07):1950037, 2019.

- Donsker and Varadhan (1983) Monroe D Donsker and SR Srinivasa Varadhan. Asymptotic evaluation of certain markov process expectations for large time. iv. Communications on pure and applied mathematics, 36(2):183–212, 1983.

- Geman and Geman (1984) Stuart Geman and Donald Geman. Stochastic relaxation, gibbs distributions, and the bayesian restoration of images. IEEE Transactions on pattern analysis and machine intelligence, pages 721–741, 1984.

- Gerber and Pafum (1998) Hans U Gerber and Gérard Pafum. Utility functions: from risk theory to finance. North American Actuarial Journal, 2(3):74–91, 1998.

- Harvey et al. (2010) Campbell R Harvey, John C Liechty, Merrill W Liechty, and Peter Müller. Portfolio selection with higher moments. Quantitative Finance, 10(5):469–485, 2010.

- Huix et al. (2024) Tom Huix, Anna Korba, Alain Durmus, and Eric Moulines. Theoretical guarantees for variational inference with fixed-variance mixture of gaussians. arXiv preprint arXiv:2406.04012, 2024.

- Ismail and Pham (2019) Amine Ismail and Huyên Pham. Robust markowitz mean-variance portfolio selection under ambiguous covariance matrix. Mathematical Finance, 29(1):174–207, 2019.

- Jézéquel et al. (2022) Rémi Jézéquel, Dmitrii M Ostrovskii, and Pierre Gaillard. Efficient and near-optimal online portfolio selection. arXiv preprint arXiv:2209.13932, 2022.

- Jordan et al. (1999) Michael I Jordan, Zoubin Ghahramani, Tommi S Jaakkola, and Lawrence K Saul. An introduction to variational methods for graphical models. Machine learning, 37:183–233, 1999.

- Kato (2024) Masahiro Kato. General bayesian predictive synthesis. arXiv preprint arXiv:2406.09254, 2024.

- Ledoit and Wolf (2003) Olivier Ledoit and Michael Wolf. Improved estimation of the covariance matrix of stock returns with an application to portfolio selection. Journal of empirical finance, 10(5):603–621, 2003.

- Li and Hoi (2018) Bin Li and Steven Chu Hong Hoi. Online portfolio selection: principles and algorithms. Crc Press, 2018.

- Luo et al. (2018) Haipeng Luo, Chen-Yu Wei, and Kai Zheng. Efficient online portfolio with logarithmic regret. Advances in neural information processing systems, 31, 2018.

- Luxenberg and Boyd (2024) Eric Luxenberg and Stephen Boyd. Portfolio construction with gaussian mixture returns and exponential utility via convex optimization. Optimization and Engineering, 25(1):555–574, 2024.

- Markowitz (1952) Harry Markowitz. Portfolio selection. The Journal of Finance, 7(1):77–91, 1952.

- Marthe et al. (2024) Alexandre Marthe, Aurélien Garivier, and Claire Vernade. Beyond average return in markov decision processes. Advances in Neural Information Processing Systems, 36, 2024.

- Merton (1969) Robert C Merton. Lifetime portfolio selection under uncertainty: The continuous-time case. The review of Economics and Statistics, pages 247–257, 1969.

- Merton (1972) Robert C Merton. An analytic derivation of the efficient portfolio frontier. Journal of financial and quantitative analysis, 7(4):1851–1872, 1972.

- Nemirovski (2004) Arkadi Nemirovski. Prox-method with rate of convergence o (1/t) for variational inequalities with lipschitz continuous monotone operators and smooth convex-concave saddle point problems. SIAM Journal on Optimization, 15(1):229–251, 2004.

- Nesterov et al. (2018) Yurii Nesterov et al. Lectures on convex optimization, volume 137. Springer, 2018.

- Orabona and Jun (2023) Francesco Orabona and Kwang-Sung Jun. Tight concentrations and confidence sequences from the regret of universal portfolio. IEEE Transactions on Information Theory, 2023.

- Parisi and Shankar (1988) Giorgio Parisi and Ramamurti Shankar. Statistical field theory. American Journal of Physics, 1988.

- Quinonero-Candela and Rasmussen (2005) Joaquin Quinonero-Candela and Carl Edward Rasmussen. A unifying view of sparse approximate gaussian process regression. The Journal of Machine Learning Research, 6:1939–1959, 2005.

- Quintana (1987) Jose Mario Quintana. Multivariate Bayesian forecasting models. PhD thesis, University of Warwick, 1987.

- Ray and Szabó (2022) Kolyan Ray and Botond Szabó. Variational bayes for high-dimensional linear regression with sparse priors. Journal of the American Statistical Association, 117(539):1270–1281, 2022.

- Robert (2007) Christian P Robert. The Bayesian choice: from decision-theoretic foundations to computational implementation, volume 2. Springer, 2007.

- Rockafellar and Wets (2009) R Tyrrell Rockafellar and Roger J-B Wets. Variational analysis, volume 317. Springer Science & Business Media, 2009.

- Sharpe (1966) William F Sharpe. Mutual fund performance. The Journal of business, 39(1):119–138, 1966.

- Sharpe (1994) William F Sharpe. The sharpe ratio. Journal of portfolio management, 21(1):49–58, 1994.

- Van Erven et al. (2020) Tim Van Erven, Dirk Van der Hoeven, Wojciech Kotłowski, and Wouter M Koolen. Open problem: Fast and optimal online portfolio selection. In Conference on Learning Theory, pages 3864–3869. PMLR, 2020.

- Wang and Blei (2019) Yixin Wang and David M Blei. Frequentist consistency of variational bayes. Journal of the American Statistical Association, 114(527):1147–1161, 2019.

- Williams and Rasmussen (2006) Christopher KI Williams and Carl Edward Rasmussen. Gaussian processes for machine learning, volume 2. MIT press Cambridge, MA, 2006.

- Yang et al. (2020) Yun Yang, Debdeep Pati, and Anirban Bhattacharya. -variational inference with statistical guarantees. The Annals of Statistics, 48(2):886–905, 2020.

Appendix A Difference Between our Work and Online Portfolio Selection

The field of machine learning has contributed to portfolio selection by framing it as an online learning problem (Cover, 1991; Cesa-Bianchi and Lugosi, 2006). The OPS approach consists in sequentially allocating capital across assets to maximize the cumulative log-wealth over time. Formally, at each time step , the investor selects a portfolio vector based on the information available up to that point, with the goal of maximizing the log-wealth achieved after rounds , where are the asset returns. This online framework has led to the development of a variety of algorithms with strong theoretical guarantees, particularly in terms of regret bounds, measuring how much worse the cumulative wealth of the algorithm is compared to that of an optimal strategy selected in hindsight. Early works such as Cover’s universal portfolio algorithm (Cover, 1991) introduced a strategy that could asymptotically achieve the same wealth as the best constant-rebalanced portfolio. More recent advances have continued to refine these results, providing tighter regret bounds and more efficient learning mechanisms in both stochastic and adversarial settings (Li and Hoi, 2018; Luo et al., 2018; Van Erven et al., 2020; Jézéquel et al., 2022; Orabona and Jun, 2023).

Despite its theoretical richness and the mathematical sophistication, the OPS literature has seen limited adoption among practitioners. A key reason for this limited uptake is the lack of practical assumptions. Most of these approaches assume minimal structure on the returns (often treating them as adversarially generated sequences) leading to strategies that have general worst-case theoretical guarantees but sometimes overly conservative for real-world scenarios. This assumption of adversarial returns is far from what is commonly observed in practice, where returns often exhibit patterns, correlations, and statistical properties that can be exploited for better performance.

Additionally, the evaluation metric used in OPS, namely the log-wealth or cumulative logarithmic return, is not commonly used by practitioners to assess portfolio performance. In practice, metrics such as risk-adjusted returns (e.g. Sharpe ratio (Sharpe, 1994) or expected exponential utilities) are more commonly employed to assess and compare portfolio strategies. While the use of log-wealth is theoretically motivated by its asymptotic properties (e.g., maximizing the growth rate of wealth), its practical implications may not align well with the objectives of real-world investors. In this work, we aim to bridge this gap by incorporating more realistic assumptions about asset returns and developing a framework that is computationally feasible and practically aligned with investor objectives.

Appendix B Proofs of Section 6

B.1 Auxiliary Lemmas

Lemma 2.

The mean-field space is closed in the space of probability measures .

Proof.

Consider any sequence in that has a limit in . Then for any , can be factorized as

where we recall that we assume that factorizes as a product of subspaces, . Then limit of exists by construction, and

which proves that the limit of any convergent sequence in has its limit in , and hence is closed in . ∎

B.2 Proof of Proposition 2

For any and any measurable in , is a convex map since it is defined as the Fenchel-Legendre transformation of , with (and the space of probability measures is a convex set). Thus, we also have that the map is convex since for any probability measure , is convex (as a linear map) and is the pointwise supremum of a family of convex function (the supremum conserves convexity (Boyd and Vandenberghe, 2004)). Taking h as and remarking that it is a convex function with respect to for a given shows that is convex: indeed, by composition of convex functions, is convex with respect to , and so . Moreover, is strongly convex on the space of probability measures , and hence is smooth (as a convex conjugate of a strongly convex function). Hence, is also smooth by composition (with the same arguments as above for the convexity).

The convergence rate mentioned follows directly from the classical results of gradient descent applied to convex, smooth functions (see, for instance, Bach (2024, Chapter 5)).

B.3 Proof of Theorem 2

The first step involves interchanging the limit and the argmin over , allowing us to express it as:

This step is non-trivial because the argmin function is a set, necessitating the use of general regularity conditions. Additionally, is defined implicitly as a supremum over a space of measures. The second step involves analyzing , for which we know how to proceed based on the statistical model introduced in Section 4.

B.3.1 Inverting Limit and Argmin

We rely on Rockafellar and Wets (2009, Theorem 7.33) for this purpose; this strong result requires to show the two following conditions:

-

C.1.

epi-converges to , where is lower-semi-continuous and proper.

-

C.2.

is a lower-semi-continuous and proper sequence.

To show that epi-converges, we first establish some general regularity properties of this sequence, from which the epi-convergence will naturally follow. For any and , we introduce the functional

| (15) |

is a uniformly continuous sequence. Since is a Polish space, is also a Polish space. According to Billingsley (2013, Th. 1.3), is a space of tight measures. By Prokhorov’s theorem, is relatively compact in the weak-* topology. Given that is closed in (Lemma 2), it follows that is also compact as a closed subset of a relatively compact space. By the Maximum theorem, is continuous on . Furthermore, for any , the function , as defined in (15), is linear with respect to (since the KL term is independent of ), making uniformly continuous in . Consequently, since is continuous on a compact set and is uniformly continuous with respect to , we have that for all and for any , there exists a such that

and therefore,

independently in , which is the definition of uniform continuity of .

is epi-convergent sequence. Since is uniformly continuous, smooth, and convex on a compact domain for any (Proposition 2), it follows that is uniformly bounded on this compact space, implying that is equicontinuous. Additionally, converges pointwise to a limit , as established by Assumption 1. By the Arzelà-Ascoli theorem, the equicontinuous sequence converges uniformly to . According to Rockafellar and Wets (2009, Theorem 7.11), epi-converges if and only if it converges continuously. Since uniform convergence implies continuous convergence, we conclude that is epi-convergent to , thereby verifying C.1.

Lower semi-continuity and proper conditions. Since is continuous, it is also lower semi-continuous. Furthermore, because converges continuously, is continuous and thus lower semi-continuous as well. To show that any preimage of a set (e.g., a closed interval) is compact, note that since is continuous, is a closed subset of . Given that is compact, is a closed subset of a compact space, and hence compact. The same reasoning applies to due to continuous convergence. Therefore, we have verified C.2.

B.3.2 Asymptotic Objective Function

We now turn our attention to computing . Since converges to a distribution , where is the fixed point of (Assumption 1), we can explicitly compute using the known form of as a function of for the statistical models under consideration. The following lemma formalizes this result.

Lemma 3.

For both GW (4.1) and AR (4.2) models, we have

where for the GW model we have

and for the AR model

which is the corresponding sample mean estimate for the GW and the AR model respectively, and the corresponding sample covariance estimate. Hence, the asymptotic variational decision writes

i.e. the Markowitz decision in .

We now prove Lemma 3 for both GW and AR model.

Proof of Lemma 3 for GW model.

Starting from Lemma 4, the asymptotic operator is the limit of the operator defined in Lemma 4 when (by Assumption 1), giving

Thanks to Assumption 1, the fixed point of denoted by satisfies

where

Plugging this solution the objective function in Lemma 5 and keeping only terms depending on , the asymptotic objective function writes

∎

Proof of Lemma 3 for AR model.

Starting from Lemma 6, the asymptotic operator writes

where denotes the last observation of the dataset.

Thanks to Assumption 1, the fixed point of denoted by satisfy

where

Plugging this solution to the objective function (Lemma 7) and keeping only terms depending on , the asymptotic objective function writes

∎

Appendix C Derivation of VB-Portfolio for Specific Models: Fixed-Point Operators and Objective Functions

Let us begin by introducing some convenient compact notations.

Definition 3 (Kronecker product).

Let and . Then the kronecker product between and , denoted by is defined as follows,

Definition 4 (Vectorization operator).

Let , such that

Then, we denote the vector of size such that .

Remark 2.

Using Definition 1, the AR model (4.2) is equivalent to the following formulation,

Proposition 3 (Properties of operator).

xx

-

•

.

-

•

.

-

•

.

We refer to Quintana (1987) for the proofs of these results.

C.1 General Fixed-Point Equation (Proof of Proposition 1)

This proof is a direct application of Bishop (Chapter 10; 2006) to our problem; we have an additional risk term , which modifies the computation of the complete joint distribution. We recall that is the probability distribution defined as . Then for any , we have

where

is called the evidence lower bound (ELBO), and is the only term that depends on . Hence, minimizing is equivalent at maximizing . Then, for any , we have

| (16) |

Keeping terms that depend on only and applying Fubini theorem, we have

The maximizer of with respect to each of the ’s can be derived (by computing the Lagragian of (16) (Jordan et al., 1999)), and we can show that the maximum is reached when

| (17) |

which can be seen as the expectation of taken with respect to all parameters with measure except . The main advantage of using mean-field assumption is that (17) yields to a natural algorithm where we update successively each ’s until stabilization.

C.2 The Gaussian-Gaussian Model

We begin with a straightforward example where the covariance matrix is assumed to be deterministically known. This setting is not realistic since estimating is one main goal of portfolio selection. Given the conjugate nature of this model, we can directly compute the optimal Bayes decision by explicitly calculating and minimizing the risk function . We show how to instantiate VB-Portfolio for this model primarily for illustrative purposes.

By putting a prior distribution on the mean, the Gaussian-Gaussian model writes

| (18) | |||||

C.2.1 Computing Directly

In this (conjugate) model, the posterior predictive and the posterior parameter can be directly computed explicitly,

where (by completing the Gaussian square, e.g. see Bishop (Chapter 2; 2006))

Therefore, in this model, the risk function given in (4) can be directly computed,

where is a constant that does not depend on , and is minimized when

| (19) |

C.2.2 VB-Portfolio Instantiated on Gaussian-Gaussian Model

While we can explicitly compute (19), we outline how VB-Portfolio operates for this simple model to provide a clear illustration. The first goal is to compute the fixed-point operator for this model (defined implicitely in Proposition 1). For this model, since the estimation only focuses on the mean return , the mean-field family writes

and the joint posterior can be written as

Therefore, from Proposition 1, the variational distribution for is given by

where and , and by doing the same as above, the variational distribution for parameter is given by

where

| (20) |

Combining these equations leads to the following fixed-point system ,

The remarkable property of the Gaussian-Gaussian case is that the operator has an unique fixed-point; defining

| (21) |

we have

The second step is to compute the objective function based on the parameters defined by by plugging these parameters to (10); for any ,

with

Since and do not depend on and given the expressions of the parameters and defined above, we have

| (22) |

and after a few simplifications, we obtain

C.3 VB-Portfolio for the Gaussian-Wishart Model

We start by deriving the fixed-point equation, and then we derive the corresponding objective function .

Lemma 4 (Solution of (9) under Gaussian-Wishart model).

Under the stationary Gaussian-Wishart model (4.1), for any , the corresponding variational distribution can be factorised as follows,

where , and . Moreover, the variational parameters satisfy a fixed-point equation , where is given as follows:

Proof.

We first express independently of the underlying statistical model;

| (23) |

where the first equation follows from the definition of in Theorem 1 and the second equation follows from Bayes rule. Since the model (4.1) involves i.i.d. observations conditionally on the parameters, (C.3) gives

By Proposition 1, we can compute each variational distribution , and :

which gives, by completing the Gaussian square with respect to the variable ,

| (24) | ||||

| where | ||||

For the mean variational distribution ,

which gives, by completing the Gaussian square with respect to the variable ,

| where | |||

∎

Finally, for the precision variational distribution ,

Identifying the corresponding terms with a Wishart distribution yields to

| where | |||

Lemma 5 (Objective function under stationary Gaussian-Wishart model).

Fir any , let be the parameters of the corresponding variational distribution under the stationary Gaussian-Wishart model (4.1). Then, the objective function can be written as

Proof.

From Lemma 4, we found that the variational distribution for the GW model can be written as

Starting from the definition of , we have, for any ,

where is a constant that does not depend on . We now aim at computing each of these terms. One can easily verify that

Moreover,

We can compute each of these terms exactly the same way we did in the proof of Lemma 4, and combining these with the terms above give the desited expression. ∎

C.4 VB-Portfolio for the AR Model

Lemma 6 (Solution of (9) under AR(1) model).

Under AR model (4.2), for any , the corresponding variational distribution can be factorised as follows,

where , , . Moreover, the variational parameters satisfy a fixed-point equation , where is given as follows:

where is the spectral decomposition of .

Proof.

First, we write by remarking

| (25) |

On behalf of (4.2), (C.4) becomes

Keeping only terms that depend on the variable ,

which gives, by completying the Gaussian square with respect tp ,

| where | |||

For the variational distribution with respect to ,

where the last line follows from Proposition 3. We can show with the exact same arguments that

and for the third term,

Adding (1), (2) and (3) and completing the corresponding Gaussian squares gives

| where | |||

The variational distribution with respect to requires more efforts:

where we refer to the proof in Lemma 4 for the computation in the second line. Then term inside the trace writes

The main difficulty here is to compute the term related to ; extracting this term gives

The first trace term of the last line writes

while the second term gives,

where we denote the spectral decomposition of the covariance matrix . Then we have

Combining all these yields to

| where | |||

∎

We next derive the corresponding objective function.

Lemma 7 (Objective function under AR model).

For any , let the parameters of the corresponding variational distribution under the AR model (4.2). Then, the objective function can is written as

Proof.

From Lemma 8, we found that the variational distribution for the AR model can be written as

Starting again from the definition of , we have, for any ,

where

Moreover,

We can compute each of these terms exactly the same way we did in the proof of Lemma 6, and combining these with the terms above give the desited expression. ∎

C.5 VB-Portfolio for the Gaussian Process Model

Lemma 8 (Solution of (9) under Gaussian-process Wishart model).

Under GP model (4.1), for any , the corresponding variational distribution can be factorised as follows,

where , , . At time step , the variational parameters satisfy a fixed-point equation , where is given as follows:

Proof.

First, we write as

First, the variational distribution can be derived as

The variational distribution can be derived by deploying the GP prior on the indices ;

where we define as the concatenated vector of size , and as the matrix of size whose entries are for . Then we have

where we define as the concatenated vector , and the concatenated vector . Therefore, we have

where we define the mean function and covariance functions on indices ,

Finally, the variational distribution can be derived as

The term inside the expectation gives

Hence,

where

∎

Lemma 9 (Objective function under Gaussian Process model).

For any , let the parameters of the corresponding variational distribution under the GP model (14). Then, the objective function can is written as

Proof.

From Lemma 8, we found that the variational distribution for the AR model can be written as

Starting again from the definition of , we have, for any ,

where

Moreover,

We can compute each of these terms exactly the same way we did in the proof of Lemma 8, and combining these with the terms above give the desited expression. ∎

C.6 Additional Models

AR(p) Model. We can extend our AR model (which is in reality an AR(1) model) to an AR(p) model with by extending the simply dimension. In fact, an AR(p) model writes

which can be written as a tensor AR(1) model,

where

is called the companion matrix. Hence, the AR(p) model reduces to an AR(1) model on with different matrix parameters to infer.

Appendix D Derivation of MCMC-Portfolio for Specific Models

We derive specific instances of Algorithm 2 for both the GW and AR models, with a particular focus on detailing the form of the conditional posteriors.

D.1 GW Model

The joint parameter posterior cannot be derived in closed-form, but we have the following conditional posteriors

Applying Gibbs sampling with these two conditional posteriors yield to a chain . For a given , the distribution is defined as

Hence, the algorithm MCMC-Portfolio(GW) is defined as follows:

D.2 AR Model

Here again, the joint posterior distribution cannot be computed in closed-form; we can compute the conditional posterior as

Therefore, we have , where

We also have the conditional posterior for the precision matrix,

Therefore, we can have samples from the joint posterior distribution . For a given sample , conditionally on the posterior samples , and the distribution is given by

The algorithm MCMC-Portfolio(AR) can be instantiated as follows:

Appendix E Additional Numerical Experiments

The code is provided in the supplementary material.

E.1 Numerical Discussions on Assumption 1

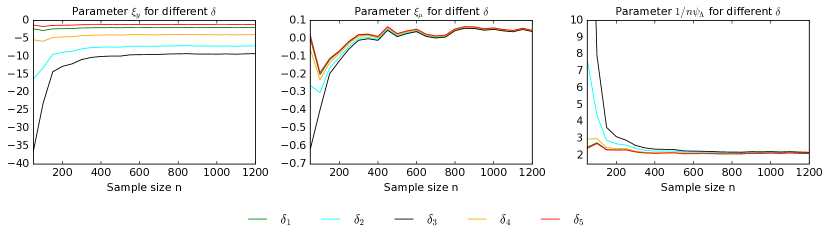

We evaluate the convergence of the variational parameters as the sample size increases. Specifically, we generate synthetic data with dimension under the GW model, and for values of , we compute the variational parameters for different random values of , using the corresponding fixed-point computation. Figure 3 illustrates that the variational distribution derived from the fixed-point equation converges to the variational distribution obtained from the asymptotic fixed-point operator.

E.2 Number of Fixed-point Iterations

We evaluate the difference in the value function, , of our algorithm when applied to the GW model on a synthetic dataset. We set and fix , and examine the impact of the number of inner iterations performed on the fixed-point computation. Figure 4 demonstrates that insufficient inner iterations result in non-convergence of the value function , as the supremum in the objective function is not reached.

E.3 Computational Complexities

By employing the mean-field assumption, our algorithm VB-Portfolio simplifies the optimization problem from a measure-based setting (Equation 5) to a finite-dimensional parametric optimization problem. The primary computational burden lies in the inversion of matrices for both the stationary and autoregressive Gaussian-Wishart models, resulting in a computational complexity of . In contrast, the Gaussian Process (GP) model faces scalability challenges, as it requires the inversion of matrices, leading to cubic complexity with respect to both dimension dataset size . Existing works such as those proposed by Quinonero-Candela and Rasmussen (2005) aim at reducing this inversion complexity; we leave this challenging task as future work.