Series-to-Series Diffusion Bridge Model

Abstract

Diffusion models have risen to prominence in time series forecasting, showcasing their robust capability to model complex data distributions. However, their effectiveness in deterministic predictions is often constrained by instability arising from their inherent stochasticity. In this paper, we revisit time series diffusion models and present a comprehensive framework that encompasses most existing diffusion-based methods. Building on this theoretical foundation, we propose a novel diffusion-based time series forecasting model, the Series-to-Series Diffusion Bridge Model (), which leverages the Brownian Bridge process to reduce randomness in reverse estimations and improves accuracy by incorporating informative priors and conditions derived from historical time series data. Experimental results demonstrate that delivers superior performance in point-to-point forecasting and competes effectively with other diffusion-based models in probabilistic forecasting.

1 Introduction

Diffusion models (Ho et al., 2020; Song et al., 2020) have emerged as powerful tools for time series forecasting, offering the capability to model complex data distributions. Building on their success in other domains, such as computer vision (Saharia et al., 2022; Rombach et al., 2022) and natural language processing (Reid et al., 2022; Ye et al., 2023), researchers have increasingly applied diffusion models to time series prediction. This approach has shown promise in capturing the intricate temporal dependencies and uncertainty in time series data, leading to significant advancements in forecasting accuracy and reliability (Rasul et al., 2021; Tashiro et al., 2021; Alcaraz & Strodthoff, 2022; Li et al., 2024).

However, the inherent stochasticity of diffusion models makes multivariate time series forecasting challenging. Specifically, most of these methods employ a standard forward diffusion process that gradually corrupts future time series data until it converges to a standard normal distribution. Consequently, their predictions originate from pure noise, lacking temporal structure, with historical time series data merely conditioning the reverse diffusion process and offering limited improvement. This approach often results in forecasting instability and the generation of low-fidelity samples (as shown in Figure 1). While diffusion-based methods perform adequately in probabilistic forecasting, their point-to-point prediction accuracy lags behind that of deterministic models, e.g., Autoformer (Wu et al., 2021), PatchTST (Nie et al., 2022), and DLinear (Zeng et al., 2023).

To improve the deterministic estimation performance of diffusion models on time series, we first revisit and consolidate existing non-autoregressive diffusion-based time series forecasting models under a unified framework, demonstrating that these models are fundamentally equivalent, differing primarily in their choice of parameters and network architecture. Based on this framework, we propose a novel diffusion-based time series forecasting model, Series-to-Series Diffusion Bridge Model (). employs the diffusion bridge as its foundational architecture, which proves effective for multivariate time series forecasting. Specifically, uses the Brownian Bridge to pin down the diffusion process at both ends, reducing the instability caused by noisy input and enabling the accurate generation of future time step features from historical time series. By adjusting the posterior variance, behaves as a deterministic generative model without any Gaussian noise, thereby ensuring stability and precise point-to-point forecasting results.

In our experiments, we employ seven real-world datasets as benchmarks, including Weather, Influenza-like Illness (ILI), Exchange Rate (Lai et al., 2018), and Electricity Transformer Temperature datasets (ETTh1, ETTh2, ETTm1, ETTm2) (Zhou et al., 2022). We conduct experiments across various time series forecasting scenarios, covering both point-to-point and probabilistic forecasting. Through extensive testing across these scenarios, our proposed method, , demonstrates superior performance over both standard conditional diffusion-based models and a wide range of advanced time series prediction models.

Our main contributions are summarized as follows:

-

•

In this paper, we propose a comprehensive framework for non-autoregressive time series diffusion models, into which most existing diffusion-based methods can be integrated. This framework clarifies the interrelationships between these methods and highlights practical implications for diffusion models aimed at point-to-point time series forecasting.

-

•

Based on this framework, we introduce the Series-to-Series Diffusion Bridge Model (), which utilizes the Brownian Bridge diffusion process to reduce the randomness in reverse process of diffusion estimations. The proposed model uses linear approaches to create informative priors and conditions, thereby improving forecast accuracy by effectively using historical information for multivariate time series.

-

•

Extensive experimental results validate the effectiveness of , which outperforms state-of-the-art time series diffusion models in point-to-point forecasting tasks. Moreover, achieves forecasting performance on par with probabilistic models.

2 Related Works

Diffusion-based Time Series Forecasting.

Recently, a range of diffusion-based methods are proposed for time series forecasting. These methods generally adhere to the framework of the standard diffusion model, with their primary distinctions stemming from variations in the denoising network and conditional mechanisms.

TimeGrad (Rasul et al., 2021) is the pioneer of these diffusion-based methods, integrating diffusion models with an RNN-based encoder to handle historical time series. However, its reliance on autoregressive decoding can lead to error accumulation and slow inference times. To tackle this problem, CSDI (Tashiro et al., 2021) employs an entire time series as the target for diffusion and combines it with a binary mask (which denotes missing values) as conditional inputs into two transformers. This masking-based conditional mechanism enables CSDI to generate future time series data in a non-autoregressive fashion. SSSD (Alcaraz & Strodthoff, 2022) uses the same conditional mechanism as CSDI, but replaces the transformers in CSDI with a Structured State Space Model (S4) to reduce the computational complexity and is more suited to handling long-term dependencies. TMDM (Li et al., 2024) integrates transformers with a conditional diffusion process to improve probabilistic multivariate time series forecasting by effectively capturing covariate dependencies in both the forward and Reverse diffusion processes. TimeDiff (Shen & Kwok, 2023) introduces two innovative conditioning mechanisms specifically designed for time series analysis: future mixup and autoregressive initialization, which construct effective conditional embeddings. To reduce the predictive instability arising from the stochastic nature of the diffusion models, MG-TSD (Fan et al., 2024) leverages the inherent granularity levels within the data as given targets at intermediate diffusion steps to guide the learning process of diffusion models. Most of the above diffusion-based methods emphasize their probabilistic forecasting ability; however, their performance in point-to-point forecasting is suboptimal.

Diffusion Bridge.

Diffusion bridges (Liu et al., 2023a; Zhou et al., 2023; Li et al., 2023a) represent a specific class of diffusion models designed to simulate the trajectory of a stochastic process between predetermined initial and final states. They are regarded as conditioned diffusion models subject to particular boundary constraints. These models, stemming from classical stochastic processes like Brownian motion or Ornstein-Uhlenbeck process, have a predetermined terminal value rather than being free.

DDBMs (Zhou et al., 2023) introduce diffusion bridges, stochastically interpolating between paired distributions to provide smoother transitions and more flexible input handling compared to traditional noise-based diffusion models. Liu et al. (2023a) propose I2SB, which constructs nonlinear diffusion bridges between two domains, making it suitable for tasks like image restoration. BBDM (Li et al., 2023a) models image-to-image translation as a bidirectional diffusion process using a Brownian bridge, directly learning domain translation and achieving competitive benchmark results. GOUB (Yue et al., 2023) combines the generalized OU process with Doob’s h-transform to create precise diffusion mappings that transform low-quality images into high-quality ones. These diffusion bridge models excel in image restoration by using degraded images as informative priors to facilitate clean image reconstruction. Bridge-TTS (Chen et al., 2023) successfully incorporates Schrödinger Bridge diffusion models into text-to-speech (TTS) synthesis task. It leverages the latent representation obtained from text input as a prior and builds a fully tractable Schrödinger bridge between it and the ground-truth mel-spectrogram. For time series data, Park et al. (2024) introduces TimeBridge, a framework that utilizes diffusion bridges to model transitions between selected prior and data distributions. This framework supports both data- and time-dependent priors, achieving state-of-the-art performance in unconditional and conditional time series generation tasks. However, the TimeBridge uses linear spline interpolation (De Boor, 1978) to generate priors for imputation tasks, which is unsuitable for time series forecasting.

3 Methodology

3.1 Preliminaries

Most diffusion-based methods for time series forecasting are designed around conditional Denoising Diffusion Probabilistic Models (DDPMs). The forward process, defined by a fixed Markov chain, progressively transforms the future time series into a Gaussian noise vector according to a predetermined variance schedule :

where denotes the length of the forecast window, and represents the number of distinct features.

With the notation and , the forward process can be rewritten as:

During inference, the model reverses the forward process by considering the following distribution:

where is initially sampled from a standard normal distribution , the subscripts from to denote the diffusion steps. is the historical data, represents the length of the lookback window.

Correspondingly, the conditional reverse process at step is described by:

Following the formulation proposed by Saharia et al. (2022), we can parameterize for either noise or data prediction as follows:

where represents the condition derived from the historical data , and is a conditioning module.

3.2 Revisiting Generalized Diffusion Model for Time Series

Most existing diffusion-based time series forecasting methods emphasize their probabilistic forecasting capabilities; however, their performance in point-to-point forecasting remains suboptimal. To develop a specialized diffusion-based model tailored for point-to-point time series forecasting, a deeper understanding of existing approaches is crucial. Therefore, we revisit and consolidate current non-autoregressive diffusion-based time series forecasting models into a unified framework, demonstrating their fundamental equivalence. The primary differences among these models lie in their choice of diffusion-related coefficients and the design of network architectures.

Recognizing components in existing models, diffusion processes can be viewed in a flexible and adaptable manner. As shown in Eq. (1), the diffusion process incorporates historical data and endows the designed models with distinct properties by adjusting the coefficients , , , and .

Theorem 1.

The non-autoregressive diffusion processes in time series can be formalized as follows:

| (1) |

The reverse diffusion process corresponding to can be formulated as:

| (2) | ||||

| (3) |

where , , and are time-dependent scaling factors. The vector acts as the conditional representation incorporating prior knowledge, with serving as the prior predictor that maps historical time series into a latent space. The initial distribution is given by . The conditioning variable guides the reverse process, where denotes the conditioning module. The function predicts the mean of given inputs , , and , while represents the reverse variance schedule.

Most existing diffusion-based time series forecasting models, including CSDI (Tashiro et al., 2021), SSSD (Alcaraz & Strodthoff, 2022), TimeDiff (Shen & Kwok, 2023), and TMDM (Li et al., 2024), can be interpreted within our proposed framework, as summarized in Table 1. The key differences lie in the choice of forward variance schedule , the learning objectives of their denoising networks, the architectures of their conditional networks , and their respective conditioning mechanisms. Specifically, CSDI, SSSD, and TimeDiff utilize identical diffusion coefficients with , aligning with the standard diffusion process. In contrast, TMDM sets , introducing a distinct variance schedule. Regarding the estimation targets, CSDI, SSSD, and TMDM focus on predicting the noise component , whereas TimeDiff directly estimates the data . The conditioning strategies also differ notably: CSDI and SSSD employ masking with zero-padding to directly condition the denoising network, implemented via Transformer and S4 blocks, respectively. TimeDiff leverages future mixup techniques and incorporates autoregressive models, while TMDM integrates a well-designed Transformer to enhance its conditioning mechanism.

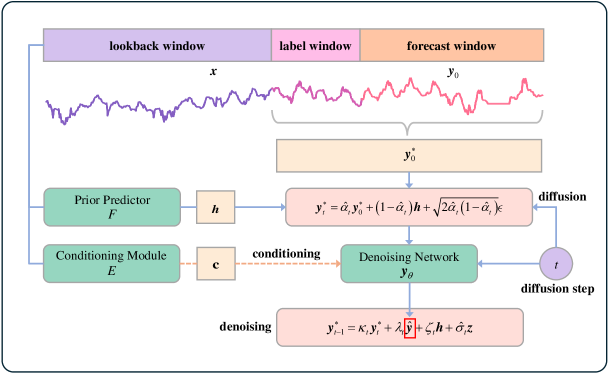

3.3 Series-to-Series Diffusion Bridge Model

As shown in Table 1, existing diffusion-based time series forecasting methods have been extensively studied using various diffusion paradigms and conditional approaches in the formulation of Theorem 1 and achieve promising predictive ability. However, most of these methods focus on the uncertainty estimation ability and typically rely on a data-to-noise diffusion process due to current conditioning mechanisms. As a result, they are often constrained by the intrinsic stochastic nature and are limited in capturing the inherent complexity and dynamic nature of real-world time series data, leading to suboptimal performance in point-to-point forecasting. To address this gap, we propose the Series-to-Series Diffusion Bridge Model (), which uses the Brownian Bridge to pin down the diffusion process at both ends, reducing the instability caused by noisy input and enabling the accurate generation of future time step features from historical time series. By adjusting the posterior variance in Theorem 1, S2DBM behaves as a deterministic generative model without any Gaussian noise, thereby ensuring stability and precise point-to-point forecasting results.

As shown in Figure 2, employs the diffusion bridge as the foundational architecture by adjusting the coefficient schedules. The diffusion bridge pins down the diffusion process at both ends, enabling the accurate generation of future time step features from historical time series data through a data-to-data process.

Corollary 1 (Brownian Bridge between Historical and Predicted Time Series).

Let the coefficient , constrained to be non-negative and decrease monotonically over time , satisfy the boundary conditions and . Additionally, define and The forward process defined in Eq. (1) can be rewritten in closed form:

| (4) |

Then, the reverse process transition defined in Eq. (3) turns into:

| (5) |

where is a data prediction model used to predict the ground truth . Here, , , and are scaling factors defined as

| (6) |

Based on the Equation 6, constructs a Brownian bridge between the initial state and the destination state , eliminating the need to sample from a noisy Gaussian prior during the sampling process, allowing for the direct assignment of . This approach captures more structural information about the target time series.

In the reverse process of , the diffusion process starts directly from . According to Eq. (5), the mean of the reverse transition is determined by both the posterior variance and the coefficient . Given , the coefficients , , and for the reverse process are analytically derived as functions of . To control the contributions of , , and to the predicted mean of , following BBDM (Li et al., 2023a) and I3SB Wang et al. (2024), we parameterize as follows:

where is a hyperparameter that scales the variance, and the selection of its numerical value is discussed in the following remark.

As a consequence of Remark 1, we discuss two instances of the reverse process in , both of which employ the same training procedure but are specifically applied to probabilistic and point-to-point forecasting, respectively.

Example 1 (Point-to-point forecasting).

When we set and , the posterior variance becomes , making the sampling process deterministic, akin to the DDIM approach. The reverse process of can be rewritten as:

Example 2 (Probabilistic forecasting).

When we set and , the posterior variance is defined as . Consequently, the reverse process of is formulated as:

Linear Model based Conditioning Method.

The condition defined in Eq. (3) represents the useful information extracted from historical data , guiding the reverse process toward . Since the design of the conditioning module significantly impacts the predictive quality of the denoising network, it is a crucial aspect of time series diffusion models. In our model, we treat as independent of the denoising network, allowing to preprocess historical data to provide an initial estimate of the future time series. This estimate is then used as the conditional input for the denoising network , thereby simplifying the forecasting task.

The model captures conditional information from historical data not only through the conditioning module , but also via the prior predictor . In time series forecasting, the lookback and forecast windows often differ, and historical sequences cannot directly provide structurally informative priors for prediction targets as damaged images do in image restoration. Therefore, we cannot directly construct a diffusion bridge between historical time series and future time series . Instead, we use the prior predictor to transform historical time series into a deterministic conditional representation , which serves as the endpoint of the diffusion process and provides guidance at the beginning of the reverse process. Both the conditional encoder network and the prior predictor in employ a simple one-layer linear model, chosen for its simplicity, explainability, and efficiency (Toner & Darlow, 2024).

Label-Guided Data Estimation.

The learnable transfer probability is an approximation of the posterior distribution . In our , the denoising network is designed to estimate the data rather than the noise, as we found that estimating the noise introduces more oscillations in the prediction results. Thus, can be expressed as:

| (7) |

In practice, we do not directly estimate the future time series . Instead, we utilize the labeling strategy employed in some transformer-based time series forecasting models, such as the Informer (Zhou et al., 2022). Specifically, we treat the terminal portion of the historical data, , as the label and integrate it with the future time series along the time dimension, denoted as . Consequently, the denoising network is tasked not only with predicting future time steps but also with reconstructing the known sequence within the label length. This methodology enables the model to more effectively capture underlying patterns in the data. The training loss for is defined as follows:

The denoising network of adopts the same architecture as CSDI but removes modules related to its original conditioning mechanism. The training and sampling procedures of are detailed in Algorithm 1 and Algorithm 2, respectively.

4 Experiments

4.1 Experimental Settings

Datasets.

In this experiment, the time series forecasting benchmark datasets employed encompass several real-world datasets: Weather, Influenza-like Illness (ILI), Exchange-Rate (Lai et al., 2018), and four Electricity Transformer Temperature datasets (Zhou et al., 2022) (ETTh1, ETTh2, ETTm1, ETTm2). These datasets are extensively utilized for testing multivariate time-series forecasting models due to their diverse and representative nature, offering insights into the model’s performance across different domains and conditions. Each dataset is normalized using the mean and standard deviation of the training part.

Baselines.

We compared our method with several state-of-the-art and representative baseline models. These include Transformer-based methods: Autoformer (Wu et al., 2021), Informer (Zhou et al., 2022), and iTransformer (Liu et al., 2023b); linear models: DLinear, NLinear (Zeng et al., 2023), and RLinear (Li et al., 2023b); as well as diffusion-based time series prediction methods: CSDI (Tashiro et al., 2021), TMDM (Li et al., 2024), and TimeDiff (Shen & Kwok, 2023).

Evaluation metrics.

To assess point-to-point forecasting performance, we employ mean squared error (MSE) and mean absolute error (MAE) as primary metrics to quantify discrepancies between forecasted and actual time series values. For evaluating the quality of probabilistic forecasts, we use the continuous ranked probability score (CRPS) (Matheson & Winkler, 1976) across individual time series dimensions and for the aggregate of all dimensions.

Implementation details.

We trained our model using the ADAM optimizer, setting the initial learning rate at 0.0001 and parameters and . We configured the number of time steps for the to be T=50 during the training and inference stages. The computational environment comprised a server with an NVIDIA GeForce RTX 3090 24GB GPU.

4.2 Main Results

Point-to-point forecasting.

| Diffusion-based Methods | Transformer-based Methods | Linear Model | |||||||||||||||||

| Methods | Ours | CSDI | TMDM | Autoformer | Informer | iTransformer | NLinear | DLinear | RLinear | ||||||||||

| Metric | MSE | MAE | MSE | MAE | MSE | MAE | MSE | MAE | MSE | MAE | MSE | MAE | MSE | MAE | MSE | MAE | MSE | MAE | |

| ETTh1 | 96 | 0.366 | 0.383 | 0.744 | 0.623 | 0.711 | 0.605 | 0.429 | 0.444 | 0.925 | 0.761 | 0.387 | 0.405 | 0.374 | 0.394 | 0.384 | 0.405 | 0.366 | 0.391 |

| 192 | 0.405 | 0.407 | 0.952 | 0.715 | 0.922 | 0.720 | 0.440 | 0.451 | 0.995 | 0.778 | 0.441 | 0.436 | 0.408 | 0.415 | 0.443 | 0.450 | 0.403 | 0.412 | |

| 336 | 0.442 | 0.430 | 1.192 | 0.837 | 0.990 | 0.737 | 0.511 | 0.488 | 1.036 | 0.782 | 0.491 | 0.462 | 0.429 | 0.428 | 0.447 | 0.448 | 0.420 | 0.423 | |

| 720 | 0.469 | 0.478 | 1.822 | 1.005 | 1.152 | 0.836 | 0.499 | 0.501 | 1.175 | 0.858 | 0.509 | 0.494 | 0.441 | 0.454 | 0.504 | 0.515 | 0.442 | 0.456 | |

| ETTh2 | 96 | 0.274 | 0.331 | 1.017 | 0.729 | 0.496 | 0.510 | 0.418 | 0.445 | 3.017 | 1.369 | 0.301 | 0.350 | 0.283 | 0.343 | 0.290 | 0.353 | 0.262 | 0.331 |

| 192 | 0.354 | 0.388 | 3.417 | 1.356 | 0.578 | 0.535 | 0.435 | 0.439 | 6.348 | 2.105 | 0.380 | 0.399 | 0.356 | 0.385 | 0.388 | 0.422 | 0.320 | 0.374 | |

| 336 | 0.433 | 0.454 | 2.642 | 1.216 | 0.715 | 0.598 | 0.480 | 0.481 | 5.628 | 1.998 | 0.424 | 0.432 | 0.362 | 0.403 | 0.463 | 0.473 | 0.326 | 0.388 | |

| 720 | 0.592 | 0.568 | 3.396 | 1.431 | 0.758 | 0.658 | 0.478 | 0.487 | 4.110 | 1.692 | 0.430 | 0.447 | 0.398 | 0.437 | 0.733 | 0.606 | 0.425 | 0.449 | |

| ETTm1 | 96 | 0.293 | 0.333 | 0.556 | 0.509 | 0.547 | 0.512 | 0.471 | 0.463 | 0.621 | 0.557 | 0.342 | 0.377 | 0.306 | 0.348 | 0.301 | 0.345 | 0.301 | 0.343 |

| 192 | 0.333 | 0.355 | 0.608 | 0.532 | 0.689 | 0.592 | 0.592 | 0.521 | 0.723 | 0.618 | 0.383 | 0.396 | 0.349 | 0.375 | 0.336 | 0.366 | 0.341 | 0.367 | |

| 336 | 0.367 | 0.377 | 0.764 | 0.622 | 0.722 | 0.602 | 0.503 | 0.486 | 1.001 | 0.746 | 0.418 | 0.418 | 0.375 | 0.388 | 0.372 | 0.389 | 0.374 | 0.386 | |

| 720 | 0.442 | 0.422 | 1.071 | 0.792 | 1.072 | 0.785 | 0.751 | 0.582 | 0.980 | 0.747 | 0.487 | 0.457 | 0.433 | 0.422 | 0.427 | 0.423 | 0.430 | 0.418 | |

| ETTm2 | 96 | 0.164 | 0.249 | 0.859 | 0.587 | 0.328 | 0.400 | 0.233 | 0.313 | 0.407 | 0.482 | 0.186 | 0.272 | 0.167 | 0.255 | 0.172 | 0.267 | 0.164 | 0.253 |

| 192 | 0.219 | 0.292 | 0.907 | 0.614 | 0.415 | 0.423 | 0.278 | 0.336 | 0.807 | 0.706 | 0.254 | 0.314 | 0.221 | 0.293 | 0.237 | 0.314 | 0.219 | 0.290 | |

| 336 | 0.274 | 0.328 | 1.584 | 0.862 | 0.871 | 0.611 | 0.379 | 0.394 | 1.453 | 0.926 | 0.316 | 0.351 | 0.274 | 0.327 | 0.295 | 0.359 | 0.273 | 0.326 | |

| 720 | 0.361 | 0.389 | 2.692 | 1.202 | 1.101 | 0.739 | 0.584 | 0.473 | 3.930 | 1.469 | 0.414 | 0.407 | 0.369 | 0.385 | 0.427 | 0.439 | 0.366 | 0.385 | |

| ILI | 24 | 2.241 | 0.983 | 3.942 | 1.293 | 4.005 | 1.183 | 3.405 | 1.290 | 5.104 | 1.544 | 2.405 | 0.987 | 2.022 | 0.925 | 2.280 | 1.061 | 2.036 | 0.969 |

| 36 | 2.811 | 1.060 | 4.982 | 1.497 | 3.456 | 1.300 | 3.522 | 1.291 | 5.158 | 1.571 | 2.328 | 0.984 | 1.974 | 0.932 | 2.235 | 1.059 | 1.928 | 0.940 | |

| 48 | 3.024 | 1.084 | 4.164 | 1.331 | 3.059 | 1.124 | 3.478 | 1.294 | 5.101 | 1.565 | 2.330 | 0.990 | 1.979 | 0.955 | 2.298 | 1.079 | 1.880 | 0.931 | |

| 60 | 3.758 | 1.229 | 5.725 | 1.651 | 2.771 | 1.163 | 2.880 | 1.154 | 5.319 | 1.596 | 2.413 | 1.015 | 1.954 | 0.949 | 2.573 | 1.157 | 2.016 | 0.976 | |

| Weather | 96 | 0.172 | 0.210 | 0.251 | 0.235 | 1.048 | 0.300 | 0.269 | 0.339 | 0.335 | 0.406 | 0.176 | 0.216 | 0.181 | 0.232 | 0.174 | 0.233 | 0.175 | 0.225 |

| 192 | 0.213 | 0.249 | 0.330 | 0.294 | 2.246 | 0.372 | 0.338 | 0.395 | 0.693 | 0.599 | 0.225 | 0.257 | 0.225 | 0.268 | 0.218 | 0.278 | 0.217 | 0.259 | |

| 336 | 0.257 | 0.287 | 0.420 | 0.357 | 3.636 | 0.470 | 0.339 | 0.381 | 0.564 | 0.527 | 0.281 | 0.299 | 0.271 | 0.301 | 0.263 | 0.314 | 0.265 | 0.294 | |

| 720 | 0.343 | 0.353 | 0.538 | 0.423 | 0.795 | 0.541 | 0.429 | 0.433 | 1.105 | 0.771 | 0.358 | 0.350 | 0.339 | 0.349 | 0.332 | 0.374 | 0.329 | 0.339 | |

| Exchange | 96 | 0.096 | 0.229 | 0.902 | 0.647 | 0.202 | 0.334 | 0.143 | 0.274 | 0.943 | 0.772 | 0.086 | 0.206 | 0.089 | 0.208 | 0.085 | 0.209 | 0.089 | 0.209 |

| 192 | 0.196 | 0.334 | 1.084 | 0.744 | 0.371 | 0.466 | 0.266 | 0.377 | 1.244 | 0.882 | 0.181 | 0.304 | 0.181 | 0.300 | 0.162 | 0.296 | 0.191 | 0.309 | |

| 336 | 0.886 | 0.733 | 0.775 | 0.678 | 1.122 | 0.852 | 0.465 | 0.509 | 1.790 | 1.070 | 0.338 | 0.422 | 0.330 | 0.415 | 0.333 | 0.441 | 0.363 | 0.434 | |

| 720 | 2.479 | 1.179 | 1.306 | 0.879 | 1.206 | 0.792 | 1.088 | 0.812 | 2.905 | 1.406 | 0.853 | 0.696 | 0.925 | 0.722 | 0.898 | 0.725 | 0.963 | 0.731 | |

| Count | 10 | 11 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 2 | 4 | 6 | 3 | 1 | 12 | 9 | |

Table 2 provides a detailed summary of the point-to-point time series forecasting results for Example 1 of our model, compared to other models. For diffusion-based methods, we evaluate results obtained from one-shot prediction. The first and second best results are in bold and underlined, respectively. The smaller the value of MSE and MAE, the more accurate the prediction result is. The performance of our surpasses that of other diffusion-based methods in most cases. Compared with the Transformer-based and Linear model-based SOTA methods, our achieves the best performance on most seetings, with the 21 first and 6 second places out of 56 benchmarks in total.

| ETTh1 | ETTm1 | Exchange | |

|---|---|---|---|

| TimeDiff | 0.407 | 0.336 | 0.018 |

| Ours | 0.397 | 0.333 | 0.018 |

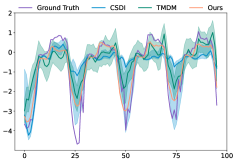

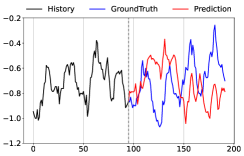

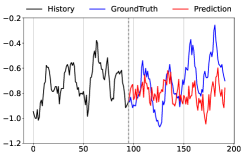

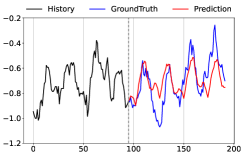

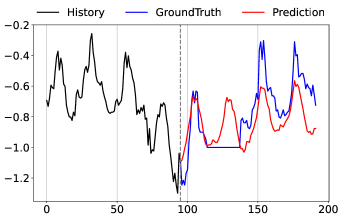

Table 3 presents the Mean Squared Error (MSE) results for the diffusion-based method TimeDiff, which employed unique settings for prediction length that differ from other methods. In response, we retrain our model according to these settings and conduct the following comparisons. Experimental results indicate that our method outperforms TimeDiff in terms of MSE. To complement the quantitative results of diffusion-based methods, Figure 3 provides visualizations of the predictions obtained by CSDI, TMDM, and the proposed on a randomly selected test example from the ETTh1 dataset. As illustrated, while CSDI delivers accurate short-term predictions (from steps 96-110), its long-term forecasts deviate significantly from the ground truth. TMDM captures the overall trend of the future time series, but its point-wise prediction accuracy shows significant oscillations, likely influenced by the noise inherent in the diffusion process, leading to fluctuating results. In contrast, effectively captures the trend and seasonality of time series.

Probabilistic forecasting.

| Dataset | ETTh1 | ETTh2 | ETTm1 | ETTm2 | Weather | |||||

|---|---|---|---|---|---|---|---|---|---|---|

| Metric | CRPS | CRPS | CRPS | CRPS | CRPS | |||||

| CSDI | 0.5120.107 | 2.0770.003 | 0.5790.096 | 2,9850.004 | 0.4280.106 | 2.0930.002 | 0.4900.104 | 2.9720.002 | 0.1900.026 | 1.7470.002 |

| TMDM | 0.3850.098 | 1.6720.003 | 0.3330.094 | 1.5460.003 | 0.3380.087 | 1.6740.002 | 0.2410.070 | 1.2130.001 | 0.2030.027 | 1.6230.002 |

| Ours | 0.3820.093 | 1.7820.003 | 0.328 | 1.554 | 0.3330.087 | 1.5530.001 | 0.2470.069 | 1.2190.001 | 0.2090.028 | 1.8450.002 |

Table 4 summarizes the probabilistic forecasting results for Example 2 of our model, compared with other diffusion-based models. We utilized 100 samples to approximate the probability distribution. The results show that our performs competitively against CSDI and TMDM in terms of CRPS and , illustrating the capabilities of our in probabilistic forecasting.

4.3 Ablation Studies

To validate each component of our proposed model, we performed a comparative analysis of prediction results using five different models on the ETTh1 and ETTm1 datasets. The results are presented in Table 5. The notation cDDPM indicates that it employs the standard diffusion process instead of the Brownian bridge process used in . The notation w/ CSDI refers to an operation that utilizes the conditioning mechanism of CSDI. Similarly, w/ CSDI indicates the adoption of the denoising network architecture from CSDI.

| Dataset | ETTh1 | ETTm1 | ||

|---|---|---|---|---|

| Metric | MSE | MAE | MSE | MAE |

| cDDPM | 0.379 | 0.392 | 0.304 | 0.345 |

| w/ CSDI | 0.755 | 0.545 | 0.416 | 0.406 |

| w/ CSDI | 0.578 | 0.520 | 0.489 | 0.457 |

| label_len=0 | 0.450 | 0.461 | 0.378 | 0.396 |

| Ours | 0.366 | 0.383 | 0.293 | 0.333 |

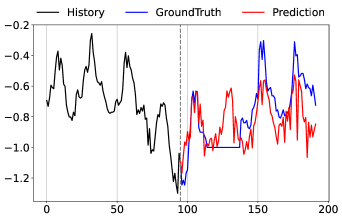

Additionally, the notation signifies that no longer reconstructs known data, focusing solely on predicting the future time series. When comparing our proposed model with cDDPM, we observe notable improvements in both MSE and MAE. Figure 4 visualizes the predictions obtained from both cDDPM and the proposed for a randomly selected test example from the ETTh1 dataset. As illustrated, significantly reduces oscillations in the predictions. Additionally, comparing w/ CSDI and w/ CSDI with demonstrates the advantages of the linear model-based conditioning method and the network architecture of . Finally, comparing with , we reveal an average reduction of 21% in MSE and 16% in MAE, indicating the contribution of the labeling strategy.

5 Conclusion

In this paper, we revisit non-autoregressive time series diffusion models and present a comprehensive framework that integrates most existing diffusion-based methods. Building on this theoretical framework, we propose the Series-to-Series Diffusion Bridge Model (). Our utilizes the Brownian Bridge diffusion process to reduce randomness in diffusion estimations, improving forecast accuracy by effectively leveraging historical information through informative priors and conditions. Extensive experimental results demonstrate that achieves superior performance in point-to-point forecasting and performs competitively against other diffusion-based models in probabilistic forecasting.

Acknowledgments

Z. Ling is supported by the National Natural Science Foundation of China (via NSFC-62406119), the Natural Science Foundation of Hubei Province (2024AFB074), and the Guangdong Provincial Key Laboratory of Mathematical Foundations for Artificial Intelligence (2023B1212010001). R. C. Qiu would like to acknowledge the National Natural Science Foundation of China (via NSFC-12141107), the Interdisciplinary Research Program of HUST (2023JCYJ012), the Key Research and Development Program of Guangxi (GuiKe-AB21196034). F. Zhou was supported by the National Natural Science Foundation of China Project (via NSFC-62106121) and the MOE Project of Key Research Institute of Humanities and Social Sciences (22JJD110001).

References

- Alcaraz & Strodthoff (2022) Juan Miguel Lopez Alcaraz and Nils Strodthoff. Diffusion-based time series imputation and forecasting with structured state space models. arXiv preprint arXiv:2208.09399, 2022.

- Chen et al. (2023) Zehua Chen, Guande He, Kaiwen Zheng, Xu Tan, and Jun Zhu. Schrodinger bridges beat diffusion models on text-to-speech synthesis. arXiv preprint arXiv:2312.03491, 2023.

- De Boor (1978) C De Boor. A practical guide to splines. Springer-Verlag google schola, 2:4135–4195, 1978.

- Fan et al. (2024) Xinyao Fan, Yueying Wu, Chang Xu, Yuhao Huang, Weiqing Liu, and Jiang Bian. Mg-tsd: Multi-granularity time series diffusion models with guided learning process. arXiv preprint arXiv:2403.05751, 2024.

- Ho et al. (2020) Jonathan Ho, Ajay Jain, and Pieter Abbeel. Denoising diffusion probabilistic models. Advances in neural information processing systems, 33:6840–6851, 2020.

- Lai et al. (2018) Guokun Lai, Wei-Cheng Chang, Yiming Yang, and Hanxiao Liu. Modeling long- and short-term temporal patterns with deep neural networks. In The 41st International ACM SIGIR Conference on Research & Development in Information Retrieval, Jun 2018. doi: 10.1145/3209978.3210006. URL http://dx.doi.org/10.1145/3209978.3210006.

- Li et al. (2023a) Bo Li, Kaitao Xue, Bin Liu, and Yu-Kun Lai. Bbdm: Image-to-image translation with brownian bridge diffusion models. In Proceedings of the IEEE/CVF conference on computer vision and pattern Recognition, pp. 1952–1961, 2023a.

- Li et al. (2024) Yuxin Li, Wenchao Chen, Xinyue Hu, Bo Chen, Mingyuan Zhou, et al. Transformer-modulated diffusion models for probabilistic multivariate time series forecasting. In The Twelfth International Conference on Learning Representations, 2024.

- Li et al. (2023b) Zhe Li, Shiyi Qi, Yiduo Li, and Zenglin Xu. Revisiting long-term time series forecasting: An investigation on linear mapping. arXiv preprint arXiv:2305.10721, 2023b.

- Liu et al. (2023a) Guan-Horng Liu, Arash Vahdat, De-An Huang, Evangelos A Theodorou, Weili Nie, and Anima Anandkumar. I2sb: Image-to-image schrödinger bridge. arXiv preprint arXiv:2302.05872, 2023a.

- Liu et al. (2023b) Yong Liu, Tengge Hu, Haoran Zhang, Haixu Wu, Shiyu Wang, Lintao Ma, and Mingsheng Long. itransformer: Inverted transformers are effective for time series forecasting. arXiv preprint arXiv:2310.06625, 2023b.

- Matheson & Winkler (1976) James E Matheson and Robert L Winkler. Scoring rules for continuous probability distributions. Management science, 22(10):1087–1096, 1976.

- Nie et al. (2022) Yuqi Nie, Nam H Nguyen, Phanwadee Sinthong, and Jayant Kalagnanam. A time series is worth 64 words: Long-term forecasting with transformers. arXiv preprint arXiv:2211.14730, 2022.

- Park et al. (2024) Jinseong Park, Seungyun Lee, Woojin Jeong, Yujin Choi, and Jaewook Lee. Leveraging priors via diffusion bridge for time series generation. arXiv preprint arXiv:2408.06672, 2024.

- Rasul et al. (2021) Kashif Rasul, Calvin Seward, Ingmar Schuster, and Roland Vollgraf. Autoregressive denoising diffusion models for multivariate probabilistic time series forecasting. In International Conference on Machine Learning, pp. 8857–8868. PMLR, 2021.

- Reid et al. (2022) Machel Reid, Vincent Josua Hellendoorn, and Graham Neubig. Diffuser: Diffusion via edit-based reconstruction. In The Eleventh International Conference on Learning Representations, 2022.

- Rombach et al. (2022) Robin Rombach, Andreas Blattmann, Dominik Lorenz, Patrick Esser, and Björn Ommer. High-resolution image synthesis with latent diffusion models. In Proceedings of the IEEE/CVF conference on computer vision and pattern recognition, pp. 10684–10695, 2022.

- Saharia et al. (2022) Chitwan Saharia, Jonathan Ho, William Chan, Tim Salimans, David J Fleet, and Mohammad Norouzi. Image super-resolution via inaterative refinement. IEEE Transactions on Pattern Analysis and Machine Intelligence, 45(4):4713–4726, 2022.

- Shen & Kwok (2023) Lifeng Shen and James Kwok. Non-autoregressive conditional diffusion models for time series prediction. arXiv preprint arXiv:2306.05043, 2023.

- Song et al. (2020) Yang Song, Jascha Sohl-Dickstein, Diederik P Kingma, Abhishek Kumar, Stefano Ermon, and Ben Poole. Score-based generative modeling through stochastic differential equations. In International Conference on Learning Representations, 2020.

- Tashiro et al. (2021) Yusuke Tashiro, Jiaming Song, Yang Song, and Stefano Ermon. Csdi: Conditional score-based diffusion models for probabilistic time series imputation. Advances in Neural Information Processing Systems, 34:24804–24816, 2021.

- Toner & Darlow (2024) William Toner and Luke Darlow. An analysis of linear time series forecasting models. arXiv preprint arXiv:2403.14587, 2024.

- Wang et al. (2024) Yuang Wang, Siyeop Yoon, Pengfei Jin, Matthew Tivnan, Zhennong Chen, Rui Hu, Li Zhang, Zhiqiang Chen, Quanzheng Li, and Dufan Wu. Implicit image-to-image schrodinger bridge for ct super-resolution and denoising. arXiv preprint arXiv:2403.06069, 2024.

- Wu et al. (2021) Haixu Wu, Jiehui Xu, Jianmin Wang, and Mingsheng Long. Autoformer: Decomposition transformers with auto-correlation for long-term series forecasting. Advances in neural information processing systems, 34:22419–22430, 2021.

- Ye et al. (2023) Jiasheng Ye, Zaixiang Zheng, Yu Bao, Lihua Qian, and Mingxuan Wang. Dinoiser: Diffused conditional sequence learning by manipulating noises. arXiv preprint arXiv:2302.10025, 2023.

- Yue et al. (2023) Conghan Yue, Zhengwei Peng, Junlong Ma, Shiyan Du, Pengxu Wei, and Dongyu Zhang. Image restoration through generalized ornstein-uhlenbeck bridge. arXiv preprint arXiv:2312.10299, 2023.

- Zeng et al. (2023) Ailing Zeng, Muxi Chen, Lei Zhang, and Qiang Xu. Are transformers effective for time series forecasting? In Proceedings of the AAAI conference on artificial intelligence, pp. 11121–11128, 2023.

- Zhou et al. (2022) Haoyi Zhou, Shanghang Zhang, Jieqi Peng, Shuai Zhang, Jianxin Li, Hui Xiong, and Wancai Zhang. Informer: Beyond efficient transformer for long sequence time-series forecasting. Proceedings of the AAAI Conference on Artificial Intelligence, pp. 11106–11115, Sep 2022. doi: 10.1609/aaai.v35i12.17325. URL http://dx.doi.org/10.1609/aaai.v35i12.17325.

- Zhou et al. (2023) Linqi Zhou, Aaron Lou, Samar Khanna, and Stefano Ermon. Denoising diffusion bridge models. arXiv preprint arXiv:2309.16948, 2023.

Appendix A Appendix

A.1 Proofs of Theorem 1

The non-autoregressive diffusion processes in time series can be formalized as follows:

| (8) |

Here, , , and are time-dependent scaling factors, and serves as the conditional representation acting as prior knowledge.

Similarly, the previous state can be expressed as:

| (9) |

We are interested in the posterior distribution . According to the properties of Gaussian distributions, this posterior is also Gaussian and can be written as:

| (10) |

where , , and are coefficients to be determined, and is the variance.

Since the sum of two independent Gaussian noises is another Gaussian noise, we have:

| (12) |

where .

Comparing this with Eq. (9), we can equate the coefficients:

| (13) |

Solving for , , and , we get:

| (14) | ||||

Since is completely determined by , the posterior distribution becomes:

| (15) |

However, this posterior depends on the unknown data distribution , making it impractical for direct use. Therefore, we introduce a learnable transition probability to approximate for all . The reverse process is defined as:

| (16) | ||||

| (17) |

Here, represents the condition guiding the reverse process, where is a conditioning network taking historical data as input, and includes all trainable parameters of the model. The mean is trained to predict given , , and , with the reverse variance schedule fixed.

When we use as the data prediction model to estimate the ground truth , the mean can be expressed as:

| (18) |

In this formulation, is a neural network that predicts from , conditioned on , , and time .

A.2 More forecasting results visualization

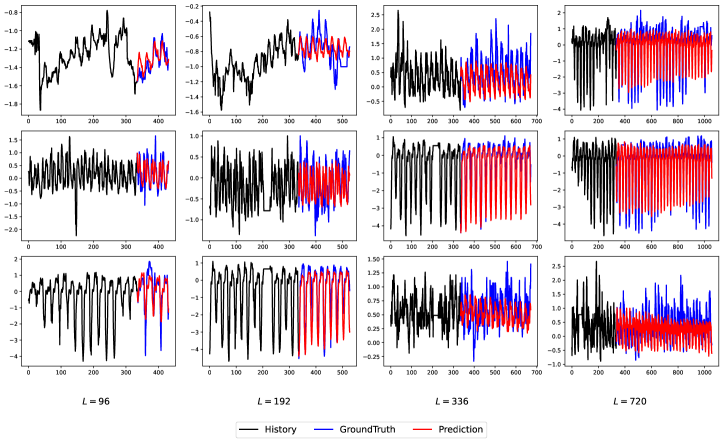

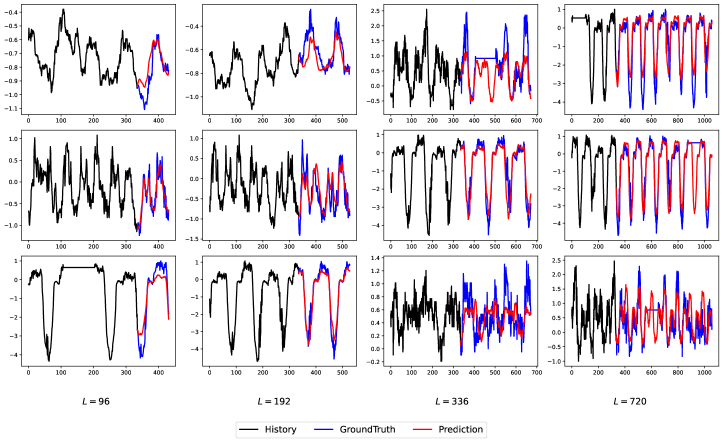

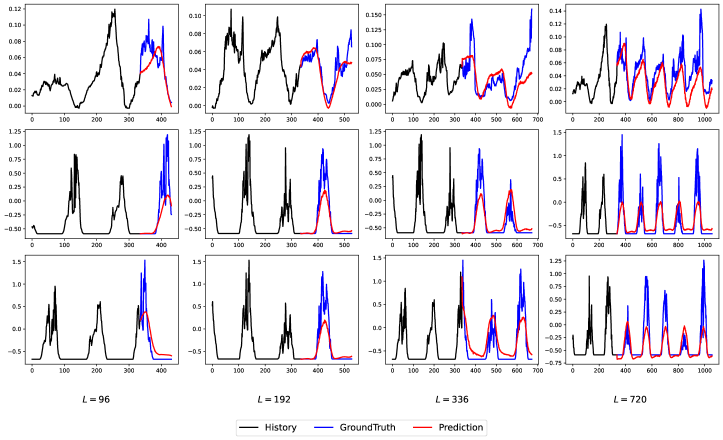

To enhance the comprehensive understanding of our forecasting methods, we present additional visualizations of our predictive results in the following sections. These supplemental images delve deeper into the performance variations of our models under different conditions. By exploring these extra results, readers can obtain a more detailed appreciation of the effectiveness and applicability of our forecasting approaches. Figures 5 and 6 and Figure 7respectively display partial predictive results of our model on the ETTh1, ETTm1, and Weather datasets.

A.3 Experimental Details

A.3.1 dataset information

We adopt seven real-world benchmarks in the experiments to evaluate the accuracy of multivariate time series forecasting, Table 6 summarizes the statistics of these datasets.

| Datasets | Channels | Granularity | Timesteps |

|---|---|---|---|

| Weather | 21 | 10 min | 59696 |

| ILI | 7 | 1 week | 966 |

| Exchange | 8 | 1 day | 7588 |

| ETTh1&ETTh2 | 7 | 1 hour | 17420 |

| ETTm1&ETTm2 | 7 | 5 min | 69680 |

We adopted the experimental settings from recent studies (Liu et al., 2023b; Zeng et al., 2023; Li et al., 2023b). Specifically, following the recommendations of Dlinear (Zeng et al., 2023), we set the input length . We assessed the prediction accuracy for lengths across the Weather, Exchange, ETTh1, ETTh2, ETTm1, and ETTm2 datasets, and for the ILI dataset.

A.3.2 implementation details

As mentioned in Section 3.3, the denoising network of adopts the same architecture as CSDI Tashiro et al. (2021) but removes modules related to its original conditioning mechanism.Both the conditional encoder network and the prior predictor in employ a simple one-layer linear model (Zeng et al., 2023). Table 7 contains the hyperparameters that for training and architecture.

| Hyperparameter | Value |

| Residual layers | 4 |

| Residual channels | 8 |

| Diffusion embedding dim | 8 |

| Schedule | Linear |

| Diffusion steps | 50 |

| Self-attention layers time dim | 1 |

| Self-attention heads time dim | 8 |

| Self-attention layers feature dim | 1 |

| Self-attention layers time dim | 8 |

| EMA decay | 0.995 |

| EMA update interval | 8 |

| Optimizer | Adam |

| Loss function | MAE |

| Max learning rate | |

| Min learning rate | |

| Individual channels | False |