Solving stochastic partial differential equations

using neural networks in the Wiener chaos expansion

Abstract.

In this paper, we solve stochastic partial differential equations (SPDEs) numerically by using (possibly random) neural networks in the truncated Wiener chaos expansion of their corresponding solution. Moreover, we provide some approximation rates for learning the solution of SPDEs with additive and/or multiplicative noise. Finally, we apply our results in numerical examples to approximate the solution of three SPDEs: the stochastic heat equation, the Heath-Jarrow-Morton equation, and the Zakai equation.

Key words and phrases:

Stochastic partial differential equations, stochastic evolution equations, Wiener chaos, Wick polynomials, Cameron-Martin, Malliavin calculus, neural networks, random neural networks, universal approximation, approximation rates, machine learning, stochastic heat equation, Heath-Jarrow-Morton equation, Zakai equation1. Introduction

Given and a probability space , we consider the numerical approximation of stochastic partial differential equations (i.e. semilinear stochastic Cauchy problems) of the form

| (SPDE) |

Hereby, the solution of (SPDE) is a stochastic process with values in a separable Hilbert space , where the initial value is assumed to be deterministic. Moreover, the randomness is induced by a -Brownian motion with values in a (possibly different) separable Hilbert space , where the operator has finite trace. In addition, the operator is the generator of a -semigroup on , and the maps as well as have suitable Lipschitz properties. For more details on the mathematical background, we refer to Section 2.

In general, stochastic partial differential equations (SPDEs) are a powerful mathematical framework to model complex phenomena influenced by both deterministic dynamics and random fluctuations. These equations extend partial differential equations (PDEs) by incorporating stochastic processes, in the same way ordinary stochastic differential equations (SDEs) generalize ordinary differential equations (ODEs). SPDEs find various applications in a wide range of fields, including surface growth models (see [32]), Euclidean quantum field theories (see [64]), fluid dynamics (see [8, 25]), stochastic evolution models of biological or chemical quantities (see [46, 51]), interest-rate models (see [24, 35]), and stochastic filtering (see [3, 54, 88]). For a more detailed introduction to the theoretical background of SPDEs, we refer to the lecture notes and textbooks [17, 18, 31, 34, 37, 43, 82, 83, 60].

However, most SPDEs cannot be solved explicitely and therefore require a numerical method to approximate the solution, which entails all the challenges encountered in the numerical approximation of both PDEs and SDEs. Typical numerical approximations consist of temporal discretizations based on Euler type or higher order methods as well as spatial discretizations based on finite difference, finite element, or Galerkin methods (see the references in the overview articles [30, 44] and the monographs [45, 52]). Recently, machine learning techniques have been used to solve SPDEs, for exampe by using physics-informed neural networks (see [89]), Fourier neural operators for parameteric PDEs (see [56]), deep neural networks (see [4, 9, 90, 81, 87]), and neural SPDEs (see [77]). Some of these results are in turn inspired by the successful neural network applications for learning PDEs (see e.g. [5, 7, 33]).

In this paper, we solve (SPDE) by first truncating the Wiener chaos expansion of its solution and then replacing the propagators (i.e. the coefficients of the Wiener chaos expansion) by neural networks. To this end, we use the universal approximation property of neural networks (first proven in [16, 38] and extended in [55, 14, 71, 15, 67]) to obtain a universal approximation result for SPDEs. Moreover, we also consider random neural networks defined as single-hidden-layer neural networks whose weights and biases inside the activation function are randomly initialized (see [40, 72, 74, 73] and in particular [28, 66]). Hence, only the linear readout needs to be trained, which significantly reduces the computational complexity compared to deterministic (i.e. fully trained) neural networks while maintaining comparable accuracy.

Furthermore, we provide some approximation rates for learning (SPDE) with coefficients of affine form. To this end, we derive the Malliavin regularity of the solution to (SPDE) (see also [62, 70]), apply the Stroock-Taylor formula in [80] to certain Hilbert space-valued random variables, and use the approximation rates for deterministic/random neural networks in [66, 67].

Finally, we provide three numerical experiments to learn the solution of (SPDE) with (possibly random) neural networks in the Wiener chaos expansion, which includes the stochastic heat equation, the Heath-Jarrow-Morton equation, and the Zakai equation. This contributes to other successful (random) neural network applications in scientific computation (see e.g. [20, 21, 84, 86, 27, 36, 42, 65, 68, 85]).

1.1. Outline

In Section 2, we recall the mathematical framework of (SPDE) and introduce the Wiener chaos expansion. In Section 3, we use (possibly random) neural networks in the chaos expansion of (SPDE) to obtain universal approximation results. In Section 4, we provide some approximation rates to learn (SPDE). In Section 5, we present three numerical examples, while all proofs are given in Section 6.

1.2. Notation

As usual, and denote the sets of natural numbers, represents the set of integers, and as well as are the sets of real and complex numbers (with imaginery unit ), respectively. For , we define . In addition, for , we denote by (and ) the (complex) Euclidean space equipped with .

Moreover, a Hilbert space is a (possibly infinite dimensional) vector space together with an inner product such that is complete under the norm . Hereby, represents the Borel -algebra of . In addition, we denote by the vector space of bounded linear operators , e.g. the identity , which is a Banach space under the norm . Moreover, a (possibly unbounded) operator is a linear operator that is only defined on a vector subspace called the domain of . Furthermore, for , we denote by the vector space of continuous paths , which is a Banach space under the norm .

In addition, for , and (open, if ), we denote by the vector space of bounded and -times continuously differentiable functions such that for every the partial derivative is bounded and continuous, which is a Banach space under the norm . If , we write , . Moreover, for , we denote by the vector space of -times continuously differentiable functions such that . In addition, we define as the closure of with respect to , which is a Banach space under . Then, if and only if is -times continuously differentiable and (see [67, Notation (v)]).

Furthermore for , a measure space , and a Banach space , we denote by the Bochner -space of (equivalence classes of) strongly -measurable maps such that , where the latter turns into a Banach space (see [41, Section 1.2.b] for more details). For finite dimensional , we obtain the usual -space of (equivalence classes of) -measurable functions . In addition, represents the -algebra of Lebesgue-measurable subsets of .

Moreover, we define the (multi-dimensional) Fourier transform of as

| (1) |

In addition, we abbreviate the real-valued function spaces by , , etc. Furthermore, we define the complex-valued function spaces as , , etc. by using the identification .

2. Stochastic partial differential equations (SPDEs)

In this section, we provide some mathematical background on existence and uniqueness of solutions to (SPDE) and consider the Wiener chaos expansion. To this end, we fix throughout the paper some , a probability space , and two separable Hilbert spaces and .

2.1. Existence and uniqueness of mild solutions

In order to recall existence and uniqueness results of mild solutions to (SPDE), we follow the textbook [17]. To this end, we denote by the vector subspace of non-negative self-adjoint nuclear111An operator is called non-negative if for all , is called self-adjoint if for all , and is called nuclear if there exist two sequences with such that for every it holds that (see [17, Appendix C]). operators . Moreover, a -valued random variable is called centered Gaussian (with covariance operator ) if for every the Fourier transform of satisfies .

Definition 2.1.

For , a process is called a -Brownian motion if

-

(i)

,

-

(ii)

has continuous sample paths, i.e. is continuous for all , and

-

(iii)

for every the random variable is centered Gaussian with covariance operator .

Standing Assumption.

For some , we fix a -Brownian motion . Moreover, denotes the usual -augmented filtration222The usual -augmented filtration generated by is defined as the smallest filtration such that is complete with respect to , is right-continuous on , and is -adapted (see [75, p. 45]). generated by .

Then, for every , the process is a real-valued Brownian motion, which implies for every and that

Note that the Hilbert space333Every non-negative self-adjoint operator has a unique non-negative self-adjoint square root satisfying (see [10, Problem 39.C.1]). Moreover, the pseudo-inverse of is defined as for (see [17, Appendix B.2]). with inner product , , is a reproducing kernel Hilbert space (RKHS) of in the sense that is continuously embedded into and for every the real-valued random variable is centered Gaussian with covariance .

In addition, since is a non-negative nuclear operator, there exists a complete orthonormal basis of ) and a sequence with such that for every it holds that (see [17, Appendix C]). Then, we define for every the process

| (2) |

which are pairwise independent real-valued Brownian motions that are able to recover the Hilbert space-valued Brownian motion in the following sense.

Lemma 2.2 ([17, Proposition 4.3]).

The processes defined in (2) are pairwise independent real-valued Brownian motions such that for every it holds that

| (3) |

where the sum converges with respect to .

Next, we recall the concept of a mild solution to (SPDE) (see also [17, p. 187]). To this end, we denote by the vector subspace of Hilbert–Schmidt operators444An operator is called Hilbert-Schmidt if (see [17, Appendix C]). , equipped with the inner product for , where is an orthonormal basis of .

We impose the following Lipschitz and linear growth conditions on the coefficients of (SPDE), where we denote by the -predictable -algebra on (see [17, p. 71+72]).

Assumption 2.3.

Let the following hold true:

- (i)

-

(ii)

The map is -measurable.

-

(iii)

The map is -measurable.

-

(iv)

There exist some such that for every , , and it holds that

-

(v)

The initial condition is deterministic.

In addition, we recall that the stochastic integral of an -predictable integrand with values in is defined as the -limit of stochastic integrals of elementary processes (see [17, Section 4.2]).

Definition 2.4.

Under Assumption 2.3, one can then show that (SPDE) admits a mild solution. The proof is based on [17, Theorem 7.2 (i)+(iii)] with a slight modification for , see Section 6.1.

Proposition 2.5 (Existence and uniqueness of mild solutions to (SPDE)).

2.2. Wiener chaos expansion

In this section, we recall the Wiener chaos expansion of the solution to (SPDE). To this end, we fix throughout the paper a set of a.e. continuous functions that form a complete orthonormal basis of the Hilbert space . Moreover, we define for every the random variable

| (6) |

Then, by using Lemma 2.2 and Ito’s isometry, the random variables are Gaussian with and for all , where we define if , and otherwise, for . Conversely, the following result shows how the Brownian motions can be recovered, whose proof is given in Section 6.1.

Lemma 2.6.

Let and . Then, the following holds true:

-

(i)

, where the sum converges with respect to .

-

(ii)

, where the sum converges with respect to .

Example 2.7.

For example, we could choose the basis functions given by and for , which yield the Fourier representation of each real-valued Brownian motion . On the other hand, the Haar wavelets give the Levy-Ciesielski construction of (see [49, Section 2.3]).

Next, we introduce the Wick polynomials associated to the -Brownian motion . To this end, we recall that the Hermite polynomials are for every defined as

| (7) |

Moreover, we consider the set of infinite matrices with finitely many non-zero positive integers and define for .

Definition 2.8.

The Wick polynomials are for every defined by

| (8) |

Remark 2.9.

Since and for all , the product in (8) consists only of finitely many factors that are not equal to one. Hence, the Wick polynomials are well-defined.

Note that the Wick polynomials form a complete orthonormal basis for . In particular, for every , the orthogonality relation holds true (see [70, Proposition 1.1.1]). In the following, we extend this result towards -spaces, whose proof can be found in Section 6.1.

Lemma 2.10.

For every the linear span of is dense in . In particular, for , the Wick polynomials form a complete orthonormal basis of .

For , Cameron and Martin proved in [12, Theorem 1] that every non-linear square-integrable functional of the Brownian motion can be represented as infinite sum of Wick polynomials. In the following, we extend this result to the -case. To this end, we define for every the truncated set of indices , which satisfies (see [61, p. 38]). The proof can be found in Section 6.2.

Theorem 2.11 (Cameron-Martin).

Remark 2.12.

Since and are Gaussian random variables (as for all ), we can decompose the expansion (9) into three different parts, i.e. for every it holds that

In numerical examples, one can then analyze when Gaussian approximation is sufficient (), or when higher order (non-Gaussian) terms are necessary ().

Remark 2.13.

For a function space and certain (SPDE), the functions satisfy a system of coupled PDEs (see e.g. [58, 63, 59, 57, 48]), which can be solved with traditional numerical methods, e.g. Fourier approaches in [61, 39]. In this paper, we also assume that is a function space, but learn the propagators by (possibly random) neural networks.

3. Universal approximation of SPDEs

In this section, we approximate the solution of (SPDE) by using (possibly random) neural networks in the truncated chaos expansion (9). To this end, we assume that is a function space.

Assumption 3.1.

For , (open, if ), and , let be a Hilbert space consisting of functions such that the restriction map

| (11) |

is a continuous dense embedding, i.e. (11) is continuous and its image is dense in .

Lemma 3.2 ([67, Lemma 4.1 (ii)]).

Let be a Hilbert space satisfying Assumption 3.1. Then, is separable.

Let us give some examples of function spaces that are Hilbert spaces satisfying Assumption 3.1. For , open, and a strictly positive -measurable function , we introduce the (weighted) Sobolev space consisting of (equivalence classes of) -times weakly differentiable functions satisfying for all (see [53, p. 5]). Note that for bounded and , we obtain the classical Sobolev space , see [2, Chapter 3].

Example 3.3 ([67, Example 2.6]).

The following Hilbert spaces satisfy Assumption 3.1:

-

(i)

with and Borel measure such that , where .

-

(ii)

with , open subset having the segment property777An open subset has the segment property if for every there exists some with and some such that for every and it holds that (see [2, p. 54])., and strictly positive bounded -measurable function such that , where .

-

(iii)

with and -measurable function such that , where .

Now, we first use deterministic neural networks to approximate the propagators in the truncated chaos expansion (9), followed in the subsequent section by random neural networks. This provides us with a universal approximation result to learn the solution of (SPDE).

3.1. Deterministic neural networks

We now recall deterministic neural networks, which are in this paper defined as single-hidden-layer feed-forward neural networks, where all the parameters are trained.

Definition 3.4.

For and , a (time-extended) deterministic neural network is of the form

| (12) |

for some denoting the number of neurons and some representing the activation function. The parameters of (12) consist of the weights and , the biases , and the linear readouts .

Remark 3.5.

Then, by combining Theorem 2.11 with the universal approximation property of deterministic neural networks (see e.g. [67, Theorem 2.8]), we can approximate the propagators in the truncated chaos expansion (9) by (time-extended) deterministic neural networks, which leads to the following universal approximation result for solutions of (SPDE). The proof is given in Section 6.4.

Theorem 3.6 (Universal approximation).

3.2. Random neural networks

To reduce the computational complexity, we also consider random neural networks which are defined as single-hidden-layer neural networks whose parameters inside the activation function are randomly initialized, whence only the linear readout needs to be trained (see [27, 66]). For the random initialization, we assume that also supports an independent and identically distributed (i.i.d.) sequence satisfying the following.

Assumption 3.7.

Let be an i.i.d. sequence of random variables, being independent of , such that for every and we have

Now, we introduce random neural networks whose parameters inside the activation function are taken from these random variables. In addition, the linear readout is also a random variable, but measurable with respect to these random initializations, i.e. with respect to .

Definition 3.8.

Let satisfy Assumption 3.1. Then, a (time-extended) random neural network is of the form

| (13) |

for some denoting the number of neurons and some representing the activation function. Hereby, the i.i.d. random variables and are the random weights, and the i.i.d. random variables are the random biases. Moreover, the -measurable random variables are the linear readouts.

Remark 3.9.

Remark 3.10.

Then, by combining Theorem 2.11 with the universal approximation property of random neural networks (see [66, Corollary 3.8]), we can approximate the propagators in the truncated chaos expansion (9) by (time-extended) random neural networks, leading to the following universal approximation result for solutions of (SPDE). The proof can be found in Section 6.5.

Theorem 3.11 (Universal approximation).

4. Approximation rates for certain SPDEs at terminal time

In this section, we provide some approximation rates to learn the solution of (SPDE) at terminal time by using deterministic and random neural networks in its chaos expansion. To this end, we assume that the Hilbert space is a weighted Sobolev space as in Example 3.3 (ii).

Moreover, we assume that (SPDE) is linear with affine coefficients and , allowing us to consider SPDEs with additive and multiplicative noise.

Assumption 4.2.

Let the following hold true:

-

(i)

The map is the generator of a -semigroup (see [17, Appendix A.2]).

-

(ii)

The map is of the form for some -measurable map and -measurable map .

-

(iii)

The map is of the form for some -measurable map and -measurable map .

- (iv)

-

(v)

The initial condition is deterministic.

Remark 4.3.

In order to obtain the approximation rates, we first show that is infinitely many times Malliavin differentiable (see Proposition 6.5) and apply the Stroock-Taylor formula (see Proposition 6.3) to upper bound the contributions of the higher order terms in the chaos expansion (10) beyond some given order . This approach also allows us to estimate the approximation error by using only real-valued Brownian motions instead of (cf. (2)) and by using only basis functions of the orthonormal basis of introduced in Section 2.2. For the latter, we additionally need the following assumption.

Assumption 4.4.

For the orthonormal basis of introduced in Section 2.2, we assume that .

To approximate the propagators in the chaos expansion (10), we use the rates for deterministic and random neural networks in [67, Theorem 3.6] and [66, Corollary 4.20], respectively. To this end, we consider pairs consisting of a ridgelet function888 is defined as the vector subspace4 of satisfying for all . and an activation function (see also [79, Definition 5.1]).

Definition 4.5.

A pair is called -admissible if the Fourier transform of (in the sense of distribution) coincides999Since induces (see [26, Equation 9.26]), the Fourier transform is defined as for all . Moreover, coincides on with if for all , where is the vector space of -measurable functions with for all compact subsets with . on with a function such that .

Remark 4.6 ([67, Remark 3.2]).

If is -admissible, then has to be non-polynomial.

Furthermore, we impose the following conditions on the propagators defined in (10).

Assumption 4.7.

4.1. Deterministic neural networks

Now, we present the approximation rate to learn (SPDE) with deterministic neural networks, where was defined in Remark 3.5. The proof is given in Section 6.7.

Theorem 4.8 (Approximation rates).

Let satisfy Assumption 4.1 (with constant ), let Assumption 4.2 hold (with constant ), and let be a mild solution of (SPDE). Moreover, let be -admissible with . In addition, let Assumption 4.4 hold (with constant ) and let Assumption 4.7 hold (with constants and ).

Then, there exist some constants101010The constant depends only on and , while the constant depends only on , (cf. (2)), , , and . such that for every there exist some with neurons satisfying

4.2. Random neural networks

Next, we present the approximation rate for learning (SPDE) using random neural networks (see Remark 3.9), whose proof can be found in Section 6.8.

Assumption 4.9.

Let111111Hereby, has probability density function , where denotes the Gamma function (see [1, Section 6.1]). be an i.i.d. sequence, being independent of .

Theorem 4.10 (Approximation rates).

Since deterministic and random neural networks admit the same rates (see [67, Theorem 3.6] and [66, Corollary 4.20]), we obtain the same approximation rate in Theorem 4.8+4.10 for learning the solution of (SPDE), which decays in the number of approximative Brownian motions , the number of basis functions from , the order of the chaos expansion , and the number of neurons .

5. Numerical Experiments

In this section, we illustrate in three numerical examples how the solution of (SPDE) can be learned by using (possibly random) neural networks in its Wiener chaos expansion. To this end, we assume that is a separable Hilbert space consisting of -times (weakly) differentiable functions , where and (open, if ). Moreover, we fix some and approximate by the process defined as

depending on whether we use deterministic neural networks or random neural networks in the chaos expansion. In this setting, we consider the two following learning frameworks.

In a supervised learning approach, we assume that the solution of (SPDE) is known at some given data points , , and . Then, we aim to minimize the empirical (weighted Sobolev) error

| (15) |

either over or over . Hereby, the constants control the contributions of the derivatives, e.g. for all means equal contribution of each order. This supervised learning approach is summarized in Algorithm 1.

Moreover, in an unsupervised learning approach, we assume that the initial value , the numbers in (2), and the coefficients , , and are given. Then, we learn that approximately satisfies (SPDE), i.e. we minimize the empirical (weighted Sobolev) error

| (16) | ||||

either over or over , where we use an Euler-Maryuama approximation of (SPDE), where the data points , , and are given, and where is an approximation of (see Lemma 2.6 (ii)). This unsupervised learning approach is summarized in Algorithm 2.

In the following121212The numerical experiments have been implemented in Python on an average laptop (Lenovo ThinkPad X13 Gen2a with Processor AMD Ryzen 7 PRO 5850U and Radeon Graphics, 1901 Mhz, 8 Cores, 16 Logical Processors). The code can be found under the following link: https://github.com/psc25/ChaosSPDE, we consider three numerical examples: the stochastic heat equation, the Heath-Jarrow-Morton (HJM) equation, and the Zakai equation. Hereby, we always choose the basis functions of as in Example 2.7.

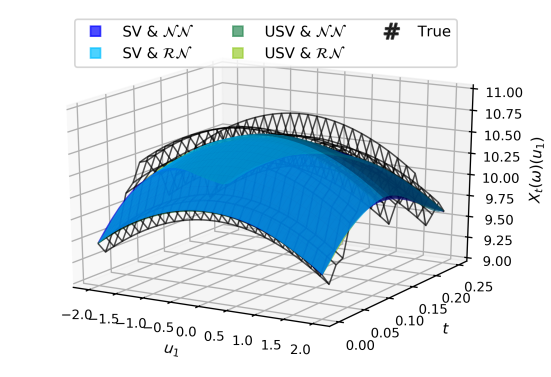

5.1. Stochastic heat equation

In the first numerical experiment, we learn the solution of the stochastic heat equation. To this end, we consider the Hilbert space with inner product , where . Moreover, we assume that (SPDE) takes the form

| (17) |

where is deterministic, and where denotes the Laplacian

| (18) |

Moreover, the map returns the constant function , while is a -Brownian motion, with . Thus, and for all , cf. (2).

Lemma 5.1.

Remark 5.2.

Let us verify Assumption 4.7. By using Lemma 5.1, Lemma 2.6 (ii), and Lemma 2.10, it follows for every that the propagator satisfies

where has zero entries except a one at position . Hence, for any with , we observe that is constant, thus satisfying Assumption 4.7. On the other hand, for , we refer to [66, Lemma 10.1] for conditions on such that has -times differentiable Fourier transform with finite constant defined in (14).

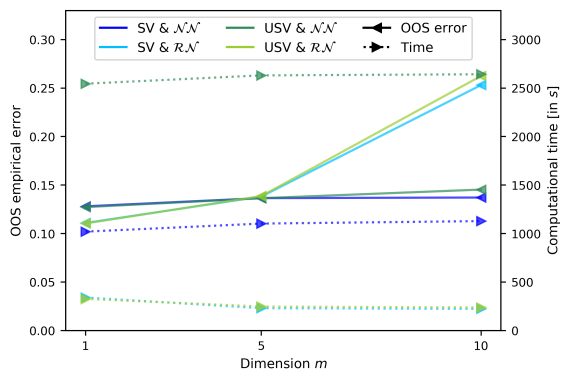

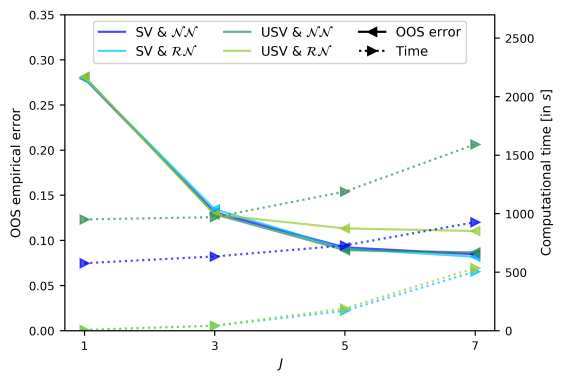

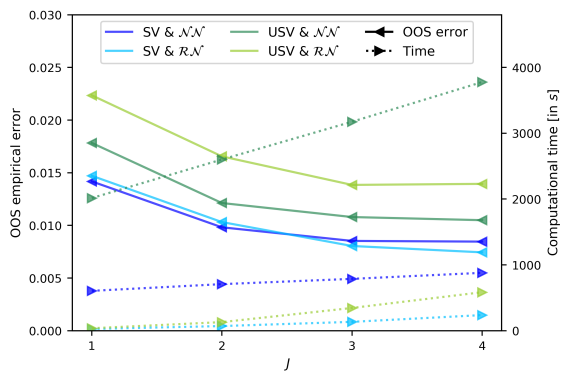

For the numerical example, we choose , , and with . Moreover, let with , let be equidistant with , and let be an i.i.d. sequence of normally distributed random variables with . After splitting the data into 80%/20% for training/testing along , we run the algorithm for both the supervised and unsupervised approach, and both with deterministic and random neural networks (using the activation function , and with and neurons, respectively). For the training of deterministic networks, we apply the Adam algorithm (see [50]) over epochs with learning rate and batchsize , while the random networks are learned with the least squares method.

Figure 1 shows that (possibly random) neural networks in the chaos expansion are able to approximate the solution of the stochastic heat equation (17) via both learning approaches described in Algorithm 1+2.

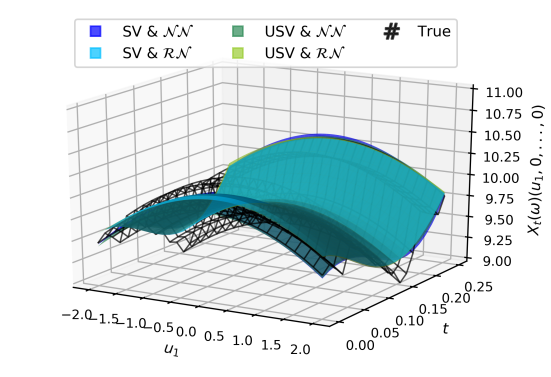

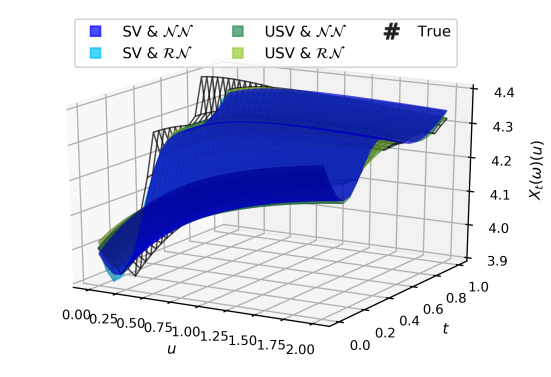

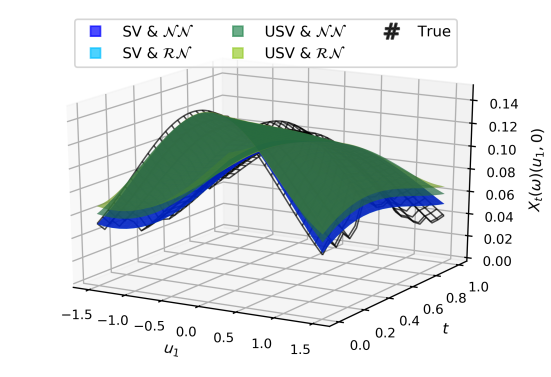

5.2. Heath-Jarrow-Morton (HJM) equation in interest rate theory

In the second example, we learn the solution of the Heath-Jarrow-Morton (HJM) equation. To this end, we assume that is a separable Hilbert space consisting of continuous curves such that for every the evaluation map is continuous. Moreover, we assume that (SPDE) takes the form

| (21) |

where is deterministic, where is the generator of the -semigroup defined by , and where is a -Brownian motion with values on a (possibly different) separable Hilbert space , with and RKHS . Moreover, the diffusion coefficient is assumed to be -measurable, and the drift coefficient is given by the famous HJM no-arbitrage condition (see [13, Eq. 6.2]), i.e.

| (22) |

for , where is an orthonormal basis of , and is any -measurable map.

Remark 5.3.

The solution of the HJM equation (21) describes the instantaneous forward rate. Indeed, let be the spot interest rate. Then, for any and , the price of a zero coupon bond with maturity date and nominal value is defined as . Hence, if for -a.e. , the process defined as

expresses the instantaneous forward rate in the sense that for every and it holds that . For more details, we refer to [13, Chapter 6].

For the numerical experiment, we let and consider the Hilbert space consisting of absolutely continuous curves satisfying , equipped with the inner product , for (see also [13, Section 6.3.3] and [22]). Moreover, we set and consider a real-valued -Brownian motion , with , and therefore and for all , cf. (2). In addition, we assume that the spot interest rate follows a Vasiček model

where is deterministic, and where as well as are given parameters. Then, by [13, Equation 2.33] (see also [23, Section 5.4.1]), this corresponds to the HJM equation (21) with coefficients and by (22), whose solution is given by

| (23) |

Now, we choose , , , , , and , let with , let be an equidistant time grid with , and let and be an i.i.d. sequence of random variables with , where is a normalizing constant. After splitting the data into 80%/20% for training/testing along , we run the algorithm for both the supervised and unsupervised approach, and both with deterministic and random neural networks (using the activation function , and with and neurons, respectively), where we choose for , , , and . This means that the empirical error (15) becomes now

and analogously for (16), which is a truncated empirical version of the norm of . For the training of deterministic networks, we apply the Adam algorithm (see [50]) over epochs with learning rate and batchsize , while the random networks are learned with the least squares method.

Figure 2 shows that deterministic and random neural networks in the Wiener chaos expansion are able to learn the solution of the HJM equation (21) via both learning approaches described in Algorithm 1+2. Moreover, Figure 2 (2) shows that a Gaussian approximation () is sufficient (see Remark 2.12).

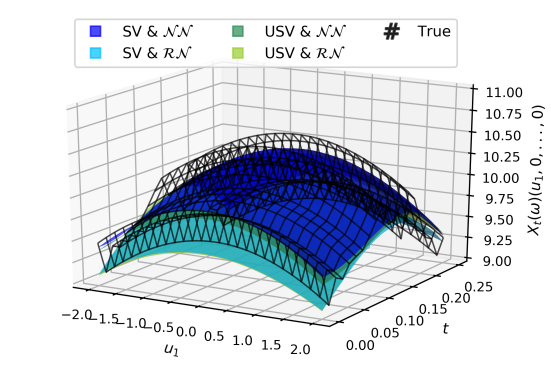

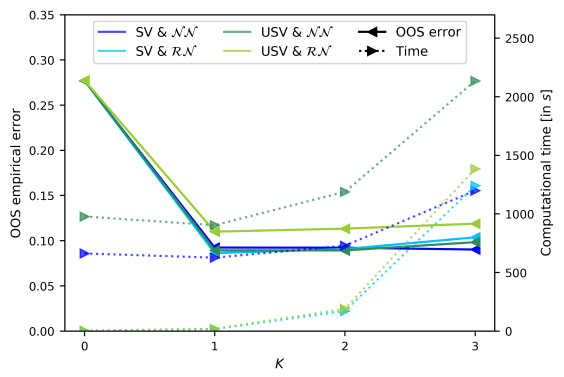

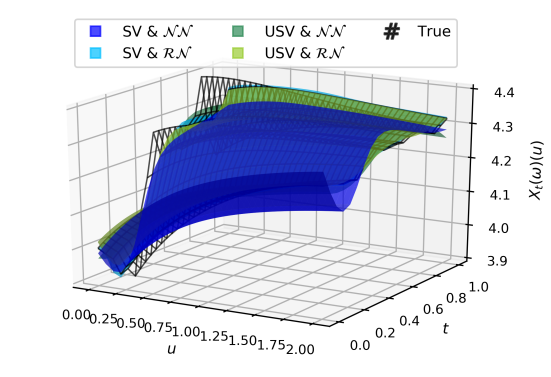

5.3. Zakai equation in filtering

In the third example, we consider the Zakai equation in filtering theory (see [47, 54, 88, 76]), which describes the evolution of an unnormalized density function of the conditional distribution of an unobservable process. To this end, we consider for some fixed the Hilbert space , where . Moreover, for , we assume that is an unobserved signal process satisfying

| (24) |

where is -measurable with probability density function , where and are the SDE-coefficients, and where is an -dimensional Brownian motion. Then, is a Markov process with generator

| (25) |

where and . Moreover, we assume that is the observed process, which satisfies

| (26) |

where is a continuous function, and where is an -dimensional Brownian motion, independent from . Then, by assuming that , we can apply [76, Theorem 6.3] to conclude that the solution of the SPDE

| (27) |

describes at each time an unnormalized density function of the conditional distribution of given the observations of , which means that

where is the adjoint131313In fact, is defined as the adjoint of in (25), i.e. as the operator such that for every it holds that . Hence, by applying integration by parts, it follows that for all , where and . of given in (25), and where is the -dimensional Brownian motion from (26). Note that (27) is of the form (SPDE) with coefficients and given by

where . Since depends on the randomness of both Brownian motions and (the latter via in and ), we have to include both of them into the computation of the Wick polynomials . This means that we consider the ()-valued -Brownian motion , with , and thus for all , and for all , cf. (2).

For the numerical example, we choose and , the drift function , and diffusion function , with denoting the matrix having all entries equal to one, and assume that , i.e. . Moreover, we consider and . In addition, let with , let be an equidistant grid with , and let be an i.i.d. sequence of normally distributed random variables with . After splitting the data into 80%/20% for training/testing along , we run the algorithm for both the supervised and unsupervised approach, and both with deterministic and random neural networks (using the activation function , and with and neurons, respectively). For the training of deterministic networks, we apply the Adam algorithm (see [50]) over epochs with learning rate and batchsize , while the random networks are learned with the least squares method.

Figure 3 shows that the truncated Wiener chaos expansion with deterministic and random neural networks can learn the solution of the Zakai equation (27) using both Algorithm 1+2. Hereby, the true solution of (27) is approximated with the Monte-Carlo method in [6].

5.4. Conclusion

Figure 1-3 empirically demonstrate that deterministic and random neural networks in the truncated Wiener chaos are able to learn the solution of (SPDE). In the supervised learning approach (see Algorithm 1), the solution of (SPDE) is provided as a target, whereas the unsupervised learning approach (see Algorithm 2) recovers the solution by minimizing the (squared) difference of the left- and right-hand side of (SPDE). The latter is naturally more challenging and results in a higher out-of-sample error. Moreover, random neural networks have a slightly lower approximation accuracy than deterministic neural networks but are computationally more efficient (see also [66, Section 6] for a comparison).

6. Proofs

6.1. Proof of auxiliary results in Section 2

Proof of Proposition 2.5.

For any , we first apply [17, Theorem 7.2 (i)] to conclude that exists, is unique up to modifications among the -predictable processes satisfying , and admits a continuous modification.

Now, for , we use [17, Theorem 7.2 (iii)] (with constant depending only on , , , and ) and that the initial condition is deterministic (see Assumption 2.3 (v)) implying that to obtain that

On the other hand, for , we use Jensen’s inequality, [17, Theorem 7.2 (iii)] (with exponent and constant depending only on , , and ), that the initial condition is deterministic (see Assumption 2.3 (v)) implying that , and the inequality for any to conclude that

| (28) | ||||

Hence, defining the constant by if , and by if , we obtain the result. ∎

Lemma 6.1.

Let be separable. Then, is separable.

Proof.

By using that is separable, there exists a sequence that is dense in . From this, we define the countable set

where . Then, is a -submodule (i.e. for every and it holds that ). Moreover, is a subalgebra (i.e. for every it holds that and ) which is point separating (i.e. for every distinct there exists some with ) and nowhere vanishing (i.e. for every there exists some with ). In addition, for every , the set is dense in . Then, we can apply the vector-valued Stone-Weierstrass theorem in [11, p. 103] to conclude that is dense in . Since is countable, is separable. ∎

Proof of Lemma 2.6.

For (i), we fix some and . Then, by using the definition of in (6), that , Ito’s isometry, and that is a complete orthonormal basis of , it follows that

For (ii), we use Minkowski’s inequality, that is an orthonormal basis of , that , that are identically distributed for any , Lemma 2.2, and (i) to conclude that

which completes the proof. ∎

Proof of Lemma 2.10.

Fix some . Moreover, we define the map

returning the stochastic integral of a deterministic function at terminal time . Then, by using Ito’s isometry in [17, Proposition 4.28] (with141414The trace of a nuclear operator is defined as . for any , see [17, Appendix C]), it follows for every that

and that

which shows that is an isonormal process in the sense of [70, Definition 1.1.1]. Hence, by using [70, Exercise 1.1.7] (see also [69, Theorem 2.2.4 (i)]), we conclude that

| (29) |

is dense in , where consists of polynomials of the form for some and , where .

Now, we show that is also dense in . Let us define for every the deterministic function satisfying , where is an orthonormal basis of . Since for any and for any , it therefore suffices to show that

| (30) |

is dense in . To this end, we fix some and . Then, by using that (29) is dense in there exists some , , and such that

| (31) |

Moreover, for every fixed , we use that the system forms an orthonormal basis of to conclude that there exist some and such that (with ) satisfies

| (32) |

where , and where is the constant in [17, Theorem 4.36] (with exponent ). Hence, for every , we use [17, Theorem 4.36] (with exponent and constant , which is increasing in ), the inequality (32), that , that , and that to conclude that

| (33) | ||||

Thus, by using Minkwoski’s inequality, the inequality (31), Taylor’s theorem, i.e. that for any , together with Minkwoski’s inequality, the generalized Hölder’s inequality (with exponents ), the inequality (33), that , and that , it follows for belonging to (30) (as for any ) that

Since and were chosen arbitrarily, this shows that (30) is dense in and therefore that is also dense in . Finally, for , the Wick polynomials are by [70, Proposition 1.1.1] a complete orthonormal basis of . ∎

6.2. Proof of Theorem 2.11

Proof of Theorem 2.11.

For (9), we fix some . Then, by using the continuous modification, Proposition 2.5, and that the Brownian motion is the only random force driving (SPDE), we observe that . Moreover, by combining [41, Lemma 1.2.19 (i)] with Lemma 2.10, the linear span of is dense in . Hence, there exist some and such that

which shows the conclusion in (9).

For (10), we fix an orthonormal basis of . Then, we claim that is an orthonormal basis of the Bochner space , where is the inner product. Indeed, by using that are by Lemma 2.10 orthonormal in and that are by assumption orthonormal in , it follows for every and that

Moreover, by combining [41, Lemma 1.2.19 (i)] with Lemma 2.10, we conclude that the linear span of is dense in . This shows that is an orthonormal basis of . Hence, the chaos expansion (10) follows as an orthogonal expansion along the basis elements of . ∎

6.3. Proof of auxiliary results in Section 3

Lemma 6.2.

Let satisfy Assumption 3.1. Then, the time-extended restriction map

| (34) |

is a continuous dense embedding. Moreover, for every and , it holds that .

Proof.

In order to show that (34) is a continuous embedding, we observe that for every it holds that

Next, for showing that (34) is a dense embedding, we fix some and . Moreover, we define the collection of open subsets for , which forms an open cover of . Then, by using that is compact, there exists some and such that is a finite subcover of . In addition, for every , we use that the restriction map (11) is a dense embedding (see Assumption 3.1) to conclude that there exists some such that . Thus, by using a partition of unity subordinate to (i.e. functions such that for all and , that for all , and that for all ), we conclude for the function that

Since and were chosen arbitrarily, this shows that (34) is a dense embedding.

Finally, we use the previous step to conclude that satisfies the conditions151515To be precise, if , we need to consider instead of in order to have an open set for [67, Definition 2.3]. However, by continuous extension, we observe that (34) is a continuous dense embedding if and only if is a continuous dense embedding. of [67, Definition 2.3]. Hence, by applying [67, Lemma 2.5], it follows for every and that . ∎

6.4. Proof of Theorem 3.6

Proof of Theorem 3.6.

Fix some . Then, by using Theorem 2.11, there exists some and such that

| (35) |

Moreover, by using Lemma 6.2, we observe that satisfies the conditions of [67, Definition 2.3]. Hence, we can apply the universal approximation result for deterministic neural networks in [67, Theorem 2.8] to conclude that for every there exists some such that

| (36) |

Thus, by combining (35) and (36) with Minkowski’s inequality, it follows that

which completes the proof. ∎

6.5. Proof of Theorem 3.11

Proof of Theorem 3.11.

Fix some . Then, by using Theorem 2.11, there exists some and such that

| (37) |

Moreover, by using Lemma 6.2, we observe that satisfies the conditions of [67, Definition 2.3]. Hence, we can apply the universal approximation result for random neural networks in [67, Theorem 2.8] to conclude that for every there exists some such that

| (38) |

Thus, by using Minkowski’s inequality, that is independent of for any (as are by Assumption 3.7 independent of ), and the inequalities (37)+(38), it follows that

which completes the proof. ∎

6.6. Proof of auxiliary results in Section 4

Proof of Remark 4.3.

Let Assumption 4.2 hold. Then, Assumption 2.3 (i)+(v) are satisfied. Moreover, by using Assumption 4.2 (ii)+(iii), the map is -measurable and the map is -measurable, which shows Assumption 2.3 (ii)+(iii). In addition, by using that (as ) together with and Assumption 4.2 (iv), we obtain for every , , and that

and that

which proves that Assumption 2.3 (iv) also holds. Hence, we can apply Proposition 2.5 to conclude that (SPDE) admits a unique mild solution . ∎

6.6.1. Malliavin calculus for Hilbert space-valued random variables

In order to prove the approximation rates in Theorem 4.8+4.10, we first apply the Stroock-Taylor formula in [80] to Hilbert space-valued random variables that are infinitely many times Malliavin differentiable. To this end, we recall some notions of Malliavin calculus for Hilbert space-valued random variables (see e.g. [62, 78, 70, 13]) and introduce the abbreviations and for any and any Hilbert space . Moreover, we denote the stochastic integral of every deterministic function by . In addition, we define as the linear span of polynomial -valued random variables of the form

| (39) |

for some , , , and a polynomial . Then, for any , we define the -th Malliavin derivative of in (39) as

where the element denotes the function

with , and where can be understood as the -times iterated space of Hilbert-Schmidt operators equipped with . Note that , that for any , and that is closeable. Moreover, we define as the closure of with respect to the norm induced by

Then, the operator is linear and continuous (see [70, Proposition 1.5.7]). In addition, we define the vector space .

Furthermore, for any , we define the -th divergence operator as the adjoint of the -th Malliavin derivative . More precisely, the domain consists of all for which there exists a constant such that for every it holds that . In this case, is defined as the unique element in such that for every we have

| (40) |

Note that and that the restriction is continuous (see [70, Proposition 1.5.7]).

Then, we apply the Stroock-Taylor formula in [80, Theorem 6] to random variables in . To this end, we define the subset and denote by the projection onto the Wick polynomials of order .

Proposition 6.3.

Proof.

We follow the proof of [80, Theorem 6]. To this end, we fix some and , and assume that is an orthonormal basis of . Then, by using the definition of the Wick polynomials (see Definition 2.8), that for any and with (see [80, Lemma 1]), that there are possibilities to form with indices , that together with (40), the linearity of the expectation and inner product, that is continuous (see [70, Proposition 1.5.7]), and that is an orthonormal basis of , it follows that

| (42) | ||||

where the sums in the first six lines converge in , and where the sum in the second last line converges in . Since was chosen arbitrarily and the Wick polynomials are orthonormal among different orders (see Lemma 2.10), we obtain the expansion (41). ∎

Moreover, we compute an upper bound for the -norm of the -th divergence operator of some given (see also [19, Proposition 2.3] for the case ).

Lemma 6.4.

For , let . Then, and it holds that

| (43) |

Proof.

Fix some and . Then, by iteratively using [70, Proposition 1.2.2] and the notations for any as well as for any and , it follows for every that

Hence, by taking the expectation and using that , Minkowski’s inequality, that forms an orthonormal basis of the Hilbert space , and that there are possibilities to form with , we have for every that

Next, for a fixed orthonormal basis of , let denote the set of convex combinations built from . Then, for every , it holds that

Finally, by using the dual norm of , that is dense in (see Lemma 2.10 and [41, Lemma 1.2.19 (i)]), that , the identity (40), and linearity, it follows that

which completes the proof. ∎

6.6.2. Malliavin regularity of solution to (SPDE)

For the proof of the approximation rates in Theorem 4.8+4.10, we first show that the solution of (SPDE) belongs at each time to . Then, by upper bounding its Malliavin derivatives, we can estimate the higher order terms in the chaos expansion (10).

To this end, we generalize the results in [78, Theorem 7.1], [13, Section 5.5], and [52, Theorem 5.7] from to . We use the notations for , and for , for , and for and given in (2).

Proposition 6.5.

Let Assumption 4.2 hold and let be a mild solution of (SPDE). Then, by using the constants (see Proposition 2.5), , and (cf. (2)), the following holds true:

-

(i)

For every we have . Moreover, for every , a.e. , every , and every it holds that

(44) -

(ii)

For every , a.e. , every , and every , it holds that

(45) -

(iii)

For every , a.e. , every , and every , it holds that

(46) -

(iv)

For every , a.e. , every , and every , it holds that

(47)

Proof.

For (i), we show by induction on that with (44) holding for . For , the results follows from [13, Lemma 5.3] and [13, p. 152]. Now, for the induction step, we fix some , assume that with (44) holding for , and aim to prove that with (44) holding for . To this end, we fix some and (such that (44) holds for ), and define . Then, by using (44) for , the -valued process satisfies for every that

| (48) | ||||

Hence, by using the initial value and that the coefficients as well as satisfy the Lipschitz and linear growth condition (see Assumption 4.2 (iv)), we can apply [13, Lemma 5.3] to conclude that for all . On the other hand, for every , we have . Since and were chosen arbitrarily, this shows that and thus . Moreover, by using (48), the chain rule for the Malliavin derivative (see [13, Proposition 5.2]), the Malliavin derivative of a time integral (see [52, Proposition 4.8]), the Malliavin derivative of a stochastic integral with -predictable integrand (see [13, Proposition 5.4]), and that for any and with , it follows for a.e. , every , and every that

Otherwise if , we observe that . This shows that (44) holds for , terminates the induction step, and therefore proves (i).

For (ii), we use induction on to show (45). For the induction initialization , we fix some . Moreover, by using that , that (as ), and Assumption 4.2 (iv), we obtain for every and that

| (49) | ||||

In addition, by using again that and Assumption 4.2 (iv), we have for every and that

| (50) |

and that

| (51) |

Then, by inserting the inequality for any into (44), using the inequality (49) together with Jensen’s inequality as well as Ito’s isometry in [17, Corollary 4.29] (using the integrand and that ), and the inequality for any together with the inequalities (50)+(51), we conclude for a.e. and every that

Hence, by using the Gronwall inequality and that by Proposition 2.5, it follows for a.e. and every that

which shows (45) for , a.e. , and any . Since for any , we obtain (45) for , completing the proof of the induction initialization. Now, for the induction step, we fix some , assume that (45) holds for , and aim to show that (45) holds for . To this end, we fix some . Moreover, by using that , Assumption 4.2 (iv), and that (as ), we conclude for every and that

| (52) | ||||

Then, by inserting the inequality for any into (44), by using the inequality (49) together with Jensen’s inequality as well as Ito’s isometry in [17, Corollary 4.29] (using the integrand and that ), and the inequality for any together with the inequalities (50)+(51), it follows for a.e. with and every that

Hence, by using the Gronwall inequality together with the induction hypothesis (i.e. that (45) holds for ), it follows for a.e. with and every that

which shows (45) for , a.e. , and any . Otherwise, if , we choose a permutation such that and use that is by (44) symmetric (i.e. that for all permutations , where and ) to conclude for a.e. and every that

which shows (45) for , a.e. , and any . Since for any , we obtain (45) for , completing the induction step and therefore proving (ii).

For (iii), we fix some . Then, by using that is an orthonormal basis of together with Minkowski’s inequality, the inequalities (51)+(45), and the Cauchy-Schwarz inequality together with , it follows for a.e. fixed , every fixed with satisfying , and every fixed that

Hence, we can apply [17, Proposition 4.28] to conclude that

Thus, by taking the expectation in (44), we obtain the identity (46).

For (iv), we use induction on to show (47). For the induction initialization , we fix some . Then, by applying the triangle inequality in (46) and using the inequalities (49)+(50), we conclude for a.e. and every that

Hence, by using the Gronwall inequality and that by Proposition 2.5, it follows for a.e. and every that

which shows (47) for , a.e. , and any . Since for any , we obtain (47) for , completing the proof of the induction initialization. Now, for the induction step, we fix some , assume that (47) holds for , and aim to show that (47) holds for . To this end, we fix some . Then, by applying the triangle inequality in (46) and using the inequalities (49)+(50), it follows for a.e. with and every that

Hence, by using the Gronwall inequality together with the induction hypothesis (i.e. that (47) holds for ), it follows for a.e. with and every that

which shows (47) for , a.e. , and any . Otherwise, if , we choose a permutation satisfying and use that is by (46) symmetric (i.e. that for all permutations , where and ) to conclude for a.e. and every that

which shows (47) for , a.e. , and any . Since for any , we obtain (45) for , completing the induction step and proving (iv). ∎

6.7. Proof of Theorem 4.8

Proof of Theorem 4.8.

Let be a mild solution of (SPDE) satisfying Assumption 4.2+4.7 and fix some . Then, we can split the approximation error into four parts: (i) The truncation error of by using only Wick polynomials up to order ; (ii) the projection error by using only the first basis elements of ; (iii) the projection error by using only the first basis elements of ; (iv) the approximation error of by a deterministic neural network with neurons, for .

For 6.7, we use that the Wick polynomials are orthonormal in (see Lemma 2.10), the projection onto the Wick polynomials of order , Proposition 6.3, and Lemma 6.4 to obtain that

Hence, by using Proposition 6.5 (iv), that , the identity for any , and the constant (depending only on , , and ), it follows that

| (53) | ||||

This bounds the truncation error of by using the Wick polynomials only up to order .

For 6.7, we fix some and an orthonormal basis of . Then, by using that is an orthonormal basis of together with the same steps as in line 1-7 of (42), Lemma 6.4, that for any and Hilbert space with complete orthonormal basis , that is an orthonormal basis of , we obtain that

| (54) | ||||

Hence, using Proposition 6.5 (iv), that , the inequality for any , as well as the constant (depending only on , (cf. (2)), , and ), we have

| (55) | ||||

This bounds the projection error by using only the basis elements of .

For 6.7, we fix again some and an orthonormal basis of . Then, by following the arguments of (54) (including line 1-7 of (42) and Lemma 6.4), we obtain that

Hence, Proposition 6.5 (iv), that by Fubini’s theorem (with ), that , and the same steps as in (55) together with the constant (depending only on , (cf. (2)), , , and ) show that

| (56) | ||||

This bounds the projection error by using only the basis elements of .

For 6.7, we fix some . Then, by using Assumption 4.7, i.e. that is either constant (and thus can be approximated by a deterministic neural network having neurons without any error, where we set ) or that has -times differentiable Fourier transform such that the constant defined in (14) is finite, we can apply the approximation rate for deterministic neural networks in [67, Theorem 3.6] together with [67, Proposition 3.8] to obtain a constant (depending only on and ) and some deterministic neural network with neurons such that

Hence, by using that the Wick polynomials are orthonormal in , we have

| (57) | ||||

This bounds the approximation error of by some deterministic neural network with neurons.

6.8. Proof of Theorem 4.10

Proof of Theorem 4.10.

Let be a mild solution of (SPDE) with coefficients satisfying Assumption 4.2 and fix some . Then, by following the proof of Theorem 4.8, the approximation error can be split up into the four parts 6.7-6.7. While 6.7-6.7 consist of the same steps as in the proof of Theorem 4.8, part 6.7 is now the approximation error of by a random neural network with neurons, for .

For 6.7, we fix some . Then, by using Assumption 4.7, i.e. that the function is either constant (and thus can be approximated by a random neural network having neurons without any error, where we set ) or that has -times differentiable Fourier transform such that the constant defined in (14) is finite, we can apply the approximation rate for random neural networks in [66, Corollary 4.20] together with [66, Proposition 4.22] to obtain the same constant as in Theorem 4.8 and a random neural network with neurons such that

Since the Wick polynomials are orthonormal in and is independent of (as are by Assumption 4.9 independent of ), it follows that

| (59) | ||||

This bounds the approximation error of by some random neural network with neurons.

6.9. Proof of results in Section 5

Proof of Lemma 5.1.

Acknowledgments:

Financial support by the Nanyang Assistant Professorship Grant (NAP Grant) Machine Learning based Algorithms in Finance and Insurance is gratefully acknowledged.

References

- [1] Milton Abramowitz and Irene Ann Stegun. Handbook of mathematical functions with formulas, graphs, and mathematical tables. Applied mathematics series / National Bureau of Standards 55, Print. 9. Dover, New York, 9th edition, 1970.

- [2] Robert A. Adams. Sobolev Spaces. Pure and applied mathematics. Academic Press, 1975.

- [3] Alan Bain and Dan Crisan. Fundamentals of Stochastic Filtering. Stochastic Modelling and Applied Probability, 60. Springer New York, New York, NY, 1st edition, 2009.

- [4] Christian Beck, Sebastian Becker, Patrick Cheridito, Arnulf Jentzen, and Ariel Neufeld. Deep learning based numerical approximation algorithms for stochastic partial differential equations and high-dimensional nonlinear filtering problems. arXiv e-prints 2012.01194, 2020.

- [5] Christian Beck, Sebastian Becker, Patrick Cheridito, Arnulf Jentzen, and Ariel Neufeld. Deep splitting method for parabolic PDEs. SIAM Journal on Scientific Computing, 43(5):A3135–A3154, 2021.

- [6] Christian Beck, Sebastian Becker, Patrick Cheridito, Arnulf Jentzen, and Ariel Neufeld. An efficient Monte Carlo scheme for Zakai equations. Communications in Nonlinear Science and Numerical Simulation, 126:107438, 2023.

- [7] Christian Beck, Sebastian Becker, Philipp Grohs, Nor Jaafari, and Arnulf Jentzen. Solving the Kolmogorov PDE by means of deep learning. Journal of Scientific Computing, 88(73), 2021.

- [8] Bjorn Birnir. The Kolmogorov-Obukhov theory of turbulence: A mathematical theory of turbulence. SpringerBriefs in Mathematics. Springer, New York, 1st edition, 2013.

- [9] Kasper Bågmark, Adam Andersson, and Stig Larsson. An energy-based deep splitting method for the nonlinear filtering problem. Partial Differential Equations and Applications, 4(2), 2023.

- [10] Haïm Brézis. Functional Analysis, Sobolev Spaces and Partial Differential Equations. Universitext. Springer, New York, 2011.

- [11] R. Creighton Buck. Bounded continuous functions on a locally compact space. Michigan Mathematical Journal, 5(2):95–104, 1958.

- [12] Robert H. Cameron and William T. Martin. The orthogonal development of non-linear functionals in series of Fourier-Hermite functionals. Annals of Mathematics, 48(2):385–392, 1947.

- [13] René Carmona and Michael Tehranchi. Interest Rate Models: an Infinite Dimensional Stochastic Analysis Perspective. Springer, Berlin, Heidelberg, 2007.

- [14] Tianping Chen and Hong Chen. Approximation capability to functions of several variables, nonlinear functionals, and operators by radial basis function neural networks. IEEE Transactions on Neural Networks, 6(4):904–910, 1995.

- [15] Christa Cuchiero, Philipp Schmocker, and Josef Teichmann. Global universal approximation of functional input maps on weighted spaces. arXiv e-prints 2306.03303, 2023.

- [16] George Cybenko. Approximation by superpositions of a sigmoidal function. Mathematics of Control, Signals and Systems, 2(4):303–314, 1989.

- [17] Giuseppe Da Prato and Jerzy Zabczyk. Stochastic Equations in Infinite Dimensions. Encyclopedia of Mathematics and its Applications. Cambridge University Press, 2nd edition, 2014.

- [18] Robert C. Dalang, Davar Khoshnevisan, Carl Mueller, David Nualart, Yimin Xiao, and Firas Rassoul-Agha. A minicourse on stochastic partial differential equations. Lecture notes in mathematics; 1962. Springer, Berlin, 1st edition, 2009.

- [19] Nualart David and Moshezakai Zakai. Generalized multiple stochastic integrals and the representation of Wiener functionals. Stochastics, 23(3):311–330, 1988.

- [20] Suchuan Dong and Zongwei Li. Local extreme learning machines and domain decomposition for solving linear and nonlinear partial differential equations. Computer Methods in Applied Mechanics and Engineering, 387:114–129, 2021.

- [21] Vikas Dwivedi and Balaji Srinivasan. Physics informed extreme learning machine (PIELM) – a rapid method for the numerical solution of partial differential equations. Neurocomputing, 391:96–118, 2020.

- [22] Damir Filipovic. Consistency Problems for Heath-Jarrow-Morton Interest Rate Models. Lecture Notes in Mathematics, 1760. Springer, Berlin, Heidelberg, 1st edition, 2001.

- [23] Damir Filipović. Term-structure models: A graduate course. Springer Finance. Springer, Berlin, 2009.

- [24] Damir Filipović, Stefan Tappe, and Josef Teichmann. Term structure models driven by Wiener processes and Poisson measures: Existence and positivity. SIAM Journal on Financial Mathematics, 1(1):523–554, 2010.

- [25] Franco Flandoli and Eliseo Luongo. Stochastic Partial Differential Equations in Fluid Mechanics. Lecture Notes in Mathematics Series; Volume 2330. Springer, Singapore, 1st edition, 2023.

- [26] Gerald B. Folland. Fourier analysis and its applications. Brooks/Cole Publishing Company, Belmont, California, 1st edition, 1992.

- [27] Lukas Gonon. Random feature neural networks learn Black-Scholes type PDEs without curse of dimensionality. Journal of Machine Learning Research, 24(189):1–51, 2023.

- [28] Lukas Gonon, Lyudmila Grigoryeva, and Juan-Pablo Ortega. Approximation bounds for random neural networks and reservoir systems. The Annals of Applied Probability, 33(1):28–69, 2023.

- [29] Ian Goodfellow, Yoshua Bengio, and Aaron Courville. Deep Learning. MIT Press, 2016.

- [30] I. Gyöngy. Approximations of stochastic partial differential equations. In Stochastic Partial Differential Equations and Applications, Lecture notes in pure and applied mathematics; volume 227, New York, 2002. CRC Press.

- [31] Martin Hairer. An introduction to stochastic PDEs. arXiv e-prints 0907.4178, 2009.

- [32] Martin Hairer. Solving the KPZ equation. Annals of Mathematics, 178(2):559–664, 2013.

- [33] Jiequn Han, Arnulf Jentzen, and Weinan E. Solving high-dimensional partial differential equations using deep learning. Proceedings of the National Academy of Sciences, 115(34):8505–8510, 2018.

- [34] Philipp Harms. Lecture notes on SPDEs. Albert-Ludwigs-Universität Freiburg (University of Freiburg), 2017.

- [35] Philipp Harms, David Stefanovits, Josef Teichmann, and Mario V. Wüthrich. Consistent recalibration of yield curve models. Mathematical Finance, 28(3):757–799, 2018.

- [36] Calypso Herrera, Florian Krach, Pierre Ruyssen, and Josef Teichmann. Optimal stopping via randomized neural networks. arXiv e-prints 2104.13669, 2021.

- [37] Helge Holden, Bernt Øksendal, Jan Ubøe, and Tusheng Zhang. Stochastic Partial Differential Equations: A Modeling, White Noise Functional Approach. Universitext. Springer New York, New York, NY, 2nd edition, 2010.

- [38] Kurt Hornik, Maxwell Stinchcombe, and Halbert White. Multilayer feedforward networks are universal approximators. Neural Networks, 2(5):359–366, 1989.

- [39] Thomas Y. Hou, Wuan Luo, Boris L. Rozovsky, and Hao-Min Zhou. Wiener chaos expansions and numerical solutions of randomly forced equations of fluid mechanics. Journal of Computational Physics, 216(2):687–706, 2006.

- [40] Guang-Bin Huang, Qin-Yu Zhu, and Chee-Kheong Siew. Extreme learning machine: Theory and applications. Neurocomputing, 70(1):489–501, 2006. Neural Networks.

- [41] Tuomas Hytönen, Jan M.A.M. van Neerven, Mark C. Veraar, and Lutz Weis. Analysis in Banach Spaces, volume 63 of Ergebnisse der Mathematik und ihrer Grenzgebiete. 3. Folge. Springer, Cham, 2016.

- [42] Antoine Jacquier and Žan Žurič. Random neural networks for rough volatility. arXiv e-prints 2305.01035, 2023.

- [43] Arnulf Jentzen. Stochastic partial differential equations: Analysis and numerical approximations. Lecture Notes, ETH Zurich, 2016.

- [44] Arnulf Jentzen and Peter E. Kloeden. The numerical approximation of stochastic partial differential equations. Milan Journal of Mathematics, 77:205–244, 2009.

- [45] Arnulf Jentzen and Peter E. Kloeden. Taylor Approximations for Stochastic Partial Differential Equations. Society for Industrial and Applied Mathematics, 2011.

- [46] Gopinath B. Kallianpur and Jinbo Xiong. Stochastic models of environmental pollution. Advances in Applied Probability, 26(2):377–403, 1994.

- [47] Rudolf E. Kalman. A new approach to linear filtering and prediction problems. Journal of Basic Engineering, 82(1):35–45, 03 1960.

- [48] Evangelia A. Kalpinelli, Nikolaos E. Frangos, and Athanasios N. Yannacopoulos. A Wiener chaos approach to hyperbolic SPDEs. Stochastic Analysis and Applications, 29(2):237–258, 2011.

- [49] Ioannis Karatzas and Steven Shreve. Brownian Motion and Stochastic Calculus. Springer Science + Business Media, Berlin Heidelberg, 2nd corrected ed. 1998. corr. 6th printing 2004 edition, 1998.

- [50] Diederik P. Kingma and Jimmy Ba. Adam: A method for stochastic optimization. In Yoshua Bengio and Yann LeCun, editors, 3rd International Conference on Learning Representations, ICLR 2015, San Diego, CA, USA, May 7-9, 2015, Conference Track Proceedings. 2015.

- [51] Michael A. Kouritzin and Hongwei Long. Convergence of Markov chain approximations to stochastic reaction-diffusion equations. The Annals of Applied Probability, 12(3):1039–1070, 2002.

- [52] Raphael Kruse. Strong and Weak Approximation of Semilinear Stochastic Evolution Equations. Lecture Notes in Mathematics, 2093. Springer International Publishing, Cham, 1st edition, 2014.

- [53] Alois Kufner. Weighted Sobolev spaces. Teubner-Texte zur Mathematik Bd. 31. B.G. Teubner, Leipzig, 1980.

- [54] Harold J. Kushner. On the differential equations satisfied by conditional probablitity densities of Markov processes, with applications. Journal of The Society for Industrial and Applied Mathematics, Series A: Control, 2:106–119, 1964.

- [55] Moshe Leshno, Vladimir Ya. Lin, Allan Pinkus, and Shimon Schocken. Multilayer feedforward networks with a nonpolynomial activation function can approximate any function. Neural Networks, 6(6):861–867, 1993.

- [56] Zongyi Li, Nikola Kovachki, Kamyar Azizzadenesheli, Burigede Liu, Kaushik Bhattacharya, Andrew Stuart, and Anima Anandkumar. Fourier neural operator for parametric partial differential equations. arXiv e-prints 2010.08895, 2020.

- [57] Sergey V. Lototsky, , and Boris L. Rozovsky. Stochastic Differential Equations: A Wiener Chaos Approach, pages 433–506. Springer, Berlin, Heidelberg, 2006.

- [58] Sergey V. Lototsky, Remigijus Mikulevicius, and Boris L. Rozovsky. Nonlinear filtering revisited: A spectral approach. SIAM Journal on Control and Optimization, 35(2):435–461, 1997.

- [59] Sergey V. Lototsky and Boris L. Rozovsky. Wiener chaos solutions of linear stochastic evolution equations. The Annals of Probability, 34(2):638–662, 2006.

- [60] Sergey V. Lototsky and Boris L. Rozovsky. Stochastic Partial Differential Equations. Universitext. Springer International Publishing, Cham, 1st edition, 2017.

- [61] Wuan Luo. Wiener Chaos Expansion and Numerical Solutions of Stochastic Partial Differential Equations. PhD thesis, California Institute of Technology, 2006.

- [62] Paul Malliavin. Stochastic calculus of variation and hypoelliptic operators. Proceedings of the International Conference on Stochastic Differential Equations, pages 195–263, 1978.

- [63] Remigijus Mikulevičius and Boris L. Rozovsky. Linear parabolic stochastic PDE and Wiener chaos. SIAM Journal on Mathematical Analysis, 29(2):452–480, 1998.

- [64] Jean-Christophe Mourrat and Hendrik Weber. Convergence of the two-dimensional dynamic Ising-Kac model to . Communications on Pure and Applied Mathematics, 4:717–812, 2017.

- [65] Ariel Neufeld and Philipp Schmocker. Chaotic hedging with iterated integrals and neural networks. arXiv e-prints 2209.10166, 2022.

- [66] Ariel Neufeld and Philipp Schmocker. Universal approximation property of Banach space-valued random feature models including random neural networks. arXiv e-prints 2312.08410, 2023.

- [67] Ariel Neufeld and Philipp Schmocker. Universal approximation results for neural networks with non-polynomial activation function over non-compact domains. arXiv e-prints 2410.14759, 2024.

- [68] Ariel Neufeld, Philipp Schmocker, and Sizhou Wu. Full error analysis of the random deep splitting method for nonlinear parabolic PDEs and PIDEs with infinite activity. arXiv e-prints 2405.05192, 2024.

- [69] Ivan Nourdin and Giovanni Peccati. Normal approximations with Malliavin calculus: from Stein’s method to universality. Cambridge tracts in mathematics; 192. Cambridge University Press, Cambridge, 1st edition, 2012.

- [70] David Nualart. The Malliavin Calculus and Related Topics. Probability and Its Applications. Springer Science + Business Media, Berlin Heidelberg, 2nd edition, 2006.

- [71] Allan Pinkus. Approximation theory of the MLP model in neural networks. Acta Numerica, 8:143–195, 1999.

- [72] Ali Rahimi and Benjamin Recht. Random features for large-scale kernel machines. In Proceedings of the 20th International Conference on Neural Information Processing Systems, NIPS’07, pages 1177–1184, Red Hook, NY, USA, 2007. Curran Associates Inc.

- [73] Ali Rahimi and Benjamin Recht. Uniform approximation of functions with random bases. In 2008 46th Annual Allerton Conference on Communication, Control, and Computing, pages 555–561, 2008.

- [74] Ali Rahimi and Benjamin Recht. Weighted sums of random kitchen sinks: Replacing minimization with randomization in learning. In D. Koller, D. Schuurmans, Y. Bengio, and L. Bottou, editors, Advances in Neural Information Processing Systems, volume 21. Curran Associates, Inc., 2008.

- [75] Daniel Revuz and Marc Yor. Continuous martingales and Brownian motion. Grundlehren der mathematischen Wissenschaften 293. Springer, Berlin, 3rd edition, 1999.

- [76] Boris L. Rozovsky and Sergey V. Lototsky. Stochastic Evolution Systems : Linear Theory and Applications to Non-Linear Filtering. Probability Theory and Stochastic Modelling, 89. Springer International Publishing, Cham, 2nd edition, 2018.

- [77] Cristopher Salvi, Maud Lemercier, and Andris Gerasimovics. Neural stochastic PDEs: Resolution-invariant learning of continuous spatiotemporal dynamics. In Alice H. Oh, Alekh Agarwal, Danielle Belgrave, and Kyunghyun Cho, editors, Advances in Neural Information Processing Systems, 2022.

- [78] Marta Sanz Solé. Malliavin calculus with applications to stochastic partial differential equations. Fundamental sciences. Mathematics. EPFL Press, Lausanne, 2005.

- [79] Sho Sonoda and Noboru Murata. Neural network with unbounded activation functions is universal approximator. Applied and Computational Harmonic Analysis, 43(2):233–268, 2017.

- [80] Daniel W. Stroock. Homogeneous chaos revisited. Séminaire de probabilités de Strasbourg, 21:1–7, 1987.

- [81] Bin Teng, Yufeng Shi, and Qingfeng Zhu. Solving high-dimensional forward-backward doubly SDEs and their related SPDEs through deep learning. Personal Ubiquitous Computing, 26(4):925–932, 2021.

- [82] Jan M.A.M. van Neerven, Mark C. Veraar, and L. Weis. Stochastic evolution equations in UMD Banach spaces. Journal of Functional Analysis, 255(4):940–993, 2008.

- [83] John B. Walsh. An introduction to stochastic partial differential equations. In René Carmona, Harry Kesten, John B. Walsh, and P.L. Hennequin, editors, École d’Été de Probabiltés de Saint Flour XIV - 1984, Lecture Notes in Mathematics, pages 265–439, Berlin Heidelberg, 1986. Springer.

- [84] Yiran Wang and Suchuan Dong. An extreme learning machine-based method for computational PDEs in higher dimensions. arXiv e-prints 2309.07049, 2023.

- [85] Xuwei Yang, Anastasis Kratsios, Florian Krach, Matheus Grasselli, and Aurelien Lucchi. Regret-optimal federated transfer learning for kernel regression – with applications in American option pricing. arXiv e-prints 2309.04557, 2023.

- [86] Yunlei Yang, Muzhou Hou, and Jianshu Luo. A novel improved extreme learning machine algorithm in solving ordinary differential equations by Legendre neural network methods. Advances in Difference Equations, 2018:469, 2018.

- [87] Yao Yao. Deep learning-based numerical methods for stochastic partial differential equations and applications. Master’s thesis, University of Calgary, 2021. Available at http://hdl.handle.net/1880/113159.

- [88] Moshe Zakai. On the optimal filtering of diffusion processes. Zeitschrift für Wahrscheinlichkeitstheorie und Verwandte Gebiete, 11:230–243, 1969.

- [89] Dongkun Zhang, Ling Guo, and George Em Karniadakis. Learning in modal space: Solving time-dependent stochastic PDEs using physics-informed neural networks. SIAM Journal on Scientific Computing, 42(2):A639–A665, 2020.

- [90] He Zhang, Ran Zhang, and Tao Zhou. A predictor-corrector deep learning algorithm for high dimensional stochastic partial differential equations. arXiv e-prints 2208.09883, 2022.