TradExpert: Revolutionizing Trading with Mixture of Expert LLMs

Abstract

The integration of Artificial Intelligence (AI) in the financial domain has opened new avenues for quantitative trading, particularly through the use of Large Language Models (LLMs). However, the challenge of effectively synthesizing insights from diverse data sources and integrating both structured and unstructured data persists. This paper presents TradeExpert, a novel framework that employs a mix of experts (MoE) approach, using four specialized LLMs, each analyzing distinct sources of financial data, including news articles, market data, alpha factors, and fundamental data. The insights of these expert LLMs are further synthesized by a General Expert LLM to make a final prediction or decision. With specific prompts, TradeExpert can be switched between the prediction mode and the ranking mode for stock movement prediction and quantitative stock trading, respectively. In addition to existing benchmarks, we also release a large-scale financial dataset to comprehensively evaluate TradeExpert’s effectiveness. Our experimental results demonstrate TradeExpert’s superior performance across all trading scenarios.

Introduction

The fusion of artificial intelligence with financial analytics has spawned a new era of innovation, particularly with the infusion of Large Language Models (LLMs) into the realm of finance. These models, which have formerly excelled in natural language processing (NLP) tasks, are now being tailored to decode the complex and cryptic narratives of financial data. This adaptation is driven by a crucial insight: Financial markets are not just numbers-crunching engines but complicated information systems where the subtleties of news articles, reports, and economic indicators interweave to influence market dynamics.

Before the advent of LLMs, traditional financial models (Zeng et al. 2023; Yang et al. 2020; Liu et al. 2020; Baek and Kim 2018), primarily relied on quantitative methods such as statistical analysis, time series forecasting, and econometric models. These models often struggled to incorporate unstructured data such as news articles or financial reports without manual intervention. As a result, the development of LLMs tailored for financial applications has progressed rapidly. Initial ventures into this domain repurposed general LLMs such as GPTs (Brown 2020; Achiam et al. 2023) and LLaMAs (Touvron et al. 2023a, b; AI@Meta 2024) to interpret financial texts. However, more specialized language models such as FinBERT (Araci 2019), BloombergGPT (Wu et al. 2023), and FinGPT (Yang, Liu, and Wang 2023) have since evolved, demonstrating enhanced proficiency in understanding and predicting market movements from unstructured data. These models were specifically fine-tuned or pre-trained on vast amounts of financial corpus. This extensive training on domain-specific datasets has allowed them to better capture typical patterns in the financial corpus. Despite these advancements, the challenge remains to effectively synthesize insights from diverse data sources like historical stock prices, alpha factors, fundamental data, news articles, etc. In addition, integration of the deluge of unstructured financial texts with structured quantitative metrics still remains to be investigated with language models.

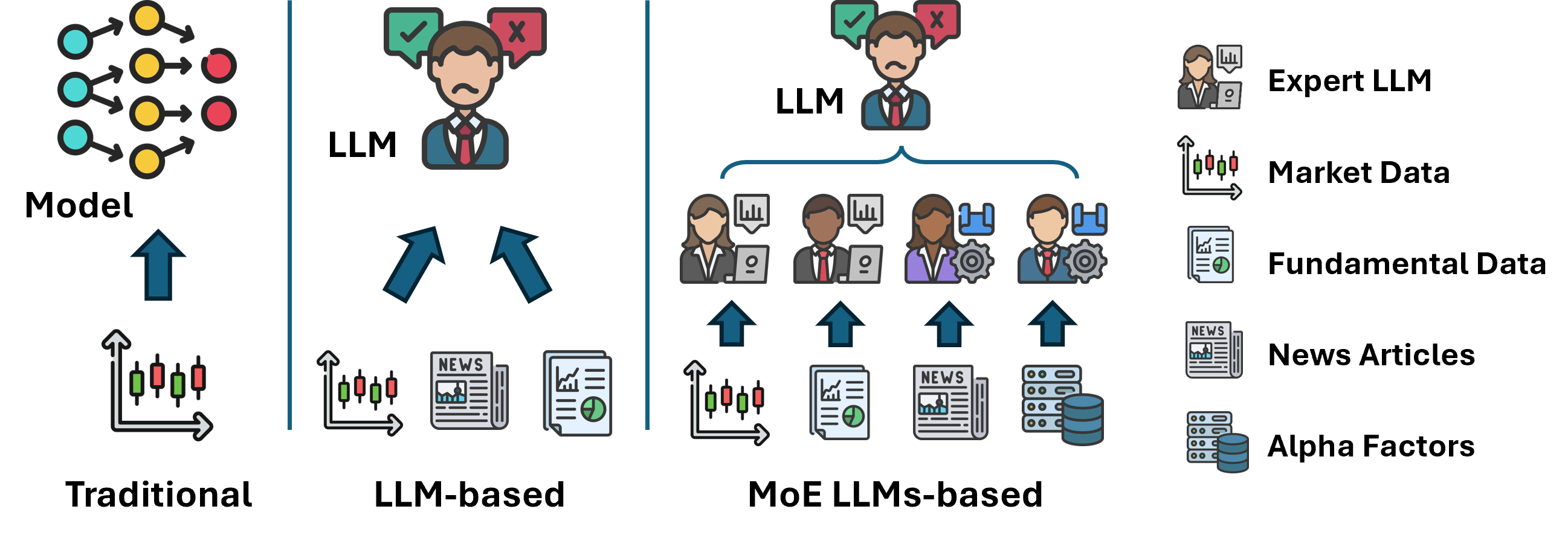

To this end, we propose the TradExpert framework, which stands at the confluence of these challenges. It leverages a Mixture of Experts (MoE) approach (Eigen, Ranzato, and Sutskever 2013; Du et al. 2022; Shen et al. 2023), involving multiple LLMs each specialized in distinct facets of financial data—news articles, market data, alpha factors, and fundamental data. This not only enhances the model’s ability to process diverse data modalities but also allows for a more nuanced understanding of how different factors interact to influence market trends. Figure 1 illustrates differences among traditional, LLM-based, and MoE LLMs-based financial models. In TradeExpet, each expert works with a distinct focus and produces specialized reports, which are finally summarized and analyzed by a general expert, just like the structured division of labor seen in the real world. Specifically, TradExpert employs specialized LLMs to first independently analyze different data sources, then integrates these analyses via another LLM that synthesizes insights to predict market movements and inform trading strategies. Innovatively, we utilize a reprogramming mechanism to convert time series data to embeddings aligned with LLMs. In addition, we propose two modes for the General Expert LLM, prediction mode and ranking mode, for stock movement prediction and stock trading strategies, respectively. In ranking mode, we innovatively let the LLM serve as a comparator within a relaxed sorting algorithm, enabling the selection of the Top-K ranked stocks for trading. To comprehensively evaluate our method, we have also collected a large-scale datasets, which will be publicly released.

Oue contributions can be summarized as follows.

-

•

We present TradExpert, a novel framework that employs an MoE approach, integrating four LLMs each specialized to analyze distinct sources of financial data, imitating the structured division of labors seen in the real world.

-

•

We utilize the LLM as a comparator within a relaxed sorting algorithm, which enables trades with the Top-K ranked stocks based on TradExpert’s prediction.

-

•

We release a comprehensive dataset encompassing a wide range of financial data, which serves as a new benchmark for financial analysis.

-

•

Our comprehensive experiments show that TradExpert consistently outperforms state-of-the-art baselines across all trading scenarios. Ablation studies validate the effectiveness of the modules proposed in TradExpert.

Related Work

Financial Language Models

have significantly advanced in recent years, blending NLP techniques with financial analytics to extract meaningful insights from vast amounts of unstructured financial data. To begin with, FinBert (Araci 2019) is a financial domain-specific variant of BERT, pretrained on a large corpus of financial communications. In 2023, BloombergGPT (Wu et al. 2023) emerged as a 50-billion-parameter model trained on a vast financial dataset. FLANG (Shah et al. 2022) introduced a financial language model with specialized masking and objectives. Astock (Zou et al. 2022) provided a platform for studying NLP-aided stock auto-trading algorithms on the Chinese market. BBT-FinT5 (Lu et al. 2023) advanced Chinese financial NLP with a large-scale pre-trained model. FinMA (Xie et al. 2023) showcased a model fine-tuned on a multi-task instruction datasets. FinGPT (Yang, Liu, and Wang 2023) provided an open-source framework for financial LLMs. InvestLM (Yang, Tang, and Tam 2023) showed the effectiveness of instruction tuning for investment-related tasks. FinReport (Li et al. 2024b) introduced a system for automatic financial report generation. Lastly, AlphaFin (Li et al. 2024a) integrated retrieval-augmented generation techniques for financial analysis. Collectively, these works demonstrate the evolution of financial NLP models and benchmarks, advancing the capabilities of LLMs in financial applications.

Integration of Text and Financial Data

has also been rapidly developed for stock movement prediction. StockNet (Xu and Cohen 2018) developed a deep generative model that jointly exploits text and price signals for stock movement prediction. SLOT (Soun et al. 2022) improved upon this by using self-supervised learning to handle sparse and noisy tweet data, capturing multi-level price trends. CH-RNN (Wu et al. 2018) introduced a hybrid deep sequential modeling approach that leverages social text for stock prediction, incorporating cross-modal attention mechanisms. More recently, studies (Lopez-Lira and Tang 2023; Chen et al. 2023) have explored the use of ChatGPT for stock movement prediction, comparing its performance with traditional state-of-the-art models. These works collectively demonstrate the increasing sophistication of models that integrate text and financial data, highlighting the potential for improving trading scenarios.

Problem Definition

In this study, we aim to trade stocks using a framework that incorporates Large Language Models (LLMs).

The input data comprises four primary components:

-

•

News: Textual information from news articles pertinent to the stock and market conditions.

-

•

Market Data: Historical OHLCV (Open, High, Low, Close, Volume) data representing the stock’s trading activity.

-

•

Alpha Factors: Quantitative indicators and signals believed to possess predictive power regarding stock price movements.

-

•

Fundamental Data: Earnings call transcripts and fundamental metrics reflecting the company’s economic health and performance.

Task 1: Stock movement prediction

is a fundamental challenge in quantitative trading, which involves the prediction of future price trends based on multifaceted data sources. Formally, let denote our dataset, where represents the input vector for the -th stock on day , and is the corresponding label indicating whether the stock price will rise or fall on day . The input can be expressed as:

| (1) |

Our objective is to learn a predictive function parameterized by such that , where is modeled using LLMs. The model outputs a binary prediction, “Rise” or “Fall” indicating the predicted stock price movement.

Task 2: Stock trading simulation

involves evaluating the performance of Buy-and-Hold strategy based on the Top-K ranked stocks sorted by TradExpert. This task simulates real-market trading scenarios to assess the profitability and risk of TradExpert using metrics including Annualized Return (AR), Sharpe Ratio (SR), Annualized Volatility (AV), and Maximum Drawdown (MD).

Datasets

In this study, we collected a comprehensive datasets encompassing various data sources including four primary components: News, Market Data, Alpha Factors, and Fundamental Data. The period covered by all data sources spans 4 years from January 1, 2020, to December 31, 2023.

Stastics

News

is collected from several reputable financial news sources, including Yahoo Finance, Reuters, InvestorPlace, GlobeNewswire, The Motley Fool, etc. This dataset comprises a total of 524,995 news articles for stocks on S&P 500 list, with an average word count of 596.4 words per article. Each news article is associated with a list of related stock tickers.

Market Data

consists of historical daily OHLCV records for stocks on S&P 500 list. This dataset includes a total of 481,484 records, offering a detailed view of the stocks’ trading activity over the specified period.

Alpha Factors

incorporates 108 technical indicators and factors with their expressions, which are believed to possess predictive power regarding stock price movements.

Fundamental Data

includes earnings call transcripts, financial statements, and fundamental metrics. The earnings call transcripts are sourced from Seeking Alpha, with 16 transcripts (4 years, quaterly updated) available for each stock. Fundamental metrics include Earnings Per Share (EPS), Price-to-Earnings Ratio (P/E Ratio), Book Value Per Share (BVPS), etc.

Data Split

The datasets were split into training, validation, and test sets based on chronological order to ensure that future data remains unseen during the training process. The split was performed as follows: Training set: January 1, 2020, to June 30, 2022. Validation set: July 1, 2022, to December 31, 2022. Testing set: January 1, 2023, to December 31, 2023.

| Instructions and Prompts | Responses | |||||

|---|---|---|---|---|---|---|

| News | News articles |

|

||||

| Market |

|

Movement | ||||

| Alpha |

|

Movement | ||||

| Fundamental |

|

|

Methodology

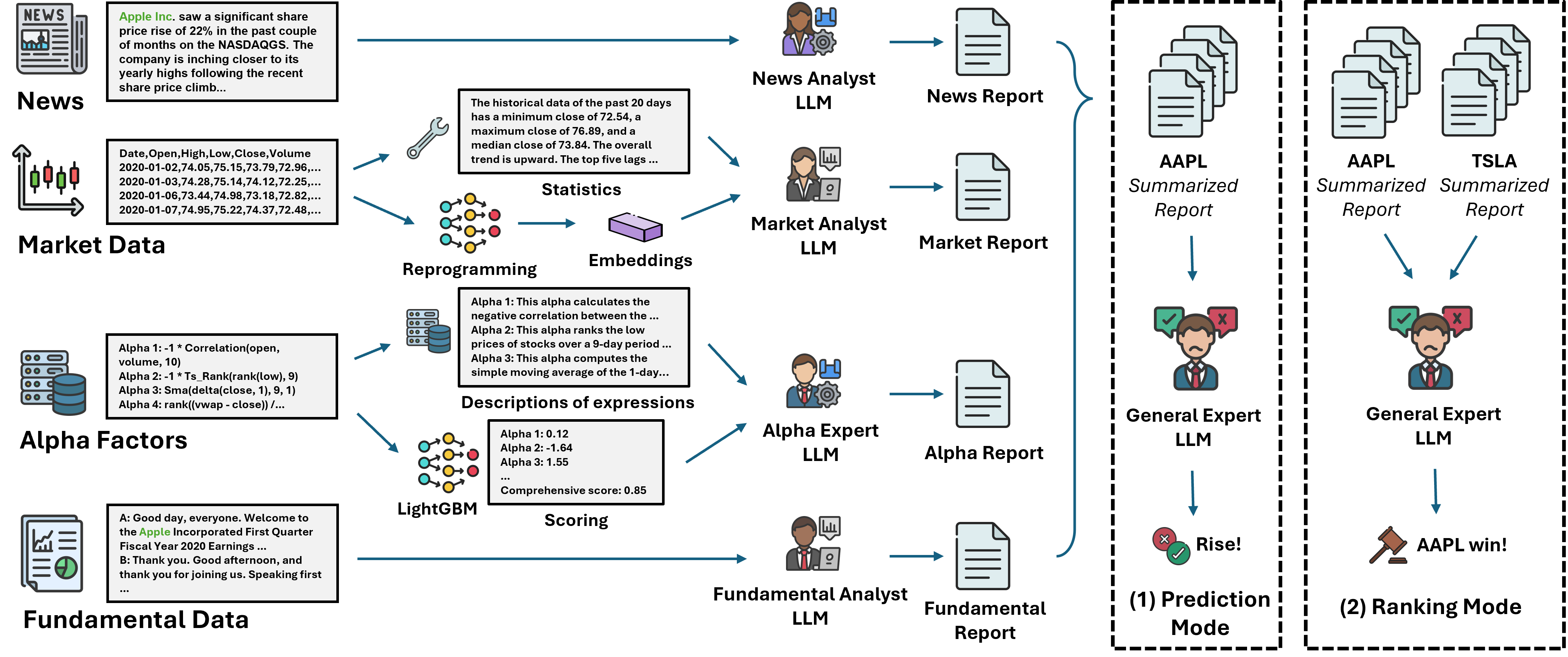

In this study, we propose TradExpert, a novel framework leveraging the MoE LLMs approach, where four LLMs serve as specialized experts for distinct sources of financial data. A General Expert LLM then synthesizes the summaries of the four Expert LLMs to produce the final output. The pipeline of TradExpert is shown in Figure 2.

In TradExpert, all expert LLMs are built on the LLaMA-2-7B backbone LLM (Touvron et al. 2023b) and are supervised and fine-tuned using the LoRA mechanism (Hu et al. 2022). Before training and fine-tuning, we preprocess the raw datasets to construct prompts, instructions, and ground-truth responses for each LLM. An overall description of the preprocessed datasets is demonstrated in Table 1. The details will be introduced in the following.

News Analyst

The News Analyst LLM is designed to analyze texts of news articles to predict stock movements. The prompt and instruction for fine-tuning the LLM are shown in Figure 3. The outputs from the News Analyst LLM include not only a prediction of the stock movement but also a reasoning of how the news article relates to the predicted movement in order to employ a Chain-of-Thought (CoT) (Wei et al. 2022) reasoning approach. The ground-truth reasonings are pre-generated by the OpenAI GPT-4 API using instructions and prompts that incorporate the actual stock movements and the texts of news articles.

Market Analyst

The Market Analyst LLM focuses on analyzing historical OHLCV (Open, High, Low, Close, Volume) data to predict stock movements. However, time series data is inherently continuous and lacks the discrete token structure that LLMs are designed to process. This misalignment poses a significant challenge in effectively utilizing LLMs on time series. To this end, we utilize a reprogramming mechanism (Jin et al. 2024) to reprogram the input financial time series into text prototype representations.

Formally, let an OHLCV data instance be which consists of variables across time steps. is first divided and embedded into a sequence of patch embeddings , where and are the number of patches and the patch embedding dimension respectively. The patches are then reprogrammed using a collection of text prototypes , which is achieved by linearly probing the LLM’s pre-trained word embedding , where and are the size of the vocabulary of the LLM and the text prototypes ( ), and is the embedding dimension. The reprogrammed patches are generated using a multi-head cross-attention mechanism: , where query , key , and value for each head . The reprogrammed embeddings are obtained by aggregating the outputs from each attention head and projecting them to the hidden dimensions of the backbone LLM. Finally, the reprogrammed embeddings are augmented with a language description of statistics extracted from TSFresh (Christ et al. 2018), serving as prompts for the Alpha Expert. An example of instruction and prompt is shown in Figure 4.

Alpha Expert

The Alpha Expert specializes in processing expression-based alpha factors, which are technical indicators and algorithm-generated factors believed to possess predictie power regarding stock price movements.

We leverage GPT-4’s capability of understanding complex expressions to pre-generate a language description for each factor. In this way, we built our Alpha database, where an alpha record consists of:

-

•

Expression: The mathematical or logical formula used to compute the alpha factor based on OHLCV data. E.g. rank(ts_argmax(corr(ts_rank(close, 10), ts_rank(volume, 10), 10), 5))

-

•

Description: Generated by GPT-4 with prompts that include the expression.

For each stock, we first calculate the values of all alpha factors based on OHLCV data and then derive a comprehensive score via a LightGBM-based model (Ke et al. 2017). Subsequently, we select Top-K alphas that contribute most significantly to this comprehensive score. Descriptions of these Top-K alphas are retrieved from the database and, along with the calculated values, are included in the prompts and instructions for the Alpha Expert.

Fundamental Analyst

The Fundamental Analyst LLM specializes in analyzing fundamental data, including earnings call transcripts and financial metrics, to predict stock price movements on a quarterly basis. The procedure of the Fundamental Analyst LLM is similar to that of the News Analyst LLM, with key differences being that the fundamental data is updated quarterly and, therefore, the movement predictions are made for the next quarter. The response should include a prediction in one of the following five categories: “Strong Rise”, “Moderate Rise”, “No Change”, “Moderate Fall”, or “Strong Fall”, followed by a reasoning.

General Expert

The General Expert LLM can operate in two distinct modes: prediction mode and ranking mode. Both modes begin by summarizing the reports (historical conversation including instructions, prompts, and responses) from the four specialized experts due to the limitations on input context length of the backbone LLM.

In prediction mode, used for stock movement prediction, the summarized reports are used to construct a prompt with a prediction prefix. Given the summarized reports, the General Expert LLM outputs a binary prediction indicating whether the stock will rise or fall.

In ranking mode, used for stock trading, the General Expert LLM functions as a comparator to establish the ranking ability. Specifically, given the summarized reports of two stocks, the General Expert LLM would determine which stock is likely to perform better in the future. To generate a Top-K ranking of stocks, we employ a relaxed comparison-based sorting similar to BubbleSort: We initially compare every pair of stocks and count the number of wins for each stock. Subsequently, we sort these counts to establish the rankings for stocks. Although algorithms like QuickSort and vanilla BubbleSort offer fewer comparisons for Top-K selection on average and , we propose to use this relaxed comparison-based sorting alogrithm with due to the non-transitive nature of LLM-based comparator (Liu et al. 2024). Therefore, more comparisons tend to yield more accurate rankings in practice.

The General Expert LLM is finetuned on both tasks of stock movement prediction and stock comparison simultaneously. The instructions and prompts are shown in Figure 5.

| BigData22 | ACL18 | CIKM18 | S&P500 (Ours) | |||||

| Acc ↑ | MCC ↑ | Acc ↑ | MCC ↑ | Acc ↑ | MCC ↑ | Acc ↑ | MCC ↑ | |

| Hybrid Models | ||||||||

| ALSTM-W | 0.48 | -0.01 | 0.53 | 0.08 | 0.54 | 0.03 | 0.55 | 0.10 |

| ALSTM-D | 0.49 | 0.01 | 0.53 | 0.07 | 0.50 | -0.04 | 0.54 | 0.05 |

| StockNet | 0.53 | -0.02 | 0.54 | -0.02 | 0.52 | -0.02 | 0.56 | 0.06 |

| SLOT | 0.55 | 0.10 | 0.59 | 0.21 | 0.56 | 0.09 | / | / |

| Large Language Models | ||||||||

| GPT-4 | 0.54 | 0.03 | 0.52 | 0.02 | 0.57 | 0.02 | 0.58 | 0.10 |

| Gemini | 0.55 | 0.04 | 0.52 | 0.04 | 0.54 | 0.02 | 0.59 | 0.11 |

| LLaMA2-7B-chat | 0.54 | 0.05 | 0.51 | 0.01 | 0.55 | -0.03 | 0.57 | 0.06 |

| LLaMA2-70B | 0.47 | 0.00 | 0.51 | 0.01 | 0.49 | -0.07 | 0.57 | 0.02 |

| LLaMA3-8B | 0.55 | 0.02 | 0.52 | 0.02 | 0.57 | 0.03 | 0.53 | 0.04 |

| FinMA-7B | 0.51 | 0.02 | 0.51 | 0.03 | 0.50 | 0.08 | 0.59 | 0.09 |

| FinGPT-7B-lora | 0.45 | 0.00 | 0.49 | 0.00 | 0.42 | 0.00 | 0.51 | 0.05 |

| InternLM | 0.56 | 0.08 | 0.51 | 0.02 | 0.57 | -0.03 | 0.60 | 0.06 |

| Falcon | 0.55 | 0.00 | 0.51 | 0.00 | 0.47 | -0.06 | 0.52 | 0.03 |

| Mixtral-7B | 0.46 | 0.02 | 0.49 | 0.00 | 0.42 | -0.05 | 0.54 | 0.04 |

| MoE Larage Language Models | ||||||||

| TradExpert-NM | 0.59 | 0.12 | 0.60 | 0.15 | 0.59 | 0.12 | 0.64 | 0.19 |

Experiments

In this section, we conduct a comprehensive evaluation for TradExpert framework on two main tasks: stock movement prediction and stock trading simulation. Our experiments aims to address the following research questions: RQ1: How does TradExpert perform in stock movement prediction compared with state-of-the-art baselines? RQ2: What are the potential profits and associated risks of TradExpert in the backtesting on the real market? RQ3: How effective is the reasoning capability of TradExpert for unstructured data? RQ4: What is the significance of each expert within the TradExpert framework? RQ5: Why we choose the relaxed comparison-based sorting algorithm in TradExpert?

Datasets

We include two categories of datasets in our experiments:

- •

-

•

Proprietary Datasets: We also utilize our proprietary datasets, which include extensive historical OHLCV data, news articles, alpha factors, and fundamental metrics for a comprehensive analysis.

Experimental Setup

In our experiments, the four expert LLMs and the General Expert LLM are bulit on the LLaMA-2-7B bakcbone model (Touvron et al. 2023b) and are finetuned via LoRA (Hu et al. 2022) mechanism.

Stock Movement Prediction:

TradExpert works in prediction mode, that is, the General Expert LLM reponses a binary prediction indicating whether a stock will rise or fall the next day. Methods are evaluated using binary classification metrics such as accuracy (Acc) and Matthews Correlation Coefficient (MCC).

Stock Trading Simulation:

TradExpert works in ranking mode, that is, the General Expert LLM acts as a comparator to sort the stocks. We simulate the real profit and risk of TradExpert by executing trades based on the Top-K ranked stocks. TradExpert and baselines are evaluated using metrics including Annualized Return (AR), Sharpe Ratio (SR), Annualized Volatility (AV), and Maximum Drawdown (MD).

Baselines

For stock movement prediction, the baselines include: (1) Hybrid Models: StockNet (Xu and Cohen 2018), ALSTM-W (Soun et al. 2022), ALSTM-D (Soun et al. 2022), SLOT (Soun et al. 2022). 2) Large Language Models: GPT-4 (Achiam et al. 2023), Gemini (Team et al. 2023), LLaMA2-70B (Touvron et al. 2023b), LLaMA3-8B (AI@Meta 2024), FinMA-7B (Xie et al. 2023), FinGPT-LlaMA2-7B (Yang, Liu, and Wang 2023), InternLM-7B (Cai et al. 2024), Falcon-7B (Almazrouei et al. 2023), Mixtral-7B (Jiang et al. 2023).

For stock trading simulation, the baselines include: (1)Traditional Models: Random Forest (Breiman 2001), Decision Tree (Loh 2011), SVM (Cortes and Vapnik 1995). (2) Deep Learning Models: A2C (Mnih et al. 2016), PPO (Schulman et al. 2017), SARL (Ye et al. 2020), EIIE (Jiang, Xu, and Liang 2017), and DeepTrader (Wang et al. 2021). To reduce computational costs in backtesting, we evaluated all methods on datasets with stocks on the DOW 30 list, a subset of the S&P 500, with around 30 stocks.

Results

Stock Movement Prediction

We implemented all baselines ourselves or utilized existing open-source codes, except the closed-source model SLOT, for which we refer to the metrics reported in the relevant paper. To ensure a fair comparison, we only included the News Analyst and Market Analyst in TradExpert, named TradExeprt-NM. The results are shown in Table 2. As we can see, among hybrid models, SLOT achieves outstanding accuracy and MCC on the ACL18, benefitting from the proposed global market guidance. Among LLMs, InternLM shows remarkable performance, particularly on our proprietary S&P500 dataset. Our proposed TradExpert-NM, utilizing a mixture of expert LLMs approach, consistently outperformed other models across all datasets except for MCC on the ACL18, showcasing its superior performance. Noting that BigData22, ACL18, and CIKM18 are relatively small datasets with texts from tweets, while our S&P500 dataset consist of news articles with much more words. This difference in text lengths contributes to the more significant improvements obtained by TradExpert-7B-NM on the S&P500 dataset.

Stock Trading Simulation

We perform backtesting to evaluate TradExpert and baselines. To reduce computational costs in backtesting, we limit the stock pool to about 30 stocks on the DOW 30, a subset of the S&P 500. For TradExpert, we implement a Buy-and-Hold trading strategy on the Top-K stocks ranked by TradExpert. The backtesting period is the same as the testing period of our datasets, which ranges from January 1, 2023, to December 31, 2023. The results summarized in Table 3 demonstrate TradExpert’s superior performance across all metrics considered. Among traditional models, XGBoost achieved a relatively high return but also exhibited high volatility and drawdown, indicating greater risk. Deep learning models generally outperformed traditional models. Among them, DeepTrader stood out with the highest return and Sharpe ratio. TradExpert, our proposed model, significantly outperformed all other models with an exceptional AR of 49.79% and the lowest AV of 9.95%. This combination yielded an outstanding Sharpe ratio of 5.01, indicating a high return per unit of risk. Figure 6 shows the trends of cumulative returns over time for all methods.

| AR ↑ | AV ↓ | SR ↑ | MD ↓ | |

| DJI Index | 13.92% | 11.41% | 1.22 | 9.70% |

| Traditional Models | ||||

| SVM | 15.77% | 26.67% | 0.59 | 19.94% |

| XGBoost | 21.58% | 27.29% | 0.79 | 21.90% |

| LightGBM | 2.17% | 22.74% | 0.1 | 21.29% |

| Deep Learning Models | ||||

| A2C | 19.16% | 11.29% | 1.7 | 9.09% |

| PPO | 16.62% | 11.51% | 1.44 | 9.45% |

| EIIE | 23.64% | 13.73% | 1.72 | 10.07% |

| SARL | 21.87% | 14.72% | 1.49 | 8.52% |

| DeepTrader | 32.45% | 17.86% | 1.82 | 15.32% |

| MoE Large Language Models | ||||

| TradExpert | 49.79% | 9.95% | 5.01 | 6.56% |

| Configuration | AR ↑ | AV ↓ | SR ↑ | MD ↓ |

|---|---|---|---|---|

| TradExpert | 49.79% | 9.95% | 5.00 | 6.56% |

| w/o Market | 30.87% | 16.43% | 1.88 | 13.29% |

| w/o News | 31.92% | 18.36% | 1.74 | 13.04% |

| w/o Alpha | 41.65% | 11.38% | 3.66 | 8.94% |

| w/o Fundamental | 44.32% | 10.68% | 4.15 | 7.82% |

| Model | RankIC ↑ | RankICIR ↑ |

|---|---|---|

| TradExpert-MA | 0.12 | 0.90 |

| Alpha Combination | 0.07 | 0.65 |

| RankIC ↑ | RankICIR ↑ | Time | |

|---|---|---|---|

| RelaxedSort† | 0.12 | 0.90 | |

| BubbleSort | 0.06 | 0.65 | |

| QuickSort | 0.03 | 0.38 |

Ablation Study

The Impacts of Experts

To evaluate the effectiveness of each expert within the TradExpert framework, we created multiple versions of TradExpert, each with a specific expert removed. By comparing the performance of these modified frameworks, we can assess the impact of each expert on the overall functionality of TradExpert. The results in Table 4 reveal the varying degrees of impact of each expert. The Market Analyst and the News Analyst emerged as the most critical, significantly influencing profitability and risk management, as seen by the largest drop in AR and AV when they were removed, respectively. The Alpha Expert is obviously less impactful than the Market Analysts and the News Analysts. The Fundamental Analyst had the smallest effect on daily trading metrics, but provided essential long-term stability, evident from the modest changes in AR and MD upon its removal. This highlights a strategic balance in TradExpert, where each expert contributes uniquely to the final decision and prediction.

The Effectiveness of Structured Data Reasoning.

We show the effectiveness by comparing TradExpert-MA with traditional models for structured data like OHLCV data and alpha factors. We use a genetic programming-based symbolic regression model as our baseline, which mines alpha expressions aimed at predicting the RankIC of day ’s returns. TradExpert-MA is built on top of the same alphas, where News and Fundamental experts were removed to exclude affects from other sources. We compare TradExpert-MA with the combination of alphas using metrics of RankIC and RankICIR. The results are shown in Table 5. The improvements over the alpha combination demonstrate the reasoning ability of TradExpert for structured data.

The Choices of Ranking algorithm

In TradExpert, we implement the Top-K ranking by sorting all stocks completely using a relaxed comparison-based algorithm, where TradExpert serves as the comparator. To justify our choice of this seemingly cumbersome approach, we conducted comparison experiments with other theoretically more efficient ranking algorithms. Specifically, our alternatives include QuickSort and BubbleSort with time complexity and , respectively. The comparison results in Table 6 demonstrate that our approach outperforms others, despite having a higher computational complexity. This is attributed to the non-transitive nature of LLM-based comparator. Therefore, a greater number of comparisons yield more accurate rankings in TradExpert.

Conclusion

In this study, we introduced TradeExpert, a novel framework that harnesses the power of LLMs to enhance stock trading strategies. By integrating multiple specialized LLMs, each focused on distinct aspects of financial data, TradeExpert provides a comprehensive and nuanced analysis that significantly outperforms traditional financial models in practice. Looking ahead, our goal is to explore how to employ TradeExpert in the high-frequency trading scenario and extend its capabilities to encompass a wider range of global markets.

Limitation

Although TradExpert has notable strengths, its processing time poses certain challenges. On average, it takes 4.7 seconds for a single stock with an Nvidia A5000 GPU. For daily trading, this processing time is generally manageable. However, for scenarios demanding quicker decision-making, such as high-frequency trading, TradExpert’s latency becomes a notable drawback.

References

- Achiam et al. (2023) Achiam, J.; Adler, S.; Agarwal, S.; Ahmad, L.; Akkaya, I.; Aleman, F. L.; Almeida, D.; Altenschmidt, J.; Altman, S.; Anadkat, S.; et al. 2023. Gpt-4 technical report. arXiv preprint arXiv:2303.08774.

- AI@Meta (2024) AI@Meta. 2024. Llama 3 Model Card.

- Almazrouei et al. (2023) Almazrouei, E.; Alobeidli, H.; Alshamsi, A.; Cappelli, A.; Cojocaru, R.; Debbah, M.; Goffinet, É.; Hesslow, D.; Launay, J.; Malartic, Q.; et al. 2023. The falcon series of open language models. arXiv preprint arXiv:2311.16867.

- Araci (2019) Araci, D. 2019. Finbert: Financial sentiment analysis with pre-trained language models. arXiv preprint arXiv:1908.10063.

- Baek and Kim (2018) Baek, Y.; and Kim, H. Y. 2018. ModAugNet: A new forecasting framework for stock market index value with an overfitting prevention LSTM module and a prediction LSTM module. Expert Systems with Applications, 113: 457–480.

- Breiman (2001) Breiman, L. 2001. Random forests. Machine learning, 45: 5–32.

- Brown (2020) Brown, T. B. 2020. Language models are few-shot learners. arXiv preprint ArXiv:2005.14165.

- Cai et al. (2024) Cai, Z.; Cao, M.; Chen, H.; Chen, K.; Chen, K.; Chen, X.; Chen, X.; Chen, Z.; Chen, Z.; Chu, P.; Dong, X.; Duan, H.; Fan, Q.; Fei, Z.; Gao, Y.; Ge, J.; Gu, C.; Gu, Y.; Gui, T.; Guo, A.; Guo, Q.; He, C.; Hu, Y.; Huang, T.; Jiang, T.; Jiao, P.; Jin, Z.; Lei, Z.; Li, J.; Li, J.; Li, L.; Li, S.; Li, W.; Li, Y.; Liu, H.; Liu, J.; Hong, J.; Liu, K.; Liu, K.; Liu, X.; Lv, C.; Lv, H.; Lv, K.; Ma, L.; Ma, R.; Ma, Z.; Ning, W.; Ouyang, L.; Qiu, J.; Qu, Y.; Shang, F.; Shao, Y.; Song, D.; Song, Z.; Sui, Z.; Sun, P.; Sun, Y.; Tang, H.; Wang, B.; Wang, G.; Wang, J.; Wang, J.; Wang, R.; Wang, Y.; Wang, Z.; Wei, X.; Weng, Q.; Wu, F.; Xiong, Y.; Xu, C.; Xu, R.; Yan, H.; Yan, Y.; Yang, X.; Ye, H.; Ying, H.; Yu, J.; Yu, J.; Zang, Y.; Zhang, C.; Zhang, L.; Zhang, P.; Zhang, P.; Zhang, R.; Zhang, S.; Zhang, S.; Zhang, W.; Zhang, W.; Zhang, X.; Zhang, X.; Zhao, H.; Zhao, Q.; Zhao, X.; Zhou, F.; Zhou, Z.; Zhuo, J.; Zou, Y.; Qiu, X.; Qiao, Y.; and Lin, D. 2024. InternLM2 Technical Report. arXiv:2403.17297.

- Chen et al. (2023) Chen, Z.; Zheng, L. N.; Lu, C.; Yuan, J.; and Zhu, D. 2023. ChatGPT informed graph neural network for stock movement prediction. arXiv preprint arXiv:2306.03763.

- Christ et al. (2018) Christ, M.; Braun, N.; Neuffer, J.; and Kempa-Liehr, A. W. 2018. Time series feature extraction on basis of scalable hypothesis tests (tsfresh–a python package). Neurocomputing, 307: 72–77.

- Cortes and Vapnik (1995) Cortes, C.; and Vapnik, V. 1995. Support-vector networks. Machine learning, 20: 273–297.

- Du et al. (2022) Du, N.; Huang, Y.; Dai, A. M.; Tong, S.; Lepikhin, D.; Xu, Y.; Krikun, M.; Zhou, Y.; Yu, A. W.; Firat, O.; et al. 2022. Glam: Efficient scaling of language models with mixture-of-experts. In International Conference on Machine Learning, 5547–5569. PMLR.

- Eigen, Ranzato, and Sutskever (2013) Eigen, D.; Ranzato, M.; and Sutskever, I. 2013. Learning factored representations in a deep mixture of experts. arXiv preprint arXiv:1312.4314.

- Hu et al. (2022) Hu, E. J.; Shen, Y.; Wallis, P.; Allen-Zhu, Z.; Li, Y.; Wang, S.; Wang, L.; and Chen, W. 2022. LoRA: Low-Rank Adaptation of Large Language Models. In International Conference on Learning Representations.

- Jiang et al. (2023) Jiang, A. Q.; Sablayrolles, A.; Mensch, A.; Bamford, C.; Chaplot, D. S.; Casas, D. d. l.; Bressand, F.; Lengyel, G.; Lample, G.; Saulnier, L.; et al. 2023. Mistral 7B. arXiv preprint arXiv:2310.06825.

- Jiang, Xu, and Liang (2017) Jiang, Z.; Xu, D.; and Liang, J. 2017. A deep reinforcement learning framework for the financial portfolio management problem. arXiv preprint arXiv:1706.10059.

- Jin et al. (2024) Jin, M.; Wang, S.; Ma, L.; Chu, Z.; Zhang, J. Y.; Shi, X.; Chen, P.-Y.; Liang, Y.; Li, Y.-F.; Pan, S.; et al. 2024. Time-LLM: Time Series Forecasting by Reprogramming Large Language Models. In The Twelfth International Conference on Learning Representations.

- Ke et al. (2017) Ke, G.; Meng, Q.; Finley, T.; Wang, T.; Chen, W.; Ma, W.; Ye, Q.; and Liu, T.-Y. 2017. Lightgbm: A highly efficient gradient boosting decision tree. Advances in neural information processing systems, 30.

- Li et al. (2024a) Li, X.; Li, Z.; Shi, C.; Xu, Y.; Du, Q.; Tan, M.; and Huang, J. 2024a. AlphaFin: Benchmarking Financial Analysis with Retrieval-Augmented Stock-Chain Framework. In Proceedings of the 2024 Joint International Conference on Computational Linguistics, Language Resources and Evaluation (LREC-COLING 2024), 773–783.

- Li et al. (2024b) Li, X.; Shen, X.; Zeng, Y.; Xing, X.; and Xu, J. 2024b. FinReport: Explainable Stock Earnings Forecasting via News Factor Analyzing Model. In Companion Proceedings of the ACM on Web Conference 2024, 319–327.

- Liu et al. (2020) Liu, X.-Y.; Yang, H.; Chen, Q.; Zhang, R.; Yang, L.; Xiao, B.; and Wang, C. D. 2020. FinRL: A deep reinforcement learning library for automated stock trading in quantitative finance. arXiv preprint arXiv:2011.09607.

- Liu et al. (2024) Liu, Y.; Zhou, H.; Guo, Z.; Shareghi, E.; Vulic, I.; Korhonen, A.; and Collier, N. 2024. Aligning with human judgement: The role of pairwise preference in large language model evaluators. arXiv preprint arXiv:2403.16950.

- Loh (2011) Loh, W.-Y. 2011. Classification and regression trees. Wiley interdisciplinary reviews: data mining and knowledge discovery, 1(1): 14–23.

- Lopez-Lira and Tang (2023) Lopez-Lira, A.; and Tang, Y. 2023. Can chatgpt forecast stock price movements? return predictability and large language models. arXiv preprint arXiv:2304.07619.

- Lu et al. (2023) Lu, D.; Wu, H.; Liang, J.; Xu, Y.; He, Q.; Geng, Y.; Han, M.; Xin, Y.; and Xiao, Y. 2023. Bbt-fin: Comprehensive construction of chinese financial domain pre-trained language model, corpus and benchmark. arXiv preprint arXiv:2302.09432.

- Mnih et al. (2016) Mnih, V.; Badia, A. P.; Mirza, M.; Graves, A.; Lillicrap, T.; Harley, T.; Silver, D.; and Kavukcuoglu, K. 2016. Asynchronous methods for deep reinforcement learning. In International conference on machine learning, 1928–1937. PMLR.

- Schulman et al. (2017) Schulman, J.; Wolski, F.; Dhariwal, P.; Radford, A.; and Klimov, O. 2017. Proximal policy optimization algorithms. arXiv preprint arXiv:1707.06347.

- Shah et al. (2022) Shah, R. S.; Chawla, K.; Eidnani, D.; Shah, A.; Du, W.; Chava, S.; Raman, N.; Smiley, C.; Chen, J.; and Yang, D. 2022. When FLUE Meets FLANG: Benchmarks and Large Pretrained Language Model for Financial Domain. In Proceedings of the 2022 Conference on Empirical Methods in Natural Language Processing (EMNLP). Association for Computational Linguistics.

- Shen et al. (2023) Shen, S.; Hou, L.; Zhou, Y.; Du, N.; Longpre, S.; Wei, J.; Chung, H. W.; Zoph, B.; Fedus, W.; Chen, X.; et al. 2023. Mixture-of-experts meets instruction tuning: A winning combination for large language models. arXiv preprint arXiv:2305.14705.

- Soun et al. (2022) Soun, Y.; Yoo, J.; Cho, M.; Jeon, J.; and Kang, U. 2022. Accurate stock movement prediction with self-supervised learning from sparse noisy tweets. In 2022 IEEE International Conference on Big Data (Big Data), 1691–1700. IEEE.

- Team et al. (2023) Team, G.; Anil, R.; Borgeaud, S.; Wu, Y.; Alayrac, J.-B.; Yu, J.; Soricut, R.; Schalkwyk, J.; Dai, A. M.; Hauth, A.; et al. 2023. Gemini: a family of highly capable multimodal models. arXiv preprint arXiv:2312.11805.

- Touvron et al. (2023a) Touvron, H.; Lavril, T.; Izacard, G.; Martinet, X.; Lachaux, M.-A.; Lacroix, T.; Rozière, B.; Goyal, N.; Hambro, E.; Azhar, F.; et al. 2023a. Llama: Open and efficient foundation language models. arXiv preprint arXiv:2302.13971.

- Touvron et al. (2023b) Touvron, H.; Martin, L.; Stone, K.; Albert, P.; Almahairi, A.; Babaei, Y.; Bashlykov, N.; Batra, S.; Bhargava, P.; Bhosale, S.; et al. 2023b. Llama 2: Open foundation and fine-tuned chat models. arXiv preprint arXiv:2307.09288.

- Wang et al. (2021) Wang, Z.; Huang, B.; Tu, S.; Zhang, K.; and Xu, L. 2021. DeepTrader: a deep reinforcement learning approach for risk-return balanced portfolio management with market conditions Embedding. In Proceedings of the AAAI conference on artificial intelligence, volume 35, 643–650.

- Wei et al. (2022) Wei, J.; Wang, X.; Schuurmans, D.; Bosma, M.; Xia, F.; Chi, E.; Le, Q. V.; Zhou, D.; et al. 2022. Chain-of-thought prompting elicits reasoning in large language models. Advances in neural information processing systems, 35: 24824–24837.

- Wu et al. (2018) Wu, H.; Zhang, W.; Shen, W.; and Wang, J. 2018. Hybrid deep sequential modeling for social text-driven stock prediction. In Proceedings of the 27th ACM international conference on information and knowledge management, 1627–1630.

- Wu et al. (2023) Wu, S.; Irsoy, O.; Lu, S.; Dabravolski, V.; Dredze, M.; Gehrmann, S.; Kambadur, P.; Rosenberg, D.; and Mann, G. 2023. Bloomberggpt: A large language model for finance. arXiv preprint arXiv:2303.17564.

- Xie et al. (2023) Xie, Q.; Han, W.; Zhang, X.; Lai, Y.; Peng, M.; Lopez-Lira, A.; and Huang, J. 2023. PIXIU: a large language model, instruction data and evaluation benchmark for finance. In Proceedings of the 37th International Conference on Neural Information Processing Systems, 33469–33484.

- Xu and Cohen (2018) Xu, Y.; and Cohen, S. B. 2018. Stock movement prediction from tweets and historical prices. In Proceedings of the 56th Annual Meeting of the Association for Computational Linguistics (Volume 1: Long Papers), 1970–1979.

- Yang, Liu, and Wang (2023) Yang, H.; Liu, X.-Y.; and Wang, C. D. 2023. FinGPT: Open-Source Financial Large Language Models. FinLLM Symposium at IJCAI 2023.

- Yang et al. (2020) Yang, H.; Liu, X.-Y.; Zhong, S.; and Walid, A. 2020. Deep reinforcement learning for automated stock trading: An ensemble strategy. In Proceedings of the first ACM international conference on AI in finance, 1–8.

- Yang, Tang, and Tam (2023) Yang, Y.; Tang, Y.; and Tam, K. Y. 2023. Investlm: A large language model for investment using financial domain instruction tuning. arXiv preprint arXiv:2309.13064.

- Ye et al. (2020) Ye, Y.; Pei, H.; Wang, B.; Chen, P.-Y.; Zhu, Y.; Xiao, J.; and Li, B. 2020. Reinforcement-learning based portfolio management with augmented asset movement prediction states. In Proceedings of the AAAI conference on artificial intelligence, volume 34, 1112–1119.

- Zeng et al. (2023) Zeng, Z.; Kaur, R.; Siddagangappa, S.; Rahimi, S.; Balch, T.; and Veloso, M. 2023. Financial time series forecasting using cnn and transformer. arXiv preprint arXiv:2304.04912.

- Zou et al. (2022) Zou, J.; Cao, H.; Liu, L.; Lin, Y.; Abbasnejad, E.; and Shi, J. Q. 2022. Astock: A new dataset and automated stock trading based on stock-specific news analyzing model. arXiv preprint arXiv:2206.06606.