On the Gaussian process limit of Bayesian Additive Regression Trees

Abstract

Bayesian Additive Regression Trees (BART) is a nonparametric Bayesian regression technique of rising fame. It is a sum-of-decision-trees model, and is in some sense the Bayesian version of boosting. In the limit of infinite trees, it becomes equivalent to Gaussian process (GP) regression. This limit is known but has not yet led to any useful analysis or application. For the first time, I derive and compute the exact BART prior covariance function. With it I implement the infinite trees limit of BART as GP regression. Through empirical tests, I show that this limit is worse than standard BART in a fixed configuration, but also that tuning the hyperparameters in the natural GP way yields a competitive method, although a properly tuned BART is still superior. The advantage of using a GP surrogate of BART is the analytical likelihood, which simplifies model building and sidesteps the complex BART MCMC. More generally, this study opens new ways to understand and develop BART and GP regression. The implementation of BART as GP is available in the Python package https://github.com/Gattocrucco/lsqfitgp.

1 Introduction

BART

Bayesian Additive Regression Trees (BART) is a nonparametric Bayesian regression method, introduced by [4, 5]. It defines a prior distribution over the space of functions by representing them as a sum of binary regression trees, and then specifying a stochastic tree generation process. The posterior is then obtained with Metropolis-Gibbs sampling over the trees. See [17] for a review and [7, ch. 5] for a textbook treatment.

BART’s success

BART has proven empirically effective, and is gaining popularity in multiple fields [42, consider, e.g.,]. As a single illustrative example, I consider its application in causal inference, where it was introduced by [16]. In this context, BART is used for response surface methods, i.e., nonparametric modeling of the potential outcome conditional on the covariates in each treatment group. The Atlantic Causal Inference Conference (ACIC) data challenge has confirmed BART as one of the best methods [8, 13, 12, 44], in particular to infer heterogeneity in causal effects by subgroup. In causal inference, nonparametric models are useful because the quantity of interest is the (counterfactual) difference in some outcome variable between two (or more) treatment conditions, not the specific shape of the relationship linking covariates to outcome. In observational studies, i.e., without randomized assignment to treatment, strong unjustified functional assumptions, e.g., linear regression, can severely bias the effect estimate [22, §14.7, p. 332].

BART vs. Gaussian processes

Another general method for response surface modeling is Gaussian process (GP) regression (see [11] for a textbook treatment and [29] for its application in causal inference), which uses as prior distribution a Gaussian process, i.e., a multivariate Normal on the unknown function values. This allows to write analytically the posterior as a linear algebra calculation, conditional on some free parameters of the covariance function, which may be more convenient compared to the Markov chain Monte Carlo (MCMC) of BART.

The main disadvantage of GP regression is that in general the computational complexity is a hefty , with the number of datapoints, the number of predictors, and the number of free covariance function parameters; this can be alleviated with scaling techniques [11, ch. 9], but not in full generality. With fixed number of MCMC samples and number of trees, BART is instead [17, although these assumptions are too strong in practice, see].

BART and GP regression are also considered different in their statistical features and performance. Typically GP regression is presented as less flexible than BART [23, see, e.g.,]. However, the BART prior distribution is defined by summing i.i.d. regression trees. Due to the central limit theorem, this implies that, as , the BART prior becomes Normal, and thus BART becomes equivalent to GP regression, with a specific covariance function [28, th. 1]. [5, §2.2.5, p. 273] observe empirically that, starting from , the predictive performance drastically increases with , until a value of in the hundredths, and then decreases again but very slowly; but they do not investigate the asymptotic behaviour.

Thus, at the same time, there is an indicative argument that BART should be similar to a GP, but also reported experience that BART and GPs are in practice pretty different. This seeming contradiction is best exemplified in [28, §5.2, p. 554], who states that the BART prior covariance function can be approximated by the Laplace kernel

| (1) |

and that GP regression with this kernel is typically worse than BART. [28] then hypothesizes that the reason behind this performance gap is the BART prior with a finite number of trees being more flexible than a GP prior, thus allowing BART to better adapt to the data.

However, there could be another source for the discrepancy he observed: the Laplace kernel is only a loose approximation of the actual covariance function of BART. The present work starts from the following questions: how does BART compare with its infinite trees GP limit, taking care to compute precisely its prior covariance function? And would there be any advantages in using the GP limit in place of BART?

Summary of the results

In section 2.3, I provide the first explicit expression of the BART prior covariance function, and in section 3 a way to compute it with sufficient efficiency and accuracy to be used in practice for GP regression. In section 4 I run GP regressions with this covariance function, both on real (section 4.1) and synthetic (section 4.2) data, comparing it against standard BART. This shows that the infinite trees limit of a given BART model is on average worse than the finite trees case. However, I also find that in practice, using the GP limit of BART for its own sake, without hewing to a strict limit of a fixed BART configuration, produces a method which is competitive with BART. This is interesting for applications because a GP formulation makes model extension and combination easier, and removes occasional MCMC headaches.

2 Theory

Sections 2.1 and 2.2 recap BART and GP regression. Section 2.3 presents the exact covariance function of BART derived here.

2.1 The BART prior

BART, as a complete regression method, is the combination a prior distribution over a space of regression functions, represented as an ensemble of decision trees, and a dedicated MCMC algorithm to sample from the posterior. My interest here lies mostly in the definition of the prior distribution, which I recap following the notation of [5].

Decision trees

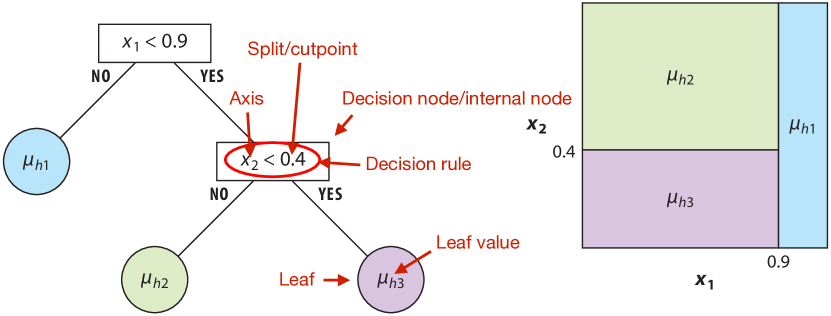

A decision tree is a way to represent a stepwise function using a binary tree. Each non-leaf node contains a decision rule defined by a splitting axis and a splitting point , partitioning the input space in two half-spaces along the plane , orthogonal to axis . Each half is assigned to a children. Children nodes in turn further divide their space amongst their own children. Leaf nodes contain the constant function value to be associated to their whole assigned rectangular subregion. A minimal tree consisting of a single root leaf node represents a flat function. See Figure 1 for an illustration.

Decision trees for regression

A decision tree can be used to represent a parametrized family of functions for regression. The parameters are the tree structure , including decision rules, and the leaf values . I indicate the function represented by the tree with . To use this model in Bayesian inference, it is necessary to specify a prior distribution over . I factorize the prior as and specify the two parts separately.

Prior over tree structure

The distribution is defined by the following recursive generative model [3, see]. Fix an axes-aligned grid in the input space, not necessarily evenly spaced, by specifying a set of cutpoints for each axis . Start generating the tree from the root, descending as nodes are added. At each new node, consider the subset of cutpoints which are available in its assigned subregion along each axis, and keep only the axes with at least one split available. If there are none, the node is a leaf. If there are any, decide with probability if the node is nonterminal, i.e., if it should have children, where is the depth of the node, at the root, and and are two fixed hyperparameters. If the node is nonterminal, its splitting axis is drawn from the allowed ones with a categorical distribution (typically uniform), and the cutpoint along the chosen axis is drawn uniformly at random from the available ones.

Prior over leaf values

If a node terminates, its leaf function value is sampled from a Normal distribution with mean and standard deviation , independently of other leaves. This defines .

Complete regression model

The BART regression model uses a sum of independent trees, each with the prior above:

| (2) |

Hyperparameters

The free hyperparameters in the model, to be chosen by the user, are:

-

•

The splitting grid. The two common defaults are 100 equally spaced splits along each axis in the range of the data, or a split midway between each observed value along each axis.

-

•

The number of trees , default 200. This should grow with the sample size, but there is no known precise scaling.

-

•

and , regulating the depth distribution of the trees. Default 0.95 and 2.

-

•

and , which set the prior mean and variance and of . By default set based on some measure of the location and scale of the data.

-

•

and , which regulate the prior on the variance of the error term. By default , while is set to some measure of squared scale of the data.

2.2 Gaussian process regression

Definition of Gaussian process

A stochastic process is a Gaussian process if all its finite marginals are multivariate Normals. In symbols:

| (3) |

The functions and are respectively called mean function and covariance function or kernel. The domain is an arbitrary index space . If , the kernel regulates the continuity and smoothness of the process in the mean-square sense, its correlation length, and its long-range memory.

Bayesian inference with Gaussian processes

Bayesian Gaussian process regression takes advantage of the fact that the marginals are Normal, and easily computable from and , to produce a posterior distribution given observed values of the process and a Gaussian process prior over it. Following the notation of [38], let be the observed function values, and the unknown function values to infer. With the joint distribution written as

| (4) | ||||

| the posterior on is | ||||

| (5) | ||||

where is any 1-inverse of , i.e., a matrix that satisfies . In particular, the Moore-Penrose pseudoinverse is a valid choice, and if the matrix is invertible. The posterior covariance matrix is a generalized Schur complement, indicated with . For the proof of the conditioning formula see [40, ex. 7.4, p. 295]; for the general properties of the multivariate Normal, see [45].

In the typical application there are independent Normal error terms between the latent function and the data. Since Normal distributions can be summed, the error term is absorbed into the definition of the Gaussian process.

Hyperparameters

If mean and covariance function depend on additional hyperparameters , the distribution can be set up as a hierarchical model with a marginal prior for and the Gaussian process being the conditional distribution given . The posterior density on is then given by

| (6) | ||||

| while the posterior on becomes | ||||

| (7) | ||||

with the conditional posterior given by Equation 5.

It is common practice to find a single “optimal” value of , e.g., its marginal maximum a posteriori (MAP). This is convenient, but often substantially deteriorates the quality of the predictive posterior distribution, shrinking its variance [32, e.g.,]. If the hyperparameters carry some meaning in the model, and inference about them is sought, a Laplace approximation of the posterior is usually inadequate, but may be sufficient for the predictive posterior.

In principle it is possible to use Gaussian process regression with all hyperparameters fixed a priori. This however is a bad idea in most circumstances, because a single multivariate Normal distribution is too “rigid” for almost all prediction tasks.

Computational speed aspects

The typical bottlenecks are, at each step of the iterative algorithm that maximizes or samples the posterior for in Equation 6, computing the decomposition of the prior covariance matrix and computing the gradient of the log-determinant term in the log-likelihood. Their computational complexities are respectively and where and are the dimensionalities of and . As a reference, on my personal machine with and 64 bit floating point, the matrix occupies of RAM, the Cholesky decomposition takes , and diagonalization takes . Due to the quadratic memory and cubic time scaling, it is challenging to significantly increase and even with larger computers. Thus one of the drawbacks of GP regression is that in general it does not scale to large datasets.

2.3 The BART prior correlation function

Since BART defines a prior over functions, it has a prior covariance function, like Gaussian processes. Using the notation of Equation 2 for and section 2.2 for :

| (8) |

For convenience, from here onwards I fix the variance to 1, or, in other words, I work with the correlation function instead of the covariance function.

The BART correlation function is equal to the probability that the two points end up in the same tree leaf under the generative definition of the prior [28, §5.2]:

| (9) |

Previous literature provided expressions for this \autocites[th. 4.1]oreilly2022[prop. 1]linero2017[prop. 1]balog2016, but making simplyfing assumptions to ease analytical computability. The following theorem provides the first exact derivation of the BART correlation function:

Theorem 1.

The BART prior correlation function of the latent regression function is given recursively by

| (10) | ||||

| (11) | ||||

| (12) | ||||

| (13) | ||||

| (14) | ||||

| (15) |

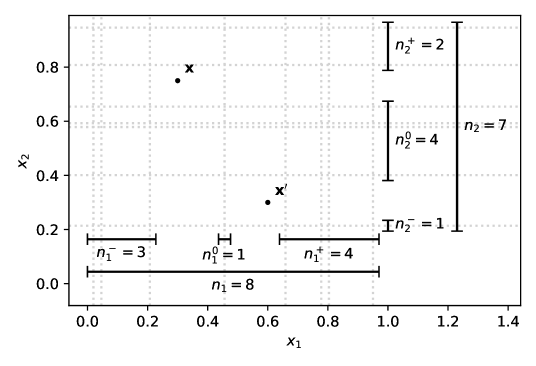

where , , and are, respectively, the number of splitting points below, between, and above the predictors vectors and , counted separately along each covariate dimension (see Figure 2),

while are the (unnormalized) selection probabilities for the predictor axes. All predictors with shall be excluded beforehand.

Proof.

See section A.1. ∎

For completeness I also considered the case , but in the following I will always assume . Note that the vectors appearing in recursive evaluations of the function are different from the ones initially obtained from and , due to the modifications indicated by the subscripts and . I consider arbitrary axis weights , but where not specified otherwise, in numerical experiments I will set .

The number of trees never appears in Theorem 1: the prior distribution changes with , but its covariance function stays the same.

In the following, I always work with the recursive function , representing the “sub-correlation function” of a subtree at depth , instead of the final correlation function . All the results apply to by considering that . I also manipulate directly without involving and , so the results apply to any valid sequence of probabilities . The next theorem formally characterizes the properties of that reflect corresponding properties of the prior:

Theorem 2.

The BART sub-correlation function defined in Theorem 1 has the following properties:

-

1.

.

-

2.

Assuming , then .

-

3.

, in particular .

-

4.

Assuming , then .

-

5.

Assuming and , then ; the conditions on and are satisfied for any if and .

-

6.

Given and , then .

-

7.

Given , then .

-

8.

If (satisfied by ), and , then

-

9.

If , which occurs if and , then

Proof.

See section A.2. ∎

Property 1 is just the fact that a function value is totally correlated with itself. Properties 2 and 3 reflect that BART has a random intercept term with prior variance due to the possibility of the trees not growing at all. Property 4 says that any degree of separation (w.r.t. the grid) allows the function values to differ, and property 5 that, apart from degenerate cases, the lower bound can be reached only by maximally separated points, i.e., points that sit at completely opposite corners of the splitting grid hypercube envelope. Properties 6 and 7 mean that the correlation monotonically decreases as points get farther along each axis.

Properties 8 and 9 show two opposite limiting cases of BART. For , the trees can at most reach depth 1, so each tree can split at most on one predictor. This means that the regression function has no interactions, in the usual sense that it can be written as a sum of functions each acting only on one predictor, property which is reflected by the correlation function. Instead, if and , the trees continue growing until exhausting all the available splits, so the process becomes white noise (in grid space). Notice that in the case the process is stationary (in grid space) because it depends only on the distance between the two points.

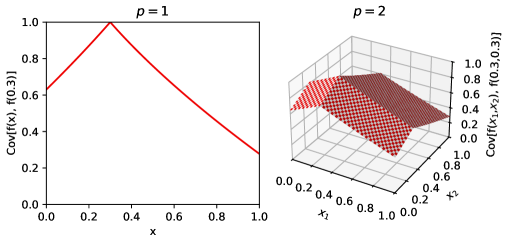

Figure 3 shows the correlation function with the default values of the hyperparameters given by [5]. It’s interesting to note how close the function is to the no-interaction limit of property 8: the profile is almost straight. That small amount of curvature makes the difference between a regression without interactions and a rich model like BART. This is an instance of the general observation that it is difficult to infer the properties of a stochastic process by visually looking at its correlation function, and that small numerical differences in correlation can correspond to large qualitative differences in inference.

3 Computation of the BART prior correlation function

Computing exactly the BART prior correlation following Equation 12 amounts, in words, to walking recursively through all possible trees, calculating the probability of each, and checking whether it puts the two points in different leaves. Albeit finite, the number of possible trees is huge, making the computation unfeasible.

Analogously to the previous literature, I make simplifying assumptions that allow to compute an approximation. However, I hew close to the exact BART specification, deriving a proper approximation method that gives guaranteed bounds and converts additional computational power in arbitrary accuracy. In particular, I take these steps:

-

1.

Limit the maximum depth of the trees (section 3.1).

-

2.

Instead of just an estimate, get an upper and a lower bound on the exact result by putting either an upper or a lower bound in the truncated leaves in place of the subtree computation. These bounds are themselves valid (i.e., positive semi-definite) covariance functions (section 3.1).

-

3.

“Collapse” the recursion at various depths to reduce the combinatorial explosion, in a way which again preserves positive semi-definiteness and bounding properties (section 3.2).

-

4.

Compute two steps of the recursion analytically in closed form instead of actually branching, to get two tree levels “for free” (section 3.4).

-

5.

Use slow-to-compute bounds to measure empirically the accuracy of a more approximate fast-to-compute estimate (section 3.5).

I now describe in detail each of these in turn.

3.1 Truncated correlation function

As first step in constructing a computationally tractable approximation to the sub-correlation function (defined in Theorem 1), I truncate the trees at depth , i.e., stop the recursion after steps. The BART prior is designed to favor shallow trees, and the well-functioning of its MCMC scheme relies on the trees being shallow, so this should give a good approximation.

By property 3, Theorem 2, , so I stop the recursion by replacing the term with , , an interpolation between the lower and upper bounds. I handle separately the case, since I want the function to represent a correlation function, which must yield 1 in that case.

Definition 1.

The truncated sub-correlation function , with , is defined recursively as

| (16) | ||||

| (17) | ||||

| (18) | ||||

| (19) |

The following theorems show that can be used to approximate or place bounds on , with accuracy and computational cost that increase with . Intuitively, the truncation of the recursion corresponds to a variant of the BART model with a limit on the depth of the trees, so shares the qualitative properties of , and is practically equivalent at high . See section A.3 for the proofs.

Theorem 3.

As is varied in , linearly interpolates between a lower and upper bound on .

Theorem 4.

The bounding interval by truncation to is contained in the one with , i.e., .

Theorem 5.

is a valid correlation function, and the properties of Theorem 2 hold for as well, apart when referring to a level deeper than .

3.2 Pseudo-recursive truncated correlation function

Due to the recursive iteration over all possible decision rules, the calculation of is exponential in with a high base, so it is still unfeasible but for the lowest . As a further step in making the approximation faster to compute, I modify the recursion to “restart” at various levels: at some pre-defined depths, the arguments to the recursive invocation of the function are set to the initial arguments, instead of the modified values handed down by preceding levels.

Computationally, this allows to share the same function value across branches of the recursion, effectively limiting the combinatorial growth to the depth spans without resets. It also allows to share terms between different levels, although the utility of this is not evident at this point of the exposition.

Definition 2.

The pseudo-recursive truncated sub-correlation function , with and , is defined as , but in the recursion the functions are evaluated at the initial arguments determined using the full splitting grid, instead of the restricted ones handed down by the recursion:

| (20) | ||||

| (21) | ||||

| (22) | ||||

| (23) | ||||

| (24) |

For convenience, I define the shorthand

| (25) |

This corresponds to a modification of the BART model in which at the reset depths the decision rules are not bound to be consistent with the decision rules of ancestor nodes [28, which was already used more extensively in], so the result is still a valid correlation function with the same qualitative properties, as formally stated in the next theorem.

Theorem 6.

is a valid correlation function.

The following theorems show that improves on as upper bound on . Unfortunately, is not a lower bound, because resetting the set of possible decision rules tends to increase the correlation, as the presence of logically empty leaves reduces the total effective number of leaves and thus also the probability of separating any two points.

Theorem 7.

is an upper bound on .

Theorem 8.

if , in particular and .

For the proofs, see section A.4.

3.3 Special-casing of one recursion level

Since the recursion step (Equations 12, 19, 24) is arithmetically simple, expanding the recursion (i.e., plugging the recursive definition within itself one or more times) and simplifying the resulting expression looks promising as a way to make the calculation faster.

For starters, I plug the base case into the recursive step: if , (Definition 1) reduces to

| (26) | ||||

| (27) |

It is worthwhile to look at the bounds given by in this case:

| (28) |

First, note that the upper bound in Equation 28 is equal to the case of property 8, Theorem 2. This means that the no-interactions limit of BART is an upper bound on the general correlation function. Second, consider the width of the interval:

| (29) |

where I defined . The term is proportional to how close the two points are. This suggests that the maximum estimation error in using as approximation of is low for correlations between faraway points and is maximum for almost overlapping points.

Usage with the pseudo-recursion

With , I am considering an expansion only at the bottom level of the recursion. However, in the pseudo-recursive function (Definition 2), it is possible to use this expansion at all intermediate reset levels . To see this, consider that in Equation 24, if , the terms of the inner summations are all identical, and so can be collected exactly like in Equation 26.

3.4 Special-casing of two recursion levels

The recursive step (Equation 12) has two stacked summations, one along predictors and one along the cutpoints. With the convention of placing cutpoints between observed predictor values, the cost of the operation (taking the subsequent levels as given) is . In GP regression, the correlation function is invoked to compute each entry of the covariance matrix, for a total cost of . This complexity is prohibitive because it’s higher than the already expensive bottleneck (see section 2.2). Thus I need to not use the recursion step even once.

The one-level expansion (Equation 26) is a sum that separates predictors, so it represents a model without interactions. This is probably too rigid as approximation, even if stacked with the pseudo-recursion as . So I want to “compress” at least two recursion levels, expanding the recursion step within itself and simplifying until I get an expression. Fortunately, this is possible, as stated in the next theorem.

Theorem 9.

admits the following non-recursive expression:

| (30) | ||||

| (31) | ||||

| where | ||||

| (32) | ||||

| (33) | ||||

| (34) | ||||

and is the digamma function [34, §5.15].

Proof.

See section A.5. ∎

Like the one-level expansion of the previous section, this two-level expansion can be used at all reset depths in the pseudo-recursive version, allowing to compute without actual recursions.

Computational optimizations

Even if Equation 31 is , in practice the computation time of the expression as written is too high because of its sheer length and the usage of a special function. A lot can be gained by carefully re-arranging the operations. The formula is typically applied to compute a covariance matrix, so there is a list of points and the formula is evaluated at all possible pairs . I state the following without proof: even though the calculation is overall , the terms that involve only one of or instead of both require only , and those that involve neither or ; by re-arranging the expression and re-writing it in terms of instead of , only a small number of terms actually require , and they are simple operations. This kind of optimizations is common in GP regression [10, see, e.g.,].

3.5 Final choice of estimate and its accuracy

Putting together the results of the previous sections, I have that and are efficiently computable lower and upper bounds on , and are themselves valid (p.s.d.) correlation functions.

To get a single estimate of the correlation function, I could set a constant interpolation coefficient to pick a value within the bounds. However, some numerical tests show that the upper bound is already pretty close to the true value, and that is sufficient to get most of the gain from increasing , so to make the computation faster and simpler, I decide to use directly as estimate.

To measure the accuracy of as estimate of , in Appendix B I compute narrow bounding intervals at high depth (spending a lot of computation) on a range of values of hyperparameters, split configurations, and pairs of points, and compare it with the estimate to determine a maximum error. The result is that the correlation thus computed is accurate to 0.007 with predictors, and to 0.0005 with , relatively to the interval , at the default BART hyperparameters , . These figures are not proven bounds, because of the many arbitrary choices in this empirical verification.

Numerical cross checks

There are various error-prone parts in the calculation of the correlation function, in particular all the arbitrary details of the BART model (section 2.1) and the cumbersome calculation of the two-level expansion (Theorem 9). To make the results dependable, I want to be confident there is not even one mistake, not in the math nor in the implementation. I assure this in two ways. First, I check many self-consistency properties of the correlation function that do not need an oracle reference value, like the properties in Theorem 2. Second, I sample from the BART prior by explicitly generating the trees, compute the sample covariance matrix, and compare it with my covariance function. All these tests work out fine, see Appendix C for the details.

4 GP regression with the BART kernel

Due to the splitting grid in predictor space being finite, the BART prior over the sum of trees is effectively a distribution over a finite-dimensional vector, where each component is the value of the regression function in one cell of the grid. The regression function is a sum of a priori i.i.d. terms, one per tree. Then, due to the multivariate CLT [46, 16], as the number of trees tends to infinity, the prior converges to a multivariate Normal distribution, and so regression with the BART model becomes equivalent to GP regression.

Using the efficiently computable approximation of the BART prior correlation function derived in the previous section, I can implement BART with an infinite number of trees as a GP regression. This is interesting both as an exploration of the BART model, and as a potential surrogate to use in place of BART.

In section 4.1, I compare the predictive performance of BART against the one of its infinite trees limit, in various configurations. In section 4.2, I use the GP surrogate to replace the BART components of BCF, a causal inference model, and compare its accuracy at inferring an average causal effect against other competitors in a simulated data competition.

4.1 Out-of-sample predictive accuracy on real data

I take the 42 datasets of the original BART article [5, 26], and compare the predictions of various regression methods on held-out test sets, with 20 random 5:1 train/test splits for each dataset. The dataset sizes range approximately from to , and the number of features from to (with dummies).

The regression methods I consider are:

-

•

MCMC: standard BART.

-

•

MCMC-CV: BART cross-validated as in [5], tuning parameters , , , .

-

•

MCMC-XCV: BART cross-validated with the pre-packaged routine xbart provided by dbarts [9], tuning parameters , , .

-

•

GP: the infinite trees limit of MCMC as GP regression.

-

•

GP-hyp: like GP but tuning the parameters , , .

-

•

GP+MCMC: standard BART with parameters set to those found by GP-hyp.

I take care to set up MCMC and GP such that GP is the infinite trees limit of MCMC, with all other model details identical. I also make an effort to accurately reproduce the benchmark in [5] with MCMC-CV. For the other methods, I take more freedom in the configuration to obtain good performance in various ways.

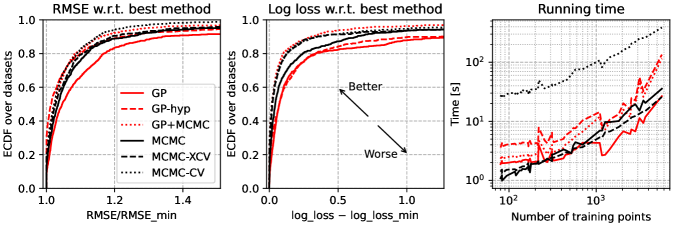

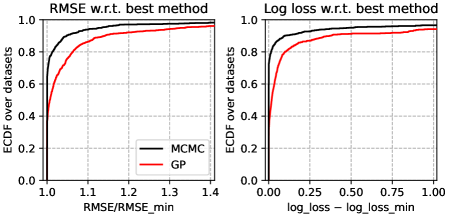

I compare the methods by looking at the distribution across datasets of RMSE and log-loss for each method, shown in Figure 4. Compared to the RMSE, the log-loss is a more stringent metric that takes into account not just the central value but the complete joint distribution of the predictions, weighing together inaccuracy, overconfidence, underconfidence, and mismatch of the correlational structure.

I interpret the results as follows:

-

•

MCMC is better than GP, so the infinite trees limit of BART, without other modifications, is worse than the original. This is loosely in line with what reported in [28, §5.2, p. 554] (that used a looser approximation of the kernel), and with the analogous result for the GP limit of wide Neural networks [1, §5].

-

•

GP-hyp is overall almost as good as MCMC. This is a fairer comparison in some sense, as tuning GP hyperparameters is standard practice. In the BART vs. GP discussion in [14, 1052], they observe that choosing the right kernel in GP regression is important, that BART is a complex mixture of Gaussian processes, and that BART empirically seems to do better than GP by adapting to the data covariance structure. (In this optic, BART is already a GP regression, but with a huge number of hyperparameters.) This result suggests that tuning a few hyperparameters with the right kernel may be sufficient to make a simple GP as flexible as BART.

-

•

The top performers are MCMC-CV and GP+MCMC. It is known that tuning the hyperparameters improves BART \autocites[fig. 2]chipman2010[18]imai2022[445]imai2013[§5.4 p. 55, §6.2 p. 58]dorie2019. Interestingly, these two methods tune different hyperparameters and in a different way.

-

•

If I also take into account convenience, I consider MCMC-XCV the winner, as it runs fast and mostly works out of the box with little configuration, but achieves a good log-loss profile.

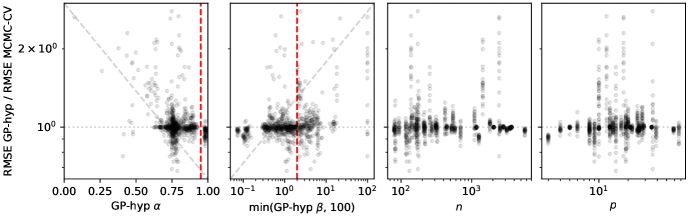

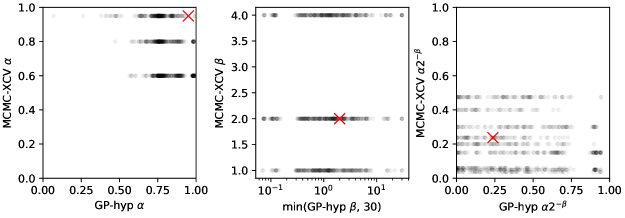

Further investigations (see section D.5) show that GP-hyp seems to be taking advantage of tuning and , the parameters that regulate the depth of the trees, employing a wide span of settings which go from depth one (no interactions) to very deep trees. This suggests that standard BART might benefit from a similar extreme exploration of tree depth settings, although it’s not granted that the behavior should transfer over. MCMC-XCV tunes those parameters as well, in a more limited fashion, but surprisingly there is no relationship at all between the values chosen by the two methods. I also find GP-hyp does worse, with MCMC-CV as reference, on low noise datasets where accurate predictions are possible, and better on noisy ones.

Overall the GP-based methods are slower than BART, taking MCMC-XCV as the BART champion. Apart from scaling worse with sample size, which is an (in this context) inherent limit of GP regression, they are also slower at low sample size. Detailed timings of my code indicate that the bottleneck of these GP regressions is evaluating the kernel (and its derivatives w.r.t. hyperparameters) to compute the prior covariance matrix, which has complexity . This is not the most common bottleneck of GP regression, it is caused by my kernel being inordinately sophisticated.

See Appendix D for the complete details of the models and of the analysis.

4.2 Inferential accuracy on synthetic data

I build a GP version of Bayesian Causal Forests (BCF) [14], replacing its two BART components with GP regression with the BART kernel. BCF is a BART-based method taylored to causal inference problems, in the basic observational setting where a causal effect is estimated by adjusting for deconfounding covariates via regressions and .

I test this method on the pre-made synthetic datasets of the Atlantic Causal Inference Conference (ACIC) 2022 Data Challenge [44]. I use the datasets of a competition, instead of generating them myself, because I expect them to be better that what I would make, and because I can immediately compare my method against the many participants. The goal of the competition is estimating average causal effects, both grand and within subgroups, in longitudinal data with the treatment active from a certain time onwards. The study is not randomized, but the provided covariates are guaranteed to be sufficient for adjustment.

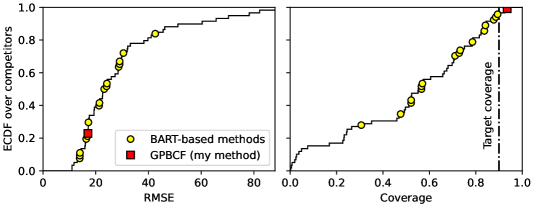

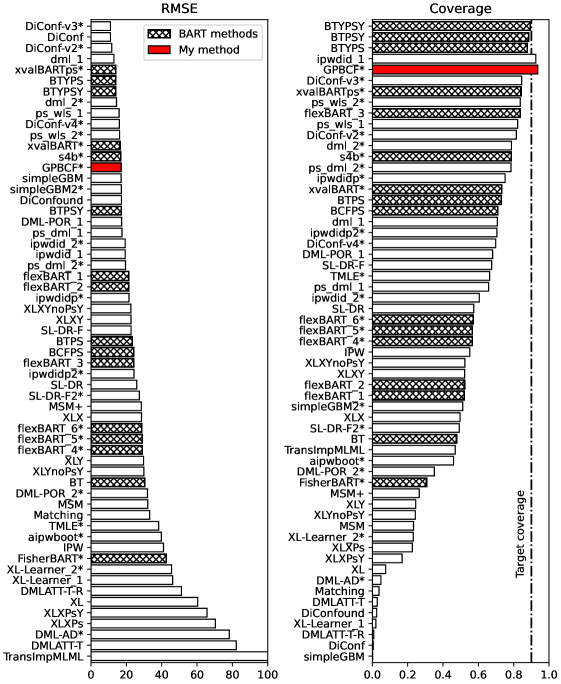

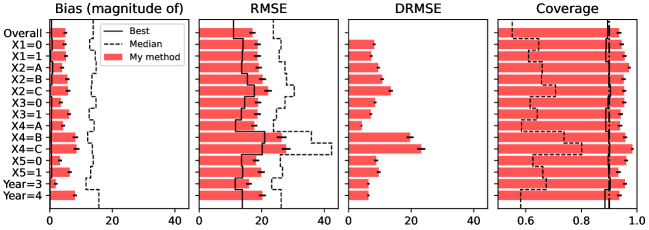

The results are summarized in Figure 5.

The complete details are in Appendix E. Overall, my GPBCF method performs in line with the other BART-based methods, including standard BCF, providing evidence that in practice the infinite trees limit of BART is a functional regression method.

In particular, GPBCF excels in having coverage close to the target confidence level, and overcovering instead of undercovering like almost all other competitors. This is probably due to the fact that I take into account the uncertainty over the hyperparameters by sampling their posterior distribution. This is made easy by the GP formulation: I find the mode with BFGS and do a simple Laplace approximation. The running time of the whole procedure is about 1 minute with 1000 datapoints.

5 Conclusions

Results

I provide the first calculation of the prior covariance function of BART. With it, I show empirically that the infinite trees Gaussian process limit of BART is not as statistically performant as the standard finite-trees BART, in line with what was expected from the literature and with the analogous result for the GP limit of Neural networks. However, if I forsake carrying out a strict limit of the BART model, and instead tune the GP limit with standard GP methodology, I get a method with similar performance. BART is still overall superior.

Applications

My GP limit of BART can be used right away in place of BART. My Python module for GP regression, lsqfitgp [37], provides packaged BART-like and BCF-like GP regression routines, and a function to compute the prior covariance matrix and its derivatives for arbitrary usage. The GP version of BCF is potentially the most useful as standard BCF uses a Gibbs sampler on two BART components that reportedly can get stuck.

Pro

The general advantage of the GP version is having an analytical likelihood function. This simplifies extending the model arbitrarily, and allows to do away with the MCMC, making the computation more reliable and hyperparameter tuning easier.

Con

A disadvantage is that GP regression does not scale to large datasets, and in this particular case the bottleneck of the computation is the evaluation of the kernel, so existing agnostic techniques that accelerate the covariance matrix decomposition do not help, while approximate techniques would probably reduce the statistical performance. This also applies to the number of predictors , as the kernel calculation unconditionally involves all predictors, while the MCMC uses a stable number of predictors per cycle. Another disadvantage is that the predictive performance that can be obtained from standard BART is on average higher.

Extensions

There are many straightforward further developments of this work, e.g., making the GP versions of BART variants, or scaling the inference to large datasets. However, I think the most interesting result is not the specific method I obtained, but showing in general that BART—a method considered to be of a different kind than Gaussian processes, with different use cases—is instead in a practical sense similar to an appropriate GP regression. This suggests to me that the important matters to investigate are:

-

•

Whether the BART prior, ostensibly a complex Normal mixture, is actually well approximated by a simple Normal mixture; and if so, if this can be changed to improve BART.

-

•

Developing new GP kernels in general: if it’s possible to almost match BART with the constraint of using its own limit kernel with just three free hyperparameters, it should be possible to surpass it.

Acknowledgements

I thank Hugh Chipman for providing the data files used in [5]; and Antonio Linero, Fabrizia Mealli, Alessandra Mattei, Joseph Antonelli, Jared Murray and Francesco Stingo for useful comments and suggestions. I used the following open-source scientific software: Numpy [15], Scipy [47], Matplotlib [19]. I did this work as a PhD candidate at the Department of Statistics, Computer Science, Applications (DISIA) “G. Parenti” of the University of Florence (UNIFI), Italy, and as a visiting researcher at the Department of Statistics and Data Science (SDS) of the University of Texas at Austin (UT Austin), USA.

References

- [1] Sanjeev Arora et al. “On Exact Computation with an Infinitely Wide Neural Net” In Advances in Neural Information Processing Systems 32 Curran Associates, Inc., 2019 URL: https://proceedings.neurips.cc/paper/2019/hash/dbc4d84bfcfe2284ba11beffb853a8c4-Abstract.html

- [2] Matej Balog et al. “The Mondrian Kernel” In 32nd Conference on Uncertainty in Artificial Intelligence (UAI), 2016 URL: https://www.auai.org/uai2016/proceedings/papers/236.pdf

- [3] Hugh A. Chipman, Edward I. George and Robert E. McCulloch “Bayesian CART Model Search” In Journal of the American Statistical Association 93.443 Taylor & Francis, 1998, pp. 935–948 DOI: 10.1080/01621459.1998.10473750

- [4] Hugh A. Chipman, Edward I. George and Robert E. McCulloch “Bayesian Ensemble Learning” In Advances in Neural Information Processing Systems 19 MIT Press, 2006, pp. 265–272 URL: https://proceedings.neurips.cc/paper/2006/hash/1706f191d760c78dfcec5012e43b6714-Abstract.html

- [5] Hugh A. Chipman, Edward I. George and Robert E. McCulloch “BART: Bayesian additive regression trees” In The Annals of Applied Statistics 4.1 Institute of Mathematical Statistics, 2010, pp. 266–298 DOI: 10.1214/09-AOAS285

- [6] Hugh A. Chipman and Robert McCulloch “BayesTree: Bayesian Additive Regression Trees”, 2024 URL: https://cran.r-project.org/package=BayesTree

- [7] Michael J. Daniels, Antonio R. Linero and Jason Roy “Bayesian Nonparametrics for Causal Inference and Missing Data” ChapmanHall/CRC, 2023 DOI: 10.1201/9780429324222

- [8] Vincent Dorie et al. “Automated versus Do-It-Yourself Methods for Causal Inference: Lessons Learned from a Data Analysis Competition” In Statistical Science 34.1 Institute of Mathematical Statistics, 2019, pp. 43–68 DOI: 10.1214/18-STS667

- [9] Vincent Dorie et al. “dbarts: Discrete Bayesian Additive Regression Trees Sampler”, 2024 URL: https://CRAN.R-project.org/package=dbarts

- [10] Ethan N. Epperly, Joel A. Tropp and Robert J. Webber “Embrace rejection: Kernel matrix approximation by accelerated randomly pivoted Cholesky”, 2024 arXiv: https://arxiv.org/abs/2410.03969

- [11] Robert B. Gramacy “Surrogates: Gaussian Process Modeling, Design, and Optimization for the Applied Sciences” New York: ChapmanHall/CRC, 2020, pp. 560 DOI: 10.1201/9780367815493

- [12] Susan Gruber, Geneviève Lefebvre, Tibor Schuster and Alexandre Piché “Atlantic Causal Inference Conference 2019 Data Challenge”, 2019 Atlantic Causal Inference Conference URL: https://sites.google.com/view/ACIC2019DataChallenge

- [13] P. Hahn, Vincent Dorie and Jared S. Murray “Atlantic Causal Inference Conference (ACIC) Data Analysis Challenge 2017”, 2019 arXiv: https://arxiv.org/abs/1905.09515

- [14] P. Hahn, Jared S. Murray and Carlos M. Carvalho “Bayesian Regression Tree Models for Causal Inference: Regularization, Confounding, and Heterogeneous Effects (with Discussion)” In Bayesian Analysis 15.3 International Society for Bayesian Analysis, 2020, pp. 965–2020 DOI: 10.1214/19-BA1195

- [15] Charles R. Harris et al. “Array programming with NumPy” In Nature 585.7825 Springer ScienceBusiness Media LLC, 2020, pp. 357–362 DOI: 10.1038/s41586-020-2649-2

- [16] Jennifer L. Hill “Bayesian Nonparametric Modeling for Causal Inference” In Journal of Computational and Graphical Statistics 20.1 Taylor & Francis, 2011, pp. 217–240 DOI: 10.1198/jcgs.2010.08162

- [17] Jennifer L. Hill, Antonio R. Linero and Jared Murray “Bayesian Additive Regression Trees: A Review and Look Forward” In Annual Review of Statistics and Its Application 7.Volume 7, 2020 Annual Reviews, 2020, pp. 251–278 DOI: https://doi.org/10.1146/annurev-statistics-031219-041110

- [18] Shunsuke Horii and Yoichi Chikahara “Uncertainty Quantification in Heterogeneous Treatment Effect Estimation with Gaussian-Process-Based Partially Linear Model” In Proceedings of the AAAI Conference on Artificial Intelligence 38.18, 2024, pp. 20420–20429 DOI: 10.1609/aaai.v38i18.30025

- [19] J.. Hunter “Matplotlib: A 2D graphics environment” In Computing in Science & Engineering 9.3 IEEE COMPUTER SOC, 2007, pp. 90–95 DOI: 10.1109/MCSE.2007.55

- [20] Kosuke Imai and Michael Lingzhi Li “Statistical Inference for Heterogeneous Treatment Effects Discovered by Generic Machine Learning in Randomized Experiments” arXiv, 2022 DOI: 10.48550/ARXIV.2203.14511

- [21] Kosuke Imai and Marc Ratkovic “Estimating treatment effect heterogeneity in randomized program evaluation” In The Annals of Applied Statistics 7.1 Institute of Mathematical Statistics, 2013, pp. 443–470 DOI: 10.1214/12-AOAS593

- [22] Guido W. Imbens and Donald B. Rubin “Causal Inference for Statistics, Social, and Biomedical Sciences: An Introduction” Cambridge University Press, 2015 DOI: 10.1017/CBO9781139025751

- [23] Seonghyun Jeong and Veronika Rockova “The Art of BART: Minimax Optimality over Nonhomogeneous Smoothness in High Dimension” In Journal of Machine Learning Research 24.337, 2023, pp. 1–65 URL: http://jmlr.org/papers/v24/22-0382.html

- [24] Adam Kapelner and Justin Bleich “bartMachine: Machine Learning with Bayesian Additive Regression Trees” In Journal of Statistical Software 70.4, 2016, pp. 1–40 DOI: 10.18637/jss.v070.i04

- [25] Adam Kapelner and Justin Bleich “bartMachine: Bayesian Additive Regression Trees”, 2023 URL: https://cran.r-project.org/package=bartMachine

- [26] Hyunjoong Kim, Wei-Yin Loh, Yu-Shan Shih and Probal Chaudhuri “Visualizable and interpretable regression models with good prediction power” In IIE Transactions 39.6 Taylor & Francis, 2007, pp. 565–579 DOI: 10.1080/07408170600897502

- [27] A.. Kinderman and J.. Monahan “Computer Generation of Random Variables Using the Ratio of Uniform Deviates” In ACM Trans. Math. Softw. 3.3 New York, NY, USA: Association for Computing Machinery, 1977, pp. 257–260 DOI: 10.1145/355744.355750

- [28] Antonio R. Linero “A review of tree-based Bayesian methods” In Communications for Statistical Applications and Methods 24.6, 2017, pp. 543–559 DOI: 10.29220/csam.2017.24.6.543

- [29] Antonio R. Linero and Joseph L. Antonelli “The how and why of Bayesian nonparametric causal inference” In WIREs Computational Statistics, 2022, pp. e1583 DOI: 10.1002/wics.1583

- [30] Erin Lipman, Dan R.C. Thal and Mariel M. Finucane “American Causal Inference Conference 2022 Data Challenge”, 2022 Mathematica URL: https://acic2022.mathematica.org/

- [31] Robert McCulloch et al. “BART: Bayesian Additive Regression Trees”, 2024 URL: https://cran.r-project.org/package=BART

- [32] Kevin P. Murphy “Probabilistic Machine Learning: Advanced Topics” MIT Press, 2023 URL: http://probml.github.io/book2

- [33] Eliza O’Reilly and Ngoc Mai Tran “Stochastic Geometry to Generalize the Mondrian Process” In SIAM Journal on Mathematics of Data Science 4.2, 2022, pp. 531–552 DOI: 10.1137/20M1354490

- [34] F… Olver et al. “NIST Digital Library of Mathematical Functions”, Release 1.1.6 of 2022-06-30, 2022 URL: http://dlmf.nist.gov/

- [35] Judea Pearl “Causality” Cambridge University Press, 2009 DOI: 10.1017/CBO9780511803161

- [36] Giacomo Petrillo “Gattocrucco/bart-gp-article: First version” Zenodo, 2024 DOI: 10.5281/zenodo.13997071

- [37] Giacomo Petrillo “Gattocrucco/lsqfitgp: Release early, release often, then hide in a foreign country and wait one year” Zenodo, 2024 DOI: 10.5281/zenodo.13930793

- [38] Carl Edward Rasmussen and Christopher K.. Williams “Gaussian Processes for Machine Learning”, 2006 URL: http://www.gaussianprocess.org/gpml/

- [39] D.. Rubin “Estimating causal effects of treatments in randomized and nonrandomized studies” In Journal of Educational Psychology 66.5 American Psychological Association, 1974, pp. 688–701 DOI: 10.1037/h0037350

- [40] James R. Schott “Matrix analysis for statistics” Hoboken, New Jersey: John Wiley & Sons, 2017

- [41] Rodney Sparapani, Charles Spanbauer and Robert McCulloch “Nonparametric Machine Learning and Efficient Computation with Bayesian Additive Regression Trees: The BART R Package” In Journal of Statistical Software 97.1, 2021, pp. 1–66 DOI: 10.18637/jss.v097.i01

- [42] Yaoyuan Vincent Tan and Jason Roy “Bayesian additive regression trees and the General BART model” In Statistics in Medicine 38.25, 2019, pp. 5048–5069 DOI: 10.1002/sim.8347

- [43] Alexander Terenin “Gaussian Processes and Statistical Decision-making in Non-Euclidean Spaces”, 2022 arXiv: https://arxiv.org/abs/2202.10613

- [44] Dan R.C. Thal and Mariel M. Finucane “Causal Methods Madness: Lessons Learned from the 2022 ACIC Competition to Estimate Health Policy Impacts” In Observational Studies 9.3, 2023, pp. 3–27 DOI: 10.1353/obs.2023.0023

- [45] Y.. Tong “The Multivariate Normal Distribution” Springer New York, 1990 DOI: 10.1007/978-1-4613-9655-0

- [46] A.. van der Vaart “Asymptotic Statistics”, Cambridge Series in Statistical and Probabilistic Mathematics Cambridge University Press, 1998 DOI: 10.1017/CBO9780511802256

- [47] Pauli Virtanen et al. “SciPy 1.0: Fundamental Algorithms for Scientific Computing in Python” In Nature Methods 17, 2020, pp. 261–272 DOI: 10.1038/s41592-019-0686-2

- [48] In‐Kwon Yeo and Richard A. Johnson “A new family of power transformations to improve normality or symmetry” In Biometrika 87.4, 2000, pp. 954–959 DOI: 10.1093/biomet/87.4.954

Appendix A Proofs

A.1 Proof of Theorem 1

I follow the notation of [5] and section 2.1. First observe that, since the BART prior is a sum of i.i.d. trees, the covariance function can be computed on a single tree:

| (35) |

where, since is the variance of all the leaves of the tree, is the correlation function. To evaluate this function, consider that, if the two points and end up in the same cell of the stepwise function represented by the tree, i.e., in the same leaf, then they are assigned the same value, so their correlation is 1. Instead, if they are separated by any tree split, they are assigned to distinct leaves, and since the leaves are independent, their correlation is 0. The marginal correlation is thus

| (36) |

as stated in [28, §5.2]. To continue the calculation, first introduce the counts of allowed splitting points , and respectively before, between and after and along each predictor axis, totalling (see Figure 2). These counts change while traversing the tree, since each children of a splitting node is assigned only a subset of the space, and thus a subset of the splitting points.

Let be the probability that a subtree at depth does not separate the two points with its allowed splits, in particular . Then I proceed by expanding the probabilities following the recursive definition of the tree prior:

|

Now if then and thus the result is 1. The same holds if , but for all , the axis weight . In particular the following total weight must be nonzero:

|

|||||||

| (38) | |||||||

Now I consider separately the probabilities appearing in the last expression. The simplest one is

| (39) |

The other probability expands as

| (40) |

Now consider separately the three probabilities appearing in the last expression. First:

| (41) |

Then, given that the current split is not separating, it must fall either in or , and only one of the children can divide the two points again, so

| (42) |

where when is in , only the left subtree has a chance to separate again the two points, since the right one is assigned to the space to the right of both points, and viceversa for in . Finally

| (43) |

and by putting together Equations 38, 39, 40, 41, 42, 43, I obtain Equation 12:

To simplify the next proofs and calculations, I assume the weights positive. To handle zero weights, I fix the convention that all predictors with shall be ignored. This gives the correct result, since at each recursive step the summation term would be multiplied by , and if then .

A.2 Proof of Theorem 2

A.2.1 Property 1

Here I check that the recursive formula for the correlation (Theorem 1) satisfies . Written in terms of splitting counts, this translates to . I prove it by induction over and . The base case, , corresponds to the base case of the recursion. Now, assuming that the property holds for all counts up to some given and , I show that it is valid also if one component of is incremented by 1:

| (I have extracted from the summations the term with and ) | ||||

| (44) | ||||

The case where is incremented is analogous.

A.2.2 Property 2

The recursive step applies, rather than the base case. So

| (45) |

A.2.3 Property 3

I prove it by induction along the recursion. The recursion either bottoms down at the base case or when the inner summations are empty. The base case trivially is in . Next, assuming that , I prove that , using the recursive step for . The inner summations over have and terms in , so overall they are bounded in . Since , the whole term of the outer summation over is in , which in turn means that the complete summation is in . I remain with which is in .

A.2.4 Properties 4 and 5

Now I prove that is a necessary condition for reaching the lower bound , provided the nontermination probabilities are such that the bounds are not degenerate () and that the subtree has a nonzero termination probability ().

Assume . This implies that the outer summation over is equal to 0. Since all the terms are nonnegative, each one of them must be zero too, so under the assumption I have and respectively for all less than and . Since , this is not possible, so the only way to yield a zero summation is to have no terms, i.e., .

Now instead consider , under the assumption . I prove that necessarily . The term which multiplies must be 0, so each term of the outer summation over must be equal to . Since the summations over together yield at most , so the only way to achieve the bound is to have , which implies .

A.2.5 Properties 6 and 7

Intuitively, points which are more distant w.r.t. the grid along all axes should have lower correlation. In fact, if the movement is split in two steps, first shrinking the grid outside of the points, then enlarging it between, this property holds separately for both variations:

| (46) | |||||||

| (47) |

I prove the inequalities by recursion. The base case satisfies. Assuming Equation 46 holds for , I prove it for :

| My goal is replace primed terms with unprimed ones. I apply the inequality to each term: | ||||

| I am left with primed terms in the inner summation ranges and in the denominator. Extending the summations preserves the inequality, while increasing the denominator has the opposite effect, so I have to deal with both at once. Since the function is increasing, with , it is sufficient to observe that the terms added to the summations, i.e., those with , are greater than the previous ones, which again derives from the inequality assumed on . Thus: | ||||

| Finally, for the condition on the outer summation, implies , so the latter condition can only eventually add nonnegative terms compared to the first: | ||||

Analogously, assuming Equation 47 holds for :

| Since , I can replace the denominator. This time the condition is less restrictive than , so the set of summation terms potentially gets larger. However, if then necessarily , so the corresponding term is zero: | ||||

A.2.6 Property 8

If , then with the recursive step, and with the base case. Assuming , the recursive step applies to , so

| (48) |

A.2.7 Property 9

The case if is already covered by property 1. If , the recursive case applies, with the recursion bottoming when the inner summations are empty. Now I prove that when . Base case:

| (49) |

The calculation for the induction step is analogous to the one of the base case, with the zeros given by rather than the summations being empty. Finally:

| (50) |

A.3 Truncated correlation function

A.3.1 Proof of Theorem 3

In the recursive step, depends linearly on the terms, and with nonnegative coefficients. This implies that the inlined expansion to depth of is linear and increasing w.r.t. the terms . So, if I replace with a lower or upper bound on its value, as in the definition of , I get respectively a lower or upper bound on . Moreover, by linearity, any interpolation between the two bounds at level corresponds to an interpolation at level . In the special case , .

A.3.2 Proof of Theorem 4

I have to prove that

| (51) |

It is sufficient to prove the property for . It also sufficient to check the bottom case , since the higher levels of the recursion are identical even if is different, and depend with positive coefficients on lower levels. This reduces the inequalities to the general bounds for the correlation function (property 3, Theorem 2):

| (52) | ||||

| (53) |

A.3.3 Proof of Theorem 5

A.4 Pseudo-recursive truncated correlation function

A.4.1 Proof of Theorem 6

I’ll prove that is p.s.d. by showing it stems from the correlation function of a variant of BART.

Starting from BART, modify it by re-allowing all splits at levels to : instead of forcing the subtrees to use only the regions delimited by the splits of the ancestor nodes, they start off with the initial complete set of splits. This may look wasteful because it produces redundant decision rules and empty leaves where no point ever falls, but it’s formally valid.

The correlation function of this process is obtained from the calculation in the proof of Theorem 1 (section A.1), with two modifications.

First, like in Definition 2, duplicate the arguments of the sub-correlation function, to “remember” the initial arguments: is the probability that a subtree with root at depth does not separate the two points and , with the splits to use in decision rules, potentially restricted, and all the splits. In particular the correlation function is

| (54) |

Second, modify Equation 42 as

| (55) |

has the right recursive step, but it’s not yet equal to because it does not terminate at depth and it lacks the interpolation coefficient . To add these features, set for and like in the proof of Theorem 5 (section A.3.3). This finally yields as correlation function of the process.

A.4.2 Proof of Theorem 7

In the recursive step, the sub-correlation function at depth always depends with nonnegative coefficients on the sub-correlation function at depth . Thus replacing with an upper bound on it produces in turn an upper bound on .

Restricting the available splits keeps unchanged while reducing , so by property 6, Theorem 2, evaluated on the original unrestricted splits is greater than evaluated on restricted splits.

Using these two facts, I can recursively modify in a non-decreasing way until it’s equal to . The base case is . I plug this bound into the recursive step for , obtaining an upper bound on it, and yielding , and so on until . Here I replace the restricted with the initial ones, obtaining again an upper bound equal to . I continue until .

A.4.3 Proof of Theorem 8

Consider and , with . Their recursive expansions are identical until hitting level . At that point, the first invokes , while the second , which is equal to 1 by Equations 22 and 23. Since because it is a correlation function (see section A.4.1), and the recursive step depends with nonnegative coefficients on the sub-correlations, the inequality back-propagates up to .

A.5 Proof of Theorem 9

Here I derive the formula for of Equation 31. In the following I assume since otherwise I can shortcut to . I start from Equation 19:

| and expand again : | ||||||||||||||||

| Note that, since , and . I continue simplyfing the expression: | ||||||||||||||||

| I take out the terms with from the sums over : | ||||||||||||||||

| Where if and otherwise, even if is not well defined. So now I can remove all the exceptions of the kind : | ||||||||||||||||

| Now the only nontrivial summation terms are the fractions where appears. My goal is to write them as harmonic sums () which can be written in terms of the digamma function , so it would be convenient to remove the exception indicated by the braces. I can do this by extracting the terms from the summations. This brings the added simplification that, if , necessarily . I also need to remember that the term is missing if the summation is empty, i.e., if : | ||||||||||||||||

| Notice there are many terms to be summed over. However, the terms in change as runs over its range because of the conditions . I remove them by adding and subtracting the missing term: | ||||||||||||||||

| So I define and replace it throughout: | ||||||||||||||||

| To have only in the denominators, I add and subtract to the numerators and split the fractions: | ||||||||||||||||

| So I can reduce all the terms which do not depend on and be left with a harmonic sum: | ||||||||||||||||

|

Now I use the identity from [34, eq. 5.4.14]

|

||||||||||||||||

| Now all the outer conditions are on . By grouping them together and reordering, I obtain: | ||||||||||||||||

| Observing that, if and , then , , and , calculation shows that the two large conditional terms would yield 0 anyway if the condition was false, so I can remove the outer braces: | ||||||||||||||||

| Which allows to gather some terms, arriving at Equation 31: | ||||||||||||||||

Next levels

It is probably possible to obtain an formula for for any by writing generalized harmonic sums in terms of higher order polygamma functions. However the calculation would be even more tedious and error-prone than for due to the need to keep track of the special cases that multiply going down the recursion, so I did not attempt it. It would likely also not be computationally convenient because the bottleneck in my code is currently evaluating the formula for due to its sheer length.

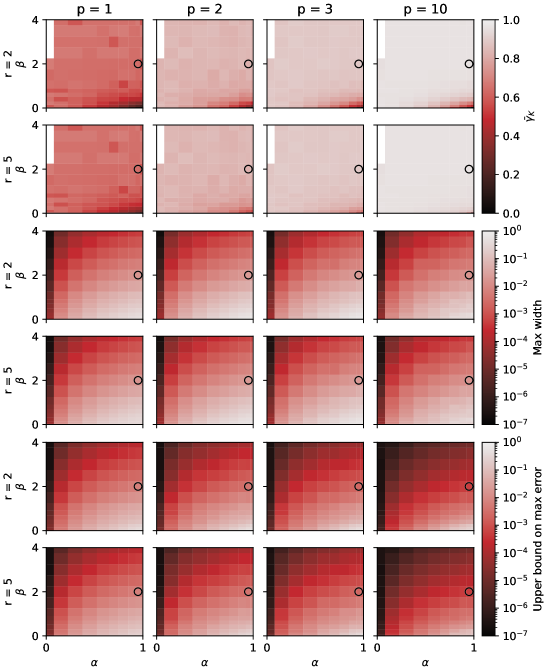

Appendix B Accuracy of the calculation of the prior correlation function

With numerical experiments, I justify the choice made in section 3.5 of using as approximate estimate of , and measure its estimation error. The idea is computing accurate reference values by reaching higher depths, and then compare them with the the less accurate but fast repeated depth 2 calculation.

Setup of the experiment

For each combination of the following values of hyperparameters and , number of predictors , base truncation depth , and recursions :

| 0.01 | 0.15 | 0.30 | 0.45 | 0.60 | 0.70 | 0.80 | 0.90 | 0.95 | 0.99 | 1.00 | |||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0.0 | 0.1 | 0.2 | 0.4 | 0.6 | 0.8 | 1.0 | 1.5 | 2.0 | 2.5 | 3.0 | 3.5 | 4.0 | |

| 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | ||||

| 1 | 2 | 3 | 4 | 5 | |||||||||

| 2 | 5 |

I generate quasi-Monte Carlo pairs of locations on a grid with splits per axis and evaluate the lower and upper bounds and on . I modify the functions with the substitution to have them range in instead of . The locations are re-sampled for each combination of , , .

Determination of an accurate reference value

I somewhat arbitrarily define a “most accurate” estimate of , as the point which has the same interpolation coefficient with respect to the and intervals at :

| (58) |

where . This choice is made on the intuition that, since the function is recursive, the position of the more accurate interval within the larger one gives an indication on the position of deeper intervals w.r.t. the one at . In particular, in the white noise limit (property 9, Theorem 2), , so is exact.

Interpolation coefficient

For base depths , I compute the interpolation coefficient that yields the reference value :

| (59) |

I will leave implicit that depends on , , , , , and the pairs of locations.

Averaging of the interpolation coefficient

I’d like to have a single “good” value for each combination of hyperparameters. I define as the median of over location pairs, weighted with the bounding interval width .

The reason for weighting with interval width is that the value of is more important when the width is larger: if the width is small, the lower and upper bounds are close, so are all the interpolated values in between. The maximum error is indeed proportional to the width.

The reason for using a median instead of an average is to ignore points where the value of is very different from the others.

There is a potential problem in that averaging over locations could create artefacts that depend on the distribution of locations. As increases, it is less likely for a pair of points to be close, so the typical correlation is smaller. On the other hand, this may simply reflect the actual usage of the correlation function. I haven’t investigated this issue.

Bound on the estimation error

At fixed hyperparameters, I compute the maximum over location pairs of the width of the bounding interval, and an upper bound on the maximum error in estimating with :

| (60) |

I used the interval at depth , , because it is the narrowest one, thus producing the smallest error bound possible. Figure 6 shows , the maximum width, and maximum error, only at base depth , since this is the depth that matters for calculations.

As expected, in the white noise corner and (property 9, Theorem 2). Increasing makes a difference almost only in this corner. For other values of the hyperparameters, the relationship looks flat (at fixed ), and increases quite quickly from to but then stabilizes, suggesting an asymptote w.r.t. at . This means that the reference value is pretty close to the upper bound . The upper bound on the maximum error at the default BART values , is, both at and :

| 1 | 2 | 3 | 10 | |

|---|---|---|---|---|

| error | 0.0065 | 0.0040 | 0.0022 | 0.0005 |

Appendix C Numerical cross checks

This section extends section 3.5, providing assurance that the calculation of the kernel is correct.

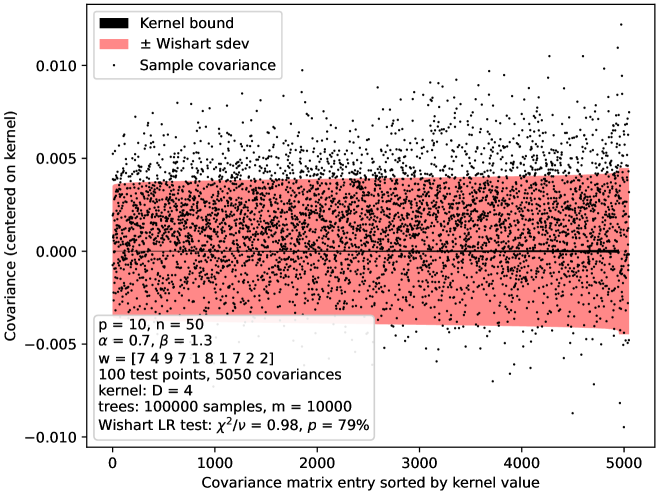

C.1 Comparison between kernel and generative tree process

To check at once the correctness of the derivations of the BART correlation function (Theorem 1), its truncated version (Definition 1), the special-casing (Theorem 9), and the computer implementation based on them, I sample directly from the BART prior, generating the trees, and compare the sample covariance matrix with the one computed with my kernel.

I fix some arbitrary values of the hyperparameters, the number of predictors, the splitting grid, and 100 predictor vectors. I generate samples to have a precise estimate of the covariance, and use trees to make the distribution of the samples Normal within good approximation. I use the Normality of the samples to assume a scaled Wishart distribution for the sample covariance matrix and perform a likelihood ratio test for the equality of the covariance to the one computed by the kernel. I use as kernel estimate, increasing until the maximum error is much smaller than the Wishart standard deviation, reaching . Note that, due to sufficiency, a Normal LR test on the samples would be identical to the Wishart LR test on the sample covariance matrix. The result is shown in Figure 7. The test does not reject the equality hypothesis.

C.2 Self-consistency of the correlation function

I check numerically the following qualitative properties and corner cases of the correlation function on a large set of values of hyperparameters, problem sizes and locations:

- •

-

•

if (Theorem 4).

-

•

if .

-

•

if .

- •

- •

-

•

is invariant under: per-axis swapping of with , simultaneous reordering of and , appending zeros to with any , appending zeros to with any .

-

•

under either one of these sufficient conditions: if , , .

-

•

Using the closed-form formulas for and (Equations 26 and 31) yields the same result as walking through the recursion (Equation 19).

-

•

.

Appendix D Out-of-sample predictive accuracy on real data

I compare GP regression with my BART kernel against the original BART MCMC by comparing their predictions on held-out test sets on a series of datasets. This section extends section 4.1.

D.1 Data

I use the 42 datasets of the original BART paper [5, 26]. The dataset size ranges from to , while the number of predictors ranges from to . The outcome is log- or sqrt-transformed if its distribution looks skewed, and standardized; and categorical predictors are converted to binary dummies, one for each stratum. Each dataset is randomly split 5:1 in train:test parts, 20 times. The train parts are again randomly split in 5 folds for cross-validation. After partitioning and dummyfication, the training sample size ranges from to , and the number of predictors from to . Hugh Chipman kindly provided their original data files, so I have exactly the same transformations, train/test splits, and folds of [5].

D.2 Methods

I test six methods, with this naming scheme:

- MCMC

-

standard BART (section D.2.1).

- MCMC-CV

-

BART cross-validated as in [5] (section D.2.2).

- MCMC-XCV

-

BART cross-validated with the pre-packaged routine xbart provided by dbarts (section D.2.3)

- GP

-

the infinite trees limit of BART as GP regression (section D.2.4).

- GP-hyp

-

like GP but with hyperparameter tuning (section D.2.5).

- GP+MCMC

-

standard BART with hyperparameters set to those found by the GP regression (section D.2.6).

D.2.1 Method: MCMC

I mostly reproduce the setup of [5]. See Equation 2 for the definition of the model. The hyperparameters are set to

-

•

.

-

•

, .

-

•

.

-

•

.

-

•

, .

-

•

.

-

•

is set such that , where is the error standard deviation estimated by OLS (with an intercept), i.e., the sum of squared residuals over the degrees of freedom.

-

•

The splitting grid is set by taking the unique set of values in the training set for each predictor, and putting a cutpoint midway between each one.

Instead of the original implementation BayesTree, I use the BART package, because it seems to be more adherent to the exact specification of the BART model (see section D.7). I run 4 MCMC chains in parallel, discarding the first 1000 samples from each, and keeping a total of 1000 samples over all chains, so 250 per chain. I then merge all the chains. The burn-in of 1000 is higher than the default 200; I do this because my personal experience has taught me that 200 is often too low to get reasonable convergence.

D.2.2 Method: MCMC-CV

I optimize some of the hyperparameters of the MCMC method with cross validation. The folds are described in section D.1. I reproduce the CV procedure of [5], exploring the cartesian product of these sets of parameter values:

-

•

,

-

•

,

-

•

.

The combination which yields the lowest RMSE over all folds is chosen. The MCMC configuration is the same as MCMC for all CV runs. I use dbarts instead of BART, because it is faster, and because it seems to match BayesTree in its details (see section D.7), such that MCMC-CV overall should be an accurate reproduction of the “BART-cv” method showcased in [5].

D.2.3 Method: MCMC-XCV

I use the built-in CV routine xbart of the package dbarts, trying combinations of these hyperparameters:

-

•

,

-

•

,

-

•

,

with one repetition per combination (reps = 1). Instead of imposing the setup of section D.2.1, I leave the configurations to their default values; the only difference this should entail is that the splitting grid is evenly spaced in the range of the data, but I’m not sure. For the full run after the CV, the only non-default configuration I adopt is to set the number of MCMC samples as in section D.2.1. The general idea of this setup is to use a good existing tool as-is, to emulate the applied usage of BART.

D.2.4 Method: GP

I implement a GP regression following closely the setup of MCMC. The only differences are that the latent function is a GP instead of a sum of trees, and that BART forbids leaves containing less that 5 datapoints; the latter should not make a visible difference as this is unlikely to happen due to the trees being shallow. The kernel is as explained in section 3.5 and Appendix B, and the variance and mean of the GP are matched to those of the sum of trees, such that the GP represents the infinite trees limit.

The only free parameter which is not part of the GP is the error variance . The posterior density on is

| (61) |

where is the prior correlation matrix computed with the kernel, and I have left implicit the other hyperparameters. Since is positive, I do the inference working with .

Evaluating the Normal density requires computing the a decomposition of the covariance matrix, which is of the form (); this is the bottleneck of the calculation. The default option for this task is the Cholesky decomposition. However, since to draw samples the density is evaluated at multiple values, it is convenient to use a decomposition which is slower but can be computed only once and recycled: I diagonalize , so , with orthogonal and diagonal. Since , the same change of basis diagonalizes the whole matrix: . The rest of the calculation does not require any linear algebra operation as expensive as producing .

To sample the posterior I use the ratio of uniforms method, a rejection sampling method apt for unnormalized densities with unbounded support [27]. To tune the acceptance of the method, I find the MAP and other extrema with some numerical minimizations. I draw 1000 independent samples. To compute the posterior mean I combine the formula for GP regression posterior mean (Equation 5) with iterated expectation:

| (62) |

D.2.5 Method: GP-hyp

Starting from the GP method, I optimize the hyperparameters , , , by fixing them to their marginal a posteriori mode. I use L-BFGS to maximize the Normal density of the GP times a prior on the free hyperparameters. To improve the quality of the approximation, I follow the heuristic of transforming the hyperparameters such that their prior is standard Normal, and find the mode in the trasformed space. The prior is:

| (63) | ||||

| (64) | ||||

| (65) | ||||

| (66) |

The inverse gamma prior on keeps it away from 0, to forbid the case , where the latent function becomes equivalent to the error term.

I plug the optimized values of , and into the same procedure of the GP method, thus re-deriving the posterior on conditional on the other parameters.

D.2.6 Method: GP+MCMC

Starting from GP-hyp, instead of running GP with the optimized values of the hyperparameters , , , I use MCMC implemented with dbarts.

D.3 Performance metrics

I evaluate the models on two standard out-of-sample prediction error metrics: RMSE and log-loss.

RMSE

The RMSE is the root mean square error of an estimate w.r.t. the true outcome values from a test set not used as data. As estimate I take the predictive posterior mean, since the mean minimizes the expected squared error.

| (67) |

Since the data is standardized, the RMSE is comparable across different datasets, and should yield at most about 1.

Log-loss

The log-loss is a distributional metric that takes into account the whole posterior. It is defined as minus the log posterior density, evaluated at the actual true value:

| (68) |

It is divided by the number of test samples, to make it comparable across cases with different sample sizes.

It is justified as the only proper scoring procedure which is invariant under changes of variables, i.e., the expected value of the log-loss is minimized by computing it with the same distribution used to take the expectation, and reparametrizations can only shift the log-loss by a constant, since they just add a jacobian factor to the probability density.

Since the data is standardized, typically the log-loss should fall in or nearby. However, due to using a Normal error distribution in the model, which is light-tailed, the log-loss can explode to very high values if the error variance is estimated too small. For this reason, the log-loss is a quite “strict” metric to judge models, and it is often not useful alone: the light-tailedness is an accident of design for computability, while the statisticians using the model understand that in practice prediction errors are not best represented by a Normal distribution.

Computation of the log-loss in MCMC

The MCMC used in BART does not produce directly a posterior density. However the error term density is not modified by conditioning on the data due to the errors being independent, which allows to estimate the marginal density by averaging the error density over the posterior samples:

| (69) |

To compute the logarithm of Equation 69, I use a single logsumexp function that avoids under/overflow.

Computation of the log-loss in GP regression

With GP regression, the posterior density is computable analytically because it is a multivariate Normal density (Equation 5). However I noticed that this yields a systematically lower log-loss than using Equation 69. So, to make the comparison fairer, I first draw samples from the posterior and then apply the same procedure I use for MCMC.

There are multiple ways to draw posterior samples in GP regression. I pick a method particularly suited to my specific context, in which the only free non-GP parameter of the model is the error variance . Using the notation of section 2.2, instead of starting from the posterior covariance matrix , I diagonalize both and , generate samples with covariance matrix , and use Matheron’s rule [43, 72] to transform them to samples with covariance matrix :

| (70) | ||||

| (71) | ||||

| (72) | ||||

| (73) | ||||

| (74) | ||||

| (75) | ||||

| (76) |