[table]capposition=top

Optimal life insurance and annuity decision under money illusion

Abstract

This paper investigates the optimal consumption, investment, and life insurance/annuity decisions for a family in an inflationary economy under money illusion. The family can invest in a financial market that consists of nominal bonds, inflation-linked bonds, and a stock index. The breadwinner can also purchase life insurance or annuities that are available continuously. The family’s objective is to maximize the expected utility of a mixture of nominal and real consumption, as they partially overlook inflation and tend to think in terms of nominal rather than real monetary values. We formulate this life-cycle problem as a random horizon utility maximization problem and derive the optimal strategy. We calibrate our model to the U.S. data and demonstrate that money illusion increases life insurance demand for young adults and reduces annuity demand for retirees. Our findings indicate that the money illusion contributes to the annuity puzzle and highlights the role of financial literacy in an inflationary environment.

Keywords: Money illusion, life insurance, annuity, inflation

1 Introduction

Life insurance and annuity decision-making are crucial in studying the life-cycle model, aiding individuals in managing the mortality and financial risks in long-term investments. Yaari, (1965) pioneers adding the random horizon to the life cycle model, highlighting the separability of consumption and bequest decisions when insurance is an option. Fischer, (1973) examines the life-cycle model in discrete time, observing that individuals with labor income are inclined to purchase life insurance early in life and sell it later on, and proposes annuity purchases to solve the short-sale constraints of life insurance. Richard, (1975) delves into an individual’s life and annuity decisions within a continuous-time framework, finding that those anticipating high future income are likely to purchase life insurance regardless of relative preference in consumptions and bequests. Pliska and Ye, (2007) extend Richard, (1975)’s bounded lifetime assumption to an unbounded scenario, exploring life insurance demand across various economic factors and drawing significant economic insights. For pertinent work, we refer to Hakansson, (1969), Huang and Milevsky, (2008), Koijen et al., (2011), Ekeland et al., (2012), Kwak and Lim, (2014), Wei et al., (2020), Bernard et al., (2021), Fischer et al., (2023), Li et al., (2023), Kizaki et al., (2024), and Wang and Chen, (2024), among others. However, none of the existing literature considers the effects of money illusion on an individual’s consumption, investment, and insurance demands.

The concept of money illusion, whereby individuals assess their utility based on nominal rather than real monetary value, was introduced in Fisher, (1928) and is substantiated by empirical research (e.g. Shafir et al.,, 1997; Fehr and Tyran,, 2001, 2007; Svedsäter et al.,, 2007). In the economics literature, Brunnermeier and Julliard, (2008) demonstrates that reducing inflation can significantly increase house prices for individuals affected by money illusion. Miao and Xie, (2013) explores economic growth and determines that money illusion influences an agent’s perception of real wealth growth and risk. Basak and Yan, (2010) highlight the substantial impact of money illusion on stock equilibrium prices. Lioui and Tarelli, (2023) find that individuals influenced by money illusion tend to shift from inflation-indexed to nominal bonds. For more related work, we refer to David and Veronesi, (2013), Chen et al., (2009), Chen et al., (2013), He and Zhou, (2014), and Eisenhuth, (2017). In actuarial science literature, Wei and Yang, (2023) study the money illusion effect within a defined-contribution plan framework. They reveal that the money illusion decreases an individual’s holdings of inflation-linked bonds and results in substantial welfare loss. Donnelly et al., (2024) extend Wei and Yang, (2023)’s work with a minimum guarantee at retirement time. They find that the minimum guarantee can significantly reduce welfare loss caused by money illusion. However, both papers focus solely on the pre-retirement arrangement, overlooking post-retirement management. Furthermore, neither paper considers the individual’s mortality risk, leaving research gaps to study the individual’s insurance and annuity demands under the money illusion.

We consider the money illusion effect in a life cycle model. The family comprises the breadwinner and the rest of the family, both affected by money illusion in their consumption decisions. For the financial market, we adopt a two-factor model proposed by Koijen et al., (2011) to describe time-varying real interest rates, inflation rates, and risk premiums. The family can invest a part of the wealth in a stock index, nominal bonds, inflation-linked bonds, and a cash account. Simultaneously, they allocate the other part of the wealth to purchase life insurance to manage the breadwinner’s mortality risk. Specifically, the family continuously pays the premium while the breadwinner is alive. Upon the breadwinner’s death, the rest of the family receives a death benefit comprising the wealth and a life insurance payment, after which they continue managing their investments independently. We formulate this life-cycle problem as a random horizon utility maximization problem. The family’s consumption utility combines nominal and real consumption, reflecting their inclination towards nominal monetary values over real values. In addition, the timeline is divided into three scenarios: pre-breadwinner’s death and retirement, post-breadwinner’s retirement but pre-breadwinner’s death, and post-breadwinner’s death. We derive the corresponding Hamilton-Jacobi-Bellman (HJB) equations and the optimal strategies. Under the standard constant relative risk aversion (CRRA) utility function, we obtain explicit solutions for both value functions and optimal strategies. Global existence conditions are presented to ensure that the explicit solutions do not explode in finite time. Furthermore, we prove that the explicit solutions exactly solve the HJB equations via the verification theorem.

We calibrate our model to the U.S. data and numerically illustrate the money illusion effect on the family’s consumption, investment, and insurance demands. Through dynamic analysis, we plot the expected trajectories of optimal strategies evolving over time. We observe that both the high-risk-aversion breadwinner and the rest of the family will shift from an increasing to a decreasing consumption pattern when considering the money illusion. Regarding investment strategies, the family will short fewer short-term nominal bonds in exchange for longing for more long-term nominal bonds before late age (age 80), with an opposite trend following this threshold. The demand for inflation-linked bonds diminishes due to the influence of money illusion, while the impact on stock index investments remains minimal. For insurance strategies, the breadwinner purchases life insurance at working age and switches to annuities near retirement. Introducing the money illusion leads to a higher life insurance demand and a lower annuity demand for the breadwinner. The static analysis shows that the optimal consumption and annuity strategies follow an upward “U-shape” pattern with two factors (interest rate and inflation rate factors). In contrast, the life insurance strategy displays a downward “U-shape” pattern. This is because life insurance safeguards future income and substitutes for current consumption, contrasting with annuities bolstering current consumption through income streams. Lastly, we investigate the family’s welfare loss from the money illusion. We observe that welfare loss increases with the degree of money illusion and the risk-aversion coefficient. This escalation is attributed to the risk-averse behavior of individuals, leading them to allocate more to riskless assets. While non-illusioned investors perceive inflation-linked bonds as riskless, illusioned investors favor nominal bonds, creating a divergence in welfare loss stemming from the preference discrepancy.

Our paper contributes to the existing literature in three aspects: (i) We study the money illusion effect on the trading strategy over short-term nominal bonds, long-term nominal bonds, inflation-linked bonds, and stock indexes. We find that when ignoring inflation risk, the family reduces the short position in short-term nominal bonds and long more long-term nominal bonds. Additionally, they decrease holdings in inflation-linked bonds while maintaining a steady stance on stocks. (ii) We explore the influence of money illusion on consumption strategies. Our results suggest a shift in consumption patterns from increasing to decreasing when ignoring the inflation risk. (iii) In examining life insurance and annuity decisions, we discover that neglecting inflation risk leads to an increased demand for life insurance but a reduced demand for annuities among breadwinners. This phenomenon contributes to the annuity puzzle, a well-documented issue where individuals exhibit reluctance to purchase annuities close to retirement age. Existing explanations for the annuity puzzle include annuity mispricing (Davidoff et al., (2005)), bequest motives (Lockwood, (2012)), mortality misperceive (Han and Hung, (2021)), risk aversion (Milevsky and Young, (2007)), and time inconsistency (Zhang et al., (2021)), etc. Our analysis introduces a novel perspective by highlighting money illusion as a potential driver of the annuity puzzle, particularly in an inflationary economic environment.

The rest of the paper is organized as follows: Section 2 introduces the model settings, including the financial market, mortality, wealth process, and breadwinner’s objective. Section 3 solves the optimization problem via the HJB equations. Global existence and verification theorem are proved for explicit solutions. Section 4 calibrates the model with U.S. data, conducts sensitivity analysis of the optimal strategies, and analyzes the welfare loss. Section 5 concludes.

2 Model settings

2.1 Financial market

We consider a financial market similar to that proposed by Koijen et al., (2011), which incorporates time variations in real interest rates, inflation rates, and risk premia. Let be a filtered complete probability space. We use a four-dimensional vector of independent Brownian motions to characterize the financial risk, which generates the filtration .

Within the financial market, the real short rate is modelled as affine in a single factor, ,

Meanwhile, the expected inflation rate is influenced by a second factor, ,

These two factors are governed by an Ornstein-Uhlenbeck process

| (1) |

where , , . The evolution of realized inflation is captured by the stochastic differential equation (SDE)

| (2) |

where represents the level of the (consumer) price index at time and . The equity index is given by

where the drift term is defined as , with representing the instantaneous nominal short rate as specified in (3) below. To aid in model identification, we impose the condition that the volatility matrix is lower triangular.

We postulate the nominal state price density evolve as

where the market prices of risk, denoted by , are affine in the term-structure variables, i.e.,

We follow Koijen et al., (2011) to impose restrictions on and

with and . The real state price density is governed by

which implies the instantaneous nominal short rate can be expressed as

| (3) |

where and .

Finally, we present the prices of nominal and inflation-linked bonds, deriving from the standard approach in the literature (e.g. Duffie and Kan,, 1996). The time- price of a nominal bond with maturity has an exponential affine form

where and are determined by the following ordinary differential equation (ODE) system

| (4) | |||

| (5) |

Additionally, the dynamics of are governed by

Similarly, the time- real price of an inflation-linked bond with maturity is

| (6) |

where and are subject to the ODE system

where represents the -th unit vector in . Then, the nominal price of the inflation-linked bond, , follows the SDE

2.2 Mortality

This subsection introduces the breadwinner’s mortality risk. We use to denote the future lifetime of a breadwinner aged , which is a non-negative random variable independent of the financial market (i.e., is independent of the filtration associated with the financial market). We then define the following probabilities

where represents the probability that the breadwinner aged survives to at least age , and is the probability that the breadwinner dies before age . In actuarial science, it is conventional to define the instantaneous force of mortality (or hazard rate) as

leading to the relationships

The probability density function of is then expressed as for .

2.3 Wealth Process

We consider two dates of interest: the breadwinner’s retirement time denoted by and the terminal time denoted by . The breadwinner can purchase life insurance before the first time of death time and retirement time . The nominal wealth follows

where the initial condition is , represents the nominal income, is the nominal insurance premium, denotes the nominal consumption for the breadwinner, represents the nominal consumption for the rest of the family, and is the volatility matrix given by

We introduce the real wealth , leading to the SDEs

| (7) |

In equation (7), the initial condition is . is the breadwinner’s real income satisfying

| (8) |

where is a deterministic function. The real insurance premium is denoted by , represents the real consumption for the breadwinner, and is the real consumption for the rest of the family. At the death time

2.4 Preference

Let and denote the consumption utility of the breadwinner and the rest of the family, respectively. The rest of the family typically includes the spouse and/or children, with the spouse being the more commonly considered member (see Bernheim,, 1991; Inkmann et al.,, 2011). These consumption utilities depend not only on real consumption but also on inflation , which captures the family’s preference for nominal monetary value over real value. Inspired by Huang and Milevsky, (2008), Huang et al., (2008), and Kwak et al., (2011), we make the assumption that the rest of the family has a certain life expectancy. The family’s objective is to determine values for , , , and that maximize the expectation

| (9) | |||

| (10) |

Here, , and are non-negative weight parameters for consumption utilities that satisfy , and represents the utility discount factor. Equation (10) transforms a random horizon problem into a fixed horizon problem.

3 Optimization problem

3.1 HJB equations and optimal strategies

Based on three divisions of time intervals, we introduce the first value function as

for , where is short for . The secondary value function is defined as

for . Lastly, for , we define a primary value function

| (11) |

By the dynamic programming principle, the first value function satisfies the HJB equation

| (12) |

where is the infinitesimal generator given by

After solving it, the optimal consumption and trading strategy are given by

| (13) | |||||

| (14) |

The HJB equation for the secondary value function is subject to

| (15) |

where is the infinitesimal generator given by

and the optimal strategies are

| (16) | |||||

| (17) | |||||

| (18) | |||||

| (19) |

where is the partial derivative with the second variable of .

For the primary value function, we need a special treatment for the income process . Following the approach in Deelstra et al., (2003), we introduce the surplus process as

| (20) |

where represents the time- value of (discounted) future income

Applying Ito’s formula, we can express the differential of as

| (21) | |||||

Assuming the existence of a process , we can rewrite the above SDE as

| (22) | |||||

which allows us to derive the by comparing the relevant terms in (21) and (22)

Furthermore, we derive the SDE for the surplus process by combining (7) and (22)

| (23) | |||||

where and . The SDE (23) represents the investment in the financial market and the purchase of life insurance with premium . When the breadwinner dies before retirement, the surplus process has the following jump

Then, by definition (20), and given that at , the objective function (11) can be transformed to

where is short for . Moreover, the corresponding HJB equation is

| (24) |

where is the infinitesimal generator given by

| (25) |

and the optimal strategies are

| (26) | |||||

| (27) | |||||

| (28) | |||||

| (29) |

where is the partial derivative with the second variable of .

3.2 Explicit solutions under CRRA utility

Inspired by Miao and Xie, (2013), Wei and Yang, (2023), and Donnelly et al., (2024), we restrict consumption utilities to the following form

where and represent the real and nominal consumptions, respectively, and represents the degree of money illusion. For tractability, we assume and to obtain explicit solutions. When , the breadwinner is non-illusioned and only considers real consumption. When , the breadwinner is fully-illusioned and focuses solely on nominal consumption. As increases from 0 to 1, the breadwinner increasingly values the nominal value and ignores inflation risk.

Under this utility specification, we derive explicit solutions for the HJB equations (12)-(24). These explicit solutions provide valuable insights into optimal strategies considering varying degrees of money illusion.

Proposition 3.1.

The candidate solution to HJB (12) is given by

where

Functions , , and follow the ODE system

| (30) | |||

| (31) | |||

| (32) |

in which

The candidate strategies are given by

Proposition 3.2.

3.3 The global existence and verification theorem

Several linear ODEs, including (31) and (32), which are linear ODEs, determine the candidate solutions. These equations have unique solutions that exist globally (see Theorem 1.1.1. in Abou-Kandil et al.,, 2012). However, the ODE (30) is a Hermitian matrix Riccati differential equation (HRDE), which requires special treatment for its existence. The HRDE can be represented as a matrix in the following way

| (38) |

where is the 2nd-order identity matrix, and

which is called the Hamiltonian matrix. The global existence of the HRDE (38) is heavily influenced by the relative risk aversion coefficient , which is also a factor for the verification theorem. Inspired by Honda and Kamimura, (2011), we divide the proofs in this subsection into two cases and .

Proposition 3.4.

For candidate solution , define its admissible set as

For candidate solution , define its admissible set as

Notice is the special case of restricted to when , , and . Similarly, is the special case of restricted to when . The same approach used in Proposition 3.4 can be applied to prove the global existence and verification theorems for and .

For , the existence of (30) can be established using Radon’s Lemma with additional conditions. Let represent a solution to the linear system of differential equations

| (39) |

According to Radon’s Lemma (see Theorem 3.1.1 in Abou-Kandil et al.,, 2012), the solution to (30) can be expressed as . Next, we only need to guarantee the candidate solution’s global existence. For tractability, we adopt the assumption by Abou-Kandil et al., (2012) that is diagonalizable. This means that there exists a 4-dimensional basis of eigenvectors

where denotes the complex vector space of complex vectors. The corresponding eigenvalues are sorted by their real parts

Let , where denotes the complex vector space of complex matrices, then the solution to (39) can be expressed as

where . Furthermore, define

| (40) |

we can finally prove the following proposition of global existence and verification.

Proposition 3.5.

For candidate solution , define its admissible set as

For candidate solution , define its admissible set as

4 Numerical results

4.1 Model calibration

According to the parameter settings in Huang and Milevsky, (2008), we consider a breadwinner who is 35 years old at the initial time and retires at the age of 65. The family ceases making investment decisions at the breadwinner’s age of 95, so and . The breadwinner allocates wealth among 3-year nominal bonds, 10-year nominal bonds, 10-year inflation-linked bonds, the equity index, and cash () and also purchases life insurance. Following Koijen et al., (2011), we suppose that the growth rate in the real income (8) is given by

which corresponds to an individual with a high school education in the estimates of Cocco et al., (2005) and Munk and Sørensen, (2010). We assume the breadwinner’s force of mortality is subject to the Gompertz law

and set other base model parameters as

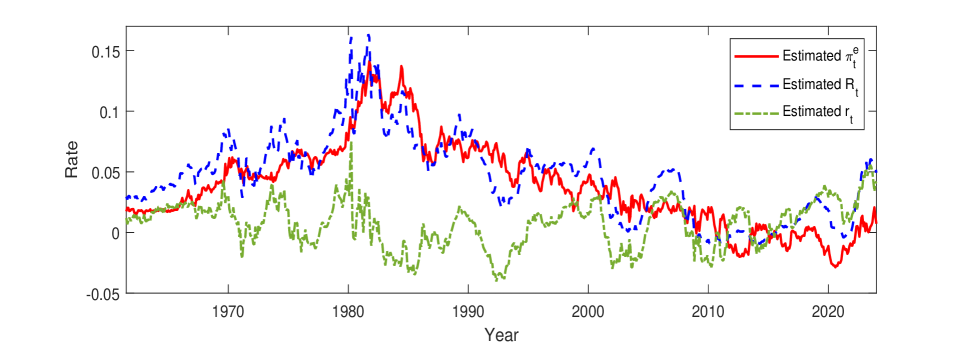

We utilize monthly data from the U.S. financial market, spanning from June 1961 to December 2023. To estimate the parameters, we employ zero-coupon nominal yields from Gurkaynak et al. (2007), comprising eight different maturities: three months, six months, one year, two years, three years, five years, seven years, and ten years. The realized inflation index is obtained from the CRSP’s Consumer Price Index for All Urban Consumers (CPI-U NSA index). Additionally, we utilize the equity index based on the CRSP’s value-weighted NYSE/Amex/Nasdaq index, which includes dividend payments.

We implement a Kalman filter algorithm to estimate the two factors and model parameters, detailed in Appendix D. The results are presented in Table 1 and Figure 1. Aligned with Koijen et al., (2011), we observe that , which indicates that expected inflation is more persistent than the real short rate. In terms of innovations, we detect a negative correlation between the real short rate and expected inflation (). Regarding the equity index process, we find that the risk premium diminishes with the real short rate and expected inflation (). Moreover, the unconditional price of risk, , is negative for the real short rate and expected inflation but positive for the equity index. Notably, all the parameters in the conditional price of risk, , are negative, implying that the price of risk decreases with two factors . Figure 1 depicts the estimated short rates and expected inflation.

| Parameter | Estimate | Parameter | Estimate | Parameter | Estimate |

| Average short rate & average expected inflation | |||||

| 0.01254 | 0.05120 | 0.03831 | |||

| Two-factor process | |||||

| 0.61921 | 0.18894 | 0.02209 | |||

| -0.00673 | 0.01408 | ||||

| Realized inflation process | |||||

| 0.00042 | 0.00207 | 0.01363 | |||

| Equity index process | |||||

| 0.04600 | -1.97000 | -1.41000 | |||

| -0.01974 | -0.01785 | -0.00793 | |||

| 0.15410 | |||||

| Prices of risk of real short rate, inflation, and equity | |||||

| 0.00487 | -0.17007 | 0.27943 | |||

| -9.92002 | -9.98001 | -14.05465 | |||

| -10.30593 | |||||

The parameters in the table are annualized. , , , and can be obtained by solving three equations: , , . So, there are 21 parameters in total to be estimated.

4.2 Sensitivity of optimal strategies to the age

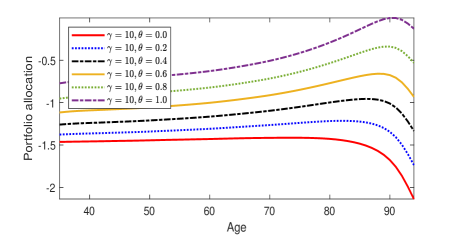

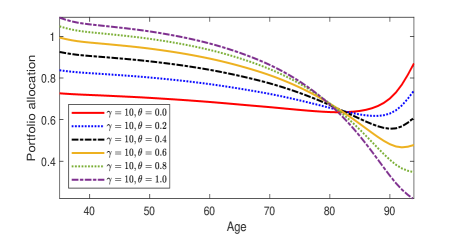

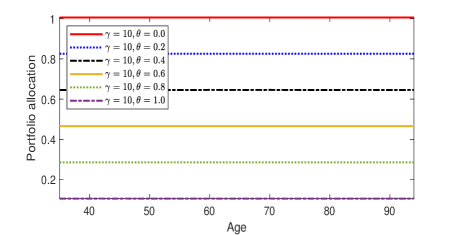

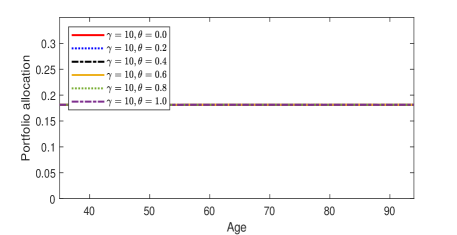

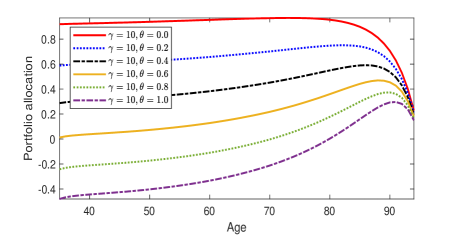

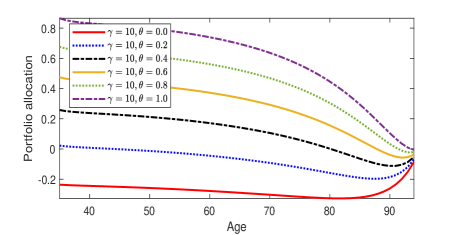

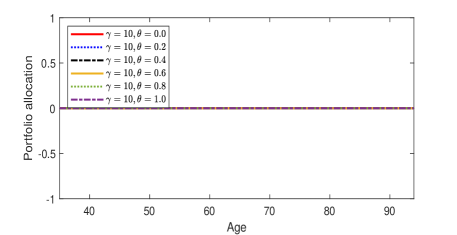

In this subsection, we analyze how the optimal strategies change with age. We conduct Monte Carlo simulations involving 10,000,000 paths, using a time step of one year. The expected trading, consumption, and insurance strategies are shown in Figures 2 - 5. Specifically, Figures 2 and 3 correspond to a risk aversion coefficient of , while Figures 4 and 5 correspond to .

To obtain more insightful observations, we decompose the optimal trading strategy in (36) into the following three components

| (43) |

Among three components, the standard myopic demand (SMD) characterizes the risk-return trade-off of the assets. The inflation hedging demand (IFHD) represents the family’s aspiration to hedge against realized inflation ( is the volatility term of , as specified in (2)). Lastly, the intertemporal hedging demand (ITHD), determined by the investment horizon, reflects the family’s intent to hedge against potential changes in future investment opportunity sets.

We present the unconditional expectations of SMD and IFHD in Table LABEL:Expected_smd_ifhd. The expected SMD is a constant vector because in (1) follows a normal distribution , where . Moreover, is zero as the fourth entry of is zero, which is implied by the assumption that is lower triangular.

| Values | -0.293846 | 0.226313 | 0.105499 | 0.181331 |

|---|---|---|---|---|

| -2.089113 | 0.735923 | 0.900000 | 0.000000 | |

| -1.671290 | 0.588739 | 0.720000 | 0.000000 | |

| -1.253468 | 0.441554 | 0.540000 | 0.000000 | |

| -0.835645 | 0.294369 | 0.360000 | 0.000000 | |

| -0.417823 | 0.147185 | 0.180000 | 0.000000 | |

| 0.000000 | 0.000000 | 0.000000 | 0.000000 |

is the th entry of the standard myopic demand vector. is the th entry of the inflation hedging demand vector.

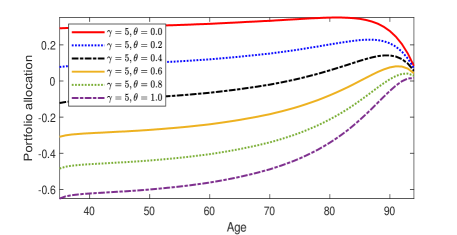

We plot the expected optimal trading strategies in Figure 2. A comparison between Figures 2(a) and 2(b) reveals that the breadwinner is likely to short the short-term nominal bond in favor of the high-risk premium from the long-term nominal bond. When goes to 1 (implying a higher valuation of the nominal value by the breadwinner), there is a decrease in shorting the short-term nominal bond and an increase in longing the long-term nominal bond. Figures 2(c) and 2(d) indicate that the breadwinner tends to long the inflation-linked bond and stocks. When goes to 1, the demand for inflation-linked bonds decreases, while the demand for stocks remains unchanged. The expected ITHD is also depicted in Figure 2. The and are zero, given the third and fourth rows of are zero. Finally, we observe that ITHD predominantly influences the evolution of expected investment strategies.

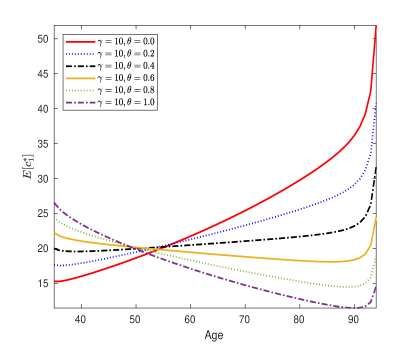

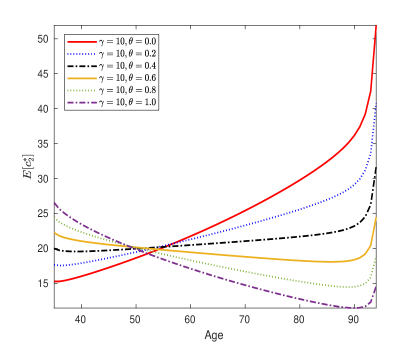

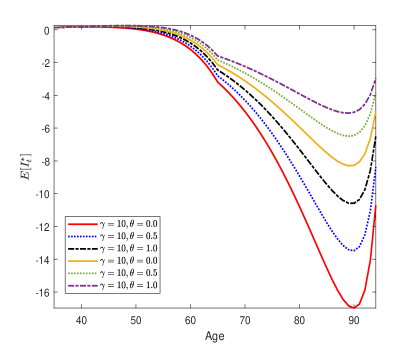

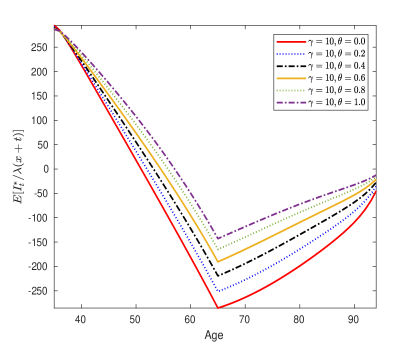

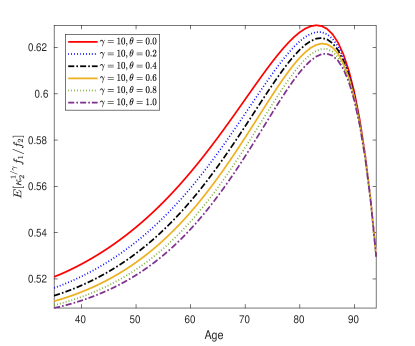

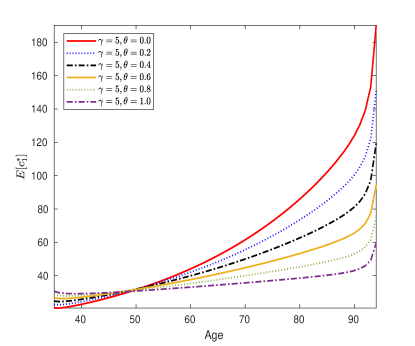

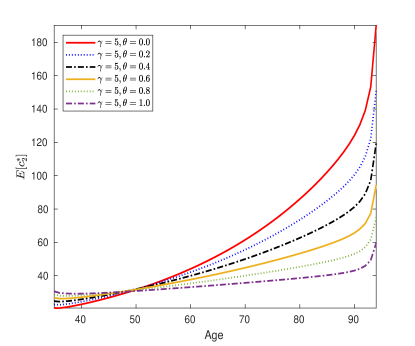

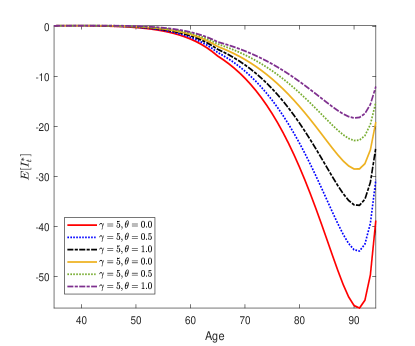

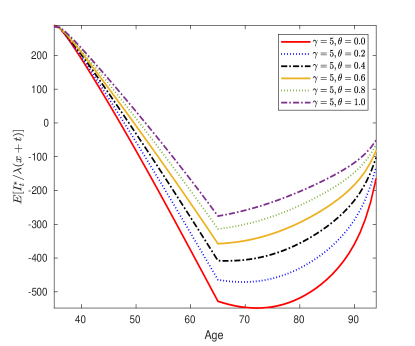

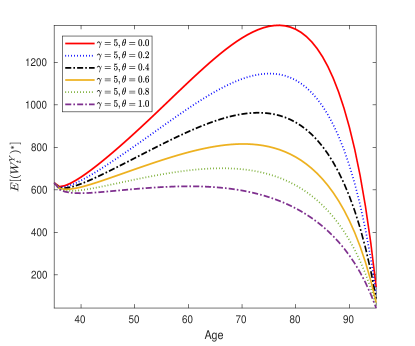

Figure 3 shows the expected optimal consumption and insurance strategies. It is noticeable that both the breadwinner and the family exhibit a higher consumption rate in their early years when they disregard inflation risk (i.e., the consumption pattern transitions from increasing to decreasing as approaches 1). From Figure 3(c), we obtain three key observations for the insurance premium: (1) change from positive to negative through time; (2) the positive range is significantly smaller than the negative range; (3) moves upward as approaches 1. Observation (1) can be understood in the context of the opposing roles of life insurance and annuities. Life insurance protects a breadwinner’s income before retirement, while an annuity serves as a source of “income” after retirement. Consequently, to safeguard income, the breadwinner purchases life insurance () prior to retirement and switches to an annuity () approaching retirement (as interpreted in Fischer, (1973), Pirvu and Zhang, (2012), and Shen and Wei, (2016)). Observation (2) is reflected in the maximum positive value in Figure 3(c) being 0.277k USD per year and the maximum negative value being 16.04k USD per year. This aligns with the real-world scenario where life insurance is considerably cheaper than an annuity. Despite the significant price gap, Figure 3(d) demonstrates that life insurance and annuities’ expected payoffs (insurance face value) are within the same range. Observation (3) reveals that the demand for life insurance increases and the demand for annuity decreases when the family ignores inflation risk. In addition to life insurance demand, we also examined the breadwinner’s bequest demand. After rearranging (37), we define the bequest-wealth ratio as

| (44) |

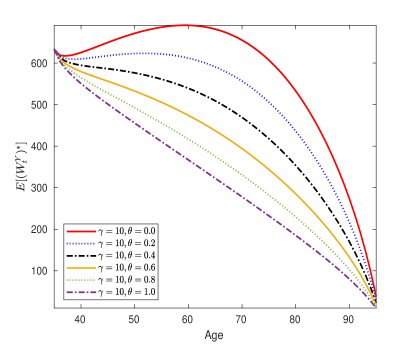

where the right-hand side is the ratio of the death benefit over the surplus process. We plot the expected curves of surplus process and wealth-bequest ratio in Figures 3(e) and 3(f). The figures show that they both perform a hump shape and move downward when the inflation risk is ignored.

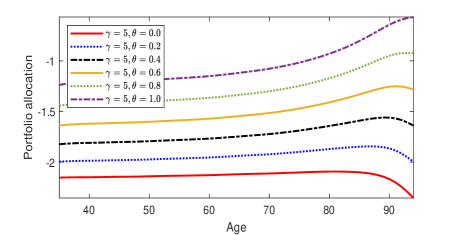

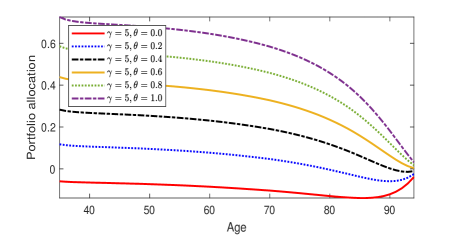

We also plot the optimal strategies under in Figures 4 and 5 as the family becomes more risk-seeking. Compared to the case of , we find: (1) the family will short more short-term nominal bonds and long more long-term nominal bonds, inflation-linked bonds, and stocks. (2) Their demand for life insurance decreases while their annuity demand increases. (3) Their expected surplus process sharply increases, but their bequest-wealth ratio slightly declines.

In general, the whole family increases their life insurance demand and reduces their annuity demand when ignoring the inflation risk. This observation leads us to two key conclusions: (1) Money illusion might contribute to the annuity puzzle, which is a phenomenon of individuals not purchasing sufficient annuities to fund their retirement. (2) Promoting inflation education could increase retirees’ voluntary purchase of annuities.

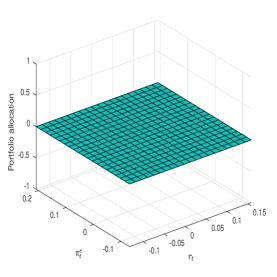

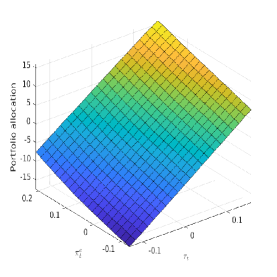

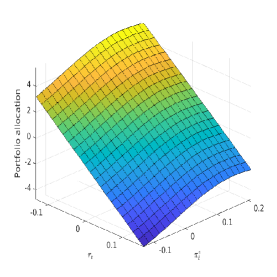

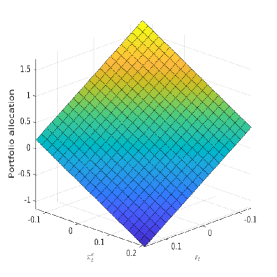

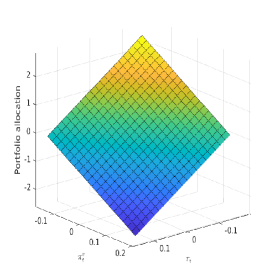

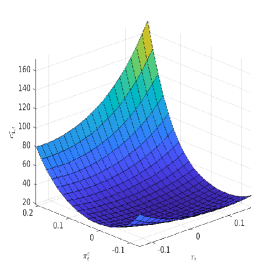

4.3 Sensitivity of optimal strategies concerning the two factors

This section performs a static analysis of optimal strategies, considering two factors . For all figures in this section, the range for is set as , and for , it is . These ranges represent the maximum values for and , respectively, in the Monte Carlo simulation. This simulation is conducted with 10,000,000 paths, with a time step of one year.

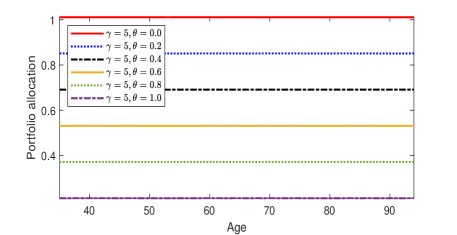

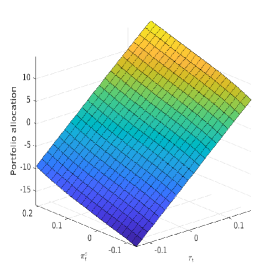

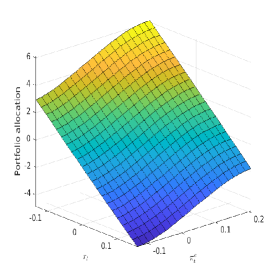

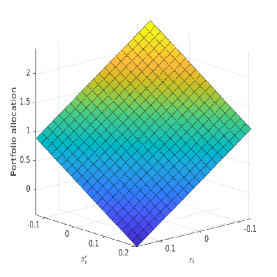

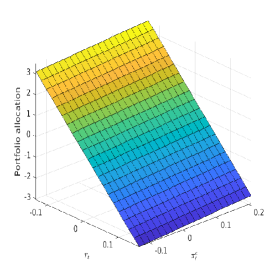

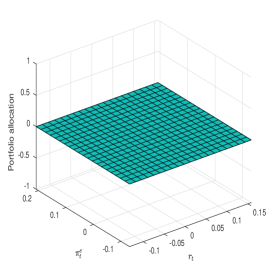

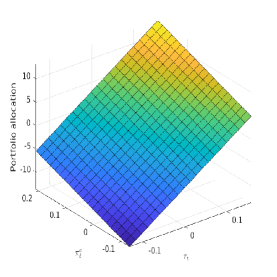

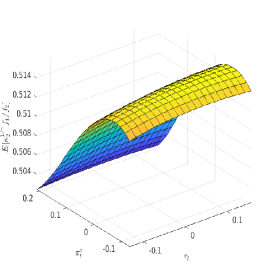

Figure 6 illustrates the optimal trading strategy considering two factors without money illusion (). The demand for nominal bonds escalates when the expected inflation increases. On the other hand, the demand for short-term nominal bonds rises with the real short rate , while the demand for long-term nominal bonds shows an inverse relation. This outcome indicates that short-term nominal bonds are more favorable when two factors fluctuate over a short period. Figures for inflation-linked bonds and stocks are also presented, showing a decrease when and increase. In addition to the optimal trading strategy , we plot the figures for standard myopic demand (SMD) and intertemporal hedging demand (ITHD). According to (43), and are null as the third and fourth entries of are zeros. Furthermore, the inflation hedging demand (IFHD) is outlined in Table 2, depicted as a constant vector that decreases linearly with . Our sensitivity analysis reveals that ITHD primarily shapes the breadwinner’s allocation in long-term nominal bonds, whereas SMD governs the allocations to the other three financial instruments.

Figure 7 shows the optimal trading strategy under . When compared with Figure 6, it is evident that when the entire family ignores inflation risk, they make several adjustments to their short-period allocations: (1) They purchase more short-term nominal bonds and fewer long-term nominal bonds. (2) They reduce their long positions and increase their short positions in inflation-linked bonds. (3) Their trading strategy for stocks remains relatively unchanged.

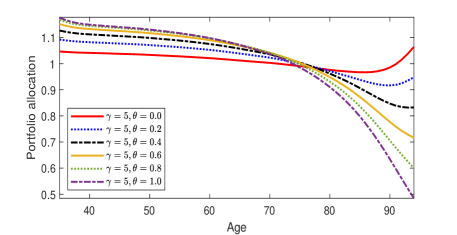

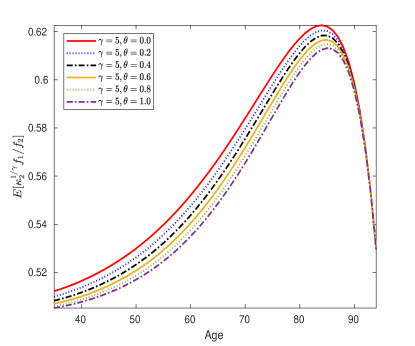

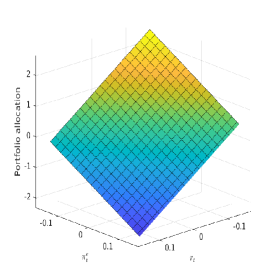

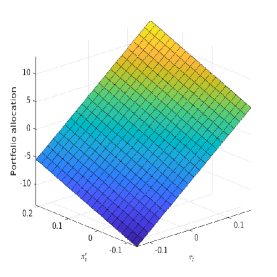

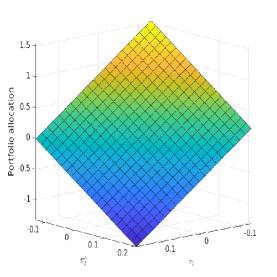

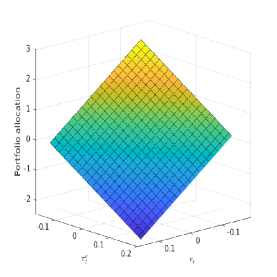

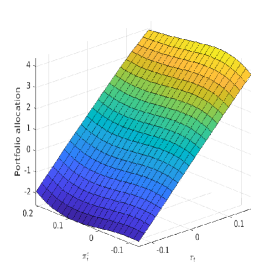

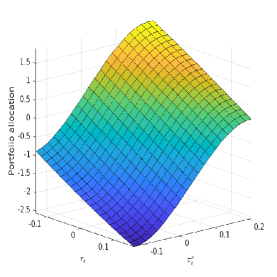

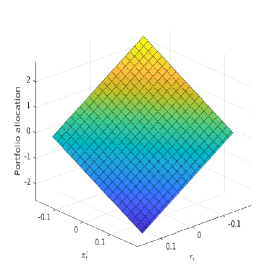

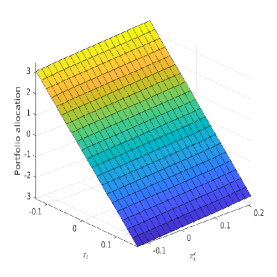

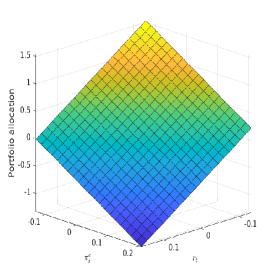

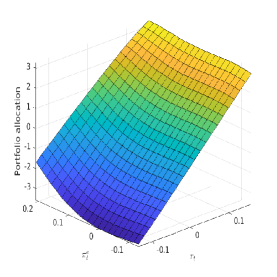

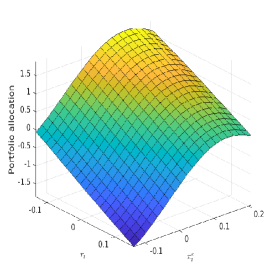

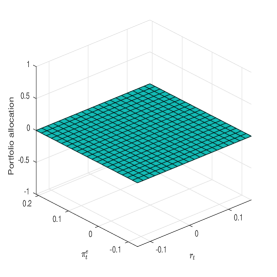

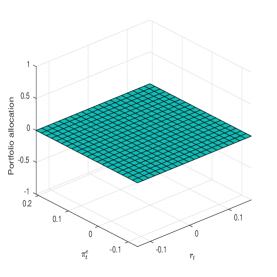

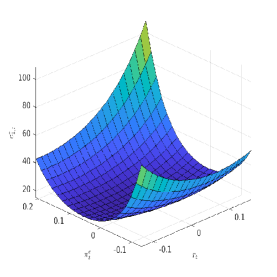

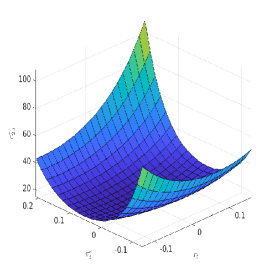

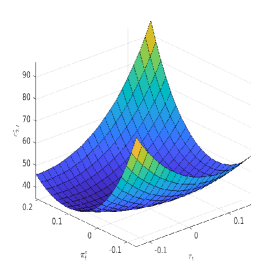

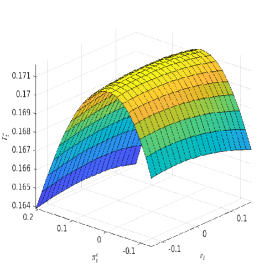

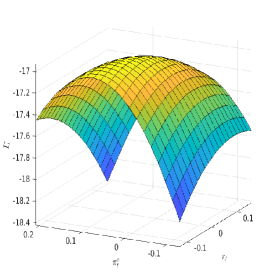

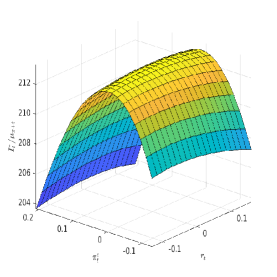

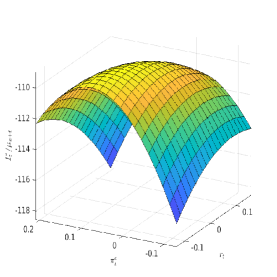

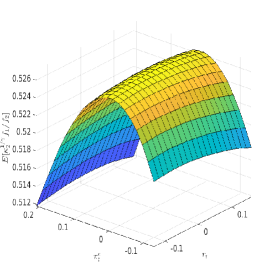

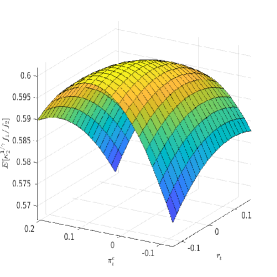

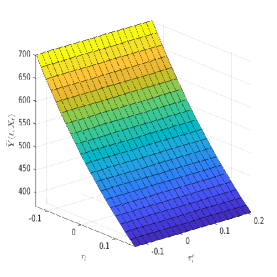

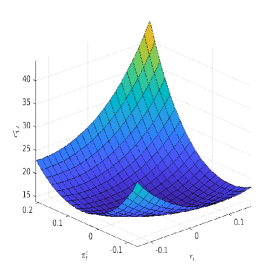

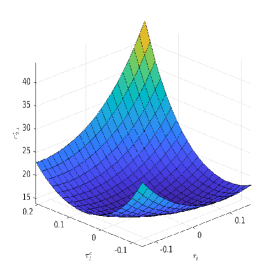

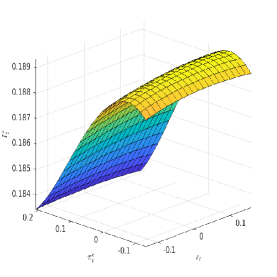

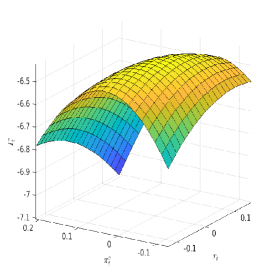

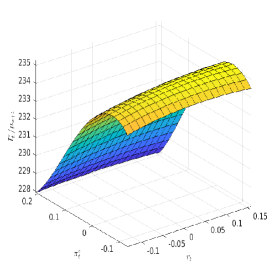

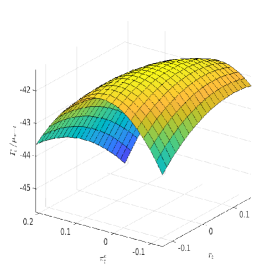

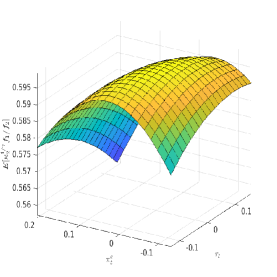

Figure 8 plots the optimal consumption and insurance/annuity strategies when . The results show that the family’s consumption and annuity purchases follow an upward “U-shape” with respect to the two factors (see Figure 8(f), the negative downward “U-shape” of means a positive upward “U-shape” annuity demand). In comparison, life insurance purchases exhibit a downward “U-shape” with two factors. In other words, when the real short rate and the expected inflation rate are both high or low, the family increases their consumption and annuity purchases while reducing their life insurance purchases. A potential explanation for the above observation is that life insurance protects future income, acting as a substitute for current consumption. Simultaneously, annuities function as a source of current income, supplementing current consumption. As a result, annuity demand shows an upward “U-shape” aligned with consumption. In contrast, life insurance demand performs a downward “U-shape”. Moreover, we also find the following interesting findings: (1) Life insurance demand is more sensitive to expected inflation than to the real short rate. (2) Annuity demand is sensitive to expected inflation and real short rates. Lastly, according to (44), we plot the figures for the bequest-wealth ratio and future income. The result shows that the bequest-wealth ratio primarily shapes the demand for life insurance and annuities.

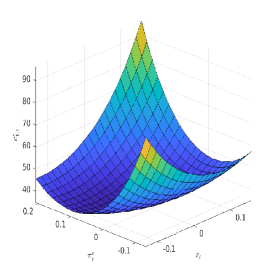

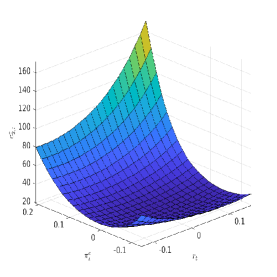

Figure 9 displays the optimal consumption, life insurance, and annuity strategies when . Compared with Figure 8, we find that the family ignoring the inflation risk will: (1) consume more in their early years and consume less in their old years, (2) buy more insurance and fewer annuities, and (3) slightly decrease their bequest-wealth demand. These results coincide with the sensitivity analysis to age, as detailed in Section 4.2.

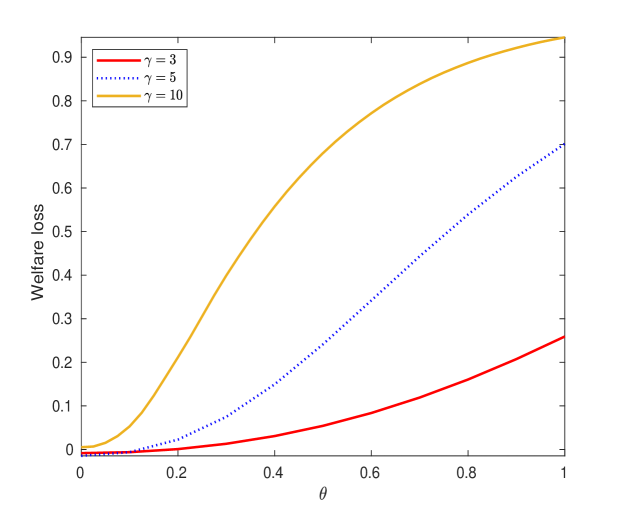

4.4 Welfare loss

This section evaluates the welfare loss resulting from the money illusion. We presume the family is non-illusioned, demonstrating rational preferences and full awareness of inflation risk. Specifically, the family’s objective follows (9) under

We use to denote the value function when non-illusioned family adopts strategies (34) - (37) under . Additionally, we denote for the non-illusioned family forced to adopt strategies (34) - (37) under money-illusion degree . Obviously, the non-illusioned family will obtain a lower value function under the money-illusioned strategies, i.e.,

Inspired by Basak and Yan, (2010), Xue et al., (2019), Tan et al., (2020), and Wei and Yang, (2023), we define the welfare loss as

| (45) |

Substitute (33) into (45), we have

where is the function under . Solving it, we obtain the formula for welfare loss

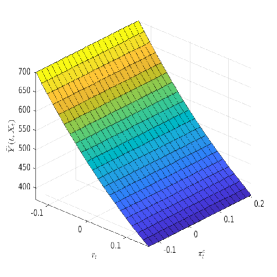

We employ the Monte Carlo method to simulate , with the results depicted in Figure 10. The findings reveal that welfare loss escalates with money illusion, and the rate of increase varies with relative risk aversion. For a family with , the maximum welfare loss is less than . For a family with , a welfare loss is experienced when the money illusion degree attains . For a family with , a welfare loss is incurred earlier when reaches . Generally, when a family becomes more risk-averse, they decrease their allocation to risky assets. The non-illusioned family perceives inflation-linked bonds as risk-free assets, while the illusioned family leans towards nominal bonds. Consequently, heightened risk aversion amplifies the welfare loss of money illusion.

5 Conclusion

This paper investigates a life-cycle model under the money illusion, where households exhibit a preference for nominal over real money. The household can invest a part of the money in nominal bonds, inflation-linked bonds, a stock index, and a nominal cash account and use the other part of the money to purchase life insurance and annuities. We formulate this problem as a random-horizon utility maximization problem and derive its corresponding explicit solutions under CRRA utility. Our model, calibrated to U.S. data, illustrates that money illusion elevates life insurance demand for young adults while diminishing annuity demand for retirees. Sensitivity analysis reveals that annuity demand exhibits an upward “U-shape” with respect to the real interest rate and expected inflation, consistent with the upward “U-shape” of consumption but contrasting with the downward “U-shape” of life insurance. Lastly, numerical simulations show that the welfare loss from the money illusion is significant, regardless of the risk aversion coefficient. In general, our paper enriches the existing literature by showing that money illusion can contribute to annuity puzzles. We recommend that insurance companies enhance their educational efforts regarding inflation risk to encourage voluntary annuity purchases among retirees.

References

- Abou-Kandil et al., (2012) Abou-Kandil, H., Freiling, G., Ionescu, V., and Jank, G. (2012). Matrix Riccati Equations in Control and Systems Theory. Birkhäuser.

- Basak and Yan, (2010) Basak, S. and Yan, H. (2010). Equilibrium asset prices and investor behaviour in the presence of money illusion. The Review of Economic Studies, 77(3):914–936.

- Bensoussan, (2004) Bensoussan, A. (2004). Stochastic Control of Partially Observable Systems. Cambridge University Press.

- Bernard et al., (2021) Bernard, C., Aquino, L. D. G., and Levante, L. (2021). Optimal annuity demand for general expected utility agents. Insurance: Mathematics and Economics, 101:70–79.

- Bernheim, (1991) Bernheim, B. D. (1991). How strong are bequest motives? evidence based on estimates of the demand for life insurance and annuities. Journal of political Economy, 99(5):899–927.

- Brunnermeier and Julliard, (2008) Brunnermeier, M. K. and Julliard, C. (2008). Money illusion and housing frenzies. The Review of Financial Studies, 21(1):135–180.

- Chen et al., (2009) Chen, C. R., Lung, P. P., and Wang, F. A. (2009). Stock market mispricing: money illusion or resale option? Journal of Financial and Quantitative Analysis, 44(5):1125–1147.

- Chen et al., (2013) Chen, C. R., Lung, P. P., and Wang, F. A. (2013). Where are the sources of stock market mispricing and excess volatility? Review of Quantitative Finance and Accounting, 41:631–650.

- Cocco et al., (2005) Cocco, J. F., Gomes, F. J., and Maenhout, P. J. (2005). Consumption and portfolio choice over the life cycle. The Review of Financial Studies, 18(2):491–533.

- David and Veronesi, (2013) David, A. and Veronesi, P. (2013). What ties return volatilities to price valuations and fundamentals? Journal of Political Economy, 121(4):682–746.

- Davidoff et al., (2005) Davidoff, T., Brown, J. R., and Diamond, P. A. (2005). Annuities and individual welfare. American Economic Review, 95(5):1573–1590.

- Deelstra et al., (2003) Deelstra, G., Grasselli, M., and Koehl, P.-F. (2003). Optimal investment strategies in the presence of a minimum guarantee. Insurance: Mathematics and Economics, 33(1):189–207.

- Donnelly et al., (2024) Donnelly, C., Khemka, G., and Lim, W. (2024). Money illusion in retirement savings with a minimum guarantee. Scandinavian Actuarial Journal, pages 1–24.

- Duffie and Kan, (1996) Duffie, D. and Kan, R. (1996). A yield-factor model of interest rates. Mathematical finance, 6(4):379–406.

- Durbin and Koopman, (2012) Durbin, J. and Koopman, S. J. (2012). Time series analysis by state space methods, volume 38. OUP Oxford.

- Eisenhuth, (2017) Eisenhuth, R. (2017). Money illusion and market survival. Macroeconomic Dynamics, 21(1):1–10.

- Ekeland et al., (2012) Ekeland, I., Mbodji, O., and Pirvu, T. A. (2012). Time-consistent portfolio management. SIAM Journal on Financial Mathematics, 3(1):1–32.

- Fehr and Tyran, (2001) Fehr, E. and Tyran, J.-R. (2001). Does money illusion matter? American Economic Review, 91(5):1239–1262.

- Fehr and Tyran, (2007) Fehr, E. and Tyran, J.-R. (2007). Money illusion and coordination failure. Games and Economic Behavior, 58(2):246–268.

- Fischer et al., (2023) Fischer, M., Jensen, B. A., and Koch, M. (2023). Optimal retirement savings over the life cycle: A deterministic analysis in closed form. Insurance: Mathematics and Economics, 112:48–58.

- Fischer, (1973) Fischer, S. (1973). A life cycle model of life insurance purchases. International Economic Review, pages 132–152.

- Fisher, (1928) Fisher, I. (1928). The money illusion. Adelphi Co.

- Hakansson, (1969) Hakansson, N. H. (1969). Optimal investment and consumption strategies under risk, an uncertain lifetime, and insurance. International Economic Review, 10(3):443–466.

- Han and Hung, (2021) Han, N.-W. and Hung, M.-W. (2021). The annuity puzzle and consumption hump under ambiguous life expectancy. Insurance: Mathematics and Economics, 100:76–88.

- Harvey, (1990) Harvey, A. C. (1990). Forecasting, Structural Time Series Models and the Kalman Filter. Cambridge university press.

- He and Zhou, (2014) He, X. D. and Zhou, X. Y. (2014). Myopic loss aversion, reference point, and money illusion. Quantitative Finance, 14(9):1541–1554.

- Honda and Kamimura, (2011) Honda, T. and Kamimura, S. (2011). On the verification theorem of dynamic portfolio-consumption problems with stochastic market price of risk. Asia-Pacific Financial Markets, 18(2):151–166.

- Huang and Milevsky, (2008) Huang, H. and Milevsky, M. A. (2008). Portfolio choice and mortality-contingent claims: The general hara case. Journal of Banking & Finance, 32(11):2444–2452.

- Huang et al., (2008) Huang, H., Milevsky, M. A., and Wang, J. (2008). Portfolio choice and life insurance: The crra case. Journal of Risk and Insurance, 75(4):847–872.

- Inkmann et al., (2011) Inkmann, J., Lopes, P., and Michaelides, A. (2011). How deep is the annuity market participation puzzle? The Review of Financial Studies, 24(1):279–319.

- Kizaki et al., (2024) Kizaki, K., Saito, T., and Takahashi, A. (2024). A multi-agent incomplete equilibrium model and its applications to reinsurance pricing and life-cycle investment. Insurance: Mathematics and Economics, 114:132–155.

- Koijen et al., (2011) Koijen, R. S., Nijman, T. E., and Werker, B. J. (2011). Optimal annuity risk management. Review of Finance, 15(4):799–833.

- Kraft, (2004) Kraft, H. (2004). Optimal portfolios with stochastic interest rates and defaultable assets. Springer Science & Business Media.

- Kwak and Lim, (2014) Kwak, M. and Lim, B. H. (2014). Optimal portfolio selection with life insurance under inflation risk. Journal of Banking & Finance, 46:59–71.

- Kwak et al., (2011) Kwak, M., Shin, Y. H., and Choi, U. J. (2011). Optimal investment and consumption decision of a family with life insurance. Insurance: Mathematics and Economics, 48(2):176–188.

- Li et al., (2023) Li, X., Yu, X., and Zhang, Q. (2023). Optimal consumption and life insurance under shortfall aversion and a drawdown constraint. Insurance: Mathematics and Economics, 108:25–45.

- Lioui and Tarelli, (2023) Lioui, A. and Tarelli, A. (2023). Money illusion and tips demand. Journal of Money, Credit and Banking, 55(1):171–214.

- Lockwood, (2012) Lockwood, L. M. (2012). Bequest motives and the annuity puzzle. Review of economic dynamics, 15(2):226–243.

- Miao and Xie, (2013) Miao, J. and Xie, D. (2013). Economic growth under money illusion. Journal of Economic Dynamics and Control, 37(1):84–103.

- Milevsky and Young, (2007) Milevsky, M. A. and Young, V. R. (2007). Annuitization and asset allocation. Journal of Economic Dynamics and Control, 31(9):3138–3177.

- Munk and Sørensen, (2010) Munk, C. and Sørensen, C. (2010). Dynamic asset allocation with stochastic income and interest rates. Journal of Financial Economics, 96(3):433–462.

- Pirvu and Zhang, (2012) Pirvu, T. A. and Zhang, H. (2012). Optimal investment, consumption and life insurance under mean-reverting returns: The complete market solution. Insurance: Mathematics and Economics, 51(2):303–309.

- Pliska and Ye, (2007) Pliska, S. R. and Ye, J. (2007). Optimal life insurance purchase and consumption/investment under uncertain lifetime. Journal of Banking & Finance, 31(5):1307–1319.

- Rees, (1922) Rees, E. (1922). Graphical discussion of the roots of a quartic equation. The American Mathematical Monthly, 29(2):51–55.

- Richard, (1975) Richard, S. F. (1975). Optimal consumption, portfolio and life insurance rules for an uncertain lived individual in a continuous time model. Journal of Financial Economics, 2(2):187–203.

- Shafir et al., (1997) Shafir, E., Diamond, P., and Tversky, A. (1997). Money illusion. The quarterly journal of economics, 112(2):341–374.

- Shen and Wei, (2016) Shen, Y. and Wei, J. (2016). Optimal investment-consumption-insurance with random parameters. Scandinavian Actuarial Journal, 2016(1):37–62.

- Svedsäter et al., (2007) Svedsäter, H., Gamble, A., and Gärling, T. (2007). Money illusion in intuitive financial judgments: Influences of nominal representation of share prices. The Journal of Socio-Economics, 36(5):698–712.

- Tan et al., (2020) Tan, K. S., Wei, P., Wei, W., and Zhuang, S. C. (2020). Optimal dynamic reinsurance policies under a generalized denneberg’s absolute deviation principle. European Journal of Operational Research, 282(1):345–362.

- Wang and Chen, (2024) Wang, T. and Chen, Z. (2024). Optimal portfolio and insurance strategy with biometric risks, habit formation and smooth ambiguity. Insurance: Mathematics and Economics, 118:195–222.

- Wei et al., (2020) Wei, J., Cheng, X., Jin, Z., and Wang, H. (2020). Optimal consumption–investment and life-insurance purchase strategy for couples with correlated lifetimes. Insurance: Mathematics and Economics, 91:244–256.

- Wei and Yang, (2023) Wei, P. and Yang, C. (2023). Optimal investment for defined-contribution pension plans under money illusion. Review of Quantitative Finance and Accounting, 61(2):729–753.

- Xue et al., (2019) Xue, X., Wei, P., and Weng, C. (2019). Derivatives trading for insurers. Insurance: Mathematics and Economics, 84:40–53.

- Yaari, (1965) Yaari, M. E. (1965). Uncertain lifetime, life insurance, and the theory of the consumer. The Review of Economic Studies, 32(2):137–150.

- Zhang et al., (2021) Zhang, J., Purcal, S., and Wei, J. (2021). Optimal life insurance and annuity demand under hyperbolic discounting when bequests are luxury goods. Insurance: Mathematics and Economics, 101:80–90.

Appendix A Proofs of Proposition 3.1 to Proposition 3.3

Proof.

We first prove the Proposition 3.3, i.e., is the candidate solution to the HJB equation (24). The derivatives of the candidate solution are given by

Substitute these derivatives into the HJB equation (24), we can verify that the equality holds. Thus, is indeed the candidate solution to the HJB equation (24). By inserting into (26)-(29), we can then derive the optimal strategies (34)-(37).

Appendix B Proof of Proposition 3.4

We can establish the global existence of by utilizing Theorems 4.1.4. and 4.1.6. from Abou-Kandil et al., (2012). It is worth noting that their comparison theorem can be easily adapted from a semi-definite matrix case to a definite matrix case. Since is both existent and negative for all , the candidate solution in (33) also exists.

To prove the verification theorem, we define the value process for any and

| (46) |

By Ito’s formula, we have

| (47) |

where is the infinitesimal generator defined in (25) and satisfies

| (48) |

Next, fix and denote the conditional expectation of the value process as

where is short for . Then, we have

| (49) |

For candidate solutions, is the special case of when , , and . Moreover, is the special case of when . One can easily verify and first, then use the same approach to verify by induction. We only verify in the following part since has the most complex form.

The proof verification theorem has three steps:

-

Step 1:

Verify the optimal strategy is in the admissible set .

Recall from (36)

which satisfies a linear growth with due to the linear growth of and . Next, substitute (34) - (37) into (23), we have

(50) where . Given that the drift term and volatility term of SDE (1) are almost surely sample continuous, we can utilize Proposition 1.1 in Kraft, (2004) to demonstrate the existence of a unique strong solution for SDE (23) under . As a result, we can conclude that .

-

Step 2:

Verify for any .

We first introduce the following useful lemma.

Lemma B.1.

Assume a -dimensional stochastic process is driven by a -dimensional Brownian motion

where is a constant n-dimensional vector, is a borel function and a continuous function

satisfying

where is the Euclidean norm and represents the set of Lebesgue measurable function , such that . If a stochastic process , , grows linearly with respect to ( ), then we have

where

Proof.

The proof is an extension of Lemma 4.1.1. in Bensoussan, (2004) to the case where and share the same Brownian motion. ∎

-

Step 3:

Verify under the optimal strategy .

Since maximizes the HJB (24) and is the solution to (24), the equality in (51) holds

for , where

It is straightforward to demonstrate that satisfies the linear growth condition. Thus, according to Lemma B.1, is a martingale. Considering and , we can establish the following equality for .

(53) By combining (52), (53), and (49), we can verify that

, and obtained from (34)-(37) represents the optimal strategy.

The proof is complete.

Appendix C Proof of Proposition 3.5

Proof.

By substituting into (40), we obtain a quartic equation

where the coefficients are given as follows

Moreover, the discriminant of is defined as

As stated in Rees, (1922), if condition (41) is satisfied, then (40) has four distinct real roots, which implies that the Hamiltonian matrix has four different real eigenvalues. This guarantees the diagonalizability of and the full rank of its eigenvector matrix . According to Radon’s lemma (see Theorem 3.1.1. in Abou-Kandil et al.,, 2012), we can express , and the existence and negative definiteness of can be derived from (42). Given that exists and for , the candidate solution in (33) is globally existent.

Similar to Appendix B, the verification theorem can be proven in three steps. However, there are two differences in this case. First, in Step 1, we need to verify that . It is straightforward to observe that the solution to (1) satisfies

which satisfies the requirement of the admissible set (3.5). The argument for the existence of a strong solution remains the same as Step 1 in Appendix B.

Second, in Step 2, we can adopt Fatou’s lemma rather than Lemma B.1 to prove the inequality (52), as the value process (B) is bounded below by zero when . Define

and let for . For , the stochastic integral is a martingale. Therefore, by using (24), (B), and , we obtain

| (54) |

Given that and for any under , we can prove

| (55) | |||||

where the first inequality follows from Fatou’s lemma and the second inequality is obtained by taking conditional expectations on both sides of (C). This completes the proof. ∎

Appendix D Estimation details for financial market

Let denote the vector of states in the financial market. Then, it evolves as follows

where

and represents the -th unit vector in and . Applying Ito’s formula, the transition equation for states satisfies

| (56) |

where

For monthly data, we set . Ten financial variables are observed each month, including the inflation index, equity index, and yield rates of nominal zero-coupon bonds across eight different maturities. Following Koijen et al., (2011), we assume that the yield rates are observed with independent errors. Let denote the yield rates of nominal zero-coupon bonds at time with maturity . Then, the measurement equation for the states can be expressed as

| (57) |

where is the observation vector. Furthermore, the coefficients in (57) are

where and are given by (4) and (5) respectively, is the 2nd-order identity matrix, and are the measurement errors in yields to be estimated.

Let denote the set of past observations for . We define the conditional means and variances as follows

Next, we can express the Kalman filter iteration for (56) and (57) as

Let represent the vector of all model parameters, which encompasses 21 parameters in Table 1 and eight parameters in . Then, we can derive the log-likelihood function from the “prediction error decomposition” (see Chapter 3.4 in Harvey, (1990))

Finally, we can utilize the “SSM” package in Matlab to estimate the maximum likelihood estimator (MLE) of the unknown parameters . Alternative estimation methodologies include the Expectation–maximization (EM) algorithm and Markov chain Monte Carlo (MCMC) algorithm, as detailed in Chapters 7.3.4 and 13.4 of Durbin and Koopman, (2012).