\ul

Temporal Relational Reasoning of Large Language Models for Detecting Stock Portfolio Crashes

Abstract.

Stock portfolios are often exposed to rare consequential events (e.g., 2007 global financial crisis, 2020 COVID-19 stock market crash), as they do not have enough historical information to learn from. Large Language Models (LLMs) now present a possible tool to tackle this problem, as they can generalize across their large corpus of training data and perform zero-shot reasoning on new events, allowing them to detect possible portfolio crash events without requiring specific training data. However, detecting portfolio crashes is a complex problem that requires more than basic reasoning abilities. Investors need to dynamically process the impact of each new information found in the news articles, analyze the the relational network of impacts across news events and portfolio stocks, as well as understand the temporal context between impacts across time-steps, in order to obtain the overall aggregated effect on the target portfolio. In this work, we propose an algorithmic framework named Temporal Relational Reasoning (TRR). It seeks to emulate the spectrum of human cognitive capabilities used for complex problem-solving, which include brainstorming, memory, attention and reasoning. Through extensive experiments, we show that TRR is able to outperform state-of-the-art solutions on detecting stock portfolio crashes, and demonstrate how each of the proposed components help to contribute to its performance through an ablation study. Additionally, we further explore the possible applications of TRR by extending it to other related complex problems, such as the detection of possible global crisis events in Macroeconomics.

1. Introduction

In equity investing (Koa et al., 2023, 2024), investors typically form stock portfolios (Markowitz, 1952) to diversify their risk across multiple stocks. This could be done by selecting the stocks from across different categories, based on geographical regions (Rouwenhorst, 1998) and/or business sectors (Che et al., 2022), etc. , in order to dampen the impacts of events that affect any specific category. However, there also exist rare, fat-tailed events (Mandelbrot, 2001) that are unprecedented in history and cause the market to be increasingly interconnected (Taleb, 2007), which can result in crashes (e.g., 2007 global financial crisis (Goldin and Vogel, 2010), 2020 COVID-19 stock market crash (Naeem et al., 2021)). Even though stock portfolios have extensively considered various risks when they are curated, they are often still ill-prepared to handle these events (Taleb, 2007), as they do not have past statistics or historical information to learn from. There are currently limited works (Taleb et al., 2022) on detecting portfolio crash events.

Today, Large Language Models (LLMs) present a possible toolset for detecting these crash events, without requiring specific training data. This stems from their known capabilities to perform zero-shot reasoning (Kojima et al., 2022), which can be attributed to their ability to generalize (Bender et al., 2021; Yang et al., 2023) across the large corpus of data they have previously been trained on. This allows them to identify repeating patterns on new emerging events, and potentially detect possible crashes before they happen. In this work, we explore the use of LLMs to detect possible stock portfolio crashes, given an input set of financial news events.

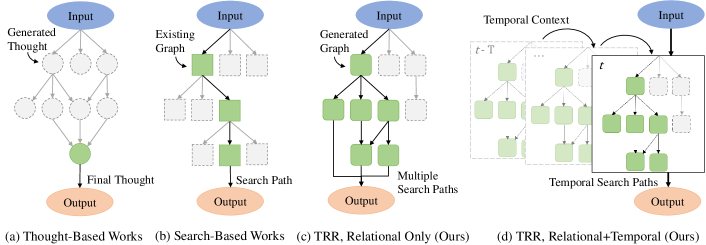

Detecting portfolio crashes is a complex problem that requires more than basic reasoning abilities. Currently, there are some reasoning frameworks for LLMs to handle complex tasks: Thought-based frameworks (e.g., Tree-of-Thoughts (ToT) (Yao et al., 2024), Graph-of-Thoughts (GoT) (Besta et al., 2024)) break down a task into generated sub-steps that can be merged to solve the task; Search-based frameworks (e.g., Think-on-Graph (ToG) (Sun et al., 2024)) search through an existing Knowledge Graph of facts to find a reasoning path that can answer questions on a single entity. However, among these methods, we can still identify three challenges for our task. (1) The current methods focus mainly on tackling isolated problems, such as solving a task through sequential thoughts or answering questions from a static graph of information. However, these methods do not deal with the constantly evolving nature of news events, which would require the dynamic processing of new information. (2) Portfolio crashes are often caused by the unexpected interconnectivity of its constituent stocks in response to unprecedented events (Goldin and Vogel, 2010; Naeem et al., 2021). While current frameworks combine thoughts or search for a single path on a Knowledge Graph (see Figure 1), they do not reason across multiple search paths, which could reveal these interconnectivity between news events and portfolio stocks within the graph. (3) It is also known from stock prediction works that there exists temporal context dependency (Xu and Cohen, 2018; Hu et al., 2018) between news events when considering their impacts on stock prices. While there are some LLM works on temporal graphs (Zhang et al., 2024; Xiong et al., 2024), these works focus on performing question-answering on individual graphs with temporal information in the nodes or edges, and do not handle information across multiple graphs captured at different time-steps.

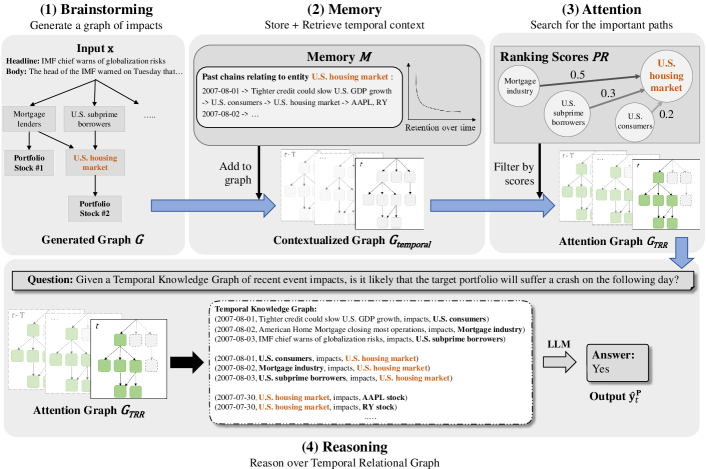

To tackle the above-mentioned problems, we propose an algorithmic framework named Temporal Relational Reasoning (TRR), which seeks to emulate the spectrum of human cognitive capabilities that are used for complex problem-solving (see Figure 2). Given a set of financial news articles, we brainstorm for all possible impacts on the target portfolio of stocks by dynamically generating chains of sub-impacts through related entities. To understand the temporal context of these impacts, we simulate the associative memory of humans by retrieving past related events which have affected the same entities, from a stored temporal ”memory-bank” that decays over time (Zhong et al., 2024). To analyze the interconnectivity across the relational network of impacts, we first mimic the attention of investors by utilizing the PageRank algorithm (Page et al., 1999), to filter the most important impact chains that will affect the target portfolio, and reduce the size of the final graph. We then emulate investors’ reasoning process by reasoning across the filtered temporal-relational graph, to determine if a crash is likely to occur.

To demonstrate the effectiveness of TRR, we perform extensive experiments over multiple portfolios and time periods, and show that our method can outperform deep-learning models and other LLM reasoning frameworks in predicting portfolio crashes. Through an ablation study, we also demonstrate how each component of TRR helps to contribute to its performance. Furthermore, we explore the applications of our method to other related complex problems by extending it to a macroeconomic setting. By viewing the global economy as a network of regional economies, we determine if any series of news could result in possible global financial crises, by tracing their overall impacts using TRR. We find that TRR can also predict crisis events more effectively than other available methods.

The main contributions of this work can be summarized as below:

-

•

We investigate the limitations of zero-shot reasoning LLMs on complex problems such as detecting portfolio crashes, which require the processing of information across a temporal-relational network.

-

•

We propose a solution that uses a LLM to reason over a self-generated, temporal-relational graph. This is done through an algorithmic framework that emulates the human cognitive capabilities used for solving complex problems, which include brainstorming, memory, attention and reasoning.

-

•

We conduct extensive experiments across multiple portfolio structures and time periods, and show that our TRR framework can detect portfolio crashes more effectively than state-of-the-art models. Given these results, we further explore other possible applications of TRR on related complex problems, and utilize the framework to detect global crisis events in the macroeconomics setting.

2. Related Works

Relational Stock Prediction Utilizing relational information to predict stock prices have been widely explored in multiple previous works. Early works (Ding et al., 2014, 2015) have studied the use of relational tuples in the form of (Actor, Action, Object, Timestamp) to learn embeddings, such that similar events (Ding et al., 2014) or similar stock entities (Ding et al., 2015) would have similar representative vectors. The tuples are generated with rule-based techniques (Zhang and Clark, 2011) from news headlines, as opposed to the LLM-based method in our work.

Later works would improve on this using graph-based methods (Ding et al., 2016; Feng et al., 2019; Sawhney et al., 2020), by learning embeddings across a Knowledge Graph to represent stock entities. These works utilize stock relational information from external Knowledge Graphs such as Freebase (Bollacker et al., 2008) or Wikidata (Vrandečić and Krötzsch, 2014) to train their models. However, these models rely mainly on the static relation information retrieved from a central database, and do not consider possible changes in the connectivity between stocks, that could result from news events.

In a more recent work (Chen et al., 2023), LLMs were used to infer relations between stocks from news headlines, resulting in more dynamic relational data. This information is then used to generate stock embeddings using a Graph Neural Network, which are used to train a deep-learning model for stock prediction. In contrast to this, our work focus on zero-shot reasoning frameworks in order to detect crashes across a portfolio of stocks, that often occur due to events that are unprecedented in historical training data.

Reasoning Frameworks for Large Language Models LLMs are known for their zero-shot reasoning capabilities (Kojima et al., 2022), which has been largely attributed to their ability to generalize knowledge across the large corpus of data it was trained on (Yang et al., 2023; Brown et al., 2020). To enhance this capability, researchers have proposed frameworks to tackle more advanced tasks, such as ToT (Yao et al., 2024), GoT (Besta et al., 2024). In particular, these works were stated (Yao et al., 2024) to be inspired by general problem-solving strategies from the 1950s (Newell et al., 1959), which can be seen as searching through a combinatorial problem space to find a task solution. Since then, the original research has led to works discussing more complex problems with multiple entities (Greff et al., 2020; Spiliopoulou, 2022).

Another line of research deals with enhancing the reliability of LLMs’ responses by using Knowledge Graphs containing external information, such as StructGPT (Jiang et al., 2023) and ToG (Sun et al., 2024). A key observation from these works is the ability of LLMs to reason over Knowledge Graph inputs, provided in the form of Knowledge tuples. However, while these works focus on extracting specific tuples from an existing Knowledge Graph of information to answer questions, we extract a sub-graph of tuples from a generated graph of impacts to understand market conditions and detect possible portfolio crashes.

3. Temporal Relational Reasoning

Our TRR framework seeks to emulate the spectrum of human cognitive capabilities that are used together for complex problem-solving (see Figure 2). It consists of four phases: 1. Brainstorming, which generates a graph of sub-impacts on affected entities; 2. Memory, which retrieves relevant past impact chains that contain the same entities; 3. Attention, which extracts the most important impact chains to form a new sub-graph; 4. Reasoning, which reasons over this sub-graph to to determine if a portfolio crash will occur. We will formalize the task and the four cognitive phases in this section.

For our task, we start with a portfolio of stocks, , where is a single stock and . For each day, given a set of news articles , we aim to make a binary prediction on whether a crash will occur on portfolio on the following day, i.e., .

3.1. Brainstorming

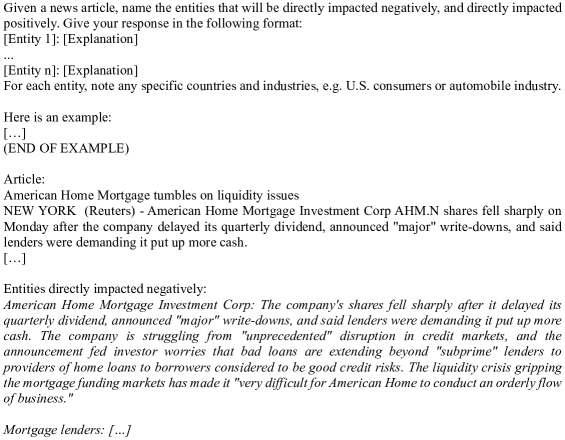

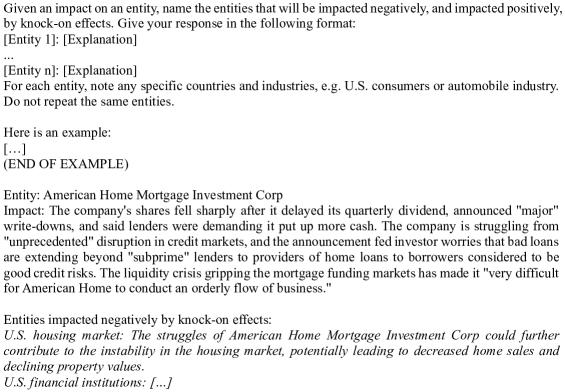

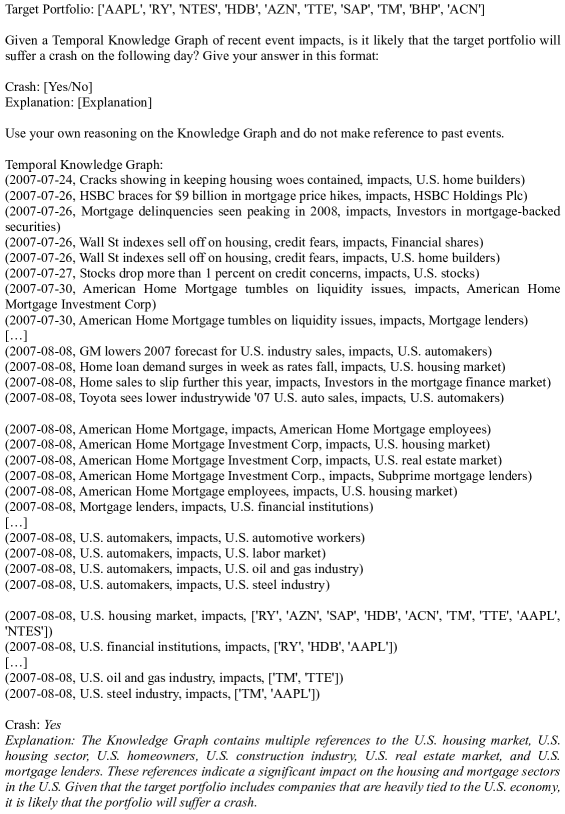

To obtain the overall impact of each news event on our selected portfolio, we first brainstorm for all possible chains of sub-impacts that lead to its constituent stocks. We model this as a directed graph . The set of vertices is , which starts from each news article , passes through all impacted sub-entities where , and ends at the portfolio stocks . The set of edges is , which simply represent the direction of impact between the vertices. Some possible examples are (American Home Mortgage closing most operations, impacts, Mortgage industry) and (Mortgage industry, impacts, U.S. housing market).

To generate new vertices for the graph, we iteratively prompt an LLM to generate possible affected entities given each news article or previously affected sub-entity. Hence, for all vertices at iteration , we have , where is the number of new vertices generated. This is done iteratively until the chain of impacts reaches a portfolio stock , or the max number of iterations is reached. Repeated entities are merged (Besta et al., 2024) as a single vertex on the graph.

For notation, we also refer to each individual chain of impact as , where . Each chain starts from a news article , passes through any number of impacted entities, and ends at a stock .

3.2. Memory

For understanding the temporal context of news events, we equip TRR with a memory module, which stores all previous mentions of impacted sub-entities. We denote the memory module as , where is the collection of all the previous impact chains that contains entity . With the memory module, we are then able to perform retrieve and store functions:

-

(a)

On each day, for each impacted entity that is generated by the LLM, we search the memory module for its previous mentions and add them to our daily graph , which give us a new temporal contextualized graph . We can obtain: .

-

(b)

At the end of each day, we then update the memory module with the daily chains of impact, i.e., , which stores the temporal context for future time periods.

Here, the additional temporal context allows us to form a temporal relational graph , which represents the Relational+Temporal variant of our TRR framework (see Figure 1).

In addition, human collective memory on news events tend to fade over time (Halbwachs, 2020; Au Yeung and Jatowt, 2011), which can lessen their impact on the market. The temporal decay of memory has previously been modelled with an exponential decay in both the social sciences (Lorenz-Spreen et al., 2019; Halbwachs, 2020) and LLM works (Zhong et al., 2024). Following this, we also track the memory retention of each impact with a variable , where is the time-step when entity impacted entity , and is a decay rate constant to be determined. The variable will be used in the next phase to decide if an impact is considered in the market context.

3.3. Attention

The overall contextualized graph is too large to be used in LLMs, given their token limits. While other works deal with this by merging thoughts (Besta et al., 2024) or finding a single answering path (Sun et al., 2024), we want to maintain a relational graph of information (see Figure 1) to provide the LLM with an overview of the market. In a similar fashion, the amount of news that investors can process each day is also limited, and their attention is usually focused on more important information (Xu et al., 2023; Hirshleifer et al., 2011).

contains a network of impact chains, with varying impact strengths on the target portfolio. To obtain the most important information on this network, we draw inspiration from the PageRank algorithm (Page et al., 1999) by assigning ranking scores to each entity. This is done by iteratively transferring scores across the entities following the direction of impact, until the convergence of scores. Furthermore, the scores are weighted (Xing and Ghorbani, 2004) based on their retention in memory from the previous phase. For an entity and the set of its parent vertices , the score it receives in each iteration can be formulated as , where is the number of outgoing impacts from entity .

Using the ranking scores , we then filter for all the impact chains containing the top- highest scoring entities, where is to be defined. These are used to form a new sub-graph , which represents the most important information for each day that investors would pay attention to.

3.4. Reasoning

Finally, to determine if a portfolio crash will occur, we reason over the generated temporal-relational graph . This emulates the reasoning process of investors, who will assess their portfolio risks by considering the most relevant news impacts and how the constituent stocks would be interconnected (Baitinger and Papenbrock, 2017; De Prado, 2016). Following previous graph-based LLM works (Sun et al., 2024; Zhang et al., 2023), we let a LLM reason on the graph in the form of relational tuples (Yuan et al., 2024). Each tuple can be formalized as , where is the time-step when the impact was generated, and are the subject and object entities, and is the direction of impact. Given the stock portfolio and the graph in the form of tuples, we then prompt the LLM to generate our portfolio crash prediction. This step can be formalized as . An example of the prompt can be found in Appendix C.

4. Experiments

We extensively evaluate TRR across multiple portfolios and time periods to demonstrate its effectiveness. We form two diversified portfolios using common investor strategies: (1) Country-neutral portfolio, where each constituent stock company is based in a different country (Rouwenhorst, 1998); (2) Sector-neutral portfolio, where each stock company is from a different market sector (Che et al., 2022) (see Appendix A).

For the experiments, we select three notable time periods containing events which have caused a big impact on the stock market: (a) June-August 2007 (Global financial crisis); (b) March-May 2010 (Greek government debt crisis); (c) January-March 2020 (COVID-19 stock market crash). Each time period consists of three months, and the mentioned events can be found towards its middle, which allows us to capture news impacts from both the stable (i.e., before portfolio crash) and crash periods.

| Dataset | 2007 | 2010 | 2020 | ||||||

|---|---|---|---|---|---|---|---|---|---|

| Time Period |

|

|

|

||||||

|

2,831 | 3,303 | 7,177 | ||||||

|

0.108 | 0.078 | 0.161 | ||||||

|

0.046 | 0.063 | 0.210 |

4.1. Dataset and Evaluation Metrics

| Model | 2007 | 2010 | 2020 | |||

|---|---|---|---|---|---|---|

| Country-Neu | Sector-Neu | Country-Neu | Sector-Neu | Country-Neu | Sector-Neu | |

| BiGRU+Att | ||||||

| IO | ||||||

| CoT | ||||||

| GoT | ||||||

| ToG | ||||||

| TRR (Ours) | ||||||

For news data, we use the Reuters financial news dataset (Ding et al., 2014), which we also extend to the year 2020 to cover the selected time periods. The dataset contains general financial news from Reuters111https://www.reuters.com/ which are not filtered by any stock or country. This allows the LLM to decide by itself if each article is relevant to the target portfolio.

To generate the labels for portfolio crash, we first retrieve the price data of each constituent stock from Yahoo Finance222https://finance.yahoo.com/, and calculate their daily percentage returns. Next, we average across these to obtain the portfolio returns for each day. To find portfolio crashes, we set a threshold to capture sharp falls in value (Kourouma et al., 2010). We label returns as a crash, which represents the bottom percentile of the overall returns series. In addition, as the occurrences of these crashes are rare (see Table 1), the dataset is largely imbalanced and prediction models that predict all False (i.e., no crashes) would produce a high accuracy score. Following works that deal with highly imbalanced classification in Object Detection (Padilla et al., 2020) and Medical Imaging (Vaid et al., 2022) tasks, we use the Area Under Receiver Operating Characteristics curve (AUROC) as our metric, which can capture the trade-off between True and False Positives across all thresholds.

4.2. Baselines

As the task of detecting portfolio crashes is not widely explored currently, we compare with multiple zero-shot LLM frameworks, such as standard IO prompting, Chain-of-Thought (CoT) (Wei et al., 2022), Graph-of-Thoughts (GoT) (Besta et al., 2024) and Think-on-Graph (ToG) (Sun et al., 2024). In addition, we also compare with a non-zero-shot deep-learning model (Bi-GRU + Attention (Hu et al., 2018)) that has been trained on past Reuters news data from the same dataset. While this model seemingly has an ”advantage” by having task-related training data, we argue that they are not able to handle unprecedented events that has not previously occurred, such as COVID-19. We highlight our implementation of the baselines below.

Deep-Learning Model:

BiGRU+Attention (Hu et al., 2018): For the deep-learning model, we use a BiGRU+Attention model, that was originally used for stock price classification. As this model requires training data, it was trained on the available Reuters news data before the test period, from October 2006 to May 2007. For training, the independent variables are the news article headlines, while the ground truth are the binary crashes. The model is trained for 50 epochs with early stopping, with a learn rate of 1e-3 and batch size of 32.

Large Language Models:

Input-output (IO) prompting: For this LLM baseline, we simply use the news articles as input and prompt the LLM to generate a crash prediction for the portfolio. As this is a huge amount of text which goes beyond any LLM’s token limits, we use only the headlines of the news articles as input.

Chain-of-Thoughts (CoT) (Wei et al., 2022): This LLM baseline largely follows the same methodology as IO prompting, but includes an additional line of prompt which instructs the LLM to ”think step-by-step”.

Graph-of-Thoughts (GoT) (Besta et al., 2024): In this LLM baseline, we first provide the LLM with the retrieved news articles, and use GoT to divide and merge thoughts to arrive at a crash prediction for the target portfolio. This is done in a similar fashion as our TRR framework - we first split the portfolio into individual stocks, and prompt the LLM to discover the impact on each stock using sub-thoughts. These thoughts are then combined to find the overall impact on the portfolio. However, the key difference between this method and ours is that the thoughts are not used to form a temporal Knowledge Graph, and that there was no pruning of the combined information, which was done in our Attention phase.

Think-on-Graph (ToG) (Sun et al., 2024): The ToG framework requires an existing factual Knowledge Graph, in order to search for a reasoning path that can tackle the task. To adapt it for our problem, we use the graph of impacts that was formed in our Brainstorming Phase. We then use ToG to find the best reasoning path on this graph to answer the prompt. Following the original work, this is done by identifying the most relevant paths at each depth via a beam search process, and checking if they are sufficient to make a crash prediction. This is repeated iteratively at each depth until the LLM respond that it has sufficient information to make a prediction, or the maximum depth of the graph is reached. When this happens, the most relevant path is then provided to the final LLM to make its prediction.

4.3. Parameter Settings

For all LLM experiments, we use OpenAI GPT-3.5-turbo to generate the responses, with a temperature setting of 0.0. For the last reasoning phase, we repeat the prediction prompt 5 times for each model and report the average AUROC and standard deviation. For the main experiments, we set to 1 and to 6. These parameters will be explored further in the ablation study.

5. Results

Table 2 reports the main results for our task. From the table, we can make the following observations:

-

•

The deep-learning model, BiGRU + Attention, shows results that lie close to 0.5. This is because the model predicts mostly False (Note that All-True or All-False predictions produce an AUROC of exactly 0.5). Portfolio crashes are often rare, which causes a large bias towards False predictions when training the model. In addition, it is likely that the model is unable to handle events that are previously unseen in the train set, causing them to predict False on the unprecedented crash events.

-

•

Among the thought-based frameworks (i.e., IO, CoT and GoT), we can see a clear rising trend in the AUROC metric. This shows that it is beneficial to break down the task of predicting portfolio crashes into smaller thought processes. Going further, we observe that the search-based ToG was able to outperform these models. As the input dataset was not manually filtered, it is likely that there are numerous news articles that contain noisy information not relevant to the specified portfolio. By first searching for an impact path from the articles to the portfolio, ToG was able to find the most relevant information that can help it to decide if a possible portfolio crash will occur.

-

•

Finally, our TRR framework was able to outperform all models, by an average of 10.6% over the strongest baseline (ToG). By considering multiple impact paths that are relevant to the portfolio and also the relationship between these paths, TRR was able to get a more holistic overview of the various market forces on the portfolio, which can help it to detect possible crashes more accurately.

5.1. Ablation Study

Next, we perform an ablation study by removing the individual components in TRR, which include its relational, temporal (memory) and the memory decay. For removing the relational component, we repeat the results from the ToG experiment, given that generating a relational graph forms the backbone of the TRR model. In our implementation, ToG was used to search for a single path across the graph to make its prediction, and hence does not consider the relations between multiple paths. For removing the temporal component, we remove the memory module (we set ), hence not providing any past temporal context to the LLM for reasoning. Finally, for removing the decay component, we set the memory retention to a constant value (we set for all ). These experiments were conducted over the dataset for year 2007, on the Country-Neutral portfolio.

| Variant | AUROC |

|---|---|

| No relational | |

| No temporal | |

| No decay | |

| TRR (Ours) |

Table 3 reports the AUROC over the different variants of ablation models. From the table, we can observe that each component helped to contribute to the overall performance of the model. Both the relational and temporal components provide additional graph paths to the LLM during the reasoning phase without degrading the performance, which shows that useful information was extracted from the graph as opposed to noisy data. These paths help to provide additional contextual information regarding each news impact, which allows the LLM to better determine if a crash will occur. We can also observe that the memory decay component helps to improve the AUROC results. It is likely that events that are further back in history would have a lesser impact on the stock prices, as these events start to fade away from public memory (Lorenz-Spreen et al., 2019), making it effective to decay their importance weightage.

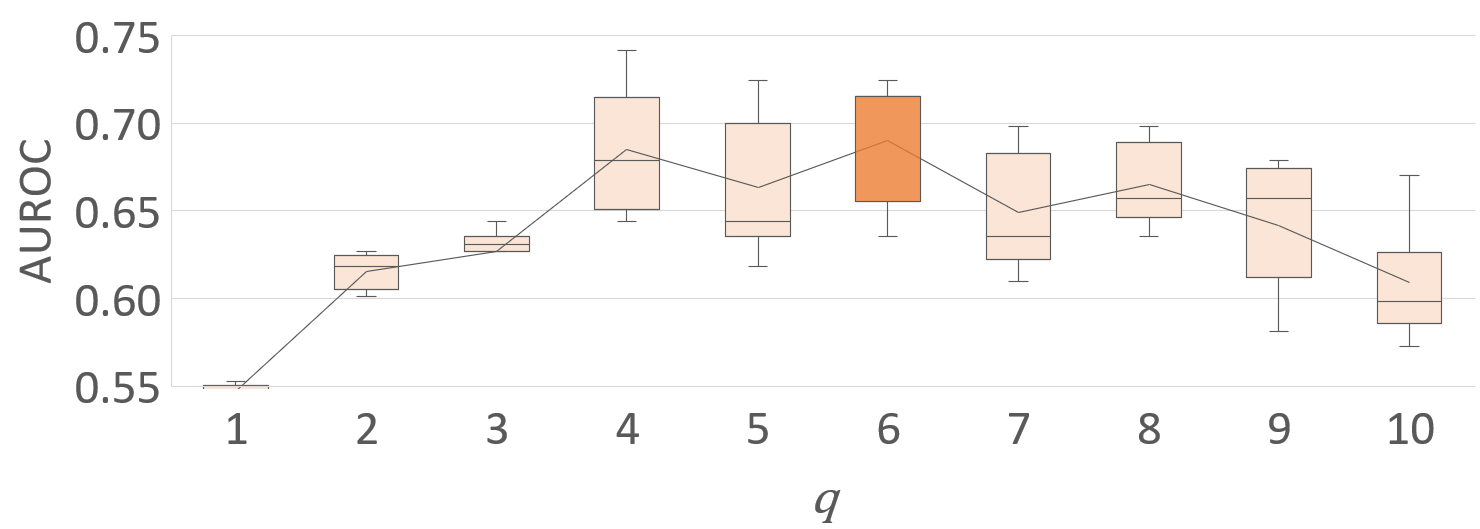

5.2. Parameter Selection

For choosing the parameters, we conduct ablation studies over different values of and , which determine the memory decay rate and top- entities that investors would pay attention to respectively. These experiments were conducted over the dataset for year 2007, on the Country-Neutral portfolio.

| AUROC | |

|---|---|

| 0.1 | |

| 0.5 | |

| 1 | |

| 2 | |

| 10 |

Table 4 reports the AUROC over different values of the decay rate constant . Here, it is observed that the AUROC drops as both increases and decreases. Note that in the memory module, the memory retention of each impact was tracked by the variable , which is then used to weigh the ranking scores . As decreases, the memory retention tends towards very small values, i.e., , which also causes the ranking scores for all entities to shift towards an equal value of zero. Because of this, the top entities for the attention graph would be chosen more randomly, resulting in poorer prediction performance. On the other hand, as increases, the memory retention tends towards a value of one, i.e., . This causes the ranking scores to be weighted more equally, and the top entities selection for will become less affected by the temporal information. At very high values of , the weights will remain constant at , which is equivalent to having no decay in the memory component. Higher causes the AUROC value to fall, highlighting the usefulness of the memory decay process. Through the ablation study, we set .

Figure 3 shows the range of AUROC values over 5 runs, across different values of . The value of determines the number of top entities to be considered in the attention graph , which the LLM will perform reasoning on to make a crash prediction. We can observe that at small values of , too limited information was provided to the LLM, resulting in poorer AUROC performance that is fairly consistent. However, as increases, more relevant information is provided for the LLM to perform reasoning over. This results in better AUROC but with a larger standard deviation, as the LLM could choose different parts of the information to focus on. Finally, at very high values of , there is a dip in the AUROC performance, given that there might now be too much noisy information provided. This also highlights the importance of forming an attention sub-graph, instead of providing all information directly into the LLM, which could affect its performance. Through the ablation study, we set .

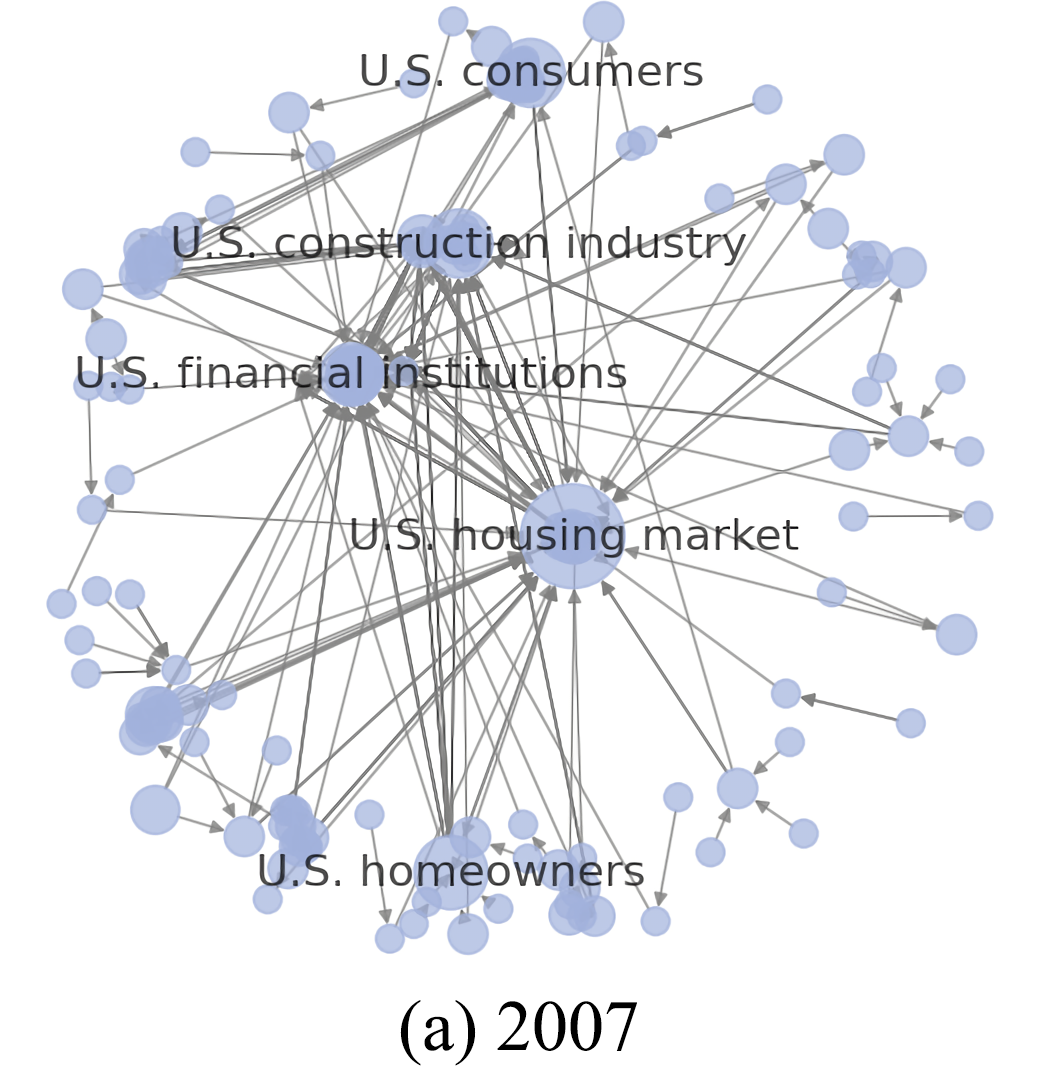

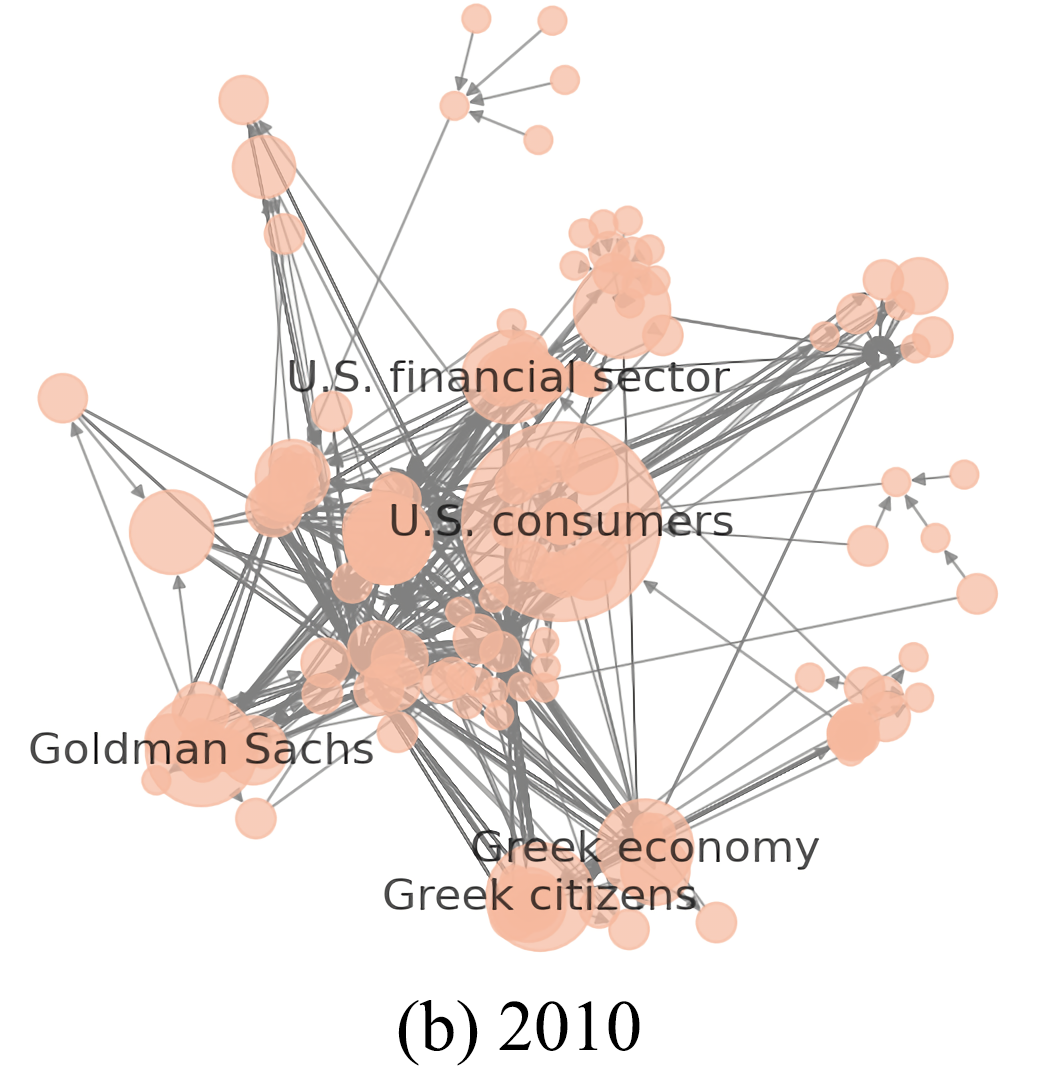

5.3. Graph Analysis

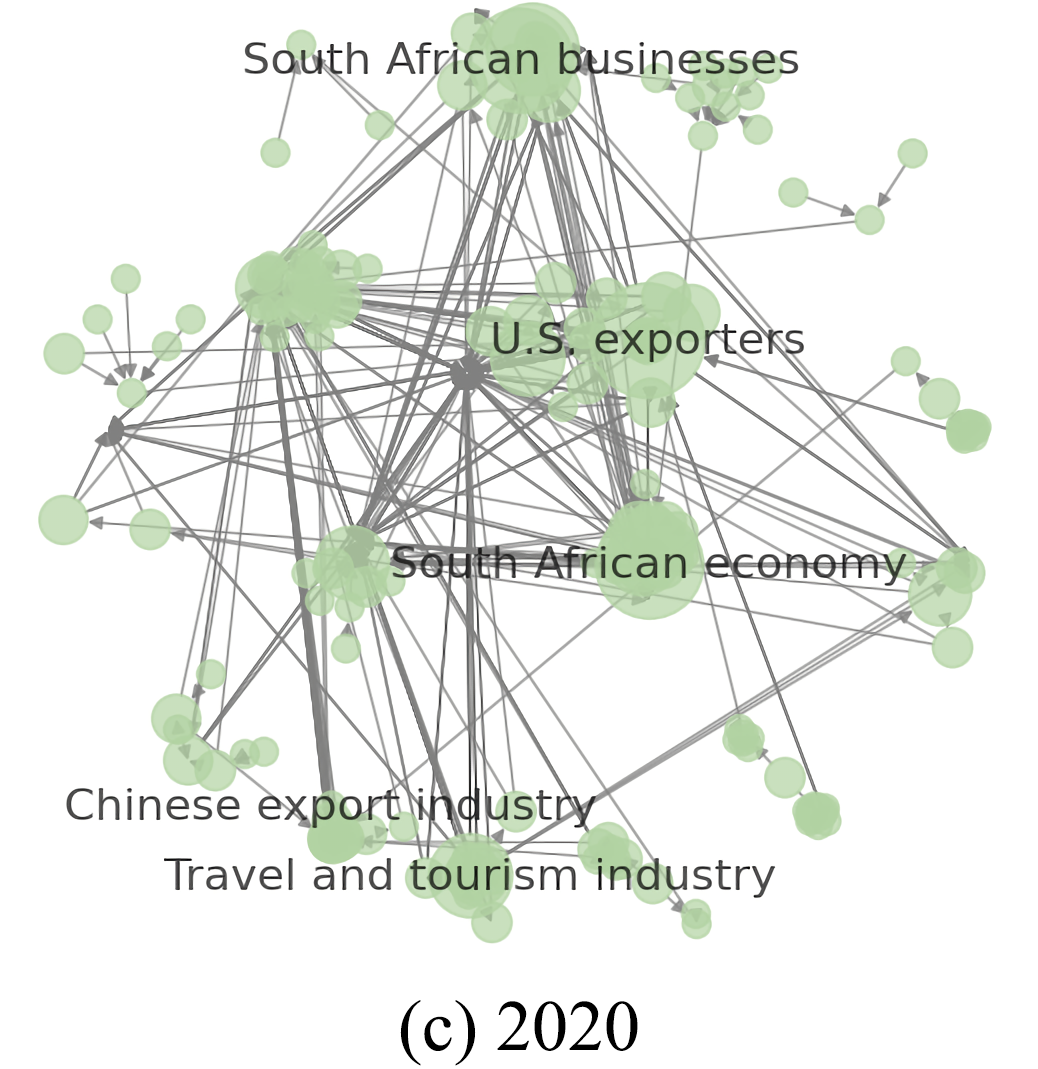

In addition, we explore the generated graphs by visualizing an example from each dataset over the crash periods. For each graph, we project the vertex sizes based on the number of incoming edges. To prevent overcrowding, we label only the top few vertices with the highest number of incoming edges.

Figure 4 showcases the graphs generated using the series of news articles, which are used by the LLM to detect portfolio crashes for the next day. From the graphs, we can qualitatively determine that TRR was able to highlight the most important information that caused the portfolio crashes in real life. Within the 2007 dataset, TRR was able to find that the U.S. housing market was impacted more than other entities from the given news, as shown from its higher number of incoming edges. This coincides with the global financial crisis in 2007, which was caused by the housing bubble. From the 2010 dataset, TRR was able to capture the impact on the Greece citizens and the Greek economy, which aligns with the Greek government debt crisis. In the 2020 dataset, the top impacted entities were less obvious as they were spread out over various entities. However, the impacted entities, such as the export and tourism industries, show the impacts that was caused by the COVID-19 pandemic.

Importantly, we note that the input news articles were not manually filtered in any way. The TRR model was able to find these ”top-impacted entities” on its own by tracing the impacts of each news event individually, and obtaining the relevance of each impacted entity through the ranking scores.

5.4. Additional Experiments

From the optimistic results on portfolio crash detection above, we explore the generalizability of TRR to a closely-related task. In Macroeconomics, it is a crucial task to develop warning indicators for economic crisis events (Babecky et al., 2013; Püttmann, 2018; Zheng, 2020), in order for policymakers to take preemptive measures to mitigate these events. By viewing the global economy as a network of regional economies, we can utilize our TRR framework to trace the impacts on each individual economy, then reason over these impacts to detect possible widespread crisis globally. For this task, instead of a binary prediction, we prompt the LLM to output the probability of a global crisis, for its application as a continuous warning indicator.

For this experiment, we now set our ”portfolio” P as a series of economies, e.g., the American economy, European economy, Asian economy, etc. , and use TRR to trace the impacts of news events to these entities. For the crisis labels, we use the TED spread, which is the difference between the interest rates on interbank loans and short-term government debt. It has been shown in empirical works that a TED spread above 48 basis points is indicative of economic crisis (Boudt et al., 2017), as lenders switch to safer government investments when they believe the risk of default on interbank loans is rising. We label the TED spread above 0.48 as a crisis. In addition, we also provide the past 5 days of TED spread data in the input LLM prompt for context.

For the baselines, we use the Financial Stress Indicator (FSI) (Püttmann, 2018), the volatility index (VIX) (Jiang and Tian, 2007) and the yield curve (Yield) values (Harvey, 1986) from the previous day as indicators. In particular, the FSI is one of the earliest works in economics that use newspaper articles as a financial indicator. This is done by searching the article headlines for financial keywords, such as ”economy”, ”gold” or ”railroads”. The reporting frequency of these terms were found to correlate heavily with crisis events in the work (Püttmann, 2018). More details on our implementation, the dataset and baselines for this task is found in Appendix B.

Table 5 reports the results for the crisis detection task. From the table, we can observe the following:

-

•

Among most of the models (including TRR), the 2011 dataset typically produce the lowest AUROC results. The 2011 dataset corresponds with the Greek government debt crisis, whose impact was mostly contained within the European economy. While there were still some spillover effects on the other economies, they were not as prevalent as those from the global financial crisis or COVID-19. For our model, this makes it harder to capture the interconnectedness between the graph entities.

-

•

The keyword-based FSI seems to drop greatly in performance in the 2020 dataset. This is likely because the keywords used, such as ”gold” or railroads”, were not relevant in this period, which correspond to the COVID-19 event. Given that it is hard for humans to predict what event would cause the next crisis, it is also difficult to know what keywords to search for in advance. Hence, it becomes crucial to utilize tools that can do zero-shot reasoning over unseen events, such as LLMs.

-

•

Our proposed TRR framework was able to outperform most baselines, except for the 2020 dataset, where the economic indicators (i.e., VIX and yield curve) showed exceptional predictive performance. However, for this case, our performance is still comparable to these methods, even without the use of statistical information. This highlights TRR as a possible useful tool for practitioners.

| Dataset | 2007 | 2011 | 2020 |

|---|---|---|---|

| FSI | \ul | ||

| VIX | |||

| Yield | \ul | ||

| TRR (Ours) | \ul | ||

| Improvement | 14.49% | 83.54% | -3.95% |

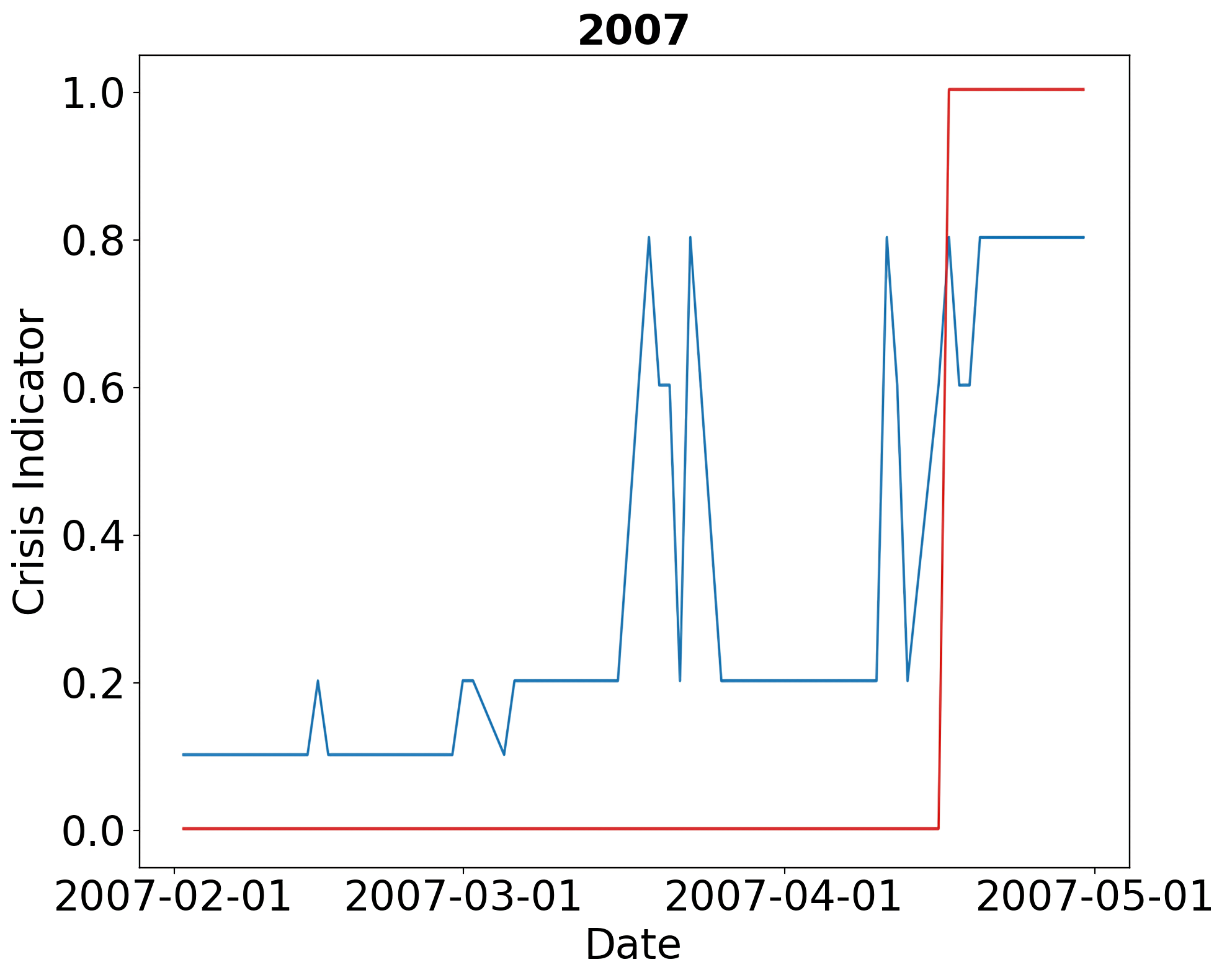

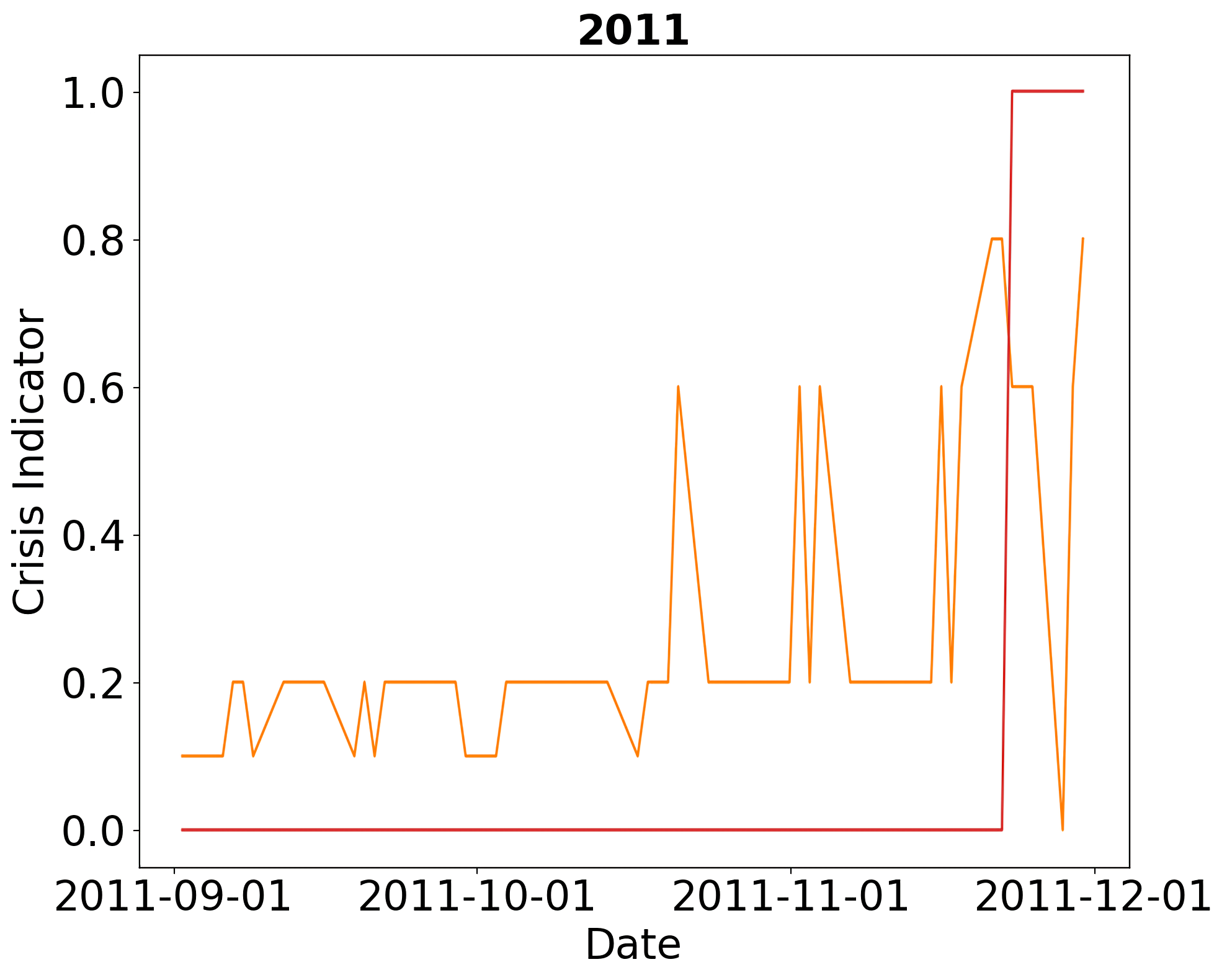

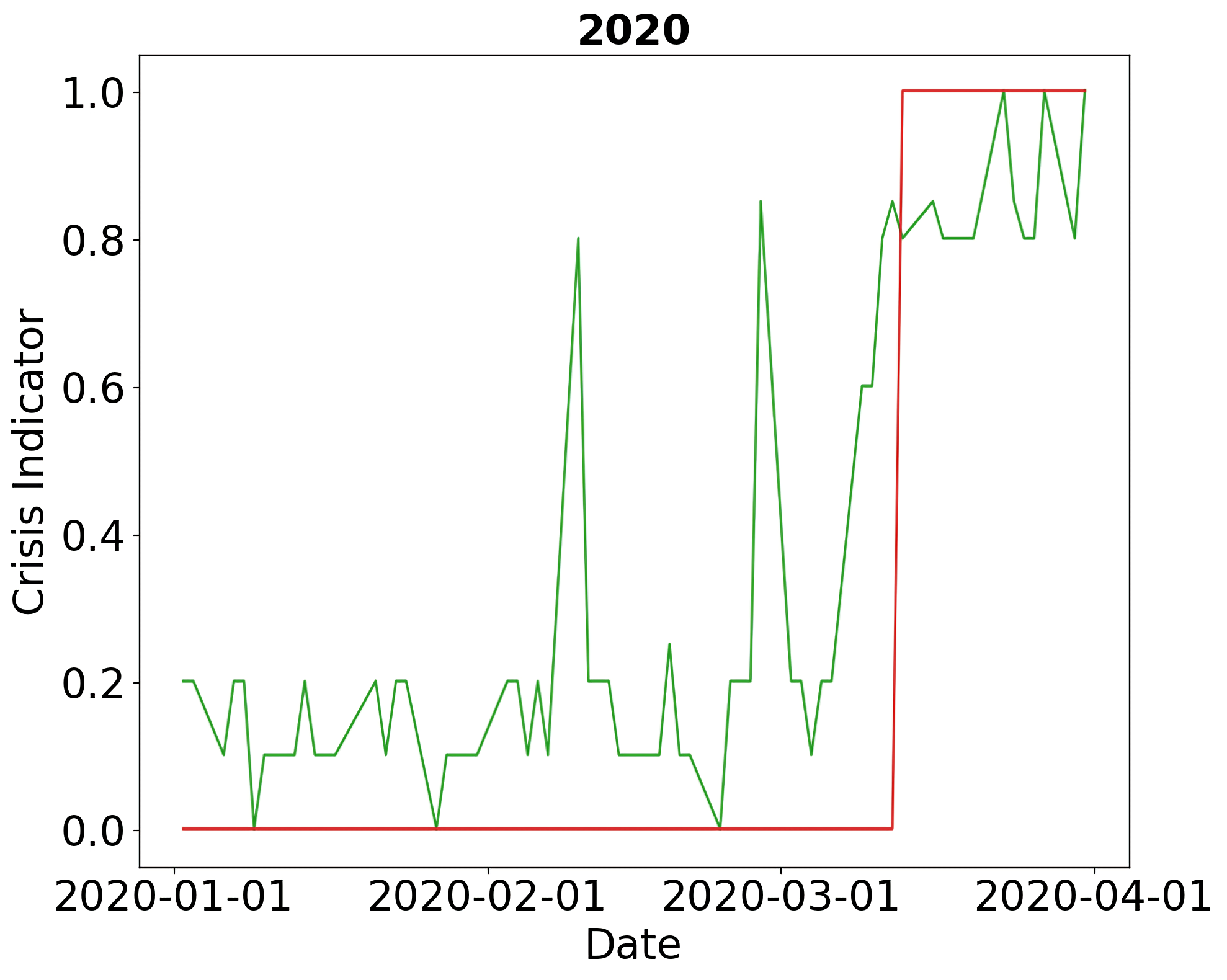

Figure 5 provides some qualitative examples of the crisis indicator generated from our TRR framework. In addition to the AUROC performance, we note that our indicator shows a peak at the start of the crisis date, which is also an important consideration. However, we also note some limitations of our method: Firstly, the indicator is not continuous to a certain extent. As the values for each day are generated individually, the LLM does not have a sense of the continuity or smoothness in the data, which could limit its application as a continuous indicator; Secondly, we note that the disjoint peaks do not always correspond to the crisis dates, which could result in false alarms when used as a crisis indicator. Because of this, caution must be taken when utilizing this work in a practical application.

6. Conclusion and Future Work

In this work, we explored the main task of portfolio crash detection, which was difficult to solve before the advent of LLMs, due to the unprecedented nature of crash-related events. We proposed our TRR framework, which is able to do zero-shot reasoning across relational and temporal information through a set of human cognitive capabilities. Through extensive experiments, we show that TRR is able to outperform state-of-the-art frameworks on detecting portfolio crashes. Furthermore, we also explored the generalizability of TRR by using it to develop a crisis warning indicator in macroeconomics.

The results of this work open up some possible future directions for research. Firstly, each of the individual components in TRR can be expanded with more specialized techniques. For example, the memory component in TRR can be augmented with a more advanced symbolic database (Hu et al., 2023); the PageRank algorithm is also dated and can be replaced with newer information retrieval-based methods (Wu et al., 2021). Secondly, for the crisis detection task, more baselines could be studied (Babecky et al., 2013; Jordà et al., 2017), such as government debt, external trade flows, etc. These statistical indicators could also be used together with our TRR method in a ensemble system, which could help to improve the prediction capability of the warning indicator.

References

- (1)

- Au Yeung and Jatowt (2011) Ching-man Au Yeung and Adam Jatowt. 2011. Studying how the past is remembered: towards computational history through large scale text mining. In Proceedings of the 20th ACM international conference on Information and knowledge management. 1231–1240.

- Babecky et al. (2013) Jan Babecky, Tomas Havranek, Jakub Mateju, Marek Rusnak, Katerina Smidkova, and Borek Vasicek. 2013. Leading indicators of crisis incidence: Evidence from developed countries. Journal of International Money and Finance 35 (2013), 1–19.

- Baitinger and Papenbrock (2017) Eduard Baitinger and Jochen Papenbrock. 2017. Interconnectedness risk and active portfolio management. Journal of Investment Strategies (2017).

- Baker et al. (2020) Scott R Baker, Nicholas Bloom, Steven J Davis, Kyle Kost, Marco Sammon, and Tasaneeya Viratyosin. 2020. The unprecedented stock market reaction to COVID-19. The review of asset pricing studies 10, 4 (2020), 742–758.

- Bender et al. (2021) Emily M Bender, Timnit Gebru, Angelina McMillan-Major, and Shmargaret Shmitchell. 2021. On the dangers of stochastic parrots: Can language models be too big?. In Proceedings of the 2021 ACM conference on fairness, accountability, and transparency. 610–623.

- Besta et al. (2024) Maciej Besta, Nils Blach, Ales Kubicek, Robert Gerstenberger, Michal Podstawski, Lukas Gianinazzi, Joanna Gajda, Tomasz Lehmann, Hubert Niewiadomski, Piotr Nyczyk, et al. 2024. Graph of thoughts: Solving elaborate problems with large language models. In Proceedings of the AAAI Conference on Artificial Intelligence, Vol. 38. 17682–17690.

- Bollacker et al. (2008) Kurt Bollacker, Colin Evans, Praveen Paritosh, Tim Sturge, and Jamie Taylor. 2008. Freebase: a collaboratively created graph database for structuring human knowledge. In Proceedings of the 2008 ACM SIGMOD international conference on Management of data. 1247–1250.

- Boudt et al. (2017) Kris Boudt, Ellen CS Paulus, and Dale WR Rosenthal. 2017. Funding liquidity, market liquidity and TED spread: A two-regime model. Journal of Empirical Finance 43 (2017), 143–158.

- Brown et al. (2020) Tom Brown, Benjamin Mann, Nick Ryder, Melanie Subbiah, Jared D Kaplan, Prafulla Dhariwal, Arvind Neelakantan, Pranav Shyam, Girish Sastry, Amanda Askell, et al. 2020. Language models are few-shot learners. Advances in neural information processing systems 33 (2020), 1877–1901.

- Che et al. (2022) Yuezhang Che, Shuyan Chen, and Xin Liu. 2022. Sparse index tracking portfolio with sector neutrality. Mathematics 10, 15 (2022), 2645.

- Chen et al. (2023) Zihan Chen, Lei Nico Zheng, Cheng Lu, Jialu Yuan, and Di Zhu. 2023. ChatGPT informed graph neural network for stock movement prediction. arXiv preprint arXiv:2306.03763 (2023).

- De Prado (2016) Marcos Lopez De Prado. 2016. Building diversified portfolios that outperform out of sample. The Journal of Portfolio Management 42, 4 (2016), 59–69.

- Ding et al. (2014) Xiao Ding, Yue Zhang, Ting Liu, and Junwen Duan. 2014. Using structured events to predict stock price movement: An empirical investigation. In Proceedings of the 2014 conference on empirical methods in natural language processing (EMNLP). 1415–1425.

- Ding et al. (2015) Xiao Ding, Yue Zhang, Ting Liu, and Junwen Duan. 2015. Deep learning for event-driven stock prediction. In Twenty-fourth international joint conference on artificial intelligence.

- Ding et al. (2016) Xiao Ding, Yue Zhang, Ting Liu, and Junwen Duan. 2016. Knowledge-driven event embedding for stock prediction. In Proceedings of coling 2016, the 26th international conference on computational linguistics: Technical papers. 2133–2142.

- Feng et al. (2019) Fuli Feng, Xiangnan He, Xiang Wang, Cheng Luo, Yiqun Liu, and Tat-Seng Chua. 2019. Temporal relational ranking for stock prediction. ACM Transactions on Information Systems (TOIS) 37, 2 (2019), 1–30.

- Goldin and Vogel (2010) Ian Goldin and Tiffany Vogel. 2010. Global governance and systemic risk in the 21st century: Lessons from the financial crisis. Global Policy 1, 1 (2010), 4–15.

- Greff et al. (2020) Klaus Greff, Sjoerd Van Steenkiste, and Jürgen Schmidhuber. 2020. On the binding problem in artificial neural networks. arXiv preprint arXiv:2012.05208 (2020).

- Halbwachs (2020) Maurice Halbwachs. 2020. On collective memory. University of Chicago press.

- Harvey (1986) Campbell Russell Harvey. 1986. Recovering expectations of consumption growth from an equilibrium model of the term structure of interest rates. The University of Chicago.

- Hirshleifer et al. (2011) David Hirshleifer, Sonya S Lim, and Siew Hong Teoh. 2011. Limited investor attention and stock market misreactions to accounting information. The Review of Asset Pricing Studies 1, 1 (2011), 35–73.

- Hu et al. (2023) Chenxu Hu, Jie Fu, Chenzhuang Du, Simian Luo, Junbo Zhao, and Hang Zhao. 2023. Chatdb: Augmenting llms with databases as their symbolic memory. arXiv preprint arXiv:2306.03901 (2023).

- Hu et al. (2018) Ziniu Hu, Weiqing Liu, Jiang Bian, Xuanzhe Liu, and Tie-Yan Liu. 2018. Listening to chaotic whispers: A deep learning framework for news-oriented stock trend prediction. In Proceedings of the eleventh ACM international conference on web search and data mining. 261–269.

- Jiang and Tian (2007) George J Jiang and Yisong S Tian. 2007. Extracting model-free volatility from option prices: An examination of the VIX index. Journal of Derivatives 14, 3 (2007).

- Jiang et al. (2023) Jinhao Jiang, Kun Zhou, Zican Dong, Keming Ye, Xin Zhao, and Ji-Rong Wen. 2023. StructGPT: A General Framework for Large Language Model to Reason over Structured Data. In Proceedings of the 2023 Conference on Empirical Methods in Natural Language Processing. 9237–9251.

- Jordà et al. (2017) Òscar Jordà, Moritz Schularick, and Alan M Taylor. 2017. Macrofinancial history and the new business cycle facts. NBER macroeconomics annual 31, 1 (2017), 213–263.

- Koa et al. (2023) Kelvin J.L. Koa, Yunshan Ma, Ritchie Ng, and Tat-Seng Chua. 2023. Diffusion Variational Autoencoder for Tackling Stochasticity in Multi-Step Regression Stock Price Prediction. In Proceedings of the 32nd ACM International Conference on Information and Knowledge Management. 1087–1096.

- Koa et al. (2024) Kelvin J.L. Koa, Yunshan Ma, Ritchie Ng, and Tat-Seng Chua. 2024. Learning to Generate Explainable Stock Predictions using Self-Reflective Large Language Models. In Proceedings of the ACM on Web Conference 2024. 4304–4315.

- Kojima et al. (2022) Takeshi Kojima, Shixiang Shane Gu, Machel Reid, Yutaka Matsuo, and Yusuke Iwasawa. 2022. Large language models are zero-shot reasoners. Advances in neural information processing systems 35 (2022), 22199–22213.

- Kourouma et al. (2010) Lancine Kourouma, Denis Dupre, Gilles Sanfilippo, and Ollivier Taramasco. 2010. Extreme value at risk and expected shortfall during financial crisis. Available at SSRN 1744091 (2010).

- Lorenz-Spreen et al. (2019) Philipp Lorenz-Spreen, Bjarke Mørch Mønsted, Philipp Hövel, and Sune Lehmann. 2019. Accelerating dynamics of collective attention. Nature communications 10, 1 (2019), 1759.

- Loughran and McDonald (2011) Tim Loughran and Bill McDonald. 2011. When is a liability not a liability? Textual analysis, dictionaries, and 10-Ks. The Journal of finance 66, 1 (2011), 35–65.

- Mandelbrot (2001) Benoit B Mandelbrot. 2001. Scaling in financial prices: I. Tails and dependence. Quantitative Finance 1, 1 (2001), 113.

- Markowitz (1952) Harry Markowitz. 1952. Portfolio Selection. The Journal of Finance 7, 1 (1952), 77–91. https://doi.org/10.1111/j.1540-6261.1952.tb01525.x arXiv:https://onlinelibrary.wiley.com/doi/pdf/10.1111/j.1540-6261.1952.tb01525.x

- Naeem et al. (2021) Muhammad Abubakr Naeem, Saba Sehrish, and Mabel D Costa. 2021. COVID-19 pandemic and connectedness across financial markets. Pacific Accounting Review 33, 2 (2021), 165–178.

- Newell et al. (1959) Allen Newell, John C Shaw, and Herbert A Simon. 1959. Report on a general problem solving program. In IFIP congress, Vol. 256. Pittsburgh, PA, 64.

- Padilla et al. (2020) Rafael Padilla, Sergio L Netto, and Eduardo AB Da Silva. 2020. A survey on performance metrics for object-detection algorithms. In 2020 international conference on systems, signals and image processing (IWSSIP). IEEE, 237–242.

- Page et al. (1999) Lawrence Page, Sergey Brin, Rajeev Motwani, Terry Winograd, et al. 1999. The pagerank citation ranking: Bringing order to the web. (1999).

- Püttmann (2018) Lukas Püttmann. 2018. Patterns of panic: Financial crisis language in historical newspapers. Available at SSRN 3156287 (2018).

- Rouwenhorst (1998) K Geert Rouwenhorst. 1998. International momentum strategies. The journal of finance 53, 1 (1998), 267–284.

- Sawhney et al. (2020) Ramit Sawhney, Shivam Agarwal, Arnav Wadhwa, and Rajiv Shah. 2020. Deep attentive learning for stock movement prediction from social media text and company correlations. In Proceedings of the 2020 Conference on Empirical Methods in Natural Language Processing (EMNLP). 8415–8426.

- Spiliopoulou (2022) Evangelia Spiliopoulou. 2022. Modeling Event Implications via Multi-faceted Entity Representations. Ph. D. Dissertation. Carnegie Mellon University.

- Sun et al. (2024) Jiashuo Sun, Chengjin Xu, Lumingyuan Tang, Saizhuo Wang, Chen Lin, Yeyun Gong, Heung-Yeung Shum, and Jian Guo. 2024. Think-on-graph: Deep and responsible reasoning of large language model with knowledge graph. In International Conference on Learning Representations.

- Taleb (2007) N.N. Taleb. 2007. The Black Swan: The Impact of the Highly Improbable. Random House Publishing Group. https://books.google.com.sg/books?id=gWW4SkJjM08C

- Taleb et al. (2022) Nassim Nicholas Taleb, Yaneer Bar-Yam, and Pasquale Cirillo. 2022. On single point forecasts for fat-tailed variables. International Journal of Forecasting 38, 2 (2022), 413–422.

- Vaid et al. (2022) Akhil Vaid, Kipp W Johnson, Marcus A Badgeley, Sulaiman S Somani, Mesude Bicak, Isotta Landi, Adam Russak, Shan Zhao, Matthew A Levin, Robert S Freeman, et al. 2022. Using deep-learning algorithms to simultaneously identify right and left ventricular dysfunction from the electrocardiogram. Cardiovascular Imaging 15, 3 (2022), 395–410.

- Vrandečić and Krötzsch (2014) Denny Vrandečić and Markus Krötzsch. 2014. Wikidata: a free collaborative knowledgebase. Commun. ACM 57, 10 (2014), 78–85.

- Wei et al. (2022) Jason Wei, Xuezhi Wang, Dale Schuurmans, Maarten Bosma, Fei Xia, Ed Chi, Quoc V Le, Denny Zhou, et al. 2022. Chain-of-thought prompting elicits reasoning in large language models. Advances in neural information processing systems 35 (2022), 24824–24837.

- Whaley (2000) Robert E Whaley. 2000. The investor fear gauge. Journal of portfolio management 26, 3 (2000), 12.

- Whaley (2009) Robert E Whaley. 2009. Understanding the VIX. Journal of Portfolio Management 35, 3 (2009), 98–105.

- Wu et al. (2021) Jiancan Wu, Xiang Wang, Fuli Feng, Xiangnan He, Liang Chen, Jianxun Lian, and Xing Xie. 2021. Self-supervised graph learning for recommendation. In Proceedings of the 44th international ACM SIGIR conference on research and development in information retrieval. 726–735.

- Xing and Ghorbani (2004) Wenpu Xing and Ali Ghorbani. 2004. Weighted pagerank algorithm. In Proceedings. Second Annual Conference on Communication Networks and Services Research, 2004. IEEE, 305–314.

- Xiong et al. (2024) Siheng Xiong, Ali Payani, Ramana Kompella, and Faramarz Fekri. 2024. Large Language Models Can Learn Temporal Reasoning. In Proceedings of the 62nd Annual Meeting of the Association for Computational Linguistics (Volume 1: Long Papers). 10452–10470.

- Xu et al. (2023) Liao Xu, Xuan Zhang, and Jing Zhao. 2023. Limited investor attention and biased reactions to information: Evidence from the COVID-19 pandemic. Journal of Financial Markets 62 (2023), 100757.

- Xu and Cohen (2018) Yumo Xu and Shay B Cohen. 2018. Stock movement prediction from tweets and historical prices. In Proceedings of the 56th Annual Meeting of the Association for Computational Linguistics (Volume 1: Long Papers). 1970–1979.

- Yang et al. (2023) Jingfeng Yang, Hongye Jin, Ruixiang Tang, Xiaotian Han, Qizhang Feng, Haoming Jiang, Shaochen Zhong, Bing Yin, and Xia Hu. 2023. Harnessing the power of llms in practice: A survey on chatgpt and beyond. ACM Transactions on Knowledge Discovery from Data (2023).

- Yao et al. (2024) Shunyu Yao, Dian Yu, Jeffrey Zhao, Izhak Shafran, Tom Griffiths, Yuan Cao, and Karthik Narasimhan. 2024. Tree of thoughts: Deliberate problem solving with large language models. Advances in Neural Information Processing Systems 36 (2024).

- Yuan et al. (2024) Chenhan Yuan, Qianqian Xie, Jimin Huang, and Sophia Ananiadou. 2024. Back to the future: Towards explainable temporal reasoning with large language models. In Proceedings of the ACM on Web Conference 2024. 1963–1974.

- Zhang et al. (2023) Yichi Zhang, Zhuo Chen, Wen Zhang, and Huajun Chen. 2023. Making large language models perform better in knowledge graph completion. arXiv preprint arXiv:2310.06671 (2023).

- Zhang and Clark (2011) Yue Zhang and Stephen Clark. 2011. Syntactic processing using the generalized perceptron and beam search. Computational linguistics 37, 1 (2011), 105–151.

- Zhang et al. (2024) Zeyang Zhang, Xin Wang, Ziwei Zhang, Haoyang Li, Yijian Qin, and Wenwu Zhu. 2024. LLM4DyG: Can Large Language Models Solve Spatial-Temporal Problems on Dynamic Graphs?. In Conference on Knowledge Discovery and Data Mining (ACM SIGKDD).

- Zheng (2020) Huanhuan Zheng. 2020. Coordinated bubbles and crashes. Journal of Economic Dynamics and Control 120 (2020), 103974.

- Zhong et al. (2024) Wanjun Zhong, Lianghong Guo, Qiqi Gao, He Ye, and Yanlin Wang. 2024. Memorybank: Enhancing large language models with long-term memory. In Proceedings of the AAAI Conference on Artificial Intelligence, Vol. 38. 19724–19731.

Appendix A Portfolio Construction

To construct our portfolios, we select the top market capitalization stocks from each country or sector that have historical data since 2007 (i.e., newer big companies such as Alibaba Group or Spotify were not considered due to lack of data). We limit the portfolio sizes to 10 due to the LLM token limits, at the time of the experiments. The constituent stocks of the portfolios are found in Table 6 and 7.

| Company | Country |

|---|---|

| Apple Inc. | U.S. |

| Royal Bank of Canada | Canada |

| NetEase, Inc. | China |

| HDFC Bank Limited | India |

| AstraZeneca PLC | UK |

| TotalEnergies SE | France |

| SAP SE | Germany |

| Toyota Motor Corporation | Japan |

| BHP Group Limited | Australia |

| Accenture PLC | Ireland |

| Company | Sector |

|---|---|

| HSBC Holdings PLC | Financials |

| Novo Nordisk A/S | Healthcare |

| ASML Holding N.V. | Technology |

| General Electric Company | Industrials |

| Amazon.com, Inc. | Consumer Discretionary |

| Linde PLC | Materials |

| Alphabet Inc. | Communication Services |

| Shell PLC | Energy |

| Unilever PLC | Consumer Staples |

| National Grid PLC | Utilities |

Appendix B Details of Additional Experiments

We detail the experimental setup for the crisis detection task in this section. For this task, we redefine our portfolio of target entities as a set of regional economies, i.e., .

| Dataset | 2007 | 2011 | 2020 | ||||||

|---|---|---|---|---|---|---|---|---|---|

| Time Period |

|

|

|

||||||

|

4,005 | 5,655 | 7,177 | ||||||

|

0.206 | 0.138 | 0.210 |

Using the same dataset of Reuters financial news articles, we then use our TRR framework to trace their impacts to these entities. On this dataset, the selected time period was slightly shifted to capture the timestamps where the TED spread first goes above 48 points, resulting from the same crisis events as the portfolio crash detection task. The statistics of this dataset can be found in Table 8.

For the baselines, we choose a news article-based indicator and some financial indicators that are commonly used by practitioners to measure the economy health. We provide more details on each of these selected indicators below.

Financial Stress Indicator (FSI) (Püttmann, 2018): The FSI is one of the earliest works in economics that uses newspaper articles as a financial indicator. The motivation was to observe what people are thinking before the crisis event (and hence reported in the news), and not what researchers find out in hindsight. The indicator is formed by first searching headlines for keywords from a list of 120 words and phrases (Püttmann, 2018) on economics and financial markets. Sentiment analysis (Loughran and McDonald, 2011) is then performed on the headlines to obtain an overall sentiment score on the economy for each day, which forms the financial indicator.

Volatility Index (VIX) (Jiang and Tian, 2007): The VIX is a measure of the stock market’s volatility expectations by tracking the expected annualized change in the S&P 500 index for the next 30 days. It is also referred to by investors as the fear gauge (Whaley, 2000), as it reflects investors’ expectations of near-term market volatility. The VIX indicator has been shown to spike over periods of crisis events (Whaley, 2009; Baker et al., 2020).

Yield Curve (Harvey, 1986): For the yield curve indicator, we use the difference between interest rates of the 10-year Treasury bond and the 2-year Treasury bond. An inverted yield curve (i.e., when the 2-year bond yield exceeds the 10-year bond yield) typically signals an upcoming economic crisis (Harvey, 1986), as investors begin to believe that the risk of holding long-term government debt is higher.

The TED spread, VIX and yield curve data are all taken from the Federal Reserve Economic Data333https://fred.stlouisfed.org/ .

Appendix C Examples of LLM Prompts

We provide some examples of the LLM prompts and responses, for better replicability of our work.

Figure 6 and 7 show the initial and subsequent iterations of the Brainstorm prompt respectively. Given each news article from the dataset, the Brainstorm prompts will first generate the direct impacts, then trace their following knock-on effects repeatedly. This is done until the the chain of impacts reaches a portfolio stock, or the max number of iterations is reached. The responses are then used to form our graph of impacts. When forming our graph, we keep only the impacted entities and remove the explanations, which were only used to elicit a better reasoning process in the LLM (see CoT (Wei et al., 2022)).

Figure 8 shows the final generated temporal-relational graph in its tuple form, and the Reasoning prompt used for analyzing this graph. The tuples are organized first by their relational level in the graph, then temporally by their dates. Similar as above, the generated explanations are used for eliciting a better reasoning process in the LLM, and are not explicitly evaluated in our work. However in this case, the explanations are also used to ensure that the LLM does not refer to past events (e.g., ”A portfolio crash will occur because the dates of the provided events correspond to the 2007 Global Financial Crisis…”), but contains actual reasoning on the information given in the graph.