\ul

Risk Premia in the Bitcoin Market

Abstract

Based on options and realized returns we analyze risk premia in the Bitcoin market through the lens of the Pricing Kernel (PK). We identify that: 1) The projected PK into Bitcoin returns is W-shaped and steep in the negative returns region; 2) Negative Bitcoin returns account for 33% of the total Bitcoin index premium (BP) in contrast to 70% of S&P500 equity premium explained by negative returns. Applying a novel clustering algorithm to the collection of estimated Bitcoin risk-neutral densities, we find that risk premia vary over time as a function of two distinct market volatility regimes. In the low-volatility regime, the PK projection is steeper for negative returns and has a more pronounced W-shape than the unconditional one, implying particularly high BP for both extreme positive and negative returns and a high Variance Risk Premium (VRP). In high-volatility states, the BP attributable to positive and negative returns is more balanced and VRP is lower. Overall, Bitcoin investors are more worried about variance and downside risk in low volatility states.

Keywords: Risk Premium, Pricing Kernel, Cryptocurrency, Density Clustering, Nonparametric Estimation

JEL classification: G12, G13, C14, C38

1 Introduction

The cryptocurrency market is central to the digital economy, encompassing thousands of cryptocurrencies, hundreds of exchanges, and billions of U.S. dollars in global market capitalization. As this market grows, financial derivatives on cryptocurrencies and crypto-traded funds are becoming increasingly popular. Similar to traditional assets, crypto derivatives can provide valuable information about risk premia, which reflect the compensation demanded by market participants for taking on risk. While the literature extensively covers risk premia for traditional assets, particularly equities, a thorough analysis of these premia in the cryptocurrency market remains absent. Aiming to fill this gap, this paper is the first to analyze bitcoin risk premia using option data, focusing on the bitcoin return premium (BP) and variance risk premium (VRP).

We characterize Bitcoin risk premium properties through the lens of the Pricing Kernel (PK). First, we built a reliable joint dataset of Bitcoin returns and options to document several important stylized facts of unconditional bitcoin risk premia. Second, we propose a new two-stage methodology to identify modes of variation of Bitcoin risk-premium depending on market conditions. On the first stage, we construct a time-series sequence of physical and risk-neutral probability measures, implying a time-series sequence of PKs that allows us to directly assess risk premium dynamic properties. Then, adopting a novel functional clustering method we group risk-neutral measures identifying two relevant volatility regimes and their corresponding conditional measures of risk premia (BP and VRP).

Bitcoin is the first decentralized and most widely adopted digital currency, with a market capitalization of $1.3 trillion. It facilitates peer-to-peer transactions on a digital platform, supported by Bitcoin blockchain technology, which uses cryptography—hence the term "crypto." This paper focuses on bitcoin as a digital asset.111In the U.S., Bitcoin is considered a commodity and falls under the Commodity Futures Trading Commission (CFTC). Some studies compare Bitcoin to commodities (see [15, 45, 3]), while others treat it as a currency (see [61, 70]). Unlike equities, bitcoin does not pay dividends, but its value reflects net transactional benefits on the platform ([14]). Determining its fair value is challenging, given its reliance on blockchain technology and its ecosystem.222See [7], [29], [44], [65], [64], [41] for discussions on tokenization and the adoption of cryptocurrencies. Additionally, bitcoin’s price appears disconnected from traditional macro-finance markets.333[15] reports limited correlations between cryptocurrencies and traditional asset classes, with macro indicators having minimal impact on crypto markets. [50] found no significant link between bitcoin returns and consumption or production growth. [3] note that before Covid-19, bitcoin’s VRP did not align with other assets, though it became highly correlated with equity and gold VRP during the pandemic. These features attract a range of investors, from safe-haven seekers to speculators, driving price fluctuations. While earlier studies explored bitcoin price drivers to assess risk premia ([50]), we focus on risk premia implied by European options prices and returns. Our empirical analysis uses Bitcoin Index (BTC) option data from Deribit, the largest cryptocurrency derivatives exchange.444Cryptocurrency options are mainly traded on platforms like Deribit, which specializes in bitcoin and ethereum derivatives. Established in 2016, Deribit is now registered in Panama. Traditional exchanges like the CME also offer cryptocurrency options, but centralized exchanges account for less than 10% of open interest and volume, cf. [2].

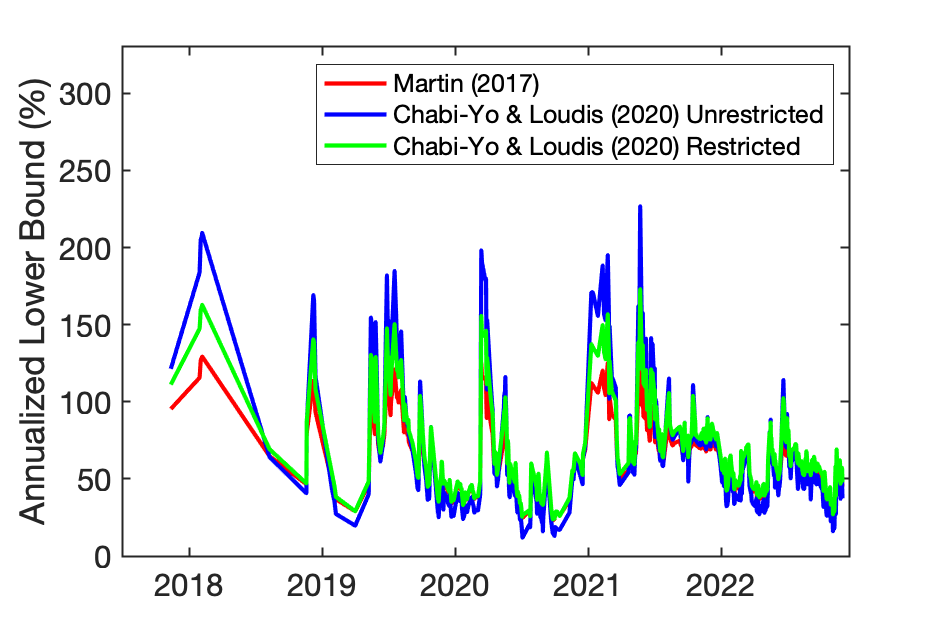

Employing nonparametric statistical techniques on options data and return time series allows us to identify patterns in the BTC market and compare them with traditional financial assets. We start by calculating unconditional measures of risk premia based on BTC returns only. For a one-month horizon, we find that the BTC return premium averages 66% per annum, significantly higher than traditional investments in currencies, commodities, and stocks.555This point estimate for the premium is well-known to be a noisy measure. In the paper we also estimate lower bounds for the BP based on measures extracted from option’s data, in the spirit of [53] and [23]. These conditional lower bound risk premiums are within the range of 20% to 200% between 2018 and 2023 as shown in Figure B.4. Moreover, the annualized BTC VRP is much higher than that of traditional assets, averaging between 7 and 14%, compared to a 2% VRP for the S&P500 ([16]). Despite the BTC volatility is more than twice that of traditional assets like S&P500, BTC’s annualized Sharpe Ratio (SR) of 0.84 is substantially higher than S&P500’s.666For comparison, the S&P 500 equity premium ranges between 5% and 20% per year ([53]) and the S&P 500 Sharpe Ratio is approximately 0.5 ([30]), while SPY’s Sharpe Ratio is 0.45 ([33]).

While unconditional measures of risk premia can be estimated from BTC returns alone, their characterization across return states requires a richer dataset, which options provide. Using the risk premium decomposition method of [12], we find that large positive returns (20% to 60%) contribute 47% of the BTC premium, compared to less than one-third for the S&P 500. [45] report an "inverse leverage effect" for bitcoin, similar to commodities, which may explain these findings. [60] also show that most jumps in the bitcoin market are positive, contrasting with the belief that jumps signal price crashes. Furthermore, [4] document symmetric or upward-sloping implied volatility due to significant upward movements in BTC options. Overall these results are compatible with high prices for Out-of-the-Money (OTM) calls that directly contribute to an increase of risk premium in the positive BTC returns region.

We analyze risk premia across different states by examining the prices of Arrow-Debreu securities per unit of real probability per state, derived directly from the pricing kernel (PK), which we estimate nonparametrically ([47, 1, 59]). Similar to the S&P 500 index, the BTC empirical PK exhibits a U-shape, a characteristic usually linked to a high variance risk premium (VRP) and negative returns for out-of-the-money (OTM) calls ([21], [9], [28]). For BTC returns ranging from 20% to 60%, which account for approximately 50% of the index risk premium, we find an average price of risk of 0.62, contrasting with an average price of risk of 1.00 for positive S&P 500 returns ([12]). For returns between -60% and -20% account for 33% of the Bitcoin premium (BP) with an average price of risk of 1.33, significantly lower than the 2.63 found for the S&P 500. Overall, we conclude that BTC investors pay a lower premium per return state than S&P500 investors to be protected against either downside or upside risk.

A natural follow-up question is whether risk premia change with market conditions. To explore this, we propose a clustering approach to identify distinct market regimes based solely on option prices. Given their forward-looking nature, options are more sensitive to market changes, making them ideal for capturing these conditions. Using a distance-based clustering method (see [55]), we group time-varying risk-neutral density (RND) functions derived from option prices. The goal is to cluster RNDs so that those in the same group reflect similar investor behavior under similar market regimes. We identify two clusters: one representing a high-volatility (HV) regime and the other, low-volatility (LV).

In the high-volatility regime, the contribution of large positive and negative returns to the BP is roughly the same, around 40%, in line with standard preference models. The price of risk is higher than the unconditional estimates for large positive returns and lower for negative returns, indicating that when volatility is high calls are on average more expensive and puts less expensive than their corresponding unconditional average prices. In addition, VRP is lower in this regime, suggesting that investors are less concerned with variance risk. On the other hand, under the low-volatility regime, returns for out-of-the-money (OTM) call options are often positive, indicating that investors take leveraged bets to exploit the upward potential of the BTC market. At the same time, the deep out-of-the-money calls are negative on average, consistent with investors paying a premium to protect themselves against volatility risk. The VRP is higher in this regime, indicating that BTC investors are more concerned with variance risk during the LV regime, which is intriguing. The PK is still U-shaped, but the market price of risk of large negative returns is higher compared to the HV estimates. This suggests that losses are more painful for investors during periods of low volatility, which is consistent with the findings of [63] for S&P 500.777[63] show that negative returns are substantially more painful to investors when they occur in periods of low volatility, which is reflected in a steeper projected pricing kernel (lower price of risk) and larger risk premia on out-of-the-money put options. For the positive returns during the LV regime, the lower price of risk leads to cheaper call options with strikes between 20% to 60%, leading to gain opportunities for long-call investors. Indeed, our estimates for the BP are slightly higher in this regime compared to the HV. A plausible interpretation for this is that BTC investors increase their risk appetite when benchmarking their performance relative to the index, prompting investors to buy call options to take advantage of the index’s upward potential (see [38]).888For DAX, [38] find that PK peak occurs during periods of low volatility, low uncertainty, and high returns.

This paper is structured as follows. We start with a brief literature review in the next subsection. Section 2 provides a detailed overview of the data. Sections 3 and 4 introduce the theoretical framework and the estimation methodology, followed by Section 5, which highlights the main findings. Section 6 provides a thorough summary of the findings and implications of this article, and offers recommendations for future research.

1.1 Related literature

In this article, we empirically document stylized features of risk premia in the BTC market by employing methods commonly used for traditional assets. We estimate unconditional risk premia implied by options data and returns, decompose them based on return states, and introduce a statistical method to track how risk premia vary with market conditions. Our work connects with three main strands of literature.

The first strand analyzes risk premia in cryptocurrencies using BTC options and returns. While studies on cryptocurrency indexes are on a more developed stage, research on digital currency derivatives remains in its infancy, with limited exploration of cryptocurrency options risk premia999An exception is [3], who are the first to estimate a Variance Risk Premium for Bitcoin, though using a limited data set of options.. We contribute to this literature by documenting the existence and variation, over returns states and market regimes, of BP and VRP in the BTC market. Our unconditional BP estimates align with those reported by [35] and [73], who use returns data on BTC with the early-adoption phase (before 2014) excluded. [26] show that Bitcoin’s pricing kernel is decoupled from the consumption kernel, with minimal impact from real-economy shocks, like the Covid-19 crisis. In a similar setup, [74] explore pricing kernel term structures, while [45] study co-jumps between price and volatility and their impact in Bitcoin option prices. [20] propose an equilibrium model with diffusive and jump risks that lead to sizable risk premiums that increase with strike and decrease in maturity.

The second strand of literature focuses on the decomposition of risk premia on return states. The price of risk is naturally expressed as a function of returns through the projected PK, and plenty of studies characterize projected PK using options and returns data. Most of these studies focus on the equity market; see references below. However, the literature on the decomposition of EP on return states is relatively sparse and mostly limited to equity premia. We contribute to this literature by documenting the unconditional patterns of BP function and PK. Our paper follows closely [12] for the unconditional EP decomposition using nonparametric techniques. Using the same methodology, [6] study the EP implied by Zero Days to Expiration (0DTE) options. A parametric approach is proposed by [24] to decompose return and higher order risk premia on regions of down, up, and moderate market returns.

The third strand of literature relates to the conditional estimation of options implied risk premia, pricing kernel risk, and return premium decomposition. Most of the early work prespecifies the conditioning variables to investigate the main features of the conditional estimates. Among these, variance is the most used variable to explain the monotonicities in the pricing kernel of S&P 500 index. For instance, [17] propose a Heston-type model that leads to a U-shaped PK when the variance risk premium is positive. Their approach is similar to [28], who propose an augmented [43] model that nests a U-shaped PK in the presence of a positive variance premium parameter. [22] find that PK increases in market volatility, which can explain the shape of the PK. [66] find that PK decreases in the market index return when conditioned by the market variance, while the unconditional estimates of the PK may appear U-shaped when the relationship between returns and variance is positive. In contrast, [63] claims that volatility evolves independently of the pricing kernel. [48] investigate the shape of the unconditional PK during a high and low VIX regime and find that once the information is consistently conditioned, the PK is always nonincreasing. [38] analyze the shape of the German DAX index PK in relation to the VRP as a proxy of market uncertainty and report a humped-shaped PK during low uncertainty and a U-shaped PK during high uncertainty. In comparison, we have LV and high VRP for BTC, which implies that BTC investors increase their risk appetite during high uncertainty. Other studies suggest that the shape of the pricing kernel varies across different economic conditions by linking them to the macro-finance and market-specific variables. [59] find that the slope of the PK is positively correlated with indicators of recession, such as widening of credit spreads, and negatively correlated with indicators of expansion. [37] find that PK hump is more pronounced when the economic indicators suggest an expanding economy, while it shrinks in recessions. In contrast to these studies, we propose a statistical approach that relies on distance-based clustering to identify relevant market regimes for the BTC market. This allows us to characterize risk premia in two main regimes by impolitely using information from the entire market. We find that variance (both RV and BVIX) is an important variable for characterizing the drivers of the clusters; we name them HV and LV regimes. We also acknowledge that factors other than volatility drive the underlying data process. Indeed, BP and VRP have different patterns, as do the shape of BP and PK functions. Our novel contribution to the existing literature lies in applying established clustering statistical techniques within the context of financial data analysis. This approach applies to any liquid options market and does not require the pre-specification of conditioning variables.

2 Data

The data contains cash-settled European-style options traded on the Deribit exchange and daily BTC prices, available via the Blockchain Research Center (BRC). Daily USD denominated BTC prices are collected from January 2014 to December 2022. Deribit calculates BTC prices as a weighted average across eleven major cryptocurrency exchanges101010We discard earlier data since prior to 2014 Bitcoin prices were very volatile and less reliable. For instance, BTC skyrocketed from $13 at the beginning of 2013 to $1000 by November of this year, increasing by over 75 times in just 11 months. Bitcoins are divisible, such that the quantity traded can be expressed in decimals ([60]), and are traded around the clock on several exchanges.

We use daily options transaction data spanning from July 2017 to December 2022. The raw data includes timestamp, order type (call or put), volume, instrument price, strike price, spot (price of the underlying), implied volatility, and transaction type (buy or sell). Each contract has a lot size of 1 . All prices and instruments are denominated in U.S. Dollars. Following [18], we implement some filtering to mitigate potential errors in the raw data. A notable distinction in our paper is the nature of transaction data, which provides a single option price per transaction rather than separate bid and ask prices. Further, we exclude option observations where i) option price is under 10 USD, indicative of deep out-of-the-money and illiquid options; ii) transactions are non-unique, iii) implied volatility is missing or non-positive, iv) no-arbitrage conditions are violated. Moreover, we exclude the days with fewer than 100 transactions. Consequently, our dataset comprises 1301 days, including 7,832,590 transactions.

We define time-to-maturity measured in days for each option contract. The moneyness of a contract is , where is the strike price, and denotes the current BTC price. From Deribit (via BRC), we obtain the daily BTC settlement prices calculated as the average of the underlying BTC index over the last 30 minutes before settlement time (8 am UTC) for the corresponding maturity date. The trading fees are 0.03% of the underlying or 0.0003 BTC per option contract, capped at 12.5% of the contract’s value.

Setting a good proxy for BTC’s risk-free interest rate and cost-of-carry is challenging. There are no BTC bonds traded on the market. Although BTC futures could be used to estimate the cost-of-carry rate of holding BTC security, the market frictions on unregulated exchanges such as Deribit can lead to unreliable proxies. BTC does not pay dividends, but implicit costs originate in low liquidity, leading to stale futures prices and jumps in the index, counterparty risk, and transaction costs that would need to be accurately evaluated as they also vary over time.111111Another approach proposed in the literature ([76]) is perpetual contracts. Although perpetual contracts are more liquid than futures on Deribit, they can only recover a flat term structure of the cost-of-carry rate. Besides, neither approach allows us to disentangle the interest rate from the cost-of-carry rate. Therefore, we set the interest rate to zero. This assumption is in line with the practice of Deribit exchanges. For short-term contracts, this assumption is innocuous. We use the first moment of the BTC returns under the risk-neutral measure for the cost-of-carry rate.

The summary statistic presented in Table 2 highlights the essential option characteristics, including time-to-maturity (TTM), moneyness, and implied volatility (IV) from Deribit. Similar to [67], we find that the range of moneyness in the Bitcoin options market is significantly wider than that of traditional options markets, which can be attributed to the highly volatile nature of BTC. The average BTC IV level of 0.82 basis points is much higher than the average S&P 500 IV level of 18% as in [5, 42]121212[50] demonstrates that Bitcoin returns exhibit significantly higher volatility compared to stocks, ranging from 5 to 10 times greater depending on the investment horizon. Furthermore, options with shorter tenors are more frequently traded than those with longer tenors.

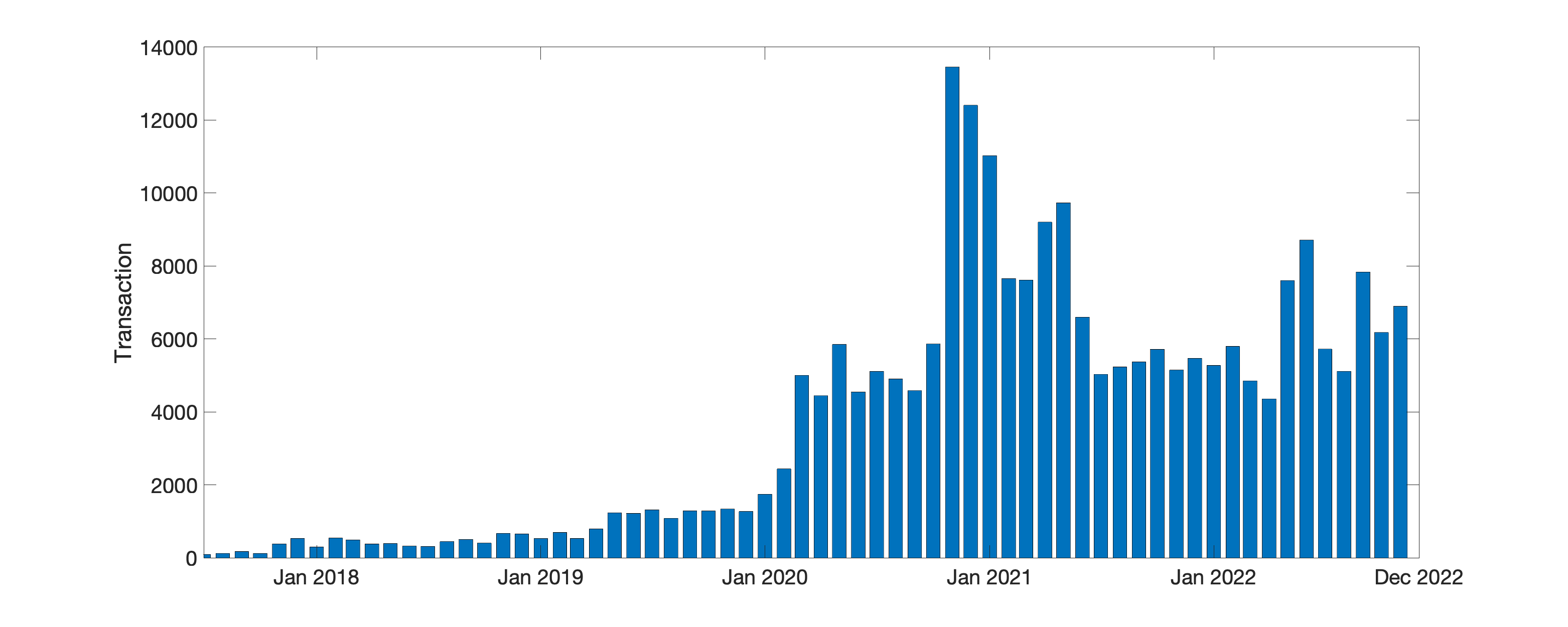

Before 2020, the average daily transaction volume was approximately 646 contracts; after 2020, this number increased to 3,721 contracts, which is almost a 476% increment. A similar trend for average daily transactions is observed in SPX options, albeit the increase is only around 20 %, from 921,948 contracts before 2020 to 1,109,514 contracts after 2020. More information about the data can be found in Appendix A.1. We display the average daily BTC option transactions per month for SPX options and BTC options in Figure A3 in the Appendix.

Summary statistics of BTC options Call Put TTM Moneyness IV TTM Moneyness IV Mean 29.27 1.21 0.82 24.57 0.91 0.89 Median 9 1.06 0.77 8 0.94 0.82 Std. Dev. 49.95 0.55 0.29 44.08 0.19 0.37 Min 1 0.08 0.05 1 0.07 0.1 Max 372 17.71 5 372 15.67 5 The table gives a summary statistic of the filtered BTC call and put options traded daily from July 1, 2017, to December 17, 2022. It showcases the option characteristics, such as the time to maturity (TTM), moneyness, and the implied volatility (IV) from Deribit. The number of transactions for call options amounts to 3,940,541 and 3,468,020 for put options. Consequently, our dataset comprises 1,301 days that include a total of 7,832,590 BTC option transactions, with a daily average transaction volume of 3,721 options contracts.

3 Theoretical Framework

Let the price process of the Bitcoin index be a nonnegative semimartingale with continuously distributed marginals under the physical measure , equipped with a filtration . In what follows, we focus on unconditional distributions of the -days ahead returns .131313Working with simple net returns enables a direct comparison to [12].

The arbitrage-free assumption implies the existence of an equivalent measure (to ) identified with a risk-neutral pricing rule. Under such a measure, discounted prices have the martingale property, such that the returns satisfy , with being the (average) risk-free rate. Furthermore, we assume that the probability measures and are differentiable with respect to the returns. Then, for each value of the returns and , with being the risk-neutral density and being the physical density.

3.1 Equity Premium Decomposition

One way to gain insights into the pricing of risk and the risk behavior of investors is to analyze the equity premium. Under no-arbitrage, it holds that the unconditional bitcoin return premium, that we denote as BP, is

| (1) |

where and . We utilize a novel method proposed by [12], originally used to analyze the S&P 500 market, to investigate the decomposition of BP in different returns states, such that

| (2) |

For ease of interpretation, we use a standardization by the equity premium that guarantees that the function approaches zero for returns in the far left tail and one for returns in the far right tail. Note that the function is not restricted to be monotonically increasing. Equation (1) indicates that BP increases when the physical density exceeds the risk-neutral density for negative return states, and the risk-neutral density is greater than the physical density for positive return states. Consequently, the function can take intermediary values larger than one and smaller than zero.

The no-arbitrage assumption is also equivalent to the existence of a positive random variable , called a stochastic discount factor (SDF), such that . We refer to the projection of the SDF on the set of Bitcoin returns as the pricing kernel function with . The pricing kernel is the Radon-Nykodim derivative of the risk-neutral measure with respect to the physical measure. Given the assumption that the two measures admit probability density functions, the pricing kernel can be computed as the ratio of two densities for

| (3) |

To help us characterize risk pricing in more complex markets with dynamic stochastic variance and jumps, we employ the variance risk premium (VRP):

| (4) |

where and . A positive VRP indicates that variance buyers are willing to pay a premium to hedge away upward movements in the index return variance. At the same time, a negative VRP signifies that the buyers request a positive amount to participate in a stochastic volatility market. The VRP in Equation (4) is defined differently than the BP in that a premium is paid to avoid the variance risk of the asset, hence the resulting sign inversion for the moments under the two measures. Note that neither the Black-Scholes model nor the conventional consumption-based model with constant relative-risk aversion (CRRA) preferences can generate a non-zero variance premium (e.g., [31]).

The shapes of the and functions are intimately related and contain information about the entire distribution of returns. Both functions can provide direct information about the VRP. A connection between the , the shape of the , and the prices of risk focusing on the negative returns are provided by [12]. Further, [6] document the link between the and for positive returns. They emphasize how a U-shaped PK induces a non-monotonic pattern in , i.e., a hump with a decaying region necessarily in the range of positive returns. Specifically, an increasing PK with values larger than one for positive returns is compatible with locally decreasing BP, which signals a positive VRP. We additionally highlight how the shape of a PK function with priced (and not priced) variance risk affects the shape of the BP function. The presence of VRP affects the shape of the pricing kernel in a non-trivial way. For the region of negative returns, VRP leads to a steeper negative slope , while for the region of positive returns, the slope increases and may even become positive, potentially leading to a (locally) increasing . For this reason, in practice, a U-shaped PK with a monotonically increasing region for positive returns above a given threshold is often documented in connection to a high VRP.141414The exact range of options that yield negative returns depends on where the U-shaped is formed, as it is not guaranteed that the increasing region appears exactly ATM.

3.2 Density Clustering

Previous studies on the equity premium (EP) and variance risk premium (VRP) have largely focused on unconditional analysis. This work introduces a nonparametric, data-driven approach for conditional analysis, uncovering time-varying patterns in the pricing kernel, Bitcoin premium, and VRP. We utilize a sequence of risk-neutral densities to capture expectations and identify similar market regimes. Our objective is to group these densities into homogeneous clusters, where densities within a cluster are more similar to each other than to those in different clusters. The process involves three steps: (1) applying a log-based transformation to the densities, (2) computing the Euclidean distance matrix of the transformed densities, and (3) using hierarchical clustering to identify distinct clusters.

A straightforward way to cluster densities is to focus only on a specific time-to-maturity , ignoring others—what we refer to as the univariate approach. While simple to implement, this method faces a key drawback: Bitcoin data is inherently noisy, causing instabilities in the clustering results. This limitation naturally leads to a more robust clustering of the densities, which we call the multivariate approach. Assuming the risk-neutral density is estimable across a continuum of strikes at time t, viewing these densities as a composition allows us to capture a more nuanced representation of investors’ future expectations. Alternatively, this can be seen as utilizing the entire implied volatility (IV) curve rather than a single IV function for a given . The multivariate approach outperforms the univariate one by incorporating information across both the moneyness and expiry dimensions, leading to more reliable clustering results.

Because a density function satisfies the constraints and , densities are not situated within a vector space. Consequently, traditional functional data analysis methods based on Hilbert space are not applicable [56]. An isomorphic mapping of the density from the separable Hilbert space to the standard space is required to perform standard statistical operations. Different transformations are possible, such as taking the natural logarithm. As outlined in [52] and [32], a straightforward isomorphism that has shown better results in practice is the centered-log-ratio (CLR) transformation. The transformation is applied to the RND function and is defined as

| (5) |

with the geometric mean of the risk-neutral density function . The transformation is performed separately for each .

In the second step, we compute the distance, following [55], between all pairs of transformed densities indexed by and . The distance is defined as:

where and . Building upon the resulting Euclidean distance matrix, the risk-neutral densities are grouped into homogeneous clusters, where homogeneity is measured by the symmetric distance measure of the transformed densities. In case of , it follows that for all and .

We apply the agglomerative hierarchical clustering method with the ward linkage on the calculated Euclidean distance matrix [72]. The Ward method, which minimizes the overall within-cluster variance, has the advantage of producing well-balanced clusters. MOreover, the obtained clusters are also robust with respect to the choice of linkage (complete, single or average). More details on the agglomerative clustering method are given in Chapter 14 in [40].

4 Estimation Procedure

To unify the various methods in existing research that combine option prices, underlying asset prices, and investment decision data, we employ flexible estimation procedures. All our estimators are semi-parametric or nonparametric. This approach enables us to better understand the underlying phenomena without imposing rigid models.

4.1 Physical Density

The physical density is estimated using the empirical probability density function (PDF) of returns. Robustness checks with kernel density estimation show results largely consistent with those from the empirical PDF.

First, the empirical PDF is estimated as a histogram of the full sample of overlapping returns, denoted as simple returns , where is the daily BTC price for . Following [12], we smooth the empirical PDF between the 10th and 90th return percentile using a 10th-order polynomial. For the tail regions, the Generalized Extreme Value (GEV) distribution is employed, analogous to the technique outlined in Section 4.2. Thus,

| (6) |

where is the estimation projection from the full sample overlapping returns to the physical density, and are the left and right tails estimated by the GEV distribution, respectively. The histogram estimate is denoted as and its smoothed version is denoted as . The 10th and 90th percentiles are denoted as and , respectively. Using the full sample overlapping returns as input, the unconditional overall physical density is estimated as .

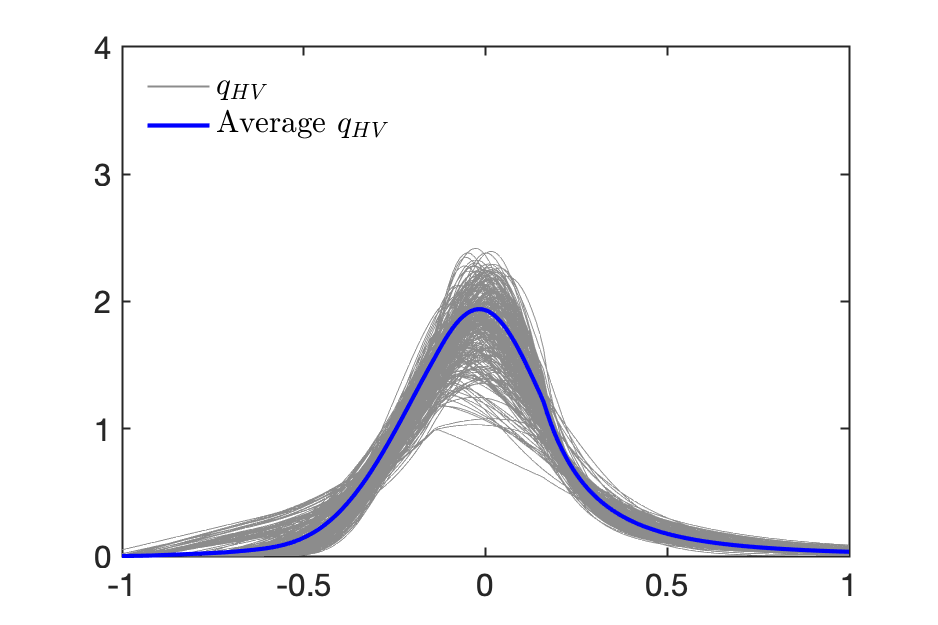

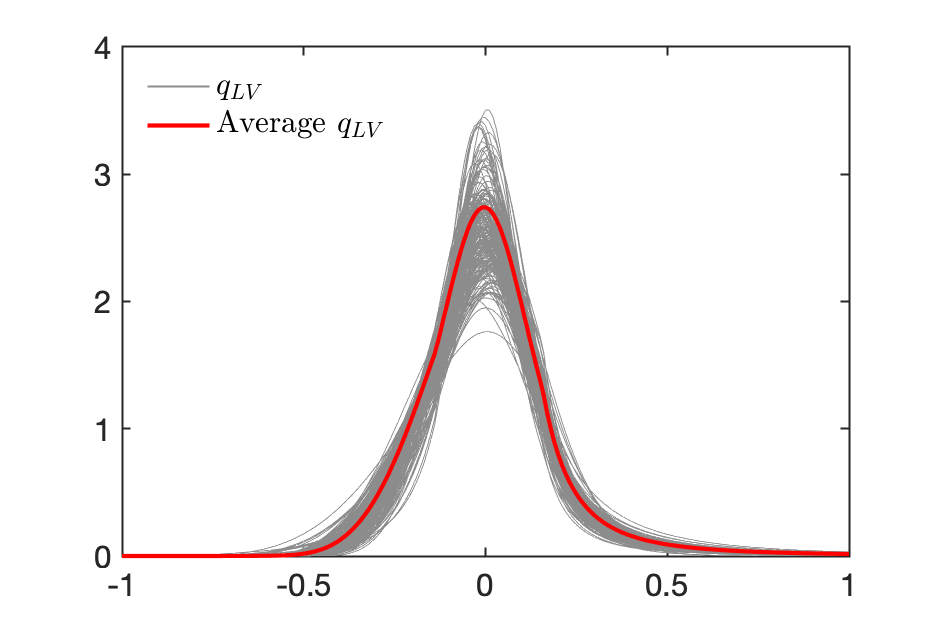

We refer to conditional and cluster-specific density, interchangebly. For each cluster, the conditional density is estimated using rescaled returns. Specifically, the rescaled returns are obtained from the full sample overlapping returns according to the volatility levels in each cluster and standardized by the unconditional volatility, as denoted by

| (7) |

The cluster-specific density is thus estimated separately using the rescaled returns , i.e., and .

Equation (7) is based on the realized variance (RV) to make estimates in the two clusters comparable. The average RV for cluster is denoted as and represents the average overall RV. Each cluster is represented as a set of dates for , which we obtain by our clustering methodology. Finally, the annualized RV on day is calculated as the sum of squared log returns over the past days,

An alternative way to rescale is to use the second moment of the kernel density estimated per cluster, divided by the second moment of the overall kernel density. We have conducted robustness investigations for this method, and the estimated densities are not significantly different. Results can be provided on request.

4.2 Procedure for the Risk Neutral Density

The estimation of the risk-neutral density consists of several carefully designed steps, described below.

Interpolation of the Implied Volatility

To estimate the risk-neutral density from options, we concentrate on options transactions with maturities ranging from 3 to 60 days and moneyness between 0.5 and 2. We exclude options with shorter or longer maturities and those with a wider range of moneyness due to excessive noise and insufficient liquidity.

For each date and maturity, we employ the local polynomial estimator on the discretely observed IVs, as detailed by [58], to estimate a smooth IV curve151515This approach is wildly used

in practice, see also [46] for smoothing with splines.. This ’pre-smoothing’ approach improves the parameter calibration of the SVI model.

The smoothed IVs are subsequently used for estimation of the parametric Stochastic Volatility Inspired (SVI) model proposed by [36]. The SVI model facilitates the interpolation of additional IV curves across different dates and maturities and, in principle, also allows for extrapolation of IV over a broader moneyness range. In addition to the baseline model, we follow [12] and assume the linearity of the parameters in .

The implied variance is given by

| (8) |

where denotes the log-moneyness, represents the time-to-maturity and and are parameters that need to be estimated. Similarly to Gatheral (2004), to enforce no-arbitrage we impose the constraints that , , and . Further details about the interpolation are provided in Appendix A.3, and the interpolated IV surface is shown in Figure A5. As a result of our interpolation scheme, we obtain 547 days of monthly () IVs, with an average of .

The interpolated IV curves are then projected into risk-neutral density by the Black-Scholes model via

where is the call option price derived from the Black-Scholes model, is the strike price, and is the risk-free rate, which we assume to be . Through a change of variable, to be consistent with physical density, the RND is represented as a function of returns ,

| (9) |

Finally, for each day , we estimate the time-varying RND using Equation (9), denoted by . The resulting RND estimate is a composition of nonparametric pre-smoothing of the discrete IV observations and a parametric interpolation of these pre-smoothed IVs.

Averaging the RND

Let us define the average estimated risk-neutral density for the overall sample as

| (10) |

where is an estimator at time . The average estimated conditional risk-neutral density for the clusters is given as

| (11) |

To enhance the reliability of the extreme parts of the risk-neutral densities, we fit the tails using the GEV distribution as detailed by [34], which is outlined in Remark 1.

Remark 1.

The tails of the risk-neutral densities are estimated using the generalized extreme value (GEV) distribution following [34]. The GEV distribution function is defined by

| (12) |

It requires estimating three parameters for both the left and right tails. We focus on two specific points for each tail, considering the Cumulative distribution Function (CDF) and Probability Density Function (PDF). The synthetic GEV tails at these points are optimized by minimizing the discrepancy between the empirical risk-neutral density and the synthetic tails, considering the congruence of both CDF and PDF. Additionally, we ensure that the first moment of the risk-neutral density with synthetic tails corresponds to the risk-free rate, assuming that this rate is zero. A carefully worked out procedure description is given in A.4.

4.3 Pricing Kernel, Bitcoin Premium and the Variance Risk Premium

In this section, we introduce the estimation of the major objectives of our work, the pricing kernel, the Bitcoin premium, and the variance risk premium. As our focus is not on the inference of these quantities, we do not derive confidence intervals and confidence bands. For consistency results on confidence bands of the pricing kernel, see [39].

Pricing Kernel

The pricing kernel is estimated following Equation (3). However, it is of interest to obtain a single pricing kernel, referring to the whole sample instead of one for each day. For this reason, we use the average risk-neutral density as defined in Equation (10).

The physical density is estimated by , on the full sample overlapping returns. Thus, we obtain the pricing kernel by plug-in as

| (13) |

where the estimates and is explained in Section 4.2 and 4.1, respectively. Further, the pricing kernel conditional on the clusters is estimated as

| (14) |

where is the estimated physical density on the rescaled returns as defined in (7).

Bitcoin Premium

The unconditional equity premium, which we denote as Bitcoin Premium (BP) is estimated by plug-in of the risk-neutral and physical estimates

| (15) |

with the decomposed BP estimated as

| (16) |

The first annualized empirical moments under the and measures are given by and , respectively. Since the empirical first moment of the estimated risk-neutral density might deviate from zero, for comparison, can also be calculated based on .

The conditional BP for both clusters is defined as

| (17) |

with the decomposed BP defined as

| (18) |

where is the estimated physical density on the rescaled returns defined in Equation (7).

Variance Risk Premium

Estimating the variance risk premium is one of the main interests in this work. Recall that the variance risk premium is defined as the annualized -variance minus the annualized -variance,

| (19) |

where is an estimator for and is an estimator for . Hereby, the empirical -variance is based on either the risk-neutral density or the BVIX. Let us define the (average) annualized -variance based on risk-neutral density as

| (20) |

where is the (non-annualized) first empirical moment of the average density over .

Moreover, a daily Bitcoin Volatility Index (BVIX) is constructed, similar to the VIX methodology but based on BTC options. The BVIX reflects a market-specific reflection Bitcoin volatility directly captured from options, and no extrapolation is used to obtain the BVIX. As an alternative measure of -variance, the average of the squared BVIX is derived by . Details on the calculation of BVIX are provided in Appendix A.2.

The -variance is either the second moment of the density estimated by the empirical PDF of full sample overlapping returns, or the average realized variance . The density-based -variance is obtained by integrating the squared deviation of returns from their means over the physical densities

| (21) |

Note that both and represent annualized physical variance. While RV is time-varying, remains constant within each cluster over time. An alternative way to estimate the variance risk premium is via a zero beta strategy as in [48] and applied to the BTC market by [75].

The conditional VRP for both clusters is defined as

| (22) |

with and . The cluster-specific annualized variance under the measure is estimated as

| (23) |

and the BVIX based annualized -variance is

| (24) |

The conditional annualized -variance is estimated based on conditional physical density

| (25) |

or conditional RV

| (26) |

Remark 2.

Following earlier studies, this work relies on option-based volatility as a proxy for -volatility. We calculate the daily index values for different tenors - the BVIX. Our methodology for constructing the BVIX utilizes intraday option data on BTC. It is based on fair pricing of variance swaps employed by the CBOE to compute the Volatility Index (VIX), a measure of the stock market’s expectation of volatility based on S&P 500 index options. As a supplement, the square root of the risk-neutral variance is used, which integrates the squared deviation of returns from the mean over the risk-neutral density for a specified maturity. Both BVIX and density-based -volatility are annualized for consistency.

To determine the -volatility based on the -density in each cluster, we compute the average risk-neutral densities for dates within each cluster. Likewise, the -volatility based on BVIX in each cluster is calculated as the conditional mean of BVIX values for dates associated with each cluster. For the overall -volatility, we take the average of both the risk-neutral densities and BVIX values, considering all dates encompassed by the two clusters.

4.4 Data-dependent Clustering of Risk Neutral Densities

After the unconditional estimation of the BP, PK, and VRP, a more refined analysis is of interest. The risk-neutral density contains information about beliefs of the market about the future as well as their risk preferences. We believe that the preferences and future beliefs of BTC investors change over time. Thus, tools from functional data analysis are applied to separate the densities across time in a sound way. This enables the investigation of BP, PK, and VRP within two homogeneous regimes. In a well-studied index such as the S&P 500, a separation of the past observations can be conducted by comparing the VIX to a threshold, e.g. the median VIX value [48]. In principle, we could use a similar approach using our calculated BVIX measure. However, the risk-neutral densities include more information than a market volatility index, resulting in a more nuanced analysis. We first estimate the risk-neutral density as described in Section 4.2 and take the CLR transformation of Equation 5. For the multivariate clustering approach introduced in Section 3.2, only the dates are selected, at which all four time-to-maturities of interest are observed, that is , and

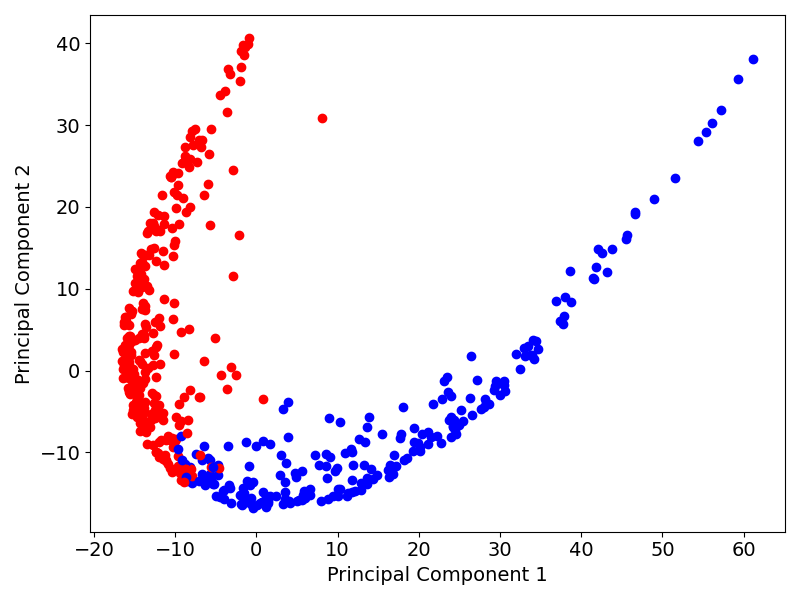

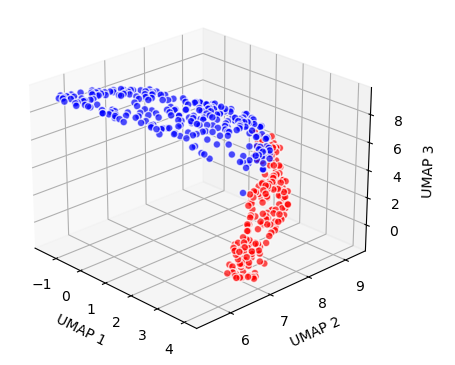

Further, the choice of clusters is underlined by visualizing the risk-neutral densities and the distance matrix in a low-dimensional graph. The first two principal components of the distance matrix are illustrated in Figure 7(a). Second, the Uniform Manifold Approximation and Projection (UMAP) technique [54] is applied, which absorbs non-linear dependencies between the risk-neutral densities. It is elaborated in more detail in Appendix A.6. By marking the reduced-form quantities with the respective cluster, the robustness of the clustering results is confirmed. The UMAP results are illustrated in Figure 7(b). As the low dimensional structure of the risk-neutral densities as well as the distance matrix indicates, selecting two clusters is indeed a reasonable choice.

The proposed classification is based on the endogenous variation of risk measures. To enhance the interpretability of the resulting clusters, we run a logistic regression of the cluster labels on the first four moments of the risk-neutral densities at each day. The regression results are included in Table B.1. As expected, the coefficients of the moments are highly significant. In particular, a higher variance increases the probability of being in the high-volatility cluster. On the contrary, a higher mean, skewness, and kurtosis161616To check for robustness, we estimated Gaussian tails of the risk-neutral density instead of the GEV distribution and reran the logistic regression. It shows that neither clustering nor the results of Table B.1 change significantly. are associated with a higher probability of being in the low volatility cluster. It shows that the variance explains most of the variation in the clusters with an measure of , compared to the other moments. Even if we run a multiple regression on all moments jointly, it barely increases the explained variation in the clusters. This association gives us reason to refer to the first cluster as the high volatility (HV) cluster. In analogy, the second cluster is referred to as the low volatility (LV) cluster.

5 Empirical Results

Our research focuses on a 27-day investment horizon. Table 5 summarizes our main results for the unconditional and conditional BP and VRP estimates. The BP for BTC is significantly higher than that of traditional investment assets such as currencies, commodities, and stocks, averaging around 66% per year. The unconditional annualized implied and realized variances, proxied by squared BVIX (or the second moment of the density) and RV, are also high: 0.71 (0.63) and 0.57, respectively. The corresponding variance risk premium is 0.14 (0.07), much higher than that of the S&P 500 index—approximately 2%, according to [16]. 171717 We have also experimented with the physical variance based on the unconditional smoothed physical probability density. The estimates of conditional variances are very similar (0.75 in HV and 0.54 in LV), while the unconditional variance estimate of 0.66 is slightly higher. The estimated variance risk premium of 0.05 (-0.02) is relatively small compared to the S&P 500 index, which is a relatively puzzling behavior. Therefore, we only report the results using the standard methodological approach in the literature. We further analyze estimates across market regimes to verify if the VRP remains positive and stable, as observed in the full sample. Our results show that risk-neutral and physical variances vary across clusters. Specifically, the HV cluster describes a highly volatile market, identifiable by high second moments of BTC returns, where the monthly annualized variances are 0.88 (0.80) for the risk-neutral and 0.76 for the physical measure, respectively.

Risk Premia Panel A: Bitcoin Premium Based on density Based on Overall HV LV Overall HV LV 0.66 0.73 0.55 0.67 0.69 0.62 0.67 0.69 0.62 0.67 0.69 0.62 0.01 -0.03 0.07 0 0 0 Panel B: Bitcoin Variance Risk Premium Based on density Based on BVIX Overall HV LV Overall HV LV 0.07 0.04 0.10\tmark[] 0.14 0.12 0.17 0.63 0.80\tmark[***] 0.43\tmark[***] 0.71 0.88\tmark[***] 0.50\tmark[***] 0.57 0.76\tmark[***] 0.33\tmark[***] 0.57 0.76\tmark[***] 0.33\tmark[***] Days 505 278 227 482 271 211 Panel A: Estimates of the unconditional BP and conditional . Panel B: Estimates of the unconditional VRP and conditional . Unconditional estimates are referred to as ’Overall’, and the conditional ones are cluster-specific for . is estimated as the first moment of density, as the sample mean of realized variances. For and , we illustrated two estimation approaches. All the estimates are annualized. We use ANOVA to test if the conditional estimates are different than the unconditional ones ( no difference), with , and denoting significance level.

In contrast, the LV cluster describes a less volatile market, identifiable by relatively smaller variance proxies, with a risk-neutral variance of 0.50 (0.43) and physical variance of 0.33. The variances under the two measures in both market regimes are quite different and introduce a substantial VRP. Surprisingly, the low volatility cluster is characterized by a higher VRP of 0.17 (0.10) compared to the high volatility cluster of 0.12 (0.04), suggesting a potential disconnect between variance and VRP. Comparative analysis of reveals that consistently exceeds the second moment of density by approximately 8%, both in unconditional and conditional cases.

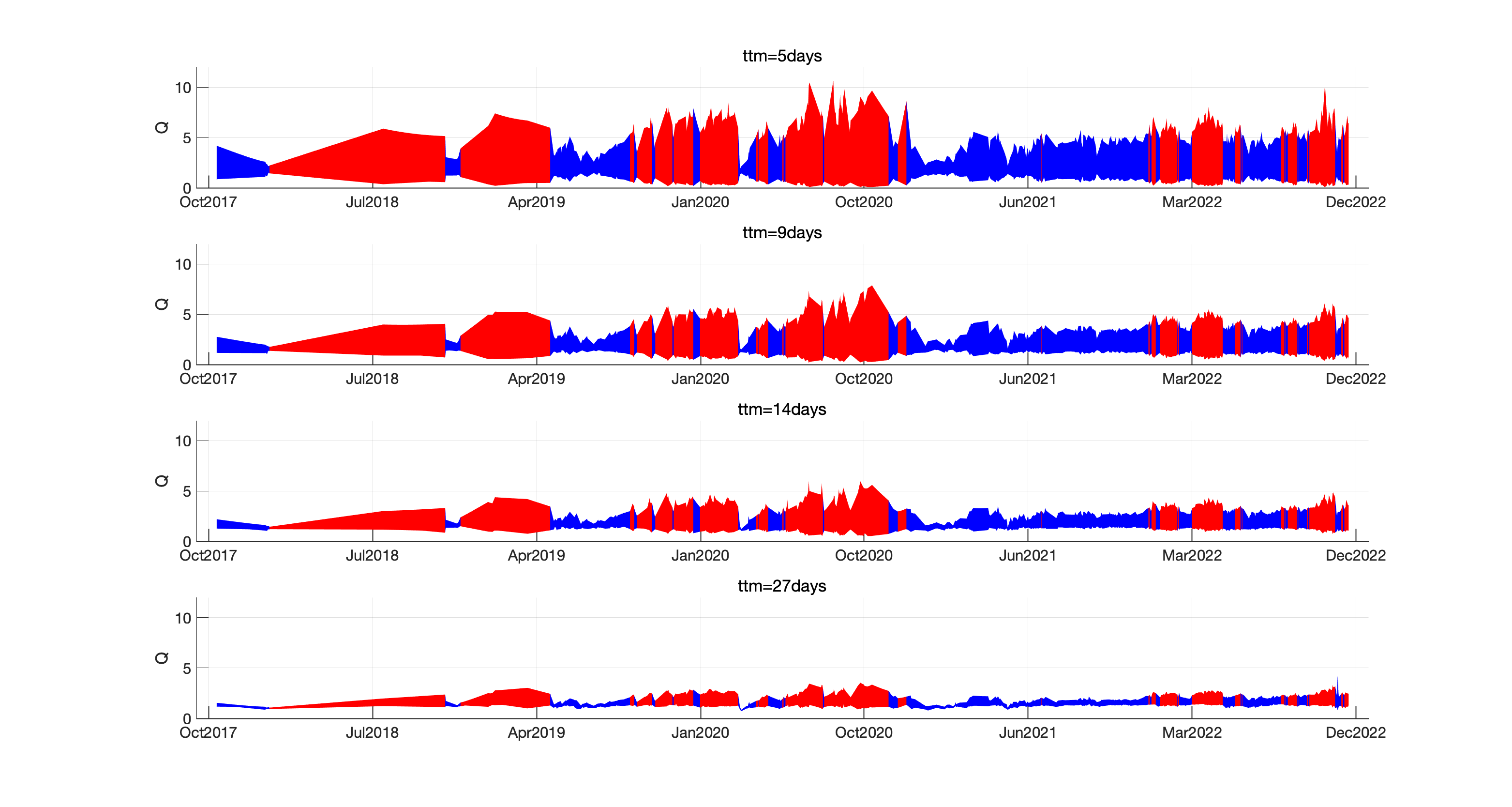

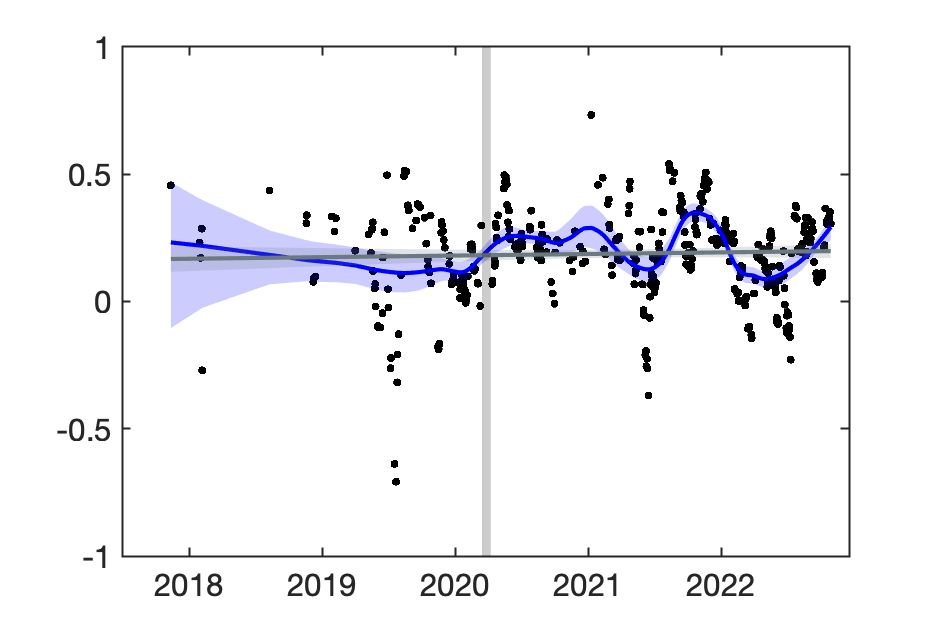

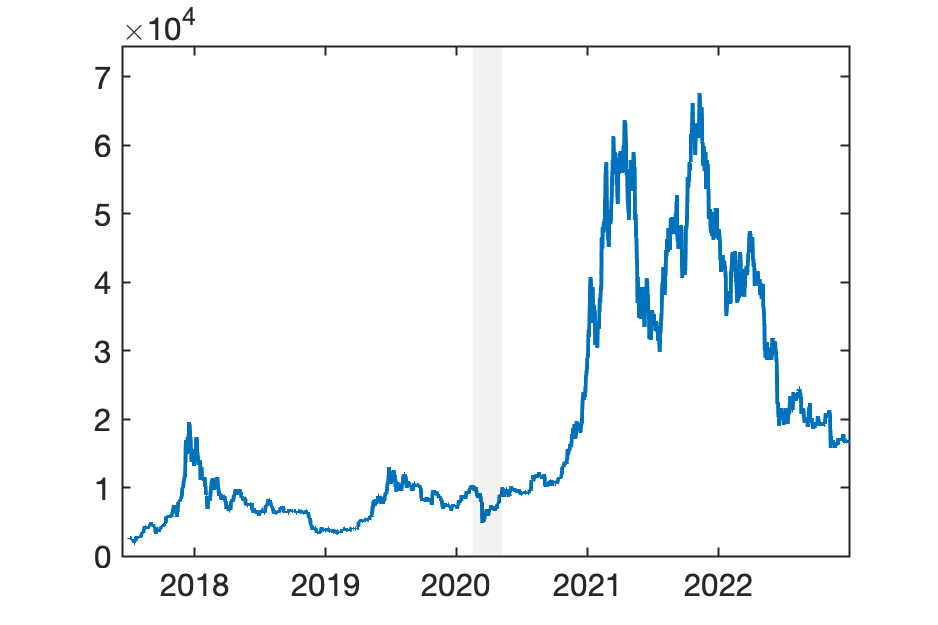

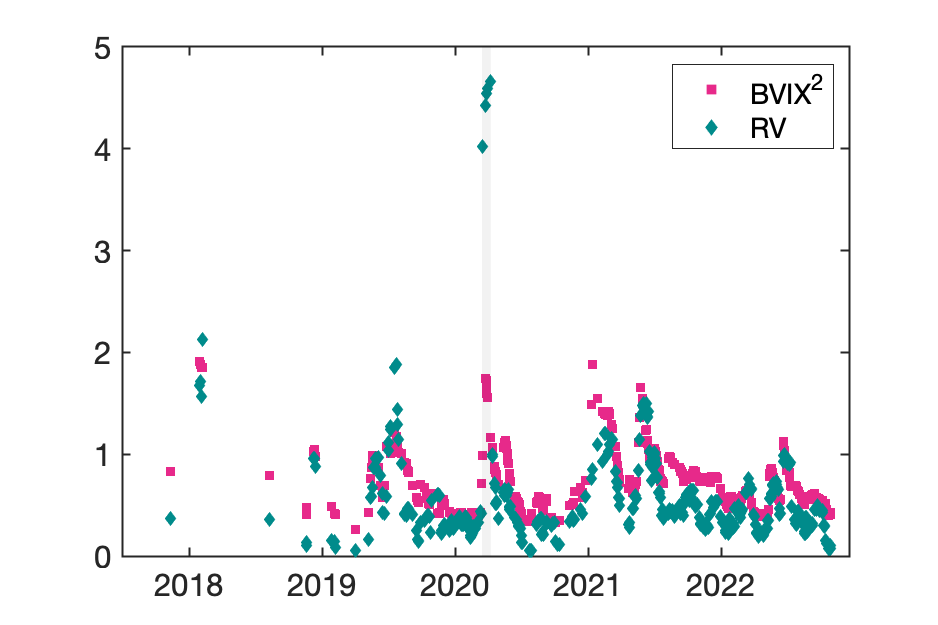

The plots in Figure B4 show the BP and VRP estimates over time. We observe a temporal clustering of observations, probably due to the volatility clustering present in the data. There is a slight tendency for the BP to decline over time, while the VRP is slightly increasing over time. Further, we look closer into the components of the VRP. The time series of and RV in Figure B5 (b) indicate a tendency of positive comovement, with generally exceeding RV, apart from a period between Mar 15, 2020 and April 8, 2020 when RV significantly surpassed and VRP takes values below -2 as marked in Figure B4 (b).

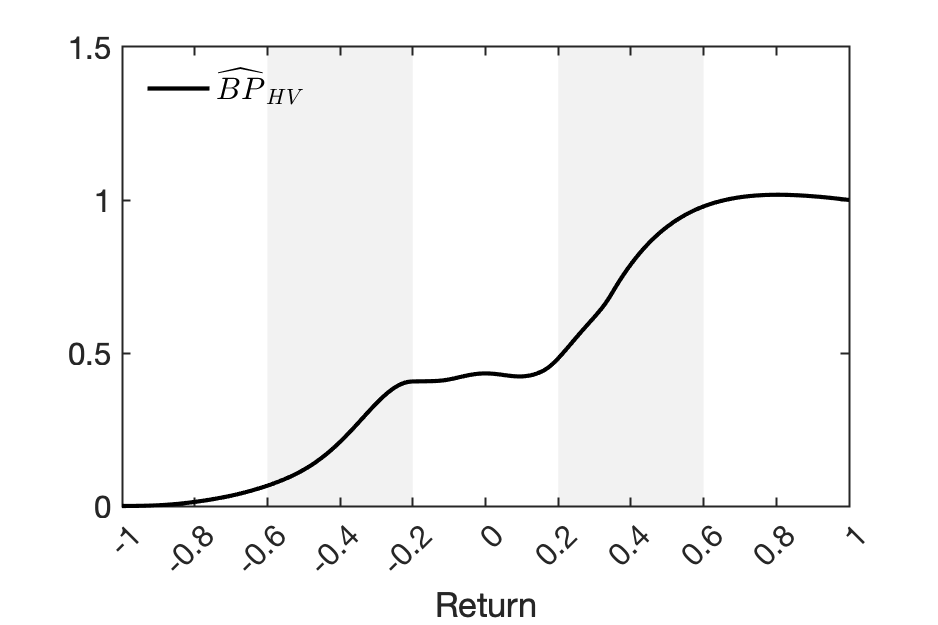

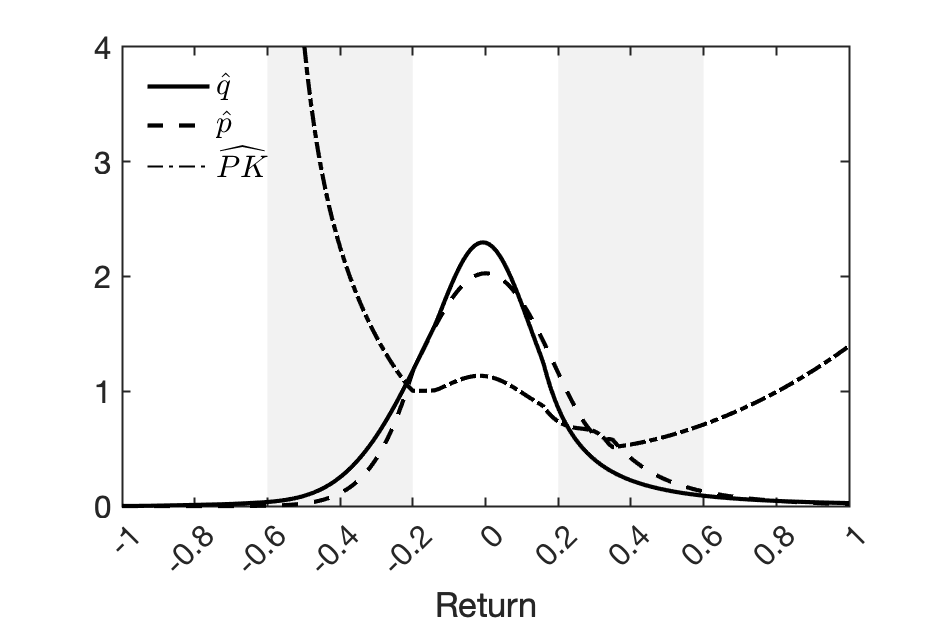

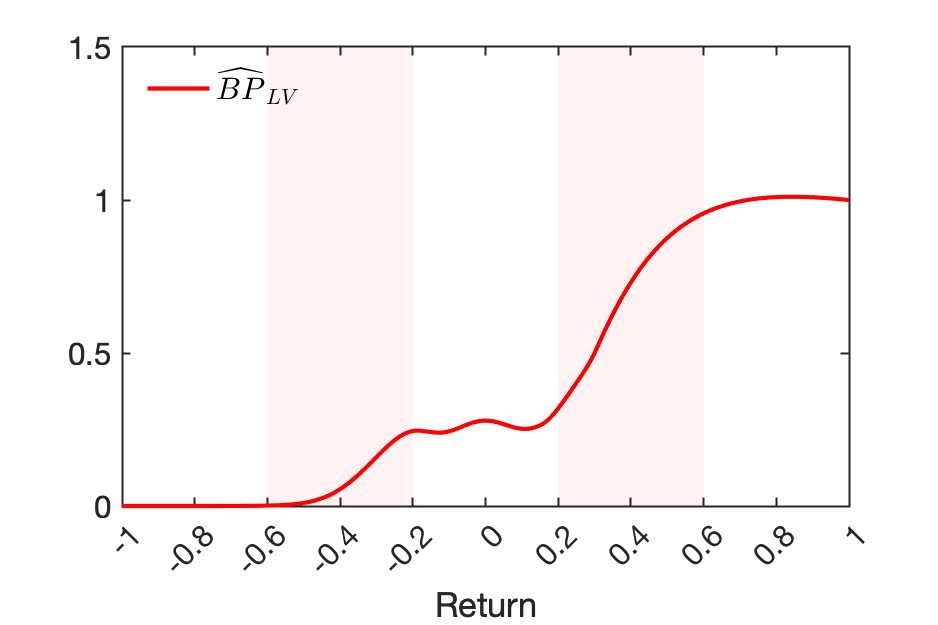

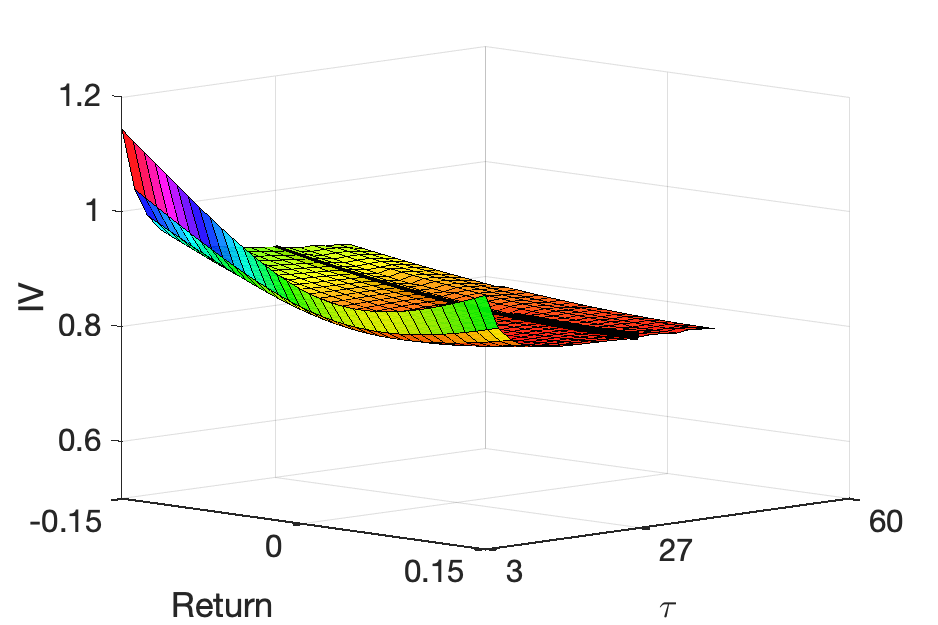

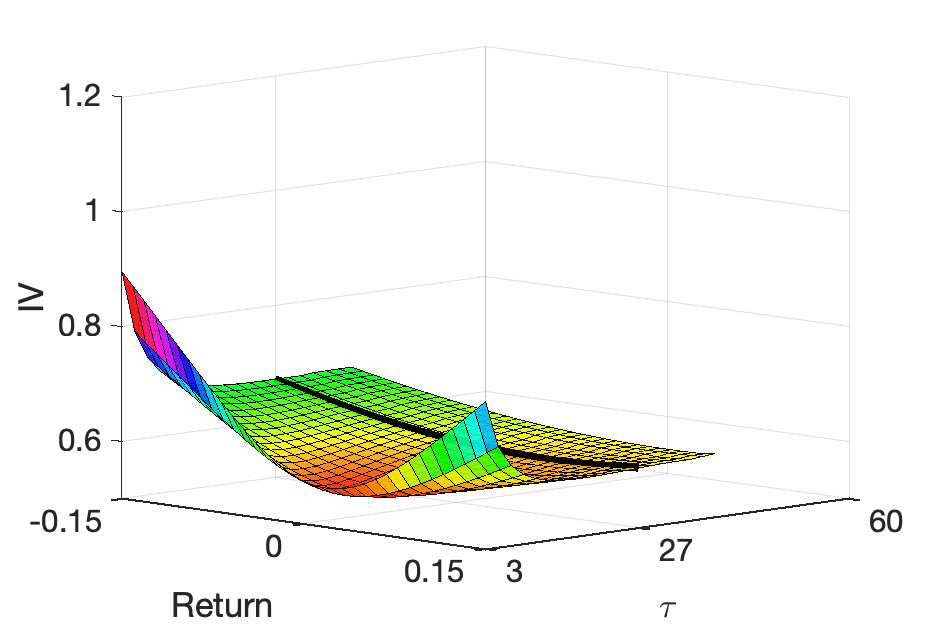

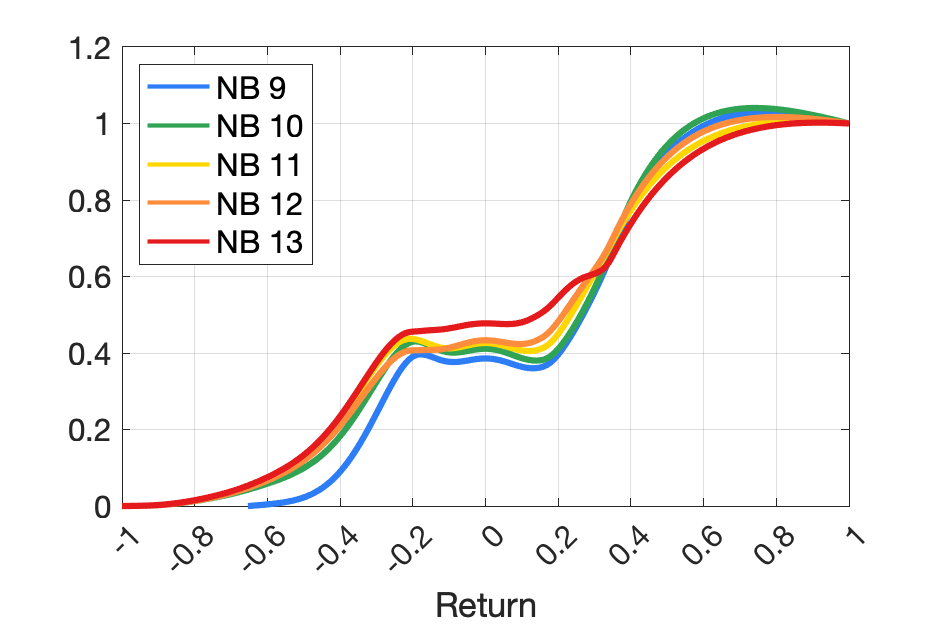

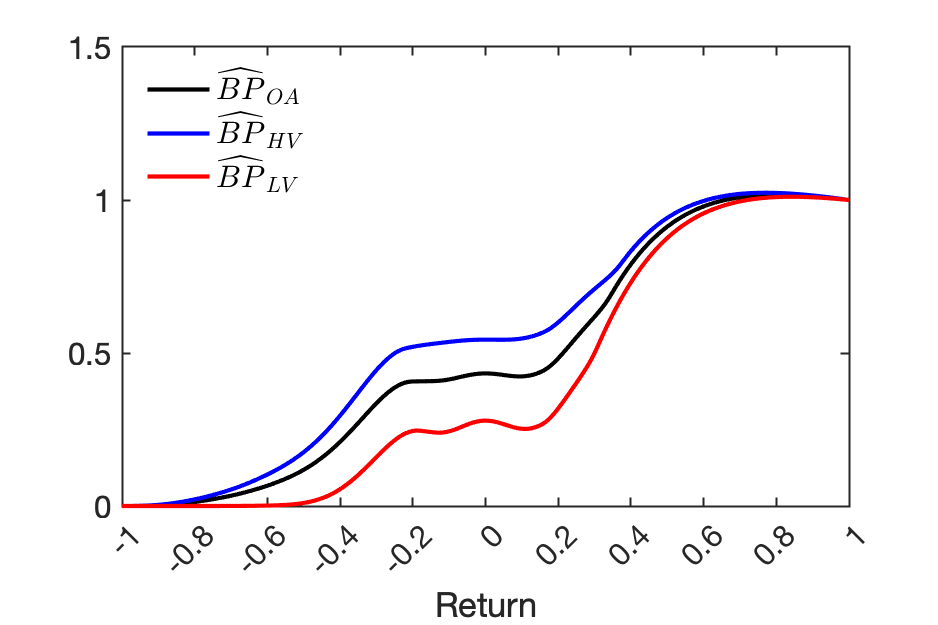

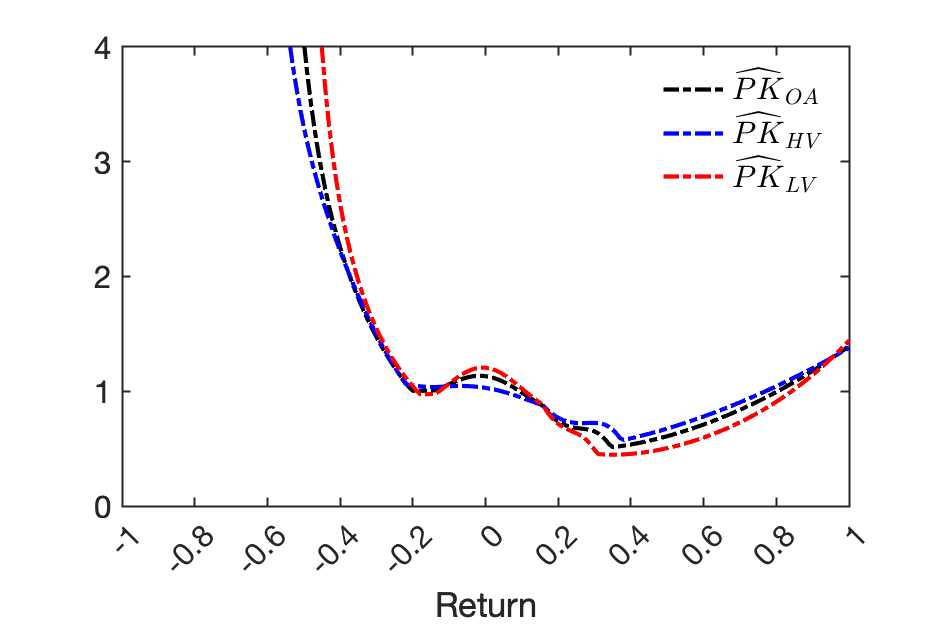

For the unconditional BP and PK estimates in Figure 1, we find that negative monthly returns between -60% and -20% and positive returns ranging from 20% - 60% account for 33.97% and 48.35%, respectively, to the Bitcoin premium. These features are interesting because they suggest that in the Bitcoin market, most of the contribution to the Bitcoin premium can be attributed to positive returns. The low contribution of the negative returns contrasts with the first moment premium for S&P 500 where (monthly) S&P 500 returns between -30% and -10% account for two-thirds of the equity premium reported by [12]. Next, we look closer into these functions across market regimes.

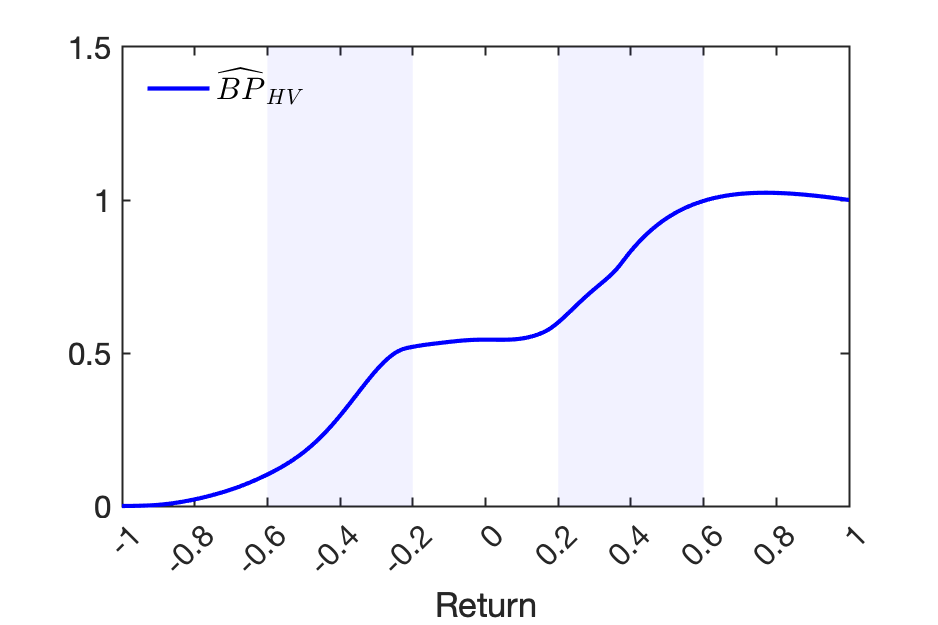

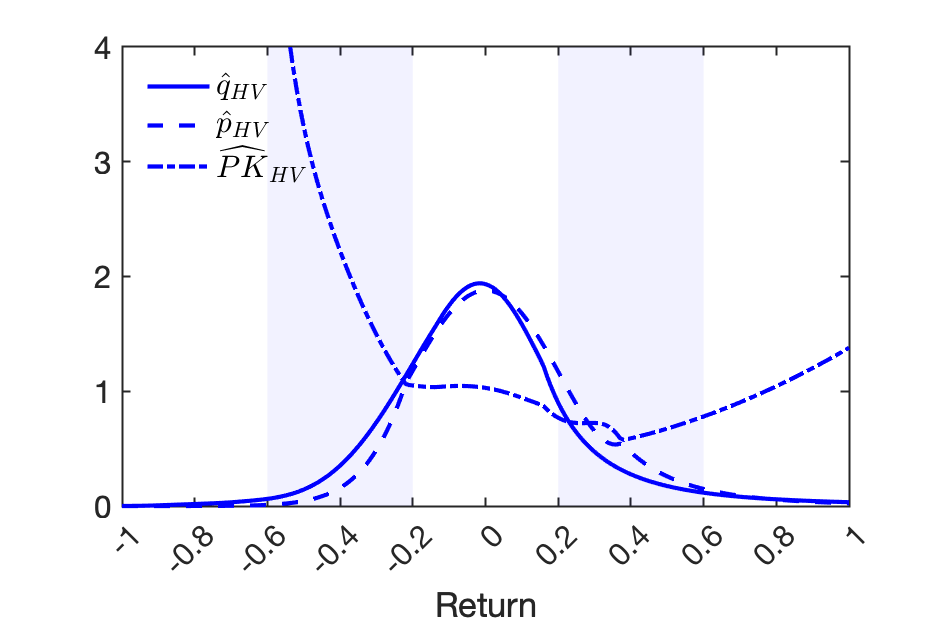

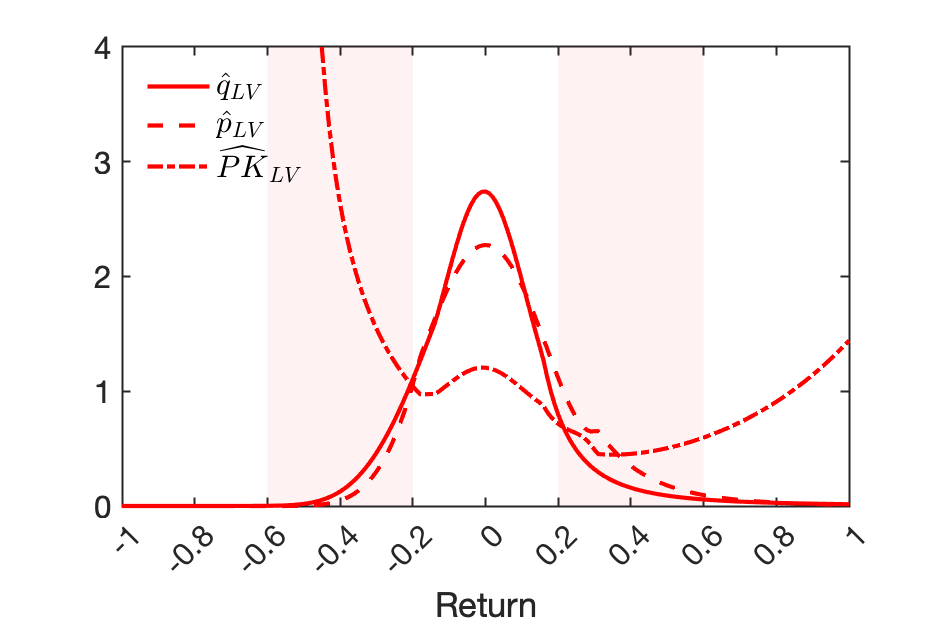

Figure 1 displays the BP function and the PK function for the two clusters, revealing several noteworthy characteristics. Notably, the shape of the HV cluster is more akin to the unconditional BP(x). But there are also some important differences. First, the high negative returns have a stronger impact on the BP(x), i.e., states of returns between -80% to -50% account for around 15% of the BP, indicating that investors are concerned about rare disasters. Secondly, the significance of positive returns is much reduced, with returns ranging from 20% to 60% contributing only 38.66% to the BP. The pricing kernel slope exhibits similarity in both the unconditional and high volatility regimes. There is a slight increment in the pricing kernel slope in the region of positive returns. The LV cluster, characterized by low volatility, exhibits a steeper increase in the region of positive returns. We identify a novel pattern of returns ranging from 20% to 60% that exhibits a significant 62.17% positive contribution to the BP. The negative returns from -60% to -20% only contribute 19.87% to the BP. The PK in LV regime, as well as in the unconditional and HV regime, consistently exhibits a U-shaped pattern. Across all three cases, the portion of PK being above 1 for returns above 0.6 corresponds to a slightly declining BP(x). Figure B2 offers an intuitive comparison of the PKs. Notbaly, the PK’s slope for negative returns is steeper in the LV cluster, suggesting a higher level of risk averson.

To better understand the relationship between BP and PK, we calculate the price of risk as the ratio of the average density to the density, . Table 5 presents the BP contribution, physical probability, and price of risk for the intervals [-0.6, -0.2] and [0.2, 0.6], similar to Table 1 in [12]. For negative states, the price of risk for BTC is approximately 1.48, which is lower than the 2.63 for the S&P 500 as reported by [12], but comparable to levels found in [19], [10], [11], and [71].

Characteristics of BP, and in influential states Negative states Positive states BP(-0.2)-BP(-0.6) BP(0.2)-BP(0.6) Overall 0.34 0.09 1.48 0.48 0.18 0.62 HV 0.42 0.11 1.53 0.39 0.19 0.69 LV 0.24 0.07 1.44 0.62 0.16 0.54 BP(-0.2)-BP(-0.6) and BP(0.2)-BP(0.6) are BP contributions on the intervals. is the physical probability on such states and is the corresponding price of risk.

5.1 Discussion

The calibration of long-run risks and habit models to the S&P 500 index data in [12] suggests a symmetric contribution to the BP of positive and negative returns (each captures approximately 50% of the BP). However, the range of returns relevant for explaining the BP is confined to a tight interval of [-20%, 20%] monthly returns. These patterns suggest that the mean slope of the BP in both regions is approximately the same. In the case of BTC, this work shows that the positive returns contributing to the BP encompass a narrower range, in contrast to the negative returns that are more widely distributed. Simply put, the over the positive returns exhibit a higher slope, whereas it has a lower slope over the negative returns. This disparity implies that the long-term risks and habit models tend to overlook a crucial aspect of the crash. [71] combines the long-run risks and disaster mechanisms, but her model yields a too large contribution of the extreme events to the BP. This suggests that a different mechanism may be required to link the two models to explain the BTC market if one wants to build on long-run risk and habit models.

Relying on fully nonparametric estimates, we document an increase in risk aversion in the Bitcoin market in less volatile markets, as evidenced by a steeper slope of the pricing kernel over negative returns. This finding is consistent with [63] that negative returns are substantially more painful to investors in periods of low volatility. It is important to note, however, that while [63] employ a parametric specification of the pricing kernel, we use a fully nonparametric approach and still obtain the same results. Additionally, their study focuses on the negative returns side, whereas we examine the pricing kernel across the entire range of returns.181818In the appendix, the authors display the parametric estimates of the PK for the entire range of returns, yet they do not delve into an extensive explanation of the pricing kernel variation for the positive range of returns. Our non-parametric estimates are consistent with their parametric estimates for this region.

Our results align with those of [63] in terms of the direction of change of the PK slope as a function of volatility. However, our methodological approach is fundamentally different. Their approach involves selecting an exogenous variable to proxy for index volatility.191919Two proxies are being used in their study: conditional stock market volatility forecasts using a HAR model and realized variance based on intraday prices, as well as the VIX index. They plot their parametric estimates for the 10th and 90th percentile of volatility and observe a U-shaped pricing kernel with a pronounced convexity for low volatility, which is consistent with our findings. They then perform a maximum likelihood estimation of a parametrically specified pricing kernel, which depends on the ex-ante chosen volatile. In contrast, our approach is fully nonparametric and does not involve the pre-selection of a conditioning variable. We interpret the clusters by investigating their drivers and find volatility to be instrumental. However, we acknowledge that the explanatory power of volatility in this regard is limited, as there may be other market forces at play.202020For instance, we uncover that VRP tends to be higher when volatility is low, suggesting a disconnect between variance and uncertainty, as proxied by VRP. This relation might be obfuscated in other empirical frameworks. Therefore, our approach is more general. It is reassuring that two disparate methodological frameworks using different datasets lead to the same stylized facts. Our research corroborates the relationship between PK slopes (concavity) and volatility in both the S&P 500 index and the Bitcoin market.

6 Conclusion

This work uses marginal projections of the Pricing Kernel on the space of Bitcoin index returns to study Bitcoin risk premium properties. The Bitcoin index first moment premium and volatility risk premium are estimated from joint options and returns data over the most extensive period available. A Bitcoin Premium decomposition is applied as a function of returns. We also propose a new functional clustering method applied to a sequence of time-series of Bitcoin risk-neutral measures that allows us to obtain conditional measures for Bitcoin first moment and variance risk premia. Overall we find that, Bitcoin first moment, Variance risk Premia and premium for positive returns are all much larger than the corresponding measures for traditional assets like S&P500. Our findings for the Bitcoin BP decomposition can not be reconciled with any traditional macro-finance model, including habits ([19]), long-run risks model ([10]), rare disaster ([11]), and disappointment aversion ([62]).

Acknowledgements

The authors thank Wolfgang Härdle and Gustavo Freire for their helpful feedback and support.

References

- [1] Yacine Aït-Sahalia and Andrew W Lo “Nonparametric risk management and implied risk aversion” In Journal of Econometrics 94.1, 2000, pp. 9–51

- [2] Carol Alexander, Ding Chen and Arben Imeraj “Crypto quanto and inverse options” In Mathematical Finance 33.4 Wiley, 2023, pp. 1005–1043

- [3] Carol Alexander and Arben Imeraj “The Bitcoin VIX and Its Variance Risk Premium” In The Journal of Alternative Investments PAGEANT MEDIA LTD, 2021

- [4] Carol Alexander and Arben Imeraj “Delta hedging bitcoin options with a smile” In Quantitative Finance Informa UK Limited, 2023, pp. 1–19

- [5] Caio Almeida, Jianqing Fan, Gustavo Freire and Francesca Tang “Can a Machine Correct Option Pricing Models?” In Journal of Business & Economic Statistics Taylor & Francis, 2022, pp. 1–14

- [6] Caio Almeida, Gustavo Freire and Rodrigo Hizmeri “0DTE Asset Pricing” In Available at SSRN, 2024

- [7] Susan Athey, Ivo Parashkevov, Vishnu Sarukkai and Jing Xia “Bitcoin Pricing, Adoption, and Usage: Theory and Evidence” In Social Science Research Network, 2016

- [8] Gurdip Bakshi and Nikunj Kapadia “Delta-Hedged Gains and the Negative Market Volatility Risk Premium” In The Review of Financial Studies 16.2 Narnia, 2003, pp. 527–566

- [9] Gurdip Bakshi, Dilip Madan and George Panayotov “Returns of claims on the upside and the viability of U-shaped pricing kernels” In Journal of Financial Economics 97.1, 2010, pp. 130–154

- [10] Ravi Bansal and Amir Yaron “Risks for the Long Run: A Potential Resolution of Asset Pricing Puzzles” In The Journal of Finance 59.4 John Wiley & Sons, Ltd, 2004, pp. 1481–1509

- [11] Robert J Barro “Rare Disasters, Asset Prices, and Welfare Costs” In The American Economic Review 99.1, 2009, pp. 243–264

- [12] Tyler Beason and David Schreindorfer “Dissecting the Equity Premium” In The Journal of Political Economy 130.8 The University of Chicago Press, 2022, pp. 2203–2222

- [13] Geert Bekaert and Marie Hoerova “The VIX, the variance premium and stock market volatility” In Journal of Econometrics 183.2, 2014, pp. 181–192

- [14] Bruno Biais, Christophe Bisière, Matthieu Bouvard, Catherine Casamatta and Albert J Menkveld “Equilibrium bitcoin pricing” In The Journal of Finance 78.2 Wiley, 2023, pp. 967–1014

- [15] Daniele Bianchi “Cryptocurrencies As an Asset Class? An Empirical Assessment” In The Journal of Alternative Investments 23.2, 2020, pp. 162–179

- [16] Tim Bollerslev, George Tauchen and Hao Zhou “Expected Stock Returns and Variance Risk Premia” In The Review of Financial Studies 22.11 Narnia, 2009, pp. 4463–4492

- [17] Nicole Branger, Christian Schlag and Sonia Zaharia “An equilibrium foundation for the Heston stochastic volatility model and U-shaped pricing kernels”, 2011

- [18] Matthias Büchner and Bryan Kelly “A factor model for option returns” In Journal of Financial Economics 143.3, 2022, pp. 1140–1161

- [19] John Y Campbell and John H Cochrane “By Force of Habit: A Consumption-Based Explanation of Aggregate Stock Market Behavior” In The Journal of Political Economy 107.2 The University of Chicago Press, 1999, pp. 205–251

- [20] Melanie Cao and Batur Celik “Valuation of bitcoin options” In Journal of Futures Markets 41.7 Wiley, 2021, pp. 1007–1026

- [21] Peter Carr and Liuren Wu “Variance Risk Premiums” In The Review of Financial Studies 22.3 Oxford Academic, 2009, pp. 1311–1341

- [22] Fousseni Chabi-Yo “Pricing Kernels with Stochastic Skewness and Volatility Risk” In Management Science 58.3 INFORMS, 2012, pp. 624–640

- [23] Fousseni Chabi-Yo and Johnathan Loudis “The conditional expected market return” In Journal of Financial Economics 137.3 Elsevier BV, 2020, pp. 752–786

- [24] Fousseni Chabi-Yo and Johnathan A Loudis “A decomposition of conditional risk premia and implications for representative agent models” In Management Science INFORMS, 2023

- [25] Cathy Yi-hsuan Chen and Dmitri Vinogradov “Coins With Benefits: On Existence, Pricing Kernel and Risk Premium of Cryptocurrencies”, 2021

- [26] Wei Chen, Huilin Xu, Lifen Jia and Ying Gao “Machine learning model for Bitcoin exchange rate prediction using economic and technology determinants” In International Journal of Forecasting 37.1 Elsevier BV, 2021, pp. 28–43

- [27] Ing-Haw Cheng “The VIX Premium” In The Review of Financial Studies 32.1 [Oxford University Press, The Society for Financial Studies], 2019, pp. 180–227

- [28] Peter Christoffersen, Steven Heston and Kris Jacobs “Capturing option anomalies with a variance-dependent pricing kernel” In The Review of Financial Studies 26.8 Oxford University Press, 2013, pp. 1963–2006

- [29] Lin William Cong, Ye Li and Neng Wang “Tokenomics: Dynamic adoption and valuation” In The Review of Financial Studies 34.3 Oxford University Press (OUP), 2021, pp. 1105–1155

- [30] Ian Dew-Becker, Stefano Giglio and Bryan Kelly “Hedging macroeconomic and financial uncertainty and volatility” In Journal of Financial Economics 142.1, 2021, pp. 23–45

- [31] Itamar Drechsler “Uncertainty, time-varying fear, and asset prices” In The Journal of Finance 68.5 Wiley, 2013, pp. 1843–1889

- [32] Matthias Eckardt, Jorge Mateu and Sonja Greven “Generalised functional additive mixed models with compositional covariates for areal Covid-19 incidence curves” In arXiv preprint arXiv:2201.08362, 2022

- [33] Guanhao Feng and Jingyu He “Factor investing: A Bayesian hierarchical approach” In Journal of Econometrics 230.1, 2022, pp. 183–200

- [34] Stephen Figlewski “Estimating the implied risk neutral density” VolatilityTime Series Econometrics: Essay in Honor of Robert F. Engle …, 2008

- [35] Sean Foley, Simeng Li, Hamish Malloch and Jiri Svec “What is the expected return on Bitcoin? Extracting the term structure of returns from options prices” In Economics letters 210, 2022, pp. 110196

- [36] Jim Gatheral “A parsimonious arbitrage-free implied volatility parameterization with application to the valuation of volatility derivatives” In Presentation at Global Derivatives, 2004

- [37] Maria Grith, Wolfgang Härdle and Juhyun Park “Shape Invariant Modeling of Pricing Kernels and Risk Aversion” In Journal of Financial Econometrics 11.2 Oxford Academic, 2013, pp. 370–399

- [38] Maria Grith, Wolfgang K Härdle and Volker Krätschmer “Reference-Dependent Preferences and the Empirical Pricing Kernel Puzzle” In Review of Finance 21.1 Oxford Academic, 2017, pp. 269–298

- [39] Wolfgang Karl Härdle, Yarema Okhrin and Weining Wang “Uniform Confidence Bands for Pricing Kernels” In Journal of Financial Econometrics 13.2, 2015, pp. 376–413

- [40] Trevor Hastie, Robert Tibshirani, Jerome H Friedman and Jerome H Friedman “The elements of statistical learning: data mining, inference, and prediction” Springer, 2009

- [41] Nikolaus Hautsch, Christoph Scheuch and Stefan Voigt “Building trust takes time: limits to arbitrage for blockchain-based assets” In Review of Finance, 2015

- [42] Steven L Heston, Kris Jacobs and Hyung Joo Kim “The pricing kernel in options” Divisions of Research & StatisticsMonetary Affairs, Federal Reserve Board, 2023

- [43] Steven L Heston and Saikat Nandi “A Closed-Form GARCH Option Valuation Model” In The Review of Financial Studies 13.3 Oxford Academic, 2000, pp. 585–625

- [44] Franz J Hinzen, Kose John and Fahad Saleh “Bitcoin’s limited adoption problem” In Journal of Financial Economics 144.2 Elsevier BV, 2022, pp. 347–369

- [45] Ai Jun Hou, Weining Wang, Cathy YH Chen and Wolfgang Karl Härdle “Pricing cryptocurrency options” In Journal of Financial Econometrics 18.2 Oxford University Press, 2020, pp. 250–279

- [46] Roni Israelov and Bryan T Kelly “Forecasting the distribution of option returns” In Available at SSRN 3033242, 2017

- [47] Jens Carsten Jackwerth “Recovering Risk Aversion from Option Prices and Realized Returns” In The Review of Financial Studies 13.2 Oxford Academic, 2000, pp. 433–451

- [48] Matthew Linn, Sophie Shive and Tyler Shumway “Pricing Kernel Monotonicity and Conditional Information” In The Review of Financial Studies 31.2, 2018, pp. 493–531

- [49] Francis Liu, Artur Sepp and Natalie Packham “On Crypto Traders’ Preferences towards Jumps”, 2023

- [50] Yukun Liu and Aleh Tsyvinski “Risks and Returns of Cryptocurrency” In The Review of Financial Studies 34.6 Oxford Academic, 2021, pp. 2689–2727

- [51] Andrew W. Lo “The Statistics of Sharpe Ratios” In Financial Analysts Journal 58.4, 2002, pp. 36–52

- [52] Jitka Machalova, Karel Hron and Gianna Serafina Monti “Preprocessing of centred logratio transformed density functions using smoothing splines” In Journal of Applied Statistics 43.8 Taylor & Francis, 2016, pp. 1419–1435

- [53] Ian Martin “What is the Expected Return on the Market?” In The Quarterly Journal of Economics 132.1 Oxford Academic, 2017, pp. 367–433

- [54] Leland McInnes, John Healy, Nathaniel Saul and Lukas Großberger “UMAP: Uniform Manifold Approximation and Projection” In Journal of Open Source Software 3.29, 2018, pp. 861

- [55] Jie Peng and Hans-Georg Müller “Distance-based clustering of sparsely observed stochastic processes, with applications to online auctions” In The Annals of Applied Statistics 2.3, 2008, pp. 1056–1077

- [56] Alexander Petersen and Hans-Georg Müller “Functional data analysis for density functions by transformation to a Hilbert space” In Annals of Statistics, 2016

- [57] Jeroen VK Rombouts, Lars Stentoft and Francesco Violante “Dynamics of variance risk premia: A new model for disentangling the price of risk” In Journal of Econometrics 217.2 Elsevier, 2020, pp. 312–334

- [58] Cameron Rookley “Fully Exploiting the Information Content of Intra Day Option Quotes: Applications in Option Pricing and Risk Management”, 1997

- [59] Joshua V Rosenberg and Robert F Engle “Empirical pricing kernels” In Journal of Financial Economics 64.3, 2002, pp. 341–372

- [60] Olivier Scaillet, Adrien Treccani and Christopher Trevisan “High-frequency jump analysis of the bitcoin market” In Journal of Financial Econometrics 18.2 Oxford University Press, 2020, pp. 209–232

- [61] Linda Schilling and Harald Uhlig “Some simple bitcoin economics” In Journal of Monetary Economics 106 Elsevier BV, 2019, pp. 16–26

- [62] David Schreindorfer “Macroeconomic Tail Risks and Asset Prices” In The Review of Financial Studies 33.8 Oxford Academic, 2020, pp. 3541–3582

- [63] David Schreindorfer and Tobias Sichert “Volatility and the pricing kernel” In Swedish House of Finance Research Paper, 2023

- [64] Michael Sockin and Wei Xiong “A model of cryptocurrencies” In Management Science 69.11 Institute for Operations Researchthe Management Sciences (INFORMS), 2023, pp. 6684–6707

- [65] Michael Sockin and Wei Xiong “Decentralization through tokenization” In The Journal of Finance 78.1 Wiley, 2023, pp. 247–299

- [66] Zhaogang Song and Dacheng Xiu “A tale of two option markets: Pricing kernels and volatility risk” In Journal of Econometrics 190.1, 2016, pp. 176–196

- [67] Huei-Wen Teng and Wolfgang K Härdle “Financial analytics of inverse BTC options in a stochastic volatility world” In Available at SSRN 4238213, 2022

- [68] Paul C Tetlock “The Implied Equity Premium”, 2023

- [69] Viktor Todorov “Variance Risk-Premium Dynamics: The Role of Jumps” In The Review of Financial Studies 23.1 Society for Financial Studies, 2010, pp. 345–383

- [70] Harald Uhlig “On Digital Currencies”, 2024

- [71] Jessica A Wachter “Can time-varying risk of rare disasters explain aggregate stock market volatility?” In The Journal of Finance 68.3 Wiley, 2013, pp. 987–1035

- [72] Joe H Ward Jr “Hierarchical grouping to optimize an objective function” In Journal of the American Statistical Association 58.301 Taylor & Francis, 1963, pp. 236–244

- [73] Matthew S Wilson “The Bitcoin premium: A persistent puzzle” In The B E Journal of Macroeconomics 24.1 Walter de Gruyter GmbH, 2024, pp. 135–148

- [74] Julian Winkel and Wolfgang Karl Härdle “Pricing Kernels and Risk Premia implied in Bitcoin Options” In Risks 11.5 Multidisciplinary Digital Publishing Institute, 2023, pp. 85

- [75] Julian Winkel and Wolfgang Karl Härdle “Volatility Premia of Digital Assets”, 2023

- [76] Julian Winkel and Wolfgang Karl Härdle “Empirical Option Returns and the Risk-Free Rate in Crypto Asset Markets”, 2024

- [77] Hao Zhou “Variance risk premia, asset predictability puzzles, and macroeconomic uncertainty” In Annual Review of Financial Economics 10.1 Annual Reviews, 2018, pp. 481–497

[appendices] \printcontents[appendices]l1

Appendices

Appendix A Main Appendix

A.1 Further Data Analysis

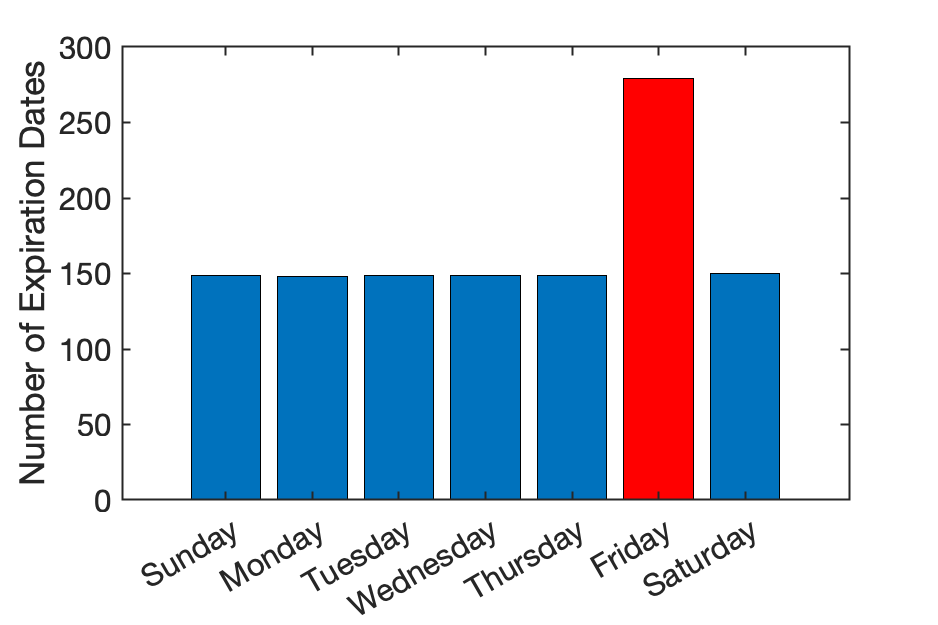

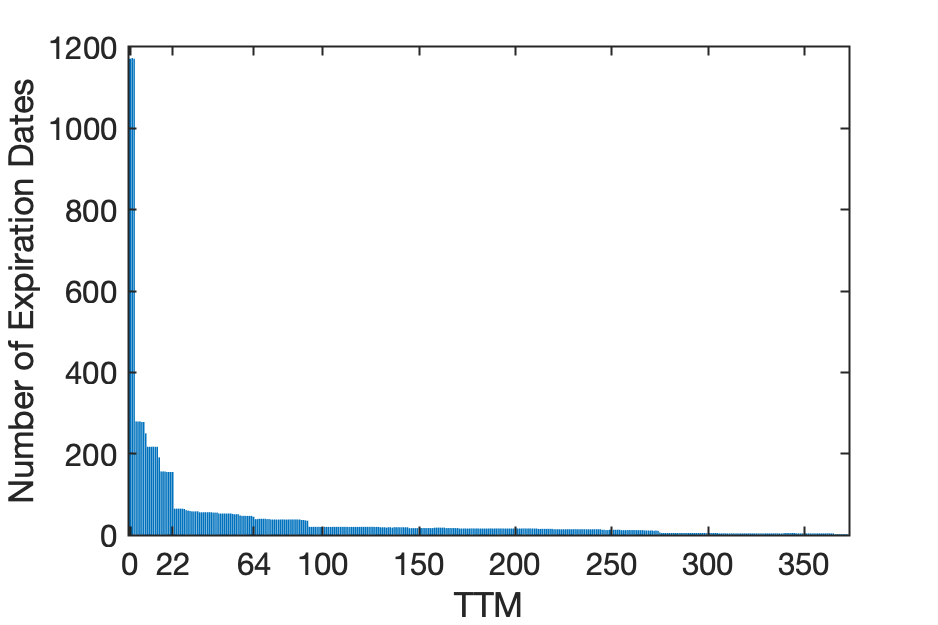

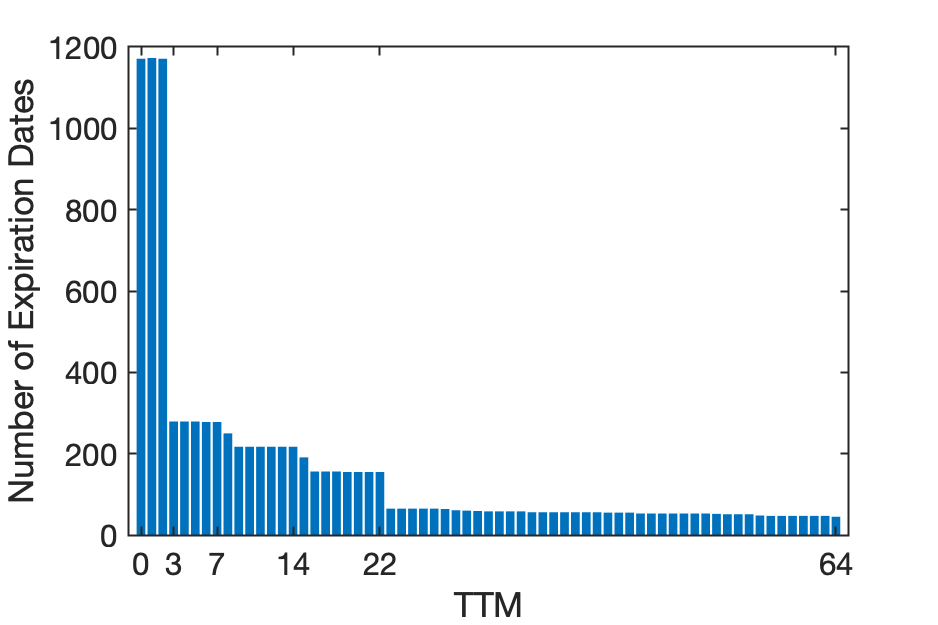

Two types of BTC options are traded on Deribit: those with shorter tenors that expire daily at 08:00 UTC and those with longer tenors that expire on Fridays at 08:00 UTC. Figure A1 presents the weekly distribution of expiration dates in our dataset for both types of options. Specifically, options with a TTM of two days or less expire on every day of the week, including Friday, while options with a TTM exceeding two days only expire on Fridays.

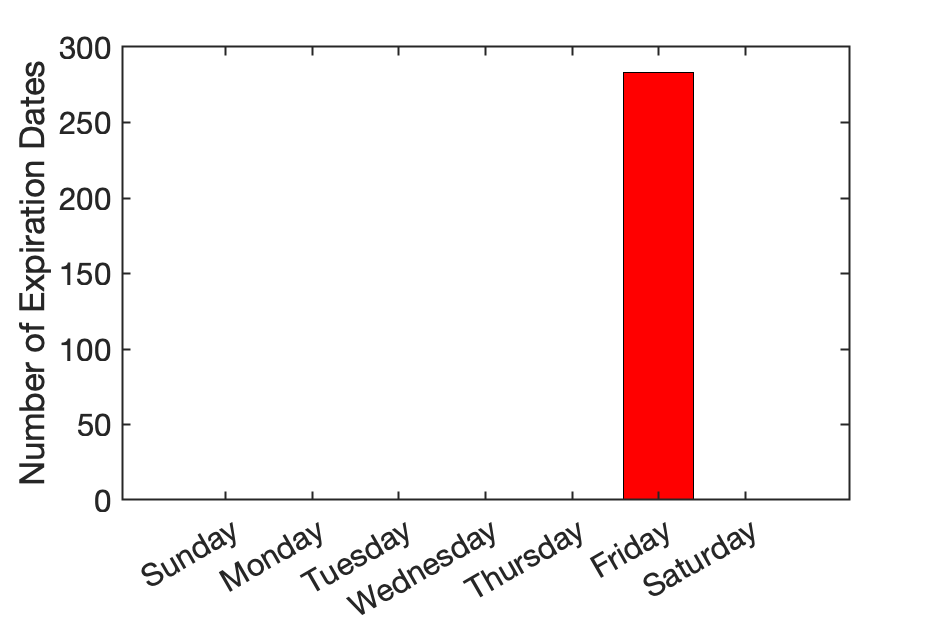

Additionally, it is important to note that options with varying TTMs might have distinct expiration dates. As the TTM diminishes to 0 for a given option, its expiration date remains constant. Figure A2 illustrates our dataset’s observed expiration dates for different TTMs. Options with TTMs shorter than three days exhibit a significantly higher number of expiration dates, corroborating that these options expire daily in contrast to others expire only on Fridays. Consequently, the variety of expiration dates tends to decrease as the TTM lengthens. For options with longer maturity, there is a noticeable scarcity in the number of expiration dates, indicating a lower trading volume. Figure A3 illustrates the average daily BTC option transactions per month.

|

Table A.1 gives an overview of the average implied volatility on different batches. We notice for both call and put options, IV initially decreases as moneyness increases and then rises past ATM, representing a "volatility smile" commonly seen in the traditional security markets. Furthermore, options with shorter maturity, particularly those deep OTM and deep ITM, tend to exhibit higher levels of IV. Notably, put options generally display higher IV compared to call options.

Implied volatility of BTC options [in level] Call options Moneyness (0, 9] [10, 26] [27, 33] >33 Average 1.31 1.05 0.92 0.92 1.07 0.88 0.79 0.77 0.80 0.82 0.70 0.73 0.73 0.78 0.81 0.79 0.73 0.73 0.76 0.86 1.04 0.90 0.87 0.88 0.92 Average 0.81 0.82 0.83 0.86 0.82 Put options Moneyness (0, 9] [10, 26] [27, 33] >33 Average 1.25 1.03 0.97 0.94 1.05 0.87 0.77 0.75 0.80 0.80 0.70 0.74 0.74 0.80 0.78 0.88 0.79 0.76 0.80 1.00 1.69 1.17 0.89 0.93 1.19 Average 0.89 0.90 0.88 0.90 0.89 This table presents the average implied volatility for the BTC option over moneyness and maturity. The columns are categorized based on the time to maturity in days. The IVs are calculated and listed by Deribit.

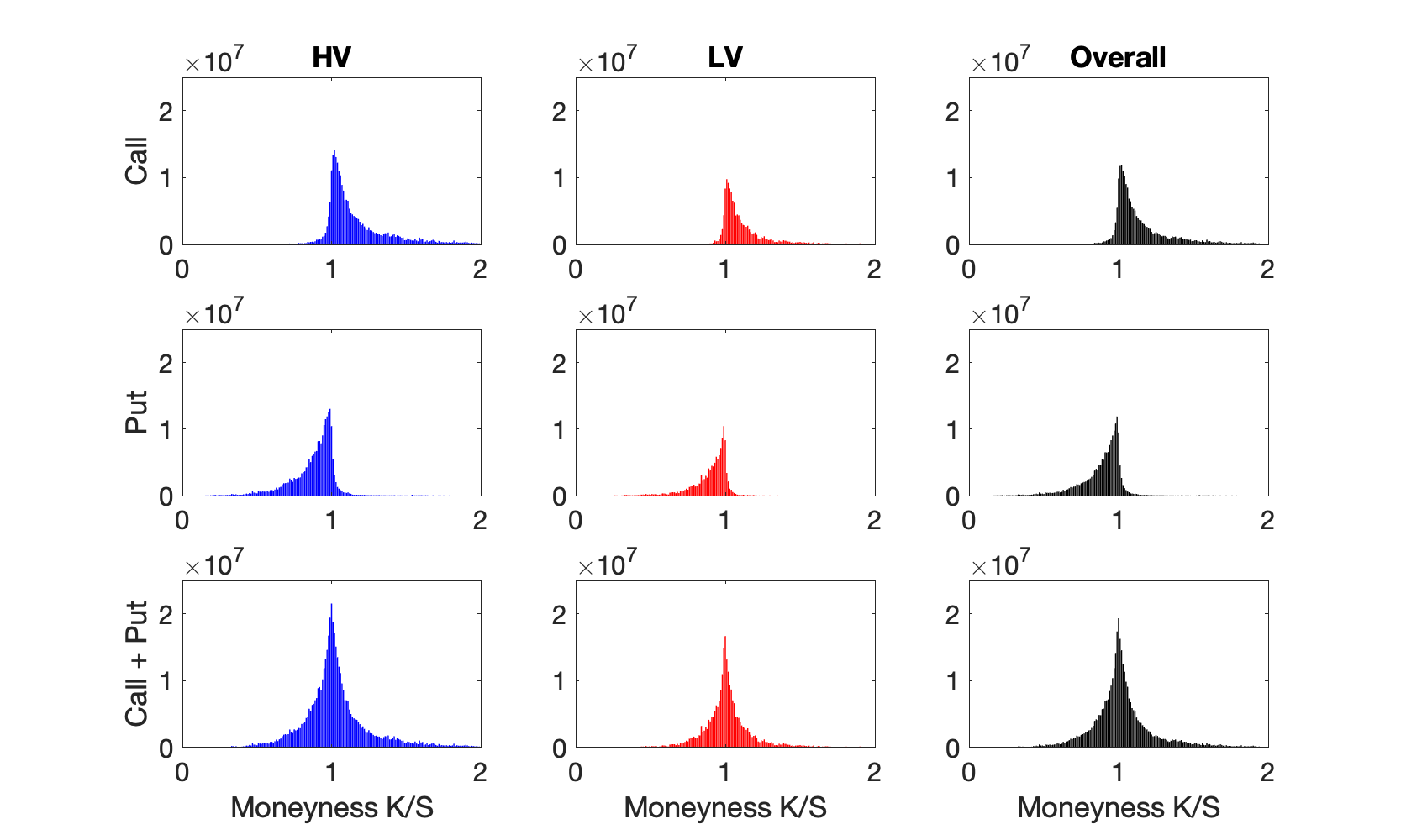

Table A.1 presents the transaction patterns of call and put options, classified into different moneyness and maturity groups. The results reveal that OTM options are predominant for both call and put options, accounting for more than 60% of the total, with deep OTM options making up more than 35%. In contrast, in-the-money (ITM) options constitute less than 10%, with deep ITM options accounting for less than 4%. Regarding the term structure, more than half of the options have maturities of less than 10 days, with a slightly higher proportion of put options (54.43%) compared to call options (51.12%). Moreover, call options with maturities of more than 33 days constitute 24.05%, whereas put options with maturities of more than 33 days account for 20.10%.

Summary statistics on transaction contracts of BTC options [in %] Call options Moneyness (0, 9] [10, 26] [27, 33] >33 Subtotal 0.99 0.55 0.19 1.42 3.15 2.99 0.85 0.19 0.86 4.89 22.50 3.93 0.53 1.77 28.74 16.67 5.00 0.70 2.29 24.65 7.97 10.48 2.41 17.71 38.57 Total 51.12 20.81 4.02 24.05 100.00 Put options 10.38 10.53 2.11 12.83 35.84 18.44 5.41 0.72 2.64 27.22 22.54 4.16 0.49 1.97 29.16 2.10 0.90 0.17 1.07 4.25 0.97 0.80 0.17 1.59 3.53 Total 54.43 21.80 3.66 20.10 100.00 This table presents the proportion of traded BTC option contracts over moneyness and maturity. The sample covers transactions between July 1, 2017 and December 17, 2022. The columns are categorized based on the time to maturity in days. The transactions are measured as the number of traded contracts.

Table A.1 provides summary statistics on option transaction quantity in BTC units, given that each option is denominated in BTC. The distribution of transaction quantity closely mirrors that of transaction contracts, with an even greater proportion of out-of-the-money options. Table A.1 presents the summary statistics on option transaction volume in USD, calculated as the traded quantity multiplied by the BTC price in USD. Options with longer maturities and in-the-money options typically possess higher values, resulting in over half of the total value being attributed to long-maturity options. Additionally, the OTM value portion is lower than transaction and volume due to their lower values.

Summary statistics on BTC option quantity [in %] Call options Moneyness (0, 9] [10, 26] [27, 33] >33 Subtotal 0.46 0.37 0.11 0.90 1.85 1.55 0.63 0.18 0.66 3.03 17.21 3.71 0.51 1.53 22.94 16.14 6.17 0.82 2.30 25.43 8.84 13.10 3.45 21.37 46.75 Total 44.19 23.98 5.07 26.75 100.00 Put options 13.21 13.35 2.83 13.87 43.26 17.83 6.73 0.85 2.48 27.89 18.12 4.14 0.53 1.52 24.31 1.11 0.57 0.11 0.70 2.49 0.47 0.56 0.08 0.94 2.05 Total 50.74 25.35 4.40 19.51 100.00 This table presents the proportion of quantity [in %] of the BTC option data over moneyness and maturity. The data spans from July 1, 2017, to December 17, 2022. The columns are categorized based on the time to maturity in days. The quantity is measured in terms of the number of BTC units.

Summary statistics on BTC option transaction volume valued in USD [in %] Call options Moneyness (0, 9] [10, 26] [27, 33] >33 Subtotal 2.01 2.72 0.56 9.15 14.45 2.38 1.74 0.58 3.09 7.79 8.53 6.11 1.07 5.04 20.74 4.52 6.02 1.21 6.17 17.92 1.30 6.21 2.20 29.39 39.10 Total 44.19 22.81 5.61 52.84 100.00 Put options Moneyness (0, 9] [10, 26] [27, 33] >33 Subtotal 5.37 5.37 1.50 16.69 25.40 6.30 6.30 1.14 6.98 19.79 9.85 6.32 1.00 5.59 22.76 2.08 1.52 0.33 3.59 7.53 2.88 3.46 0.69 17.48 24.51 Total 22.01 22.98 4.67 50.34 100.00 This table presents summary statistics for the volume of BTC options. The volume is measured in USD, i.e., volume = quantity BTC price (USD) summed in each category. The data spans from July 1, 2017, to December 17, 2022. The columns are categorized based on the time to maturity in days. Within each moneyness and maturity category, the entries provide the volume proportions in percentage.

A.2 Estimation of the BVIX

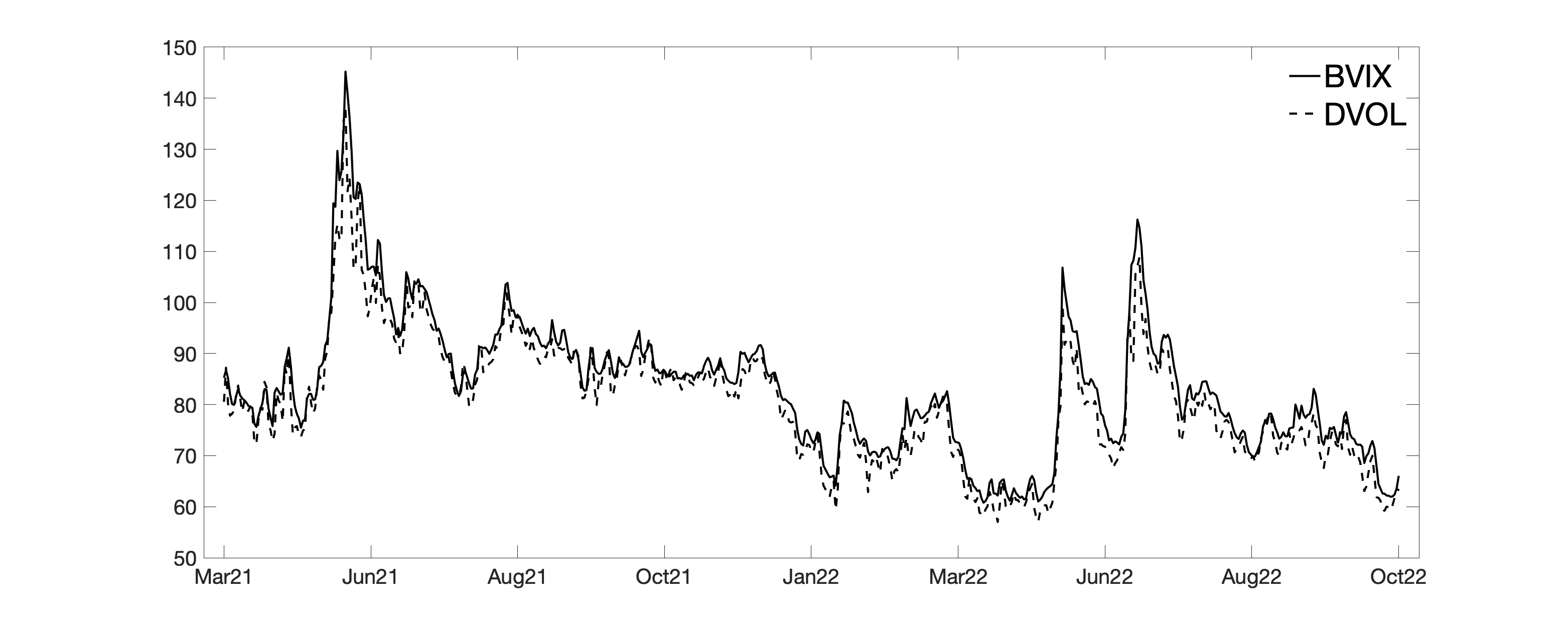

The BVIX is calculated using the BTC transaction data as described in Section 2. We calculate the variances and by closely following the original VIX methodology of CBOE and interpolate the time-weighted average as

| (27) |

where and is the time to settlement (in years) of the near and next-term options, respectively. A comparison of the BVIX to the Dvol index by Deribit is conducted in Figure A4. As we see, both indices are closely related.

A.3 Interpolation of the IV Surface

The SVI model is widely popularized due to its parametric specification as well as good performance in the interpolation of IVs. Additionally assuming linearity in allows a more flexible representation of the implied volatility surface, providing a better fit to data by allowing each parameter to exhibit its term structure.

We are using the IV of each transaction given by the Deribit exchange, as described in Section 2. After applying local polynomial estimation, we obtain a smooth curve of IV for a given day as a function of moneyness. The parameters are linear functions of and capture various characteristics of the volatility smile such as its level, slope, and curvature. More specifically, the parameters are denoted as and . The parameter vector is estimated by minimizing the root mean squared error (RMSE)

where is the (squared) observed IV and is the implied variance as defined in Equation 8 for day and corresponding transaction .

|

|

|

|

A.4 Estimation of Parametric Tails

Inspired by [34], we use the Generalized Extrem Value (GEV) distribution to fit the tails of the risk-neutral density. Acknowledging the fact that transaction limits truncate the density at both lower and upper extremes, we address the concern that this truncation neglects trading at deeply in-the-money and deeply out-of-the-money options. To rectify this, our objective is to construct a density with extended tails that captures these extreme areas. It covers the full return support and satisfies essential moment conditions. For example, the integration of the density has to equal to one and the first moment of the density has to align with the assumed risk-free rate.

We use the GEV distribution to fit both, the left and the right tail. However, we deviate from [34] in two aspects due to the special nature of the BTC data, the target points selection and the moment conditions.