Short Paper: Atomic Execution is Not Enough for Arbitrage Profit Extraction in Shared Sequencers

Abstract

There has been a growing interest in shared sequencing solutions, in which transactions for multiple rollups are processed together. Their proponents argue that these solutions allow for better composability and can potentially increase sequencer revenue by enhancing MEV extraction. However, little research has been done on these claims, raising the question of understanding the actual impact of shared sequencing on arbitrage profits, the most common MEV strategy in rollups. To address this, we develop a model to assess arbitrage profits under atomic execution across two Constant Product Market Marker liquidity pools and demonstrate that switching to atomic execution does not always improve profits. We also discuss some scenarios where atomicity may lead to losses, offering insights into why atomic execution may not be enough to convince arbitrageurs and rollups to adopt shared sequencing.

Keywords:

Sequencers Atomic Execution Arbitrage MEV Rollups1 Introduction

Decentralized Finance (DeFi)has been essential to the growth of the Ethereum ecosystem, attracting many users and successful applications. Recently, it has expanded to Layer-2 (L2)scaling solutions like rollups, where trading volumes are rising, with some rollups now experiencing more daily activity than Ethereum itself [4]. With this growth in adoption comes more opportunities for Maximal-Extractable Value (MEV) — a collection of techniques for extracting value from transaction inclusion and reordering [3]. The most prevalent form of MEVon rollups is arbitrage, in which arbitrageurs exploit price differences between centralized exchanges and/or Decentralized Exchanges (DEXs) [10].

A relevant consideration for MEVin rollups is sequencer design. The sequencer is the operator responsible for receiving and scheduling user transactions for processing, and most rollups currently use an independent centralized sequencer [6]. Recent proposals have introduced an alternative — shared sequencers. Shared sequencing schemes propose to process transactions for multiple rollups together, allowing for better composability between rollups. Despite being a recent topic, Astria [1] already has a solution in production, while Radius [8], NodeKit [7], and Expresso Systems [9, 2] are in the test phase. However, we have not yet seen significant adoption from rollups.

Proponents of shared sequencing argue that it can enhance MEVextraction in cross-rollup arbitrage, thus adding a potential for increased revenue for rollups. Arbitrageurs can already execute cross-rollup arbitrage by submitting independent transactions to each rollup. However, this strategy involves additional liquidity and currency risk costs.

In this context, shared sequencing offers two relevant properties for arbitrageurs: atomic execution and atomic bridging. Atomic execution allows an arbitrageur to bundle two swaps (one for each rollup) and have the guarantee that if one of the swaps reverts, the other will also revert. This property requires control over block-building on the rollups running full nodes of the rollups to guarantee execution validity. Atomic bridging goes further by allowing for bridge operations between rollups, eliminating the need for liquidity across different chains. An arbitrageur can take a flash loan on one rollup, swap tokens, bridge them to another rollup for the second swap, and then bridge the tokens back to repay the loan. Yet, this property is significantly more challenging to achieve and requires additional trust assumptions on the shared sequencing infrastructure.

With the added complexities of implementing atomic bridging, in this work, we aim to understand how arbitrage profits can be impacted by a shared sequencing solution that only provides atomic execution. Even though this property seems intuitively beneficial for arbitrageurs, we argue this is not always true. In fact, atomic execution is insufficient to consistently improve MEVextraction for arbitrageurs and therefore to increase revenue for sequencers.

Concretely, we build a model to assess the difference in terms of the expected arbitrage profit of switching to a shared sequencing regime with atomic execution. Here, we consider a cross-rollup arbitrage between two Constant Product Market Maker (CPMM)liquidity pools and compute the expected profit obtained by the arbitrageur given key parameters such as the prices in the pools and the probabilities of failure of the swaps. Then, we analyze how this difference in expected profit changes with these parameters and conclude that an arbitrageur does not always benefit from atomic execution. We also discuss and provide some intuition as to why atomic execution leads to losses in some particular cases.

These results are consistent with previous work from Mamageishvili and Schlegel [5], in which they consider how atomic execution impacts arbitrageurs’ latency competition and their incentives to invest in latency. Interestingly, they observe that in a regime where transaction order and inclusion is determined through bidding, the revenue of shared sequencing is not always higher than that of separate sequencing and depends on the transaction ordering rule applied and the arbitrage value potentially realized.

2 Modelling Arbitrage Extraction

Before describing the model to estimate the impact of atomic execution for cross-rollup arbitrage, we must define some concepts and variables.

2.1 Preliminaries

We begin by assuming that an arbitrageur identifies an opportunity to arbitrage the pools of the token pair in two different rollups, and . The arbitrage opportunity is identified at the end of the last sequenced block of each rollup. At this time, the pool in rollup has a price of and token reserves of , while the same pool in rollup has a price of and token reserves of . Note that we are considering prices denominated in token . In other words, and . Without loss of generality, let’s assume that .

We further assume that the arbitrageur maintains liquidity on both rollups, which is kept in the target tokens and . Concretely, the arbitrageur’s liquidity is (for token ) and (for token ). We can value the total liquidity of the arbitrageur in units of token using an external price , and thus, .

In practice, arbitrageurs do not maintain their liquidity in different tokens, preferring to hedge currency risk by only holding stable tokens such as USDC. In our case, this would mean maintaining liquidity in the stable token and converting back and forth between the target tokens ( and ) and the stable token. However, looking at the impact on liquidity for the target tokens allows for a simpler model while distilling the key aspects of how atomicity impacts arbitrage profit extraction across different scenarios.

In this setup, the arbitrageur will perform two swaps (one in each rollup) to extract this arbitrage opportunity:

-

•

Swap in rollup : Pay units of token and receive units of token in rollup .

-

•

Swap in rollup : Pay units of token and receive units of token .

We define and as the random variables representing whether the swaps and (respectively) fail. These variables take the value 1 if the swap fails and 0 if the swap is successful. Here, we assume that the failure probabilities for each rollup are independent.

It is important to note that we are ignoring transaction costs in our model. This assumption allows us to avoid converting these costs (usually denominated in ETH) to the target token , simplifying the analysis. On the other hand, given the current state of rollups, we expect transaction costs to be low enough not to change the conclusions substantially.

2.2 Profit Variables

Given the arbitrage opportunity defined above, the profit an arbitrageur will extract is simply the difference in liquidity resulting from the swaps and , which ultimately depends on the trade sizes (, , , and ) and the failure outcomes ( and ).

Under the non-atomic sequencing regime, one swap can fail while the other does not. Therefore, the difference in liquidity for each target token after the arbitrage is defined as:

| (1) |

and

| (2) |

On the other hand, under the atomic execution regime, if one of the swaps reverts, the other swap will also revert. Thus, under this regime:

| (3) |

and

| (4) |

Using the external price , we can define the overall profit under each sequencing regime as:

| (5) |

Now, we only need to derive the optimal trade sizes , , , and , which we do in the following subsection.

2.3 Trade Sizes

To derive the trade sizes of the two swaps, we assume that both pools are CPMMs, charge the same trading fee , and that the arbitrageur will execute the optimal trade (i.e., sizing their trade to extract the maximal value from the two target pools). We will further assume that, from the time the arbitrage opportunity is identified to the time the arbitrage trade is executed, no uninformed traders will submit further transactions that shift the prices in affected pools.

In the swap , the arbitrageur sends units of token to the pool and pays a fee of . Here, we consider that the DEXis processing fees outside of the pool reserves, which means that when a trader wishes to swap a given amount of tokens and pay , only part of this payment goes to the pool reserve. Concretely, is added to the poor reserves, while is paid to Liquidity Providers (LPs). This is the case of Uniswap V3 pools, for instance.

We can derive how many tokens the arbitrageur receives in a trade of by using the property of CPMMpools in which the product of the two token reserves must always be a constant:

| (6) |

If the arbitrageur executes this trade, the price after the trade will be:

| (7) |

Using similar logic for the swap , the arbitrageur pays units of token and receives the following units of token :

| (8) |

And, at the end of the trade, the price of the pool will be:

| (9) |

When the arbitrageur executes the optimal trade, they will pay in rollup the same units of tokens they received in rollup , which means that . With this equality and equations 6 and 8, we can describe the trade sizes , , and based on the optimal initial size .

As for , the optimal trade occurs when the prices in both pools at the end of the trade are equal, i.e., . We can use this to derive :

| (10) |

3 Atomicity Profit Conditions

Based on the model developed in Section 2, the impact on arbitrage profits of moving from a non-atomic regime to an atomic regime depends on the combined outcome of the random variables and , which represent whether each swap fails. Recall that they take the value 1 if the swap fails and 0 otherwise.

There are four possible combined outcomes for these two variables. For each, we can describe the difference in arbitrage profits between the atomic and non-atomic regimes (i.e., ):

-

•

. In this outcome, both swaps execute, and thus, the difference in arbitrage profits between the two regimes is zero.

-

•

. In this outcome, both swaps fail. Thus, the difference in arbitrage profits between the two regimes is again zero.

-

•

. In this outcome, swap fails, but swap executes. Here, there is a difference since, in the atomic regime, both swaps would be reverted. Therefore,

-

•

. In this outcome, swap executes, while swap fails. Again, there is a difference in this combined outcome since, in the atomic regime, both swaps would be reverted. Therefore,

Now, if we define and as the probability of swaps and failing, respectively, we can describe the expected value of the profit difference as follows:

| (11) |

Interestingly, we can rewrite equation 13 in terms of the price paid by the arbitrageur in each swap, namely, and . Note that here we are using again the fact that :

| (12) |

Equation 12 highlights that the expected gain that an arbitrageur will experience when switching from a non-atomic regime to an atomic regime ultimately depends on a few key parameters.

-

1.

We have the trade size . Recall from Section 2 that the trade size is determined by the state of the pools in each rollup, namely, the token reserves, the price difference, and the trading fee. In general, the larger the pools’ reserves and the price difference, the larger the optimal trade sizes. Since , the pools’ state does not control whether the difference is negative or positive on average. Instead, it has a multiplicative effect on the expected profit difference, controlling the size of this difference.

-

2.

We have the external price and its relative position to the prices experienced by the arbitrageur in their optimal trade, and . These prices are always between the initial price of the pool before the arbitrage and the end price after the arbitrage is executed (i.e., and ).

-

3.

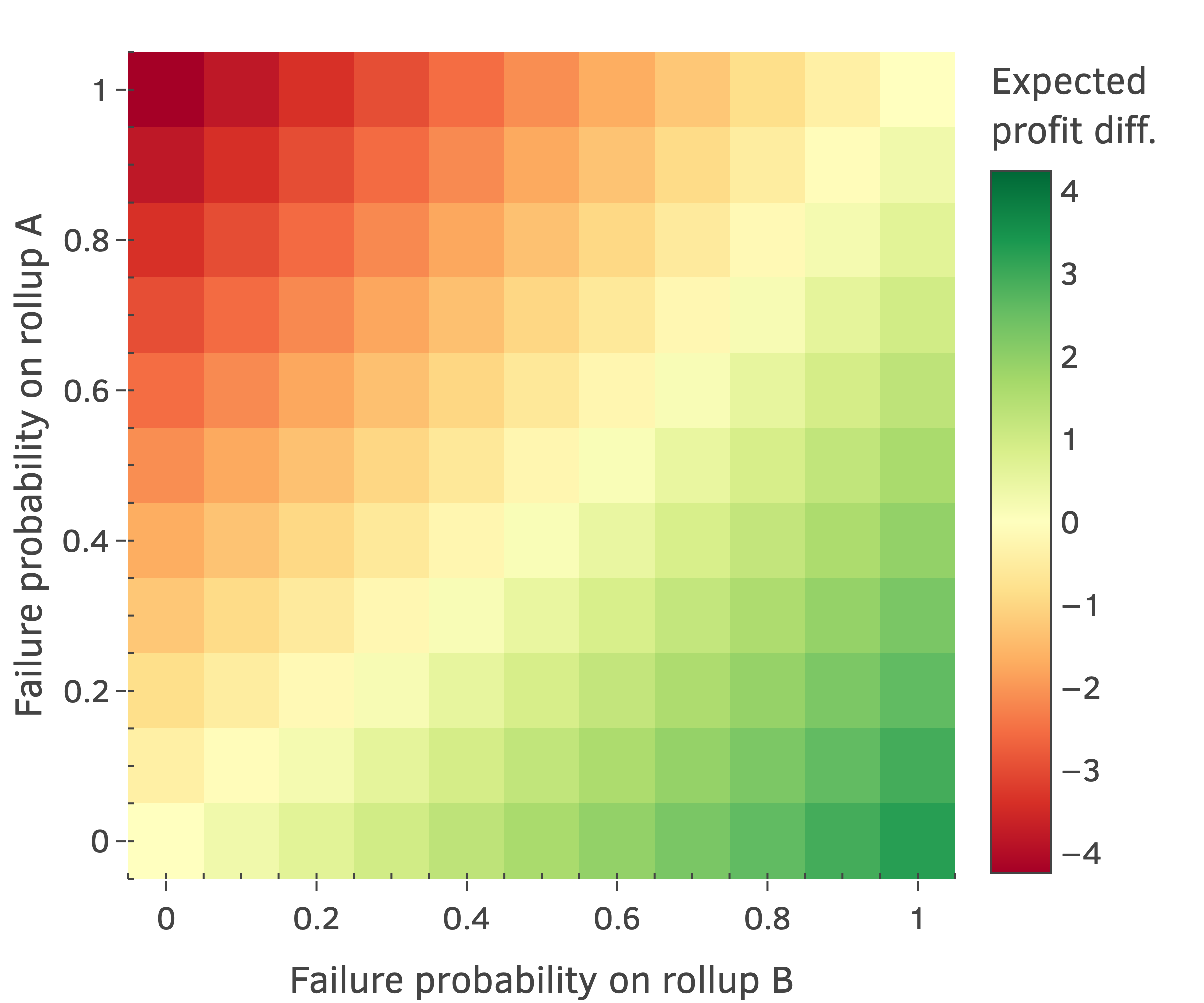

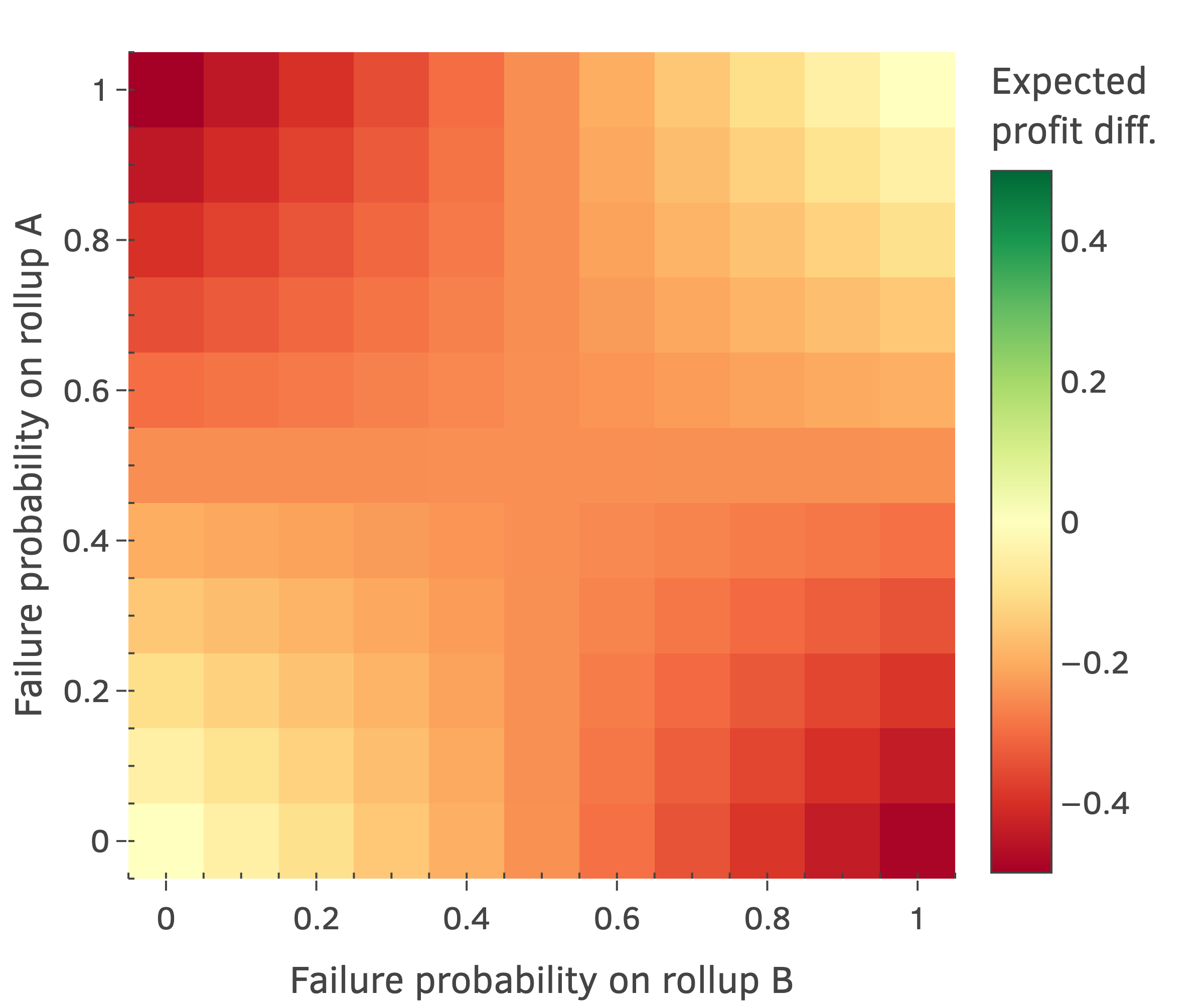

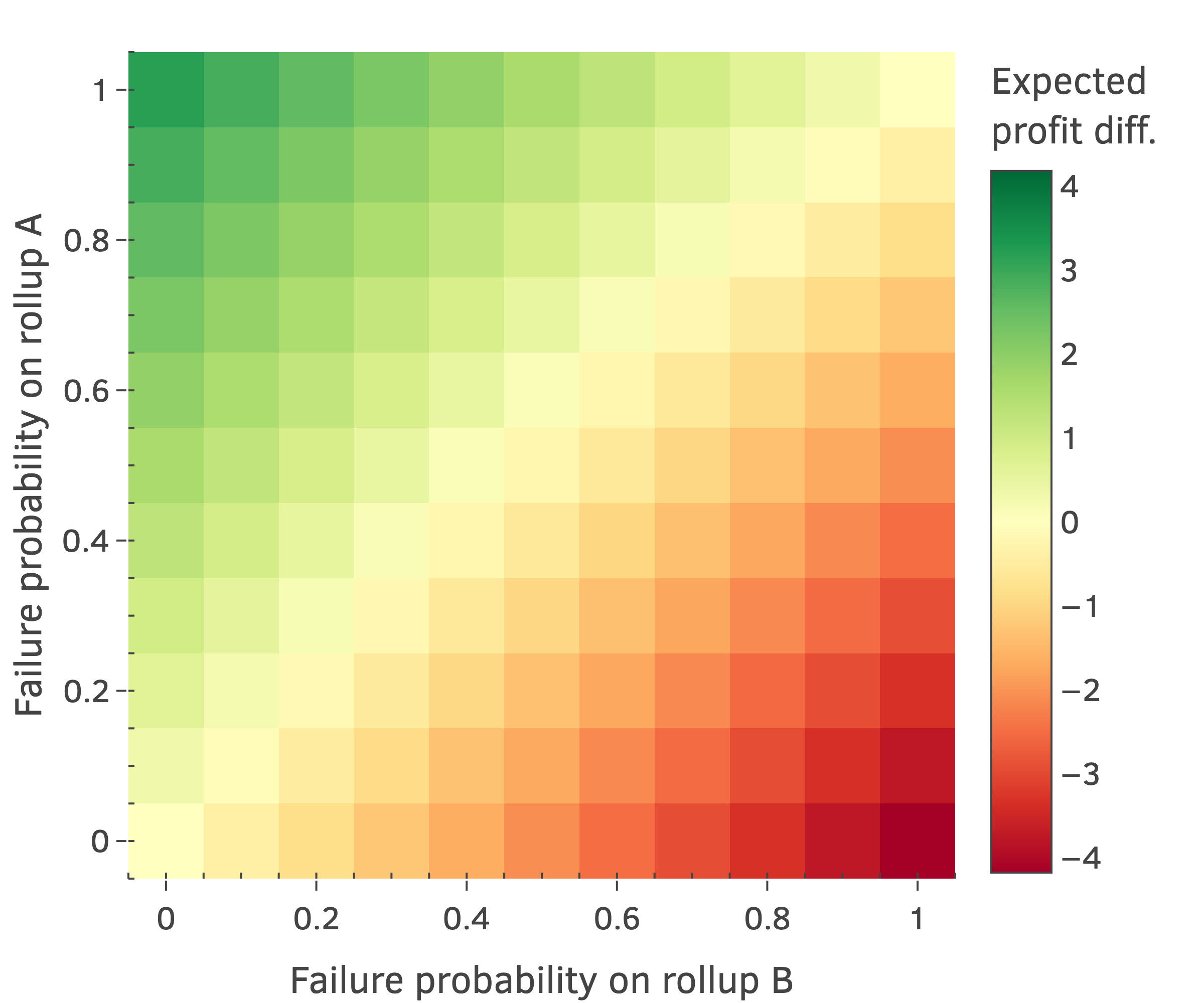

There are the failure probabilities and , which we will analyze together with the external price. Figure 1 provides an example for each of the three possible configurations of the relative position of and and , and the full range of failure probabilities and .

()

()

()

When the external price is larger than both pool prices (Figure 1(a)), the expected profit difference can be positive or negative, depending on the failure probabilities. If failures are more likely on rollup , the difference is positive, meaning that the arbitrageur will profit on average by switching to the atomic regime. However, if failures are more likely on rollup , the difference is negative, and switching is no longer profitable.

Intuitively, this relationship makes sense. When the external price has a larger difference to the price on rollup than the price differences in the two rollups, it would be better to arbitrage rollup against the external price than to arbitrage it against rollup . Therefore, having swap failing and swap executing leads to a net gain for the arbitrageur when valued against this external price (which means that atomicity is worse for the arbitrageur).

On the other hand, when the external price is smaller than both pool prices (Figure 1(c)), the relationship is inverted. In this case, the rationale is similar, and switching to an atomic regime is only advantageous when failures are more likely on rollup since arbitraging rollup against the external price generates more profit than arbitraging it against rollup .

Finally, there is the case where the external price is between the two pool prices (Figure 1(b)). This can arguably be the most likely case if we assume that the external price comes from a more liquid venue and that the pools on the two rollups hover around this more stable price. Interestingly, the expected profit difference is always negative in this case, independently of the failure probabilities. Similarly to the previous cases, when we value liquidity using an external price, and one of the swaps fails and the other executes, we are, in a way, arbitraging the pool that did not fail against the external price. When the external is between the prices in each pool, having only one swap failing is always better than having both reverting, as we would collect some additional profit from arbitraging the pool that did not fail against the external price.

Focusing on the failing probabilities, there is a special case we can analyze. If the two failure probabilities are equal (i.e., ), the expected profit difference is always negative, meaning that, on average, the arbitrageur should stick with the status quo without atomicity. This result comes directly from Equation 12:

| (13) |

4 Conclusions

Our work studies cross-rollup arbitrage in the context of a shared sequencing system offering atomic execution, a feature that ensures either all or none of a sequence of arbitrage transactions across multiple rollups are executed. Here, we investigate whether atomic execution is sufficient to significantly boost arbitrage profits and, in turn, sequencer revenue.

Our results reveal that arbitrage profits do not always improve under atomic execution, and thus, this feature alone is not enough to convince both arbitrageurs and rollup operators to switch to this new approach. When considering a case where an arbitrageur exploits an opportunity between two CPMM pools and values the final profit using an external price, we find that whether switching from non-atomic to atomic execution is net positive for the arbitrageur depends on the failure probabilities of the swaps in each rollup and the relative difference of the external price to the pool prices.

This work could be extended in multiple ways. Firstly, we assume that the arbitrageur maintains their liquidity in the tokens being arbitraged. However, arbitrageurs may keep liquidity in a stable token and convert it on demand to address volatility; our model could be extended to account for this conversion. Secondly, we do not consider transaction costs. Although it is currently low and likely to remain such for rollups, adding this cost would be another possible extension to the model. Thirdly, and more importantly, one could explore how prevalent the scenarios in which atomic execution is not beneficial to an arbitrageur are. This would require a detailed empirical analysis of various pools across different deployed rollups and varying time periods.

References

- noa [2024] Astria: The Shared Sequencer Network (Feb 2024), URL https://www.astria.org/blog/astria-the-shared-sequencer-network

- Bearer et al. [2024] Bearer, J., Bünz, B., Camacho, P., Chen, B., Davidson, E., Fisch, B., Fish, B., Gutoski, G., Krell, F., Lin, C., Malkhi, D., Nayak, K., Shen, K., Xiong, A., Yospe, N., Long, S.: The Espresso Sequencing Network: HotShot Consensus, Tiramisu Data-Availability, and Builder-Exchange (2024), URL https://eprint.iacr.org/2024/1189, publication info: Preprint.

- Daian et al. [2020] Daian, P., Goldfeder, S., Kell, T., Li, Y., Zhao, X., Bentov, I., Breidenbach, L., Juels, A.: Flash Boys 2.0: Frontrunning in Decentralized Exchanges, Miner Extractable Value, and Consensus Instability. In: 2020 IEEE Symposium on Security and Privacy (SP), pp. 910–927 (May 2020), doi:10.1109/SP40000.2020.00040, URL https://ieeexplore.ieee.org/document/9152675, iSSN: 2375-1207

- Gogol et al. [2024] Gogol, K., Messias, J., Miori, D., Tessone, C., Livshits, B.: Layer-2 Arbitrage: An Empirical Analysis of Swap Dynamics and Price Disparities on Rollups (Jun 2024), doi:10.48550/arXiv.2406.02172, URL http://arxiv.org/abs/2406.02172, arXiv:2406.02172 [cs]

- Mamageishvili and Schlegel [2023] Mamageishvili, A., Schlegel, J.C.: Shared Sequencing and Latency Competition as a Noisy Contest (Oct 2023), URL http://arxiv.org/abs/2310.02390, arXiv:2310.02390 [cs]

- Motepalli et al. [2023] Motepalli, S., Freitas, L., Livshits, B.: SoK: Decentralized Sequencers for Rollups (Oct 2023), doi:10.48550/arXiv.2310.03616, URL http://arxiv.org/abs/2310.03616, arXiv:2310.03616 [cs]

- NodeKit [2024] NodeKit: The Composable Network: Unifying Chains with Javelin, the first Superbuilder (Aug 2024), URL https://nodekit-tinywins.vercel.app/posts/the-composable-network

- Radius [2023] Radius: Radius: Trustless Shared Sequencing Layer (May 2023), URL https://medium.com/@radius_xyz/radius-trustless-shared-sequencing-layer-b293dfa75db

- Systems [2023] Systems, E.: The Espresso Sequencer (Mar 2023), URL https://hackmd.io/@EspressoSystems/EspressoSequencer

- Torres et al. [2024] Torres, C.F., Mamuti, A., Weintraub, B., Nita-Rotaru, C., Shinde, S.: Rolling in the Shadows: Analyzing the Extraction of MEV Across Layer-2 Rollups (Apr 2024), URL http://arxiv.org/abs/2405.00138, arXiv:2405.00138 [cs]