Sequential Design with Derived Win Statistics

Abstract

The Win Ratio has gained significant traction in cardiovascular trials as a novel method for analyzing composite endpoints (Pocock and others, 2012). Compared with conventional approaches based on time to the first event, the Win Ratio accommodates the varying priorities and types of outcomes among components, potentially offering greater statistical power by fully utilizing the information contained within each outcome. However, studies using Win Ratio have largely been confined to fixed design, limiting flexibility for early decisions, such as stopping for futility or efficacy. Our study proposes a sequential design framework incorporating multiple interim analyses based on Win Ratio or Net Benefit statistics. Moreover, we provide rigorous proof of the canonical joint distribution for sequential Win Ratio and Net Benefit statistics, and an algorithm for sample size determination is developed. We also provide results from a finite sample simulation study, which show that our proposed method controls Type I error maintains power level, and has a smaller average sample size than the fixed design. A real study of cardiovascular study is applied to illustrate the proposed method. Sequential Design; Win Ratio; Net Benefit; U-Statistics; Hierarchical Composite Endpoint

1 Introduction

The use of composite endpoints as primary outcomes is common in randomized clinical trials, particularly in cardiovascular (CV) trials. A frequently used composite endpoint in CV trials is Major Adverse Cardiac Events, which typically include CV death, myocardial infarction, stroke, hospitalization, and other related events (Sharma and others, 2020). The popularity of composite endpoints stems from two key advantages: (1) Potentially increase the event rate and statistical power, thereby reducing the required sample size; (2) Eliminate the need for multiplicity adjustments, and (3) Provide a unified measure of treatment effect.

There are two primary approaches to comparing composite endpoints between subjects: by event time or by clinical priority. The former approach, often called the traditional composite endpoint (TCE), is defined as the time to the first event (Pocock, 1997). The second approach, known as the hierarchical composite endpoint (HCE), involves comparing each component of the endpoint between the subjects based on a predefined clinical priority order of HCE (Buyse, 2010; Pocock and others, 2012). Compared to TCE, HCE addresses the challenges of analyzing prioritized outcomes by allowing different components of the composite endpoint to carry varying levels of clinical importance. In addition, non-event outcomes with clinical meaning could also be included in HCE. A more detailed discussion of the advantages and challenges of HCE in comparison to TCE can be found in Redfors and others (2020).

Given the advantages of HCE, Buyse (2010) introduced the concept of Net Benefit (NB) based on HCE, defined as the difference between the probability that a treated subject wins against a control and the probability that a control wins against a treated subject, to assess treatment effects. Pocock and others (2012) later proposed the Win Ratio (WR) as a metric for quantifying treatment effects on composite endpoints by the ratio between win and loss proportion for pairwise comparison, building on a similar hierarchical approach. The large-sample theory for the WR in fixed design studies has been rigorously developed using U-statistics (Bebu and Lachin, 2016). To facilitate hypothesis testing and study design, Luo and others (2017) provided a closed-form variance estimator under the null hypothesis. The asymptotic properties of WR can be readily extended to the NB and other test statistics derived from win statistics. Additionally, Mao and others (2022) introduced a sample size calculation method for fixed design studies, incorporating a combination of copula models (Oakes, 1989), U-statistics, and numerical computations. Currently, according to the online registry ClinicalTrials.gov’s data, there is a sharp rise in both the number of trials and the patients involved to adopte this Win Ratio or related methodology Mao (2024).

To date, research has predominantly focused on fixed design methodologies. However, clinical trials often benefit from more flexible approaches that allow for early decisions based on interim data. Group sequential designs are a common type of adaptive clinical trial design that offers flexibility over fixed designs, enabling decisions regarding early stopping for futility or efficacy (Pocock, 1977). Group sequential tests for continuous, binary, and time-to-event outcomes are well-documented in the literature. Despite the development of fixed design methods for win statistics, sequential designs remain under-explored in the literature. Bergemann and others conducted a pilot study that demonstrated independent increments for sequential NB and approximately independent increments for sequential WR, both of which are crucial for developing sequential designs (Jennison and Turnbull, 1997; Scharfstein and others, 1997). Establishing the asymptotic canonical distribution is a critical component in developing sequential designs (Jennison and Turnbull, 2000). However, the canonical joint normality of sequential test statistics has yet to be formally established (Jennison and Turnbull, 2000). Up to now, there is also a lack of power analysis and corresponding sample size determination methods for sequential designs based on win statistics.

In our study, we developed a sequential design based on NB and WR test statistics. Firstly, we reviewed the fixed design based on NB and WR test statistics and its asymptotic normality in Section 2. Next, in Section 3, we extended to group sequential setting and rigorously proofed the canonical joint distribution for sequential NB and WR test statistics. Variance estimation methods are also provided in this section. Then, power analysis and type-I error control are discussed in detail in Section 4. In addition, we provide a sample size determination algorithm in Section 4 considering the practical application. Section 5 conducted a detailed numerical analysis to mimic the scenario of a CV trial using HCE. Then, we illustrate our developed design based on sequential derived win statistics to a real-world example from the HF-ACTION in section 6. Finally, the conclusion and discussion for this provided sequential design are provided in Section 7.

2 Derived Win Statistics for Fixed Design

In this section, we begin by illustrating the framework of the Win Statistics within a fixed design, particularly focusing on HCE that involve both terminal and non-terminal events. Next, we extend the proposed framework to accommodate general mixed-type HCE. In the final part of this section, we present the asymptotic properties of the derived Win Statistics, including the Win Ratio and Net Benefit.

2.1 Basic Setting and Consideration with Survival Outcome Only

Firstly, we consider the HCE to consist of a terminal and a non-terminal event. The terminal event, such as the event of death, censors the event of the non-terminal event. That is to say, we could not observe the non-terminal event after the terminal event happens. This setting of the composite endpoint is commonly used in CV trials where for instance CV death is the terminal event and the non-fatal stroke, hospitalization of heart failure, or nonfatal MI is the non-terminal event as considered (Luo and others, 2017; James and others, 2024). To help for illustration, in this subsection, we denote the composite endpoint as the time to death for the terminal event and the time to hospitalization of heart failure as the non-terminal event. These two variables are usually correlated. In addition, may right-censor but not vice versa. As for censoring distribution, we have the following two assumptions:

[Common Censoring] We assume the censoring time is shared by all -composite time-to-event endpoints within the same subject. In addition, following Fine and Gray (1999), we assume the independence of censoring time and both composite time-to-event endpoints: {Assumption}[Independence of Censoring Time and Composite Endpoints] We assume

Remark 2.1.

Both common censoring and independence assumption of the censoring time based on 2-composite time-to-event endpoints above could be extended to a more general case with composite time-to-event endpoints.

Due to the censoring time and the terminal event , we observe and , along with the event indicators and . Here and in the following, we define as the minimum value between and . It is important to note that if both events are non-terminal, the observation value of each non-terminal event is the minimum of the censoring time and its respective time-to-event, without involving the terminal event in taking the minimum. Suppose in a fixed random trial design, there are patients in the treatment arm and patients in the control arm. We denote observed outcome for subject in the treatment arm and for subject in the control arm. Here and in the sequel, we denote subject and without superscript to denote the subject in the treatment group and and superscript as in the control group.

Furthermore, following the definition from Luo and others (2017), for two subjects and , we define win indicator ( over ) based on event of death and event of hospitalization as and respectively. Similarly, the loss indicator ( against ) are and respectively. Then, other scenarios are inconclusive and we define tie indicators are and respectively.

Next, following Bebu and Lachin (2016) we define the winner, loser, and tier considering the composite endpoints as . Notice that elements in and are ordered according to priority, starting with the terminal event . Then, following the partial ordering (Rauch and others, 2014), we define comparison between and as

| (2.1) | ||||

If , then is called a winner, while is a loser. Similarly, we could define and here is a loser but is a winner. Lastly, if neither or , we define this comparison as inconclusive or tie, denoted as By definition of (2.1), we show its rationality in terms of logistics. Due to the priority of , we first compare the and see if there is a winner. We could also conclude that the winner ( over ) happens on if and only if . If we cannot tell the winner or the loser based on , where , we then check the next endpoint, . It should be noted that the indicator function here differs from the study by Dong and others (2020), as they consider as the indicator of winner happens on , which overestimates the probability of winner. Additionally, we find that only happens when death or hospitalization from the control arm is observed. Similar logistics happen in .

2.2 Win Statistics based on Mixed-Type Data Contexts

In this subsection, we extend the data type of outcomes in the hierarchy composite endpoint to the general setting. In this case, some non-event outcomes can be included, such as quality of life score and physiological measures.

Assume that the HCEs consist of a total of outcomes, which may differ in data type. Following the notation above, the observed HCEs for subject in the treatment group are denoted as , where the outcomes in are ordered according to clinical priority. Furthermore, the -th outcome in can be continuous, binary, ordinal, or time-to-event. When is time-to-event, it is denoted as , where represents the observed event time and is the censoring indicator. Similarly, we define observed hierarchy composite endpoints of subject in the control group are noted as .

Next, a pairwise comparison is performed between subject in the treatment group and subject in the control group, starting with the first outcome and continuing until a winner is determined. The winner, loser, or tie for each outcome between these two subjects is defined based on the data type of the outcome, as shown in Table 1.

| Outcome Data Type | Winner | Loser | Tie |

|---|---|---|---|

| Binary | |||

| Continuous or Ordinal | |||

| Time-to-event |

In the following subsection, we proposed the kernel function and Win- and Loss- statistics for fixed design following the logistics above. First, for each pairwise comparison between and , win kernel function and loss kernel function are defined as

| (2.2) |

With the defined kernel function above, the Win Statistics and Loss Statistics are proposed as the summation across all pairwise comparisons, where

| (2.3) |

Here, and are the total number of wins and losses in the treatment group among pairwise comparisons, respectively. For , the variance can be expressed as:

| (2.4) |

where, for any , we define

and

2.3 Asymptotic Property of Derived Win Statistics: Net Benefit and Win Ratio

Derived from the proposed Win and Loss Statistics, two additional derived Win Statistics are introduced: Net Benefit and Win Ratio. The Net Benefit, also known as the Win Difference or Win-Loss Buyse (2010); Luo and others (2017), is defined as with its corresponding estimand given by Furthermore, we can derive the variance of the Net Benefit (NB) as

| (2.5) |

Next, the Win Ratio (WR), is proposed as with its corresponding estimand given by . Additionally, the approximate variance of the WR can be derived as

| (2.6) | ||||

Details of the derivation process of are shown in the Appendix.

Then we apply these derived Win statistics to a fixed design scenario. Let be the total sample size and suppose sample size and both tend to infinity in such a way that

Suppose and all have finite values for . The joint distribution of Win Statistics and is asymptotically normal, which follows

| (2.7) |

where the components of the variance-covariance matrix are given by

Many previous studies have shown the above results of the asymptotic joint distribution of generalized U statistics, like Lehmann (1999), Bebu and Lachin (2016), and Lee (2019). Based on the asymptotic joint and shown in formula (2.7), we can establish the asymptotic joint distribution of different derived versions of Win-statistics, such as the Net Benefit and Win Ratio. For example, the asymptotic joint distribution of NB, , can be established by linear transformation:

| (2.8) |

where .Thus, we have

| (2.9) |

It is worth stating that the results of asymptotic normality for can also be derived by the Central limit theorem. In addition, based on the variance formula of NB (2.5), we can also show as .

Moreover, by Delta method applying on formula (2.7), the asymptotic property of log WR, , and follows

| (2.10) |

and for variance formula (2.6), we can show as . Thus we have,

| (2.11) |

Notice that both asymptotic results ( formula 2.8 and 2.10) are tiny different from Bebu and Lachin (2016) and Bergemann and others .

3 Sequential Design based on Derived Win-Statistics

In this section, we consider the scenario of a sequential design with multiple interim analyses, where the test statistic in each interim is based on the Win statistics introduced in Section 2. This section also helps to establish the following sequential design based on the NB and WR.

In the context of a group sequential design characterized by a total of interim analyses, denote the cumulative sample size at interim by for the treatment arm and the control arm, respectively, with . We developed the following mild condition C1 following mild conditions on the sample sizes at different monitoring times for both groups is necessary for the following theoretical development.

-

Condition C1: Let be the total sample size and . It is true that and , as and for , where positive constants satisfies that .

Remark 3.1.

Condition C1 requires that the sample size ratios between two arms and among different trial stages will converge as the total sample size increases. However, in practice, researchers only need to ensure that the proportion of subjects enrolled for each arm during each stage is not negligible, one simple example is to split subjects between arms and among stages evenly.

Define sequential Win or Loss statistics at -th interim analysis as

| (3.1) |

First, we show general results of the joint asymptotic normality on both basic win and loss U statistics in each stage by Hájek Projection. In detail, we initially establish the asymptotic normality of a random vector associated with projections at each interim analysis. Following this, we establish the desired joint asymptotic normality of sequential Win and Loss statistics, . The Hájek projection principle, as outlined by van der Vaart (1998), specifies that projecting onto the Hilbert Space to be , where

| (3.2) |

and projection on such will result in

| (3.3) |

with variance formula

| (3.4) |

Under condition C1, the limitation of variance formula can be derived as

| (3.5) |

Lemma 3.2.

Joint Asymptotic Normality of Projection for Win- and Loss- Statistics

Considering the Hájek projection of onto as defined by formula (3.3), define Under Condition C1, we obtain

| (3.6) | ||||

as and for . Here, represents the -dimensional multivariate normal distribution with a zero mean vector of dimension , and a symmetric variance-covariance matrix . Specifically, with the diagonal elements are 1 and for off-diagonal elements, and for , and we have

| (3.7) | ||||

as and for .

Remark 3.3.

As for the asymptotic covariance of two Hájek projections statistics with the same kernel function (i.e ) but at different stages , we have

which is also the limit of . The above results are the independent increments of the sequential statistics by Kim and Tsiatis (2020). Independent increments only happen at two basic win Statistics with the same kernel function. Detailed proof of lemma 3.2 is shown in Appendix.

Based on the results of Lemma 3.2, we can also derive the asymptotic distribution of non-normalized Hájek sequential basic statistics. Specifically, we have

| (3.8) |

where for the asymptotic variance-covariance matrix , and for , and we have

Based on Lemma 3.2, we can establish the joint asymptotic normality of sequential standardized Win statistics (seq-SW) and Loss statistics (seq-SL) , where

Theorem 3.4.

Joint Asymptotic Normality for Sequential Win and Loss Statistics

- 1.

-

2.

(Non-Standardized Version) For the sequential non-standardized Win- (seq-NSWs) and Loss- statistics (seq-NSLs) , under Condition C1, we have

(3.10) where is evaluated in formula (3.8).

Remark 3.5.

It is clear that the non-standardized version of Theorem 3.4 is an extension to the K-stage sequential design from the fixed design of the asymptotic joint normal distribution of Win- and Loss-statistics from Bebu and Lachin (2016) (formula 2.7). Moreover, this theorem is vital to help establish the following asymptotic normality results of our sequential derived Win- and Statistics (e.g., NB and WR). Detailed proof of Theorem 3.4 is shown in Appendix 11. Part 2 of the non-standardized version can be derived from the standardized version in Part 1.

With the results of Theorem 3.4, we construct logically the derived Win statistics and find their joint asymptotic distribution. For each interim with , marginal asymptotic property of Win Statistics derived from in Section LABEL:Sec:_Fixed_IPCWWinStat can be applied to . That is to say, for each interim , we have Net Benefit and Win Ratio which are both derived from Win- and Loss- statistics and their standardized versions are defined as

| (3.11) |

Variance of Net Benefit in stage , , can be easily derived based on formula (2.5) by substituting for , respectively. Also similarly, can be derived in the same manner.

3.1 Joint Asymptotic Distribution of Sequential Net Benefit and Win Ratio

In this section, we establish the joint asymptotic normality for the proposed sequential Net Benefit (NB) and sequential Win Ratio (WR), considering both the standardized versions (sequential SNBs and SWRs) and the corresponding non-standardized versions (sequential NSNBs and NSWRs). The following propositions demonstrate the properties of the derived Net Benefit and Win Ratio statistics in sequential design scenarios.

Canonical Joint Distribution for Sequential Net Benefit

Considering sequential standardized Net Benefit (seq-SNB) or their non-standardized versions (seq-NSNB), we have the following results:

-

1.

(Independent Increment of Net Benefit) For any pair of seq-SNBs at different stages , we have

For the non-standardized version, we have

-

2.

(Joint Asymptotic Normality of Net Benefit) Under Condition C1, for the seq-SNBs, we have

(3.12) as and for . The asymptotic variance-covariance matrix is given by where the diagonal elements are 1, and the off-diagonal elements for are defined as

For the seq-NSNB, we have

(3.13) where the asymptotic variance-covariance matrix is given by with elements for defined as

Canonical Joint Distribution for Sequential Win Ratio

Considering sequential standardized Win-Ratio statistics (seq-SWR) or their non-standardized version (seq-NSWR), we have the following results:

-

1.

(Asymptotic Independent Increment of Win Ratio) For any pair of seq-SWR at different stages , we have

For seq-NSWR, we have

-

2.

(Joint Asymptotic Normality of Win Ratio) Under Condition C1, For seq-SWR, we have

(3.14) as and for . Asymptotic variance-covariance matrix is given by where the diagonal elements are 1, and off-diagonal elements for , is defined as

where for simplicity, we define

(3.15) For seq-NSWR, we have

(3.16) where asymptotic variance-covariance matrix is given by for , we have

Remark 3.6.

Both results for Part (1) of Proposition 3.1 and 3.1 are known as the independent increments of the sequential statistics by Kim and Tsiatis (2020) and we have shown it also applies to our sequential Net Benefit and Win Ratio statistics. In addition, results for Part (2) of Proposition 3.1 and 3.1 both help to establish the sequential test statistics in the design setting, such as Type-I error control and Power analysis. Detailed proof for Proposition 3.1 and 3.1 are provided in Appendix.

After establishing the joint normality and independent increment properties, we consider the construction of hypothesis test statistics. The variance estimation method for both sequential SNBs and SWRs needs to be provided for our sequential statistics. Additionally, the asymptotic variance-covariance matrix must be estimated to ensure Type-I error control and power analysis.

For the sequential statistics, we need to estimate , , and for seq-SNBs and seq-NSNBs. Furthermore, we need to estimate and for SWRs and NSWRs. In our study, empirical estimators for , , , , and are provided in the Appendix. In this study, we test the hypothesis of the sequential study with the null hypothesis against the one-sided alternative hypothesis . Therefore, we propose seq-SNBs and seq-SWRs test statistics corresponding to the monitoring times under the null hypothesis as follows:

| (3.17) |

where and are empirical estimates for and , respectively, by plugin the empirical estimator of , , , , and to their corresponding estimation formula. In addition, empirical estimators for seriers of variance-covariance matrix , , and could also be derived. Non-standardized versions of sequential test statistics could also be developed. Details of empirical estimators are provided in the Web Supplementary Material.

4 Power Analysis and Sample Size Determination

4.1 Type I Error Spending and Theoretical Power

In this section, we present a framework for Type I error controlling and evaluating theoretical power, including a discussion on the alpha spending method and critical boundaries. The framework employed here followed Lan and Demets (1983). As for the alpha spending function, Kim and Demets (1987) recommended several strictly convex and monotonically increasing alpha spending functions developed by Lan and Demets (1983) and Kim and Demets (1987). In our study, we utilize for alpha spending function, where denotes the information fraction up to interim time point , defined as for sequential NBs or for sequential WRs, for . This alpha spending function is derived from the Kim-Demets power family . As is shown in Kim and Demets (1987), a strictly convex alpha spending function leads to a steady increase in partial Type I error, resulting in monotonically decreasing critical boundaries .

The partial Type I error values, or partial alpha values, at each monitoring time are set as with at the outset and for the family parameter. Critical boundaries can be estimated using the split alpha values by the alpha spending function under the null hypothesis . Assuming a one-sided hypothesis test, we follow Slud and Wei (1982) in constructing discrete sequential critical boundaries . This is achieved by setting

| (4.1) |

for . Here, follows the K dimensional under the null hypothesis, with a zero mean vector and a variance-covariance matrix could be valued by any one of previous four developed variance-covariance matrix, , , and under the .

To evaluate the theoretical power, we employ the critical boundaries determined under the null hypothesis and compute the rejection probabilities across monitoring times. The rejection probabilities are defined as follows:

| (4.2) |

for . Here follows a K-dimensional multivariate Normal distribution under the alternative hypothesis and is the estimand and it could be or under the . The sum of these rejection probabilities yields the overall theoretical power, i.e.,

4.2 Sample Size Determination

For sample size determination, we need to specify the distribution of each outcome in and further under and , respectively. Considering testing and study design, it is necessary to evaluate (under ), (under ) and (under ) displayed in (4.1 and 4.2), both of which are critical for theoretical power calculation. First, can be easily approximated by with very large data samples from the pre-specified distributions for and under by its empirical estimator . Similarly, and can be approximated by their empirical estimator and (given Web Supplementary Material) using very large generated and data sample or called super-population as well under and , respectively.

It can be very tedious, if not impossible, to provide explicit formulas for a group sequential design as is possible for a fixed design. For simplicity, we assume that the total sample size is evenly split between the two arms and across stages. We propose an iterative approach to find the sample size for the proposed sequential design, as outlined in Algorithm 1 when stages are planned.

The basic idea behind this algorithm is to search for different sample sizes and identify the one that results in the required power. The key step in this process is determining the testing power for each sample size, which can be achieved through the aforementioned theoretical power evaluation approach. Furthermore, this algorithm can be extended to scenarios where the sample size is unevenly allocated between the two arms or across different interim stages.

-

•

Total alpha level

-

•

Alpha spending method

-

•

Theoretical power level

-

•

Marginal Distribution of each outcome and copula method for the joint distribution

5 Numerical Analysis

In this section, we conduct a numerical analysis to mimic the scenario of a cardiovascular trial, whose primary outcome typically includes an HCE of death , hospitalization for heart failure , and New York Heart Association (NYHA) Functional Classification (James and others, 2024). The first two outcomes are time-to-event, and the last is four levels of ordinal outcome, with small to large representing deterioration. Following the notation above, we denote the HCE in the treatment arm as We compare the fixed method and sequential method in these scenario settings, according to but not limited to power level and Type-I error. For simplicity, we assume an overall number of stages and an allocation ratio for each stage and arm we have

Considering the correlation between outcomes in the HCE, a trivariate Clayton copula is applied to generate the outcomes in HCE, where the copula parameter, denoted as , is derived from a common Kendall’s across all pairwise comparisons (Oakes, 1989; Hofert and others, 2018). Specifically, the copula parameter is calculated using the relationship , which facilitates the modeling of right tail dependence. This assumption implies that the strength of dependence between endpoints, as measured by Kendall’s , is uniform across all three dimensions of the copula. Suppose survival outcome death and hospitalization both follow exponential distributions with parameters and . Let be the hazard rate for the th event, where if subject in the treatment group and on the standard group. For ordinal outcome , we consider following proportional odds model

| (5.1) |

for , where denotes as population proportion of level in group . Independent of time-to-event outcomes, we assume that the censoring variable follows a uniform distribution on the interval . To be noted, in our study, could be extended to follow any kind of distribution, like exponential distribution or uniform distribution .

The hypotheses are established as and . Throughout the simulation, the parameters and were held constant, while , , and were varied in different simulation settings. We test the scenarios combination where or 0.4 under the and or 24. Type I error was controlled at the 0.05 level, with the power fixed at 90%. Four methods were compared based on their theoretical and attained power or Type I error levels: seq-SNB, seq-SWR, fix-SNB, and fix-SWR. The last two represent fixed designs with standardized NB and WR. For simplicity, the sample size across different methods was kept the same in the same scenario and was determined by seq-SNB using Algorithm 1. For each scenario, 10,000 Monto Carlo simulations are generated to obtain the attained corresponding Type-I error and power level. For comparison, the bias between attained and theoretical Type-I or power level was also reported.

Simulation results are shown in Table 2 (Type I error control) and Table 3 (Power analysis at the 90% level). Firstly, bias for both Type I error rates and power levels is minimal across all methods and parameter scenarios, indicating that the asymptotic theory is well-supported. In Table 3, fixed-design methods exhibit slightly higher power than sequential designs. As a result, they require a smaller maximum sample size (MSS), though not necessarily a smaller average sample size (ASN). When accounting for early stopping, sequential methods demonstrate a markedly reduced ASN. Regarding the different parameter settings under , the larger the value of , the smaller the sample size needed to achieve the corresponding power level. Finally, there is no clear difference regarding the attained power level between seq-SNBs and seq-SWRs.

| c | Method | MSS | Attained Type I Rate (%) | Type I Error Bias (%) | ||

|---|---|---|---|---|---|---|

| 0 | 0 | 12 | seq-SNBs | 432 | (0.60, 2.36, 5.02) | (0.04, 0.14, 0.02) |

| seq-SWRs | (0.57, 2.22, 5.03) | (0.01, 0.00, 0.03) | ||||

| fix-SNB | 5.20 | 0.20 | ||||

| fix-SWR | 5.17 | 0.17 | ||||

| 24 | seq-SNBs | 456 | (0.57, 2.38, 5.06) | (0.01, 0.16, 0.06) | ||

| seq-SWRs | (0.59, 2.31, 5.07) | (0.03, 0.09, 0.07) | ||||

| fix-SNB | 5.00 | 0.00 | ||||

| fix-SWR | 5.07 | 0.07 | ||||

| 0 | 12 | seq-SNBs | 279 | (0.79, 2.36, 4.99) | (0.23, 0.14, -0.01) | |

| seq-SWRs | (0.53, 2.30, 5.04) | (-0.03, 0.08, 0.04) | ||||

| fix-SNB | 5.24 | 0.24 | ||||

| fix-SWR | 5.11 | 0.11 | ||||

| 24 | seq-SNBs | 303 | (0.64, 2.26, 5.06) | (0.08, 0.04, 0.06) | ||

| seq-SWRs | (0.57, 2.25, 5.37) | (0.01, 0.03, 0.37) | ||||

| fix-SNB | 4.74 | -0.26 | ||||

| fix-SWR | 5.43 | 0.43 | ||||

| 0 | 0 | 12 | seq-SNBs | 228 | (0.66, 2.69, 5.53) | (0.10, 0.47, 0.53) |

| seq-SWRs | (0.51, 2.19, 4.99) | (-0.05, -0.03, -0.01) | ||||

| fix-SNB | 4.78 | -0.22 | ||||

| fix-SWR | 5.55 | 0.55 | ||||

| 24 | seq-SNBs | 189 | (0.94, 2.59, 5.64) | (0.38, 0.37, 0.64) | ||

| seq-SWRs | (0.54, 2.19, 5.04) | (-0.02, -0.03, 0.04) | ||||

| fix-SNB | 5.21 | 0.21 | ||||

| fix-SWR | 4.73 | -0.27 | ||||

| 0 | 12 | seq-SNBs | 165 | (0.74, 2.63, 5.82) | (0.18, 0.41, 0.82) | |

| seq-SWRs | (0.58, 2.30, 5.15) | (0.02, 0.08, 0.15) | ||||

| fix-SNB | 5.31 | 0.31 | ||||

| fix-SWR | 5.07 | 0.07 | ||||

| 24 | seq-SNBs | 141 | (0.90, 2.63, 5.33) | (0.34, 0.41, 0.33) | ||

| seq-SWRs | (0.71, 2.34, 5.16) | (0.15, 0.12, 0.16) | ||||

| fix-SNB | 5.60 | 0.60 | ||||

| fix-SWR | 5.02 | 0.02 |

| c | Method | MSS (ASN) | Attained Power Level (%) | Bias of Power (%) | ||

|---|---|---|---|---|---|---|

| 0.2 | 0.2 | 12 | seq-SNBs | 432 (352) | (22.49, 66.61, 90.91) | (1.57, 0.94, 0.60) |

| seq-SWRs | 432 (352) | (21.15, 66.54, 90.92) | (0.60, 1.55, 0.96) | |||

| fix-SNB | 432 | 91.44 | 0.17 | |||

| fix-SWR | 432 | 91.49 | 0.59 | |||

| 24 | seq-SNBs | 456 (372) | (22.22, 66.37, 90.98) | (1.43, 0.94, 0.86) | ||

| seq-SWRs | 456 (371) | (20.48, 65.99, 90.77) | (0.05, 1.23, 0.98) | |||

| fix-SNB | 456 | 91.70 | 0.56 | |||

| fix-SWR | 456 | 91.42 | 0.65 | |||

| 0.4 | 12 | seq-SNBs | 279 (228) | (22.59, 65.42, 90.01) | (1.77, -0.12, -0.25) | |

| seq-SWRs | 279 (227) | (21.11, 65.84, 90.92) | (0.87, 1.36, 1.29) | |||

| fix-SNB | 279 | 91.44 | 0.23 | |||

| fix-SWR | 279 | 91.39 | 0.76 | |||

| 24 | seq-SNBs | 303 (247) | (21.39, 64.81, 89.35) | (0.64, -0.59, -0.81) | ||

| seq-SWRs | 303 (247) | (19.89, 64.88, 89.35) | (-0.31, 0.50, -0.23) | |||

| fix-SNB | 303 | 90.70 | -0.43 | |||

| fix-SWR | 303 | 90.66 | 0.08 | |||

| 0.4 | 0.2 | 12 | seq-SNBs | 228 (186) | (22.47, 65.44, 89.95) | (1.68, -0.09, -0.30) |

| seq-SWRs | 228 (186) | (20.28, 64.46, 89.37) | (0.16, 0.16, -0.15) | |||

| fix-SNB | 228 | 90.55 | -0.66 | |||

| fix-SWR | 228 | 90.04 | -0.50 | |||

| 24 | seq-SNBs | 189 (154) | (22.84, 66.20, 90.64) | (2.33, 1.14, 0.63) | ||

| seq-SWRs | 189 (154) | (19.95, 63.78, 89.93) | (0.25, 0.24, 0.83) | |||

| fix-SNB | 189 | 90.98 | 0.01 | |||

| fix-SWR | 189 | 91.16 | 1.03 | |||

| 0.4 | 12 | seq-SNBs | 165 (135) | (23.85, 66.76, 90.80) | (3.00, 1.05, 0.42) | |

| seq-SWRs | 165 (134) | (20.70, 66.20, 90.20) | (0.79, 2.22, 0.83) | |||

| fix-SNB | 165 | 90.83 | -0.50 | |||

| fix-SWR | 165 | 91.16 | 0.78 | |||

| 24 | seq-SNBs | 141 (115) | (23.19, 65.21, 89.72) | (2.67, 0.04, -0.36) | ||

| seq-SWRs | 141 (115) | (19.35, 63.06, 89.26) | (-0.07, -0.04, 0.41) | |||

| fix-SNB | 141 | 90.28 | -0.77 | |||

| fix-SWR | 141 | 91.08 | 1.19 |

6 Real Data Analysis

In this section, we apply our developed design based on sequentially derived win statistics to a real-world example from the HF-ACTION, a cardiovascular study conducted by O’Connor and others (2009). The primary objective was to evaluate the effect of adding exercise training to the usual patient care on the composite endpoint of all-cause hospitalization and death . In our study, we focus on a high-risk subgroup consisting of 426 non-ischemic patients with baseline cardio-pulmonary exercise tests no longer than nine minutes before reporting discomfort. In this subgroup, 205 patients were assigned to receive exercise training in addition to usual care and 221 were assigned to receive usual care alone. Data can be found in R package rmt. In our study, we utilize an HCE, denoted as , where represents observed event time and is observed indicator for endpoint , prioritized by clinical priority. The first hospitalization event was used in the HCE.

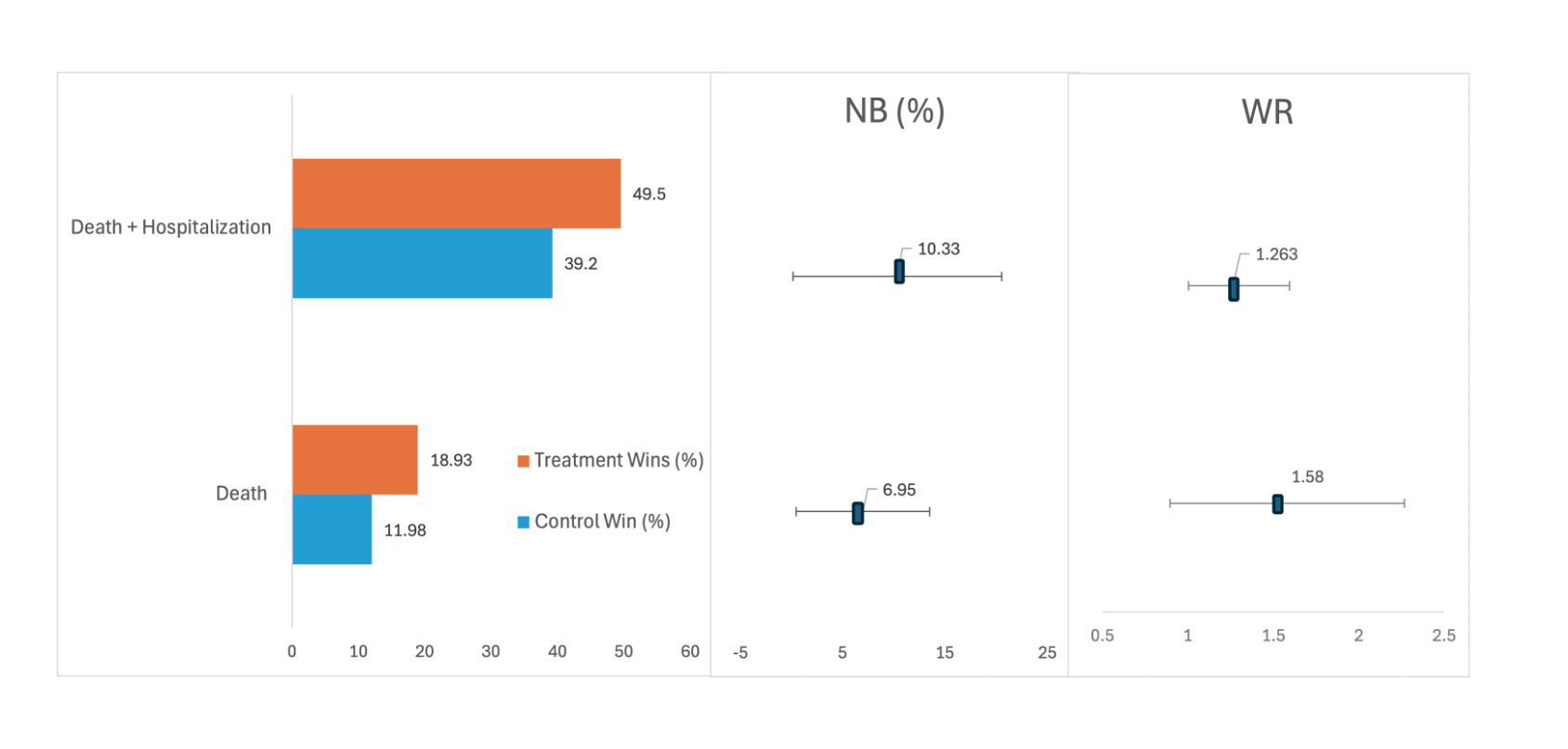

Analysis based on fixed design method is reported in Figure 1 and details can be found in Table 4. The HCE including events of death and hospitalization resulted in 49.50% wins for treatment and 39.20% for control (Net Benefit, 10.33%; 95% confidence interval [CI], 0.12% to 20.53%. Win Ratio, 1.265; 95% CI, 1.001 to 1.594). The endpoint with death only resulted in 18.93% wins for treatment and 11.98% for control (Net Benefit, 6.95%; 95% [CI], 4.14% to 13.48%. Win Ratio, 1.580; 95% CI, 0.895 to 2.265).

| HCE Components | Wins | Losses | Ties | NB (95% CI) | WR (95% CI) |

|---|---|---|---|---|---|

| Death | 18.93% | 11.98% | 69.09% | 6.95% (4.14%, 13.48%) | 1.580 (0.895, 2.265) |

| Death + Hospitalization | 49.50% | 39.20% | 11.26% | 10.33% (0.12%, 20.53%) | 1.263 (1.001, 1.594) |

Next, we compare seq-SNBs, seq-SWRs, fix-SNB, and fix-SWR based on the HF-ACTION data for theoretical power and average sample size. Empirical estimators for , , , , and were derived from the HF-ACTION data. The asymptotic variance for each method was estimated via plug-in empirical estimators. Critical boundaries, theoretical power, and average sample size based on the estimated variance for each method are reported in Table 5. For each method, theoretical power is calculated based on the actual sample size from this subgroup. Accordingly, the average sample size is decided based on the maximum sample size and theoretical power for each stage. From the results in Table 5, both sequential methods have a relatively smaller average sample size than both fixed design methods while maintaining the power level.

| Method | ASN | Critical Boundaries | Theoretical Power Level (%) |

|---|---|---|---|

| seq-SNBs | 367 | (2.54, 2.07, 1.74) | (7.94, 33.44, 61.49) |

| seq-SWRs | 368 | (2.54, 2.07, 1.73) | (7.92, 33.01, 61.01) |

| fix-SNB | 426 | 1.64 | 63.27 |

| fix-SWR | 426 | 1.64 | 62.71 |

7 Concluding Remarks

The Win Ratio has been gaining traction as an analytical method in biomedical research due to its ability to incorporate study outcomes of different types with a clinical priority order into a single composite endpoint. This approach eliminates the need for multiple testing adjustments and provides a unified interpretation of treatment effects, regardless of the outcome data type. In this study, we developed a sequential design framework based on the Win Ratio and Net Benefits test statistics. Our proposed method effectively controls the Type I error rate while achieving the desired power. Furthermore, by allowing for early determination of treatment efficacy or futility, the sequential design requires a smaller average sample size compared to the fixed design, as expected, for both Win Ratio and Net Benefit test statistics.

One limitation of this study pertains to the estimand for the Win Ratio, which can vary depending on the censoring or follow-up distribution. A more natural estimand in such cases would be the Win Ratio, assuming all patients were followed for the same duration (Mao, 2024; Oakes, 2016). To address the issue of varying censoring distributions, our sequential study censors participants recruited in each stage after each interim analysis, meaning no additional follow-up data is collected for these individuals. As a result, pairwise comparisons for constructing the Win-statistics are limited to subjects with the same follow-up distribution across different groups.

A more practical alternative would be to avoid administrative censoring after interim analyses and to continue following up to the next stage. This approach would allow the collection of long-term information for each participant. However, one must carefully consider whether comparing patients with differing follow-up times is meaningful. Moreover, the pairwise comparison between the same pair of subjects can vary across different interim analyses due to differences in follow-up times. As a result, the joint canonical distribution may not hold for the sequential Win Ratio or Net Benefit, potentially undermining the applicability of a sequential design in this context.

8 Data availability statement

The real study data that support the findings in this paper are openly available on the Comprehensive R Archive Network (CRAN; https://cran.r-project.org/web/packages/rmt/index.html).

References

- Bebu and Lachin (2016) Bebu, Ionut and Lachin, John M. (2016). Large sample inference for a win ratio analysis of a composite outcome based on prioritized components. Biostatistics 17(1), 178–187.

- (2) Bergemann, Tracy, Schindler, Jerry and Hanson, Tim. Group sequential methods for the win ratio. Available at SSRN 4450923.

- Buyse (2010) Buyse, Marc. (2010). Generalized pairwise comparisons of prioritized outcomes in the two-sample problem. Statistics in medicine 29(30), 3245–3257.

- Dong and others (2020) Dong, Gaohong, Mao, Lu, Huang, Bo, Gamalo-Siebers, Margaret, Wang, Jiuzhou, Yu, GuangLei and Hoaglin, David C. (2020). The inverse-probability-of-censoring weighting (ipcw) adjusted win ratio statistic: an unbiased estimator in the presence of independent censoring. Journal of biopharmaceutical statistics 30(5), 882–899.

- Fine and Gray (1999) Fine, Jason P and Gray, Robert J. (1999). A proportional hazards model for the subdistribution of a competing risk. Journal of the American statistical association 94(446), 496–509.

- Hofert and others (2018) Hofert, Marius, Kojadinovic, Ivan, Mächler, Martin and Yan, Jun. (2018). Elements of copula modeling with R. Springer.

- James and others (2024) James, Stefan, Erlinge, David, Storey, Robert F, McGuire, Darren K, de Belder, Mark, Eriksson, Niclas, Andersen, Kasper, Austin, David, Arefalk, Gabriel, Carrick, David and others. (2024). Dapagliflozin in myocardial infarction without diabetes or heart failure. NEJM evidence 3(2), EVIDoa2300286.

- Jennison and Turnbull (1997) Jennison, C. and Turnbull, B. W. (1997). Group-sequential analysis incorporating covariate information. 92, 1330–1341.

- Jennison and Turnbull (2000) Jennison, C and Turnbull, B. W. (2000). Group Sequential Methods with Applications to Clinical Trials. Boca Raton: Chapman & Hall/CRC.

- Kim and Demets (1987) Kim, K. and Demets, D. L. (1987). Design and analysis of group sequential tests based on the type i error spending rate function. Biometrika 72, 149–154.

- Kim and Tsiatis (2020) Kim, KyungMann and Tsiatis, Anastasios A. (2020). Independent increments in group sequential tests: a review. SORT: statistics and operations research transactions 44(2), 0223–264.

- Lan and Demets (1983) Lan, K. K. Gordon and Demets, D. L. (1983). Discrete sequential boundaries for clinical trials. Biometrika 70, 659–663.

- Lee (2019) Lee, A J. (2019). U-statistics: Theory and Practice. Routledge.

- Lehmann (1999) Lehmann, Erich Leo. (1999). Elements of large-sample theory. Springer.

- Luo and others (2017) Luo, Xiaodong, Qiu, Junshan, Bai, Steven and Tian, Hong. (2017). Weighted win loss approach for analyzing prioritized outcomes. Statistics in medicine 36(15), 2452–2465.

- Mao (2024) Mao, Lu. (2024). Defining estimand for the win ratio: Separate the true effect from censoring. Clinical Trials, 17407745241259356.

- Mao and others (2022) Mao, Lu, Kim, KyungMann and Miao, Xinran. (2022). Sample size formula for general win ratio analysis. Biometrics 78(3), 1257–1268.

- Oakes (1989) Oakes, David. (1989). Bivariate survival models induced by frailties. Journal of the American Statistical Association 84(406), 487–493.

- Oakes (2016) Oakes, D. (2016). On the win-ratio statistic in clinical trials with multiple types of event. Biometrika 103(3), 742–745.

- O’Connor and others (2009) O’Connor, Christopher M, Whellan, David J, Lee, Kerry L, Keteyian, Steven J, Cooper, Lawton S, Ellis, Stephen J, Leifer, Eric S, Kraus, William E, Kitzman, Dalane W, Blumenthal, James A and others. (2009). Efficacy and safety of exercise training in patients with chronic heart failure: Hf-action randomized controlled trial. Jama 301(14), 1439–1450.

- Pocock (1977) Pocock, Stuart J. (1977). Group sequential methods in the design and analysis of clinical trials. Biometrika 64(2), 191–199.

- Pocock (1997) Pocock, Stuart J. (1997). Clinical trials with multiple outcomes: a statistical perspective on their design, analysis, and interpretation. Controlled clinical trials 18(6), 530–545.

- Pocock and others (2012) Pocock, Stuart J, Ariti, Cono A, Collier, Timothy J and Wang, Duolao. (2012). The win ratio: a new approach to the analysis of composite endpoints in clinical trials based on clinical priorities. European heart journal 33(2), 176–182.

- Rauch and others (2014) Rauch, Geraldine, Jahn-Eimermacher, Antje, Brannath, Werner and Kieser, Meinhard. (2014). Opportunities and challenges of combined effect measures based on prioritized outcomes. Statistics in Medicine 33(7), 1104–1120.

- Redfors and others (2020) Redfors, Björn, Gregson, John, Crowley, Aaron, McAndrew, Thomas, Ben-Yehuda, Ori, Stone, Gregg W and Pocock, Stuart J. (2020). The win ratio approach for composite endpoints: practical guidance based on previous experience. European Heart Journal 41(46), 4391–4399.

- Scharfstein and others (1997) Scharfstein, D. O., Tsiatis, A. A. and Robins, J. M. (1997). Semiparametric efficiency and its implication on the design and analysis of group-sequential studies. 92, 1342–1350.

- Sharma and others (2020) Sharma, Abhinav, Pagidipati, Neha J, Califf, Robert M, McGuire, Darren K, Green, Jennifer B, Demets, Dave, George, Jyothis Thomas, Gerstein, Hertzel C, Hobbs, Todd, Holman, Rury R and others. (2020). Impact of regulatory guidance on evaluating cardiovascular risk of new glucose-lowering therapies to treat type 2 diabetes mellitus: lessons learned and future directions. Circulation 141(10), 843–862.

- Slud and Wei (1982) Slud, Eric and Wei, LJ. (1982). Two-sample repeated significance tests based on the modified wilcoxon statistic. Journal of the American Statistical Association 77(380), 862–868.

- van der Vaart (1998) van der Vaart, A. W. (1998). Asymptotic Statistics. Cambridge: Cambridge University Press.

- Wolter and Wolter (2007) Wolter, Kirk M and Wolter, Kirk M. (2007). Introduction to variance estimation, Volume 53. Springer.

Appendix

9 Variance for Derived Win-statistics

9.1 Variance of Win Ratio Statistics

In this subsection, we derive the asymptotic variance of the Win Ratio. The below derivation process follows a similar idea from Bergemann and others . First, we review the results of Taylor expansions for the moments of functions of random variables. Given and as the mean and the variance of a random variable , respectively. According to Wolter and Wolter (2007), the Taylor expansion of the expected value or first moment of can be found as

Suppose and the Taylor expansion of first moment of yields

Mentioned that there are tiny mistakes in Bergemann and others derivation of this part and we corrected them in our results. Then, we need to apply the results of Taylor’s expansion again to simplify the above results. Considering arbitrary two random variables , denote for random variable transformation of .

| (By Taylor expansion ) | ||||

Thus, we have the below approximation

Using above results, we can derive the approximation of For , we have

and also

9.2 Empirical Estimators of Variance

In this subsection, we present the consistent empirical estimators for , , , , and , which are key components of the variance for both the Win Ratio and Net Benefit. Firstly, the empirical estimators of and are given by their respective sample means, denoted as and . For , the estimator is defined as

which serves as a consistent estimator for .

Next, we derive the empirical estimators for covariance estimators. Firstly, we take as an example to illustrate its empirical estimator.

We have already proposed the consistent estimator for and respectively. Thus, the consistent estimator for is Denote

and the U-statistics with kernel is a consistent estimator for Thus, we proposed the consistent estimator for as

Similarly, consistent empirical covariance estimators for , and are

and

where

and

Here we plug in and with and as their corresponding empirical estimators. With these empirical estimators, empirical estimators for , and asymptotic variance-covariance as shown in Proposition 1 and 2 could be derived.

10 Proof of Lemma 1

The projection of onto Hilbert Space can be written as , where

| (10.1) | ||||

Firstly, let’s explore the term further. For given ,

-

•

if then .

-

•

if denote which is a function of and we have . To be noted, notation means that only the element of the treatment arm of is given with kernel function .

Similarly, we can ignore terms in when , since their values are zero. Denote which is a function of and we have Notation means that only element of control arm of is given. Thus the projection can be written as

| (10.2) |

Furthermore, based on Theorem 12.6 in van der Vaart (1998), the variance of projection of

| (10.3) |

Without loss of generality, we first show the asymptotic normality for the case when there are only 2 monitoring times in sequential design. As all go to we have the following asymptotic normality results by multivariate Central limit theorem:

and

It is obviously that random vectors and are mutually independent. Then for arbitrary constant vector and

where and are mutually independent normal distribution with and Thus, the joint distribution where Therefore, as all goes to

| (10.4) |

Then, it can be shown that

| (10.5) |

where

Owing to Slutsky’s Theorem as it applies to matrices and vectors, and considering that a linear transformation of a normal distribution remains normal in the limiting distribution, it follows that

| (10.6) |

where and the limit means taking the limit as all goes to By formula (10.5), variance-covariance matrix

To be noted, applying block multiplication on calculating make calculations simpler. For instance, we can partition dimensional matrix into, eight diagonal square matrices. Similarly, we also can partition dimensional matrix in to 16 squares matrices with dimension of

We can extend our proof of 2 times to the joint asymptotic normality for sequential monitoring times

| (10.7) |

Generally, represents the -dimensional multivariate normal distribution with a zero mean vector of size , and a symmetric variance-covariance matrix with the diagonal elements are 1. As for off-diagonal elements, and for , and we have

as and .

11 Proof of Theorem 1

is the projection of given by formula (3.3) for . We have shown that the form of with variance in formula (3.4). It is true that given Condition C1, as Specifically, by Theorem 11.2 from van der Vaart (1998) van der Vaart (1998),

for This indicates that the difference between the normalized forms of and converges to zero in probability. Additionally, it is evident that:

These findings, combined with Lemma 3.2, demonstrate that converges in distribution to a standard normal distribution, allow us to further deduce:

| (11.1) | ||||

for . This convergence in probability extends jointly to all estimators, leading us to conclude:

| (11.2) |

as , for . Building upon these results, we apply Slutsky’s Theorem on lemma 3.2. Given that for each and , we establish the asymptotic normality of our estimators:

| (11.3) |

as , for . This completes our proof for the asymptotic normality of the estimators.

12 Proof of Proposition 1

12.1 Proof of (1)

Consider two test statistics and computed from and subjects in the treatment group and and subjects in the control group at the two time points and , with .

If , then and this demonstrate that the independent increment assumption is met Kim and Tsiatis (2020).

| (12.1) | ||||

Thus, .

12.2 Proof of (2)

According to Theorem 1 in the main manuscript, sequential win statistics

where for and is a covariance-variance matrix. Considering the form of IPCW-adjusted sequential Net Benefit statistics where , we construct dimension matrix , such that .

| (12.2) | ||||

The block matrix approach is applied to , where each block is defined as

Similarly, applying the block matrix approach to , it is partitioned into matrices. Each block can be written as , where each block is given by

Denote as and for . where

By independent increment,

And, also we can simplify

Thus,

13 Proof of Proposition 2

13.1 Proof of part (1) of Proposition 2

Similarly setting with 10, consider two test statistics and computed from and subjects in the treatment group and and subjects in the control group at the two time points and , with .

If , then and this demonstrate that the independent increment assumption is met Kim and Tsiatis (2020). The below proof follows a similar idea from Bergemann et al. (2023) Bergemann and others .

As is shown in the derivation of in Appendix 9.1, we have the below approximation by Taylor expansion for moments of functions of random variables :

Given the above results,

| (By Taylor Expansion Results) | ||||

| (By Results from Lemma 1) |

Plugin the results above back to , we obtain

Thus,