Approximating Multiple Robust Optimization Solutions in One Pass via Proximal Point Methods

Abstract

Robust optimization provides a principled and unified framework to model many problems in modern operations research and computer science applications, such as risk measures minimization and adversarially robust machine learning. To use a robust solution (e.g., to implement an investment portfolio or perform robust machine learning inference), the user has to a priori decide the trade-off between efficiency (nominal performance) and robustness (worst-case performance) of the solution by choosing the uncertainty level hyperparameters. In many applications, this amounts to solving the problem many times and comparing them, each from a different hyperparameter setting. This makes robust optimization practically cumbersome or even intractable. We present a novel procedure based on the proximal point method (PPM) to efficiently approximate many Pareto efficient robust solutions at once. This effectively reduces the total compute requirement from to , where is the number of robust solutions to be generated, and is the time to obtain one robust solution. We prove this procedure can produce exact Pareto efficient robust solutions for a class of robust linear optimization problems. For more general problems, we prove that with high probability, our procedure gives a good approximation of the efficiency-robustness trade-off in random robust linear optimization instances. We conduct numerical experiments to demonstrate.

1 Introduction

One of the main obstacles in deploying robust optimization models for real-world decision-making under uncertainty is determining an appropriate trade-off between nominal performance and worst-case performance before the uncertainty is realized. For example, in portfolio optimization, setting the level of risk aversion is challenging. Similarly, in adversarial machine learning, choosing the adversarial perturbation set parameters to balance average accuracy versus accuracy under adversarial attacks is a critical decision. Decision makers often need to obtain and test multiple robust solutions, each corresponding to a different solution on the efficiency-robustness Pareto frontier, before deciding which one to deploy.

To obtain multiple robust solutions, decision makers adjust hyperparameters such as the shape and size (radius) of the uncertainty set (Soyster, 1973; Ben-Tal and Nemirovski, 1999; Bertsimas and Sim, 2004) or by employing globalized robust optimization approaches that use penalty functions and coefficient hyperparameters (Ben-Tal et al., 2006; 2009). Consequently, generating each robust solution demands solving a different instance of the robust optimization problem, which is generally more computationally expensive than solving their deterministic counterparts. For instance, adversarial training is more expensive than traditional training because it involves solving an inner maximization problem to find adversarial attacks. In theory, the robust counterpart of linear programs (LPs) with ellipsoidal uncertainty sets becomes second-order cone programs (SOCPs), and the robust counterpart of uncertain SOCPs becomes semidefinite programs (SDPs). As a result, finding the right robust solution can be prohibitively costly in practice, let alone finding many of them to compare.

To address this challenge, we propose a new way of thinking about this problem, along with a novel proximal point method (PPM)-based algorithm to approximate efficiency-robustness Pareto efficient robust solutions, reducing the computational cost from to , where is the number of different robust solutions on the Pareto frontier and is the cost of solving a single instance of a robust optimization problem. Specifically, the procedure first solves for the “most-robust” solution, then uses it as the starting point to perform proximal point updates towards the “least-robust” (deterministic counterpart) solution. We discover, intriguingly, the proximal point trajectory approximates the set of Pareto efficient robust solutions that we want to obtain in the first place.

We prove that for robust LPs with uncertain objective functions under the simplex decision domain and ellipsoidal uncertainty sets, the proximal point trajectory are exactly Pareto efficient robust solutions. For robust LPs with a random polyhedron domain, we prove that with high probability, the performances of the Pareto efficient robust solutions are bounded by the performances of two proximal point trajectories. To validate, we conduct numerical experiments at the end on portfolio optimization and adversarially robust deep learning.

2 Problem Setting and Main Idea

2.1 Notations

We denote the dual norm of as , defined as . The -norm, , is given by . The infinity norm, , is defined as . The ball of radius around with respect to the norm is represented by , and the ball of radius around the origin is denoted as . The projection operator onto the set is denoted as . Finally, represents a vector of ones.

2.2 Problem Setting

We start with a constrained optimization problem with parameters in the objective function:

The decision variable is subject to a compact and convex domain , is an uncertain vector, which is only known to belong to an uncertainty set . The robust counterpart is

| (1) |

where the uncertainty set takes the following form:

Here is some fixed nominal vector, can be interpreted as the perturbation, and is a nonempty compact convex set. In the case that is empty, (RC) reduces to a nominal optimization problem with no uncertainty:

Consequently, we define the efficient decision, as the optimizer to problem (P) and the robust decision, as the optimizer to problem (RC), i.e.,

For any , its efficiency, and robustness, is defined respectively as its performance under nominal or worst-case uncertainty defined as

It is easy to verify that the following inequalities hold

In practice, the trade-off between the efficiency and robustness of robust solutions can be controlled by adjusting the size of the uncertainty set. Specifically, we define an efficiency-robustness Pareto efficient robust solution with a nonempty compact convex uncertainty set such that as

For instance, under norm-ball uncertainty sets, we define the set of efficiency-robustness Pareto efficient robust solutions as the set of robust solutions generated while adjusting the radius of the norm-ball uncertainty set:

Comparing with existing notions of Pareto efficiency of robust solutions (Iancu and Trichakis (2014)) which requires no other robust solutions that perform as least as well across all uncertainty realizations and better for some uncertainty realizations, we relax the requirement and trade-off worst-case performance with the performance under a nominal uncertainty realization.

2.3 Main Idea

If the uncertainty set radius for is set too large, then a solution of (RC) tends to be overly conservative and gives bad average case performance, i.e., low . If the radius is set too small, then the solution may not perform reliably under large out-of-sample perturbations or adversarial attacks , i.e., resulting in low . What is the right ?

Existing literature (Mohajerin Esfahani and Kuhn (2018); Blanchet et al. (2019b; a)) points to ways to choose based on statistical theory, using observed perturbation data to estimate . But in practice, we may not have any data about . Even if we do, such designs are known in the robust optimization community to be overly conservative. The only practical option is to solve the problem (RC) many times, each with a different , and compare the solutions in terms of their average case and worst-case performances.

Our main contribution is proposing a completely new way of thinking about this problem. Instead of solving (RC) times where is the number of solutions we want to compare, we can approximate these Pareto efficient robust solutions within two algorithmic passes. The first pass is to obtain a robust solution for (RC) with a large value . Then we use as the initial point of an iterative (proximal point) algorithm, to solve for the problem (RC) with (i.e., the nominal problem (P)). The intermediate iterates for provide a reasonable, sometimes perfect, representation of the Pareto efficient robust solutions.

3 Technical Preliminaries

3.1 Generalized Proximal Point Methods and The Central Paths

Here we introduce the generalized proximal point method and the central path for the nominal problem (P). Importantly, we introduce a preliminary result toward the proof of our main theorem, which is the equivalence between the sequence generated by the proximal point method for a linear problem (P) and the central path of the linear problem (P).

We begin with the introduction of the generalized proximal point method where a Bregman distance is in place of the usual Euclidean distance. First, we define the Bregman distance. We assume the distance-generating function satisfies the following technical assumptions:

-

A1.

is strictly convex, closed, and continuously differentiable in .

-

A2.

If is a sequence in which converges to a point in the boundary of , and is any point in , then .

The Bregman distance w.r.t. is defined as

Example 1.

-

•

Let , then .

-

•

Let , then .

Let , the generalized proximal point method for solving the problem (P) generates a sequence as

where satisfies .

The central path of the problem (P) with barrier function induced by the Bregman distance as is defined as and

The following result states for a linear problem (P), the proximal point method sequence and the central path are equivalent.

Proposition 1 (Theorem 3 in Iusem et al. (1999)).

For problem (P) with linear objective functions and a closed and convex polyhedron domain, . Assume that satisfies A1 and A2. Let by the central path of the problem (P) w.r.t. and let be the proximal point method sequence for the problem (P) with Bregman distance . If the sequence is defined as

then

3.2 Correspondence between Robust Optimization and Risk Measure Minimization

Our analysis also draws from the deep connection between robust optimization and risk measure minimization. Specifically, it has been shown that risk measures can be mapped explicitly to robust optimization uncertainty sets and vice versa (Natarajan et al. (2009); Bertsimas and Brown (2009)). In particular, we utilize the following correspondence between the robust optimization ellipsoidal uncertainty set and the mean-standard deviation risk measure.

Lemma 1 (Correspondence between Ellipsoidal Robust Linear Optimization and and Mean-Variance Risk Minimization).

Under some closed convex polyhedron domain and ellipsoidal uncertainty set where is a symmetric matrix, The robust optimization problem

| (2) |

is equivalent to the following mean-standard deviation risk measure minimization problem

| (3) |

4 Theory: Equivalence between the Pareto efficient Robust Solutions and the Proximal Point Method Trajectory

In this section, we show that under the simplex domain and ellipsoidal uncertainty set, a set of Pareto efficient robust solutions to uncertain linear optimization problems with uncertainty in the objective function can be obtained exactly as a proximal point method trajectory. Further, for random problem instances with random polyhedron domains, we show that the performances of the Pareto efficient solutions are bounded probabilistically in between the performances of two proximal point method trajectories. The main implication of our result is the following: instead of solving a different instance of a robust optimization problem to arrive at each solution on the efficiency-robustness Pareto frontier, an entire “menu” of solutions on the efficiency-robustness Pareto frontier can be obtained approximately, under some condition exactly in a single pass via gradient methods.

4.1 Exact Result: Simplex Domain and Ellipsoidal Uncertainty Set

We first consider the case of Pareto efficient robust solutions to robust linear optimization problems with uncertain objective functions under the simplex domain and ellipsoidal uncertainty sets. We show a proximal point sequence is contained within the set of Pareto efficient robust solutions. In particular, we have the following theorem.

Theorem 1 (Correspondence Between Pareto-Efficiency Robust Solutions and the Proximal Point Trajectory).

Under linear objective functions, . Let be the set of Pareto efficient robust solutions under simplex domain and ellipsoidal uncertainty set where satisfies . Let be the proximal point sequence w.r.t. , associated with sequence and starting point . If the sequence is defined as

and let be such that . Then

4.2 Implication of Theorem 1

Theorem 1 inspires an efficient algorithm for generating multiple (approximate) Pareto efficient robust solutions in two passes: first, solve the robust problem (RC) for ; second, solve the nominal problem (P) with proximal point method initialized with , finally the trajectory of the proximal point method are approximate Pareto efficient robust solutions. Specifically, we present the following algorithms.

For linear objective functions, the proximal point method updates are reduced to vanilla gradient descent updates. For general objective functions beyond linear functions, performing the proximal point method may not be computationally affordable. In practice, the proximal point method can be approximated by computationally cheap extra-gradient and optimistic gradient methods (Mokhtari et al. (2020)). In Section 5, we demonstrate the empirical performance of Algorithm 1 for general problems where the conditions for our exact results in Theorem 1 no longer hold.

4.3 Proof of Theorem 1

Theorem 1 follows by the combination of Proposition 1, 2 and 3, which together show the notions of proximal-point sequences, central path, mean-variance risk minimization solutions and Pareto efficient robust solutions all coincide under simplex domain and ellipsoidal uncertainty set. Here we present Proposition 2 and 3.

Proposition 2 (Correspondence between Mean-Variance Risk Minimization Solutions and the Central Path).

Under simplex domain , assume the covariance matrix of the returns satisfies , Let the set of Pareto efficient solutions to the mean-variance risk measure minimization problem be

Let the central path be

where which is induced by and is the minimum variance solution defined as . Then

Proposition 3 (Correspondence Between Pareto-Efficiency Robust Solutions and the Central Path).

Under simplex domain and ellipsoidal uncertainty set where satisfies , let the Pareto efficient robust solutions be

Let the central path be

where which is induced by and . Let be such that . Then

4.4 Probabilistic Performance Bound: Random Polyhedron Domain and Ellipsoidal Uncertainty Set

To extend the result to more general domains beyond simplex domains. In this subsection, we show that under ellipsoidal uncertainty sets, the performance (measured by efficiency and robustness) of the Pareto efficient robust solutions with random polyhedron domains with constraint coefficients generated i.i.d. from bounded distributions are bounded between the performance of two sets of Pareto efficient robust solutions with two simplex domains with a small scaling factor, hence by Theorem 1, between the performance of two proximal point trajectories with high probability.

We denote the Pareto efficient robust solution with domain and ellipsoidal uncertainty set as

Alternatively, we define

where we assume is chosen such that .

Corollary 4.

Consider a random polyhedron , where and are i.i.d. according to a bounded distribution with support and for all . Define simplex . Then for all ,

where .

4.5 Multiple Uncertain Constraints

In this subsection, we extend the result to robust linear optimization problems with multiple uncertain linear constraints. We show that under uncertain linear constraints, the Pareto efficient robust solutions can be obtained by solving a set of saddle point problems. Specifically, we study the following problem

where is the uncertainty set for uncertain parameter in constraint for all . We assume the constraints share the same ellipsoidal uncertainty set, i.e., . Consequently, the Pareto efficient robust solutions are the set

where

In general, the conventional approach for solving for a Pareto efficient robust solution requires dual reformulation of the robust constraints resulting in a computationally harder problem than the deterministic counterpart. Our next result shows for the specific problem setting of (RCWUC), its Pareto efficient robust solutions can be obtained by solving a set of saddle-point problems via gradient descent-ascent-like methods.

Proposition 5.

is equal to a set of saddle-point solutions where

The proof of Proposition 5 is presented in Appendix B. As a result of Proposition 5, a set of approximate Pareto efficient robust solutions can be obtained by running the following algorithm for a set of values.

5 Performance of Algorithm 1: Numerical Studies

In this section, we present two experiments testing the empirical performance of generating a set of approximate efficiency-robustness Pareto efficient robust solutions via Algorithm 1.

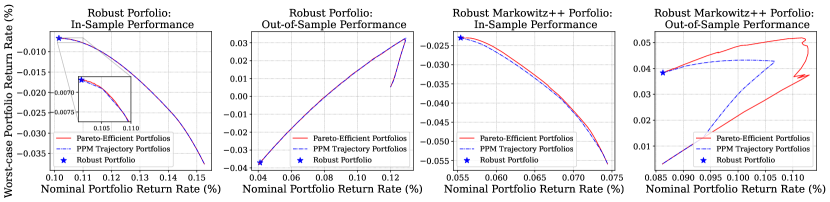

5.1 Robust Portfolio Optimization

Robust Portfolio Optimization. In portfolio optimization, we are concerned with constructing a portfolio as a convex combination of stocks. The returns of the stocks are modeled by a random vector, . We assume that from historical data, we estimated the expectation and the covariance matrix of to be and . In the robust approach to the problem, we assume the realization of the uncertain return lies within an uncertainty set which we design as an ellipsoidal uncertainty set . Our objective is to choose the portfolio weight that minimizes the worst-case loss (or equivalently maximizes the worst-case return) under a simplex domain, leading to the following robust portfolio optimization problem,

As a consequence of Lemma 3, (RPO) is equivalent to the classic mean-standard deviation risk measure minimization problem,

To further test the performance of algorithm 1 beyond the simplex domain required for our exact result in Theorem 1, we also consider the extended Markowitz model (Markowitz++) proposed by Boyd et al. (2024) with additional practical constraints and objective terms corresponding to e.g., shorting, weight limits, cash holding/borrowing constraints and costs. The detailed formulation of the Markowitz++ portfolio problem is in Appendix C.

Experiment design. We first construct portfolios with in-sample historical stock return data, before testing the nominal and worst-case returns of each portfolio on out-of-sample stock return data. As the benchmark, we first construct exact Pareto efficient robust portfolios by solving exactly the problem (RPO)/Markowitz++ under various levels of . Then we deploy algorithm 1 to generate approximate Pareto efficient robust portfolios, i.e., we use the (RPO)/Markowitz++ portfolio with the largest to initialize the PPM method for solving the nominal portfolio optimization problem with , the PPM trajectory are approximate Pareto efficient robust portfolios. Specifically, we choose our decision space as stocks from SP 500 companies. We use the historical daily return data of the 20 stocks over 3 years (from 2021-01-01 to 2023-12-30) and estimate the moment information and as our in-sample data for constructing portfolios; the assumed unseen future daily return of the 20 stock for the next 8 months (from 2024-01-01 to 2024-08-01) are used to estimate and which serve as our out-of-sample data for evaluating the nominal and worst-case returns of each portfolio.

Results. The result is shown in figure 1. For the vanilla robust portfolio problem (RPO), although the assumption in Theorem 1 is not satisfied in this experiment, the performance of PPM method generated portfolios matches closely to that of the exact Pareto efficient robust portfolios. For the Markowitz++ portfolio problem, the domain further deviates from our simplex requirement for the exact result in Theorem 1, algorithm 1 still produces good approximate Pareto efficient robust portfolios. At the same time, the computation cost of solving multiple (RPO) problems with various levels of is reduced to solving the most robust (RPO) problem and solving the nominal problem by performing PPM updates.

5.2 Adversarially Robust Deep Learning

| Method | Cost per Pareto efficient robust network (min) | Cost to generate Pareto efficient robust networks (min) |

|---|---|---|

| Algorithm 1 with ExtraFullGD | ||

| FGSM (Wong et al. (2020)) |

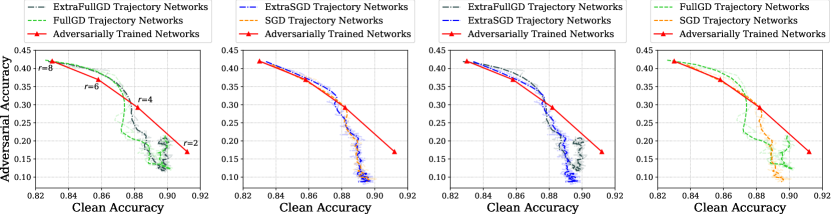

In this subsection, we present experiment results that evaluate the performance of our PPM-based procedure (Algorithm 1) for efficiently generating multiple adversarially robust neural networks trading-off clean accuracy (test accuracy with a clean test set) with adversarial accuracy (test accuracy with a test set under adversarial perturbations).

Adversarial training as robust optimization. The goal in adversarially robust deep learning is to learn networks that are robust against adversarial attacks (i.e., perturbations on the input examples that aim to deteriorate the accuracy of classifiers). A common strategy to robustify networks is adversarial training, which can be formulated as the following robust optimization problem,

| (8) |

where is the distribution generating pairs of examples and labels , is a neural network parameterized by , is the perturbation with perturbation set , and is the lost function. Typically, the perturbation set is designed as norm-balls, whose size can be controlled via the radius parameter, . Naturally, we can apply our framework and define a clean accuracy-adversarial accuracy Pareto efficient robust networks as networks adversarially trained under different levels of perturbation set radius, . The trade-off between clean accuracy and adversarial accuracy in adversarially robust deep learning has been observed empirically Wang et al. (2020); Su et al. (2018) and studied theoretically Raghunathan et al. (2020); Tsipras et al. (2019); Pang et al. (2022). In practice, given the nonconvex-nonconcave loss function, the adversarial training is solved approximately via iteratively performing the following: first approximately solving the inner maximization problem, followed by gradient method update on the parameter (Madry et al. (2018)).

Experiment design. As the benchmark for algorithm 1, we first adversarially train networks under different perturbation set radius, to learn a set of clean accuracy-adversarial accuracy Pareto efficient robust networks. Then we run Algorithm 1 by performing standard training but with the key difference of initializing the network parameter with the parameter of the most robust network (i.e., the adversarially trained network with the largest ). Finally, the output of Algorithm 1, i.e., the standard training parameter sequence with robust parameter initialization, corresponds to a set of approximate clean accuracy-adversarial accuracy Pareto efficient robust networks.

Specifically, we use the CIFAR10 dataset, a PreAct ResNet18 architecture, and the cross entropy loss. The set of Pareto efficient robust networks are adversarially trained using fast gradient sign method (FGSM) with random initialization and fast training methods (Wong et al. (2020)) (shown to be as effective as projected gradient descent (PGD)-based training but with a much lower cost) and norm ball perturbation sets, , with in . The Algorithm 1 is initialized with the parameter of the adversarially trained network with perturbation sets , after initialization, four variants of the standard training are performed with the following gradient methods: 1) Vanilla stochastic gradient descent (SGD); 2) Stochastic extra gradient descent (ExtraSGD); 3) Gradient descent with the gradient of the full train set (FullGD); 4) Extra gradient descent with the gradient of the full train set (ExtraFullGD). The implementation for extra gradient descent is adopted from Gidel et al. (2019). Each variant can be considered as an approximation to PPM in Algorithm 1, where ExtraSGD is a better approximation to PPM than SGD, and ExtraFullGD is a better approximation to PPM than ExtraSGD. SGD and ExtraSGD have a learning rate of ; FullGD and ExtraFullGD have a learning rate of . The four variants of the standard training are each performed for 100 epochs, generating one approximate Pareto efficient robust network per epoch. The trajectories of four variants of the standard training are each a set of approximate clean accuracy-adversarial accuracy Pareto efficient robust networks. Finally, all networks’ clean accuracy and adversarial accuracy are evaluated correspondingly on a clean test set and on an adversarial test set with PGD attacks.

Results. The results evaluating the performance of our PPM-based procedure for generating approximate clean (test) accuracy-adversarial (test) accuracy Pareto efficient robust networks are shown in Figure 2. The networks generated by our gradient method trajectories initially approximate/surpass both the clean and adversarial accuracy of adversarially trained networks with perturbation set radius, in , before generating networks with both lower clean and adversarial accuracy that than of adversarially trained network with . The initial approximation/surpassing in performance against adversarially trained networks shows our procedure can generate adversarially robust networks as effective as traditional adversarial training. The later drop in performance is mainly contributed by the low learning rate, although tuning the gradient methods is not the focus of our paper, it opens up future works for investigating the gradient method designs in Algorithm 1 that can improve upon our current approximates using constant learning rates. Comparing the performance across the four trajectories corresponding to the four gradient method variants, using the full gradient of the training set improves both clean and adversarial accuracy against using the stochastic gradient; extra gradient improves both the clean and adversarial accuracy against the vanilla gradient, with the ExtraFullGD trajectory generated networks having the best performance amount the four sets of networks. This result is as expected since ExtraFullGD is the best approximation for PPM.

The computation cost result in Table 1 shows our PPM-based procedure reduces the computation cost of generating Pareto efficient robust networks from to , where is the cost of a single adversarial training. Specifically, algorithm 1 generates a set of approximate Pareto efficient robust networks with the cost of a single pass of adversarial training (costing 15.12 minutes) plus a single pass of standard training with robust parameter initialization for epochs (costing minutes, where each epoch of standard training costs minutes, and one approximate Pareto efficient robust network is generated per epoch).

References

- Ben-Tal and Nemirovski (1999) A. Ben-Tal and A. Nemirovski. Robust solutions of uncertain linear programs. Operations Research Letters, 25:1–13, 8 1999. ISSN 01676377. doi: 10.1016/S0167-6377(99)00016-4.

- Ben-Tal et al. (2006) Aharon Ben-Tal, Stephen Boyd, and Arkadi Nemirovski. Extending scope of robust optimization: Comprehensive robust counterparts of uncertain problems. Mathematical Programming, 107:63–89, 6 2006. ISSN 0025-5610. doi: 10.1007/s10107-005-0679-z.

- Ben-Tal et al. (2009) Aharon Ben-Tal, Laurent El Ghaoui, and Arkadi Nemirovski. Robust Optimization. Princeton University Press, 1 edition, 2009.

- Bertsimas and Brown (2009) Dimitris Bertsimas and David B. Brown. Constructing uncertainty sets for robust linear optimization. Operations Research, 57(6):1483–1495, 2009. doi: 10.1287/opre.1080.0646. URL https://doi.org/10.1287/opre.1080.0646.

- Bertsimas and Sim (2004) Dimitris Bertsimas and Melvyn Sim. The price of robustness. Operations Research, 52:35–53, 2 2004. ISSN 0030-364X. doi: 10.1287/opre.1030.0065.

- Blanchet et al. (2019a) Jose Blanchet, Yang Kang, and Karthyek Murthy. Robust wasserstein profile inference and applications to machine learning. Journal of Applied Probability, 56(3):830–857, 2019a. doi: 10.1017/jpr.2019.49.

- Blanchet et al. (2019b) Jose Blanchet, Yang Kang, Karthyek Murthy, and Fan Zhang. Data-driven optimal transport cost selection for distributionally robust optimization. In 2019 Winter Simulation Conference (WSC), pages 3740–3751, 2019b. doi: 10.1109/WSC40007.2019.9004785.

- Boyd et al. (2024) Stephen Boyd, Kasper Johansson, Ronald Kahn, Philipp Schiele, and Thomas Schmelzer. Markowitz portfolio construction at seventy, 2024. URL https://arxiv.org/abs/2401.05080.

- El Housni and Goyal (2017) Omar El Housni and Vineet Goyal. Beyond worst-case: A probabilistic analysis of affine policies in dynamic optimization. In I. Guyon, U. Von Luxburg, S. Bengio, H. Wallach, R. Fergus, S. Vishwanathan, and R. Garnett, editors, Advances in Neural Information Processing Systems, volume 30. Curran Associates, Inc., 2017. URL https://proceedings.neurips.cc/paper_files/paper/2017/file/01a0683665f38d8e5e567b3b15ca98bf-Paper.pdf.

- Gidel et al. (2019) Gauthier Gidel, Hugo Berard, Gaëtan Vignoud, Pascal Vincent, and Simon Lacoste-Julien. A variational inequality perspective on generative adversarial networks. In International Conference on Learning Representations, 2019. URL https://openreview.net/forum?id=r1laEnA5Ym.

- Iancu and Trichakis (2014) Dan A. Iancu and Nikolaos Trichakis. Pareto efficiency in robust optimization. Management Science, 60:130–147, 1 2014. ISSN 0025-1909. doi: 10.1287/mnsc.2013.1753.

- Iusem et al. (1999) Alfredo N. Iusem, B. F. Svaiter, and João Xavier da Cruz Neto. Central paths, generalized proximal point methods, and cauchy trajectories in riemannian manifolds. SIAM Journal on Control and Optimization, 37(2):566–588, 1999. doi: 10.1137/S0363012995290744. URL https://doi.org/10.1137/S0363012995290744.

- Madry et al. (2018) Aleksander Madry, Aleksandar Makelov, Ludwig Schmidt, Dimitris Tsipras, and Adrian Vladu. Towards deep learning models resistant to adversarial attacks. In International Conference on Learning Representations, 2018. URL https://openreview.net/forum?id=rJzIBfZAb.

- Mohajerin Esfahani and Kuhn (2018) Peyman Mohajerin Esfahani and Daniel Kuhn. Data-driven distributionally robust optimization using the Wasserstein metric: performance guarantees and tractable reformulations. Mathematical Programming, 171(1):115–166, 2018. ISSN 1436-4646. doi: 10.1007/s10107-017-1172-1. URL https://doi.org/10.1007/s10107-017-1172-1.

- Mokhtari et al. (2020) Aryan Mokhtari, Asuman Ozdaglar, and Sarath Pattathil. A unified analysis of extra-gradient and optimistic gradient methods for saddle point problems: Proximal point approach. In Silvia Chiappa and Roberto Calandra, editors, Proceedings of the Twenty Third International Conference on Artificial Intelligence and Statistics, volume 108 of Proceedings of Machine Learning Research, pages 1497–1507. PMLR, 26–28 Aug 2020. URL https://proceedings.mlr.press/v108/mokhtari20a.html.

- Natarajan et al. (2009) Karthik Natarajan, Dessislava Pachamanova, and Melvyn Sim. Constructing risk measures from uncertainty sets. Operations Research, 57(5):1129–1141, 2009. doi: 10.1287/opre.1080.0683. URL https://doi.org/10.1287/opre.1080.0683.

- Pang et al. (2022) Tianyu Pang, Min Lin, Xiao Yang, Jun Zhu, and Shuicheng Yan. Robustness and accuracy could be reconcilable by (Proper) definition. In Kamalika Chaudhuri, Stefanie Jegelka, Le Song, Csaba Szepesvari, Gang Niu, and Sivan Sabato, editors, Proceedings of the 39th International Conference on Machine Learning, volume 162 of Proceedings of Machine Learning Research, pages 17258–17277. PMLR, 17–23 Jul 2022. URL https://proceedings.mlr.press/v162/pang22a.html.

- Raghunathan et al. (2020) Aditi Raghunathan, Sang Michael Xie, Fanny Yang, John C. Duchi, and Percy Liang. Understanding and mitigating the tradeoff between robustness and accuracy. In Proceedings of the 37th International Conference on Machine Learning, ICML’20. JMLR.org, 2020.

- Soyster (1973) A. L. Soyster. Technical note—convex programming with set-inclusive constraints and applications to inexact linear programming. Operations Research, 21:1154–1157, 10 1973. ISSN 0030-364X. doi: 10.1287/opre.21.5.1154.

- Su et al. (2018) Dong Su, Huan Zhang, Hongge Chen, Jinfeng Yi, Pin-Yu Chen, and Yupeng Gao. Is robustness the cost of accuracy? – a comprehensive study on the robustness of 18 deep image classification models. In Vittorio Ferrari, Martial Hebert, Cristian Sminchisescu, and Yair Weiss, editors, Computer Vision – ECCV 2018, pages 644–661, Cham, 2018. Springer International Publishing. ISBN 978-3-030-01258-8.

- Tsipras et al. (2019) Dimitris Tsipras, Shibani Santurkar, Logan Engstrom, Alexander Turner, and Aleksander Madry. Robustness may be at odds with accuracy. In International Conference on Learning Representations, 2019. URL https://openreview.net/forum?id=SyxAb30cY7.

- Wang et al. (2020) Yisen Wang, Difan Zou, Jinfeng Yi, James Bailey, Xingjun Ma, and Quanquan Gu. Improving adversarial robustness requires revisiting misclassified examples. In International Conference on Learning Representations, 2020. URL https://openreview.net/forum?id=rklOg6EFwS.

- Wong et al. (2020) Eric Wong, Leslie Rice, and J. Zico Kolter. Fast is better than free: Revisiting adversarial training. In International Conference on Learning Representations, 2020. URL https://openreview.net/forum?id=BJx040EFvH.

Appendix A Proofs of Results in Section 3

Proof of Lemma 3. Denote ,

Appendix B Proofs of Results in Section 4

Lemma 2.

Assume ,

Proof. By KKT condition,

denote we have,

Given , we have

Finally, by ,

hence, .

Proof of Proposition 2. For all we have

where the fourth equality is by Lemma 2, and the fifth equality is due to .

Proof of Proposition 3. The result is a direct consequence of Lemma 3 and Proposition 2.

The second equality is due to Lemma 3, the fourth equality is by Proposition 2, and finally the fifth equality follows from Lemma 3.

Our performance bound in corollary 4. builds on the following result that a random polyhedron with constraint coefficients generated i.i.d. according to bounded distributions is sandwiched between two simplices with high probability.

Lemma 3 (Theorem 2.1. in El Housni and Goyal [2017]).

Consider a random polyhedron , where and are i.i.d. according to a bounded distribution with support and for all . Define simplex . Then

where .

By the monotonicity of ,

where

Applying the method of Lagrangian, can reformulated as the solution to the following saddle-point problem

Appendix C Markowitz++

The Markowitz++ proposed by Boyd et al. [2024] extends the classical Markowitz Portfolio by introducing practical constraints and objective terms. In the experiment, we include the option for shorting, holding limits on each asset, the option for cash holding/borrowing, and the associated costs. The formulation of the Markowitz++ problem is shown below,

| (14a) | ||||

| s.t. | (14b) | |||

| (14c) | ||||

| (14d) | ||||

The decision variables are stock weights ( for holding, for shorting), is the cash weight ( denotes diluting the portfolio with cash, denotes borrowing). The objective function now includes the additional term of holding costs, as defined by equation (5) in Boyd et al. [2024] and weighted by the parameter . The first constraint enforces all weights sum to one, the second constraint corresponds to the maximum shorting position and maximum holding position on each asset, and the last constraint applies lower and upper limits on the cash weight. Finally, the nominal and worst-case return trade-off is controlled by adjusting the parameter, .