\toolName: Monitoring and Identifying Attacks in Cross-Chain Bridges

Abstract

Cross-chain bridges are widely used blockchain interoperability mechanisms. However, several of these bridges have vulnerabilities that have caused 3.2 billion dollars in losses since May 2021. Some studies have revealed the existence of these vulnerabilities, but little quantitative research is available, and there are no safeguard mechanisms to protect bridges from such attacks. We propose \toolName, the first mechanism for monitoring bridges and detecting attacks against them. \toolName relies on a cross-chain model powered by a Datalog engine, designed to be pluggable into any cross-chain bridge. Analyzing data from the Ronin and Nomad bridges, we successfully identified the transactions that led to losses of $611M and $190M USD, respectively. \toolName not only uncovers successful attacks but also reveals unintended behavior, such as 37 cross-chain transactions () that these bridges should not have accepted, failed attempts to exploit Nomad, over $7.8M locked on one chain but never released on Ethereum, and $200K lost due to inadequate interaction with bridges. We provide the first open-source dataset of 81,000 s across three blockchains, capturing $585M and $3.7B in token transfers in Nomad and Ronin, respectively.

1 Introduction

In recent years, there has been a remarkable adoption of blockchain interoperability through the use of cross-chain protocols [30, 37]. The most popular cross-chain protocols are cross-chain bridges (or simply bridges ). Bridges connect decentralized applications across various blockchains, facilitating the transfer and exchange of data and assets between heterogeneous blockchains [37]. A special type of bridge, called canonical or native bridges, support rollups, a form of layer two (L2) mechanism, by providing liquidity from a source bride (e.g., Ethereum) to the rollup (e.g., Optimism) [48, 16, 2, 1, 11].

The cross-chain ecosystem is growing. During 2023, cross-chain protocols raised more than half a billion USD in investment rounds [39, 41, 42, 52, 57, 28], and processed millions of cross-chain transactions () daily [27]. In February 2024, non-native cross-chain bridges had a total value locked (TVL) of around 8 billion USD [9] and native bridges 36 billion USD, highlighting the growing interest in the technology, despite its numerous hacks: from May 2021 to August 2024, hackers stole a staggering amount of 3.2 billion USD in cross-chain protocols [30], and have caused losses of several tens of millions in other Decentralized Finance (DeFi) protocols indirectly impacted by them [15].

Not even extensively audited bridges are immune to vulnerabilities [27]. Also, several bridges have been exploited multiple times [59, 25, 32, 17, 18, 51, 14, 29, 56, 23]. On the other hand, the collapse of DeFi protocols can affect different ecosystems, as bridges interconnect them [65, 36]. An additional highlight from existing studies is that protocols take too long to react to an attack [18, 23, 31], suggesting that teams may not be sufficiently prepared to address integrity breaches, possibly due to lack of prior awareness, observability, monitoring, or good SecOps practices [30]. In the most recent attack, which targeted the Ronin bridge in August 2024, the team reported that the bridge was paused roughly 40 minutes after the first on-chain activity was spotted [56]. Establishing effective incident response frameworks is crucial for swift and efficient identification and response to malicious activity, minimizing losses, and improving attacker identification.

Some authors have studied cross-chain security, listing and systematizing vulnerabilities and attacks across the relevant layers of cross-chain [45, 43, 60, 64, 63, 30]. However, quantitative studies with real-world data are still lacking. Furthermore, there is a lack of safeguard mechanisms to protect bridges from such attacks due to the associated challenges. Variations in contract implementations, security models, and token types across different chains make it difficult to monitor and safeguard these systems consistently. Additionally, the use of intermediary protocols and the extraction of data from various sources (e.g., transaction data or events emitted by contracts) increase the challenge. The semantics of cross-chain protocols are rooted in multiple factors, such as the bridging model or the assets being transferred/exchanged, which are composed of data from outside a single blockchain. To capture this complexity, we leverage the concept of cross-chain model [35], powered by a Datalog engine [40]. A cross-chain model captures the necessary security properties of a bridge (in terms of integrity, accountability, and availability [30]). In short, we formalize the expected behavior of the bridge through cross-chain rules (model), and compare it to real-world activity (fitness) to identify deviations. Deviations may take two forms: malicious behavior (attack) or unintended behavior.

We bridge the gaps mentioned above by providing the first quantitative study on cross-chain security. This paper has the following main contributions:

-

•

\toolName, a pluggable monitoring and detection mechanism powered by a cross-chain model. A Datalog engine identifies deviations from expected behavior defined in terms of cross-chain rules written in Datalog.

-

•

The first empirical analysis backed by data on the vulnerabilities of cross-chain bridges and user practices. We release the first open-source dataset of cross-chain transactions, consisting of over 81,000 s.

The paper is structured as follows. Section 2 covers preliminary information on blockchain, smart contracts, and Datalog. Section 3 gives an overview of the cross-chain bridge and network model. Section 4 details the design of \toolName. Section 5 presents the empirical results of deploying \toolName in two bridges. Section 6 outlines the discussion and limitations. Finally, the related work and conclusions are given in Sections 7 and 8.

2 Background

We provide an overview of the necessary background to understand the remainder of this paper.

2.1 Blockchain and Smart Contracts

Consider a blockchain a sequence of blocks , where is the nth block such that each is cryptographically linked to . Each block contains a root of the current state trie, which contains the state of the blockchain, represented as key-value pairs . Each key represents an account – either an Externally Owned Account (EOA) controlled by a cryptographic key pair or a Contract Account. The latter contain code that enforce the so-called smart contracts, that execute in the native virtual machine of the blockchain – e.g., the Ethereum Virtual Machine (EVM).The execution of in changes the state . Examples of state changes include triggering the execution of smart contracts or actions natively supported by the blockchain, such as transferring native currency or triggering internal transactions (that can recursively trigger additional state changes). Smart contracts enable the execution of code, which can define tokens – by following common interfaces, such as the ERC-20 or ERC-721 – or arbitrary logic, such as validating Merkle proofs or digital signatures. Code execution may emit events that can be understood as execution logs (also called topics in the context of transaction receipts). Events emitted in the context of a network are referred to as local events.

2.2 Cross-Chain Model

A cross-chain model contains a set of cross-chain rules that evaluate incoming local events from multiple domains (e.g., networks) [35]. The data in these events is merged with additional context – e.g., domain IDs, global temporal markers, or asset valuations – to form cross-chain events. A collection of cross-chain events from multiple domains represents state transitions across them, collectively forming a cross-chain transaction (). To validate a , individual events are verified against cross-chain rules that define the expected behavior.

2.3 Datalog

This paper proposes defining a cross-chain model as a Datalog program. Such a program comprises a finite set of facts and rules [40]. Both are represented as Horn clauses in the form , where is the head of the clause; is the body; and each is a predicate with arguments . The arguments can be variables or constants. Additional predicates can enforce conditions or constraints on these arguments. A Datalog fact asserts a predicate that is true about the world. Technically, it is a special kind of clause that does not have a body. We define cross-chain rules as Datalog rules by decomposing them into relevant predicates that encapsulate cross-chain events. All facts are created based on the bridge-related data extracted from the underlying blockchains. Datalog has been widely used to perform analysis on large datasets of on-chain data; some examples are smart contract code analysis [44] and EVM execution trace analysis [54].

To illustrate our idea, consider a basic scenario. Consider a cross-chain transaction that involves two local transactions, and , occurring on blockchains A and B, respectively. According to the lock-unlock paradigm [37, 38] must be deemed valid only if is finalized in A. To model this example using a Datalog rule, we define the following predicates: Transaction(chain_id, tx_hash, ts) that represents a transaction with hash tx_hash in blockchain with ID chain_id, included in a block with timestamp timestamp_tx; LockAsset(asset_id, tx_hash) and UnlockAsset(asset_id, tx_hash) that define that an asset with asset_id has been, respectively, locked/minted in a transaction with hash tx_hash. In the example, we assume as the finality parameter of A in seconds. The Datalog rule is in Listing 1.

3 System and Network Models

In this section, we present the proposed cross-chain bridge model, the network model, and the technical challenges associated with securing bridges.

3.1 Cross-Chain Bridge Model

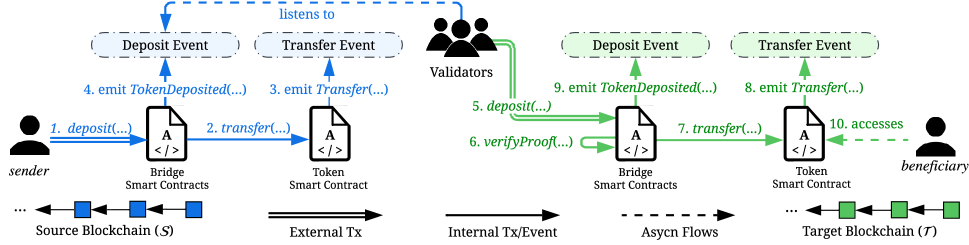

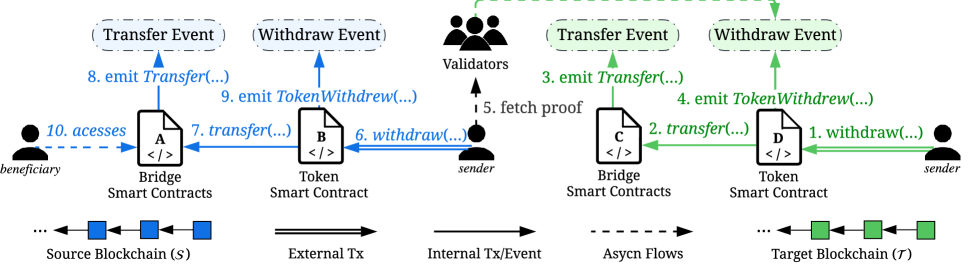

Cross-chain bridges are decentralized applications (dApps) that solve the interoperability problem across blockchains [36]. Contrary to most DeFi dApps, these dApps span over two or more blockchains, rather than being confined to one. Figure 2 illustrates the components that make up a cross-chain bridge, showing a source chain () and a target chain () with a one-way flow for token deposits. This process begins with the user issuing a Deposit transaction***we exemplify our model with the lock-unlock paradigm. Still, the mint-burn paradigm could also be used. on , where user funds are escrowed by being transferred to a bridge contract . This triggers the emission of events by each contract and . Then, entities of the bridge that listen to these events (validators) issue the corresponding Deposit transaction on . It releases the same amount of funds to the beneficiary’s address after verifying that the transfer is valid . This generates events and . The user can access their tokens by interacting with the corresponding token contract . The withdrawal process is similar (so it is not represented for simplicity): the user initiates a transaction on to escrow funds, followed by a transaction on releasing the same amount of funds to the beneficiary’s address. A key difference is that the user (or an off-chain party called relayer, a service that a bridge can offer) triggers the final transaction on the source chain during withdrawals. This process contrasts with the deposit process, which is managed by validators.

3.2 Network Model

Similarly to previous works [30, 33], we assume that the blockchains underlying a cross-chain bridge are live and safe [47, 50]. This means the attacks studied in this paper are performed at the protocol level. Consider the last block broadcasted in blockchain as . Thus, there is , usually measured in the number of blocks. Hence, the probability of a transaction not being included in all honest nodes’ local chains until is negligible. A transaction included in a block that is more than blocks deep in the blockchain is considered stable (or final).

3.3 Technical challenges

This work tackles several significant technical challenges:

-

(C1) Ad-hoc bridge implementations. The addresses of contracts involved in bridges are sometimes not well documented and not verified[30]. Implementations differ in different chains (and differences are not well documented). The challenge increases when bridges use proxy contracts and can swap bridging logic after initial deployment (many attacks happened after bridge contract updates [30]).

-

(C2) Different security approaches and security assumptions. Interoperability mechanisms are usually placed along a wide spectrum of trust and centralization [36]. Such different models have their unique attack vectors and corresponding mitigation strategies.

-

(C3) Native tokens vs. wrapped tokens and different bridging models. Handling ERC-20 tokens or other contract-based tokens differs from dealing with native tokens. The first emit events, but the latter do not or may not involve internal blockchain transactions, which are harder to track. Also, protocols differ according to the bridging models (lock-unlock, lock-mint, burn-mint) and the type of tokens supported, as different tokens are usually handled by different contracts, standards, and even implemented in different programming languages.

-

(C4) Use of intermediary protocols. Users may use intermediary protocols that manage interactions with bridge contracts (e.g., bridge aggregators [58]), which extend the attack vector and introduce new vulnerabilities.

-

(C5) Single-transaction attacks. Protecting against attacks performed in a single transaction is much more challenging than protecting against attacks that drain the bridge funds in multiple ones, as there is more time to react. The possibility of transactions being privately relayed to block builders makes the task even more challenging.

-

(C6) Multiple-chain analysis and transient data. Bridges have multiple contracts deployed in each blockchain and connect a wide range of different chains. One requires access to nodes of multiple blockchains, including less popular ones. The data is heterogeneous and sometimes transient (e.g., different finality models throughout the time).

4 \toolName

This section presents the architecture of \toolName, the mechanism for extracting facts from blockchain events, and the architecture and functionality of the Cross-Chain Rules Validator.

4.1 Architecture

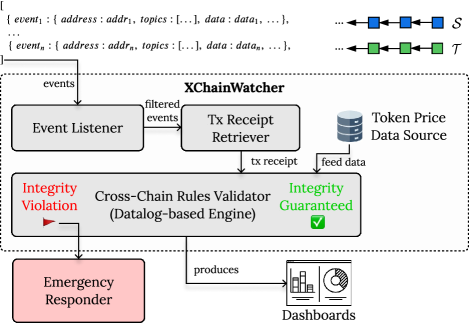

The architecture of \toolName is depicted in Figure 3. \toolName contains multiple components to realize the required functions.

Event Listener. \toolName requires access to each blockchain in which the cross-chain protocol is deployed and to the transactions that trigger deposits or withdrawals of funds from bridge contracts. The tool is agnostic to the validator architecture [30] and the proving system used [61, 33], so that other transactions related to the bridge protocol, such as the submission of cryptographic proofs, are irrelevant. This generality addresses (C2). We consider transactions from all addresses to any address, provided that they include events emitted by a bridge contract (C4). For static analysis of cross-chain data, one can load all events using the eth_getLogs RPC method via an archive RPC node for each involved blockchain. For live deployments, libraries such as Web3.js, web3.py, and Ethers.js offer methods (e.g., contract.on in Ethers.js) to receive real-time event notifications.

Transaction (Tx) Receipts Retriever. This component is responsible for gathering transaction receipts from final transactions that emit the listened events.

Cross-Chain Rules Validator. Consumes and decodes transaction receipt data from the Transaction Receipts Retriever. It also consumes token price data from an external source [24]. This data is fed into the Datalog engine as Datalog facts. Cross-chain rules, modeled as Datalog rules, evaluate all facts. The failure of a Datalog rule verification signifies an integrity breach in the protocol [35].

Emergency Responder. As pointed out in earlier studies [30] (and confirmed in Section 5.3.5), cross-chain hacks usually encompass multiple transactions. If a cross-chain rule violation is found, the bridge operator can respond by immediately halting the system through a transaction. This transaction must be accepted into the blockchain as soon as possible and in a fashion that resists MEV strategies [55].†††Maximal Extractable Value (MEV) strategies allow maximizing the value extracted by ordering transactions in a block – e.g., front-running [55] The design of this mechanism is out of scope and hence left for future work, as it focuses on reaction instead of attack identification.

4.2 Cross-Chain Rules Validator

Figure 4 presents the architecture of the Cross-Chain Rules Validator. This is a modular and extensible tool designed to validate bridge events. There are two main steps in the pipeline: extracting facts from transaction receipts and evaluating them through cross-chain rules.

4.2.1 Fact Extraction

The Bridge Facts Extractor is tailored to the specific architecture of the bridge, extracting static facts from the bridge: bridge_controlled_address, token_mapping, cctx_finality, and wrapped_native_token (cf. Listing 2). Similarly, the CCTX Facts Extractor is designed to be bridge implementation-specific, where the remaining facts are extracted based on the decoding of bridge events according to the implementation of each bridge contract. Both facts extractor components function as replaceable plugins, allowing the extension of \toolName to support cross-chain protocols on various blockchains.

In the facts extraction process, each transaction is assumed to potentially emit an unlimited number of events, e.g., when batch operations are involved. The extraction of data from relevant events involves extracting the first element in the topics list of the transaction receipt, which is equal to the hash of the event signature. For instance, topic[0] for any event with signature Deposit(address,address,uint256) is keccak256("Deposit(address,address,uint256)"). We gather addresses of interest, including proxies, various contract versions, and deployed contracts through documentation and analysis of the source code of each contract. When event information is insufficient to build the Datalog facts, additional data is extracted from decoding the data field of the transaction or by iterating over the execution traces, needed when dealing with internal transactions. Listing 2 presents a complete list of the types of facts collected by \toolName.

4.2.2 Cross-Chain Model

The definition of cross-chain rules can be done by modeling either specific attacks (as in knowledge-based intrusion detection) or the expected behavior of the protocol (as in anomaly-based intrusion detection). We adopt the latter approach, which allows us to capture not only already known attacks, but also unexpected or unusual behaviors in the protocol. We analyze various protocols to ensure the universality of the rule set across multiple bridges with different architectures and security assumptions. Some of the bridge protocols we analyzed have been attacked, while others have not. We analyzed Polygon PoS [20], the Ronin Bridge [22], the Nomad Bridge [8], and the PolyNetwork protocol [19].

Cross-Chain Rules

Each rule enforces a specific set of validations necessary to determine the validity of events within a single blockchain or across blockchains. We explain each rule, but due to size constraints, we present the formalization in Datalog in Appendix C. Rules are classified as isolated (I) or dependent (D). An isolated rule operates independently of the state of other ledgers, such as the deposit of tokens in source chain . In contrast, a dependent rule relies on prior transactions or states from other ledgers, such as the deposit of tokens in , which depends on the tokens being deposited in first. Additionally, each rule is prefixed with SC, TC, or CCTX to indicate whether it involves state from (SC), (TC), or both chains (CCTX).

Rule 1 (I). SC_ValidNativeTokenDeposit states that for the deposit of native tokens into the bridge to be valid, a bridge contract must emit a TokenDeposited event, a Deposit event emitted by the wrapped version of the native contract (e.g., token WETH in Ethereum), and a non-reverting transaction that transfers the number of funds natively in tx.value. It also asserts that the token contract provided is indeed the native currency of , the validity of the token mappings (i.e. if users are trying to deposit tokens into using a different token than what they are using in ), and finally the order of the events emitted by each contract (cf. Figure 2). To address C4, we do not check whether the transaction targets a bridge contract as it may target an intermediary protocol contract. We only verify that the deposit event from the token contract must escrow tokens to a valid bridge contract, asserted using bridge_controlled_address. When dealing with native token transfers, value is sometimes transferred in an internal transaction; in those cases, we extract the amount transferred in the first internal transaction to build the transaction fact. This rule guarantees that the flow 1 – 4 (in blue) in Figure 2 is valid for native tokens.

Rule 2 (I). SC_ValidERC20TokenDeposit guarantees that the user escrowed a certain amount of tokens (depending on the bridging model transferring to a bridge-controlled or the null address) and a bridge contract emits a TokenDeposited event. We would choose the latter in a bridge with a burn model. In a bridge with a lock model, the lock is enforced by putting tokens in escrow. The ability to handle this dichotomy addresses (C1). This rule guarantees that the flow 1 – 4 (in blue) in Figure 2 is valid for ERC 20 tokens.

Rule 3 (I). TC_ValidERC20TokenDeposit outputs valid token deposits in . It captures the valid relation between TokenDeposited events emitted by the bridge contract and the respective token contract in which tokens are being released/minted in terms of sender, beneficiary, token, amount being transferred, and order of events. This rule guarantees that the flow 5 – 9 (in green) in Figure 2 is valid for any token being deposited.

Rule 4 (D). CCTX_ValidDeposit captures behavior from both and , and cross-references events emitted on both chains for deposits of tokens, hence outputs a list of valid . A valid cross-chain transaction for a deposit – transferring tokens from to – must ensure that all parameters from all events on both chains are matched (including amounts, tokens, sender, and beneficiary). Their causality must be respected (e.g., the transaction in happens after the one on plus the finality parameter). This rule guarantees that the entire flow of Figure 2 is valid for any tokens.

Given that the bridge functions similarly in both directions ( and ), for rules 5 to 8, we only highlight the differences from the rules above:

Rule 5 (I). TC_ValidNativeTokenWithdrawal guarantees that for every escrow of native tokens on the target chain, there is a TokenWithdrew event emitted by a bridge contract and a non-reverting transaction (external or internal) sending funds to a bridge contract. The same checks in Rule 1 are enforced in this rule – e.g., the transfer of tokens must still be transferred from the sender to the bridge contract.

Rule 6 (I). TC_ValidERC20TokenWithdrawal guarantees that for every TokenWithdrew event emitted by the bridge contract on , there is a Transfer event in the contract related to the token being withdrawn. The same checks in Rule 2 are enforced in this rule.

Rule 7 (I). SC_ValidERC20TokenWithdrawal assures that for every TokenWithdrew event emitted by the bridge contract on , there is a Transfer event in the contract related to the token being withdrawn. The same checks in Rule 3 are enforced in this rule.

Rule 8 (D). CCTX_ValidWithdrawal correlates withdrawal events emitted firstly on and then on . The same checks in Rule 4 are enforced in this rule but in the opposite direction.

5 XChainWatcher Deployment

This section details the implementation of \toolName and its instantiation for monitoring two bridges. Both the data and the source code are available on GitHub for reproducibility.‡‡‡Link omitted for double-blind review

5.1 Setup and Implementation

We selected two previously exploited bridges to analyze the effectiveness of \toolName: the Nomad bridge and the Ronin bridge. This selection allows us to test \toolName against bridges that have suffered attacks and whose architecture and security assumptions differ. We used Blockdaemon’s Universal API to retrieve blockchain data from Ethereum mainnet, Moonbeam, and Ronin. We implemented a fallback to native RPC methods (namely eth_getLogs and eth_getTransactionReceipt) when the API could not provide the necessary data. Using several bridge providers helps (C6). Souffle [46] was used as Datalog engine.

5.1.1 Data Collection

We selected a comprehensive interval of interest for both bridges, including the attack dates. Table 1 lists the timestamps used for data extraction. To avoid missing cross-chain transactions occurring near the start and end of the interval of interest, denoted , we incorporated additional intervals before and after that interval ( and , respectively). For example, if there is a deposit of tokens in near , the corresponding transaction in might fall outside (within ). Therefore, additional intervals were included to capture cross-chain transactions with at least one local event within the interval, ensuring a comprehensive collection of relevant data. We used this technique to mitigate (C1).

| \CT@drsc@ | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Nomad Bridge | – |

|

|

|

||||||||

| Ronin Bridge |

|

|

|

|

||||||||

| \CT@drsc@ |

-

•

Note: The interval of interest is .The table presents dates and corresponding unix timestamps in parenthesis.

In the analysis on the Nomad bridge, we extracted 20,551 transactions from Ethereum, 16,737 transactions from Moonbeam, and 20,308 transactions on both from/to other chains, which were only used for data analysis. In the additional period, we collected an additional 1,774 transactions on Ethereum, from the latest versions of the deployed bridge contracts (C6). On the Ronin bridge, 72,820 transactions were extracted from Ethereum and 75,102 from Ronin. In the additional period, we collected additional 516,657 and 151,325 transactions on Ethereum and Ronin, respectively. The data collection totaled 875,274 transactions across the studied bridges and chains.

| \CT@drsc@ | \adl@mkpreamc\@addtopreamble\@arstrut\@preamble | \adl@mkpreamc\@addtopreamble\@arstrut\@preamble | ||||||

| Fact Name | # Facts | \adl@mkpream|c\@addtopreamble\@arstrut\@preamble | Single Token Events | Single Bridge Events | # Facts | \adl@mkpream|c\@addtopreamble\@arstrut\@preamble | Single Token Events | Single Bridge Events |

| erc20_transfer (only Deposits in ) | 4,263 | 11,450 | 39 | 6,245 | 44,707 | 83 | ||

| sc_deposit | 7,187 | (14 phishing attempts) | 38,462 | (3 phishing attempts) | ||||

| sc_token_deposited | 11,411 | (25 transfers to bridge) | 0 | 43,989 | (80 transfers to bridge) | 0 | ||

| \adl@mkpreamr\@addtopreamble\@arstrut\@preamble | $93.86K | $113.00K | ||||||

| erc20_transfer (only Deposits in ) | 11,417 | 44,471 | ||||||

| tc_token_deposited | 11,417 | 0 | 0 | 43,990 | 0 | 0 | ||

| erc20_transfer (only Withdrawals in ) | \adl@mkpreamc|\@addtopreamble\@arstrut\@preamble | 5,316 | 3 | 7 | \adl@mkpreamc|\@addtopreamble\@arstrut\@preamble | 35,892 | 2 | |

| tc_withdrawal | 464 | (3 invalid addresses) | (7 attack attempts) | 0 | 0 | (2 unmapped tokens) | ||

| tc_token_withdrew | 5,320 | 35,413 | ||||||

| erc20_transfer (only Withdrawals in ) | \adl@mkpreamc|\@addtopreamble\@arstrut\@preamble | 4,899 | 2 | \adl@mkpreamc|\@addtopreamble\@arstrut\@preamble | 26,102 | 1 | ||

| sc_withdrawal | 0 | (2 phishing attempts) | 0 | 19,219 | (1 phishing attempt) | 0 | ||

| sc_token_withdrew | 4,869 | 25,470 | ||||||

| \CT@drsc@ | ||||||||

-

•

Note: The Single Token Events column shows the number of events emitted by token contracts (or native token transfers) without a corresponding event from the bridge contracts. Conversely, the Single Bridge Events column displays events emitted by bridge contracts that lack any corresponding token contract or native token transfer events. In multiple cells, there is a high discrepancy between the number of events emitted by token and bridge contracts in column # Facts, not identified in the subsequent columns, due to multiple token deposits involving several transfers between intermediary parties – for example, a user sends tokens to an intermediary contract, which then transfers the funds to the bridge.

5.1.2 Nomad Bridge

The Nomad bridge connects six blockchains. We selected the most active blockchains in terms of bridge usage: Ethereum () and Moonbeam (). The bridge operates based on fraud proofs [36, 30]. A set of relayers transfers state proofs between blockchains. Watchers are off-chain parties with a predefined time window to challenge the relayed data. The data is optimistically accepted if no challenge is received within this window. According to the project documentation, this time window was set to 30 minutes [6] during the selected time frame. The main bridge contract (0xd3df…ce2d) on Moonbeam was deployed on January 11, 2022 (). Hence, there is no . The Nomad bridge was exploited on August 2, 2022, causing the bridge contracts to be paused until December 15, 2022. After this date, new transactions depositing tokens into the bridge on Ethereum started being reissued. We only collect withdrawals in Ethereum in to match the multiple withdrawal requests performed on Moonbeam in that did not complete.

5.1.3 Ronin Bridge

The Ronin bridge connects Ethereum () and the Ronin blockchain () and operates based on a multi-signature of trusted validators [36, 30]. Deposits and withdrawals are executed when a threshold of validators issues a transaction to the bridge contract, attesting to it. The Ronin bridge was deployed in early 2021, and the attack occurred on March 22, 2022. The interval of interest spans approximately four months, from the start of 2022 to April 28, 2022, when the main bridge contract on Ronin (0xe35d…6b4b) was paused (0xe806…19fd). To capture incomplete withdrawals on before the attack, we analyze additional data on Ethereum between . This required scanning for events in the newer version of the main bridge contract (0x6419…af08), which was deployed on Ethereum after the attack on June 22, 2022. Finally, based on the same logic as above, we also captured additional deposits in Ethereum to capture cross-chain transactions initiated before the interval of interest, whose deposit in Ronin is at the beginning of .

5.2 Results: Loss of User Funds

After extracting all the facts, we compared the number of events emitted by token contracts (and native transfers of funds) and the number of events emitted by bridge contracts. A mismatch allows the identification of exploit or unusual behavior. Table 2 presents the results. We manually inspected the mismatches, which are further analyzed below.

Depositing on . On the Nomad bridge, we detected 4,263 token deposits (erc20_transfer), 7,187 native value transfers (sc_deposit), and 11,411 TokenDeposited events emitted by the bridge contract (sc_token_deposited), which reveals that 39 value transfers did not have a corresponding bridge event emitted. Further analysis showed that 14 of these transactions are phishing attempts, characterized by numerous events emitted by tokens marked in block explorers as having a bad reputation (e.g., 0x88fc…864a). The remaining 25 transactions were single-event transactions that called the Transfer function of multiple reputable ERC20 tokens, with a total of approximately $93.86K (US dollars) sent to the bridge without triggering a cross-chain transfer (e.g., 0x7e4e…8d88). On the Ronin bridge, we identified 83 unmatched value transfers, in which 3 were related to phishing attempts and 80 were also random transfers of value to the bridge contract, which account for $113.00K (e.g., 0xe898…148d).

Depositing on . Notably, there was no discrepancy between the number of erc20_transfer and tc_token_deposited events on both bridges.

Withdrawals on . In the Nomad bridge, we identified three transactions where funds were withdrawn to invalid Ethereum addresses. Each transaction involved a newly deployed contract 0x58fb…45dd, which interacted with the Nomad bridge contract using a 32-byte string instead of a 20-byte Ethereum address in the destination address field. Therefore, this leads to unparseable data from our tool (the parser is programmed to parse only valid 20-byte addresses). Therefore, token transfers were successfully parsed, but the bridge event was not, which generated this inconsistency. Additionally, we discovered seven transactions from a single address attempting to exploit the bridge using different inputs in the “token” field. The attacker first attempted to provide a bridge address as a token, probably to gain control over the bridge (0x56e6…afe1). The following 3 transactions involved a newly created contract that was not mapped to a token in (e.g., 0xebd6…bfa9 with token 0x2422…Aefb). Finally, in the latter two, the user attempts to withdraw funds from a (fake) token contract called Wrapped ETH (ETH) (0xcbb4…b91F), to unlock real ETH on Ethereum (e.g., 0x7cd7…03f1). Fortunately, these transactions reverted and all attempts failed. On the Ronin bridge, we identified two events emitted by the bridge contract without a match on erc20_transfer or sc_withdrawal. These were trying to withdraw unmapped tokens to .

Withdrawals on . The analysis highlights three events where funds were transferred from a bridge address without emitting corresponding bridge events: 2 using Nomad and 1 using the Ronin bridge. These instances were linked to phishing attempts and marked accordingly in block explorers (e.g., 0x3587…39ca and 0x78b6…2766, respectively).

Key Findings. Attackers engage in phishing attempts using low-value tokens to interact with bridge contracts. According to Certik, a reputable security firm in the area, in the first half of 2024, more than $498M were lost in phishing attacks [3]. One key finding from this analysis is the inconsistent logic of bridges. In some cases, bridges emit events without transferring tokens. We see the opposite in others, especially when dealing with these valueless tokens. The reasons for these discrepancies and how different bridge implementations across various chains handle them remain unclear, leading to an ad hoc monitoring process that requires individual analysis for each case. Finally, we uncover that over $206K worth of various reputable tokens was transferred to bridge addresses without interacting with the protocol. Despite warnings from the user interface of multiple DeFi protocols against directly sending funds to bridge addresses (which can cause irreversible loss of funds), it seems a common practice.

5.3 Results: Cross-Chain Rules

We proceed to analyze the results with cross-chain rules. Table 3 presents the number of events captured by each Datalog rule and highlights the unmatched values, i.e., the number of events captured that were not matched by any event on the other blockchain. Section 5.3.1 presents the general findings of the rules that capture cross-chain transactions: Rule 4 and 8, CCTX_ValidDeposit and CCTX_ValidWithdrawal, respectively. The results of the remaining rules are presented in detail in Sections 5.3.2 to 5.3.4.

[c] \CT@drsc@ \adl@mkpreamc\@addtopreamble\@arstrut\@preamble \adl@mkpreamc\@addtopreamble\@arstrut\@preamble Datalog Rule Captured Unmatched Captured Unmatched \adl@mkpreamc\@addtopreamble\@arstrut\@preamble SC_ValidNativeTokenDeposit 7,187 0 38,462 10 SC_ValidERC20TokenDeposit 4,223 6 5,527 0 TC_ValidERC20TokenDeposit 11,417 13 43,990 11 (101 ) CCTX_ValidDeposit 11,404 – 43,979 – \adl@mkpreamc\@addtopreamble\@arstrut\@preamble TC_ValidNativeTokenWithdrawal 464 239 (2381 ) 0 0 TC_ValidERC20TokenWithdrawal 4,846 589 (4911 ) 35,411 12,581 (11,8141 ) SC_ValidERC20TokenWithdrawal 4,869 387 25,470 2,640 (7321 ) CCTX_ValidWithdrawal 4,482 – 22,830 – \CT@drsc@

-

1

values after retrieving data in the additional intervals ( and ).

-

•

Note: We mark in red violations that may cause loss of funds to the bridge.

5.3.1 CCTX Priority, latency, and integrity

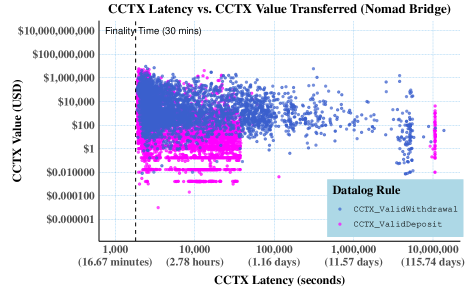

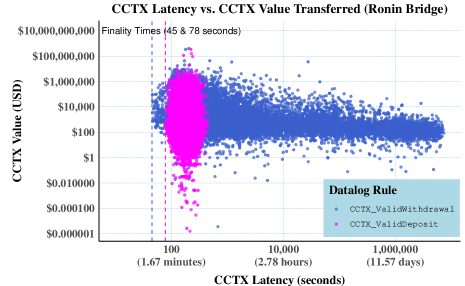

In this section, we analyze different cross-chain transaction metrics. First, we analyzed deposits and withdrawals to understand if there is a correlation between their value and processing time. Figure 5 shows the relationship between the latency and value transferred per , for the Nomad bridge. The equivalent visualization for the Ronin bridge is in Appendix B.1. A key observation from the plot is that all cctxs accepted by \toolName start at the 30-minute mark, which aligns with our expectations, as the Nomad fraud-proof window is set for this period enforced by cctx_finality.

The plot shows that the entire range of transferred values is distributed throughout the full spectrum of latencies, suggesting no correlation between transaction value and latency (the Pearson correlation coefficient is ), i.e., transactions of higher value do not necessarily require more time to process. In addition, Table 4 compares deposits and withdrawals for both bridges. The data only considers cross-chain transactions fully completed before the attack, which prevents the results from being distorted by the bridges’ pause.

| \CT@drsc@ | \adl@mkpreamc\@addtopreamble\@arstrut\@preamble | \adl@mkpreamc\@addtopreamble\@arstrut\@preamble | ||

|---|---|---|---|---|

| CCTX_Dep | CCTX_Withd | CCTX_Dep | CCTX_Withd | |

| No. CCTXs | 10,417 | 4,286 | 43,708 | 22,631 |

| Min Latency | 1,875.00 | 1,860.00 | 78.00 | 45.00 |

| Max Latency | 60,938.00 | 13,708,549.00 | 459.00 | 7,346,416.00 |

| Avg Latency | 8,016.91 | 193,614.49 | 191.24 | 159,541.28 |

| Std Dev Latency | 8,782.65 | 909,019.02 | 45.62 | 660,017.66 |

| Median Latency | 2,579.00 | 4,556.00 | 187.00 | 330.00 |

| Total Value | $363.81 M | $221.50 M | $1,695.73 M | $2,044.90 M |

| \CT@drsc@ | ||||

-

•

Note: We abbreviate CCTX_ValidDeposit to CCTX_Dep and CCTX_ValidWithdrawal to CCTX_Withd.

User- vs. Bridge Operator-Driven Latency. In Table 4, we compare the metrics of token deposits and withdrawals. The longest cross-chain token deposits took nearly 17 hours to complete using the Nomad bridge (0x3575…8fff in and 0x7b48…b3f7 in ) and 7.65 minutes using the Ronin bridge (0xd1bf…6705 in and 0xf4f2…f3db in ). In contrast, the longest withdrawal took over five months using the Nomad Bridge (0x8afe…85bb in and 0xdfaa…e3cb in ) and almost 3 months using Ronin (0x2c2e…1b9b in and 0xb8f2…fb5b in ). In the Ronin bridge, the minimum latency almost touches the finality of each blockchain (45 and 78 seconds, for Ronin and Ethereum, respectively). In the scope of each bridge, although the minimum latency for deposits and withdrawals is similar – slightly higher than the corresponding finality time – withdrawals exhibit significantly greater data dispersion by two and four orders of magnitude in the Nomad and Ronin bridges, respectively. This variance is also evident in the data shown in Figure 5. The differences in latency can be attributed to the different mechanisms involved in the cross-chain bridge model, as discussed in Figure 2 and Section 3.1. When depositing, validators typically send the final transaction to . In contrast, during withdrawals, users are responsible for completing the process (in the analyzed bridges). Because users are left alone in this process, they either delay withdrawing funds in or abandon the process midway through, well beyond the finality time of or the fraud-proof window time (later confirmed by our data in Section 5.3.4).

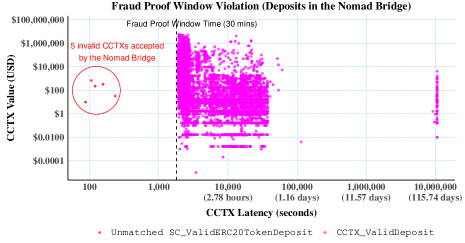

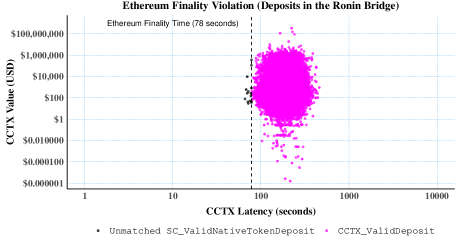

Cross-Chain Finality Violations. One of the most intriguing findings in this paper is the identification of 37 violations of cross-chain rules – 5 on the Nomad bridge and 32 on the Ronin bridge – which were accepted by both bridges at the time, transferring a total value of $1.3K and $667K, respectively. Five instances involvingSC_ValidERC20TokenDeposit and TC_ValidERC20TokenDeposit matched each other but were not captured by CCTX_ValidDeposit. On the Ronin bridge, there were 10 events emitted on each side of the bride that did not match for a valid deposit (CCTX_ValidDeposit), and 22 events on each side that did not match for a withdrawal (CCTX_ValidWithdrawal). Figures 6 for the Nomad bridge (and 11 and 12 in Appendix B.2, for Ronin) demonstrate the reason why these violations were missed by CCTX_ValidDeposit and CCTX_ValidWithdrawal. In the first, the time difference between the initial deposit in (0xeb06…0fea) and the corresponding deposit on (0x2cdc…ef0c) was as short as 87 seconds, approximately 20 times less than the required fraud-proof window. This finding is particularly concerning because it implies that the security mechanisms of the bridge were bypassed. Not only did it fail to comply with the fraud-proof time window, but it was very close to the finality period of the source chain (Ethereum) at the time of the attack – before “The Merge” [13] was around 78 seconds. On the Ronin bridge, the fastest deposit took 66 seconds (0x4688…cdf3 and 0xc299…279d), which is less than Ethereum’s finality period. On the other hand, the fastest withdrawal took 11 seconds (). These practices represent a significant risk in cross-chain transaction validation and open the door to multiple attack vectors, especially when considering smaller blockchains or ones more prone to forks.

5.3.2 Deposits in

From this Section onward, we dive deeper into the unmatched events of rules 1 – 3 and 5 – 7 in Table 3. On the Nomad bridge, the deposit rules in , SC_ValidNativeTokenDeposit and SC_ERCNativeTokenDeposit, had 6 unmatched events. The analysis on Section 5.3.1 uncovered the explanation for 5. In the remaining event, a user issued a transaction (0x7941…1393) in that deposits 10 DAI to address 0x3333…5Be5 in . A manual search on Moonbeam on the destination address did not reveal any transaction of the equivalent deposit of funds. On the Ronin bridge, all ten unmatched events were identified due to not respecting the finality period of (Ethereum).

5.3.3 Deposits in

From the 13 unmatched TC_ValidERC20TokenDeposit in Nomad, five have already been explained in Section 5.3.1. We present the analysis of the remaining 8. 5 transactions that caused the Nomad bridge operator to deploy new ERC20 tokens on Moonbeam. The vulnerability stemmed from a lack of contract verification. According to the documentation [5], anyone could deploy a new token on Moonbeam and link it to any token on Ethereum. Two transactions in (0x7fe7…bf27 and 0x398d…53d7) deployed new token contracts, mapping them to contracts called WRAPPED GLMR in (e.g., 0x92C3…7178), which is the native token of the Moonbeam blockchain, even though the token contract already exists in and is already mapped by the bridge (0xba8d…A663). We found other transactions deploying new token contracts that were not used by anyone since the deployment, and tried withdrawing funds to Ethereum. If anyone can deploy a contract on Moonbeam and make it a mapping of WETH’s contract on Ethereum, then it would be possible to withdraw WETH on Ethereum.

We also highlight one transaction (0xacab…c2f0) that created a token contract on Moonbeam linking it to renBTC on Ethereum (0xEB4C…B27D). This transaction was carried out by the first attacker of the Nomad bridge, but in itself does not constitute an attack as there were no funds stolen (0x8ce6…90a0). When the Nomad bridge was hacked, this vulnerability went unnoticed. We are the first to highlight it as a critical concern for the architecture of cross-chain protocols. The final unmatched transaction is a transfer of 10 DAI. Recalling 5.3.2, a transaction deposited 10 DAI into the bridge and did not have a match in . However, these transactions have the same deposit_id, making them linkable. We found that the EOA withdrawing funds was not the beneficiary intended by the sender when depositing on S (0x3333…5Be5). Therefore, this represents a cross-chain violation, because another besides the intended beneficiary withdrew the funds. We searched for transactions between these two addresses, looking for a transaction with a similar functionality as an Approval – in which one user authorizes another to act on behalf of the first – but nothing was found.

On the Ronin bridge, we found one unmatched deposit event in , made at the beginning of the selected interval, suggesting a match with a deposit in in . As expected, loading the additional data as Datalog facts revealed a match for the event slightly before . The remaining ten are unmatched due to not conforming with cctx_finality (cf. Section 5.3.1).

5.3.4 Withdrawals in

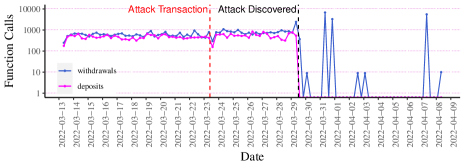

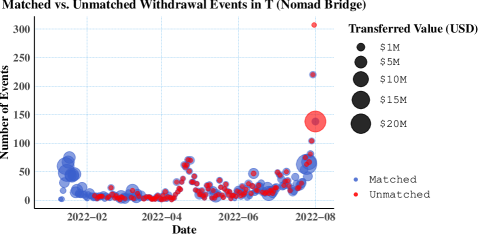

According to Table 3, TC_ValidNativeTokenWithdrawal and TC_ValidERC20TokenWithdrawal always captured more events than CCTX_ValidWithdrawal on both bridges. These represent withdrawals on , in which no corresponding action was found in . A first hypothesis to explain the high number of unmatched events is whether these values are a consequence of the attack, i.e., multiple users tried (unsuccessfully) withdrawing funds as the bridge was paused. To test this hypothesis, we plot in Figure 7 a visual comparison of matched and unmatched withdrawal events emitted on on the Nomad bridge (Figure 13 in Appendix for the Ronin bridge). As expected, close to when the hack happened in August 2022, there were many unmatched withdrawal events emitted in . In Nomad, 24 hours before the attack, 313 events were withdrawing over $24.7M. In Ronin, we identified 468 events that were withdrawing $24.3M. Not surprisingly, in the event of an attack, it is difficult to withdraw tokens or complete s, due to the bridge being paused after the attack on Ethereum (). However, it is also noticeable that throughout the entire period in which the bridge was functioning, there were always multiple low-value unmatched events, following the same trend as the matched ones. These are funds escrowed in – i.e., tokens transferred by the users to the bridge contracts – in which the corresponding tokens were never unlocked/minted on , within .

Matching Withdrawals with Additional Data. According to the analysis of CCTX_ValidWithdrawals in Section 5.3.1, the latency of token withdrawals surpassed four months. To accurately present the data related to unmatched withdrawals, we explore how many of these are matched by new events emitted in on the additional data interval after the attack (i.e., , in which is the most accurate data at the date of writing, July 2024). We found 99 additional withdrawal events on Ethereum for Nomad and 787 for Ronin. Those matched events on Moonbeam and Ronin, respectively. Surprisingly, the last cross-chain transaction identified on the Nomad bridge matched an event emitted on Moonbeam on August 3, 2022 – a day after the attack – (0xdb3c…74a9) with a withdrawal event on Ethereum emitted on a transaction issued on May 07, 2024 (0x5b03…8481) – representing a cross-chain transaction with 55,568,159 seconds (1.7 years vs the expected minutes) of latency.

[c] \CT@drsc@ \adl@mkpreamc\@addtopreamble\@arstrut\@preamble \adl@mkpreamc\@addtopreamble\@arstrut\@preamble Before Attack After Attack Total Before Attack After Attack Total Unmatched withdrawal events in 541 188 729 11,574 220 11,794 Addresses with balance at withdrawal date 95 26 121 5,988 66 6,054 Addresses with balance at withdrawal date and still today 55 17 72 5,212 49 5,261 Addresses with balance at withdrawal date 185 46 231 7,381 88 7,469 Total Value (in million of USD) $0.34M $3.27M 1 $3.62M 1 $1.09M $0.09M $1.18M Addresses that tried withdrawing more than once 34 23 58 932 21 956 Addresses that tried withdrawing exactly once 460 136 592 9,490 176 9,657 \CT@drsc@

-

1

A single address is responsible for $3M.

Remaining Unmatched Withdrawals on . On the Nomad bridge, from the initial 828 unmatched withdrawal events, 99 were matched using additional data, leaving 729 events still unmatched with an event on Ethereum (). Following the same logic on the Ronin bridge, 11,794 events were unmatched. We further analyze these events to uncover the reasons behind this unusual behavior. Strangely, many of the destination addresses (beneficiaries on Ethereum) targeted by these events on had no funds or had not made any transactions to date. Table 5 illustrates these findings, separating metrics extracted before and after (i.e., as a consequence of) the attack. Our analysis revealed that, spanning both bridges, 6,175 addresses on Ethereum (49%) had a zero balance at the time of the withdrawal event, in which 5,333 (43%) are still holding a zero balance at the time of writing. As a consequence, users cannot withdraw their assets. Bridge aggregators are tackling this problem [58].

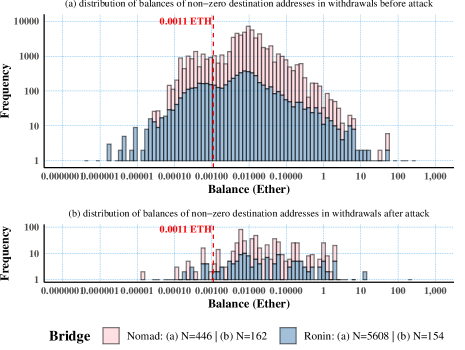

Furthermore, according to the Ronin documentation, users should have a minimum of 0.0011 ETH to cover gas fees for issuing a transaction on Ethereum to withdraw funds [26]. We use this value as a simple approximation on both bridges. However, 7,700 addresses (61%) lacked sufficient funds to meet this requirement. The total value of unwithdrawn funds amounts to $4.8M, in which a single transaction attempted to withdraw $3M on the Nomad bridge. Excluding this outlier, the amount not withdrawn is $1.8M. Figure 8 shows the distribution of balances of destination addresses with non-zero balances when the withdrawal event was triggered in . To assess the attack’s impact on these values, we divided the analysis into pre-attack and post-attack periods. The data shows that the attack does not seem to have any influence. The number of data points before the attack is much higher (97%), suggesting that this is a common practice when the bridge is functioning normally. Interestingly, even users with many funds, including those with over 10 or 200 ETH in their addresses, were involved in this behavior (cf. Figure 8). Another noteworthy finding is the difference between unique addresses that attempted to withdraw funds once versus those that tried multiple times. Some users repeatedly attempted withdrawals, while others seemingly gave up, likely considering their funds lost. This may also be attributed to user inexperience and inadequate UI/UX. The Pearson correlation coefficient between the number of withdrawal attempts and the amount withdrawn is negligible, at , showing no meaningful relationship.

5.3.5 Withdrawals in

The attack on both bridges analyzed in this paper was performed on the source chain (Ethereum), allowing attackers to trigger the withdrawal of assets without corresponding events on the target chains. As shown in Table 3, 387 unmatched events were identified under SC_ValidERC20TokenWithdrawal on the Nomad bridge. We divided these into two sets based on the timestamp of the first attacking transaction. The attack-related set contained 381 events between 2022-08-01 21:32 and 2022-08-02 00:04, while the remaining six events occurred well before the attack (between January and May 2022). Among these, 3 involved unmapped tokens, and the other three corresponded to events that we could not decode earlier (in Section 5.3.3) because the destination Ethereum address is represented as a 32-byte string. Surprisingly, the off-chain validators managing the Nomad bridge successfully decoded these addresses, identifying 3 additional s. The 381 events confirmed as part of the attack involved 279 unique addresses and totaled $159,577,598 of stolen funds. These events had only 14 unique withdrawal IDs, indicating that attackers copy-pasted data from other transactions, exploiting the bridge’s acceptance of any data as valid proof [15]. Our analysis identified 279 addresses exploiting the protocol, the majority of which were contracts deployed in bulk to scatter funds across multiple addresses. We traced the transactions and identified 45 unique EOAs responsible for deploying these contracts. We cross-referenced our findings with data from Peckshield, a reputable security firm, which provided a list of addresses involved in exploiting the bridge at the time of the attack [53]. We identified nine more EOAs than Peckshield (41 EOAs). Peckshield found five additional addresses that are marked in our dataset as out-of-scope, as their origin chain was not Moonbeam. This attack is known to be a $190 million hack. However, since there is no open-source dataset of all transactions related to the attack, we could not compare our results with other analyses.

Matching Withdrawals with Additional Data. On the Ronin bridge, around 2,640 events were unmatched. We extract additional data in capturing for withdrawals of funds in the Ronin blockchain. We capture over 500k additional transactions in this interval over 3.5 months. We take into account the maximum latency of withdrawals in the Ronin bridge (cf. Table 4), of around 3 months, and added some margin. With the additional data, we matched 1,908 events. Hence, 732 were still left unmatched. Unfortunately, due to rate limits in extracting data on the Ronin blockchain and the amount of events emitted from the initial deployment of contracts to , we could not decrease to that date. However, to exclude withdrawals before , we based ourselves on the withdrawal_id. The withdrawal_id is a counter incremented for each withdrawal event emitted in the bridge contract. From those 732 unmatched events, 708 had a withdrawal ID less than the withdrawal_id of the first event included in , suggesting that they were emitted before our interval of collection data. Leaving us with 24 unmatched withdrawal events in the selected interval. 22 of these transactions were unmatched due to the finality break, already explained in Section 5.3.1. The remaining two were transactions issued by the same address (0x098b…2f96) on March 23, 2022 13:29 (0xc28f…d0b7) and 13:31 (0xed2c…9b08), transferring a total of $565.64M. These two transactions are the ones also identified in the industry as pertaining to the Ronin bridge hack.

6 Discussion and Limitations

Here, we present the discussion and limitations of our work.

Rule modeling and additional data. Modeling the cross-chain rules is a process that involves a manual exploration of transactions and token contracts (challenge C3) in multiple blockchains, with the minor help of each of the protocol’s documentation. We did our best to ensure that no transaction moving funds from each bridge was left out of our analysis in the selected time frames by cross-referencing data from RPC Nodes, Blockdaemnon’s Universal API, and exporting raw data from block explorers. The smallest dataset was the Nomad bridge’s, but it spans the time from the deployment of their contracts until the date of writing. Also, due to the rate limits in the access for Ronin RPC nodes, we could not extend the analysis of the Ronin bridge to the deployment of the contracts in January 2021.

Starting the analysis “midway through” hardens the isolation of the attack, as there have probably been unmatched transactions since this time. However, the fact that 500K additional transactions spanning 3.5 months were not enough to cover the data in the interval supports the findings in this work (cf. Table 4). This paper focuses on analyzing bridge security, specifically during relevant time intervals that include previous attacks. Each of the 81K s encompasses data from multiple blockchains and external sources, with the total value transacted ($4.3B) reflecting the usual amounts in these protocols. Although we did not analyze additional attacked bridges (due to the cumbersome data extraction process), our findings validate the cross-chain rules and suggest that they would have identified further attacks.

Involvement with sanctioned addresses. Recent studies on cross-chain hacks reveal that attackers often use mixing services like Tornado Cash before launching attacks [30]. This metric can be added as a constraint in each Datalog rule. However, identifying sanctioned addresses during specific timeframes is difficult due to the unavailability of such datasets with the required granularity. While this analysis helps check for direct and indirect interactions, not all associations with mixing services imply malicious intent.

Emerging solutions. Our solution accommodates various bridging models and is adaptable to include additional token standards, new chains (including private ones), and privacy-preserving bridges. Data from this paper suggests that users are largely unaware of the complexities of cross-chain protocols, highlighting the need for further research on improving the user experience and user interfaces in asset bridging. Bridge aggregators seem promising solutions [34, 58, 36].

7 Related Work

The concept of a cross-chain model was first introduced in Hephaestus [35], a cross-chain model generator, highlighting the importance of defining cross-chain rules to identify misbehavior. We use the definition of cross-chain transactions, which this paper formally defines. Xscope [62] designed a set of cross-chain rules to detect three types of attacks on cross-chain bridges. However, the paper focuses on smaller chains with a limited dataset. SmartAxe [49] is a generalized framework for detecting vulnerabilities in bridge contracts through static analysis of smart contracts bytecode. The solution focuses on pre-deployment analysis, whereas our research targets the post-deployment phase. In the industry, Hyperlane[7], Range[21], and Layer Zero’s Precrime[10] provide analysis tools for bridges. However, these are proprietary and lack technical documentation, systematic evaluation, and datasets, making it challenging to compare directly to our work. This paper provides the first quantitative analysis of bridges using a representative dataset, uncovering unique security insights on these protocols. Based on what we have learned, we offer helpful directions to find similar and new attacks on other bridges. Finally, while post-attack analyses typically trace the flow of funds using tools like Chainalysis[4], \toolName enables immediate retrieval of the same data by applying cross-chain rules.

8 Conclusion

This paper proposes \toolName, a monitoring and attack identification framework for cross-chain bridges powered by a cross-chain model enforced by a datalog engine. We uncover significant vulnerabilities within cross-chain bridges, such as 1) transactions accepted in one chain before the finality time of the original one elapsed; 2) users trying to exploit a protocol through the creation of fake versions of wrapped Ether to withdraw real Ether on the Ethereum blockchain; 3) bridge contract implementations handling unexpected inputs differently across chains. In addition, we identify every transaction involved in previous hacks on the Nomad and Ronin bridges. We show that although only 49 unique externally owned accounts (EOAs) exploited Nomad, there were 380 exploit events, with each address deploying multiple exploit contracts to obscure the flow of funds. Finally, our study highlightes a critical user awareness gap – many users struggle to withdraw funds due to the highly manual nature of the process, contrasting with the more streamlined deposit process managed by bridge operators. This user error has led to over $4.8M in unwithdrawn funds due to users mistakenly sending funds to addresses they do not control or that have never been active. This paper is the first to empirically analyze the performance and security vulnerabilities underlying cross-chain bridges. Our open-source dataset provides a valuable resource for future research and development in this critical area.

Ethics Considerations

This research identifies and analyzes attacks on cross-chain bridges, uncovering security flaws and focusing on user practices within these protocols. We have carefully considered the ethical implications of our findings for all stakeholders involved.

Our research does not interfere with the functioning of the protocols studied. The Nomad bridge is currently deactivated – accepting only withdrawals through a recovery address – and is thus unaffected by our work. The analysis of the Ronin Bridge focuses on data from 2021 until mid-2022, addressing a specific attack. Since then, contracts and documentation have evolved, and new studies on more recent data are needed to represent a current and accurate picture of the protocol. While disclosing vulnerabilities could undermine user trust and cause market instability, providing insights to users on these protocols and security practices will ultimately increase confidence, leading to more informed usage and broader adoption of blockchain technology. Furthermore, our research relies solely on publicly available data (e.g., pseudonymous addresses and transactions registered in public blockchains), ensuring that we respect individuals’ privacy. We have not collected or analyzed private or sensitive information, nor tried to deanonymize end-users’ addresses.

We contacted the Nomad and Ronin bridge teams, shared our manuscript, and disclosed the vulnerabilities we identified. While the Nomad bridge team did not respond, the Ronin bridge team acknowledged our findings and granted permission to include the information in this paper.

Open Science Policy

This study aims to present unique findings to the community, and we are committed to transparency and collaboration by making all aspects of our research accessible. Our goal is to improve the overall security of cross-chain bridges and educate users about their practices. To this end, we have made all of our work open-source, including the full dataset, scripts, and source code, available on GitHub. We call on practitioners and researchers to contribute, adding new cross-chain protocols and providing new insights.

References

- [1] Arbitrum — the future of ethereum. https://arbitrum.io/.

- [2] Base. https://base.org.

- [3] Certik – hack3d: The web3 security quarterly report – q2 + h1 2024. https://www.certik.com/resources/blog/hack3d-the-web3-security-quarterly-report-q2-h1-2024.

- [4] Chainalysis. https://www.chainalysis.com/.

- [5] Faq | nomad docs. https://docs.nomad.xyz/token-bridge/faq.

- [6] Glossary | nomad docs. https://docs.nomad.xyz/resources/glossary.

- [7] Hyperlane. https://hyperlane.xyz/.

- [8] Introduction | nomad docs. https://docs.nomad.xyz/nomad-101/introduction.

- [9] L2beat – the state of the layer two ecosystem. https://l2beat.com/bridges/summary.

- [10] Layerzero security update – april 2022. https://medium.com/layerzero-official/layerzero-security-update-april-2022-4c27a22380b4.

- [11] Mantle | mass adoption of decentralized and token-governed technologies. https://www.mantle.xyz.

- [12] Mapped tokens – polygon knowledge layer. https://docs.polygon.technology/pos/reference/mapped-tokens/.

- [13] The merge | ethereum.org. https://ethereum.org/en/roadmap/merge/.

- [14] Multichain - rekt 2. https://rekt.news/multichain-rekt2/.

- [15] Nomad bridge - rekt. https://rekt.news/nomad-rekt/.

- [16] Optimism. https://optimism.io/.

- [17] Poly network - rekt. https://rekt.news/polynetwork-rekt/.

- [18] Poly network - rekt 2. https://rekt.news/poly-network-rekt2/.

- [19] Polynetwork. https://www.poly.network/#/.

- [20] Pos - polygon knowledge layer. https://docs.polygon.technology/pos/.

- [21] Range. https://www.range.org/.

- [22] Ronin bridge | ronin docs. https://docs.roninchain.com/apps/ronin-bridge.

- [23] Ronin network - rekt. https://rekt.news/ronin-rekt/.

- [24] See crypto prices, charts, and live data | bitget. https://www.bitget.com/price.

- [25] Thorchain - rekt 2. https://rekt.news/thorchain-rekt2/.

- [26] Withdraw an erc20 token | ronin docs. https://docs.roninchain.com/apps/ronin-bridge/withdraw-token#step-3-confirm-your-withdrawal.

- [27] $225 million raised in wormhole token sales. https://wormhole.com/wormhole-secures-225-million-in-funding-round/, November 2023.

- [28] Supra completes over $24m in early stage funding to date. https://finance.yahoo.com/news/supra-completes-over-24m-early-134500320.html, September 2023.

- [29] Multichain (Previously Anyswap). Anyswap multichain router v3 exploit statement. https://medium.com/multichainorg/anyswap-multichain-router-v3-exploit-statement-6833f1b7e6fb, Jul 2021.

- [30] A. Augusto, R. Belchior, M. Correia, A. Vasconcelos, L. Zhang, and T. Hardjono. Sok: Security and privacy of blockchain interoperability. In 2024 IEEE Symposium on Security and Privacy (SP), pages 234–234, Los Alamitos, CA, USA, may 2024. IEEE Computer Society.

- [31] Rob Behnke. Explained: The pnetwork hack. https://www.halborn.com/blog/post/explained-the-pnetwork-hack-september-2021, October 2021.

- [32] Rob Behnke. Explained: The thorchain hack (july 2021). https://www.halborn.com/blog/post/explained-the-thorchain-hack-july-2021, Jul 2021.

- [33] Rafael Belchior, Dimo Dimov, Zahary Karadjov, Jonas Pfannschmidt, André Vasconcelos, and Miguel Correia. Harmonia: Securing cross-chain applications using zero-knowledge proofs. Submitted to IEEE Transactions on Dependable and Secure Computing, December 2023. Citation Key: belchiorHarmoniaSecuringCrossChain2023.

- [34] Rafael Belchior, Sabrina Scuri, Iulia Mihaiu, Nuno Nunes, and Thomas Hardjono. Towards a Common Standard Framework for Blockchain Interoperability - A Position Paper. October 2023.

- [35] Rafael Belchior, Peter Somogyvari, Jonas Pfannschmidt, André Vasconcelos, and Miguel Correia. Hephaestus: Modeling, analysis, and performance evaluation of cross-chain transactions. IEEE Transactions on Reliability, 73(2):1132–1146, 2024.

- [36] Rafael Belchior, Jan Süßenguth, Qi Feng, Thomas Hardjono, André Vasconcelos, and Miguel Correia. A brief history of blockchain interoperability. Communications of the ACM, 2024.

- [37] Rafael Belchior, André Vasconcelos, Sérgio Guerreiro, and Miguel Correia. A survey on blockchain interoperability: Past, present, and future trends. ACM Comput. Surv., 54(8), oct 2021.

- [38] Rafael Belchior, André Vasconcelos, Miguel Correia, and Thomas Hardjono. Hermes: Fault-tolerant middleware for blockchain interoperability. Future Generation Computer Systems, April 2022.

- [39] Tom Blackstone. Layerzero raises $120m to expand cross-chain messaging efforts. https://cointelegraph.com/news/layerzero-raises-120m-to-expand-cross-chain-messaging-efforts, April 2023.

- [40] Stefano Ceri, Georg Gottlob, Letizia Tanca, et al. What you always wanted to know about Datalog (and never dared to ask). IEEE Transactions on Knowledge and Data Engineering, 1(1):146–166, 1989.

- [41] Vishal Chawla. Union labs raises $4 million to develop cross-chain bridge enabled by zk proofs. https://www.theblock.co/post/263310/union-labs-raises-4-million-to-develop-cross-chain-bridge-enabled-by-zk-proofs.

- [42] James Cirrone. Crypto funding: A $72m week for cross-chain oracles, nft merchandise. https://blockworks.co/news/funding-cross-chain-oracle-nft-merchandise, October 2023.

- [43] Li Duan, Yangyang Sun, Wei Ni, Weiping Ding, Jiqiang Liu, and Wei Wang. Attacks against cross-chain systems and defense approaches: A contemporary survey. IEEE/CAA Journal of Automatica Sinica, 10(8):1643–1663, 2023.

- [44] Christof Ferreira Torres, Antonio Ken Iannillo, Arthur Gervais, and Radu State. The eye of horus: Spotting and analyzing attacks on ethereum smart contracts. In Nikita Borisov and Claudia Diaz, editors, Financial Cryptography and Data Security, Lecture Notes in Computer Science, page 33–52, Berlin, Heidelberg, 2021. Springer.

- [45] Terje Haugum, Bjørnar Hoff, Mohammed Alsadi, and Jingyue Li. Security and Privacy Challenges in Blockchain Interoperability - A Multivocal Literature Review. In Proceedings of the International Conference on Evaluation and Assessment in Software Engineering 2022, EASE ’22, pages 347–356, New York, NY, USA, June 2022. Association for Computing Machinery.

- [46] Herbert Jordan, Bernhard Scholz, and Pavle Subotić. Soufflé: On synthesis of program analyzers. In Computer Aided Verification: 28th International Conference, CAV 2016, Toronto, ON, Canada, July 17-23, 2016, Proceedings, Part II 28, pages 422–430. Springer, 2016.

- [47] Aggelos Kiayias, Alexander Russell, Bernardo David, and Roman Oliynykov. Ouroboros: A provably secure proof-of-stake blockchain protocol. In Annual international cryptology conference, pages 357–388. Springer, 2017.

- [48] Matter Labs. zksync — accelerating the mass adoption of crypto for personal sovereignty. https://zksync.io.

- [49] Zeqin Liao, Yuhong Nan, Henglong Liang, Sicheng Hao, Juan Zhai, Jiajing Wu, and Zibin Zheng. Smartaxe: Detecting cross-chain vulnerabilities in bridge smart contracts via fine-grained static analysis. Proc. ACM Softw. Eng., 1(FSE), jul 2024.

- [50] Satoshi Nakamoto. Bitcoin: A peer-to-peer electronic cash system. Satoshi Nakamoto, 2008.

- [51] Poly Network. The poly network exploit analysis. https://polynetwork.medium.com/the-poly-network-exploit-analysis-b0a77aff6078, November 2023.

- [52] Margaux Nijkerk. Coinbase, framework venture funds invest $5m in socket protocol, in bet on blockchain interoperability, September 2023.

- [53] PeckShieldAlert [@PeckShieldAlert]. #peckshieldalert peckshield has detected 41 addresses grabbed $152m (80%) in the @nomadxyz_bridge exploit, including 7 mev bots ($7.1m), @raricapital arbitrum exploiter ($3.4m), and 6 white hat ($8.2m). https://x.com/PeckShieldAlert/status/1554350737957998592, Aug 2022.

- [54] Daniel Perez and Benjamin Livshits. Smart contract vulnerabilities: Vulnerable does not imply exploited. In 30th USENIX Security Symposium (USENIX Security 21), pages 1325–1341. USENIX Association, August 2021.

- [55] Kaihua Qin, Liyi Zhou, and Arthur Gervais. Quantifying blockchain extractable value: How dark is the forest? In 2022 IEEE Symposium on Security and Privacy (SP), pages 198–214, 2022.

- [56] Ronin [@Ronin_Network]. Earlier today, we were notified by white-hats about a potential exploit on the ronin bridge. after verifying the reports, the bridge was paused approximately 40 minutes after the first on-chain action was spotted., Aug 2024.

- [57] Squid. Squid raises $3.5 million to build next-generation cross-chain swaps powered by axelar. https://medium.com/@squidrouter/squid-raises-3-5-million-to-build-next-generation-cross-chain-swaps-powered-by-axelar-c3284bf33b02, January 2023.

- [58] S. Subramanian, A. Augusto, R. Belchior, A. Vasconcelos, and M. Correia. Benchmarking blockchain bridge aggregators. In 2024 IEEE International Conference on Blockchain (Blockchain), pages 37–45, Los Alamitos, CA, USA, aug 2024. IEEE Computer Society.

- [59] THORChain. Eth parsing error and exploit. https://medium.com/thorchain/eth-parsing-error-and-exploit-3b343aa6466f, Jun 2021.

- [60] Ruoyu Yin, Zheng Yan, Xueqin Liang, Haomeng Xie, and Zhiguo Wan. A survey on privacy preservation techniques for blockchain interoperability. Journal of Systems Architecture, page 102892, Apr 2023.

- [61] Alexei Zamyatin, Dominik Harz, Joshua Lind, Panayiotis Panayiotou, Arthur Gervais, and William Knottenbelt. Xclaim: Trustless, interoperable, cryptocurrency-backed assets. In 2019 IEEE Symposium on Security and Privacy (SP), page 193–210, May 2019.

- [62] Jiashuo Zhang, Jianbo Gao, Yue Li, Ziming Chen, Zhi Guan, and Zhong Chen. Xscope: Hunting for cross-chain bridge attacks. In Proceedings of the 37th IEEE/ACM International Conference on Automated Software Engineering, ASE ’22, New York, NY, USA, 2023. Association for Computing Machinery.

- [63] Mengya Zhang, Xiaokuan Zhang, Yinqian Zhang, and Zhiqiang Lin. Security of cross-chain bridges: Attack surfaces, defenses, and open problems. In Proceedings of the 27th International Symposium on Research in Attacks, Intrusions and Defenses, RAID ’24, page 298–316, New York, NY, USA, 2024. Association for Computing Machinery.

- [64] Qianrui Zhao, Yinan Wang, Bo Yang, Ke Shang, Ming Sun, Haijun Wang, Zijiang Yang, and Xin He. A comprehensive overview of security vulnerability penetration methods in blockchain cross-chain bridges. Authorea (Authorea), Oct 2023.

- [65] ZhiyuanSun. ’terra hit us incredibly hard’: Sunny aggarwal of osmosis labs. https://cointelegraph.com/magazine/connecting-blockchains-crossroads-sunny-aggarwal-osmosis-dex/, October 2022.

Appendix A Cross-Chain Bridge Model: Withdrawal Flow

Figure 2 presents the architecture of a cross-chain bridge with the flow for token deposits. In this Section, we present the opposite flow, for withdrawing tokens, depicted in Figure 9. The process begins with a Withdraw transaction on , where user funds are escrowed, enforced by a transfer of funds from the sender to the bridge contract . These processes trigger the emission of events by each contract and . Validators listen for events emitted by the bridge contracts and generate proofs. The user uses these proofs to issue the corresponding Withdraw transaction on . It releases the same amount of funds to the beneficiary’s address after verifying proof that such transfer is valid. This process also generates events and . The user is able to access their tokens by interacting with the corresponding token contract .

Appendix B Additional Data Visualizations

In this Section, we present the same visualization for the data collected on the Ronin Bridge.

B.1 CCTX Latency

Section 5.3.1 presents visualizations of data related to the Nomad Bridge, namely through Figure 5. The equivalent figure for the Ronin Bridge is Figure 10. Similarly, and as highlighted by Table 4, there is a great discrepancy between deposits and withdrawals. Comparing with the Nomad Bridge data, in this Figure we do not see all deposits and withdrawals starting at the 30 minute mark, instead, we highlight the finality times of each blockchain connected by the Ronin Bridge – Ronin and Ethereum – 45 and 78 seconds, respectively. Additionally, even more envident than the data and findings on the Nomad Bridge, the standard deviation is around 45 seconds for the latency of deposits, and 600K seconds (?? days) for withdrawals. The different processes involved in withdrawing funds – i.e., being managed by users instead of operators – allows minimizing the operational costs associated to maintaining the bridge, because validators are not required to issue transactions, and therefore pay gas fees, on (Ethereum on both cases) for every withdrawal request.

B.2 Cross-Chain Finality Violations

In Section 5.3.1 we draw insights over violations of the cross-chain rules due to s not respecting the fraud-proof time window, when using the Nomad Bridge. Here, we present similar insights, considering data from the Ronin Bridge. Contrarily to the Nomad Bridge, there is no fraud-proof time window, therefore, the time it takes for s to be completed depends on the finality of each chain. We found 32 violations in the Ronin Bridge, in which 10 were events Deposits of tokens, and 22 events Withdrawals of tokens. Figure 11 depicts the first 5 s and Figure 12 depicts the 11 s considered invalid withdrawals.

Appendix C Cross-Chain Rules

Section 4.2.2 presents the cross-chain model, including a description of the cross-chain rules. The cross-chain rules can be specified in two ways. Specification in the negative tense – model attacks that exploit specific vulnerabilities. By failing in such a rule, the cross-chain model knows precisely where the vulnerability is located and further action can be taken accordingly. Alternatively, rules can be defined in a positive tense – i.e., we model the expected behavior of transactions interacting with the bridge contracts. The definition of the rules in this way allows the cross-chain model to identify conformance with expected behavior. Failing in such a rule but not failing one in a negative sense allows for the identification of new vulnerabilities and attacks. In this paper, we model cross-chain rules in the positive tense, which allows not only the identification of attacks but also misuses of the protocol. Listing 3 presents the definition of rule 1 to 4 in Datalog, related to the deposit of tokens. Similarly, Listing 4 presents the definition of rule 5 to 8 in Datalog, related to the withdrawal of tokens.

Appendix D Unmatched Withdrawals

Similarly to the data presented in Section 5.3.4 for the Nomad bridge, we present the data relative to the withdrawals of tokens in for the Ronin bridge in Figure 13. The same pattern observed in Figure 7 is observed, where there were recurrent unmatched events throughout the entire interval of interest. The number of unmatched events captured amounted to 12,581, whereas the number of matched events is 22,830.