Abstract.

In recent years, a range of measures of “partial” stochastic dominance have been introduced. These measures attempt to determine the extent to which one distribution is dominated by another. We assess these measures from intuitive, axiomatic, computational and statistical perspectives. Our investigation leads us to recommend a measure related to optimal transport as a natural default.

Keywords: Stochastic dominance, optimal transport

Partial Stochastic Dominance via

Optimal

Transport111Corresponding author:

john.stachurski@anu.edu.au,

RSE, College of Business and Economics, Australian National University,

ACT, Australia.

Takashi Kamihigashia and John Stachurskib

aCenter for Computational Social Science, Kobe University

bResearch School of Economics, Australian National University

1. Introduction

(First order) stochastic dominance is one of the most fundamental concepts in social welfare and decision making under uncertainty (see, e.g., [5, 11]). At the same time, stochastic dominance is fragile. For example, two normal distributions can only be ordered by stochastic dominance if their variances are exactly identical, even if one mean is orders of magnitude larger than the other. Such fragility is problematic for quantitative work.

In response, researchers have introduced many different notions of “partial” stochastic dominance. One is “restricted stochastic dominance,” which compares the order of cumulative distribution functions (cdfs) only up to some specified point in the domain [1, 2, 3]. Another is “almost stochastic dominance,” which was developed in the finance literature [6, 8]. A third kind of measure was proposed in [4], analyzing degree of stochastic dominance in the context of income mobility analysis. Still more measures are considered in [11].

Despite the obvious practical relevance of a measure of partial stochastic dominance, none of the above have a clear axiomatic foundation. At the same time, some measures become complex outside of the one-dimensional case. These observations suggest that now is a good time to consider measures of partial stochastic dominance collectively. While doing so, we make the case for what we believe is the most natural measure of partial stochastic dominance. The measure can be understood as the solution to an optimal transport problem.

2. A Measure of Dominance

Let be Polish with Borel sets and closed partial order (i.e., a partial order on such that is closed in the product topology). A function is called increasing if implies , and decreasing if is increasing. Let be the set of increasing Borel measurable on with (that is, ). Let be all finite measures on and be all with . A measure is said to be stochastically dominated by and we write if and for all . For probability measures , an alternative characterization is

| (1) |

where is the set of all couplings of and [12]. (Given , a pair of -valued random variables defined on some probability space is called a coupling of if and for all .) The short summary of our paper is: in light of (1), why not use

| (2) |

as the default measure of partial stochastic dominance? We answer this question in stages. Existence of the maximum for each pair is verified below.

Note that we can rewrite as , where . The infimum is a standard optimal transport problem. In particular, is nonnegative, bounded and lower-semicontinuous (since is a closed partial order), so, by Theorem 4.1 of [13], a solution exists. In particular, the “max” in (2) is justified. From now on, we call a pair that attains the maximum in (2) an optimal coupling.

It now follows from Kantorovich duality that can be replaced by a supremum over supporting “prices.” In particular,

| (3) |

where is all with . This is (iii) of Theorem 5.10 of [13]. (See “Particular case 5.16” on p. 60.) The existence of a maximizer is guaranteed by the same theorem. Clearly is just the set of decreasing functions on with . Hence we can rewrite (3) as

| (4) |

These expressions have additional representations that can be useful in some settings. For example, if and are cdfs, then one can show has the simple representation

| (5) |

The representation in (4) is very similar to measures of partial stochastic dominance studied in [11]. They use essentially the same measure but replace with the set of all increasing functions satisfying a Lipschitz bound with respect to the underlying metric. Such a measure is more attuned to topology but lacks the some of the advantages of (4) described below.

3. Alternative Measures

Here and below, a measure of degree of stochastic dominance is any function

| (6) |

Clearly is a measure of degree of stochastic dominance in the sense of (6). Another is the quantile ratio measure proposed in [4]. Let and let be the usual order on . Letting and be cdfs on , define

| (7) |

Here is a grid of specified values in , typically corresponding to some quantile points. Thus measures the fraction of times that is observed over specified test points. Clearly satisfies when pointwise (i.e., ), which corresponds to (6).

Another version of partial stochastic dominance is restricted stochastic dominance (see, e.g. [1, 3]). Let and be one dimensional cdfs on an interval . Given , distribution is said to be dominated by in the restricted sense if for all . We can turn this into a measure by considering the largest such , defined by

| (8) |

After normalizing we get

| (9) |

Evidently is a measure of degree of stochastic dominance in the sense of (6).

Another measurement for partial stochastic dominance is almost stochastic dominance [7, 6]. Once again the context is with the usual order . For cdfs and on , the measure can be expressed as

| (10) |

where for any . Intuitively, if is almost dominated by , then on most of its domain, and for most . Hence is close to 1. In order to ensure that the measure is defined for all pairs , we adopt the convention that when .

4. Axioms

Next we propose two axioms for degree of stochastic dominance . The first says that should not be large unless the distributions are nearly ordered. To state it, we write to indicate pointwise ordering on and define, for each ,

Think of as the set of “ordered component pairs” corresponding to . If is “almost” dominated by , then we can choose relatively large components. (Recall that, to admit the ordering , we insist that total mass is equal, so must hold.)

Axiom 4.1.

For each and , there exists a in such that .

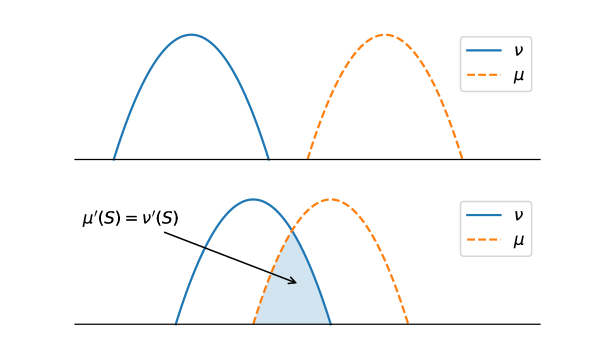

Figure 1 helps to illustrate the axiom, with and represented by densities. In the top subfigure, is in no sense dominated by , so we wish to enforce . Axiom 4.1 does enforce this, since, for this pair , we cannot extract an ordered component pair with positive mass. Hence is always zero.

In the lower subfigure, there is some overlap in probability mass, so we should permit . Inspection shows this to be true. For example, we could take both and to be the function enclosing the shaded region (the pointwise infimum of the density representations of and ), so that, as measures again, the area of the shaded region. Since this is positive, can be positive.

Proposition 4.1.

If is a measure of degree of stochastic dominance that satisfies Axiom 4.1, then if and only if .

Proof.

Suppose that satisfies Axiom 4.1 and that . Then for some in . From this we immediately have and , and hence , which is all we need to show. ∎

The second axiom plays the opposite role. It implies that is close to when is “nearly” dominated by .

Axiom 4.2.

Given and , the ordering implies for and .

Axiom 4.2 uses the natural convexity of to implement “continuity near 1” while avoiding being tied to a particular topology.

The axioms we have listed are strong enough to give uniqueness:

Proof.

First we claim that satisfies Axiom 4.1. To see this, let be an optimal coupling for , attaining the maximum in (2). Set and . This pair satisfies and . To see that satisfies Axiom 4.2, fix and let the decompositions in Axiom 4.2 be given, with and . Let be an optimal coupling of for . Let where is independent and binary with . Let . Then . Hence , and Axiom 4.2 holds.

Now let be an arbitrary measure of degree of stochastic dominance satisfying Axioms 4.1–4.2. Fix in and let be an optimal coupling of . Define and the probabilities

We have , since, when is increasing,

For we have , which can be decomposed as . Since satisfies Axiom 4.2, we have .

For the reverse inequality, recall from the arguments above that we can obtain an ordered component pair satisfying . Since satisfies Axiom 4.1, we have for all . Hence . ∎

5. Measures vs Axioms

Let us reconsider measures of stochastic dominance other than . By Theorem 4.1, they fail at least one of the axioms. For example, regarding Axiom 4.2, note that fails whenever the grid has at least three points. To see this let , and be any cdfs on such that on . Let and let

Since , Axiom 4.2 implies that . On the other hand, on any interior point . Hence in (7) is at most 2, and . Since can be arbitrarily close to 1 this contradicts Axiom 4.2.

For this same pair , the fact that on implies that for defined in (8), and hence for the restricted stochastic dominance measure defined in (9). Likewise, for the same pair, , where is the almost stochastic dominance measure. Hence and also fail to satisfy Axiom 4.2.

Regarding Axiom 4.1, the measures , and all fail. To see this, let and, given some positive number , let put mass on and on , and let put all mass on . Let be the cdf of and let be a draw from . Let and be the cdf of and a draw from respectively. Since is certainly we have if and only if , and hence for all couplings. On the other hand, iff , and hence . If then , and hence fails Axiom 4.1. The measures and also give values larger than when is small, although the details are omitted.

6. Final Comments

We end with some avenues for future research. One is that an estimation theory for should be straightforward to construct. For example, if we replace the cdfs and in (5) with empirical counterparts and , then is a simple transform of the statistic used in the one-sided two-sample Kolmogorov-Smirnov test. This allows for construction of confidence intervals and hypotheses tests related to the value of .

Another topic of interest is computation. In higher dimensional settings, computation is difficult for all measures of partial stochastic dominance, but at least has an interpretation as the solution to an optimal transport problem. Computing solutions of optimal transport problems is an active research area [10].

Third, there is some connection between the measure , which takes values in the interval and represents the continuum between no dominance and complete first order dominance, and the measure proposed in [9], which represents the continuum between first order and second order stochastic dominance. Clarifying this connection and investigating the preceding two topics are left for future work.

7. Acknowledgements

We gratefully acknowledge JSPS KAKENHI Grant 15H05729 and Australian Research Council Grant DP120100321.

References

- [1] Anthony B Atkinson. On the measurement of poverty. Econometrica, 55(4):749–764, 1987.

- [2] Russell Davidson and Jean-Yves Duclos. Statistical inference for stochastic dominance and for the measurement of poverty and inequality. Econometrica, 68(6):1435–1464, 2000.

- [3] Russell Davidson and Jean-Yves Duclos. Testing for restricted stochastic dominance. Econometric Reviews, 32(1):84–125, 2013.

- [4] Gary S Fields, Jesse B Leary, and Efe A Ok. Stochastic dominance in mobility analysis. Economics Letters, 75(3):333–339, 2002.

- [5] Hans Föllmer and Alexander Schied. Stochastic Finance: An Introduction in Discrete Time. De Gruyter Textbook Series. De Gruyter, 2011.

- [6] Moshe Leshno and Haim Levy. Preferred by “all” and preferred by “most” decision makers: Almost stochastic dominance. Management Science, 48(8):1074–1085, 2002.

- [7] Haim Levy. Stochastic dominance and expected utility: survey and analysis. Management Science, 38(4):555–593, 1992.

- [8] Moshe Levy. Almost stochastic dominance and stocks for the long run. European Journal of Operational Research, 194(1):250–257, 2009.

- [9] Alfred Müller, Marco Scarsini, Ilia Tsetlin, and Robert L Winkler. Between first-and second-order stochastic dominance. Management Science, 63(9):2933–2947, 2017.

- [10] Gabriel Peyré and Marco Cuturi. Computational optimal transport. Now Publishers, 2019.

- [11] Stoyan V Stoyanov, Svetlozar T Rachev, and Frank J Fabozzi. Metrization of stochastic dominance rules. International Journal of Theoretical and Applied Finance, 15(02), 2012.

- [12] Volker Strassen. The existence of probability measures with given marginals. The Annals of Mathematical Statistics, pages 423–439, 1965.

- [13] Cédric Villani. Optimal transport: old and new. Springer Science, 2008.