Non-linear dependence and Granger causality:

A vine copula approach

Abstract

Inspired by Jang et al. (2022), we propose a Granger causality-in-the-mean test for bivariate Markov stationary processes based on a recently introduced class of non-linear models, i.e., vine copula models. By means of a simulation study, we show that the proposed test improves on the statistical properties of the original test in Jang et al. (2022), constituting an excellent tool for testing Granger causality in the presence of non-linear dependence structures. Finally, we apply our test to study the pairwise relationships between energy consumption, GDP and investment in the U.S. and, notably, we find that Granger-causality runs two ways between GDP and energy consumption.

1 Introduction

The notion of Granger causality was seminally introduced by Granger (1969), and then usefully applied in several scientific fields, including economics, finance, neuroscience, genomics, and climate science (Shojaie and Fox, 2022), where the characterization of the dependence relations between time series is a relevant issue. It is based on the comparison of the quality of the prediction when forecasting future values of one series with or without the information about the past values of the other time series. In other words, a time series has a Granger causal influence on another time series if its past values facilitate the prediction of the other time series. Therefore, briefly, testing Granger causality means checking if there is an improvement in prediction if we leverage not only the past values of the considered series but also the past values of the other series.

In this paper, we propose a novel Granger causality-in-the-mean test for bivariate Markov stationary processes, which is based on vine copula models. Vine copulas are highly flexible models that allow for computationally tractable estimation, model selection procedures, and the representation of a wide array of different joint distributions (Czado and Nagler, 2022). Formally, exploiting the concept of pair copula construction (Joe, 1996), a multivariate copula is constructed using bivariate copulas as building blocks, overcoming the limited and restrictive selection of multivariate copulas. As shown in recent literature (Brechmann and Czado, 2015; Beare and Seo, 2015; Smith, 2015; Nagler et al., 2022), vine copulas are non-linear models that can represent multivariate time series by capturing both their cross-sectional and serial dependence within the same model, giving place to a myriad of applications in the context of time series modelling, one of them being the study of Granger causality.

In literature, there are already several tests differing from each other in the models and techniques used for measuring and estimating the correspondent measure of Granger causality. Granger’s original formulation and most of the existing tests are based on linear models such as Vector Autoregressive (VAR) models. Yet, the application of these tools to non-linear systems may not be appropriate (Ancona et al., 2004). Therefore, a few non-linear Granger causality tests have been proposed (Hiemstra and Jones, 1994; Diks and Panchenko, 2006; Diks and Wolski, 2016; Song and Taamouti, 2018; Kim et al., 2020). In economics, the Hiemstra and Jones (1994) test (HJ test hereafter) has been the most popular approach for testing non-linear Granger causality (Bai et al., 2017); however, it has been shown through simulation studies that this test has a tendency to over-reject the null hypothesis. Diks and Panchenko (2006) proposed a modified version of the HJ test that overcomes the rejection rate issues by changing the test statistics and providing some guidelines for the optimal bandwidth selection based on the sample size. Afterwards, Diks and Wolski (2016) extended the setting by Diks and Panchenko (2006) from a bivariate to a multivariate one. Song and Taamouti (2018) introduced a model-free measure of non-linear Granger causality that takes the form of a log-difference between restricted and unrestricted mean squared errors, building a test by means of a non-parametric estimate of this measure using kernel estimators of mean squared errors. Hiemstra and Jones (1994), Diks and Panchenko (2006), Diks and Wolski (2016) and Song and Taamouti (2018) introduce non-parametric methods. More recently, exploiting the measure of Song and Taamouti (2018), Jang et al. (2022) proposed a semi-parametric Granger causality test based on vine copulas, which can capture non-linear dependencies with a good statistical performance in terms of size and power if compared to the aforementioned tests. In line with this recent literature, our aim is to propose a test that extends and improves on the family of semi-parametric non-linear Granger causality tests, which statistical properties are not heavily dependent on the choices of bandwidth or smoothing parameters, as it is instead the case for most of the existing non-parametric non-linear Granger causality tests.

In this contribution, we start from the test procedure proposed in Jang et al. (2022) and incorporate some relevant methodological differences. Thus, we build our non-linear Granger causality-in-the-mean test for bivariate Markov stationary processes, which we call M-vine Granger causality test. By means of a simulation study based on the setting from Song and Taamouti (2018), we find that the M-vine test has a higher power than the original version from Jang et al. (2022) in all scenarios considered, whil still controlling its size under or considerably close to the predefined significance level. Moreover, for linear specifications and large samples, our test displays a power that resembles the one from a traditional Granger-causality test based on linear models, even if the latter is based on the real data generating process. Yet, for non-linear specifications, the M-vine test has a substantially higher power than the linear Granger-causality test. Hence, we show that our test improves on the statistical properties of the original one in Jang et al. (2022) and makes it an excellent tool for testing Granger causality in the presence of non-linear dependence structures.

Finally, we apply the M-vine Granger causality test to study the pairwise causal relationships between GDP, energy consumption and investment in the U.S. The nexus between energy consumption and economic growth has been studied in various works (Kraft and Kraft, 1978; Chen et al., 2007; Payne, 2009b; Ozturk, 2010). Nonetheless, results appear to be diverse and often conflicting, even when they refer to the same country: for instance, in Appendix A.3, Table 10, we provide a synthetic recap of the results from different studies that specifically investigated Granger causality between energy consumption and economic growth with a focus on the United States. Here, we provide our contribution by means of the M-vine test, and we compare results with the S-vine test and a more classical linear test based on VARs. At significance level, we find a Granger causality relationship that runs from GDP to energy consumption, which is in line with previous literature (Kraft and Kraft, 1978; Fallahi, 2011; Aslan et al., 2014)). Yet, at the same time, we also find that there is an albeit less significant Granger causality running from energy consuption to economic growth that is still in line with other pieces of economic literature (Stern, 1993, 2000; Bowden and Payne, 2009; Fallahi, 2011). Crucially, only our M-vine test is able to catch the two-way Granger causality between energy consumption and GDP.

The rest of the paper is organized as follows. Section 2 introduces the methodology and the setting of the M-vine test, while section 3 studies the statistical properties of the proposed test by means of a simulation study. In section 4, we present a macroeconomic application to pairwise relationships energy consumption, GDP and investment in the U.S. Conclusions and final remarks are offered in Section 5.

2 Methodology

Measures of Granger causality are classified into three types, according to the criterion chosen to measure their prediction quality: namely, Granger causality in the mean, in the quantiles or in the distributions. Here, we focus only on the first, which is the most widely used in literature, while we refer to Lee and Yang (2014) and Candelon and Tokpavi (2016) for the others. Nonetheless, we believe it is important to remark that the methodology that we present can be naturally extended to Granger causality in quantiles (Song and Taamouti, 2021; Hyuna Jang and Noh, 2023).

Let be a strictly stationary bivariate stochastic process, that is

where the symbol means equality in distribution. Suppose also that is a Markov process of order (more briefly, a -Markov process), that is

Set and .

Definition 1

(Granger causality in the mean) We say that causes in the sense of Granger, if

where

are the mean squared errors of the optimal prediction of given the past observations of and given the past observations of both and , respectively.

A measure for Granger causality in the mean has been proposed in Song and Taamouti (2018) as

Note that is a non-negative quantity, which is equal to zero when there is no Granger causality in the mean (i.e. when the two above mean squared errors are equal).

Moreover, it is not restricted to a given model for the distributions of the involved random variables.

This measure can be used to construct a statistical test in order to check the presence or absence of Granger causality in the mean

for two -Markov stationary time series.

Jang et al. (2022) proposed a semi-parametric Granger causality test based on the above measure , estimated using a copula approach, which is able to capture non-linear dependence while having desirable statistical properties when compared to other existing tests. This test is our starting point. We here propose a test of Granger causality in the mean based on the M-vine copula structure presented in Beare and Seo (2015) for a bivariate Markov stationary stochastic process. The presented test improves both on the size and the power when compared to the one in Jang et al. (2022), and it is more suitable for empirical applications since it takes into account possible non-linear dependencies that are commonly encountered when working with real data. Please, refer to Appendix A.1 for some recalls on the notion of copulas and, in particular, on vine copulas.

2.1 M-vine Granger causality test

Let be a bivariate Markov stationary stochastic process and let be a sample of it.

To simplify notation, from now on,

we will assume , but everything can be naturally extended to any .

We can split the proposed test, which we call the M-vine Granger causality test, into two parts, say part A and part B: the first regards the estimation of the Granger causality (in the mean) measure, and part B concerns the computation of the -value of the test.

We start by describing part A. We use the sample version of the above-recalled measure , that is

where the quantities and are computed as follows:

-

Step A1)

we fit an M-vine copula model and estimate its respective parameters for the observations from the series , that is for ;

-

Step A2)

using the model of Step 1), for each , we generate i.i.d. predictions of given , so that we obtain

-

Step A3)

repeat Step 1) and Step 2) for the observations from the bivariate series , that is for , in order to obtain

Introducing the sample estimates of both conditional expectations in , we obtain

Thus, roughly speaking, a sample estimate of Granger causality in the mean, i.e. , measures the log-difference between

the prediction error related to the model with an M-vine copula structure fitted only on the information set from ,

and the prediction error computed with the M-vine copula model fitted to the entire sample

form both and , that is using the information set of both series.

In line with the definition of Granger causality in the mean, if this estimated quantity is significantly

higher than zero, we reject the null hypothesis of no Granger causality (in the mean) from to : indeed, under the null hypothesis, the measure is zero, and so, the higher is the value of the

statistics , the more statistically significant is the evidence of the presence of

Granger causality (in the mean) running from to . Regarding ,

we can choose it by taking into account the goodness of fit of the models to the data.

In order to test if is statistically greater than zero, we rely, as in Jang et al. (2022), on a bootstrap method, which takes inspiration from Paparoditis and Politis (2000). The procedure relies on the M-vine copula model fitted on the entire sample in order to generate bootstrapped samples under the null hypothesis and use them for computing the value for the test. More precisely, the part B of the proposed procedure works as follows:

-

Step B1)

from the first tree of the found M-vine copula structure, extract, for each , both the copula between and , say , related to the conditional distribution of given , and the copula between and , say , related to the conditional distribution of given ;

-

Step B2)

using the estimated marginal distribution , generate , and, conditional on this value draw from ;

-

Step B3)

using also the estimated marginal distribution , conditional on , draw from ;

-

Step B4)

using this bootstrapped sample , compute the bootstrapped version of the test statistic under the null hypothesis, say ;

-

Step B5)

repeat the above steps times, so that we get bootstrapped samples and so for ;

-

Step B6)

compute the bootstrapped -value for the test by

Therefore, we reject the null hypothesis of no Granger causality (in the mean) when , where is a given significance level.

2.2 Differences with the S-vine Granger causality test by Jang et al. (2022)

There are two relevant differences between the test by Jang et al. (2022) and the one we propose. Firstly, in the above-described Step 1A), we choose the class of the M-vine copulas to fit the data. The same model is then used in the bootstrap procedure to construct the -value for the test. On the contrary, Jang et al. (2022) use a more general class of copula models, i.e., the S-vine copulas, but then they restrict to the M-vine copulas in the bootstrap procedure (part B). The justification of this fact given in Jang et al. (2022) simply relies on the implementation of the bootstrap procedure: indeed, to draw the samples in the above Steps B2) and B3), both and are needed, and these two copulas are guaranteed to be present in the first tree of a given M-vine structure, whilst these two copulas might not appear in an S-vine structure. Consequently, in Jang et al. (2022), the conditional distribution used for computing the bootstrapped sample of the Granger causality might be different from the ones in the model fitted to the data to estimate the Granger causality measure. In our procedure, the two parts, A and B, of the Granger causality test are aligned: they rely on the same class of vine copulas.

Secondly, in the above Step 1A), we fit the M-vine copula model on the entire sample, i.e., on all the observations, while Jang et al. (2022) split the entire sample into a training set, say observations from to (usually ), and a testing set, say observations from to . Therefore, the fit of the -vine copula model is performed only on the training set, while the testing set is used to compute the Granger causality statistics. The latter choice implies that all the predictions and for , used to compute the Granger causality statistics are based on a model fitted only on the observations from . In real applications, when the time series are not perfectly stationary or the sample is small, this way of proceeding could generate poor estimates of the Granger causality measure. This is especially true in the case of non-linearities in the data generating process. In our case, instead, predictions are based on a model fitted to the entire sample, and this potentially makes our test better at detecting Granger causality, especially when the dependence structure is not linear. In the next subsection, we show that our variant has a better performance in terms of size and power.

3 Simulation Study

In this section, we analyse the statistical performance of our M-vine Granger causality test (briefly, M-vine test) and compare it, in terms of size and power, with the traditional linear Granger-causality test based on VAR models 111The linear test refers to a Wald test based on restricted and unrestricted VAR models, and their results are obtained after application of grangertest from the R package lmtest. and the S-vine Granger causality test (S-vine test) by Jang et al. (2022). We recall that, as shown in Jang et al. (2022), the last one has a good statistical performance in terms of size and power when compared to other non-linear Granger causality tests (Diks and Panchenko, 2006; Song and Taamouti, 2018; Kim et al., 2020). Specifically, through a simulation study, they show that S-vine test, ST test (Song and Taamouti, 2018) and KLH test (Kim et al., 2020) are the ones whose size is closer to the predefined significance level, whereas the size of DP test (Diks and Panchenko, 2006) is considerably smaller than the significance level and this suggests a tendency of this test to under-reject. Indeed, in terms of statistical power, Jang et al. (2022) evidences that DP test is the one that performs the worst. On the contrary, S-vine test shows, in large samples ( for Markov processes of order ), a good power for all the dependence structure, while KLH test has an excellent power only when working with linear or quasi-linear models and ST test displays a good power exclusively when the dependence structure is non-linear. In the following, we will show that our M-vine test outperforms S-vine test in all the considered scenarios, exhibiting a very good power already starting from in the case of Markor order .

We performed a simulation study based on the assessment models from Song and Taamouti (2018).

We used their three size assessment models and their three power assessment models while incorporating an additional fourth power assessment model where both series come from non-linear specifications:

Size assessment models

- S1

-

,

- S2

-

,

- S3

-

,

Power assessment models

- P1

-

,

- P2

-

,

- P3

-

,

- P4

-

,

where are i.i.d. from a standard bivariate normal distribution.

Recall the size of a test corresponds to the probability of incorrectly rejecting the null hypothesis when it is true,

whilst the power of a test is the probability of correctly rejecting the null hypothesis when it is false.

Consequently, the size assessment models correspond to data-generating processes for which there is no Granger causality

from to (note that S3 exhibits Granger causality from to , but not from to ),

whereas the models used for the power assessment of the test are built under the presence of Granger causality

from to .

For the simulation study, we used simulations for each model with sample sizes of , and ,

and computed the empirical size and power using a significance level . Furthermore,

for part A of the procedure, we used i.i.d. predictions for each series to estimate the

conditional expectations and, for part B, i.e. the bootstrapping procedure to obtain the -values, we used a number

of bootstrapped samples. We used in the computation of the test statistics

in accordance with the choice in Jang et al. (2022).

| Model | T=50 | T=100 | T=200 | ||||||

| M-vine | Jang et al. | Linear | M-vine | Jang et al. | Linear | M-vine | Jang et al. | Linear | |

| S1 | 0.046 | 0.066 | 0.058 | 0.050 | 0.070 | 0.048 | 0.056 | 0.050 | 0.058 |

| S2 | 0.044 | 0.052 | 0.058 | 0.052 | 0.080 | 0.054 | 0.062 | 0.066 | 0.056 |

| S3 | 0.058 | 0.070 | 0.060 | 0.054 | 0.054 | 0.052 | 0.050 | 0.070 | 0.046 |

| Model | T=50 | T=100 | T=200 | ||||||

| M-vine | Jang et al. | Linear | M-vine | Jang et al. | Linear | M-vine | Jang et al. | Linear | |

| P1 | 0.706 | 0.630 | 0.958 | 0.916 | 0.856 | 1.000 | 0.996 | 0.978 | 1.000 |

| P2 | 0.544 | 0.442 | 0.802 | 0.720 | 0.676 | 0.982 | 0.942 | 0.886 | 1.000 |

| P3 | 0.430 | 0.238 | 0.348 | 0.716 | 0.384 | 0.388 | 0.986 | 0.644 | 0.392 |

| P4 | 0.684 | 0.426 | 0.530 | 0.972 | 0.628 | 0.518 | 1.000 | 0.950 | 0.508 |

Table 1 shows evidence that the M-vine test and the linear test control

the empirical size under or around the significance level of better than the S-vine test. In terms of power, the M-vine test outperforms the S-vine test, in every power assessment model, in small and large samples, with the biggest difference when working with series from the data-generating model P3, that exhibit a quadratic dependence relationship. Furthermore, the power of the M-vine test seems to increase as the sample size grows faster than the one of the S-vine test. Notice that the M-vine and the S-vine tests have the same bootstrapped version of the test statistic, i.e. , and so the difference in the performance relies upon the computation of , that explains the difference in the obtained -values. When compared to the Linear test, the M-vine test tends to have a smaller power across the assessment models P1 and P2 that corresponds to linear or roughly linear models, respectively; this difference is decreased as we move to larger samples, becoming negligible at . On the contrary, the power of M-vine test is substantially bigger than the one of the Linear test when working with non-linear model specifications, such as P3 and P4, particularly when working with larger samples: indeed, the power of the Linear test does not increase as the sample size grows, remaining considerably low. Hence, the presented analyses show that the M-vine test is an excellent tool for detecting the Granger causality in the presence of non-linear dependencies, filling in a gap present in the current literature.

| Model | T=50 | T=100 | T=200 | ||||||

| M-vine | Jang et al. | Linear | M-vine | Jang et al. | Linear | M-vine | Jang et al. | Linear | |

| S1 | 0.456 | ||||||||

| (0.249) | 0.520 | ||||||||

| (0.313) | 0.489 | ||||||||

| (0292) | 0.462 | ||||||||

| (0.264) | 0.504 | ||||||||

| (0.305) | 0.509 | ||||||||

| (0.294) | 0.476 | ||||||||

| (0.276) | 0.502 | ||||||||

| (0.287) | 0.494 | ||||||||

| (0.285) | |||||||||

| S2 | 0.463 | ||||||||

| (0.260) | 0.519 | ||||||||

| (0.313) | 0.480 | ||||||||

| (0.291) | 0.471 | ||||||||

| (0.268) | 0.501 | ||||||||

| (0.305) | 0.496 | ||||||||

| (0.290) | 0.473 | ||||||||

| (0.277) | 0.538 | ||||||||

| (0.311) | 0.487 | ||||||||

| (0.292) | |||||||||

| S3 | 0.474 | ||||||||

| (0.251) | 0.527 | ||||||||

| (0.304) | 0.495 | ||||||||

| (0.293) | 0.457 | ||||||||

| (0.267) | 0.516 | ||||||||

| (0.307) | 0.483 | ||||||||

| (0.282) | 0.474 | ||||||||

| (0.277) | 0.507 | ||||||||

| (0.293) | 0.507 | ||||||||

| (0.292) |

| Model | T=50 | T=100 | T=200 | ||||||

| M-vine | Jang et al. | Linear | M-vine | Jang et al. | Linear | M-vine | Jang et al. | Linear | |

| P1 | 0.092* | ||||||||

| (0.187) | 0.190 | ||||||||

| (0.308) | 0.011** | ||||||||

| (0.058) | 0.021** | ||||||||

| (0.085) | 0.074* | ||||||||

| (0.214) | 0.000*** | ||||||||

| (0.001) | 0.001*** | ||||||||

| (0.007) | 0.014** | ||||||||

| (0.104) | 0.000*** | ||||||||

| (0.000) | |||||||||

| P2 | 0.159 | ||||||||

| (0.234) | 0.290 | ||||||||

| (0.335) | 0.046** | ||||||||

| (0.113) | 0.093* | ||||||||

| (0.199) | 0.165 | ||||||||

| (0.298) | 0.004*** | ||||||||

| (0.025) | 0.017** | ||||||||

| (0.085) | 0.050* | ||||||||

| (0.162) | 0.000*** | ||||||||

| (0.000) | |||||||||

| P3 | 0.214 | ||||||||

| (0.268) | 0.454 | ||||||||

| (0.356) | 0.294 | ||||||||

| (0.309) | 0.091* | ||||||||

| (0.201) | 0.348 | ||||||||

| (0.354) | 0.262 | ||||||||

| (0.303) | 0.011*** | ||||||||

| (0.089) | 0.216 | ||||||||

| (0.328) | 0.245 | ||||||||

| (0.277) | |||||||||

| P4 | 0.121 | ||||||||

| (0.233) | 0.311 | ||||||||

| (0.355) | 0.195 | ||||||||

| (0.276) | 0.015** | ||||||||

| (0.104) | 0.190 | ||||||||

| (0.310) | 0.195 | ||||||||

| (0.275) | 0.000*** | ||||||||

| (0.000) | 0.033** | ||||||||

| (0.148) | 0.266 | ||||||||

| (0.305) |

-

•

* , ** , *** , with denoting the average -value.

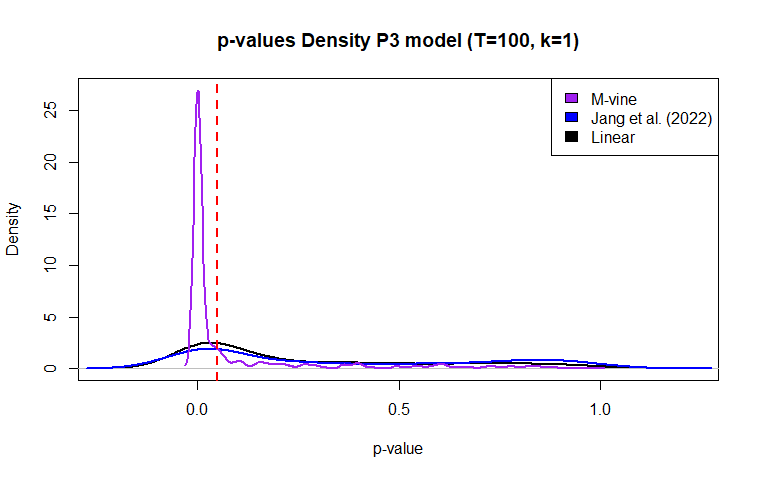

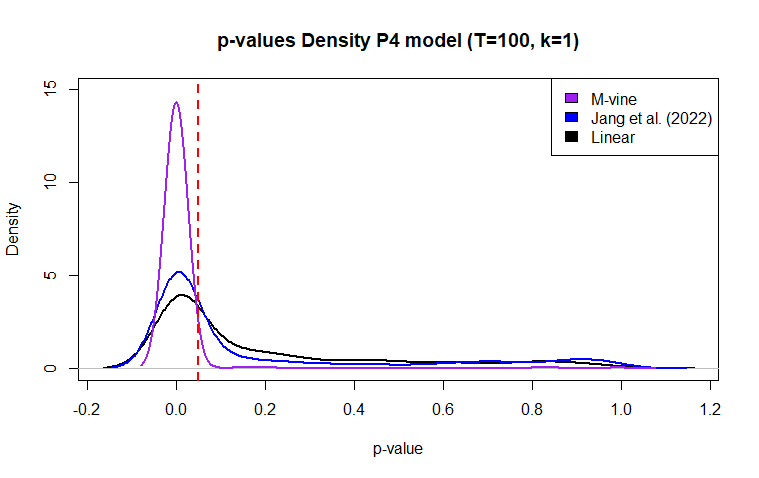

Table 3 and 3 show the average -value across simulations for each size and power assessment model, respectively, together with their empirical standard deviation. One can see that, on average, the -values for all methods are around the significance level in every size assessment model. However, those of the M-vine approach have the lower standard deviation among the three tests in all size models, both in small and larger samples. On the other hand, from Table 3, we can see that for the linear (P1) and close to linear (P2) model specifications, the -values of the Linear method are the ones that are, on average, further below the predefined significance level, also displaying the lower standard deviation. When working with non-linear dependence structures (P3 and P4), this no longer holds as the -values for the M-vine procedure are, on average, closer to the significance level, and they exhibit the lower empirical deviation out of the three methods. In Figure 1 we plot the distributions of the -values obtained with each method in cases P3 and P4 with in order to further support the previous considerations

Thus far, we have assumed that is a first-order Markov process (i.e. ), and, under this condition, the M-vine test results to have good statistical properties for sample size . In order to analyse how these properties change when working with higher-order Markov processes, we repeat the simulation study for the case . The selection of this particular Markov order is driven by the empirical application from Section 4, as it is the only other Markov order, besides , obtained by our selection procedure when fitting the M-vine models to the U.S. macroeconomic data (we refer to Section 4.1 for a detailed description of the data). To adjust the simulation study for , we modified the previously presented size and power assessment models so that they represent the same dependence structure scenarios, but letting be a bivariate Markov stationary stochastic process of order . The modified assessment models are given in Appendix A.2. Table 5 and Table 6 show the empirical size and power of each test when applied to a bivariate Markov stationary process of order . From them, we can see that overall the results exhibit the same pattern as the case of , with the M-vine test still outperforming in terms of power the S-vine test in both linear and non-linear assessment models. Moreover, when compared to the linear test, the M-vine test has a comparable performance when the processes have a linear or almost linear dependence and the sample size is large enough, while it performs better in non-linear cases. However, we note that for the order , the power of the M-vine test seems to converge to 1 at a slower pace than in the case of . Thus, for , we require a greater to let the M-vine test have a good power in the cases P3 and P4.

| Model | T=50 | T=100 | T=200 | ||||||

| M-vine | Jang et al. | Linear | M-vine | Jang et al. | Linear | M-vine | Jang et al. | Linear | |

| S1 | 0.066 | 0.070 | 0.040 | 0.048 | 0.040 | 0.032 | 0.042 | 0.070 | 0.048 |

| S2 | 0.054 | 0.046 | 0.050 | 0.048 | 0.044 | 0.040 | 0.058 | 0.038 | 0.050 |

| S3 | 0.058 | 0.058 | 0.052 | 0.054 | 0.088 | 0.052 | 0.058 | 0.080 | 0.060 |

| Model | T=50 | T=100 | T=200 | ||||||

| M-vine | Jang et al. | Linear | M-vine | Jang et al. | Linear | M-vine | Jang et al. | Linear | |

| P1 | 0.802 | 0.428 | 1.000 | 0.986 | 0.788 | 1.000 | 1.000 | 0.986 | 1.000 |

| P2 | 0.618 | 0.316 | 0.960 | 0.870 | 0.626 | 1.000 | 0.998 | 0.922 | 1.000 |

| P3 | 0.204 | 0.126 | 0.194 | 0.467 | 0.305 | 0.217 | 0.820 | 0.524 | 0.242 |

| P4 | 0.210 | 0.132 | 0.272 | 0.547 | 0.237 | 0.290 | 0.872 | 0.436 | 0.368 |

4 Application: energy consumption, economic growth and investment

The nexus between energy consumption and economic growth is important in times when economic and environmental sustainability are at stake. On the one hand, the correlation is positive everywhere in the world. No wealthy country consumes only a little energy, and no poor country consumes a lot of energy. Yet, beyond correlations, we believe it is important to investigate whether there is any Granger causality between the two variables, especially in a period in which we do have concerns about the impact on the environment and the depletion of natural resources that are needed to generate energy. In the latest decades, since Kraft and Kraft (1978), the nexus between energy consumption and economic growth has been analysed in a wide array of studies. Nonetheless, results appear to be diverse and often conflicting as some of them find neutrality, whilst others find a causal relationship, often running in different directions. As pointed out in Chen et al. (2007), the main reason for conflicting results might be the perspective taken from different countries that have their own energy policies, institutions, and cultural factors. However, we can find conflicting conclusions even when they refer to the same country. Indeed, the employment of data sets with different proxy variables for energy consumption or different temporal frequencies, as well as different econometric methods, can certainly contribute to different findings about the energy-growth relationship. Therefore, by now, previous literature (Payne, 2009b; Ozturk, 2010) has been inconclusive about policy recommendations for either a specific country or across different nations. Most of these studies apply a notion of Granger causality tests based on linear models, such as Vector Auto Regressive models (VAR). Only a small number of studies experiment with non-linear models (Huang et al. (2008), Chiou-Wei et al. (2008), Fallahi (2011)). In Appendix A.3, Table 10, we provide a snapshot of the results from different studies that specifically investigated Granger causality between energy consumption and economic growth with a focus on the United States. Finally, we include in our study also the U.S. time series for investment, proxied by using the Gross Fixed Capital Formation, to show how Granger causality can work differently when considering a variable that is not supposed to have a short-term impact on GDP. Crucially, we decide to investigate the U.S. case for two reasons. On the one hand, it is the most investigated case, and we will not find it difficult to compare our results with previous applications. On the other hand, it is easier to find longer time series that are available for our variables of interest.

4.1 Data

We assemble our data set from different sources. We obtain real GDP and Gross Fixed Capital Formation (investment hereafter) from the Federal Reserve Economic Data (FRED) as made available by the Federal Reserve Bank of St. Louis 222Accessible through https://fred.stlouisfed.org/. Energy consumption data are proxied by the so-called total primary energy consumption measured in quadrillion British thermal units (BTU), which is made freely available by the U.S. Energy Information Administration (EIA) 333Accessible through https://www.eia.gov/opendata/. Crucially, we consider all the time series with a quarterly frequency in the period 1973-2018.

| Variable | Notation |

| Real GDP | |

| Energy Consumption | |

| Investment |

4.2 Results

A preliminary investigation of the time series for this empirical application is available in Appendix A.4. To proceed, we need stationarity of the time series. Thus, we work with the first differences of original variables after testing that they are indeed stationary by means of the Phillips-Perron test (Phillips and Perron, 1988). First of all, we focus on how the fit to the entire data set of an M-vine model compares to both an S-vine model (on which the test from Jang et al. (2022) is based) and a traditional linear model, i.e., a VAR. Table 8 shows the results of the fit of these models in terms of the Akaike Information Criterion (AIC) for each pair of variables considered in the analysis. The Markov order of each bivariate process is selected by iteration, fitting M-vine copulas with Markov orders from to , thus keeping the one with the better fit according to the AIC. Analogously, the same process is repeated for the case of S-vine models. For the linear model, we select the optimal amount of lags in the bivariate VAR models based on the AIC. That is, we sequentially fit VAR models with an increasing number of lags, and then we pick the one with the minimum AIC 444Please note that we implement the command VARselect from the RStudio package VAR Modelling (vars)..

| Variables | M-vine | S-vine | VAR |

| -50.69 | |||

| -50.69 | |||

| 2185.22 | |||

| -226.27 | |||

| -226.27 | |||

| 3529.93 | |||

| -333.70 | |||

| -273.62 | |||

| 1967.58 |

Table 8 put in evidence the non-linear dependence structure between every pair of considered variables: indeed, once we allow for non-linear models, the goodness of fit is considerably higher. Furthermore, when comparing the goodness of fit between the two vine copula models, one can notice that the M-vine and the S-vine models exhibit almost the same AIC. In particular, in the first two cases, the model selected is exactly the same for both vine copula models, suggesting that the M-vine is the structure that has the best goodness of fit among all the vine structures that can represent stationary time series (i.e. S-vine copulas).

| Causality flow | |||

| (fromto) | (M-vine) | (Jang et al.) | (Linear) |

| 0.015** | 0.030** | 0.078* | |

| 0.080* | 0.395 | 0.206 | |

| 0.535 | 0.710 | 0.465 | |

| 0.265 | 0.195 | 0.006*** | |

| 0.200 | 0.140 | 0.436 | |

| 0.035** | 0.045** | 0.032** |

-

•

* , ** , *** . The null hypothesis of no Granger causality is rejected at a given significance level if .

The results we obtain with our M-vine test, the test from Jang et al. (2022), and the more traditional test based on a linear model are prima facie relatively similar. Please recall that the null hypothesis of these tests is that no Granger causality exists, and it is rejected at a given significance level if . Remarkably, the most important difference in the results is for the pair GDP and energy consumption. In fact, as Table 9 shows, all three methods find that Granger causality runs from GDP to energy consumption, although the linear test shows a relatively weaker statistical significance at level, in line with the findings from Kraft and Kraft (1978), Fallahi (2011) and Aslan et al. (2014).

Interestingly, only the M-vine test detects an inverse Granger causality from energy consumption to GDP at the level. In this specific case, findings are in line with Stern (1993, 2000); Bowden and Payne (2009); Fallahi (2011). As shown in Table 8, the difference we observe when we compare the M-test and the VAR is due to a non-linear dependence structure between the variables. In this case, we argue that the M-vine and the S-vine tests are better than a classical VAR test at catching the underlying functional form. Moreover, as already shown with the simulation study in previous paragraphs, the M-vine test outperforms the S-vine test thanks to the methodological differences we discussed in section 2.2. Hence, the differences that we record in the -values of Table 9.

Notably, our findings point to a two-way Granger causality between energy consumption and GDP that is important from an economic perspective. Inevitably, energy consumption is a relevant expenditure component for consumers and producers of any budget. For this reason, economic growth is reflected necessarily on increasing energy consumption. From another point of view, we can say that the demand for energy is quite rigid for both consumers and producers.

Please note how another important difference arises when we test the pairwise causal relationship between investment and economic growth. In this case, the linear test rejects the null hypothesis, thus finding evidence of a Granger causality that runs from investment to GDP, whilst both non-linear tests find no Granger-causal relationship in either direction. In this regard, please consider that Table 8 shows the VAR model has absolutely the worst fit when modelling the dependence structure between investment and economic growth. Once again, we believe this is a hint that the results of non-linear tests are more reliable when applied to relationships that can hardly be proxied as linear. From an economic perspective, we know that investment might not have a direct effect on GDP, but it can contribute indirectly to economic growth in the medium term after raising the technological abilities of a country and, thus, its production.

Finally, all three methods find evidence that investment Granger-causes energy consumption growth. In this case, we believe that the tests are catching the intrinsic prediction power of investment plans that always require the use of additional energy resources.

5 Concluding remarks

Motivated by the recent literature about non-linear Granger causality tests, our aim was to construct a semi-parametric Granger causality-in-the-mean test for bivariate -Markov stationary processes based on vine copulas. Departing from the procedure in Jang et al. (2022), we added coherence between the two parts of the test, i.e, the estimation of the Granger causality measure and the computation of the -value, by fitting the same M-vine structure in both parts. In addition, we modified the approach by fitting the vine copula model to the entire sample. Therefore, by means of a simulation study with time series from different data generating processes and Markov orders, we showed that we improve on the statistical properties, making the proposed M-vine test an excellent tool for testing Granger causality in the presence of non-linear dependence structures.

Finally, in an application, we use the M-vine test to study the relationship between energy consumption, economic growth and investment in the U.S. Crucially, the copula-based M-vine test revealed a two-way Granger causality between energy consumption and GDP that was not detected by the other tests. We argue that, indeed, a quite rigid demand for energy can be the basis for the two-way prediction power in the relationship.

More in general, we conclude that vine copulas are able to model the dependence structure of multiple stochastic processes, better catching intrinsic non-linearities. A possible avenue for future research is the extension of vine copula-based tests to multivariate settings.

Acknowledgments

Irene Crimaldi is partially supported by the project MOTUS - Automated Analysis and Prediction of Human Movement Qualities (code P2022J8AXY, cup: D53D23017470001), financed by the Italian Ministry of University and Research (PRIN 2022 PNRR)

Appendix A Appendix

A.1 Vine copula models

Copula models constitute a type of dependence-capturing models, which in contrast to VAR allow for non-linear dependences when working with high dimensional data. Their advantage relies on the fact that the univariate distributions of the elements from a multivariate system can be selected freely and then model the dependence structure independently of these marginals by linking them through an appropriate copula function. However, copula functions have their own limitations. Particularly, when dealing with high-dimensional random vectors the set of available parametric copulas is considerably limited and so the selection of a suitable high-dimensional copula function could result difficult. Vine copulas come as an alternative: since the large amount of existing bivariate copula families to be employed, the vine copula approach consists in the decomposition of a multivariate copula density into a product of bivariate copula densities through the use of the pair-copula construction (Joe (1996)). Nevertheless, the number of possible decompositions becomes difficult to track and organize: in fact, the number of possible decompositions increases super-exponentially with the dimension of the random vector (Morales Napoles, 2010). Then, Regular vines (R-vines) were introduced as a graphical way of specifying the sequence of trees that characterises all valid factorizations of a -dimensional copula. Briefly, as defined on Cooke and Kurowicka (2006) an R-vine on random variables is a set of graphs where each tree has a node set and an edge set , such that:

-

1.

has node set and edge set . Namely, each node of is associated to one variable from the random vector whose dependence is being modeled.

-

2.

For , has node set .

-

3.

Proximity condition: if two edges in tree are joined as nodes in the following tree , then they must share a common node in .

Each edge in any of the trees of a given R-vine is associated to a bivariate copula and three subsets of the nodes from the first tree , they are:

-

•

: the conditioning set of .

-

•

: the conditioned set of which contains necessarily two elements.

-

•

: the complete union of , that is .

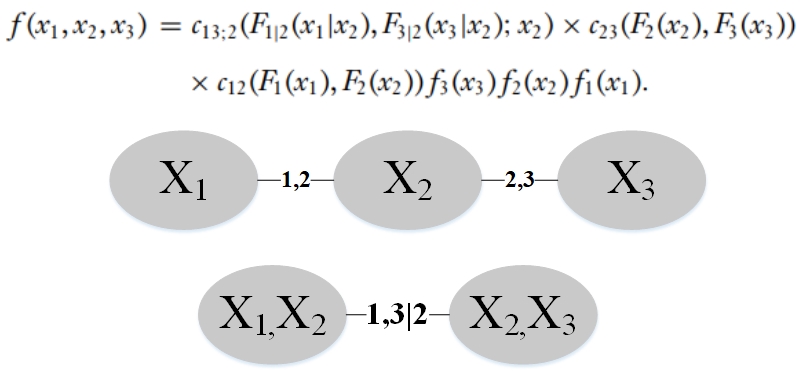

Figure 2 provides an example of one possible pair copula decomposition for a three dimensional random vector, which is going to be used to clarify the introduced concepts. To begin with, notice that, since we are working in dimension three, the total number of trees is 2. The first tree has node set and edge set , whereas the second tree has and respectively. Furthermore, let us consider the edge which has conditioning set , conditioned set and thus its complete union is .

To generalise, for a -dimensional random vector , its joint density can be expressed as the following product of bivariate copula densities and of all the marginal densities:

A.1.1 Vine copula models for stationary time series: S-vine copulas

Remarkably, R-vines are only able to capture the cross-sectional dependence of a random vector: indeed, they model the joint distribution of a random vector , leveraging on independent observations of it. Therefore, afterwards, vine copula specifications for modeling time series that are able to capture both cross-sectional and serial dependence have been developed (Brechmann and Czado (2015), Beare and Seo (2015), Smith (2015) and Nagler et al. (2022)). In particular, the latter work (Nagler et al. (2022)) builds upon the previous papers to generalize all the vine copula structures that can guarantee strict stationarity of a time series. Instead of considering a random vector whose observations are assumed independent over time, we take a stationary time series for which we aim to capture its cross-sectional and serial dependence through a vine copula specification. Therefore, we now aim to model a joint distribution in the form of . Note that, before each node from the first tree corresponds to one of the considered random variables (); whereas the nodes from the first tree are now associated to a tuple corresponding to the random variable , where represents the time period and is the variable index. The same applies for the elements of the conditioned set and the conditioning set associated to each edge .

Graphically, the structure of these models can be seen as a vine that captures the cross sectional dependence of each vector . Then, each of these cross-sectional vines are connected between two consecutive time periods and through one edge linking one vertex from each of them. S-vine copulas allow for arbitrary cross-sectional structures and also an arbitrary selection of the variable that is going to connect two consecutive cross-sectional vines. In terms of estimation, S-vines select the edge between the two variables that have the highest correlation between time periods.

A.1.2 A sub-class of S-vine copulas: M-vine copulas

M-vine copula models were one of the first vine copula structures able to represent time series by accounting for both cross sectional and serial dependence. They were first introduce in Beare and Seo (2015), particularly, in order to model stationary multivariate higher order Markov chains. Formally, a regular vine on the node set with trees , , is an M-vine if the following conditions are satisfied:

-

1.

-

2.

For each pair of adjacent columns , , the restriction of to is a Drawable vine (D-vine).

where the restriction555For a formal definition we refer to Definition 6 in Beare and Seo (2015). of to corresponds to the structure that is left after all nodes that are not included in are deleted from , as well as all the edges in the first tree of that are connected to these nodes and the edges in subsequent trees that would include them.

Graphically, M-vines can be seen as cross-sectional vines that are connected to the vine associated to the following (and/or previous) time period through an edge linking two nodes that lie in the same end of the vine, i.e between nodes and as represented in Figure 3. These class of structures are able to guarantee stationarity of a multivariate time series, in fact Theorem 3 from Beare and Seo (2015) shows that a multivariate time series that realises a M-vine copula specification is stationary if and only if the M-vine structure is translation invariant. Intuitively, translation invariance requires that the cumulative distribution functions associated to any two nodes in the same row of the first tree structure are the same, and that the same copula is assigned to any two edges whose conditioned and conditioning set differs just by column translations, i.e translations across time. Additionally, M-vines can represent -Markov stationary time series, imposing the Markov property by requiring certain copulas from the vine specification to be independence copulas. For a formal definition of translation invariance and the required conditions to ensure the -Markov property of a given time series using M-vine structures, we refer to Definition 9 and Theorem 4 from Beare and Seo (2015), respectively.

The main difference between M-vine and S-vine copulas rely on the fact that the tree structures for a M-vine are fixed as the cross-sectional vines have to be connected across time periods through an edge between two nodes lying in the same end of the vine. On the other hand, S-vines allow for general cross-sectional structures (not necessarily D-vines) and provide a higher degree of freedom for connecting them across time compared to M-vines. This indeed provide more flexibility for S-vines in order to fit different kind of data; however, in cases when we need to guarantee the presence of one or some specific copulas in the vine structure, this can be an undesirable feature: for instance, in the bootstrap procedure from Part B of Section 2.1, where the copulas and are needed to generate bootstrapped samples under the null hypothesis, using an S-vine structure is not feasible as these two copulas might not appear in its first tree. Therefore, even if S-vines constitute a more general class of vine copulas that can ensure stationarity of a time series (in which M-vines are a sub-class), for some cases where we need to impose some particular conditions on the dependence structure, fitting a more restrictive vine structure (e.g. an M-vine) could be beneficial.

A.2 Size and power assessment models for

Size assessment models

- S1

-

,

- S2

-

,

- S3

-

,

Power assessment models

- P1

-

,

- P2

,

,

where are i.i.d from a standard bivariate normal distribution.

A.3 Previous literature: Granger-causality relationship between Energy Consumption and Economic Growth

We here provide a summary of the results provided by the previous literature related to the Granger causality between energy consumption and economic growth in the United States.

| Author(s) | Time period | Model | Causality flow |

| Kraft and Kraft (1978) | 1946-1974 | VAR | |

| Yu and Hwang (1984) | 1974-1990 | VAR | |

| Stern (1993) | 1947-1990 | VAR | |

| Stern (2000) | 1948-1994 | VAR | |

| Payne (2009a) | 1949-2006 | VAR | |

| Bowden and Payne (2009) | 1949-2006 | VAR | |

| Fallahi (2011) | 1960-2005 | Markov switching VAR | |

| Aslan et al. (2014) | 1973-2013 | Wavelet analysis and VAR |

Notes: Given two variables and , notation refers to a unidirectional flow of Granger-causality from variable to , illustrates a bidirectional flow of Granger-causality between both variables, and refers to the case of no Granger causality between them in any directions.

A.4 Preliminary time series analysis for the application

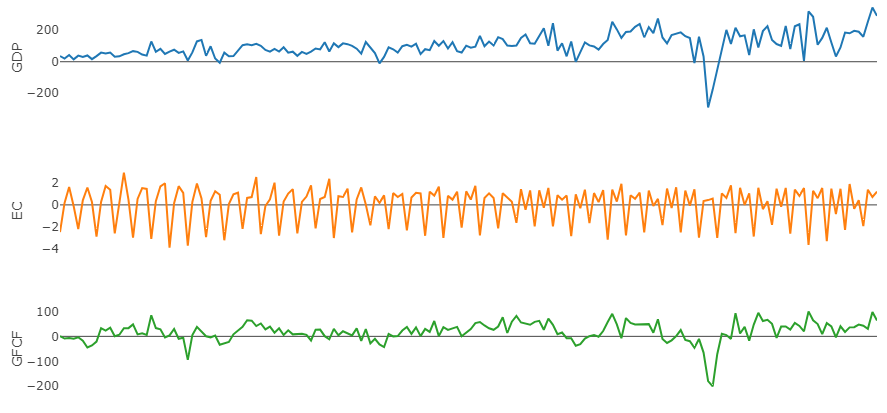

As presented in Figure 4, one can observe that each variable that is considered in the analysis seems to be stationary, in first differences, around their respective means.

Moreover, we test the presence of unit roots through a Phillips-Perron test (Phillips and Perron, 1988) applied to each series in first differences. Recall, that the null hypothesis of the Phillips-Perron test is that the series has a unit root. Given the results in Table 11, we are able to see that the null hypothesis is rejected at a significance level, supporting the previous intuition that every series considered in first differences is stationary.

| Variable | -value |

References

- Ancona et al. (2004) Ancona, N., D. Marinazzo, and S. Stramaglia (2004, Nov). Radial basis function approach to nonlinear granger causality of time series. Phys. Rev. E 70, 056221.

- Aslan et al. (2014) Aslan, A., N. Apergis, and S. Yildirim (2014). Causality between energy consumption and gdp in the u.s.: Evidence from wavelet analysis. Frontiers in Energy 8(1), 1 – 8. Cited by: 61.

- Bai et al. (2017) Bai, Z., Y. Hui, Z. Lv, W.-K. Wong, and Z.-Z. Zhu (2017). The hiemstra-jones test revisited.

- Beare and Seo (2015) Beare, B. K. and J. Seo (2015). Vine copula specifications for stationary multivariate markov chains. Journal of Time Series Analysis 36(2), 228–246.

- Bowden and Payne (2009) Bowden, N. and J. E. Payne (2009). The causal relationship between u.s. energy consumption and real output: A disaggregated analysis. Journal of Policy Modeling 31(2), 180–188.

- Brechmann and Czado (2015) Brechmann, E. C. and C. Czado (2015). Copar—multivariate time series modeling using the copula autoregressive model. Applied Stochastic Models in Business and Industry 31(4), 495–514.

- Candelon and Tokpavi (2016) Candelon, B. and S. Tokpavi (2016). A nonparametric test for granger causality in distribution with application to financial contagion. Journal of Business & Economic Statistics 34(2), 240–253.

- Chen et al. (2007) Chen, S.-T., H.-I. Kuo, and C.-C. Chen (2007). The relationship between gdp and electricity consumption in 10 asian countries. Energy Policy 35(4), 2611–2621.

- Chiou-Wei et al. (2008) Chiou-Wei, S. Z., C.-F. Chen, and Z. Zhu (2008). Economic growth and energy consumption revisited – evidence from linear and nonlinear granger causality. Energy Economics 30(6), 3063–3076.

- Cooke and Kurowicka (2006) Cooke, R. and D. Kurowicka (2006). Uncertainty Analysis With High Dimensional Dependence Modelling.

- Czado and Nagler (2022) Czado, C. and T. Nagler (2022). Vine copula based modeling. Annual Review of Statistics and Its Application 9(Volume 9, 2022), 453–477.

- Diks and Panchenko (2006) Diks, C. and V. Panchenko (2006). A new statistic and practical guidelines for nonparametric granger causality testing. Journal of Economic Dynamics and Control 30(9), 1647–1669. Computing in economics and finance.

- Diks and Wolski (2016) Diks, C. and M. Wolski (2016). Nonlinear granger causality: Guidelines for multivariate analysis. Journal of Applied Econometrics 31(7), 1333–1351.

- Fallahi (2011) Fallahi, F. (2011). Causal relationship between energy consumption (ec) and gdp: A markov-switching (ms) causality. Energy 36(7), 4165–4170.

- Granger (1969) Granger, C. W. J. (1969). Investigating causal relations by econometric models and cross-spectral methods. Econometrica 37(3), 424–438.

- Hiemstra and Jones (1994) Hiemstra, C. and J. D. Jones (1994). Testing for linear and nonlinear granger causality in the stock price-volume relation. The Journal of Finance 49(5), 1639–1664.

- Huang et al. (2008) Huang, B.-N., M. Hwang, and C. Yang (2008). Causal relationship between energy consumption and gdp growth revisited: A dynamic panel data approach. Ecological Economics 67(1), 41–54.

- Hyuna Jang and Noh (2023) Hyuna Jang, J.-M. K. and H. Noh (2023). Vine copula granger causality in quantiles. Applied Economics 0(0), 1–10.

- Jang et al. (2022) Jang, H., J.-M. Kim, and H. Noh (2022). Vine copula granger causality in mean. Economic Modelling 109, 105798.

- Joe (1996) Joe, H. (1996). Families of m-variate distributions with given margins and m(m-1)/2 bivariate dependence parameters. Lecture Notes-Monograph Series 28, 120–141.

- Kim et al. (2020) Kim, J.-M., N. Lee, and S. Y. Hwang (2020). A copula nonlinear granger causality. Economic Modelling 88, 420–430.

- Kraft and Kraft (1978) Kraft, J. and A. Kraft (1978). On the relationship between energy and gnp. The Journal of Energy and Development 3(2), 401–403.

- Lee and Yang (2014) Lee, T. H. and W. Yang (2014). Granger-causality in quantiles between financial markets: Using copula approach. International Review of Financial Analysis 33(C), 70–78.

- Morales Napoles (2010) Morales Napoles, O. (2010). Counting Vines, pp. 189–218.

- Nagler et al. (2022) Nagler, T., D. Krüger, and A. Min (2022). Stationary vine copula models for multivariate time series. Journal of Econometrics 227(2), 305–324.

- Ozturk (2010) Ozturk, I. (2010). A literature survey on energy–growth nexus. Energy Policy 38(1), 340–349.

- Paparoditis and Politis (2000) Paparoditis, E. and D. Politis (2000, 02). The local bootstrap for kernel estimators under general dependence conditions. Annals of the Institute of Statistical Mathematics 52, 139–159.

- Payne (2009a) Payne, J. E. (2009a). On the dynamics of energy consumption and output in the us. Applied Energy 86(4), 575–577.

- Payne (2009b) Payne, J. E. (2009b). Survey of the international evidence on the causal relationship between energy consumption and growth. Journal of Economic Studies 37(1), 53–95.

- Phillips and Perron (1988) Phillips, P. C. B. and P. Perron (1988). Testing for a unit root in time series regression. Biometrika 75(2), 335–346.

- Shojaie and Fox (2022) Shojaie, A. and E. B. Fox (2022). Granger causality: A review and recent advances. Annual Review of Statistics and Its Application 9(1), 289–319.

- Smith (2015) Smith, M. (2015). Copula modelling of dependence in multivariate time series. International Journal of Forecasting 31(3), 815–833.

- Song and Taamouti (2018) Song, X. and A. Taamouti (2018, April). Measuring Nonlinear Granger Causality in Mean. Journal of Business & Economic Statistics 36(2), 321–333.

- Song and Taamouti (2021) Song, X. and A. Taamouti (2021). Measuring granger causality in quantiles. Journal of Business & Economic Statistics 39(4), 937–952.

- Stern (1993) Stern, D. I. (1993). Energy and economic growth in the usa: A multivariate approach. Energy Economics 15(2), 137–150.

- Stern (2000) Stern, D. I. (2000). A multivariate cointegration analysis of the role of energy in the us macroeconomy. Energy Economics 22(2), 267–283.

- Yu and Hwang (1984) Yu, E. S. and B.-K. Hwang (1984). The relationship between energy and gnp: Further results. Energy Economics 6(3), 186–190.