Cointegrated Matrix Autoregression Models

Abstract

We propose a novel cointegrated autoregressive model for matrix-valued time series, with bi-linear cointegrating vectors corresponding to the rows and columns of the matrix data. Compared to the traditional cointegration analysis, our proposed matrix cointegration model better preserves the inherent structure of the data and enables corresponding interpretations. To estimate the cointegrating vectors as well as other coefficients, we introduce two types of estimators based on least squares and maximum likelihood. We investigate the asymptotic properties of the cointegrated matrix autoregressive model under the existence of trend and establish the asymptotic distributions for the cointegrating vectors, as well as other model parameters. We conduct extensive simulations to demonstrate its superior performance over traditional methods. In addition, we apply our proposed model to Fama-French portfolios and develop a effective pairs trading strategy.

KEYWORDS: Cointegration; Multivariate Time Series; Matrix-valued Time Series; Pairs Trading.

1 Introduction

Cointegration refers to a long-run, stable relationship between two or more non-stationary time series data. It has become more and more observed and recognized in econometrics, finance, and other fields. The term ‘cointegration’ was first introduced in the late 1980s, see Granger (1981), Granger and Weiss (1983) and Engle and Granger (1987). Since then, the phenomenon of cointegration has been widely studied and various methods have been developed for testing and estimation. Statistical analyses of cointegration models were developed by Johansen (1988), Johansen (1991), and Johansen et al. (1995), among others. They derived the testing of cointegration ranks between multiple time series variables and the maximum likelihood estimator of the cointegrating vectors through a vector error correction model (VECM), which is now widely used and considered to be standard in the literature.

Recently, Wang (2014) studied the martingale limit theorem for a nonlinear cointegrated regression model. Doornik (2017) proposed a novel estimation procedure for the I(2) cointegrated vector autoregressive model. Franchi and Johansen (2017) studied the vector cointegration model allowing for multiple near unit roots using adjusted quantiles. Cai et al. (2017) studied the bivariate threshold VAR cointegration model. Zhang et al. (2019) proposed a new method for identifying cointegrated components of nonstationary time series. She and Ling (2020) studied the full rank and reduced rank least squares estimators of the heavy-tailed vector error correction models. Gao and Tsay (2021) proposed a new procedure to build factor models for high-dimensional unit-root time series. Guo et al. (2022) proposed an automated estimation method of heavy-tailed vector error correction models. To the best of our knowledge, there has been no prior research on cointegration for matrix-valued time series. This paper aims to fill this gap in the literature by presenting a cointegrated matrix autoregressive models (CMAR).

In this paper, we present a novel extension of the cointegrated VAR model, which focuses on the cointegration of matrix-valued time series, denoted by , a matrix observed at time . We introduce the error correction model in bilinear form, with row-wise and column-wise cointegrating vectors and , respectively, which enable the transformation of into a stationary process , while the original process is a non-stationary I(1) process. Our proposed approach presents a promising alternative to traditional cointegration analysis, which is in line with the recent work on autoregressive models for stationary processes by Chen et al. (2021), Xiao et al. (2021).

To estimate the coefficient matrices, especially the cointegrating vectors, for the proposed model, we introduce two different estimators based on the least squares and likelihood principles respectively. We obtain both the least squares estimator (LSE) and the maximum likelihood estimator (MLE) using iterative algorithms. We establish the asymptotics for all the proposed estimators, with a special focus on the estimators of the cointegration space, represented by . Our analysis reveals that the process may exhibit different properties in different directions. These findings have important implications for the interpretation and analysis of the cointegration phenomenon of the matrix-valued time series. The proposed estimators are evaluated through extensive simulations, with better performance over traditional vector cointegration methods.

To demonstrate the practical application of our proposed approach, we develop a pairs trading strategy using real-world data from the Fama-French portfolios. Given that the stocks can be naturally grouped into a matrix format based on factors such as Operating Profitability and Book-to-Market ratio, we apply our model and build an equilibrium relationship among the portfolios. Leveraging this stationary relationship, we can execute short and long trades accordingly. The back-testing results demonstrate that our strategy has the potential to outperform the market, especially during bear markets.

The rest of this paper is organized as follows. We briefly review the cointegrated vector autoregressive models, and then introduce the cointegrated matrix autoregressive model in Section 2, and discuss its basic properties. The estimators are presented in Section 3. Asymptotic properties of the estimators are established in Section 4. In Section 5, we carry out extensive numerical studies to demonstrate the properties and performance of the model and the corresponding estimators, and compare with the classical vector cointegration models. In Section 5.2, we develop a pairs trading strategy based on the proposed matrix cointegration model. All the proofs and some additional theorems and simulations are collected in Appendix Cointegrated Matrix Autoregression Models.

Notations. For ease of reading, here we highlight some notations that are frequently used. Throughout this paper, we use the bold uppercase letters for matrices (e.g. ), and the bold lowercase letters for vectors (e.g. ). We use and to denote the matrix Frobenius norm and spectral norm respectively. The Kronecker product of two matrices is denoted by . Note that the notations , refer to some new matrices to be defined later, and they should not be regarded as entries of or . For any matrix of full rank (assuming ), we denote by a matrix of rank such that . We define , such that , and is the projection of onto the space spanned by the columns of . We use to denote the difference operator such that .

2 Cointegrated Matrix Autoregression Models

2.1 Cointegrated Vector Autoregression Models

To fix notations, we briefly introduce some basic concepts about the cointegrated vector autoregression models (CVAR). For a more thorough analysis on the vector cointegration models, see Johansen et al. (1995).

Consider a vector time series . If we allow unit roots in the characteristic polynomial of the process that is non-stationary, but some linear combination , , can be made stationary by a suitable choice of , then is called cointegrated and is the cointegrating vectors. The number of linearly independent cointegrating vectors is called the cointegration rank, and the space spanned by the cointegrating vectors is the cointegration space. We define the order of cointegration as follows.

Definition 1.

The vector process is called integrated of order zero I(0) if such that . It is called integrated of order one I(1) if is I(0).

The autoregressive equations are given in the error-correction form

| (1) |

where the are IID , is a constant term. The equations determine the process as a function of initial values , and the . Let denote the vector polynomial derived from (1),

The basic assumption which will be used throughout is as follows,

Assumption 1.

The characteristic polynomial satisfies the condition that if , then either or .

If is a root we say that the process has a unit root. The following representation theorem in Johansen et al. (1995) provides sufficient and necessary conditions on the coefficients of the autoregressive model for the process to be integrated of order one.

Theorem 1.

If implies that or , and , such that , where , are matrices of rank . A necessary and sufficient condition that and can be given initial distributions such that they become I(0) is that has full rank. In this case the solution of (1) has the representation

| (2) |

where , . Thus is a cointegrated I(1) process with cointegrating vectors .

By building upon the aforementioned results, a comprehensive framework was established for formulating and estimation in the context of cointegration, as detailed in works such as (Johansen, 1988, 1991; Johansen et al., 1995; Johansen and Swensen, 1999), among others. In the following sections, we extend these works to the case of matrix time series.

2.2 Cointegrated MAR Models

At each time , a matrix is observed. We introduce the cointegrated matrix autoregression models (CMAR) of the form

| (3) |

where are coefficient matrices of ranks , and are coefficient matrices without rank constraints, for , . The matrix is a constant term. is a matrix white noise. The low rank assumption implies that where and are both full rank matrices. and are cointegrating vectors.

The model (3) offers a parsimonious representation of the cointegrated vector autoregressive models (CVAR). Taking vectorization on both sides of (3), it becomes

| (4) |

In comparison to the CVAR model (1), the CMAR model imposes further constraints on the coefficients by requiring them to take the form of a Kronecker product, such that , , and the cointegrating vectors . If the vector process is integrated of order one such that is stationary, then it is equivalent to say the matrix process is stationary. The concept of I(0) and I(1) for matrix-valued time series can be naturally extended from the vector case.

Definition 2.

The matrix process is called integrated of order zero I(0) if such that . It is called integrated of order one I(1) if is I(0).

The characteristic polynomial for the process given in (3) is

The unit root condition of a matrix time series can be expressed as follows:

Assumption 2.

If , then either or .

A necessary and sufficient condition that and can be given initial distributions such that they become I(0) is that satisfies the conditions of Theorem 1. It is worth noting that if is I(0), then is stationary. However, either or may not be stationary. Therefore, both row-wise and column-wise cointegrating vectors are necessary.

2.3 Identifiability

If we require that and , , then each coefficient matrix , , , is identified up to a sign change. We also assume is the left singular vectors of such that , . The estimators can be normalized by any non-zero matrix , denoted as . Note that the projection matrix would remain unique regardless of how we normalize , i.e., the choice of non-zero matrix would not affect the projection matrix. In section 4, we first derive asymptotic results for , such that is normalized by . We then extend this to the estimators with any normalizing matrix that . Then we establish the asymptotic distribution for the projection matrix .

3 Estimation

We propose to use the alternating algorithm, updating one, while holding the other fixed. Specifically, suppose in the model (3), , are given, we discuss how to estimate , , and . The previous studies by Chen et al. (2020), Zebang et al. (2021), and Xiao (2021) have also employed a similar alternating algorithm to estimate the coefficients, but their analysis assumed that the process was stationary, while our model is in the error-correction form. To avoid confusion, we adopt the convention that denotes the -th column of . The -th column of the model equation (3) can be written as

which can be viewed as the cointegrated vector autoregressive models when , are fixed. For the estimation, in Section 3.1, we introduce the MLE estimator when is separable, which is related to maximum likelihood analysis in Johansen et al. (1995) and canonical correlation analysis in Anderson (2003), Velu and Reinsel (2013). Then we consider the least squares method in Section 3.2. The MLE and LSE estimators are respectively denoted as and .

3.1 Maximum Likelihood Estimation

We commence our analysis of the likelihood by examining a basic model,

| (5) |

which we later extend it to the model (3). We assume that the covariance matrix of takes the form of a Kronecker product

| (6) |

Under the normality, the log likelihood of the model (5) is given apart from a constant by

| (7) |

We describe an iterative procedure to estimate and given and . We rewrite the model by columns as

Let , and , then the preceding equation can be viewed as a cointegrated vector autoregressive model with IID errors:

| (8) |

Then we can apply the estimation procedure of Maximum Likelihood Estimation (MLE) in the classical vector cointegration analysis (Johansen et al., 1995), which is also similar to the reduced rank regression (Anderson, 2003; Velu and Reinsel, 2013). Let

where the full rank estimation . Take , where is the -th leading unit eigenvector of . Then , can be updated as

Given and , an update of and can be similarly obtained.

Next, we extend the aforementioned analysis to model (3), which involves additional differentiation of previous observations. Similarly, we can express model (3) by columns as follows:

Let , , and be stacked vector variables

with length . Let be the coefficient corresponding to with dimension , which is the matrix consisting of . Let . Thus, the above equation can be regarded as a cointegrated vector autoregressive model in the error-correction form,

| (9) |

Apart from the previously defined and , we require the following notations:

The full rank least squares estimator is given by and , where , . Denote . Let

Take . is the -th leading unit eigenvector of . Then , , can be updated as

where . It involves a joint estimation with stacked estimated parameters , such that the leading sub-matrix is , and the last sub-matrix is . Given , and , an update of , and can be similarly obtained.

3.2 Least Squares Estimation

We denote the least squares estimator by . Suppose are given. The alternating lease squares estimator of the model (3) minimizes the following residuals under the rank constraint :

| (10) |

Take , where is the -th leading unit eigenvector of . Define . Then , can be updated as

where , ,

Given and , an update of and can be similarly obtained.

4 Asymptotics

In this section, we give the asymptotic distribution of the LSE and MLE estimators of the general form (3), where denoted as and . We first establish the central limit theorem of , and . Then we derive asymptotic results for , such that is normalized by . We then extend this to the estimators with any normalizing matrix that . We also establish the asymptotic distribution for the projection matrix . The asymptotic analysis involve heavy notations. First of all, we make the convention that , and , . In the table below, we list notations that appear in Theorems of both LSE and MLE estimators.

| Notations | |

|---|---|

| for | |

| , where | |

| the estimator normalized by such that | |

| the estimator normalized by such that | |

| , and orthogonal to and , where | |

| is the SVD decomposition | |

| , where , , | |

| , |

Define

where . Then define , and , where , and for .

4.1 Asymptotics for matrix I(1) processes

The probability properties of a matrix I(1) process provide the foundation for analyzing the asymptotic distribution of proposed estimators. In this section, we extend some classical results for vector I(1) processes to matrix I(1) processes. By the Representation Theorem 1, after vectorization, the process (3) can be expressed as a combination of a random walk, a linear trend and a stationary process:

| (11) |

where , , , , and is the stationary part. Denote , , as the -dimensional Brownian motion such that is . Then we have

Denote . By the formula of , we have . If , the Singular Value Decomposition (SVD)

in which is a square diagonal matrix of size , is a semi-unitary matrix. Then we can take and be orthogonal to and , such that . Then the estimator

| (12) |

where , , .

Lemma 1.

Let and be orthogonal to and where is the compact SVD decomposition. Then has full rank . As and , we have

| (13) | ||||

| (14) |

Define then we have

It follows that

| (15) |

where .

The proof is given in Appendix B. Thus, the asymptotic properties of the process depend on which linear combination of the process we consider. If we examine the processes , , and separately, we observe different types of dominant terms. In particular, for , the process is dominated by the linear trend, while for , the dominating term is the random walk part. If we consider linear combinations of the form , the process becomes stationary.

To introduce the asymptotics of estimators, we introduce some notations following the results of Lemma 1.

| (16) |

such that

Similarly, we can define and we combined the rows of , to make ,

4.2 Asymptotics for LSE estimators

Theorem 2.

Assume that are IID with mean zero and finite second moments. Assume that , and the Assumption 2 holds. Then the asymptotic distribution of the LSE estimator is given by

| (17) |

where , .

The proof is given in Appendix B. The parameters not involving cointegrating vectors and constant terms are asymptotically normal under a convergence rate of . Theorem 2 includes the CVAR model considered Johansen et al. (1995) as a special case with . The asymptotic properties of the constant term can be obtained directly from Johansen et al. (1995), and we put it in Appendix A.

Theorem 3.

Assume the same conditions as Theorem 2. In addition, assume the error matrix are IID normal. It holds that

| (18) |

Corollary 1.

The proof of Theorem 3 and Corollary 1 are given in Appendix B. It is shown above is super-consistent that . And note that the speed of convergence is different in the different directions and corresponding to different behaviors of the process and as given in Lemma 1. As we known is normalized by such that . Next, we generalize the results to the estimators with any normalizing matrix that .

Theorem 4.

Assume the same conditions as Theorem 3. Let , , such that , . Then we have

| (21) | |||

| (22) |

where , and , are block sub-matrices such that .

Furthermore, we examine the estimated cointegration space, represented by the projection matrix , which is unique regardless of the choice of normalization. Note the true cointegration space , since we require , .

Theorem 5.

Assume the same conditions as Theorem 3. It holds that

| (23) | ||||

where is the permutation matrix such that .

4.3 Asymptotics for MLE estimators

Theorem 6.

Theorem 7.

Assume the same conditions as Theorem 6. It holds that

| (25) |

Corollary 2.

Theorem 8.

Assume the same conditions as Theorem 6. Let , such that . Then we have

where , and , are block sub-matrices such that .

Theorem 9.

Assume the same conditions as Theorem 6. It holds that

| (26) | ||||

where is the permutation matrix such that .

5 Numerical Results

5.1 Simulations

In this section, we investigate the empirical performance of the proposed estimators under various simulation setups. The simulations compare the proposed alternating least square estimator (LSE), the maximum likelihood estimator (MLE), and the estimator of the cointegrated vector autoregressive model (CVAR) as a benchmark.

The true ranks are taken as known. Given dimensions and ranks , , the observed data are simulated according to the model (3) with . The coefficient matrix is generated according to , where the elements of the diagonal matrix are IID absolute standard normal random variables, and the orthogonal matrix and are randomly generated from the Haar measure. The matrix is generated in the same way. The matrices are generated in a similar way except that , and are matrices. Note that , so we have the decomposition . Denote , , . After vectorization, the model (4) without the constant term can be written in a compact form

To generate an I(1) process, we set the spectral radius . The model with and without the constant term are both studied. If included the constant term, is generated randomly with entries are IID standard normal random variables, and . The error tensors are IID normal with covariance matrix , for which we consider two settings:

-

(I)

, where the elements of the diagonal matrix are equally spaced over the interval , and is a random orthogonal matrix generated from the Haar measure.

-

(II)

takes the form , where and are generated similarly as the in Setting I, except that the diagonal entries of are equally spaced over .

For each configuration of sample size , dimensions and ranks , we repeat the simulation 100 times, and show the box plots of the estimation error

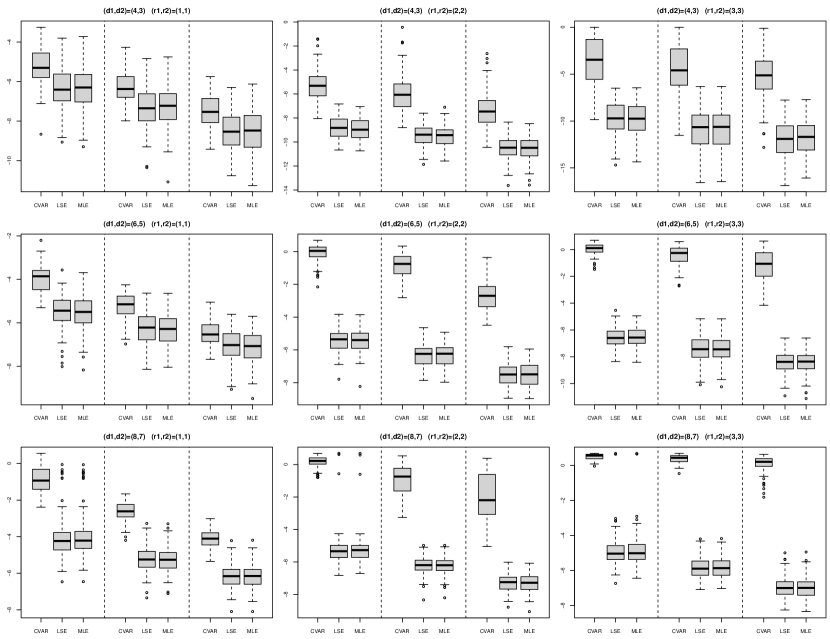

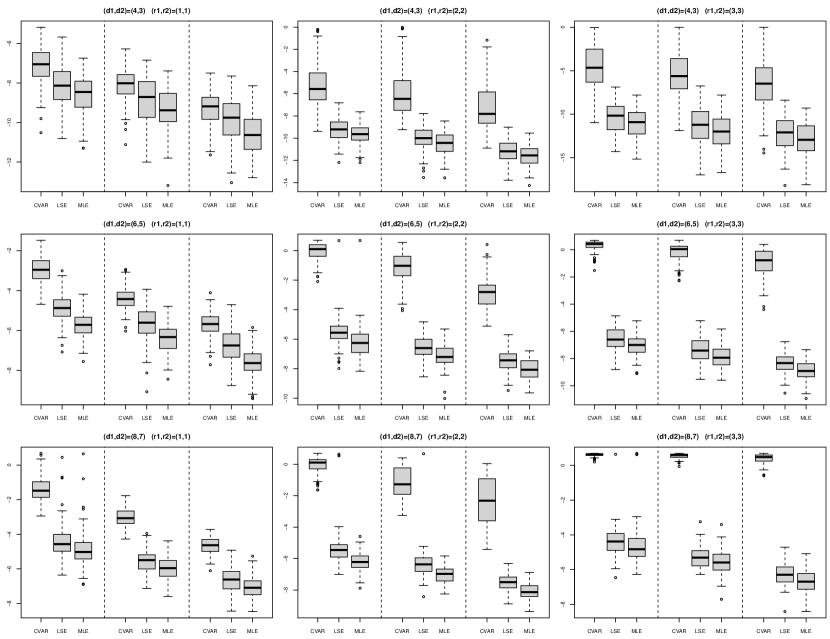

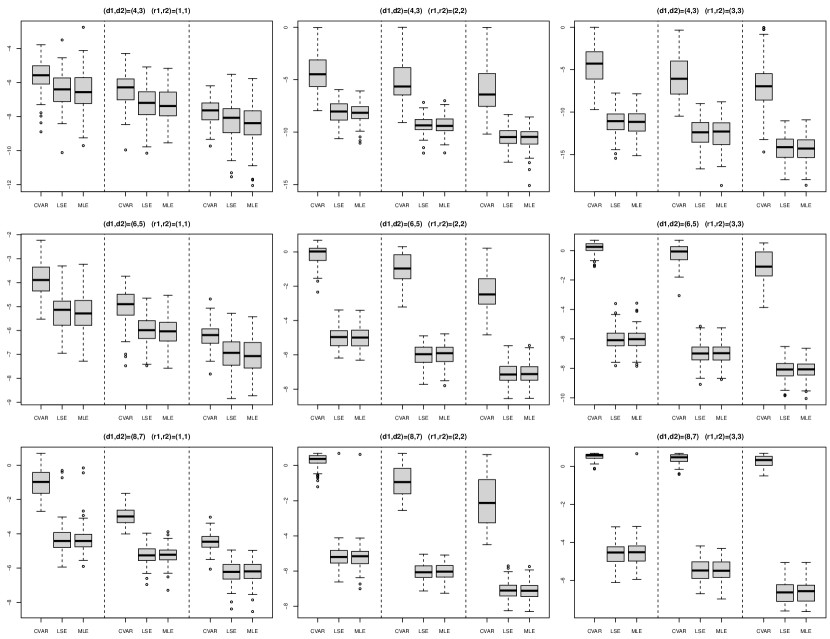

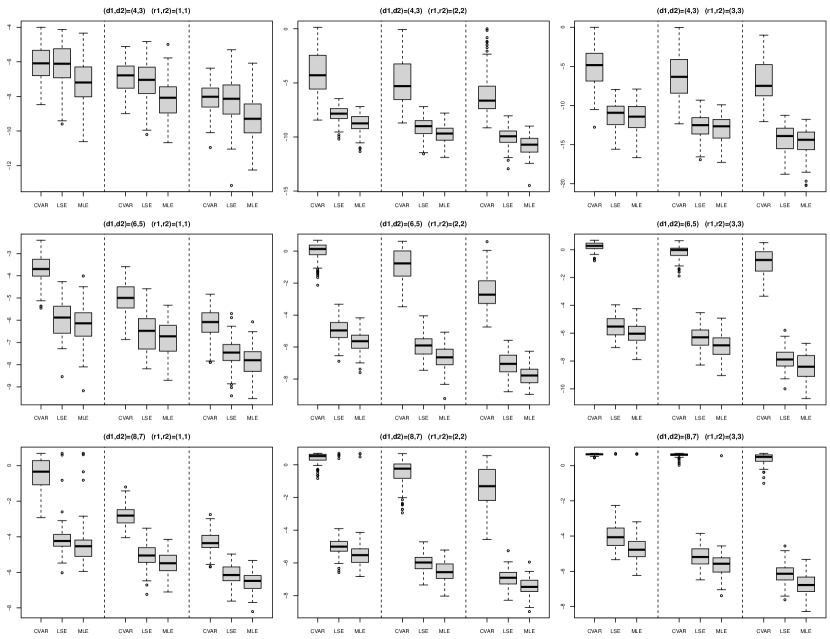

where is the projection matrix of . For a particular simulation setting with multiple repetitions, the coefficient matrices , , . We consider the model with the constant term, under the two settings of , represented by Figure 3 and Figure 4, respectively. Also, Figure 1 under Setting I and Figure 2 under Setting II are simulated without the constant term.

It is evident from both figures that the advantage of LSE and MLE over CVAR increases with higher dimensions. Furthermore, for fixed dimensions, this advantage remains significant as the ranks increase, since the CVAR does not consider the Kronecker structure of the cointegrating vectors. Additionally, from Figure 1, under Setting I of the error covariance matrix, MLE and LSE performs very similarly, even though the covariance matrix does not have the form (6). While Figure 2 explicitly depicts the advantages of MLE over LSE under Setting II, which is assumed for MLE. The LSE and MLE also both performs much better than CVAR in the model including the constant term, as seen in Figure 3 with Setting I and Figure 4 with Setting II.

5.2 Pairs Trading

We apply our model to a well-known investment strategy on Wall Street, referred to as pairs trading, i.e., relative-value arbitrage strategies involving two or more securities. Pairs trading is a widely used trading strategy in the investment industry, popular among hedge funds and investment banks. The references provided are commonly cited works in the literature on pairs trading. Vidyamurthy (2004) provides an introduction to pairs trading and related strategies, while Gatev et al. (2006) study the performance of pairs trading on US equities over 40 years, and Krauss (2017) reviews the growing literature on pairs trading frameworks.

This strategy involves a two-step process. First, pairs of assets whose prices have historically moved together are identified during a formation period. Second, a trading strategy is designed to short the winner and buy the loser if the prices diverge and the spread widens. The key step is how to identify and formulate the pairs. Various methods have been proposed in the literature, including minimum distance between normalized historical prices (Gatev et al., 2006), and the cointegration analysis based on vector error-correction models (Vidyamurthy, 2004; Zhao and Palomar, 2018), or even simply by the intuition of experienced traders. Among all these methods, cointegration is a very interesting property that can be exploited in finance for trading. Idea is that while it may be difficult to predict individual stocks, it may be easier to predict relative behavior of stocks.

In this section, we focus on using the cointegrating vectors estimated by the proposed CMAR model for pairs formation. For example, we use daily data of Fama-French portfolios from July 2021 to Dec 2022 to formulate the pairs in the first 12 months, and subsequently implement a rolling trading strategy for the following six months. The data is publicly available at the data library maintained by Prof. Kennth R. French. Specifically, since the Fama-French portfolios are grouped into a matrix-valued time series based on the Market Ratio (five levels from low to high) and Operating Profitability (five levels from low to high), we estimate the cointegrating vectors using the CMAR model (3) with and including the constant term. Firstly, we employ the maximum likelihood estimation with . Second, let and denote the positive and negative parts of , respectively. Then, the portfolios formulated by can be viewed as the spread between the two sub-portfolios, and , where the negative sign corresponding to is being shorted.

Since the cointegration model assumes that is stationary, it can be viewed as an equilibrium relationship which will revert to its historical mean repeatedly. We design the trading strategy as follows: suppose the first day of trading is , and denote , as the historical mean and standard deviation of in the pairs formation period (the 12 months prior to ). Then we would have three situations on day one of trading . (1) If , we opened the position by longing and shorting , then wait until the day that , we closed the position by selling all and buying back all , where is the selected thresh-hold. (2) If on day one of trading, , the actions and positions would be reversed (long and short then close the position when ). (3) If neither of the above two cases occurs, we wait until one of these cases happens and denote that day as , and then take actions accordingly.

In particular, we used a rolling strategy, such that each time when the position is closed at , the parameters , , and are re-estimated using the data from the 12 months prior . The money is then reinvested by opening long positions first, and becomes the new , and the above trading rules are adopted again. The returns are compounded over time. We repeated this rolling strategy until the last day of the trading period . On the last day , the position was closed, regardless of the price.

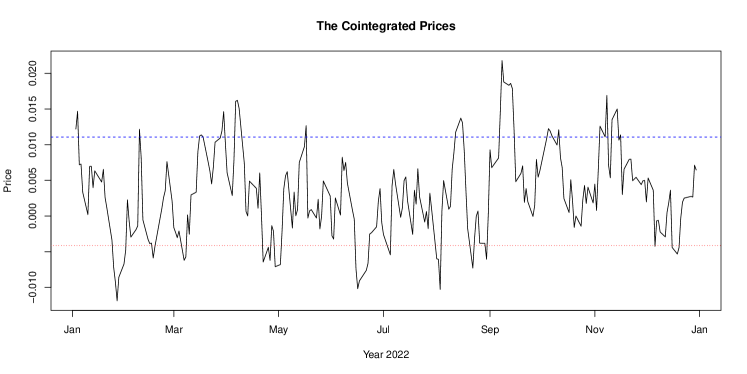

Figure 5 illustrates the movement of the spread from January 3, 2022 to December 30, 2022. The last position was opened on December 19, 2022 and closed on December 30, 2022. Although the spread did not touch the upper threshold on the closing day, it still increased, resulting in a positive cash flow for the final trade.

The top row of Table 1 displays the cumulative returns of our strategy during the trading period from July 1, 2022 to December 30, 2022. To provide a benchmark for comparison, we also tested the trading strategy proposed in Gatev et al. (2006), in which equal value positions are opened, with one dollar long and one dollar short each time. Our strategy outperforms both the market and the benchmark for the year 2022. It is effective not only during bear markets but also when the market is relatively stable, as seen in the first half of 2018 and 2015. Furthermore, if we extend our trading period to the entire year, our strategy can beat the market in 2020.

| Trading Period | S&P | |||

|---|---|---|---|---|

| 2022 Jul-Dec | ||||

| 2022 Jan-Jun | ||||

| 2018 Jan-Jun | ||||

| 2015 Jan-Jun | ||||

| 2020 | ||||

The equal value strategy does not perform well since it uses pairs formulated by cointegration but does not trade them in proportion to their share ratio. While our strategy performs well for almost all threshold values, we still need to explore how to select the threshold in a consistent way. Moreover, since pairs trading can be viewed as a hedging method, making it difficult to beat the market in a strong bull market like 2021, however, it is particularly effective in the bear markets like 2022.

6 Conclusions

We introduce the cointegrated matrix autoregressive model (CMAR), which relies on an autoregressive term involving bilinear cointegrating vectors in the error-correction form, with rank deficiency of the coefficient matrices. Comparing with the traditional vector error-correction model (CVAR) (Engle and Granger, 1987; Johansen et al., 1995), the CMAR model considers the natural matrix structure of the data and hence can better reveals the underlying cointegration relations among the variables, leads to more efficient estimation. On the other hand, we use the MAR estimates as the warm-start initial values for the estimation of the CMAR model. Both LSE and MLE are studied, where the latter is considered under an additional assumption that the covariance tensor of the error matrix is separable. Our numerical analysis suggests that even if the separability assumption on the covariance tensor does not hold, MLE still has reasonable and almost equally good performance, comparing with LSE. On the other hand, MLE can perform much better when that assumption does stand. Therefore, we would recommend the use of MLE in practice.

There are a number of directions to extend the study of the cointegrated matrix autoregressive model. Firstly, the bilinear form of the cointegrating vectors in the proposed model renders traditional testing methods inadequate, thus motivating the exploration of novel testing procedures specific to the matrix-form model. Moreover, studying processes with hybrid cointegrated orders would be more practical and interesting. However, testing and estimation for such models can be more challenging. More importantly, the asymptotic analysis has been carried out for the fixed dimensional case in the current paper. It is interesting and important to study the model under the high dimensional paradigm. Also, the model can be extended for tensor time series as well.

References

- Anderson (2003) T. W. Anderson. An Introduction to Multivariate Statistical Analysis. Wiley Series in Probability and Statistics. Wiley-Interscience, Hoboken, NJ, 3rd edition, 2003.

- Cai et al. (2017) Biqing Cai, Jiti Gao, and Dag Tjøstheim. A new class of bivariate threshold cointegration models. Journal of Business & Economic Statistics, 35(2):288–305, 2017.

- Chen et al. (2020) Rong Chen, Han Xiao, and Dan Yang. Autoregressive models for matrix-valued time series. Journal of Econometrics, 2020.

- Chen et al. (2021) Rong Chen, Han Xiao, and Dan Yang. Autoregressive models for matrix-valued time series. Journal of Econometrics, 222(1):539–560, 2021.

- Doornik (2017) Jurgen A Doornik. Maximum likelihood estimation of the i(2) model under linear restrictions. Econometrics, 5(2):19, 2017.

- Engle and Granger (1987) Robert F Engle and Clive WJ Granger. Co-integration and error correction: representation, estimation, and testing. Econometrica: journal of the Econometric Society, pages 251–276, 1987.

- Franchi and Johansen (2017) Massimo Franchi and Søren Johansen. Improved inference on cointegrating vectors in the presence of a near unit root using adjusted quantiles. Econometrics, 5(2):25, 2017.

- Gao and Tsay (2021) Zhaoxing Gao and Ruey S Tsay. Modeling high-dimensional unit-root time series. International Journal of Forecasting, 37(4):1535–1555, 2021.

- Gatev et al. (2006) Evan Gatev, William N Goetzmann, and K Geert Rouwenhorst. Pairs trading: Performance of a relative-value arbitrage rule. The Review of Financial Studies, 19(3):797–827, 2006.

- Granger (1981) Clive WJ Granger. Some properties of time series data and their use in econometric model specification. Journal of econometrics, 16(1):121–130, 1981.

- Granger and Weiss (1983) Clive WJ Granger and Andrew A Weiss. Time series analysis of error-correction models. In Studies in econometrics, time series, and multivariate statistics, pages 255–278. Elsevier, 1983.

- Guo et al. (2022) Feifei Guo, Shiqing Ling, and Zichuan Mi. Automated estimation of heavy-tailed vector error correction models. Statistica Sinica, 32:2171–2198, 2022.

- Hall and Heyde (2014) Peter Hall and Christopher C Heyde. Martingale limit theory and its application. Academic press, 2014.

- Johansen (1988) Søren Johansen. Statistical analysis of cointegration vectors. Journal of economic dynamics and control, 12(2-3):231–254, 1988.

- Johansen (1991) Søren Johansen. Estimation and hypothesis testing of cointegration vectors in gaussian vector autoregressive models. Econometrica: journal of the Econometric Society, pages 1551–1580, 1991.

- Johansen and Swensen (1999) Søren Johansen and Anders Rygh Swensen. Testing exact rational expectations in cointegrated vector autoregressive models. Journal of Econometrics, 93(1):73–91, 1999.

- Johansen et al. (1995) Søren Johansen et al. Likelihood-based inference in cointegrated vector autoregressive models. Oxford University Press on Demand, 1995.

- Krauss (2017) Christopher Krauss. Statistical arbitrage pairs trading strategies: Review and outlook. Journal of Economic Surveys, 31(2):513–545, 2017.

- She and Ling (2020) Rui She and Shiqing Ling. Inference in heavy-tailed vector error correction models. Journal of Econometrics, 214(2):433–450, 2020.

- Velu and Reinsel (2013) Raja Velu and Gregory C Reinsel. Multivariate reduced-rank regression: theory and applications, volume 136. Springer Science & Business Media, 2013.

- Vidyamurthy (2004) Ganapathy Vidyamurthy. Pairs Trading: quantitative methods and analysis, volume 217. John Wiley & Sons, 2004.

- Wang (2014) Qiying Wang. Martingale limit theorem revisited and nonlinear cointegrating regression. Econometric Theory, 30(3):509–535, 2014.

- Xiao (2021) Han Xiao. Reduced rank autoregressive models for matrix time series. Technical report, Rutgers, 2021.

- Xiao et al. (2021) Han Xiao, Yuefeng Han, Rong Chen, and Chengcheng Liu. Reduced rank autoregressive models for matrix time series. Technical report, Rutgers University, 2021.

- Zebang et al. (2021) Li Zebang, Yu Ruofan, Chen Rong, Han Yuefeng, Xiao Han, and Yang Dan. tensorts: an r package for factor and autoregressive models for tensor time series. Technical report, Rutgers, 2021.

- Zhang et al. (2019) Rongmao Zhang, Peter Robinson, and Qiwei Yao. Identifying cointegration by eigenanalysis. Journal of the American Statistical Association, 114(526):916–927, 2019.

- Zhao and Palomar (2018) Ziping Zhao and Daniel P Palomar. Mean-reverting portfolio with budget constraint. IEEE Transactions on Signal Processing, 66(9):2342–2357, 2018.

Appendix A Additional Theorems

A.1 Asymptotic for the constant term

The asymptotic properties of the constant term can be obtained directly from Johansen et al. (1995). For convenience, we reproduce the relevant results below. Define

We denote , which can be calculated by the known parameters, since both and are stationary. And we have

where , . Let and choose orthogonal to and , which span the whole space. Define

Theorem 10.

The asymptotic distribution of the constant term is found from

| (27) | ||||

where .

Proof.

See Chapter 13 of Johansen et al. (1995). ∎

A.2 Asymptotic for the model without the constant term

We only highlight some major differences and show some results for LSE as examples. In Section 4, we investigated the process in three different directions, where has a full rank of . However, in the following, we only consider two directions . Consider LSE estimator for example.

| (28) |

Since we can view the model as

| (29) |

where is stationary matrix-valued time series. We can get the CLT for . Define

and .

Theorem 11 (CLT for ).

The asymptotic distribution of is given by

where .

The process of the model without the constant term does not have the linear trend and is given as a mixture of a random walk and a stationary process:

| (30) |

where , , , and is the stationary part. Thus, we only consider two directions .

Lemma 2.

Theorem 12.

Let , . Then we have

| (31) |

where is defined as

We omit the details for MLE since the theorems can be derived similarly with respect to the above two directions .

Appendix B Proof of the Theorems

We collect the proofs of Lemma 1, Theorem 2, Theorem 3, Corollary 1, Theorem 4, Theorem 5 in this section. Proof of Theorem 1 can be found in Chapter 4 Johansen et al. (1995). For the following proofs, unless otherwise specified, we omit the subscript or for brevity and simply use to denote the estimator used in each particular theorem.

B.1 Proof of the Lemma 1

Proof.

Since the vectorized CMAR process has the representation (11) by Theorem 1, we see that is decomposed into a random rank, a linear trend, and a stationary process. Taking inverse vectorization of both sides of (11), such that makes the vector back into a matrix , the weak convergence of follows from Theorem 1. Since the random walk part gives in the limit; and the trend part vanishes because by the orthogonal construction of and ; and the stationary part also vanishes by the factor .

The weak convergence of can be also derived from (11). The random walk term and the stationary term tend to zero by the factor , the linear term converges to .

And note that the weak convergence of the average follows from the continuous mapping theorem, where the function is continuous.

∎

B.2 Proof of Theorem 2

To prove Theorem 2, we first state and prove the following lemma. Consider the general form

| (32) |

where is a constant matrix, and , . Denote , , . We introduce the notation for the stacked vectors and the corresponding parameters,

where which is full rank so invertible. where . Note that .

Using the above notations, we can rewrite the model (32) as follows:

| (33) |

The following lemma states the is asymptotic normal with the convergence rate . In addition, the projection matrix is super-consistent with the convergence rate .

Lemma 3.

For the LSE estimators,

-

(a)

;

-

(b)

;

-

(c)

;

-

(d)

;

where , . Moreover,

-

(e)

.

Proof.

Recall that , orthogonal to such that , . To prove (a) to (d), it is sufficient to show for any sequence such that ,

| (34) |

Without loss of generality, to simplify notations, consider the model without term and ,

| (35) |

The proof can be extended to the model (32) under same idea. Then, to prove (a), (b) and (d), it is sufficient to show for any sequence such that ,

| (36) |

Now we write

| (37) | ||||

Denote . Note that

Note . By Representation Theorem 1, we know that is I(0) and is I(1). Assuming the fourth moment of exists, by calculating the variance, we know that

| (38) |

where is a symmetric positive definite matrix. Thus, exists sequence such that and ,

Since , we have . By Portmanteau lemma,

So,

| (39) |

On the boundary set ,

| (40) |

On the other hand, by calculating the variance, we know that

| (41) |

Combining (37), (40) and (41), we have

| (42) |

Now we are ready to give the proof of Theorem 2.

Proof.

By the gradient condition of (10) for , and , , we have

| (48) | ||||

where , and we plug in the formula (32) for . In particular, for , we have

| (49) |

Take the (49) into gradient conditions (48), and note that

Then taking vectorization of (49), and after some algebra we have

where and are defined at the beginning of Section 4 that

, where , and for . By martingale central limit theorem (Hall and Heyde, 2014),

It follows that

where . ∎

B.3 Proof of Theorem 3

To prove Theorem 3, we first state and prove the following lemma.

Lemma 4.

Define

Then

| (50) | ||||

| (51) | ||||

| (52) |

Proof.

Proof of Theorem 3.

Proof of Corollary 1.

(19) and (20) are the marginal distribution of the first and second components in (18). Since

After some algebra we have

which is the Shur compliment in terms of . By the formula for the inverse of in terms of Shur compliment of , we can rewrite the first components in Theorem 3 as

Similarly we can derive the formula (20) using the Shur compliment of . ∎

B.4 Proof of Theorem 4

B.5 Proof of Theorem 5

For the proof of the Theorem 5, we need the following lemma. Suppose

where is a symmetric random matrix such that as , and . Let . If , we have

| (54) |

On the other hand, note that

which implies that

| (55) |

Proof.

Let be the eigenvalue decomposition. Then

And it can be shown that . The claim follows by . ∎

Proof of Theorem 5.

Since the projection matrix remains the same for using different normalization matrix . We may assume that is normalized by itself such that . Then, by gradient conditions, we have

| (56) | ||||

Observe that . On the other hand, since , it follows that

Denote , . By (54) and (56) we have,

| (57) | ||||

where

converges to the right hand side of the limit distribution in Theorem 3. And we denote

Similarly, we can have

| (58) | ||||

| (59) | ||||

where

which is not a full rank matrix, since However, the tricky part is that now we can use Lemma 5 again here, we will use the form (55), where .

First, we can verify that

For simplicity of notations we only consider left-top block. Denote , and eigen decomposition , then

| (60) |

where

We have two ways to verify 60. One is since

then,

B.6 Proof of Theorem 6 to 9

The proofs of all theorems in the Section 4.3 would be very similar with the proofs for the theorems in Section 4.2. With the exception that takes the form of a Kronecker product (6), and they are minimizing the likelihood function (7). We only need to prove the following Lemma, and omit the rest of the proofs.

Lemma 6.

For the MLE estimators,

-

(a)

;

-

(b)

, where , ;

-

(c)

;

-

(d)

;

-

(e)

;

-

(f)

.

Proof.

The proof would be very similar to the proof of Theorem 4 in Chen et al. (2021). Here we only address some major differences. Without loss of generality, to simplify notations, consider the model without term and ,

| (61) |

The proof can be extended to the model (32) under the same idea. Denote the precision matrix , where , . And we define

| (62) | ||||

where which is full rank so invertible. where . Note that . By the above definition, is made up by the stationary components, while is made up by two components, one is the stationary part , and the other is non-stationary part but controlled by the factor . Then the model 61 can be written as

| (63) |

where , and is the corresponding error matrix. For the unrestricted CVAR model, its log like likelihood at the parameters is

| (64) |

where and . Let , and . Then we can show that and , and consequently . Then we can prove (a) that by the very similar proof of Theorem 4 in Chen et al. (2021). The rest of the proof of Lemma 6 would follow by (a) and same arguments in Lemma 3. ∎