Addressing misspecification in contextual optimization

Abstract

We study a linear contextual optimization problem where a decision maker has access to historical data and contextual features to learn a cost prediction model aimed at minimizing decision error. We adopt the predict-then-optimize framework for this analysis. Given that perfect model alignment with reality is often unrealistic in practice, we focus on scenarios where the chosen hypothesis set is misspecified. In this context, it remains unclear whether current contextual optimization approaches can effectively address such model misspecification. In this paper, we present a novel integrated learning and optimization approach designed to tackle model misspecification in contextual optimization. This approach offers theoretical generalizability, tractability, and optimality guarantees, along with strong practical performance. Our method involves minimizing a tractable surrogate loss that aligns with the performance value from cost vector predictions, regardless of whether the model is misspecified or not, and can be optimized in reasonable time. To our knowledge, no previous work has provided an approach with such guarantees in the context of model misspecification.

1 Introduction

1.1 Problem overview

In a number of real-world problems, the decision makers are faced with uncertainty over relevant parameters and this uncertainty can be reduced by acquiring side information. For example, consider a traffic routing problem where a fixed amount of traffic is to be allocated over a directed graph in a way that minimizes total edge cost. The edge costs are unknown at the time of making this decision, but depend on some observable features (or context variables) that are correlated with the edge costs, such as weather, time of day, construction, and so on. Suppose that we have access to data containing previous realizations of edge costs and context variables. The decision-maker faces the task of designing a policy that maps the observed contextual information into minimum cost routing decisions. A general setting for problems of this type, typically referred to as contextual optimization problems, involves simultaneously learning a decision policy within a certain model class and solving an optimization problem using predicted costs. In this paper, we are concerned with contextual optimization with model misspecification; that is, problems in which the class of prediction models may not contain the model that recovers the true (unknown) parameters.

For simplicity, we consider that unknown parameters appear linearly in the objective function of the stochastic optimization problem:

where is a random variable correlated with the context , is the joint probability distribution of and (which we will refer to as the data distribution), and is a bounded convex set. When making a decision, the decision maker does not know , and only the context variable is observed. Let be a set of feasible policies, i.e. a set of functions which maps a context to a decision . Our goal is to find a policy approximately minimizing the cost resulting from making a decision given a context , i.e.

| (1) |

This policy involves choosing an element from the optimal solution set of problem (1), which therefore may not have desired continuity and smoothness properties to enable tractable parametrizations for learning an optimal policy. A commonly used approach to mitigate this issue is to “predict-then-optimize” (Hu et al., (2022), Elmachtoub and Grigas, (2022), Sun et al., (2023)). This approach, instead of learning directly a policy, involves first selecting a suitable cost vector predictor from a given hypothesis set (where is the predicted cost vector associated with context ), and then using an optimization solver to determine the policy satisfying for every context , to make decisions.

A recent active literature considers the problem of finding cost prediction models that take into account the downstream optimization problem and minimize the resulting decision error, measured as the difference between the true cost of the decision induced by the predicted cost and the optimal cost. This approach is referred to as the Integrated Learning and Optimization (ILO) approach. Most of this literature considers the well-specified case, where the hypothesis set contains the ground truth cost predictor . The misspecified case, where this ground truth is not in the hypothesis set actually arises frequently in practice because of incomplete specification of costs or insufficient knowledge about the underlying data distribution. However, many practical situations may necessitate solving a contextual optimization problem in which the hypothesis set does not contain the ground truth predictor. In particular, the decision maker may only have an incomplete specification of the relationship between context and cost variables or insufficient knowledge about the underlying data distribution. For example, in the traffic routing problem, we may not have complete knowledge of how contextual information impacts edge costs or may not have access to all the relevant data needed to ensure accurate cost prediction. We refer to such problems as contextual optimization under misspecification. Despite their practical significance, these problems have not received much attention in the literature, with the notable exception of some recent papers such as Huang and Gupta, (2024) and some empirical studies (see for example Donti et al., (2017), McKenzie et al., (2023), Kotary et al., (2023)), but neither of these provides global optimality properties.

1.2 Our focus and contributions

In this paper, we develop a computationally tractable approach to minimize the decision error (i.e., target performance) when the hypothesis set is misspecified, using historical data. In contrast to prior work, our approach ensures global optimality. For any cost vector , we denote a solution to the optimization problem returned by an oracle, which could be an off-the-shelf solver for example. We consider that the hypothesis set is parametric, i.e. it can be written as . We would like to minimize the following function: . In general, the solution to is not always unique, so we rewrite by accounting for the worst case solution:

| (2) |

where for every , . Minimizing can be quite challenging because in general it is non-convex, non-smooth, and non-continuous. Moreover, in practice, we do not have access to , but rather a set of empirical samples .

Previous works (Bertsimas and Kallus, (2020), Elmachtoub and Grigas, (2022), Sun et al., (2023), Loke et al., (2022)) have suggested ways to address poor regularity properties of the target performance function, leading to various procedures that aim to minimize the function but assume that is well-specified. However, these procedures do not naturally extend to contextual optimization problems under misspecification. To the best of our knowledge, the current literature does not provide a procedure to minimize with theoretical guarantees when is misspecified.

Our work addresses these gaps in the literature by providing a tractable procedure to minimize when is misspecified. Our procedure enjoys both strong optimality guarantees and generalization performance. We also experimentally evaluate the performance of our procedure and show it indeed has good performance compared to mainstream methods. Importantly, our procedure leverages an intuitive surrogate loss function which naturally arises under mild assumptions on and , and does not require to be well-specified. The proposed surrogate loss has the same set of minimizers as (see Theorem 1). We show that our loss function generalizes well to out-of-sample distributions (i.e. optimizing the surrogate loss where is approximated by the uniform distribution over a historical dataset can yield a good solution for , see Theorem 2), and it is tractable in the sense that it has no bad local minima and saddle points (see Theorem 4).

Our approach contrasts with contextual optimization in the well-specified case which has been extensively studied in the literature. Previous works have mainly adopted two types of approaches: Sequential Learning and Optimization (SLO) (Hu et al., (2022), Bertsimas and Kallus, (2020)) and Integrated Learning and Optimization (ILO) (Elmachtoub and Grigas, (2022), Donti et al., (2017), Sun et al., (2023))111We have not mentioned the Decision Rule Optimization approach since SLO and ILO perform a priori better in theory and in practice (see Elmachtoub et al., (2023)).. For both of these approaches, the general idea is to approximately optimize given a hypothesis set and a set of past observations . SLO consists of focusing solely on the prediction of the cost by choosing the cost predictor with the smallest prediction error without taking into account the downstream optimization task, whereas ILO consists of finding a cost predictor which yields good decision performance rather than being a good approximation of . A well-known ILO approach is to design a surrogate loss function, as notably adopted by Elmachtoub and Grigas, (2022). In Elmachtoub and Grigas, (2022), a new convex surrogate function is introduced (called the SPO+ loss), which is consistent with when is well-specified, i.e. a minimizer of the expected value of their convex surrogate function,

where for every ,

is also a minimizer of the target performance loss . However, no theoretical optimality guarantees are provided when is misspecified.

To further motivate the necessity of a new approach to address misspecification, we show in the following example that SLO and SPO+ are not suitable to handle misspecification.

Example 1

Consider that the context variable x takes value 0 with probability 1, the underlying cost vector is and the hypothesis set where and . This misspecified problem is associated with the decision-making task modeled as a linear program:

The optimal decision for the abovementioned problem is . By direct calculation, we can see that the cost prediction yields the optimal decision but does not. However, we have and . Therefore, the cost prediction made by SPO+ and SLO is , which will yield a suboptimal decision.

Our novel ILO approach addresses these limitations by ensuring that optimal decision performance is recovered even under model misspecification. Our surrogate loss function is directly related to an optimality condition for minimizing the target loss . In fact, this surrogate is a nonnegative function and can be written as the difference between the minimum of two functions that depend on the chosen parameter , with the property that the minimal value of the first function is equal to the minimal value of the second function if and only if is a minimizer of . Importantly, this property holds regardless of whether is misspecified.

Assuming the hypothesis set is linear, our surrogate loss function has good landscape properties: every local minimum to this surrogate, is a global minimum. While it is not known whether approaches in previously mentioned works are successful in solving contextual optimization problems under misspecifiation, our approach ensures that the set of minimizers of proposed surrogate coincides with the set of minimizers of the target loss (see Theorem 1) even when is misspecified.

Our surrogate loss function is tractable to minimize because it can be written as a difference of non-smooth convex functions (see Proposition 2), we can find a stationary point using first order methods applied on its Moreau envelope. Our surrogate is tractable in the sense that every one of its stationary points is a global minimum (see Theorem 4). We provide theoretical guarantees bounding the gap between the value of our loss when averaging over the in-sample distribution and the out-of-sample distribution. We further give experimental evidence of our surrogate’s generalization properties, and show that it outperforms SPO+ and SLO when the level of misspecification of is reasonably high.

1.3 Quantiyfing the level of misspecification

A classical metric to quantify the level of misspecification of a given hypothesis set is the or norm of the distance between the parameter (or the function) one seeks to estimate and the chosen hypothesis set. In our setting, it can be written as

This metric has been previously adopted in statistics and contextual bandits (Foster et al., (2020), Krishnamurthy et al., (2021)). We argue that can be a good metric for evaluating the effect of misspecification for prediction problems, but not for contextual optimization problems in which parameter estimates enter in downstream optimization problem. This can be seen by noting that in our setting, the best achievable cost should not change when multiplying the elements of by a positive constant, whereas is not invariant to such a transformation. To address this, we introduce a new metric to quantify misspecification in contextual optimization.

Definition 1

We define the misspecification gap as

The function class is well-specified if , and misspecified otherwise.

Note that the first term is the smallest possible value of the target loss when choosing a cost predictor from , and the second term is the smallest possible value of the target loss in the case where contains the ground truth cost predictor. First, this definition of model misspecification is weaker than the previous one. Indeed, if , then necessarily . Second, is clearly invariant when multiplying the cost predictors by a constant. Furthermore, the misspecification gap captures the optimality gap caused by model misspecification. In other words, it is the difference between the best possible performance in the misspecified case and the best possible performance in the well-specified case.

For a given cost predictor , denoting and we can see that SLO focuses on bringing as close as possible to , whereas it is more natural to focus on bringing as close to as possible, since small prediction error does not necessarily mean good decision performance in the misspecified case. In the other hand, even if current ILO methods such as SPO+ aim to bring as close to , it is unclear whether they can do so in the misspecified case, whereas our surrogate loss’s optimality gap dominates (see Theorem 3).

1.4 Previous approaches to Integrated Learning and Optimization

A more comprehensive review of contextual optimization approaches can be found in the survey by Sadana et al., (2024).

Directly optimizing the target loss.

One of the first instances of the ILO method can be traced back to Donti et al., (2017) who provide a practical way to differentiate the target loss under some regularity conditions. Similarly, others have attempted to directly minimize using some estimation of its gradient, such as unrolling (Domke, (2012) Monga et al., (2021)), which consists of keeping track of operations while running gradient descent in order to differentiate the final gradient descent iterate as a function of the model parameters, and implicit differentiation (Amos and Kolter, (2017) Agrawal et al., (2019) McKenzie et al., (2023) Sun et al., (2022)). However, is non-differentiable in general, and even if it were, there is no guarantee that it would be convex. This implies that gradient-based algorithms mentioned above do not guarantee convergence to optimum of the target loss. In contrast, our approach consists of minimizing a tractable smooth surrogate that has the same set of minimizers as . This allows us to avoid the challenge coming from the lack of regularity properties for .

Optimizing a surrogate loss.

Another increasingly popular approach, which is most relevant to ours, is optimizing the target loss using a smooth convex surrogate loss. In Elmachtoub and Grigas, (2022), a new convex surrogate function, named SPO+. Minimizing SPO+ is proven to also minimize the target loss when the hypothesis set is well-specified, but no consistency results are provided when the chosen predictor class is misspecified. Furthermore, SPO+ seems to outperform SLO (i.e. yield better decision performance) when is misspecified, since SLO only focuses on the accuracy of the prediction step, but completely disregards the performance in the optimization step, whereas ILO specifically focuses on the decision performance, and when the hypothesis set is misspecified, maximizing the prediction accuracy of the underlying cost will not necessarily result in good decision performance. Moreover, when is well-specified, SLO methods outperform ILO (Hu et al., (2022), Elmachtoub and Grigas, (2022)). Hu et al., (2022) give theoretical and experimental evidence showing that classical SLO methods generalize better than SPO+ when the hypothesis set is well-specified. In fact, evidence in Elmachtoub et al., (2023) suggests that in the well-specified case, SLO might likely have better performance than ILO approaches, and such a behavior is inverted in the misspecified case. Most previous works have not theoretically considered the misspecified case. In Huang and Gupta, (2024), a new surrogate is introduced based on an approximation of the directional derivative of , and is shown to be theoretically consistent with . However, only local optimality results are provided for this surrogate, whereas in our work, we provide global optimality guarantees.

Another alternative is the surrogate introduced by Sun et al., (2023), which attempts to maximize the nonbasic reduced costs (when the cost is taken equal to the predicted cost) of past realizations of ground truth optimal decisions. Such a method does not require the knowledge of historical costs, but only solutions of previously seen linear programs. In order for this surrogate to be consistent, authors assume that the chosen hypothesis set is well-specified in the sense of our definition, i.e. . On one hand, this assumption is weaker than the usual definition of well-specification, which requires that the hypothesis set contains the ground truth predictor. On the other hand, this surrogate is only designed for linear objectives with linear constraints. Our surrogate only requires the set of feasible decisions to be convex and bounded. In a related paper, Liu et al., (2021) use a neural network structure in an inventory management problem to learn a mapping which provides the optimal merchandise order quantity and order time, and give theoretical guarantees in the well-specified setting. Other surrogates have been considered in the literature (Kallus and Mao, (2023) Loke et al., (2022) Jeong et al., (2022)), which despite having good practical performance benefits, do not seem to theoretically tackle the misspecified case as opposed to our work.

The remainder of this paper is organized as follows. In section 2, we formulate our problem and give the intuition behind our approach, as well as provide our main consistency theorem. We give an exact characterization of the minimizers of . In section 3, we first establish a generalization bound of the in-sample surrogate loss , where is the uniform distribution over the dataset , proving that minimizing the in-sample surrogate indeed provides a good near-optimal solution for the out-of-sample surrogate , then provide a procedure to tractably minimize it, and finally show that minimizing our surrogate with our procedure indeed yields a good near-optimal solution for . In section 4, we provide experimental evidence showing that our approach indeed performs better than state-of-the-art methods when the hypothesis set is misspecified. Finally, in section 5, we make some concluding remarks.

2 Our approach

2.1 Rewriting under a generic assumption

Recall from (2) that the generic form of the target loss function in our contextual optimization problem involves the worst case value of when because the solution to is not necessarily unique in theory. In practice, however, is likely to be unique. For example, in the common case where is a continuous random variable and is a polyhedron (or more generally when the set of directions for which the solution to is of Lebesgue measure equal to zero), uniqueness holds with probability 1. Hence, due to practical reasons and theoretical convenience, we make the following assumption henceforth:

Assumption 1

For any such that almost surely, has a unique solution with probability when .

We denote the set of measurable mappings from the support of the joint probability of to the set of feasible decisions . Under Assumption 1, we can see that the problem of minimizing target loss can be written as follows:

| (3) | ||||

| (4) |

In the formulation above, the minimum was taken outside of the expectation because, to minimize the function for , it is sufficient to select as the minimizer of for every possible realization of . The following proposition provides a sufficient condition for Assumption 1 to hold when is a polyhedron.

Proposition 1

If the context variable x has a continuous probability distribution and the mapping is a nonzero analytic function for any , then Assumption 1 holds for any polyhedron that satisfies for any and any nonzero .

Proof. Let be all the faces of , where is a finite index set. Let be an arbitrary tangent direction of and let be a finite set. Let be the set containing all such that the solution to the linear program is not unique. Then any satisfies for some . Therefore, if for some . Let and . We have . By the assumption in the Proposition, is a nonzero analytic function and then by Mityagin, (2015), is a zero-measure set. Therefore, is a zero-measure set since is finite. Finally, since is of measure zero and is a continuous random variable, lies outside of almost surely, i.e. the solution to is unique almost surely.

Our task now becomes to solve the bilevel optimization problem (3). Since known approaches to solving bilevel problems cannot be directly applied to solve (3), we develop an approach based on a surrogate loss function that enjoys two properties:

-

1.

Consistency: The optimal solutions for the surrogate loss are also optimal for the target loss;

-

2.

Tractability: The surrogate loss is tractable to optimize.

2.2 Introducing our surrogate loss function

We denote , , and . Let . We first study the property when satisfies and almost surely. The inequality ensures that the condition is feasible, and the inequality ensures that the condition is not trivial. Notice that if we take , any satisfying is a minimizer of . When Assumption 1 holds, and when almost surely, contains only one element for almost every . Hence, we denote to be the unique solution in when contains only one element. The condition can be rewritten as when almost surely. For a given and , if satisfies

| (5) |

then we have, almost surely, as for each , the unique minimizer of over is given by , according to Assumption 1.

If satisfies , and is the measurable mapping satisfying condition (5) (and hence almost surely), then we have . This suggests that adding the linear constraint to (5) does not change the set of minimizers of when . Defining , our latter statement means that if , the two optimization problems

| (6) |

and

| (7) |

would result in identical values of the objective function. The above analysis suggests that a possible approach is to use the difference of the optimal function values of the two above optimization problems to be the surrogate function. We introduce a new surrogate loss function – referred as Consistent Integrated Learning and Optimization (CILO) loss – for contextual optimization under misspecification.

Definition 2

(CILO loss) For , we define the function as

The following example shows that whereas SLO and SPO+ fail to provide a minimizer for , this new surrogate successfully does so.

Example 2

We revisit example 1. We have seen that SPO+ and SLO do not pick the best element of the hypothesis set . If we choose . For a given , we denote as the value of (which does not depend on ) for any .

| (8) | ||||

| s.t. | (9) | |||

| (10) | ||||

| (11) |

Here, (10) and (11) are the constraints involved in the definition of (which in the definition are written as and ). We denote such that and .

We see that indeed here, the global minimum of this new loss is optimal for the target loss.

We will now prove that the consistency observed in example 2 holds in general. The lemma below will be useful when proving our main consistency theorem.

Lemma 1

For every such that , is non-negative.

By the above analysis, we know that any such that satisfies . Interestingly, we can show the reverse direction: if and is nonzero almost surely, then .

Theorem 1

Let such that . Under Assumption 1, for every with almost surely, if and only if is a minimizer of . In particular, when , is a minimizer of if and only if it is a minimizer of .

Proof. Let such that and satisfying almost surely. Assume that is optimal for , i.e. . Let be the solution of (7). Then implies

Since the random variable is positive almost surely, the equality above implies that almost surely, i.e. is also a minimizer of , and hence under Assumption 1, we have almost surely. This finally gives

The other direction is already shown before during the development of .

This result also suggests that a natural approach to minimizing is to first find a tractable method for minimizing the CILO loss for an appropriate choice of auxiliary parameter , while ensuring that the candidate minimizer satisfies almost surely. Although is unknown, one might expect that if the optimization procedure can achieve a sufficiently small value of , the corresponding minimizer would likely ensure that the original target loss function is less than . To select the auxiliary parameter , one can perform a line search within a suitable interval and choose the parameter that yields the smallest value of the CILO loss. We will now proceed to develop a tractable procedure to optimize (so that the line search for the best is also feasible) and formalize the relationship between near optimality and the corresponding value of the target loss . In doing so, we address the key limitation of current literature in contextual optimization – namely, previously proposed surrogate loss functions, while tractable, only satisfy theoretical optimality under well-specified settings. These approaches may provide reasonably good experimental performance for some misspecified settings; however, there currently does not exist an approach that is guaranteed to ensure global optimality for any level of misspecification. We bridge this gap in Section 3.

3 Technical approach

In this section, we formalize our technical approach based on the CILO loss function and the consistency result. We first mention three key issues that our approach seeks to address. In the remainder of the paper, we denote by the norm.

Firstly, we do not have access to the joint distribution P of random variables ; instead we assume that we have access to a historical dataset , where is the number of samples and each sample , is sampled from . Thus, we seek to optimize the empirical version of CILO, denoted , where is the uniform distribution over the dataset . The question we need to address is whether by minimizing empirical CILO, we can obtain good generalization performance (i.e., guarantees on out-of-sample CILO loss). Theorem 2 shows that this is indeed the case.

Secondly, the CILO loss is a non-convex and non-smooth function, and we need a technique to optimize it in a tractable manner. We address this issue by leveraging Moreau envelope smoothing technique (Sun and Sun, (2021)) to transform the problem of minimizing into another optimization problem whose objective function enjoys good landscape; in particular it is smooth and has no “bad” first-order stationary points or local minima (see Theorem 4). Consequently, this smoothed optimization problem is conducive to gradient descent.

Thirdly, to guarantee consistency, we must ensure that the optimization procedure is able to find minimizer that verifies 0 almost surely (see Theorem 1). We address this issue by refining our smoothing procedure so that gradient descent on smoothed CILO loss results in a minimizer that verifies almost surely (see Theorem 5).

These three steps together ensure that we have a tractable approach to minimizing empirical CILO loss, resulting in solution that has good generalization perform optimality guarantee.

3.1 Generalization performance

We study the generalization performance of the empirical version of CILO loss and show that by optimizing the empirical CILO loss , we can ensure a nearly optimal value for its out of sample counterpart . We first make the following boundedness assumptions.

Assumption 2

is closed and bounded. We denote .

Assumption 3

There exists such that for all , .

Assumption 4

When , . Furthermore, there exists such that the gradient with respect to , , is piecewise continuous and bounded by for every and .

The first part of Assumption 4 is natural when we assume that there exists such that . By reparametrizing the hypothesis set as , we obtain . Furthermore, a direct consequence of this assumption is that for every and ,

We now present our main generalization result.

Theorem 2

Notice here that when the hypothesis set is misspecified, we have , and consequently the term is bounded. If is (nearly) well-specified, we can choose a larger to guarantee the generalization bound to be good. This theorem implies that our surrogate loss can generalize when is large and hence minimizing the empirical version of the surrogate loss yields small optimality gap for its out-of-sample counterpart . Using Theorem 1 and Theorem 2, we can deduce that finding such that almost surely and minimizing yields an optimal value for .

Theorem 1 ensures that the closer is to optimality for for a well-chosen , the closer it is to optimality for . When is nearly optimal for , we aim to quantify how close it is to optimality for . By adopting a stability assumption regarding the linear optimization problem, we can establish a more concrete accuracy bound for the solution obtained from the empirical version .

3.2 Relationship between the optimality gaps of and

For ease of presentation, we make the following assumption from now on:

Assumption 5

For , almost surely.

Assumption 5 holds when for every , is a nonzero analytic function and has a continuous distribution. In this case, the set of zeroes of is of measure equal to zero (see Mityagin, (2015)) and consequently does not belong to this set almost surely. This assumption, coupled with Assumption 1, implies that for any , the problem has a unique solution almost surely.

We give a more concrete optimality guarantee obtained by minimizing . We first mention the assumption in Hu et al., (2022) which enables the authors to get good generalization guarantees for SLO in the well-specified case. Note that we will not be making this assumption, but we mention it just for reference.

Assumption 6

Assume that is a polyhedron. We denote the set of extreme points of . For a given context , we denote

Assume that for some ,

We make a similar assumption, which is independent of the ground truth predictor, but rather depends on the chosen hypothesis set.

Assumption 7

Assume that is a polyhedron. We denote the set of extreme points of . For a given context , we denote for every ,

Assume that for some and , for every

The assumption above ensures the stability of the target loss . Specifically, it strengthens the uniqueness guarantee provided by Assumption 1. Besides ensuring that has a unique solution almost surely, it offers a sharper measure for how sensitive the mapping is to deviations from with high probability. This is a reasonable assumption when the distribution of is continuous. Indeed, when is a polyhedron, denoting for , , and

Assumption 7 can be rewritten as

| (12) |

We do not need to focus on the term , as it is both upper bounded and bounded away from zero. Therefore, inequality (12) is equivalent to having a norm that is bounded away from zero with high probability, and an angle that is bounded away from when is bounded away from . In other words, is likely to have a direction that is not too close to being perpendicular to one of the faces of the polyhedron –that is, the probability of this direction to be falling within one of the red cones shown in Figure 1 decays to as the cones get more narrow. When follows a continuous distribution, such a property on the direction of is reasonable.

In contrast with our assumption, we have no control on whether Assumption 6 is verified or not, and also cannot verify if it is satisfied unless we have access to the ground truth predictor . Our assumption depends only on the chosen hypothesis set, which is something the decision maker can control. A consequence of this assumption is an inequality providing a more precise quantification of how optimality transferred from to .

The following theorem provides a relationship between optimality gaps of and when is bounded away from , i.e. there exists such that .

The proof of this theorem can be found in appendix 5.5. Assuming that is bounded away from 0 is crucial here, because when , the uniqueness property in Assumption 1 is not guaranteed, and the consistency in Theorem 1 is not satisfied. Similarly, when is close to 0, exhibits poor behavior, as it approaches the scenario where consistency breaks down. The key idea of the proof relies on the following sensitivity inequality resulting from Assumption 7 which holds for every and mapping :

where are positive constants. The left-hand side equals for a well-chosen , while the right-hand side is directly related to . Optimizing over in the right-hand side yields the desired inequality. By omitting the term and the dependence of the right-hand side on , it is possible to obtain a stronger bound. Specifically, if we assume the existence of such that for every and every mapping ,

| (13) |

the bound holds when is bounded away from . This bound is stronger since for every .

Remark 1

This theorem suggests that to minimize , one should seek an approximate minimizer of for a well-chosen with kept away from zero. By applying Theorem 2, it follows that it suffices to find some such that is small while ensuring remains bounded away from zero.

If inequality (13) holds, we can obtain the bound without requiring to be a polyhedron.

3.3 Optimizing our surrogate

Based on theorems 1, 2, and 3, it is sufficient to find a such that is small and is kept bounded away from zero to minimize . The empirical surrogate loss can be written as:

where

| (14) | |||

| (15) |

The equality in (14) is satisfied because choosing a policy minimizing is equivalent to choosing minimizing for every in .

Landscape properties and smoothing.

We take a closer look at the structure of our surrogate. We make the following mild assumption.

Assumption 8

The function is differentiable for every , and there exists such that for all and ,

This assumption is sufficient for to be written as a difference of two convex functions. Specifically, we have the following result:

The proof of the proposition above (see appendix 5.4) relies on the fact that under assumptions 8 and 2, and are both weakly convex functions, and consequently their difference is a difference of convex functions.

We aim to find that minimizes . A natural approach is to identify a stationary point of (i.e., a where the subgradient of contains 0). Despite having a DC structure, it may still be non-smooth, making the task of finding a stationary point challenging. To address this, we introduce a smoothed version of .

Definition 3

(s-CILO loss) For all and , let

We define a smooth surrogate to the CILO loss, which we call the s-CILO loss

| (16) |

Following Sun and Sun, (2021) (proposition 1, page 10), the smooth surrogate above has the following property: for every stationary point of , and are equal and are stationary points of . Similar to , s-CILO satisfies the positivity property and the fact that its minimum value is equal to from .

We now have a way to find a stationary point of . A practical way to ensure that the iterates of an optimization algorithm for do not converge to is to add a constraint where . Since the function can be written as a difference of two convex functions, we can find a constrained stationary point to (see Pang et al., (2017) for tractability results for DC constrained minimization).

The DC structure of our surrogate enables us to find a stationary point of , thus allowing us to approximately minimize the target loss . Moreover, as we will demonstrate (see Theorem 4 below), for specific choices of the hypothesis set (e.g., a linear hypothesis set), our surrogate has a favorable landscape, meaning that every stationary point of is a global minimum. Consequently, first-order optimization algorithms can effectively find a global minimum of our surrogate.

From now on, we assume that our hypothesis set is linear, meaning there exists a mapping such that for all , . In this scenario, Assumption 5 is satisfied if is full rank almost surely. Additionally, Assumption 8 is inherently satisfied, and Assumption 4 can be replaced with the following:

Assumption 9

For any , the largest singular value of is bounded above by .

With this special choice of hypothesis set, our surrogate loss and its smoothed version enjoy good landscape properties. In particular, every stationary point of is a global minimum. We formulate our main landscape result.

Theorem 4

-

1.

For all , and have a non-empty subgradient at , and for some , where and are respectively the subgradients of and at ;

-

2.

For all , if for some , then , hence is a minimizer.

- 3.

The proof of this theorem is in appendix 5.6.

Assuming a priori that running gradient descent to optimize our smooth surrogate, we do not fall into the case almost surely, our practical procedure to optimize is the following. In the algorithm below, is the uniform distribution over the dataset , and is the uniform distribution over the testing dataset .

Now, the only remaining problem to address is the case where the algorithm gives .

Avoiding zero solutions.

Even if we successfully minimize , we could encounter the pathological case where , which would fail to ensure that almost surely. In this situation, the conditions for Theorems 1 and 3 would not be satisfied. To prevent this, we leverage the linear structure of the hypothesis set. We begin by stating a few propositions that highlight key properties of our surrogate when the hypothesis set is linear.

Definition 4

For a set in and element , denote the distance between and .

Proposition 3

Let and , we denote

can be rewritten as

The following is a key lemma to prove Proposition 3, and also to design the procedure which will enable us to optimize .

Lemma 2

For every , we have

-

1.

with and ;

-

2.

with and .

The key idea behind the lemma above is to simply swap min and max in the definitions of and (see Definition 3). The proof of the proposition and the lemma can be found in appendix 5.8 and 5.7.

We observe that exhibits an interesting structure: when minimizers , its distances from and are equal. However, when running gradient descent on , we want to avoid the scenario where . This happens when the gradient descent iterates converge inside the set . To address this, we aim to push the gradient descent iterates outside the sets and . We achieve this by leveraging the structure of , applying the logarithm to the two distances to ensure they do not equal zero.

Definition 5

(log-CILO loss) Let , we define for every ,

| (17) |

We call this function the log-CILO loss.

The function inherits the properties we previously observed in . Specifically, since for every (due to the fact that ), and because the logarithm is a non-decreasing function, we have for every . Furthermore, similar to , if is a minimizer of , then the distances and are equal. Additionally, it can be shown that any stationary point of is also a stationary point of (see Theorem 5).

If gradient descent is used to optimize and a subsequence of the iterates converges outside the set (and hence outside as well), we can recover from the limit of this sequence a that is bounded away from zero and serves as a minimizer of . As a result, by Theorems 2 and 3, we successfully obtain a desirable approximate minimizer of . However, if every limit point of the gradient descent iterates converges within the sets and , the function can be used instead. Gradient descent applied to will not yield iterates converging inside the sets and due to the presence of barriers. The following proposition outlines the possible outcomes when running gradient descent on .

Proposition 4

Consider the backtracking line search gradient descent method applied to the function , ensuring sufficient decrease at each iteration (refer to Algorithm 3.1 in Nocedal and Wright, (1999)). Suppose the gradient descent sequence has at least one limit point. There are two possible cases:

-

1.

The limit point lies strictly outside the interior of or ;

-

2.

The limit point lies on the common boundary of and .

Proof. Let be the sequence of iterates generated by applying gradient descent to . Suppose a subsequence of this sequence converges to a limit point . If is not on the boundary of or , then by Nocedal and Wright, (1999), is a stationary point of . We now show that if the limit point lies on the boundary of , then it must also lie on the boundary of . Indeed, on the one hand, the objective function is non-increasing, so for all . On the other hand, , which implies that . Therefore, , yielding the desired result.

If the gradient sequence converges to the common boundary of and , the corresponding sequence approaches zero, which is not a desirable solution. Fortunately, this issue can be addressed. Since the sequence converges to a limit point on the boundary of and which is also a stationary point of , there must exist some such that is an -stationary point of . We then move orthogonally away from the boundary of (see Figure 2). This yields a new approximate stationary point that is sufficiently distant from both and . As a result, the corresponding is an approximate global minimizer of that is bounded away from zero.

The following theorem provides an overview of this procedure, as well as a relationship between the optimality for and .

Theorem 5

We define and to be respectively the projection of on and on . Suppose that is an -solution of , i.e. for some , and . We have . Furthermore, if , letting with and , we have

-

•

The value of is dominated by . In particular, we have and .

-

•

The norm of the resulting candidate solution for is bounded from above and below. In particular, .

Figure 2 summarizes the construction of .

Hence, the theorem above provides us with an algorithm to optimize :

-

1.

Run gradient descent on .

-

2.

If we obtain a solution reasonably far from , we simply return that iterate as an output. Else, we run gradient descent on .

-

3.

If the gradient descent iterates do not converge to a common boundary to and , we return the final iterate as an output. Else, we use the procedure in Theorem 5 to obtain a near stationary point which is far from the boundary, and return it as an output.

We can now combine all our results to provide optimality guarantees for . The procedure described above enables us to find a limit point that is an -stationary solution for . As a result, by Theorem 4 and Theorem 5, we obtain a near-stationary point for that is bounded away from zero. Furthermore, Theorem 2 allows us to conclude that we have achieved a good solution for . Theorem 3 confirms that we have indeed found a solution such that , up to a small approximation error. Finally, choosing a suitable using line search provides us with a solution such that is small.

4 Computational experiments

4.1 Experimental setting

To create a framework where we can enforce misspecification and progressively analyze how the performance of different methods varies with the level of misspecification , we need to define a model that allows for easy adjustment of the misspecification level while still yielding meaningful results. We define a model which can easily be slightly changed to be misspecified. In order to do so, we define for , to be a linear combination of polynomial functions of . This could be written in a compact way as , where is a real valued matrix, and is a vector whose coordinates are polynomial in . Furthermore, we define for and as a linear combination of the coordinates of . To increase the level of misspecification, we can omit some coordinates of in the linear combination. This can also be written compactly as , where is a matrix representation of and is a truncated version of , depending on the desired level of misspecification. We set to be a polyhedron and written as where () and . is closed and bounded, so Assumption 2 holds. In every experiment, we sample while all of its coordinates are conditioned to be between and . and the coefficients of from a standard normal Gaussian distribution, and to be equal to , where has standard normal random coefficients. We set . We write

Furthermore, for any matrix , we denote the th row of . We set the ground truth model to be where . We also write for , , where and . Here, is the number of coordinates (or features) we will be removing from to obtain , and hence causing the model to be misspecified. This can be written coherently with our theoretical setting. Indeed, we can write for all , and , , where

We denote the resulting hypothesis set when the number of removed coordinates from is equal to . We have, for any . Also, since for any such that , the inclusion is satisfied, we have . In other words, is increasing with . Furthermore, since the coordinates of the matrices and are bounded, Assumptions 3 and 4 are satisfied. Additionally, because the function is nonzero and analytic for any , and for any nonzero in the polyhedron , Proposition 1 ensures that Assumption 1 holds. Moreover, Assumption 8 is satisfied because the hypothesis set is linear.

4.2 Experimental results

We revisit the comparison performed by Hu et al., (2022). In their work, SLO is compared to SPO+, showing that when the hypothesis set is well-specified, SLO achieves a smaller value of than SPO+. Conversely, when the model is misspecified, SPO+ performs better. We extend this comparison by including our method as well. The exact losses minimized for each method are as follows:

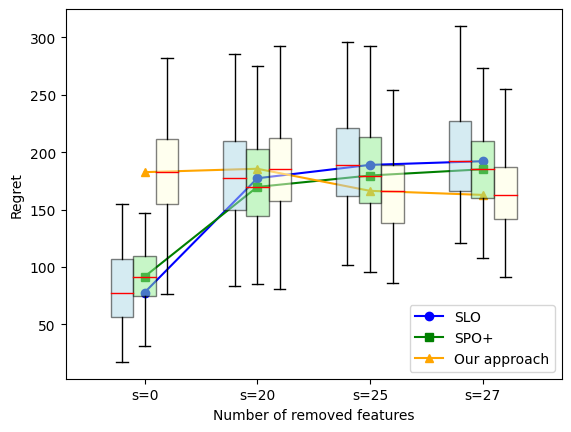

To optimize , we run gradient descent on its surrogate loss (we did not need to optimize the surrogate because the iterates did not converge to ). We choose by line search. We use as a lower bound to , and where is the solution obtained by optimizing . We test 96 evenly spaced values of in the interval , and pick yielding the solution with the best decision performance. is likely to fall into (or near) the interval , and enjoys good optimality guarantees for , which ensures that the solution we obtain yields a small value for . For every value of , we run 96 experiments to get the distribution of the testing loss for every method, and get results in the box plots in Figure 3. For every experiment, we sample , the ground truth parameter , and a training dataset containing 20 samples drawn from distribution , and run gradient descent on the three loss functions we are optimizing. All the experiments were run on the MIT Lincoln Lab supercloud (Reuther et al., (2018)).

In Figure 3, we plot the regret yielded by SLO, SPO+ and our approach, i.e. the value of

We can see that the more the model is misspecified, our method performs better compared to SPO+ and SLO. This is because whereas it is unclear whether SPO+ and SLO are capable of minimizing , our approach enjoys good theoretical guarantees. However, the more well-specified the model is, the better is SLO, which is coherent with the conclusions made in Hu et al., (2022) and Elmachtoub et al., (2023). We also notice that removing features (as long as a reasonable number of features remain) improves the performance of our approach. One possible reason for this is that our approach overfits more easily than other methods when the hypothesis set is complex (and consequently far from the misspecified case). Further investigation is yet to be done to explain this phenomenon.

5 Conclusion

In this paper, we provide a novel approach to address model misspecification in contextual optimization. State-of-the-art methods are mainly capable of optimizing the target loss representing the decision performance resulting from predictions of the random costs only when the chosen hypothesis set is well-specified. In the misspecified setting, it has been unclear whether it is possible to minimize and provide theoretical guarantees. Our surrogate loss function successfully optimizes the target loss and retrieves a good element from the chosen hypothesis set in terms of decision performance in a reasonable time. Even though our surrogate is non-convex and non-smooth, we exploited its structure: it is a difference of two convex functions, which could be smoothed in order to be optimized. We show experimentally and theoretically that our approach outperforms state-of-the-art methods when the hypothesis set is misspecified. To our knowledge, our approach is the first to provably optimize the target loss when the hypothesis set is misspecified, without requiring regularity of . Although we have proven theoretical guarantees when the chosen hypothesis set is linear, we strongly believe that these results can be generalized to a wider class of predictors. Furthermore, we have run experiments using synthetic data, and have yet to do more experiments using real world datasets to compare our approach to other state-of-the-art methods.

References

- Agrawal et al., (2019) Agrawal, A., Amos, B., Barratt, S., Boyd, S., Diamond, S., and Kolter, J. Z. (2019). Differentiable convex optimization layers. Advances in neural information processing systems, 32.

- Amos and Kolter, (2017) Amos, B. and Kolter, J. Z. (2017). Optnet: Differentiable optimization as a layer in neural networks. In International Conference on Machine Learning, pages 136–145. PMLR.

- Bertsimas and Kallus, (2020) Bertsimas, D. and Kallus, N. (2020). From predictive to prescriptive analytics. Management Science, 66(3):1025–1044.

- Domke, (2012) Domke, J. (2012). Generic methods for optimization-based modeling. In Artificial Intelligence and Statistics, pages 318–326. PMLR.

- Donti et al., (2017) Donti, P., Amos, B., and Kolter, J. Z. (2017). Task-based end-to-end model learning in stochastic optimization. Advances in neural information processing systems, 30.

- Elmachtoub and Grigas, (2022) Elmachtoub, A. N. and Grigas, P. (2022). Smart “predict, then optimize”. Management Science, 68(1):9–26.

- Elmachtoub et al., (2023) Elmachtoub, A. N., Lam, H., Zhang, H., and Zhao, Y. (2023). Estimate-then-optimize versus integrated-estimation-optimization: A stochastic dominance perspective. arXiv preprint arXiv:2304.06833.

- Foster et al., (2020) Foster, D. J., Gentile, C., Mohri, M., and Zimmert, J. (2020). Adapting to misspecification in contextual bandits. Advances in Neural Information Processing Systems, 33:11478–11489.

- Hu et al., (2022) Hu, Y., Kallus, N., and Mao, X. (2022). Fast rates for contextual linear optimization. Management Science, 68(6):4236–4245.

- Huang and Gupta, (2024) Huang, M. and Gupta, V. (2024). Learning best-in-class policies for the predict-then-optimize framework. arXiv preprint arXiv:2402.03256.

- Jeong et al., (2022) Jeong, J., Jaggi, P., Butler, A., and Sanner, S. (2022). An exact symbolic reduction of linear smart predict+ optimize to mixed integer linear programming. In International Conference on Machine Learning, pages 10053–10067. PMLR.

- Kallus and Mao, (2023) Kallus, N. and Mao, X. (2023). Stochastic optimization forests. Management Science, 69(4):1975–1994.

- Kotary et al., (2023) Kotary, J., Dinh, M. H., and Fioretto, F. (2023). Backpropagation of unrolled solvers with folded optimization. arXiv preprint arXiv:2301.12047.

- Krishnamurthy et al., (2021) Krishnamurthy, S. K., Hadad, V., and Athey, S. (2021). Adapting to misspecification in contextual bandits with offline regression oracles. In International Conference on Machine Learning, pages 5805–5814. PMLR.

- Liu et al., (2021) Liu, M., Qi, M., and Shen, Z.-J. M. (2021). End-to-end deep learning for automatic inventory management with fixed ordering cost. Available at SSRN 3888897.

- Loke et al., (2022) Loke, G. G., Tang, Q., and Xiao, Y. (2022). Decision-driven regularization: A blended model for predict-then-optimize. Available at SSRN 3623006.

- McKenzie et al., (2023) McKenzie, D., Fung, S. W., and Heaton, H. (2023). Faster predict-and-optimize with three-operator splitting. arXiv preprint arXiv:2301.13395.

- Mityagin, (2015) Mityagin, B. (2015). The zero set of a real analytic function. arXiv preprint arXiv:1512.07276.

- Monga et al., (2021) Monga, V., Li, Y., and Eldar, Y. C. (2021). Algorithm unrolling: Interpretable, efficient deep learning for signal and image processing. IEEE Signal Processing Magazine, 38(2):18–44.

- Nocedal and Wright, (1999) Nocedal, J. and Wright, S. J. (1999). Numerical optimization. Springer.

- Pang et al., (2017) Pang, J.-S., Razaviyayn, M., and Alvarado, A. (2017). Computing b-stationary points of nonsmooth dc programs. Mathematics of Operations Research, 42(1):95–118.

- Reuther et al., (2018) Reuther, A., Kepner, J., Byun, C., Samsi, S., Arcand, W., Bestor, D., Bergeron, B., Gadepally, V., Houle, M., Hubbell, M., Jones, M., Klein, A., Milechin, L., Mullen, J., Prout, A., Rosa, A., Yee, C., and Michaleas, P. (2018). Interactive supercomputing on 40,000 cores for machine learning and data analysis. In 2018 IEEE High Performance extreme Computing Conference (HPEC), pages 1–6. IEEE.

- Sadana et al., (2024) Sadana, U., Chenreddy, A., Delage, E., Forel, A., Frejinger, E., and Vidal, T. (2024). A survey of contextual optimization methods for decision-making under uncertainty. European Journal of Operational Research.

- Sun et al., (2023) Sun, C., Liu, S., and Li, X. (2023). Maximum optimality margin: A unified approach for contextual linear programming and inverse linear programming. In International Conference on Machine Learning, pages 32886–32912. PMLR.

- Sun et al., (2022) Sun, H., Shi, Y., Wang, J., Tuan, H. D., Poor, H. V., and Tao, D. (2022). Alternating differentiation for optimization layers. arXiv preprint arXiv:2210.01802.

- Sun and Sun, (2021) Sun, K. and Sun, X. A. (2021). Algorithms for difference-of-convex (dc) programs based on difference-of-moreau-envelopes smoothing. arXiv e-prints, pages arXiv–2104.

- Wainwright, (2019) Wainwright, M. J. (2019). High-dimensional statistics: A non-asymptotic viewpoint, volume 48. Cambridge university press.

Appendix

5.1 Proof of Theorem 2

Proof. We proceed in two steps.

Step 1. We first prove the Lipschitz continuity of the generalization, i.e. that there exists a constant such that for every ,

| (18) |

For every , using Lagrangian duality,

| (19) | ||||

| (20) | ||||

| (21) | ||||

| (22) |

In (22), we have switched the min and the max because of strong duality, since the objective function we are optimizing is linear. For a given , we denote to be the optimal dual variable corresponding to in the minimization problem above. Let and . We have

We now bound the two terms above on the right side of the inequality. We have

In the left hand side of the inequality above, we can see that if , then replacing by gives a larger term than the one above, and when , replacing by gives a larger term than the one above as well. Let such that replacing and by makes the expression above larger. We have, by replacing and by in the inequality above, we get

where for every ,

is a convex bounded set, and for all and the two functions , , are both differentiable with respect to . Moreover, and (where is the jacobian of at ) are both continuous with respect to for all and . Hence, using Danskin’s theorem, we can say that for all , and are both subdifferentiable, and that for all , , . These two sets are bounded by because of Assumption 4. This means that the two functions in the equality above are both lipschitz, which makes lipschitz.

We can also easily prove that the inequality above is also true when we replace by . Hence, we can deduce that

which yields the desired result of step 1.

Step 2. We will now prove the desired generalization bound by bounding the generalization gap locally in balls covering the set which represents the possible values of . Let be a set of balls of radius (for the norm ) such that . According to Wainwright, (2019), it is possible to choose such that . For every , let be an element of . For a given we would like to bound the probability using Hoeffding’s inequality. In order to do that, we first notice that using Lagrangian duality, we get

where and are respectively optimal dual variables in the bottom and top line above. As we have seen before, there exists such that replacing and by makes the above term larger. Hence, we have

Hence, we have . This enables us to apply Hoeffding’s inequality to the term on the right given that we bound the random variable

It is easy to see that using Cauchy-Schwartz inequality, we have

In order to upper bound the right-hand side, we need to upper bound . In order to do this, we prove that the Lagrange multiplier for and is bounded for any . We will prove it is the case for , and the proof for will immediately follow. Assuming is the Lagrange multiplier for , we have

| (23) | ||||

| (24) | ||||

| (25) |

Inequality (23) holds because the left-hand side is the evaluation of the right-hand side at . Hence,

This yields

Hence, we get the following upper bound for the random variables we are working with

we can apply Hoeffding’s inequality, and say that

This yields

By denoting , we can say that with probability at least , we have

which gives

Now we have for every , denoting such that ,

| (26) | ||||

| (27) | ||||

| (28) |

Inequality (28) is resulting from the Lipschitz inequality (18). Taking , we get

Since we have , we can replace in the inequality above by and get

5.2 Proof of Lemma 1

Proof. Since the only difference between the right and left optimization problems in is an additional constraint added to the right problem, it is clear that it will yield a higher value than the right one for any , and consequently we have that indeed is positive.

5.3 Proof of Proposition 1

Proof. For any the uniqueness of the solution to the linear program is a consequence of the condition . Since the set has a zero Lebesgue measure and that has a continuous distribution, it follows that

i.e. when , the linear program has a unique solution almost surely.

5.4 Proof of Proposition 2

Proof. We denote for every and , . We want to prove that for every , is weakly convex. More precisely, we want to prove that there exists such that for every , is convex. We have for every , using assumptions 8 and 2,

We denote for every and , . We have for every ,

Hence, for every , is convex. This implies that for any measurable mapping , is convex. Consequently, and are both maximums of a family of convex functions, and hence are also convex functions. Finally we have for every ,

Finally, we can write for every ,

which is indeed a difference of convex functions.

5.5 Proof of Theorem 3

Proof. Let and . Assumption 7 gives

where

We have for , denoting , ,

Hence, we have

| (29) |

We denote for , , and ,

and the event defined by

Hence, we have for every mapping and ,

Furthermore, we have for every

Notice that (29) can be rewritten as . Hence, we have

In conclusion, we have for every and every , and mapping ,

the inequality above is trivially verified when . Also, when taking , we get

Let . Assume that is bounded away from . We have

To optimize the right hand side and ignoring the constant, we take . This gives

5.6 Proof of Theorem 4

Proof.

-

1.

We denote for all , , and for all , , In this case, for all , the loss writes as

Let and be the set of minimizers of respectively over and over . Given that and are compact sets, and for all is differentiable, and is continuous, we can say by Danskin’s theorem that for all ,

The two inequalities and are due to the fact that and are convex sets. Furthermore, we have for all ,

where . All of the above clearly yields

which is the result we were seeking to prove.

-

2.

From the above, it is clear that for a given if , then . Furthermore, using the very first definition of , since , we have for all ,

In conclusion, is a lower bound of , and if for a given , , then , i.e. is a minimizer of .

-

3.

is the difference of the Moreau envelope of two convex functions, hence it is the difference between two differentiable convex functions. this yields that is differentiable. Furthermore, if is a stationary point of then using proposition 1 from Sun and Sun, (2021), is indeed a stationary point of . Furthermore, we have for every , We consider an -stationary point of , i.e. . Using Danskin’s theorem, we get

Where and . By looking at the proof of Lemma 2, we can easily see that we also have where and where . Let . We have

(30) (31) (32) (33) (34) (35) (36) (37) Here, is defined for any as . The last equality 37 is due to the fact that the subgradient of at some is in (which can be proven thanks to Danskin’s theorem) and is hence bounded by . We can see that inequality 37 is indeed the inequality we were seeking to obtain. Taking gives that stationarity for implies global optimality for .

5.7 Proof of Lemma 2

Proof. The main idea of the proof is to switch min and max in the definitions of and .

-

1.

We have for all ,

(38) (39) (40) (41) (42) (43) The equality between 43 and 42 holds because of Sion’s minimax theorem: since and are convex sets, is upper semi-continuous and concave for any , and is lower semicontinuous and convex for any , we can switch min and max. In 43, the minimum is reached when the gradient with respect to is zero, i.e. , which gives . In this case, we get

The calculations above also give us immediately that where .

-

2.

The proof of the second property is almost identical to the previous one. It suffices to replace by and by .

5.8 Proof of Proposition 3

This proposition immediately follows from Lemma 2.

5.9 Proof of Theorem 5

Proof. We will sequentially prove the two points. We assume that is a stationary point of . In this case, we have

This yields

Taking the norm in both sides, we get , and finally, replugging this in the equality above, we directly get , i.e. . Let us now prove the second result. We denote and . We assume now that . This inequality gives us two inequalities

Hence, we have

Let such that , i.e.

| (44) |

We have

| (45) | ||||

| (46) | ||||

| (47) |

The last inequality is due to inequality 44 and . We finish by proving this last equality. We have for every ,

| (48) | ||||

| (49) | ||||

| (50) |

Notice that when the left-hand side in 50 is minimized (i.e. , the right-hand side takes the same value. Hence, is also a minimizer of the left-hand side, i.e. . Finally, inequality 47 yields

Which gives

Using this, we also prove the bound on the gradient of . Using the properties of the projection , we have

We finish by proving the bound on . Using Lemma 3, we have , hence,