Information criteria for the number of

directions of extremes in high-dimensional data

Abstract

In multivariate extreme value analysis, the estimation of the dependence structure in extremes is a challenging task, especially in the context of high-dimensional data. Therefore, a common approach is to reduce the model dimension by considering only the directions in which extreme values occur. In this paper, we use the concept of sparse regular variation recently introduced by meyer_sparse to derive information criteria for the number of directions in which extreme events occur, such as a Bayesian information criterion (BIC), a mean-squared error-based information criterion (MSEIC), and a quasi-Akaike information criterion (QAIC) based on the Gaussian likelihood function. As is typical in extreme value analysis, a challenging task is the choice of the number of observations used for the estimation. Therefore, for all information criteria, we present a two-step procedure to estimate both the number of directions of extremes and an optimal choice of . We prove that the AIC of meyer_muscle23 and the MSEIC are inconsistent information criteria for the number of extreme directions whereas the BIC and the QAIC are consistent information criteria. Finally, the performance of the different information criteria is compared in a simulation study and applied on wind speed data.

keywords:

[class=MSC] 62H30keywords:

and

1 Introduction

Multivariate extreme value statistics analyses the probabilities of joint extreme events in multivariate data with a wide range of applications, such as finance, insurance, meteorology, hydrology and, more generally, environmental risks due to the influence of climate change. This is a challenging task, especially for high-dimensional data, where modern research combines knowledge from extreme value theory with multivariate statistics and machine learning.

Multivariate regular variation is a classical concept for modeling multivariate extremes (resnick1987, resnick2007, Falk:Buch). Suppose is a -dimensional random vector and there exists an index (tail index) and a measure on the unit sphere (spectral measure) such that

| (1.1) |

for all and all Borel sets with , then is called multivariate regularly varying of index . The spectral measure contains the information about the dependence structure in the extremes of and therefore a particular goal is the determination of . However, in high-dimensional data sets where is large, this can be challenging and computationally intensive because the dependence structure in the extremes is usually complex. In the case of high dimensions, the spectral measure is often sparse and has support in a lower-dimensional subspace. Therefore, a standard approach from multivariate statistics is to first apply a dimension reduction method to find the support of and then to estimate , which drastically reduces the computational time and the quality of the estimation.

The literature on dimension reduction methods for multivariate extremes using statistical learning methods has grown rapidly in recent years. Starting with chautru who first applies a principal component analysis (PCA) and then a cluster analysis with spherical -means to the spectral measure of a multivariate regularly varying random vector to find a group of variables that are jointly extreme. The reconstruction error of PCA is then analyzed in DS:21 and recently, Sabourin_et_al_2024 extend the PCA approach to Hibert-valued regularly varying random objects, whereas AMDS:22 use with kernel PCA a nonlinear generalization of PCA. In addition, CT:19, MR4582715 apply a PCA to the tail pairwise dependence matrix. The unsupervised learning approach of using spherical -means, a variant of -means, for cluster analysis in extreme observations was taken up in AMDS:24, Bernard_2013, JW:20, Fomichov:Ivanovs. The topic of this paper is support identification of the spectral measure, related literature on support identification is damex, tawn, meyer_muscle23, pmlr-v139-jalalzai21a. A completely different line of research to represent the sparsity structure in multivariate models are graphical models as, e.g., Engelke:Hitz, Engelke:Volgushev, engelke2024, Gissibl_et_al, Gissibl_et_al:2018, to name only a few. A very nice overview of recent advances in probabilistic and statistical aspects of sparse structures in extremes is given in Engelke:Ivanovs.

The support of can be identified by the disjoint partition of the unit sphere into sets of the form

| (1.2) |

Knowing for all allows us to draw conclusions about the support of and the directions of the extremes. Of course, implies that the components in the set are jointly extreme, we have an extreme event in the direction . However, the disjoint partition of consists of sets so it is huge for large values of , and estimating is non-trivial. On the one hand, and therefore the interior of is the empty set. As a consequence, if then the convergence in (1.1) for does not necessarily hold. On the other hand, if has a continuous distribution there are empirically no observations in the set . Therefore, the empirical estimator for based on 1.1 is not consistent and useful anymore. To avoid this problem, the support detection algorithm DAMEX (Detecting Anomalies among Multivariate EXtremes) of damex works with truncated -cones to generate continuity sets that approximate the sets in (1.2), and tawn use the concept of hidden regular variation on a collection of nonstandard subcones of .

A completely different approach to mitigate this problem is proposed in meyer_sparse, meyer_muscle23 by introducing the concept of sparse regular variation, which is equivalent to regular variation under some mild assumptions (see Section 2 for a definition). The main difference between regular variation and sparse regular variation is that the self-normalization in (1.1) is replaced by the Euclidean projection of for large , where the Euclidean projection is defined as in duchi as . The advantage of this approach is that usually has more zero entries than and therefore, is more sparsely populated and advantageous when only a few components are extreme together, as in a high-dimensional setting. Since their empirical estimator for the number of extreme directions in the sparse regularly varying model is biased, indeed overestimates the true number of directions, they develop an Akaike Information Criterion (AIC) consisting of two steps. In the first step, they estimate the number of extreme directions by the AIC for bias selection, but as usual, in extreme value theory, the estimation depends on the chosen threshold that goes into the estimation; the observations above this threshold determine the extreme observations. Therefore, they extend the AIC for bias selection to an AIC for threshold selection, where the threshold is also estimated. What is really special is that they were able to develop a method to estimate the number of extreme directions and the threshold at the same time, both of which are very challenging tasks on their own. But as we prove in Section 3, the AIC for bias selection is not a weakly consistent information criterion, as is often the case for Akaike’s information criteria, and so we develop alternatives. Consistency is examined only for bias selection and not for threshold selection, because there is no ”true” threshold. On the one hand, the threshold must be chosen high enough to ensure that the asymptotic results hold. On the other hand, if the threshold is set too high, non-extreme observations may be included, biasing the results.

In this paper we use the approach of meyer_muscle23 of sparse regular variation and propose three different information criteria to estimate the number of extreme directions and the choice of the threshold, the BIC, QAIC and MSEIC for bias selection and threshold selection, which are particularly suitable for high dimensional data with a sparsity structure in the extreme behavior. Thus, we develop procedures to estimate the number of extreme directions and the optimal choice of the threshold at the same time. The application of these information criteria is very simple in practice and not computationally intensive. Besides the AIC, the Bayesian Information Criterion (BIC), which goes back to schwarz, is the most popular in practice and tries to select the model with the highest posterior probability. The statistical model behind our BIC is the same as that of the AIC in [meyer_muscle23], where we fit a multinomial model to the relative number of extreme observations in the subspaces and derive an asymptotic upper bound on the posterior likelihood, which then defines the BIC. In contrast, the QAIC for Quasi-Akaike Information Criterion approximates the Kullback-Leibler divergence of the true model and a Gaussian model, rather than a multinomial model as used in the AIC and BIC, respectively. The advantage of BIC and QAIC over AIC is that they are consistent information criteria for bias selection. Finally, the third method, MSEIC, stands for mean-squared error information criteria, because we approximate the mean-squared error (MSE) of the relative number of extreme observations and the true probabilities of extremes in the different subspaces . Although MSEIC is not consistent for bias selection, it performs extremely well in all simulations.

Structure of the paper

The paper is organized as follows. In Section 2 we properly define extreme directions based on the concept of sparse regular variation and introduce consistent and asymptotically normally distributed estimators for the probabilities of the extreme directions as in meyer_muscle23. We also present statistical models for some of our information criteria. The main results of the paper are derived in Sections 3, 4, 5 and 6. In Section 3 we examine the AIC for the bias selection of meyer_muscle23 and conclude that it is not a consistent information criterion. This is in contrast to the popular BIC and QAIC for bias selection. In Section 4-6 we first develop the BIC, then the QAIC and finally the MSEIC for bias selection and threshold selection, and prove that the BIC for bias selection is a consistent information criterion. Furthermore, in Section 5 we introduce the QAIC for bias and threshold selection and in Section 6 similarly the MSEIC. In addition, we derive in these sections that BIC and QAIC are consistent information criteria for bias selection, while MSEIC is not consistent. Finally, we compare all information criteria in a simulation study in Section 7 and apply them to extreme wind data from the Republic of Ireland in Section 8. Finally, we draw some conclusions in Section 9. The main proofs of the paper are moved to the appendix, while the proofs of some auxiliary results can be found in the supplementary material.

Notation

In this paper, we use the following notation. For a vector and a set we write for and for a diagonal matrix with the components of on the diagonal. Furthermore, is the identity matrix, is the zero vector and is the vector containing only . Moreover, is the -norm and is the Euclidean norm for . The unit sphere is defined with respect to the -norm. For , operations as and are meant component-wise. The gradient of a function is written as for and the partial derivative with respect to the -the component of is . By we denote the absolute value of a real number and by the cardinality of a set , but the meaning should be clear from the context. In addition, is the power set of the set and . Finally, is the notation for convergence in distribution and is the notation for convergence in probability.

2 Preliminaries

This section addresses the main concepts of the paper which are based on meyer_sparse, meyer_muscle23. We start with an introduction into sparse regular variation and then derive a proper definition of extreme direction in Section 2.1. The challenging task in the statistical inference of extreme directions is the detection of the bias directions which are rigorously defined and motivated in Section 2.2. Then, in Section 2.3, we give an overview on the statistical inference of the empirical estimator of the probabilities of extreme directions and the assumptions of the present paper. Finally, in Section 2.4, we present statistical models on which the information criteria are based.

2.1 Sparse regular variation and extreme directions

First, we introduce the concept of sparse regular variation with the Euclidean projection defined as .

Definition 2.1.

An -valued random vector is called sparse regular varying, if a -valued random vector and a non degenerate random variable exist such that

for all and all Borel sets with .

Remark 2.2.

Note that is Pareto-distributed for an and models the radial part, whereas the -valued random vector corresponds to the angular part. Therefore, we write briefly .

A proper definition of extreme directions is now the following using that is the power set of the set and .

Definition 2.3.

A direction is an extreme direction, if The set of all extreme directions is denoted as

Remark 2.4.

-

(a)

The use of the -projection leads to a sparse representation, in the sense that under more components are projected to zero compared to the normalization . Therefore, it is not surprising that according to meyer_sparse, implies for . Thus, an extreme direction under regular variation is as well an extreme direction under sparse regular variation but the opposite does not necessarily hold. However, the maximal directions under regular variation and sparse regular variation are equivalent such that we do not lose much information on the support of under sparse regular variation.

-

(b)

Since the preimages are sets with positive Lebesgue measure, the sets are continuity sets of . Finally, from meyer_sparse we know that

so that can be estimated empirically in contrast to .

The aim of the paper is to estimate , the number of extreme directions under sparse regular variation, through the use of information criteria.

2.2 Bias directions

A major challenge for the estimation of the extreme directions is that the empirical estimators of the probabilities , , detect more extremal directions than there are true extremal directions, which we call bias directions. To understand the idea of bias directions better we require some further notation. Suppose is the order statistic of and the number of extreme observations used for the estimations is denoted by , whereas we assume that as . Suppose that there exists a sequence of high thresholds for such that and as . Due to meyer_muscle23 the empirical estimator

of the probability

| (2.1) |

is a consistent estimator, so that the empirical observed set of extreme directions is

To be able to relate the true set of extreme directions with the empirically estimated set of extreme directions, we define the set

where

Of course, implies such that trivially, and . Under the Assumption HRV, a shorthand for hidden regular variation, we can say more.

Assumption HRV.

For every we define the cone

and suppose that the random vector is multivariate regular varying on with tail index and exponent measure satisfying

A conclusion from meyer_muscle23 is then that under Assumption HRV even

holds. Thus, the empirical estimator tends to overestimate the set of extreme directions (but does not underestimate it). On the one hand, for large and with this means that is not an extreme direction. But on the other hand, for large there might be a with which is not an extreme direction; a mathematical more rigorous interpretation is given in meyer_muscle23. Such a direction is referred to as a bias direction. The main challenge is to identify these bias directions.

2.3 Statistical inference for the probabilities of extreme directions

The general assumptions of the present paper are motivated by the statistical inference of the probabilities of extreme directions as derived in meyer_muscle23. To understand the statistical inference and hence, the assumptions, we have to enumerate the in the following way with as defined in (2.1):

where the remaining with , are ordered in an arbitrary but fixed order such that for . We write briefly for ,

where

Finally, we define the associated vectors

In the next theorem, we summarize the asymptotic behavior of these estimators as derived in meyer_muscle23.

Proposition 2.5.

Suppose Assumption HRV holds and the sequence in with and satisfies almost surely for all large enough. Furthermore, assume that for some and any as ,

-

(a)

Then, as ,

-

(b)

If additionally as and , then as ,

Motivated by this result we define for any

and suppose the following assumption throughout the paper.

Assumption A.

-

(A1)

Suppose is a sequence in with and . Furthermore almost surely for all large enough, which implies almost surely for all large enough.

-

(A2)

almost surely for all large enough.

-

(A3)

Suppose that as ,

-

(A4)

Suppose that as ,

Remark 2.6.

The following lemma is a direct consequence of Assumption A.

Lemma 2.7.

Suppose Assumption A and A holds. Then the following statements are valid.

-

(a)

and as .

-

(b)

For and ,

-

(c)

For and ,

and similarly,

2.4 Statistical models

A challenging task in extreme value theory is the optimal choice of , the number of extreme observations used for the estimation procedure. Therefore, we follow a two-step procedure as motivated in meyer_muscle23. In the first step, we fix and estimate the relevant extreme directions and separate them from the so-called bias directions using some information criteria. Therefore this step is called bias selection. In the second step, we estimate the threshold , this step is therefore named threshold selection. In the following subsections, we present some statistical models for the bias selection in Section 2.4.1 and the statistical models for the threshold selection in Section 2.4.2.

2.4.1 The local model for the bias selection

The random vector is multinomial distributed with repetitions and unknown -dimensional probability vector which converges for to . To detect the bias directions and hence, to estimate , the idea is now to fit for any a multinomial distribution from the class where is defined as

and the parameter space is defined as

which reflects that there are bias directions. Finally, we define

We summarize this in the following model.

MODEL : The family of multinomial distributions with likelihood function

and log-likelihood function

| (2.2) |

is called Model .

Now, an information criterion aims to find the Model from which best fits the distribution of and results in an estimator for . Then, for a given estimator of we estimate the probability vector by

| (2.3) |

where

| (2.4) |

is the maximum likelihood estimator (MLE) of the multinomial model (see meyer_muscle23, Section 4.1). Finally, we define

as estimator for .

2.4.2 The global model for the threshold

Next, we extend the previous model and assume that is not fixed anymore, it has additionally to be estimated. For this task, we use all observations and not only the largest observations. We consider an artificial random vector in which includes extreme and non-extreme observations, where the components count the number of extreme observations in the subsets . The -th component counts the number of non-extreme values and is -distributed for some . To be more precise we assume that with

and the conditional distribution given satisfies

| (2.5) |

The idea of this assumption is that if we have extreme observations (and hence, non-extreme observations), then the distribution of the extreme directions in the global model is the same as that of the local model with threshold .

Now, the approach to detect the bias directions and the threshold is similar to the previous section. We fit a multinomial distribution from the class to the artificial random vector where is defined as

and the parameter space is

Finally, we define

This ends in the following model.

MODEL : The family of multinomial distributions with log-likelihood function

| (2.6) |

is called Model .

To link the global model with the local model we require further assumptions.

Assumption B.

-

(B1)

Suppose and are independent, and for we have as ,

-

(B2)

Suppose for we have as ,

-

(B3)

There exist constants such that

3 Akaike information criterion

We start to investigate the Akaike information criterion () of meyer_muscle23 for the number of extreme directions defined as

for fixed , which is motivated by minimizing the expected Kullback-Leibler (KL) divergence between the true distribution of and the multinomial distribution where is the MLE given in (2.4). The number of extreme directions is then estimated via

Theorem 3.1.

Suppose Assumption A and A holds. Then

The proof is given in Section A.1. This statement concludes that the is not a weakly consistent information criterion because asymptotically there exists a positive probability of overestimating . In the high sample size and fixed dimension setting with and this is a typical property of the (see ModelSelection, C:16).

4 Bayesian information criterion

In addition to the , the Bayesian information criterion (BIC) introduced in schwarz is the most popular one. The basic idea of the BIC is to find the model with the highest posterior probability given the data. First, we derive a BIC for in Section 4.1 and then for in Section 4.2. The proofs of this section can be found in Section A.2.

4.1 Bayesian information criterion for the number of extreme directions

In the following, we derive a BIC for by bounding the posterior probability as in bicgeneralisation. Therefore, we assume throughout this section Model and use the following notation. Let be a discrete prior distribution over the set of models , be the prior density over the parameter space given Model , be the likelihood function of Model if we observe and be the (unknown) marginal probability of . Given the data the goal is to determine the Model with the highest posterior probability for . Therefore, note that Bayes Theorem yields for the posterior density for and

Hence, the posterior probability for is

Consequently maximizing the posterior probability is equivalent to minimizing

| (4.1) |

For the derivation of the BIC, we require further assumptions.

Assumption C.

For any we assume the following:

-

(C1)

There exist constants such that the prior density on satisfies

-

(C2)

The prior distribution is a uniform distribution on , i.e. for .

-

(C3)

and .

Remark 4.1.

Assumption in (C3) ensures that does not converge to zero too quickly. Assumptions (C1) and (C2) concern the prior distribution and they result from the fact, that we have no information about possible prior distributions. The lower bound of Assumption (C1) can be relaxed since it is only necessary in a neighborhood of . However, it has been omitted in this paper for the sake of brevity.

The next theorem gives an upper bound for

whereby denotes the conditional expectation regarding the prior density on . This results then in an upper bound for the negative log posterior probability of the -th Model given .

Plugging in Assumption (C2) and the upper bound in Theorem 4.2 in section 4.1 results in

This motivates the definition of the following information criterion, where the terms are neglected as they are not influenced by .

Definition 4.3.

For the number of extreme directions with fixed the Bayesian information criterion concerning the upper bound () is defined as

and an estimator for is .

Motivated by the , which is based on the largest eigenvalue from Lemma A.2, we define a BIC based on a lower bound for the posterior distribution by using the smallest eigenvalue from Lemma A.2.

Definition 4.4.

For the number of extreme directions with fixed the Bayesian information criterion concerning the lower bound () for Model is defined as

and an estimator for is .

Theorem 4.5.

Suppose Assumption A and A holds. Then

-

(a)

-

(b)

Thus, in contrast to the criterion, both information criteria are weakly consistent and select asymptotically with probability the true Model . Analog to the , this is also a typical property of Bayesian information criteria (see ModelSelection, C:16).

4.2 Bayesian information criterion for the threshold

In the following, we determine an upper bound for the posterior probability of the global Model analog to the previous Section 4.1 using the following assumptions.

Assumption D.

Suppose the following statements hold.

-

(D1)

There exist constants such that the prior density on satisfies

-

(D2)

The prior distribution is a uniform distribution on , i.e. for .

-

(D3)

and .

-

(D4)

For the following upper bound

holds.

Remark 4.6.

- (a)

- (b)

- (c)

In analogy to Section 4.1, the goal is to derive asymptotic bounds for which we obtain through upper bounds for

| (4.2) |

where denotes the conditional expectation with respect to the prior density on given Model .

Theorem 4.7.

Compared to Theorem 4.2 in the previous section, we take additionally the expectation in Theorem 4.7 to achieve a connection between the global model and the local model.

Theorem 4.7 motivates the definition of the following information criterion, where the expectation is omitted, the inequality is divided by and the term as well as are neglected as they are either constant concerning or converge to zero uniformly.

Definition 4.8.

For the number of exceedances the Bayesian information criterion concerning the upper bound () for the threshold for Model is defined as

for , with estimator for for .

Similarly to Definition 4.4 we also define the Bayesian information criterion based on the lower bound for the threshold .

Definition 4.9.

For the number of exceedances the Bayesian information criterion concerning the lower bound () for the threshold for Model is defined as

with estimator for .

5 Quasi-Akaike information criterion

Next, we propose an information criterion that is motivated by the Akaike information criterion and therefore it is called quasi-Akaike information criterion (), but instead of working with the likelihood function of a multinomial distribution as in meyer_muscle23 (cf. Section 3) we use the likelihood function of a Gaussian distribution. The advantage of this information criterion, in contrast to the , is that it is consistent. The proofs of this section are given in Section A.3.

5.1 Quasi Akaike information criterion for the number of directions

The reason behind employing the likelihood function of a Gaussian distribution for the is that due to Assumption A the asymptotic behavior as ,

holds, i.e. the asymptotic distribution of is similar to the distribution of a -variate normal distribution with mean and covariance matrix . Therefore, the idea is to calculate the expected Kullback-Leibler divergence of the true distribution of with density and the normal distribution , where is defined as

The likelihood function of is denoted by . For we use the estimator

| (5.3) |

where is an i.i.d. copy of .

Remark 5.1.

In summary, we calculate

| (5.4) |

Remark 5.2.

The is based on the multinomial distribution whereas the is based on the multivariate normal distribution. Although it seems at first view that both approaches are different they are related due to local limit theorems for the multinomial distribution as given in multinomial_local_limit.

Next, we derive an auxiliary result that helps to approximate the second term in (5.4) for .

Proposition 5.3.

Therefore, for we approximate the second term in 5.4 by

and neglect the expectation. The first term in 5.4 and the do not influence the choice of the model, therefore we skip them. This leads to the following definition of the theoretic quasi-information criterion for ,

If this information criterion works as well since

| and for we have | ||||

Therefore, the information criterion does not select .

Moreover, since

it does not matter if we use the estimator or with . Therefore, we finally define the following quasi-information criterion based on the estimators and since in applications and hence, is unknown.

Definition 5.4.

For the number of extreme directions with fixed the quasi Akaike information criterion () is defined as

for and an estimator for is .

Remark 5.5.

-

(a)

During the derivation of the we assumed that is constant and hence, it should not influence the optimal value of the . However, the simulation study shows that in applications has a significant impact on the performance of the because in practice depends on .

-

(b)

The derivation of a with an estimator based on the likelihood function of the normal distribution is possible with similar results but leads to a more elaborate and longer calculation. In this case, the estimator is given by

The performance of both approaches is similar and therefore only is included in the simulation study.

Theorem 5.6.

Suppose Assumption A and A holds. Then

Compared to the , the has the advantage that it is weakly consistent for fixed in contrast to the .

5.2 Quasi Akaike information criterion for the threshold

For the for the threshold we follow the definition of the global model for the in meyer_muscle23 which is defined as

with as in Section 3. However, since we consider two times the negative likelihood instead of just the negative likelihood we include additionally the factor and obtain the following information criterion.

Definition 5.7.

For the number of exceedances the quasi-Akaike information criterion () for the threshold for the Model is defined as

for with estimator for .

Remark 5.8.

An interpretation of this information criterion is as follows. The division by can be seen as a weight, which is assigned to a pair . Therefore, when is large, the weight of the corresponding model gets smaller. Also, corresponds to the relative proportion of extreme observations and acts as a penalty for increasing .

6 Mean squared error information criterion

Finally, we propose an information criterion based on the mean squared error (MSE) for both the number of directions in Section 6.1 as well as for the threshold in Section 6.2. The proofs of this section are moved to Section A.4.

6.1 Mean squared error information criterion for the number of extreme directions

The basic idea of the AIC is to minimize the Kullback-Leibler distance of the true distribution and a parametric family of distributions. This minimum is approximated by the expected Kullback-Leibler distance of the true distribution and the estimated distribution as is done in 5.4. In the following, we use the same ideas but instead of using the Kullback Leibler distance we use the normalized mean-squared error (MSE) of the parameter estimator and find an approximation of

| (6.1) |

instead of as is done in 5.4, where

for . The reason for this normalization is that, due to Assumption A, . First, we derive an auxiliary result that helps to approximate .

Theorem 6.1.

Therefore, for we approximate (6.1) by

Analogously to Section 5 we neglect the expectation, which leads to the following information criterion.

Definition 6.2.

For the number of extreme directions with fixed the mean squared error information criterion () is defined as

for with . An estimator for is defined by .

Theorem 6.3.

Suppose Assumption A and A holds. Then

In particular, for this information criterion is consistent, but unfortunately not for . However, this is not surprising because the basic ideas are related to the AIC which is also not a consistent information criterion. However, the simulation study in Section 7 shows that MSEIC performs extremely good in practice.

6.2 Mean squared error information criterion for the threshold

Next, we extend the information criterion to choose the optimal threshold . Therefore, we use not only our knowledge about the extreme observations but also our knowledge of the non-extreme observations, similarly as in the global model only that we do not have a distributional assumption. As before we assume here that pertains the information about the observed extreme directions and the non-extreme observations, where is assumed to be binomially distributed. The MSE information criterion for the threshold is then defined as weighted MSE

| (6.2) |

with weight for the estimation of the probabilities of extreme directions and weight for the estimation of the probability of non-extremes. Since we want to make statements about the optimal choice of which models the number of extreme directions, the weight in the estimation of the probabilities of the extreme directions is chosen higher. A connection between the MSE information criterion for the threshold and the MSE information criterion for the number of extreme directions exists through the following theorem.

Since is not influenced by and is of a smaller order than by Assumption (B3), we neglect and the last term. Consequently, we define the following information criterion.

Definition 6.5.

For the number of exceedances the mean squared error information criterion () for the threshold for the Model is defined as

with estimator for .

Remark 6.6.

The general structure of this threshold information criterion differs from the other derived information criteria for the threshold selection as

Therefore, we performed a simulation study with the criterion , defined analog to . The simulation study confirms that this choice of information criteria is not the suitable choice. The result is not surprising, since is not based on a likelihood-based approach.

7 Simulation study

In this section, we compare the performance of the different information criteria by a simulation study. Throughout these examples, is between and of the data. Therefore, we simulate times a multivariate regularly varying random vector of dimension . For the distribution of we distinguish two cases. Either exhibits asymptotic independence (Section 7.2) or has a max mixture distribution (Section 7.3). These examples can be found in meyer_muscle23 and tawn as well. In both examples, we estimate the parameters and by and , respectively, based on observations with the different information criteria: and . Then we estimate the probability vector by given in 2.3. The code for the following simulations is available at https://gitlab.kit.edu/projects/164856.

7.1 Error measures

To quantify the discrepancy between the true distribution and the estimated distribution in 2.3 we use different measures. We start with the Hellinger distance, which is for discrete probability measures and with probabilities and for given by where and . Since our primary goal is the identification of the relevant directions , we employ alternative measures. These measures evaluate the validity of a detected direction, without considering the weight assigned to it.

To be more precise, the confusion matrix visualizes the performance of an information criterion. Suppose an information criterion gives as an estimator for the number of true directions of possible directions. Then we define the confusion matrix for the different information criteria (IC)

| Theoretic direction | No theoretic direction | #Directions | |

| IC detects direction | True positive (TP) | False positive (FP) | |

| IC detects no direction | False negative (FN) | True negative (TN) | |

| #Directions |

and as error measures

| Accuracy Error | |||

| Error |

which reflects the errors. If we take and , respectively, we obtain the original definition in confusion_matrix such that our error measures are negatively oriented and a lower value is better. The Accuracy Error measures the relative number of false classified directions, whereas the Error is the harmonic mean based on the precision and the recall. Note, that the precision error is the relative amount of actual theoretical directions to the number of detected directions whereas the recall gives the proportion of theoretical directions.

7.2 Asymptotic tail independent model

In the first example, we consider -dimensional i.i.d. random vectors whose spectral measure only concentrates on the axis. To define their distribution, we assume that with and

Note that and . Suppose now under the condition of and are i.i.d. with empirical cumulative marginal distribution function of . Then define the random vectors , , as

which are regularly varying with tail index and exhibit pairwise asymptotic independence (resnick1987, Corollary 5.28 and resnick2007, Proposition 9.4) such that the extreme directions are the axes.

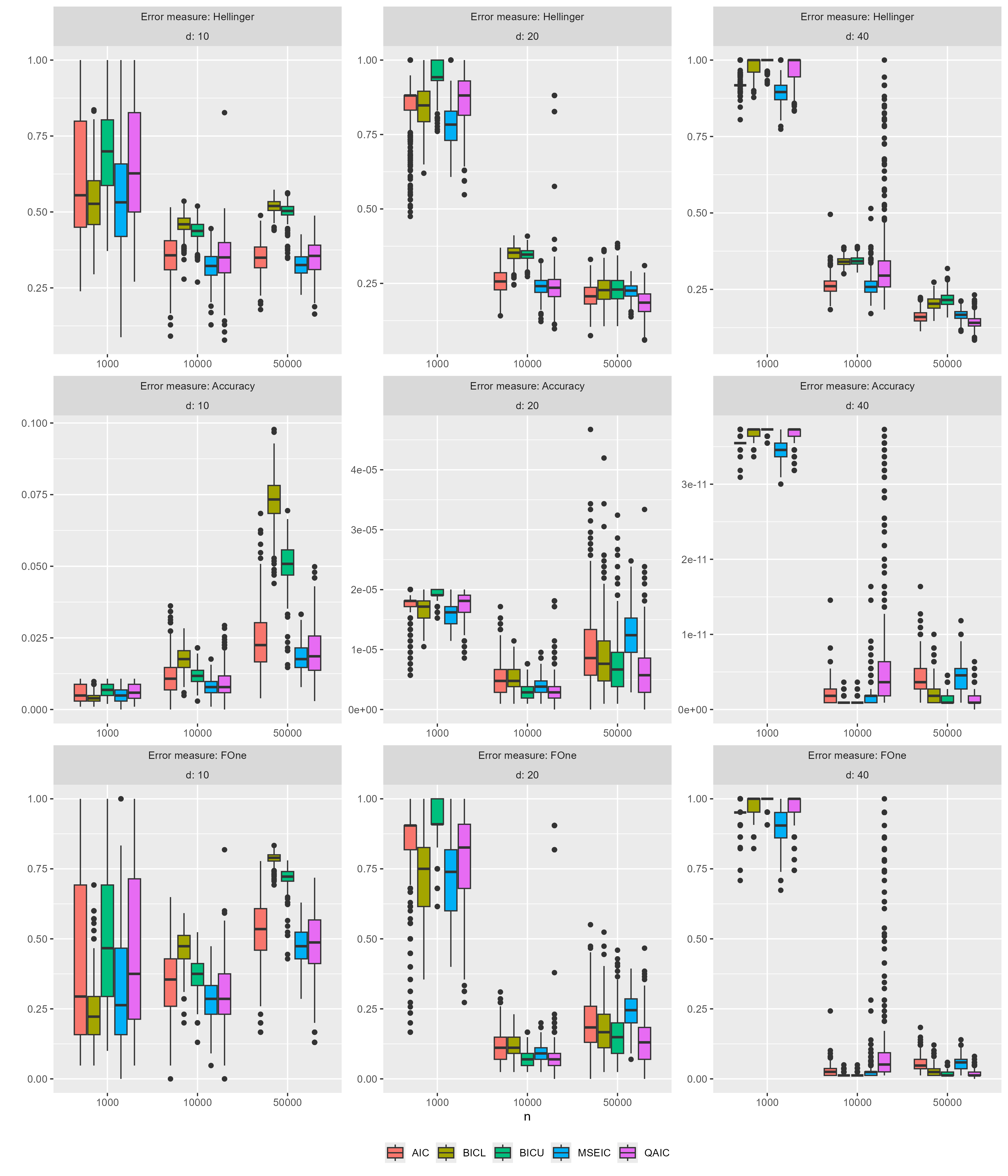

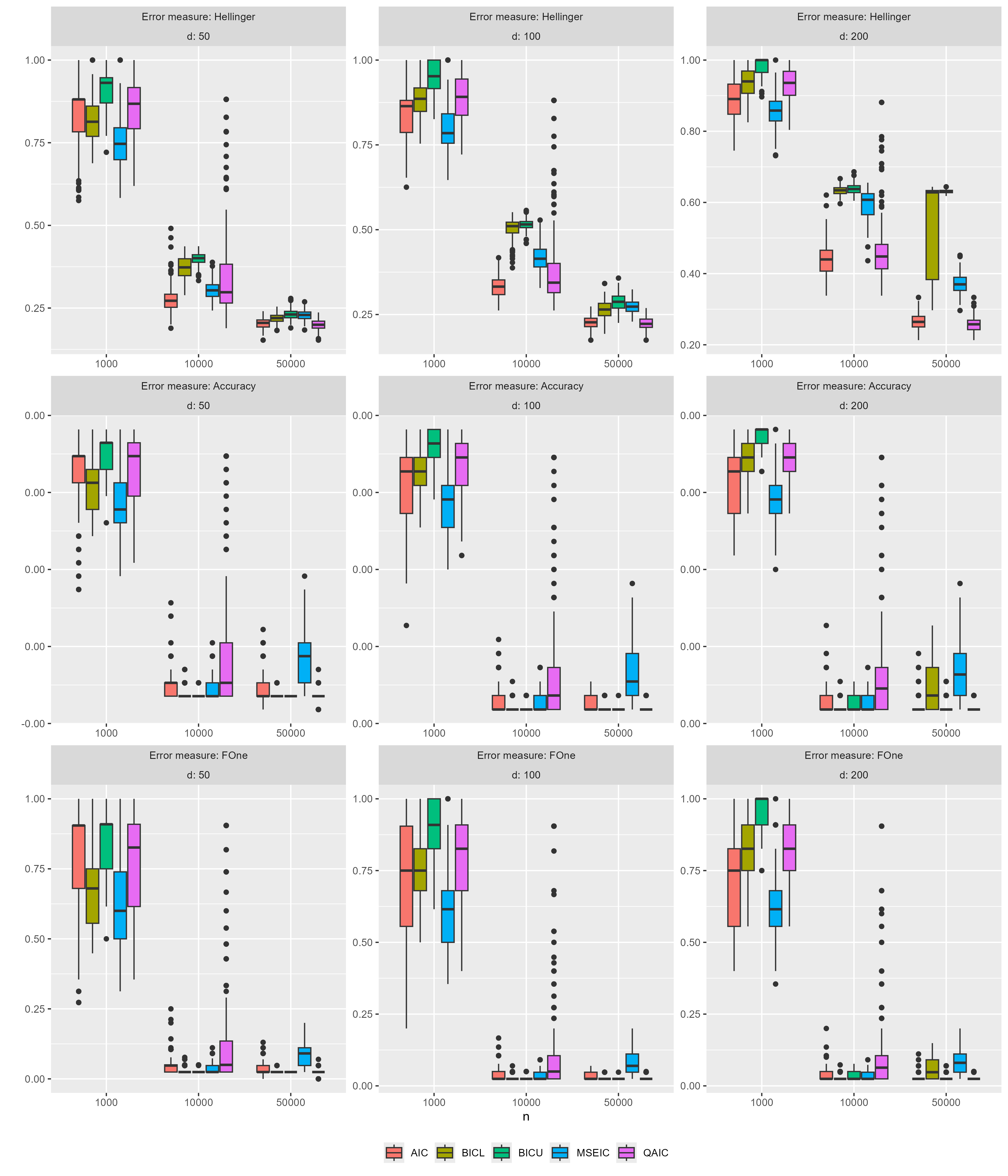

For the comparison, we run simulations with 500 repetitions and sample sizes , respectively and calculate the different error measures.

The results are presented in Figure 1, where we can see that the error measures behave similarly. For the Hellinger distance, we have an increase in the performance of all information criteria as grows, except for where the Hellinger distance of the and slightly increases from to . For the Accuracy Error increases if increases across all information criteria. However, for and the Accuracy and the Error appear to be the lowest for data of size over all information criteria except for .

7.3 Max-mixture model

Next, we use the max-mixture model of tawn which exhibits asymptotic dependence. Here the spectral measure is not discrete and we need to estimate the support of via a Monte-Carlo simulation, where we use the implementation of meyer_muscle23.

For suppose is a -dimensional random vector with Fréchet(1) distributed margins and the following dependence structure. First, have a bivariate Gaussian copula with correlation parameter . On the other hand, and have a three-dimensional and five-dimensional extreme value logistic copula, respectively, with dependence parameter . Then the regular varying vector of index is defined as

Since the Gaussian copula exhibits pairwise asymptotic independence, the random vector puts mass on the cones and by the choice of the scaling factors, each cone has the same probability.

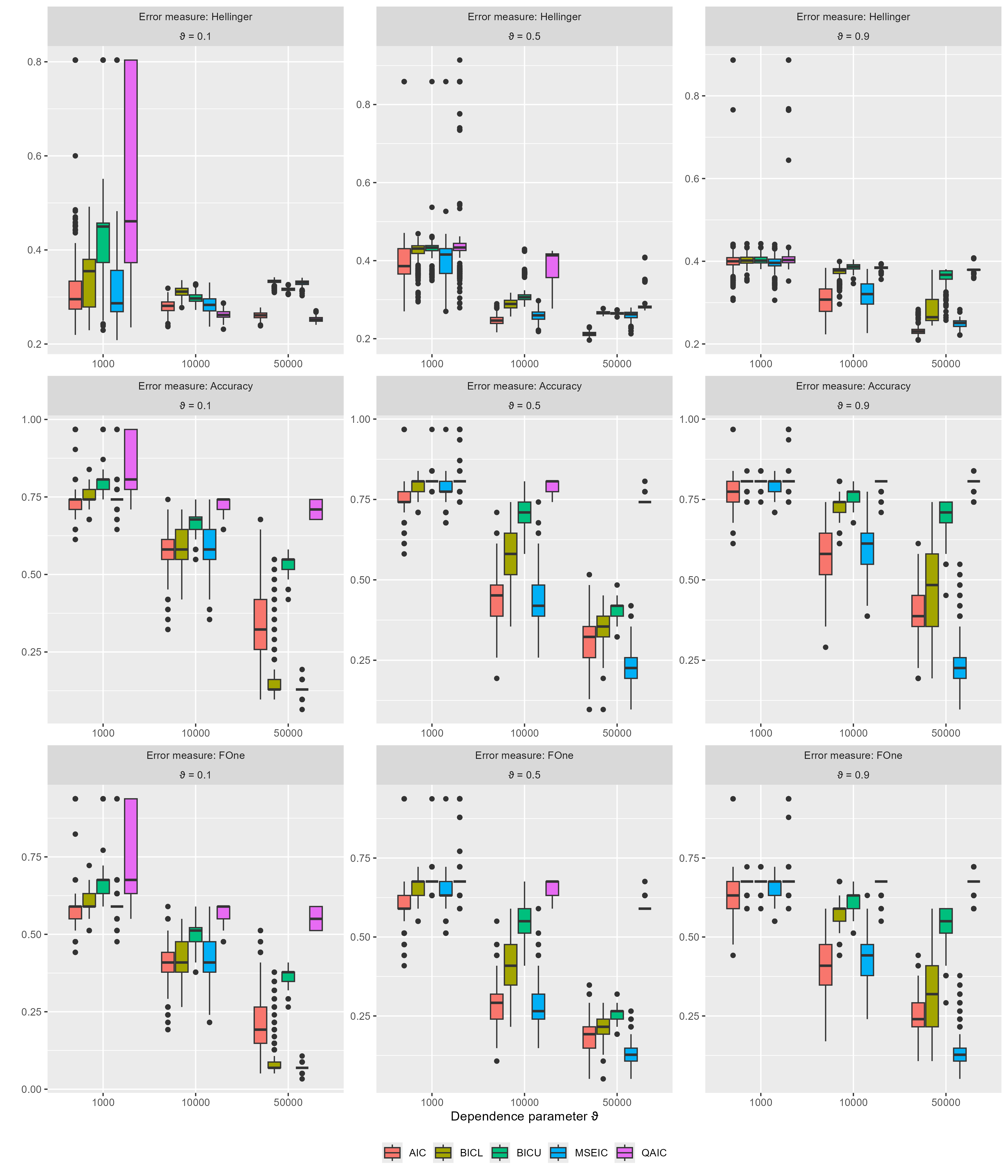

The simulation results of repetitions and sample sizes are given in Figure 2.

The figure shows similar patterns of all information criteria and in particular, that the overall performance of the information criteria decreases when the dependence parameter increases, except for the when . Thus, an increase in dependency hurts the quality of the estimation. In this example, a higher sample size results in an improvement of the accuracy and the Error, particularly for and which have for and the lowest Accuracy Error and Error over all information criteria. In general, the behavior of the Error is similar to the Accuracy Error in all situations. One noteworthy aspect is that we do not know the true distribution of , we estimated it via a Monte Carlo simulation. As a result, there occurred a few directions in with very small probability mass, which can influence the Error measures.

8 Application to real-world data

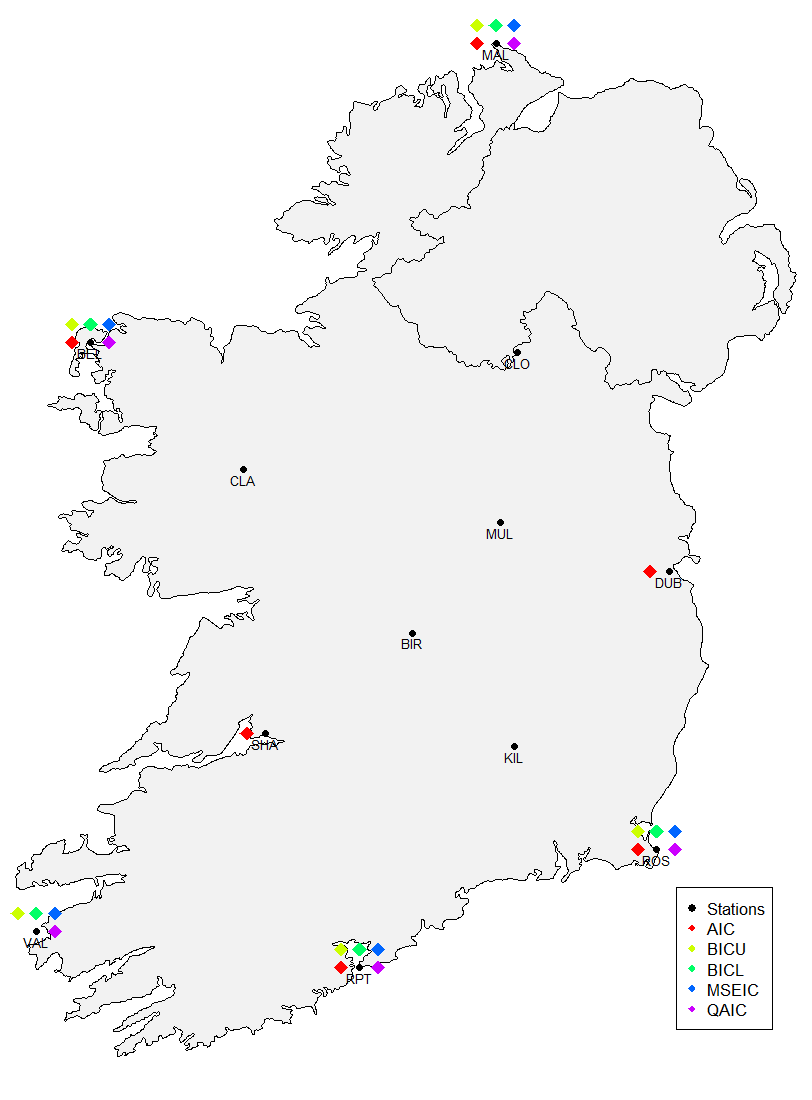

In this section, we examine the dependence structure of extreme wind speeds using the same example as meyer_muscle23. For this purpose, the daily average wind speed at synoptic meteorological stations in the Republic of Ireland from 1961 until 1978 with observations are considered. The data was subject to HR89 and taken from StatLibData. To what extent dependencies exist, that are not due to the geographical proximity, will be analyzed in the following. The locations of the stations are shown in Figure 4 and consist of: Belmullet (BEL), Birr (BIR), Claremorris (CLA), Clones (CLO), Dublin (DUB), Kilkenny (KIL), Malin Head (MAL), Mullingar (MUL), Roche’s Pt. (RPT), Rosslare (ROS), Shannon (SHA) and Valentia (VAL). For the preprocessing, we use the same Hill estimator as meyer_muscle23. We considered values of between and .

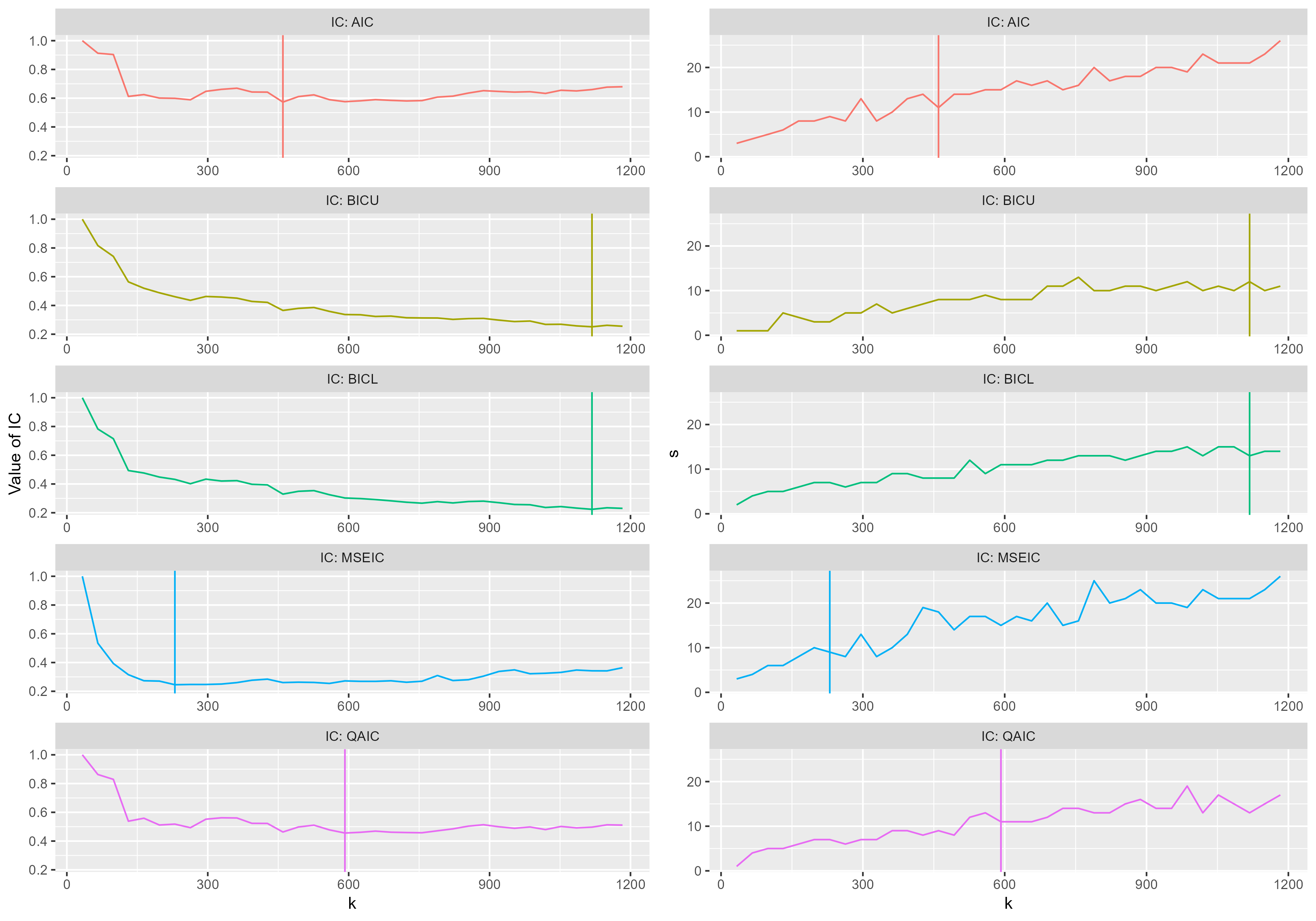

The values of the estimators for , and are presented in Table 1.

| IC | |||

|---|---|---|---|

| 460 | 0.07 | 11 | |

| 1118 | 0.17 | 12 | |

| 1118 | 0.17 | 13 | |

| 230 | 0.03 | 9 | |

| 592 | 0.09 | 11 |

The number of extreme observations varies between and , which corresponds to to of the data. However, the information criteria reported between and number of extreme directions, which is not a large range compared to the choice of . On the left-hand side of Figure 3, the values of the information criteria are plotted against the threshold , while on the right-hand side, the number of estimated directions is mapped as well against . The vertical lines indicate the minimum of the information criteria. It appears that for the number of extremal directions, there is a more distinct plateau around the optimal value for and compared to and .

A graphic of the Republic of Ireland is given in Figure 4, where the black dots highlight the different locations of the stations. Colored diamonds close to a station are markers for estimated extreme wind speeds at that station based on an information criterion. All information criteria only identify stations on the coast as extreme, all inland stations have non-extreme wind speeds. missed one station on the coast, which is Valentia located more than km away from the other stations. and recovered the same maximal clusters and missed the coastal stations Shannon and Dublin. The first station, Shannon, is connected to the ocean but nearly kilometers away from the open sea. The second station, Dublin, is oriented towards the Irish Sea, rather than the Atlantic Ocean. All information criteria identified Belmullet, Mullingar, Rosslare and Roche’s Pt., and four out of five information criteria also recognized Valentia.

9 Conclusion

In this paper, we developed three different information criteria for both the number of extreme directions as well as for the choice of the optimal threshold . Where the BIC is based on a Bayesian approach for a multinomial model in analogy to the of meyer_muscle23, the uses the ideas of an Akaike information criteria but it is based on a Gaussian likelihood function in comparison to the AIC. In contrast, for no likelihood assumption is necessary, it uses the MSE. The advantage of , and is that they are weakly consistent information criteria for the extreme direction , where AIC and tend to overestimate for large sample sizes, although we do not see this phenomenon in the simulations. In particular, performs extraordinarily well in all simulations but all information criteria performed quite well, none is particularly superior in all situations. Finally, the information criteria were successfully applied to a real-world data set, where , , and detected the same extreme clusters.

References

- Avella-Medina, Davis and Samorodnitsky [2022] {barticle}[author] \bauthor\bsnmAvella-Medina, \bfnmMarco\binitsM., \bauthor\bsnmDavis, \bfnmRichard A.\binitsR. A. and \bauthor\bsnmSamorodnitsky, \bfnmGennady\binitsG. (\byear2022). \btitleKernel PCA for multivariate extremes. \bjournalarXiv: 2211.13172. \endbibitem

- Avella Medina, Davis and Samorodnitsky [2024] {barticle}[author] \bauthor\bsnmAvella Medina, \bfnmMarco\binitsM., \bauthor\bsnmDavis, \bfnmRichard A.\binitsR. A. and \bauthor\bsnmSamorodnitsky, \bfnmGennady\binitsG. (\byear2024). \btitleSpectral learning of multivariate extremes. \bjournalJ. Mach. Learn. Res. \bvolume25. \endbibitem

- Bernard et al. [2013] {barticle}[author] \bauthor\bsnmBernard, \bfnmElsa\binitsE., \bauthor\bsnmNaveau, \bfnmPhilippe\binitsP., \bauthor\bsnmVrac, \bfnmMathieu\binitsM. and \bauthor\bsnmMestre, \bfnmOlivier\binitsO. (\byear2013). \btitleClustering of Maxima: Spatial Dependencies among Heavy Rainfall in France. \bjournalJournal of Climate \bvolume26 \bpages7929-7937. \endbibitem

- Burnham and Anderson [1998] {bbook}[author] \bauthor\bsnmBurnham, \bfnmKenneth P.\binitsK. P. and \bauthor\bsnmAnderson, \bfnmDavid Raymond\binitsD. R. (\byear1998). \btitleModel selection and inference: a practical information theoretic approach. \bpublisherSpringer, \baddressNew York. \endbibitem

- Cavanaugh and Neath [1999] {barticle}[author] \bauthor\bsnmCavanaugh, \bfnmJoseph E.\binitsJ. E. and \bauthor\bsnmNeath, \bfnmAndrew A.\binitsA. A. (\byear1999). \btitleGeneralizing the derivation of the Schwarz information criterion. \bjournalComm. Statist. Theory Methods \bvolume28 \bpages49–66. \endbibitem

- Chautru [2015] {barticle}[author] \bauthor\bsnmChautru, \bfnmEmilie\binitsE. (\byear2015). \btitleDimension reduction in multivariate extreme value analysis. \bjournalElectron. J. Stat. \bvolume9 \bpages383–418. \endbibitem

- Claeskens [2016] {barticle}[author] \bauthor\bsnmClaeskens, \bfnmGerda\binitsG. (\byear2016). \btitleStatistical Model Choice. \bjournalAnnu. Rev. Stat. Appl. \bvolume3 \bpages233-256. \endbibitem

- Clémençon, Huet and Sabourin [2024] {barticle}[author] \bauthor\bsnmClémençon, \bfnmStephan\binitsS., \bauthor\bsnmHuet, \bfnmNathan\binitsN. and \bauthor\bsnmSabourin, \bfnmAnne\binitsA. (\byear2024). \btitleRegular variation in Hilbert spaces and principal component analysis for functional extremes. \bjournalStochastic Process. Appl. \bvolume174 \bpagesPaper No. 104375, 22. \endbibitem

- Cooley and Thibaud [2019] {barticle}[author] \bauthor\bsnmCooley, \bfnmD.\binitsD. and \bauthor\bsnmThibaud, \bfnmE.\binitsE. (\byear2019). \btitleDecompositions of dependence for high-dimensional extremes. \bjournalBiometrika \bvolume106 \bpages587–604. \endbibitem

- Cover [2006] {bbook}[author] \bauthor\bsnmCover, \bfnmThomas M.\binitsT. M. (\byear2006). \btitleElements of information theory. \bpublisherWiley-Interscience. \endbibitem

- Drees and Sabourin [2021] {barticle}[author] \bauthor\bsnmDrees, \bfnmHolger\binitsH. and \bauthor\bsnmSabourin, \bfnmAnne\binitsA. (\byear2021). \btitlePrincipal component analysis for multivariate extremes. \bjournalElectron. J. Stat. \bvolume15 \bpages908–943. \endbibitem

- Duchi et al. [2008] {barticle}[author] \bauthor\bsnmDuchi, \bfnmJohn\binitsJ., \bauthor\bsnmShalev-Shwartz, \bfnmShai\binitsS., \bauthor\bsnmSinger, \bfnmYoram\binitsY. and \bauthor\bsnmChandra, \bfnmTushar\binitsT. (\byear2008). \btitleEfficient projections onto the ball for learning in high dimensions. \bjournalProceedings of the 25th International Conference on Machine Learning \bpages272-279. \endbibitem

- Engelke and Hitz [2020] {barticle}[author] \bauthor\bsnmEngelke, \bfnmSebastian\binitsS. and \bauthor\bsnmHitz, \bfnmAdrien S.\binitsA. S. (\byear2020). \btitleGraphical models for extremes. \bjournalJ. R. Stat. Soc. Ser. B. Stat. Methodol. \bvolume82 \bpages871–932. \bnoteWith discussions. \endbibitem

- Engelke and Ivanovs [2021] {barticle}[author] \bauthor\bsnmEngelke, \bfnmSebastian\binitsS. and \bauthor\bsnmIvanovs, \bfnmJevgenijs\binitsJ. (\byear2021). \btitleSparse structures for multivariate extremes. \bjournalAnnu. Rev. Stat. Appl. \bvolume8 \bpages241–270. \endbibitem

- Engelke and Volgushev [2022] {barticle}[author] \bauthor\bsnmEngelke, \bfnmSebastian\binitsS. and \bauthor\bsnmVolgushev, \bfnmStanislav\binitsS. (\byear2022). \btitleStructure learning for extremal tree models. \bjournalJ. R. Stat. Soc. Ser. B. Stat. Methodol. \bvolume84 \bpages2055–2087. \endbibitem

- Engelke et al. [2024] {barticle}[author] \bauthor\bsnmEngelke, \bfnmSebastian\binitsS., \bauthor\bsnmHentschel, \bfnmManuel\binitsM., \bauthor\bsnmLalancette, \bfnmMichaël\binitsM. and \bauthor\bsnmRöttger, \bfnmFrank\binitsF. (\byear2024). \btitleGraphical models for multivariate extremes. \bjournalhttps://arxiv.org/abs/2402.02187. \endbibitem

- Falk [2019] {bbook}[author] \bauthor\bsnmFalk, \bfnmMichael\binitsM. (\byear2019). \btitleMultivariate extreme value theory and D-norms. \bseriesSpringer Series in Operations Research and Financial Engineering. \bpublisherSpringer, Cham. \endbibitem

- Fomichov and Ivanovs [2023] {barticle}[author] \bauthor\bsnmFomichov, \bfnmV.\binitsV. and \bauthor\bsnmIvanovs, \bfnmJ.\binitsJ. (\byear2023). \btitleSpherical clustering in detection of groups of concomitant extremes. \bjournalBiometrika \bvolume110 \bpages135–153. \endbibitem

- Gissibl and Klüppelberg [2018] {barticle}[author] \bauthor\bsnmGissibl, \bfnmNadine\binitsN. and \bauthor\bsnmKlüppelberg, \bfnmClaudia\binitsC. (\byear2018). \btitleMax-linear models on directed acyclic graphs. \bjournalBernoulli \bvolume24 \bpages2693–2720. \endbibitem

- Gissibl, Klüppelberg and Lauritzen [2021] {barticle}[author] \bauthor\bsnmGissibl, \bfnmNadine\binitsN., \bauthor\bsnmKlüppelberg, \bfnmClaudia\binitsC. and \bauthor\bsnmLauritzen, \bfnmSteffen\binitsS. (\byear2021). \btitleIdentifiability and estimation of recursive max-linear models. \bjournalScand. J. Stat. \bvolume48 \bpages188–211. \endbibitem

- Goix, Sabourin and Clémençon [2017] {barticle}[author] \bauthor\bsnmGoix, \bfnmNicolas\binitsN., \bauthor\bsnmSabourin, \bfnmAnne\binitsA. and \bauthor\bsnmClémençon, \bfnmStephan\binitsS. (\byear2017). \btitleSparse representation of multivariate extremes with applications to anomaly detection. \bjournalJ. Multivariate Anal. \bvolume161 \bpages12–31. \endbibitem

- Haslett and Raftery [1989] {barticle}[author] \bauthor\bsnmHaslett, \bfnmJohn\binitsJ. and \bauthor\bsnmRaftery, \bfnmAdrian E.\binitsA. E. (\byear1989). \btitleSpace-Time Modelling with Long-Memory Dependence: Assessing Ireland’s Wind Power Resource. \bjournalJ. R. Stat. Soc. Ser. C. Appl. Stat. \bvolume38 \bpages1–50. \endbibitem

- Jalalzai and Leluc [2021] {binproceedings}[author] \bauthor\bsnmJalalzai, \bfnmHamid\binitsH. and \bauthor\bsnmLeluc, \bfnmRémi\binitsR. (\byear2021). \btitleFeature Clustering for Support Identification in Extreme Regions. In \bbooktitleProceedings of the 38th International Conference on Machine Learning (\beditor\bfnmMarina\binitsM. \bsnmMeila and \beditor\bfnmTong\binitsT. \bsnmZhang, eds.). \bseriesProceedings of Machine Learning Research \bvolume139 \bpages4733–4743. \bpublisherPMLR. \endbibitem

- Janßen and Wan [2020] {barticle}[author] \bauthor\bsnmJanßen, \bfnmAnja\binitsA. and \bauthor\bsnmWan, \bfnmPhyllis\binitsP. (\byear2020). \btitle-means clustering of extremes. \bjournalElectron. J. Stat. \bvolume14 \bpages1211-1233. \endbibitem

- Meyer and Wintenberger [2021] {barticle}[author] \bauthor\bsnmMeyer, \bfnmNicolas\binitsN. and \bauthor\bsnmWintenberger, \bfnmOlivier\binitsO. (\byear2021). \btitleSparse regular variation. \bjournalAdv. in Appl. Probab. \bvolume53 \bpages1115–1148. \endbibitem

- Meyer and Wintenberger [2023] {barticle}[author] \bauthor\bsnmMeyer, \bfnmNicolas\binitsN. and \bauthor\bsnmWintenberger, \bfnmOlivier\binitsO. (\byear2023). \btitleMultivariate Sparse Clustering for Extremes. \bjournalJ. Amer. Statist. Assoc. \bpages1-12. \endbibitem

- Ouimet [2021] {barticle}[author] \bauthor\bsnmOuimet, \bfnmFrédéric\binitsF. (\byear2021). \btitleA precise local limit theorem for the multinomial distribution and some applications. \bjournalJ. Statist. Plann. Inference \bvolume215 \bpages218-233. \endbibitem

- Powers [2008] {barticle}[author] \bauthor\bsnmPowers, \bfnmDavid\binitsD. (\byear2008). \btitleEvaluation: From Precision, Recall and F-Factor to ROC, Informedness, Markedness and Correlation. \bjournalMach. Learn. Technol. \bvolume2. \endbibitem

- Resnick [1987] {bbook}[author] \bauthor\bsnmResnick, \bfnmS. I.\binitsS. I. (\byear1987). \btitleExtreme Values, Regular Variation, and Point Processes. \bpublisherSpringer. \endbibitem

- Resnick [2007] {bbook}[author] \bauthor\bsnmResnick, \bfnmS. I.\binitsS. I. (\byear2007). \btitleHeavy-Tail Phenomena: Probabilistic and Statistical Modeling. \bpublisherSpringer. \endbibitem

- Rohrbeck and Cooley [2023] {barticle}[author] \bauthor\bsnmRohrbeck, \bfnmChristian\binitsC. and \bauthor\bsnmCooley, \bfnmDaniel\binitsD. (\byear2023). \btitleSimulating flood event sets using extremal principal components. \bjournalAnn. Appl. Stat. \bvolume17 \bpages1333–1352. \endbibitem

- Schwarz [1978] {barticle}[author] \bauthor\bsnmSchwarz, \bfnmGideon\binitsG. (\byear1978). \btitleEstimating the dimension of a model. \bjournalAnn. Statist. \bvolume6 \bpages461–464. \endbibitem

- Simpson, Wadsworth and Tawn [2020] {barticle}[author] \bauthor\bsnmSimpson, \bfnmE. S.\binitsE. S., \bauthor\bsnmWadsworth, \bfnmJ. L.\binitsJ. L. and \bauthor\bsnmTawn, \bfnmJ. A.\binitsJ. A. (\byear2020). \btitleDetermining the dependence structure of multivariate extremes. \bjournalBiometrika \bvolume107 \bpages513–532. \endbibitem

- StatLib---Datasets-Archive [2023] {bmisc}[author] \bauthor\bsnmStatLib---Datasets-Archive (\byear2023). \btitleWind. \bhowpublishedhttp://lib.stat.cmu.edu/datasets/wind.data, accessed October 26, 2023. \endbibitem

Appendix A Proofs

A.1 Proofs of Section 3

Proof of Theorem 3.1.

Step 1: Suppose . By the definition of the and the log-likelihood function in section 2.4.1 it follows that

| (A.1) |

where we used that . Inserting the alternative representation

where

gives that

| (A.2) |

For the asymptotic behavior we apply Assumption (A3) which results in

| (A.3) |

and thus,

This and the Taylor expansion of the logarithm

we insert in A.2 such that

Since (Lemma 2.7(a)) we receive

Due to A.3 and the continuous mapping theorem we finally obtain as ,

| (A.4) |

Obviously,

Step 2: Suppose . We obtain analog to A.1 that

| (A.5) |

A direct consequence of for (Lemma 2.7(c)) and is that

Furthermore, Lemma 2.7(b) yields for and thus, as ,

| (A.6) |

while we used for . Next, we apply the log sum inequality (Log_Sum_ineq, Theorem 2.7.1) to the limit of A.6 and receive

| (A.7) |

since . Dividing A.5 by and using A.6 and A.7 gives

and thus, the assertion follows. ∎

A.2 Proofs of Section 4

A.2.1 Proof of Theorem 4.2

In the next two lemmata, we derive auxiliary results used for the derivation of an upper bound of the posterior probability . First, in Lemma A.1, we give a Taylor approximation of the log-likelihood function of Model , and second, in Lemma A.2, we present boundaries for the eigenvalues of the Hessian of the log-likelihood function; the proofs of these auxiliary results are included in Section B.1 of the Supplementary Material. Finally, for the proof of the upper bound of the log-posterior distribution in Theorem 4.2 we combine these two results.

Lemma A.1.

Let the assumptions of Theorem 4.2 hold. Define the ball

with radius for around . Then the following statement holds

Lemma A.2.

Let the assumptions of Theorem 4.2 hold. Define and . For we have on the one hand,

and on the other hand,

Proof of Theorem 4.2..

The integrand is a -dimensional Gaussian density with expectation vector and covariance matrix . Furthermore, due to the definition of , Assumption (C3) and Lemma 2.7, the asymptotic behavior

| (A.9) |

holds in probability. Let . Since the Markov inequality yields

as almost surely, where we used in the last step A.9. Thus,

| (A.10) |

Inserting A.10 into A.8 gives then

Since for , we receive the upper bound

and finally,

which is the statement. ∎

A.2.2 Proof of Theorem 4.5

Proof of Theorem 4.5.

(a) Note that

We consider now the different cases and separately.

Step 1: Suppose . We receive with A.4 that

Dividing the last equation by results in

where we used .

Step 2: Suppose . Here we have as in the proof of Theorem 3.1 and due to that

and thus, the assertion follows.

(b) Again, note that

By a calculation analog to part (a), the is also consistent since as . ∎

A.2.3 Proof of Theorem 4.7

First, we derive some auxiliary results before we prove Theorem 4.7. Therefore, note that due (2.6) (cf. Equation (1.23) in the Supplementary Material of meyer_muscle23) and , the likelihood function of Model can be written as

| (A.11) |

for , where

| (A.12) |

is the likelihood function of the binomial model. Next, we define the following expectations with respect to the Lebesgue measure . Let

| (A.15) |

Then taking the expectation and logarithm in A.11 results under Assumption (D1) in

| (A.16) |

In the following two auxiliary lemmata, we determine upper bounds for the expectation of both summands.

Proposition A.3.

Proposition A.4.

Proof of Theorem 4.7..

For the ease of notation we define as zero if . Inserting the bounds derived in Proposition A.3 with constant and Proposition A.4 with constant into A.16 gives for sufficiently large that

| (A.17) |

Next, we simplify . Therefore, we use the following calculation. Let be a positive random variable with finite positive variance. For and we the inequality holds, which is equivalent to . Then we have

and in particular for we receive

Since and the previous inequality gives

| (A.18) |

for a constant independent of and . Furthermore, we use the inequality

| (A.19) |

to derive a bound for . Hence, using the upper bound A.19, A.18 and applying Jensen inequality we receive that

for a constant independent of and . Additionally to the last inequality, we obtain by A.19 and A.18 (for instead of and instead of , respectively) that

| (A.20) |

for some constant independent of and holds, where we used that the bracket in the second last equation is negative.

A.3 Proofs of Section 5

A.3.1 Proof of Proposition 5.3

Before we are able to present the proof of Proposition 5.3 we require some auxiliary lemmata whose proofs are moved to Appendix C of the Supplementary Material. In the following, we work with the -dimensional multivariate normal distribution which has a negative log-likelihood function

Lemma A.5.

Lemma A.6.

Suppose the assumptions of Proposition 5.3 hold and is defined analog to in (5.3).

-

(a)

Then as ,

-

(b)

Suppose satisfies

Then as ,

Proof of Proposition 5.3..

Using a Taylor expansion of around yields the existence of a random vector with

such that

Applying Lemma A.6 (b) gives

Inserting the definition of and , , yield

Next, we move some terms on the right-hand side and use (cf. Lemma 2.7 (c) and the assumption ) and as defined in Lemma A.5 , which result in

by Lemma A.5, where . Since

the assertion follows.

∎

A.3.2 Proof of Theorem 5.6

Proof of Theorem 5.6.

Step 1: Suppose .

We have for and due to Lemma 2.7(b,c) we have as ,

and similarly as well as . Thus,

and Therefore, we have as ,

Step 2: Suppose . In this case, we have by Lemma 2.7(b,c) that

and similarly as well as . Hence, with the continuous mapping theorem we receive for , and as . Thus, as ,

which gives the statement. ∎

A.4 Proofs of Section 6

A.4.1 Proof of Theorem 6.1

The proof of Theorem 6.1 is similar to the proof of Proposition 5.3. In the first step, we start to calculate the Jacobian vector of for , which is

and the Hessian matrix is

Lemma A.7.

Suppose Assumption A holds, and is defined analogously to in (5.3). Then as ,

Lemma A.8.

Suppose Assumption A holds, and is defined analogously to in (5.3).

-

(a)

Then as ,

-

(b)

Suppose satisfies

Then as ,

A.4.2 Proof of Theorem 6.3

Proof of Theorem 6.3.

Step 1: Suppose .

An application of Lemma 2.7(b,c) gives on the one hand,

where we already applied that for . Moreover,

Hence,

| (A.21) |

On the other hand, define

By Assumption (A3) we have Furthermore, since for by Lemma 2.7(c), it follows that

| (A.22) |

Combining A.21 and A.22 yields

Step 2: Suppose . An application of (A.22) and Lemma 2.7(c) yield

| (A.23) |

Since the analog holds when is replaced by . Using defined as above, we have the representation Thus, when inserting the definition of we get with A.23 that

Similar to the proof of Theorem 3.1, there exists a positive probability that the right-hand side is positive. Hence, the assertion follows. ∎

A.4.3 Proof of Theorem 6.4

Before we are able to present the proof of Theorem 6.4 we require some auxiliary lemmata whose proofs are moved to Appendix D in the Supplementary Material.

Lemma A.10.

For the equality

holds.

Proof of Theorem 6.4.

For and we have as a consequence of Lemmas A.9 and A.10 that

Therefore, it follows that

Due to the asymptotic behavior as ,

where we used the additional assumption as , we can conclude the statement. ∎

SUPPLEMENTARY MATERIAL FOR

INFORMATION CRITERIA FOR THE NUMBER OF

DIRECTIONS OF EXTREMES IN HIGH-DIMENSIONAL DATA

BY LUCAS BUTSCH AND VICKY FASEN-HARTMANN

Supplementary Material B Auxiliary results for the Bayesian information criterion

In this section, we present supplementary results for Section 4.

B.1 Proof of Lemma A.1 and Lemma A.2

First, we provide the proofs of the auxiliary results of Section A.2.1 in this subsection.

Lemma A.1.

Let the assumptions of Theorem 4.2 hold. Define the ball

with radius for around . Then the following statement holds

Proof.

First, we apply a multivariate Taylor expansion to the log-likelihood function around the MLE at analog to Lemma 2 of meyer_muscle23 (based on a generalization of Cauchy’s Mean Value Theorem (see Cauchy_Mean_Value)) which gives the existence of a constant such that

Thus, we receive for the left hand side in (a) that

| (B.1) |

Therefore, to prove the statement, we show that the right side is . Inserting the derivatives of the log-likelihood function

| (B.5) | ||||

and applying the triangle inequality yields

In the following we only show that is uniformly ; the calculation for is similar but with a faster rate, since and . Therefore, an application of the mean value theorem to the function yields

| (B.6) |

Since and we obtain

Finally, and (due to Assumption (C3)) which results in the uniform convergence of and the statement follows. ∎

Next, we derive boundaries for the eigenvalues of the second-order derivative of the log-likelihood function.

Lemma A.2.

Let the assumptions of Theorem 4.2 hold. Define and . For we have on the one hand,

and on the other hand,

Proof.

Let . Inserting the MLE in the second order derivative in B.5 yields

The eigenvalues of and are

and

respectively. By with we denote the ordered eigenvalues of Then Weyl’s inequality (cf. weyl_ineq, p. 239, Theorem 4.3.1) and Assumption (A2) yield

| (B.7) |

An application of A.2.5 in multivariate_statistics and inequality (B.7) give then with

the statement. ∎

B.2 Proof of Proposition A.3

Proof.

First, we find an upper bound for the first term. Therefore, note that for the equality

| holds. An application of A.18 in the first step (which holds as well in analog form for ) and Assumption (B1) in the second step give then | ||||

| where we used in the calculations as well that due Assumption (B3). Finally, we apply again A.18 to receive | ||||

| (B.8) | ||||

Similarly, we obtain as well

| (B.9) |

A consequence of the log-likelihood function (cf. (2.4.1)), (B.8) and (B.9) is then

| (B.10) |

By the last equality on page 28 in meyer_muscle23 and we receive that

| (B.11) | ||||

and

| (B.12) |

for some constants independent of and .

B.3 Proof of Proposition A.4

The target of this section is to prove Proposition A.4.

Lemma B.1.

The proof of the lemma is analog to the proof of Theorem 4.2 by taking the uniform distribution on as the prior density and is therefore omitted.

Proof.

Without loss of generality, we assume in the following that the constant , which is independent of and , is chosen sufficiently large such that the following inequalities hold.

Under Assumption (B3) we allowed use the second equation on page 31 in the proof of Lemma 6 in meyer_muscle23

A combination with the asymptotic expansion in the last equation on page 31 in the proof of Lemma 6 in meyer_muscle23

gives then

By Assumption (B3) follows the existence of a positive constant such that

Since and for we have

as , it follows the existence of a constant such that

A combination of Lemma B.1 and the equation above gives the existence of a constant such that

| (B.13) |

Inserting

into B.13 yields

| (B.14) |

We have by Assumption (B3) that for some and thus,

| (B.15) |

for some .

Supplementary Material C Auxiliary results for the quasi-Akaike information criterion

In this section, we present supplementary results for Section 5.

C.1 Proof of Lemma A.5

Proof.

From Assumption (A4) and the continuous mapping theorem we receive that

Finally, it follows from the independence of and as well as , by Assumption A, that as ,

∎

C.2 Proof of Lemma A.6

Lemma A.6.

Suppose the assumptions of Proposition 5.3 hold and is defined analog to in (5.3).

-

(a)

Then as ,

-

(b)

Suppose satisfies

Then as ,

Proof.

-

(a)

The derivatives of the log-likelihood function are

and

Hence,

First, note that due to Lemma A.5 and . Therefore, it remains to investigate . We define the function as with Jacobian vector

Then, and From Assumptions (A4) we already get the asymptotic behavior

Then an application of the delta-method yields

or equivalently

On the other hand, Lemma A.5 implies that

Finally, this results in

- (b)

∎

Supplementary Material D Auxiliary results for the mean squared error information criterion

In this section, we present supplementary results for Section 6.

D.1 Proof of Lemma A.9

D.2 Proof of Lemma A.10

Lemma A.10.

For the equality

holds.

Proof.

A straightforward calculation gives with

the statement. ∎

Supplementary Material E Additional simulation study

E.1 Asymptotic dependent model

In this section, we present an additional simulation study for a model with asymptotic dependence which can also be found in meyer_tail. Consequently not only directions with are relevant. Let be an valued random vector and , such that

The parameters specify the number of one, two, and three-dimensional directions. In the following we denote by the exponential distribution with parameter . The marginal distributions of are defined by

The random vector in Definition 2.1 puts mass on the sets

In total there are directions with probability mass and the goal is again to identify these directions. For the comparison, we run simulations with 500 repetitions and sample sizes of , respectively, and such that we have directions of extremes.

In Figure 5 we can see that the error measures behave similarly. For all we have an increase in performance across all information criteria as for most of the information criteria. Also, tends to overfit, when the sample size is and includes more directions than necessary. On the other hand, , and do not exhibit this tendency. Further, performs in comparison to the other information criteria better when the sample size is small. When considering only the Hellinger distance, then the and are superior for , but not for the or the accuracy. The influence of an increasing dimension is modest, as the number of relevant directions is fixed.

References

- Fujikoshi, Ulyanov and Shimizu [2010] {bbook}[author] \bauthor\bsnmFujikoshi, \bfnmYasunori\binitsY., \bauthor\bsnmUlyanov, \bfnmVladimir Vladimirovič\binitsV. V. and \bauthor\bsnmShimizu, \bfnmRyoichi\binitsR. (\byear2010). \btitleMultivariate statistics: high-dimensional and large-sample approximations. \bpublisherWiley. \endbibitem

- Hille [1964] {bbook}[author] \bauthor\bsnmHille, \bfnmEinar\binitsE. (\byear1964). \btitleAnalysis 1. \bpublisherBlaisdell Publ. Co. \endbibitem

- Horn and Johnson [2013] {bbook}[author] \bauthor\bsnmHorn, \bfnmRoger A.\binitsR. A. and \bauthor\bsnmJohnson, \bfnmCharles R.\binitsC. R. (\byear2013). \btitleMatrix analysis, \bedition2. ed., 1. publ. ed. \bpublisherCambridge Univ. Press. \endbibitem

- Meyer and Wintenberger [2020] {barticle}[author] \bauthor\bsnmMeyer, \bfnmNicolas\binitsN. and \bauthor\bsnmWintenberger, \bfnmOlivier\binitsO. (\byear2020). \btitleTail inference for high-dimensional data. \bjournalarXiv: 2007.11848v1. \endbibitem

- Meyer and Wintenberger [2023] {barticle}[author] \bauthor\bsnmMeyer, \bfnmNicolas\binitsN. and \bauthor\bsnmWintenberger, \bfnmOlivier\binitsO. (\byear2023). \btitleMultivariate Sparse Clustering for Extremes. \bjournalJ. Amer. Statist. Assoc. \bpages1-12. \endbibitem