A study on two-metric projection methods

1 Abstract

The two-metric projection method is a simple yet elegant algorithm proposed by Bertsekas in 1984 to address bound/box-constrained optimization problems. The algorithm’s low per-iteration cost and potential for using Hessian information makes it a favourable computation method for this problem class. However, its global convergence guarantee is not studied in the nonconvex regime. In our work, we first investigate the global complexity of such a method for finding first-order stationary solution. After properly scaling each step, we equip the algorithm with competitive complexity guarantees. Furthermore, we generalize the two-metric projection method for solving -norm minimization and discuss its properties via theoretical statements and numerical experiments.

2 Introduction

In this work, we revisit the two-metric projection method proposed by Bertsekas [2] to solve the bound-constrained problem:

| (1) |

where is Lipschitz continuously differentiable and is bounded below by on the feasible region. Two-metric projection method is simple and elegant, but its global complexity guarantees are absent in literature. We observe that this traditional method finds an approximate first-order optimal point in iterations, which is suboptimal in literature [3]. By properly scaling the diagonal matrix, we equip the method with a worst-case complexity that matches the lower bound () of using first-order methods to solve this problem class. Moreover, we try to generalize the method and propose a two-metric adaptive projection method for the -norm minimization,

| (2) |

We show that our method is well-defined and decreases the value of the objective function at each iteration for which is not a critical point. For (2), inexact proximal-Newton-type methods, or successive quadratic approximation (SQA) methods [4], are widely used for their superlinear convergence in terms of iterations. A key difference between the two-metric adaptive projection and these methods is the per-iteration cost: in each iteration, SQA needs to find approximate solutions to regularized quadratic programs, while our method at worst needs to solve a linear equation - the Newton system and compute a single cheap adaptive projection step. Preliminary numerical experiments verify the asymptotic superlinear convergence of the two-metric adaptive projection method when employing Hessian.

3 First-order optimal point

We can write first-order optimality conditions for (1), (also known as stationarity conditions) at a point as follows:

| (3) | |||

3.1 Approximate first-order optimal points

Next, we define -approximate first-order optimal points (-1o).

Definition 1

For , is an -1o point of (1), if and

| (4) |

where is a diagonal matrix such that if ; otherwise.

Definition 1 is motivated by the first-order optimal conditions of (1). In fact, if we let = 0, then 0-1o satisfies (3) exactly. The following lemma further justifies Definition 1 and our purpose to find an -1o given small .

Lemma 1

Consider problem (1), suppose that we have a positive scalar sequence with and vector sequence with and such that is -1o according to Definition 1. Then satisfies first-order optimal conditions (3).

Proof

Denote diagonal matrix where coorespond to in Definition 1 with . Our claim that satisfies (3) is a consequence of the following three observations.

-

1.

Feasibility of follows from closedness of .

-

2.

, . By taking limits, we have

-

3.

We claim that if , we must have . Assume the contrary, if , there exist a , for all we have and , then

By taking limits, we have , which is contradicting with .

Overall, satisfies (3).

4 Two-metric projection

The two-metric projection method for solving (1) is as follows:

where denotes Euclidean projection onto the feasible region, is the stepsize, . is a symmetric positive definite matrix in . Define

where , , is a fixed tolerance and is a fixed diagonal positive definite matrix. We suppose that is diagonal w.r.t. , i.e.,

| (5) |

Denote . Let and be the subvector of and w.r.t index set , and be the submatrix of and w.r.t. . is the diagonal matrix which corresponds to , and in Definition 1 with and . Then the algorithm can be formally stated as follows.

Remark 1

We do not need to consider if or not in the Algorithm 1, since if , then

Complexity of Algorithm 1 is revealed in the following theorem.

Theorem 4.1

Consider Algorithm 1. Suppose that , for all and . . Lipschitz constant for is . Then and the following holds: for any , the algorithm will stop within number of iterations and output an -1o that satisfies Definition 1.

Remark 2

We suppress the proof of Theorem 4.1 due to page limit. Note that the best complexity of first-order methods for Lipschitz smooth function in literature is . The reason to cause this gap is the possible small stepsize in the current form of two-metric projection. Motivated by this gap, we design a scaled two-metric projection method to enlarge the stepsize and improve the complexity guarantees.

5 Scaled two-metric projection

In this section, we apply an extended scaled version of the two-metric projection algorithm. The only difference between the scaled version and the traditional version is that we use a diagonal matrix to scale . We update using:

Where is defined as follows:

| (6) |

Define . The Algorithm is formally the same as Algorithm 1 with only different . The following theorem shows an improved complexity guarantee for this algorithm.

Theorem 5.1

Consider Algorithm 2. Suppose that , for all and . . Lipschitz constant for is . Then and the following holds. For any , the algorithm will stop within number of iterations and output an that satisfies Definition 1.

Proof

First we show that . Denote , . Note that and . If such that

| (7) |

we have the following properties:

| (8) |

| (9) |

Therefore,

| (10) | ||||

Since , we have:

| (11) |

| (12) |

| (13) |

Then,

| (14) |

Note that and we have:

| (15) |

Therefore,

| (16) | ||||

Since , we have:

| (17) | |||

which indicates that,

| (18) |

Therefore, if , we have:

From Lipschitz continuity of , we have that for any satisfying ,

| (19) | ||||

If satisfies , then we have:

| (20) |

Let . Due to the definition of , and . Thus . This further indicates that

| (21) |

Next, we consider the iteration complexity of Algorithm 1.

| (22) |

If

| (23) |

Then,

| (24) | ||||

Else,

| (25) |

Then,

| (26) |

Therefore, if hold, from (22)(26)(28) we have:

| (27) | ||||

Suggest that the algorithm will stop within number of iterations, then,

| (28) |

This further indicates that,

| (29) |

6 Generalize the method for -norm regularization problem

We consider the -norm regularization problem:

| (30) |

where is Lipschitz continuously differentiable and is bounded below by . For any local optimal point of -norm regularization problem, we give the following first-order necessary conditions:

Theorem 6.1 (First-order necessary conditions)

If is an local optimal point of -norm regularization problem, then

| (31) |

specifically,

| (32) |

We propose an two-metric adaptive projection algorithm for resolution. We update using:

where and is associated to and defined as below:

| (33) |

| (34) |

where is the stepsize, . is a symmetric positive definite matrix in . Define , , . We suppose that is diagonal w.r.t. , i.e.,

| (35) |

Denote . Let , and be the subvector of , and w.r.t index set , and be the submatrix of and w.r.t. . Then the algorithm can be formally stated as in Algorithm 2.

| (36) |

For Algorithm 2, we have the following three theorems.

Theorem 6.2

if and only if satisfy (32).

Proof

Assume that for all , we have . Then, if , we have:

| (37) |

which indicates that

| (38) |

Note that,

| (39) |

combine the above two equations, we get

| (40) |

For , we have

| (41) |

For , we have

| (42) |

For , we also have

| (43) |

To sum up, we have

| (44) |

Since is positive definite, we must have

| (45) |

which indicate (32). The other side is trivial.

Theorem 6.3

For , small enough, we have

| (46) |

Proof

From Lipschitz continuity of , we have the following inequality:

| (47) |

so that

| (48) |

For , and have the same sign for small enough. So that we have

| (49) | ||||

Note that, for , we have

| (50) |

for , we have

| (51) |

From the above two equations, we get

| (52) |

For all , we also have

| (53) |

so that

| (54) |

Overall, if and small enough such that and have the same sign when .,

| (55) |

Theorem 6.4

The right-hand side of (50) is nonnegative and is positive for all if and only if does not satisfy (32).

Proof

Note that

| (56) |

since is positive definite. Note that

| (57) |

Therefore, both sides are trivial.

In conclusion, the algorithm is well-defined and decreases the value of the objective function at each iteration , in which is not a critical point.

6.1 Numerical experiment

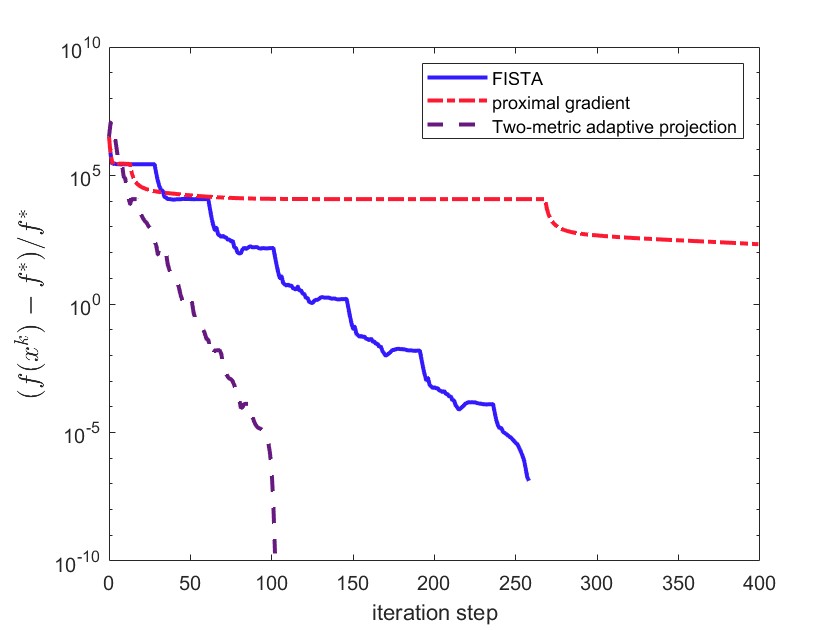

We use Algorithm 2 to solve the LASSO problem: where and each element of follows the normal distribution, and the real solution is a sparse vector with only 10% none zero element, we derive by setting . To accelerate the algorithm’s convergence rate, a continuity strategy can be adopted to gradually reduce the larger regularization parameter from to . Then the algorithm can be formally stated as follows.

Note that, in LASSO is and , we set in algorithm 2, since is positive semi-definite. The result is shown in Figure 1.

7 Conclusion

In this article, we first define an approximate first-order optimal point for the bound-constrained problem. We investigate the iteration complexity of the two-metric projection method proposed by Bertsekas, the algorithm terminates within iterations and finds a point that is approximately first-order optimal to tolerance . By scaling the diagonal matrix, we equip the method with a worst-case complexity theory that matches the best-known theoretical bounds for bound-constrained optimization and even unconstrained optimization. We also try to generalize the two-metric projection algorithm for composite optimization, we propose a framework called two-metric adaptive projection, which is suitable for solving the -norm minimization problem.

In future work, we will consider the convergence properties of our two-metric adaptive projection and propose a general algorithm for composite optimization.

References

- [1] Amir Beck and Marc Teboulle. A fast iterative shrinkage-thresholding algorithm for linear inverse problems. SIAM Journal on Imaging Sciences, 2(1):183–202, 2009.

- [2] Dimitri P Bertsekas. Projected newton methods for optimization problems with simple constraints. SIAM Journal on Control and Optimization, 20(2):221–246, 1982.

- [3] Yair Carmon, John C Duchi, Oliver Hinder, and Aaron Sidford. Lower bounds for finding stationary points i. Mathematical Programming, 184(1-2):71–120, 2020.

- [4] Jorge Nocedal and Stephen J Wright. Numerical optimization. Springer, 1999.

- [5] Neal Parikh, Stephen Boyd, et al. Proximal algorithms. Foundations and trends® in Optimization, 1(3):127–239, 2014.