Bayesian CART models for aggregate \zzzclaim modeling

Abstract

This paper proposes three types of Bayesian CART (or BCART) models for aggregate \zzzclaim amount, namely, frequency-severity models, sequential models and joint models. We propose a general framework for the BCART models applicable to data with multivariate responses, which is particularly useful for the joint BCART models with a bivariate response: the number of claims and aggregate claim amount. To facilitate frequency-severity modeling, we investigate BCART models for the right-skewed and heavy-tailed claim severity data by using various distributions. We discover that the Weibull distribution is superior to gamma and lognormal distributions, due to its ability to capture different tail characteristics in tree models. Additionally, we find that sequential BCART models and joint BCART models, which incorporate dependence between the number of claims and \zzzaverage severity, are beneficial and thus preferable to the frequency-severity BCART models in which independence is assumed. The effectiveness of these models’ performance is illustrated by carefully designed simulations and real insurance data.

Keywords: average severity; dependence; DIC; information sharing; zero-inflated compound Poisson gamma distribution.

1 Introduction

In the classical formula of non-life insurance pricing, the pure premium is determined by multiplying the expected \zzzclaim frequency with the conditional expectation of average severity, assuming independence between the number of claims and claim amounts; see, e.g., [1, 2] and references therein. With the assumed independence, the frequency-severity models treat these two components separately by generalized linear models (GLMs) traditionally, assuming distributions from the exponential family. The frequency study focuses on the occurrences of \zzzclaims, and the severity study — provided that a claim has occurred — investigates the claim amount. In recent years, a growing body of literature emphasizes the importance of understanding the interrelated nature of \zzzclaim occurrences and their associated claim amounts to improve model applicability.

There are two widely discussed strategies to address the issue of dependence. The first one, known as the copula method, is commonly employed to model the dependence structure between the number of \zzzclaims and claim amounts; see, e.g., [3, 4, 5] and references therein. By the nature of the number of \zzzclaims and claim amounts, the dependence modeling requires the development of mixed copula for which some margins are discrete and others are continuous. We refer to [6, 7] for relevant discussions. In parallel, the adoption of Bayesian approaches to copula modeling, as seen in [8], has contributed to refining copula-based modeling techniques. By augmenting the likelihood with latent variables and employing efficient Markov Chain Monte Carlo (MCMC) sampling schemes, copula models with discrete margins can be estimated using the resulting augmented posterior; see, e.g., [9]. However, the challenge persists in selecting the appropriate copula family and parameters, as discussed in [10, 11, 12]. A second strategy is to directly enable the severity component of the model to depend on the frequency component. Specifically, the number of \zzzclaims is introduced as a covariate in the \zzzaverage severity modeling, formulating a conditional severity model; see, e.g., [13, 14]. This method has been popular because it is easy to implement and interpret.

As a comparable alternative, the aggregate claim cost can be directly modeled using Tweedie’s model which assumes a Poisson sum of gamma variables for the \zzzaggregate claim amount. This modeling approach simplifies the analysis by accommodating discrete claim numbers and continuous claim amounts in one distribution; see, e.g., [15]. Concurrently, discussions regarding the suitability of GLMs for aggregate \zzzclaim amount analysis have focused on the trade-off between model complexity and predictive performance, emphasizing the benefits and contexts where Tweedie’s model excels and where alternative methodologies may be better; see, e.g., [16]. Recently, a novel approach is introduced to reduce computational costs for Tweedie’s parameter estimation within GLMs, as seen in [17]. In a related advance, [18] proposed fitting the Tweedie distribution within GLMs through the Expectation-Maximization (EM) algorithm, which is conceptually analogous to iteratively re-weighted Poisson-gamma modeling on an augmented dataset. This approach simplifies the problem by leveraging expectations of latent variables. Numerical examples indicate that the EM-based method outperforms the traditional likelihood maximization approach, particularly in terms of computational efficiency and accuracy. We refer to [19, 18, 20] for recent developments of Tweedie’s model. While both are considered in the literature, the insurance industry typically favours the separated frequency-severity models.

More recently, machine learning methods have been introduced in the context of insurance by adopting actuarial loss distributions to capture the characteristics of insurance claims. We refer to [21, 22, 1, 23, 24] for recent discussions. Insurance pricing models are heavily regulated and must meet specific requirements before being deployed in practice, which poses challenges for most machine learning methods. As discussed in [2, 24], tree models are considered appropriate for insurance rate-making due to their transparent nature. In our previous work [24], we have demonstrated the superiority of Bayesian classification and regression tree (BCART) models in \zzzclaim frequency analysis. In this sequel we construct some novel insurance pricing models using BCART for both \zzzaverage severity \zzzand aggregate claim amount.

Specifically, inspired by the types of claim loss models discussed above, we introduce and investigate three corresponding types of BCART models. We first discuss a benchmark frequency-severity BCART model, where the number of claims and \zzzaverage severity are modeled separately using BCART. Furthermore, We propose two other types of BCART models, with an aim to incorporate the underlying dependence between the number of claims and \zzzaverage severity. These are sequential BCART models (motivated by [13, 14]) and joint BCART models (motivated by [15, 25]). In contrast to the frequency-severity and sequential BCART models which result in two separate trees for the number of claims and \zzzaverage severity, the joint BCART models generate one joint tree for the aggregate claim amount.

The main contributions of this paper are as follows:

-

•

We implement BCART models for average severity including gamma, lognormal and Weibull distributions and for aggregate \zzzclaim amount including compound Poisson gamma (CPG) and zero-inflated compound Poisson gamma (ZICPG) distributions. These are not currently available in any R package.

-

•

To explore the potential dependence between the number of \zzzclaims and average severity, we propose novel sequential BCART models that treat the number of \zzzclaims (or its \zzzestimate) as a covariate in average severity modeling. The effectiveness is illustrated using simulated and real insurance data.

-

•

We present a general framework for the BCART models applicable for multivariate responses, extending the MCMC algorithms discussed in [24]. There have been very few discussions on Bayesian tree models with multivariate responses in the current literature, with the only exception [26] as we are aware of. As a particular application, we propose novel joint BCART models with a bivariate response to simultaneously model the number of claims and aggregate claim amount. In doing so, we employ the commonly used distributions such as CPG and ZICPG. The potential advantages of information sharing using one joint tree compared with two separate trees are also illustrated by simulated and real insurance data.

-

•

For the comparison of one joint tree (generated from the joint BCART models) with two separate trees (generated from the frequency-severity or sequential BCART models), we propose some evaluation metrics which involve a combination of trees using an idea of [27]. We also propose an application of the Adjusted Rand Index (ARI) in assessing the similarity between trees. Although ARI is widely used in cluster analysis, its application to tree comparisons seems to be a novel idea. The use of ARI enhances the understanding of the necessity of information sharing, an aspect not covered in relevant literature; see, e.g., [28].

Outline of the rest of the paper: In Section 2, we briefly review the BCART framework, introducing a more general MCMC algorithm for BCART models with multivariate responses. Section 3 introduces the notation for insurance \zzzclaim data and investigates three types of BCART models for the aggregate claim amount. Section 4 develops a performance assessment of the proposed aggregate \zzzclaim models using simulation examples. In Section 5, we present a detailed analysis of real insurance data using the proposed models. Section 6 concludes the paper.

2 Bayesian CART: A general framework

The BCART models, as introduced in the seminal papers [29, 30], provide a Bayesian perspective on CART models. In this section, we give a brief review of the BCART model using a more general framework that applies to multivariate response data; see [24] for the univariate case.

2.1 Data, model and training algorithm

Consider a matrix-form dataset with indepedent observations. For the -th observation, is a vector of explanatory variables (or covariates) sampled from a space , while is a vector of response variables sampled from a space . For the severity (or frequency) modeling, is a space of real positive (or integer) values. For aggregate \zzzclaim modeling, is a space of 2-dimensional vectors with two components: an integer number of \zzzclaims and a real valued aggregate \zzzclaim amount.

A CART has two main components: a binary tree with terminal nodes which induces a partition of the covariate space , denoted by , and a parameter which associates the parameter value with the -th terminal node. Note that here we do not specify the dimension and range of the parameter which should be clear from the context. If is located in the -th terminal node (i.e., ), then has a (joint) distribution , where represents a parametric family indexed by . By associating observations with the terminal nodes in the tree , we can re-order the observations such that

where is an matrix with denoting the number of observations and denoting the -th observed response in the -th terminal node, and is an analogously defined design matrix. We make the typical assumption that conditionally on , response variables are independent and identically distributed (IID). The CART model likelihood is then

| (1) |

Given , a Bayesian analysis involves specifying a prior distribution , and inference about and is based on the joint posterior using a suitable MCMC algorithm. Since indexes the parametric model whose dimension depends on the number of terminal nodes of the tree, it is usually convenient to apply the relationship , and specify the tree prior distribution and the terminal node parameter prior distribution , respectively. This strategy, introduced by [31], offers several advantages for Bayesian model selection as outlined in [29].

The prior distribution has two components: a tree topology and a decision rule for each of the internal nodes. We follow [29], in which a draw of the tree is obtained by generating, for each node at depth (with for the root node), two child nodes with probability

| (2) |

where are parameters controlling the structure and size of the tree. This process iterates for until we reach a depth at which all the nodes cease growing. After the tree topology is generated, each internal node is associated with a decision rule which will be drawn uniformly among all the possible decision rules for that node. We refer to [24] for detailed discussion on the choice of the prior distribution .

It is important to choose the form for which it is possible to analytically margin out to obtain the integrated likelihood

| (3) |

where in the second equality we assume that conditional on the tree with terminal nodes as above, the parameters , have IID priors , which is a common assumption. Examples where this integration has a closed-form expression can be found in, e.g., [29, 32].

When there is no obvious prior distribution such that the integration in (2.1) is of closed-form, particularly, for non-Gaussian distributed data , a data augmentation method is usually utilized in the literature, e.g., [33, 24]. Here, we present a general framework in which apart from including a data augmentation, some components of are assumed to be known a priori, but some others are assumed to be unknown. More precisely, we assume , where are the parameters that are treated as known and computed using \zzzMethod of Moments Estimation (MME), or Maximum Likelihood Estimation (MLE), and are the unknown parameters that need to be estimated in the Bayesian framework. This newly proposed framework aims to reduce the overall computational time of the algorithm and overcome the difficulty of finding an appropriate prior for some parameters even with the data augmentation (that is why is assumed known a priori). Under this framework, we augment the data by introducing a latent variable so that the integration in (4) is computable for augmented data . The integrated likelihood is given as

where

| (4) | ||||

with defined according to the partition of .

Combining the augmented integrated likelihood with tree prior , allows us to calculate the posterior of

| (5) |

When using MCMC to conduct Bayesian inference, can be updated using a Metropolis-Hastings (MH) algorithm with the right-hand side of (5) used to compute the acceptance ratio. Starting from the root node, the MCMC algorithm for simulating a Markov chain sequence of pairs using the posterior given in (5), is given in Algorithm 1 in which commonly used proposals (or transitions) for include grow, prune, change and swap (see [29]). See [24] for further details.

Input:

Data and current values

1:

Generate a candidate value with probability distribution

2:

Estimate , using MME (or MLE)

3:

Sample

4:

Set the acceptance ratio

5:

Update with probability , otherwise, set

6:

Sample

Output:

New values

Remark 1

(a). In Algorithm 1, the sampling steps should be done only as required. For example, in Step 2, needs to be estimated only for those nodes that were involved in the proposed move from to .

2.2 Model selection and prediction

The MCMC algorithm described in Algorithm 1 can be used to search for desirable trees, and we use the three-step approach proposed in [24] to select an “optimal” tree among those visited trees; see Table 1. To this end, we let be two user input integers which represent the belief of where the optimal number of terminal nodes of the tree might fall into. Note that in the following sections, we introduce the DIC for different models based on the idea that DIC“goodness of fit”“complexity”. See [34, 35] for discussion on DIC in a general Bayesian framework.

| Step 1: | Set a sequence of hyper-parameters such that for , the MCMC algorithm converges to a region of trees with terminal nodes. |

| Step 2: | For each in Step 1, select the tree with maximum likelihood from the convergence region, where is an output from Algorithm 1. |

| Step 3: | From the trees obtained in Step 2, select the optimal one using \zzzdeviance information criterion (DIC). |

Suppose , with terminal nodes and parameter , is the selected tree from the above approach. For new the predicted is defined as

| (6) |

where denotes the indicator function and is the partition of by .

3 Aggregate claim amount modeling with Bayesian CART

This section introduces the BCART models for aggregate claim amount by specifying the response distribution within the framework outlined in Section 2. We begin by introducing the type of insurance \zzzclaim data that will be discussed in this paper. A \zzzclaim dataset with policyholders can be described by , where represents rating variables (e.g., driver age, age of the car and car brand in car insurance); is the exposure in yearly units, quantifying the duration the policyholder is exposed to risk; is the number of \zzzclaims reported during exposure time of the policyholder, and is the aggregate (total) claim amount.

Before describing our models, we recall some basics on the aggregate claim amount modeling as motivation; see, e.g., [36, 14, 3] for discussions. Consider a given (generic) policyholder, and assume unit exposure (i.e., ), for simplicity. The aggregate claim amount of the policyholder can be expressed as

| (7) |

where is the number of \zzzclaims within a year and denotes the severity of the -th claim. It is also assumed that , given , are IID positive random variables which are independent of . Let denote a generic random variable for claim severity and, by convention, when .

We are primarily interested in estimating the pure premium defined as (we remark that generally the pure premium should be defined as , i.e., the expected claim amount per year). We also define the average severity as when and when . It can be easily derived that

| (8) |

When a vector of covariates for this policyholder is available, it can be incorporated into a pricing model through separate models for frequency and severity (or average severity ), this is the so-called frequency-severity model. Traditionally, both frequency and (average) severity components are modeled by GLMs. In the literature (see, e.g., [2, 37, 38]), there are two ways to model the average severity; one is to model claim severity \zzz which induces a model for the average severity , and the other way is to directly model the average severity when . In the first way, the distribution for \zzz is usually restricted to the exponential distribution family (EDF) due to the convolution property. More precisely, assuming , with mean and dispersion , we have, , which means that modeling severity is equivalent to modeling the average severity only when is included as a weight in the model for In the second way, is directly modeled, the choice of its distribution is thus much richer. These are discussed in Section 3.1.

Next, we discuss the covariance between (or ) and . We have

which means that and (or given ) are obviously correlated. Furthermore,

which means that and are also correlated, but and given are uncorrelated. However, and given are not generally independent; see [3] for a simple argument.

The above calculations show that model (7) is plausible for data with positive or zero correlations between \zzzthe number of claims and severity. However, as discussed in [14], \zzzthe number of claims and average severity are often negatively correlated in many types of insurance data, particularly, in collision automobile insurance data. \zzzIn our real data analysis below, we observe a similar negative correlation, following the approach in [14]. To better model \zzzthis type of data and capture the underlying dependence between \zzzthe number of claims and average severity, we introduce two other types of BCART models. First, following the idea of [13, 14] we introduce the sequential BCART models by including (or its estimate ) as a covariate when modeling the average severity in (8). Second, motivated by [15, 25], we introduce joint BCART models by considering as a bivariate response. By its nature, the dependence between \zzzthe number of claims and \zzzaverage severity is directly incorporated in the sequential BCART models. In the joint BCART models, the dependence caused by potentially shared information (through covariates) can be captured in a selected single tree. These BCART models will be discussed in detail in Sections 3.2 and 3.3, respectively.

3.1 Frequency-severity BCART models

Recall that the BCART models for the frequency component of (8) have been discussed in [24]. Here we shall focus on the BCART modeling of the average severity component of (8). More precisely, we will discuss a gamma distribution (as an example in the EDF) with included as a weight, and three other distributions to directly model the average severity without including as a weight, namely, gamma, lognormal, and Weibull. For this purpose, we will only consider a data subset with , and denote by the size of this subset. The subset of average severity data will be denoted by .

3.1.1 Average severity modeling using gamma distribution with as a weight

Assume the generic average severity follows a gamma distribution with parameters being multipliers of , i.e., with . Note that this is equivalent to assuming that the individual severity follows Gamma() distribution, due to the convolution property. Recall that the probability density function (pdf) of the Gamma() distribution and its mean and variance are given as

| (9) |

where is the gamma function. It is known that gamma distribution is right-skewed and relatively light-tailed.

According to the general BCART framework in Section 2, considering a tree with terminal nodes and the two-dimensional parameter for the -th terminal node, we assume for the -th observation, where and , with being the corresponding partition of . Specifically, for -th observation such that , we have (with compressed in )

The mean and variance of are thus given by and , respectively.

For each terminal node , we treat as known and as unknown and shall not apply any data augmentation. According to the notation used in Section 2 this means and . Here will be estimated using MME, i.e.,

| (10) |

where and are the empirical mean and variance of the average severity, respectively, and is the average claim number of the data in the -th terminal node. We treat as uncertain and use a conjugate gamma prior with hyper-parameters . Denote the associated data in terminal node as . The integrated likelihood for the terminal node can then be obtained as

| (11) | ||||

Clearly, from (3.1.1), we see that the posterior distribution of conditional on data (, ) and the estimated parameter , is given by

The integrated likelihood for the tree is thus given by

Next, we discuss the DIC for this tree. \zzzFollowing [24], a DICt for terminal node can be defined as where the posterior mean of is given by

| (12) |

the goodness-of-fit is given as

and the effective number of parameters is defined by

| (13) | ||||

where is added for the parameter which was estimated upfront, and the difference of the last two terms on the right-hand side of the first line is the effective number for the unknown parameter . See [34] for general discussions on the effective number of \zzzparameters in Bayesian models. Some direct calculations yield that

with being the digamma function, and thus

Consequently, the DIC of the whole tree is obtained as

| (14) |

3.1.2 Average severity modeling using distributions without as a weight

Three distributions (gamma, lognormal and Weibull) will be used to model the average severity . See Table 2 for basic properties of lognormal and Weibull distributions, recalling also (9).

| Distribution | Lognormal () | Weibull () |

| Mean | ||

| Variance | ||

| Characteristics | \zzzpositively skewed, | \zzzpositively skewed, |

| heavy-tailed | versatile tail behaviour |

Selecting among these three distributions for certain data may pose a considerable challenge, and scholars have extensively explored this topic; see, e.g., [39]. In average severity modeling, insurers want to gain more insights into the right tail. The gamma distribution would be a suitable model for losses that are not catastrophic, such as auto insurance. The lognormal distribution is more suitable for fire insurance, which may exhibit more extreme values than auto insurance. Moreover, the Weibull distribution has the ability to handle different scenarios by tuning the shape parameter to adapt to different tail characteristics.

We demonstrate how to apply these distributions in BCART models for the average severity data. The idea, as in the previous section, is to specify the distributions/parameters in the general BCART framework of Section 2. We only give some key information below, and defer some detailed calculations to \zzzAppendix A.

Consider a tree with terminal nodes for the average severity data. In gamma and Weibull models, we respectively assume , and , where , . In a lognormal model, we assume that , where , and .

For each terminal node , we treat one parameter as known and the other as unknown, that is, according to the notation in Section 2, is for the gamma and Weibull models and is for the lognormal model, and is for the gamma and Weibull models and is for the lognormal model. Furthermore, we apply a conjugate prior for and , namely, a Gamma() prior for the in the gamma model, a Normal() prior for the in the lognormal model, and an inverse-Gamma() prior for the in the Weibull model, i.e.,

| (15) |

with Estimates for the unknown parameters, calculations of the integrated likelihood and DICt for these three models are given in Appendix \zzzA. We can then use the above procedure leading to the predictions obtained using (6) from different models, as displayed in Table 3.

| Distribution | Gamma() | LN() | Weib() |

| Prediction | |||

| Parameter | obtained using MME | obtained using MME | |

| estimation |

Remark 2

(a). \zzzThere are different ways to parameterize the Weibull distribution, either with two or three parameters; see, e.g., [40]. For simplicity, we adopt the common parameterization with two parameters; see, e.g., [41].

(b). In the above BCART models for average severity we have assumed that one parameter of the distribution is treated as known and the other is treated as unknown which is given a conjugate prior. We note that this is not the only way to implement the BCART algorithms. There are other ways to treat the parameters. For example, for the gamma distribution, the following two alternative approaches can be considered:

-

•

Treat the parameter as known and use a prior for , i.e., where are prior hyper-parameters.

-

•

Treat both and as unknown and use a joint prior for them, i.e., where are prior hyper-parameters; see, e.g., [41].

Although the joint prior can be used to obtain estimators for and simultaneously in the Bayesian framework, it is not formulated as an exact distribution, leading to less accurate estimators. The first way also has this shortcoming. For the lognormal distribution, a normal and inverse-gamma joint prior can be used for the parameters and ; see, e.g., [41]. These more complicated cases are not considered in our current implementation.

(c). Many other distributions can also be used to model average severity, such as Pareto, generalized gamma, generalized Pareto distributions, and so on. However, they either have too many parameters or are challenging to make explicit calculations in the Bayesian framework. We believe further research into the selection of these distributions is worth exploring; see, e.g., [11, 42, 43] for some insights on the application of these distributions to insurance pricing.

In the frequency-severity BCART models, we obtain two trees for frequency and \zzzaverage severity respectively. The pure premium can be calculated using the predictions from these two trees together with the pricing formula (8). There can be many different combinations of predictions for the frequency-severity models, i.e., any model discussed in [24] for frequency and any model introduced above for average severity can be adopted.

One benefit of modeling frequency and \zzzaverage severity separately using two trees is that the important risk factors associated with each component can be discovered separately. However, it can be challenging to interpret two trees as a whole, since several policyholders may be classified in one group by the frequency tree but in a different group by the \zzzaverage severity tree. In the next section, we discuss the combination of two trees for prediction and interpretation.

3.1.3 Evaluation metrics for frequency-severity BCART models

In this section, we begin by exploring some performance evaluation metrics for average severity BCART models. Then we introduce the idea of combining two trees to derive evaluation metrics for the frequency-severity BCART models. Application of these evaluation metrics \zzzwill be discussed in Sections 4 and 5.

Evaluation metrics for average severity trees

We use the same performance measures that were introduced in [24]. Suppose we have obtained a tree with terminal nodes and the corresponding predictions given in Table 3. Consider a test dataset with observations. Denote the number of test data in terminal node by , and denote the associated data in terminal node as . The evaluation metrics are listed below.

-

M1:

The residual sum of squares (RSS) is given by

-

M2:

The squared error (SE), based on a sub-portfolio (i.e., those instances in the same terminal node) level, is defined by

-

M3:

Discrepancy statistic (DS) is defined as a weighted version of SE, given by where \zzz for different models are given in Table 4.

-

M4:

Model Lift indicates the ability to differentiate between groups of policyholders with low and high risks (average severity here), and is defined by using the data and their predicted values in the most and least risky \zzzgroups. We use a similar approach as in [24] to calculate Lift for the \zzzaverage severity tree models; more details on these calculations can be found in [44].

| Dist. | GammaN | Gamma | Lognormal | Weibull |

| ) |

Evaluation metrics for two trees from the frequency-severity model

The \zzzfrequency-severity BCART model yields two trees (one for frequency and the other for average severity). Now, we discuss ways that these two trees can be combined to evaluate model performance based on the aggregate \zzzclaim amount (or called pure premium) prediction .

First, note that RSS(), similarly defined as in the above M1, can be easily employed. More precisely, given the independence assumption between \zzzthe number of claims and (average) severity in the frequency-severity models, we have, by (8),

| (16) |

where is obtained from the \zzzclaim frequency tree and is obtained from the average severity tree. Obviously, the calculation of RSS() focuses only on the individual observations without considering the structure of the two involved trees.

Next, we introduce three metrics dependent on tree structure as defined in the above M2–M4 for the aggregate \zzzclaim amount . To this end, we need to combine those two trees to form a joint partition of the covariate space . The idea is natural – individual tree partitions are superimposed to form a joint partition. This process evolves by merging all the splitting rules from both trees. The splits of each tree contribute to a refined segmentation of the covariate space, resulting in a joint partition that represents the collective behaviour of the original two tree partitions; see [27]. Once a joint partition is obtained, we can derive SE, DS and Lift for the pure premium using a similar approach as for the average severity tree mentioned above. Details of all these evaluation metrics are as follows.

Suppose we have obtained a joint partition with groups and the corresponding predictions for group given in (16). Consider a test dataset with observations. Then, using the notation above we have

-

M1’:

The residual sum of squares

-

M2’:

The squared error

-

M3’:

The discrepancy statistic where is the estimated model variance of in the -th group which is derived using the model specific assumptions and its parameter estimates. More specifically, if the average severity model is as in Section 3.1.1, we can rewrite as in (7) with following independent gamma distribution with parameters as in (9). Thus, we use to derive an estimate of for the -th group, together with corresponding estimated parameters for given in Section 3.1.1 and for different frequency models in [24]. Further, if the average severity model is as in Section 3.1.2, assuming and are independent, we use to derive an estimate for for the -th group, together with corresponding estimated parameters for different average severity models in Tables 3–4 and for different frequency models in [24].

-

M4’:

Model Lift - \zzzsimilarly defined as M4 and [24].

Remark 3

We remark that for each of the BCART models, we apply the three-step approach in Table 1 to select a tree model. The above evaluation metrics are then used to evaluate the performance of these tree models on test data, based on which we can select a best tree model among different types of BCART models. As observed in [24] when discussing different types of frequency BCART models, all four metrics yield the same type of tree model choice based on their performance on test data. It is worth pointing out that within a certain type of BCART model, the test data performance using SE and DS aligns with the tree model selected using the three-step approach and thus they are deemed to be preferred metrics for comparison. See also Sections 4 and 5 for further discussion.

3.2 Sequential BCART models

In this section, we introduce the sequential model to better capture the potential dependence between \zzzthe number of claims and average severity. One popular approach in the literature, e.g., [13, 14], is to treat the number of \zzzclaims as a covariate for the average severity modeling in (8). Following this idea, our sequential BCART model consists of two steps: first, model the frequency component of (8) using the BCART models developed in [24], and then, treat the number of \zzzclaims as a covariate (also treated as \zzza model weight in the GammaN model) for the average severity component in (8) using the BCART models introduced in Section 3.1.1 or 3.1.2.

When modeling average severity with as a covariate, there are usually two ways to treat , namely, either use as a numeric covariate (see [14]) or treat as a factor (see [45]). In this \zzzpaper, we propose another way of including the information of claim count for the average severity modeling, that is, we use the estimation of claim count from the frequency BCART model as a numeric covariate. The underlying idea for this proposal is as follows. The frequency tree will classify the policyholders with similar risk (in terms of claim frequency) into the same group and assign similar estimations (the value of them depends also on their exposure). If the claim count information is highly correlated to the average severity, then the estimated value will be chosen as the splitting covariate and the policyholders in the same frequency group will be more likely (than using ) to be classified into the same group by the average severity tree. In doing so, we expect the sequential model would be able to better capture the potential dependence between \zzzthe number of claims and average severity. This is \zzzdemonstrated to be true by our simulation examples and real insurance data below.

Note the similarity in the general structure of the sequential BCART and the frequency-severity BCART models; the only difference is that the claim count (or ) is treated as a covariate in the average severity modeling within the sequential BCART models. As a result, the sequential BCART models will also produce two trees, one for frequency and the other for average severity. Although no independence is assumed between the number of \zzzclaims and \zzzaverage severity, for simplicity we still estimate the pure premium by the product of the estimations from these two trees; see (16). Furthermore, the evaluation metrics introduced in Section 3.1.3 will also be applied to the sequential BCART models. Clearly, if the optimal average severity tree obtained from the sequential BCART models does not involve claim count (or ) as a splitting covariate, we would expect a similar result to the frequency-severity BCART models.

3.3 Joint BCART models

Different from the previous two types of BCART models where separate tree models are used for the frequency and average severity, in this section we introduce the third type of BCART models, called joint BCART models, where we consider as a bivariate response; see [15, 25] for a similar treatment in GLMs. We discuss two commonly used distributions for aggregate claim amount , namely, CPG and ZICPG distributions. The presence of a discrete mass at zero makes them suitable for modeling aggregate claim amount; see, e.g., [16, 46, 47]. As in [24], for the ZICPG models we need to employ a data augmentation technique. We also explore different ways to embed exposure. The advantage of modeling frequency and (average) severity components separately has been recognized in the literature; see, e.g., [16, 3]. In particular, this separate treatment can reflect the situation when the covariates that affect the frequency and severity are very different. However, one disadvantage is that it takes more effort to combine the two resulting tree models, as we have already seen in Section 3.1.3. Compared to the use of two separate tree models, the advantage of joint modeling is that the resulting single tree is easier to interpret as it simultaneously gives estimates for frequency, pure premium and thus (average) severity. Additionally, for the situation where frequency and (average) severity are linked through shared covariates, using a parsimonious joint tree model might be advantageous; this will be illustrated in the examples in Section 4.

3.3.1 Compound Poisson gamma model

We consider a response in the framework of Section 2, where is Poisson distributed with parameter and defined in (7) with individual severity following a gamma distribution with parameters . In the following, is called a compound Poisson gamma random variable, denoted by . Note that the CPG distribution is a particular Tweedie distribution which is quite popular for aggregate \zzzclaim amount modeling; see, e.g., [25, 48].

According to the general BCART framework in Section 2, considering a tree with terminal nodes and with , for the three-dimensional parameter for the -th terminal node, we assume , and for the -th observation, where , and . Specifically, for -th observation such that , we have the joint distribution

where denotes the pmf of the Poisson distribution with parameter .

For each terminal node , we treat as known, and , as unknown without any data augmentation. Adopting the notation used in Section 2 this means and . Here will be estimated as in (10) using a subset of data with . We treat and as uncertain and use \zzzindependent conjugate gamma priors, i.e., and , where the superscript (or ) indicates this hyper-parameter is assigned for the parameter (or ). Denoting the associated data in terminal node as before, then given the estimated parameter , the integrated likelihood for terminal node can be obtained as

It can be seen that the posterior distribution of and , conditional on data \zzzand the estimated are given respectively by

The integrated likelihood for the tree is thus given by

We now discuss DIC which can be derived similarly as in Section 3.1.1 with a two-dimensional unknown parameter . We first focus on DICt of terminal node . It follows that

where

| (17) |

Therefore, \zzzthe effective number of parameters for terminal node is given by

| (18) | |||||

where the first terms are due to the estimation of . Hence, we obtain

Then the DIC of the tree is obtained by . Using the above results, we can use the approach presented in Table 1, together with Algorithm 1, to search for a tree which can be used for prediction with (6). Given a tree, the estimated pure premium per year in terminal node is

| (19) |

3.3.2 Zero-inflated compound Poisson gamma model

In this section, we again consider a bivariate response , where is now zero-inflated Poisson distributed and is defined in (7) with individual severity following a gamma distribution with parameters . In the following, is called a zero-inflated compound Poisson gamma random variable. Unlike the CPG models, for ZICPG models we now introduce a data augmentation strategy as in [24] to obtain a closed form expression for the integrated likelihood; see (3.3.2) below. Motivated by the discussion on the ZIP-BCART models in [24], we construct three ZICPG models according to how the exposure is embedded into the modeling. We try to cover all three ZICPG models in a general set-up, which requires some general notation for exposure.

Again we consider a tree with terminal nodes and . Denoting the data in terminal node by , we introduce the following general joint distribution for the -th observation in this node:

| (20) | ||||

where we use to denote the “exposure” for the zero mass part and to denote the “exposure” for the Poisson part. The above general formulation can cover three different models as special cases. Namely, 1) setting and , then the exposure is only embedded in the Poisson part, yielding the ZICPG1 model; 2) setting and then the exposure is only embedded in the zero mass part, yielding the ZICPG2 model; 3) setting means the exposure is embedded in both parts, yielding the ZICPG3 model. Note that is the probability that zero is due to the point mass component.

For computational convenience, a data augmentation scheme is used. To this end, we introduce two latent variables and , and define the data augmented likelihood for the -th data instance in terminal node as

| (21) | ||||

where the support of the function is . It can be shown that (20) is the marginal distribution of the above augmented distribution; \zzzsee Appendix B for more details.

By conditional arguments, we can also check that , given data and parameters ( and ), has a Bernoulli distribution, i.e., and if . Furthermore, .

For each terminal node , we treat as known, and as unknown and apply the above data augmentation. According to the notation used in Section 2 this means and . Here will be estimated as in (10) using a subset of data with . As before, we choose independent conjugate gamma priors for , , and , i.e., Then, the integrated augmented likelihood for terminal node can be obtained as

| (22) |

The integrated augmented likelihood for the tree is thus given by

Now, we discuss the DIC for this tree. It is derived that

| (23) | |||||

where

| (24) |

and is given in (17). Furthermore, direct calculations yield the effective number of parameters for terminal node given by

and thus

Using these formulae for ZICPG, we can follow the approach presented in Table 1, together with Algorithm 1 (here ), to search for a tree which can then be used for prediction with (6). Given a tree, the estimated pure premium per year in terminal node is given as

| (25) |

Remark 4

We observe that the effective number of parameters does not depend on exposures and , illustrating that the way to embed the exposure does not affect the effective number of parameters. This is intuitively reasonable and is in line with the observations for NB and ZIP models in [24].

3.3.3 Evaluation metrics for joint models

Note that the ultimate goal in insurance rate-making is to set the pure premium based on the estimate of the aggregate \zzzclaim amount . Thus, for joint models, we focus on evaluation metrics defined via the second component in the bivariate response . We follow the definitions of M1’–M4’ in Section 3.1.3; here the number of groups is the number of terminal nodes .

Suppose we have obtained a tree with terminal nodes and corresponding predictions given in (19) or (25). Consider a test dataset with observations. Denote the test data in terminal node by . The RSS, SE and Lift are defined by M1’, M2’ and M4’ respectively, with replaced by . The DS is also similarly defined by M3’, but with being equal to \zzz for the CPG model, and for the ZICPG model.

3.4 Two separate trees versus one joint tree: adjusted rand index

In this section, we extend our focus to examine the similarity between the BCART generated optimal trees. This exploration will give us confidence and valuable insights into whether information sharing through one joint tree is essential for model accuracy and effectiveness, compared to separate trees.

Measuring the similarity of two trees is generally challenging, particularly when there are variations in the number of terminal nodes or the structure (balanced/unbalanced) of the two trees; see [49] and the references therein. We propose to explore one simple index commonly employed in cluster analysis comparison, namely, the adjusted Rand Index (ARI) which is a widely recognized metric for assessing the similarity of different clusterings; see, e.g., [50, 51, 52]. We extend its application to evaluate the similarity of two trees. This is a natural application since a tree generates a partition of the covariate space which automatically induces clusters (i.e. observations belonging to the same leaf) of policyholders in the insurance context.

The ARI measures the similarity between two data partitions by comparing the number of pairwise agreements and disagreements, adjusting for the possibility of random clustering to ensure that the index values are corrected for chance. This results in a score ranging from to , where indicates perfect agreement, suggests a similarity no better than random chance, and negative values imply less agreement than expected by chance. The ARI is particularly valued for its ability to account for different cluster sizes and number of clusters, making it a robust metric. Our results use the adj.rand.index function in the R package fossil (see more details in [53]).

4 Simulation examples

In this section, we investigate the performance of the BCART models introduced in Section 3 by using simulated data. \zzzIn Scenario 1, the effectiveness of sequential BCART models in capturing the dependence between the number of \zzzclaims and average severity is examined. Scenario 2 focuses on the influence of shared information between the number of \zzzclaims and average severity.

In the sequel, we use the abbreviation Gamma-CART to denote CART for the Gamma model, and other abbreviations can be similarly understood (e.g., ZICPG1-BCART denotes the BCART for ZICPG1 model).

4.1 Scenario 1: Varying dependence between the number of \zzzclaims and average severity

Given the similarities and differences between the frequency-severity models and the sequential models, this simulation example aims to demonstrate the capability of the sequential BCART models to address the dependence between the number of \zzzclaims and average severity. The performance of using different forms of \zzzclaims count ( or its estimate ) within sequential models is also examined. \zzzIn the following analysis, we treat as a numeric variable. As the current focus is not on comparing different distributions applied for \zzzclaim frequency and average severity, for the sake of simplicity we use the Poisson and gamma distributions for both frequency-severity models and sequential models. Besides, to simplify the setting and to reflect the importance of treating (or ) as a covariate in the average severity modeling, we model directly as in Section 3.1.2, without using as a model weight in the gamma distribution, i,e., . Additionally, since both frequency-severity models and sequential models have the same \zzzclaim frequency tree, in the following model comparison, we focus on the average severity tree. The evaluation metrics introduced in Section 3.1.3 will be employed for this comparison.

We simulate with independent observations. Here , with independent components for . We assume exposure for simplicity, as it is not a key feature in this context. Moreover, , where

| (28) |

We obtained for 901 occurrences, for which we set . For the remaining 4099 cases, is generated from a gamma distribution with a pre-specified and varying dependence parameter , i.e., , in which the shape (fixed as 1 for simplicity) and rate parameters are chosen to maintain the \zzzempirical average claim amount to be around 500, aligning with real-world scenarios. The data is split into two subsets: a training set with observations and a test set with observations. In this case, our goal is to examine how the dependence modulated by influences the performance of both frequency-severity models and sequential models, and the performance of incorporating (or ) into the sequential models. If the models choose (or ) as a splitting covariate, it would indicate that the claim count plays an important role in average severity modeling, and thus sequential models should be preferred.

Table 6 presents a numerical summary of the average severity and conditional correlation coefficients between the number of \zzzclaims and average severity for datasets with different values of . It is obvious that by changing the value of , the conditional correlation between the number of \zzzclaims and average severity varies. For simplicity, we only focus on the case where , indicating a strong \zzznegative conditional dependence between them. Intuition suggests that sequential models are expected to perform better in capturing strong dependence, and the stronger the dependence, the better the relative performance of sequential models. In contrast, when there is only a weak dependence (e.g., =0.00001) in the data, the claim count (or ) is unlikely to be selected as a splitting covariate in sequential models, resulting in frequency-severity models and sequential models being the same.

| \zzzValues of | |||

| Mean | 828 | 764 | 206 |

| Median | 494 | 458 | 92 |

| Max | 9713 | 7211 | 5138 |

| Standard deviation | 983 | 855 | 324 |

| -0.01 | -0.05 | -0.41 |

| Training data | Test data | |||||||

| Model | DIC | RSS( | SE | DS | Lift | |||

| Gamma-BCART (4) | 0.95 | 10 | 7.95 | 2769 | 8.34 | 0.0927 | 0.0331 | 1.42 |

| Gamma-BCART (5) | 0.99 | 10 | 9.94 | 2716 | 8.18 | 0.0894 | 0.0309 | 1.85 |

| Gamma-BCART (6) | 0.99 | 7 | 11.92 | 2738 | 8.11 | 0.0904 | 0.0319 | 1.92 |

| Gamma1-BCART (4) | 0.95 | 10 | 7.97 | 2698 | 8.20 | 0.0909 | 0.0321 | 1.61 |

| Gamma1-BCART (5) | 0.99 | 10 | 9.96 | 2644 | 8.04 | 0.0875 | 0.0297 | 2.06 |

| Gamma1-BCART (6) | 0.99 | 7 | 11.94 | 2663 | 7.97 | 0.0886 | 0.0305 | 2.16 |

| Gamma2-BCART (4) | 0.95 | 10 | 7.98 | 2682 | 8.09 | 0.0903 | 0.0312 | 1.65 |

| Gamma2-BCART (5) | 0.99 | 10 | 9.98 | 2618 | 7.91 | 0.0866 | 0.0292 | 2.09 |

| Gamma2-BCART (6) | 0.99 | 7 | 11.97 | 2635 | 7.83 | 0.0875 | 0.0300 | 2.18 |

First, looking at the model selection on training data in Table 6, although we do not have any true tree structure, all models consistently choose a tree with five terminal nodes based on DIC. Notably, the best performing model is Gamma2-BCART (with DIC), validating our proposed approach of treating as a covariate. Moreover, the larger difference \zzzin DICs between the Gamma model without claim count (or its estimate) as a covariate (i.e., Gamma-BCART) and \zzzthose with it (i.e., Gamma1-BCART and Gamma2-BCART) suggests that models \zzzincorporating claim count (or its estimate) as a covariate perform better when there is stronger inherent dependence in the data. In addition, when examining the splitting rules used in the optimal tree, both trees from Gamma1-BCART and Gamma2-BCART \zzzuse the claim count (or ) in the second split step, and they have similar split points. Subsequently, we compare the performance on test data in Table 6. We observe that Gamma2-BCART models perform best among these three types of BCART models according to all four metrics. Furthermore, for each type of BCART model, both metrics \zzzSE and DS confirm that the selected tree with 5 terminal nodes performs the best, which validates the model selection from the training data (see also Remark 3).

We perform an additional 10 repeated experiments using the same model to create new training and test datasets. We also use the same data-generating procedure to create 10 different datasets. In both scenarios, we arrive at the same conclusion as for Table 6 (results not shown here). This consistency indicates that the results are not merely due to random variation or specific datasets but reflect a true and reliable characteristic of the model being studied.

We also test these three models with different values of and in (28). Based on several additional simulations, we observe the following consensus: 1) When the dependence between the number of \zzzclaims and average severity is weak, both frequency-severity models and sequential models exhibit similar performance. In such a case, we recommend the former since they reduce computation time; 2) When the dependence is stronger, sequential models outperform frequency-severity models by selecting the number of \zzzclaims (or its estimate) as a covariate for average severity; 3) Gamma2-BCART outperforms Gamma1-BCART, which validates our discussion in Section 3.2.

4.2 Scenario 2: Covariates sharing between the number of \zzzclaims and average severity

In this scenario, we consider two simulations where common covariates are used for parameters representing the number of \zzzclaims and average severity. The objective is to assess the effectiveness of frequency-severity BCART models and joint BCART models, that is, whether it is preferred to share information using one joint tree. To this end, we consider CPG distribution in joint BCART models, and correspondingly, Poisson distribution and gamma distribution involving as a model weight in the frequency-severity BCART models to keep consistency for comparison. We first explain these two simulations and then present some findings and suggestions.

Simulation 2.1: We simulate a dataset with independent observations. Here , with independent components , , , , and , where \zzz (or stands for continuous (or discrete-type) uniform distribution. Moreover, , where

If then , otherwise follows a gamma distribution, i.e., , where

For simplicity, we assume , and the values of are selected as such that the average \zzzclaim amount is around 200, which is close to the situation in real-world scenarios. See Figure 2 for an illustration of the true covariate space partition and corresponding values of parameters.

Simulation 2.2: We keep most simulation settings as in Simulation 2.1, except the partition of the covariate space; see Figure 2. Specifically,

and for non-zero , generate , where

The specific design here is that both components of the response variable (,) are affected by the same covariates and . In Simulation 2.1 they share similar split points, while for Simulation 2.2 they have quite different split points. The variables are all noise variables. We aim to compare separate BCART trees versus one joint BCART tree.

Each simulation dataset is split into a training set with observations and a test set with observations. The outputs from training data and test data for the BCART models are presented in Tables 7–8 for Simulation 2.1 and Tables 10–10 for Simulation 2.2.

| Model | DIC | |||

| Poisson-BCART (3) | 0.95 | 15 | 2.98 | 3697 |

| Poisson-BCART (4) | 0.99 | 13 | 3.98 | 3572 |

| Poisson-BCART (5) | 0.99 | 10 | 4.97 | 3616 |

| Gamma-BCART (3) | 0.95 | 10 | 5.97 | 30586 |

| Gamma-BCART (4) | 0.99 | 10 | 7.97 | 30319 |

| Gamma-BCART (5) | 0.99 | 8 | 9.96 | 30414 |

| CPG-BCART (3) | 0.99 | 5 | 8.92 | 34017 |

| CPG-BCART (4) | 0.99 | 4 | 11.90 | 33582 |

| CPG-BCART (5) | 0.99 | 3 | 14.89 | 33711 |

| Model | RSS() | \zzzSE | \zzzDS | \zzzLift |

| -BCART (3/3) | 3.03 | 0.1324 | 0.0833 | 2.13 |

| -BCART (4/4) | 2.89 | 0.1245 | 0.0791 | 2.21 |

| -BCART (5/5) | 2.81 | 0.1273 | 0.0812 | 2.23 |

| CPG-BCART (3) | 3.01 | 0.1319 | 0.0820 | 2.15 |

| CPG-BCART (4) | 2.84 | 0.1211 | 0.0769 | 2.27 |

| CPG-BCART (5) | 2.78 | 0.1254 | 0.0795 | 2.29 |

| Model | DIC | |||

| Poisson-BCART (3) | 0.95 | 15 | 2.97 | 3875 |

| Poisson-BCART (4) | 0.99 | 12 | 3.97 | 3669 |

| Poisson-BCART (5) | 0.99 | 10 | 4.96 | 3724 |

| Gamma-BCART (3) | 0.95 | 10 | 5.97 | 32156 |

| Gamma-BCART (4) | 0.99 | 10 | 7.96 | 31798 |

| Gamma-BCART (5) | 0.99 | 8 | 9.96 | 31904 |

| CPG-BCART (8) | 0.99 | 5 | 23.85 | 36174 |

| CPG-BCART (9) | 0.99 | 3 | 26.81 | 35622 |

| CPG-BCART (10) | 0.99 | 2 | 29.79 | 35781 |

| Model | RSS() | \zzzSE | \zzzDS | \zzzLift |

| -BCART (3/3) | 3.21 | 0.152 | 0.091 | 2.18 |

| -BCART (4/4) | 3.04 | 0.140 | 0.073 | 2.30 |

| -BCART (5/5) | 2.95 | 0.141 | 0.079 | 2.32 |

| CPG-BCART (8) | 3.23 | 0.160 | 0.097 | 2.15 |

| CPG-BCART (9) | 3.08 | 0.142 | 0.088 | 2.24 |

| CPG-BCART (10) | 3.01 | 0.146 | 0.090 | 2.25 |

We start by looking at the DICs on training data in Tables 7 and 10. For Simulations 2.1 and 2.2, both Poisson-BCART and Gamma-BCART can find the optimal tree with the correct 4 terminal nodes. However, the selected joint CPG-BCART tree for Simulation 2.1 has only 4 terminal nodes which is different from its simulation scheme that should result in a covariate space partition with 9 groups. In contrast, the selected joint CPG-BCART tree for Simulation 2.2 has 9 terminal nodes which is consistent with its simulation scheme. This result for the frequency-severity BCART models is expected, based on our earlier discussion of the separated frequency and average severity models. Now we look into the details of the selected joint tree to explore the reason. For Simulation 2.1, we see that both and are used in the tree and the split points for them are close to 0.5 which is the mean of 0.47 and 0.53 for , and also the mean of 0.52 and 0.48 for . Since these split values are very close, it is reasonable for the joint BCART model to select a split value around their mean, resulting in a selected joint tree with 4 terminal nodes. For Simulation 2.2 the selected joint tree includes 9 terminal nodes, which is also reasonable because the split values for both variables are far apart.

The results for test data are shown in Tables 8 and 10. For Simulation 2.1 we see that the joint model performs better than the frequency-severity model, while for Simulation 2.2 the opposite is observed.

In the above, we \zzzfocused on using evaluation metrics to assess model performance. We now calculate the ARI for these three trees, using the test data. First, for Simulation 2.1 we have

This confirms the preference of joint models in Simulation 2.1, as the ARI values indicate \zzzstrong similarity. \zzzThis suggests that information sharing can avoid redundant use of similar information, which is evident in the similarities between the two trees. Next, for Simulation 2.2 we have

This indicates that the frequency-severity model should be preferred in Simulation \zzz2.2 as the ARI values are smaller, especially the first. It is not obvious how to determine a specific ARI threshold that indicates when sharing information becomes worthwhile. This requires further research.

Building on the above findings in Simulation 2.2, our investigation shows that both the frequency-severity model and joint model identify the optimal trees as expected, indicating that information sharing may not be necessary. Further exploration reveals that the parameter estimates of the joint tree are not as accurate as those for the frequency-severity trees. This discrepancy arises because the joint tree uses less data for the estimates in some of the 9 terminal notes, compared to the separate two trees, each of which only has 4 terminal nodes. We suspect that, with fewer observations the differences will increase, and vice versa. To investigate this intuition, we use the same data generation scheme with different sample sizes (ranging from 1,000 to 50,000) to conduct 10 repeated experiments for each size. Labelling the regions in Figure 2 as , Tables 11 and 12 respectively present the average absolute parameter estimation errors for and , along with their standard deviations. We observe from these tables that as the amount of data increases, the differences between the two model estimates become smaller. This investigation suggests if less data is available the frequency-severity models may be preferred as they produce more accurate parameter estimates than the joint models, while if more data is available the joint models may be preferred to save computation time.

| Region | Model | ||||

| Region A | FS CPG | 5.45 (0.522) 5.42 (0.521) | 4.74 (0.317) 4.75 (0.295) | 3.76 (0.241) 3.79 (0.251) | 0.95 (0.207) 0.95 (0.172) |

| Region B | FS CPG | 5.04 (0.414) 5.28 (0.498) | 3.96 (0.259) 4.06 (0.280) | 2.86 (0.250) 2.99 (0.308) | 0.80 (0.216) 0.87 (0.267) |

| Region C | FS CPG | 5.04 (0.414) 5.41 (0.502) | 3.96 (0.259) 4.22 (0.321) | 2.86 (0.250) 3.05 (0.311) | 0.80 (0.216) 0.88 (0.269) |

| Region D | FS CPG | 5.31 (0.479) 5.63 (0.465) | 3.84 (0.310) 4.97 (0.285) | 2.62 (0.343) 2.72 (0.322) | 1.07 (0.189) 1.30 (0.303) |

| Region E | FS CPG | 5.48 (0.457) 6.01 (0.448) | 4.00 (0.309) 4.69 (0.413) | 2.82 (0.321) 3.38 (0.411) | 1.11 (0.273) 1.13 (0.269) |

| Region F | FS CPG | 5.48 (0.457) 6.40 (0.472) | 4.00 (0.309) 5.02 (0.435) | 2.82 (0.321) 3.62 (0.424) | 1.11 (0.273) 1.15 (0.280) |

| Region G | FS CPG | 5.31 (0.479) 5.91 (0.492) | 3.84 (0.310) 5.12 (0.345) | 2.62 (0.343) 3.01 (0.338) | 1.07 (0.189) 1.33 (0.312) |

| Region H | FS CPG | 5.48 (0.457) 6.34 (0.462) | 4.00 (0.309) 4.83 (0.428) | 2.82 (0.321) 3.51 (0.420) | 1.11 (0.273) 1.14 (0.276) |

| Region I | FS CPG | 5.48 (0.457) 6.44 (0.501) | 4.00 (0.309) 5.23 (0.447) | 2.82 (0.321) 3.80 (0.431) | 1.11 (0.273) 1.15 (0.279) |

| Region | Model | n= | |||

| Region A | FS CPG | 4.52 (0.525) 5.44 (0.547) | 4.35 (0.497) 4.72 (0.543) | 4.08 (0.261) 4.54 (0.379) | 2.79 (0.224) 2.89 (0.252) |

| Region B | FS CPG | 4.52 (0.525) 5.21 (0.568) | 4.35 (0.497) 4.63 (0.526) | 4.08 (0.261) 4.40 (0.369) | 2.79 (0.224) 2.86 (0.251) |

| Region C | FS CPG | 9.52 (0.739) 10.32 (0.943) | 7.56 (0.563) 8.25 (0.713) | 6.36 (0.481) 6.67 (0.523) | 5.15 (0.295) 5.27 (0.311) |

| Region D | FS CPG | 4.52 (0.525) 5.40 (0.570) | 4.35 (0.497) 4.66 (0.523) | 4.08 (0.261) 4.42 (0.375) | 2.79 (0.224) 2.88 (0.254) |

| Region E | FS CPG | 4.52 (0.525) 5.04 (0.541) | 4.35 (0.497) 4.50 (0.522) | 4.08 (0.261) 4.32 (0.377) | 2.79 (0.224) 2.84 (0.249) |

| Region F | FS CPG | 9.52 (0.739) 9.88 (0.802) | 7.56 (0.563) 7.83 (0.610) | 6.36 (0.481) 6.55 (0.457) | 5.15 (0.295) 5.23 (0.302) |

| Region G | FS CPG | 7.65 (0.859) 9.35 (0.983) | 6.52 (0.719) 7.94 (0.825) | 4.39 (0.455) 5.24 (0.480) | 2.95 (0.297) 3.21 (0.342) |

| Region H | FS CPG | 7.65 (0.859) 8.96 (0.951) | 6.52 (0.719) 7.23 (0.802) | 4.39 (0.455) 4.99 (0.473) | 2.95 (0.297) 3.12 (0.325) |

| Region I | FS CPG | 4.53 (0.592) 4.62 (0.595) | 4.01 (0.589) 4.00 (0.578) | 2.77 (0.137) 2.76 (0.141) | 1.96 (0.122) 1.96 (0.124) |

We also run several other simulation examples which are not shown here. From our results, we conclude that: when two trees have similar splitting rules (high ARI), one joint tree is more effective through information sharing. Conversely, if all covariates affecting \zzzclaim frequency and average severity are different (ARI is close to ), two trees outperform one joint tree. This conclusion aligns with our intuition and can be generalized to a wider field; see also [28].

5 Real data analysis

We illustrate our methodology with the insurance dataset dataCar, available from the library insuranceData in R; see [54] for details. This dataset is based on one-year vehicle insurance policies taken out in 2004 or 2005. There are 67,856 policies of which 93.19% made no \zzzclaims. A description of the variables is given in Table 13. We split this dataset into training (80%) and test (20%) datasets such that the proportion of non-zero \zzzclaims is the same in both training and test datasets.

| Variable | Description | Type |

| numclaims (\zzz) | number of claims | numeric |

| exposure (\zzz) | in yearly units, between 0 and 1 | numeric |

| claimscst0 (\zzz) | total claim amount for each policyholder | numeric |

| veh_value | vehicle value, in $10,000s | numeric |

| veh_age | vehicle age category, 1 (youngest), 2, 3, 4 | numeric |

| agecat | driver age category, 1 (youngest), 2, 3, 4, 5, 6 | numeric |

| veh_body | vehicle body, one of: HBACK, UTE, STNWG, HDTOP, PANVN, SEDAN, TRUCK, COUPE, MIBUS, MCARA, BUS, CONVT, RDSTR | character |

| gender | Female or Male | character |

| area | coded as A B C D E F | character |

| \zzzStatistics | Min | Mean | Max | Standard Deviation | Skewness | Kurtosis |

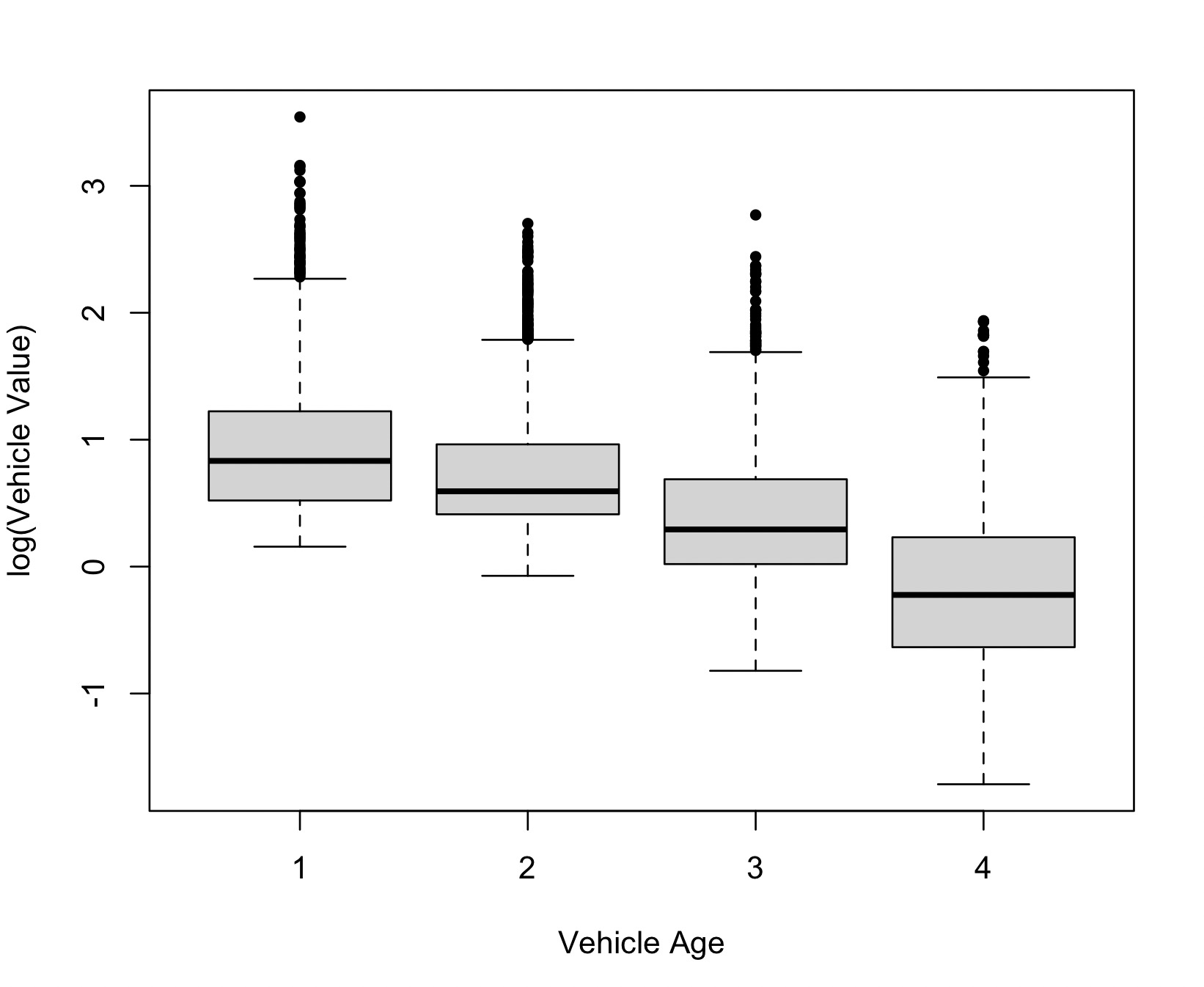

| Average severity | \zzz200 | \zzz1916 | 55922 | \zzz3461 | \zzz5 | \zzz48 |

5.1 Average severity modeling

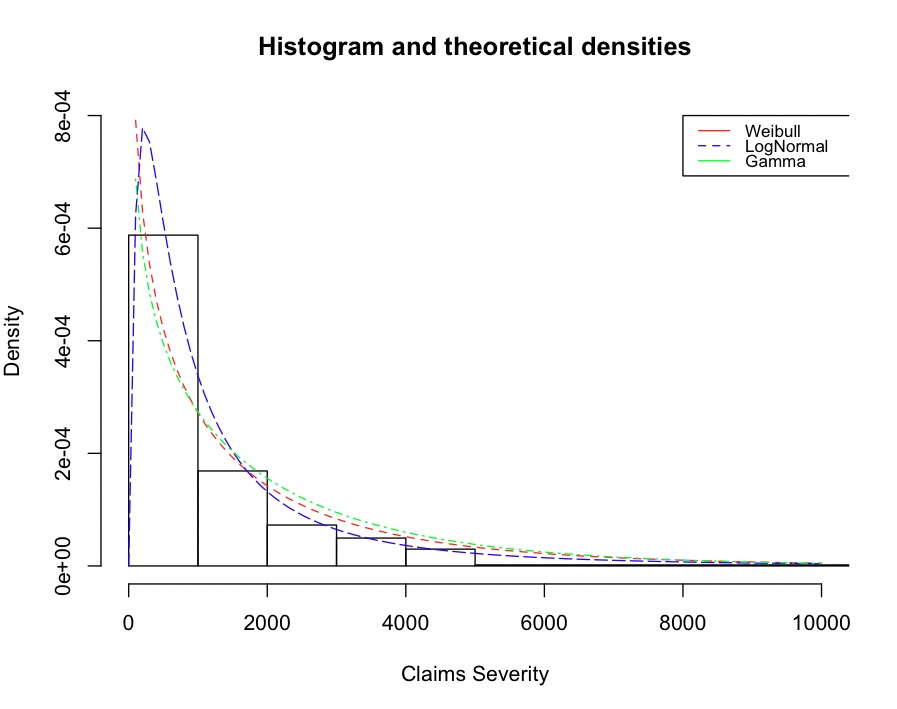

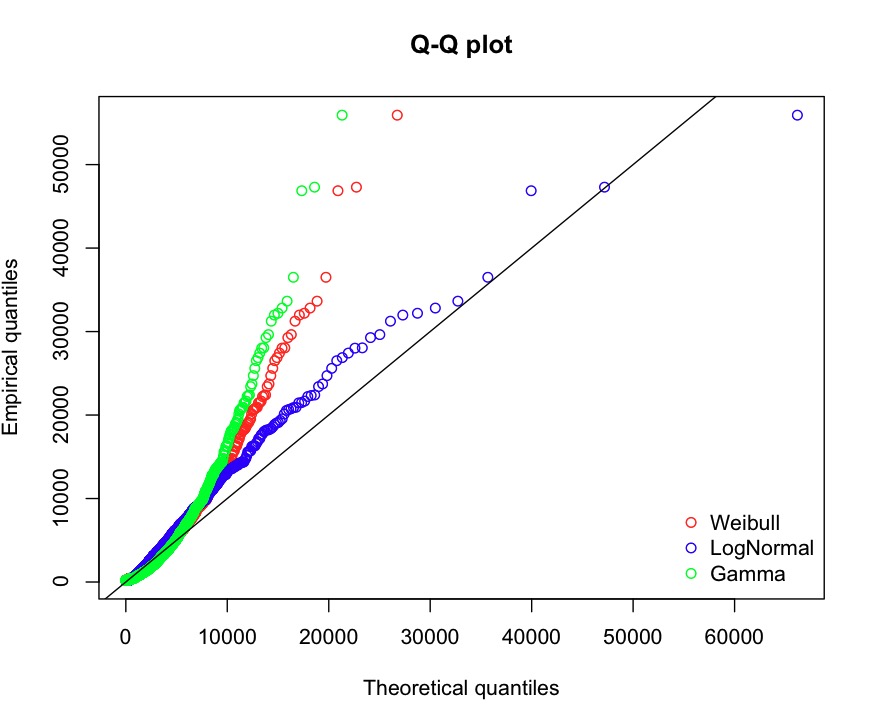

For average severity modeling, we consider a subset of the data with . Among all 67,856 policies, 4,624 policies satisfy this requirement (3,699 in the training data, and 925 in the test data). We calculate the average severity by dividing the total claim amount by the number of claims for each policyholder. A numerical summary of the average severity data is displayed in Table 14, \zzzindicating that the average severity data exhibit right-skewness and heavy tails. We start with some exploratory analysis, fitting gamma, lognormal and Weibull distributions to the whole data. From Figures 3 and 4 we see that all distributions can capture the right-skewed feature, however, none of them correctly captures the heavy right tail of the distribution. It appears that the lognormal distribution fits slightly better when the data are treated as IID. However, as we will see below the lognormal distribution will not be the best choice in the BCART models for this data.

For comparison, we first run some benchmark CART models. We have tried to fit the ANOVA-CART using both the original and log-transformed training data. Neither of them gives us any reasonable result since no split is identified, resulting in only a root node tree. We use the R package distRforest (cf. [56]) to fit Gamma-CART and LN-CART and both of the trees, after cost-complexity pruning, have 5 terminal nodes. As far as we are aware there is no R package with the Weibull distribution implemented for regression trees.

We then apply the proposed Gamma-BCART, LN-BCART, and Weib-BCART to the same data. The DICs in Table 15 indicate that all these BCART models choose a tree with 4 terminal nodes.

| Training data | Test data | |||||||

| Model | DIC | RSS() | SE | DS | Lift | |||

| Gamma-GLM | - | - | - | - | 1.4335 | - | - | - |

| Gamma-CART (5) | - | - | - | - | 1.4173 | 464 | 0.00171 | 1.625 |

| LN-CART (5) | - | - | - | - | 1.4168 | 458 | 0.00168 | 1.629 |

| Gamma-BCART (3) | 0.99 | 4 | 5.97 | 78061 | 1.4201 | 486 | 0.00181 | 1.567 |

| Gamma-BCART (4) | 0.99 | 3.5 | 7.97 | 77779 | 1.4176 | 457 | 0.00154 | 1.615 |

| Gamma-BCART (5) | 0.99 | 2 | 9.95 | 77982 | 1.4158 | 472 | 0.00167 | 1.643 |

| LN-BCART (3) | 0.99 | 5 | 5.97 | 78022 | \zzz1.4193 | \zzz483 | \zzz0.00178 | \zzz1.570 |

| LN-BCART (4) | 0.99 | 4 | 7.97 | 77741 | \zzz1.4171 | \zzz449 | \zzz0.00149 | \zzz1.628 |

| LN-BCART (5) | 0.99 | 3 | 9.96 | 77893 | \zzz1.4153 | \zzz456 | \zzz0.00161 | \zzz1.649 |

| Weib-BCART (3) | 0.99 | 7 | 5.98 | 77932 | 1.4177 | 473 | 0.00164 | 1.604 |

| Weib-BCART (4) | 0.99 | 5 | 7.98 | 77646 | 1.4154 | 433 | 0.00131 | 1.661 |

| Weib-BCART (5) | 0.99 | 4 | 9.98 | 77821 | 1.4136 | 446 | 0.00144 | 1.693 |

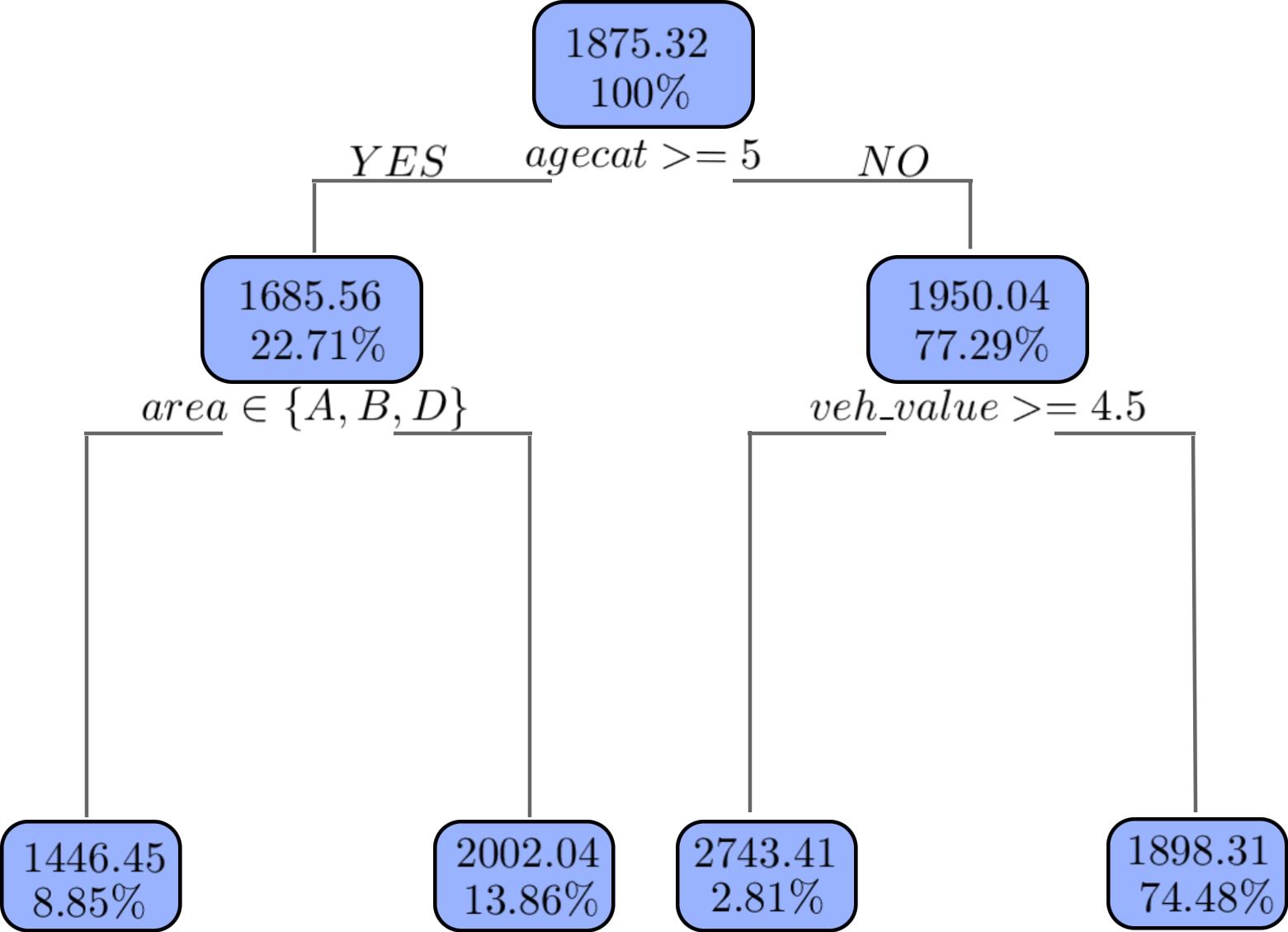

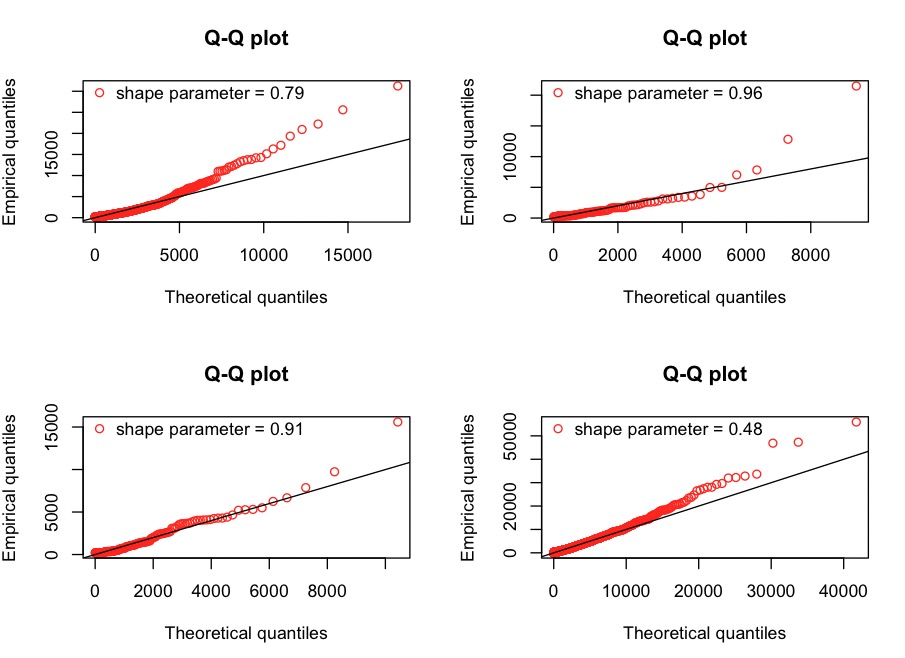

We also examine the splitting rules used in each tree. Gamma-CART uses both “agecat” and “veh_value” twice, with the first one being “agecat”. In contrast, LN-CART uses three different variables, “veh_value” first, followed by “veh_body” and “area”. All trees from BCART models, i.e., Gamma-BCART, LN-BCART, and Weib-BCART, have the same tree structure and splitting variables (“agecat”, “veh_value”, and “area”), while the split values/categories are slightly different. Weib-BCART, in particular, can identify a more risky group (i.e., the one with estimated \zzzaverage severity equal to 2743.41); see Figure 5. This may be because, as discussed in Section 3.1.2, Weib-BCART can flexibly control the shape parameter to adapt to data with different tail characteristics, allowing it to handle cases where some groups (terminal nodes) have lighter tails, and others have heavier tails. In Figure 6, we observe that although all shape parameters are smaller than one, indicating heavy tails for average severity data within each terminal node, the selected Weib-BCART tree shows improved data fitting compared to Figure 4. Similar improvements are obtained from Gamma-BCART and LN-BCART (with their Q-Q plots not shown here). We also use a standard Gamma-GLM for this dataset. We find that only the variable “gender” is significant, and thus no interaction is considered in the Gamma-GLM. Interestingly, “gender” does not appear in any of the CART and BCART models. In summary, though the variables used for different models may differ, there seems to be a consensus that “agecat” is still significantly important for average severity modeling, as Gamma-CART and all BCART models use it in the first split, and “veh_value” is another relatively important variable. This observation aligns, to some extent, with our initial analysis of the relationship between covariates and average severity; see Table 18 below. Particularly, in comparison to CARTs, BCART models reveal another important variable, “area”.

The performance on the test data of the selected tree models above is given in Table 15. It is evident that the Gamma-GLM is not as good as the tree models, \zzzas reflected in RSS(). The study yields the following model ranking: Weib-BCART, LN-BCART, Gamma-BCART, LN-CART, Gamma-CART. This ranking is consistent with our expectations. First, it is common that average severity data is heavy-tailed. Second, the Weibull distribution is advantageous, because it can effectively handle varying tail characteristics in different tree nodes.

5.2 Aggregate \zzzclaim modeling

5.2.1 Model fitting and comparison

We now fit the three BCART models with aggregate \zzzclaim data, namely, frequency-severity models, sequential models, and joint models. For frequency-severity models, numerous combinations of \zzzclaim frequency and average severity models are possible; see [24] for the frequency models and Section 5.1 for \zzzaverage severity models. \zzzHere, we choose ZIP2-BCART and Weib-BCART as the optimal tree models for frequency-severity models (see [24] and Section 5.1). Note that although ZIP2-BCART and Weib-BCART are identified as the best for claim frequency and average severity separately, it is unclear whether they remain optimal when combined. This will be examined and discussed below. For joint models, we discuss the CPG-BCART model and three types of ZICPG-BART models. Because of these choices, we also include the frequency-severity BCART model with Poisson and gamma distributions for comparison. For sequential BCART models, we consider Poisson-BCART (or called P-BCART) and ZIP2-BCART for claim frequency. Subsequently, we treat the claim count (or ) as a covariate in the corresponding Gamma-BCART and Weib-BCART for average severity. The resulting models are called Gamma1-BCART (or Gamma2-BCART, with from P-BCART) and Weib1-BCART (or Weib2-BCART, with from ZIP2-BCART).

Table 16 presents the DICs for the average severity part in the sequential models and for the joint models. We see that in the average severity modeling with (or ) as a covariate, all of them choose an optimal tree with 4 terminal nodes. Upon inspecting the tree structure, (or ) is indeed used in the first step in all those optimal trees. All of them replace the previously used variable “agecat” by the covariate (or ). We suspect this may be due to a strong relationship between the covariates and “agecat”, as verified in the claim frequency analysis (see [24]). Furthermore, by comparing the DICs of all Gamma-BCART and Weib-BCART models in Tables 15 and 16 (with/without or as a covariate), we \zzzfind that the model performance improves when considering (or ) as a covariate, especially when using . For joint models, i.e., CPG-BCART and three ZICPG-BCART models, all of them choose optimal trees with 5 terminal nodes. Among them, ZICPG3-BCART, with the smallest DIC (), is deemed to be the best.

| Model | \zzz | DIC | ||

| Gamma1-BCART (3) | 0.99 | 4 | 5.97 | 78032 |

| Gamma1-BCART (4) | 0.99 | 3.5 | 7.97 | 77750 |

| Gamma1-BCART (5) | 0.99 | 2 | 9.96 | 77854 |

| Gamma2-BCART (3) | 0.99 | 4 | 5.98 | 78024 |

| Gamma2-BCART (4) | 0.99 | 3.5 | 7.97 | 77743 |

| Gamma2-BCART (5) | 0.99 | 2 | 9.97 | 77849 |

| Weib1-BCART (3) | 0.99 | 7 | 5.98 | 77911 |

| Weib1-BCART (4) | 0.99 | 5 | 7.98 | 77619 |

| Weib1-BCART (5) | 0.99 | 4 | 9.98 | 77804 |

| Weib2-BCART (3) | 0.99 | 7 | 5.98 | 77893 |

| Weib2-BCART (4) | 0.99 | 5 | 7.98 | 77608 |

| Weib2-BCART (5) | 0.99 | 4 | 9.98 | 77787 |

| CPG-BCART (4) | 0.99 | 10 | 11.96 | 105710 |

| CPG-BCART (5) | 0.99 | 8 | 14.93 | 105626 |

| CPG-BCART (6) | 0.99 | 7 | 17.92 | 105643 |

| ZICPG1-BCART (4) | 0.99 | 11 | 15.97 | 102314 |

| ZICPG1-BCART (5) | 0.99 | 10 | 19.95 | 102198 |

| ZICPG1-BCART (6) | 0.99 | 7.5 | 23.92 | 102225 |

| ZICPG2-BCART (4) | 0.99 | 12 | 15.95 | 102265 |

| ZICPG2-BCART (5) | 0.99 | 11 | 19.94 | 102134 |

| ZICPG2-BCART (6) | 0.99 | 8 | 23.92 | 102167 |

| ZICPG3-BCART (4) | 0.99 | 14 | 15.94 | 102247 |

| ZICPG3-BCART (5) | 0.99 | 12 | 19.93 | 102120 |

| ZICPG3-BCART (6) | 0.99 | 9 | 23.90 | 102158 |

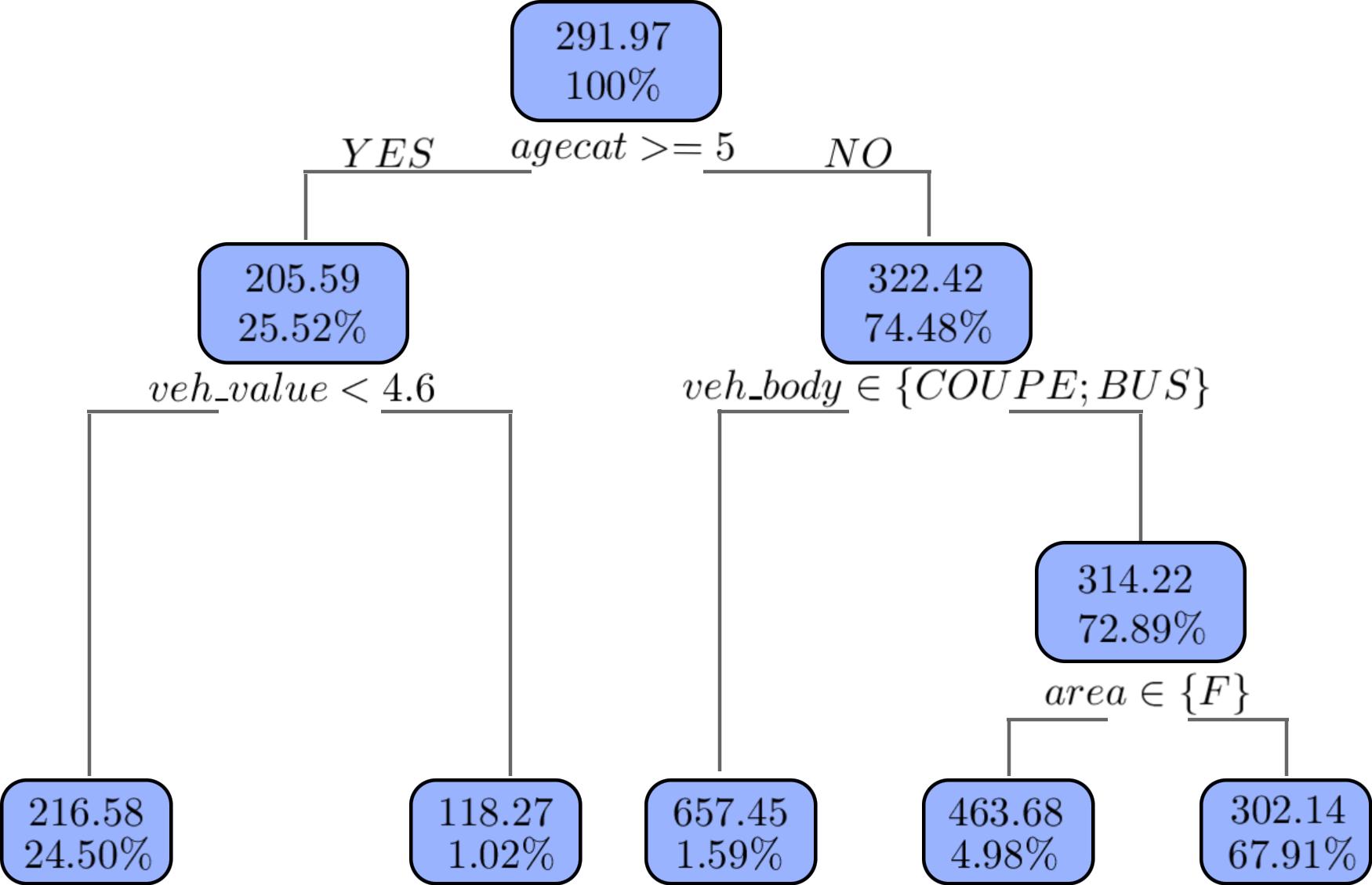

We again examine the splitting rules used in the selected trees. All models use the same splitting variables (“agecat”, “veh_value”, “veh_body”, and “area”), but the order of use and the tree structures vary. Notably, “agecat” is consistently the first variable. Among them, ZICPG3-BCART demonstrates the ability to identify a riskier group (i.e., the one with an estimated pure premium equal to 657.45; see Figure 7), possibly due to the same reason as discussed in [24] for the outstanding performance of ZIP2-BCART for claim frequency. Besides, we observe that the tree structure of ZICPG3-BCART is quite similar to ZIP2-BCART. However, ZICPG3-BCART identifies another important variable “area”, which was recognized as important for average severity before (see Section 5.1). We also fit a CPG-GLM to the data. We find that only the variable “agecat” is significant, aligning with its consistent selection as the first splitting variable in almost all the BCART models. It is also worth mentioning that CART is not included in this analysis due to the absence of R packages that can directly use CPG \zzz(or ZICPG) to process the data.

The performance of the selected trees for the test data is given in Table 17. As before, GLM exhibits poorer performance compared to tree models, as evidenced by RSS(). \zzzWe discuss the three types of aggregate claim models from various perspectives. The meaning of the abbreviations can be found in the captions of Tables 16–17.

| Model | RSS () | \zzzSE | \zzzDS | \zzzLift |

| CPG-GLM | 1.5187 | - | - | - |

| -BCART (5/4) | 1.4874 | 242.12 | 8.32 | 2.532 |

| -BCART (5/4) | 1.4813 | 238.14 | 8.19 | 2.538 |

| -BCART (5/4) | 1.4798 | 237.29 | 8.16 | 2.540 |

| -BCART (5/4) | 1.4844 | 240.89 | 8.27 | 2.534 |

| -BCART (5/4) | 1.4790 | 237.01 | 8.14 | 2.541 |

| -BCART (5/4) | 1.4779 | 236.45 | 8.09 | 2.544 |

| CPG-BCART (4) | 1.4791 | 237.42 | 8.15 | 2.542 |

| CPG-BCART (5) | 1.4781 | 235.98 | 7.93 | 2.547 |

| CPG-BCART (6) | 1.4778 | 236.29 | 8.02 | 2.549 |

| ZICPG1-BCART (4) | 1.4670 | 232.87 | 7.85 | 2.560 |

| ZICPG1-BCART (5) | 1.4497 | 229.73 | 7.56 | 2.584 |

| ZICPG1-BCART (6) | 1.4478 | 231.35 | 7.79 | 2.587 |

| ZICPG2-BCART (4) | 1.4612 | 232.15 | 7.81 | 2.563 |

| ZICPG2-BCART (5) | 1.4434 | 229.41 | 7.52 | 2.595 |

| ZICPG2-BCART (6) | 1.4417 | 231.10 | 7.77 | 2.597 |

| ZICPG3-BCART (4) | 1.4598 | 231.24 | 7.79 | 2.570 |

| ZICPG3-BCART (5) | 1.4415 | 228.88 | 7.45 | 2.601 |

| ZICPG3-BCART (6) | 1.4409 | 229.53 | 7.69 | 2.604 |

-

1.

A comparison of our frequency-severity models suggests using the combination of two best models for \zzzclaim frequency and average severity respectively \zzzbased on all evaluation metrics, i.e., -BCART -BCART. In the sequential models, the same conclusion as in Section 4.1 is reached: using the \zzzestimate of the claim count is superior to using itself when treating them as a covariate in the average severity tree. Regarding joint models, ZICPG models outperform the CPG model, with ZICPG3-BCART being the best.

-

2.

When comparing frequency-severity models and sequential models, it is evident that adding (or ) as a covariate improves performance, \zzzas shown by all evaluation metrics, i.e., -BCART -BCART -BCART. The same ranking is observed for another combination, i.e., -BCART -BCART -BCART. This is reasonable, as real data often \zzzexhibit a \zzznegative conditional correlation between the number of \zzzclaims and average severity, favouring sequential models that consider this correlation over frequency-severity models assuming independence.

-

3.

In comparing frequency-severity models and joint models, \zzzall evaluation metrics indicate that the \zzzoptimal CPG-BCART (or ZICPG-BCART) \zzzchosen by DIC consistently outperforms \zzzfrequency-severity models, suggesting that sharing information is beneficial for this dataset, i.e., one joint tree exhibits better performance. Exploration of the reasons is provided below.

-

4.