Undominated monopoly regulation††thanks: We are grateful to Dirk Bergemann, Sushil Bikhchandani, Rahul Deb, Yingni Guo, Mallesh Pai, Alessandro Pavan, Jeevant Rampal, Bruno Strulovici, and Vilok Taori for helpful discussions. We thank seminar participants at Ashoka University, Higher School of Economics at St. Petersburg, University of Liverpool, Conference on Mechanisms and Institution Design in Budapest, and Meeting of the Society for Social Choice and Welfare in Paris for their comments.

Abstract

We study undominated mechanisms with transfers for regulating a monopolist who privately observes the marginal cost of production. We show that in any undominated mechanism, there is a quantity floor, which depends only on the primitives, and the regulator’s operation decision is stochastic only if the monopolist produces at the quantity floor. We provide a near-complete characterization of the set of undominated mechanisms and use it to (a) provide a foundation for deterministic mechanisms, (b) show that the efficient mechanism is dominated, and (c) derive a max-min optimal regulatory mechanism.

Keywords: regulation, undominated mechanisms, floor randomized mechanisms, downward distortion.

JEL Classification: D82, L51

1 Introduction

We consider the problem of regulating a monopolist who privately observes the marginal cost of production. The regulator’s payoff is a weighted sum of the consumer surplus and the monopolist’s profit, with a strictly smaller weight on the monopolist’s profit. Given such preferences, the regulator would like to maximize the consumer surplus irrespective of the cost (type) of the monopolist. However, incentive constraints imply that increasing consumer surplus at a given type reduces the consumer surplus at lower types. A seminal paper, Baron and Myerson (1982), studies the optimal resolution of this trade-off when the regulator uses transfers and maximizes the expected payoff with respect to a prior over the space of plausible marginal costs. Most of the subsequent literature, both with and without transfers, assumed expected payoff maximization by the regulator subject to incentive (IC) and participation (IR) constraints of the monopolist (see Armstrong and Sappington (2006) for an extensive survey).

This paper takes the first step in understanding the prior-free criterion of undomination in the context of regulatory mechanisms. A regulatory mechanism must specify an operation decision, which may be stochastic; a quantity decision, which is contingent on the monopolist operating; and a transfer decision on the amount of subsidy/tax to the monopolist, which is also contingent on the monopolist operating. A regulatory mechanism is undominated if no other mechanism gives the regulator a strictly higher payoff at some marginal cost of the monopolist without lowering the regulator’s payoff at other costs. Such prior-free undominated mechanisms are relevant particularly when the regulator lacks confidence in the belief over the plausible marginal costs or fears ex-post criticism of the subjective belief used while choosing the regulatory mechanism. The concept of undomination is also useful for refining the set of worst-case optimal mechanisms when it is not a singleton.

Our first main result shows that an undominated regulatory mechanism must be a floor randomized mechanism. A floor randomized mechanism is defined by partitioning the type space into three disjoint intervals (with the possibility that some of these intervals may be empty) and a quantity floor , which we define precisely later. In the first interval (containing the low-cost types), the (monopolist) firm operates for sure and produces quantity higher than the quantity floor . In the second interval, with intermediate-cost types, the firm operates with positive probability (possibly less than one) and produces quantity . The firm is shut in the third interval, which contains high-cost types. Thus, the operation decision is stochastic only at the quantity floor .

A general incentive compatible (IC) and individually rational (IR) mechanism is characterized by the monotonicity of the product of quantity and operation probability, and an envelope formula specifying the transfer. On the other hand, floor randomized mechanisms (which are IC and IR) have several structural properties that make them easier to handle: (i) whenever the monopolist is allowed to operate, the quantity produced is bounded below by ; (ii) operation decision is stochastic only when the quantity produced equals ; (iii) both quantity and operation decisions are monotone.

Using these properties of floor randomized mechanisms, we derive two further necessary conditions for undomination. The first condition is what we call downward distortion. It requires that the quantity produced at every type be lower than the efficient quantity at that type. Thus, there is a type-dependent upper bound on the quantity to be produced (the quantity floor is type-independent). The second condition is technical and requires the product of the quantity and the operation decisions to be left continuous. Thus, we show that every undominated mechanism is a floor randomized mechanism satisfying downward distortion and left-continuity. Conversely, every floor randomized mechanism satisfying left-continuity and a stricter version of downward distortion is undominated.222The stricter version of downward distortion requires that the quantity produced at every type must be strictly lower than the efficient quantity at that type. Thus, undomination, despite being a weak criterion, puts significant structure on the set of IC and IR mechanisms.

Our analysis has three critical implications for regulation design. First, we show that for every IC and IR mechanism and for every prior over the marginal costs, there exists a deterministic IC and IR mechanism that generates more expected payoff for the regulator than . This provides a foundation for deterministic mechanisms in our model and explains why the optimal regulatory mechanism in Baron and Myerson (1982) is deterministic. The second implication concerns the efficient mechanism, where the firm always operates and produces efficient quantity (maximizing total surplus). We show that the efficient mechanism is dominated. The third implication is for an ambiguity-averse regulator who evaluates any mechanism by the worst expected payoff it generates over a set of priors. We call the mechanism that gives the highest such worst payoff as max-min optimal mechanism. We establish that if the set of priors contains a prior that (first-order) stochastically dominates every other prior in the set, then the max-min optimal mechanism is the optimal mechanism for that prior.

As an essential step in proving the result on max-min optimal regulatory mechanisms, we show that undominated mechanisms are monotonic. The regulator’s expected payoff increases as the distribution over marginal cost decreases in the first-order sense. In general, an arbitrary IC regulatory mechanism need not be monotonic. This observation contrasts sharply with IC mechanisms for selling a single good. As Hart and Reny (2015) shows, every IC mechanism for selling a single good is monotonic.

The rest of the paper is organized as follows. Section 2 describes the model. In Section 3, we discuss floor randomized mechanisms and show it is without loss to restrict our search of undominated mechanisms in the class of floor randomized mechanisms. Section 4 gives a near-complete characterization of undominated mechanisms. We discuss the implications of our results for regulation design in Section 5. Finally, related literature is discussed in Section 6, and Appendices A-C contain all the proofs.

2 Model

A regulator oversees a market with a unit mass of consumers and a monopolist selling a single product. We begin by describing the market and then discuss the regulatory mechanisms.

2.1 Market

The total cost incurred by the monopolist in producing a quantity of the product is given by . The parameter denotes the fixed cost which is incurred only when . The parameter denotes the marginal cost of production for the monopolist. The monopolist is perfectly informed about its fixed cost and marginal cost.

Let be a strictly decreasing inverse demand function that represents the preferences of the unit mass of consumers. If the monopolist charges a uniform price of , where , exactly units of the product are sold in the market, and the consumers get a total value of

The associated consumer surplus (CS) is given by and the profit of the monopolist is . Finally, the total surplus (TS) is the sum of consumer surplus and profit of the monopolist, i.e.,

If zero units are sold, i.e. , the consumer surplus, monopolist’s profit, and total surplus are all zero.

Throughout the paper, we impose the following assumptions on the primitives. We assume that the marginal cost can take values in the interval , where . Further, satisfies the following conditions.

-

A1.

is continuous and for some .

-

A2.

and are such that .

Assumptions [A1] is a technical assumption on . Assumption [A2] is a joint condition on , and . Intuitively, it says that it is “efficient” to let the type with the highest marginal cost operate in the complete information benchmark.

2.2 Regulatory mechanisms

The regulator perfectly knows the fixed cost of the monopolist and the inverse demand function. However, when it comes to the marginal cost, the regulator only knows that it belongs to .

The regulatory apparatus employed in disciplining the behavior of the monopolist can be summarized through a regulatory mechanism . By revelation principle, we focus on direct regulatory mechanisms in which the monopolist first reports the marginal cost to the regulator, who then enforces two decisions and on the monopolist and transfers a contingent subsidy to the monopolist. More specifically, a regulatory mechanism is given by , where

-

•

Operation decision. The map denotes the probability with which the monopolist is allowed to operate.

-

•

Quantity rule. If the monopolist is allowed to operate, the map prescribes the quantity to be produced by the monopolist.

-

•

Subsidy rule. If the monopolist is allowed to operate, the map represents the subsidy each type of monopolist receives.

Throughout the paper, we focus attention on regulatory mechanisms such that if and only if . This restriction is without loss and will simplify of the exposition.333If , the monopolist is not allowed to operate indicating that value of is inconsequential in determining the regulator’s surplus which will be given by equation (3). Similarly, if , the total cost of production as well as value to consumers are both . Thus, for all values of the regulator gets the same payoff. Given such a regulatory mechanism, , the utility of a type monopolist from truthfully reporting its type is

| (1) |

On the other hand, the corresponding consumer surplus (CS) is

| (2) |

where (2.2) is obtained by substituting from equation (1). Observe, equation (1) uniquely defines the subsidy for given . Thus, it is without loss of generality to write a mechanism as . On the other hand, we denote a deterministic mechanism, i.e., a mechanism where for all , as by suppressing . We follow this convention throughout the paper.

A regulatory mechanism is incentive compatible (IC) if for all

Furthermore, the regulatory mechanism is individually rational (IR) if for all . We now state a lemma establishing the exact connection between incentive compatibility and individual rationality of the mechanism and certain properties of . To do so, fix and let be such that

Then, is called a subgradient of at . Let be the set of all subgradients of at . The following lemma states if is IC, then .

Lemma 1 (Baron and Myerson (1982))

The following are equivalent:

-

1.

is IC.

-

2.

is convex, decreasing, and for all

-

3.

is decreasing and for all

Further, is IR if and only if .

In standard screening problems, a single monotone function characterizes incentive compatibility (for instance, in single-object auctions, it is the increasing allocation rule). By contrast, in our setup, the incentive compatibility is characterized by the product of two potentially non-monotonic functions and . By Lemma 1, this product must decrease in for a mechanism to be IC.

2.3 Regulator’s surplus and undominated mechanisms

If the monopolist is of type , the regulator’s surplus from an IC and IR mechanism is

where is the weight the regulator puts on the monopolist’s profit. We can further simplify the regulator’s surplus using equation (2.2) to

| (3) | ||||

| (4) |

Thus, the regulator’s surplus can be separated into two parts: the total surplus, which is independent of , and the weighted disutility from the rent paid to the monopolist. The regulator is concerned about total surplus as well as how the total surplus is distributed across the consumers and the monopolist. As decreases, the distributional concerns of the regulator get stronger. The extreme scenario is when , where the regulator’s surplus equals consumer surplus.444If , the regulator’s surplus reduces to the total surplus. In this case, the regulator is concerned only about efficiency, and it is well known that the efficient quantity is produced in the optimal mechanism.

We now introduce a prior-free notion of comparing two IC and IR mechanisms.

Definition 1

An IC and IR mechanism dominates an IC and IR mechanism if

with strict inequality holding for some . In this case, we say is dominated.

An IC and IR mechanism is undominated if it is not dominated.

In what follows, we aim to characterize the set of undominated mechanisms.

2.4 Remarks on the model

Some remarks are in order about the modelling of regulatory mechanisms. First, it appears that the regulatory mechanism only controls quantity, and price is determined from inverse demand function. However, we can recast the mechanism to control price, and quantity can be determined by the demand function (as is done in Armstrong and Sappington (2004)).

Second, our regulatory mechanisms use transfers. These transfers come from the consumers and go to the firm (if they are negative, these are taxes collected from the firm that go to the consumers). Implicitly, we assume a budget-balance constraint for the regulator. This is standard in the literature that follows Baron and Myerson (1982) - for departures, see Laffont and Tirole (1986).

Just like us, Baron and Myerson (1982) assume that the type of the monopolist is a single dimensional parameter that affects the cost in a linear way. However, in their model affects both the fixed cost and the marginal cost: the total cost of producing quantity in their model is for a monopolist with type . Thus, setting , we get our model. Similar to Amador and Bagwell (2022), this simplification allows us to convey the intuition for our results transparently.

3 Floor randomized mechanisms

This section introduces a subclass of IC and IR mechanisms called floor randomized mechanisms. Every IC and IR mechanism can be transformed into a unique floor randomized mechanism. Our main result will show that converting an arbitrary mechanism to a floor randomized mechanism improves the regulator’s surplus at every type.

As an essential step in defining a floor randomized mechanism, we first describe the quantity floor, , which is the unique solution to the following equation:

The LHS is the consumer surplus when the monopolist produces quantity in absence of any regulation. The equation solves for quantity where this consumer surplus equals fixed cost. To see that a unique positive solution exists, note that is a strictly increasing function with equals zero and , where the latter inequality follows from Assumption [A2].

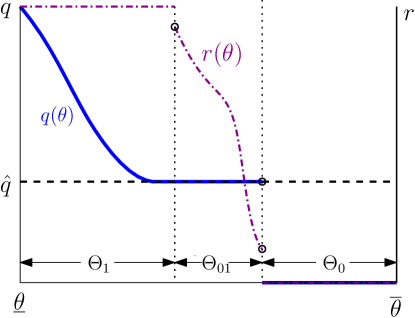

Next, we define a floor randomized mechanism where we use the notation for any pair of disjoint intervals to mean for every and every .

Definition 2

An IC and IR mechanism is floor randomized if and the type space can be partitioned into three disjoint intervals such that and

Figure 1 plots (solid line) and (dash-dotted line) on the vertical axes and illustrates the interval partitioning of the type space in a floor randomized mechanism. It also sheds light on several other features of a floor randomized mechanism:

-

•

quantity floor: whenever the monopolist is allowed to operate with a positive probability, it produces a quantity weakly above . Thus, if is empty, a deterministic mechanism with quantity-floor is floor randomized.

-

•

floor randomization: if the operation decision is random for some type of the monopolist, this type is prescribed quantity equals the floor .

-

•

individual monotonicity: in a floor randomized mechanism both and are decreasing.

Starting with an arbitrary IC and IR mechanisms , which need not be floor randomized, we can obtain a floor randomized mechanism as follows: Let , which decreases in because is IC, and define

At every , we have equals . Consequently, the mechanism , where , is incentive compatible and individually rational with . Moreover, it is also floor randomized with and . Notice that is true when . Our first main result shows that the transformed mechanism improves the regulator’s surplus at every type. Formally,

Theorem 1

Any IC and IR mechanism that is not floor randomized is dominated by a floor randomized mechanism.

Thus, the set of undominated mechanisms is a subset of the set of floor randomized mechanisms. The proof of Theorem 1 is in Appendix A. To see the main idea behind this proof, consider a deterministic IC and IR mechanisms in which every type is allowed to operate and produces a strictly positive quantity . Furthermore, assume that . Clearly, is not floor randomized. In its floor randomized transformation, , every type is allowed to operate with probability and produces a quantity . We now argue that moving from deterministic operation to stochastic operation can make the regulator better off at every . To see why, consider the difference

where . If was a concave function, then Jensen’s inequality would have implied that the difference is negative. However, is not concave because of the discontinuity at . Figure 2 plots , and pictorially depicts both the terms in the difference. As can be seen, the expected value of is denoted by the (). On the other hand, the value of is denoted by (), and lies at a lower level. Thus, randomization is valuable to the regulator for quantities as it reduces the occurrence of the fixed cost and simultaneously increases the value to the consumers relative to a deterministic mechanism.

4 Undominated mechanisms

In this section, we provide a near-complete characterization of undominated mechanisms, and show that not every floor randomized mechanism is undominated. We begin by introducing a new deterministic IC and IR mechanism , where and

Thus, the efficient quantity rule assigns every marginal cost the quantity that maximizes . Because is strictly decreasing is single valued, positive, and strictly decreasing.555At a given , is the unique maximizer of the total surplus because it is the only quantity satisfying the first-order condition and . To see why the latter inequality holds, observe where the first inequality follows from being strictly decreasing and the last one holds because of assumption [A2]. Moreover, continuity and monotonicity of (assumption [A1]) ensures that is continuous. The next observation compares to the quantity floor .

Observation 1

For every , we have .

This observation, which is proven in Appendix B, states that the quantity floor is strictly below the efficient quantity for every type. We further partition the set of floor randomized mechanisms based on whether or not the quantity produced is weakly below the efficient quantity at all types.

Definition 3

A mechanism satisfies downward distortion (DD) if

with an equality at . If the inequality is strict for every , then we say that mechanism satisfies strict downward distortion (strict DD).

As we establish later in this section, the quantity rule of every undominated mechanism will satisfy DD. In addition, undominated mechanisms must also be left continuous.

Definition 4

A mechanism is left continuous if the product is left continuous.

Our next main results shows that undominated mechanisms satisfy downward distortion and left-continuity.

Theorem 2

Suppose is an IC and IR mechanism. Then, the following statements are true:

-

1.

If is undominated, then it is floor randomized, left continuous, and satisfies DD.

-

2.

If is dominated, then it is dominated by a floor randomized and left-continuous mechanism satisfying DD.

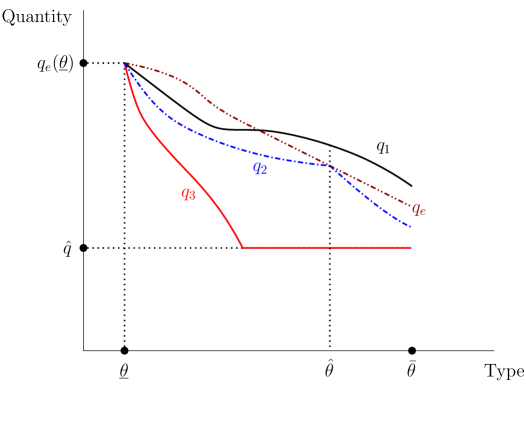

Figure 3 plots quantity rules , and for three floor randomized mechanisms in which the monopolist always operates. The mechanism corresponding to the quantity rule violates DD, and by part (1) of Theorem 2, it is dominated. To see the intuition, consider another floor randomized mechanism where . For , which is shown in the figure, the total surplus is strictly larger under because . On the other hand, the rent paid to the monopolist is smaller because for all . The proof in the Appendix B generalizes this intuition beyond deterministic floor randomized mechanisms. Moreover, it shows why left-continuity is also necessary.

Next, we show that strict DD, a stronger version of DD, and the remaining necessary conditions imply undomination.

Theorem 3

If a mechanism is floor randomized, left continuous, and satisfies strict DD, then it is undominated.

In Figure 3, the quantity rule satisfies DD but violates strict DD. Hence, Theorem 3 is silent whether the mechanism corresponding to is dominated or not. On the other hand the quantity rule satisfies strict DD and is left continuous. Hence, the corresponding floor randomized mechanism is undominated.

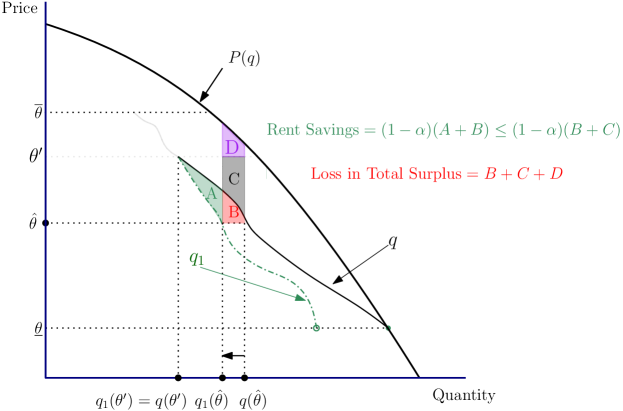

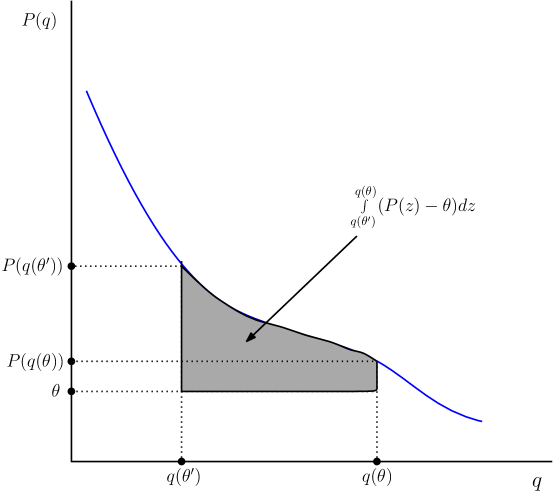

The proof of Theorem 3 is in Appendix B. Here, we discuss the role of strict DD in the proof. Consider a quantity rule , which satisfies strict DD and corresponds to a deterministic floor randomized mechanism . Such a is depicted in the Figure 4. The price-axis also plots the types, whereas the horizontal axis plots quantity. To show that is undominated, it must be that that any other mechanism cannot improve the regulator’s surplus at some type without lowering it at other types. In particular, the quantity rule , which is obtained by lowering at some types, should not be able to improve the regulator’s surplus at . The rent saving corresponding to is given by . Whereas the corresponding loss in the total surplus is given by . The strict DD ensures that , and therefore, even if and area equals area , the rent saving is always strictly smaller than the loss in the total surplus.666Observe, in the context of shown in Figure 4, we always have . This is because is the area of a triangular region that has the same base and same height as the rectangle with area . Thus, can never dominate .

5 Implications for regulation

This section delves into the implications of our findings for regulatory design. First, it discusses why deterministic regulatory mechanisms are focal and identifies properties of optimal mechanisms (expected regulator surplus maximizing mechanism for a given prior) invariant to the details of the regulator’s prior. Then, it discusses the efficient mechanism. Finally, it identifies the max-min optimal mechanism for a regulator who entertains a set of priors over the marginal costs.

5.1 Deterministic regulatory mechanisms

In this section, we use the properties of undominated mechanisms stated in Theorem 1 and 2 to establish that focusing attention on deterministic mechanisms is without loss of generality in a certain sense. For every IC and IR mechanism and a prior over , define

We show the following.

Proposition 1

For every IC and IR mechanism and every prior over , there exists a deterministic mechanism such that

To prove this, fix an IC and IR mechanism and a prior . First, either is undominated or by Theorem 2, there exists a mechanism that dominates and is floor randomized. By Theorem 1, if is undominated, it is also floor randomized. Hence, we conclude that there exists a floor randomized mechanism (where may be same as ) such that

| (5) |

Now, let . Let be the set of all floor randomized mechanisms for the quantity rule :

Clearly, is non empty because it contains . In fact, it contains multiple elements when over an interval of s. Observe that is a convex and compact set: if and are two mechanisms in , their convex combination gives another floor randomized mechanism. Hence, by Krien-Milman theorem, the set is convex hull of its extreme points, where we define an extreme point as follows.

Definition 5

A mechanism is an extreme point if there does not exist two other mechanisms such that for some

The next lemma shows that every extreme point of is a deterministic mechanism.

Lemma 2

Every extreme point of is deterministic.

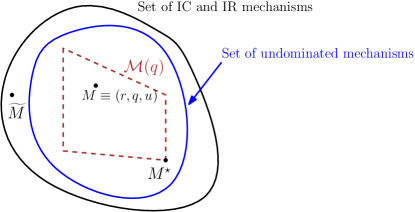

The proof of the above Lemma is similar to the proof of Lemma 4 in Manelli and Vincent (2007) and is given in Appendix C.777Lemma 4 in Manelli and Vincent (2007) shows that in a model where a seller is selling a single object to a single buyer, the extreme points of the set of IC mechanisms are deterministic mechanisms. In our model, this is not enough to guarantee the centrality of deterministic mechanism. Further, neither the set of undominated mechanisms nor the set of floor randomized mechanisms form a convex set. However, fixing a floor randomized mechanism , the set is convex. It shows that any mechanism involving randomization, that is for some , can be written as a convex combination of two mechanisms in the set .

Thus, any objective function that is linear in both and will attain its maximum at a deterministic mechanism. In particular, fixing , consider the following objective function, which is linear in .

As a result, Lemma 2 implies that a maximum over all can be achieved at a deterministic mechanism . Hence, there exists a deterministic mechanism such that

where we used the fact that . Using (5), we get the desired inequality of Proposition 1. The pictorial depiction of the discussion so far is given in Figure 5.

An important implication of Proposition 1 concerns optimal regulation design for a given prior. We say a mechanism is optimal for a prior over if for every IC and IR mechanism ,

We say has a quantity floor is whenever .

Corollary 1

For every prior over , there always exists a deterministic optimal mechanism for the prior that satisfies DD and has quantity floor.

The corollary follows from Proposition 1, which implies it is without loss of generality to focus attention on deterministic undominated mechanisms while searching for the optimal mechanism. The result follows because every undominated mechanism satisfies DD and has a quantity floor. Corollary 1 identifies properties of optimal mechanisms that are invariant to the regulator’s prior. Moreover, it does not require any assumptions on the regulator’s prior, and therefore, generalizes a finding of Baron and Myerson (1982), which states that for any distribution that admits positive density, the optimal mechanism is deterministic.

5.2 Efficient mechanism is dominated

Let be a deterministic IC and IR mechanism in which each type produces quantity and . We call the efficient mechanism. Clearly, the efficient mechanism is floor randomized because it is deterministic and for all (Observation 1). Moreover, it is continuous, and satisfies DD. However, it violates strict DD, and therefore, Theorem 3 is silent on whether is undominated. The next result shows that is dominated, no matter what is, when is twice continuously differentiable.

Theorem 4

If is twice continuously differentiable, then the efficient mechanism is dominated.

Theorem 4 highlights the limits of our necessary (Theorem 2) and sufficient (Theorem 3) conditions in identifying undominated mechanisms. It exhibits that some mechanisms satisfy the necessary conditions and are still dominated.888It is possible to strengthen Theorem 4 further. Call a mechanism partially efficient if the associated quantity rule equals the efficient quantity rule for some interval of types. The proof of Theorem 4 can be adapted to show that every partially efficient mechanism is dominated.

It is worth noting that if , equation (4) implies that the regulator’s surplus at type in a mechanism is , which is uniquely maximized at with . Therefore, is an undominated mechanism.999There are other undominated mechanisms. All of them have the same quantity rule , but differ from only in the value of . Because the regulator’s surplus does not depend on the value of , any positive value for ensures IR and defines a different undominated mechanism.

5.3 Max-min optimal mechanism

While the optimal mechanism design in Baron and Myerson (1982) fixes a prior and derives an optimal mechanism, the regulator may be ambiguity averse. To model this, let denote the set of all probability distributions over . We assume that the regulator considers probability distributions in a set to be plausible. Suppose there exists such that for every , where is the first-order stochastic domination relation. For example, if , this assumption is automatically satisfied with being the distribution that puts all the probability mass at . We solve for the max-min optimal mechanism for , where

Definition 6

An IC and IR mechanism is max-min optimal for if for every IC and IR mechanism

Proposition 2

The optimal mechanism for prior is max-min optimal for .

If we further assume that admits a continuous and positive density, then the optimal mechanism for is the Baron and Myerson (1982) optimal mechanism. Consequently, max-min optimal mechanism is the Baron and Myerson (1982) optimal mechanism for .

The proof of Proposition 2, which is given in Appendix C, is based on the following lemma, which is of independent interest. It shows that for any floor randomized mechanism satisfying DD, the expected regulator’s surplus for prior is higher than that for prior , where . This lemma leverages the unique feature of floor randomized mechanisms that operation decisions are monotone functions.

Lemma 3

If is a floor randomized mechanism that satisfies DD, then for all such that ,

The proof of Lemma 3 is in Appendix C. If we treat a distribution in as a “technology”, then has the interpretation that is a better technology than (because puts more probability mass on lower marginal costs). A consequence of Lemma 3 is that as the technology gets better the regulator’s expected surplus improves from a floor randomized mechanism satisfying DD.

6 Related literature

There is an extensive theoretical literature on mechanism design approach to regulation. Armstrong and Sappington (2006) and Armstrong and Sappington (2004) are excellent surveys, where the latter provides a unified treatment of various results in the literature. We work in the model of Baron and Myerson (1982), which derives the optimal regulatory mechanism for a regulator who does not observe the marginal cost. The optimal regulatory mechanism depends on the prior. In contrast, our analysis is prior-free and seeks to understand undominated mechanisms.

While we, like Baron and Myerson (1982), assume that the inverse demand function is known to the regulator, Lewis and Sappington (1988a) analyzes a model where the regulator observes the cost function of the monopolist but not the inverse demand function. Lewis and Sappington (1988b); Armstrong (1999) analyze optimal regulatory mechanisms when the regulator does not know the cost and inverse demand functions.101010Dana Jr (1993); Armstrong and Rochet (1999) study the multidimensional versions of the problem. Using ideas from the delegation literature, Amador and Bagwell (2022) derives optimal regulatory mechanisms in the single-dimensional case when the regulator cannot use transfers. Yang and Zentefis (2023) show that the optimal regulation for oligopolistic competition is a yardstick price cap mechanism. Also, there are papers that consider the moral hazard aspect of regulation. For instance, Laffont and Tirole (1986) considers a model where the regulator observes the fixed cost and the marginal cost, but the monopolist can put unobservable effort into lowering these costs.

A recent contribution by Guo and Shmaya (2024) analyzes robust regulatory mechanisms in a setup where the regulator does not know the inverse demand function or the monopolist’s cost function. In their paper, the regulator evaluates regulatory mechanisms by their worst-case regret, which is the difference between their complete information and the actual payoffs. They show that a price-cap mechanism is robustly optimal even in a setting where transfers are feasible. Our approach complements their analysis as it is also non-Bayesian but differs in the robustness criterion. Undomination, despite being a very weak robustness criterion, puts significant restrictions like floor randomization and downward distortion on the set of IC and IR mechanisms.

Undominated mechanism design has been studied in other models of mechanism design. For instance, in the multidimensional screening problem (where a monopolist is selling multiple goods to a buyer with multidimensional private values), Manelli and Vincent (2007) consider undominated selling mechanisms for the monopolist and show that they are optimal for some prior distribution over values of the buyer. Unlike us, they do not give necessary and sufficient conditions for a mechanism to be undominated.

For allocating a single object to multiple agents (with quasilinear utility), Sprumont (2013) characterizes undominated mechanisms in the class of strategy-proof, ex-post individually rational, feasible (weak budget-balance), anonymous, and envy-free mechanisms – see similar characterizations in Athanasiou and Valletta (2021) in the context of a public good problem. When selling multiple objects to a set of buyers who demand at most one object, Kazumura et al. (2020) show that a generalization of the Vickrey-Clarke-Groves (VCG) mechanism is the unique undominated mechanism among the class of strategy-proof and ex-post individually rational mechanisms satisfying no-subsidy, no-wastage, and equal treatment of equals.111111The generalization of VCG is necessary because they allow agents to have non-quasilinear preferences. As is apparent, this literature focuses on settings with many agents and characterizes undominated mechanisms under additional constraints than IC and IR. A recent work by Borgers et al. (2024) analyze undominated mechanisms in a single object private values auction model, and shows that any second price auction with a positive reserve price is undominated.

As alluded in the introduction, an arbitrary IC and IR regulatory mechanism need not be monotonic, that is, the expected regulator surplus may reduce even when the distribution over marginal cost gets better as per first-order stochastic dominance relation. However, undominated regulatory mechanisms, as shown by our Lemma 3, are always monotone.121212An example of a dominated mechanism that is not monotone is available upon request. This idea of considering monotone mechanisms (i.e., designer’s payoff increases as the prior distribution over the agent’s valuation gets better) was first introduced in the mechanism design literature by Hart and Reny (2015). They show that deterministic and symmetric IC mechanisms are monotone if the monopolist is selling multiple goods, but every IC mechanism is monotone if the monopolist is selling a single good.

Finally, our result on max-min optimal regulation contributes to the literature on robust mechanism design. This literature is reviewed in Carroll (2019) – also see Carroll (2017) who find a max-min optimal mechanism in the multidimensional screening model. A recent contribution by Bergemann et al. (2023) discusses max-min optimal procurement mechanisms for a government that evaluates a mechanism by the ratio of actual consumer surplus and its value in the complete information benchmark.

Appendix A Proofs of Section 3

Proof of Theorem 1. Let be an IC and IR mechanism, and be its unique floor randomized transformation. Recall, for every , we have . Thus, using the notation , we can write

Because is an IR mechanism, , and therefore,

| (6) |

To complete the proof, it suffices to show that the RHS of inequality (6) is non-negative for all , and it is positive for some . Before we show that, consider the second term on the RHS of inequality (6). If , then , and therefore, the whole term is zero. Thus, this term can be thought of as a convex combination of points on the graph of the function . More formally, if , then

A similar interpretation also applied to the first term on the RHS. Thus, to evaluate the RHS of inequality (6), we need to consider the concave closure of , which is the smallest concave function weakly above .

Observe is strictly increasing and strictly concave for all , where is the unique such that . This is because the derivative of at is which is positive and strictly decreasing. However, has a discontinuity at because and . This means that is not concave. The concave closure of function is denoted by and is given by

Since is such that , it follows that defines the concave envelope of . Thus, is linearly increasing in till . For , is strictly concave and equals . Figure 2 in the main text graphically illustrates .

Pick . If , then the regulator’s surplus is identical under both and . Below, we consider two cases and argue that the RHS of the inequality (6) is non-negative for all .

Case 1. Let be such that . Hence, by definition and . Then,

where the inequality follows from concavity of and . If , then inequality is strict because of the strict concavity of on .

Case 2. Let be such that . Then, and . Moreover,

where the second equality follows from the definition of , the second inequality follows because for all , and the last inequality follows from concavity of and . If , this inequality is strict.

To complete the proof, observe that is not floor randomized, and therefore, we must have at least one where but or and . That is, the RHS of inequality (6) is positive at this .

Appendix B Proofs of Section 4

Proof of Observation 1. Let . Notice that is strictly increasing and continuous in as . Further, by definition of , we have . Now,

where the inequality follows from assumption . By continuity and monotonicity of , we have . This further implies for all because decreases in . Finally, consider

where the last inequality holds because and is strictly decreasing.

Proof of Theorem 2. Suppose is undominated. By Theorem 1, it is floor randomized. Lemma 4 and Lemma 5, which are stated and proved below, establish that a floor randomized mechanism violating DD or left-continuity is dominated. Thus, completing the proof of Part 1.

As for Part 2, consider a dominated IC and IR mechanism , which is not floor randomized. By Theorem 1, is dominated by its floor randomized transformation . We can further use Lemma 4 and Lemma 5 to transform into another floor randomized mechanism that dominates and satisfies DD and left-continuity.

Lemma 4

Proof. Define a new quantity rule as follows

Consider mechanism , where and for all . Moreover,

| (9) |

Both and are decreasing in because is a floor randomized mechanism. Moreover, also decreases in . Thus, as well as decrease in . Monotonicity of in along with equation (9) implies is IC. It is also IR with . To see why

is a floor randomized mechanisms, consider the following two cases.

case 1. Suppose . In this case, for all . Thus, differs from only at , implying that . Furthermore,

case 2. If , then differs from only on a subset of . For every in this subset, , and therefore, . Consequently,

We now argue that mechanism satisfies DD and all the relevant inequalities in the statement of Lemma 4 hold. Observe that for all , and thus, satisfies DD. Moreover, for all with a strict inequality where violates DD. We also have

Thus, to complete the proof it suffice to show that the total surplus under is larger than that under at every . Total surplus is unchanged for if and . For such that or , we have . By definition of , total surplus is higher in than in .

Lemma 5

Suppose is a floor randomized mechanism satisfying DD. Then, there exists another floor randomized mechanism satisfying DD and left-continuity such that

with equality holding for almost all . Moreover, the above inequalities are strict at s where violates left-continuity.

Proof. Because is decreasing, it violates left-continuity at countably many types. Let be the set of such types. We modify and at these types to obtain a new quantity rule and a new operation decision .

By construction, is left continuous at all , and as a result, it is also left continuous at all . Therefore, the IC and IR mechanism , where , is also left continuous. Moreover, is floor randomized and satisfies DD because satisfies both these properties. Below, we argue that dominates .

For mechanism , the regulator’s surplus at any type is

Because differs from on measure zero types, we have for all . Thus, it is enough to show that

Fix . First, suppose that . Then, . However, . Otherwise, will be continuous at , a contradiction. In particular, we have and , and a larger expected total surplus under at . To complete the proof, consider the remaining case where . Because is floor randomized, . Moreover, by construction, either or . Because both and satisfy DD, the increase in quantity or probability of operation increases the expected total surplus at .

Proof of Theorem 3. Suppose is a floor randomized, left-continuous mechanism that satisfies strict DD. By contradiction, assume is dominated by another mechanism . Part (2) of Theorem 2 implies that we can find such that it is floor randomized, left continuous, and satisfies DD. Let

By Lemma 6, has a positive measure. Next, define

is a finite real number because is non-empty and bounded. Clearly, . In what follows, the proof obtains a contradiction by showing that there exists , in a left neighbourhood of , at which the regulator gets a higher surplus under mechanism . To do so, it considers two cases: 1) , and 2) .

Case 1. If , then (since is a floor randomized mechanism). There exists , along with a corresponding left-neighbourhood of , such that

Inequality holds because is decreasing in and left continuous at . As for inequality , it follows from the definition of . Thus, for every , we have and . Furthermore, . To see why, notice that and being floor randomized imply . In both these cases, inequality implies . Now, let

which is a strictly positive. Thus, there exists such that , where . Consider the difference

where inequality follows from . As for equality , it uses the fact that . To reach a contradiction and complete the proof, it suffices to show that the right hand side of the above equation is positive.

| (since for all ) and ) | ||

| (since for all ) | ||

where the last inequality follows from Lemma 1 () and the fact that .

Case 2. Suppose . Then, by Lemma 7, . Because both and are floor randomized, for all . Therefore, it suffices to focus on and , which are left continuous on , for comparing the regulator’s surplus for types below .

There exists a non-empty left-neighbourhood of such that

Inequality holds because of the definition of . Whereas, inequality is guaranteed because ( satisfies strict DD) and is left continuous and decreasing. Let

which is strictly positive. Thus, there exists such that , where . Now, consider the difference

To reach a contradiction and complete the proof, it suffices to show that the right hand side of the above equation is positive.

| (since and ) | |||

| (since for all ) | |||

| (since for all ) | |||

| (since and by definition of ) | |||

where the last inequality follows from .

Lemma 6

The set has a positive measure.

Proof. Both and satisfy DD, and therefore, . Thus, the total surplus from both the mechanisms at is the same. Because dominates , it must be that the rent paid by the monopolist of type is lower in than in , that is,

| (10) |

If the inequality is an equality, for almost all , and by left-continuity of and , for all . Because both and are floor randomized mechanisms, this implies , which is a contradiction. Thus, inequality (10) is strict, and for a positive measure of . Consequently, has a positive measure.

Lemma 7

If , then and .

Proof. For all , we have . Therefore, the rent paid by the monopolist of type is lower in than in , that is . It must be that the expected total surplus is higher in than at :

| (11) |

Otherwise, cannot dominate at , a contradiction. We now use this inequality to show the desired result.

Suppose . In this case, . If , then . Else, . In both these cases, we have . Thus,

Using equation (11), we conclude that and .

Appendix C Proofs of Section 5

Proof of Lemma 2. Let be such that for some . It suffices to show that is not an extreme point of . That is, it is enough to establish that there exists two decreasing functions and , both taking values in , and satisfying

Notice that the above equation, in combination with will then imply , establishing that can be written as convex combination of two mechanism, and , both in .

To do so, consider

It is easy to see that for all . Both and are feasible, that is, they take values in . Finally, both and are decreasing because is decreasing. If for some , then . Therefore, can be written as convex combination of two more decreasing functions.

Proof of Theorem 4. Let . We begin by arguing that there exists an interval on which is either concave or convex. If for all , then any closed interval contained in is the desired interval. Otherwise, for some . By continuity of the second derivative, we can find a closed interval containing where is either concave or convex. Let and .

Because is either concave or convex on , it is differentiable almost everywhere. Let , where for all , be a subgradient of at (it is equal to the derivative of almost everywhere). Then, we can write

In the interval , if is concave then is increasing. On the other hand, if is convex on , then is decreasing. Consider the following quantity rule

where with if is concave and if is convex. First, we assume that is concave on . Step 1 shows that is decreasing, and therefore, , where is an IC and IR mechanism. Step 2 establishes that dominates . Finally, Step 3 considers the case of being convex and highlights changes to Steps 1 and 2.

Step 1. Observe is decreasing on as is decreasing (IC of ). Thus, it suffices to show that is decreasing in the interval . To do so, note that is decreasing and concave, and hence, is decreasing and concave on . As a result, is also decreasing and concave on . Thus, for every , we have , where and is increasing. Moreover, whenever is differentiable in . For any such that , we have

| (12) |

where the first inequality follows since is increasing and the last inequality holds because .

Step 2. Now we show that mechanism dominates mechanism . Since for all , we get . For all , since , we immediately conclude that . For , the reduction in the total surplus is

| (integrating along the price axis) | ||||

| ( is decreasing and ) | ||||

| (by definition of ) | ||||

| (since ) | (13) |

Using increasingness of and the fact that , we get

Substituting this in equation (13), we get

| (14) |

Next, reduction in rent paid at is

Hence, for any , we get

Since , we see that the last expression is positive except for , where it is zero. This establishes that dominates .

Step 3. To complete the proof we consider the case that is convex on . In this case, the proof is similar to the case when is concave. Below, we highlight main changes. First, we choose .

Since and are decreasing and , inequality (12) in Step 1 reduces to

As for Step 2, identical simplifications lead to the counterpart of inequality (14) by using is decreasing

The proof is completed by comparing and .

Proof of Lemma 3. Let be a floor randomized mechanism satisfying DD. It suffices to prove that for all such that ,

Let be such that for all . We first establish , where . Clearly, , and thus, it suffices to show that the first inequality holds. If , we have . If , by Observation 1, . Since , we get .

Henceforth, we assume that and show that with a strict inequality holding if . Both and are decreasing functions because is floor randomized. Further, by Observation 1, total surplus at and are non-negative. Then,

| (since and ) | ||||

| (15) | ||||

Observe that the third integral is always non-negative and it is positive if . Thus, it suffices to show that the first integral is weakly larger than the second. Observe that the first integral can be equivalently written in terms of instead of . Formally,

| (16) |

Figure 6 pictorially depicts this change of variable. Observe by DD and because and are decreasing. Notice that each integral on the right-hand side of (16) is non-negative because and are decreasing.

Now, suppose , then (16) implies

| (17) |

where the second inequality holds because is decreasing. If , we know by DD, , and hence, . This implies that . Again, using equation (16), we get

| (by DD) | |||||

| (since is decreasing) | |||||

| (18) | |||||

Thus, (15) implies that with a strict inequality holding for .

Proof of Proposition 2. We begin by arguing that it is without loss to focus attention on floor randomized mechanisms satisfying DD and left-continuity. To see why, pick any IC and IR mechanism that violates either of these properties. By Theorem 2, there exists a floor randomized mechanism satisfying DD and left-continuity, say , that dominates . Moreover,

where equality holds because of Lemma 3. As for inequality , it holds because dominates . Notice that the set of floor randomized mechanisms satisfying DD and left-continuity is non-empty, and therefore, there exists a max-min optimal mechanism which satisfies these three properties.

To complete the proof, it suffices to argue that , where

| (19) |

is indeed max-min optimal in the set of floor randomized mechanisms satisfying DD and left-continuity. By Lemma 3, infimum occurs at for all such mechanisms. And because of equation (19), mechanism attains the maximum regulator’s surplus among all such mechanisms at .

References

- Amador and Bagwell (2022) Amador, M. and K. Bagwell (2022): “Regulating a monopolist with uncertain costs without transfers,” Theoretical Economics, 17, 1719–1760.

- Armstrong (1999) Armstrong, M. (1999): “Optimal regulation with unknown demand and cost functions,” Journal of Economic Theory, 84, 196–215.

- Armstrong and Rochet (1999) Armstrong, M. and J.-C. Rochet (1999): “Multi-dimensional screening: A user’s guide,” European Economic Review, 43, 959–979.

- Armstrong and Sappington (2004) Armstrong, M. and D. E. Sappington (2004): “Toward a synthesis of models of regulatory policy design with limited information,” Journal of Regulatory Economics, 26, 5–21.

- Armstrong and Sappington (2006) ——— (2006): “Regulation, competition and liberalization,” Journal of Economic Literature, 44, 325–366.

- Athanasiou and Valletta (2021) Athanasiou, E. and G. Valletta (2021): “Undominated mechanisms and the provision of a pure public good in two agent economies,” Social Choice and Welfare, 57, 763–795.

- Baron and Myerson (1982) Baron, D. P. and R. B. Myerson (1982): “Regulating a monopolist with unknown costs,” Econometrica, 50, 911–930.

- Bergemann et al. (2023) Bergemann, D., T. Heumann, and S. Morris (2023): “Cost based nonlinear pricing,” Cowles Foundation for Research in Economics, Yale University.

- Borgers et al. (2024) Borgers, T., J. Li, and W. Kexin (2024): “Undominated mechanisms,” Presented at Conference of Mechansms and Institution Design.

- Carroll (2017) Carroll, G. (2017): “Robustness and separation in multidimensional screening,” Econometrica, 85, 453–488.

- Carroll (2019) ——— (2019): “Robustness in mechanism design and contracting,” Annual Review of Economics, 11, 139–166.

- Dana Jr (1993) Dana Jr, J. D. (1993): “The organization and scope of agents: Regulating multiproduct industries,” Journal of Economic Theory, 59, 288–310.

- Guo and Shmaya (2024) Guo, Y. and E. Shmaya (2024): “Robust monopoly regulation,” Working Paper.

- Hart and Reny (2015) Hart, S. and P. J. Reny (2015): “Maximal revenue with multiple goods: Nonmonotonicity and other observations,” Theoretical Economics, 10, 893–922.

- Kazumura et al. (2020) Kazumura, T., D. Mishra, and S. Serizawa (2020): “Strategy-proof multi-object mechanism design: Ex-post revenue maximization with non-quasilinear preferences,” Journal of Economic Theory, 188, 105036.

- Laffont and Tirole (1986) Laffont, J.-J. and J. Tirole (1986): “Using cost observation to regulate firms,” Journal of Political Economy, 94, 614–641.

- Lewis and Sappington (1988a) Lewis, T. R. and D. E. Sappington (1988a): “Regulating a monopolist with unknown demand,” American Economic Review, 986–998.

- Lewis and Sappington (1988b) ——— (1988b): “Regulating a monopolist with unknown demand and cost functions,” The RAND Journal of Economics, 438–457.

- Manelli and Vincent (2007) Manelli, A. M. and D. R. Vincent (2007): “Multidimensional mechanism design: Revenue maximization and the multiple-good monopoly,” Journal of Economic Theory, 137, 153–185.

- Sprumont (2013) Sprumont, Y. (2013): “Constrained-optimal strategy-proof assignment: Beyond the Groves mechanisms,” Journal of Economic Theory, 148, 1102–1121.

- Yang and Zentefis (2023) Yang, K. H. and A. K. Zentefis (2023): “Regulating oligopolistic competition,” Journal of Economic Theory, 212, 105709.