Joint-perturbation simultaneous pseudo-gradient

Abstract

We study the problem of computing an approximate Nash equilibrium of a game whose strategy space is continuous without access to gradients of the utility function. Such games arise, for example, when players’ strategies are represented by the parameters of a neural network. Lack of access to gradients is common in reinforcement learning settings, where the environment is treated as a black box, as well as equilibrium finding in mechanisms such as auctions, where the mechanism’s payoffs are discontinuous in the players’ actions. To tackle this problem, we turn to zeroth-order optimization techniques that combine pseudo-gradients with equilibrium-finding dynamics. Specifically, we introduce a new technique that requires a number of utility function evaluations per iteration that is constant rather than linear in the number of players. It achieves this by performing a single joint perturbation on all players’ strategies, rather than perturbing each one individually. This yields a dramatic improvement for many-player games, especially when the utility function is expensive to compute in terms of wall time, memory, money, or other resources. We evaluate our approach on various games, including auctions, which have important real-world applications. Our approach yields a significant reduction in the run time required to reach an approximate Nash equilibrium.

1 Introduction

We tackle the problem of computing an approximate Nash equilibrium of a game with a black-box utility function, for which we lack access to gradients. A standard way to learn player strategies for a game is to use simultaneous gradient ascent, in which, at each iteration, each player myopically adjusts its parameters to increase its own utility, treating the other players as fixed. Computing the simultaneous gradient requires taking gradients of the utility function, which are unavailable in the black-box setting. To address this obstruction, one can employ evolution strategies, a family of methods that perturbs parameters and evaluates the function at those perturbed points in order to optimize some objective. This yields an unbiased estimator of the gradient of a smoothed version of the original objective function, also called a pseudo-gradient. Computing the simultaneous pseudo-gradient through the standard approach requires a number of utility function evaluations that is linear in the number of players. Our contribution is to introduce a new method which requires a number of function evaluations that is only constant in the number of players. It performs a joint perturbation on all players’ strategies at once, rather than perturbing each one individually. When utility function evaluation is expensive (in terms of wall time, memory, money, etc.) and the number of players is large, this can yield dramatic benefits for training. We benchmark our approach on several games, including various auctions, showing a significant reduction in training time.

2 Related research

Black-box zeroth-order optimization uses only function evaluations to optimize a black-box function with respect to a set of inputs. In particular, it does not require gradients. There is a class of black-box optimization algorithms called evolution strategies (ES) (Rechenberg and Eigen, 1973; Schwefel, 1977; Rechenberg, 1978; Bäck, 1996; Bäck et al., 1997; Eiben and Smith, 2003). These maintain and evolve a population of parameter vectors. Natural evolution strategies (NES) (Wierstra et al., 2008; Yi et al., 2009; Wierstra et al., 2014) represent the population as a distribution over parameters and maximize its average objective value using the score function estimator. For many parameter distributions, such as Gaussian smoothing, this is equivalent to evaluating the function at randomly-sampled points and estimating the gradient as a sum of estimates of directional derivatives along random directions (Fu et al., 2015; Duchi et al., 2015; Nesterov and Spokoiny, 2017; Shamir, 2017; Berahas et al., 2022).

Li and Wellman (2021) tackle the problem of solving symmetric one-shot Bayesian games with no given analytic structure, high-dimensional type and action spaces, many players, and general-sum payoffs. They represent agent strategies in parametric form as neural networks, and apply NES to optimize them. For pure equilibrium computation, they formulate the problem as bi-level optimization and use NES to implement both inner-loop best response optimization and outer-loop regret minimization. For mixed equilibrium computation, they adopt an incremental strategy generation framework in which NES produces a finite sequence of approximate best-response strategies. They then calculate equilibria over this finite strategy set via a model-based optimization process. Both methods use NES to search for strategies over the functional space of policies, given only black-box simulation access to noisy payoff samples.

To tackle symmetric auctions, Bichler et al. (2021) present a learning method called neural pseudogradient ascent (NPGA) that represents strategies as neural networks and applies policy iteration on the basis of gradient dynamics in self-play to provably learn local equilibria. The method follows the simultaneous gradient of the game and uses a smoothing technique to circumvent discontinuities in the ex post utility functions of auction games. (In auctions, discontinuities arise at the bid value where an arbitrarily small change makes the difference between winning and not winning.) The method converges to a Bayesian Nash equilibrium for a wide variety of symmetric auction games.

Whereas symmetric auction models are widespread in the theoretical literature, in most auction markets in the field, one can observe different classes of bidders having different valuation distributions and strategies. Asymmetry of this sort is almost always an issue in real-world multiobject auctions, in which different bidders are interested in different packages of items. Such environments require a different implementation of NPGA with multiple interacting neural networks having multiple outputs for the different allocations in which the bidders are interested. Bichler et al. (2023b) analyze a wide variety of asymmetric auction models. Their results show that they closely approximate Bayesian Nash equilibria in all models in which the analytical Bayes–Nash equilibrium is known. Additionally, they analyze new and larger environments for which no analytical solution is known and verify that the solution found approximates equilibrium closely.

Bichler et al. (2023a) introduce an algorithmic framework for Bayesian games with continuous type and action spaces, such as auctions. It discretizes the type and action spaces and then learns distributional strategies (Milgrom and Weber, 1985) (a form of mixed strategies for Bayesian games) via online convex optimization, specifically simultaneous online dual averaging (SODA). They show that the equilibrium of the discretized game approximates an equilibrium in the continuous game. Discretization can work well for small games, but does not scale to high-dimensional observation and action spaces.

Martin and Sandholm (2023) study the problem of computing an approximate Nash equilibrium of continuous-action game without access to gradients. They model players’ strategies as artificial neural networks. In particular, they use randomized policy networks to model mixed strategies. These take noise in addition to an observation as input and can flexibly represent arbitrary observation-dependent, continuous-action distributions. Being able to model such mixed strategies is crucial for tackling continuous-action games that lack pure-strategy equilibria. They apply this method to continuous Colonel Blotto games, single-item and multi-item auctions, and a visibility game, showing that it can quickly find a high-quality approximate equilibrium.

3 Formulation

Throughout the paper, we use the following notation. The operator denotes the tensor product. The operator denotes the elementwise a.k.a. Hadamard product. If is a set, is the set of all Borel probability measures on . If is a family indexed by , . If is a probability measure for , is the product measure.

Strategic-form game.

A strategic-form game is a tuple where is a set of players, is a set of strategies for , and is a utility function. A strategy profile is an element of , that is, an assignment of a strategy to each player. The notation denotes excluding . Given a strategy profile, a best response (BR) for a player is a strategy that maximizes its utility given the other players’ strategies. That is, given , a BR for is an element of . A Nash equilibrium (NE) is a strategy profile for which each player’s strategy is a BR to the other players’ strategies. That is, it is an such that for all .

Exploitability.

Given , the BR utility of is , i.e., the highest utility it could attain by unilaterally changing its strategy. Player ’s regret is , which is the highest utility it could gain from unilaterally changing its strategy. The exploitability is defined as . It is non-negative everywhere and zero precisely at NE. Consequently, it is used as a standard measure of “closeness” to NE in the literature (Lanctot et al., 2017; Lockhart et al., 2019; Walton and Lisy, 2021; Timbers et al., 2022). If NE exist, computing them is equivalent to globally minimizing exploitability.

Mixed strategies.

For any game , there exists a mixed-strategy game where and . That is, each player’s strategy is a probability measure over its original strategy set (i.e., a mixed strategy), and its utility is the resulting expected utility in the original game. A mixed-strategy NE is an NE of the mixed-strategy game.111 More generally, one can consider settings where randomness is a limited resource (e.g., only a limited number of random bits are available to the agent) or where the agent can only mix between a limited number of pure strategies (i.e., its mixed strategy must be sparse). Alternatively, its mixed strategy may be restricted to some class of representable distributions, such as an explicit parametric model or implicit density model like a Generative Adversarial Network (Goodfellow et al., 2014, 2020).

Continuous game.

A continuous-action game is a game whose strategy sets are subsets of Euclidean space, e.g., . The following theorems apply to such games. Nash (1950) showed that if each is nonempty and finite, a mixed-strategy NE exists. Glicksberg (1952) showed that if each is nonempty and compact, and each is continuous, a mixed-strategy NE exists. Glicksberg (1952); Fan (1952); Debreu (1952) showed that if each is nonempty, compact, and convex, and each is continuous and quasiconcave in , a pure strategy NE exists. Dasgupta and Maskin (1986) showed that if each is nonempty, compact, convex, and is upper semicontinuous and graph continuous and quasiconcave in , a pure strategy NE exists. They also showed that if each is nonempty, compact, and convex, and is bounded and continuous except on a subset (defined by technical conditions) and weakly lower semicontinuous in , and is upper semicontinuous, a mixed-strategy NE exists. Rosen (1965) proved the uniqueness of a pure NE for continuous-action games under diagonal strict concavity assumptions. Most equilibrium-finding algorithms in the literature target discrete-action games, raising the question of how to compute equilibria for continuous-action games.

4 Method

In order to build up to our method, we first introduce some key concepts in a gradual fashion.

Pseudo-gradient.

Let be a natural number, be a function, be the -dimensional standard normal distribution, be a scalar, and

| (1) |

Assume . Then , where is a Gaussian kernel. It is a property of convolutions that . Therefore, since is smooth (i.e., infinitely differentiable), is also smooth. This holds even if itself is not even continuous. In the literature, is called the pseudo-gradient of . It satisfies the identity

| (2) |

This gives us an unbiased estimator that forms the basis of OpenAI ES (Salimans et al., 2017), a natural evolution strategies method, as described in §2.

Applications.

The pseudo-gradient can be used to perform zeroth-order, i.e. gradient-free, optimization of . This can be useful in cases where straightforward stochastic gradient ascent is not possible or desirable. For example, might not be differentiable. Alternatively, it might have gradients for which unbiased estimators are unavailable or have high variance. The use of pseudo-gradients for optimization has been studied by Duchi et al. (2015); Nesterov and Spokoiny (2017); Shamir (2017); Salimans et al. (2017); Berahas et al. (2022); Metz et al. (2021), among others. It has been shown to be a scalable alternative to classical methods in reinforcement learning (Salimans et al., 2017).

Variance reduction.

We define

| (3) | ||||

| (4) | ||||

| (5) |

as the single-point (SP), forward-difference (FD), and centered-difference (CD) (or antithetic) estimators, respectively. These are all unbiased estimators of the pseudo-gradient. However, the first has a large variance, so the latter two are typically used in practice Berahas et al. (2022). The variance of the pseudo-gradient estimator can be further reduced by taking a mean over many perturbations, as in , where are independent. Other variance reduction techniques are surveyed in Mohamed et al. (2020), among other works.

Pseudo-Jacobian.

We extend the preceding concept of the pseudo-gradient from a scalar-valued function to a vector-valued function. Let , , and

| (6) |

By analogy with the pseudo-gradient, we call the pseudo-Jacobian of . Furthermore, it satisfies the identity

| (7) |

Therefore, we have an unbiased estimator for it.

Simultaneous gradient.

One common approach to game-solving in the literature is simultaneous gradient ascent (SGA), which is defined as follows. Let be a utility function, where is the number of players and is the dimensionality of each player’s strategy parameters. The simultaneous gradient of is the function where . That is, it is the derivative of each parameter with respect to utility of the player that parameter belongs to. Equivalently, , where is the Jacobian of . SGA consists of running the ODE . That is, each player tries to greedily increase their own utility, acting as if the other players are fixed. Explicitly, it uses the iteration scheme for , where is a stepsize.

Mertikopoulos and Zhou (2019) analyze the conditions under which SGA converges to Nash equilibria. They prove that, if the game admits a pseudoconcave potential or if it is monotone, the players’ actions converge to Nash equilibrium, no matter the level of uncertainty affecting the players’ feedback. Bichler et al. (2021) write that most auctions in the literature assume symmetric bidders and symmetric equilibrium bid functions Krishna (2002). This symmetry creates a potential game, and SGA provably converges to a pure local Nash equilibria in finite-dimensional continuous potential games (Mazumdar et al., 2020). Thus in any symmetric and smooth auction game, symmetric gradient ascent with appropriate (square-summable but not summable) step sizes almost surely converges to a local ex-ante approximate Bayes-Nash equilibrium (Bichler et al., 2021, Proposition 1).

Optimistic gradient.

Another approach to game-solving in the literature is optimistic gradient ascent (OGA), which iterates for , where . In the standard version of OGA, . OGA uses the past simultaneous gradient to create an extrapolation or prediction of the future simultaneous gradient , and updates according to this prediction. OGA converges in some games where SGA fails to converge or diverges. OGA has been analyzed by Popov (1980), Daskalakis et al. (2018), and Hsieh et al. (2019), among others.222There are also other learning dynamics in the literature, which are surveyed and analyzed by Balduzzi et al. (2018), Letcher et al. (2019b), Letcher et al. (2019a), Mertikopoulos and Zhou (2019), Mazumdar et al. (2019), Hsieh et al. (2021), and Willi et al. (2022), among others, but these are beyond the scope of this paper.

Simultaneous pseudo-gradient.

Both SGA and OGA, as well as other game-solving approaches in the literature, require computing the simultaneous gradient . However, in some situations, does not exist because is not differentiable. In other situations, is differentiable, but obtaining an unbiased estimator of its gradient is difficult or intractable. This can happen if, for example, is an expectation (with respect to a distribution parameterized by ) of some non-differentiable function. An example of such a situation is an auction, which we will describe in §5.

To resolve this problem, we replace the gradient of in the definition of with a pseudo-gradient. Explicitly,

| (8) |

for each Player , where and is a multivariate standard normal distribution of the same dimension as . In other words, we estimate the pseudo-gradient of (which is a scalar-valued function, since it outputs only the utility of Player ) with respect to the parameters of Player . This is the approach taken by Bichler et al. (2021). It requires one perturbation for each player and subsequent evaluation of . Therefore, the number of utility function evaluations per iteration is linear in the number of players.

Joint perturbation.

Inspired by all of the preceding concepts that have been discussed, we combine (1) the identity , (2) the concept of the pseudo-Jacobian, and (3) the identity to obtain an estimator that requires only a single, joint perturbation across all players. In particular, we notice that

| (9) | ||||

| (10) | ||||

| (11) | ||||

| (12) | ||||

| (13) | ||||

| (14) | ||||

| (15) | ||||

| (16) |

Therefore, we obtain the following unbiased estimator:

| (17) |

In terms of indices, for clarity:

| (18) |

With this new estimator, the number of utility function evaluations per iteration is now constant in the number of players, rather than linear. This dramatically reduces the number of utility function evaluations when there are many players. Therefore, it makes game solving significantly more efficient in many-player games, especially when the utility function is expensive to evaluate in terms of wall time, memory, money, or other resources such as real-world experiments. We can use this simultaneous pseudo-gradient estimator inside schemes like simultaneous gradient ascent, extragradient ascent (Korpelevich, 1976), optimistic gradient ascent (Popov, 1980; Daskalakis et al., 2018), and so on. We call our method joint-perturbation simultaneous pseudo-gradient (JPSPG), in contrast to the classical method, simultaneous pseudo-gradient (SPG).

5 Experiments

We test our approach against the classical approach on several continuous-action games, in particular on many kinds of auction and on continuous Goofspiel (which can be thought of as a kind of auction with budget constraints). Our experimental hyperparameters are as follows. For each experiment, we run 8 trials. In each graph, solid lines show the mean across trials, and bands show the standard error of the mean. The classical method is shown in blue, while our method is shown in orange. We use a stepsize of . For the Gaussian smoothing, we use a perturbation scale of . We use a batch size per iteration of . To update parameters, we use the AdaBelief optimizer (Zhuang et al., 2020). For each player’s strategy network, we use a single hidden layer of size 64, the ReLU activation function, and He initialization (He et al., 2015) for initializing the network’s weights. Each experiment was run individually on one NVIDIA A100 SXM4 40GB GPU.

We estimate the exploitability of the learned strategy profile as follows. First, we compute approximate best responses for each player via reinforcement learning, specifically OpenAI ES (Salimans et al., 2017). For this, we use the same batch size and optimizer as before. The best responses are trained for iterations. Second, as described in Section 3, exploitability is defined as , where is the best-response strategy for player to . We estimate each occurrence of in this expression by averaging over samples of game play.

Next we proceed to presenting the benchmark settings and the performance of the methods on those settings.

5.1 Multi-item unit-demand auction

An auction is a mechanism by which a set of items are sold to a set of bidders, who have valuations for items or sets thereof. Auctions play a central role in the study of markets and are used in a wide range of real-world contexts (Krishna, 2002), such as advertising, commodities, radio spectrum allocation, real estate, and more. To evaluate their method, Bichler et al. (2021) used auctions as a benchmark.

Here, we consider a type of multi-item auction called a unit-demand auction. In this auction, we have bidders and non-identical items. Each bidder has a private valuation for each item . Furthermore, each bidder has unit demand, meaning that its value for a bundle of items is the same as that for the maximum-value item in that bundle: , where is a bundle of items. Housing markets are often given as an example of unit-demand preferences. This model was first studied by Shapley and Shubik (1971). This is a special case of a limited-demand model with units in which each bidder has use for at most units, as described in Krishna (2002, §13.4.2 and §13.5.2). The single-unit case corresponds to .

For our experiment, we use a prior where bidder-item valuations are independently sampled uniformly at random from the unit interval. Each player submits a bid for each item . To allocate items, our auction mechanism assigns items to bidders in a way that maximizes the sum of bids across players. This requires solving a linear assignment problem, which can be described as follows. Given a bid matrix , compute a binary assignment that satisfies the following:

| maximize | (19) | ||||

| subject to | (20) | ||||

| (21) | |||||

| (22) | |||||

That is, maximize the sum of values subject to the constraint that each item is assigned to at most one bidder and each bidder receives at most one item.

The linear assignment problem was first described in a seminal paper by Kuhn (1955), who introduced a solution approach called the Hungarian method. Subsequently, various algorithms have been devised in the literature. We use the modified Jonker-Volgenant algorithm (Jonker and Volgenant, 1988) given in Crouse (2016), as implemented in the Python scientific computing library scipy (Virtanen et al., 2020), and reimplement it in JAX (Bradbury et al., 2018). This algorithm has a time complexity of .

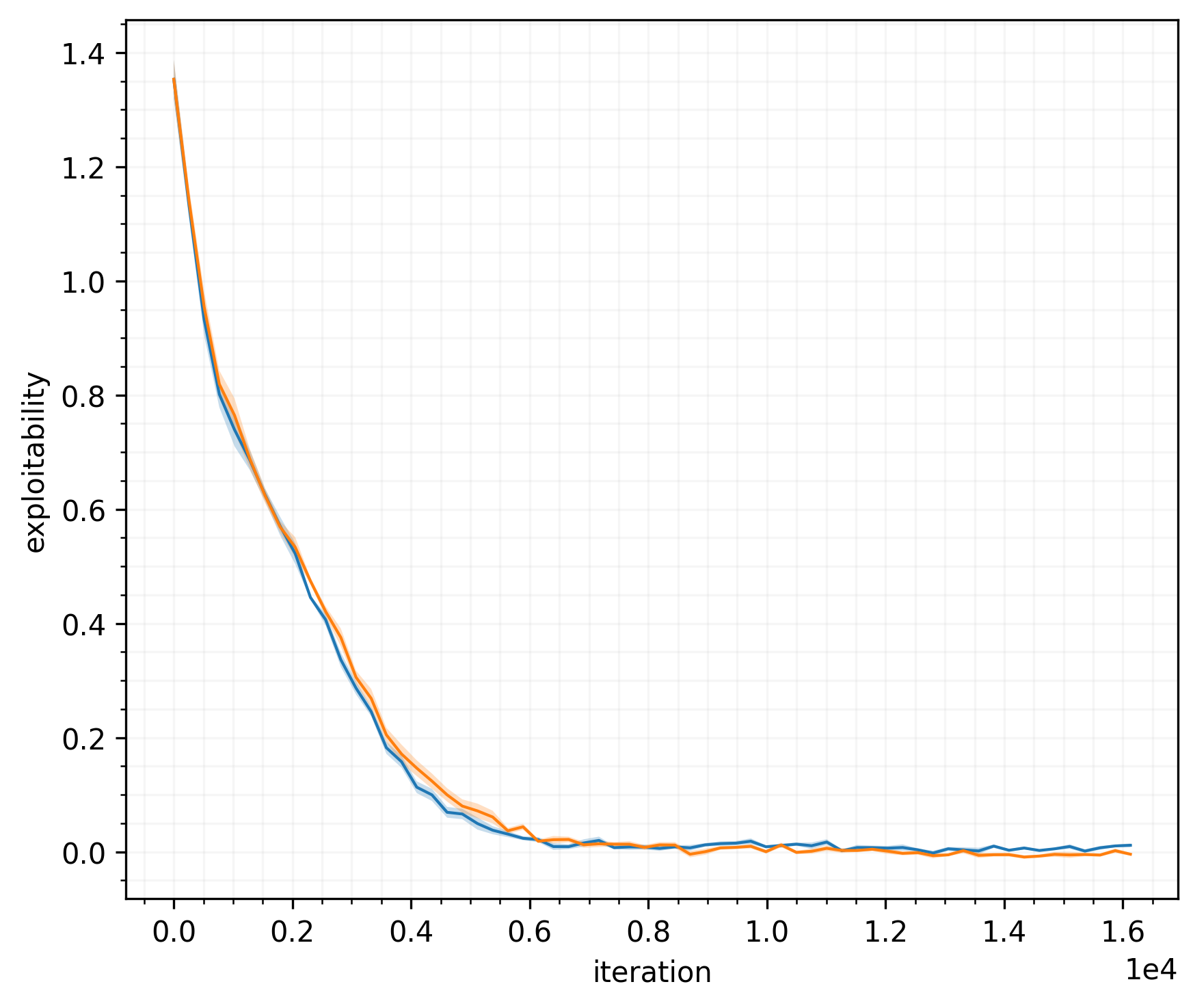

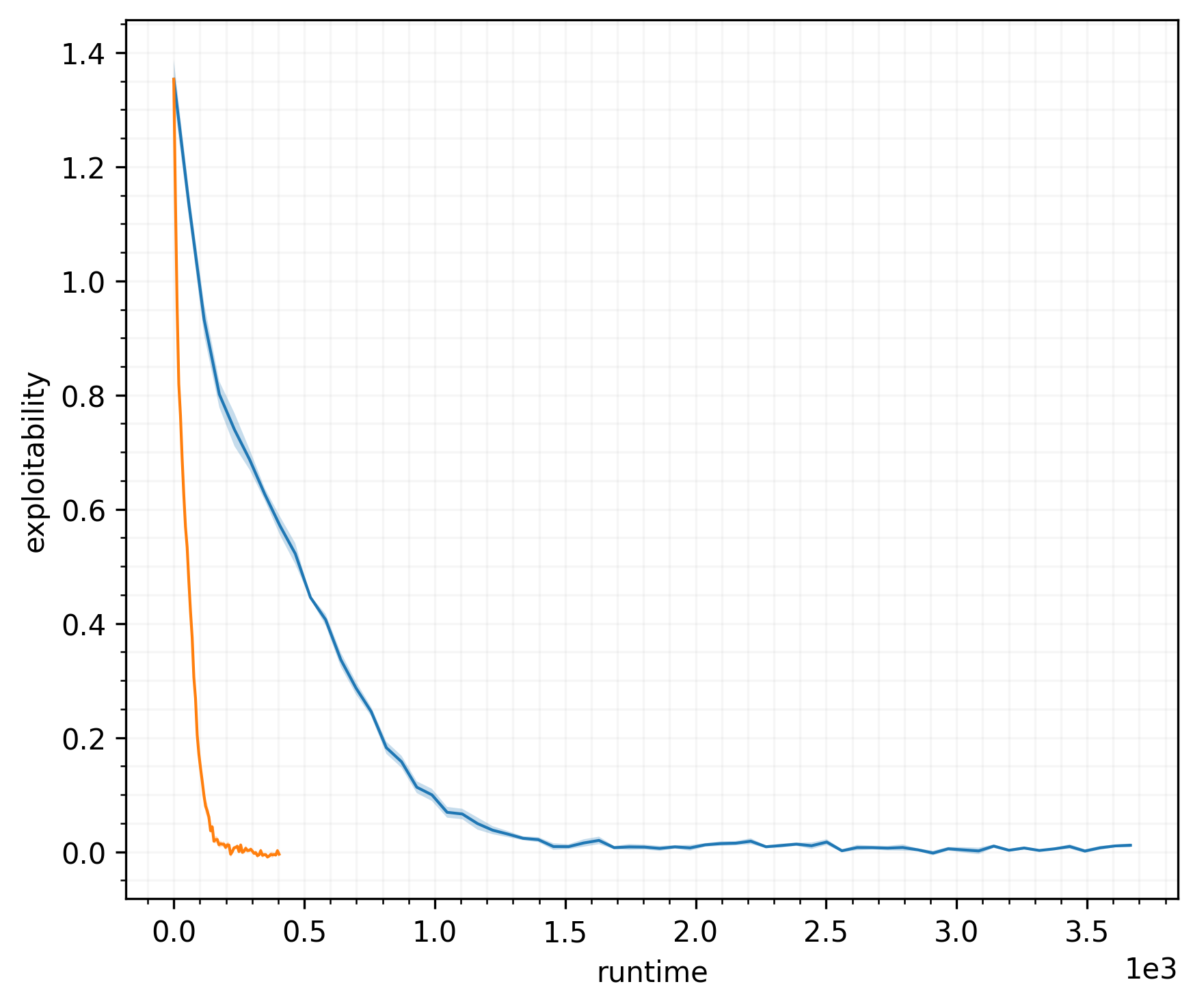

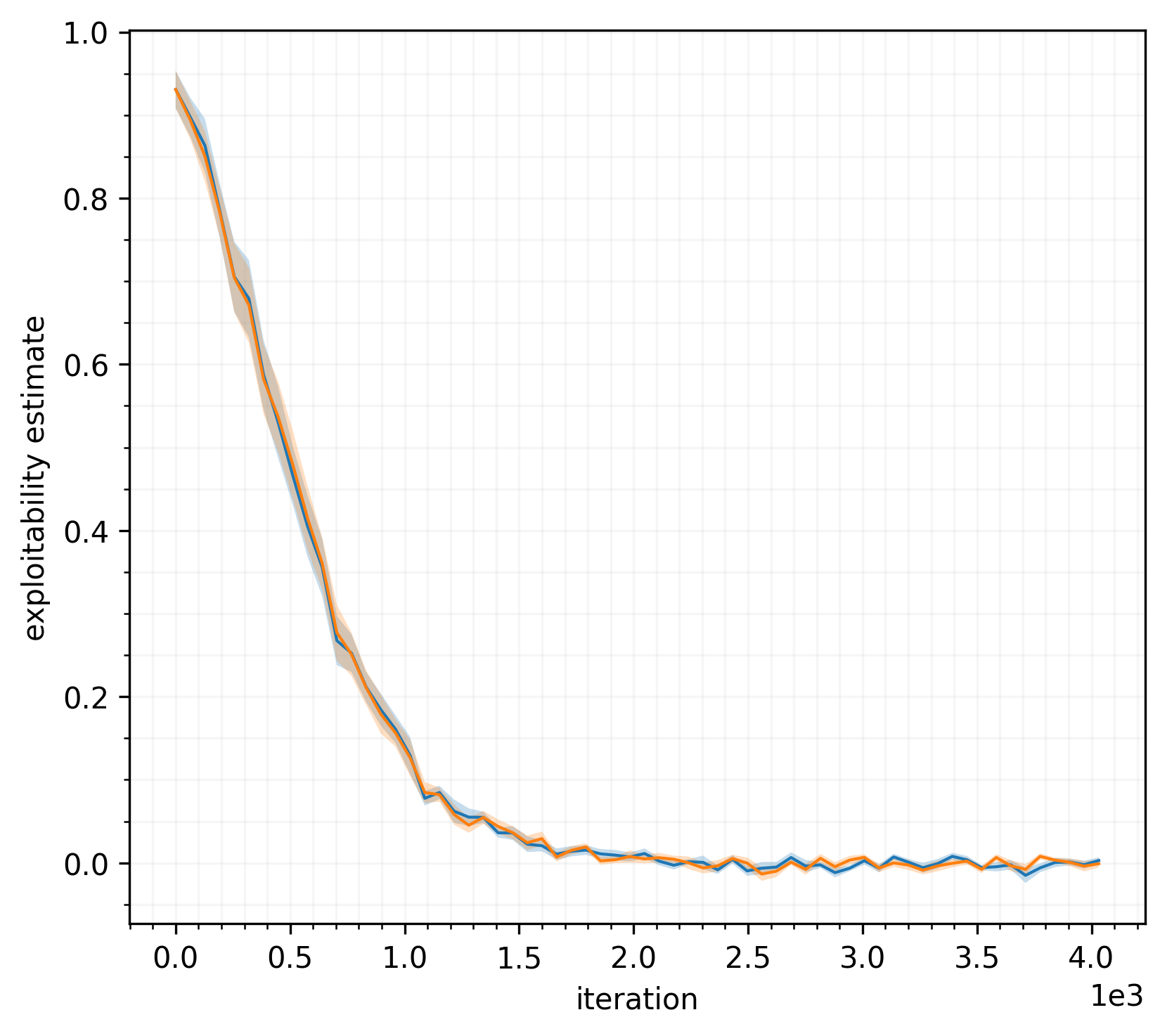

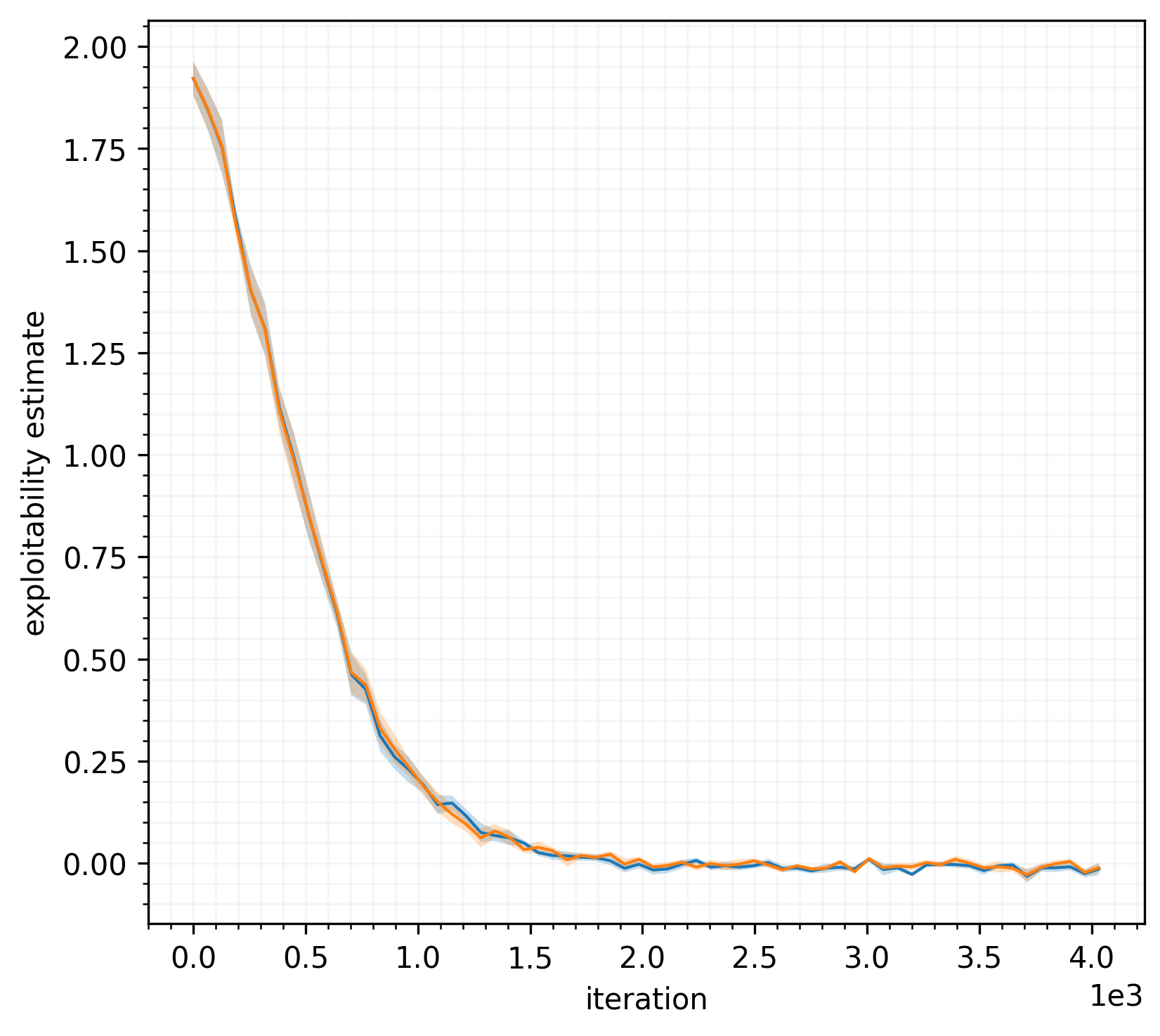

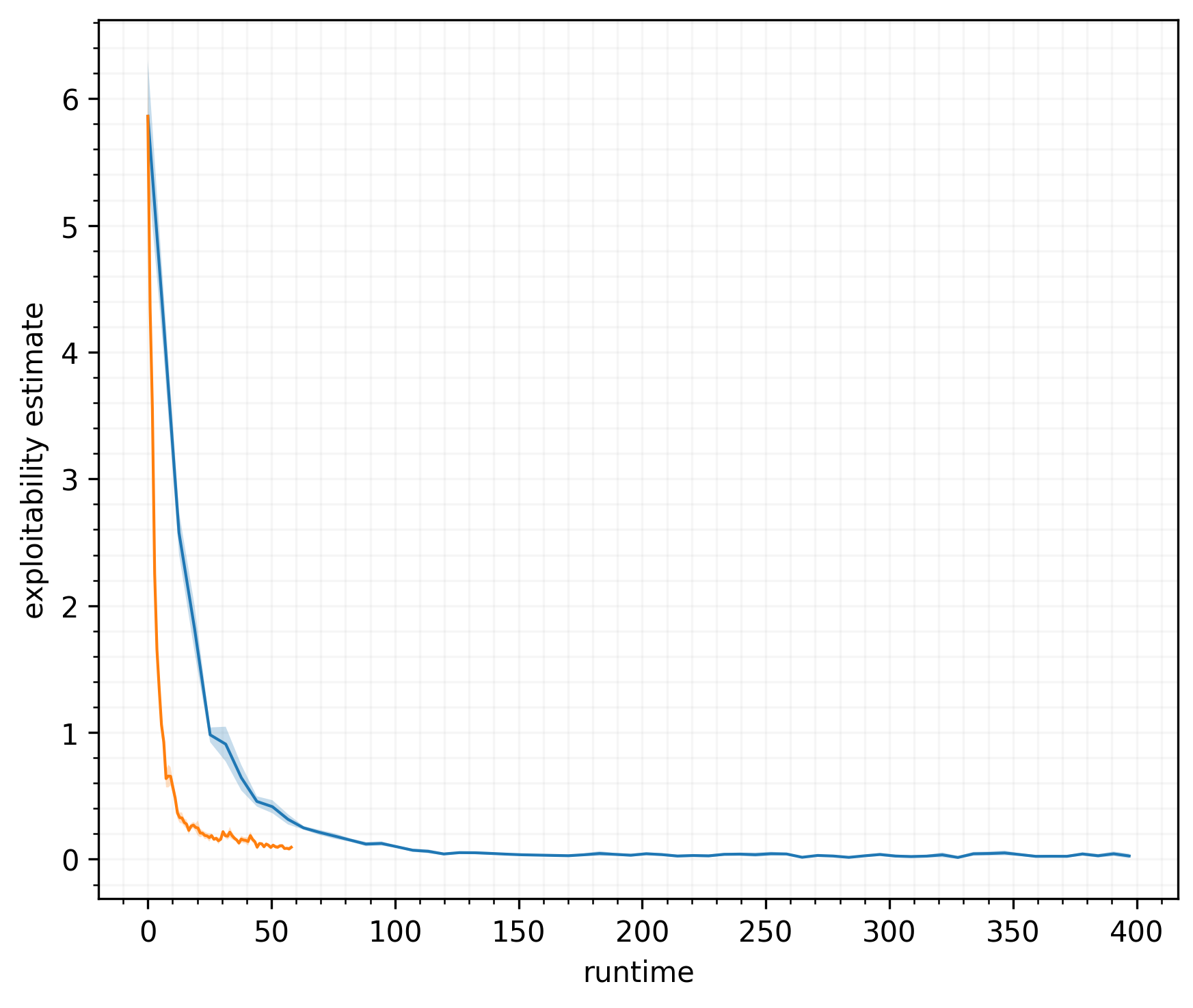

Figures 1 and 2 show the exploitability over the course of training for a 10-player, 10-item unit-demand auction and 20-player, 20-item unit-demand auction, respectively. The figures shows that both our method and the classical method attain a similar exploitability for a given iteration count, but our method is significantly faster in terms of run time (here expressed in seconds). This is to be expected, because the standard method requires evaluations of the utility function per batch instance, each of which requires solving an assignment problem, which is expensive, whereas ours only requires a single utility function evaluation. The advantage of our method increases as the size of the problem instance grows.

5.2 Knapsack auction

Another type of auction is a knapsack auction. We follow the description given in Aggarwal and Hartline (2006). In a knapsack auction, an auctioneer auctions off space in a knapsack of known capacity . Each player seeks to place exactly one object in the knapsack. Player values the placement of its object in the knapsack at . The valuations are private data of each respective player. Each object takes up a certain amount of space in the knapsack. Player ’s object takes space , and these sizes are publicly known. Thus, the s are public while the s are private. Each player submits a bid . Knapsack auctions are also studied in Dütting et al. (2014) and Berg et al. (2010), who model the problem of bidding in ad auctions as a penalized multiple choice knapsack problem.

As Aggarwal and Hartline (2006) note, the knapsack auction problem models several interesting applications. For example, consider running a single auction to sell advertising space on a web page over the course of a day. Suppose statistical information is available for each advertiser as to how many showings (i.e., impressions) are necessary for to result in a user click-through and as well how many times the web page itself will be viewed in a day. The number of impressions necessary to generate a click-through corresponds to the s and the number of total views corresponds to the capacity of the knapsack, .

Each utility function evaluation requires solving an optimization problem of the form:

| maximize | (23) | |||

| subject to | (24) | |||

| (25) |

where is the number of players, is the vector of stated values (bids) for each player, is the corresponding vector of sizes, is a binary vector indicating whether each player is included in the knapsack. Player ’s final utility is . That is, it is the difference between their private value and their submitted bid, assuming they are included in the knapsack, and zero otherwise.

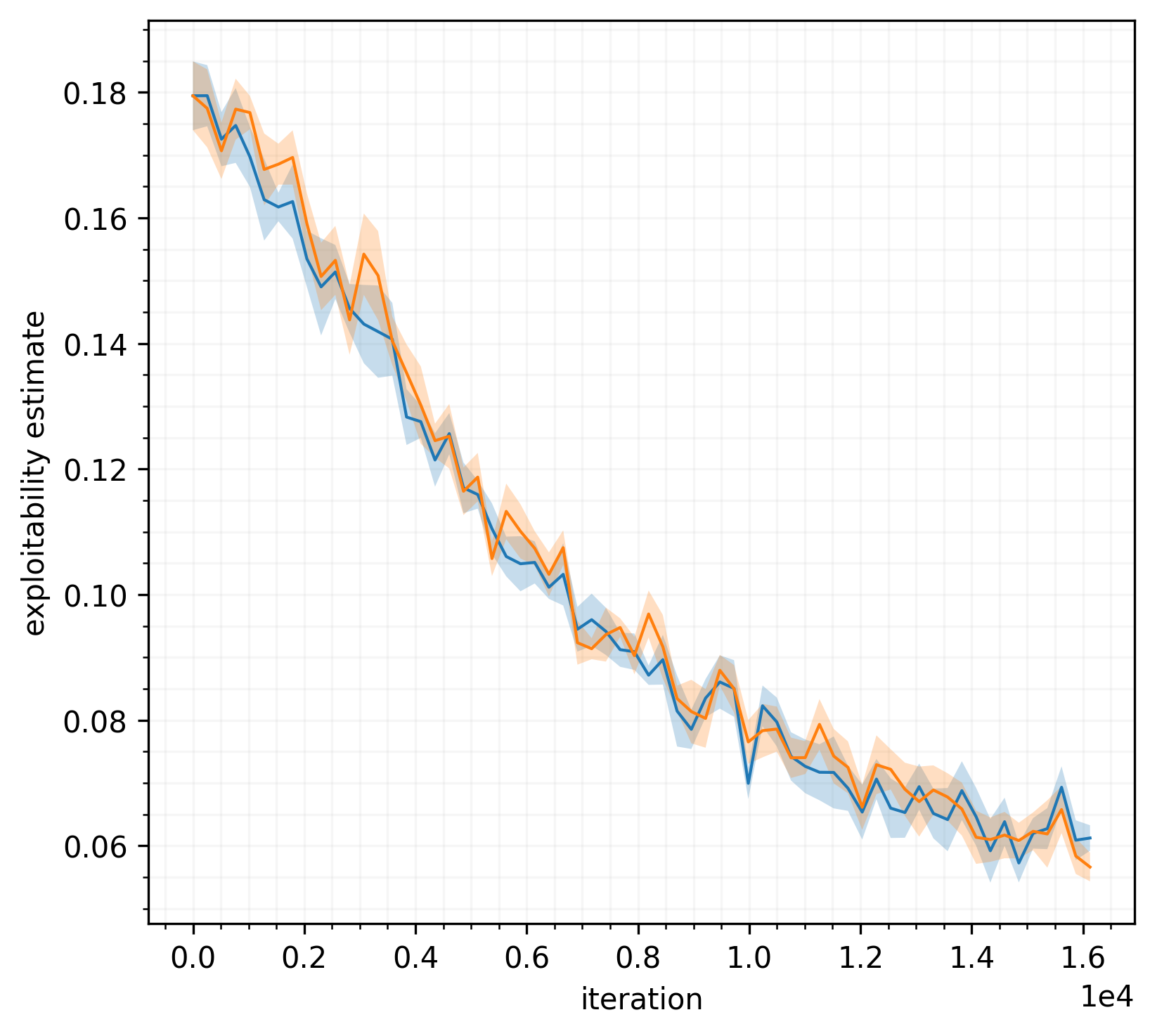

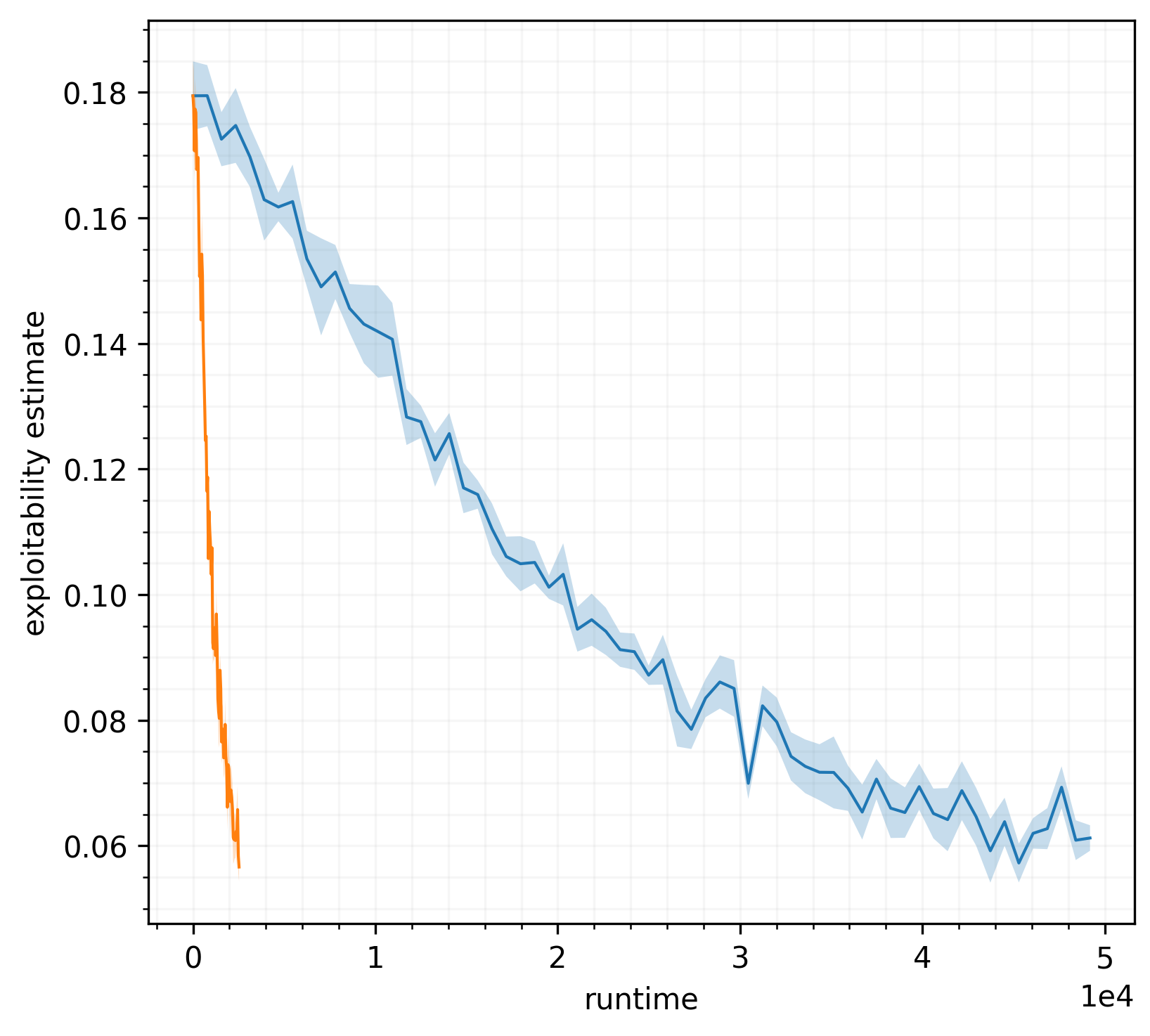

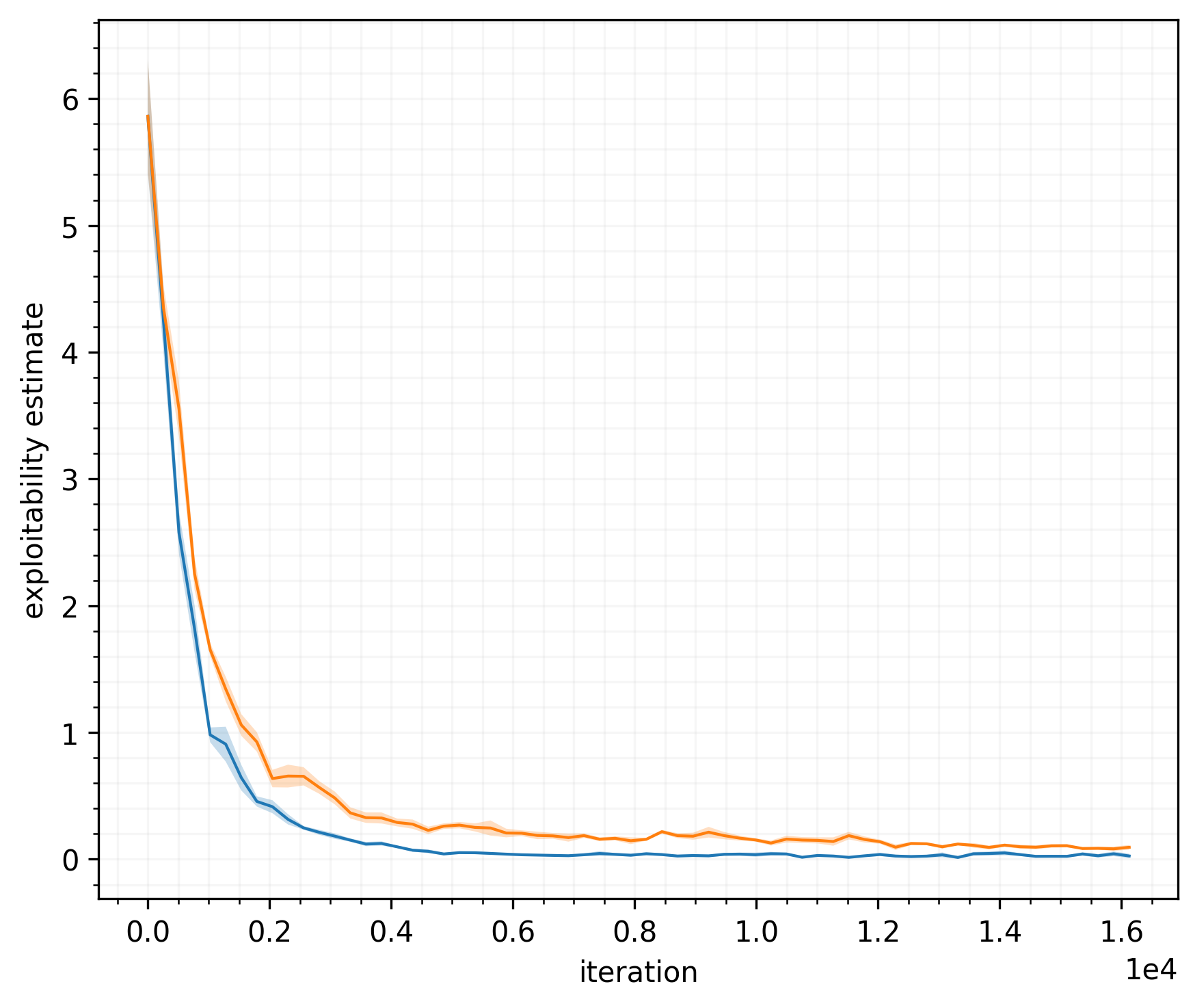

This problem can be solved using integer linear programming (ILP). For this, we use the milp function included in SciPy’s library (Virtanen et al., 2020), which uses the HiGHS optimization solver (Huangfu and Hall, 2018; Hall et al., 2023). Solving an integer program can be expensive (integer linear programming is NP-hard), so reducing the number of utility function evaluations during learning should result in a significant speedup. In our experiment, we sample the s and s from the standard uniform distribution, and sample from the standard uniform distribution on . Experimental results on the knapsack auction are shown in Figure 3 for 10 players and Figure 4 for 20 players. As expected, our method requires fewer utility function evaluations per iteration and thus yields a significantly lower training time for attaining the same exploitability.

5.3 Sequential auction for multiple identical items

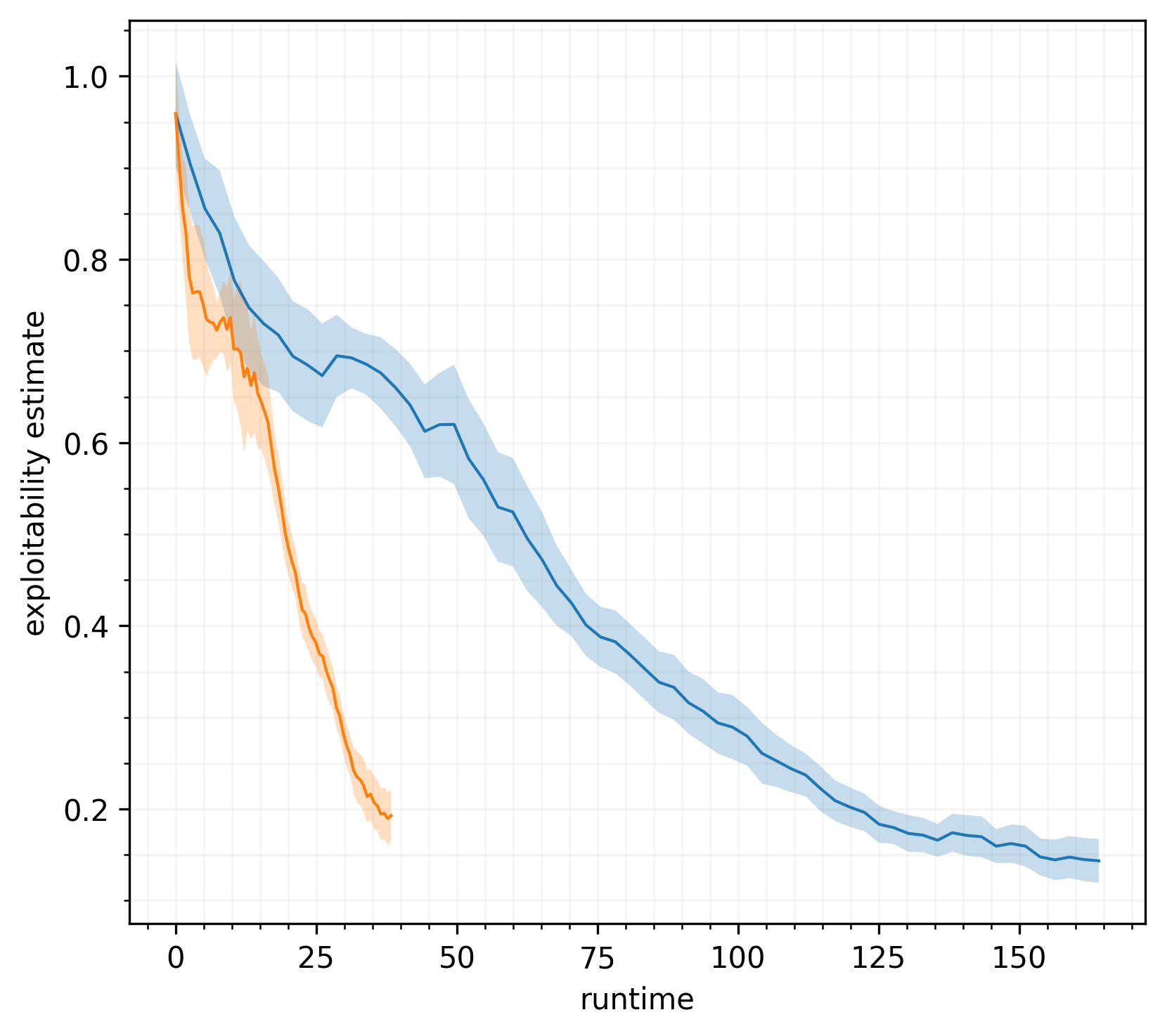

Consider a multi-item unit-demand auction in which identical items are sold sequentially, rather than simultaneously. We follow the description given in Krishna (2002, §15.1). In this auction, identical items are sold to bidders using a sequence of first-price sealed-bid auctions. Specifically, on each of rounds, one of the items is auctioned using the first-price format, and the price at which it is sold—the winning bid—is announced. We focus on the single-unit demand setting, in which each bidder has use for at most one unit. Thus a bidder leaves the game once it has won an item. Each bidder has a private value is that is sampled from the standard uniform distribution. On round , a bidder’s observation consists of its own private value as well as all the prices of the preceding rounds, . Results are shown in Figure 5. Our method performs much better in terms of wall time.

5.4 Continuous-action Goofspiel

Goofspiel, also known as the game of pure strategy, is a card game invented by mathematician Merrill Flood in the 1930s (Tucker, 1984). This game is played with a standard 52-card deck. The cards of one suit are given to one player, the cards of a second suit are given to the other player, and the cards of a third suit are shuffled and placed face down in the middle. The cards are valued from low to high as 1 (Ace), 2, 3, …, 10, 11 (Jack), 12 (Queen), and 13 (King). A round consists of turning up the next card from the middle pile and letting the players simultaneously “bid” on this “prize” card. Players bid by choosing one of their own cards and revealing it at the same time as the other player. The player with the highest bid wins the value of the prize card. In a tie, the prize value is split between the players. All three cards are then discarded. The game ends after 13 rounds, and the winner is the player with the highest score. Because of its simple mechanics but complex strategy, Goofspiel is commonly used as an example in game theory and artificial intelligence (Ross, 1971; Dror, 1989; Ferguson and Melolidakis, 2001; Grimes and Dror, 2013; Rhoads and Bartholdi, 2012; Lanctot et al., 2014).

We consider the following continuous-action variant of Goofspiel. Instead of receiving a deck of discrete bids consisting of all cards of one suit, each player has a continuous budget that they can spend to bid on the prize card in each round. In each round, their continuous bid is subtracted from their budget. This can, if desired, be thought of as modeling a multi-round, multi-item, auction-like scenario with a budget constraint for each bidder. To allow the players to randomize over their 1-dimensional actions (the bids), we inject their strategy networks with 1-dimensional latent input noise in addition to the observation, as described in Martin and Sandholm (2023).

Figure 6 shows the exploitability over the course of training on 20-player continuous-action Goofspiel. Our method attains low exploitability with significantly faster run time than the classical method.

6 Conclusions and future research

We tackled the problem of computing an approximate Nash equilibrium of a game with a black-box utility function, for which we lack access to gradients. To do this, we combined equilibrium-seeking gradient dynamics with a new zeroth-order approach to computing the simultaneous gradient. This approach reduces the number of utility function evaluations per iteration from linear in the number of players to constant in the number of players. Our method performs a joint perturbation on all players’ strategies at once, rather than perturbing each one individually. When utility function evaluation is expensive (e.g., in terms of wall time, memory, or other resources), this can significantly reduce the cost of training. We compared our approach to the standard one on several games, showing a significant reduction in training time. For future work, we would like to test and analyze the combination of our joint-perturbation approach with alternative equilibrium-seeking dynamics, such as extragradient and optimistic gradient dynamics.

Acknowledgements

This material is based on work supported by the Vannevar Bush Faculty Fellowship ONR N00014-23-1-2876, National Science Foundation grants RI-2312342 and RI-1901403, ARO award W911NF2210266, and NIH award A240108S001.

References

- Aggarwal and Hartline [2006] Gagan Aggarwal and Jason D Hartline. Knapsack auctions. In Annual ACM-SIAM Symposium on Discrete Algorithms (SODA), 2006.

- Bäck [1996] Thomas Bäck. Evolutionary algorithms in theory and practice. Oxford University Press, 1996.

- Bäck et al. [1997] Thomas Bäck, David B. Fogel, and Zbigniew Michalewicz. Handbook of evolutionary computation. IOP Publishing Ltd., 1997.

- Balduzzi et al. [2018] David Balduzzi, Sebastien Racaniere, James Martens, Jakob Foerster, Karl Tuyls, and Thore Graepel. The mechanics of n-player differentiable games. In International Conference on Machine Learning (ICML), 2018.

- Berahas et al. [2022] Albert S. Berahas, Liyuan Cao, Krzysztof Choromanski, and Katya Scheinberg. A theoretical and empirical comparison of gradient approximations in derivative-free optimization. Foundations of Computational Mathematics, 2022.

- Berg et al. [2010] Jordan Berg, Amy Greenwald, Victor Naroditskiy, and Eric Sodomka. A knapsack-based approach to bidding in ad auctions. In European Conference on Artificial Intelligence (ECAI). IOS Press, 2010.

- Bichler et al. [2021] Martin Bichler, Maximilian Fichtl, Stefan Heidekrüger, Nils Kohring, and Paul Sutterer. Learning equilibria in symmetric auction games using artificial neural networks. Nature Machine Intelligence, 2021.

- Bichler et al. [2023a] Martin Bichler, Max Fichtl, and Matthias Oberlechner. Computing Bayes–Nash equilibrium strategies in auction games via simultaneous online dual averaging. Operations Research, 2023a.

- Bichler et al. [2023b] Martin Bichler, Nils Kohring, and Stefan Heidekrüger. Learning equilibria in asymmetric auction games. INFORMS Journal on Computing, 2023b.

- Bradbury et al. [2018] James Bradbury, Roy Frostig, Peter Hawkins, Matthew James Johnson, Chris Leary, Dougal Maclaurin, George Necula, Adam Paszke, Jake VanderPlas, Skye Wanderman-Milne, et al. JAX: Composable transformations of Python+NumPy programs, 2018.

- Crouse [2016] David F. Crouse. On implementing 2d rectangular assignment algorithms. IEEE Transactions on Aerospace and Electronic Systems, 2016.

- Dasgupta and Maskin [1986] P. Dasgupta and Eric Maskin. The existence of equilibrium in discontinuous economic games 1: Theory. Review of Economic Studies, 53:1–26, 1986.

- Daskalakis et al. [2018] Constantinos Daskalakis, Andrew Ilyas, Vasilis Syrgkanis, and Haoyang Zeng. Training GANs with optimism. In International Conference on Learning Representations (ICLR), 2018.

- Debreu [1952] Gerard Debreu. A social equilibrium existence theorem. Proceedings of the National Academy of Sciences, 1952.

- DeepMind et al. [2020] DeepMind, Igor Babuschkin, Kate Baumli, Alison Bell, Surya Bhupatiraju, Jake Bruce, Peter Buchlovsky, David Budden, Trevor Cai, Aidan Clark, Ivo Danihelka, Antoine Dedieu, Claudio Fantacci, Jonathan Godwin, Chris Jones, Ross Hemsley, Tom Hennigan, Matteo Hessel, Shaobo Hou, Steven Kapturowski, Thomas Keck, Iurii Kemaev, Michael King, Markus Kunesch, Lena Martens, Hamza Merzic, Vladimir Mikulik, Tamara Norman, George Papamakarios, John Quan, Roman Ring, Francisco Ruiz, Alvaro Sanchez, Laurent Sartran, Rosalia Schneider, Eren Sezener, Stephen Spencer, Srivatsan Srinivasan, Miloš Stanojević, Wojciech Stokowiec, Luyu Wang, Guangyao Zhou, and Fabio Viola. The DeepMind JAX Ecosystem, 2020. URL http://github.com/google-deepmind.

- Dror [1989] Moshe Dror. Simple proof for Goofspiel: the game of pure strategy. Advances in Applied Probability, 1989.

- Duchi et al. [2015] John C. Duchi, Michael I. Jordan, Martin J. Wainwright, and Andre Wibisono. Optimal rates for zero-order convex optimization: The power of two function evaluations. IEEE Transactions on Information Theory, 2015.

- Dütting et al. [2014] Paul Dütting, Vasilis Gkatzelis, and Tim Roughgarden. The performance of deferred-acceptance auctions. In Proceedings of the ACM Conference on Economics and Computation (EC), 2014.

- Eiben and Smith [2003] Agoston E. Eiben and James E. Smith. Introduction to evolutionary computing. Springer, 2003.

- Fan [1952] Ky Fan. Fixed point and minimax theorems in locally convex topological linear spaces. Proceedings of the National Academy of Sciences, 1952.

- Ferguson and Melolidakis [2001] Thomas S. Ferguson and Costis Melolidakis. Games with finite resources. International Journal of Game Theory, 2001.

- Fu et al. [2015] Michael C. Fu et al. Handbook of simulation optimization. Springer, 2015.

- Glicksberg [1952] I. L. Glicksberg. A further generalization of the Kakutani fixed point theorem, with application to Nash equilibrium points. Proceedings of the American Mathematical Society, 3(1):170–174, 1952.

- Goodfellow et al. [2014] Ian Goodfellow, Jean Pouget-Abadie, Mehdi Mirza, Bing Xu, David Warde-Farley, Sherjil Ozair, Aaron Courville, and Yoshua Bengio. Generative adversarial nets. In Conference on Neural Information Processing Systems (NeurIPS), 2014.

- Goodfellow et al. [2020] Ian Goodfellow, Jean Pouget-Abadie, Mehdi Mirza, Bing Xu, David Warde-Farley, Sherjil Ozair, Aaron Courville, and Yoshua Bengio. Generative adversarial networks. Communications of the ACM, 2020.

- Grimes and Dror [2013] Mark Grimes and Moshe Dror. Observations on strategies for Goofspiel. In 2013 IEEE Conference on Computational Intelligence in Games (CIG), 2013.

- Hall et al. [2023] J. Hall, I. Galabova, L. Gottwald, and M. Feldmeier. Highs–high performance software for linear optimization, 2023.

- He et al. [2015] Kaiming He, Xiangyu Zhang, Shaoqing Ren, and Jian Sun. Delving deep into rectifiers: Surpassing human-level performance on ImageNet classification. In International Conference on Computer Vision (ICCV), 2015.

- Heek et al. [2023] Jonathan Heek, Anselm Levskaya, Avital Oliver, Marvin Ritter, Bertrand Rondepierre, Andreas Steiner, and Marc van Zee. Flax: A neural network library and ecosystem for JAX, 2023. URL http://github.com/google/flax.

- Hsieh et al. [2021] Ya-Ping Hsieh, Panayotis Mertikopoulos, and Volkan Cevher. The limits of min-max optimization algorithms: Convergence to spurious non-critical sets. In International Conference on Machine Learning (ICML), 2021.

- Hsieh et al. [2019] Yu-Guan Hsieh, Franck Iutzeler, Jérôme Malick, and Panayotis Mertikopoulos. On the convergence of single-call stochastic extra-gradient methods. In Conference on Neural Information Processing Systems (NeurIPS), 2019.

- Huangfu and Hall [2018] Qi Huangfu and J. A. Julian Hall. Parallelizing the dual revised simplex method. Mathematical Programming Computation, 2018.

- Hunter [2007] J. D. Hunter. Matplotlib: A 2d graphics environment. Computing in Science & Engineering, 2007.

- Jonker and Volgenant [1988] Roy Jonker and Ton Volgenant. A shortest augmenting path algorithm for dense and sparse linear assignment problems. In DGOR/NSOR: Papers of the 16th Annual Meeting of DGOR in Cooperation with NSOR/Vorträge der 16. Jahrestagung der DGOR zusammen mit der NSOR, 1988.

- Korpelevich [1976] G. M. Korpelevich. The extragradient method for finding saddle points and other problems. Ekonomika i Matematicheskie Metody, 1976.

- Krishna [2002] Vijay Krishna. Auction Theory. Academic Press, 2002.

- Kuhn [1955] Harold W. Kuhn. The hungarian method for the assignment problem. Naval research logistics quarterly, 1955.

- Lanctot et al. [2014] Marc Lanctot, Viliam Lisý, and Mark H. M. Winands. Monte Carlo tree search in simultaneous move games with applications to Goofspiel. In Computer Games, 2014.

- Lanctot et al. [2017] Marc Lanctot, Vinicius Zambaldi, Audrunas Gruslys, Angeliki Lazaridou, Karl Tuyls, Julien Pérolat, David Silver, and Thore Graepel. A unified game-theoretic approach to multiagent reinforcement learning. In Conference on Neural Information Processing Systems (NeurIPS), pages 4190–4203, 2017.

- Letcher et al. [2019a] Alistair Letcher, David Balduzzi, Sébastien Racaniere, James Martens, Jakob Foerster, Karl Tuyls, and Thore Graepel. Differentiable game mechanics. Journal of Machine Learning Research, 2019a.

- Letcher et al. [2019b] Alistair Letcher, Jakob Foerster, David Balduzzi, Tim Rocktäschel, and Shimon Whiteson. Stable opponent shaping in differentiable games. In International Conference on Learning Representations (ICLR), 2019b.

- Li and Wellman [2021] Zun Li and Michael P Wellman. Evolution strategies for approximate solution of bayesian games. In AAAI Conference on Artificial Intelligence (AAAI), 2021.

- Lockhart et al. [2019] Edward Lockhart, Marc Lanctot, Julien Pérolat, Jean-Baptiste Lespiau, Dustin Morrill, Finbarr Timbers, and Karl Tuyls. Computing approximate equilibria in sequential adversarial games by exploitability descent. In Proceedings of the International Joint Conference on Artificial Intelligence (IJCAI), 2019.

- Martin and Sandholm [2023] Carlos Martin and Tuomas Sandholm. Finding mixed-strategy equilibria of continuous-action games without gradients using randomized policy networks. In Proceedings of the International Joint Conference on Artificial Intelligence (IJCAI), 2023.

- Mazumdar et al. [2020] Eric Mazumdar, Lillian J. Ratliff, and S. Shankar Sastry. On gradient-based learning in continuous games. SIAM Journal on Mathematics of Data Science, 2020.

- Mazumdar et al. [2019] Eric V. Mazumdar, Michael I. Jordan, and S. Shankar Sastry. On finding local Nash equilibria (and only local Nash equilibria) in zero-sum games. arXiv:1901.00838, 2019.

- Mertikopoulos and Zhou [2019] Panayotis Mertikopoulos and Zhengyuan Zhou. Learning in games with continuous action sets and unknown payoff functions. Mathematical Programming, 2019.

- Metz et al. [2021] Luke Metz, C. Daniel Freeman, Samuel S. Schoenholz, and Tal Kachman. Gradients are not all you need. arXiv:2111.05803, 2021.

- Milgrom and Weber [1985] Paul Milgrom and Robert Weber. Distributional strategies for games with incomplete infromation. Mathematics of Operations Research, 10:619–632, 1985.

- Mohamed et al. [2020] Shakir Mohamed, Mihaela Rosca, Michael Figurnov, and Andriy Mnih. Monte carlo gradient estimation in machine learning. Journal of Machine Learning Research, 2020.

- Nash [1950] John Nash. Equilibrium points in n-person games. Proceedings of the National Academy of Sciences, 36:48–49, 1950.

- Nesterov and Spokoiny [2017] Yurii Nesterov and Vladimir Spokoiny. Random gradient-free minimization of convex functions. Foundations of Computational Mathematics, 2017.

- Popov [1980] Leonid Denisovich Popov. A modification of the Arrow-Hurwicz method for search of saddle points. Mathematical notes of the Academy of Sciences of the USSR, 1980.

- Rechenberg [1978] I. Rechenberg. Evolutionsstrategien. In Simulationsmethoden in der medizin und biologie. Springer, 1978.

- Rechenberg and Eigen [1973] I. Rechenberg and M. Eigen. Evolutionsstrategie: Optimierung technischer systeme nach prinzipien der biologischen evolution. Frommann-Holzboog Stuttgart, 1973.

- Rhoads and Bartholdi [2012] Glenn C. Rhoads and Laurent Bartholdi. Computer solution to the game of pure strategy. Games, 2012.

- Rosen [1965] J. Ben Rosen. Existence and uniqueness of equilibrium points for concave n-person games. Econometrica, 1965.

- Ross [1971] Sheldon M Ross. Goofspiel—the game of pure strategy. Journal of Applied Probability, 8(3):621–625, 1971.

- Salimans et al. [2017] Tim Salimans, Jonathan Ho, Xi Chen, Szymon Sidor, and Ilya Sutskever. Evolution strategies as a scalable alternative to reinforcement learning. arXiv:1703.03864, 2017.

- Schwefel [1977] Hans-Paul Schwefel. Numerische optimierung von computer-modellen mittels der evolutionsstrategie. Birkhäuser Basel, 1977.

- Shamir [2017] Ohad Shamir. An optimal algorithm for bandit and zero-order convex optimization with two-point feedback. Journal of Machine Learning Research, 2017.

- Shapley and Shubik [1971] Lloyd S. Shapley and Martin Shubik. The assignment game i: The core. International Journal of Game Theory, 1971.

- Timbers et al. [2022] Finbarr Timbers, Nolan Bard, Edward Lockhart, Marc Lanctot, Martin Schmid, Neil Burch, Julian Schrittwieser, Thomas Hubert, and Michael Bowling. Approximate exploitability: Learning a best response. In Proceedings of the International Joint Conference on Artificial Intelligence (IJCAI), 2022.

- Tucker [1984] Albert W. Tucker. The Princeton mathematics community in the 1930s: transcript number 11, 1984.

- Virtanen et al. [2020] Pauli Virtanen, Ralf Gommers, Travis E. Oliphant, Matt Haberland, Tyler Reddy, David Cournapeau, Evgeni Burovski, Pearu Peterson, Warren Weckesser, Jonathan Bright, Stéfan J. van der Walt, Matthew Brett, Joshua Wilson, K. Jarrod Millman, Nikolay Mayorov, Andrew R. J. Nelson, Eric Jones, Robert Kern, Eric Larson, C J Carey, İlhan Polat, Yu Feng, Eric W. Moore, Jake VanderPlas, Denis Laxalde, Josef Perktold, Robert Cimrman, Ian Henriksen, E. A. Quintero, Charles R. Harris, Anne M. Archibald, Antônio H. Ribeiro, Fabian Pedregosa, Paul van Mulbregt, and SciPy 1.0 Contributors. SciPy 1.0: Fundamental Algorithms for Scientific Computing in Python. Nature Methods, 2020.

- Walton and Lisy [2021] Michael Walton and Viliam Lisy. Multi-agent reinforcement learning in OpenSpiel: A reproduction report. arXiv:2103.00187, 2021.

- Wierstra et al. [2008] Daan Wierstra, Tom Schaul, Jan Peters, and Juergen Schmidhuber. Natural evolution strategies. In 2008 IEEE Congress on Evolutionary Computation, 2008.

- Wierstra et al. [2014] Daan Wierstra, Tom Schaul, Tobias Glasmachers, Yi Sun, Jan Peters, and Jürgen Schmidhuber. Natural evolution strategies. Journal of Machine Learning Research, 2014.

- Willi et al. [2022] Timon Willi, Alistair Hp Letcher, Johannes Treutlein, and Jakob Foerster. COLA: Consistent learning with opponent-learning awareness. In International Conference on Machine Learning (ICML), 2022.

- Yi et al. [2009] Sun Yi, Daan Wierstra, Tom Schaul, and Jürgen Schmidhuber. Stochastic search using the natural gradient. In International Conference on Machine Learning (ICML), 2009.

- Zhuang et al. [2020] Juntang Zhuang, Tommy Tang, Yifan Ding, Sekhar C. Tatikonda, Nicha Dvornek, Xenophon Papademetris, and James Duncan. Adabelief optimizer: Adapting stepsizes by the belief in observed gradients. Conference on Neural Information Processing Systems (NeurIPS), 2020.

Appendix A Code

For our experiments, we used Python 3.12.3 with the following libraries:

-

•

jax 0.4.30 [Bradbury et al., 2018]: https://github.com/google/jax

-

•

flax 0.8.5 [Heek et al., 2023]: https://github.com/google/flax

-

•

optax 0.2.3 [DeepMind et al., 2020]: https://github.com/google-deepmind/optax

-

•

matplotlib 3.9.1 [Hunter, 2007]: https://github.com/matplotlib/matplotlib

-

•

scipy 1.14.0 [Virtanen et al., 2020]:https://github.com/scipy/scipy

An implementation of the classical method, as well as our method, is shown below.