On the Impact of Predictor Serial Correlation on the LASSO

Abstract

We explore inference within sparse linear models, focusing on scenarios where both predictors and errors carry serial correlations. We establish a clear link between predictor serial correlation and the finite sample performance of the LASSO, showing that even orthogonal or weakly correlated stationary AR processes can lead to significant spurious correlations due to their serial correlations. To address this challenge, we propose a novel approach named ARMAr-LASSO (ARMA residuals LASSO), which applies the LASSO to predictor time series that have been pre-whitened with ARMA filters and lags of dependent variable. Utilizing the near-epoch dependence framework, we derive both asymptotic results and oracle inequalities for the ARMAr-LASSO, and demonstrate that it effectively reduces estimation errors while also providing an effective forecasting and feature selection strategy. Our findings are supported by extensive simulations and an application to real-world macroeconomic data, which highlight the superior performance of the ARMAr-LASSO for handling sparse linear models in the context of time series.

Keywords: Time series, serial correlation, spurious correlation, LASSO.

1 Introduction

The LASSO (Tibshirani, 1996) is perhaps the most commonly employed approach to handle regressions with a large number of predictors. From a theoretical standpoint, its effectiveness in terms of estimation, prediction, and feature selection is contingent upon either orthogonality or reasonably weak correlation among predictors (see Zhao and Yu 2006; Bickel et al. 2009; Negahban et al. 2012; and Hastie 2015). This hinders the use of the LASSO for the analysis of economic time series data, which are notoriously characterized by intrinsic multicollinearity; that is, by predictor correlations at the population level (Forni et al., 2000; Forni and Lippi, 2001; Stock and Watson, 2002a; De Mol et al., 2008; Medeiros and F.Mendes, 2012). A common procedure to address this issue is to model multicollinearity and remove it, as proposed, e.g., by Fan et al. (2020), who filter time series using common factors and then apply the LASSO to the filtered residuals. However, mitigating or even eliminating multicollinearity is not the end of the story, as effectiveness of the LASSO can also be affected by spurious correlations. These occur when predictors are orthogonal or weakly correlated at the population level, but a lack of sufficient independent replication (lack of degrees of freedom) introduces correlations at the sample level, potentially leading to false scientific discoveries and incorrect statistical inferences (Fan and Zhou, 2016; Fan et al., 2018). This issue has been broadly explored in ultra-high dimensional settings, where the number of predictors can vastly exceed the available sample size (Fan et al., 2014). We argue that in time series data, lack of independent replication can be due not only to a shortage of available observations but also to serial correlation.

This article introduces two elements of novelty. First, we establish an explicit link between serial correlations and spurious correlations. At a theoretical level, we derive the density of the sample correlation between two orthogonal stationary Gaussian AR(1) processes, and show how such density depends not only on the sample size but also on the degree of serial correlation; at any given sample size, an increase in serial correlation results in a larger probability of sizable spurious correlations. Then we use extensive simulations to show how this dependence holds in much more general settings (e.g., when the underlying processes are not orthogonal, or non Gaussian ARMA).

Second, we propose an approach that, using a filter similar to that proposed by Fan et al. (2020), rescues the performance of the LASSO in the presence of serially correlated predictors. Our approach, which we name ARMAr-LASSO (ARMA residuals LASSO), relies upon a working model where, instead of the observed predictor time series, we use as regressors the residuals of ARMA processes fitted on such series, augmented with lags of the dependent variable. We motivate our choice of working model and provide some asymptotic arguments concerning limiting distribution and feature selection consistency. Subsequently, we employ the mixingale and near-epoch dependence framework (Davidson, 1994; Adamek et al., 2023) to prove oracle inequalities for the estimation and forecast error bounds of the ARMAr-LASSO, while simultaneously addressing the issue of estimating ARMA residuals. To complete the analysis, we use simulations to validate and generalize the theoretical result. Furthermore, we apply our methodology to a high-dimensional dataset for forecasting the consumer price index in the Euro Area. Simulations and empirical exercises demonstrate that the ARMAr-LASSO produces more parsimonious models, better coefficient estimates, and more accurate forecasts than LASSO-based methods applied to time series. Notably, both theoretical and numerical results concerning our approach hold even in contexts of factor-induced multicollinearity, provided that the idiosyncratic components are orthogonal or weakly correlated processes exhibiting serial correlation. Code and replicability material is available at https://doi.org/10.5281/zenodo.13335323.

Our work complements the vast literature on error bounds for LASSO-based methods in time series analysis, which addresses estimation and forecast consistency in scenarios with autocorrelated errors and autoregressive processes (Bartlett, 1935; Granger and Newbold, 1974; Granger et al., 2001; Hansheng Wang and Jiang, 2007; Wang et al., 2007; Hsu et al., 2008; Nardi and Rinaldo, 2011; Chronopoulos et al., 2023; Baillie et al., 2024). Moreover, our methodology aligns with the prevailing literature on pre-whitening filters, which are commonly employed to mitigate autocorrelation in the error component or to enhance cross-correlation analysis. For instance, Robinson (1988) suggests obtaining residuals from partial linear models and then applying least squares to estimate a non-parametric component. Belloni et al. (2013) propose a similar approach in high-dimensional settings, using LASSO on the residuals from a parametric component. Hansen and Liao (2019) show that, in panel data model inference, applying a PCA filter to eliminate multicollinearity and using LASSO on its residuals can produce reliable confidence intervals. Finally, as mentioned, Fan et al. (2020) illustrate how latent factors create strong dependencies among regressors, complicating feature selection, while selection improves on idiosyncratic components.

The remainder of the article is organized as follows. Section 2 introduces the problem setup and our results concerning the link between serial correlations and spurious correlations. Section 3 introduces the ARMAr-LASSO and explores its theoretical properties. Section 4 presents simulations and real data analyses to evaluate the performance of our proposed methodology. Section 5 provides some final remarks.

We summarize here some notation that will be used throughout. Bold letters denote vectors, for example . Supp denotes the support of a vector, that is, , and the support cardinality. The norm of a vector is for , with , and with the usual extension . Bold capital letters denote matrices, for example , where is the -row -column element. Furthermore, denotes a -length vector of zeros, the identity matrix, and the sign of a real number . To simplify the analysis, we frequently make use of arbitrary positive finite constants .

2 Problem Setup

Consider the linear regression model

| (1) |

where is a vector of predictors, is a unknown -sparse vector of regression coefficients, i.e. , and is an error term. We impose the following assumptions on the processes and .

Assumption 1:

and are non-deterministic second order stationary processes.

Under Assumption 1, the predictors and the error terms are weakly stationary and admit an ARMA representation of the form

| (2) | |||

| (3) |

where the innovation processes , are sequences of zero-mean white noise () with finite variances (see Reinsel 1993, ch. 1.2 for details).

Assumption 2:

for any and ; and for any and .

There are several approaches to estimate when is comparable to or larger than (Zhang and Zhang, 2012; James et al., 2013); here we focus on the LASSO estimator (Tibshirani, 1996) given by where is the weight of the penalty and must be “tuned” to guarantee that regression coefficient estimates are effectively shrunk to zero – thus ensuring predictor, or feature, selection.

However, linear associations among predictors are well known to affect LASSO performance. Bickel et al. (2009); Bühlmann and van de Geer (2011) and Negahban et al. (2012) have shown that the LASSO estimation and prediction accuracy are inversely proportional to the minimum eigenvalue of the predictor sample covariance matrix. Thus, highly correlated predictors deteriorate estimation and prediction performance. Moreover, Zhao and Yu (2006) proved that the LASSO struggles to differentiate between relevant (i.e., ) and irrelevant (i.e., ) predictors when they are closely correlated, leading to false positives. Thus, highly correlated predictors may also deteriorate feature selection performance. The weak irrepresentable condition addresses this issue ensuring both estimation and feature selection consistency through bounds on the sample correlations between relevant and irrelevant predictors (Zhao and Yu 2006, see also Bühlmann and van de Geer 2011). Nevertheless, orthogonality or weak correlation seldom hold in the context of economic and financial data. For instance, decades of literature provide evidence for co-movements of macroeconomic variables (Forni et al., 2000; Forni and Lippi, 2001; Forni et al., 2005; Stock and Watson, 2002a, b). Special methods have been proposed to mitigate the negative effects of these linear associations, such as Factor-Adjusted Regularized Model Selection (FarmSelect) (Fan et al., 2020), which applies the LASSO to the idiosyncratic components of economic variables, obtained by filtering the variables through a factor model. Although approaches such as FarmSelect can be very effective in addressing multicollinearity, strong spurious correlations can emerge at the sample level and affect the LASSO even when predictors are orthogonal or weakly correlated at the population level. This is the case for large regressions, where the number of predictors is comparable to or even larger than the sample size, and even more so for large regressions involving time series, where independent replication can be further hindered by serial correlations. This article focuses specifically on spurious sample-level correlations; in the next section, we introduce a theoretical result linking serial correlations within time series to the sample correlations between them.

2.1 Serial and Sample Correlations for Time Series

Consider a first order -variate autoregressive process , , where are autoregressive coefficients such that for each , and . Assume that each is standardized so that and , and let be the sample covariance, or equivalently, correlation matrix – with generic off-diagonal element and eigenvalues . Here with , and , for . Our next task is to link , , to serial correlations. To this end, the following theorem provides an approximation for the density of the sample correlation coefficient.

Theorem 1:

Let be a stationary -variate Gaussian AR(1) process with autoregressive residuals . Let , where and are the autoregressive coefficients of the -th and -th processes, respectively. Then, the density of is approximated by

Proof: see Supplement B.1

Theorem 1 shows that, in a finite sample setting, the density and thus the probability of observing sizable spurious correlations between two orthogonal Gaussian autoregressive processes, depends on their degrees of serial correlation, i.e., on both the magnitude and the sign of . When , an increase in results in a density with thicker tails, and thus a higher . This, in turn, leads to a higher probability of a small minimum eigenvalue (as a consequence of the inequality ; see Supplement A for details), and a higher chance of breaking the irrepresentable condition if, say, one of the processes is relevant for the response and the other is not ( and , or vice versa). When , an increase in results in a density more concentrated around the origin. In Supplement C we provide an extensive numerical validation of Theorem 1, investigating the impact of the sign of , as well as more realistic scenarios with correlated, non-Gaussian, and/or ARMA processes, through multiple simulation experiments.

We conclude this Section with a simple “toy experiment”. We generate data for from a -variate process , where all components share the same autoregressive coefficient , , and . Because of orthogonality, the maximum off-diagonal element and the minimum eigenvalue of the population correlation matrix are, respectively, and . We consider , and . For each scenario we calculate the average and standard deviation of and over 5000 Monte Carlo replications. Results are shown in Figure 1; a stronger persistence (higher ) increases the largest spurious sample correlations and decreases the smallest eigenvalue. However, as expected, an increase in the sample size from (panel (a)) to (panel (b)), reduces the impact of . For example, the values of and in the case of and are quite similar to those obtained for and .

Note that these results are valid for any type of orthogonal or weakly correlated predictors, as long as they carry serial correlations. These predictors can be either directly observed variables or, for example, factor model residuals.

3 The ARMAr-LASSO

We now switch to describing ARMAr-LASSO (ARMA residuals LASSO), the approach that we propose to rescue LASSO performance in the presence of serially correlated predictors. ARMAr-LASSO is formulated as a two-step procedure. In the first step we estimate a univariate ARMA model on each predictor. In the second step, we run the LASSO using, instead of the original predictors, the residuals from the ARMA model, i.e., estimates of the ’s in equation (2), plus one or more lags of the response. We start by introducing the “working model” on which our proposal relies; that is, the model that contains the true (not observable) ARMA residuals (their estimation will be addressed later)

| (4) |

Model (4) is the linear projection of on , which contains ARMA residuals and lagged values of the response. represents the corresponding best linear projection coefficients and is the error term, which is unlikely to be a white noise. It should be noted that the choice of is arbitrary and that some lags will be relevant while others will not. The relevant lags will be directly selected using LASSO. Model (4) is misspecified, in the sense that it does not correspond to the true data generating process (DGP) for the response, but it is similar in spirit to the factor filter used in the literature to mitigate multicollinearity (Fan et al., 2020). The idea behind model (4) is to leverage the serial independence of the terms, thereby avoiding the risk of sizable spurious correlation. However, the terms alone may explain only a small portion of the variance of , particularly in situations with high persistence. This is why we introduce the response lags as additional predictors; these amplify the signal in our model and consequently improve the forecast of . We list some important facts that capture how misspecification affects coefficient estimation and feature selection.

Fact 1:

(on the ARMA residuals) () ; () , , and , .

Fact 1 follows from Assumptions 1 and 2. Fact 1 () ensures that the least square estimator of is unbiased and consistent (see Supplement D). Fact 1 () is crucial for feature selection among the ’s. In particular, removes population level multicollinearity, while removes the risk of spurious correlation due to serial correlation (see Section 2.1).

Fact 2:

(on the lags of ) () can be ; () , .

Fact 2 () relates to the possible misspecification of the working model (4), which leads to an endogeneity problem between and the lags of . However, as previously said, the lags of and the corresponding parameters are introduced to enhance the variance explained, and thus the ability to forecast the response – tolerating a potential endogenous variable bias. Fact 2 () relates to potential correlations between the lags of , which is serial in nature. This implies that relevant lags may be represented by irrelevant ones. However, selection of relevant lags of is not of interest in this context.

Next, we provide three illustrative examples. In the first, and simplest, predictors and error terms have an AR(1) representation with a common coefficient; we refer to this as the common AR(1) restriciton case. In the second, the AR(1) processes have different autoregressive coefficients. Finally, in the third, predictors admit a common factor representation with AR(1) idiosyncratic components. Note that in all the examples .

Example 1:

(common AR(1) restriction). Suppose both predictors and error terms in model (1) admit an AR(1) representation; that is, and . In this case

Thus, under the common AR(1) restriction (also known as common factor restriction, Mizon 1995), the working model (4) is equivalent to the true model (1) because of the decomposition of the AR(1) processes and .

Remark 1:

Example 2:

(different AR(1) coefficients). Suppose and , where . Then the working model (4) has where . Therefore, and .

Example 3:

In the next section, we will show the limiting distribution and feature selection consistency of the LASSO estimator of in working model (4), which is obtained as

| (5) |

where is a tuning parameter. Next, in Section 3.2, we will establish oracle inequalities for the estimation and forecast error bounds of the ARMAr-LASSO, where we also tackle the problem of estimating the ’s. Henceforth, we assume that each row of the design matrix has been standardized to have mean 0 and variance 1, which implies . Moreover, where is a nonnegative definite matrix.

Let . To derive theoretical results for ARMAr-LASSO, we rely on the fact that, due to Assumptions 1 and 2, depends almost entirely on the “near epoch” of its shock. In particular, it is characterized as near-epoch dependent (NED) (refer to Davidson 1994 ch. 17 and Adamek et al. 2023 for details). NED is a very popular tool for modeling dependence in econometrics. It allows for cases where a variable’s behavior is primarily governed by the recent history of explanatory variables or shock processes, potentially assumed to be mixing. Davidson (1994) shows that even if a variable is not mixing, its reliance on the near epoch of its shocks makes it suitable for applying limit theorems, particularly the mixingale property (see Supplement B.4 for details). The NED framework accommodates a wide range of models, including those that are misspecified as our working model (4). For instance, in Examples 2 and 3, have a moving average representation with geometrically decaying coefficients, and are thus NED on and , respectively.

3.1 Asymptotic Results

This section is devoted to the asymptotic behavior and feature selection consistency of the LASSO applied to working model (4). Our results build upon Theorem 2 of Fu and Knight (2000) and Theorem 1 of Zhao and Yu (2006). Let be the mean vector, and the covariance matrix, of . The following theorem provides the asymptotic behavior of the LASSO solution.

Theorem 2:

Let Assumptions 1 and 2 hold. If and is nonsingular, then the solution of the optimization in (5) is such that

where and

is an dimensional random vector with a distribution.

Proof: see Supplement B.2

Next, we consider the feature selection properties of (5). Let denote the number of relevant lags of , and separate the coefficients of relevant and irrelevant features into and , respectively. Also, let and denote the rows of corresponding to relevant and irrelevant features. We can rewrite in block-wise form as follows

where , , and . We then introduce a critical assumption on .

Assumption 3:

(weak irrepresentable condition (Zhao and Yu, 2006)) Assuming is invertible, where the inequality holds element-wise.

Zhao and Yu (2006) showed that Assumption 3 is sufficient and almost necessary for both estimation and sign consistencies of the LASSO. The former requires . The latter requires and implies selection consistency; namely, as . Zhao and Yu (2006) also provided some conditions that guarantee the weak irrepresentable condition. The following are examples of such conditions: when for any (Zhao and Yu 2006, Corollary 2); when for (Zhao and Yu 2006, Corollary 3); or when these conditions are block-wise satisfied (Zhao and Yu 2006, Corollary 5). As a consequence of Fact 1 (), exhibits a block-wise structure, whereby one block encompasses the correlations between ’s and another block encompasses the correlations between lags of . Thus, Assumption 3 is satisfied if, for instance, the bound holds for the first block and the power decay bound holds for the second (see also Nardi and Rinaldo 2011). The following theorem states the selection consistency of our LASSO solution under Assumption 3.

Theorem 3:

Proof: see Supplement B.3

3.2 Oracle Inequalities

In this section, we derive the oracle inequalities that provide bounds for the estimation and forecast errors of the ARMAr-LASSO. We need the following two Assumptions, which bound the unconditional moments of the predictors in the true model (1), and of the predictors (ARMA residuals and response lags) and errors in the working model (4).

Assumption 4:

There exist constants such that .

Assumption 5:

Consider . There exist constants such that .

To derive the error bound of the ARMAr-LASSO estimator from (5), we follow the typical procedure presented in technical textbooks (see as example Bühlmann and van de Geer 2011, ch. 6). We need to be sufficiently large to exceed the empirical process with high probability. In addition, since equation (5) is formulated in terms of true ARMA residuals instead of the estimated ones; we need the two to be sufficiently close. To this end, let and be the vector of the autocovariance functions of the -th variable and its estimate, respectively. We thus have the following Theorem.

Theorem 4:

Proof: see Supplement B.4.

Theorem 4 establishes that the inequalities we need for the error bound of the proposed ARMAr-LASSO estimator hold with high probability. The term is chosen arbitrarily as a sequence that grows slowly as . However, we can use any sequence that tends to infinity sufficiently slowly. For example, Adamek et al. (2023) use to derive the properties of LASSO in a high-dimensional time series model under weak sparsity. Note that the importance of inequality () stems from the role of in the estimation of ARMA coefficients (see Brockwell and Davis 2002, ch. 5). Next, we introduce an assumption on the “restricted” positive definiteness of the covariance matrix of the predictors, which allows us to generalize subsequent results to the high-dimensional framework.

Assumption 6:

(restricted eigenvalue) For and any subset with cardinality , let and . Define the compatibility constant

| (6) |

and assume that . This implies that

Assumption 6, named restricted eigenvalue condition (Bickel et al., 2009), restricts the smallest eigenvalue of as a function of sparsity. In particular, instead of minimizing over all of , the minimum in (6) is restricted to those vectors which satisfy , and where has cardinality . Therefore, the compatibility constant is a lower bound for the restricted eigenvalue of the matrix (Bühlmann and van de Geer 2011, p. 106). Note also that if , the restricted eigenvalue condition is trivially satisfied if is nonsingular, since for every , and so . In other words, we require , where is the minimum eigenvalue of .

Remark 3:

Let be the compatibility constant of the restricted eigenvalue of . Since this captures how strongly predictors are correlated in the sample, as a consequence of the theoretical treatment of Section 2.1, we have with high probability as the degree of serial correlation increases (when both and are nonsingular, we have with high probability). Of course, and also depend on the cardinalities and . However, here we emphasize the role of serial correlation.

The following theorem, which expresses the oracle inequalities for the ARMAr-LASSO, is a direct consequence of Theorem 4.

Theorem 5:

Proof: see Supplement B.5

Remark 4:

Under the additional assumption that one can also establish, as an immediate corollary to Theorem 5, the following convergence rates: () ; () .

4 Simulations and Empirical Application

In this section, we analyze the performance of the ARMAr-LASSO by means of both simulations and a real data application.

4.1 Monte Carlo Experiments

The response variable is generated using the model , and we consider the following DGPs for the predictors and error terms:

-

(A)

Common AR(1) Restriction: .

-

(B)

Common AR(1) Restriction with Common Factor: , where .

-

(C)

General AR/ARMA Setting: ; ; ; , for , and . The error terms are generated as .

-

(D)

General AR/ARMA Setting with Common Factor: , where . Idiosyncratic components and the error terms are generated as in (C).

The shocks are generated as follows: with , with , and . For the DGPs in (A) and (C) we set , while for the DGPs in (B) and (D) we set to generate predictors primarily influenced by the common factor, with weakly correlated AR and/or ARMA idiosyncratic components. Finaly, we vary the value of to explore different signal-to-noise ratios (SNR).

We compare our ARMAr-LASSO (ARMAr-LAS) with the standard LASSO applied to the observed time series (LAS), LASSO applied to the observed time series plus lags of (LASy), and FarmSelect as proposed by Fan et al. (2020), which employs LASSO on factor model residuals (FaSel). Each method’s performance is evaluated based on average results from 1000 simulations, focusing on the coefficient estimation error (CoEr), the Root Mean Square Forecast Error (RMSFE), and the percentages of true positives (%TP) and false positives (%FP). Simulations vary in the number of variables (dimensionality), by setting , and maintaining a constant sample size of . In this way we cover low (), intermediate (), and high () dimensional scenarios. For all methods, the tuning parameter is selected using the Bayesian Information Criterion (BIC). Regardless of the choice of , is always taken to have the first 10 entries equal to 1 and all others equal to 0.

4.1.1 Common AR(1) Restriction

For DGPs (A) and (B) we investigate different settings varying (), along with the SNR (). For our working model, the ’s are obtained by filtering each series with an AR(1) process, and we consider ; that is, we take one lag of as additional predictor. Results are presented in Tables 1 and 2 for DGPs (A) and (B), respectively. We report here findings for SNR values of 1 and 5, but complete results are provided in Supplement E. For each SNR, CoEr and RMSFE (both relative to LAS), as well as %TP, and %FP are given for every and value considered (the best CoEr and RMSFE are in bold). For DGPs (A), ARMAr-LAS achieves the best CoEr and RMSFE across different , and SNR values, demonstrating superior accuracy in both estimation and forecasting compared to LAS, LASy, and FaSel. ARMAr-LAS demonstrates also superior performance in feature selection, with a higher true positives rate and a lower false positives rate. These gains are more evident under conditions of stronger serial correlation (when is 0.6 or higher). For DGPs (B), ARMAr-LAS confirms the better performance in all considered metrics and across values of , and SNR, with the exception of SNR=1 where LASy achieves better CoEr, especially for low and intermediate . This indicates the effectiveness of our proposal in handling DGPs with a factor structure, where the multicollinearities might be more complex than for simple AR processes.

4.1.2 General AR/ARMA Setting

Next we evaluate a context where the common AR(1) restriction does not hold. For our working model, the ’s are obtained by filtering each series with an ARMA() process, with the orders and (max 2) selected via BIC. We consider ; that is, three lags as additional predictors. Results are presented in Table 3 for SNR . ARMAr-LAS outperforms LAS, LASy, and FaSel in terms of accuracy in coefficient estimation, forecasting, and feature selection across both DGPs (C) and (D). The effectiveness of our proposal in these settings highlights its suitability also when tackling differing AR and ARMA processes and common factors, where the working model (4) does not coincide with the true DGP of .

| n | 50 | 150 | 300 | ||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0.3 | 0.6 | 0.9 | 0.95 | 0.3 | 0.6 | 0.9 | 0.95 | 0.3 | 0.6 | 0.9 | 0.95 | ||||||||

| SNR 1 | |||||||||||||||||||

| CoEr | |||||||||||||||||||

| LASy | 0.99 | 0.84 | 0.49 | 0.51 | 0.99 | 0.86 | 0.62 | 0.65 | 0.86 | 0.86 | 0.86 | 0.86 | |||||||

| FaSel | 1.12 | 1.16 | 2.25 | 2.91 | 1.12 | 1.33 | 2.19 | 2.95 | 1.17 | 1.75 | 1.27 | 1.20 | |||||||

| ARMAr-LAS | 0.98 | 0.82 | 0.36 | 0.34 | 0.98 | 0.82 | 0.50 | 0.52 | 0.82 | 0.83 | 0.83 | 0.82 | |||||||

| RMSFE | |||||||||||||||||||

| LASy | 0.98 | 0.90 | 0.79 | 0.80 | 0.99 | 0.89 | 0.90 | 0.83 | 0.99 | 0.92 | 0.89 | 0.89 | |||||||

| FaSel | 0.97 | 0.97 | 0.94 | 0.94 | 0.97 | 0.98 | 0.97 | 0.93 | 0.89 | 0.94 | 0.93 | 0.95 | |||||||

| ARMAr-LAS | 0.97 | 0.83 | 0.62 | 0.63 | 0.96 | 0.82 | 0.73 | 0.67 | 0.99 | 0.84 | 0.76 | 0.73 | |||||||

| % TP | |||||||||||||||||||

| LAS | 61.10 | 56.70 | 60.90 | 62.90 | 58.80 | 54.00 | 56.60 | 57.20 | 57.20 | 52.50 | 54.90 | 56.80 | |||||||

| LASy | 61.70 | 57.10 | 51.70 | 52.50 | 59.00 | 54.10 | 49.60 | 51.80 | 57.40 | 52.40 | 48.60 | 52.00 | |||||||

| FaSel | 12.60 | 16.60 | 44.50 | 49.10 | 29.60 | 37.20 | 49.60 | 54.80 | 51.20 | 48.40 | 52.50 | 57.40 | |||||||

| ARMAr-LAS | 64.70 | 65.60 | 68.10 | 71.10 | 61.50 | 62.20 | 65.10 | 68.00 | 59.60 | 60.00 | 62.80 | 67.40 | |||||||

| % FP | |||||||||||||||||||

| LAS | 2.70 | 7.70 | 42.00 | 44.40 | 1.00 | 3.40 | 17.40 | 16.30 | 0.40 | 2.00 | 9.60 | 9.40 | |||||||

| LASy | 2.80 | 5.00 | 19.50 | 24.20 | 1.00 | 1.80 | 8.10 | 9.50 | 0.40 | 1.00 | 4.70 | 6.00 | |||||||

| FaSel | 2.20 | 6.20 | 36.90 | 39.70 | 0.80 | 3.60 | 16.30 | 16.60 | 11.50 | 7.30 | 9.30 | 9.30 | |||||||

| ARMAr-LAS | 3.20 | 3.60 | 3.80 | 3.90 | 1.10 | 1.10 | 1.20 | 1.30 | 0.50 | 0.50 | 0.60 | 0.60 | |||||||

| SNR 5 | |||||||||||||||||||

| CoEr | |||||||||||||||||||

| LASy | 1.00 | 0.94 | 0.83 | 0.84 | 1.00 | 0.95 | 0.89 | 0.89 | 1.00 | 0.96 | 0.92 | 0.92 | |||||||

| FaSel | 1.59 | 1.48 | 2.30 | 3.11 | 1.37 | 1.36 | 2.37 | 3.21 | 1.78 | 1.58 | 2.36 | 3.18 | |||||||

| ARMAr-LAS | 0.95 | 0.79 | 0.45 | 0.44 | 0.96 | 0.82 | 0.60 | 0.59 | 0.97 | 0.81 | 0.64 | 0.62 | |||||||

| RMSFE | |||||||||||||||||||

| LASy | 1.00 | 0.97 | 0.92 | 0.94 | 1.00 | 0.97 | 0.98 | 0.94 | 1.00 | 0.98 | 0.96 | 0.97 | |||||||

| FaSel | 0.99 | 1.01 | 0.95 | 0.97 | 0.96 | 0.99 | 0.94 | 0.89 | 0.92 | 0.95 | 0.93 | 0.95 | |||||||

| ARMAr-LAS | 0.98 | 0.85 | 0.64 | 0.63 | 0.98 | 0.83 | 0.71 | 0.67 | 0.98 | 0.85 | 0.73 | 0.74 | |||||||

| % TP | |||||||||||||||||||

| LAS | 90.70 | 84.60 | 80.50 | 82.60 | 89.80 | 84.00 | 80.60 | 81.40 | 88.90 | 83.20 | 81.90 | 81.60 | |||||||

| LASy | 90.70 | 85.20 | 79.40 | 81.30 | 89.80 | 84.10 | 79.90 | 80.90 | 89.00 | 83.50 | 81.10 | 81.00 | |||||||

| FaSel | 27.50 | 34.10 | 58.50 | 64.30 | 57.30 | 65.80 | 77.00 | 81.90 | 81.10 | 79.20 | 81.30 | 83.90 | |||||||

| ARMAr-LAS | 92.70 | 92.40 | 93.60 | 94.70 | 91.10 | 91.30 | 92.70 | 94.10 | 90.50 | 90.70 | 92.10 | 93.70 | |||||||

| % FP | |||||||||||||||||||

| LAS | 3.80 | 9.70 | 41.00 | 42.90 | 1.30 | 4.00 | 15.00 | 12.90 | 0.60 | 2.40 | 8.60 | 7.80 | |||||||

| LASy | 3.70 | 8.30 | 34.60 | 37.30 | 1.30 | 3.40 | 12.60 | 11.20 | 0.60 | 2.10 | 7.60 | 7.00 | |||||||

| FaSel | 7.00 | 13.10 | 38.90 | 40.90 | 2.30 | 5.50 | 15.80 | 15.00 | 6.90 | 5.90 | 8.60 | 8.40 | |||||||

| ARMAr-LAS | 4.50 | 4.40 | 4.40 | 4.80 | 1.40 | 1.40 | 1.50 | 1.50 | 0.70 | 0.70 | 0.70 | 0.80 | |||||||

| SNR 1 | |||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| CoEr | |||||||||||||||||||

| LASy | 0.99 | 0.96 | 0.88 | 0.94 | 1.00 | 0.96 | 0.93 | 0.97 | 1.00 | 0.95 | 0.95 | 0.97 | |||||||

| FaSel | 1.18 | 1.19 | 2.15 | 2.29 | 1.07 | 1.10 | 1.86 | 1.91 | 4.12 | 3.10 | 1.74 | 1.76 | |||||||

| ARMAr-LAS | 1.11 | 1.03 | 0.86 | 0.88 | 1.09 | 1.02 | 0.95 | 0.96 | 1.10 | 1.02 | 0.98 | 0.99 | |||||||

| RMSFE | |||||||||||||||||||

| LASy | 0.98 | 0.89 | 0.79 | 0.81 | 0.99 | 0.91 | 0.91 | 0.85 | 1.00 | 0.91 | 0.85 | 0.87 | |||||||

| FaSel | 1.00 | 1.00 | 1.00 | 0.98 | 0.99 | 1.02 | 0.99 | 0.95 | 1.21 | 1.04 | 0.96 | 0.95 | |||||||

| ARMAr-LAS | 0.96 | 0.81 | 0.62 | 0.63 | 0.97 | 0.85 | 0.79 | 0.69 | 0.98 | 0.84 | 0.76 | 0.73 | |||||||

| % TP | |||||||||||||||||||

| LAS | 58.60 | 50.40 | 57.20 | 60.90 | 44.70 | 38.50 | 41.90 | 42.60 | 37.60 | 31.50 | 34.80 | 35.60 | |||||||

| LASy | 59.00 | 51.80 | 42.40 | 46.80 | 45.30 | 39.80 | 31.90 | 34.80 | 38.00 | 31.90 | 26.30 | 29.40 | |||||||

| FaSel | 4.40 | 13.00 | 50.80 | 55.00 | 3.70 | 10.00 | 37.40 | 41.00 | 63.10 | 48.20 | 32.30 | 34.60 | |||||||

| ARMAr-LAS | 62.10 | 63.30 | 65.40 | 69.20 | 48.60 | 50.30 | 53.50 | 57.80 | 40.30 | 42.40 | 46.50 | 52.30 | |||||||

| % FP | |||||||||||||||||||

| LAS | 12.50 | 15.40 | 42.60 | 44.70 | 6.00 | 7.90 | 18.80 | 17.70 | 3.70 | 4.80 | 10.40 | 9.90 | |||||||

| LASy | 12.70 | 14.30 | 22.40 | 26.20 | 6.10 | 6.90 | 10.20 | 10.90 | 3.70 | 4.10 | 6.00 | 6.50 | |||||||

| FaSel | 0.60 | 5.10 | 42.60 | 44.00 | 0.20 | 2.00 | 19.80 | 20.40 | 48.80 | 34.00 | 11.60 | 11.20 | |||||||

| ARMAr-LAS | 14.00 | 14.30 | 14.60 | 14.90 | 6.70 | 7.10 | 7.10 | 7.50 | 4.00 | 4.30 | 4.50 | 4.60 | |||||||

| SNR 5 | |||||||||||||||||||

| CoEr | |||||||||||||||||||

| LASy | 1.00 | 1.00 | 1.01 | 1.01 | 1.00 | 1.00 | 1.01 | 1.01 | 1.00 | 1.00 | 1.01 | 1.01 | |||||||

| FaSel | 1.33 | 1.23 | 1.44 | 1.43 | 1.20 | 1.15 | 1.25 | 1.17 | 2.39 | 1.75 | 1.19 | 1.12 | |||||||

| ARMAr-LAS | 0.93 | 0.80 | 0.65 | 0.61 | 0.94 | 0.84 | 0.72 | 0.65 | 0.95 | 0.85 | 0.74 | 0.69 | |||||||

| RMSFE | |||||||||||||||||||

| LASy | 1.00 | 0.97 | 0.93 | 0.94 | 1.00 | 0.98 | 0.96 | 0.95 | 1.00 | 0.97 | 0.95 | 0.97 | |||||||

| FaSel | 1.07 | 1.05 | 0.97 | 0.98 | 1.06 | 1.07 | 0.96 | 0.90 | 1.23 | 1.02 | 0.96 | 0.91 | |||||||

| ARMAr-LAS | 0.97 | 0.84 | 0.67 | 0.64 | 0.97 | 0.85 | 0.73 | 0.66 | 0.97 | 0.86 | 0.74 | 0.71 | |||||||

| % TP | |||||||||||||||||||

| LAS | 93.30 | 86.50 | 81.60 | 83.70 | 89.50 | 80.90 | 73.80 | 73.00 | 85.70 | 76.40 | 71.80 | 68.90 | |||||||

| LASy | 93.30 | 87.00 | 80.30 | 82.00 | 89.40 | 81.40 | 72.60 | 71.50 | 85.70 | 76.80 | 70.00 | 67.10 | |||||||

| FaSel | 53.90 | 61.40 | 73.50 | 76.50 | 51.80 | 55.90 | 71.70 | 75.90 | 82.70 | 73.70 | 71.80 | 71.10 | |||||||

| ARMAr-LAS | 94.70 | 95.30 | 95.60 | 96.50 | 91.20 | 90.90 | 92.10 | 94.30 | 88.20 | 87.50 | 90.50 | 91.60 | |||||||

| % FP | |||||||||||||||||||

| LAS | 16.50 | 20.10 | 42.90 | 46.50 | 8.40 | 10.90 | 16.70 | 14.40 | 5.40 | 6.80 | 9.90 | 8.40 | |||||||

| LASy | 16.30 | 18.90 | 37.80 | 41.90 | 8.30 | 10.30 | 14.80 | 12.90 | 5.40 | 6.40 | 8.80 | 7.60 | |||||||

| FaSel | 5.90 | 16.40 | 45.30 | 48.80 | 1.60 | 6.30 | 21.40 | 21.20 | 40.40 | 26.30 | 13.40 | 12.20 | |||||||

| ARMAr-LAS | 17.20 | 17.00 | 17.20 | 17.80 | 8.80 | 8.80 | 9.00 | 9.00 | 5.70 | 5.60 | 5.80 | 5.80 |

| DGPs (C) | DGPs (D) | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| n | 50 | 150 | 300 | 50 | 150 | 300 | |||

| CoEr | |||||||||

| LASSOy | 0.92 | 1.01 | 1.06 | 0.92 | 1.01 | 1.03 | |||

| FaSel | 1.50 | 1.84 | 1.90 | 2.12 | 2.09 | 2.00 | |||

| ARMAr-LAS | 0.62 | 0.76 | 0.81 | 0.60 | 0.71 | 0.76 | |||

| RMSFE | |||||||||

| LASSOy | 0.92 | 0.96 | 0.98 | 0.93 | 0.94 | 0.95 | |||

| FaSel | 1.37 | 1.28 | 1.23 | 1.31 | 1.43 | 1.48 | |||

| ARMAr-LAS | 0.65 | 0.73 | 0.77 | 0.66 | 0.71 | 0.74 | |||

| % TP | |||||||||

| LASSO | 79.80 | 80.60 | 80.60 | 76.60 | 70.40 | 65.10 | |||

| LASSOy | 78.50 | 79.40 | 80.20 | 73.90 | 68.30 | 63.60 | |||

| FaSel | 35.80 | 59.30 | 65.90 | 30.00 | 24.90 | 20.40 | |||

| ARMAr-LAS | 94.90 | 93.30 | 92.50 | 93.70 | 90.90 | 88.10 | |||

| % FP | |||||||||

| LASSO | 36.20 | 16.10 | 9.70 | 40.00 | 18.50 | 11.00 | |||

| LASSOy | 31.50 | 13.80 | 8.70 | 34.20 | 16.20 | 9.90 | |||

| FaSel | 12.30 | 7.60 | 5.00 | 10.20 | 3.90 | 2.20 | |||

| ARMAr-LAS | 7.80 | 2.40 | 1.20 | 19.20 | 9.20 | 5.80 | |||

4.2 Empirical Application

We consider Euro Area (EA) data composed by 309 monthly macroeconomic time series spanning the period between January 1997 and December 2018. The series are listed in Supplement F, grouped according to their measurement domain: Industry & Construction Survey (ICS), Consumer Confidence Indicators (CCI), Money & Interest Rates (M&IR), Industrial Production (IP), Harmonized Consumer Price Index (HCPI), Producer Price Index (PPI), Turnover & Retail Sale (TO), Harmonized Unemployment Rate (HUR), and Service Surveys (SI). Supplement F also reports transformations applied to the series to achieve stationarity (we did not attempt to identify or remove outliers). The target variable is the Overall EA Consumer Price Index (CPI), which is transformed as I(2) (i.e. integration of order 2) following Stock and Watson (2002b):

where , and is the forecasting horizon. We compute forecasts of at horizons and using a rolling -year window ; the models are re-estimated at each , adding one observation on the right of the window and removing one observation on the left. The last forecast is December 2018. The methods employed for our empirical exercise are:

-

•

Univariate AR(): the autoregressive forecasting model based on lagged values of the target variable, i.e. , which serves as a benchmark.

-

•

LASSO (Tibshirani, 1996): forecasts are obtained from the equation where is the sparse vector of penalized regression coefficients estimated by the LASSO, and .

-

•

FaSel (Fan et al., 2020): the FarmSelector that applies feature selection on factors residuals. The forecasting equation is where is a -dimensional vector of factors estimated with PCA (as in Stock and Watson (2002a, b)), , where is the matrix of loadings, and is the sparse vector obtained applying LASSO on . The number of factors is chosen with the approach described in Ahn and Horenstein (2013).

-

•

ARMAr-LASSO: our proposal, where LASSO is applied to the estimated ARMA residuals. Forecasts are obtained from the equation where is the sparse vector of penalized regression coefficients estimated by the LASSO on the estimated ARMA residuals, and .

For the AR() benchmark the lag order is selected by BIC within . For the ARMAr-LASSO, estimated residuals are obtained filtering each time series with an ARMA(), where and are selected by BIC within , . The shrinkage parameter of LASSO, FaSel and ARMAr-LASSO is also selected by BIC. Forecasting accuracy for all methods is evaluated using the root mean square forecast error (RMSFE), defined as

where and are the first and last time points used for the out-of-sample evaluation. For LASSO, FaSel and ARMAr-LASSO we also consider the number of selected variables. Table 4 reports ratios of RMSFEs between pairs of methods (RMSFE (ratio)), as well as significance of the corresponding Diebold-Mariano test (Diebold and Mariano, 1995). Furthermore, the column “Selected Varables (Av.)” reports the average number of selected variables with ARMAr-LASSO (on the left side of the vertical bar), and LASSO or FaSel (on the right side of the vertical bar). Notably, ARMAr-LASSO produces significantly better forecasts than the classical LASSO, FaSel and the AR(), and provides a more parsimonious model than the LASSO and FaSel. This is, in principle, consistent with the theoretical analysis we provided earlier. The sparser ARMAr-LASSO output may be due to fewer false positives, as compared to other LASSO-based methods – since the latter suffer from the effects of spurious correlations induced by serial correlation. However, since in this real data application we do not know the true DGP, any comments regarding accuracy in feature selection is necessarily speculative.

| Method 1 | Method 2 | RMSFE (ratio) | Selected Variables (Av.) | |||||||

|---|---|---|---|---|---|---|---|---|---|---|

| =12 | =12 | |||||||||

| ARMAr-LAS | LASSO | 0.69*** | 0.82* | 6.067.9 | 6.260.9 | |||||

| ARMAr-LAS | FarSel | 0.71*** | 0.73*** | 6.077.2 | 6.272.5 | |||||

| ARMAr-LAS | AR() | 0.94 | 0.89* | – | – | |||||

| LASSO | AR() | 1.36 | 1.08 | – | – | |||||

| FarSel | AR() | 1.31 | 1.21 | – | – | |||||

-

•

Note: For AR() coefficients are estimated using the R function lm. For ARMAr-LAS estimated residuals are obtained by means of an ARMA() filter. The penalty parameter is selected with BIC using the R package HDeconometrics.

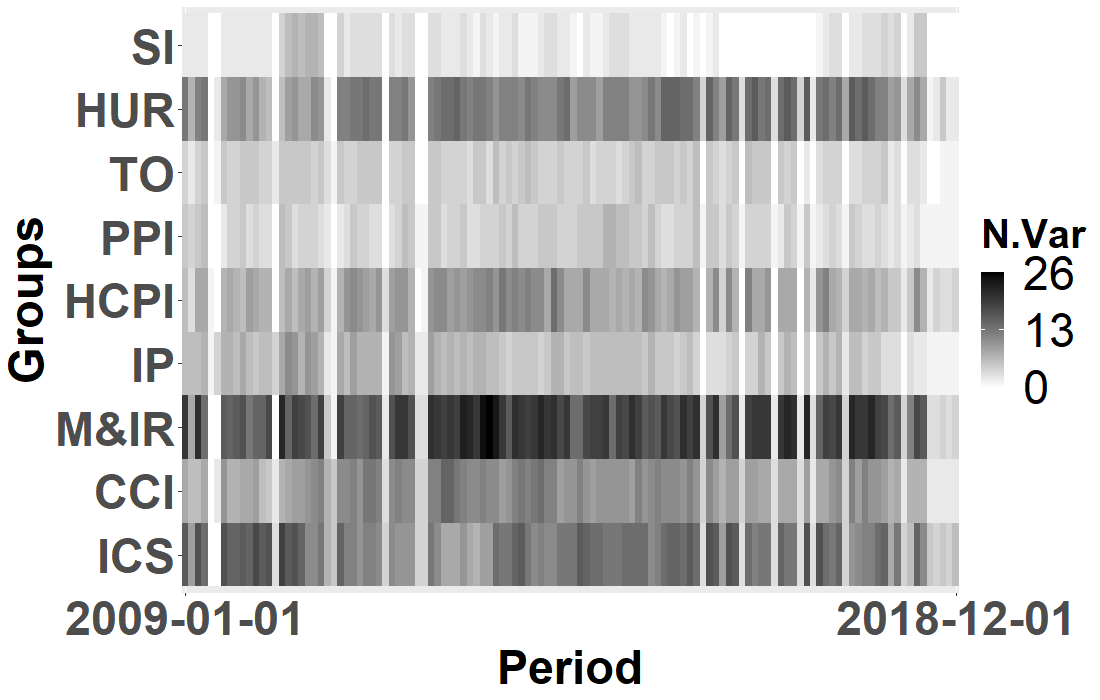

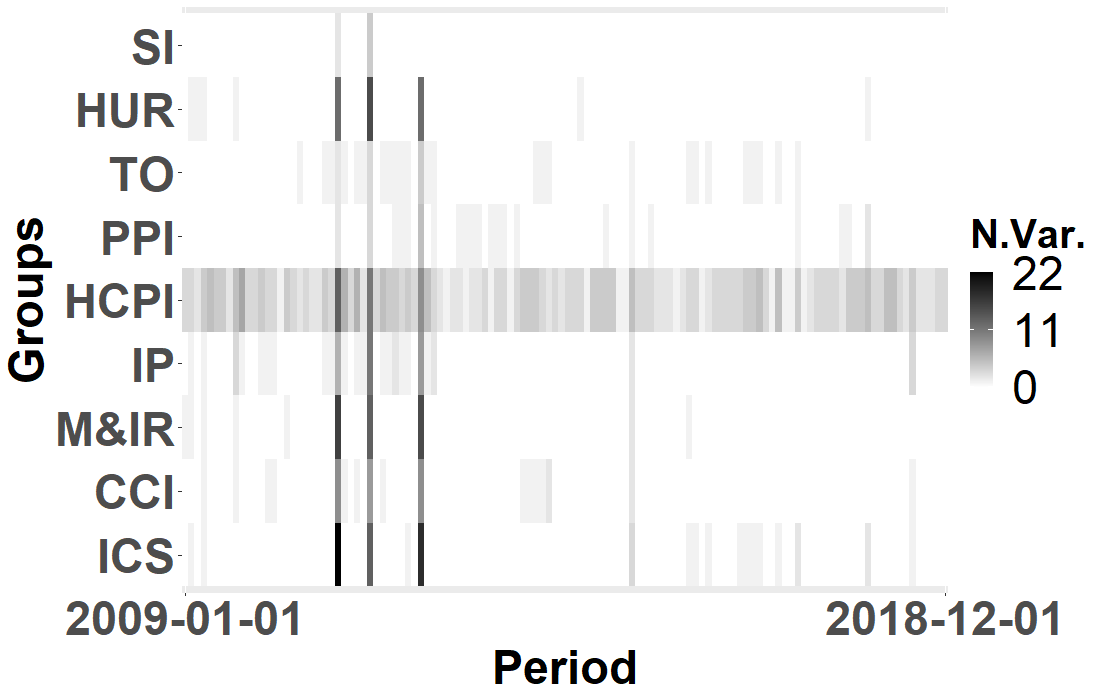

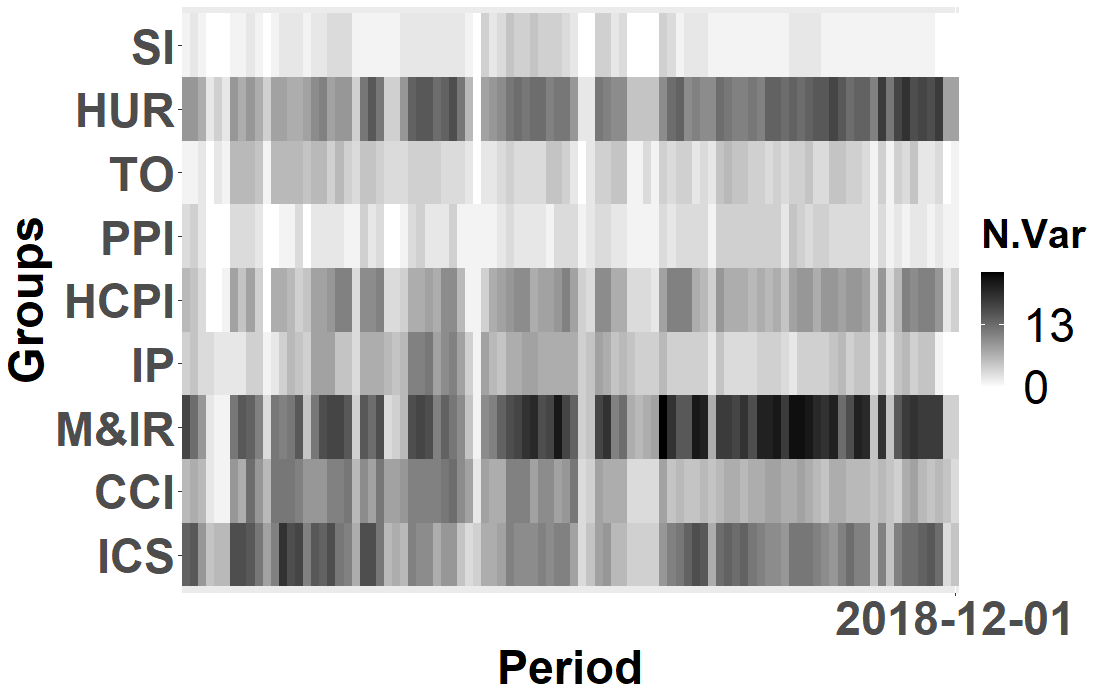

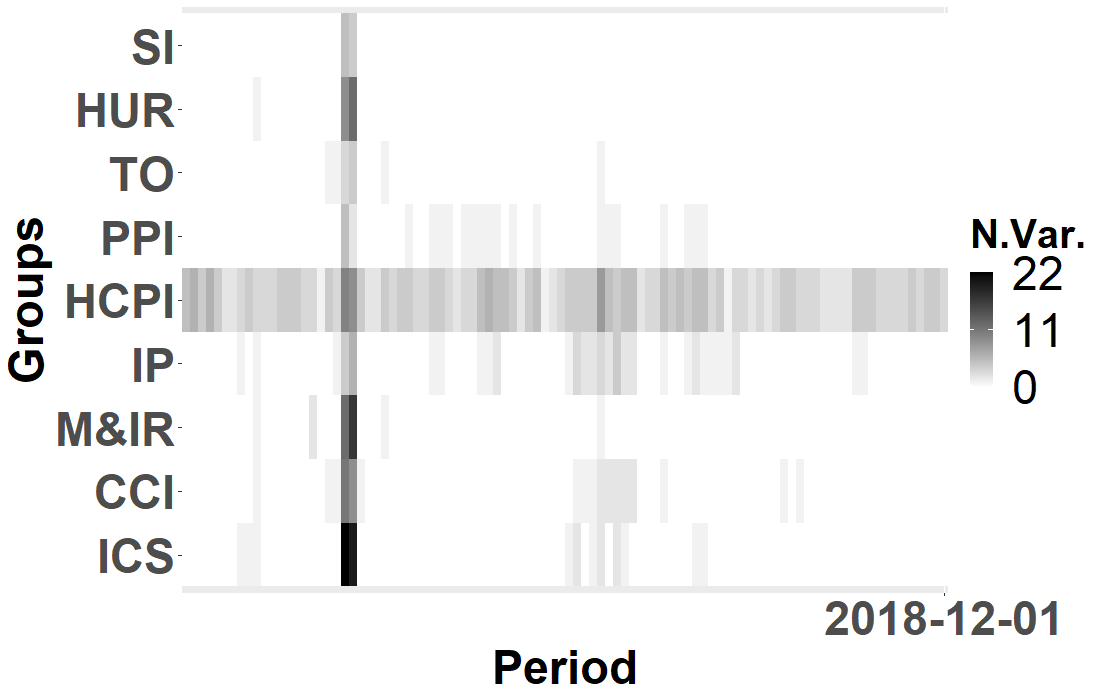

In terms of selected variables, Figure 2 summarizes patterns over time for LASSO and ARMAr-LASSO. The heatmaps represent the number of selected variables categorized according to the nine main domains (see above). LASSO selects variables largely, though not exclusively, from the domains ICS, M&IR and HUR. ARMAr-LASSO is more targeted, selecting variables in the HCPI domain. The top 5 variables in terms of selection frequency across forecasting samples are listed in Table 5. Regardless of the forecasting horizon , the top predictor for ARMAr-LASSO is the Goods Index. The other top predictors, also in the HCPI domain, include EA measurements (e.g., Services Index), or are specific to France and Germany (e.g., All-Items). In summary, ARMAr-LASSO exploits cross-sectional information mainly focusing on prices, and accrues a forecasting advantage – as LASSO uses many more variables to produce significantly worse forecasts.

| Rank | Selected Variables | |||

|---|---|---|---|---|

| =12 | ||||

| I° | Goods, Index | Goods, Index | ||

| 85.8% | 85.4% | |||

| II° | Industrial Goods, Index | Services, Index | ||

| 47.5% | 43.8% | |||

| III° | Services, Index | All-Items (De) | ||

| 40.8% | 35.4% | |||

| IV° | All-Items Excluding Tobacco, Index | All-Items Excluding Tobacco, Index | ||

| 32.5% | 32.3% | |||

| V° | All-Items (Fr) | Industrial Goods, Index | ||

| 24.2% | 30.2% | |||

5 Concluding Remarks

In this paper, we demonstrated that the probability of spurious correlations between stationary orthogonal or weakly correlated processes depends not only on the sample size, but also on the degree of predictors serial correlation. Through this result, we pointed out that serial correlation negatively affects the finite sample estimation and forecasting error bounds of LASSO. In order to improve the performance of LASSO in a time series context, we proposed an approach based on applying LASSO to pre-whitened (i.e., ARMA filtered) time series. This proposal relies on a working model that mitigates large spurious correlation and improves both estimation and forecasting accuracy. We characterized limiting distribution and feature selection consistency, as well as finite sample forecast and estimation error bounds, for our proposal. Furthermore, we assessed its performance through Monte Carlo simulations and an empirical application to Euro Area macroeconomic time series. Through simulations, we observed that ARMAr-LASSO, i.e., LASSO applied to ARMA residuals, reduces the probability of large spurious correlations and outperforms LASSO-based benchmarks from the literature applied to the original predictors in terms of both coefficient estimation and forecasting. The empirical application confirms that ARMAr-LASSO improves the forecasting performance of the benchmarks and produces more parsimonious models.

References

- Adamek et al. (2023) Adamek, R., S. Smeekes, and I. Wilms (2023). Lasso inference for high-dimensional time series. Journal of Econometrics 235(2), 1114–1143.

- Ahn and Horenstein (2013) Ahn, S. C. and A. R. Horenstein (2013). Eigenvalue ratio test for the number of factors. Econometrica 81(3), 1203–1227.

- Anderson (2003) Anderson, T. W. (2003). An Introduction to Multivariate Statistical Analysis (3rd ed.). New York.

- Baillie et al. (2024) Baillie, R. T., F. X. Diebold, G. Kapetanios, K. H. Kim, and A. Mora (2024, June). On robust inference in time series regression. Working Paper 32554, National Bureau of Economic Research.

- Bartlett (1935) Bartlett, M. S. (1935). Some aspects of the time-correlation problem in regard to tests of significance. j-J-R-STAT-SOC-SUPPL 98(3), 536–543.

- Belloni et al. (2013) Belloni, A., V. Chernozhukov, and C. Hansen (2013, 11). Inference on Treatment Effects after Selection among High-Dimensional Controls†. The Review of Economic Studies 81(2), 608–650.

- Bickel et al. (2009) Bickel, P. J., Y. Ritov, and A. B. Tsybakov (2009, Aug). Simultaneous analysis of lasso and dantzig selector. The Annals of Statistics 37(4), 1705–1732.

- Brockwell and Davis (1991) Brockwell, P. and R. Davis (1991). Time Series: Theory and Methods. Springer Series in Statistics. Springer.

- Brockwell and Davis (2002) Brockwell, P. J. and R. A. Davis (2002). Introduction to time series and forecasting. Springer.

- Bühlmann and van de Geer (2011) Bühlmann, P. and S. van de Geer (2011). Statistics for high-dimensional data. Springer Series in Statistics. Springer, Heidelberg. Methods, theory and applications.

- Chronopoulos et al. (2023) Chronopoulos, I., K. Chrysikou, and G. Kapetanios (2023). High dimensional generalised penalised least squares.

- Davidson (1994) Davidson, J. (1994). Stochastic limit theory: An introduction for econometricians. OUP Oxford.

- De Mol et al. (2008) De Mol, C., D. Giannone, and L. Reichlin (2008). Forecasting using a large number of predictors: Is bayesian shrinkage a valid alternative to principal components? Journal of Econometrics 146(2), 318–328.

- Diebold and Mariano (1995) Diebold, F. X. and R. S. Mariano (1995, July). Comparing Predictive Accuracy. Journal of Business & Economic Statistics 13(3), 253–263.

- Fan et al. (2014) Fan, J., F. Han, and H. Liu (2014, feb). Challenges of big data analysis. National Science Review 1(2), 293–314.

- Fan et al. (2020) Fan, J., Y. Ke, and K. Wang (2020). Factor-adjusted regularized model selection. Journal of Econometrics 216(1), 71 – 85. Annals Issue in honor of George Tiao: Statistical Learning for Dependent Data.

- Fan et al. (2018) Fan, J., Q.-M. Shao, and W.-X. Zhou (2018, Jun). Are discoveries spurious? distributions of maximum spurious correlations and their applications. The Annals of Statistics 46(3).

- Fan and Zhou (2016) Fan, J. and W.-X. Zhou (2016). Guarding against spurious discoveries in high dimensions. Journal of Machine Learning Research 17(203), 1–34.

- Forni et al. (2000) Forni, M., M. Hallin, M. Lippi, and L. Reichlin (2000). The generalized dynamic-factor model: Identification and estimation. The Review of Economics and Statistics 82(4), 540–554.

- Forni et al. (2005) Forni, M., M. Hallin, M. Lippi, and L. Reichlin (2005). The generalized dynamic factor model: One-sided estimation and forecasting. Journal of the American Statistical Association 100(471), 830–840.

- Forni and Lippi (2001) Forni, M. and M. Lippi (2001, 02). The generalized dynamic factor model: Representation theory. Econometric Theory 17, 1113–1141.

- Fu and Knight (2000) Fu, W. and K. Knight (2000). Asymptotics for lasso-type estimators. The Annals of Statistics 28(5), 1356 – 1378.

- Geyer (1996) Geyer, C. J. (1996). On the asymptotics of convex stochastic optimization. Unpublished manuscript 37.

- Glen et al. (2004) Glen, A. G., L. M. Leemis, and J. H. Drew (2004). Computing the distribution of the product of two continuous random variables. Computational Statistics & Data Analysis 44(3), 451–464.

- Granger et al. (2001) Granger, C., N. Hyung, and Y. Jeon (2001). Spurious regressions with stationary series. Applied Economics 33(7), 899–904.

- Granger and Newbold (1974) Granger, C. and P. Newbold (1974). Spurious regressions in econometrics. Journal of Econometrics 2(2), 111 – 120.

- Granger and Morris (1976) Granger, C. W. J. and M. J. Morris (1976). Time series modelling and interpretation. Journal of the Royal Statistical Society. Series A (General) 139(2), 246–257.

- Hansen (1991) Hansen, B. E. (1991). Strong laws for dependent heterogeneous processes. Econometric Theory 7, 213 – 221.

- Hansen and Liao (2019) Hansen, C. and Y. Liao (2019). The factor-lasso and k-step bootstrap approach for inference in high-dimensional economic applications. Econometric Theory 35(3), 465–509.

- Hansheng Wang and Jiang (2007) Hansheng Wang, G. L. and G. Jiang (2007). Robust regression shrinkage and consistent variable selection through the lad-lasso. Journal of Business & Economic Statistics 25(3), 347–355.

- Hastie (2015) Hastie, T. (2015). Statistical learning with sparsity : the lasso and generalizations. Chapman & Hall/CRC monographs on statistics & applied probability ; 143. Boca Raton, FL: CRC Press.

- Hsu et al. (2008) Hsu, N.-J., H.-L. Hung, and Y.-M. Chang (2008). Subset selection for vector autoregressive processes using lasso. Computational Statistics & Data Analysis 52(7), 3645–3657.

- James et al. (2013) James, G., D. Witten, T. Hastie, and R. Tibshirani (2013). An introduction to statistical learning: with applications in r.

- Jiang (2009) Jiang, W. (2009). On uniform deviations of general empirical risks with unboundedness, dependence, and high dimensionality. Journal of Machine Learning Research 10(4).

- Medeiros and F.Mendes (2012) Medeiros, M. C. and E. F.Mendes (2012, August). Estimating High-Dimensional Time Series Models. Textos para discussão 602, Department of Economics PUC-Rio (Brazil).

- Mizon (1995) Mizon, G. E. (1995). A simple message for autocorrelation correctors: Don’t. Journal of Econometrics 69(1), 267–288.

- Nardi and Rinaldo (2011) Nardi, Y. and A. Rinaldo (2011). Autoregressive process modeling via the lasso procedure. Journal of Multivariate Analysis 102(3), 528–549.

- Negahban et al. (2012) Negahban, S. N., P. Ravikumar, M. J. Wainwright, and B. Yu (2012, Nov). A unified framework for high-dimensional analysis of -estimators with decomposable regularizers. Statistical Science 27(4).

- Newey and West (1987) Newey, W. K. and K. D. West (1987). A simple, positive semi-definite, heteroskedasticity and autocorrelation consistent covariance matrix. Econometrica 55(3), 703–708.

- Proietti and Giovannelli (2021) Proietti, T. and A. Giovannelli (2021). Nowcasting monthly gdp with big data: A model averaging approach. Journal of the Royal Statistical Society Series A 184(2), 683–706.

- Reinsel (1993) Reinsel, G. (1993). Elements of Multivariate Time Series Analysis. Graduate Texts in Mathematics. Springer-Verlag.

- Robinson (1988) Robinson, P. M. (1988). Root-n-consistent semiparametric regression. Econometrica 56(4), 931–954.

- Stock and Watson (2002a) Stock, J. H. and M. W. Watson (2002a). Forecasting using principal components from a large number of predictors. Journal of the American Statistical Association 97(460), 1167–1179.

- Stock and Watson (2002b) Stock, J. H. and M. W. Watson (2002b). Macroeconomic forecasting using diffusion indexes. Journal of Business & Economic Statistics 20(2), 147–162.

- Stock and Watson (2008) Stock, J. H. and M. W. Watson (2008). Introduction to econometrics / James H. Stock, Mark W. Watson. (Brief ed. ed.). The Addison-Wesley series in economics. Pearson/Addison-Wesley.

- Stuart and Ord (1998) Stuart, A. and K. Ord (1998). Kendall’s advanced theory of statistics (Sixth ed.), Volume 1, Classical Inference and Relationship.

- Tibshirani (1996) Tibshirani, R. (1996). Regression shrinkage and selection via the lasso. Journal of the Royal Statistical Society Series B 58, 267–288.

- Wang et al. (2007) Wang, H., G. Li, and C.-L. Tsai (2007). Regression coefficient and autoregressive order shrinkage and selection via the lasso. Journal of the Royal Statistical Society Series B: Statistical Methodology 69(1), 63–78.

- Zhang and Zhang (2012) Zhang, C.-H. and T. Zhang (2012). A general theory of concave regularization for high-dimensional sparse estimation problems. Statistical Science, 576–593.

- Zhao and Yu (2006) Zhao, P. and B. Yu (2006, December). On model selection consistency of lasso. The Journal of Machine Learning Research 7, 2541–2563.

Supplement - On the Impact of Predictor Serial Correlation on the LASSO

Appendix A Upper Bound for

To support this argument, we start by recalling an inequality that links off-diagonal elements and eigenvalues of ; namely, Because of this, for any given we have

which emphasizes how the probability of a generic sample correlation being large in absolute value affects the probability of the minimum eigenvalue being small – and thus the estimation error bounds of the LASSO, as established by Bickel et al. (2009). As the next example shows, point the inequality can be easily fixed.

Example A.1:

Let and be vectors from the standard basis of , . Moreover, let , satisfying , and let be a correlation matrix with be the -th column. Then we have

Thus, for all and so

Appendix B Theoretical Results

B.1 Proof of Theorem 1

Consider a first order -variate autoregressive process , , where are the autoregressive coefficients where for each , and the autoregressive residuals are assumed to be . Here with , and , for .

In this setting, we focus on the density of the sample correlation coefficient defined as

where , since , . In particular, when , and , then

| (7) |

Note that is the least squares regression coefficient of on , and is the sum of the square of residuals of such regression. Thus, to derive the finite sample density of we need the sample densities of and .

Remark B.1:

In contrast to asymptotic statements, our theoretical analysis is intended to derive distributions and densities of estimators that hold for . Hence we will not employ the usual concepts of convergence in probability and in distribution; rather we will use a notion of approximation, whose “precision” needs to be evaluated. The precision of our approximations will be extensively tested under several finite scenarios in Supplement C.

Sample Distribution of .

We start by deriving the sample distribution of , the OLS regression coefficient for on . The same holds if we regress on .

Lemma B.1:

The sample distribution of is approximately .

Proof: We first focus on the distribution of the sample covariance between and , which is

| (8) |

where , for , and . Since and are standard Normal, we have (see Glen et al. 2004 and Supplement H)

Moreover, the quantity

is a linear combination of the sample covariances between the residual of a time series at time and the lagged residuals of the other time series. Note that is a linear combination of , . However, because , we can approximate as a linear combination of centered Normals with variance , so that

and

Since is times the sample variance of , . Therefore, is Normally distributed and, based on the approximation of mean and variance of a ratio (see Stuart and Ord 1998), we have and

Lemma B.1 shows that the OLS estimate is normally distributed with a variance that strongly depends on the degree of predictors serial correlation. In this context, it is common to adjust the standard error of the OLS to achieve consistency in the presence of heteroskedasticity and/or serial correlation; this leads, for instance, to the Heteroskedasticity and Autocorrelation Consistent (HAC) estimator of Newey and West (1987) (NW). However, NW estimates can be highly sub-optimal (or inefficient) in the presence of strong serial correlation (Baillie et al., 2024). In Supplement G we provide a simulation study to corroborate the result in Lemma B.1.

Sample Distribution of .

Here we derive the sample distribution of the sum of the square of residuals obtained by regressing on .

Lemma B.2:

The sample distribution of is approximately .

Proof: To obtain the sample distribution of we adapt Theorem 3.3.1 in Anderson (2003, p. 75) to the case of AR(1) processes.

Consider a orthogonal matrix with first row and let , , . We have

Then, from Lemma 3.3.1 in Anderson (2003, p. 76), we have

Thus, approximates the sum of Normal variables with variance . Now, let be the variable obtained by standardizing . We have

| (9) |

The right side of (9) is a Gamma distribution with shape parameter and rate parameter .

Sample Density of .

Note that and are independent. Using Lemmas B.1 and B.2 and Equation (7) we can now derive the density of the sample distribution of .

Because of Lemma B.1, is approximately . Let , and . In the reminder of the proof, we consider the distributions of and in Lemmas B.1 and B.2 as exact, not approximate. Thus, we have the densities

| (10) | ||||

| (11) |

We focus on

Now define and . Then

The integral on the right hand side can be represented by using the gamma function

Thus we obtain

Substituting with and with , we obtain the density

The density of is thus

Next, define , from which , and . We can use these quantities to write

Thus, the (finite) sample density of , taking the densities in (10) and (11) as exact, is

B.2 Proof of Theorem 2

Define where, . We note that is minimized at and

where

and

Since does not depend on , minimizing with respect to is equivalent to minimizing with respect to . Thus, in order to show that is the minimizer of it is sufficient to show that it is the minimizer of .

| (12) | ||||

| (13) | ||||

| (14) |

for all . Thus, we see that

By the Argmin Theorem (Geyer, 1996), we can claim that , which implies that , which would prove the Theorem. In what follows we show that for all . Note that

Recall that

As we have . Note that , has mean , autocovariance function such that , and autocorrelation coefficient such that . Thus, we can apply the CLT for dependent processes (see Brockwell and Davis 1991, ch. 7.3) to obtain

Therefore, where,

Applying Slutsky’s theorem, we have

Recall . When ,

that is a consequence of the assumption . Thus, when , we have to show that . Observe that

where the last equality is due to . Therefore

We can now say that . Hence

Using Slutsky’s theorem, and combining the two results, we have

which shows that

B.3 Proof of Theorem 3

Define two distinct events:

implies that the signs of the relevant predictors are correctly estimated, while and together imply that the signs of the irrelevant predictors are shrunk to zero. To show , it is sufficient to show that . Using the identity of we have that

Note that by the union bound, Markov’s inequality and the mixingale concentration inequality (see Hansen 1991, Lemma 2), we have that

| (15) |

Conducting a similar analysis for we obtain

B.4 Proof of Theorem 4

Before providing the proof of Theorem 4, we introduce some important definitions.

Definition B.1:

Let be a probability space and let and be sub--fields of . Then

is known as the strong mixing coefficient. For a sequence let and similarly define . The sequence is said to be -mixing (or strong mixing) if lim where

Definition B.2:

(Mixingale, Davidson (1994), ch. 16). The sequence of pairs in a filtered probability space where the are integrable r.v.s is called -mixingale if, for , there exist sequences of non-negative constants and such that as and

hold for all and . Furthermore, we say that is -mixingale of size - with respect to if for some .

Definition B.3:

(Near-Epoch Dependence, Davidson (1994), ch. 17). For a possibly vector-valued stochastic sequence , in a probability space let , such that is a non-decreasing sequence of -fields. If for a sequence of integrable r.v.s satisfies

where and is a sequence of positive constants, will be said to be near-epoch dependent in -norm (-NED) on . Furthermore, we say that is -NED of size - on if for some .

Note that we use the same notation for the constants and sequence as for the near-epoch dependence, since they play the same role in both types of dependence.

To simplify the analysis, we frequently make use of arbitrary positive finite constants , as well as of its sub-indexed version , whose values may change from line to line throughout the paper, but they are always independent of the time and cross-sectional dimension. Generic sequences converging to zero as are denoted by . We say a sequence is of size if for some .

Remark B.2:

Under Assumptions 1 and 2 of the main text the process is -NED of size , with , while the process is -NED of size , with . By Theorems 17.5 in ch.17 of Davidson (1994), they are also and -Mixingale, respectively. In later theorems, the NED order and sequence size are important for asymptotic rates. Assumption 5 requires to have slightly more moments than . More moments mean tighter error bounds and weaker tuning parameter conditions, but a high imposes stronger model restrictions. Under strong dependence, fewer moments are needed, and the reduction from to reflects the cost of allowing greater dependence through a smaller mixing rate.

The proof of Theorem 4 follows that of Theorem 1 in Adamek et al. (2023). We need of the two following auxiliary Lemmas.

Proof of Lemma B.3: By the union bound we have

Now, we apply the Triplex inequality (Jiang, 2009) and obtain

For the first term we have

so we need .

Without loss of generality, by assumptions 1, 2 and 4, as a consequence of the Cauchy-Schwarz inequality, and Theorems 17.5,17.8-17.10 in Davidson (1994), is -bounded and -mixingale with respect to , with non negative mixingale constants and mixingale sequence of size -, with . Therefore, for the Jensen inequality, we have that . Thus, for the second term we have

so we need .

For the third term, by Holder’s and Markov’s inequality we have that

so we need

We jointly bound the three terms by a sequence as follows:

First, note that . Moreover, we assume that . We isolate from the first and third terms

Since we have a lower and upper bound on , we need to make sure both bounds are satisfied:

Isolating , we have that Assuming , we have that and therefore we need to ensure that

| (16) |

Thus, when (16) is satisfied, and .

Note that under assumption 4 we have that , since , instead of , given that is a -mixingale of size .

Proof of Lemma B.4: By assumptions 1, 2, 5 and Theorems 17.5, 17.9 and 17.10 in Davidson (1994), we have that is an -mixingale of appropriate size. By the union bound, the Markov’s inequality and the Hansen’s mixingale concentration inequality, it follows that

This means that . The Lemma follows from choosing , for which .

B.5 Proof Theorem 5

The proof is based on the relevant contribution on LASSO oracle inequalities provided in Chapter 6 of Bühlmann and van de Geer (2011).

By Lemma 6.1 in Bühlmann and van de Geer (2011) we obtain

Note that the empirical process , i.e., the random part can be easily bounded in terms of the norm of the parameters, such that,

The penalty is chosen such that . The event has to hold with high probability, where . Lemma B.4 and Theorem 4 of the main text prove that and for some .

Since under and by Assumption 6, we can use the following dual norm inequality (Theorem 6.1 Bühlmann and van de Geer 2011)

which leads to

with probability at least . The result of the Theorem follows from choosing , for a large enough constant .

Appendix C Monte Carlo Experiments

In this Section, we conduct Monte Carlo experiments to assess numerically the approximation of the density of described in Section 2.1. After, we expand the theoretical results in more generic contexts, relaxing the assumption that the predictors are orthogonal Gaussian AR(1) processes. We indicate the density of obtained by simulations as .

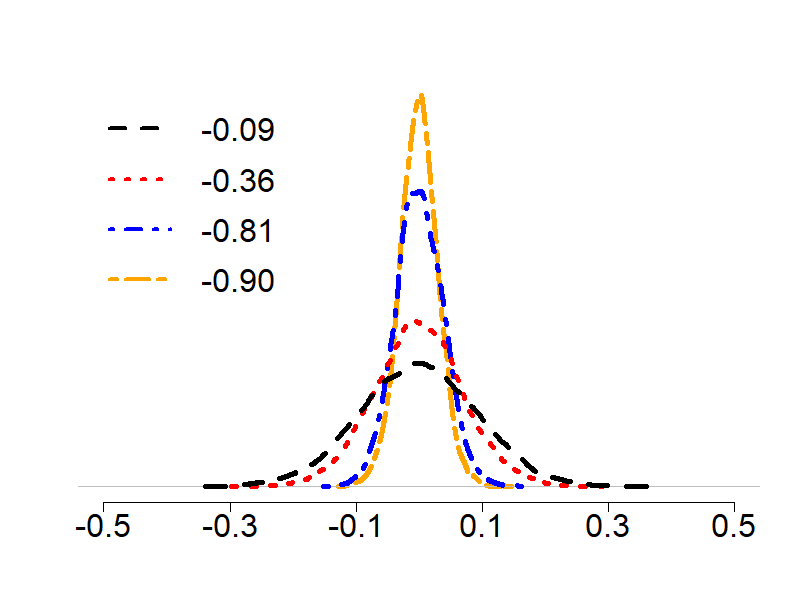

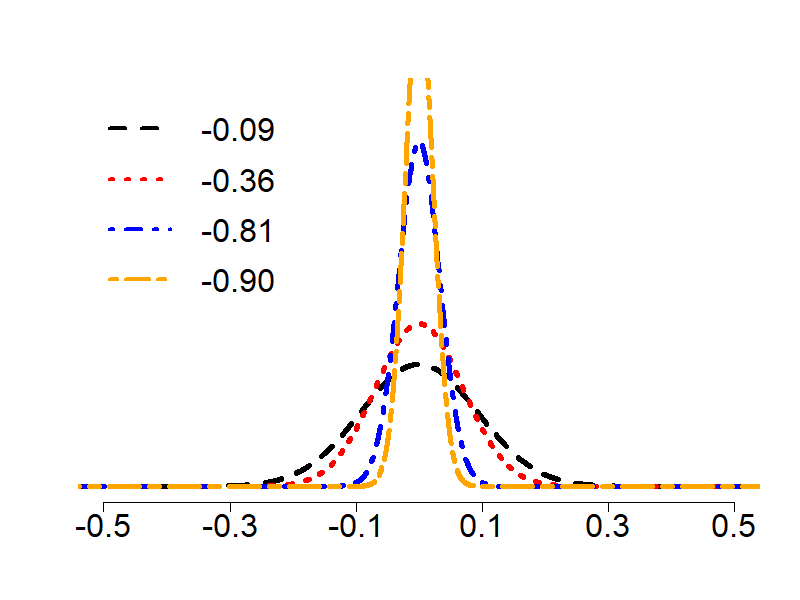

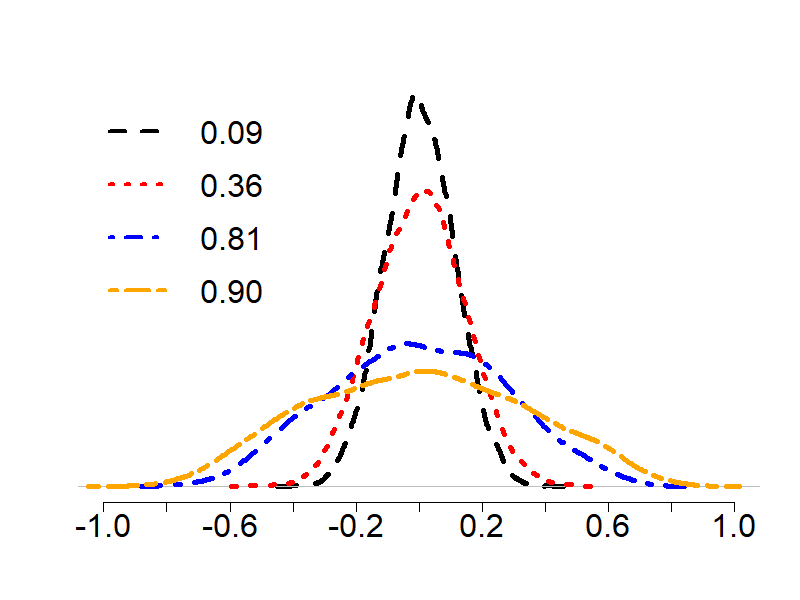

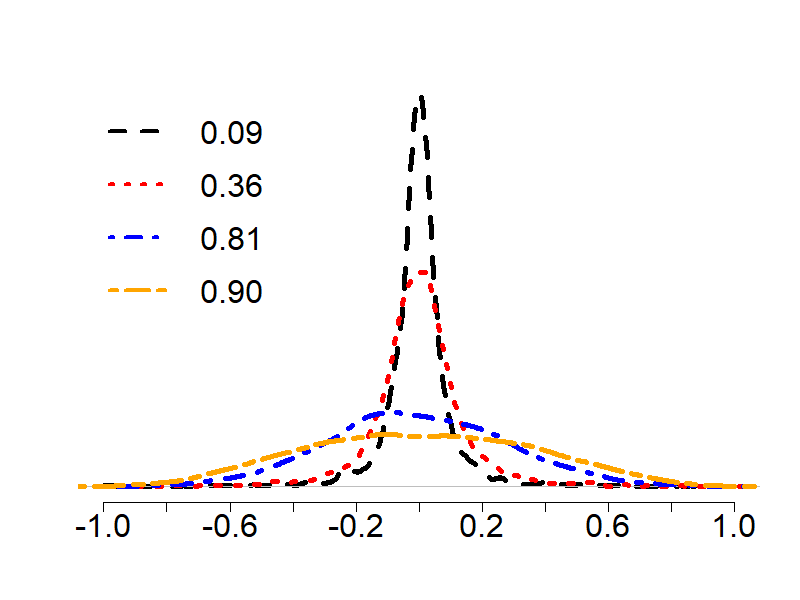

C.1 Numerical Approximation of to

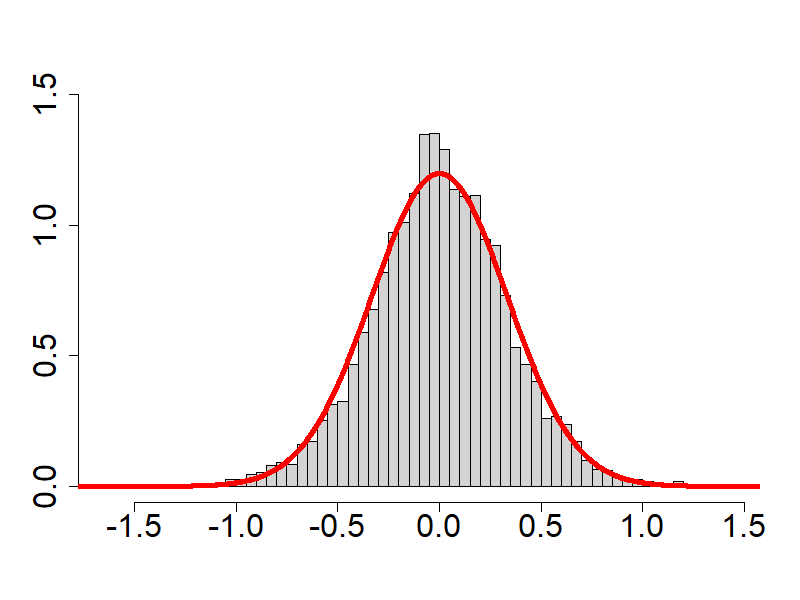

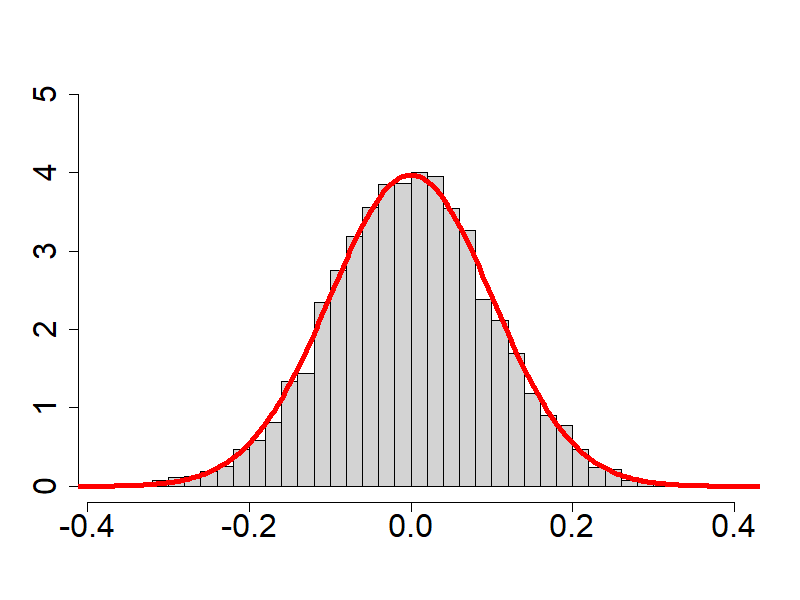

We generate data from the bivariate process for , where is a diagonal matrix with the same autocorrelation coefficient in both positions along the diagonal, and . We consider and – thus, the parameter in , here equal to , takes values 0.09, 0.36, 0.81, 0.90. The first row of Figure 3 (Plots (a), (b), (c)) shows, for various values of and , the density generated through 5000 Monte Carlo replications. The second row of Figure 3 (Plots (d), (e), (f)) shows the corresponding . These were plotted using 5000 values of the argument starting at -1 and increasing by steps of size 0.0004 until 1. As expected, we observe that the degree of approximation of to improves as increases and/or decreases. In particular, Plots (a) and (d) in Figure 3, where , show that approximates well for a low-to-intermediate degree of serial correlation (, i.e. ). In contrast, in cases with high degree of serial correlation (, i.e. ), has larger tails compared to ; that is, the latter over-estimates the probability of large spurious correlations. However, it is noteworthy that the difference between the two densities is negligible for (Figure 3, Plots (b) and (e) for , and Plots (c) and (f) for ), also with high degree of serial correlation (, i.e. ). These numerical experiments corroborate the fact that the sample cross-correlation between orthogonal Gaussian AR(1) processes is affected by the degree of serial correlation in a way that is well approximated by . In fact, for a sufficiently large finite , we observe that , , increases with in a similar way for and .

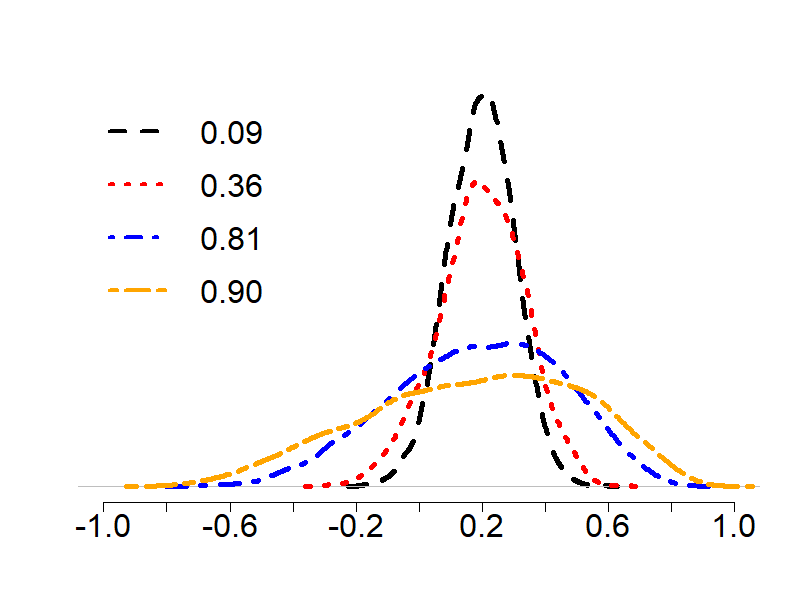

The Impact of

In Section 2.1 of the main text we pointed out that the impact of on depends on . In particular, when , an increment on makes the density of more concentrated around . In order to validate this result, we run simulations with and different values for the second element of the diagonal of ; namely, . Results are shown in Plots (a) and (b) of Figure 4. In this case, we see that when and increases, increases its concentration around in a way that is, again, well approximated by .

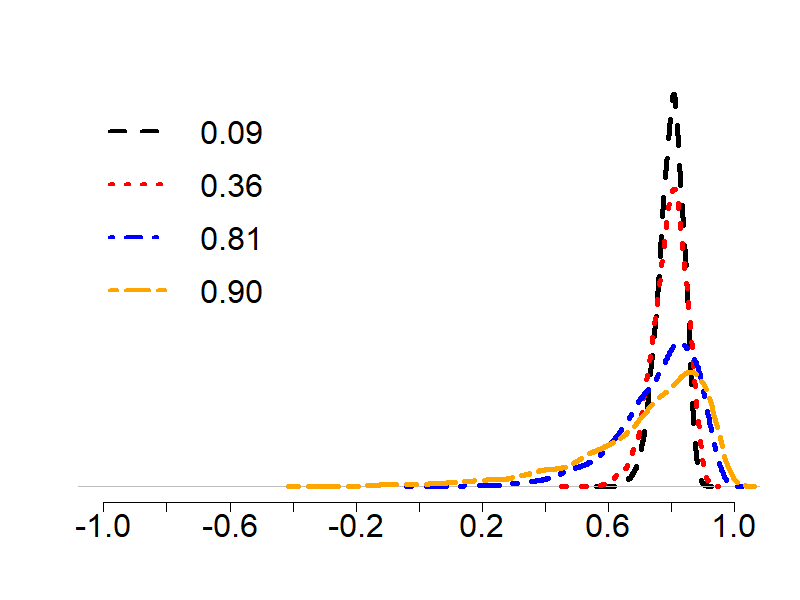

C.2 General Case

To generalize our findings to the case of non-Gaussian weakly correlated AR and ARMA processes, we generate predictors according to the following DGPs: , and , where and . Moreover, we generate and from a bivariate Laplace distribution with means , variances , and . In these more general cases, we do not know an approximate theoretical density for . Therefore, we rely entirely on simulations to show the effect of serial correlation on . Plot (c) of Figure 4 shows obtained from 5000 Monte Carlo replications for the different values of . In short, also in the more general cases where predictors are non-Gaussian, weakly correlated AR(3) and ARMA(2,1) processes, the probability of getting large sample cross-correlations depends on the degree of serial correlation. More simulation results are provided below.

C.3 More General Cases

We study the density of in three different cases: non-Gaussian processes; weakly and high cross-correlated processes; and ARMA processes with different order. Note that for the first two cases the variables are AR(1) processes with and autocorrelation coefficient . Since we do not have for these cases, we rely on the densities obtained on 5000 Monte Carlo replications, i.e. , to show the effect of serial correlation on .

The Impact of non-Gaussianity

The theoretical contribution reported in Section 2.1 requires the Gaussianity of and . With the following simulation experiments we show that the impact of on the density of is relevant also when and are non-Gaussian random variables. To this end, we generate and from the following distributions: Laplace with mean 0 and variance 1 (case (a)); Cauchy with location parameter 0 and scale parameter 1 (case (b)); and from a -student with 1 degree of freedom (case (c)). Figure 5 reports the results of the simulation experiment. We can state that regardless the distribution of the processes, whenever , the probability of large values of increases with . As a curiosity, this result is more evident for the case of Laplace variables, whereas for Cauchy and -student the effect of declines.

The Impact of Population Cross-Correlation

Since orthogonality is an unrealistic assumption for most economic applications, here we admit population cross-correlation. In Figure 6 we report when the processes are weakly cross-correlated with , and when the processes are multicollinear with (usually we refer to multicollinearity when ). We observe that the impact of on depends on the degree of (population) cross-correlation as follows. In the case of weakly correlated processes, an increase in yields a high probability of observing large sample correlations in absolute value. In the case of multicollinear processes, on the other hand, an increase in leads to a high probability of underestimating the true population cross-correlation.

Density of in the case of ARMA processes

To show the effect of serial correlation on a more general case, we generate and through the following ARMA processes

where and . In Figure 7 we report the density of in the case of and . With no loss of generality we can observe that gets larger as increases, that is increases with .

Appendix D Least Square Applied to Working Model

Here, we describe two asymptotic results on estimation and forecasting performance of the non-penalized fit, which we prove under strong simplifying assumptions and validate in more general settings through simulations in Section 4. The following Proposition describes the asymptotic behavior of the non-penalized, least square fit of working model (4) in terms of estimation.

Proposition D.1:

Let , for each . Moreover, let be the variance of and be the asymptotic coefficient of determination, where . As , the least squares estimates for model (4) converge as follows: .

Proof: To simplify notation, we report results in matrix form, where the subscript denotes the corresponding matrix or vector of period lagged values. We start with the case of common AR(1) restriction. We consider the following model . As a consequence of Assumption 2 in the text of the main paper:

Let:

Moreover, .

Our working model consists in using as regressors of the OLS model to obtain and . We have the following preliminary results:

Thus,

and applying the preliminary results above gives:

from which

After some algebra we get:

The results holds for . Note that in the case of a common AR(1) restriction with a common factor, the proof follows by considering the same procedure where , where and are the fraction of variance of explained by (the common factor) and (the idiosyncratic component), respectively.

D.1 Monte Carlo Experiments: ARMAr-OLS

In this section, we validate the theoretical properties of our working model within an asymptotic, non-sparse context, by estimating it with the OLS. We refer to it as ARMAr-OLS. We set , and for . We then conduct a comparative analysis between OLS applied to ’s and ARMAr-OLS. We first simulate , where where , with , and . We investigate different situations with . Table 6 presents the average on 1000 simulations of root mean square forecast error (RMSFE) and coefficient estimation error (CoEr) of ARMAr-OLS relative to OLS for various values of under the common AR(1) restriction when and when . We observe an improvement in RMSFE for ARMAr-OLS over OLS as , due to the SNR in ARMAr-OLS, which also results in more accurate coefficient estimates. To generalize these results, we conduct a new simulation study where ; ; ; ; , for . The error term follows an AR(2) pattern, . The results are now reported in Table 7 and show that, also in a general setting out-off the common AR(1) restriction, our working model maintains an advantage in both coefficient estimation and forecasting compared to the classical OLS applied to the ’s.

| 0.3 | 0.6 | 0.9 | 0.95 | 0.3 | 0.6 | 0.9 | 0.95 | ||

|---|---|---|---|---|---|---|---|---|---|

| RMSFE | 0.96 | 0.79 | 0.44 | 0.32 | 0.95 | 0.79 | 0.46 | 0.31 | |

| CoEr | 0.93 | 0.74 | 0.36 | 0.26 | 0.94 | 0.72 | 0.35 | 0.25 | |

| RMSFE | 0.60 | 0.57 |

| CoEr | 0.14 | 0.29 |

Appendix E Experiments

| n | 50 | 150 | 300 | ||||||||||||||||

| 0.3 | 0.6 | 0.9 | 0.95 | 0.3 | 0.6 | 0.9 | 0.95 | 0.3 | 0.6 | 0.9 | 0.95 | ||||||||

| SNR | |||||||||||||||||||

| RMSFE | |||||||||||||||||||

| LASSOy | 0.98 | 0.88 | 0.73 | 0.74 | 0.99 | 0.89 | 0.80 | 0.80 | 0.99 | 0.89 | 0.83 | 0.83 | |||||||

| FaSel | 0.96 | 0.97 | 0.95 | 0.95 | 0.97 | 0.96 | 0.96 | 0.95 | 0.88 | 0.92 | 0.95 | 0.94 | |||||||

| ARMAr-LAS | 0.98 | 0.83 | 0.62 | 0.62 | 0.98 | 0.86 | 0.72 | 0.70 | 0.99 | 0.84 | 0.75 | 0.72 | |||||||

| % TP | |||||||||||||||||||

| LASSO | 46.70 | 43.70 | 55.10 | 57.40 | 43.20 | 39.80 | 46.10 | 47.80 | 40.30 | 37.40 | 44.50 | 45.20 | |||||||

| 0.5 | LASSOy | 47.50 | 44.20 | 36.90 | 38.60 | 44.10 | 40.10 | 34.70 | 37.80 | 40.70 | 38.20 | 33.50 | 35.70 | ||||||

| FaSel | 7.90 | 11.40 | 42.10 | 44.00 | 18.30 | 25.10 | 39.40 | 44.80 | 39.20 | 36.00 | 41.70 | 45.40 | |||||||

| ARMAr-LAS | 49.90 | 51.80 | 54.60 | 58.10 | 45.90 | 47.80 | 51.00 | 54.80 | 42.50 | 45.10 | 48.00 | 52.20 | |||||||

| % FP | |||||||||||||||||||

| LASSO | 2.20 | 7.00 | 42.60 | 45.40 | 0.70 | 3.00 | 17.90 | 17.40 | 0.40 | 1.80 | 10.00 | 9.60 | |||||||

| LASSOy | 2.40 | 4.00 | 11.10 | 16.10 | 0.70 | 1.40 | 5.20 | 7.20 | 0.40 | 0.80 | 3.20 | 4.20 | |||||||

| FaSel | 1.20 | 5.00 | 37.10 | 38.80 | 0.70 | 2.90 | 16.20 | 17.20 | 11.60 | 9.30 | 9.90 | 9.60 | |||||||

| ARMAr-LAS | 2.70 | 2.90 | 3.30 | 3.10 | 0.80 | 1.00 | 1.10 | 1.00 | 0.50 | 0.50 | 0.50 | 0.50 | |||||||

| RMSFE | |||||||||||||||||||

| LASSOy | 0.98 | 0.90 | 0.79 | 0.80 | 0.99 | 0.89 | 0.90 | 0.83 | 0.99 | 0.92 | 0.89 | 0.89 | |||||||

| FaSel | 0.97 | 0.97 | 0.94 | 0.94 | 0.97 | 0.98 | 0.97 | 0.93 | 0.89 | 0.94 | 0.93 | 0.95 | |||||||

| ARMAr-LAS | 0.97 | 0.83 | 0.62 | 0.63 | 0.96 | 0.82 | 0.73 | 0.67 | 0.99 | 0.84 | 0.76 | 0.73 | |||||||

| % TP | |||||||||||||||||||

| LASSO | 61.10 | 56.70 | 60.90 | 62.90 | 58.80 | 54.00 | 56.60 | 57.20 | 57.20 | 52.50 | 54.90 | 56.80 | |||||||

| 1 | LASSOy | 61.70 | 57.10 | 51.70 | 52.50 | 59.00 | 54.10 | 49.60 | 51.80 | 57.40 | 52.40 | 48.60 | 52.00 | ||||||

| FaSel | 12.60 | 16.60 | 44.50 | 49.10 | 29.60 | 37.20 | 49.60 | 54.80 | 51.20 | 48.40 | 52.50 | 57.40 | |||||||

| ARMAr-LAS | 64.70 | 65.60 | 68.10 | 71.10 | 61.50 | 62.20 | 65.10 | 68.00 | 59.60 | 60.00 | 62.80 | 67.40 | |||||||

| % FP | |||||||||||||||||||

| LASSO | 2.70 | 7.70 | 42.00 | 44.40 | 1.00 | 3.40 | 17.40 | 16.30 | 0.40 | 2.00 | 9.60 | 9.40 | |||||||

| LASSOy | 2.80 | 5.00 | 19.50 | 24.20 | 1.00 | 1.80 | 8.10 | 9.50 | 0.40 | 1.00 | 4.70 | 6.00 | |||||||

| FaSel | 2.20 | 6.20 | 36.90 | 39.70 | 0.80 | 3.60 | 16.30 | 16.60 | 11.50 | 7.30 | 9.30 | 9.30 | |||||||

| ARMAr-LAS | 3.20 | 3.60 | 3.80 | 3.90 | 1.10 | 1.10 | 1.20 | 1.30 | 0.50 | 0.50 | 0.60 | 0.60 | |||||||

| RMSFE | |||||||||||||||||||

| LASSOy | 1.00 | 0.97 | 0.92 | 0.94 | 1.00 | 0.97 | 0.98 | 0.94 | 1.00 | 0.98 | 0.96 | 0.97 | |||||||

| FaSel | 0.99 | 1.01 | 0.95 | 0.97 | 0.96 | 0.99 | 0.94 | 0.89 | 0.92 | 0.95 | 0.93 | 0.95 | |||||||

| ARMAr-LAS | 0.98 | 0.85 | 0.64 | 0.63 | 0.98 | 0.83 | 0.71 | 0.67 | 0.98 | 0.85 | 0.73 | 0.74 | |||||||

| % TP | |||||||||||||||||||

| LASSO | 90.70 | 84.60 | 80.50 | 82.60 | 89.80 | 84.00 | 80.60 | 81.40 | 88.90 | 83.20 | 81.90 | 81.60 | |||||||

| 5 | LASSOy | 90.70 | 85.20 | 79.40 | 81.30 | 89.80 | 84.10 | 79.90 | 80.90 | 89.00 | 83.50 | 81.10 | 81.00 | ||||||

| FaSel | 27.50 | 34.10 | 58.50 | 64.30 | 57.30 | 65.80 | 77.00 | 81.90 | 81.10 | 79.20 | 81.30 | 83.90 | |||||||

| ARMAr-LAS | 92.70 | 92.40 | 93.60 | 94.70 | 91.10 | 91.30 | 92.70 | 94.10 | 90.50 | 90.70 | 92.10 | 93.70 | |||||||

| % FP | |||||||||||||||||||

| LASSO | 3.80 | 9.70 | 41.00 | 42.90 | 1.30 | 4.00 | 15.00 | 12.90 | 0.60 | 2.40 | 8.60 | 7.80 | |||||||

| LASSOy | 3.70 | 8.30 | 34.60 | 37.30 | 1.30 | 3.40 | 12.60 | 11.20 | 0.60 | 2.10 | 7.60 | 7.00 | |||||||

| FaSel | 7.00 | 13.10 | 38.90 | 40.90 | 2.30 | 5.50 | 15.80 | 15.00 | 6.90 | 5.90 | 8.60 | 8.40 | |||||||

| ARMAr-LAS | 4.50 | 4.40 | 4.40 | 4.80 | 1.40 | 1.40 | 1.50 | 1.50 | 0.70 | 0.70 | 0.70 | 0.80 | |||||||

| RMSFE | |||||||||||||||||||

| LASSOy | 1.00 | 0.98 | 0.96 | 0.95 | 1.00 | 0.98 | 0.97 | 0.95 | 1.00 | 0.99 | 0.99 | 0.99 | |||||||

| FaSel | 1.01 | 0.95 | 0.95 | 0.95 | 1.02 | 0.98 | 0.92 | 0.89 | 0.92 | 0.94 | 0.91 | 0.90 | |||||||

| ARMAr-LAS | 0.97 | 0.80 | 0.63 | 0.62 | 0.97 | 0.84 | 0.70 | 0.63 | 0.99 | 0.84 | 0.74 | 0.68 | |||||||

| % TP | |||||||||||||||||||

| LASSO | 97.60 | 94.20 | 89.40 | 90.60 | 97.40 | 93.20 | 90.20 | 88.80 | 97.20 | 93.60 | 91.20 | 90.00 | |||||||

| 10 | LASSOy | 97.60 | 94.40 | 89.30 | 90.60 | 97.40 | 93.40 | 89.80 | 88.20 | 97.20 | 93.60 | 90.60 | 89.50 | ||||||

| FaSel | 35.50 | 45.60 | 65.70 | 72.30 | 67.10 | 77.50 | 88.60 | 90.60 | 90.00 | 90.10 | 90.90 | 92.60 | |||||||

| ARMAr-LAS | 98.30 | 98.40 | 98.50 | 98.80 | 98.10 | 98.00 | 98.20 | 98.70 | 97.70 | 97.80 | 98.10 | 98.60 | |||||||