AlAli and Ararat

Systemic Values-at-Risk

Systemic Values-at-Risk and their Sample-Average Approximations

Wissam AlAli

\AFFDepartment of Industrial Engineering, University of Houston, Houston, TX,

\EMAILwialali@uh.edu \AUTHORÇağın Ararat

\AFFDepartment of Industrial Engineering, Bilkent University, Ankara, Turkey,

\EMAILcararat@bilkent.edu.tr

This paper investigates the convergence properties of sample-average approximations (SAA) for set-valued systemic risk measures. We assume that the systemic risk measure is defined using a general aggregation function with some continuity properties and value-at-risk applied as a monetary risk measure. We focus on the theoretical convergence of its SAA under Wijsman and Hausdorff topologies for closed sets. After building the general theory, we provide an in-depth study of an important special case where the aggregation function is defined based on the Eisenberg-Noe network model. In this case, we provide mixed-integer programming formulations for calculating the SAA sets via their weighted-sum and norm-minimizing scalarizations. To demonstrate the applicability of our findings, we conduct a comprehensive sensitivity analysis by generating a financial network based on the preferential attachment model and modeling the economic disruptions via a Pareto distribution.

Systemic risk measure, Eisenberg-Noe model, value-at-risk, sample-average approximation, Hausdorff convergence.

1 Introduction

1.1 Background and Literature Review

Systemic risk refers to potential disturbances within the financial system that can spread across institutions, markets, and economies, causing adverse outcomes. This often triggers a cascading sequence leading to financial contagion. Hence, recognizing the potential repercussions underscores the importance of proactive measures and risk management strategies.

Risk management has gained substantial attention, particularly after the swift onset of the 2008 financial crisis. This crisis, marked by the rapid devaluation of mortgage-related securities, impacted both the United States and global financial systems, leading to the downfall of numerous prominent institutions (Kotz 2009). It underscored the profound interconnectedness of global financial systems, illustrating how minor shocks can generate significant disruptions in the economy (Silva et al. 2017).

Recent research has introduced innovative ideas on systemic risk measures and allocation methods, focusing on breaking down such measures into an aggregation function and a monetary risk measure (Chen et al. 2013, Kromer et al. 2016). The aggregation function gauges societal impact, while capital allocations, representing potential bailout costs, are added post-aggregation. A noteworthy framework assigns capital allocations to institutions before aggregation, as discussed in Feinstein et al. (2017), Biagini et al. (2019b), Armenti et al. (2018), proving particularly useful for regulatory purposes and crisis prevention. These models yield multivariate risk measures based on the set of feasible capital allocations.

The intriguing aspect of systemic risk lies in its connection to complex interconnections among organizations, rather than individual entities. Traditional risk measures such as value-at-risk, conditional value-at-risk, and negative expectation are adequate when risk is solely tied to a single firm’s performance, irrespective of its interconnections. However, systemic risk demands a broader view, requiring an analysis of the distribution of total profits and losses across all firms in the economy, as exemplified in Acharya et al. (2012), Tarashev et al. (2010), Adrian and Brunnermeier (2016), Amini et al. (2020), Brunnermeier and Cheridito (2019).

In this paper, we focus on financial networks where members are interconnected through contractual obligations, and interbank payments are determined by a clearing process based on uncertain operating cash flows. The model in Eisenberg and Noe (2001) depicts a financial system as a static directed network of banks with specified interbank liabilities. They propose two methods for calculating a clearing vector, representing payments to fulfill interbank obligations, assuming positive operating cash flows for each bank. The first method, the fictitious default algorithm, iteratively computes the clearing vector through a finite number of updates. The second approach formulates a concise continuous optimization problem based on liabilities, operating cash flows, and an increasing arbitrary objective function, yielding a linear programming problem when a linear objective function is selected.

The fictitious default algorithm is widely preferred by researchers working on financial network models. In Suzuki (2002), a similar method for evaluating clearing vectors is proposed, expanding on Eisenberg and Noe (2001) and considering cross-shareholdings. In Cifuentes et al. (2005), systemic risk is examined in terms of institution liquidity and asset price instability. The model in Elsinger (2009) extends the Eisenberg-Noe model by integrating a cross-holdings structure, relaxing the assumption of positive cash flows and exploring the model under certain seniority assumptions. In Rogers and Veraart (2013), default costs are introduced to the Eisenberg-Noe model, and the necessity of bailing out delinquent institutions is investigated. A comprehensive network model is developed in Weber and Weske (2017) by incorporating cross-holdings, fire sales, and bankruptcy costs simultaneously. We refer the reader to Kabanov et al. (2018) for a detailed overview of these models and algorithms for calculating clearing vectors. Recently, in Ararat and Meimanjan (2023), an extension of the Rogers-Veraart model is proposed in which the operating cash flows are unrestricted in sign. In contrast to these works, the focus in Ararat and Meimanjan (2023) is on the mathematical programming approach rather than fixed point algorithms, and it is shown that one can find a clearing vector for the Rogers-Veraart model by solving a mixed-integer linear programming problem.

The operating cash flows of the network members often face uncertainty due to correlated risk factors, represented as a random vector with possibly correlated components. The resulting clearing vector becomes a deterministic function of this random operating cash flow vector, determined by the clearing mechanism. Building on this concept, recent research initiated in Chen et al. (2013) focuses on defining systemic risk measures capturing necessary capital allocations for network members to control certain (non-linear) averages across scenarios. By utilizing the clearing mechanism, a random aggregate quantity associated with the clearing vector—such as total debt paid or total equity generated—is defined. This quantity serves as a deterministic and scalar aggregation function of the operating cash flow vector. In Chen et al. (2013), a systemic risk measure is defined as a scalar functional of the operating cash flow vector, quantifying the risk of the random aggregate quantity using convex risk measures like negative expected value, average value-at-risk, or entropic risk measure.

The systemic risk measure in Chen et al. (2013) denotes the total capital requirement for the system to maintain an acceptable risk level for the aggregate quantity. Since this total capital is only deployed after the shock is aggregated, allocating it back to system members poses an unresolved question, requiring a separate procedure. To address this, set-valued and scalar systemic risk measures that are sensitive to capital levels are proposed in Feinstein et al. (2017) and Biagini et al. (2019b), respectively. These functionals aim to identify deterministic capital allocation vectors directly complementing the random operating cash flow vector. The augmented cash flow vector is aggregated, and the risk of the resulting random aggregate quantity is controlled using a convex risk measure, akin to Chen et al. (2013). The set-valued systemic risk measure in Feinstein et al. (2017) represents the set of all feasible capital allocation vectors, treating the measurement and allocation of systemic risk as a joint problem.

When the underlying aggregation function is suitably simple, the sensitive systemic risk measures studied in Feinstein et al. (2017) and Biagini et al. (2019b) exhibit advantageous theoretical properties. In Ararat and Rudloff (2020), assuming a monotone and concave aggregation function and a convex base risk measure, it is shown that the set-valued sensitive systemic risk measure becomes a convex set-valued risk measure according to the framework in Hamel et al. (2011), and dual representations are obtained in terms of the conjugate function of the aggregation function.

The computation of set-valued risk measures is usually handled by formulating an associated vector optimization problem whose upper image gives the risk measure; see Hamel et al. (2013), Feinstein and Rudloff (2017), Löhne and Rudloff (2014). In Ararat and Meimanjan (2023), the mixed-integer programming formulations of clearing vectors for the Rogers-Veraart model are combined with the vector optimization approach to compute systemic risk measures based on polyhedral convex risk measures. Different from the vector optimization approach, a grid search algorithm is proposed in Feinstein et al. (2017) for computing systemic risk measures. Notably, all these works assume that the underlying probability space is finite to ensure that the corresponding vector optimization problems are finite-dimensional (or a finite number of clearing vectors are computed in the grid search). This is a significant drawback as, in practice, the operating cash flow vector may be better modeled via a continuous heavy-tailed distribution such as the Pareto distribution.

1.2 Contribution

In this paper, we study the convergence properties of sample-average approximations (SAA) for set-valued systemic risk measures within a general probability space, putting particular emphasis on the theoretical aspects of SAA convergence. We assume that the underlying monetary risk measure is value-at-risk, which enables us to formulate our optimization problems as chance-constrained programming problems. We name the resulting systemic risk measure as systemic value-at-risk. By utilizing the SAA framework for chance-constrained programming proposed in Pagnoncelli et al. (2009), Ahmed and Shapiro (2008), and Chen et al. (2019), our primary contribution lies in extending the SAA framework to set-valued risk measures, a novel direction in the literature, and proving the almost sure convergence of these approximations under Wijsman and Hausdorff topologies for closed sets. Our convergence results encompass both sensitive and insensitive cases, and they allow for a general aggregation subject to some continuity conditions, demonstrating the robustness of our theoretical framework.

Specifically, our results reveal that for the sensitive case, where risk measures exhibit non-convexity and lack dual representations, the convergence of weighted-sum scalarizations and distance functions, often called norm-minimizing scalarizations in the current paper, is established through an intricate analysis of the underlying chance-constrained programming problems. On the technical level, the problems considered in Pagnoncelli et al. (2009) are closely related to our scalarization problems. However, unlike the form considered there, our problems involve an almost sure selection constraint in addition to the usual chance constraint given by the value-at-risk. Hence, we start by proving a technical result (Proposition 3.3 in Section 3 below) that is well-suited for our purposes. With this tool, we prove convergence for a general scalarization, followed by the Wijsman and Hausdorff convergence of the sample-average approximations to the true systemic value-at-risk.

We apply our theory on the systemic value-at-risk in which the aggregation function is based on the Eisenberg-Noe model. We verify that this aggregation function satisfies the assumptions made for the general theory to work as long as the random operating cash flow vector has a continuous distribution with full support on the positive orthant. In addition to the convergence results, we also address the computational challenges inherent in calculating the SAA for this systemic value-at-risk. To that end, we propose mixed-binary linear and quadratic programming formulations for the weighted-sum and norm-minimizing scalarizations of the SAA, respectively. These formulations are embedded in the grid search algorithm in Feinstein et al. (2017) as well as a modified version of it proposed here.

In the last part of the paper, we undertake a comprehensive computational validation of our proposed methodologies. Drawing insights from Bollobás et al. (2003) and van der Hofstad (2016, Chapter 8) on preferential attachment models, we employ this model detailed to generate network data. We model the random operating cash flow vectors via the Pareto distribution for its effective portrayal of heavy-tailed behavior, as indicated in Cont et al. (2010).

The rest of the main paper is organized as follows. In Section 2, we provide a general framework for systemic risk measures that is not particularly restricted to convex monetary risk measures. The core of the paper is Section 3, where we prove all the convergence results for SAA. In Section 4 we delve into the Eisenberg-Noe model, verify the assumptions of the general convergence results in this setting, and also provide mixed-integer programming formulations for computing the SAA sets. We present the computational results in Section 5. Some additional theoretical results as well as all proofs are collected in the electronic companion at the end of the main text.

2 Systemic Risk Measures

We start by introducing some notation that will be used throughout the paper. Given real numbers , we denote by their minimum and by their maximum; we also define , and . Let . We denote by the -dimensional Euclidean space whose elements are expressed as column vectors. We define as the vector of ones and as the vector of zeros in ; we define as the identity matrix. For each , we denote by the standard unit vector in . Let and . We write for the -norm of and denotes the closed -ball centered at with radius . We denote by and the componentwise minimum and maximum of , respectively. We also write () whenever () for each . We also define and . We say that a function is increasing if implies for every ; it is called strictly increasing if and imply for every .

We denote by the Borel -algebra on and by the Lebesgue measure on . Let be sets. We define their Minkowski sum by , with the convention , and write for every . The interior, closure, boundary of are denoted by , respectively. We define the indicator function of by for and by for . Given a function and parameters , we define

The Hausdorff distance between and (with respect to the -norm) is defined as , where . Given a sequence of closed subsets of and a nonempty closed set , we say that Wijsman-converges to if converges to for every ; we say that Hausdorff-converges to if converges to . It is well-known that Hausdorff convergence implies Wijsman convergence (Aliprantis and Border 2006, Corollary 3.65) and the converse also holds when for some compact set (Beer 1987, Theorem 2.5).

Let us fix a probability space . We denote by the space of all -measurable random vectors that are identified up to -almost sure equality. Hence, (in)equalities between random variables are understood in the -almost sure sense. For each , we define for and . Then, for each , the space is a Banach space with respect to the norm . A multifunction is called -measurable if for every closed set . A function is called a normal integrand if its epigraphical multifunction is closed-valued and measurable.

In this section, we review the scalar-valued systemic risk measures introduced in Chen et al. (2013) and the set-valued systemic risk measures introduced in Feinstein et al. (2017). Since the expositions in these works and other related works, e.g., Biagini et al. (2019a), Ararat and Rudloff (2020), Ararat and Meimanjan (2023), assume either bounded random variables and/or finite-valued aggregation functions, we give a self-contained exposition tailored for the current paper. The proofs of all results are given in Section 8.

2.1 Aggregation Functions and Acceptance Sets

Let us consider a financial network with institutions. The sample space contains all possible scenarios that may affect the ability of the institutions to meet their obligations within the network. Hence, we model the operating cash flow vector of the network as a random vector , where is understood as the future value of the external assets of institution under scenario . For the definitions of the systemic risk measures, we fix a linear subspace of that contains all deterministic random vectors, e.g., with , and consider only .

To define systemic risk measures, the realizations of the operating cash flow vector are aggregated into a scalar quantity by taking into account the structure of the network. This is achieved through an increasing function , usually referred to as the aggregation function. Given a realization for the operating cash flow vector, the scalar is a quantification of the impact of this cash flow profile on society. In this paper, most results will be shown by choosing based on an Eisenberg-Noe network, as we will define precisely in Section 4; in this case, will also be a concave function. Let us introduce effective domain of by

and the collection of all random vectors that yield finite aggregate outcomes almost surely by

We work under the following assumption for .

is a nonempty closed subset of and the restriction of on is continuous and bounded.

Similar to , we fix a linear subspace that contains all deterministic random variables. Let be a monetary risk measure (see Föllmer and Schied (2016, Section 4.1)), that is, it satisfies the following two properties:

-

•

Monotonicity: implies for every .

-

•

Translativity: for every , .

The acceptance set of is defined as

Moreover, can be calculated using via

In this paper, most results will be shown by choosing as value-at-risk, which is recalled in the next example.

Example 2.1

Assume that and let , . For each , the value-at-risk of at level with threshold is defined as

It is easy to verify that the above infimum is attained, i.e., . Clearly, and is called the value-at-risk of at level in the literature (see Föllmer and Schied (2016, Section 4.4)). We work with general for convenience in the sequel. It is easy to verify that the corresponding acceptance set is given by

We work under the following domain assumption that connects and :

For every , it holds .

2.2 Insensitive Systemic Risk Measures

Using an aggregation function and an acceptance set as primitives, in Chen et al. (2013), scalar-valued systemic risk measures of the form

| (1) |

are studied. Here, calculates the minimum capital requirement for the aggregate random variable to be acceptable. Since the capital is allocated for the whole network after aggregation, such functionals are also called insensitive systemic risk measures (see Ararat and Rudloff (2020)). The following property of is an immediate consequence of the monotonicity of .

Lemma 2.2

Under Section 2.1, implies for every .

2.3 Sensitive Systemic Risk Measures

As a sensitive alternative to given by (1), in Feinstein et al. (2017), systemic risk measures are defined as set-valued functionals that assign to a random vector all capital allocation vectors, assigned before aggregation, that yield acceptable aggregate outcomes. To keep the dimension of this set reasonably low compared to the size of the network, we formulate this systemic risk measure by using the concept of grouping as discussed in Feinstein et al. (2017) and Ararat and Meimanjan (2023). We assume that the financial institutions are partitioned into nonempty groups, where the size of group is denoted by . In particular, . The institutions within each group will have an identical designated capital level. For this purpose, we introduce a binary matrix , called the grouping matrix, where if and only if institution belongs to group . Then, for a capital allocation vector for groups, the actual capital allocation vector for the network is calculated as .

Example 2.3

The case of groups is suitable for core-periphery networks. Let us write and for the sets of core and peripheral banks, respectively. Then, we may write the grouping matrix as

where and . For instance, when and , we have for every .

With the structure above, the set-valued systemic risk measure proposed in Feinstein et al. (2017) is defined as

Thanks to the monotonicity of , the set-valued functional has properties that are analogous to the properties of as a risk measure. These are given in the next lemma and they make an example of a set-valued risk measure in the sense of Hamel and Heyde (2010), Hamel et al. (2011).

Lemma 2.4

Under Section 2.1, has the following properties:

-

•

Monotonicity: implies for every .

-

•

Translativity: for every , .

-

•

Upper set property: for every .

2.4 Scalarizations of Sensitive Systemic Risk Measures

Given , the set can be seen as the so-called upper image of the vector optimization problem

and solving this problem (approximately) typically involves solving some scalar optimization problems, called scalarizations, associated to it. A general scalarization problem can be formulated as

where is a given function, its optimal value is given by

In this paper, we are interested in two types of scalarizations. The first is the well-known weighted sum scalarization, which is formulated as

for a given weight parameter , and its optimal value is given by

The second one is the norm-minimizing scalarization, which is formulated as

for a given reference point , and its optimal value is given by

3 Systemic Values-at-Risk and Their Sample-Average Approximations

In this paper, we study systemic risk measures with taken as value-at-risk (see Example 2.1). For convenience, we rename them as systemic values-at-risk in the next definition. Throughout this subsection, we fix an aggregation function that satisfies Section 2.1 and Section 2.1. We also fix and . The proofs of all results are given in Section 10.

Definition 3.1

(i) Let . The insensitive systemic value-at-risk of at level with threshold is defined as

(ii) Let . The sensitive systemic value-at-risk of at level with threshold is defined as

The calculations of and involve solving a chance-constrained optimization problem due to the probabilistic constraints in their definitions. When is an infinite sample space, these constraints can be expressed in terms of multivariate integrals, which are difficult to deal with in an optimization problem, except for some special distribution classes for . In this section, we introduce sample-average approximations (SAA) for the sensitive value-at-risk and prove their almost sure convergence to its true value. Each SAA problem is essentially a special case of the true problem in which the random vector is defined on a finite probability space and, as we will do later, it can be reformulated as a mixed-integer programming problem using binary variables. We limit the scope of the main text to the sensitive case, which is more interesting from a capital allocation perspective and also more challenging mathematically due to the appearance of set-valued functions. In Section 9, we prove a convergence result for the insensitive systemic value-at-risk.

Proposition 3.3 below is a generalization of Pagnoncelli et al. (2009, Proposition 2.1) and it will be used repeatedly in the sequel as a technical tool for the convergence arguments. Before stating it, we recall the notion of epi-convergence for scalar-valued functions.

Definition 3.2

(Rockafellar and Wets 2009, Definition 7.1, Proposition 7.2) Let be extended real-valued functions on , where . We say that the sequence epi-converges to if the following conditions hold for every :

-

(i)

For every sequence in converging to , it holds .

-

(ii)

There exists a sequence in converging to such that .

Proposition 3.3

Let with a sequence of independent copies. Let ( with ) be an open set. Let () be a Carathéodory function, where . For each , , and , let

Then, the following properties hold:

-

(i)

For each , the function is a normal integrand.

-

(ii)

The function is lower semicontinuous.

-

(iii)

The sequence epi-converges to almost surely.

As an application of Proposition 3.3, we verify the closed-valuedness of the sensitive systemic value-at-risk in the next lemma.

Lemma 3.4

For every , the set is closed; in particular, it holds .

3.1 SAA for the Sensitive Systemic Value-at-Risk

Let us fix a random vector . By passing to the countably infinite product space if necessary, we assume the existence of a sequence of independent copies of .

Let . For each , we define

Note that this is a special case of the sensitive systemic risk measure for a random vector whose support is . Unlike in the insensitive case, the calculation of is not straightforward and the difficulty of the calculation depends largely on the structure of the aggregation function. In Section 5, we will discuss an algorithm for calculating when the aggregation function is based on the Eisenberg-Noe model.

We check the set-valued measurability of in the next lemma.

Lemma 3.5

Let . The multifunction is closed-valued and measurable.

3.1.1 Convergence of a General Scalarization

Thanks to Lemma 3.5, composing with the first independent copies of yields the random set . To prove the convergence of this random set to the true set in various senses, we will first prove a convergence result for their scalarizations. To that end, let be a function and be a set. For each , we consider the value

Lemma 3.6

Let . Suppose that is a continuous function and is a closed set. Then, the function is measurable.

Thanks to Lemma 3.6, is a random variable. We also consider the true value

For the convergence results to follow, we work under the following assumption, which asserts that the above scalarization problem has an optimal solution that can be approximated by a sequence of feasible solutions that are strictly feasible in the value-at-risk constraint.

There exist such that , and a sequence in that converges to and satisfies , for every .

Theorem 3.7

Under Section 3.1.1, suppose that is continuous, and is nonempty and compact. Then, the sequence converges to almost surely.

3.1.2 Convergence of a Weighted-Sum Scalarization

Weighted-sum scalarizations for systemic risk measures are useful when it is desirable to find the minimum total capital allocation required for the network or a subset of it. For instance, with , the value gives the minimum total capital requirement of the entire network; given a group , the value gives the minimum total capital requirement of each bank in group . These scalarizations are also used in algorithms for calculating systemic risk measures. For instance, assuming the finiteness of the scalarizations, the vector is called the ideal point of and it can be used to construct an initial outer approximation for since we have .

The result of this section states that the weighted-sum scalarizations of a restricted version of the SAA converges to that of the original systemic risk measure under the following assumption. This assumption will later be verified for the Eisenberg-Noe model in Section 4.2.

Given and a compact set such that , there exist such that , and a sequence in that converges to and satisfies , for every .

Theorem 3.8

Let . Assume that there exists a compact set such that

and Section 3.1.2 holds for . Then, the sequence converges to almost surely.

3.1.3 Wijsman Convergence of the Sensitive Value-at-Risk

Due to well-known lack of convexity for value-at-risk, the set may fail to be convex in general. Hence, its weighted-sum scalarizations do not provide sufficient information to characterize the entire set. Hence, to study the convergence behavior of SAA as sets, we study the convergence of the distance functions of SAA in this subsection. This yields the Wijsman convergence of SAA.

For the results of this section, we will work under the following additional assumption on .

is bounded with respect to , i.e., there exists such that .

The boundedness property in Section 3.1.3 is automatically transferred to the sensitive systemic value-at-risk as the next lemma shows.

Lemma 3.9

Suppose that Section 3.1.3 holds and . Then, is bounded with respect to , i.e., there exists such that and .

Remark 3.10

As discussed in Section 3.1.2, the finiteness of the weighted-sum scalarizations along the standard unit vectors also guarantees that is bounded with respect to .

Remark 3.11

In general, the boundedness of a closed set with respect to is weaker than its Motzkin-decomposability, i.e., the existence of a compact set such that . For instance, the set is bounded with respect to but it is not Motzkin-decomposable; see Dörfler and Löhne (2024, Section 1).

The following is the analogous version of Section 3.1.2 for distance functions.

Given such that and , let . For every , there exist such that , and a sequence in that converges to and satisfies , for every .

The next theorem is one of the main results of the paper and it establishes the Wijsman convergence of SAA for a sensitive systemic value-at-risk that is bounded with respect to .

Theorem 3.12

Assume that . Suppose that Section 3.1.3 and Section 3.1.3 hold for given by Lemma 3.9. Then, the sequence Wijsman-converges to almost surely.

3.1.4 Hausdorff Convergence of the Sensitive Systemic Value-at-Risk

For the final general result of the paper, we study the Hausdorff convergence of SAA to the sensitive systemic value-at-risk. This convergence type is often preferred for being naturally generated by the Hausdorff distance , which is a metric with values in .

As a preparation for the convergence result, we state some useful properties of distance functions in the next two lemmata.

Lemma 3.13

Assume that and let . Then, there exists such that

Moreover, such satisfies .

Lemma 3.14

Assume that and there exist with such that

| (2) |

where . Let . Then, it holds

As noted in Section 2, Hausdorff convergence is stronger than Wijsman convergence, and the two convergence types coincide for closed subsets of a compact set. To obtain Hausdorff convergence, we will work under the Motzkin-decomposability assumption as in Section 3.1.2; see Remark 3.11 as well. The next assumption is a modification of Section 3.1.3 for our current purpose.

Given a compact set such that , for every , there exist such that , and a sequence in that converges to and satisfies , for every .

Remark 3.15

It is easy to check that Section 3.1.4 implies Section 3.1.3.

Theorem 3.16

Assume that there exist with such that

and

almost surely for every , where . Suppose that Section 3.1.4 holds for this choice of . Then, the sequence Wijsman- and Hausdorff-converges to almost surely.

4 Sensitive Systemic Value-at-Risk for Eisenberg-Noe Model

This section serves as a case study of the general theory established in Section 3. We consider the Eisenberg-Noe network model, which introduces a mechanism for clearing the interbank liabilities within the network. Based on this mechanism, we define an aggregation function, and study the corresponding sensitive systemic value-at-risk as well as its SAA. One of the crucial tasks is to verify the assumptions on the existence of strictly feasible approximating sequences for optimizers, e.g., Section 3.1.2 and Section 3.1.4, for this model. It turns out that this is a highly nontrivial point and it can be addressed by a deeper analysis of the aggregation function as will be done in the proof of Theorem 4.8.

Unless stated otherwise, the proofs of all results are given in Section 11.

4.1 Eisenberg-Noe Model

In this subsection, we recall the network model in Eisenberg and Noe (2001) and introduce its aggregation function to be used in the definition of the sensitive systemic value-at-risk. We consider a financial network with nodes representing the member institutions.

Definition 4.1

(Eisenberg and Noe 2001, Section 2.2) A triplet is called an Eisenberg-Noe network with institutions if is a right stochastic matrix with for every , , and .

In the above definition,

-

•

denotes the total amount of liabilities of node and we refer to as the total obligation vector;

-

•

denotes the fraction of total liabilities of node owed to node and we refer to as the relative liability matrix; note that holds for each , i.e., not all claims are owed a single node;

-

•

denotes the total value of the assets of node and we refer to as the operating cash flow vector.

Let us fix an Eisenberg-Noe network . Next, we recall the notion of a clearing (payment) vector, which adheres to the principles of limited liability and absolute priority.

Definition 4.2

(Eisenberg and Noe 2001, Definition 1) A vector is called a clearing vector for if it satisfies the following properties:

-

•

Limited liability: For each , it holds .

-

•

Absolute priority: For each , either or holds.

Limited liability indicates that a node cannot pay more than it has and absolute priority means that each node either meets its obligations in full or it defaults by paying as much as it has. It is easy to see that a clearing vector is equivalently characterized as a solution of the fixed point equation , where is defined by

| (3) |

According to Eisenberg and Noe (2001, Theorem 1), with respect to the componentwise order , a maximal and minimal clearing vector always exist. Moreover, the maximal clearing vector can be found by solving an optimization problem as recalled below.

Lemma 4.3

In Section 7, we prove a novel result that nicely complements Lemma 4.3: we show that the set of all clearing vectors of an Eisenberg-Noe network can be seen as a mixed-integer linear projection problem.

In Lemma 4.3, when we take for each , the optimal value of (4) yields the total payment made at clearing. We define this quantity as an aggregation function of the Eisenberg-Noe model. More precisely, let us define by

| (5) |

The next lemma shows that is an aggregation function that satisfies the assumptions posed in Section 2 and Section 3.

Lemma 4.4

is a concave and increasing function that satisfies Section 2.1 and Section 3.1.3.

4.2 Sensitive Systemic Value-at-Risk and its SAA

Let us fix a pair , where and is a right stochastic matrix with for every . Then, for every , the triplet is an Eisenberg-Noe network with institutions for almost every .

Within the framework of Section 4, let us take and , , and . By Lemma 4.4, Section 2.1 and Section 3.1.3 hold. Since , we have . Moreover, since is bounded on , we have for every so that Section 2.1 also holds.

Let us fix and . Let us also fix as a random operating cash flow vector. The sensitive systemic value-at-risk corresponding to the Eisenberg-Noe model evaluated at is given by

We discuss the nonemptiness of in the next proposition.

Proposition 4.5

It holds if and only if .

Since Section 2.1 holds, is bounded with respect to by Lemma 3.9; indeed, as a lower bound vector we may take defined by

since the requirement is equivalent to . Let us also define by

and set

| (6) |

Remark 4.6

The definition of guarantees that is feasible for the problem of calculating . In particular, we have .

In order for the SAA convergence results of Section 3.1, we verify the assumptions of these results for the Eisenberg-Noe model. We first show that the “interesting” part of can be bounded by a compact set as assumed in Theorem 3.8 and Theorem 3.16.

Proposition 4.7

With defined in (6), it holds

Next, we verify Section 3.1.2 for the Eisenberg-Noe model.

Theorem 4.8

Let be defined by (6) and let . Suppose that .

-

(i)

There exists such that .

-

(ii)

Suppose further that has a continuous distribution with full support on , i.e., the measure is equivalent to restricted to . Then, there exists a sequence in that converges to and satisfies , for every .

Finally, we verify Section 3.1.4 for the Eisenberg-Noe model.

Theorem 4.9

Let be defined by (6) and let . Suppose that .

-

(i)

There exists such that .

-

(ii)

Suppose further that has a continuous distribution with full support on . Then, there exists a sequence in that converges to and satisfies , for every .

Thanks to the above verifications, the convergence results of Section 3.1 are applicable for . We summarize them in the next corollary.

Corollary 4.10

Let be defined by (6). Suppose that and has a continuous distribution with full support on .

-

(i)

For every , the sequence converges to almost surely.

-

(ii)

The sequence Wijsman- and Hausdorff-converges to almost surely.

4.3 Mixed-integer programming formulations for SAA

As in the previous subsection, we fix , , and a random operating cash flow vector . Let be a sequence of independent copies of . Let . The set-valued SAA function defined in Section 3.1 is given by

for each . Then, is the SAA for corresponding to a random sample of size . In practice, once a scenario is observed, then the SAA is realized as . Our goal is to argue that this set can be calculated by solving a finite-dimensional mixed-integer linear vector programming problem. To that end, we first reformulate the values of using binary variables in the next theorem.

Theorem 4.11

For each , it holds

| (7) |

As a consequence of Theorem 4.11, we may view as the upper image of the finite-dimensional mixed-integer linear vector programming problem

Moreover, the constraint is equivalent to , where is defined by

Hence, is naturally bounded with respect to since we have

Hence, can be calculated using the available algorithms for solving bounded nonconvex vector optimization problems, such as the one in Nobakhtian and Shafiei (2017). As immediate corollaries of Theorem 4.11, we provide a mixed-integer linear programming (MILP) formulation of the weighted-sum scalarization and a mixed-integer quadratic programming (MIQP) formulation of the norm-minimizing scalarization in Section 12; both of which will be used in the modified grid search algorithm described in Section 5.

5 Computational Results and Analysis

5.1 Algorithms for Calculating SAA

In this section, we explore techniques to approximate the SAA for the sensitive systemic value-at-risk of the Eisenberg-Noe model. In addition to the direct implementation of the grid search algorithm in Feinstein et al. (2017) (Algorithm 1), we also leverage a modified version of it using the norm-minimizing scalarizations (Algorithm 2).

Let us fix as in Section 4. Let with . Our goal is to calculate . Let . To implement the grid algorithm more effectively, we first replace with a tighter lower bound. For this purpose, we calculate the ideal point of by solving the weighted-sum scalarizations along the standard unit vectors using the MILP formulation (see Corollary 12.2). In particular,

Given a predefined approximation error , we take a finite subset , called the grid, such that, for every , there exists with . The goal of the algorithms is to detect the intersection , called the acceptable set. Then, is returned as an inner approximation of .

The individual details of the algorithms are described below.

-

(i)

SAA Computation With Clearing Vectors: At each iteration, a point is chosen from the current grid and the aggregate values are calculated for each using either a fixed point algorithm for the characterization in Equation 3 or by solving a linear programming problem based on Lemma 4.3. Then, the condition is checked. If satisfied, then so that all grid points in are labeled as acceptable. Otherwise, all points in are labeled as not acceptable so that they are removed from the grid and eliminated from future consideration. The algorithm proceeds to subsequent grid points along the diagonal trajectory until all points are classified as acceptable and not acceptable. The pseudocode is given in Algorithm 1.

-

(ii)

SAA Computation Using Norm-Minimizing Scalarizations: At each iteration, a point is chosen from the current grid and the distance is calculated by using the MIQP formulation of the norm-minimizing scalarization problem (see Corollary 12.4), along with an optimizer . All grid points in are labeled as acceptable. Moreover, all grid points that are within strictly less than -distance from the current grid point are labeled as not acceptable as these points do not belong to due to the structure of the norm-minimizing scalarization. The algorithm systematically progresses to subsequent grid points in a diagonal direction until all points are categorized as acceptable and not acceptable. The pseudocode is given in Algorithm 2.

The following theorem states the finiteness and correctness of these algorithms. Its proof is given in Section 13.

Theorem 5.1

Let an approximation error and a finite grid be given such that, for every , there exists with . Both Algorithm 1 and Algorithm 2 terminate in finitely many iterations and the returned approximation satisfies and .

5.2 Data Generation

Our analysis focuses on computing the systemic set-valued risk measure within a core-periphery framework, examining a financial system with institutions divided into core () and peripheral () groups. The computational approach employs Matlab with CVX and Gurobi on an Intel(R) Core(TM) i7-6500U CPU @2.50GHz 2.59GHz processor with 8.00 GB RAM.

We outline data generation for an Eisenberg-Noe network with banks. The network is constructed using the directed preferential attachment model in Bollobás et al. (2003), capturing a scale-free growth (van der Hofstad 2016, Chapter 8). As a result, it is observed that the vertices with the longest existence tend to have the highest degrees, a phenomenon commonly known as the “rich-get-richer” effect; see Deijfen et al. (2009), Barabási and Albert (1999), Bollobás et al. (2003), Bollobás and Riordan (2003), Cooper and Frieze (2003). Before enumerating the specific rules of the model, we clarify the notation and parameters: and represent the in-degree and out-degree of vertex at time , respectively, while denotes the number of vertices and denotes the vertex set of the graph. The parameters and are smoothing constants that ensure well-defined probabilities even when degrees are zero, influencing the initial attractiveness of vertices. The probabilities , , and , constrained by , govern the likelihood of different types of events in the network’s evolution. Starting with an initial graph with vertex set , the model evolves over time on some probability space , adhering to the following specified rules:

-

(i)

With probability , a new vertex is added along with an edge from to an existing vertex , where is chosen with respect to the distribution,

-

(ii)

With probability , an edge is added from an existing vertex to an existing vertex . The selection of and is independent and follows the distribution,

-

(iii)

With probability , a new vertex is added along with an edge from an existing vertex to , where is chosen with respect to the distribution,

It is worth noting that the model allows for loops and multiple edges, although their presence does not significantly affect the conclusions drawn. The paper showed that the in-degree and out-degree distribution follow a power law distribution (Bollobás et al. 2003, Theorem 3.1).

The matrix and vector were generated based on the adjacency matrix of the aforementioned network. The core banks set comprises the top four banks based on node degree in , while includes the remaining 16 banks. Intergroup liability matrix distinguishes core-to-core (CC), core-to-periphery (CP), periphery-to-core (PC), and periphery-to-periphery (PP) linkages as follow

The interbank nominal liability matrix is constructed from and . For core banks and , equals if and zero if . Similar rules apply for other bank classifications and connections. After computing , the total liability vector sums its rows, and the relative liability matrix is derived by normalizing .

Subsequently, the operating cash flow vector in is a multivariate random vector, generated through Pareto-distributed shocks assigned to each bank. The correlation coefficient measures the dependence among banks. The groups use a shared shape parameter and distinct scale parameters and for core and peripheral banks, respectively.

5.3 Runtime Performance Analysis

In this subsection, we compare the runtime performance of Algorithm 2 and Algorithm 1. For network construction, we use the Bollobás algorithm (Section 5.2) with the following parameters: , , , , and .

Recapping, the Eisenberg-Noe network has banks ( core and periphery) generated with parameters , , , and . The intergroup liability matrix has values

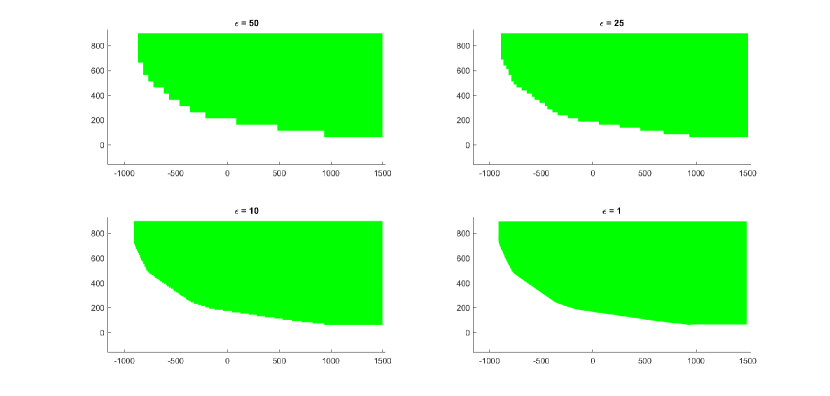

The value-at-risk parameters are taken as and . The grid algorithm uses six values for different degrees of approximation. Performance is assessed in Table 1 for ranging from 50 to 1, with their corresponding grid points.

| Grid Points # | Algorithm 1 Runtime (s) | Algorithm 2 Runtime (s) | |

|---|---|---|---|

| 50 | 570 | 24.72 | 50.04 |

| 25 | 2175 | 45.68 | 99.96 |

| 10 | 13464 | 114.19 | 505.83 |

| 1 | 1328148 | 13846.72 | 163242.83 |

In Figure 1, the -axis and -axis of each subplot represent capital injection to core and peripheral banks, respectively. The visualization of approximation sets in Figure 1 reveals that a smaller value leads to a more precise approximation of the set-valued systemic risk measure. Additionally, results in Table 1 show that Algorithm 1 outperforms, evaluating grid point acceptability using the optimization formulation in Section 2. This likely stems from the need for binary variables in the norm-minimizing scalarization problem used by Algorithm 2.

5.4 Sensitivity of the Risk Measure

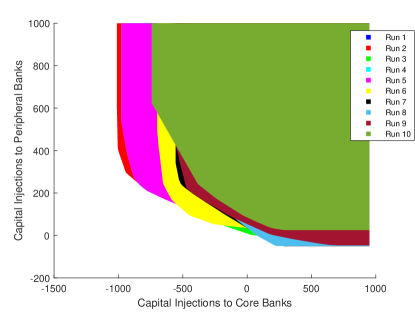

This subsection aims to assess the sensitivity of the set-valued systemic risk measure to the Bollobás network under constant parameters. Despite identical parameter values, the stochastic nature of the network results in varied network configurations across multiple iterations. Consistency is maintained with the network, operating cash flow, and set-valued risk measure parameters from Section 5.3. This ensures isolation of the network structure’s influence on the set-valued systemic risk measure. A comprehensive analysis involves 10 independently simulated networks, capturing the range of configurations possible with identical Bollobás parameters.

Figure 2a vividly demonstrates our set-valued risk measure’s sensitivity to network shape, notably with . Even minor changes in the network’s structure significantly impact the computed systemic risk measure.

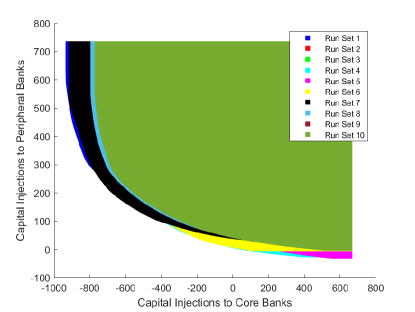

Continuing, we conduct a thorough analysis by evaluating systemic risk across 100 independently simulated networks with identical Bollobás parameters. The approach involves computing the mean value of 10 unique sets within the grid area, where each set is derived from the average of vertices obtained in 10 independent runs. This results in 10 distinct sets, each representing the mean value from 10 separate runs illustrated in Figure 2b.

5.5 Impact of the Sample Size

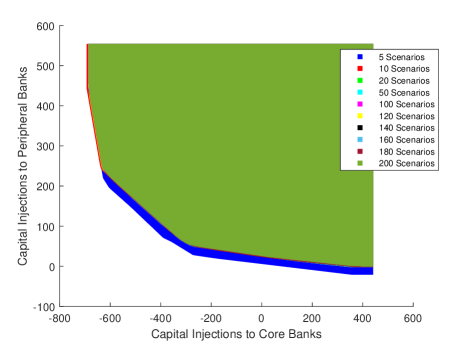

In this section, we examine the impact of varying the sample size (or number of stress scenarios), denoted as , on both computational performance and systemic risk measures. All parameters mentioned in Section 5.3 are held constant, with the exception of the scenarios count , enabling us to conduct a sensitivity analysis using this particular parameter. This analysis offers valuable insights into the convergence behavior observed with an increasing number of scenarios.

We examine a set of values for the variable , which are defined as follows: takes on the values of 5, 10, 20, 50, 100, 120, 140, 160, 180, and 200. Although the network structure remains consistent, it is anticipated that the systemic risk measures will display slight fluctuations. Nevertheless, it is expected that the computation time will increase as the number of scenarios increases, primarily because each scenario involves continuous variables.

| Grid Points # () | Time (s) | |

|---|---|---|

| 5 | 6.21 | 2908.67 |

| 10 | 5.13 | 2020.09 |

| 20 | 5.68 | 2515.88 |

| 50 | 5.08 | 2244.23 |

| 100 | 5.12 | 2677.92 |

| 120 | 5.63 | 3403.30 |

| 140 | 5.84 | 3553.30 |

| 160 | 6.30 | 4314.21 |

| 180 | 5.13 | 3361.87 |

| 200 | 5.40 | 3821.29 |

The approximations of set-valued systemic risk measures, specifically for , are shown in Figure 3. This figure highlights the relative stability of these approximations across different values, aligning with our initial hypotheses. It supports the expected connection between set-valued risk measures and the number of scenarios. In contrast, Table 2 displays computational performance and grid points for the Algorithm 1, maintaining consistent scenario counts and approximation error. Despite irregular fluctuations in grid points, the overall algorithm performance time shows inconsistent variations as the number of scenarios increases. This can be attributed to the algorithm’s sensitivity to the quantity of grid points.

5.6 Network Parameters

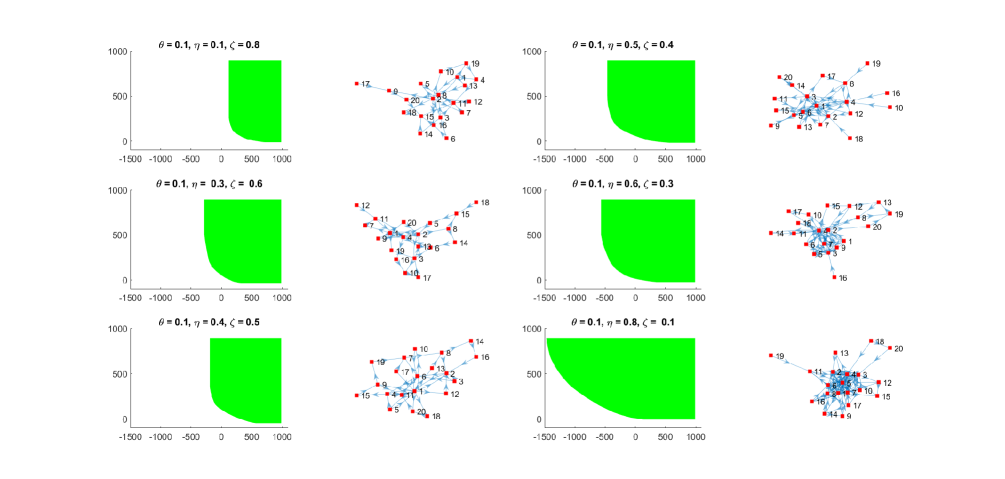

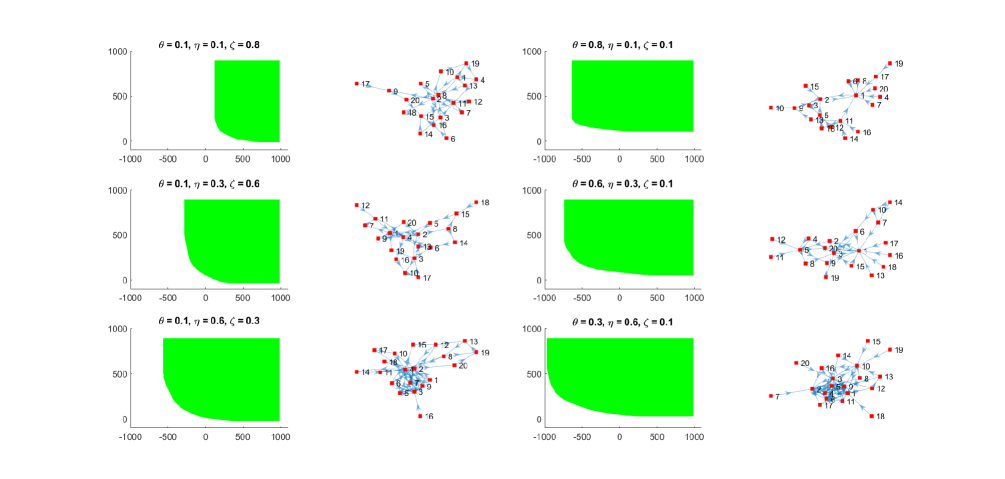

In this subsection, we conduct a sensitivity analysis on the probabilities of the Bollobás network parameter, specifically focusing on , , and . The remaining parameters from Section 5.3 are kept constant. Visual representations of systemic risk measures are found in Figure 4 for . The x-axis and y-axis in each subplot represent capital injections to core and peripheral banks, respectively, with an adjacent subplot displaying the corresponding network graph.

We analyze the following network statistics for each combination of Bollobás network parameter probabilities:

-

•

Average Degree (AD): Mean connections per node in the network, calculated as , where is the total number of nodes, and is the adjacency matrix.

-

•

Network Density (ND): The ratio of total connections to total possible connections, given by .

-

•

Total Clustering Coefficient (TCC): A metric measuring the tendency of nodes to form clusters. Computed as , where is the clustering coefficient of node .

-

•

Core-Periphery Error (CPE): Based on Craig and Von Peter (2014), CPE is a measure evaluating the disparity between observed and expected core-periphery configurations.

-

•

Core-Periphery Index (CPI): A robust measure assessing the strength of the core-periphery structure. Defined as , where and are the core and periphery sets, respectively.

The network statistics provide key insights into Bollobás network structural characteristics. Lower Core-Periphery Error (CPE) and higher Core-Periphery Index (CPI) values indicate a more pronounced core-periphery structure.

First, we aim to examine the impact of variations in the parameter on the sensitivity of the systemic risk measure. Specifically, we keep the parameter constant at a value of 0.1, and manipulate the parameter to be equal to 1 minus the sum of 0.1 and . The computational statistics for various values of the parameter, specifically , are presented in Table 3(left). The corresponding approximations are displayed in Figure 4a.

Based on the data presented in Table 3(left), it can be observed that there is a positive correlation between the variable and the average degree of each node, network density, and total clustering coefficient. As the value of increases, these network characteristics consistently increase. Furthermore, the observed rise in the value signifies a heightened presence of a core-periphery structure within the network. This finding is substantiated by the core-periphery index and core-periphery error measures discussed in Craig and Von Peter (2014).

The impact of different values of on the systemic set-valued risk measure is further illustrated in Figure 4a. As the parameter increases, there is a noticeable downward trend in the measure, indicating that higher values of are associated with a reduction in systemic risk. The correlation between the statistical variations presented in Table 3(left) highlights the significant impact of on both network dynamics and systemic risk.

In the subsequent analysis, we investigate the impact on the systemic risk measure when the parameters and are reversed, while maintaining the parameter fixed. The following parameter pairs are taken into consideration:

-

•

and .

-

•

and .

-

•

and .

Table 3 presents the computational statistics for these different network parameter combinations, and Figure 4 provides the corresponding approximations.

| , , | Network Statistics | ||||

| AD | ND | TCC | CPE | CPI | |

| 0.1, 0.1, 0.8 | 1.7 | 0.0895 | 0.3333 | 0.67 | 0.6471 |

| 0.1, 0.3, 0.6 | 1.95 | 0.1026 | 1.6333 | 0.4103 | 0.7179 |

| 0.1, 0.4, 0.5 | 2 | 0.1053 | 4.4111 | 0.375 | 0.7251 |

| 0.1, 0.5, 0.4 | 2.45 | 0.1289 | 7.1659 | 0.1837 | 0.8367 |

| 0.1, 0.6, 0.3 | 2.8 | 0.1474 | 11.293 | 0.1786 | 0.8393 |

| 0.1, 0.8, 0.1 | 3.55 | 0.1868 | 14.5913 | 0.1672 | 0.8528 |

| , , | Network Statistics | ||||

| AD | ND | TCC | CPE | CPI | |

| 0.1, 0.1, 0.8 | 1.7 | 0.0895 | 0.3333 | 0.6765 | 0.6471 |

| 0.8, 0.1, 0.1 | 1.3 | 0.0684 | 2 | 0.5385 | 0.8462 |

| 0.1, 0.3, 0.6 | 1.95 | 0.1026 | 1.633 | 0.4103 | 0.7179 |

| 0.6, 0.3, 0.1 | 1.65 | 0.0868 | 6.3 | 0.4042 | 0.8485 |

| 0.1, 0.6, 0.3 | 2.8 | 0.1474 | 11.293 | 0.1786 | 0.8493 |

| 0.3, 0.6, 0.1 | 3.2 | 0.1684 | 15.419 | 0.1744 | 0.8656 |

Upon examination of Table 3(right), it is observed that the reversing of parameters and does not yield a consistent increase or decrease in both the average degree of each node and the network density. Nevertheless, the overall clustering coefficient, as well as the core-periphery index and core-periphery error measures, suggest a more evident core-periphery structure in the network when the value of exceeds .

The results presented in Figure 4b support the conclusions drawn from Table 3, indicating that the systemic set-valued risk measure exhibits a decrease in risk as is greater than . The observed behavior can be ascribed to the emergence of a core-periphery configuration within the network, which has implications for the interconnectivity and dissemination of risks.

Through the implementation of this sensitivity analysis, we are able to acquire significant insights regarding the impact of various network parameters on the measure of systemic risk. It is worth noting that the presence of a core-periphery structure within the network has a significant impact on decreasing the systemic set-valued risk measure. This suggests that there may be opportunities to develop risk mitigation strategies based on this observation.

6 Conclusion

In this paper, we investigate the convergence properties of sample-average approximations for set-valued systemic risk measures. We have demonstrated that the optimal solutions of the SAA scalarization problems converge almost surely to the true set-valued risk measure. Moreover, we have shown that the SAA (in)sensitive set-valued risk measures converge to the true ones almost surelt in the Wijsman and Hausdorff topologies. Our modified grid algorithm, employing weighted-sum and norm-minimizing scalarizations, proves effective in approximating these systemic risk measures. Overall, this study enhances the understanding of systemic risk assessment and offers robust convergence guarantees for SAA approximations. These findings are valuable for developing more effective risk management strategies in the financial industry.

References

- Acharya et al. (2012) Viral Acharya, Robert Engle, and Matthew Richardson. Capital shortfall: A new approach to ranking and regulating systemic risks. American Economic Review, 102(3):59–64, 2012.

- Adrian and Brunnermeier (2016) Tobias Adrian and Markus K. Brunnermeier. CoVaR. The American Economic Review, 106(7):1705–1741, 2016.

- Ahmed and Shapiro (2008) Shabbir Ahmed and Alexander Shapiro. Solving chance-constrained stochastic programs via sampling and integer programming. In Tutorials in Operations Research, pages 261–269. INFORMS, 2008.

- Aliprantis and Border (2006) Charalambos D. Aliprantis and Kim C. Border. Infinite Dimensional Analysis: a Hitchhiker’s Guide. Springer, 2006.

- Amini et al. (2020) Hamed Amini, Damir Filipović, and Andreea Minca. Systemic risk in networks with a central node. SIAM Journal on Financial Mathematics, 11(1):60–98, 2020.

- Ararat and Meimanjan (2023) Çağın Ararat and Nurtai Meimanjan. Computation of systemic risk measures: a mixed-integer linear programming approach. Operations Research, 71(6):2130–2145, 2023.

- Ararat and Rudloff (2020) Çağın Ararat and Birgit Rudloff. Dual representations for systemic risk measures. Mathematics and Financial Economics, 14(1):139–174, 2020.

- Armenti et al. (2018) Yannick Armenti, Stéphane Crépey, Samuel Drapeau, and Antonis Papapantoleon. Multivariate shortfall risk allocation and systemic risk. SIAM Journal on Financial Mathematics, 9(1):90–126, 2018.

- Artstein and Wets (1995) Zvi Artstein and Roger J-B Wets. Consistency of minimizers and the SLLN for stochastic programs. Journal of Convex Analysis, 2(1–2), 1995.

- Barabási and Albert (1999) Albert-László Barabási and Réka Albert. Emergence of scaling in random networks. science, 286(5439):509–512, 1999.

- Beer (1987) Gerald Beer. Metric spaces with nice closed balls and distance functions for closed sets. Bulletin of the Australian Mathematical Society, 35(1):81–96, 1987.

- Biagini et al. (2019a) Francesca Biagini, Jean-Pierre Fouque, Marco Frittelli, and Thilo Meyer-Brandis. A unified approach to systemic risk measures via acceptance sets. Mathematical Finance, 29(1):329–367, 2019a.

- Biagini et al. (2019b) Francesca Biagini, Jean-Pierre Fouque, Marco Frittelli, and Thilo Meyer-Brandis. A unified approach to systemic risk measures via acceptance sets. Mathematical Finance, 29(1):329–367, 2019b.

- Bollobás and Riordan (2003) Béla Bollobás and Oliver M. Riordan. Mathematical results on scale-free random graphs. In Stefan Bornholdt and Hans Georg Schuster, editors, Handbook of graphs and networks: from the genome to the internet, pages 1–34. Wiley, 2003.

- Bollobás et al. (2003) Béla Bollobás, Christian Borgs, Jennifer T. Chayes, and Oliver Riordan. Directed scale-free graphs. In SODA ’03: Proceedings of the Fourteenth Annual ACM-SIAM Symposium on Discrete Algorithms, pages 132–139. SIAM, 2003.

- Brunnermeier and Cheridito (2019) Markus K Brunnermeier and Patrick Cheridito. Measuring and allocating systemic risk. Risks, 7(2):46, 2019.

- Chen et al. (2013) Chen Chen, Garud Iyengar, and Ciamac C. Moallemi. An axiomatic approach to systemic risk. Management Science, 59(6):1373–1388, 2013.

- Chen et al. (2019) Xiaojun Chen, Alexander Shapiro, and Hailin Sun. Convergence analysis of sample average approximation of two-stage stochastic generalized equations. SIAM Journal on Optimization, 29(1):135–161, 2019.

- Cifuentes et al. (2005) Rodrigo Cifuentes, Gianluigi Ferrucci, and Hyun Song Shin. Liquidity risk and contagion. Journal of the European Economic association, 3(2-3):556–566, 2005.

- Cont et al. (2010) Rama Cont, Amal Moussa, and Edson B. Santos. Network structure and systemic risk in banking systems. In Jean-Pierre Fouque and Joseph A. Langsam, editors, Handbook on Systemic Risk. Cambridge University Press, 2010.

- Cooper and Frieze (2003) Colin Cooper and Alan Frieze. A general model of web graphs. Random Structures & Algorithms, 22(3):311–335, 2003.

- Craig and Von Peter (2014) Ben Craig and Goetz Von Peter. Interbank tiering and money center banks. Journal of Financial Intermediation, 23(3):322–347, 2014.

- Deijfen et al. (2009) Maria Deijfen, Henri Van Den Esker, Remco Van Der Hofstad, and Gerard Hooghiemstra. A preferential attachment model with random initial degrees. Arkiv för matematik, 47:41–72, 2009.

- Dörfler and Löhne (2024) Daniel Dörfler and Andreas Löhne. Convex sets approximable as the sum of a compact set and a cone. Journal of Nonlinear and Variational Analysis, 8(4):681–689, 2024.

- Eisenberg and Noe (2001) Larry Eisenberg and Thomas H. Noe. Systemic risk in financial systems. Management Science, 47(2):236–249, 2001.

- Elsinger (2009) Helmut Elsinger. Financial networks, cross holdings, and limited liability. Technical report, working paper, 2009.

- Feinstein and Rudloff (2017) Zachary Feinstein and Birgit Rudloff. A recursive algorithm for multivariate risk measures and a set-valued bellman’s principle. Journal of Global Optimization, 68(1):47–69, 2017.

- Feinstein et al. (2017) Zachary Feinstein, Birgit Rudloff, and Stefan Weber. Measures of systemic risk. SIAM Journal on Financial Mathematics, 8(1):672–708, 2017.

- Föllmer and Schied (2016) Hans Föllmer and Alexander Schied. Stochastic Finance: An Introduction in Discrete-Time. De Gruyter, 4th revised and extended edition edition, 2016.

- Hamel and Heyde (2010) Andreas H. Hamel and Frank Heyde. Duality for set-valued measures of risk. SIAM Journal on Financial Mathematics, 1:66–95, 2010.

- Hamel et al. (2011) Andreas H. Hamel, Frank Heyde, and Birgit Rudloff. Set-valued risk measures for conical market models. Mathematics and financial economics, 5(1):1–28, 2011.

- Hamel et al. (2013) Andreas H. Hamel, Birgit Rudloff, and Mihaela Yankova. Set-valued average value at risk and its computation. Mathematics and Financial Economics, 7(2):229–246, 2013.

- Kabanov et al. (2018) Yuri M. Kabanov, Rita Mokbel, and Khalil El Bitar. Clearing in financial networks. Theory of Probability & Its Applications, 62(2):252–277, 2018.

- Kotz (2009) David M. Kotz. The financial and economic crisis of 2008: A systemic crisis of neoliberal capitalism. Review of radical political economics, 41(3):305–317, 2009.

- Kováčová and Rudloff (2022) Gabriela Kováčová and Birgit Rudloff. Convex projection and convex multi-objective optimization. Journal of Global Optimization, 83(2):301–327, 2022.

- Kromer et al. (2016) Eduard Kromer, Ludger Overbeck, and Katrin Zilch. Systemic risk measures on general measurable spaces. Mathematical Methods of Operations Research, 84:323–357, 2016.

- Löhne (2011) Andreas Löhne. Vector Optimization with Infimum and Supremum. Springer, 2011.

- Löhne and Rudloff (2014) Andreas Löhne and Birgit Rudloff. An algorithm for calculating the set of superhedging portfolios in markets with transaction costs. International Journal of Theoretical and Applied Finance, 17(2):1450012 (33 pages), 2014.

- Löhne and Weißing (2016) Andreas Löhne and Weißing. Equivalence between polyhedral projection, multiple objective linear programming and vector linear programming. Mathematical Methods of Operations Research, 84(2):411–426, 2016.

- Nobakhtian and Shafiei (2017) Soghra Nobakhtian and Narjes Shafiei. A benson type algorithm for nonconvex multiobjective programming problems. TOP, 25(2):271–287, 2017.

- Pagnoncelli et al. (2009) Bernardo K. Pagnoncelli, Shabbir Ahmed, and Alexander Shapiro. Sample average approximation method for chance constrained programming: theory and applications. Journal of Optimization Theory and Applications, 142(2):399–416, 2009.

- Rockafellar and Wets (2009) R. Tyrrell Rockafellar and Roger J-B Wets. Variational Analysis. Springer, 2009.

- Rogers and Veraart (2013) Leonard C. G. Rogers and Luitgard A. M. Veraart. Failure and rescue in an interbank network. Management Science, 59(4):882–898, 2013.

- Silva et al. (2017) Thiago Christiano Silva, Michel Alexandre da Silva, and Benjamin Miranda Tabak. Systemic risk in financial systems: a feedback approach. Journal of Economic Behavior & Organization, 144:97–120, 2017.

- Suzuki (2002) Teruyoshi Suzuki. Valuing corporate debt: the effect of cross-holdings of stock and debt. Journal of the Operations Research Society of Japan, 45(2):123–144, 2002.

- Tarashev et al. (2010) Nikola Tarashev, Claudio Borio, and Kostas Tsatsaronis. Attributing systemic risk to individual institutions, 2010.

- van der Hofstad (2016) Remco van der Hofstad. Random Graphs and Complex Networks. Cambridge University Press, 2016.

- Weber and Weske (2017) Stefan Weber and Kerstin Weske. The joint impact of bankruptcy costs, fire sales and cross-holdings on systemic risk in financial networks. Probability, Uncertainty and Quantitative Risk, 2:1–38, 2017.

Additional Results and Proofs

7 Projection Characterization of Set of All Eisenberg-Noe Clearing Vectors

Let be an Eisenberg-Noe network with nodes. Recall that Lemma 4.3 shows that the maximal clearing vector of the network can be found by solving a continuous optimization problem, e.g., a linear programming problem. In this section, show that the calculation of the set of all clearing vectors can be formulated as a mixed-integer polyhedral projection problem. In the recent literature, it has been shown that linear/convex vector optimization problems are closely related to polyhedral/convex projection problems; see Löhne and Weißing (2016), Kováčová and Rudloff (2022). Hence, our result can be considered as a motivating example for studying the potential connection between mixed-integer linear vector optimization problems and mixed-integer polyhedral projection problems, which we leave for future research.

Theorem 7.1

Let denote the set of all clearing vectors of . Then,

| (8) |

where is a constant.

Proof 7.2

Proof. Let denote the set on the right of (8). Let . We claim that . Since is a clearing vector, we have by limited liability. Let be defined by

| (9) |

for each . Let us fix . We consider the following two cases:

- •

- •

Therefore, .

Conversely, let . We claim that is a clearing vector. Since , there exists such that satisfies all the constraints in (8). In order to show that is a clearing vector, we verify limited liability and absolute priority.

The fact that enforces to satisfy the limited liability condition by the constraint . To show that must also satisfy the absolute priority condition, we consider the following two cases for each .

-

•

Assume that . Then, by the constraints , and . Therefore, , and thus the absolute priority condition holds.

-

•

Assume that . Then, by the constraints , and . Therefore, , and thus the absolute priority condition holds.

Hence, . \Halmos

8 Proofs of the Results in Section 2

Proof 8.1

Proof of Lemma 2.2. Let be with . Then, by the monotonicity of . Moreover, by Section 2.1. Hence, by the monotonicity of . \Halmos

Proof 8.2

Proof of Lemma 2.4. Let with . Let . Since and is monotone, we have

so that . Moreover, since and by the monotonicity of and , we have so that . Therefore, , which completes the proof of monotonicity.

Next, let and . Then, by a simple translation of sets, we obtain

which completes the proof of translativity.

Finally, let . If , then the upper set property holds trivially. Suppose that . Clearly, . Let . Since , by the monotonicity and translativity of , we have . It follows that . \Halmos

9 SAA for the Insensitive Systemic Value-at-Risk

In this section, we prove a convergence result for the insensitive systemic value-at-risk defined in Definition 3.2(i).

Let us fix an aggregation function that satisfies Section 2.1 and Section 2.1. We also fix and . Let with a sequence of its independent copies.

Let . For each , we define

Clearly, when , this is a special case of the insensitive risk measure for a random vector that is uniformly distributed over the finite set (assuming distinct values; otherwise, another discrete distribution where probabilities are integer multiples of ). Moreover, since , the calculation of reduces down to a simple quantile calculation based on a histogram. The next lemma gives simple bounds on the values of .

Lemma 9.1

Let , where . Then,

Proof 9.2

Proof of Lemma 9.1. Since is a decreasing function on , the set in the definition of is an interval that is unbounded from above. Taking yields so that the first inequality in the lemma follows. Taking yields so that the second inequality in the lemma follows. \Halmos

The measurability of is checked in the next lemma.

Lemma 9.3

Let . The function is measurable.

Proof 9.4

Proof of Lemma 9.3. Let for each and . Section 2.1 guarantees that is measurable. Hence, is a Carathéodory function. Then, by Proposition 3.3(i), the function

is a normal integrand on . In particular, the multifunction is closed-valued and measurable by Rockafellar and Wets (2009, Proposition 14.33). Then, as the pointwise infimum of this multifunction, is measurable by Rockafellar and Wets (2009, Example 14.51). \Halmos

In view of Lemma 9.3, composing the function with the first independent copies of yields the random variable . The first main result of the paper addresses the convergence of this random variable to the true value as .

Theorem 9.5

Assume that is not a flat value of the cumulative distribution function of , i.e., the set is either the empty set or a singleton. Then, the sequence converges to almost surely.

Proof 9.6

Proof of Theorem 9.5. As a first step, suppose that there exists such that . Let

By the strong law of large numbers, we have . Let . Since , there exists such that

holds for every . In particular, is feasible for the calculation of so that for every . Hence,

| (10) |

Next, note that , which implies that and it satisfies . Moreover, since the cardinality of is at most one, the cardinality of is also at most one. Hence, we have for every . Then, there exists a sequence that converges to and satisfies for every . Let . Note that . Given , by taking in (10) for each and letting , we get

Hence, almost surely.

Finally, let us define . Since for each , we have . Moreover, let for each and . Since is a Carathéodory function, by Proposition 3.3(iii), there exists with such that the sequence epi-converges to for each , where and are defined in this proposition in terms of . In particular, . Let and . Let us define . Since for each , we have and

Moreover, Lemma 9.1 and the boundedness of on imply that is a bounded sequence. Hence, it has a subsequence that converges to some . Then, by the epi-convergence property in Proposition 3.3(iii), we get

Hence, is feasible for the calculation of so that

It follows that

Therefore, almost surely, which completes the proof. \Halmos

10 Proofs of the Results in Section 3

Proof 10.1

Proof of Proposition 3.3.

(i) Since is open, the function is lower semicontinuous on (on ). Since is a Carathéodory function, is a normal integrand on by Rockafellar and Wets (2009, Proposition 14.45). It follows that is a normal integrand on .

(ii) Since is a normal integrand, by Fatou’s lemma and monotonicity of expectation, we have

for each , which shows the lower semicontinuity of .

(iii) Since is a normal integrand and it is a bounded function, the epi-convergence result is directly given by Artstein and Wets (1995, Theorem 2.3).

\Halmos

Proof 10.2

Proof of Lemma 3.4. Note that is closed and is continuous on by Section 2.1. Hence, by Tietze extension theorem, there exists a continuous function such that for every . Then, we may write

Let and for each and . Since is continuous, it is also measurable. Hence, is a Carathéodory function. Clearly, is also a Carathéodory function. Then, by Proposition 3.3(i), the functions

are lower semicontinuous on . In particular, the set

is closed. Finally, the property follows from closedness combined with the upper set property in Lemma 2.4. \Halmos

Proof 10.3

Proof of Lemma 3.5. Let be as in the proof of Lemma 3.4. For each , we may write

Since are Carathéordory functions, by Proposition 3.3(i), the functions

are normal integrands on . In particular, the multifunction

| (11) |

is closed-valued and measurable by Rockafellar and Wets (2009, Proposition 14.33). \Halmos

Proof 10.4

Proof 10.5

Proof of Theorem 3.7. First, let us consider an arbitrary vector such that and . Let . Clearly, . Moreover, let

By the strong law of large numbers, we have . In particular, as , for every , there exists such that

holds for every . Therefore, for every , is feasible for the calculation of for every . Hence,

| (12) |

Next, let and be given by Section 3.1.1. For each , we have and . Let us define

Note that . Given , taking in (12) for each and letting gives

since converges to and is continuous. Hence, almost surely.

Conversely, let be defined as in the proof of Lemma 3.5 and recall that we have (11) for each and . Let and for each . Similar to (11), note that we also have

Moreover, by Proposition 3.3(iii), there exists with such that the sequences and epi-converge to , , respectively, for each . In particular, .

Let and . By the first part of the proof, is feasible for the calculation of for every . Since is a closed set by Lemma 3.5 and is a compact set, it follows that there exists an optimal solution , i.e., and

for every . Since is compact, there exists a subsequence that converges to some . Moreover, the epi-convergence property given by Proposition 3.3(iii) yields that

as well as

In other words, we obtain

Hence, is feasible for the calculation of so that

It follows that

Therefore, almost surely. \Halmos

Proof 10.6

Proof of Theorem 3.8. Let be as given by Section 3.1.2. Note that we have

Moreover, we have since for each . Let for each . Then, the sequence satisfies Section 3.1.1 for this choice of . Therefore, by Theorem 3.7, converges to almost surely. \Halmos

Proof 10.7

Proof of Lemma 3.9. Let be as in Section 3.1.3. Since , we have

In particular, letting for each and writing , we have so that . Let . Note that we have

In particular, , i.e., . This implies that , where is defined by

for each . Hence, follows. The requirement can be satisfied by replacing by if necessary. \Halmos

Proof 10.8

Proof of Theorem 3.12. Let . Let be as in Section 3.1.3. We claim that

| (13) |

By Lemma 3.13, there exists such that

and we have . If , then we have

since ; hence, (13) holds in this case. In general, since , we have

where the equality follows as a result of an elementary calculation. Let . Note that so that

by the previous case. Hence, (13) holds in the general case as well.

Let be given by Section 3.1.3. In particular, . Thanks to (13), we have so that . Then, the definition of the distance function guarantees that

Since and converges to , there exists such that for every . Let for each . Then, the sequence satisfies Section 3.1.1 for . Hence, by Theorem 3.7, converges to almost surely.

Let

Note that . Let . We have . Hence, there exists such that for every . Let . Then, there exists such that . In particular, since , by Lemma 3.13, there exists such that . Then,

so that . By the definition of the distance function , it follows that

Since this holds for every , we conclude that

Hence, converges to almost surely.

Finally, by choosing a countable dense subset of and using the continuity of and for each , we conclude that Wijsman-converges to almost surely. \Halmos

Proof 10.9

Proof of Lemma 3.13. Let us fix , which exists by assumption. Let . Due to the definition of the distance function , we have

Since is a nonempty compact set, it follows that there exists such that . We claim that . Indeed, since , we have

Then, an elementary calculation to evaluate the above infimum yields

which implies that . \Halmos

Proof 10.10

Proof of Lemma 3.14. If , then we have trivially. Let us assume that for the rest of the proof.

The part of the claimed equality is obvious. For the part, by Lemma 3.13, note that there exists such that and we also have . On the other hand, since , we have as otherwise one could construct a point in a neighborhood of that is strictly closer to than . Then, by Löhne (2011, Definition 1.45, Corollary 1.48(iv)), is a weakly minimal point of . Hence,

| (14) |

Since we also have by (2), there exists such that . Then, (14) implies that . If , then so that , which completes the proof in this case.

Suppose that . Let . Then, we have and . Let us define a point by

Clearly, . Since , we also have . Since and , we also have . Since , for each , we have ; for each , we have

It follows that

Since , we conclude that , which completes the proof in this case too. \Halmos

Proof 10.11

Proof of Theorem 3.16. First, we show that Wijsman-converges to almost surely. Let . By Lemma 3.14, we have