Uncoupled and Convergent Learning in Monotone Games under Bandit Feedback

Abstract

We study the problem of no-regret learning algorithms for general monotone and smooth games and their last-iterate convergence properties. Specifically, we investigate the problem under bandit feedback and strongly uncoupled dynamics, which allows modular development of the multi-player system that applies to a wide range of real applications. We propose a mirror-descent-based algorithm, which converges in and is also no-regret. The result is achieved by a dedicated use of two regularizations and the analysis of the fixed point thereof. The convergence rate is further improved to in the case of strongly monotone games. Motivated by practical tasks where the game evolves over time, the algorithm is extended to time-varying monotone games. We provide the first non-asymptotic result in converging monotone games and give improved results for equilibrium tracking games.

1 Introduction

We consider multi-player online learning in games. In this problem, the cost function for each player is unknown to the player, and they need to learn to play the game through repeated interaction with other players. We focus on a class of monotone and smooth games, which was first introduced by Rosen, (1965). This encapsulates a wide array of common games, such as two-player zero-sum games, monotone-concave games, and zero-sum polymatrix games (Bregman and Fokin,, 1987). Our goal is to find algorithms that solve the problem under bandit feedback and strongly uncoupled dynamics. Within this context, each player can only access information regarding the cost function associated with their chosen actions without prior insight into their counterparts. This allows modular development of the multi-player system in real applications and leverages existing single-agent learning algorithms for reuse.

Many works have focused on the time-average convergence to Nash equilibrium on learning in monotone games (Even-Dar et al.,, 2009; Syrgkanis et al.,, 2015; Farina et al.,, 2022). However, these works only guarantee the convergence of the time average of the joint action profile. Such convergence properties are less appealing, because while the trajectories of the players converge in the time-average sense, it may still exhibit cycling (Mertikopoulos et al.,, 2018). This jeopardizes the practical use of such algorithms.

Popular no-regret algorithms such as mirror descent have demonstrated convergence in the last iterate within specific scenarios, such as two-player zero-sum games (Cai et al.,, 2023) and strongly monotone games (Bravo et al.,, 2018; Drusvyatskiy et al.,, 2022; Lin et al.,, 2021). Yet convergence to Nash equilibrium in monotone and smooth games is not available unless one assumes exact gradient feedback and coordination of players (Cai et al.,, 2022; Cai and Zheng,, 2023). It remains open as to whether a no-regret algorithm can efficiently converge to a Nash equilibrium in monotone games with bandit feedback and strongly uncoupled dynamics. In this paper, we investigate the pivotal question:

How fast can no-regret algorithms converge (in the last iterate) to a Nash equilibrium in general monotone and smooth games with bandit feedback and strongly uncoupled dynamics?

In this work, we present a mirror-descent-based algorithm designed to converge to the Nash equilibrium in static monotone and smooth games. Our algorithm is uncoupled and convergent and is applicable to the general monotone and smooth game setting. Motivated by real applications, where many games are also time-varying, we extend our study to encompass time-varying monotone games. This allows the algorithm to be deployed in both stationary and non-stationary tasks. We achieve state-of-the-art results in both monotone games and time-varying monotone games.

We summarize our main contributions as follows:

-

•

In static monotone and smooth games:

-

–

Under bandit feedback and strongly uncoupled dynamics, we show our algorithm achieves a last-iterate convergence rate of .

- –

-

–

Our algorithm is no regret albeit players may be self-interested. The individual regret is at most in monotone games and at most in strongly monotone games.

-

–

-

•

In time-varying monotone and smooth games:

-

–

If the game eventually converges to a static state within a time frame of , our algorithm achieves convergence in .

- –

-

–

2 Related Works

Monotone games

The convergence of monotone games has been studied in a significant line of research. For a strongly monotone game under exact gradient feedback, the linear last-iterate convergence rate is known (Tseng,, 1995; Liang and Stokes,, 2019; Zhou et al.,, 2020). Under noisy gradient feedback, Jordan et al., (2023) showed a last-iterate convergence rate of . Under bandit feedback, Bervoets et al., (2020) proposed an algorithm that asymptotically converges to the equilibrium if it is unique. Bravo et al., (2018) subsequently introduced an algorithm with a last-iterate convergence rate of , while also ensuring the no-regret property. Later works (Lin et al.,, 2021) further improved the last-iterate convergence rate to under bandit feedback using the self-concordant barrier function. Jordan et al., (2023) gave a result of the same rate, but with the additional assumption that the Jacobian of each player’s gradient is Lipschitz continuous. In the case of bandit but noisy feedback (with a zero-mean noise), Lin et al., (2021) showed that the convergence rate is still .

For monotone but not strongly monotone games, Mertikopoulos and Zhou, (2019) leveraged the dual averaging algorithm to demonstrate an asymptotic convergence rate under noisy gradient feedback. With access to the exact gradient information, Cai and Zheng, (2023) gave a last-iterate convergence rate of . In the context of bandit feedback, Tatarenko and Kamgarpour, (2019) proposed an algorithm that asymptotically converges to the Nash equilibrium. Table 1 provides a summary of the recent results.

Time-varying monotone games

Motivated by real-world applications such as Cournot competition, where multiple firms supply goods to the market and pricing is subject to fluctuations due to factors like weather, holidays, and politics. Duvocelle et al., (2023) studied the strongly monotone game under a time-varying cost function. When the game converges to a static state, they propose an algorithm that achieves asymptotic convergence under bandit feedback. Assuming the cost function varies across a horizon , Duvocelle et al., (2023) provided an algorithm that attains a convergence rate of under bandit feedback. Subsequent work of Yan et al., (2023) further improved this rate to under exact gradient feedback.

| Class of games | Feedback | Results | |

| Bravo et al., (2018) | StroM | bandit | (E) |

| Drusvyatskiy et al., (2022) | StroM | bandit | (E) |

| Lin et al., (2021) | StroM | bandit (N) | (E) |

| Jordan et al., (2023) | StroM | noisy gradient | |

| Ours | StroM | bandit (N) | (E & P) |

| Mertikopoulos and Zhou, (2019) | M | noisy gradient | asymptotic |

| Cai and Zheng, (2023) | M | exact gradient | |

| Tatarenko and Kamgarpour, (2019) | M | bandit | asymptotic |

| Ours | M | bandit (N) | (E) |

| Cai et al., (2023) | linear* | bandit | (E) |

| Ours | linear | bandit | (E) |

| Class of games | Time-varying property | Feedback | Results | |

| Duvocelle et al., (2023) | StroM | converging in | bandit | asymptotic |

| Ours | M | converging in | bandit | |

| Duvocelle et al., (2023) | StroM | variation path | bandit | |

| Yan et al., (2023) | StroM | variation path | exact gradient | |

| Ours | M | variation path | bandit |

3 Preliminaries

We consider a multi-player game with players, with the set of players denoted as . Each player takes action on a compact and monotone set of dimensions, and has cost function , where is the action of the -th player and is the action of all other players. We assume the radius of is bounded, i.e., . Without loss of generality, we further assume .

In this work, We study a class of monotone continuous games, where the cost functions are monotone and continuous (Assumption 3.1). Games that satisfy this assumption include monotone-concave games, monotone potential games, extensive form games, Cournot competition, and splittable routing games. A discussion of these games is available in Section 3.1. Note that the class of monotone continuous games is commonly studied in the literature (Lin et al.,, 2021; Farina et al.,, 2022).

Assumption 3.1.

For all player , the cost function is continuous, differentiable, convex, and -smooth in . Further, has bounded gradient and the gradient is a monotone operator, i.e., , .

For notational convenience, we denote .

A common solution concept in the game is Nash equilibrium, which is a state of dynamic where no player can reduce its cost by unilaterally changing its action. Our aim is to learn a Nash equilibrium of the game. Formally, the Nash equilibrium is defined as follows.

Definition 3.1 (Nash equilibrium).

An action is a Nash equilibrium if .

When the game satisfies Assumption 3.1, and is with a compact action set, it is known that it must admit at least one Nash equilibrium (Debreu,, 1952).

3.1 Examples of monotone Continuous Games

A wide range of monotone games are captured by Assumption 3.1, and we now present a few classic examples. We include more examples in the appendix.

Example 3.1 (monotone-concave game).

Consider a two-player convex-concave game, where the objective function is , . It is immediate that if is continuous, differentiable, smooth, convex in , concave in , then the game satisfies Assumption 3.1. Examples are rock paper scissors and chicken games.

Example 3.2 (Cournot competition).

In the Cournot oligopoly model, there is a finite set of firms, where firm supplies the market with a quantity of some good and is the firm’s production capacity. The good is priced as a decreasing function , where is the total number of goods supplied to the market, and are positive constants. The cost of firm is then given by , where is the cost of producing one unit of good. This is the associated production cost minus the total revenue from producing units of goods. It is clear that is continuous and differentiable, and Bravo et al., (2018) showed has positive definite and bounded hessian (is convex and smooth).

Example 3.3 (Splittable routing game).

In a splittable routing game, each player directs a flow, denoted as , from a source to a destination within an undirected graph . Each edge is linked to a latency function, represented as , which denotes the latency cost of the flow passing through the edge. The strategies available to player are the various ways of dividing or ”splitting” the flow into distinct paths connecting the source and the destination. With some restrictions on the latency function, the game satisfies Assumption 3.1 (Roughgarden and Schoppmann,, 2015).

3.2 Bandit Feedback and Strongly Uncoupled Dynamic

In this work, we focus on learning under bandit feedback and strongly uncoupled dynamics. The bandit feedback setting restricts each player to only observe the cost function with respect to the action taken . The strongly uncoupled learning dynamic (Daskalakis et al.,, 2011) means players do not have prior knowledge of cost function or the action space of other players and can only keep track of a constant amount of historical information. As the bandit feedback and strongly uncoupled dynamic only require each player to access information of its own, this allows for modular development of the multi-player system, by reusing existing single-agent learning algorithms.

4 Algorithm

Our algorithm builds upon the renowned mirror-descent algorithm. The efficacy of online mirror-descent in solving Nash equilibrium has been demonstrated under full information, or either linear or strongly monotone cost functions, with extensive investigations into its last-iterate convergence investigated in Cen et al., (2021); Lin et al., (2021); Cai et al., (2023); Duvocelle et al., (2023).

Our algorithm differs from classic online mirror descent approaches by making use of two regularizers: A self-concordant barrier regularizer to build an efficient Ellipsoidal gradient estimator and contest the bandit feedback; and a regularizer to accommodate monotone (and not strongly monotone) games. Similar use of two regularizers has also been investigated (Lin et al.,, 2021). However, their method used the Euclidean norm regularize, which cannot be extended to our setting.

Regularizers

Let be a -self-concordant barrier function (Definition 4.1), be a convex function with , . Let denote the Bregman divergence induced by . We choose such that for any , , and for some , to be convex. Notice that when is convex but not linear, we can always find such when the action set is bounded. Intuitively, this is to interpolate a function that possesses less curvature than all . We will discuss the modification to the algorithm needed when is linear in Section 5.3.

Definition 4.1.

A function is a -self concordant barrier for a closed convex set , where is an interior of , if 1) is three times continuously differentiable; 2) if , where is a boundary of ; 3) for and , we have and where .

It is shown that any closed convex domain of has a self-concordant barrier (Lee and Yue,, 2021).

Ellipsoidal gradient estimator

As our algorithm operates under bandit feedback and strongly uncoupled dynamics, we would need to design a gradient estimator while only using costs for the individual player.

Let , be the -dimensional unit sphere and the -dimensional unit ball, respectively. Our algorithm estimates the gradient using the following ellipsoidal estimator:

where is uniformly independently sampled from and are tunable parameters.

One can show that is an unbiased estimate of the gradient of a smoothed cost function . When is strongly convex, one can upper bound by the maximum eigenvalue of and it suffices to take , which recovers the results in Lin et al., (2021). However, when is convex and not strongly convex, one would need to carefully tune to control the bias from estimating the smoothed cost function. This ellipsoidal gradient estimator was first introduced by Abernethy et al., (2008) for the case of being linear, and was then extended by Hazan and Levy, (2014) to the case of strongly convex costs. In learning for games, the ellipsoidal estimator was used in the case of strongly monotone games (Bravo et al.,, 2018; Lin et al.,, 2021).

Based on the ellipsoidal gradient estimator, we present our uncoupled and convergent algorithm for monotone games under bandit feedback.

| (1) |

Implementation

Notice that solving Equation (1) is equivalent to solving a convex but potentially non-smooth optimization problem. Certain sets , including the cases when is the strategy space of a normal-form game or an extensive-form game, can be solved by proximal Newton algorithm provably in iterations (Farina et al.,, 2022). When such guarantees are not required, one could accommodate other optimization methods in solving (1). Our experiment section provides more details.

The choice of and is game-dependent. For example, when and the action set is on the positive half line, we can use the negative log function as our self-concordant barrier function and take .

5 No-regret Convergence to Nash Equilibrium

In this section, we present our main results on the last-iterate convergence to the Nash equilibrium. We show that Algorithm 1 converges to the Nash equilibrium in monotone, strongly monotone, and linear games. Such convergence is no-regret, meaning that the individual regret of each player is sublinear.

For notational simplicity, we present the results in a perfect bandit feedback model, where player observes exactly . The discussion of noisy bandit feedback, where player observes , with be a zero-mean noise, is deferred to the appendix (Theorem D.1).

5.1 Perfect Bandit Feedback

The following theorem describes the last-iterate convergence rate (in expectation) for convex and strongly convex loss under perfect bandit feedback.

Theorem 5.1.

Take , . With Algorithm 1, we have

In the case of the monotone games, Bravo et al., (2018) showed an asymptotic convergence to Nash equilibrium. To the best of our knowledge, Theorem 5.1 is the first result on the last-iterate convergence rate for monotone games. For strongly monotone games, Bravo et al., (2018) first gave a last-iterate convergence rate, which was later improved to by Lin et al., (2021).

While we defer the proof to the appendix, we discuss the main ideas of deriving the results. By the update rule, we can obtain the inequality

| (2) | ||||

where is a fixed point given. When the game is strongly monotone, we can directly use strongly monotoneity and take to be the Euclidean norm to obtain a recursive relation similar to . This amounts to applying this recursion and upper-binding the residual terms individually to obtain a last-iterate convergence. However, when the game is monotone but not strongly monotone, we will need a different approach. Notice that is a monotone operator. Using the property of Bregman divergence, we have

We then sum (2) and leverage the combination of two regularizations, which obtain

Now it suffices to properly choose a fixed point such that both the first term and the third term are bounded. When is the Nash equilibrium , the third term can be upper bounded trivially using the monotoneity of , while it does not imply a bounded first term. Therefore, we set when the first term can be bounded. Otherwise, we set it to a close enough point to , such that the first term can be bounded and the third term is bounded through a more careful calculation.

High probability result

In the case of strongly monotone game, our results show that the last-iterate convergence rate holds with high probability. This is the first high probability result for last-iterate convergence in strongly monotone games.

Theorem 5.2.

With a probability of at least , , and with Algorithm 1, we have .

5.2 Individual Low Regret

Beyond the fast convergence to Nash equilibrium, our algorithm also ensures each player with a sublinear regret when playing against other players. The sublinear regret convergence is a desirable property as the players could be self-interested in general, and want to ensure their return even when other players are not adhering to the protocol. The low regret property remains true for players that are potentially adversarial, despite the convergence to Nash equilibrium no longer holds in that case.

For player , and a sequence of actions , define the individual regret as the cumulative expected difference between the costs received and the cost of playing the hindsight optimal action. That is, , where is a fixed sequence of actions of other players. The following theorem shows a guarantee of the individual regret of each player.

Theorem 5.3.

Take , . For a fixed , a fixed sequence of , and with Algorithm 1, we have

Our result matches the regret bound for strongly monotone games (Lin et al.,, 2021), but applies to monotone games as well.

Implication on social welfare

By designing the algorithm to be no-regret, we can also show that the social welfare attained by the algorithm also converges to the optimal value.

The social welfare for a joint action is defined as . We let to denote the optimal social welfare.

Definition 5.1 (Roughgarden, 2015; Syrgkanis et al., 2015).

A game is -smooth, , , if there exists a strategy , such that for any , .

We have the following proposition which shows that the social welfare converges to optimal welfare on average.

Proposition 5.1.

With , and suppose every player employ Algorithm 1, we have .

5.3 Special Case: Linear Cost Function

When is linear, there does not exist a that is convex while making convex. Algorithm 1 therefore does not apply to the linear case. This coincides with our intuition that the landscape does not provide enough curvature information for the algorithm to utilize.

To extend the algorithm to the linear case, we modify line 6 of Algorithm 1 as

The idea is to first show the convergence of to a game with the cost . With this regularized game, we choose to be a strongly monotone function and measure the convergence in terms of the gap function . By carefully controlling , we obtain the following result.

Theorem 5.4.

With , , and Algorithm 1, we have

Similar regularization techniques have been used in the analysis of the zero-sum game (Cen et al.,, 2021; Cai et al.,, 2023). Our result matches the last-iterate convergence for zero-sum matrix game (Cai et al.,, 2023), which is a class of games with linear cost functions. However, our result is more general as it applies to multi-player linear games with monotone and compact action sets (while previous works only apply to a simplex action set). It remains open to how games with linear cost functions could be effectively learned and whether the convergence rate could be improved.

6 Application to Time-varying Game

In this section, we further apply Algorithm 1 to games that evolve over time. A time-varying game is a game where the cost function , depends on . The game is not revealed to the players before choosing their actions . We assume that satisfies Assumption 3.1 for every .

Such evolving games have applications in Kelly’s auction and power control, where the cost function may change as time-dependent values change, such as channel gains. While the changes of can be random, we discuss two cases here, 1) when converges to a static game in time, and 2) when the variation path of the Nash equilibrium, is bounded in .

Converging monotone game

Let denote the game formed by the costs , and be the game formed by the costs . Suppose converges to , and let be the set of Nash equilibrium of the game . The cost function converges to some cost function in time. The following theorem shows the last iterate convergence to .

Theorem 6.1.

With , take , , and under Algorithm 1, we have .

Evolving game and equilibrium tracking

We now discuss the case where does not necessarily converge to a game , but the cumulative changes of the equilibrium are bounded. We use the variation path to track the cumulative changes of equilibrium. In this case, the last-iterate convergence is meaningless, and the convergence is measured in terms of the average gap. Because of this, the algorithm is slightly modified and updates with .

Theorem 6.2.

Assume , . Take , , and under Algorithm 1, we have .

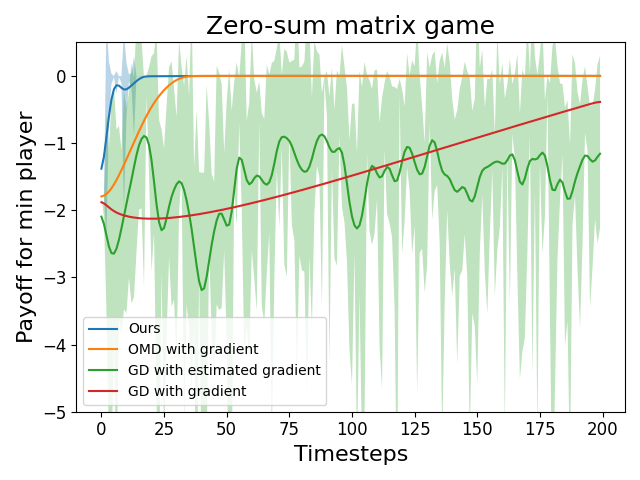

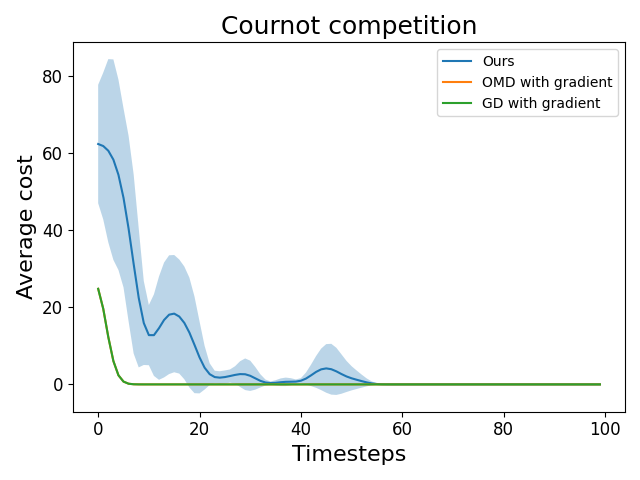

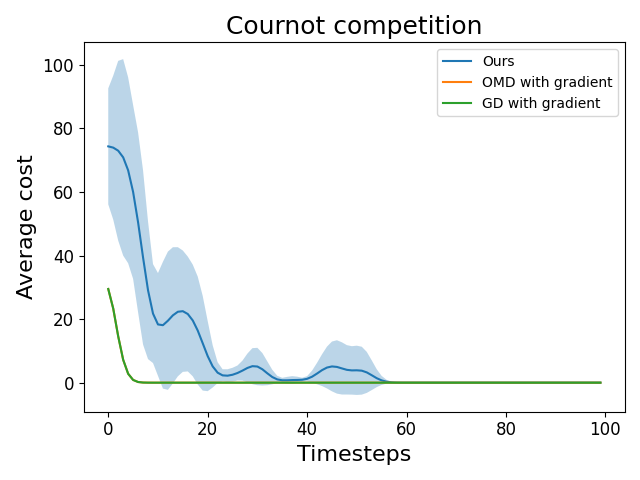

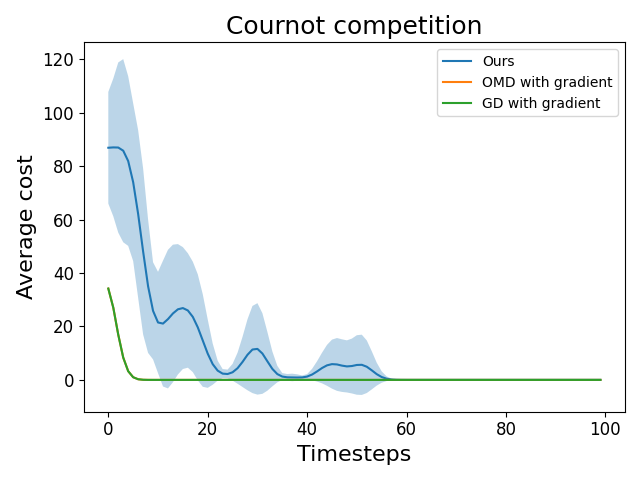

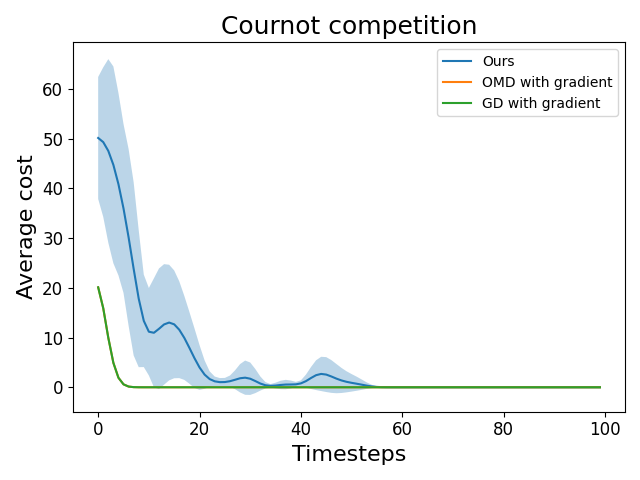

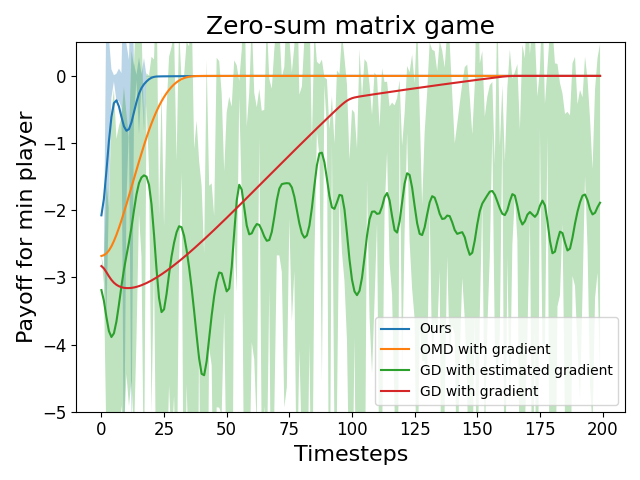

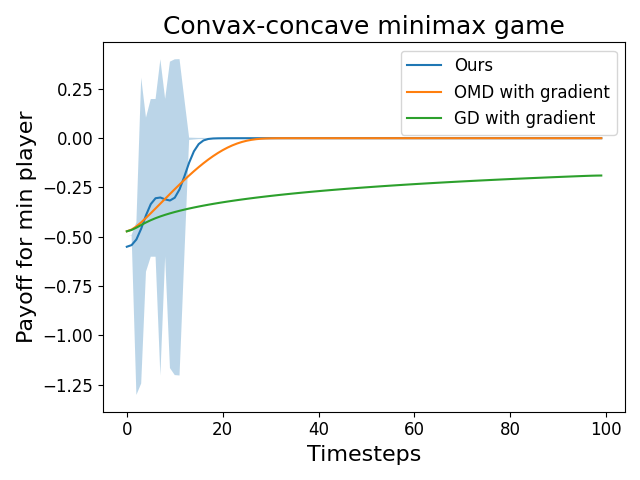

7 Experiment

In this section, we provide a numerical evaluation of our proposed algorithm in three static games. We repeat each experiment with different random seeds. We ran all experiments with a 10-core CPU, with 32 GB memory. We set , and .

We present the results of the following example games described below. More results with other parameters can be found in the Appendix K.

Cournot competition

In this Cournot duopoly model, players compete with constant marginal costs, each having individual constant price intercepts and slopes. We model the game with players, where the margin cost is , price intercept is , and the price slope is .

Zero-sum matrix game

In this zero-sum matrix game, the two players aim to solve the bilinear problem . We set this matrix to be .

monotone zero-sum matrix game

In this monotone version of the zero-sum matrix game, we regularize the game by the regularizer .

Algorithm 1 is evaluated against two baseline methods: online mirror descent and gradient descent, with exact gradient, or estimated gradient (bandit feedback). We set the learning rate to be in both zero-sum matrix games and monotone zero-sum matrix games, and in Cournot competition.

Figure 1 summarizes our experimental findings, where our algorithm attains comparable performance to online mirror descent and gradient descent with full information. We also compare our algorithm to gradient descent with an estimated gradient, using the same ellipsoidal gradient estimator. However, apart from the zero-sum matrix game, we find the baseline algorithm performs too poorly to be compared.

8 Conclusion

In this work, we present a mirror-descent-based algorithm that converges in in general monotone and smooth games under bandit feedback and strongly uncoupled dynamics. Our algorithm is no-regret, and the result can be improved to in the case of strongly-monotone games. To our best knowledge, this is the first uncoupled and convergent algorithm in general monotone games under bandit feedback. We then extend our results to time-varying monotone games and present the first result of for converging games and the improved result of for equilibrium tracking. We further verify the effectiveness of our algorithm with empirical evaluations.

References

- Abernethy et al., (2008) Abernethy, J., Hazan, E., and Rakhlin, A. (2008). Competing in the dark: An efficient algorithm for bandit linear optimization. In Conference on Learning Theory.

- Bartlett et al., (2008) Bartlett, P., Dani, V., Hayes, T., Kakade, S., Rakhlin, A., and Tewari, A. (2008). High-probability regret bounds for bandit online linear optimization. In Conference on Learning Theory.

- Bauschke et al., (2017) Bauschke, H. H., Bolte, J., and Teboulle, M. (2017). A descent lemma beyond Lipschitz gradient continuity: First-order methods revisited and applications. Mathematics of Operations Research, 42(2):330–348.

- Bervoets et al., (2020) Bervoets, S., Bravo, M., and Faure, M. (2020). Learning with minimal information in continuous games. Theoretical Economics, 15(4):1471–1508.

- Bravo et al., (2018) Bravo, M., Leslie, D., and Mertikopoulos, P. (2018). Bandit learning in concave n-person games. Advances in Neural Information Processing Systems.

- Bregman and Fokin, (1987) Bregman, L. and Fokin, I. (1987). Methods of determining equilibrium situations in zero-sum polymatrix games. Optimizatsia, 40(57):70–82.

- Cai et al., (2023) Cai, Y., Luo, H., Wei, C.-Y., and Zheng, W. (2023). Uncoupled and convergent learning in two-player zero-sum markov games. arXiv preprint arXiv:2303.02738.

- Cai et al., (2022) Cai, Y., Oikonomou, A., and Zheng, W. (2022). Finite-time last-iterate convergence for learning in multi-player games. Advances in Neural Information Processing Systems.

- Cai and Zheng, (2023) Cai, Y. and Zheng, W. (2023). Doubly optimal no-regret learning in monotone games. In International Conference on Machine Learning.

- Cen et al., (2021) Cen, S., Wei, Y., and Chi, Y. (2021). Fast policy extragradient methods for competitive games with entropy regularization. Advances in Neural Information Processing Systems.

- Chen and Lu, (2016) Chen, P.-A. and Lu, C.-J. (2016). Generalized mirror descents in congestion games. Artificial Intelligence, 241:217–243.

- Daskalakis et al., (2011) Daskalakis, C., Deckelbaum, A., and Kim, A. (2011). Near-optimal no-regret algorithms for zero-sum games. In Symposium on Discrete Algorithms.

- Debreu, (1952) Debreu, G. (1952). A social equilibrium existence theorem. Proceedings of the National Academy of Sciences, 38(10):886–893.

- Drusvyatskiy et al., (2022) Drusvyatskiy, D., Fazel, M., and Ratliff, L. J. (2022). Improved rates for derivative free gradient play in strongly monotone games. In Conference on Decision and Control. IEEE.

- Duvocelle et al., (2023) Duvocelle, B., Mertikopoulos, P., Staudigl, M., and Vermeulen, D. (2023). Multiagent online learning in time-varying games. Mathematics of Operations Research, 48(2):914–941.

- Even-Dar et al., (2009) Even-Dar, E., Mansour, Y., and Nadav, U. (2009). On the convergence of regret minimization dynamics in concave games. In Symposium on Theory of computing.

- Farina et al., (2022) Farina, G., Anagnostides, I., Luo, H., Lee, C.-W., Kroer, C., and Sandholm, T. (2022). Near-optimal no-regret learning dynamics for general convex games. Advances in Neural Information Processing Systems.

- Hazan and Levy, (2014) Hazan, E. and Levy, K. (2014). Bandit convex optimization: Towards tight bounds. Advances in Neural Information Processing Systems.

- Jordan et al., (2023) Jordan, M. I., Lin, T., and Zhou, Z. (2023). Adaptive, doubly optimal no-regret learning in strongly monotone and exp-concave games with gradient feedback. arXiv:2310.14085.

- Koller et al., (1996) Koller, D., Megiddo, N., and Von Stengel, B. (1996). Efficient computation of equilibria for extensive two-person games. Games and Economic Behavior, 14(2):247–259.

- Lee and Yue, (2021) Lee, Y. T. and Yue, M.-C. (2021). Universal barrier is n-self-concordant. Mathematics of Operations Research, 46(3):1129–1148.

- Liang and Stokes, (2019) Liang, T. and Stokes, J. (2019). Interaction matters: A note on non-asymptotic local convergence of generative adversarial networks. In International Conference on Artificial Intelligence and Statistics, pages 907–915.

- Lin et al., (2021) Lin, T., Zhou, Z., Ba, W., and Zhang, J. (2021). Doubly optimal no-regret online learning in strongly monotone games with bandit feedback. arXiv preprint arXiv:2112.02856.

- Mertikopoulos et al., (2018) Mertikopoulos, P., Papadimitriou, C., and Piliouras, G. (2018). Cycles in adversarial regularized learning. In Proceedings of the twenty-ninth annual ACM-SIAM symposium on discrete algorithms.

- Mertikopoulos and Zhou, (2019) Mertikopoulos, P. and Zhou, Z. (2019). Learning in games with continuous action sets and unknown payoff functions. Mathematical Programming, 173:465–507.

- Rosen, (1965) Rosen, J. B. (1965). Existence and uniqueness of equilibrium points for concave n-person games. Econometrica: Journal of the Econometric Society, pages 520–534.

- Roughgarden, (2015) Roughgarden, T. (2015). Intrinsic robustness of the price of anarchy. Journal of the ACM (JACM), 62(5):1–42.

- Roughgarden and Schoppmann, (2015) Roughgarden, T. and Schoppmann, F. (2015). Local smoothness and the price of anarchy in splittable congestion games. Journal of Economic Theory, 156:317–342.

- Syrgkanis et al., (2015) Syrgkanis, V., Agarwal, A., Luo, H., and Schapire, R. E. (2015). Fast convergence of regularized learning in games. Advances in Neural Information Processing Systems.

- Tatarenko and Kamgarpour, (2019) Tatarenko, T. and Kamgarpour, M. (2019). Learning nash equilibria in monotone games. In IEEE 58th Conference on Decision and Control (CDC). IEEE.

- Tseng, (1995) Tseng, P. (1995). On linear convergence of iterative methods for the variational inequality problem. Journal of Computational and Applied Mathematics, 60(1-2):237–252.

- Yan et al., (2023) Yan, Y.-H., Zhao, P., and Zhou, Z.-H. (2023). Fast rates in time-varying strongly monotone games. In International Conference on Machine Learning. PMLR.

- Zhou et al., (2020) Zhou, Z., Mertikopoulos, P., Bambos, N., Boyd, S. P., and Glynn, P. W. (2020). On the convergence of mirror descent beyond stochastic convex programming. SIAM Journal on Optimization, 30(1):687–716.

Appendix A More Example Games

Example A.1 (Extensive form game (EFG)).

EFGs are games on a directed tree. At terminal nodes denoted as , each player incurs a cost based on a function . The action set of each player, , is represented through a sequence-form polytope known as Koller et al., (1996). Considering the probability of reaching a terminal node , the cost for player is expressed as . Here, signifies the joint strategy profile, and denotes the probability mass assigned to the last sequence encountered by player before reaching . The smoothness and concavity of utilities directly arise from multilinearity.

Example A.2 (monotone potential game).

A game is called a potential game if there exists a potential function , such that, , for all . If is continuous, differentiable, smooth, and monotone in , then the game satisfies Assumption 3.1. For example, a non-atomic congestion game satisfies Assumption 3.1, as shown in Proposition 1 and 2 of Chen and Lu, (2016).

Appendix B Proof of Theorem 5.1

See 5.1

Proof.

We now upper bound the terms in Lemma J.1.

When , taking expectation conditioned on , we have . By Lemma J.2, and the choice , we have

By the definition of ,

By the smoothness of ,

Since is monotone, is positive semi-definite, and . For . Define , we have , and , where is the Dikin ellipsoid. Since , we can upper bound by , the diameter of the set . Hence . By Lemma J.5

When , we set . Then, taking expectation conditioned on , we have . By Lemma J.2, and the choice , we have

Let . When , combing and rearranging the terms, we have

Take , , then , and . Hence, we have

When , combing and rearranging the terms, we have

Take , we have

∎

Appendix C Proof of Theorem 5.3

See 5.3

Proof.

Define the smoothed version of as . Then, we decompose as

For the first term, recall that by the update rule, we have,

By Lemma J.5, for any , we have

where the last equality follows from the definition of Bregman divergence.

Therefore,

By the monotoneity of , we have

Hence

When , by Lemma J.2, we have . Taking expectation conditioned on , we have , and therefore .

Taking summation over , and take , we have

as we assumed is bounded for any .

When , taking expectation conditioned on , we have . By Lemma J.2, and the choice , we have

Taking summation over , and take , we have

as we assumed is bounded for any .

Define . Notice that , so .

-

•

If , then by Lemma J.6, , and .

-

•

Otherwise, we find a point such that and . Then ,

Therefore, .

For the second term, by Jensen’s inequality, we have

Therefore, we have .

When , by the definition of and the smoothness of ,

Since is monotone, is positive semi-definite, and . For . Define , we have , and , where is the Dikin ellipsoid. Since , we can upper bound by , the diameter of the set . Hence .

Therefore, for the third term, we have

Similarly, for the fourth term, we have .

When , by Lemma J.5, for any , we have

where the second inequality is by being positive definite, and .

Therefore, for the third term, we have

Similarly, for the fourth term, we have .

When , with , we have the regret as

When , we have the regret as

Combining the terms yields the final result. ∎

Appendix D Proof of Theorem D.1

We now consider the case where every player receive , where , and . The following theorem describes the last-iterate convergence rate (in expectation) for monotone and strongly monotone loss under noisy bandit feedback.

Theorem D.1.

With ,

Appendix E Proof of Theorem 5.2

See 5.2

Proof.

Lemma J.1, we have

By Lemma J.2, we have

We then decompose the last term as

Therefore,

Combining the terms, and with , we have

∎

Lemma E.1.

With a probability of at least , , we have

Proof.

Define . . Then, with ,

where the third inequality is by the definition of .

By the definition of gradient estimator, we have

Therefore, with

We have

Then, by Lemma 2 of Bartlett et al., (2008), with a probability of at least , ,

∎

Appendix F Proof of Theorem 5.4

See 5.4

Proof.

We consider a regularized game with operator , where , .

Similar to Lemma J.1, we have

Taking expectation conditioned on , we have . By Lemma J.2, and the choice , we have

Combing and rearranging the terms, we have

Take , we have

We can decompose as

Since , we have . Let , , we have

where the last inequality is by taking . ∎

Appendix G Proof of Proposition 5.1

See 5.1

Proof.

Appendix H Proof of Theorem 6.1

See 6.1

Proof.

We now upper bound the remaining terms by discussing them by cases.

When , taking expectation conditioned on , we have . By Lemma J.2, and the choice , we have

By the definition of ,

By the smoothness of ,

Since is monotone, is positive semi-definite, and . For . Define , we have , and , where is the Dikin ellipsoid. Since , we can upper bound by , the diameter of the set . Hence . By Lemma J.5

Let . When , combing and rearranging the terms, we have

Take , , then , and . Hence, we have

where . ∎

Appendix I Proof of Theorem 6.2

See 6.2

Proof.

We first fix a player decomposes

For the second term, we partition the horizon of play into batches , , each of length , . We will determine later. Note that the number of batches is thus . For the batch , we pick to be the Nash equilibrium of the first game. Then

where the third inequality is by the definition of .

Therefore, we have

Define the smoothed version of as . Then, for batch , we decompose as

For the first term, recall that by the update rule, we have,

By Lemma J.5, for any , we have

Therefore,

Rearranging the terms yields

By Lemma J.2, we have . Taking expectation conditioned on , we have , and therefore .

Taking summation over , and take , we have

as we assumed is bounded for any .

Define . Notice that , so .

-

•

If , then by Lemma J.6, , and .

-

•

Otherwise, we find a point such that and . Then ,

Therefore, .

By the definition of and the smoothness of ,

Since is monotone, is positive semi-definite, and . For . Define , we have , and , where is the Dikin ellipsoid. Since , we can upper bound by , the diameter of the set . Hence .

With , we have

Combining, as we have

When , , we set , , , we have

Divided by , we have

Sum over and we have the claimed result. ∎

Appendix J Auxiliary Lemmas

Lemma J.1.

Proof.

By the update rule equation 1, we have

For a fixed point , by the three-point equality of Bregman divergence, we have

Rearranging and by the non-negativity of Bregman divergence, we have,

By Lemma J.3 and the assumption that is monotone, we have

Therefore,

Summing over , by the non-negativity of Bregman divergence, we have

Define , let us consider , the equilibrium of the game.

-

•

If , we set . Let this set of player be

-

•

Otherwise, we find such that and . We set .

By Lemma J.6, and initializing to minimize , thus .

Therefore, we have

By the three-point inequality and the non-negativity of Bregman divergence, we have

By Cauchy-Schwarz and the smoothness of , we have

As is a Nash equilibrium, we have , therefore,

Hence, as ,

∎

Lemma J.2.

Take , we have

Proof.

Define

As adding the linear term does not affect the self-concordant barrier property, and is strongly monotone, is a self-concordant barrier.

Define the local norm , by Holder’s inequality, we have

Notice that

Therefore, by our assumption that ,

∎

Lemma J.3.

[Proposition 1 Bauschke et al., (2017)] For an operator that is monotone,

Proof.

By the monotonicity of , we have

where the second inequality is due to the definition of Bregman divergence. ∎

Lemma J.4 (Lemma 3 Lin et al., (2021)).

For any self-concordant function and let , , we have , where is the local norm given by .

Lemma J.5 (Lemma 7 of Lin et al., (2021)).

Suppose that is a monotone function and is an invertible matrix for each , we define the smoothed version of with respect to by where is a -dimensional unit sphere, is a -dimensional unit ball and for all . Then, the following statements hold true:

-

•

.

-

•

If is -Lipschitz continuous and we let be the largest eigenvalue of , we have .

Lemma J.6 (Lemma 2 Lin et al., (2021)).

Suppose that is a closed, monotone and compact set, is a -self-concordant barrier function for and is a center. Then, we have . For any and , we have and .

Appendix K More Experimental Results

In Figure 2 and 3 we supplement more experiment results for zero-sum matrix games and Cournot competition. Note that in Figure 3, the curve of OMD with gradient coincides exactly with the curve GD with gradient. We found similar observations that our algorithm attains comparable performance to OMD and GD with full information gradient.