Sensitivity of MCMC-based analyses to small-data removal

Abstract

If the conclusion of a data analysis is sensitive to dropping very few data points, that conclusion might hinge on the particular data at hand rather than representing a more broadly applicable truth. How could we check whether this sensitivity holds? One idea is to consider every small subset of data, drop it from the dataset, and re-run our analysis. But running MCMC to approximate a Bayesian posterior is already very expensive; running multiple times is prohibitive, and the number of re-runs needed here is combinatorially large. Recent work proposes a fast and accurate approximation to find the worst-case dropped data subset, but that work was developed for problems based on estimating equations — and does not directly handle Bayesian posterior approximations using MCMC. We make two principal contributions in the present work. We adapt the existing data-dropping approximation to estimators computed via MCMC. Observing that Monte Carlo errors induce variability in the approximation, we use a variant of the bootstrap to quantify this uncertainty. We demonstrate how to use our approximation in practice to determine whether there is non-robustness in a problem. Empirically, our method is accurate in simple models, such as linear regression. In models with complicated structure, such as hierarchical models, the performance of our method is mixed.

1 Introduction

Consider this motivating example. Angelucci et al. (2015) conducted a randomized controlled trial (RCT) in Mexico to study whether microcredit improves business profits. One might choose to analyze the data from this RCT using a simple (but non-conjugate) Bayesian model and Markov chain Monte Carlo (MCMC). Based on an MCMC estimate of the posterior mean effect of microcredit, an analyst might conclude that microcredit actually reduces profit. So, microcredit might be viewed as detrimental to the businesses in this RCT.

Next, if a policymaker wants to advocate against microcredit deployment outside of Mexico, they need to know if microcredit remains detrimental beyond the data gathered in Angelucci et al. (2015). More broadly, many researchers analyze data with Bayesian models and MCMC (Senf et al., 2020; Meager, 2022; Jones et al., 2021; Porter et al., 2022) and want to know if their conclusions generalize beyond their data.

Standard tools to assess generalization do not answer this question entirely. An analyst might use frequentist tools (confidence interval, p-values) to predict whether their inferences hold in the broader population. The validity of these methods technically depends on the assumption that the gathered data is an independent and identically distributed (i.i.d.) sample from a broader population. In practice, we have reason to suspect that this assumption is not met; for instance, it might not be reasonable to assume that data collected in Mexico and data collected in a separate country are i.i.d. from the same distribution.

As pointed out by Shiffman et al. (2023), an analyst might hope that deviations from the i.i.d. assumption are small enough that (a) their conclusions remain the same in the broader population and (b) standard tools accurately assess generalization. On the other hand, the analyst might worry that this hope is misplaced if small, realistic deviations from i.i.d.-ness could affect the substantive conclusions of an analysis. An often-realistic kind of deviation is the missingness of a small fraction of data; for instance, some percentage of the population might not respond to a survey. So, if it were possible to remove a small fraction of data and change conclusions, the analyst might worry about generalization.

Broderick et al. (2023) were the first to formulate sensitivity to dropping a small fraction of data as a check on generalization. Along with the formulation, one contribution of that work is a fast approximation to detect sensitivity when the analysis in question is based on estimating equations (Kosorok, 2008)[Chapter 13]. Regardless of how estimators are constructed, in general, the brute-force approach to finding an influential small fraction of data is computationally intractable. One would need to enumerate all possible data subsets of a given cardinality and re-analyze on each subset. Even when the fraction of data removed is small and each analysis takes little time, there are too many such subsets to consider; see the discussion at the end of section 3. For estimating equations, Broderick et al. (2023) approximate the effect of dropping data with a first-order Taylor series approximation; this approximation can be optimized very efficiently, while the brute-force approach is not at all practical.

Neither Broderick et al. (2023) nor subsequent existing work on small-data removals (Kuschnig et al., 2021; Moitra and Rohatgi, 2022; Shiffman et al., 2023; Freund and Hopkins, 2023) can be immediately applied to determine sensitivity in MCMC. Since MCMC cannot be cast as the root of an estimating equation or the solution to an optimization problem, neither Broderick et al. (2023) nor Shiffman et al. (2023) apply to our situation. As Kuschnig et al. (2021); Moitra and Rohatgi (2022); Freund and Hopkins (2023) focus on ordinary least squares (OLS), their work does not address our problem, either.

Our contributions.

We extend Broderick et al. (2023) to handle analyses based on MCMC. In section 2, we introduce necessary concepts in Bayesian decision-making, and we describe sensitivity to small-data dropping in more detail. In section 3.1, we form a first-order approximation to the effect of removing observations; to do so, we use known results on how much a posterior expectation locally changes under small perturbations to the total log likelihood (Diaconis and Freedman, 1986; Ruggeri and Wasserman, 1993; Gustafson, 1996; Giordano and Broderick, 2023). As this approximation involves posterior covariances, in section 3.2, we re-use the MCMC draws that an analyst would have already generated to estimate what happens when data is removed. Recognizing that Monte Carlo errors induce variability in our approximation, in section 3.3, we use a variant of the bootstrap Efron (1979) to quantify this uncertainty. For more discussion on how our methodology relates to existing work, see section 1.1. In section 4, we provide some theoretical bounds on the quality of our approximation.

Experimentally, we apply our method to three Bayesian analyses. In section 6, we can detect non-robustness in econometric and ecological studies. However, while our approximation performs well in simple models such as linear regression, it is less reliable in complex models, such as ones with many random effects.

1.1 Related work

Our work arguably fits into the intersection of three lines of work. We have already mentioned the first: papers on detecting sensitivity to small-data removal.

The second line of work estimates the changes that happen to a posterior expectation because of small perturbations to the total log likelihood. There are two conceptually distinct approaches to this sensitivity analysis.

-

•

One approach (e.g. Arya et al., 2022, 2023; Seyer, 2023) applies to when the posterior is approximated with a Metropolis-Hastings algorithm. In particular, this approach computes the gradient of the Metropolis-Hastings sampler to small perturbations in the total log likelihood. More broadly, there is a literature on estimating gradients for random processes with discrete components (Kleijnen and Rubinstein, 1996; Fu and Hu, 2012; Heidergott and Vázquez-Abad, 2008).

-

•

The other approach does not compute the gradient of the MCMC algorithm or steps within it. Instead, it directly computes (and then estimates) the gradient of the posterior expectation. Recent works in this literature include Giordano et al. (2018); Mohamed et al. (2020); Giordano and Broderick (2023); Giordano et al. (2023), while foundational works include Diaconis and Freedman (1986); Ruggeri and Wasserman (1993); Gustafson (1996).

In our work, we take the second approach. A priori, it is not clear which approach is superior. Two reasons to prefer the second approach over the first approach are the following. While the discrete operations in Metropolis-Hastings, e.g. the accept/reject steps, pose a key challenge in the first approach, they do not cause any issues in the second approach; the second approach is “oblivious” to details regarding how the posterior is approximated. In addition, suppose that an analyst wishes to compute gradients of multiple quantities of interest. If they follow the first approach, for each quantity of interest, they would need to re-run the sampling algorithm to estimate the gradient. Taking the second approach, the analyst needs to run the sampling algorithm only once; the analyst may then use the resulting draws to simultaneously estimate the gradient of multiple quantities of interest. On the other hand, the first approach might be better than the second approach in the following way. Our experiments later show that gradient estimates coming from the second approach can be noisy. The first approach, with the promise of variance reduction through a good choice of Markov chain coupling, might produce more accurate gradient estimates. It is an interesting direction for future work to apply the first approach to our problem and compare the performance of the two approaches.

While papers taking the second approach have already mentioned how to estimate the effect of dropping an individual observation, these estimates have not been used to assess whether conclusions based on MCMC are sensitive to the removal of a small data fraction. Some works (e.g. Gustafson, 1996; Giordano et al., 2018, 2023) generate perturbations by varying prior or likelihood choice. Giordano and Broderick (2023) estimate the frequentist variability of Bayesian procedures, a task that can be seen as equivalent to the goal of bootstrap resampling. No existing work aims to find a small fraction of data that, if dropped, would change conclusions.

The third set of works, in the Bayesian case influence literature, quantifies the importance of individual observations to a Bayesian analysis. As we will explain, existing works do not tackle our problem. Early works in this area include Johnson and Geisser (1983); Mcculloch (1989); Lavine (1992); Carlin and Polson (1991), while recent works include Marshall and Spiegelhalter (2007); Millar and Stewart (2007); van der Linde (2007); Thomas et al. (2018); Pratola et al. (2023). Such papers focus on the identification of outliers, rather than predictions about whether the conclusion changes after removing a small amount of data. Generally, this literature defines an observation to be an outlier if the Kullback–Leibler (KL) divergence between the posterior after removing the observation and the original posterior is large. For conclusions based on posterior functionals, such as the mean, we are not aware of how to systematically connect the KL divergence to the sensitivity of the decision-making process; in fact, recent work (Huggins et al., 2020) has shown that comparing probability distributions based on the KL divergence can be misleading if an analyst really cared about the comparison between the distributions’ means or variances.

2 Background

We introduce notation in two parts. First, we cover relevant concepts from Bayesian data analysis. Second, we extend the notation to dropping data.

2.1 Bayesian data analysis

Suppose we have a dataset . For instance, in regression, each observation is a vector of covariates and a response ; in this case, we write . Consider a parameter of interest. To estimate the latent , one option is to take a Bayesian approach. First, we probabilistically model the link between and the data through a likelihood function . As an example, in linear regression, consists of the coefficients and the noise , with the likelihood equaling Secondly, we specify a prior distribution over the latent parameters, and use to denote the prior density. Then, the density of the posterior distribution of given the data is

In practice, an analyst uses a functional of the posterior to make conclusions. One prominent functional is the posterior mean , where is a mapping from to . As an example, in linear regression, commonly a practitioner will make a decision based on the sign of the posterior mean of a particular regression coefficient. Other decisions are made with credible intervals. An econometrician might declare that an intervention is helping some population if the vast majority of the posterior mass for a particular coefficient lies above zero. That is, the practitioner checks if the lower bound of a credible interval lies above zero. This decision might be considered to reflect a Bayesian notion of significance. Decisions might also be made with approximate credible intervals; while exact intervals are based on posterior quantiles, an approximate interval is often based on the sum between the posterior mean and a multiple of the posterior standard deviation.

Computationally, in general, the functionals needed to make a conclusion are not available in closed form. To approximate posterior functionals, practitioners frequently use Markov chain Monte Carlo (MCMC) methods. Let denote a set of MCMC draws that target the posterior distribution; a draw refers to a single , and is the number of draws. In practice, we estimate expectations using , and make a decision based on such estimates.

2.2 Sensitivity to small-data removal

With notation for Bayesian data analyses in place, we introduce the problem of sensitivity to small-data removal.

A Bayesian analyst might be worried if the substantive decision arising from their data analysis changed after removing some small fraction of the data. For instance,

-

•

If their decision were based on the sign of the posterior mean, they would be worried if that sign changed.

-

•

If their decision were based on zero falling outside a credible interval, they would be worried if we can make the credible interval contain zero.

-

•

If their decision was based on both the sign and the significance, they would be worried if we can both change the posterior mean’s sign and put a majority of the posterior mass on the opposite side of zero.

In general, we expect an analyst to be worried if we could remove a small fraction of the data and change their decision.

To describe non-robustness precisely and to develop our approximation, we need notation to indicate the dependence of posterior functionals on the presence of data points. We introduce a vector of data weights , where is the weight for the -th observation. Each is constrained to be in the interval . The whole vector defines the so-called weighted posterior distribution.

Definition 2.1.

Let If , the weighted posterior distribution associated with has density

Note that encodes the inclusion of in the analysis. If , the -th observation is ignored; if , the -th observation is fully included. If it exists, we recover the standard posterior density by setting all weights to : . It is possible that is not integrable for some . For instance, consider the case when the prior is improper and all weights have been set to zero: . In the following, we assume that any contribution of the likelihood is enough to define a proper posterior.

Assumption 2.1.

, .

This assumption is immediate in the case of a proper prior and standard likelihood.

The notation emphasizes the dependence on , and will supersede the notation. To indicate expectations under the weighted posterior, we use the subscript ; is the expectation taken with respect to the randomness .

With the weighted posterior notation, we extend concepts from the standard analysis to the new analysis involving weights. The value of a posterior functional depends on . For instance, the posterior mean under the weighted posterior is , and we recover the standard posterior mean by setting .

The Bayesian analyst’s non-robustness concern can be formalized as follows. For , let denote the set of all weight vectors that correspond to dropping no more than of the data, i.e.

We say the analysis is non-robust if there exists a weight that a) corresponds to dropping a small amount of data ( and b) changes the conclusion.

We focus on decision problems that satisfy the following simplifying assumption: there exists a posterior functional, which we denote by , such that and the conclusion changes if and only if . If we are interested in other decision boundaries or the other direction of change, we can add a constant to or multiply it by -1, respectively; so the preceding assumption is made without loss of generality. We call the functional a “quantity of interest” (QoI).

We next show how the changes described at the start of this section fit this framework. First consider a conclusion based on the sign of the posterior mean of a parameter. If the full-data posterior mean () were positive, we would take

Since the full-data posterior mean is positive, . And is equivalent to the posterior mean (after removing the data) being negative. Next consider a conclusion based on whether zero falls in a standard approximate credible interval; we will abbreviate this situation as a conclusion based on “significance.” If the approximate credible interval’s left endpoint444Our approximate credible interval multiplies the posterior standard deviation by , which is the quantile of the standard normal, but we can replace this value with other scaling without undue effort. () were positive, we would take

is equivalent to moving the left endpoint below zero, thus changing from a significant result to a non-significant one. Finally, consider a case where our conclusion is different if we can change to a significant result of the opposite sign. If the approximate credible interval’s left endpoint were positive, we would take

On the full data, the right endpoint is above zero. is equivalent to moving the right endpoint below zero. In this case, the conclusion has changed from a positive result to a significant negative result.

Under our assumptions so far, checking for non-robustness is equivalent to a) finding the maximum value of subject to and b) checking its sign. The outcome of this comparison remains the same if we retain the feasible set, maximize the objective function , and compare the optimal value with , for being any constant that does not depend on weight. Out of later convenience, we set . As in Broderick et al. (2023, Section 2), we define the Maximum Influence Perturbation to be the largest change, induced in a quantity of interest, by dropping no more than of the data. In our notation, it is the optimal value of the following optimization problem:

| (1) |

If the Maximum Influence Perturbation is more than , then the conclusion is non-robust. The set of observations that achieve the Maximum Influence Perturbation is called the Most Influential Set; to report it, we compute the optimal solution of eq. 1 and find its zero indices.

In general, the brute force approach to solve eq. 1 takes a prohibitively long time. We need to enumerate every data subset that drops no more than of the original data. And, for each subset, we would need to re-run MCMC to re-estimate the quantity of interest. There are more than elements in . One of our later numerical studies involves observations; even for , there are more than subsets to consider. Each Markov chain already takes a noticeable amount of time to construct; in this analysis, to generate draws, we need to run the chain for minute. The total time to compute the Maximum Influence Perturbation would be on the order of years.

3 Methods

As the brute force solution to eq. 1 is computationally prohibitive, we turn to approximation methods. In this section, we provide a series of approximations to the Maximum Influence Perturbation problem.

3.1 Taylor series

Our first approximation relies on the first-order Taylor series of the quantity of interest . This idea of approximating the Maximum Influence Perturbation with Taylor series was first proposed by Broderick et al. (2023), in the context of Z-estimators. Our work extends this idea to conclusions based on MCMC.

To be able to form a Taylor series, we require that the quantity of interest is differentiable with respect to the weight . We are not aware of a complete theory (necessary and sufficient conditions) for this differentiability. However, through assumptions 3.1 and 3.2, we state a set of sufficient conditions.

Assumption 3.1.

Let be a function from to the real line. Let be a linear combination of a posterior mean of and its corresponding posterior standard deviation. In particular, there exist constants and , with no dependence on , such that

A typical choice of is the function that returns the -th coordinate of a -dimensional vector.

It might appear that constraining to be a linear combination of the posterior mean and standard deviation is overly restrictive. However, this choice encompasses many cases of practical interest; recall from section 2.2 that the quantities of interest for changing sign, changing significance, and producing a significant result of the opposite sign all take the form in assumption 3.1. Furthermore, the choice of constraining to be a linear combination of the posterior mean and standard deviation in assumption 3.1 is done out of convenience. Our framework can also handle quantities of interest that involve higher moments of the posterior distribution, and the function that combines these moments need not be linear, but we omit these cases for brevity. However, we note that posterior quantiles in general do not satisfy assumption 3.1 and leave to future work the question of how to diagnose the sensitivity of such quantities of interest.

Assumption 3.2.

For any , the following functions have finite expectations under the weighted posterior: , , (for all ), (for all ) and (for all ).

The assumption is mild. It is satisfied by for instance, linear regression under Gaussian likelihood and .

Under assumptions 2.1, 3.1 and 3.2, is continuously differentiable with respect to .

Theorem 3.1.

Take assumptions 2.1, 3.1 and 3.2. For any , is continuously differentiable with respect to on . The -th partial derivative555If lies on the boundary, the partial derivative is understood to be one-sided. at is equal to where

| (2) |

and

| (3) |

See the proof. This theorem is a specific instance of the sensitivity of posterior expectations with respect to log likelihood perturbations; for further reading, see Diaconis and Freedman (1986); Basu et al. (1996); Gustafson (1996). 3.1 establishes both the existence of the partial derivatives and their formula. Equation 2 is the partial derivative of the posterior mean with respect to the weights, while eq. 3 is that for the posterior standard deviation.

Based on 3.1, we define the -th influence as the partial derivative of at :

Then, the first-order Taylor series approximation of is

| (4) |

This approximation predicts that leaving out the -th observation () changes the quantity of interest by . Using eq. 4, we approximately solve eq. 1 by replacing its objective function but keeping its feasible set:

| (5) | ||||

| s.t. |

Solving eq. 5 is straightforward. For any , the objective function is equal to . Let be the optimal solution and be the optimal value of eq. 5. We denote to be the set of observations omitted according to : . Let be indices of the sorted in increasing order: . Let be the smallest index such that ; if none exists, set to . If , assigns weight to the observations , and to the remaining ones. Otherwise, and assigns weight to all observations. Following Broderick et al. (2023), we call the optimal objective value of eq. 5 by the name Approximate Maximum Influence Perturbation (AMIP), and denote it by . It is equal to the negative of , where equals one if its argument is true and 0 otherwise.

3.2 Estimating the influence

To solve eq. 5, we need to compute each influence . In this section, we use MCMC to estimate .

Because of 3.1 and the fact that is the partial derivative at , we know that is a function of certain expectations and covariances under the full-data posterior. Therefore, the MCMC draws from the full-data posterior, which are already used to estimate , can be used to estimate ; see algorithm 1 for the details. In a nutshell, we replace all population expectations with sample averages. The estimate of will be called .

Since is only an approximation of , we are not able to solve eq. 5 exactly; rather, we solve only an approximation of it. Algorithm 2 details the procedure. We denote the outputs of algorithm 2 by and :

| (6) |

While is a point estimate of , is a point estimate of .

Inputs:

-defining constants

Markov chain Monte Carlo draws

Fraction of data to drop

3.3 Confidence intervals for AMIP

from eq. 6 is a noisy point estimate. One concern regarding the quality of is noise due to sampling variability of . In this section, we design confidence intervals for . We begin by considering the special case when the samples come from exact sampling. Then, we relax the exact sampling assumption, and consider general Markov chain Monte Carlo samples.

3.3.1 Exact sampling

For certain prior and likelihoods, we are able to draw exact Monte Carlo samples from the posterior distribution; for instance, consider conjugate models (Diaconis and Ylvisaker, 1979) or models in which convenient augmentation schemes have been discovered, such as Bayesian logistic regression with Polya-Gamma augmentation (Polson et al., 2013). In these cases, we can assume is an i.i.d. sample of size drawn from the full-data posterior distribution. And from eq. 6 can be thought of as an estimator constructed from an i.i.d. sample, though we emphasize that the sample in question is not the data , but . To highlight the dependence between and , we will use the notation . The estimator is a complex, non-smooth function of the sample; the act of taking the minimum across the estimated influences is non-smooth. We do not attempt to prove distributional results for this estimator or use such results to quantify uncertainty. Instead, we appeal to the bootstrap (Efron, 1979), a general-purpose technique to quantify the sampling variability of estimators.

Our confidence interval construction proceeds in three steps. First, we define the bootstrap distribution of . Second, we approximate this distribution with an empirical distribution based on Monte Carlo draws. Finally, we use the range spanned by quantiles of this empirical distribution as our confidence interval for .

To define the bootstrap distribution, consider the empirical distribution of the sample :

We denote one draw from this empirical distribution by . A bootstrap sample is a set of draws: . The bootstrap distribution of is the distribution of , where the randomness is taken over the bootstrap sample but is conditional on the original sample .

Clearly, the bootstrap distribution is discrete with finite support. If we chose to, we could enumerate its support and compute its probability mass function, by enumerating all possible values a bootstrap sample can take. However, this is time consuming. It suffices to approximate the bootstrap distribution with Monte Carlo draws. We will abbreviate the draw as . We generate a total number of such draws. As increases, the empirical distribution of becomes a better approximation of the bootstrap distribution. However, the computational cost scales up with . In practice, in the hundreds is commonplace. Our numerical work uses .

We now define confidence intervals for . Each interval is parametrized by , the nominal coverage level, which is valued in . We compute two quantiles of the empirical distribution over the and quantiles.666We use R’s quantile() to compute the sample quantiles. When is not an integer, the quantile is defined by linearly interpolating the order statistics. We define the interval spanned by these two values as our confidence interval. By default, we set .

One limitation of our current work is that we do not make theoretical claims regarding the actual coverage of such confidence intervals. Although bootstrap confidence intervals can always be computed, whether the actual coverage matches the nominal coverage depends on structural properties of the estimator and regularity conditions on the sample. To verify the quality of these confidence intervals, we turn to empirics. We leave to future work the task of formulating reasonable assumptions and theoretically analyzing the actual coverage.

3.3.2 General MCMC

In section 3.3.1, we made the simplifying assumption that exact sampling was possible. We now lift this assumption and handle the case in which arose from a Markov chain Monte Carlo algorithm (e.g., Hamiltonian Monte Carlo). This case is much more common in practice than the exact sampling case.

To construct confidence intervals, one idea is to use the previous section’s construction without modification. In other words, one could apply the bootstrap to a non-i.i.d. sample. But recall that the Markov chain states are not independent of each other. Theoretically, it is known that the bootstrap struggles on non-i.i.d. samples, for even simple estimators. For example, if the estimator in question is the sample mean and the draws exhibit positive autocorrelation, under mild regularity conditions, the bootstrap variance estimate seriously underestimates the true sampling variance, even in the limit of infinite sample size (Lahiri, 2003, Theorem 2.2). In our case, the bootstrap likely struggles on the sample means that are involved in the definition of from eq. 6; for instance, it is very common for some coordinate that exhibits positive autocorrelation in practice. Therefore, we have reason to be pessimistic about the ability of bootstrap confidence intervals to adequately cover .

Fundamentally, the bootstrap fails in the non-i.i.d. case because the draws that form the bootstrap sample do not have any dependence, while the draws that form the original sample do. To improve upon the bootstrap, one option is to resample in a way that respects the original sample’s dependence structure. We recognize that the sample in question, , is a (multivariate) time series. So we focus on methods that perform well under time series dependence. One such scheme is the non-overlapping block bootstrap (Lahiri, 2003; Carlstein, 1986).777The original paper (Carlstein, 1986) did not use the term “non-overlapping block bootstrap” to describe the technique. The name comes from Lahiri (2003). The sample is divided up into a number of blocks, where each block is a vector of contiguous draws. Let be the number of elements in a block, and let denote the number of blocks.888All samples from the non-overlapping block bootstrap distribution will have length . By construction, it may be the case that . In all of our experiments, we choose so that exactly. The -th block is defined as

To generate one sample from the non-overlapping block bootstrap distribution, we first draw a set of blocks; in particular, we draw them with replacement from the original set of blocks. We call the draws . Then, we write the elements of these drawn blocks in a contiguous series. For example, when and , the two original blocks are , and . The set of possible samples from resampling include and but not .

The name “non-overlapping block bootstrap” comes from the fact that these blocks, viewed as sets, are disjoint from each other. The name is needed in Lahiri (2003) to distinguish from other blocking rules. However, we consider only the above blocking rule, so moving forward we will refer to the procedure as simply the block bootstrap. Intuitively, the block bootstrap sample is a good approximation of the original sample if the latter has short-term dependence; in such a case, the original sample itself can be thought of as the concatenation of smaller, i.i.d. subsamples, and the generation of a block bootstrap sample mimics that construction. In well-behaved probabilistic models with well-tuned algorithms, the MCMC draws can be expected to have only short-term dependence, and the block bootstrap is a good choice.

The block bootstrap has one hyperparameter: the block length . We would like both and to be large; large captures time series dependence at larger lags, and large is close to having many i.i.d. subsamples. However, since their product is constrained to be , the choice of is a trade-off. In numerical studies, we set .

Our construction of confidence intervals for general MCMC proceeds identically to the previous section’s construction, except for the step of generating the bootstrap sample: instead of drawing from the vanilla bootstrap, we draw from the block bootstrap. We will denote the endpoints of such an interval by (lower endpoint) and (upper endpoint).

Similar to the previous section, we do not make theoretical claims on the actual coverage of our block bootstrap confidence intervals; instead, we verify the quality of the intervals through later numerical studies.

3.4 Putting everything together

Now, we chain together the intermediate approximations from the previous sections to form our final estimate of eq. 1. We then explain how to use it to determine non-robustness.

Rather than a single point estimate of the Maximum Influence Perturbation, we provide the interval constructed in section 3.3. This approximation is the result of combining section 3.3, where is designed to cover with high probability, with section 3.1, where approximates the Maximum Influence Perturbation. Our final estimate of the Most Influential Set is from eq. 6. This approximation is the result of combining section 3.2, where approximates , with section 3.1, where approximates the Most Influential Set.

To determine non-robustness, we use as follows. Recall that we have assumed for simplicity that the decision threshold is zero, and that . We believe that the interval contains the quantity of interest after removing the most extreme observations. Therefore, our assessment of non-robustness depends on the relationship between this interval and the threshold zero in the following way:

-

•

. Hence, is entirely on the opposite side of compared to . We declare the analysis to be non-robust.

-

•

. Hence, is entirely on the same side of compared to . We do not declare non-robustness.

-

•

. The interval contains , and we abstain from making an assessment about non-robustness. We recommend practitioners run more MCMC draws to reduce the width of the confidence interval.

While plays the main role in determining non-robustness, plays a supporting role. For problems in which drawing a second MCMC sample is not prohibitively expensive, we can refit the analysis without the data points in . Performing the refit is one way of verifying the quality of our assessment (of non-robustness); if declares that the conclusion is non-robust, and the conclusion truly changes after removing and refitting, then we conclusively know that our assessment is correct.

4 Theory

In this section, we theoretically quantify the errors incurred by our approximations. First, in section 4.1, we analyze the error made by approximating with a first-order Taylor series. Although our analysis is limited to a simple probablistic model, we conclusively show that this error is always small relative to a natural notion of scale. Second, in section 4.2, we analyze the error made by using MCMC to estimate influences . Under more stringent assumptions than those needed to apply our procedure, we show that our estimator possesses a number of desirable properties. For one, our estimator of ( from eq. 6) is consistent in the limit .

4.1 Accuracy of first-order approximation

In this section, we investigate the error incurred by replacing with the Taylor series from section 3.1. While the Taylor series approximation applies to any model that satisfies assumptions 2.1, 3.1 and 3.2, our error analysis is limited to a normal model. To ground our analysis, we first need a notion of scale. A baseline approximation to dropping data is to do nothing, i.e. approximate with . We use the error of this “zeroth-order” Taylor series as the scale. In this section, we show that the first-order error is small in this natural scale. In appendix A, we calculate the errors for a hierarchical extension of the normal model. For such a model, although we can articulate conditions under which the first-order error is smaller than the zeroth-order error, such conditions are not immediately interpretable; we leave to future work to provide a more intuitive understanding of these conditions.

We begin by detailing the data, prior, and likelihood for the normal model. We will also specify a quantity of interest. The -th observed data point is . The parameter of interest is the population mean . The likelihood of an observation is Gaussian with a known standard deviation . In other words, the -th log-likelihood evaluated at is We choose the uniform distribution over the real line as the prior for . The quantity of interest is the posterior mean of .

We next pin down the two notions of error. We define the first-order error to be the (signed) difference between and . We mainly care when encodes the full removal of certain observations and full inclusion of the remaining ones; i.e. . If we let be the function that returns the zero indices of such a weight (), then its inverse takes a set of observation indices and produces a weight valued in . In what follows, we take and . We reformulate the error as a function of instead of by replacing with in the definition of error. After reformulation, we can write the error as follows.

For the zeroth-order approximation, i.e. approximating with , the error is

To display the error formulas, it is convenient to introduce the following notation. We define the sample average of observations as a function of : We denote the sample average of the whole dataset by .

In this model, expectations under the weighted posterior have closed forms. We can derive an explicit expression for the first-order error.

Lemma 4.1.

For the normal model, is equal to

We prove 4.1 in the proof. The error is a function of through the a) the cardinality of the set and b) the difference between the whole dataset’s sample mean, , and the sample mean for elements in . Because is a strict subset of , . So, the denominator is always non-zero, and the error is always well-defined.

We also have an explicit expression for the zeroth-order error.

Lemma 4.2.

For the normal model, is equal to

We prove 4.2 in the proof. Comparing the expression in 4.2 with the expression in 4.1, we see that the first-order error is equal to the zeroth-order error times , which is , the fraction of data removed. We are interested in close to . So, the first-order error is substantively smaller than the zeroth-order error for of interest.

4.2 Desirable properties of MCMC estimators

Recall from section 3.3 that one concern regarding the quality of is the -induced sampling uncertainty. Theoretically analyzing this uncertainty is difficult, with one obstacle being that is a non-smooth function of . In this section, we settle for the easier goal of analyzing the sampling uncertainty of the influence estimates . We expect such theoretical characterizations to play a role in the eventual theoretical characterizations of , but we leave this step to future work.

In this analysis, we make more restrictive assumptions than those needed for 3.1 to hold. We assume that the sample comes from exact sampling; the independence across draws makes it easier to analyze sampling uncertainty. We focus on the quantity of interest equaling the posterior mean ( in the sense of assumption 3.1). The choice is made out of convenience. A similar analysis can be conducted when , but we omit it for brevity. Finally, we need more stringent moment conditions than assumption 3.2.

Assumption 4.1.

The functions (across ) have finite expectation under the full-data posterior.

This moment condition guarantees that the sample covariance between and has finite variance under the full-data posterior. When proving desirable properties about the sample variance, such as consistency, one typical moment condition is that the population kurtosis is finite. Here, the assumed finite variance plays a similar role (in our analysis of sample covariance consistency) as that played by finite kurtosis (in an analysis of sample variance consistency).

With the assumptions in place, we begin by showing that the sampling uncertainty of goes to zero in the limit of .

Lemma 4.3.

Take assumptions 2.1, 3.1, 3.2 and 4.1. Take to be an i.i.d. sample. Let be the output of algorithm 1 for , , and . Then, there exists a constant such that for all and for all , .

We prove 4.3 in the proof. That the variance of individual goes to zero at the rate of is not surprising; is a sample covariance, after all.

We use 4.3 to show consistency of different estimators.

Theorem 4.1.

Take assumptions 2.1, 3.1, 3.2 and 4.1. Take to be an i.i.d. sample. Let be the output of algorithm 1 for , , and . Then converges in probability to in the limit , and converges in probability to in the limit .

We prove 4.1 in the proof. Our theorem states that the vector is a consistent estimator for the vector and is a consistent estimator for .

Not only is consistent in estimating , it is also asymptotically normal.

Theorem 4.2.

Take assumptions 2.1, 3.1, 3.2 and 4.1. Take to be an i.i.d. sample. Let be the output of algorithm 1 for , , and . Then converges in distribution to where is the matrix whose entry, , is the covariance between

and

taken under the full-data posterior.

We prove 4.2 in the proof. Heuristically, for each , the distribution of is the Gaussian centered at , with standard deviation .

4.2.1 Normal model with unknown precision.

The quantity eventually goes to zero as . But for finite , this standard deviation can be large, and can be an imprecise estimate of . To illustrate this phenomenon, we will derive in the context of a simple probabilistic model: a normal model with unknown precision.

We first introduce the model and the associated quantity of interest. The data is a set of real values: , where . The parameters of interest are the mean and the precision of the population. The log-likelihood of an observation based on and is Gaussian: The priors are chosen as follows. is distributed uniformly over the real line, and is distributed according to a gamma distribution. The quantity of interest is the posterior mean of .

For this probabilistic model, the assumptions of 4.2 are satisfied. We show that the variance behaves like a quartic function of the observation .

Lemma 4.4.

In the normal-gamma model, there exists constants , , and , where , such that for all , is equal to .

We prove 4.4 in the proof. are based on posterior expectations. For instance, the proof shows that . It is easy to show that for the normal-gamma model,

Hence, while the mean of behaves like a linear function of , its standard deviation behaves like a quadratic function of . In other words, the more influence an observation has, the harder it is to accurately determine its influence!

5 Experimental Setup

For the rest of the paper, we check the quality of our approximations empirically on real data analyses. In this section, we only describe the checks; for the actual results, see section 6.

A practitioner with a particular definition of “small data” can set to reflect their concern. We consider a number of values. We set the maximum value of to be . This choice is motivated by Broderick et al. (2023). Many analyses are non-robust to removing of the data, and we a priori think that is a large amount of data to remove. We vary in an equidistant grid of length from to . The ten values are , , , , , , , , and . In addition to these 10 values, we also consider that correponds to removing only one observation from the data: in all, there are 11 values of under consideration.

For the range of dropout fractions specified above and across three common quantities of interest corresponding to sign, significance, and significant result of opposite sign changes, we walk through what a practitioner would do in practice (although they would choose only one and one decision). Our method proposes an influential data subset and a change in the quantity of interest, represented by a confidence interval.

Ideally, we want to check if our interval includes the result of the worst-case data to leave out. We are unable to do so, since we do not know how to compute the worst-case result in a reasonable amount of time. We settle for the following checks.

In the first check, for a particular MCMC run, we plot how the change from re-running minus the proposed data compares to the confidence interval. We recommend the user run this check if re-running MCMC a second time is not too computationally expensive.

Unfortunately, such refitting does not paint a complete picture of approximation quality. For instance, the MCMC run might be unlucky since MCMC is random. To be more comprehensive, we run additional checks. We do not expect users to run these tests, as their computational costs are high. The central question is how frequently (under MCMC randomness) the confidence interval includes the result after removing the worst-case data. To assess this frequency, we recall the approximations made in constructing the confidence interval, and check the quality of each approximation separately. In one approximation, we estimate dropping data with a linear approximation; in the other approximation, we construct a confidence interval around the result of the linear approximation. So, we have two checks. The first (section 5.1) checks how frequently the confidence interval includes the result of the linear approximation, i.e. the AMIP. The second (section 5.3) checks whether the AMIP is a good approximation of dropping data. To understand why we observe the coverage in section 5.1, in section 5.2 we isolate the impact of the sorting step in the construction of our confidence interval.

5.1 Estimating coverage of confidence intervals for AMIP

We estimate how frequently covers the AMIP by using another level of Monte Carlo. Recall that is intended to be a confidence interval covering a fraction of the time. If the estimated coverage is far from , we have evidence that does not achieve the desired nominal coverage.

We draw Markov chains; we set . On each chain, we estimate the influences and construct the confidence interval . Observe that, for each , we have estimates of . We take the sample mean across chains and denote this quantity by . Because of variance reduction through averaging, is a much better estimate of than individual . We denote the indices of the most negative by . We sort across and sum the most negative . This sum is denoted by ; we use it in place of the ground truth . We use the sample mean of the indicators as the point estimate of the coverage. We also report a confidence interval for the coverage. This interval is computed using binomial tests designed in Clopper and Pearson (1934) and implemented as R’s binom.test() function.

5.2 Estimating coverage of confidence intervals for sum-of-influence

It is possible that the estimated coverage of is far from the nominal . We suspect that such a discrepancy comes from the sorting of to construct . To modularize out the sorting, we consider a target of inference that is simpler than . At a high level, we fix an index set , and define the target to be the sum of influences in : . On each sample , our point estimate is : this estimate does not involve any sorting, while does. We construct the confidence interval, , from the block bootstrap distribution of . The difference between and , which is constructed from the block bootstrap distribution of , is that the former is not based on sorting the influence estimates. If the actual coverage of is close to the nominal value, we have evidence that any miscoverage of is due to this sorting.

From section 5.1 we use and the associated and as replacement for ground truths. We set to be . We run another set of Markov chains: for each chain, we construct the confidence interval by sampling from the block bootstrap distribution of the estimator . We report the sample mean of the indicators as our point estimate of the coverage. We also report a confidence interval for the coverage. This interval is computed using binomial tests designed in Clopper and Pearson (1934) and implemented as R’s binom.test() function.

5.3 Re-running MCMC on interpolation path

Ideally, we want to know the difference between the Maximum Influence Perturbation and the AMIP. As we have established, we do not know how to compute the former efficiently. We settle for checking the linearity approximation made in section 3.1; recall that this approximation estimates with . In particular, we expect the first-order Taylor series approximation to be arbitrarily good for arbitrarily close to . By necessity, we are interested in some that has a non-trivial distance from . Plotting the quantity of interest on an interpolation path between and , we get a sense of how much we have diverged from linearity by that point.

From section 5.1, we have as our replacement for the ground truth . We focus on : is a large amount of data to remove, and a priori we expect the linear approximation to be poor. Recall that is the set of observations that are most influential according to sorted . Let be the -dimensional weight vector that is for observations in and otherwise. For , the linear approximation of is . In the extreme , we do not leave out any data. In the extreme , we leave out the entirety of i.e. of the data. An intermediate value roughly corresponds999This correspondence is not exact, since for , all observations in are included in the analysis, only with downplayed contributions. to removing of the data. We discretize with values: , , , , , , , , , , , , , , , . For each value on this grid, we run MCMC to estimate , and compare it to the linear approximation.

6 Experiments

In our experiments, we find that our approximation works well for a simple linear model. But we find that it can struggle in hierarchical models with more complex structure.

6.1 Linear model

We consider a slight variation of a microcredit analysis from Meager (2019). In Meager (2019), conclusions regarding microcredit efficacy were based on ordinary least squares (OLS). We refer the reader to Broderick et al. (2023, Section 4.3.2) for investigations of such conclusions’ non-robustness. Here, we instead consider an analogous Bayesian analysis using MCMC, and we examine the robustness of conclusions from this analysis. Even for this very simple Bayesian analysis, it is possible to change substantive conclusions by removing a small fraction of the data.

Our quality checks suggest that our approximation is accurate. Our confidence interval contains the refit after removing the proposed data. The actual coverage of the confidence interval for AMIP is close to the nominal coverage. The actual coverage of the confidence interval for sum-of-influence is also close to the nominal coverage. Even for dropping of the data, the linear approximation is still adequate.

6.1.1 Background and full-data fit

Meager (2019) studies the microcredit data from Angelucci et al. (2015), which was an RCT conducted in Mexico. There are households in the RCT. Each observation is , where is the treatment status and is the profit measured. The log-likelihood for the -th observation is Here, the model parameters are baseline profit , treatment effect , and noise scale . The most interesting parameter is ; as is binary, compares the means in the treatment and control groups. Meager (2019) estimates the model parameters with OLS.

Our variation of the above analysis is as follows. We put t location-scale distribution priors on the model parameters, with the additional constraint that the noise scale is positive; for exact values of the prior hyperparameters, see section C.1. We use Hamiltonian Monte Carlo (HMC) as implemented in Stan (Carpenter et al., 2017) to approximate the full-data posterior. We draw samples.

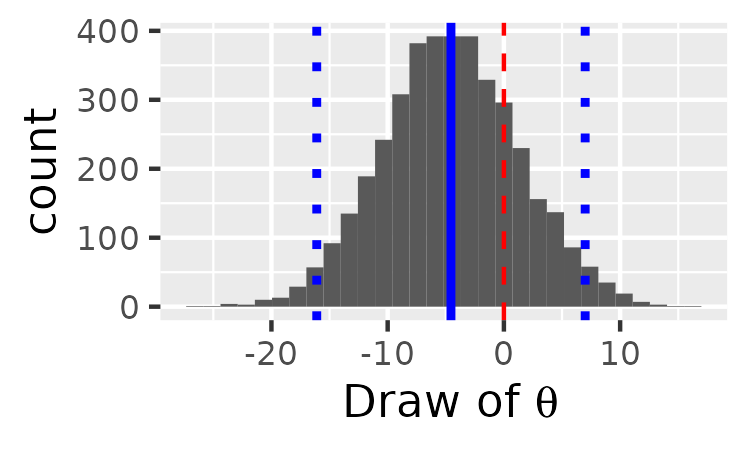

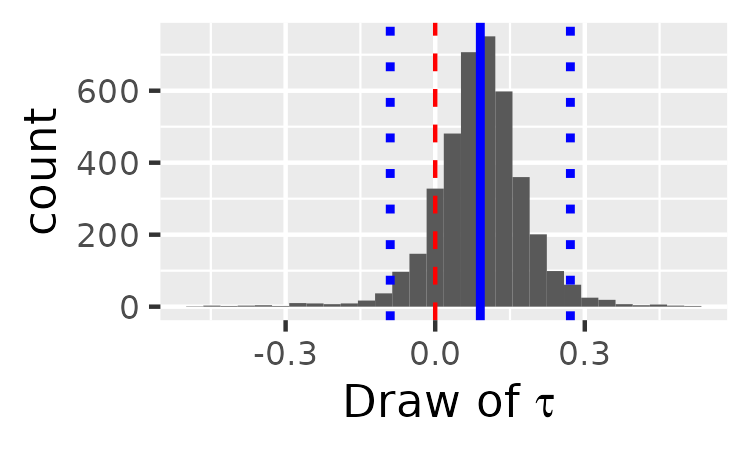

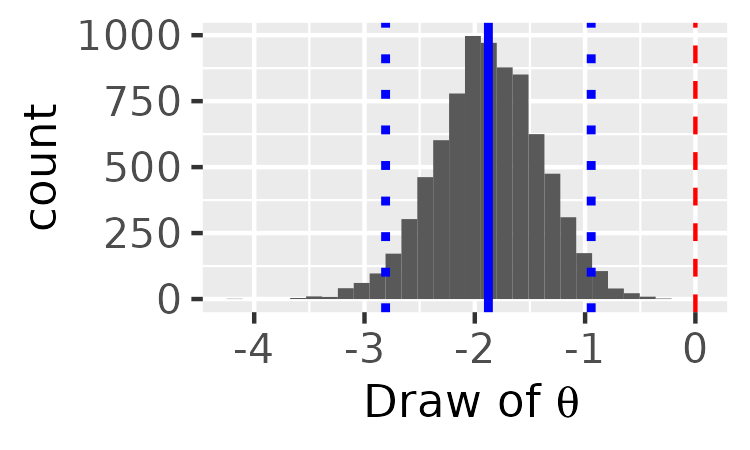

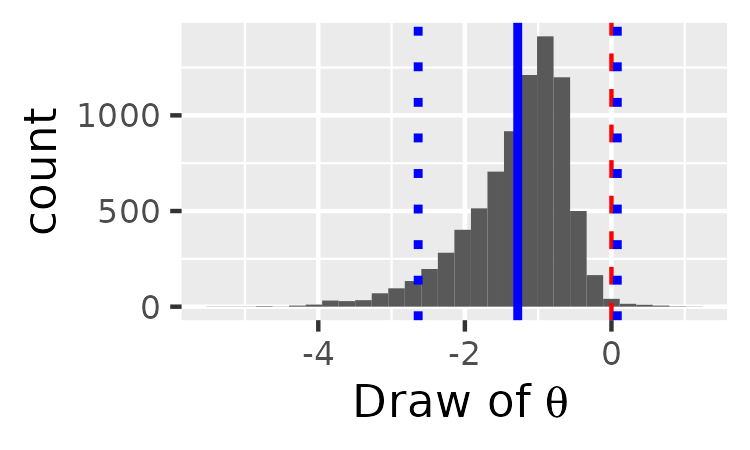

Figure 1 plots the histogram of the treatment effect draws as well as key sample summaries. The sample mean is equal101010We round to two decimal places when reporting results of our numerical studies. to . The sample standard deviation is . These values are close to the point estimate and the standard error from OLS (Meager, 2019). Our estimate of the approximate credible interval’s left endpoint is ; our estimate of the right endpoint is . Based on these summaries, an analyst would likely conclude that while the posterior mean of the effect of microcredit is negative, the uncertainty interval covers zero, so they cannot confidently conclude that microcredit either helps or hurts. These conclusions are in line with Meager (2019).

6.1.2 Sensitivity results

The running of our approximation takes very little time compared to the running of the original analysis. Generating the draws in fig. 1 took 3 minutes on MIT Supercloud (Reuther et al., 2018). For one and one quantity of interest, it took less than seconds to make a confidence interval for what happens if we remove the most extreme data subset. A user might check approximation quality by dropping a proposed subset and re-running MCMC; each such check took us around 3 minutes, the runtime of the original analysis.

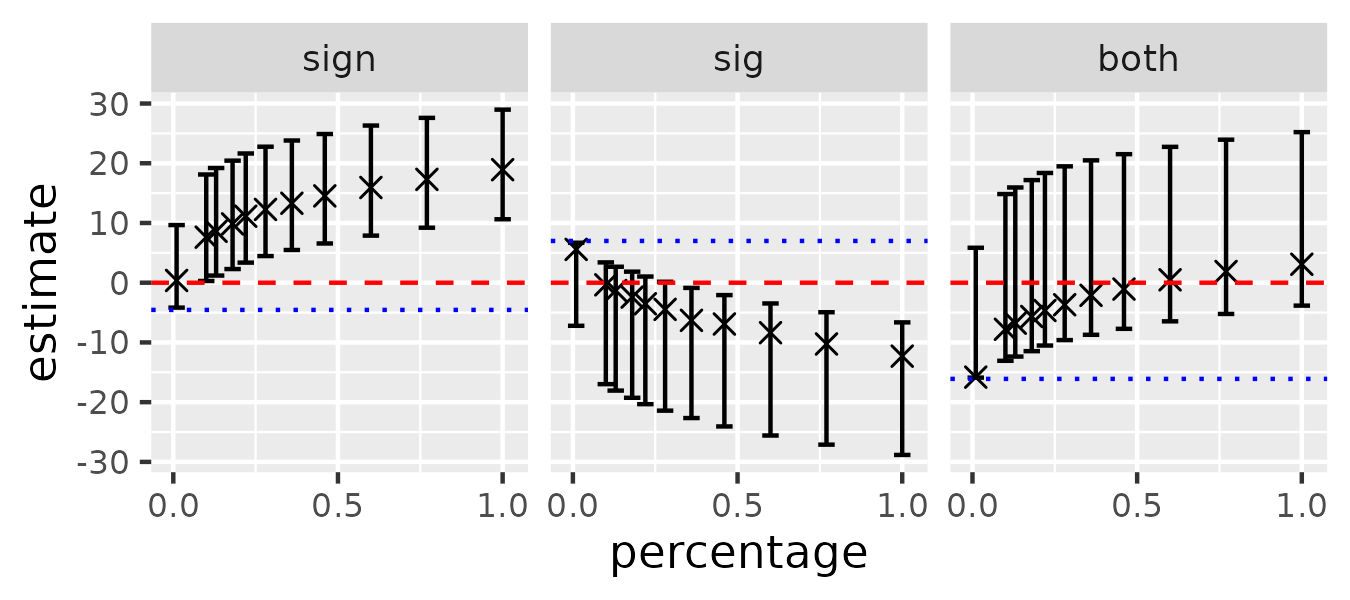

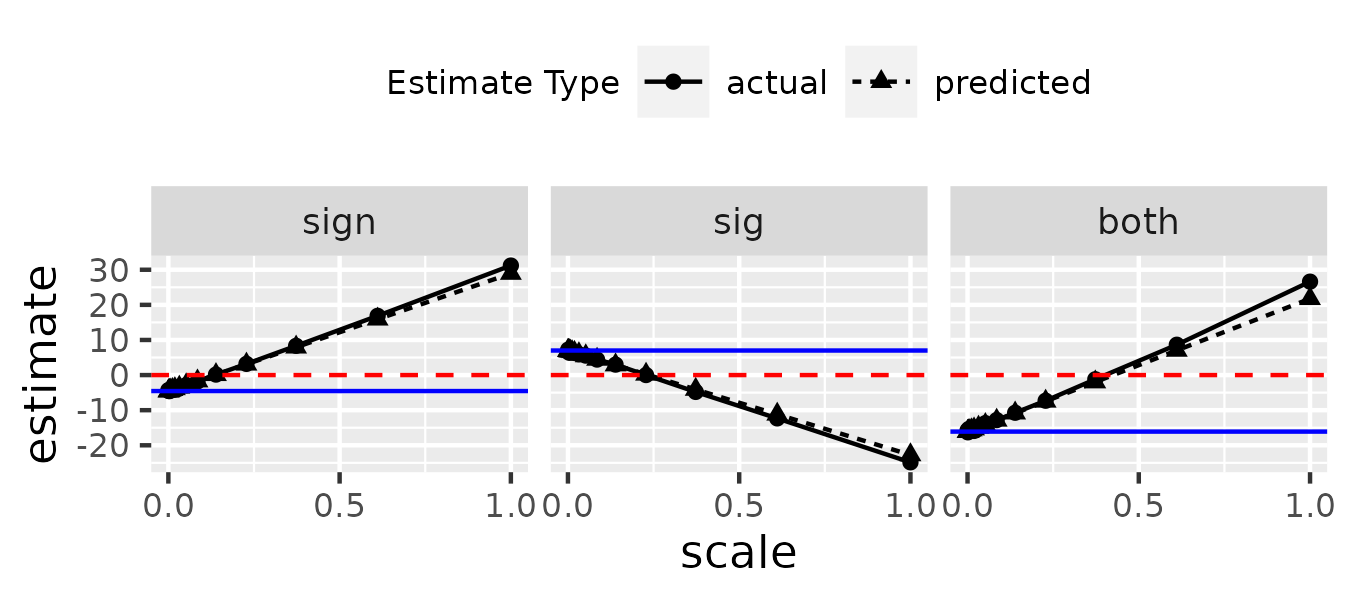

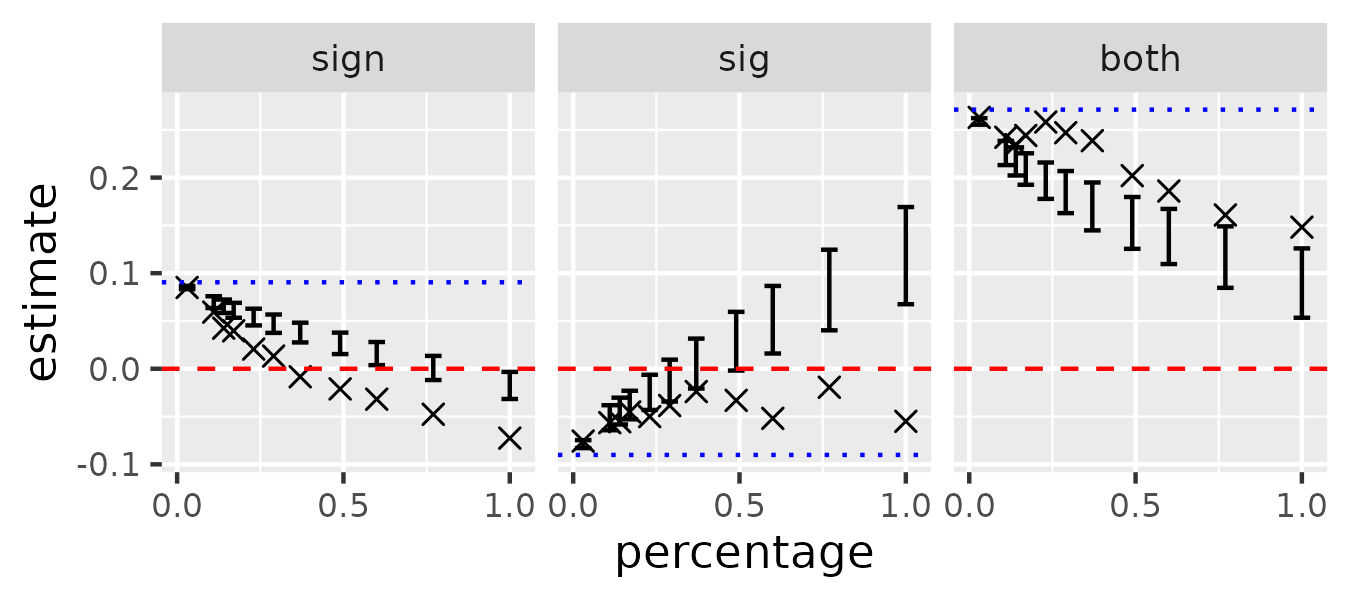

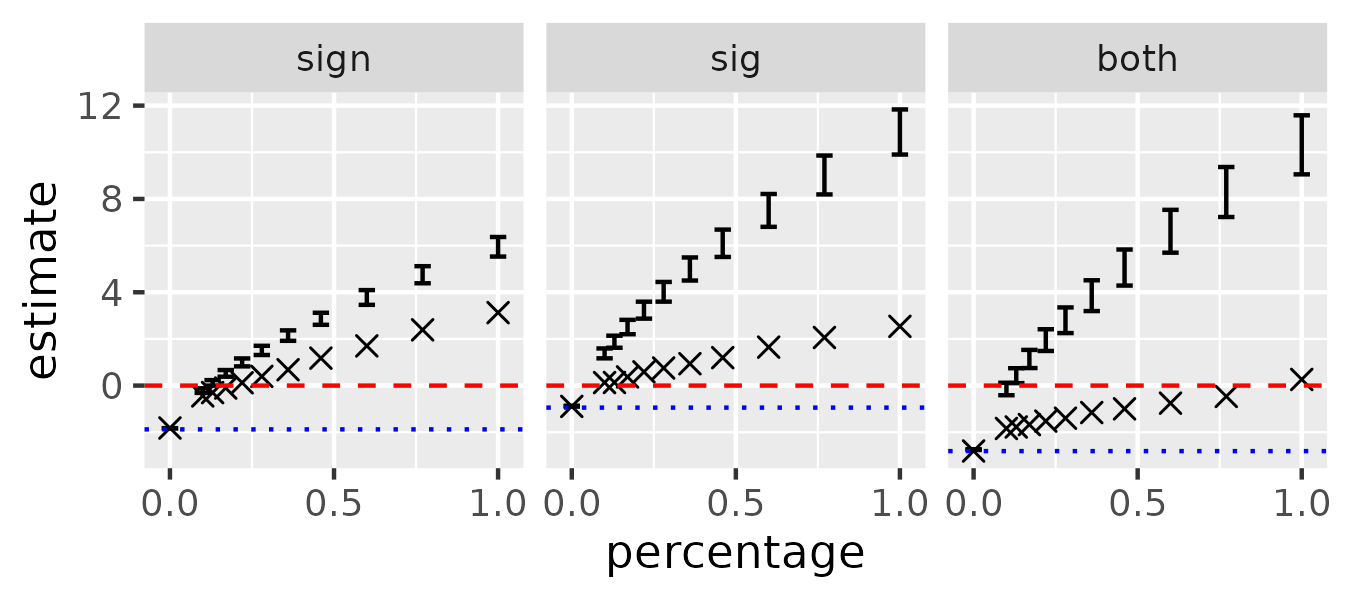

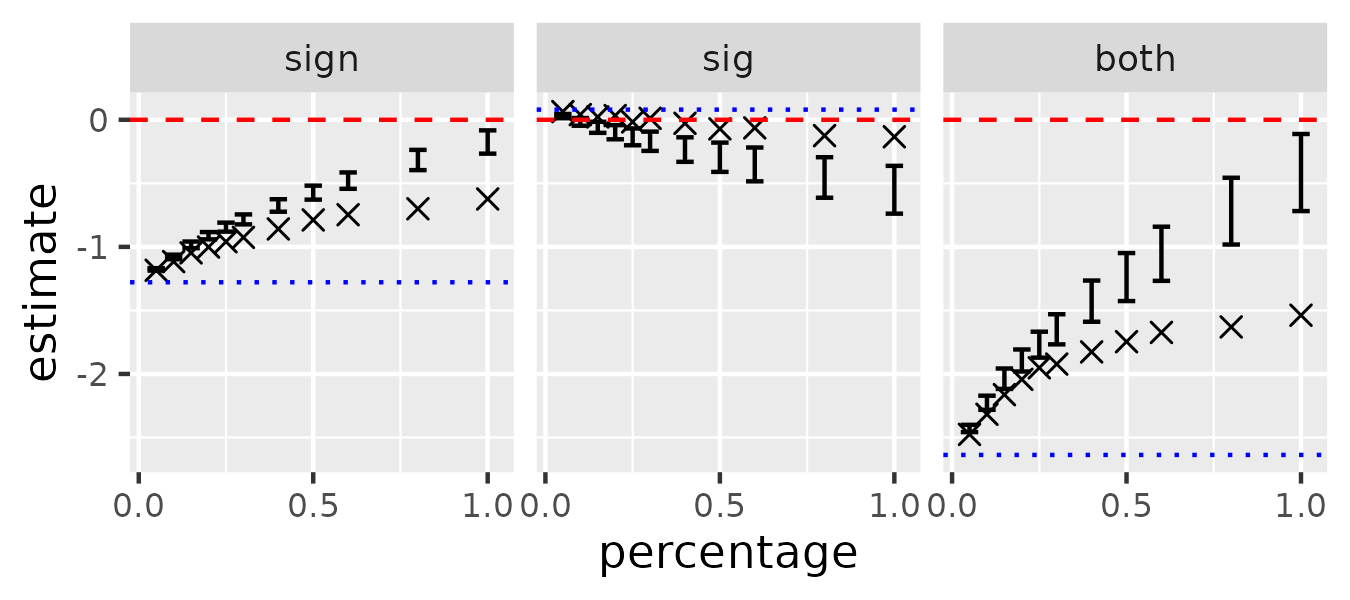

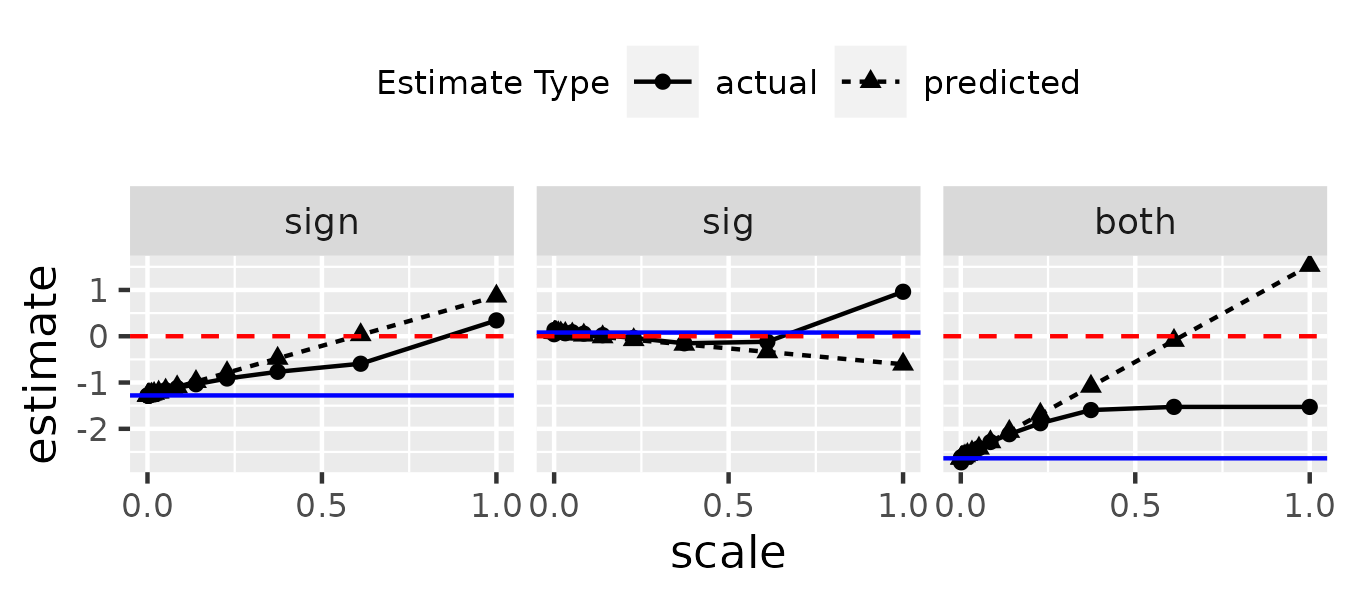

In fig. 2, we plot our confidence intervals and the result after removing the proposed data. Although the confidence intervals are wide, they are still useful. Across quantities of interest and removal fractions, our intervals contain the refit after removing the proposed data. For changing sign, our method predicts there exists a data subset of relative size at most such that if we remove it, we change the posterior mean’s sign. Refitting after removing the proposed data confirms this prediction. For changing significance, our method predicts there exists a data subset of relative size at most such that if we remove it, we change the sign of the approximate credible interval’s right endpoint; refitting confirms this prediction. Our method is not able to predict whether the result can be changed to significant effect of the opposite sign for these values and this number of samples; we recommend a larger number of MCMC samples.

6.1.3 Additional quality checks

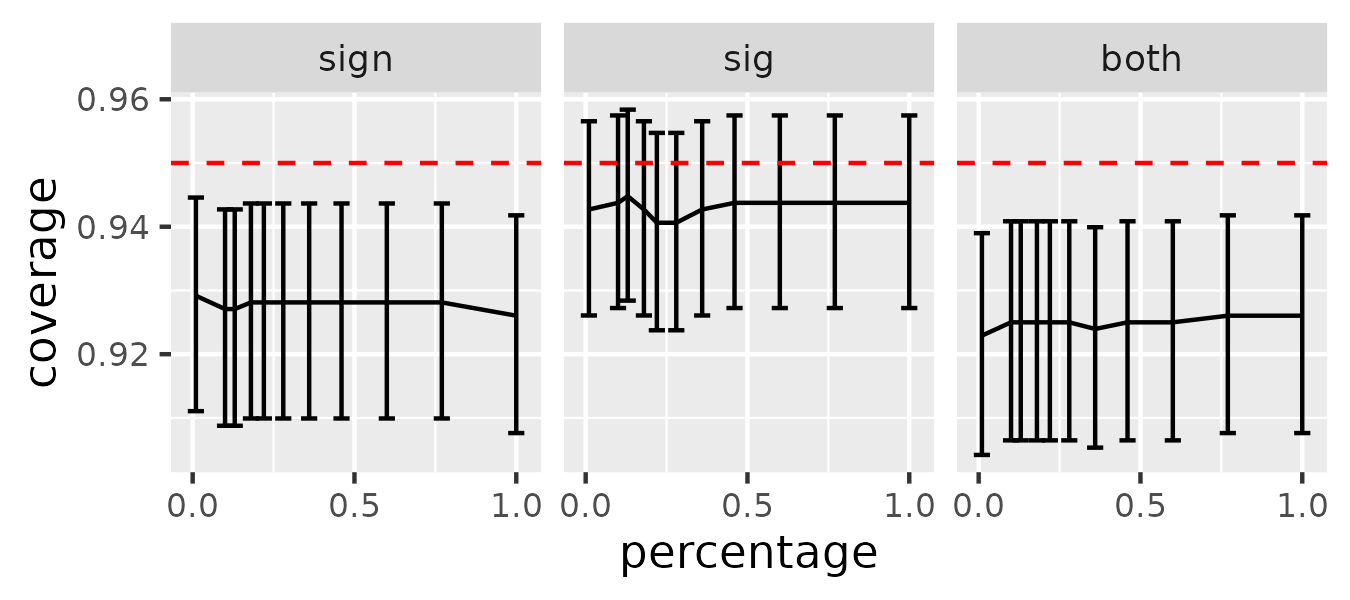

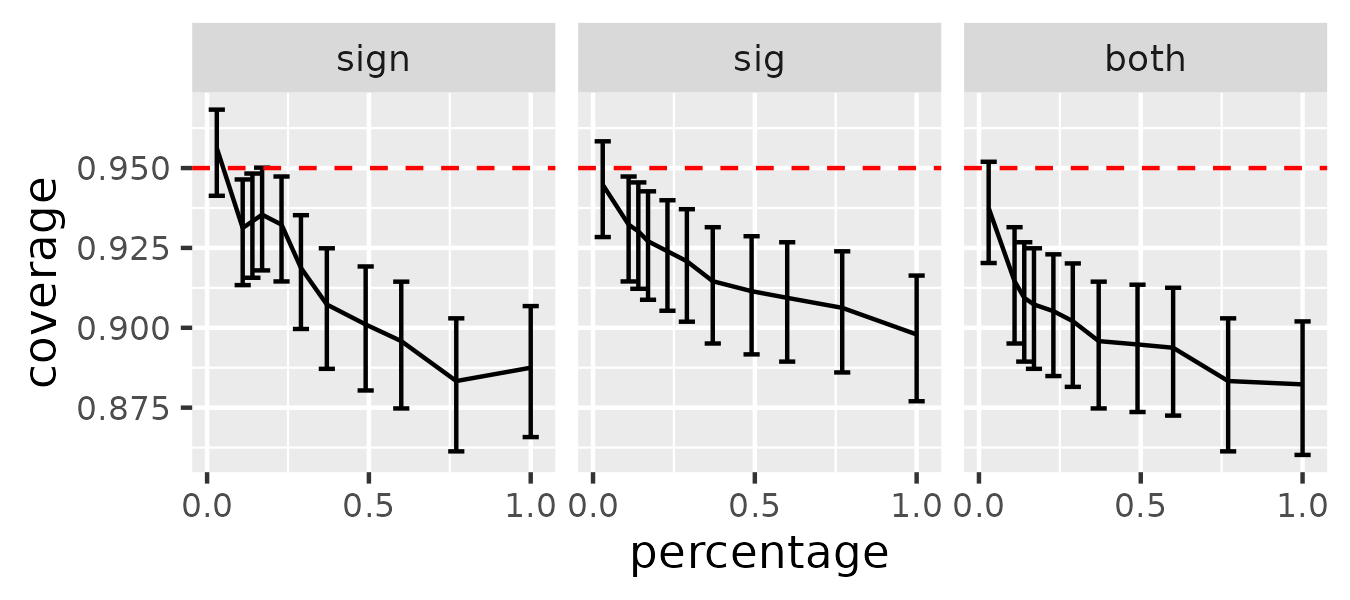

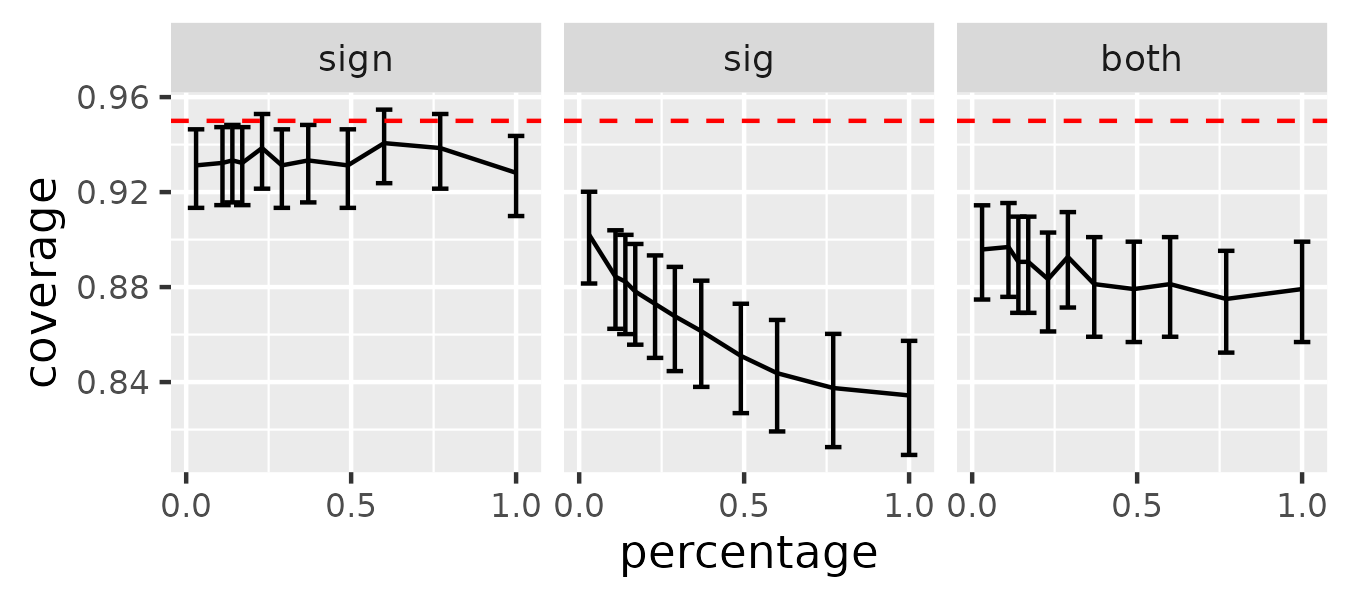

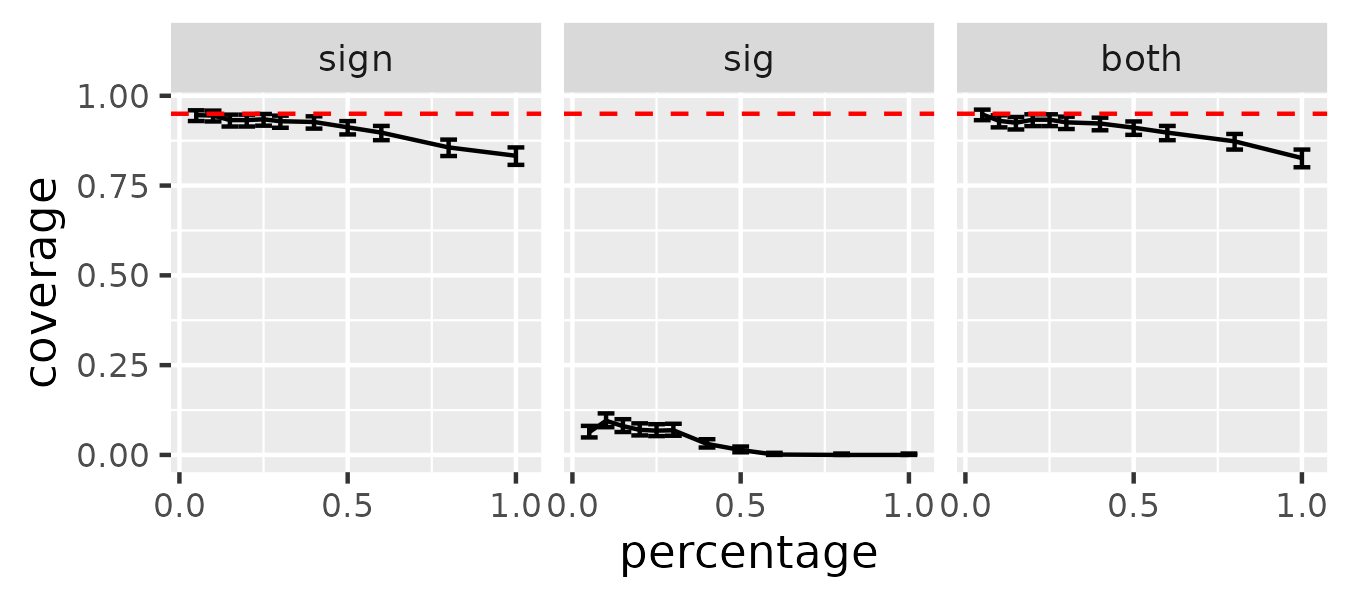

Figure 3 shows that the actual coverage of the confidence interval for the AMIP is close to the nominal one, across . As the half-width of each error bar is small (only ), we believe that the difference between the true coverage and our point estimate of it is small. For either ‘sign’ or ‘both’ QoI, the error bars do not contain the nominal . However, the difference between the point estimate and the nominal is only at worst, which is small. For the ‘sig’ QoI, the point estimate is within of the nominal value, and the error bars contain the nominal .

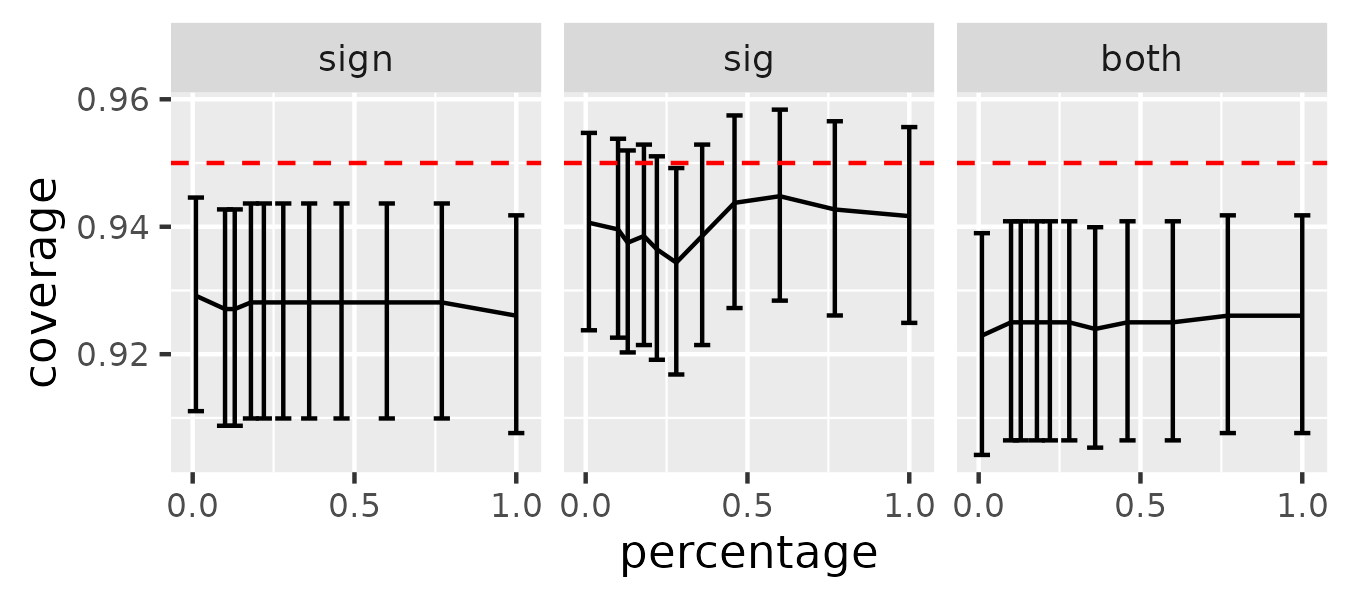

Figure 4 shows that the actual coverage of the confidence interval for the sum-of-influence is close to the nominal one across . The absolute errors between our estimate of coverage and the nominal are similar to those seen in fig. 3. This success suggests that the default block length, , is appropriate for this problem.

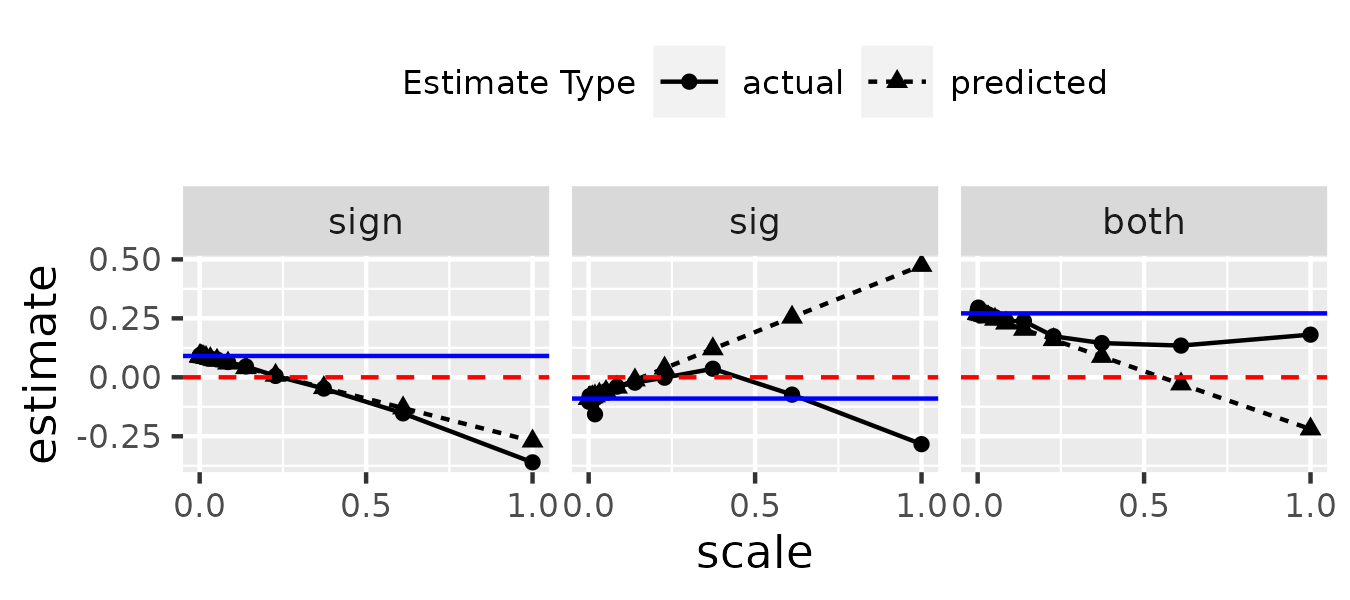

Figure 5 shows that the linear approximation works very well. It is somewhat remarkable that the linear approximation is this good even after dropping , which we consider to be a large fraction of data. The horizontal axis (‘scale’) is the same as in section 5.3. For all quantities of interest, the linear approximation and the refit lie mostly on top of each other; towards the right end of each panel, the approximation slightly underestimates the refit.

6.2 Hierarchical model on microcredit data

We consider a part of the analysis of microcredit done in Meager (2022). Originally, Meager studied a number of impacts made by microcredit, using data from seven separate RCTs analyzed under a hierarchical model fitted with MCMC. In Broderick et al. (2023), the authors fit this hierarchical model using variational inference (Blei et al., 2017) and investigate the non-robustness of the conclusions based on that fit. Here, we focus on only a component of the hierarchical model. We fit this component, which is still a hierarchical model in itself, using MCMC, and examine the fit’s non-robustness.

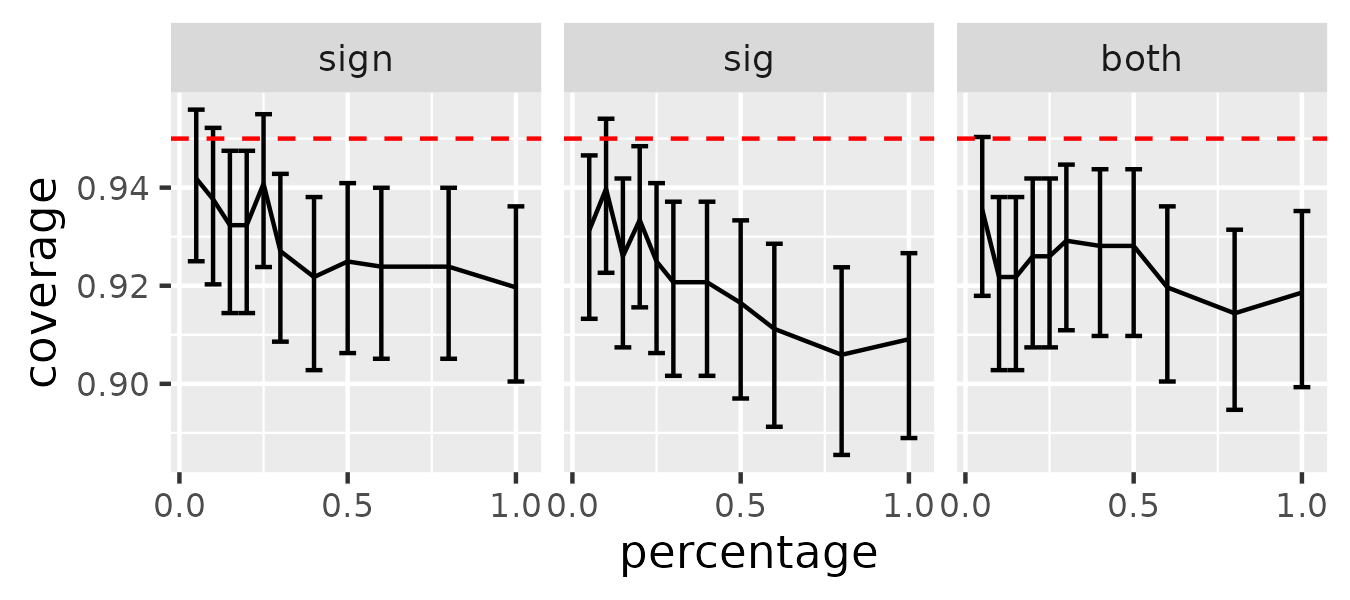

Our approximation does not work as well as it did for the linear model. For the particular MCMC run, our confidence interval does not contain the refit after removing proposed data. The confidence interval for AMIP undercovers: the relative error between estimated coverage and nominal coverage is at most . The confidence interval for the sum-of-influence also undercovers: at worst, the relative error is . The linear approximation is adequate for the posterior mean even after removing . For the credible endpoints, the approximation is good until removing roughly of the data, and breaks down after that.

As articulated in section 5, a priori, we think that is a large data fraction to remove, and we are not worried about the Maximum Influence Perturbation for such . So, that the linear approximation stops working after is not a cause for concern. It is more pressing to improve the confidence intervals. It is likely that a problem-dependent block length will outperform the default .

6.2.1 Background and full-data fit

To study the relationship between microcredit and profit, Meager (2022) combines the data from Angelucci et al. (2015) with that from Attanasio et al. (2015); Augsburg et al. (2015); Banerjee et al. (2015); Crépon et al. (2015); Karlan and Zinman (2011); Tarozzi et al. (2015). In the aggregated data, each observation is a household, with where is the treatment status, is the profit measured, and indicates the household’s country. Meager (2022) uses a tailored hierarchical model that simultaneously estimates a number of effects. This model separates the dataset into three parts: households with negative profit, households with zero profit, and households with positive profit. Microcredit is modeled to have an impact on the proportion of data assigned to each part: for households with non-zero profit, microcredit is modeled to have an impact on the location and spread of the log of absolute profit.

For our experiment, we will not look at all the impacts estimated by Meager (2022)’s model. We focus only on how microcredit impacts the households with negative realizations of profit. Meager (2022)’s model is such that to study this impact, it suffices to a) filter out observations with non-negative profit from the aggregated data and b) use only a model component rather than the entire model.

The dataset on households with negative profits has observations. The relevant model component from Meager (2022) is the following. They model all households in a given country as exchangeable, and “share strength” across countries. The absolute value of the profit is modeled as coming from a log-normal distribution. If the household is in country , this distribution has mean and variance , where are latent parameters to be learned. In other words, the access to microcredit has country-specific impacts on the location and scale of the log of absolute profit. To borrow strength, the above country-specific parameters are modeled as coming from a common distribution. For instance, there exists a global parameter, , such that the ’s are a priori independent Gaussian centered at . For complete specification of the model i.e. the list of all global parameters and the prior choice, see section C.2.

Roughly speaking, is an average treatment effect across countries. We use HMC draws to approximate the posterior. Figure 6 plots the histogram of the treatment effect draws and sample summaries. The sample mean is equal to . The sample standard deviation is . These values are in agreement with the mean and standard deviation estimates obtained from fitting on the original model and data (Meager, 2022). Our estimate of the approximate credible interval’s left endpoint is ; our estimate of the right endpoint is .

Using the summaries in fig. 6, an analyst might come to a decision based on either (1) the observation that the posterior mean is positive, or (2) the observation that the uncertainty interval covers zero and therefore they cannot be confident of the sign of the unknown parameter.

6.2.2 Sensitivity results

Running our approximation takes very little time compared to running the original analysis. Generating the draws in fig. 6 took 8 minutes. For one and one quantity of interest, it took less than seconds to make a confidence interval for what happens if we remove the most extreme data subset. A user might check approximation quality by dropping a proposed subset and re-running MCMC; each such check took us around 8 minutes, the runtime of the original analysis.

Figure 7 plots our confidence intervals and the result after removing the proposed data. In general, our confidence interval predicts a more extreme change than the actual refit achieves. The interval is therefore not conservative: if it predicts that a change is achievable, we cannot always trust that such a change is possible. The refit is not a monotone function of the proposed data’s size in the case of ‘both’ and ‘sig’. The non-monotonicity indicates that not all observations in the proposed data induce the correct direction of change (upon their removal). For instance, in the case of ‘sig’, we aim to increase the credible left endpoint, but actually, the endpoint decreases between and . Since the proposed data is from algorithm 2, it is apparent that the proposed data for is nested in the proposed data for . This means that some observations in the difference between these subsets actually decrease the left endpoint upon removal, rather than increase it.

Our method is not able to predict whether the posterior mean can change sign for these values and this number of samples; likewise, our method is not able to predict whether the result can be changed to a significant effect of the opposite sign. In either case, we recommend a larger number of MCMC samples. For changing significance, our method predicts there exists a data subset of relative size at most such that if we remove it, we change the sign of the approximate credible interval’s left endpoint. However, refitting does not confirm this prediction.

6.2.3 Additional quality checks

Figure 8 shows that the confidence interval for the undercovers, but the degree of undercoverage is arguably mild. Our confidence interval for the true coverage does not contain the nominal except for the smallest . As increases, our point estimate of the coverage generally decreases: for the largest , the difference between our point estimate and the nominal is , which translates to a relative error of . If we compare with the lower endpoint of our confidence interval for the true coverage, the worst relative error is .

Figure 8 shows that the confidence interval for sum-of-influence has the right coverage for sign change, but undercovers for significance change and generating a significant result of the opposite sign. At worst, in the case of ‘sig’, the relative error between the nominal and our estimate of true coverage is .

Intuitively, the block bootstrap underestimates uncertainty if the block length is not large enough to overcome the time series dependence in the MCMC samples. The miscoverage suggests that the default block length, , is too small for this problem. One potential reason for the difference in coverage between ‘sign’ and ‘sig’ is that, the estimate of influence for ‘sign’ involves a smaller number of objects than that for ‘sig’. While an estimate of influence for ‘sign’ involves and , an estimate of influence for ‘sig’ involves , , and . It is possible that the default block length is enough to capture time series dependence for and , but is inadequate for .

Figure 10 provides evidence that the linear approximation is adequate for less than for ‘both’ QoI and ‘sig’, but is grossly wrong for larger . Using the rough correspondence between and amount of data dropped, we say that the linear approximation is adequate until dropping of the data. For ‘both’ QoI, the refit plateaus after dropping , while the linear approximation continues to decrease. For ‘sig’, the refit decreases after dropping , while the linear approximation continues to increase. The approximation is good for ‘sign’ even after removing of the data: the refit and the prediction lie on top of each other for ‘sign’.

6.3 Hierarchical model on tree mortality data

In the final experiment, we break from microcredit and look at ecological data. In particular, we consider a slight tweak of the analysis of European tree mortality from Senf et al. (2020). Senf et al. are acutely aware of generalization concerns. While previous work on tree death had been limited in both time and space, Senf et al. (2020) designs a large study that stretches across Europe and over 30 years, in hopes of making a broad-scale assessment. Our work shows that, even after an expansive study with generalization in mind, one might still worry about applying the findings at large, because of small-data sensitivity.

Our approximation also struggles in this case. For the particular MCMC run used to estimate the full-data posterior, our confidence interval does not contain the refit after removing the proposed data. As each MCMC run is already highly time-consuming, we do not run quality checks on the whole dataset. We settle for running quality checks on a subsample of the data. On the subsampled data, the confidence interval for AMIP undercovers: the undercoverage is severe for one of the quantities of interest. However, the confidence interval for sum-of-influence is close to achieving the nominal coverage. For all three quantities of interest, the linear approximation is good up to removing roughly of the data. For two of the three, it breaks down afterwards; for the remaining one, it continues to be good up to , then falters.

As articulated in section 5, we think that dropping more than of the data is already removing a large fraction. We are not worried about the Maximum Influence Perturbation for such . So, that the linear approximation stops working after is not a cause for concern.

6.3.1 Background and full-data fit

Senf et al. (2020) studies the relationship between drought and tree death in Europe. To identify the association, they have compiled a dataset with observations. Europe is divided into regions, and the data spans 30 years. Each observation is a set of measurements made in a particular region, which we denote as , and at a particular year, which we denote as . For our purposes, it suffices to know that the measurement of (the opposite of) drought is called climatic water balance, and we denote it as . Larger values of indicate that more water is available; i.e. there is less drought. The response of interest, , is excess death of tree canopy.

In our experiment, we mostly replicate (Senf et al., 2020)’s probabilistic model: we use the same likelihood and make only an immaterial modification in the choice of priors. For the likelihood, (Senf et al., 2020) models each as a realization from an exponentially modified Gaussian distribution. Recall that such a distribution has three parameters, (), and a random variate can be expressed as the sum between a normal variate and an exponential variate with rate . When modelling , the model uses the same and for all observations. However, the mean is a function of . It is the sum of three components. The first is an affine function of ; i.e. for some latent parameters and . The second is a smoothing spline of ; it is included to capture non-linear relationships, but we do not go into details here. The third contains the random effects for the region and the time ; if the observation is located at and took place during , this term is .

At a high level, both Senf et al. (2020)’s prior and our prior share strength across regions and times by modeling the random effects as coming from a some common global distributions. However, while Senf et al. (2020) uses an improper prior, we use a proper one. Numerically, there is no perceptible difference between the two. Theoretically, we prefer working with proper priors to avoid the integrability issue mentioned around assumption 2.1. For complete specification of our model, see section C.3.

Following Senf et al. (2020), we make conclusions based on posterior functionals of . Roughly speaking, is the average (across time and space) association effect that water balance has on excess tree death. We use HMC draws to approximate the posterior. Figure 11 plots the histogram of the association effect draws and sample summaries. The sample mean is equal to . The sample standard deviation is . These estimates are very close to those reported in Senf et al. (2020, Table 1). Our estimate of the approximate credible interval’s left endpoint is ; our estimate of the right endpoint is .

In our parametrization, if were estimated to be negative, it would indicate that the availability of water is negatively associated with tree death. In other words, drought is positively associated with tree death. Based on the sample summaries, a forest ecologist might decide that drought has a positive relationship with canopy mortality, since the posterior mean is negative, and this relationship is significant, since the approximate credible interval does not contain zero.

6.3.2 Sensitivity results

Running our approximation takes very little time compared to running the original analysis. Generating the draws in fig. 11 took 12 hours. For one and one quantity of interest, it took less than minutes to make a confidence interval for what happens if we remove the most extreme data subset. A user might check approximation quality by dropping a proposed subset and re-running MCMC; each such check took us around hours, which is the runtime of the original analysis.

Figure 12 plots our confidence intervals and the result after removing the proposed data. In general, our confidence interval predicts a more extreme change than realized by the refit: hence, our interval is not conservative. The overestimation is particularly severe for the ‘both’ QoI and the ‘sig’ QoI. For changing sign, our method predicts there exists a data subset of relative size at most such that if we remove it, we change the posterior mean’s sign; refitting does not confirm this prediction, however. The smallest whose refit’s posterior mean actually changes sign is . For changing significance, our method predicts there exists a data subset of relative size at most such that if we remove it, we change the sign of the right endpoint; refitting confirms this prediction.111111The reason behind our correct prediction is likely the spacing between considered . We expect the refit to be a continuous function of . Based on the scatter plot, it is likely that the refit’s right endpoint changes sign at a between and . However, we do not evaluate the refit at any in this interval. For generating a significant result of the opposite sign, our method predicts there exists a data subset of relative size at most such that if we remove it, we change the sign of the left endpoint; refitting does not confirm this prediction, however. The smallest whose refit’s left endpoint actually changes sign is .

6.3.3 Results on subsampled data

Running MCMC on the original dataset of size over took 12 hours. In theory, we can spend time (on the order of thousands of hours) to run our quality checks, but we do not do so. Instead, we subsample observations at random from the original dataset. Each MCMC on this subsample takes only minutes, making it possible to run quality checks in a few hours instead of weeks. We hope that the subsampled data is representative enough of the original data that the quality checks on the subsampled data are indicative of the quality checks on the original data.

We use the same probabilistic model to analyze the subsampled data. Figure 13 plots the histogram of the association effect draws and sample summaries. Based on the draws, a forest ecologist might tentatively say that drought is positively associated with canopy mortality if they relied on the posterior mean, but refrain from conclusively deciding, since the approximate credible interval contains zero.

Figure 14 shows our confidence intervals and the actual refits. Similar to fig. 12, our confidence intervals predict a more extreme change than realized by the refit. The overestimation is most severe for ‘both’ QoI.

In fig. 15, the confidence interval for AMIP undercovers for all quantities of interest. The actual coverage decreases as increases. The undercoverage is most severe for ‘sig’ QoI: while the nominal level is , the confidence interval for the true coverage only contains values less than . This translates to a relative error of over . In other words, our confidence interval for significance change is too narrow, and rarely contains the AMIP. For ‘both’ QoI and ‘sig’ QoI, the worst-case relative error between the nominal and the estimated coverage, which occurs under the largest , is .

In fig. 16, the estimated coverage of the confidence interval for sum-of-influence is close to the nominal coverage. Note the stark contrast in the vertical scale of the ‘sig’ panel in fig. 15 with that in fig. 16. At worst, our point estimate of the true coverage is less than the nominal level, which is only a relative error. The success of the block bootstrap for the sum-of-influence (fig. 16) indicates that the undercoverage observed in fig. 15 can be attributed to the sorting step involved in the construction of . We leave to future work to investigate why the interference caused by the sorting step is so much more severe for changing the significance than for changing sign or generating significant result of the opposite sign.

Figure 17 shows that the linear approximation is good for the posterior mean (‘sign’ QoI) and the left credible endpoint (‘both’ QoI) up to ; in data percentages, this is roughly . For larger , the refit for ‘both’ QoI plateaus while the linear approximation continues to increase, and the linear approximation for the posterior mean slightly underestimates it. For the left endpoint (‘both’ QoI), the linear approximation is close to the refit up to (roughly of data); afterwards, the left endpoint increases while the linear approximation continues to decrease.

7 Discussion

We have provided a fast approximation to what happens to conclusions made with MCMC in Bayesian models when a small percentage of data is removed. In real data experiments, our approximation is accurate in simple models, such as linear regression. In complicated models, such as hierarchical ones with many random effects, our methods are less accurate. A number of open questions remain. We suspect that choosing the block length more carefully may improve performance; how to pick the block length in a data-driven way is an interesting question for future work. Currently, we can assess sensitivity for quantities of interest based on posterior expectations and posterior standard deviations. For analysts that use posterior quantiles to make decisions, we are not able to assess sensitivity. To extend our work to quantiles, one would need to quantify how much a quantile changes under small perturbations of the total log likelihood. Finally, we have not fully isolated the source of difficulty in complex models like those in Senf et al. (2020). In the analysis of tree mortality data, there are a number of conflating factors.

-

•

The model has a large number of parameters.

-

•

The parameters are organized hierarchically.

-

•

We use MCMC to approximate the posterior.

To determine if the difficulty comes from high dimensionality or if the error comes from hierarchical organization, future work might apply our approximation to a high-dimensional model without hierarchical structure. For instance, one might use MCMC on a linear regression with many parameters and non-conjugate priors. To check if MCMC is a cause of difficulty, one could experiment with variational inference (VI). If we chose to approximate the posterior with VI, we can use the machinery developed for estimating equations (Broderick et al., 2023) to assess small-data sensitivity. If the dropping data approximation works well there, we have evidence that MCMC is part of the problem in complex models.

8 Acknowledgments

The authors are grateful to Hannah Diehl for useful discussions and comments.

This work was supported in part by an ONR Early Career Grant (N000142012532), an NSF CAREER Award (1750286), and

a SystemsThatLearn@CSAIL Ignite Grant.

References

- Angelucci et al. (2015) Manuela Angelucci, Dean Karlan, Jonathan Zinman, Kerry Brennan, Ellen Degnan, Alissa Fishbane, Andrew Hillis, Hideto Koizumi, Elana Safran, Rachel Strohm, Braulio Torres, Asya Troychansky, Irene Velez, Glynis Startz, Sanjeev Swamy, Matthew White, Anna York, and Compartamos Banco. Microcredit Impacts: Evidence from a Randomized Microcredit Program Placement Experiment by Compartamos Banco. American Economic Journal: Applied Economics, 7:151–82, 2015.

- Arya et al. (2022) Gaurav Arya, Moritz Schauer, Frank Schäfer, and Christopher Rackauckas. Automatic differentiation of programs with discrete randomness. Advances in Neural Information Processing Systems, 35:10435–10447, 2022.

- Arya et al. (2023) Gaurav Arya, Ruben Seyer, Frank Schäfer, Kartik Chandra, Alexander K. Lew, Mathieu Huot, Vikash K. Mansinghka, Jonathan Ragan-Kelley, Christopher Rackauckas, and Moritz Schauer. Differentiating Metropolis-Hastings to Optimize Intractable Densities, 2023. URL https://arxiv.org/abs/2306.07961.