Optimal Network Pairwise Comparison

Abstract

We are interested in the problem of two-sample network hypothesis testing: given two networks with the same set of nodes, we wish to test whether the underlying Bernoulli probability matrices of the two networks are the same or not. We propose Interlacing Balance Measure (IBM) as a new two-sample testing approach. We consider the Degree-Corrected Mixed-Membership (DCMM) model for undirected networks, where we allow severe degree heterogeneity, mixed-memberships, flexible sparsity levels, and weak signals. In such a broad setting, how to find a test that has a tractable limiting null and optimal testing performances is a challenging problem. We show that IBM is such a test: in a broad DCMM setting with only mild regularity conditions, IBM has as the limiting null and achieves the optimal phase transition.

While the above is for undirected networks, IBM is a unified approach and is directly implementable for directed networks. For a broad directed-DCMM (extension of DCMM for directed networks) setting, we show that IBM has as the limiting null and continues to achieve the optimal phase transition. We have also applied IBM to the Enron email network and a gene co-expression network, with interesting results.

Keywords. Asymptotic normality, DCMM, directed-DCMM, identifiability, optimal phase transition, signed graph, sparsity.

AMS 2010 subject classification. Primary 62H30, 91C20; secondary 62P25.

1 Introduction

We are interested in the problem of pairwise network comparison or two-sample network hypothesis testing: given two independent (directed or undirected) networks for the same set of nodes, how to test whether the underlying network structures are the same.

The problem is of interest both in theory and in practice, with applications in network analysis, neuroscience, cancer research, and case-control studies, among others. In dynamic network analysis (Liu et al., 2018) and network change-point detection (Jiang et al., 2023), we frequently need to test whether the underlying structures of two networks constructed using two disjoint time intervals are the same. In cancer research and case control studies, it is conventional to use the gene co-expression data to construct two binary networks, one for the control group and the other for the diseased group, and it is of interest to test whether the underlying structures of the two networks are the same (Segerstolpe, 2016). In neuroscience, how to test the similarity of two brain graphs is an active research topic in the interdisciplinary area of neuroscience, statistics, and machine learning; see Tang (2017) for application examples on the topics of neurowiring and neuroimaging.

Real social networks frequently have severe degree heterogeneity (i.e., a degree of one node is much higher than that of another) and mixed-memberships (i.e., some nodes have nonzero weights in more than community; communities are tightly woven clusters of nodes where we have more edges within than between (Girvan and Newman, 2002)). Also, the overall sparsity levels may vary significantly from one network to another.

We are interested in both directed and undirected networks. Consider directed networks first. To capture the above features, we adopt the directed Degree-Corrected Mixed-Membership (directed-DCMM) model. For simplicity, we use the terminology of citation networks, but the model is valid for general directed networks. Consider a citation network with nodes. For two authors and , in the occurrence of citing , we say that is a citer and is a citee. Let be the adjacency matrix of the network, where

| (1.1) |

Conventionally, we do not count self citations, so all the diagonal entries of are . In directed-DCMM, we assume that there are perceivable communities , each of which can be thought as a research area (e.g., “Bayes”, “Variable Selection”). For each , we let and be two positive parameters that model the degree heterogeneity of node as a citer and as a citee, respectively. Also, we assume that node is associated with two -dimensional mixed-membership weight vectors and , where and are the weights that node puts in community as a citer and as a citee, respectively, . Moreover, for a nonnegative matrix which models the community structures, we assume that all off-diagonal entries of are independent Bernoulli variables satisfying

| (1.2) |

Let be the matrix such that . Write , , , , , and . With these notations, we can rewrite Model (1.2) as

| (1.3) |

where for short, is the diagonal matrix . Model (1.2) is the directed-DCMM model and (1.3) is its equivalent matrix form.

Next, we consider undirected networks. Similarly, let be the adjacency matrix of an undirected network, where if and there is an undirected edge between nodes and , and otherwise (similarly, all diagonal entries of are ). Undirected networks can be viewed as a special case of directed networks, where the matrix is required to be symmetric. Therefore, we can use the same modeling strategy, but we must have , , and . In this special case, directed-DCMM reduces to undirected-DCMM or DCMM for short, where we assume the upper triangular entries of are independent Bernoulli variables satisfying (note that are as above and is symmetric)

| (1.4) |

Definition 1.1.

For both directed-DCMM and DCMM, we need a mild identifiability condition; see Section 2. For analysis, we use as the driving asymptotic parameter, and allow to vary with and so to accommodate severe degree heterogeneity, mixed-memberships, flexible sparsity levels, and weak signals. See Section 2 for more discussions.

DCMM was proposed earlier (e.g., see Jin et al. (2023)). DCMM includes the Degree Corrected Block model (DCBM) (Karrer and Newman, 2011), Mixed-Membership Stochastic Block Model (MMSBM) (Airoldi et al., 2008), and Stochastic Block Model (SBM) (Holland et al., 1983) as special cases. In DCBM, we do not allow mixed-memberships so that all weight vectors are degenerate (i.e., only one nonzero entry, which is ). In MMSBM, we do not model degree heterogeneity, with . In SBM, we do not allow either mixed-memberships or degree heterogeneity. Directed-DCMM can also be viewed as an extension of directed-DCBM (Ji and Jin, 2016; Wang et al., 2020).

Now, consider two independent networks for the same set of nodes. Let and be the two adjacency matrices, and let and be the two Bernoulli probability matrices, respectively. Assume either that both and satisfy the DCMM model or that both and satisfy the directed-DCMM model. The problem of pairwise comparison is to test

| (1.5) |

Our primary interest is to find non-parametric pairwise comparison approaches that (1). work for a broad setting with only mild conditions where we allow severe degree heterogeneity, mixed-memberships, flexible sparsity levels, and weak signals, (2). have a tractable null distribution (so a testing -value can be easily computed) and are optimal in testing power, and (3). are directly implementable for both directed and undirected networks. We assess the optimality by phase transition. Phase transition is a well-known theoretical framework for assessing optimality (Donoho and Jin, 2015). It is closely related to the classical minimax framework, but may offer additional insight in many cases.

1.1 Literature review and our contributions

Spectral approach is an interesting approach to network pairwise comparison. Ghoshdastidar et al. (2020) studied a two-sample testing problem for inhomogeneous random graphs and proposed an interesting spectral approach. The paper considered a setting where we have two undirected random graph models, and , and for each model, we observe independently realized networks. The goal is to test whether or not. Translated to our setting (), their approach uses as the test statistic for pairwise comparison, where and are adjacency matrices of two independent networks. The main challenges of this approach are two fold. First, the null distribution of depends on unknown parameters in and and is hard to derive, even with the most recent techniques in Random Matrix Theory. Second, the test statistic aims to estimate (which is if and only if the null is true) but such an estimate is likely to be inconsistent in the presence of severe degree heterogeneity, where and may tend to rapidly (e.g., Bandeira and Van Handel (2016); Fan et al. (2022)). Here, , and denotes the -norm. Note also that the main focus of Ghoshdastidar et al. (2020) is on information lower bound. Therefore, their settings and primary focuses are quite different from ours.

Network comparison is related to the problem of two-sample latent space testing. Take the DCMM setting for example. Viewing the rows of the mixed-membership matrix as latent variables, the two-sample latent space testing is to test whether the mixed-membership matrices associated with two networks are the same. Among the recent works on two-sample latent space testing, Tang et al. (2017) considered the problem of testing whether two independent finite-dimensional random dot product graphs have the same generating latent positions (up to a rotation), and proposed an interesting eigen-space based approach. The approach was further adapted to a weighted SBM setting by Li and Li (2018), where the limiting null distribution of the testing statistic was derived by moment matching methods, assuming the numbers of communities is known. Despite the interesting results in this paper, the study was focused on the more specific SBM models of undirected networks. For the more general directed-DCMM and DCMM settings where we allow severe degree heterogeneity and mixed memberships, both the limiting null distribution and the power of the approach remain unknown. Note also the problem of two-sample latent space testing is different from our problem of two-sample network testing. For these reasons, it is unclear how to adapt their approach to our settings.

Two-sample network testing is also related to one-sample global testing. Given a network with communities, the goal of global testing is to test whether or . Seemingly, the problem is quite different from ours. Among existing works on one-sample global testing, Arias-Castro and Verzelen (2014) studied the problem of testing whether a graph is Erdös-Renyi or has an unusually dense subgraph, Bubeck et al. (2016) and Banerjee (2018) studied the problem for the more specific SBM setting where they proposed a signed-triangle approach. The approach was further extended by Jin et al. (2021) to the much broader DCMM settings. See also Yuan et al. (2022) for hypergraph global testing. Despite the interesting progress in these works, the problem of one-sample global testing is different from the problem of two-sample pairwise comparison considered here, so it remains unclear how to adapt those ideas to our settings.

Network comparison is also related to the change-point detection in dynamic networks (Wang et al., 2021; Liu et al., 2018; Jiang et al., 2023)), but the goal and settings of these papers are different from ours, and it is unclear how to extend their ideas to our setting.

It is a non-trivial task to find an optimal two-sample testing procedure that works for both DCMM and directed-DCMM models under only mild regularity conditions (where we allow severe degree heterogeneity, mixed memberships, flexible sparsity levels and weak signals). There are many challenges. To name a few: (1). For many test statistics, the limiting null distribution may depend on the (large number of) unknown parameters in a complicated way and is not tractable, (2). A test statistic may work well in some settings (e.g., networks that are very sparse or without severe degree heterogeneity) but lack power in others, (3). To find a test that achieves the optimal phase transition, we need to find an upper bound and a matching lower bound. This is non-trivial even for narrower settings.

In this paper, we propose Interlacing Balance Measure (IBM) as a new approach to pairwise comparison. Let and be the adjacency matrices of two independent networks (either both are directed or both are undirected) under consideration, and let . We recognize that the positive and negative entries in should be balanced in some sense when the null is true, and unbalanced otherwise. Therefore, an appropriately designed balance measure will have power for differentiating an alternative from a null.

We explain how IBM overcomes the challenges above. First, we design IBM in a way so that its mean is when the null is true and is strictly positive otherwise. Moreover, we find a convenient estimator for the variance of IBM, which is uniformly consistent for all directed-DCMM and DCMM settings considered here, with only mild regularity conditions. Using this estimator to standardize IBM and denoting the resultant testing statistic by , we show that for all directed-DCMM and DCMM settings considered here, , where for DCMM and for directed-DCMM. This way, we have derived an explicit limiting null and so have overcome the first challenge.

For the second challenge, we let and be the Bernoulli probability matrices of the two networks, respectively, and let , , and be the largest singular value of , , and , respectively. It turns out that the power of depends on , which can be viewed as the Signal-to-Noise Ratio (SNR) of . We show that for all directed-DCMM and DCMM settings (where only mild regularity conditions are imposed), in probability, as long as . Therefore, the test statistic has asymptotically full power in separating two hypotheses, for all parameters in the range of interest. This overcomes the second challenge.

For the third challenge, we show that the condition can not be substantially relaxed. In fact, for any network with Bernoulli probability matrix , we can pair it with another network with Bernoulli probability matrix so that the -divergence between two models converges to , once . This says that the proposed test achieves the optimal phase transition. This overcomes the third challenge aforementioned.

In summary, our contributions are as follows.

(1). Broadness. We propose IBM as a new test for network comparison that works for a broad setting where we allow severe degree heterogeneity, mixed memberships, flexible sparsity levels, and weak signals, with only mild regularity conditions required.

(2). Sharpness. We show the limiting null of the test statistic is and for the directed and undirected cases, respectively, and that the test statistic achieves the optimal phase transition, with an upper bound that matches the lower bound.

(3). Unified. For both directed and undirected networks, the same test works and attains the optimal phase transition.

As far as we know, our approach is new and has advantages in all three aspects above.

1.2 The IBM statistic for signed graphs

Consider two independent networks (directed or undirected) and let and be the adjacency matrices, respectively. Introduce

| (1.6) |

The entries of take values from and is the adjacency matrix of a signed graph (Harary, 1953), where each edge has a weight of either or . A cycle in a graph is a trail where the only repeated vertex is the first and the last vertices (e.g., a length- cycle is a triangle and a length- cycle is a quadrilateral). A cycle in the signed graph is called balanced if the product of the weights on all edges of the cycle is positive and unbalanced otherwise (Harary, 1953). Fixing , let , , and be the number of length- (unweighted) cycles, balanced cycles, and unbalanced cycles, respectively. It follows that and , where ‘dist’ stands for ‘distinct’. Balance checking is of primary interest for signed graphs. Intuitively, is small (in absolute value) when the null is true and is large otherwise, and so can be viewed as an (un-normalized) balance measure (Harary, 1953).

This motivates Interlacing Balance Measure (IBM) as a model-free statistic as follows. Fixing , define the order- IBM statistic by ( denotes the transpose of ):

| (1.7) |

When is symmetric, and reduces to the balance measure aforementioned. For non-symmetric , note that each term on the right hand side is a product of entries alternating between the two matrices and . For these reasons, we call the statistic the Interlacing Balance Measure (IBM).

To see why IBM is a reasonable idea, consider two independent directed-DCMM models where and for some matrices as in (1.4), and the rank of and are and , respectively. It follows that , where . Let be the -th largest singular value of . Note that the rank of is no more than . Since the entries of are independent zero-mean random variables, direct calculations show that under mild conditions,

| (1.8) |

The first claim holds, because in (1.7) we require that are distinct and that are distinct; the claim may not hold if such constraints are removed. By (1.8), has potential powers to differentiate the alternative from the null.

The statistic is defined for all . We may try to extend the statistic to the case of , but it won’t work well in this case; see Remark 2 below. In this paper, we focus on the IBM statistic with the lowest order (i.e., ). The study for higher-order IBM is similar but more tedious. When , the IBM statistic reduces to

| (1.9) |

Here, we have used the fact that when , is nonzero only when are distinct (this is not necessarily true when ).

To study the variance of , we define

| (1.10) |

We call them the Interlacing Cycle Count (ICC) statistics, because when and are symmetric, and are the respective numbers of length- cycles (quadrilaterals) in the two networks, and when and are asymmetric, and are the respective numbers of specifically oriented (interlacing) quadrilaterals in the two networks. In Section 2, we show that under mild conditions, if both networks are directed, and if both networks are undirected. This motivates the statistic . Consider the null case first. In Section 2, we show that under mild conditions,

| (1.11) |

The variances of two limiting nulls are different. This is because for any , and are two independent variables for directed networks, and for undirected networks.

Next, consider the alternative case. In Section 2, we show that under mild conditions,

| (1.12) |

Let be the -th singular value of , , and , respectively. Assuming is finite, we can further show that . Therefore, we expect to have if . This says that is able to differentiate the alternative from the null once .

Moreover, in Section 2.3, we study the minimax lower bounds. We show that the condition can not be significantly relaxed, and the test statistic achieves the optimal phase transition. Therefore, IBM not only has a tractable limiting null, but is also optimal in testing powers. See Section 2.3 for details.

We now discuss the computation cost of . For any matrices and , let be the Hadamard product of and (i.e., ), and let be the matrix where . Introduce . For a symmetric or asymmetric network, let be the average degree and let be the maximum degree. Recall that . The next lemma is proved in the supplement.

Lemma 1.1.

We have . Moreover, if we choose to store and in our code for , then the computation cost is . If instead of storing the whole matrices and , we only store the adjacency lists of and in our code, then the computation cost can be further reduced to .

The matrices and may be very sparse (i.e., most entries are ), so the overhead of computing and is large. Therefore, instead of storing the whole matrix and in our code, we can choose to only store the adjacency lists (i.e., nonzero entries) of and (when is stored in the form of adjacency list, the cost of finding the neighbors of any node is per neighbor), and the resultant computational cost is further reduced.

Remark 1. The statistic may look similar to the statistic of , but it is quite different. Consider the case where is symmetric for example. In this case, , where unlike as in (1.7), the indices are not required to be distinct. Therefore, unlike , depends on many unknown parameters and is nonzero, so it is unclear how to normalize it to have a tractable limiting null. Also, the variance of is much larger than that of , and the statistic is also less efficient in power.

Remark 2. The statistic is defined for all . If we try to extend it to the case of , then reduces to the statistic of . In this case, the statistic has a nonzero mean under the null, so it is unclear how to standardize it to have a tractable limiting null. Also, the Signal-to-Noise Ratio (SNR) of the statistic turns out to be much smaller than those in the cases of , so the statistic is less efficient in power.

Remark 3. Our idea is extendable to . Take for example (see Section E of the supplementary material). In this case, we may change the test statistic to , where and ( is similar). Equivalently, if we let , then . With such a formula, the computational costs for is the same as that of . The limiting null and power analysis of are similar to that of , but technically much more involved. For a finite , is slower in convergence to the limiting null and in computation (e.g., times slower when ), but may have a better power in some cases (it is unclear whether we can have uniform power improvement).

Remark 4. In the one-sample undirected network setting, researchers (e.g., Bubeck et al. (2016); Banerjee (2018); Jin et al. (2021) used cycle count approaches to test whether or (: number of communities). To extend their ideas to our setting, we face challenges. For example, in the undirected network case, we may compute the cycle count statistics and for two networks (similarly as in previous works) and use as the test statistic. Unfortunately, this test loses power in many cases. In face, since and , the test loses power when , but this can be an easy-to-test case as we may have . In the directed networks case, there are multiple ways to define a cycle as the edges have directions, and it is unclear which cycle count approach may give rise to optimal tests.

Remark 5. An alternative test is , where denotes the largest singular value. For simplicity, consider the DCMM case where are symmetrical. When the null is true, we can show (e.g., Jin (2015)) with high probability. For cases where , , so we may use if you are satisfied with something crude. However, in the presence of severe degree heterogeneity, may grow to rapidly as diverge, and the test is far from optimal (note also that the limiting null of is not explicit and may depend on unknown parameters). In this paper, and .

1.3 Content

2 Main results

We start by discussing the identifiability for the two models, directed-DCMM and DCMM. We then present the optimality of IBM under the DCMM model for undirected networks, where we analyze the limiting null and the power of IBM in Section 2.2, and present our results on minimax lower bound and phase transition in Section 2.3. The optimality of IBM under the directed-DCMM models for directed networks is in Section 2.4.

2.1 The identifiability for directed-DCMM and DCMM models

Consider a directed-DCMM model (1.1)-(1.3) with communities, where and are the membership vectors of node as a citer and a citee, respectively. Fix and . We call node a pure node of community as a citer (or as a citee) if (or ) is a degenerate weight vector (i.e., one entry is , others are ). We call a non-negative matrix double stochastic if the sum of each row and each column is . Lemma 2.1 discusses identifiability of directed-DCMM and is proved in the supplement

Lemma 2.1.

For any as in Model (1.1)-(1.3) where is fully indecomposable, 111We call fully indecomposable if we do not have permutation matrices such that is a block matrix where the upper right block is . we can always re-parametrize the model so that is doubly stochastic and . Conversely, if where is non-singular, fully indecomposable and doubly stochastic, , and each community has at least one node which is pure both as a citer and as a citee, then are uniquely determined by

For DCMM, Lemma 2.1 still applies, as DCMM is a special directed-DCMM, but existing works have suggested other choices of identifiability conditions. See Lemma 2.2 for example, which is proved in Jin et al. (2023).

Lemma 2.2.

In model (1.4), if is non-singular, irreducible, and has unit diagonal entries, and if each community has at least one pure node, then the model is identifiable.

To be consistent with literature works, we choose to use the conditions of Lemma 2.2 for DCMM models. Note that two sets of conditions are the same except that one requires to be doubly stochastic and the other requires to have unit diagonal entries.

2.2 The limiting null and power of IBM for DCMM models

Consider two independent undirected networks on the same set of nodes and both satisfy the DCMM model (1.4). Let and be the adjacency matrices of two networks, and be the Bernoulli probability matrices, and and be the numbers of communities, respectively. Recall that and , where and ; similar for . We assume three mild conditions as follows.

| (2.13) |

The last two conditions are necessary. The first condition is mainly for simplicity and can be relaxed. In fact, the IBM test statistic decomposes into the sum of several terms, so the total variance is the sum of many variance terms. With such a condition, one of these terms dominates in variance, so the total variance equals approximately to the variance of this particular term and has a succinct form. Without such a condition, a succinct form is hard to obtain. Same discussion for (2.23) below. We also assume

| (2.14) |

Here, as the matrices and are properly scaled, the first two are only mild conditions on the community balance. The last one is also a mild condition.

Consider the null hypothesis first. Recall that for undirected networks, the test statistic is . Under the null, , and and have the same distribution. The following lemma is proved in the supplement.

Theorem 2.1.

Theorem 2.1 shows that the limiting null of is . In practice, once we obtain the testing score for a pair of networks, we can use to approximate the -value; see our real-data analysis in Section 3. Now, fix and let be the -quantile of . Consider the IBM test where we

| (2.15) |

As , by Theorem 2.1, the Type I error of the test converges to as expected.

We now analyze the power. As before, let , and let , , and be the -th largest (in magnitude) eigenvalue of , , and , respectively. Since and are non-negative matrices, by Perron’s theorem (Horn and Johnson, 1985), and . The following theorem is proved in the supplement.

Theorem 2.2.

(Power analysis (DCMM)). Consider the pairwise comparison problem (1.5) where both networks satisfy the DCMM model (1.4) where conditions (2.13)-(2.14) hold. Assume that as and that and are fixed. Then, (1). , and , and (2). , in probability. Therefore, for any fixed , the power of the IBM test defined in (2.15) goes to as .

Remark 6. By Theorems 2.1-2.2, if we let the level of the IBM test in (2.15) depend on (i.e., ) and let tend to sufficiently slow, then the Type I error of the test , and the power of the test , so the sum of Type I and Type II errors .

Remark 7. The main condition of Theorem 2.2 is . If we relax it to for some constant , then the power of the IBM test converges to a number in . If we further relax it to , then we are in the impossibility region, where we can find many pairs of DCMM models that are asymptotically inseparable (so the sum of Type I and Type II errors of any test is ). See Section 2.3 for details, where we discuss the minimax lower bound and phase transition.

The main condition of Theorem 2.2 is . The condition has a simple form but is not completely obvious, so it is worthy to explain such a condition, especially the connection between the term and Signal-to-Noise Ratio of the IBM test statistic . The Signal-to-Noise ratio of is , but we do not have an explicit formula for it. We introduce a proxy by

| (2.16) |

We have the more challenging weak signal case and less challenging strong signal case:

| (2.17) |

Consider the weak signal case (Case 1) first. In this case, By Theorem 2.2, and . Therefore, , so the definition of SNR in (2.16) is reasonable. Recall that , where and . Let ; note that . It is seen that . By Condition (2.13), , and , and we can show that , . This says that once we assume as in Theorem 2.2. Combining these with elementary calculations, it follows that if is bounded, then

| (2.18) |

Therefore, in the weak signal case, , and the main condition of in Theorem 2.2 is the same as the condition of . This explains why the test has asymptotically full power.

We now discuss the strong signal case (Case 2). In this case, the variance of the IBM test statistic may be larger than that of the weak signal case (which is ), but the mean of is also much larger that that of the weak signal case. As a result, this is a less challenging case for pairwise comparison. In fact, by similar arguments, . Therefore, by the condition of , we have . Note that . Therefore, as long as , the IBM test statistic also has asymptotically full power in this case.

Remark 8. Our idea is readily extendable to the case where we have multiple independent samples for each of the models. Consider the DCMM case for simplicity, where and are the average of and independent adjacency matrix from two DCMM models where the Bernoulli probability matrices are , and , respectively. In this setting, we can similarly write and , where the only difference is, and are matrices of (scaled) centered Binomial instead of centered Bernoulli. In this setting, we expect to have similar results as in Section 2.1, where the SNR is at the order of , while that for our setting is . The optimality of the test statistic also implies the optimal sample complexity.

2.3 The minimax lower bound for DCMM

The key in the lower bound analysis is to find the least favorable configuration. A standard approach is to use randomization: fixing a Bernoulli probability matrix for a DCMM model with communities, we construct another Bernoulli probability matrix using and randomization. In detail, let be iid Radermacher variables. We construct a randomized Bernoulli probability matrix as follows. Recall that . We construct a new community and randomly move part of the weights of community to this new community. In detail, introduce a matrix where for , if , if , and if . For a small positive number ,

Introduce two diagonal matrices and where , for . Let , , and . Our construction for is

| (2.19) |

Let be all Bernoulli probability matrices for DCMM models with communities where as in (1.4) and the conditions of Lemma 2.2 hold. Given a positive sequence and , , define a class of DCMM models by

where is the maximum element of . The following is proved in the supplement.

Theorem 2.3.

(Least favorable configuration for DCMM). Fix , and a positive sequence such that . Given any sequence with , let denote the vector of degree parameters. We construct a sequence as in (2.19), where satisfies that .

-

•

With probability , , and , where are the first eigenvalue of , and , respectively.

-

•

Consider a null case and an alternative case as follows. For the null case, we generate two network adjacency matrices and independently with the same probability matrix . For the alternative case, we generate in the same way but generate from the random-membership DCMM associated with as in (2.19), independently of . As , the -distance between these two models tends to .

Once we have the least favorable configuration, we can obtain a minimax lower bound. Similar as before, let , be the ranks of , and , respectively, and , , and be the -th largest eigenvalue (in magnitude) of , , and , respectively. Recall that . When is finite, it holds that . Define the class of DCMM model pairs for the null by

| (2.20) |

and define a class of DCMM model pairs for the alternative case by

| (2.21) |

Within this class, we can find model pairs where , which are asymptotically inseparable as in Theorem 2.3. The following theorem is proved in the supplement.

Theorem 2.4.

(Minimax lower bound for DCMM). For any given , , and positive sequences and such that and , we have

| (2.22) |

as , where the infimum is taken over all possible tests .

Combining Theorems 2.1-2.4, we have the following phase transition. Consider a sequence of DCMM model pairs indexed by , where for each pair, and are the Bernoulli probability matrices, respectively. Consider the pairwise comparison problem where we test versus . Recall that and , , are the largest eigenvalues (in magnitude) of , respectively.

Possibility. When , the two models are asymptotically separable, and the sum of Type I and Type II errors of the IBM test .

Impossibility. When , two models are not always asymptotically separable. In fact, for each , we can pair it with an such that and the -divergence between the two models . Therefore, for any test, the sum of Type I and Type II errors is (see also Remark 7).

2.4 Optimality of the IBM test for directed-DCMM

We study the IBM test for directed networks. IBM uses the same test statistic for undirected and directed networks, but the analysis of directed networks is quite different from that of undirected networks. In Theorems 2.5-2.7 below, we study the limiting null, power, and optimality of IBM in the directed-DCMM setting.

Consider two independent directed networks on the same set of nodes that satisfy the directed-DCMM model (1.1)-(1.3). Let and be the two adjacency matrices, let and be the two Bernoulli probability matrices, and let and be the two numbers of communities, respectively. Recall that and , where , , , and ; similar for . We assume the identifiability conditions of Lemma 2.1 hold, so and . We impose the following regularity conditions :

| (2.23) |

| (2.24) |

| (2.25) |

These conditions are mild: they are similar to (2.13)-(2.14) in Section 2.2, but are slightly more complicated as the directed-DCMM has more parameters than DCMM. The condition is not needed in the undirected-DCMM, because the identifiability condition in Lemma 2.2 already yields for (similar for ).

Consider the limiting null distribution first. Recall that the IBM test statistic is . Under the null, , and so by our identifiability conditions. Especially, and have the same distribution.

Theorem 2.5.

(Null behavior (directed-DCMM)). Consider the pairwise comparison problem where both networks satisfy the directed-DCMM model (1.1)-(1.3). Suppose Conditions (2.23)-(2.24) and the identifiability conditions of Lemma 2.1 hold. As , under , we have (1). , and , (2). , , and in probability, and (3). in law.

Theorem 2.5 is proved in the supplement. Compared with Theorem 2.1, (and so ) for the directed case here, and for the undirected case there. This is because the variances of in two cases are different by a factor of . As before, fix and let be the -quantile of . Consider the IBM test where we reject the null if and only if . As , by Theorem 2.1, the Type I error of the IBM test as expected.

We now analyze the power. Similarly, let and . It is seen that . Since , , and are asymmetric, the eigenvalues are not necessarily real, so it is more convenient to consider the singular values. To abuse the notation a little bit, let , , and , be the -th singular value of , and , respectively. The following theorem is proved in the supplement.

Theorem 2.6.

(Power analysis for directed-DCMM). Consider pairwise comparison problem where both networks satisfy the directed-DCMM model (1.1)-(1.3), where conditions (2.23)-(2.24) and the identifiability conditions in Lemma 2.1 hold. Assume as and for fixed and , we have (1). and , and (2). , in probability. Therefore, for any fixed and the IBM test where we reject the null if and only if , the power of the test goes to .

Similarly, the main condition of Theorem 2.6 is . To interpret, define

| (2.26) |

We have two cases, the weak signal case where and the strong signal case where . By similar arguments, we have (a) in the weak signal case, , and the main condition of in Theorem 2.6 is equivalent to that of , and (b) in the strong signal case, as long as .

We now study the lower bound. Similarly, the goal is to show that within the class of all model pairs satisfying , there exist pairs where the two models within the pair are asymptotically inseparable (i.e., the -divergence ). In detail, let be all Bernoulli matrices for directed-DCMM models with communities where and (1.1)-(1.3) hold. Given a positive sequence , an integer , and constants , we define a class of directed-DCMM models by

where for short, . Similar as before, let , let be the rank of , and , respectively, and let , , and be the -th largest singular value of , , and , respectively. Define the class of directed-DCMM model pairs for the null case by

and define a class of diercted-DCMM model pairs for the alternative case by

The following theorem is proved in the supplement.

Theorem 2.7.

(Minimax lower bound (directed-DCMM)). Fix , , and positive sequences and such that and , we have

| (2.27) |

as , where the infimum is taken over all possible tests .

Combining Theorems 2.5-2.7, we have the following phase transition. Consider a sequence of directed-DCMM model pairs indexed by , where for each pair, and are the Bernoulli probability matrices, respectively. Recall that and . In the pairwise comparison problem, we test versus . We have the following phase transition.

Possibility. When , the two models are asymptotically separable, and the sum of Type I and Type II errors of the IBM test .

Impossibility. When , the two models are not always asymptotically separable. In fact, for each , we can pair it with an such that , and the -divergence between the two models . Therefore, for any tests, the sum of Type I and Type II errors is (see also Remark 7).

Our ideas are not tied to the DCMM or directed-DCMM models, and are extendable to general Bernoulli probability model , where . In fact, by SVD, we may write and , where and are positive diagonal matrices, are matrices where each row has unit- norm, and , consisting nonzero singular values of ; similar for . Our theorems are readily extendable if we translate the regularity conditions on and above to similar conditions on and .

3 Real-data applications

We use IBM to analyze the Enron email network and a gene co-expression network.

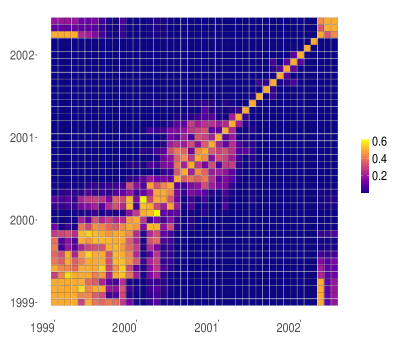

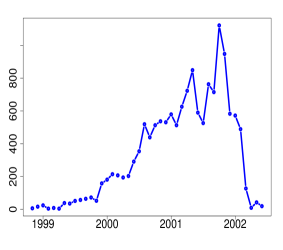

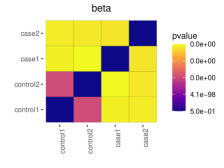

Analysis of the Enron email data. The dataset contains the email communication data of users in a total of months (November 1999 to June 2002), and provides valuable information for studying the Enron scandal. For each month during the time period, we construct an undirected and unweighted network, where nodes and are connected if and only if they had email communication during that month. This gives us a total of networks for the same of nodes, with the number of edges varying from to (see Figure 1 (right panel)). For any and , we conduct a network comparison and derive an IBM test statistic . By Theorem 2.1, the -value of the statistic is approximately . The -values are presented in Figure 1 (left panel) as a heatmap. Note that a darker cell means a smaller -value, suggesting that the difference between the two networks being compared is more significant.

The heatmap suggests that there are two major “change points”, corresponding to August of 2000 and August of 2001 (note that each time point is a month), respectively. At the first change point, what happened is that the Enron stock hit all-time high of per share with a market valuation of billion dollars, indicating an increasing popularity of the company. Note that the right panel of Figure 1 also suggests a significant increase of email numbers in that month, confirming the sudden change of the email network structure. At the second change point of August of 2001, what happened is that former CEO Jeffrey Skilling resigned on August 14th and Kenneth Lay took over. After that, the scandal was gradually discovered by the public. This explains why the network structures after August 2001 are so different from each other. Moreover, on the right panel of Figure 1, we also find drastic changes around that time point, on the number of email changes.

From the heatmap, we also observe that the monthly email network are very different since late 2001, and the underlying reason is that Enron was undergoing many significant changes. For example, in November of 2001, Enron restated the 3rd quarter earnings and the dynegy deal collapsed. In January of 2002, criminal investigation started and Kenneth Lay resigned (and was implicated in fraud later in February). For finer details of the heatmap, see Section F of the supplementary material.

Analysis of the gene co-expression network. We aim to identify subtle disparity between the gene co-expression networks from healthy and type 2 diabetic donors (T2D) based on transcriptome of thousands of islet cells. Hormone-secreting cells within pancreatic islets of Langerhans play important roles in metabolic homeostasis and disease. We leverage the transcriptome of 2,209 cells from six healthy and four T2D donors profiled using Smart-seq2 protocol in study (Segerstolpe, 2016). The cells were broadly categorized based on the transcription profiles into six major types, including exocrine ductal and acinar cells, and endocrine and cells (cell types with less than 100 cells are not detailed here), as summarized in Table 1.

| cell type | acinar | ductal | other | total | ||||

| # Normal (control) | 171 | 443 | 75 | 59 | 112 | 135 | 102 | 1097 |

| # Type 2 diabetic (case) | 99 | 443 | 122 | 55 | 73 | 251 | 69 | 1112 |

| # total | 279 | 886 | 197 | 114 | 185 | 386 | 171 | 2209 |

The transcriptome heterogeneity for healthy (controls) and T2D (cases) individuals is examined by comparing gene co-expression networks in a cell type resolved manner. To construct the gene co-expression network, the raw counts from single-cell RNAseq data are first normalized and log transformed. A total of 25525 gene expressions were detected. We restrict our analysis to 500 most highly expressed genes selected using “vst” method provided by “Seurat” toolbox (Stuart, 2019), as a convention in Single Cell literature. Then Spearman correlations between each pair of highly variable genes are calculated separately for healthy and T2D cells and for each cell type. The absolute value of correlation is hard-thresholded at quantile to generate a binary adjacency matrix (the thresholding is used to ensure the difference in average degree does not contribute to the testing significance). Also, thresholding at the quantile is equivalent to thresholding the Pearson correlations (in magnitude) at a threshold between to across six different cell types, which is common in practice. We view the binary matrix as the adjacency matrix of the gene co-expression network.

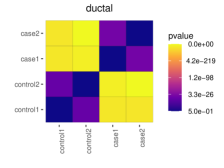

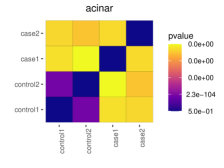

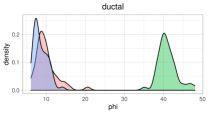

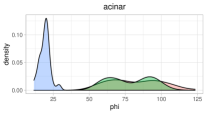

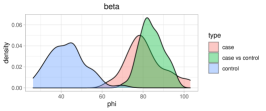

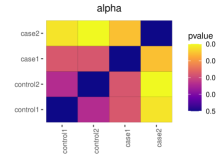

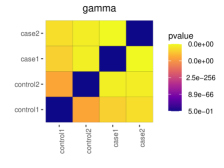

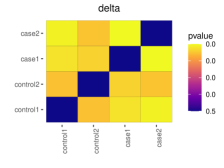

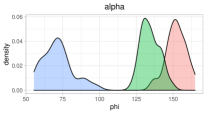

To compare the healthy versus T2D network disparity with the within-healthy or within T2D network disparity, the cells are randomly split into halves for each of cases and controls. For each random split, we construct networks as above, denoted by Case1, Case2, Control1, and Control2. For each pair of networks, we apply the IBM statistic and obtain a -values similarly as above. The process is repeated for times and the medians of -values are visualized in Figure 2. The density plot for IBM test scores are also provided.

Among the results from six cell types, ductal cells demonstrate the most remarkable distinction of gene co-expression networks between cases and controls, which results in -values in off-diagonal block orders of magnitude smaller than -values in two diagonal blocks (Figure 2). This is indicative of significant alterations in gene expression in cell from T2D subjects compared to healthy subjects. Acinar, and cells uncover similar patterns of prominent distinction between cases and controls, in addition, the two networks built from a random split of cases also express comparable disparity. For and the disease-dependent effect is less evident regarding network structure. To be more specific, the number of differentially expressed (DE) genes between the cells from T2D objects (case) and health objects (control) is 250 for ductal, 50-100 for acinar, and , and less than 10 for and . The density plots align with the biological observations that ductal cells have the highest number of differentially expressed genes, where the test statistic for case versus control test is much larger than that for the control versus control or case versus case test. Followed by acinar, and cells where the case vs control test statistic values are greater than control vs control, but not significantly higher than case vs case. For and cells, there is no evident difference between the case versus control or control versus control.

The results are consistent with the evidence revealed in previous study (Segerstolpe, 2016) that ductal cells entail the most different differentially expressed (DE) genes between cells from health and T2D donors (250 genes), followed by acinar, and cells (50-100 DE genes each), while for and cell less than 10 DE genes are identified. Results also confirm that comparing healthy and T2D gene co-expression networks in a cell-type manner uncovers the cell-level heterogeneity associated with the disease and shed light on future functional studies.

In conclusion, the IBM test statistic performs well in both data sets. It is useful for identifying change points of dynamic networks, for identifying network pairs with significant differences, and for visualizing how a large number of networks are different from each other.

4 Simulations

We investigate undirected networks and directed networks in Experiment 1 and Experiment 2, respectively, We also compare IBM with spectral methods in Experiment 3.

Experiment 1: Undirected networks. Given , we first generate , for , where and controls the -norm of . We then generate , for , where dir is the Dirichlet distribution. Let and and . We construct . We then generate . There can be multiple sources of differences between and , e.g., different degree parameters, different number of communities, or different mixed memberships. We investigate the three cases separately.

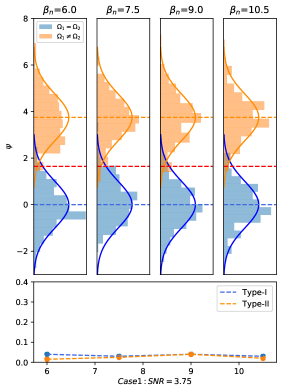

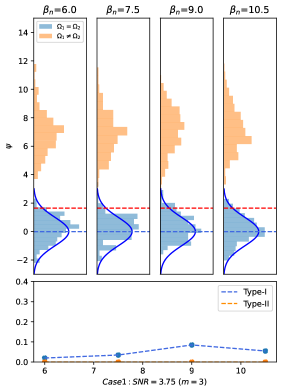

Case 1: Different degree parameters. We let , where are the same as those in and ’s are generated as follows: , for , where with representing a point mass at . We fix and let range from 6 to 10.5 with a step size 1.5. As increases, the network becomes less sparse. For each value of , we select (the off-diagonal elements of ) such that the SNR defined in (2.16) is fixed at .

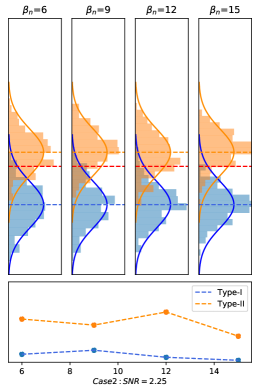

Case 2: Different numbers of communities. We construct and such that the two networks have and communities, respectively. Let and . We generate samples of from , for , and construct by , for , . Let be generated in the same way as before (see the paragraph above Case 1). Let and . In this construction, each community in is split into two communities in . Fix . We let range from 6 to 15 with a step size 3. For each , is chosen such that the SNR in (2.16) is equal to 2.25.

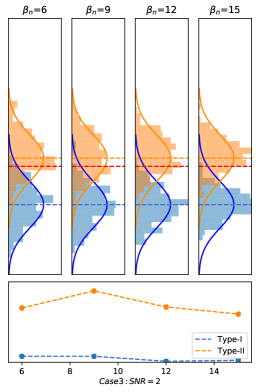

Case 3: Different mixed membership vectors. Fix . We generate in the same way as in Case 1. We then generate and , . Let and . Let range from 6 to 15 with a step size 3, where for each value of we select such that the SNR is equal to 2.

For each parameter setting, we first generate and then generate 400 independent networks, , from and 200 independent networks, , from . We use them to construct 200 instances of the null hypothesis, , and apply the level-95% IBM test to each instance. We also construct 200 instances of the alternative hypothesis, . The results are presented in Figure 3.

For a wide range of (e.g., ), the histogram of the test statistic (in blue) fits well with under the null, and the type-I error is (for in Case 3, the fitting is less well; in this setting, the null standard deviation of the test statistic is smaller than 1, which means that our test is conservative, and so the type-I error is still under control). Under the alternative, the histogram of the test statistic (in orange) converges to a normal distribution centered at the SNR (see (2.16)), and the type-II error is small as long as the SNR is properly large. From Case 1 to Case 3, we have decreased the SNR purposely so that it is increasingly more difficult to separate two hypotheses. The type-II error is also increasing. These observations validate our theory in Section 2.

Experiment 2: Directed networks. Similarly, we consider different cases of :

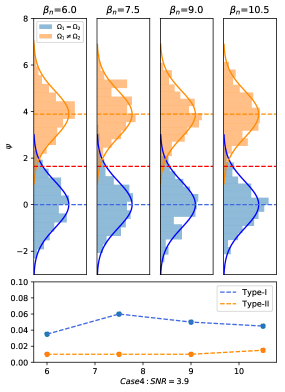

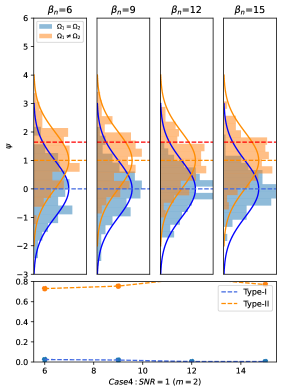

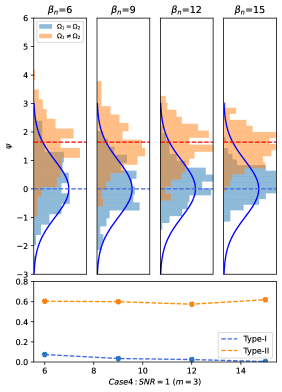

Case 4: Different degree parameters. Let and , where , , and are as follows: We draw and , and let , , , and . Fix and let range from 6 to 10.5 with a step size 1.5. For each , choose so that the SNR in (2.26) is fixed at .

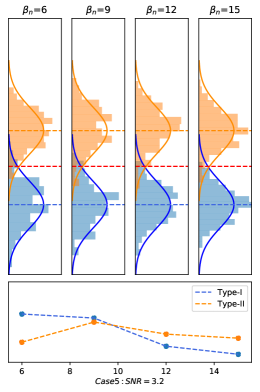

Case 5: Different numbers of communities. This setting is similar to that of Case 2, where we construct and such that the two networks have and communities, respectively. Let and . Here, and are generated in the same way as in Case 4, , and . Generate and let and , for and . Here, each (incoming or outgoing) community in is split into two in . We fix , let range from 6 to 15 with a step size 3, and choose so that the SNR is fixed at .

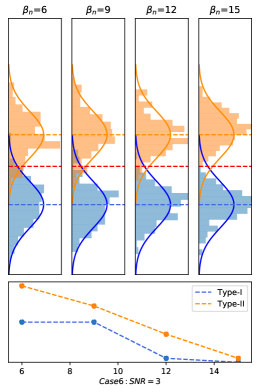

Case 6: Different membership vectors. Fix . Let be the same as in Case 4. Generate and then generate . Let and . Let range from 6 to 15 with a step size 3. Choose accordingly so the SNR in (2.26) is .

For each parameter setting, once and are generated, we then construct 200 pairs of networks under the null hypothesis and 200 pairs under the alternative hypothesis, similarly as in Experiment 1. The results are in Figure 4. Similar to the case of undirected networks, the behaviors of the test statistic both under the null and under the alternative are consistent with our theory. The type-I error is controlled under in all settings, and the type-II error is reasonably small. When is large (e.g., in Case 5 and Case 6), the variance of the IBM test statistic gets smaller than 1, under both the null and the alternative; therefore, although our test statistic tends to be conservative, the type-I and type-II errors are even smaller.

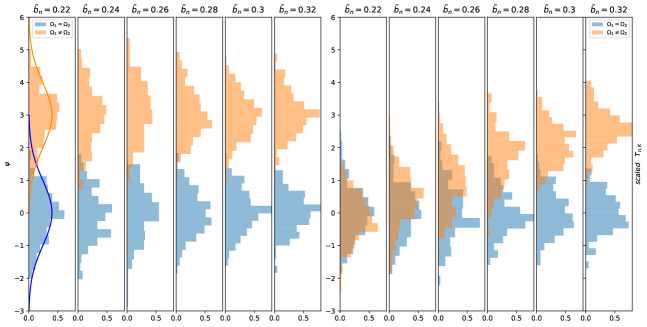

Experiment 3: Comparison with the spectral approach. We compare IBM with the test in Li and Li (2018). Their test statistic explores the difference between the principal eigen-space of two networks and is defined to be , where and contain the first eigenvectors of and , respectively, is a diagonal matrix whose diagonal elements are the largest eigenvalues (in magnitude) of , and is an orthogonal matrix that minimizes . They estimated the null distribution of by assuming that both networks follow an undirected SBM, but this estimate is not valid in our setting, as we consider the more general DCMM. Instead, we use the true mean and standard deviation of under the null hypothesis (obtained from simulating data sets from the true null model) to standardize it. The resulting test statistic is not practically feasible, but it is still interesting to see its comparison with the IBM test.

Fix . We generate and let , . Let and . Let for and for ; let for and for . We then construct and . The signal to noise ratio of the IBM test is governed by , where controls network sparsity, and control the difference between two community structure matrices. Fixing , we let range from 0.22 to 0.32, and choose coordinately to make the SNR in (2.16) fixed at 3. For each parameter setting, after is generated, we simulate 200 network pairs under the null hypothesis and 200 pairs under the alternative hypothesis. We compare the histogram of the IBM statistic with that of the (ideally standardized) . The results are in Figure 5.

We note that was designed to test . In this experiment, both the difference between and and the difference between and contribute signals. The IBM statistic captures both sources of signals and thus have higher power. In contrast, only captures the signals in . When is small, the networks are very sparse (recall that we fix the SNR; hence, a smaller yields a smaller ). It turns out that the signals in alone are too weak to separate two hypotheses. As increases, the networks get less sparse, and the power of also increases and gets close to that of IBM. Note also the IBM has an explicit limiting null, but the limiting null of is unclear under the general DCMM.

5 Discussion

Motivated by applications in social science, genetics and neurosicence, we consider the problem of testing whether the Bernoulli probability matrices of two networks are the same or not. We propose the Interlacing Balance Measure (IBM) as a new family of test statistics. IBM has several noteworthy advantages: It works for a broad class of DCMM and directed-DCMM settings allowing for different sparsity levels, severe degree heterogeneity, and mixed memberships. It has a tractable null distribution, though the models we consider have a large number of unknown parameters. The explicit limiting null allows us to approximate the -values of the test statistics. IBM is also powerful in separating the null from the alternative, and attains the optimal phase transitions. It is also a unified procedure: the same test statistic can be used for both directed and undirected networks, without modifications. We provide sharp theoretical analysis on the limiting null, power, and optimality of the test. We also apply the IBM test to analyze the Enron email network and a gene co-expression network, with interesting discoveries.

We focus on the DCMM model in this paper, but the method and theory are applicable to other network models where and have low ranks. In fact, as in Section 2.2, the SNR of the IBM statistic is , which does not depend on the particular form of DCMM. The estimate of the null variance of does not depend on the particular form of DCMM either. Therefore, results about the limiting null and the power of the IBM test are readily extendable to general low-rank network models. Also, for convenience, we assume and are finite in this paper. For the case where and diverge to , the above formula for SNR is still valid, and our results continue to be true with some mild regularity conditions (e.g., ).

The IBM test can be extended in multiple directions. Suppose we are given and independent networks drawn from and , respectively. To detect the difference between and , a similar IBM statistic can be defined based on , where and are the average of adjacency matrices of the and graphs, respectively. We expect that this test will inherit the nice properties of the IBM test and that the phase transitions will also depend on . This idea can be further extended to solve the change point detection problem in dynamic network analysis (Wang et al., 2021). In a standard binary segmentation procedure for identifying the change point, it requires to have a statistic that detects the difference between the Bernoulli probability matrices for two nested time blocks and . We may construct an IBM-type test statistic from , where is a weighted average of the adjacency matrices in time block . The fact that the IBM-type statistics have tractable null distributions will help us design a tuning-free procedure for change-point detection. It is also interesting to study the optimality of this procedure when all the networks in the series are generated from the DCMM model.

The idea of IBM may also be adapted to the problem of comparing two large covariance matrices of Gaussian ensembles (Cai et al., 2013; Zhu et al., 2017). We note that is an estimate of . This estimate is better than by removing from the sum those terms with nonzero means. The same idea is also potentially useful for detecting the difference between two covariance matrices. We leave it to future exploration.

While we focus on testing in this paper, a related question is how to identify the subset of nodes that are most different between two networks. This is similar to the problem of variable selection, and we can approach it by creating node-wise features. For example, fixing a node, we can count the node degree and the numbers of -cycles containing the node, and each of these is a node-wise feature. We can then select the subset of nodes that are most different between two networks using ideas from the variable selection literature.

References

- Airoldi et al. (2008) Airoldi, E., D. Blei, S. Fienberg, and E. Xing (2008). Mixed membership stochastic blockmodels. J. Mach. Learn. Res. 9, 1981–2014.

- Arias-Castro and Verzelen (2014) Arias-Castro, E. and N. Verzelen (2014). Community detection in dense networks. Ann. Statist. 42(3), 940–969.

- Bandeira and Van Handel (2016) Bandeira, A. S. and R. Van Handel (2016). Sharp nonasymptotic bounds on the norm of random matrices with independent entries. Ann. Probab. 44(4), 2479–2506.

- Banerjee (2018) Banerjee, D. (2018). Contiguity and non-reconstruction results for planted partition models: the dense case. Electron. J. Probab 23(18), 1–28.

- Bubeck et al. (2016) Bubeck, S., J. Ding, R. Eldan, and M. Z. Rácz (2016). Testing for high-dimensional geometry in random graphs. Random Struct. Algor. 49(3), 503–532.

- Cai et al. (2013) Cai, T., W. Liu, and Y. Xia (2013). Two-sample covariance matrix testing and support recovery in high-dimensional and sparse settings. J. Amer. Statist. Assoc. 108(501), 265–277.

- Donoho and Jin (2015) Donoho, D. and J. Jin (2015). Higher criticism for large-scale inference: especially for rare and weak effects. Statist. Sci. 30(1), 1–25.

- Fan et al. (2022) Fan, J., Y. Fan, X. Han, and J. Lv (2022). Asymptotic theory of eigenvectors for random matrices with diverging spikes. J. Amer. Statist. Assoc. 117(538), 996–1009.

- Foucart and Rauhut (2013) Foucart, S. and H. Rauhut (2013). A Mathematical Introduction to Compressive Sensing. Birkhäuser Basel.

- Ghoshdastidar et al. (2020) Ghoshdastidar, D., M. Gutzeit, A. Carpentier, and U. v. Luxburg (2020). Two-sample hypothesis testing for inhomogeneous random graphs. Ann. Statist. 48(4), 2208–2229.

- Girvan and Newman (2002) Girvan, M. and M. Newman (2002). Community structure in social and biological networks. Proc. Natl. Acad. Sci. 99(12), 7821–7826.

- Hall and Heyde (2014) Hall, P. and C. C. Heyde (2014). Martingale limit theory and its application. Academic press.

- Harary (1953) Harary, F. (1953). On the notion of balance of a signed graph. Michigan Math. J. 2(2), 143–146.

- Holland et al. (1983) Holland, P. W., K. B. Laskey, and S. Leinhardt (1983). Stochastic blockmodels: First steps. Social networks 5(2), 109–137.

- Horn and Johnson (1985) Horn, R. and C. Johnson (1985). Matrix Analysis. Cambridge University Press.

- Ji and Jin (2016) Ji, P. and J. Jin (2016). Coauthorship and citation networks for statisticians. Ann. Appl. Statist. 10(4), 1779–1812.

- Jiang et al. (2023) Jiang, B., J. Li, and Q. Yao (2023). Autoregressive networks. J. Mach. Learn. Res. 24(227), 1–69.

- Jin (2015) Jin, J. (2015). Fast community detection by SCORE. Ann. Statist. 43(1), 57–89.

- Jin et al. (2021) Jin, J., Z. T. Ke, and S. Luo (2021). Optimal adaptivity of signed-polygon statistics for network testing. Ann. Statist. 49(6), 3408–3433.

- Jin et al. (2023) Jin, J., Z. T. Ke, and S. Luo (2023). Mixed membership estimation for social networks. Journal of Econometrics 239(2), 105369.

- Johnson and Reams (2009) Johnson, C. and R. Reams (2009). Scaling of symmetric matrices by positive diagonal congruence. Linear Multilinear A 57, 123–140.

- Karrer and Newman (2011) Karrer, B. and M. Newman (2011). Stochastic blockmodels and community structure in networks. Phys. Rev. E 83(1), 016107.

- Lee (2019) Lee, A. J. (2019). U-statistics: Theory and Practice. Routledge.

- Li and Li (2018) Li, Y. and H. Li (2018). Two-sample test of community memberships of weighted stochastic block models. arXiv:1811.12593.

- Liu et al. (2018) Liu, F., D. Choi, L. Xie, and K. Roeder (2018). Global spectral clustering in dynamic networks. Proc. Nat. Acad. Sci. 115(5), 927–932.

- Segerstolpe (2016) Segerstolpe, Åsa, et al. (2016). Single-cell transcriptome profiling of human pancreatic islets in health and type 2 diabetes. Cell metabolism 24(4), 593–607.

- Sinkhorn and Knopp (1967) Sinkhorn, R. and P. Knopp (1967). Concerning nonnegative matrices and doubly stochastic matrices. Pacific Journal of Mathematics 21(2), 343–348.

- Stuart (2019) Stuart, T. et al. (2019). Comprehensive integration of single-cell data. Cell 177(7), 1888–+.

- Tang et al. (2017) Tang, M., A. Athreya, D. L. Sussman, V. Lyzinski, and C. E. Priebe (2017, 08). A nonparametric two-sample hypothesis testing problem for random graphs. Bernoulli 23(3), 1599–1630.

- Tang (2017) Tang, M. et al. (2017). A semiparametric two-sample hypothesis testing problem for random graphs. J. Comput. Graph Statist. 26, 344–354.

- Wang et al. (2021) Wang, D., Y. Yu, and A. Rinaldo (2021). Optimal change point detection and localization in sparse dynamic networks. Ann. Statist. 49(1), 203–232.

- Wang et al. (2020) Wang, Z., Y. Liang, and P. Ji (2020). Spectral algorithms for community detection in directed networks. J. Mach. Learn. Res. 21(153), 1–45.

- Yuan et al. (2022) Yuan, M., R. Liu, Y. Feng, and Z. Shang (2022). Testing community structure for hypergraphs. Ann. Statist. 50(1), 147–169.

- Zhu et al. (2017) Zhu, L., J. Lei, B. Devlin, and K. Roeder (2017). Testing high-dimensional covariance matrices, with application to detecting schizophrenia risk genes. Ann. Appl. Statist. 11(3), 1810.

Appendix A Proof of Lemma 1.1

Notice the similarity in structure of , and , to show Lemma 1.1, it suffices to show that for any matrix with and ,

| (A.1) |

and the complexity for calculating the right hand side is as claimed.

We show (A.1) first. By definition of , we only need to show

We then count the non-zeros terms where are not distinct. By , those terms could only have one of the forms in , where are distinct numbers ranging from to . Summation of type terms is

and summation of type terms is . Summation of type terms is

Thus

which proves (A.1).

It remains to consider the computation cost. Using matrix product, the complexity of is , and the complexity of and is the same as complexity of calculating . Below we show for any , the complexity of calculating is where is the averaged degree of graph induced by , then since the averaged degree for is (when ), the complexity of calculating is . For each , we can see requires summations, thus the computation cost for is . This completes proof of the first claim in Lemma.

When using the adjacency list representation of , we can create two dictionaries for each node . The key sets of the two dictionaries are

For each , and for each , . The dictionaries can be constructed by searching the in-neighbors of out-neighbors of each node ( is an in-neighbor of if and is an out-neighbor if ). Overall, it requires complexity to construct and for . And it’s easy to see that

| (A.2) |

Note that when , returns 0 at complexity. This summation also has computation complexity, which completes the proof of Lemma.

Appendix B Proof of Lemma 2.1

Consider the first part of the claim. Suppose

as in Model (1.1)-(1.3) where is fully indecomposable. It is sufficient to show we can write

where are as in Model (1.1)-(1.3) and is doubly stochastic. By Sinkhorn and Knopp (1967) (see also Johnson and Reams (2009)), there are diagonal matrices and with positive diagonal entries such that

is doubly stochastic. At the same time, for each , there are and weight vectors and (i.e., all the entries are non-negative, with a unit--norm) such that

Therefore, if we let

and

then it is seen that

This proves the claim.

We now consider the second part of the claim. Suppose we have

| (B.3) |

where both and satisfy the conditions of Lemma 2.1. The goal is to show (once this is proved, the identifiability follows from ). Note that to show this, it suffices to show that

| (B.4) |

the proof of is similar by symmetry.

We now show (B.4). We show first. By the conditions of the lemma, each of the community has at least one node which is both pure as a citer and as a citee. Without loss of generality, assume for each , node is pure in community both as a citer and as a citee. Comparing the sub-matrix of and consisting of the first rows and columns. It follows

Since both and are double stochastic and fully indecomposable, by Sinkhorn’ theorem (Sinkhorn and Knopp, 1967), there exists a constant such that

| (B.5) |

Appendix C Proof of Theorems 2.1-2.4 for directed-DCMM

C.1 Proof of Theorem 2.1

Recall that for all under the null hypothesis, it follows from definition that

which indicates

For distinct , random variables are mutually independent.

We start with deriving the mean and variance of . For the mean, it follows from that and are mean zero for all and independence that

Consider the variance. First we group the terms in into uncorrelated groups. Notice that for each term in indexed by , there are other terms in that are identical to it up to permutation. Topologically, these terms are the representation of the same quadrilateral with possible starting points and possible directions. Define , then each such -term group can be represented with one unique element in . Therefore, we can rewrite as

where the terms in the summation are now uncorrelated with each other since the underlying quadrilateral is different. It follows that

| (C.6) |

For distinct and by previous argument that has zero mean, we obtain

by the mutual independence between . Since and recall that and are independent, we find

The last equation is by . We further have

Plug it back into (C.6), we obtain

Additionally, under the null hypothesis, it’s not hard to see . Hence,

which completes the proof of the first claim.

Notice that are independent with each other for and has zero mean. Using martingale central limit theorem (the proof is analogous to that of Theorem 2.5 thus omitted), we obtain

| (C.7) |

Consider the second claim. We prove it under both the null and alternative hypothesis. First, consider the mean. By definition, , so

where by an analogy of (D.33), It remains to control the remainder term. Note that , where the last inequality is from Condition (2.14). Hence,

which gives .

Consider the variance of . We decompose as the sum of five terms:

By Cauchy-Schwarz inequality, holds for random variables . It suffices to upper bound , for .

Consider . Recall that

It is easily seen that . Furthermore, we have

| (C.8) |

By condition (2.14),

We plug it into (C.8) and use . It yields that

| (C.9) |

Consider . Recall that

It is easy to see that . We note that for and to be correlated, we must have either or ; in other words, the two underlying paths -- and -- have to be equal. We therefore have

By condition (2.14), we have

Combining the above gives

Since , the right hand side is .

Then we consider . It is easy to see that . To calculate its variance, note that and are uncorrelated unless (i) and or (ii) and . We immediately have

Since , the right hand side is .

For , first recall that

which has mean 0. Each index choice defines a undirected path --- in the complete graph of nodes. If the two paths --- and --- are not exactly overlapping, then is mean-zero, thus and are uncorrelated. In the sum above, each unique path --- is counted twice as and . We then immediately have

Moreover, . It follows that

Since , the right hand side is .

Finally, we consider . Mimicking previous argument and it follows that

Combining above, we obtain , thus completes the proof of the variance part in the second claim.

Consider the last part in the second claim. By Markov’s inequality, for any ,

Here by the first two parts in second claim of Theorem 2.1 that and , the rightmost term is no greater than

where the last two steps follows from and . This proves . Similarly, we obtain . Combining (C.7) and Slutsky’s theorem, we get in law. ∎

C.2 Proof of Theorem 2.2

Introduce the vector such that for

| (C.10) |

By , , we obtain

| (C.11) |

Consider the mean of . Recall that in the proof of Theorem 2.1, the random variables , , , , , , , are mutually independent, it follows that

Together with , and that , we obtain

The remaining part of this section is to show, for sufficiently large ,

| (C.12) |

That are non-distinct implies that there are a pair of identical indices, thus

where the second line is by Cauchy-Schwarz inequality. Thus we complete the proof of (C.12). Furthermore, by , we know . Therefore, .

Consider the variance of . Recall that

which indicates

By symmetry, we decompose as the sum of six terms

Recall the basic inequality that for random variables . It suffices to control the variance of .

Consider the variance of . Recall that are mutually independent and

| (C.13) |

Mimicking the proof of Theorem 2.1, we directly have

| (C.14) |

Consider the variance of . Recall that

where the terms in the summation are mean zero and uncorrelated with each other. We obtain

where we’ve used and so in the last inequality.

Consider the variance of . Rewrite it as

By similar argument,

Since , the above term is no more than

where we’ve used the Cauchy-Schwarz inequality. Each term above are non-negative, so the sum is no more than

By Young’s inequality that , the variance of is upper bound as

| (C.15) |

Consider the variance of . Mimicking the argument in , we find

where we’ve used in the last inequality.

Consider the variance of . Rewrite it as

Again, the terms in the above summation are mean zero and uncorrelated with each other, which indicates

| (C.16) |

Using Cauchy-Schwarz inequality, we find

Plug it into (C.16) and notice , we obtain

| (C.17) |

Combining the upper bound on variance of and notice that is non-stochastic (so the variance is ), we get

The last inequality is by . Using the fact that and , we showed the first claim.

Consider the last claim. It suffices to show for any fixed constant ,

Fixing , let be the event . By the second claim of theorem 2.1, over the event , and . Therefore,

where denotes a generic constant and by Chebyshev’s inequality, the first term in the last line

| (C.18) |

Recall that . Under the condition that , , so . Meanwhile, , thus

| (C.19) |

Furthermore, notice , the right hand side of (C.18) does not exceed

| (C.20) |

where we’ve used the property that and that . Therefore in probability under the alternative hypothesis, and the Type II error goes to .

Under the null,

so the Type I error is

Combining above, the power of the IBM test goes to as

C.3 Proof of Theorem 2.3-2.4

Our first step is to construct satisfying

| (C.21) |

where is a diminishing sequence with its value to be specify and is a binary vector (i.e., ) for .

For , we introduce as follow

It’s not hard to see is a non-negative matrix with row sums equal to . Therefore it is a valid membership matrix with communities. Rewrite

we introduce such that

It should be noted that is not a valid probability matrix for DCMM with communities, as the last two diagonal elements of are not equal to . For notation simplicity, we write in short for in the rest of the proof. Write the -th row of as , and denote the first entries of by . Let , and we have

Notice that and that

we obtain

Therefore satisfies (C.21). However, as we have mentioned before, is not a valid probability matrix for DCMM. We still need to find , and such that .

Write , and let (obviously, ). It’s not hard to verify is a valid probability matrix for DCMM with unit diagonals. Introduce a diagonal matrix such that

Also, introduce such that . Then it’s not hard to verify that is a valid membership matrix for DCMM with communities, as it’s a non-negative matrix and all rows sum up to . Combining above, we have

where is a diagonal matrix. Recall that . By , we have . Additionally, . Therefore, and for sufficiently large .

Consider the spectral norm of . Rewrite as

where is the -th column of . Then it’s not hard to see the following upper bound

| (C.22) |

Recall that , we have

where for sufficiently large , the rightmost term is

Similarly, we have

| (C.23) |

where for sufficiently large and , the rightmost term is bounded by

Combining above, we conclude that as long as , and it satisfies (C.21).

Our next step is to show for given and , can be chosen such that . We’ve already shown in the first step that if . It remains to show can additionally satisfy

for given . Without loss of generality, we may assume

where is the -th column of . As a result,

Noticing , we have by elementary algebra, which implies

Hence,

where we’ve used and (by our derivation, we actually have ). Therefore, for any given sequence , we can find sequence such that . Consequently, and .

Our last step is to construct and as follows:

where is the distribution of adjacency matrix indicated by , and is the distribution of adjacency matrix indicated by . As shown in the second step, we have and .

Write . It suffices to show

| (C.24) |

Let both be uniformly sampled from independently. We re-write the -distance as

Note that can also be viewed as generated uniformly from (thus replace by ), and by , the above equation can be rewritten as

Introduce

Let , then . By Proposition 8.13 in Foucart and Rauhut (2013), we have

| (C.25) |

Meanwhile,

| (C.26) |

Notice and for , the above quantity is no more than

where we’ve used for .

Since as for large , we can apply the tail-sum formula and get

| (C.27) |

where the last step is from .

completes the proof.

Appendix D Proof of Theorem 2.5-2.7

D.1 Proof of Theorem 2.5

Recall that under the null hypothesis, it follows that

Introduce

| (D.28) |

It follows from basic probability and the independence between and that

| (D.29) |

Furthermore, we rewrite as follows

Notice that for distinct indices , the random variables and are mutually independent. Therefore, are also mutually independent.

We now consider the mean and variance part of . For the mean, it follows from independence that

Moreover, the above term equals to since have zero means for . We then consider the variance. We first group the terms in into uncorrelated groups. Notice that for each term in indexed by , there are other terms in that are identical to it up to permutation, namely , and . Define

| (D.30) |

Then each such -term group can be represented by one unique element in .

Therefore, we can rewrite as

where the terms in the summation are now uncorrelated with each other since the underlying quadrilateral is different. It follows that

| (D.31) |

For distinct and by previous argument that has zero mean, we obtain

where we’ve again used the independence between . Recall (D.29) and since , we have

Plug it back into (D.31), we obtain

This completes the proof of the mean and variance part in the first claim.

Next, we consider the second claim. By definition,

Moreover, it follows from basic linear algebra that

To show the first equation, notice

it suffices to show

| (D.32) |

That are not distinct implies that there must be an identical pair, so

Notice , we immediately have

and

where we’ve used Cauchy-Schwarz inequality in the last equality. Similarly, we have . Combining above, we conclude

where we’ve used basic inequality that in the second last line. This completes the proof of (D.32).

Now, to complete the proof of the mean part of the second claim, it remains to show

| (D.33) |

For the first part of (D.33), since is non-negative and , we have

At the same time,

where we’ve used and for symmetric matrices with non-negative eigenvalues. By (2.24),

From here, we have shown since , which completes the first part of (D.33). For the second part of (D.33), notice by , we have , which further implies Similarly, , which completes the second half of (D.33).

Consider the variance part of the second claim. We decompose as the sum of the following terms

Using the inequality that for random variables , it suffices to upper bound for

Consider . Recall that

It is easily seen that . Furthermore, we have

| (D.34) |

By that for ,

We plug it into (D.34) and use . It yields that

| (D.35) |

By basic algebra and the fact that , .

Consider . Recall that

It is easy to see that . We then study its variance. We note that for and to be correlated, we must have that or . Therefore,

Notice that

Combining the above gives

as .

Next, we consider . Recall that

It’s not hard to see and are uncorrelated with unless (i) and , or (ii) and . Therefore,

The last line is by and .

Next, we consider . We can mimick the analysis of and derive

Next, we consider . It’s not hard to see . Mimicking the previous arguments,

At the same time, By basic algebra,

Finally we consider . Mimicking previous argument and it follows from direct calculation that

Combining above, we obtain . This completes the proof of the variance part (i.e., the second part) in the second claim.

We now consider the third part in the second claim. By Chebyshev’s inequality, for any ,

| (D.36) |

Here, by the mean and variance part in the second claim, we have and

Therefore, the rightmost term of (D.36) is no greater than

where the last two steps follows from that , and . This proves . Similarly, we obtain . Once we can show the normality of , then combined with Slutsky’s theorem, we get in law.

It now remains to prove the the normality of . Recall (D.30) and we notice that under the null

We know

For , define